RAILTEL: The Digital Backbone of India's Railways

I. Introduction & Episode Roadmap

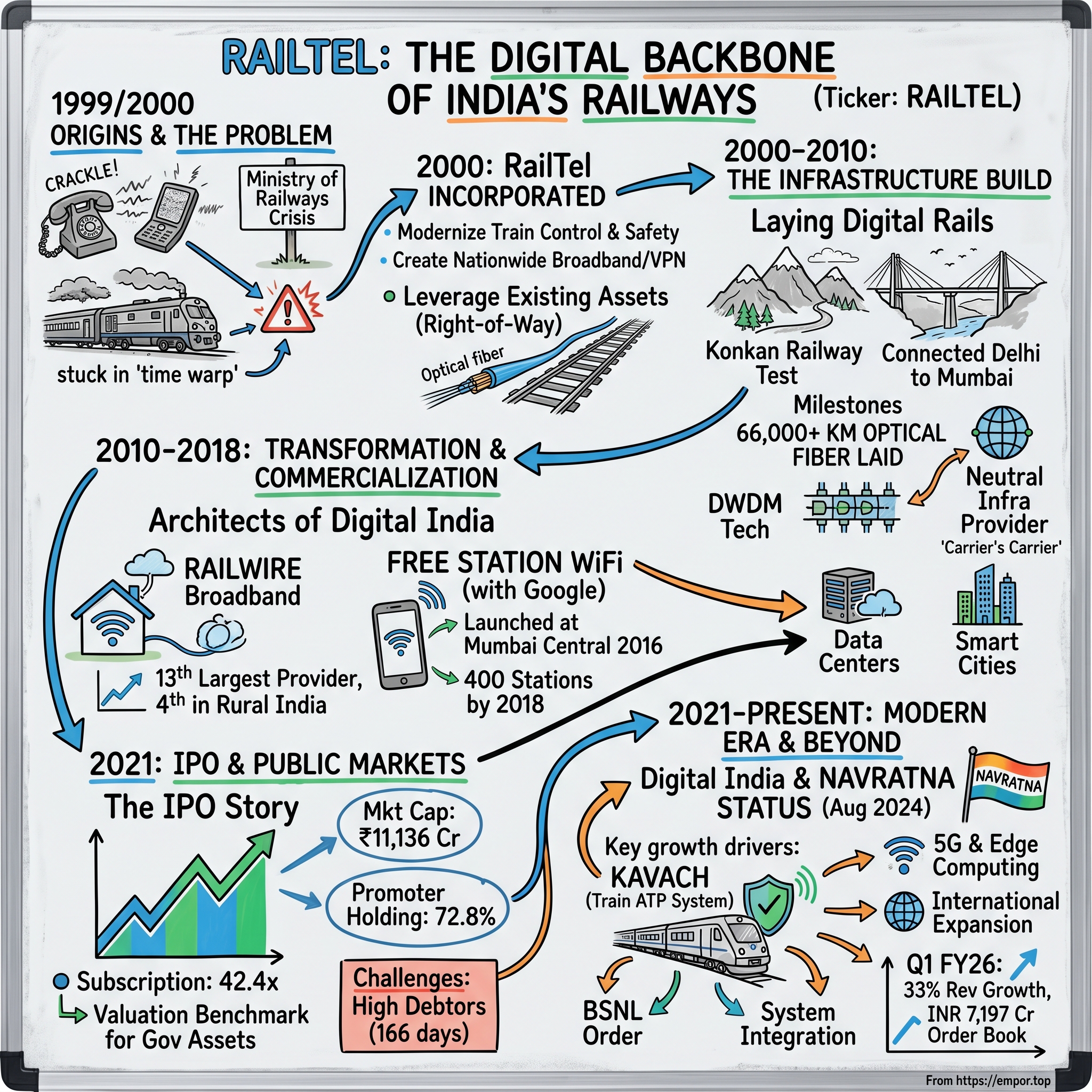

Picture this: It's 1999, and a train controller in Howrah Junction is trying to coordinate with another station 500 kilometers away. The communication? A crackling analog phone line that drops every few minutes during monsoon season. Meanwhile, just outside the station walls, India's telecom revolution is exploding—mobile towers sprouting like mushrooms, internet cafes on every corner. The Indian Railways, carrying 23 million passengers daily, was stuck in a communication time warp.

This disconnect between India's digital ambitions and its railway reality would birth one of the country's most fascinating infrastructure plays: RailTel Corporation of India. What started as a desperate need to modernize railway communications would evolve into something far more ambitious—a company that would lay 66,000 kilometers of optical fiber along railway tracks, provide WiFi to millions of train passengers, and eventually list on public markets at a valuation that would make private telcos take notice. Today, with a market cap of ₹11,136 crore, RailTel stands as a testament to what happens when government infrastructure meets commercial ambition. But to understand how a railway PSU became a key player in India's digital infrastructure story, we need to go back to when trains still ran on analog dreams and the internet was just beginning to rewire the world.

The journey we're about to explore isn't just about laying fiber optic cables along railway tracks. It's about how India found a uniquely Indian solution to its infrastructure challenge—leveraging existing assets in ways that private players never could. It's about the tensions between public service and profit, between bureaucratic inertia and entrepreneurial spirit. And ultimately, it's about whether a government-owned enterprise can compete in one of the most cutthroat sectors of the modern economy.

Our story spans the creation of one of the largest neutral telecom infrastructure providers in India owning a Pan-India optic fiber network, the complexities of taking a PSU public during a market boom, and the ongoing challenge of balancing shareholder returns with social obligations. We'll explore how RailTel built its moat, why it matters that it's a "Navratna" company, and what its journey tells us about infrastructure investing in emerging markets.

So buckle up. This isn't your typical tech unicorn story. This is infrastructure at scale, government-style, with all the drama that entails.

II. Origins & The Railway Communication Problem

The year 2000 was pivotal for India. The Y2K bug had been squashed, the dotcom boom was reaching its frenzied peak, and India's IT services industry was beginning its march toward global dominance. But step inside any Indian Railways signal box, and you'd think you'd traveled back to 1950. Train controllers communicated through ancient analog systems that would fail during monsoons, leaving millions of passengers stranded and cargo delayed. The irony was palpable: India was becoming the world's back office, but its own railway communication system belonged in a museum.

The Ministry of Railways faced a crisis that went beyond mere inconvenience. The railway network, spanning 65,000 kilometers and carrying over 8 billion passengers annually, was the circulatory system of the Indian economy. Every communication failure didn't just delay trains—it cascaded through supply chains, disrupted commerce, and in the worst cases, contributed to accidents that claimed lives. The existing overhead telegraph lines and analog phones were not just outdated; they were becoming dangerous in an era demanding split-second coordination.

Enter the vision that would become RailTel. RailTel was incorporated in 2000, with the objective of creating nationwide broadband and VPN services, telecom, and multimedia network, to modernize the train control operation and safety system of Indian Railways. But the real genius wasn't just in modernizing railway communications—it was in recognizing an opportunity hiding in plain sight.

The railways owned something invaluable: right-of-way access across the entire country. Every major city, every commercial hub, every remote town that mattered had railway lines running through it. While private telecom companies were fighting for tower locations and digging up roads for cables, the railways had a ready-made corridor that could host a fiber optic network. It was infrastructure arbitrage at its finest.

The initial mandate from the Ministry of Railways was straightforward: modernize internal communications and improve safety systems. But the team assembling at RailTel's newly minted headquarters in Delhi had bigger ambitions. They weren't just thinking about connecting railway stations; they were envisioning a parallel telecommunications backbone for the entire nation.

The challenges were monumental. How do you lay fiber optic cables along active railway lines without disrupting operations? How do you convince a bureaucracy steeped in tradition to embrace cutting-edge technology? And crucially, how do you fund a massive infrastructure project when the government's telecom budget was already stretched thin?

The answer came through a hybrid model that would define RailTel's DNA. The Company is promoted by and is in administrative control of Ministry of Railways. It is a 100% subsidiary of Ministry of Railways. But unlike traditional government departments, RailTel was incorporated as a Public Sector Undertaking with commercial flexibility. It could raise funds, enter partnerships, and most importantly, sell excess capacity to private players.

By March 2023, RailTel had laid over 66,000 kilometers of optical fiber cables across the country—but in 2000, that journey began with a single kilometer of cable laid along the Delhi-Ambala railway section. The engineers worked at night, when train traffic was minimal. They developed specialized techniques for cable laying that wouldn't interfere with track maintenance. Every meter of progress was a small victory against skeptics who said it couldn't be done.

The early team was a mix of railway veterans who understood the operational realities and young telecom engineers who brought fresh perspectives. This cultural fusion would prove crucial. The railway old-timers knew how to navigate the bureaucracy and understood safety protocols that were non-negotiable. The young engineers pushed for technologies that seemed like science fiction to government officials accustomed to telegraph systems.

One early decision would prove prophetic: RailTel would be a neutral infrastructure provider. Rather than competing with private telcos for end customers, it would provide the backbone that everyone could use. This wasn't just strategic positioning—it was recognition that in India's diverse and competitive telecom market, the real value lay in being the infrastructure layer that others built upon.

By 2001, RailTel had completed its first major stretch: connecting Delhi to Mumbai along the railway corridor. The symbolism wasn't lost on anyone. These two cities represented India's political and commercial hearts, and RailTel had just given them a digital lifeline that ran parallel to the iron rails connecting them since the British Raj.

But the real validation came from an unexpected source. Private telecom operators, initially skeptical of a government PSU entering their domain, began inquiring about leasing capacity. They had spent fortunes acquiring spectrum and building networks, but reaching India's vast hinterland remained prohibitively expensive. RailTel's network, snaking through every corner of the country along railway lines, offered a solution they couldn't replicate.

The foundation was set, but the real infrastructure build was just beginning.

III. The Infrastructure Build: Laying Digital Rails (2000-2010)

The Konkan Railway presented RailTel's first real test. This 741-kilometer stretch, carved through the Western Ghats, was an engineering marvel with 2,000 bridges and 91 tunnels. Laying fiber optic cables here wasn't just technically challenging—it was nearly impossible. The monsoons turned gentle streams into raging torrents, landslides were common, and the terrain was so treacherous that even maintaining the railway line was a constant battle.

Yet this was exactly where RailTel needed to prove itself. If it could wire the Konkan Railway, it could wire anything. The engineering team spent months studying the route, developing waterproof cable housing that could withstand the monsoons, and creating redundancy systems for the inevitable landslides. They pioneered the use of aerial optical fiber cables in certain stretches, stringing them alongside power lines where underground laying was impossible.

The technology choices made during this period would define RailTel's competitive advantage for decades. While private telcos were still debating between different fiber technologies, RailTel made a bold decision: deploy state-of-the-art Dense Wavelength Division Multiplexing (DWDM) technology from day one. This meant higher upfront costs, but it allowed multiple data streams to travel through a single fiber, dramatically increasing capacity without laying additional cables.

RailTel's network passes through around 5,000-6,000 stations across the country, covering all major commercial centers. But reaching this scale required solving a uniquely Indian problem: how do you maintain a sophisticated fiber network across a country where power outages are routine and technical expertise is concentrated in urban centers?

The answer was radical decentralization. RailTel established Network Operation Centers (NOCs) not just in major cities but in tier-2 and tier-3 towns along railway routes. They trained local railway staff in basic fiber optic maintenance, creating a distributed workforce that could respond to issues within hours rather than days. This wasn't just operational efficiency—it was job creation in areas where technical employment was scarce.

By 2005, RailTel had achieved what many thought impossible: a contiguous optical fiber network from Kashmir to Kanyakumari, from Gujarat to Assam. The network map looked like the circulatory system of a giant—main arteries along trunk railway routes, smaller vessels branching into districts, and capillaries reaching remote stations. It was beautiful in its complexity and revolutionary in its reach.

The commercial strategy during this period was equally sophisticated. RailTel positioned itself as the "carrier's carrier"—providing wholesale bandwidth to other telecom operators. This avoided direct competition with powerful private players while capturing value from India's exploding data consumption. Bharti Airtel, Reliance Communications, Tata Communications—they all became RailTel customers, often reluctantly acknowledging that the PSU had built something they couldn't replicate cost-effectively.

But the real innovation was in government services. RailTel became the backbone for critical national projects that private players wouldn't touch due to low returns. The National Knowledge Network, connecting universities and research institutions, ran on RailTel fiber. E-governance initiatives that promised to bring government services online relied on RailTel's reach into rural areas. Defense networks that required absolute reliability chose RailTel's physically secure railway corridors over conventional telecom infrastructure.

The funding model evolved during this period too. Initial capital came from the Ministry of Railways, but RailTel quickly learned to leverage its unique position. International development agencies, seeing the social impact potential, provided soft loans. Equipment vendors, eager to establish themselves in India's growing market, offered favorable credit terms. Revenue from commercial operations was plowed back into expansion, creating a virtuous cycle of growth.

By 2008, RailTel faced a new challenge: success had bred complexity. The network had grown so large and intricate that managing it required sophisticated systems. The company invested heavily in Network Management Systems, creating one of India's first truly integrated telecom operations centers. Real-time monitoring meant issues could be detected and resolved before customers noticed. Predictive maintenance algorithms—primitive by today's AI standards but revolutionary for the time—reduced downtime dramatically.

The human story during this period was equally compelling. RailTel engineers became legends in India's telecom circles. They were the ones who laid cables at 15,000 feet in Ladakh, where oxygen was scarce and temperatures dropped to minus 40. They worked through terrorist threats in Kashmir, Naxalite areas in Central India, and the scorching deserts of Rajasthan. Each kilometer of cable laid was a victory against geography, weather, and sometimes, human conflict.

The organizational culture that emerged was unique—part military precision from the railway heritage, part Silicon Valley innovation from the telecom influence. Morning meetings started with safety briefings, a railway tradition. But they ended with discussions about packet loss rates and bandwidth optimization that would fit perfectly in a tech startup. This cultural duality would become RailTel's secret weapon.

As the decade closed, RailTel had transformed from a railway modernization project into a national asset, but the next phase would test whether a PSU could truly compete in the commercial market.

IV. Transformation & Commercialization (2010-2018)

The meeting that changed RailTel's trajectory happened in a nondescript government office in 2010. The new Minister of Communications and IT had a problem: India's National Optical Fiber Network (NOFN) project, meant to connect 250,000 village panchayats, was stuck. Private players had shown little interest—the economics of rural connectivity didn't compute for shareholder-driven companies. The minister turned to RailTel with a simple question: "Can you do what they won't?"

This moment marked RailTel's transition from infrastructure provider to digital transformation enabler. The company that had spent a decade laying cables would now become the architect of Digital India's most ambitious projects. But first, it needed to transform itself.

The leadership recognized that competing in the commercial market required more than just infrastructure—it needed products and services that customers actually wanted. Enter RailWire, RailTel's bold entry into the retail broadband market. The logic was compelling: RailTel had fiber reaching into areas where no other provider operated. Why not leverage this last-mile advantage?

RailWire broadband service is ranked as the 13th largest broadband provider with over 5.8 lakhs subscribers that is the 4th largest in subscriber count in rural areas of India. But building a consumer business within a PSU was like teaching an elephant to dance. The organization had to develop customer service capabilities, billing systems, and marketing strategies—competencies entirely alien to its engineering DNA.

The solution was partnerships. RailTel created a franchise model where local cable operators and entrepreneurs could become RailWire partners. They handled customer acquisition and service while RailTel provided the backbone. It was infrastructure-as-a-platform before the term became fashionable. The model worked because it aligned incentives: local partners knew their markets, and RailTel could scale without building a massive retail organization. Then came the partnership that would transform RailTel's public perception. The free WiFi service was launched at Mumbai Central railway station in January 2016, marking the beginning of RailTel's collaboration with Google. The tech giant needed infrastructure to execute its ambitious plan to provide free WiFi at Indian railway stations. RailTel had the fiber network, the station access, and crucially, the operational capability to manage such a massive deployment.

Google will use the underlying optic fibre network of Railtel, a unit of the Indian Railways to power its free wi-fi project in over 400 railway stations in the country. The partnership was symbiotic. Google brought global technology expertise and brand credibility. RailTel provided the infrastructure backbone and local execution capability. Together, they would create what would become "the largest public Wi-Fi project in India, and among the largest in the world, by number of potential users".

The execution was remarkable in its speed and scale. In June 2018, Google announced that its Free WiFi project was now running at 400 Indian railway stations. As a result, there were more than 8 million people accessing the internet each month via the project. For many Indians, this was their first taste of high-speed internet. Students downloaded educational materials while waiting for trains. Small business owners conducted video calls with suppliers. Job seekers uploaded resumes and attended virtual interviews.

But the Google partnership taught RailTel something crucial: it could execute complex, consumer-facing projects at scale. When Google decided to wind down the Station program in 2020, RailTel didn't skip a beat. RailTel will continue to service free Wi-Fi in all those railway stations. The company had absorbed the technical know-how and operational excellence. It now manages Currently 6112+ stations are live with RailTel's RailWire Wi-Fi, making it one of the largest and fastest public Wi-Fi networks of the world.

Meanwhile, in 2018, RailTel underwent a major transformation, launching various projects aimed at providing broadband, internet services, and digital services to all major railway stations in India. The company wasn't content being just an infrastructure provider—it wanted to be a full-stack digital services company. Data centers became a strategic focus. As India's data localization requirements tightened and enterprises needed secure, compliant hosting solutions, RailTel's government backing became a competitive advantage rather than a liability.

The data center business wasn't just about rack space and cooling. RailTel understood that government departments and PSUs needed partners who understood their unique requirements—complex tender processes, stringent security audits, and the political sensitivities of data handling. Private players might offer better pricing, but RailTel offered something more valuable: trust and compliance by default.

Project execution became another growth vector. Smart city initiatives, safe city surveillance systems, and e-governance platforms—RailTel bid for and won projects that required not just technical capability but the ability to navigate India's complex federal structure. The company had mastered the art of working with multiple stakeholders: central government ministries, state governments, municipal corporations, and village panchayats.

The organizational transformation during this period was profound. RailTel hired aggressively from the private sector, bringing in talent from IT services companies and telcos. The culture began shifting from pure engineering to customer-centricity. Quality certifications were obtained not as bureaucratic exercises but as genuine attempts to improve service delivery. The company even started participating in industry conferences, something unthinkable for a PSU a decade earlier.

Financial discipline improved markedly. Project selection became more strategic, focusing on high-margin, annuity-based contracts rather than one-time implementations. The company learned to say no to projects that didn't meet return thresholds, a revolutionary concept for an organization accustomed to accepting any government mandate.

By 2018's end, RailTel had transformed from a railway telecom provider to a comprehensive ICT services company. But the biggest transformation was yet to come—taking this government-owned enterprise to the public markets.

V. The IPO Story & Public Markets Journey (2021)

February 16, 2021, 10 AM. The RailTel IPO opened for subscription with a price band of ₹93-94 per share. Within hours, the retail portion was oversubscribed. By the time the IPO closed on February 18, the overall subscription had reached 42.4 times—a staggering vote of confidence in a PSU at a time when government disinvestment had become politically contentious.

But the journey to this moment had begun years earlier. The government's decision to list RailTel wasn't just about raising capital—the company was already profitable and cash-rich. It was about something more strategic: creating a valuation benchmark for government-owned digital infrastructure assets and providing an exit opportunity for the government to reduce its stake over time.

The IPO preparation revealed both RailTel's strengths and the peculiar challenges of taking a PSU public. The company had to completely overhaul its financial reporting systems. PSU accounting, designed for government oversight, had to be translated into formats that capital markets could understand. Independent directors had to be appointed. Investor relations capabilities had to be built from scratch.

The roadshow presentations were a study in contrasts. Investment bankers in sharp suits explaining IoT and edge computing opportunities. RailTel executives, many career railway employees, discussing EBITDA margins and return on capital employed. International investors asking about competitive moats. Government officials ensuring social obligations weren't forgotten in the pursuit of profits.

The timing was fortuitous. India's stock markets were in the midst of a historic bull run. Digital transformation stories were commanding premium valuations. The COVID-19 pandemic had accelerated digital adoption, making RailTel's infrastructure more critical than ever. Retail investors, flush with liquidity and hungry for IPO gains, saw RailTel as a bet on Digital India.

The company's initial public offering raised approximately ₹819 crores. But more importantly, it created a currency—publicly traded stock—that RailTel could potentially use for acquisitions and employee retention. The listing price on February 26, 2021, was around ₹109, a 16% premium to the issue price. Within weeks, the stock touched ₹189, delivering 100% returns to IPO investors.

But the public markets journey hasn't been smooth. Mkt Cap: 11,136 Crore (down -26.9% in 1 year) reflects the volatility that comes with being a listed PSU. The stock has been buffeted by broader market sentiment toward PSUs, concerns about government interference, and questions about growth sustainability.

The quarterly earnings calls became a new form of accountability. Analysts grilled management about receivables—Company has high debtors of 166 days—a chronic issue when your primary customers are government departments with notoriously slow payment cycles. Questions about capital allocation became more pointed. Why was the company sitting on cash instead of paying higher dividends or making acquisitions?

Promoter Holding: 72.8% meant the government remained firmly in control, but minority shareholders now had a voice. The company had to balance government directives with shareholder interests—not always an easy task. When the government wanted RailTel to bid for low-margin rural connectivity projects, the company had to justify it to investors focused on profitability.

The IPO also brought unprecedented transparency. Every contract win was now material information requiring disclosure. Financial results were dissected by analysts and financial media. The company's Wikipedia page went from a stub to a comprehensive article. RailTel executives, accustomed to operating in relative anonymity, found themselves quoted in business newspapers.

Employee dynamics shifted too. The company introduced employee stock options, something unheard of in traditional PSUs. Young engineers who might have jumped to private companies now had skin in the game. The stock price became a daily topic of discussion in the cafeteria. Performance metrics shifted from purely operational to include shareholder value creation.

The competitive landscape post-IPO became more complex. Private companies could no longer dismiss RailTel as a slow-moving PSU. The quarterly results showed a company growing revenues at 30-40% annually, with operating margins that would make many private players envious. The market was forcing RailTel to become more efficient, more aggressive, and more innovative.

But perhaps the most significant change was psychological. Being publicly listed gave RailTel legitimacy in the eyes of private sector partners and customers. International vendors who earlier insisted on onerous payment terms now extended credit. Private enterprises that wouldn't consider a PSU vendor now included RailTel in RFPs. The NSE listing was a stamp of credibility that no government notification could provide.

As 2021 ended, RailTel's market cap had crossed ₹15,000 crores, making it one of the most valuable PSUs outside of oil and banking sectors. But the real test of the public markets journey was just beginning. Could RailTel deliver consistent growth while maintaining its social mandate? Could it compete with nimble private players while navigating government bureaucracy? The next phase would provide answers.

VI. Modern Era: Digital India & Beyond (2021-Present)

August 2024 brought validation that RailTel had long sought: The company was granted the Navratna status in August 2024. In India's PSU hierarchy, this wasn't just a title—it was operational freedom. Navratna companies could invest up to ₹1,000 crores without government approval, enter joint ventures, and most crucially, set their own HR policies. For RailTel, competing with private tech companies for talent, this was game-changing.

The modern RailTel is barely recognizable from its railway communication roots. 1 Aug - RailTel Q1 FY26: 33% revenue growth, INR7,197 Cr order book, INR500 Cr Kavach orders tells a story of transformation. The order book number is particularly striking—it represents multi-year visibility in a sector where quarterly volatility is the norm. The Kavach opportunity represents RailTel's most ambitious technical undertaking yet. KEC International and RailTel have partnered with Kernex Microsystems and Quadrant FutureTek respectively as 'system integrator' for rapid deployment of Kavach system. As of September 2024, the Kavach technology of RailTel – Quadrant FutureTek partnership has been cleared by Research Designs & Standards Organisation (RDSO). This isn't just another signaling project—it's positioning RailTel at the heart of India's railway safety transformation.

KAVACH is an Indian Automatic Train Protection (ATP) system indigenously developed by Research Designs & Standards Organisation (RDSO) in collaboration with Medha Servo Drives, Kernex Microsystems and HBL Power Systems. Initially it was known by the name Train Collision Avoidance System (TCAS). Kavach was adopted by Ministry of Railways as the National ATP System in July 2020. For RailTel, this represents a perfect convergence of its core competencies: railway domain expertise, telecom infrastructure, and system integration capabilities.

The scale of the Kavach opportunity is staggering. In the Budget Estimation of FY2024-25, ₹1.08 lakh crore (US$13 billion) has been allotted to deploy the Kavach 4.0 system in the network. With INR500 Cr Kavach orders already in the bag and the potential for thousands more crores as deployment accelerates, this could become RailTel's largest revenue driver over the next decade.

But Kavach is just one piece of RailTel's modern portfolio. The company has become the go-to partner for government digital initiatives that require both reach and reliability. Smart city projects leverage RailTel's fiber network to connect IoT sensors, surveillance cameras, and traffic management systems. Safe city initiatives rely on RailTel's secure data centers to process and store sensitive surveillance data. E-governance platforms run on RailTel's cloud infrastructure, bringing government services to citizens' smartphones.

1 Aug - RailTel secures Rs. 1663.8 Cr advance work order from BSNL for services till July 2028. This massive BSNL order exemplifies RailTel's new reality—it's no longer just building infrastructure; it's operating critical national systems. The BSNL partnership is particularly strategic. As the government pushes for indigenous 4G and 5G networks, RailTel's fiber backbone becomes essential infrastructure for BSNL's wireless rollout.

The financial performance reflects this transformation. The company's standalone net profit jumped 46.33% to Rs 113.45 crore on a 57.11% rise in net sales to Rs 1,308.28 crore in Q4 FY25 over Q4 FY24. These aren't the steady, single-digit growth rates typical of mature infrastructure companies. This is hyper-growth more associated with tech companies than PSUs.

The workforce has evolved dramatically too. RailTel now employs AI engineers working on predictive maintenance algorithms, cybersecurity experts protecting critical infrastructure, and data scientists optimizing network performance. The company runs hackathons, partners with IITs for research projects, and sends employees to global technology conferences. The cultural transformation from a railway department to a tech company is nearly complete.

Competition has intensified, but RailTel's response has been strategic rather than reactive. Instead of competing on price with private telcos for consumer broadband, it focuses on high-value enterprise and government contracts. Instead of bidding for every project, it cherry-picks opportunities that leverage its unique advantages—railway corridor access, government trust, and pan-India presence.

The international ambitions are particularly intriguing. The railways on Wednesday inked an agreement with a tech firm for "exploring and delivering" train collision avoidance system KAVACH implementation projects in India as well as other countries. In the statement, RailTel said the agreement with the tech firm is for "exploring and delivering KAVACH (train collision avoidance system) implementation projects in India as well as other countries". Countries across Asia and Africa, many with railway systems built during colonial times, face similar modernization challenges. RailTel's experience retrofitting legacy infrastructure with modern technology could become an exportable expertise.

The data center business has emerged as a dark horse. With data localization laws tightening and enterprises increasingly concerned about data sovereignty, RailTel's government-backed data centers offer something unique: compliance by default. Banks storing customer data, healthcare companies managing patient records, and government departments handling citizen information—all find comfort in RailTel's sovereign data centers.

Edge computing represents the next frontier. As 5G networks roll out and IoT devices proliferate, computing needs to move closer to the data source. RailTel's 6,000+ railway stations, already connected by fiber and powered reliably, are perfect edge computing locations. The company is piloting micro data centers at major stations, turning railway infrastructure into distributed computing infrastructure.

The digital payments revolution has created another opportunity. Railway stations are becoming digital transaction hubs—ticket bookings, platform vendor payments, parking fees. RailTel is positioning itself as the digital backbone enabling this transformation, providing not just connectivity but also payment processing infrastructure.

But challenges remain acute. The receivables issue—166 days of debtors—remains a persistent concern for investors. Government departments' payment delays affect cash flow and limit growth investments. The company has implemented stricter credit policies and is diversifying its customer base, but the fundamental issue of PSU payment culture persists.

Talent retention is another challenge. Young engineers trained by RailTel are constantly poached by private tech companies offering multiples of government salaries. The company has responded with performance bonuses, international training opportunities, and stock options, but competing with Silicon Valley-style compensation remains difficult.

As we look toward the future, RailTel stands at an inflection point where its infrastructure monopoly meets India's digital transformation ambitions.

VII. Business Model & Financial Architecture

The genius of RailTel's business model lies in what economists call "asset sweating"—extracting maximum value from existing infrastructure with minimal incremental investment. When RailTel lays fiber along a railway track, the primary purpose might be railway signaling, but the same fiber can simultaneously serve telecom operators, enterprise customers, and broadband users. The marginal cost of adding capacity is negligible, but each new revenue stream flows almost directly to the bottom line.

The Company's segments include Telecom Services and Project Work Services. This two-segment structure appears simple but masks sophisticated financial engineering. Telecom Services provides predictable, annuity-like revenues—bandwidth leasing contracts typically run 3-5 years with annual escalations. Project Work Services offers lumpy but high-margin revenues from government contracts. Together, they create a balanced portfolio that smooths earnings volatility.

The Telecom Services segment is the cash cow. It provides a range of telecom services to its customers, including managed data services, leased line, virtual private network, Internet leased line, data center, tower collocation, rack and space and national long-distance (NLD) for voice carriage. These services require minimal ongoing investment once infrastructure is in place. A fiber cable laid in 2005 still generates revenues in 2025 with only maintenance costs. This creates enormous operating leverage—revenue growth flows disproportionately to profits.

The Project Work Services segment is where growth happens. The Project Work Services segment includes various projects, such as national optical fiber network, telecom and information technology (IT) services related projects and enterprise-specific IT and information technology-enabled services (ITES) projects. These projects, while requiring upfront capital and execution risk, offer 15-25% EBITDA margins—exceptional for government contracts.

Let's dissect the financials. Revenue: 3,663 Cr, Profit: 317 Cr implies a net margin of 8.7%, respectable but not spectacular. But this understates the true economics. Much of the revenue includes pass-through equipment costs in project work. The core telecom services business likely operates at 30-40% EBITDA margins, comparable to global infrastructure monopolies.

The working capital challenge deserves special attention. Company has high debtors of 166 days isn't just a number—it's a structural feature of doing business with the government. RailTel essentially provides vendor financing to the Government of India. This creates a paradox: the company is profitable and cash-generative, but cash flow lags profits by 5-6 months.

Management has implemented several strategies to address this. Factoring arrangements with banks provide immediate liquidity at a cost. Stricter payment terms for new contracts include interest on delays. The company increasingly insists on advance payments for equipment procurement. But fundamentally, this is the price of accessing government contracts that private players can't win.

The capital allocation framework reflects PSU dynamics. Dividend policy must balance shareholder returns with growth investment needs. The government, holding 72.8%, needs dividend income to meet fiscal targets. But aggressive dividends could starve growth investments. RailTel has settled on a 30% payout ratio—enough to satisfy the government while retaining capital for expansion.

Investment decisions follow a unique calculus. Every project must meet three criteria: financial returns above the cost of capital, strategic alignment with government priorities, and social impact metrics. This triple bottom line approach means RailTel sometimes takes projects that pure commercial players would reject. Rural broadband deployment might not meet private equity return thresholds, but it creates social value that justifies below-market returns.

The pricing strategy is particularly nuanced. For government contracts, RailTel often prices at cost-plus, accepting lower margins for volume and strategic importance. For private sector clients, pricing is market-based, extracting premium for reliability and reach. This differential pricing maximizes both revenue and social impact, though it complicates margin analysis.

Revenue recognition adds another layer of complexity. Project revenues follow percentage completion method, requiring judgment about project progress. Telecom services revenues are recognized monthly, but collection lags create timing differences. The company maintains conservative accounting policies, often recognizing costs immediately while deferring revenue recognition until collection certainty improves.

The order book provides visibility but requires careful interpretation. INR7,197 Cr order book represents 2 years of revenue visibility, but execution timelines vary widely. Some projects execute over months; others span years. Government contracts can face delays from budget constraints, policy changes, or administrative issues. The order book is better viewed as direction indicator than precise forecast.

Cost structure reveals operational leverage. Fixed costs—primarily employee expenses and infrastructure maintenance—represent about 40% of revenues. Variable costs are mainly project-related equipment and subcontracting. This means revenue growth above 15% annually drives margin expansion, while slower growth pressures profitability. The company targets 20-25% revenue growth to optimize this leverage.

Research and development spending, minimal by tech company standards at 1-2% of revenue, focuses on practical applications rather than basic research. Projects include network optimization algorithms, predictive maintenance systems, and cybersecurity tools. The approach is pragmatic—solve immediate problems rather than pursue breakthrough innovations.

Financing strategy remains conservative. Despite negligible debt, the company maintains significant credit lines for working capital needs. Long-term debt is avoided, reflecting both strong cash generation and PSU aversion to financial leverage. This under-leveraged balance sheet could theoretically support significant debt-funded expansion, but cultural and governance factors preclude aggressive financing strategies.

The enterprise value creation model differs from typical listed companies. Short-term earnings volatility is tolerated for long-term strategic positioning. Investments in seemingly unprofitable rural infrastructure create option value for future monetization. Government relationships, impossible to value on spreadsheets, generate order flow that wouldn't exist in pure commercial relationships.

Currency exposure is minimal despite international ambitions. Most contracts are INR-denominated, and foreign equipment purchases are hedged. This limits forex gains but also protects against rupee volatility—appropriate for a company whose investors seek stability over speculation.

Tax strategy is straightforward—pay statutory rates without aggressive optimization. As a PSU, RailTel avoids complex structures that might reduce taxes but invite scrutiny. The effective tax rate of 25-30% is accepted as the price of maintaining government trust and social license.

Understanding RailTel's financial architecture requires appreciating these contradictions: profitable but cash-constrained, growing but conservative, commercial but socially conscious. It's a model that shouldn't work in theory but does in practice—because it's perfectly adapted to India's unique political economy. The question for investors isn't whether this model is optimal, but whether it's sustainable as India's economy evolves.

VIII. Playbook: The PSU Infrastructure Model

Every country has its own version of the infrastructure challenge: how do you build capital-intensive, long-term assets that markets under-provide but societies desperately need? America tried private monopolies regulated by government. China deployed state capital at unprecedented scale. Europe created public-private partnerships with mixed results. India's answer, embodied by RailTel, is more nuanced—leverage existing government assets through corporatized entities that straddle public purpose and private efficiency.

The first principle of the PSU infrastructure playbook: start with an unfair advantage. RailTel didn't begin by competing with private telcos for customers or spectrum. It began with something private players could never replicate—right-of-way access along 65,000 kilometers of railway tracks. This wasn't just physical access; it was institutional access, cultural legitimacy, and operational synergy built over 150 years of railway operations.

The second principle: be the infrastructure layer, not the application layer. RailTel could have become a consumer telecom brand, competing with Airtel and Jio for mobile subscribers. Instead, it chose to be the wholesale provider that everyone needs but no one sees. This positioning avoided direct confrontation with politically powerful private players while capturing value from the entire ecosystem's growth.

The neutral provider strategy deserves deeper examination. In markets with fierce competition and thin margins, being Switzerland has value. Telecom operators trust RailTel with their traffic because it doesn't compete for their customers. Government departments prefer RailTel because it understands their procurement processes. Enterprises choose RailTel when they need reliability over innovation. Neutrality becomes a competitive advantage when everyone else is fighting.

Managing stakeholder complexity is perhaps the hardest part of the PSU playbook. The Ministry of Railways wants better train communications. The Department of Telecom wants rural connectivity. The Finance Ministry wants dividends. Public shareholders want capital appreciation. Employees want job security and growth. Each stakeholder has veto power over certain decisions. Success requires not choosing between stakeholders but finding solutions that satisfy multiple constituencies simultaneously.

Consider RailTel's approach to rural connectivity. Pure commercial logic would avoid rural markets—low revenues, high costs, terrible returns. But RailTel frames rural connectivity as infrastructure investment that creates future option value. Today's unprofitable rural broadband connection becomes tomorrow's digital payment node, e-governance access point, and telemedicine center. The social impact justifies below-market returns while creating long-term commercial opportunities.

The PSU model also provides unique crisis resilience. During COVID-19, when private companies laid off employees and cut investments, RailTel accelerated hiring and expanded infrastructure spending. This counter-cyclical behavior, impossible for quarterly earnings-focused private companies, positioned RailTel to capture market share during the recovery. Government backing means PSUs can think in decades while private players think in quarters.

But the model has inherent limitations. Decision-making velocity is structurally slower than private competitors. A private telco CEO can approve a major investment over lunch. RailTel needs board approval, ministry consultation, and sometimes cabinet clearance. By the time decisions are made, market opportunities might have passed. The solution isn't faster decisions but better anticipation—positioning for obvious future trends rather than chasing current fads.

Talent management in the PSU model requires creativity. Government pay scales can't match private sector compensation, especially for technical roles. RailTel's solution is to offer what money can't buy—the opportunity to work on nation-building projects at unprecedented scale. The engineer who connected 400 railway stations to WiFi has a story no corporate job can match. Purpose becomes compensation.

The procurement advantage is real but double-edged. Government contracts often specify PSU preference, giving RailTel an inside track. But these contracts come with stringent audit requirements, social obligations, and political scrutiny. Every contract is potential front-page news if something goes wrong. Risk management becomes existential—one scandal can destroy decades of reputation building.

International expansion showcases both opportunities and challenges of the PSU model. RailTel's government backing opens doors in countries seeking alternatives to Chinese infrastructure investment. But the same backing creates suspicion about strategic intentions. The solution is partnering with local companies, transferring technology rather than owning assets, and positioning as capability builder rather than infrastructure owner.

The financial discipline required in this model is unique. PSUs must be profitable enough to justify their existence but not so profitable that they're accused of monopolistic behavior. They must invest aggressively in infrastructure but maintain conservative balance sheets. They must pay dividends to government but retain capital for growth. Threading these needles requires financial acrobatics that would challenge any CFO.

Innovation in the PSU model follows a different path. Rather than disrupting existing systems, PSUs excel at incremental innovation that improves reliability and reduces costs. RailTel's innovations—using railway stations as data centers, deploying aerial fiber in difficult terrain, creating distributed network operations centers—aren't revolutionary but they're perfectly adapted to Indian conditions.

The governance evolution has been remarkable. Independent directors now constitute board majorities. Audit committees have real teeth. Transparency requirements exceed many private companies. This governance upgrade wasn't voluntary—capital markets demanded it—but it's transformed PSU operations. The old stereotype of corrupt, inefficient government companies increasingly doesn't match reality, at least for Navratna PSUs.

Competition with private players requires asymmetric strategies. Private telcos have better technology, faster decision-making, and deeper pockets. RailTel competes on trust, reach, and patience. When a government department needs critical infrastructure that must work for decades, RailTel's boring reliability beats private sector innovation. When a rural area needs connectivity that won't generate profits for years, RailTel's social mandate beats private sector ROI requirements.

The sustainability question looms large. Can the PSU model survive as India's economy becomes more market-oriented? The answer depends on adaptation. RailTel is evolving from pure infrastructure provider to digital services platform. The railway heritage becomes less important than digital capabilities. Government ownership becomes less about control than about patient capital. The PSU model isn't disappearing; it's transforming.

Looking globally, the RailTel playbook offers lessons for other emerging markets. Countries with extensive government infrastructure—railways, highways, power grids—can create value by corporatizing these assets and leveraging them for digital infrastructure. The key is maintaining government support while operating with commercial discipline. It's a difficult balance, but when it works, it creates unique value that neither pure government nor pure private models can match.

The ultimate test of the PSU infrastructure model isn't financial returns but social impact. Has RailTel made India more connected? Has it improved railway safety? Has it enabled digital inclusion? By these metrics, the model has succeeded beyond expectations. The challenge now is maintaining this social impact while delivering returns that keep investors engaged—a challenge that will define RailTel's next chapter.

IX. Analysis & Investment Case

The bull case for RailTel writes itself: a monopolistic infrastructure asset, backed by the government, riding India's digital transformation wave, with minimal debt and growing at 30%+ annually. At ₹11,136 crores market cap, you're buying 66,000 kilometers of fiber optic cable, relationships with every government department, and option value on India's digital future. In developed markets, similar infrastructure assets trade at 15-20x EBITDA. RailTel trades at less than 10x.

But the bear case is equally compelling. Company has high debtors of 166 days isn't just a working capital issue—it's symptomatic of deeper structural problems. Government customers pay slowly, sometimes not at all if budgets are cut. The company has limited recourse against its largest customer, creating existential risk that private companies don't face. The 72.8% government ownership means minority shareholders have no real say in strategic decisions.

Mkt Cap: 11,136 Crore (down -26.9% in 1 year) tells us the market is skeptical. While revenues and profits grow, the stock price languishes. This isn't just about RailTel—it's about investor fatigue with PSUs generally. The market has been burned by government interference, policy flip-flops, and value-destructive decisions made for political rather than commercial reasons.

Competition is intensifying from unexpected directions. Reliance Jio, with unlimited capital and aggressive ambitions, is building its own fiber infrastructure rather than leasing from RailTel. Data center giants like Amazon and Microsoft are creating their own connectivity solutions. Starlink and other satellite providers could make terrestrial fiber obsolete in rural areas. RailTel's moat is wide but not impregnable.

The valuation puzzle requires careful consideration. On traditional metrics, RailTel looks cheap. P/E ratios in the low teens for a company growing at 30%+ seems like obvious mispricing. But these metrics assume earnings quality and growth sustainability that might not exist. When your largest customer is the government and your growth depends on political priorities, traditional valuation models break down.

The comparison with private telcos is instructive but misleading. Bharti Airtel trades at premium valuations despite lower growth because it has pricing power, customer ownership, and strategic flexibility RailTel lacks. Jio commands high multiples because markets believe in its platform ambitions. RailTel, despite superior infrastructure, trades at discounts because markets don't trust PSU governance and capital allocation.

The Navratna advantage is real but limited. The company was granted the Navratna status in August 2024. This provides operational autonomy—investment decisions up to ₹1,000 crores, international ventures, organizational restructuring. But core limitations remain. Pricing decisions on government contracts still face political pressure. Employment policies must consider social objectives. Investment decisions must balance commercial returns with public purpose.

Future growth drivers are compelling on paper. The 5G rollout requires massive fiber densification—every tower needs fiber backhaul. Smart cities need ubiquitous connectivity for IoT sensors. Railway modernization, including the Kavach rollout, requires sophisticated communication networks. Digital India initiatives depend on reliable infrastructure. RailTel is positioned at the center of all these trends.

But execution risk is substantial. Government projects face delays, scope changes, and payment issues. Technology evolution could strand investments—what if satellite internet makes fiber obsolete? Talent retention challenges could impact service quality. One major project failure or scandal could trigger government intervention that destroys shareholder value.

The investment case ultimately depends on your view of India's political economy. Optimists see RailTel as a proxy for Digital India—as the country digitizes, RailTel inevitably benefits. The government backing provides downside protection while growth potential remains enormous. Patient investors willing to tolerate PSU governance issues could see multibagger returns.

Pessimists see a value trap—optically cheap but structurally impaired. The government ownership means profits will be extracted through dividends or social mandates rather than accruing to shareholders. Competition will erode margins. Working capital issues will constrain growth. The stock will remain permanently undervalued because markets rationally discount PSU governance risks.

The middle path sees RailTel as a portfolio diversifier rather than core holding. It provides exposure to India's infrastructure buildout with government backing that reduces bankruptcy risk. The dividend yield, while modest, is sustainable. The stock won't be a multibagger, but it could deliver steady high-teens returns with lower volatility than pure private sector plays.

Risk factors deserve careful enumeration. Regulatory changes could force infrastructure sharing at uneconomic rates. Government policy could prioritize social objectives over profitability. Technology disruption could obsolete fiber infrastructure. Competition could cherry-pick profitable segments while leaving RailTel with social obligations. Key person risk is real—PSU leadership changes can dramatically impact strategy and execution.

The quality of earnings needs scrutiny. Revenue recognition on long-term projects involves estimates that could prove wrong. Receivables might need write-offs if government departments renege. Order book conversion depends on factors outside management control. Reported profits might not convert to cash flows if working capital issues persist.

Environmental, social, and governance (ESG) factors cut both ways. The social impact is undeniable—connecting rural India, enabling digital inclusion, improving railway safety. Governance has improved with independent directors and transparency requirements. But government ownership means true independence is impossible. Environmental impact from infrastructure deployment needs better disclosure.

Catalysts for rerating exist but require patience. Working capital improvement through better payment terms or factoring arrangements. Major contract wins that demonstrate competitive strength. Successful international expansion proving export potential. Government stake reduction improving float and governance. Technology partnerships that enhance capabilities.

The margin of safety calculation is complex. At current valuations, you're paying roughly book value for assets that would cost multiples to replicate. The replacement cost of 66,000 kilometers of fiber optic cable exceeds RailTel's enterprise value. But PSU assets have historically traded below replacement cost because markets doubt value realization potential.

For fundamental investors, RailTel presents a fascinating puzzle. The infrastructure is invaluable. The growth opportunity is enormous. The government backing provides stability. But the governance constraints, competitive threats, and execution risks are equally real. This isn't a simple value play or growth story—it's a complex bet on India's digital transformation filtered through the peculiar dynamics of PSU operations.

The investment decision ultimately comes down to time horizon and risk tolerance. For investors seeking quick returns and clear catalysts, RailTel will disappoint. For those willing to own infrastructure assets through cycles, accepting PSU limitations for monopolistic advantages, RailTel could deliver satisfactory returns. The key is sizing positions appropriately—enough to benefit from the upside, not so much that PSU-specific risks dominate portfolio outcomes.

X. Epilogue & Future Outlook

Stand at New Delhi Railway Station today and you'll witness a peculiar convergence. Above, high-speed trains guided by digital signaling systems. Below, kilometers of fiber optic cables humming with data. Around you, thousands of passengers streaming HD videos on free WiFi. This scene, impossible to imagine when RailTel was founded in 2000, represents something larger than infrastructure evolution—it's the physical manifestation of India's digital transformation, where railway heritage meets silicon ambitions.

The convergence of railways and digital infrastructure isn't coincidental; it's inevitable. Railways were the original network businesses—moving people and goods across vast distances, creating economic value through connectivity. Digital infrastructure follows the same logic—moving data across networks, creating value through information flow. RailTel sits at this intersection, transforming iron rails into digital highways.

Artificial intelligence and IoT are about to revolutionize railway operations in ways that make Kavach look primitive. Predictive maintenance algorithms will anticipate failures before they occur. Dynamic pricing will optimize passenger loads. Autonomous trains will eliminate human error. Smart stations will adapt to passenger flow in real-time. Each innovation requires robust, reliable, ubiquitous connectivity—exactly what RailTel provides.

But can RailTel compete with tech giants and telcos that have deeper pockets and faster reflexes? The question misframes the challenge. RailTel doesn't need to out-innovate Google or outspend Jio. It needs to be the reliable infrastructure layer that others build upon. When Google wanted to provide railway WiFi, it needed RailTel's infrastructure. When the government wants to deploy Kavach, it needs RailTel's expertise. The competitive advantage isn't in being cutting-edge; it's in being essential.

The role of PSUs in India's digital future is evolving from provider to enabler. The old model—government monopolies providing basic services—is dead. The new model—government-backed platforms enabling private innovation—is emerging. RailTel exemplifies this evolution. It doesn't compete with private players for end customers; it provides the infrastructure that makes private innovation possible.

Consider the metaverse ambitions that tech companies trumpet. Virtual worlds require massive data transmission, edge computing, and near-zero latency. RailTel's 6,000 railway stations, connected by fiber and distributed across India's geography, could become edge computing nodes for metaverse applications. The company that started by modernizing railway communications could enable India's virtual future.

Climate change adds another dimension. As extreme weather events become common, infrastructure resilience becomes critical. RailTel's cables, buried along railway tracks or strung aerially, have survived floods, cyclones, and heat waves that destroyed conventional infrastructure. This resilience, built through decades of experience with India's challenging conditions, becomes increasingly valuable as climate impacts intensify.

The geopolitical environment favors RailTel's model. As countries worry about digital sovereignty and infrastructure security, government-backed providers gain advantage over foreign corporations. RailTel's expansion into South Asia and Africa leverages this trend. Countries seeking alternatives to Chinese infrastructure investment find comfort in India's democratic credentials and RailTel's government backing.

5G and beyond present opportunities and threats. The opportunity is obvious—5G requires fiber densification that plays to RailTel's strengths. Every 5G tower needs fiber backhaul. Every edge computing node needs connectivity. The threat is subtle—if satellite internet achieves promises of universal coverage at minimal cost, terrestrial fiber could become obsolete. RailTel's response must be to move up the value chain from pure connectivity to integrated digital services.

The demographic dividend amplifies RailTel's importance. India adds 10 million internet users monthly. Each user demands more bandwidth for video streaming, online gaming, and virtual collaboration. This exponential data growth requires continuous infrastructure investment. Private players will build consumer-facing services, but they'll rely on wholesale infrastructure providers like RailTel for backbone capacity.

Regulatory evolution could transform RailTel's economics. Infrastructure sharing mandates could force private players to use RailTel's fiber rather than building parallel networks. Data localization requirements could drive demand for sovereign data centers. Universal service obligations could direct government subsidies to rural connectivity providers. Each regulatory change could expand RailTel's addressable market.

The human story remains central. RailTel employs thousands of engineers who chose public service over private sector riches. Their motivation isn't stock options but nation-building. This workforce, technically competent and mission-driven, represents intangible value not captured in financial statements. As India grapples with inequality and social division, institutions like RailTel that balance commercial success with social purpose become more, not less, important.

Financial markets will eventually recognize RailTel's value, but timing remains uncertain. The current disconnect between operational performance and stock price can't persist indefinitely. Either operations will deteriorate to match valuations, or valuations will rise to match operations. History suggests the latter is more likely, but investors need patience measured in years, not quarters.

The key question isn't whether RailTel will survive—government backing ensures that. It's whether RailTel can evolve from infrastructure provider to digital platform, from PSU to quasi-commercial entity, from domestic player to regional champion. Early evidence is promising. The Navratna status provides operational flexibility. The order book demonstrates commercial competitiveness. The Kavach partnership shows technical capability.

For long-term investors, RailTel offers a unique proposition: ownership of critical infrastructure with option value on India's digital future. The infrastructure alone—66,000 kilometers of fiber optic cable—justifies current valuations. Everything else—data centers, railway modernization, smart cities, international expansion—is free optionality. In a world of expensive markets and scarce value, that's increasingly rare.

The RailTel story ultimately transcends financial returns. It's about how societies build infrastructure that markets won't provide but development requires. It's about balancing public purpose with private efficiency. It's about leveraging historical assets for future opportunities. Whether you're an investor, policy maker, or citizen, RailTel's journey offers lessons about infrastructure, governance, and the peculiar genius of India's mixed economy model.

As trains hurtle through the Indian countryside, guided by signals transmitted through RailTel's cables, carrying passengers connected through RailTel's WiFi, we witness infrastructure poetry—the old enabling the new, the physical supporting the digital, the government empowering the private. RailTel isn't just laying cables; it's laying the foundation for India's digital century. The question for investors isn't whether to participate in this transformation, but how much volatility they can stomach along the way.

The convergence of railways and digital infrastructure that RailTel embodies isn't ending; it's just beginning. As India grows from a $3.5 trillion to a $10 trillion economy, as 500 million more Indians come online, as trains become smarter and cities become connected, RailTel's infrastructure becomes not less but more critical. The company that started as a railway modernization project could become the backbone of Digital India—a transformation as profound as the railways themselves were two centuries ago.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube