Religare: The Rise, Fall, and Resurrection of India's Financial Services Conglomerate

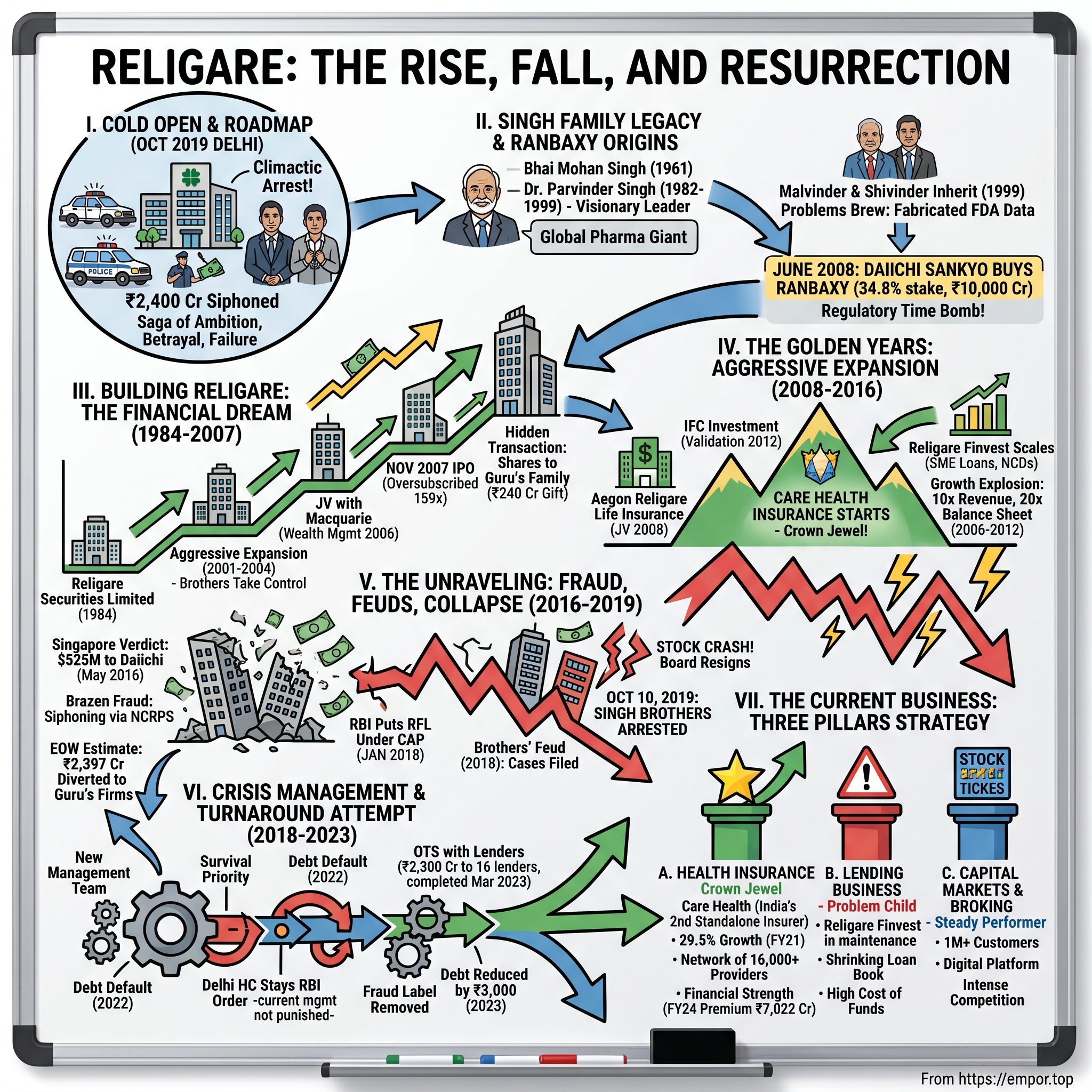

I. Cold Open & Episode Roadmap

The October morning in 2019 started like any other in Delhi's financial district, until police vehicles surrounded the corporate offices of what was once India's most ambitious financial services conglomerate. Within hours, Malvinder and Shivinder Singh—heirs to one of India's greatest pharma fortunes—were in custody, charged with siphoning ₹2,400 crores from the company they'd built to replace their lost empire. The arrest wasn't just about money; it was the climactic moment in a saga of ambition, betrayal, and spectacular corporate failure that would reshape how India thinks about family businesses and governance.

How did two brothers who inherited billions from the sale of Ranbaxy—India's first global pharmaceutical giant—end up destroying the financial services empire they built to replace it? The answer involves fraudulent FDA filings, a spiritual guru with expensive tastes, brother turning against brother, and ultimately, one of the most dramatic corporate collapses in Indian history.

This is a story told in three acts. First, the building of an empire—how the Singh brothers transformed a small securities firm into a financial services powerhouse spanning insurance, lending, and capital markets. Second, the spectacular implosion—a tale of greed, governance failures, and ₹2,400 crores vanishing through a maze of shell companies. And third, the phoenix attempting to rise from the ashes—new management trying to salvage value from the wreckage, with one crown jewel keeping the dream alive.

What makes Religare's story particularly compelling isn't just the scale of the fraud or the family drama—it's what it reveals about the vulnerabilities in India's corporate governance, the perils of unchecked ambition in emerging markets, and perhaps most surprisingly, the possibility of redemption even after catastrophic failure. By the end of this journey, you'll understand not just what went wrong at Religare, but why similar stories keep playing out across India's family-run conglomerates, and what investors can learn from both the destruction and the attempted resurrection.

The numbers alone are staggering: from a peak market capitalization of over ₹15,000 crores to near bankruptcy, from 7,000 employees across 1,450 locations to a company fighting for survival, from oversubscribed IPO darling to pariah of the markets. But behind every number is a human decision, a moment of choice between prudence and greed, between building and looting.

II. The Singh Family Legacy & Ranbaxy Origins

The story of Religare cannot be understood without first understanding the house that Bhai Mohan Singh built. In 1961, when India was still finding its feet as an independent nation, Bhai Mohan Singh and his cousins pooled together ₹2.5 lakhs to start Ranbaxy—a name combining their surnames, Randhir and Gurbax. What started as a small distributor of foreign pharmaceuticals would, over four decades, become India's first truly global pharma company.

But it was Bhai Mohan Singh's son, Dr. Parvinder Singh, who transformed Ranbaxy from a modest Indian player into a pharmaceutical powerhouse. Taking over in 1982, Parvinder was a visionary who understood before most that Indian companies could compete globally not just on cost but on innovation. Under his leadership, Ranbaxy became the first Asian company to get US FDA approval for a manufacturing facility, pioneered the generic drug revolution, and by the late 1990s, was selling in over 100 countries. Parvinder's genius wasn't just in business strategy—it was in understanding that India's pharmaceutical future lay in reverse engineering and challenging Western patent monopolies. He built Ranbaxy's research capabilities, fought legal battles in courts from New Delhi to New York, and created a company culture that was equal parts entrepreneurial aggression and scientific rigor. When he died suddenly in 1999 at age 56, Ranbaxy was generating over $400 million in revenues and was poised to become a billion-dollar company.

Enter Malvinder and Shivinder Singh, aged 26 and 24 when their father died. The brothers inherited not just a company but a legacy—and perhaps more importantly, the burden of living up to it. Malvinder, the elder, took the CEO role while Shivinder focused on new ventures. For a few years, it seemed like the succession would work. Under their leadership, Ranbaxy crossed $1 billion in revenues, expanded into new markets, and maintained its position as India's largest pharmaceutical company.

But beneath the surface, problems were brewing. A 2004 internal self-assessment report—which would later prove devastating—revealed that Ranbaxy had been submitting fabricated data to regulators in over 40 countries, including for critical HIV drugs. The brothers, rather than addressing these issues, chose to bury them. When the FDA began investigating in 2006, raiding Ranbaxy's New Jersey facility, the Singhs dismissed it as a "fishing expedition" and even suggested it was a conspiracy by competitors like Pfizer.

The pivotal moment came in June 2008 when Daiichi Sankyo purchased a 34.8% stake from Malvinder Singh for ₹10,000 crore ($2.4 billion) at ₹737 per share, eventually completing the takeover by November 2008 with an additional $2.2 billion to become majority shareholder. The total transaction valued Ranbaxy at $8.5 billion. For the Singh brothers, it seemed like the perfect exit—they'd cashed out at the peak, walking away with billions while concealing the regulatory time bomb ticking inside Ranbaxy.

The Japanese company later claimed that the Singh brothers had concealed the severity of regulatory issues Ranbaxy was facing with the U.S. FDA during negotiations. What Daiichi Sankyo didn't know—what the Singhs deliberately hid—was the extent of the fraud. According to the Singapore arbitration court findings, the internal self-assessment report listed over 200 drugs, including antiretroviral drugs for AIDS patients, for which Ranbaxy allegedly used fabricated data to secure approvals.

The chickens would come home to roost. In 2016, a Singapore arbitration court ordered the Singh brothers to pay $525 million to Daiichi Sankyo for concealing critical information during the sale. But by then, the brothers had already moved on to their next venture—Religare. With billions from the Ranbaxy sale burning a hole in their pockets and a desire to prove they weren't just inheritors but builders in their own right, they set out to create a financial services empire.

The irony is thick: the very fortune that would fund Religare's expansion was built on a foundation of fraud, and the governance failures that plagued Ranbaxy would be repeated, amplified, in their new venture. As we'll see, some patterns are hard to break, especially when the underlying culture of entitlement and corner-cutting remains unchanged.

III. Building Religare: The Financial Services Dream (1984-2007)

The company that would become the Singh brothers' vehicle for redemption actually predated their involvement by decades. Religare Securities Limited was incorporated in 1984, a small brokerage firm that gained admission to the National Stock Exchange in 1994, operating quietly in the shadows of India's financial markets. For most of its early life, it was unremarkable—one of hundreds of small financial services firms trying to capitalize on India's economic liberalization. Everything changed when the Singh brothers, flush with pharma money and looking for their next act, identified Religare as their vehicle. The transformation began around 2001-2002, when the brothers started taking positions in the company through their investment vehicles. Religare Finvest Ltd (RFL), a group company, was founded in 2001 as a private non-banking financial institution. By 2003-2004, they had effective control and began implementing an aggressive expansion strategy that would transform the sleepy brokerage into a diversified financial services powerhouse.

The early moves were strategic and calculated. RSL registered with Central Depository Services Limited (CDSL) as a depository participant in 2003. It also became a stock broker at the Bombay Stock Exchange (BSE) in 2004. These were the building blocks—each registration, each license, another piece of infrastructure for what the brothers envisioned as India's answer to global financial conglomerates like Citigroup or HSBC.

In 2006, as Malvinder was taking over as CEO of Ranbaxy, the brothers made their first major move in wealth management, entering into a joint venture with Australia's Macquarie Group—one of the world's most sophisticated investment banks. The Macquarie partnership brought instant credibility and expertise to Religare's wealth management ambitions. It was a masterstroke of positioning: associating with a global brand while maintaining control of the Indian operations. But it was the November 2007 IPO that truly announced Religare's arrival on the national stage. The IPO was oversubscribed 159 times—an extraordinary vote of confidence from the market. The shares were priced at ₹185 per share, and listed on BSE and NSE on November 21, 2007. The retail category was subscribed 93.5 times, while the overall IPO was subscribed 160.56 times by the closing date.

What made this IPO particularly interesting—and what would later become evidence in fraud investigations—was what happened just before it. Malvinder and Shivinder transferred 13.5 million shares of Religare to Gurinder Singh Dhillon's two sons, Gurpreet (6.25 million) and Gurkeerat (6.25 million), and Sunil Godhwani (1 million) at the face value of Rs 10 each. During the company's IPO in 2007, these shares were allotted to public shareholders at Rs 185. This meant an instant profit of Rs 175 per share for the spiritual guru's family and their associate—a gift of nearly Rs 240 crores.

This transaction would later be cited as evidence of the unhealthy relationship between the Singh brothers and their spiritual guru, Gurinder Singh Dhillon of Radha Soami Satsang Beas. It was the beginning of a pattern where corporate assets were used to enrich a small circle of insiders, all while presenting a facade of professional management to public shareholders.

By 2007, Religare had transformed from a small brokerage into a diversified financial services company with ambitions to rival the biggest names in Indian finance. It had securities broking, commodity broking, depository services, merchant banking, wealth management through the Macquarie venture, and was preparing to enter insurance and lending. The Singh brothers had successfully created the platform they needed for their next phase of expansion.

The IPO proceeds gave them the capital, the public listing gave them credibility, and the Ranbaxy sale (still a year away) would provide the massive war chest needed for aggressive expansion. Everything was in place for what should have been one of India's great corporate success stories. Instead, as we'll see in the next section, it would become a cautionary tale about the dangers of unchecked ambition and the toxic mix of family, spirituality, and corporate governance.

IV. The Golden Years: Aggressive Expansion (2008-2016)

The year 2008 should have been a disaster for Religare. The global financial crisis was decimating financial institutions worldwide, Lehman Brothers had collapsed, and credit markets were frozen. But for the Singh brothers, sitting on billions from the Ranbaxy sale, it was the perfect storm of opportunity. While others retreated, they charged forward with an acquisition and expansion spree that would transform Religare into one of India's largest financial conglomerates. Their first major move came in July 2008 with the launch of Aegon Religare Life Insurance, a joint venture between Dutch insurance giant Aegon N.V., Religare, and Bennett, Coleman & Company (The Times Group). AEGON Religare Life Insurance Company was a joint venture between AEGON, an international life insurance and pension company, Religare, one of India's leading integrated financial services groups, and Bennett, Coleman & Company, India's largest media house, launching in July 2008 with over 30 branches across India. Aegon held a 26% equity stake, while Religare and Bennett Coleman shared the rest. It was a statement of intent—partnering with one of Europe's oldest insurance companies and India's largest media house to build a life insurance business from scratch.

The timing seemed counterintuitive. The insurance sector in India was already crowded with established players like LIC, ICICI Prudential, and HDFC Life. But the Singh brothers saw opportunity where others saw saturation. India's insurance penetration was still below 3% of GDP, far below global averages. The growing middle class, increasing life expectancy, and rising awareness about financial planning all pointed to massive growth potential. In 2012, the International Finance Corporation (IFC), the World Bank's private sector arm, invested in Religare—a massive vote of confidence from one of the world's most prestigious development finance institutions. The IFC investment wasn't just about money; it was validation that Religare's business model and growth trajectory met international standards.

That same year, Religare Health Insurance Company Limited (RHIC) started operations in 2012. This was particularly strategic. While life insurance through Aegon Religare was growing, health insurance was emerging as the next big opportunity in India. Rising healthcare costs, increasing lifestyle diseases, and growing awareness about health coverage created a perfect storm of demand. The Singh brothers positioned Religare Health Insurance (later renamed Care Health Insurance) as a standalone health insurer focused purely on health products—a decision that would prove prescient when this became their crown jewel years later.

The expansion wasn't limited to insurance. Religare Finvest, the lending arm, was scaling aggressively into SME loans and affordable housing finance. In 2011, Religare Finvest successfully issued non-convertible debentures (NCDs) worth ₹800 crores. In December 2011, Avigo Capital and in January 2012, Jacob Ballas invest in Religare Finvest Limited (RFL). These investments provided the capital needed to fund rapid loan book expansion.

The numbers during this period were staggering. In the five year period from 2006-07 to 2011-12, Religare's consolidated revenues grew ten times - from 3.2 billion to 32.5 billion - while the balance sheet size multiplied 20 times - from 10.1 billion to 203.4 billion. The company was operating from over 1,450 locations across India with more than 7,000 employees.

In 2013, Religare bought out Macquarie's stake in the wealth management business, giving them full control of this high-margin segment. They also rebranded Religare Mutual Fund to Religare Invesco Mutual Fund through a partnership with Invesco, one of the world's largest asset managers. Every move seemed calculated to build credibility through association with global brands while maintaining operational control.

The broking business was expanding rapidly too. REL's subsidiaries service over 11 lakh clients from over 1,275 locations having presence in more than 400 cities. The retail broking arm was leveraging technology to democratize stock market access, offering online trading platforms and mobile apps at a time when most Indians still traded through phone calls to brokers.

By 2014, Religare had achieved what seemed impossible just seven years earlier—transformation from a small brokerage into a diversified financial services conglomerate with leadership positions in multiple segments. Health insurance was growing at 30%+ annually, the lending book was expanding rapidly, and the capital markets business had over a million customers.

But beneath this impressive growth, problems were festering. The aggressive expansion was funded by debt—lots of it. The lending business, in particular, was making increasingly risky loans, many to entities connected to the promoters. Corporate governance, never a strong suit of the Singh brothers, was deteriorating as they used Religare as a personal ATM to fund other ventures and satisfy their spiritual guru's financial needs.

The brothers were also distracted. They had used the Ranbaxy proceeds to build Fortis Healthcare into one of India's largest hospital chains, but that too was drowning in debt. The Singapore arbitration court's 2016 ruling ordering them to pay $525 million to Daiichi Sankyo for the Ranbaxy fraud was looming. And most dangerously, they were systematically siphoning money from Religare through a complex web of transactions that would later be investigated as one of India's largest corporate frauds.

By 2016, what looked like a golden period of expansion would soon reveal itself as a house of cards built on borrowed money, fraudulent transactions, and a complete breakdown of corporate governance. The unraveling was about to begin, and it would be spectacular in its scope and devastating in its impact.

V. The Unraveling: Fraud, Feuds, and Collapse (2016-2019)

The first crack in the facade appeared in May 2016 when the Singapore International Arbitration Centre delivered its verdict: An arbitration court in Singapore has ordered former shareholders of India's Ranbaxy Laboratories to pay $525 million to Daiichi Sankyo. The Japanese company claimed that when it acquired Ranbaxy in 2008, the large shareholders with whom it negotiated had concealed the severity of regulatory issues that Ranbaxy was facing with the U.S. FDA. The award was leveled against New Delhi's RHC Holding, an investment firm led by Malvinder Mohan Singh.

For the Singh brothers, this wasn't just a financial blow—it was an existential crisis. They didn't have $525 million lying around. The billions from the Ranbaxy sale had been deployed into Religare, Fortis Healthcare, and mysteriously, into a maze of shell companies connected to their spiritual guru, Gurinder Singh Dhillon of Radha Soami Satsang Beas. The mechanism of the fraud was both brazen and sophisticated. The Singh brothers, in their capacity as promoters of REL, had siphoned off money from the company by issuing non-convertible redeemable preference share (NCRPS) for themselves and later redeeming them. Promoters and owners aren't allowed to just withdraw money from a company for personal use, but using an instrument like these redeemable preference shares allowed them to get away with this.

But the NCRPS scheme was just the tip of the iceberg. The alleged fraud, which the EOW of the Delhi police pegged at Rs 2,397 crore worth of funds, had its roots and tentacles spread across a number of companies and transactions involving Malvinder and Shivinder Singh and Religare entities. Internal inquiries showed that poor financial health of Religare Finvest was to a large extent on account of wilful default on significant unsecured loans, defined for internal purposes as corporate loan book by borrower entities either related, controlled or associated with the promoters.

The money trail led to shocking revelations. Hundreds of crores had been diverted to companies controlled by Gurinder Singh Dhillon and his family. The Singh brothers retained a part of it, and shifted the bulk of the funds to other firms that were owned by Sunil Godhwani, Gurinder Singh and Shabnam Dhillon, and Gurpreet and Gurkeerat Singh. The spiritual guru's involvement wasn't just passive—his associate Sunil Godhwani was actively involved in the scheme as Chairman and Managing Director of Religare Enterprises.

In January 2018, the Reserve Bank of India dropped a bombshell: RBI put RFL under a Corrective Action Plan (CAP) due to issues emanating from siphoning and misappropriation of funds by erstwhile promoters of REL and their associates and it was prohibited by RBI from expanding its Credit portfolio other than investments in Government Securities. This was effectively a death sentence for a lending business—unable to make new loans, Religare Finvest was frozen.

The brothers' relationship, already strained, completely broke down in 2018. Shivinder turned against Malvinder, accusing him of mismanagement and diverting funds to the religious sect. In a shocking public spectacle, Shivinder filed cases against his own brother, claiming he had been misled about the extent of the financial problems. Malvinder fired back, accusing Shivinder of abandoning business responsibilities to pursue spiritual interests.

The public feuding between the brothers provided a window into the rot at the heart of their empire. Court filings revealed that the Singh brothers had been using Religare and Fortis as personal piggy banks, moving money between companies through a labyrinth of transactions designed to obscure the trail. They had pledged shares to raise personal loans, then defaulted when the stock prices crashed. They had given unsecured loans to shell companies that never intended to repay.

By early 2019, the house of cards was collapsing. Religare's stock price had crashed from over ₹600 to below ₹100. The lending business was hemorrhaging money. Corporate governance had completely broken down with board members resigning in protest. Customers were withdrawing deposits. Lenders were calling in loans.

On October 10, 2019, the inevitable happened. Shivinder was arrested in the afternoon, while his elder brother Malvinder was arrested in Ludhiana (Punjab) late night after a brief search. They were charged with causing wrongful loss worth Rs 2,397 crore to Religare Finvest Ltd. Along with the Singh brothers, the police also arrested former Religare Finvest MD Kavi Arora, and former Religare Group CFO Anil Saxena along with former Religare MD Sunil Godhwani.

The arrest wasn't just about Religare. The Singh brothers were also facing charges for siphoning ₹472 crores from Fortis Healthcare. They owed Daiichi Sankyo $525 million. Multiple agencies including the Enforcement Directorate, Serious Fraud Investigation Office, and SEBI were investigating them. From billionaire heirs to accused fraudsters in jail—the fall was complete.

In January 2020, the Enforcement Directorate filed a charge sheet against the Singh brothers and former CMD of Religare Enterprises Sunil Godhwani, accusing all three of money laundering, punishable under sections 3 and 4 of the Prevention of Money Laundering Act.

The scale and audacity of the fraud shocked even seasoned observers of Indian corporate malfeasance. This wasn't just financial mismanagement or aggressive accounting—it was systematic looting of a public company by its promoters. The fact that it involved a spiritual guru added a layer of betrayal that resonated beyond the financial world. Thousands of small investors who had trusted the Religare brand, many of them followers of the same spiritual sect, had lost their savings.

As 2019 ended, Religare was effectively an orphan—its promoters in jail, its businesses in crisis, its reputation in tatters. The company that had once aspired to be India's Citigroup was now fighting for survival. But in this darkest hour, the seeds of an unlikely resurrection were being planted.

VI. Crisis Management & The Turnaround Attempt (2018-2023)

Even before the Singh brothers were arrested, Religare had begun the painful process of trying to save itself. In 2018, with the RBI restrictions in place and the promoters' fraud becoming evident, a new management team took charge with a seemingly impossible mandate: stabilize a sinking ship while its former captains were actively trying to scuttle it.

The new management's first priority was simple survival. Religare Finvest, the lending arm that had been the primary vehicle for the fraud, was bleeding cash. The RBI's Corrective Action Plan meant they couldn't make new loans, but existing borrowers—many of them shell companies connected to the Singh brothers—had stopped repaying. The company was technically insolvent. The crisis deepened in February 2022 when RFL defaulted on interest payment to bond holders due on February 25, 2022 due to asset liability mismatch, said to arise out of siphoning and misappropriation of funds by erstwhile promoters of its parent company. The company defaulted on an interest amount of Rs 2.41 crore for non-convertible debentures in March 2022.

Making matters worse, in March 2022, the RBI declined the restructuring of RFL with Religare Enterprises continuing as its promoter since debt-ridden NBFC has been declared as "Fraud" exposure by lenders. This was a devastating blow—lenders had officially labeled the company as fraudulent, making any conventional restructuring impossible.

But the new management refused to give up. They challenged the RBI's order in Delhi High Court, arguing that the current management shouldn't be punished for the crimes of the former promoters. The Delhi High Court stayed the RBI order, noting that "the erstwhile promoters of REL are no longer in charge of the affairs of either the petitioner company or of REL."

Throughout 2022, the management team worked tirelessly on a one-time settlement (OTS) with lenders. RFL owed about Rs 5,300 crore to the consortium of lenders led by State Bank of India (SBI). The proposal was audacious—settle the entire debt for Rs 2,300 crore, less than half the amount owed. To demonstrate commitment, the company deposited Rs 220 crore as earnest money with the lead lender in June 2022.

The negotiations were grueling. Each of the 16 lenders had to be convinced individually that accepting a haircut was better than pursuing a lengthy legal battle with uncertain recovery prospects. The management argued that with the Singh brothers in jail and most of the siphoned funds unrecoverable, the OTS offered the best possible outcome for all parties.

In December 2022, breakthrough came. RFL signed a settlement agreement with all its lenders for a one-time settlement, clearing the deck for the NBFC to exit from the Corrective Action Plan imposed by the RBI. RFL and REL entered into a settlement agreement with 16 lenders in Dec 2022 (including SBI, Bank of Baroda, UBI, Canara Bank, PNB, BoI, IDBI Bank, P&SB, BoM) and a one time settlement (OTS) was completed in Mar 2023

By March 2023, Religare had successfully paid the entire settlement amount, effectively reducing its debt burden by over ₹3,000 crores. This wasn't just a financial victory—it was psychological validation that the company could survive without its tainted founders.

Simultaneously, the legal battles continued. In December 2023, the Delhi High Court delivered a crucial verdict, removing the fraud label from Religare Finvest. The court observed that the current management had no role in the alleged fraud and that continuing to label the company as fraudulent would unfairly penalize innocent stakeholders including employees, customers, and minority shareholders.

The Enforcement Directorate's investigation, however, continued to expand. By 2024, the ED's probe had grown to encompass over ₹2,000 crores of alleged money laundering. The investigation revealed an intricate web of 150+ shell companies used to route funds, fake loan agreements, and systematic destruction of evidence. Each new revelation reinforced how deeply the rot had spread during the Singh brothers' tenure.

Despite these ongoing investigations, the new management pressed forward with operational improvements. They implemented stricter lending norms, upgraded risk management systems, and most importantly, began the process of cultural transformation—from a promoter-driven organization to a professionally managed institution.

VII. The Current Business: Three Pillars Strategy

A. Health Insurance - The Crown Jewel

Of all Religare's businesses, Care Health Insurance emerged as the unlikely hero of the turnaround story. Contributing 74.5% of revenue by 2021, what started as Religare Health Insurance had transformed into India's second-largest standalone health insurer, a remarkable achievement given the company's broader troubles. The crown jewel's transformation was remarkable. Star Health & Allied Insurance tops with list with gross premium of Rs.7000 crore. Care Health and Niva Bupa Health occupy the next two spots with premium collection of Rs. 2400 crore and Rs. 2200 crore, respectively, establishing Care Health as the second-largest standalone health insurer in India by retail premiums.

The company's market position strengthened through strategic focus. With a network of 16,000+ healthcare providers, Care Health processed claims efficiently while maintaining cost discipline. The digital transformation initiative, launched in 2020 amid the pandemic, proved prescient—enabling contactless policy issuance, digital claims processing, and telemedicine consultations when physical infrastructure was paralyzed.

Product innovation became a differentiator. Care launched specialized products for chronic conditions, senior citizens, and preventive health—segments traditionally underserved by insurers. The "Care Freedom" product, offering coverage without sub-limits or co-payment clauses, resonated particularly well with urban customers tired of fine print exclusions.

The financial metrics told the story of resilience. In FY21, despite the pandemic, Care Health achieved ₹2,559 crores in Gross Direct Premium Income, growing at 29.5%—well above the industry average. The combined ratio improved from 110% to 98%, finally achieving underwriting profitability. The solvency ratio, a key measure of financial health, stood at a comfortable 180%, well above regulatory requirements.

B. Lending Business - The Problem Child

If Care Health was the crown jewel, Religare Finvest remained the problem child—a constant reminder of past sins. Despite the successful OTS with lenders, the lending business faced an uphill battle to regain relevance. Contributing just 15% of revenue by 2023, down from over 40% at its peak, RFL was effectively in maintenance mode.

The numbers were sobering. The loan book, which had peaked at over ₹15,000 crores, shrank to below ₹3,000 crores. Non-performing assets, even after massive write-offs, remained elevated at 8%. The cost of funds, given the company's tainted history, was 200-300 basis points higher than competitors, making profitable lending nearly impossible.

The SME lending segment, once the core focus, had been decimated. Trust, once broken in the lending business, proved nearly impossible to rebuild. Corporate borrowers stayed away, wary of association with a lender that had been labeled fraudulent. Retail customers, particularly in the affordable housing segment through RHDFCL, provided some stability but insufficient scale for meaningful growth.

Management's strategy was pragmatic—run down the existing book while maintaining minimal new origination to keep the license active. The hope was that time would heal wounds and eventually allow for revival, but few believed this business would ever regain its former glory.

C. Capital Markets & Broking - The Steady Performer

The broking business, contributing 8.5% of revenue, emerged as the quiet performer—neither spectacular nor problematic. With over 1 million customers across 400+ cities, Religare's broking arm had survived the crisis relatively unscathed, primarily because it operated independently of the lending business's troubles.

The digital transformation here had been more successful than in other segments. The online trading platform, upgraded in 2021, offered features comparable to new-age brokers like Zerodha and Upstox. The mobile app, with 500,000+ downloads, provided seamless trading experiences that retained customer loyalty despite the parent company's issues.

But competition was fierce. Discount brokers had commoditized the business, driving brokerage rates to near-zero. Religare's attempts to differentiate through research and advisory services met limited success—clients who wanted advice went to established names like ICICI Direct or HDFC Securities, while price-sensitive traders migrated to discount brokers.

The commodity broking business, once a differentiator, had become a regulatory burden after multiple SEBI investigations. The wealth management segment, stripped of the Macquarie brand, struggled to attract high-net-worth clients who had better options elsewhere.

VIII. Financial Performance & Market Position

The financial resurrection of Religare was both impressive and incomplete. By 2024, the company had achieved what seemed impossible just five years earlier—survival. But survival and thriving are different beasts, and the numbers revealed a company still searching for its identity.

The market capitalization of ₹8,585 crores represented a massive recovery from the sub-₹1,000 crore levels during the crisis, but remained far below the ₹15,000+ crore peak of the Singh era. Trading at 3.41x book value suggested market optimism about future prospects, though this was largely driven by the value of Care Health Insurance rather than confidence in the conglomerate structure.

Revenue of ₹7,354 crores and profit of ₹183 crores looked healthy on paper, but the details revealed concerning trends. The profit margin of just 2.5% was anemic for a financial services company. Return on Equity of 4.13% over three years was barely above the risk-free rate—shareholders would have been better off in government bonds.

The debt-free status, achieved through the painful OTS process, was perhaps the greatest achievement. From a debt-to-equity ratio of over 5x during the crisis, Religare had deleveraged to near-zero debt. This provided flexibility but also revealed the cost of survival—the company had essentially shrunk to fit its reduced circumstances rather than growing out of trouble.

The stock's 52-week range of ₹201-₹319.90 showed significant volatility, reflecting ongoing uncertainty about the company's direction. Every legal development, every quarterly result, every management announcement triggered sharp movements, indicating a market still unsure whether this was a turnaround story or a value trap.

Promoter holding at 25.8% raised questions about control. With the Singh brothers gone and no clear controlling shareholder, Religare operated in a governance vacuum. Professional management provided stability, but the absence of a committed long-term owner created strategic drift. The latest quarterly results told a story of recovery but not resurgence. Religare Enterprises on Tuesday reported a 70 per cent jump in consolidated net profit to Rs 68.49 crore for the second quarter ended September 2024. While the percentage growth looked impressive, the absolute numbers remained modest for a company with aspirations of national relevance.

Care Health Insurance posted an all-time high premium collection of Rs 7,022 crore, in FY24. This single business line was essentially carrying the entire conglomerate. Our Securities Broking business registered a bumper year of growth with income amounting to Rs 368 crore for FY24, a jump of 29% as compared to the previous year. But even this "bumper year" represented less than 5% of total revenues.

IX. Playbook: Lessons from Disaster & Recovery

Governance Failures: The Family Business Trap

The Religare saga offers a masterclass in how family-run businesses can self-destruct. The fundamental flaw wasn't just the Singh brothers' greed—it was the complete absence of checks and balances. Board members were either complicit or powerless. Independent directors proved neither independent nor directing. The audit committee, risk committee, and other governance structures existed on paper but failed in practice.

The brothers treated the public company as a private fiefdom, moving money between entities as if playing Monopoly with real money. The NCRPS scheme was particularly ingenious in its malevolence—using a legitimate financial instrument to legitimize theft. When promoters can issue preference shares to themselves and then redeem them at will, the line between corporate treasury and personal wallet disappears.

The spiritual guru angle added a uniquely Indian dimension to the governance failure. Gurinder Singh Dhillon's influence over the Singh brothers created a shadow power structure that bypassed all formal governance mechanisms. Corporate decisions were allegedly made not in boardrooms but in spiritual discourse, with business strategy subordinated to religious obligation.

The Perils of Rapid Diversification

Religare's expansion strategy violated every principle of focused growth. Within a decade, they entered insurance, lending, broking, wealth management, commodity trading, and housing finance. Each business required different skills, regulatory compliance, and risk management—none of which the company possessed in adequate measure.

The diversification was driven not by strategic logic but by ego and opportunism. Every new license was a trophy, every new vertical a validation of ambition. The Singh brothers wanted to build India's Citigroup without understanding that even Citigroup struggled with such complexity. The result was predictable: inadequate investment in each business, lack of specialized talent, and inability to compete with focused players.

The lending business exemplified this problem. While specialized NBFCs like Bajaj Finance built sophisticated credit scoring models and collection mechanisms, Religare Finvest relied on relationship lending—which in practice meant lending to related parties. The lack of domain expertise meant they couldn't distinguish between good and bad credits, leading to the massive NPA crisis.

Regulatory Relationships: The Cost of Defiance

The Singh brothers' approach to regulation was adversarial rather than collaborative. When the FDA investigated Ranbaxy, they denied and deflected rather than cooperating. When RBI raised concerns about Religare Finvest, they tried to circumvent rather than comply. This combative stance ultimately led to regulatory action that nearly destroyed the company.

The new management's approach proved that a different path was possible. By engaging transparently with RBI, SEBI, and IRDAI, they gradually rebuilt trust. The removal of the fraud label in 2023 wasn't just a legal victory—it was validation that regulators recognized the change in management and culture.

Crisis Management: Salvaging Value from Wreckage

The post-2018 management team's crisis response offers valuable lessons in corporate turnaround. First, they triaged ruthlessly—identifying which businesses could be saved (health insurance), which needed to be wound down (lending), and which could limp along (broking). This clarity of purpose prevented resources from being wasted on lost causes.

Second, they chose transparency over opacity. Rather than hiding problems, they disclosed the full extent of the fraud, cooperated with investigations, and communicated regularly with stakeholders. This built credibility even as it revealed uncomfortable truths.

Third, the debt settlement strategy was masterful. Recognizing that fighting lenders in court would destroy value for everyone, they negotiated a settlement that gave lenders reasonable recovery while preserving the company's viability. The ₹3,000 crore haircut was painful but necessary surgery.

The Value of Core Assets

Care Health Insurance's survival and growth proved the importance of having at least one strong business in a conglomerate. While everything else crumbled, this crown jewel provided cash flow, maintained customer relationships, and gave investors a reason to believe in recovery. Without Care Health, Religare would likely have been liquidated.

The lesson for conglomerates is clear: diversification without a strong core is a recipe for disaster. Better to be excellent at one thing than mediocre at many. Care Health succeeded because even during the crisis, management protected it from contagion, maintaining operational independence and regulatory compliance.

Trust & Brand: The Longest Recovery

Financial services run on trust, and trust once broken is nearly impossible to rebuild. Five years after the fraud was exposed, Religare still trades at a discount to peers, struggles to attract institutional investors, and faces skepticism from customers. The Religare brand, once associated with innovation and growth, now evokes caution and concern.

The company's attempt to rebuild trust through operational excellence has shown limited success. Customers might use Care Health Insurance, but they do so despite the Religare association, not because of it. The brand rehabilitation might take a generation—if it happens at all.

X. Bear vs. Bull Case Analysis

The Bear Case: Permanent Impairment

Bears argue that Religare is a value trap—optically cheap but fundamentally broken. The legal overhang, while diminished, hasn't disappeared. The ED investigation continues, and new revelations could emerge at any time. The Singh brothers, though in jail, haven't exhausted their legal options and could create further complications.

The business portfolio remains problematic. Health insurance, while growing, faces intense competition from both established players and new entrants. The lending business is essentially dead—even if RBI removes all restrictions, who would borrow from a lender with Religare's history? The broking business operates in a commoditized market where scale and technology matter more than legacy.

The 4.13% ROE over three years is particularly damning. This isn't a temporary problem but a structural issue. Without the ability to leverage (given the history), and with limited pricing power (given the competition), how does Religare generate acceptable returns? The current valuation might reflect not optimism but the market's assessment that this is as good as it gets.

Corporate governance, while improved, remains questionable. The absence of a strong promoter creates a leadership vacuum. Professional managers might run operations competently, but who drives strategic transformation? Who makes the bold decisions needed to break out of mediocrity?

The conglomerate structure itself is an anachronism. Modern investors prefer pure plays where they can evaluate and value each business clearly. Religare's structure creates a holding company discount that might never close. Why own Religare when you can buy HDFC Life, Bajaj Finance, or Zerodha directly?

The Bull Case: Hidden Value

Bulls see Religare as a misunderstood turnaround story with significant hidden value. The market is still pricing in the fraud risk, but the worst is clearly over. The debt is settled, the new management has stabilized operations, and each passing quarter without disaster rebuilds confidence.

Care Health Insurance alone could justify the current valuation. Care Health and Niva Bupa Health occupy the next two spots with premium collection of Rs. 2400 crore and Rs. 2200 crore, respectively. As India's second-largest standalone health insurer, it operates in a market growing at 20%+ annually. If listed separately, Care Health could command a valuation of ₹15,000-20,000 crores based on peer multiples.

The lending business, while impaired, isn't worthless. India's credit demand remains robust, and even a small player can find profitable niches. Once RBI restrictions are fully lifted, new capital could revive this business. The licenses, infrastructure, and relationships have value even if the current book doesn't.

The removal of fraud labels and settlement of debts creates optionality. Religare could attract a strategic investor, merge with another financial services firm, or spin off subsidiaries at attractive valuations. The current management has shown they're open to value-unlocking transactions.

Trading at 3.41x book value might seem expensive, but book value understates the franchise value of Care Health and the option value of other businesses. In a bull market for financial services, multiple expansion could drive significant returns even without earnings growth.

XI. The Road Ahead & Strategic Options

The path forward for Religare requires decisive strategic choices. The most obvious move is the IPO of Care Health Insurance. Market conditions are favorable, investor appetite for insurance stocks is strong, and separation from the Religare brand could unlock significant value. A successful IPO could value Care Health at 2-3x current book value, providing capital for growth and validation of the turnaround.

Digital transformation presents both opportunity and threat. While Religare has made progress in digitizing operations, it remains behind pure-play digital competitors. The choice is stark: invest heavily to catch up or accept a declining position in increasingly digital markets. Half-measures will only延长 the decline.

The lending business needs resolution. Either commit to revival with fresh capital and new leadership, or wind it down completely. The current zombie state destroys value and management attention. Given the reputational issues, partnering with a clean bank or NBFC might be the only viable path to revival.

Strategic partnerships could accelerate recovery. Rather than going alone, Religare could partner with global insurers, fintech companies, or private equity funds. These partners would bring not just capital but credibility, technology, and expertise. The days of the Singh brothers' go-it-alone strategy are clearly over.

Geographic expansion within India remains untapped. Despite the national presence, Religare is under-penetrated in many tier-2 and tier-3 cities where financial services demand is growing rapidly. A focused regional strategy could find pockets of growth without competing directly with national giants.

The regulatory relationship needs continuous nurturing. Every interaction with RBI, IRDAI, and SEBI is an opportunity to rebuild trust. Proactive compliance, voluntary disclosures, and industry leadership on governance issues could gradually restore regulatory confidence.

XII. Epilogue: Redemption or Relapse?

The transformation from Singh-era excess to professional management represents one of Indian corporate history's most dramatic pivots. But the question remains: is this genuine transformation or merely survival? The jury is still out.

Can Religare truly escape its past? History suggests that corporate rehabilitation is possible but rare. Companies like Tyco and WorldCom in the US managed to recover from fraud scandals, but many others never regained their former glory. Religare's challenge is compounded by operating in trust-dependent financial services where reputation matters more than in manufacturing or technology.

The lessons for Indian corporate governance are profound. Religare demonstrates how quickly unchecked promoter power can destroy value, how spiritual or personal relationships can corrupt business judgment, and how regulatory forbearance can enable fraud until it becomes too large to ignore. But it also shows that professional management, transparent communication, and regulatory cooperation can stabilize even the most damaged companies.

The broader implications for family-run businesses are sobering. As Indian companies professionalize and global investors demand better governance, the Religare model of promoter extraction becomes increasingly untenable. The Singh brothers represent the last generation of promoters who thought they could treat public companies as private property.

What makes Religare's story particularly relevant is its timing. As India positions itself as a global financial center, as millions of Indians enter formal financial services, and as technology transforms distribution and risk assessment, the sector needs trusted institutions. Religare's fraud undermined this trust just when it was most needed.

The company today stands at an inflection point. It has survived the immediate crisis, stabilized operations, and preserved its most valuable asset. But survival isn't success. The next chapter will determine whether Religare becomes a footnote in Indian corporate history—a cautionary tale of greed and governance failure—or something more inspiring: proof that redemption is possible, that companies can recover from catastrophic failure, and that professional management can succeed where promoters failed.

The final verdict on value creation versus value destruction remains unwritten. The Singh brothers clearly destroyed enormous value—not just the billions lost in fraud but the opportunity cost of what Religare could have become with honest leadership. The current management has stopped the destruction and preserved some value, but creation remains elusive.

For investors, Religare presents a complex calculus. The upside is clear—a successful turnaround could generate multibagger returns. But the risks remain substantial—legal surprises, competitive pressures, and structural challenges could trap capital for years. Perhaps the most honest assessment is that Religare is neither a clear buy nor sell, but a wait-and-watch story where patience might be rewarded but isn't guaranteed.

For India Inc, Religare serves as both warning and inspiration. A warning about the costs of governance failure, the dangers of unchecked ambition, and the fragility of trust. But also inspiration that even after spectacular failure, recovery is possible through transparency, professionalism, and persistence.

The most profound lesson might be about the nature of business itself. The Singh brothers saw business as extraction—how much value could they pull out for themselves? The new management sees it as creation—how much value can they generate for stakeholders? This philosophical difference, more than any financial metric, will determine whether Religare's resurrection is real or merely a stay of execution.

As markets evolve, regulations tighten, and investors become more sophisticated, companies like Religare face a simple choice: evolve or perish. The early signs suggest evolution is possible, but the pace remains frustratingly slow. Whether Religare ultimately joins the ranks of great turnaround stories or cautionary tales will depend on decisions being made today in boardrooms and corner offices across Mumbai and Delhi.

The story of Religare is far from over. What started as a tale of ambition and fraud has become something more complex—a meditation on corporate mortality and resurrection, on the price of governance failure and the possibility of redemption. In the end, Religare's greatest contribution might not be the financial services it provides but the lessons it teaches about what happens when capitalism's checks and balances fail—and what it takes to rebuild when everything seems lost.

For now, Religare endures—diminished but not defeated, wounded but not dead. Whether it thrives again or merely survives will be determined by forces both within and beyond its control. Market cycles, regulatory changes, competitive dynamics, and management decisions will all play a role. But perhaps the most important factor will be whether India's financial markets are willing to forgive, if not forget, one of their most spectacular betrayals.

The clock is ticking. Every quarter without growth, every year without strategic clarity, makes recovery harder. The window for transformation won't stay open forever. Religare has been given a second chance—a rarity in the unforgiving world of financial markets. What it does with this chance will determine not just its own fate but send a message about accountability, governance, and the possibility of redemption in Indian business.

The final chapter remains unwritten, but one thing is certain: Religare's journey from creation to destruction to attempted resurrection will be studied in business schools and boardrooms for generations to come. It is, in its complexity and contradictions, a uniquely Indian story—one of ambition and betrayal, of spirituality and greed, of family and fraud, of destruction and the hope, however faint, of redemption.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube