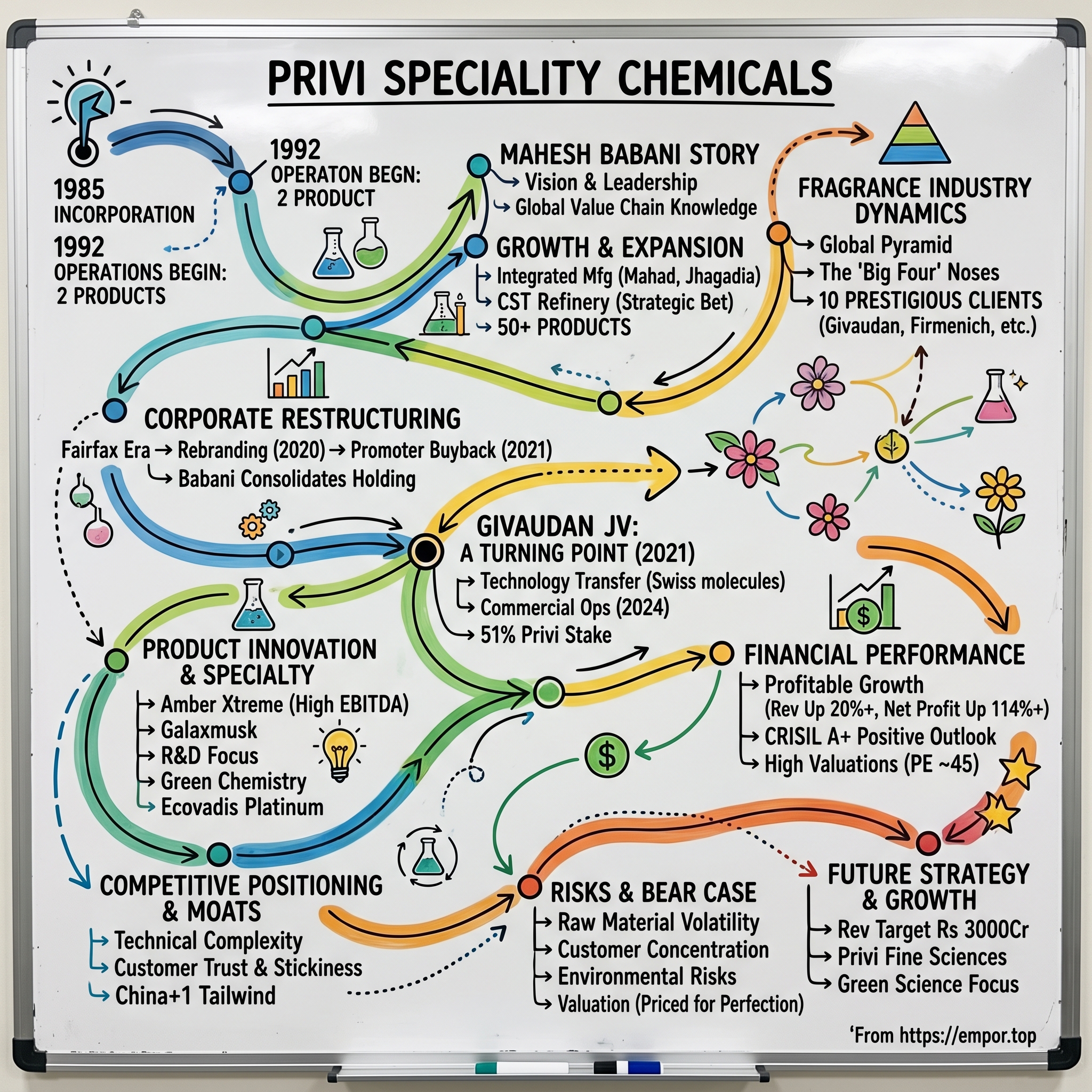

Privi Speciality Chemicals: The Sweet Smell of Success

I. Introduction & Episode Setup

Close your eyes and take a deep breath. That fresh scent in your morning shampoo, the sophisticated notes in your cologne, the clean smell of your laundry detergent—they all share a secret. Behind these everyday fragrances lies a complex global supply chain of specialty chemicals, and at its heart sits an unlikely champion: a company from Maharashtra, India, that most people have never heard of, yet touches billions of lives daily.

Privi Speciality Chemicals commands over 20% global market share in ten different aroma chemical products. Think about that for a moment—one in five molecules of certain key fragrance ingredients worldwide comes from this single Indian company. Their chemicals end up in products made by Procter & Gamble, Reckitt Benckiser, and virtually every major fragrance house from Paris to New York. Yet mention "PRIVISCL" at a dinner party, and you'll get blank stares.

This is the paradox of B2B specialty chemicals: the most successful companies are often the most invisible. While consumer brands fight for mindshare, companies like Privi quietly build monopolistic positions in niche markets, generating returns that would make Silicon Valley jealous. The stock has delivered remarkable returns to early believers, but the real story isn't just about financial performance—it's about how a small Indian startup cracked one of the most technically complex and relationship-driven industries in the world. The aroma chemicals industry is a $25 billion global market growing at 4-5% annually, yet it remains concentrated among a handful of players who have mastered the delicate balance of chemistry, scale, and customer trust. Nearly 10 of the world's largest and most prestigious fragrance companies—including Givaudan, Firmenich, Symrise, Mane, IFF, P&G, and Reckitt Benckiser—are Privi's clients. The company specializes in manufacturing, supplying, and exporting bulk aroma and fragrance chemicals, with a market cap of ₹9,491 crores, revenue of ₹2,196 crores, and profit of ₹211 crores.

What makes this story remarkable isn't just the numbers—it's the audacity. Imagine competing against Swiss and German giants with centuries of expertise, convincing the world's pickiest customers to trust you with their most closely guarded formulations, and doing it all from industrial estates in Maharashtra and Gujarat. This is a story about chemistry, certainly, but it's equally about the chemistry of building trust, the molecular structure of competitive advantage, and the complex reactions that occur when Indian entrepreneurship meets global opportunity.

Our journey today takes us from a small startup in 1992 with just two products to a company with over 50 products and 40,000 tons of annual capacity. We'll explore how Privi cracked the code of one of the most technically challenging industries, why Givaudan—the Swiss fragrance giant—chose them as their joint venture partner, and what this means for investors looking at the intersection of specialty chemicals and the India story. Because make no mistake: while you may never see Privi's name on a product label, their molecules are everywhere, and their story offers profound lessons about building global champions from emerging markets.

II. Origins & The Mahesh Babani Story

The year was 1992. India had just liberalized its economy, unleashing entrepreneurial energy that had been bottled up for decades. In this transformative moment, Mahesh Babani saw an opportunity that others had overlooked: the complex, technical world of aroma chemicals. While others rushed toward consumer-facing businesses or IT services, Babani chose molecules—specifically, the intricate compounds that create the fragrances we encounter every day.

Incorporated in 1985, Privi Speciality Chemicals Ltd (Formerly known as Privi Speciality Ltd.) is primarily engaged in the manufacturing, supply and exports of aroma and fragrance chemicals used in soaps, detergents, shampoos, and other fine fragrances. But the real story begins in 1992, when Babani transformed what was essentially a dormant entity into an operational aroma chemicals manufacturer. Privi started manufacturing aroma chemicals in the year 1992 with only two products, which it gradually expanded to a range of over 50 products today, having a capacity of over 40,000 tons per annum.

Picture the early days: a small facility in Maharashtra, basic equipment, and the daunting task of competing against established European players who had been perfecting their craft since the 19th century. Babani's vision wasn't to create another commodity chemicals company—India already had plenty of those. Instead, he targeted the high-value, technically complex molecules that required sophisticated chemistry and, crucially, the trust of global fragrance houses.

The Indian chemical industry in the early 1990s was at an inflection point. Liberalization meant access to imported technology and raw materials, but it also meant facing global competition head-on. For a startup in specialty chemicals, the challenges were immense: acquiring technical knowledge, building manufacturing capabilities that could meet international standards, and perhaps most difficult, convincing sophisticated Western buyers to source critical ingredients from an unknown Indian company. Mahesh Babani is a Commerce Graduate and has operational and managerial experience of over 30 years. But numbers on a résumé don't capture the entrepreneurial fire that drove him. He took reins of the Company in 1989 and became Managing Director in 2001, with his passion driving the company from a startup to its current scale.

What's fascinating about Babani's approach was his deep, almost obsessive focus on understanding the entire value chain. Over the past two decades, he travelled extensively across the globe and developed deep knowledge of the entire value chain of Aroma Chemical Business—from sourcing of raw materials to their processing and to the final consumers. This wasn't a desk-bound executive making decisions from spreadsheets; this was someone who understood the business at a molecular level, both literally and figuratively.

The early years were about survival and learning. Starting with just two products meant every customer mattered, every batch had to be perfect, and every relationship needed nurturing. The company faced the classic challenges of Indian manufacturing in the 1990s: erratic power supply, limited access to sophisticated equipment, and the constant need to prove that "Made in India" could meet global standards.

But Babani had chosen his battlefield wisely. The B2B invisibility that might have deterred others was actually a strategic advantage. While consumer brands battled for shelf space and advertising dollars, Privi could focus entirely on the only metrics that mattered in specialty chemicals: quality, consistency, and cost. No need for celebrity endorsements or Super Bowl ads—just molecules that worked exactly as promised, delivered on time, at a price that made CFOs smile.

The technical challenges were immense. Aroma chemicals aren't simple compounds you can cook up in a basic lab. They require sophisticated organic chemistry capabilities—hydrogenation, Grignard reactions, high vacuum distillation—processes that demand not just equipment but deep technical expertise. Building this capability from scratch in India, where the chemical industry was still largely focused on basic and commodity chemicals, was like trying to build a Swiss watch factory in a town known for making hammers.

Alongside Babani was D.B. Rao, one of the founders who had been on the Board of Directors since 1982, overseeing Operations, Research & Development, Personnel and raw material sourcing. Rao worked diligently in converting the vision to reality, handling various projects from conception to completion, and was instrumental in putting up manufacturing facilities in a swift and cost-effective manner.

The partnership between Babani's commercial acumen and Rao's technical expertise would prove crucial. While Babani traveled the world, building relationships and understanding market needs, Rao ensured that back home, the factories could deliver on those promises. It was a classic combination—the visionary and the executor—that would drive Privi's growth for decades to come.

By the late 1990s, Privi had survived its baptism by fire. The company had proven it could manufacture quality aroma chemicals, had established initial customer relationships, and most importantly, had begun to understand what it would take to compete globally. The stage was set for expansion, but first, Babani needed to understand the industry he was trying to disrupt—an industry dominated by century-old European giants who viewed their formulations as closely guarded secrets and their supplier relationships as sacred bonds.

III. The Fragrance Industry Primer & Market Dynamics

To understand Privi's audacious ambition, you first need to understand the almost feudal structure of the global fragrance industry. Picture a pyramid: at the apex sit the "Big Four"—Givaudan, Firmenich (now merged with DSM), IFF (International Flavors & Fragrances), and Symrise. These companies don't just dominate; they define the industry. Together, they control over 60% of the global fragrance market, with Givaudan alone commanding nearly 25% market share.

These aren't companies; they're institutions. Givaudan traces its roots to 1768 in Grasse, France—the perfume capital of the world. Firmenich was founded in 1895 in Geneva. These firms don't just make fragrances; they create the olfactory culture of our civilization. When Chanel needs a new perfume, when P&G wants to reformulate Tide's scent, when Unilever decides to launch a new deodorant line—they turn to these houses.

The fragrance houses operate like medieval guilds crossed with modern R&D labs. Their perfumers—called "noses" in industry parlance—train for years, sometimes decades, to master the art of blending hundreds of raw materials into harmonious compositions. These aren't just chemists; they're artists who happen to work in molecules instead of paint. A master perfumer at Givaudan might work on fragrances that will be smelled by a billion people, yet remain completely anonymous to the public.

Below the Big Four sits a second tier of regional players—companies like Mane, Robertet, and Takasago—each with their own specialties and regional strengths. And below them? That's where the aroma chemical manufacturers come in—the companies that actually produce the building blocks these fragrance houses use to create their masterpieces.

This is where the industry gets interesting from a business perspective. While the fragrance houses jealously guard their formulations—a perfume might contain 50-200 different ingredients in precise ratios—they don't manufacture most of these ingredients themselves. Instead, they source from specialized chemical companies that can produce specific molecules at scale, with consistency, and at acceptable costs.

The aroma chemicals market itself is a $25 billion global industry, growing at 4-5% annually, driven by rising incomes in emerging markets and the increasing use of fragrances in everyday products. But here's the catch: it's an incredibly complex market. There are over 3,000 different aroma chemicals in commercial use, ranging from simple esters that smell like fruits to complex musks that require 15-step synthesis processes.

Nearly 10 of the world's largest and prestigious fragrance companies are Privi's clients, including Givaudan, Firmenich, Symrise, Mane, IFF, P&G, and Reckitt Benckiser. Think about what this means: these companies, with centuries of combined experience and relationships with suppliers worldwide, chose to source critical ingredients from an Indian company that didn't exist when the Berlin Wall fell.

India's advantages in this space are multifaceted but not immediately obvious. Yes, there's the cost advantage—Indian chemical engineers earn a fraction of their Swiss or German counterparts. But that's table stakes. The real advantages run deeper:

First, chemistry talent. India produces more chemistry graduates than almost any country on Earth, a legacy of post-independence industrial policy that emphasized technical education. The Indian Institutes of Technology don't just produce software engineers; they produce world-class chemical engineers who understand complex organic synthesis.

Second, the regulatory arbitrage. Not in the sense of cutting corners—the fragrance houses would never tolerate that—but in the ability to navigate complex environmental regulations while maintaining profitability. Indian companies became experts at meeting Western environmental standards while operating in a regulatory environment that, while strict, was more focused on rapid industrialization than their European counterparts.

Third, and perhaps most importantly, the hunger. European chemical companies, comfortable with their century-old relationships and fat margins, had grown complacent. They saw aroma chemicals as a mature, slow-growth business. Indian entrepreneurs like Babani saw opportunity.

The moat of complexity in aroma chemicals cannot be overstated. These aren't commodity chemicals where the only differentiation is price. Each molecule has specific olfactory properties that can vary based on even tiny impurities. A musk compound that's 99.5% pure might smell completely different from one that's 99.9% pure. The stereochemistry matters—molecules that are mirror images of each other can smell completely different, one like roses, the other like vinegar.

This complexity creates enormous barriers to entry. You can't just build a factory and start making aroma chemicals. You need deep process knowledge, analytical capabilities to ensure purity, and most crucially, the trust of customers who are betting their brand reputations on your consistency. One bad batch that makes it into a global fragrance launch could destroy relationships built over decades.

The customer relationships in this industry operate on geological timescales. Fragrance houses don't switch suppliers lightly. When a perfumer creates a new fragrance using a specific grade of, say, Iso E Super from a particular supplier, that fragrance formulation is locked. If the brand becomes successful—think Calvin Klein's CK One or Dior's Sauvage—the supplier relationship can last for decades, generating steady, high-margin revenue streams.

This is the world Privi entered—a world of centuries-old relationships, closely guarded secrets, and quality requirements that bordered on obsessive. The idea that a small Indian company could not just enter but eventually dominate segments of this market would have seemed absurd in 1992. Yet that's exactly what happened. The question is: how?

IV. The Journey: Two Products to Fifty

The transformation from two products to fifty didn't happen overnight—it was a methodical, almost surgical expansion that revealed Babani's deep understanding of chemical value chains and market dynamics. Privi started manufacturing aroma chemicals in the year 1992 with only two products, which it gradually expanded to a range of over 50 products today, having a capacity of over 40,000 tons per annum.

The early product choices were telling. Rather than trying to compete in the most sophisticated, high-value molecules from day one, Privi started with products where India's raw material advantages were clearest. Pine-based chemicals, for instance, where India's access to crude sulfate turpentine (CST) from paper mills gave them a structural cost advantage. It wasn't glamorous, but it was smart—build credibility with simpler products, then move up the value chain.

Each new product addition followed a pattern: identify a molecule where current suppliers were either capacity-constrained or enjoying oligopolistic pricing, develop the process technology (often requiring months or years of R&D), achieve quality standards that met or exceeded incumbents, and then compete aggressively on price while maintaining margins through superior process efficiency.

The technical capabilities Privi built during this period read like a textbook of advanced organic chemistry. Hydrogenation—using hydrogen gas to modify molecular structures under high pressure with sophisticated catalysts. Grignard reactions—using organomagnesium compounds to form carbon-carbon bonds, a process so sensitive that humidity in the air can ruin entire batches. High vacuum distillation—separating compounds that would decompose at normal pressures, requiring equipment that maintains near-perfect vacuums while handling industrial volumes.

Building these capabilities required massive capital investments. State-of-the-art integrated manufacturing facilities were established both at Mahad in Maharashtra and at Jhagadia in Gujarat. These weren't just factories; they were complex chemical plants with interconnected processes where the waste stream from one product could become the raw material for another—a concept called "integrated manufacturing" that would become central to Privi's competitive advantage.

The Mahad facility, situated strategically between Mumbai and Pune, became the flagship. Picture massive stainless steel reactors, some as tall as three-story buildings, connected by miles of piping, all computer-controlled and monitored by engineers who understood both the chemistry and the engineering. The site operated 24/7, with round-the-clock shifts ensuring continuous production—because in chemicals, stopping and starting processes isn't just inefficient; it can be dangerous.

But perhaps the boldest move during this expansion phase was the CST refinery gamble. CST—crude sulfate turpentine—is a by-product of the paper pulping process, rich in terpenes that can be converted into valuable aroma chemicals. The problem? CST is notoriously difficult to process, containing hundreds of compounds that need to be separated and purified. Most companies avoided it, preferring cleaner but more expensive starting materials.

Privi didn't just build a CST refinery; they built one of only four in the world capable of processing this challenging raw material. More audaciously, they set up a refinery to process both CST and gum turpentine oil (GTO), becoming the single largest refinery globally at a single location. This wasn't just about scale—it was about flexibility. When CST prices spiked, they could switch to GTO. When certain terpenes were in short supply from one source, they could extract them from another.

The refinery investment was a masterclass in strategic thinking. By controlling the raw material processing, Privi could ensure quality from the very first step, reduce dependency on external suppliers, and capture margins that others left on the table. It also created a moat—even if competitors wanted to match Privi's cost structure in certain molecules, they'd need to replicate this entire infrastructure. The numbers tell the story of this transformation. Privi now processes crude sulfate turpentine with a CST/GTO processing capacity of 36,000/12,000 MTPA, making it the single largest refinery globally at a single location. This backward integration provides captive α and β pinenes—the fundamental building blocks for dozens of downstream products.

The scaling challenges during this period weren't just technical—they were financial and strategic. Each new product line required significant capital investment, not just in equipment but in process development, quality control systems, and market development. The company had to balance growth ambitions with financial prudence, especially given the cyclical nature of the chemicals industry.

Capital allocation decisions during this phase revealed sophisticated thinking. Rather than pursuing growth at any cost, Privi focused on products where they could achieve leadership positions. The philosophy was clear: be number one or two in a product category, or don't play at all. This meant saying no to opportunities that might have boosted revenues but diluted focus or margins.

By 2010, Privi had transformed from a small player to a recognized force in global aroma chemicals. The journey from two products to fifty wasn't just about adding SKUs—it was about building capabilities, creating competitive advantages, and establishing the foundation for what would become one of India's most successful specialty chemical companies. But the real inflection point was yet to come, as international investors began to notice this gem hidden in India's industrial landscape.

V. The Fairfax Era & Corporate Restructuring

August 2016 marked a watershed moment in Privi's corporate history. Fairfax India Holdings Corporation, the investment arm of Prem Watsa's Fairfax Financial, acquired a 51% equity stake in Privi Organics Limited. For those unfamiliar with Fairfax, imagine Warren Buffett's Berkshire Hathaway, but with a Canadian passport and a particular fondness for contrarian bets in emerging markets. Watsa, often called the "Canadian Buffett," had built a reputation for patient capital and value investing—exactly what a company like Privi needed for its next phase of growth.

The Fairfax investment wasn't just about capital—it was about credibility. When a globally respected investor backs an Indian specialty chemicals company, it sends a powerful signal to customers, competitors, and other stakeholders. Suddenly, conversations with global fragrance houses became easier. Banks were more willing to finance expansion. Talented executives were more interested in joining.

But the corporate restructuring that followed was Byzantine in its complexity. The company was formerly known as Fairchem Speciality Limited and changed its name to Privi Speciality Chemicals Limited in October 2020. This wasn't just a rebranding exercise—it was part of a complex merger and demerger that would rationalize the corporate structure and create a focused, pure-play aroma chemicals company. The details reveal the complexity of the transaction. Fairfax India completed its acquisition of approximately 51% of the outstanding shares of Privi Organics Limited for an aggregate consideration of approximately INR 3.7 billion (approximately $55 million at current exchange rates). But this was just the beginning of a corporate restructuring saga that would unfold over the next several years.

The merger with Adi Finechem created Fairchem Speciality Limited, with Fairfax India owning approximately 49% in the merged business which the parties proposed to rename Fairchem Speciality Limited. The strategic rationale was compelling: The proposed scheme brought significant diversification and synergies to both partners, with Adi Finechem gaining access to high quality research and development facilities, and Privi Organics benefiting from Adi Finechem's focus on cost optimization and capital efficiency.

Under Fairfax's ownership, Privi underwent a professionalization that's typical when institutional investors enter family-run businesses. Corporate governance improved, reporting became more transparent, and strategic planning became more formalized. The company began thinking in terms of ROCE and capital allocation efficiency rather than just revenue growth.

But the relationship between Fairfax and the founding team wasn't destined to last forever. In 2021, in a surprising turn of events, Mr. Mahesh Babani, the founder and current Chairman & Managing Director of Privi Speciality Chemicals Limited entered into an agreement with Fairfax India Holdings Corporation to buy its 48.75% shareholding in PSCL. With this transaction, Mr. Babani consolidated his holding in PSCL to 63%, and the overall promoter shareholding to 74%. The overall transaction was valued at Rs.1220 crore.

This buyback was telling. After five years of institutional ownership, Babani was confident enough in the company's prospects—and had accumulated enough capital—to regain control. It suggested that the professionalization under Fairfax had been successful, but also that Babani believed the best was yet to come and wanted to capture more of that upside himself.

The impact of the Fairfax era extended beyond corporate structure. The company's operational capabilities expanded significantly during this period. Quality systems were upgraded to meet the increasingly stringent requirements of global customers. The R&D function was formalized and expanded. Most importantly, the company's credibility with international partners reached a new level—setting the stage for what would become the most significant partnership in Privi's history.

VI. The Givaudan Joint Venture: A Turning Point

July 2021. The announcement that sent Privi's stock soaring wasn't about quarterly results or capacity expansion. It was about validation from the ultimate source: Givaudan, the Swiss giant that defines excellence in the fragrance industry, had chosen Privi as its joint venture partner in India. Givaudan has signed a joint venture agreement with Privi Speciality Chemicals Limited, India, to strengthen production capabilities for its global speciality fragrance ingredients. The structure was particularly interesting: Privi holds a 51% equity stake in the joint venture, while Givaudan retains the remaining 49%. This wasn't Givaudan taking over an Indian company; this was a partnership where the Indian company retained control.

Through the agreement, a new greenfield production plant will be built in Mahad, a city located south of Mumbai, to manufacture small-volume fragrance ingredients of medium to high complexity, also known as speciality ingredients. The significance of this cannot be overstated. Givaudan wasn't outsourcing commodity production to India—they were transferring sophisticated, high-value molecules that required complex chemistry.

Givaudan will transfer a number of small-volume products from its production facility in Vernier, Switzerland to the newly formed joint venture over the next five years. This will allow the site in Switzerland to focus resources on key strategic ingredients. Think about what this means: a Swiss company with 250 years of heritage was comfortable moving production from Switzerland—where labor costs are among the highest in the world but quality standards are unquestioned—to a facility in Maharashtra.

The market's reaction was immediate and dramatic. Privi Speciality Chemicals jumped 10.75% to Rs 1,475 after the company said that it has signed a joint venture (JV) agreement with Givaudan SA. But the real story wasn't the one-day pop—it was what this partnership represented for Privi's long-term trajectory.

Maurizio Volpi, President of Givaudan Fragrance & Beauty, didn't mince words about why they chose Privi: "Privi is not only perfectly positioned to support the region, but also highly skilled in managing the complexity of producing fragrance ingredients of different ranges of volumes. This agreement will enable us to evolve our dynamic portfolio of small signature products that enhance the perfumers palette and give their creations a competitive edge in the market".

From Privi's perspective, Mahesh Babani understood the transformative nature of this partnership: "We are excited with this opportunity to be partnering with Givaudan to support and expand their production of speciality fragrance ingredients. We look forward to showcase our knowhow and manufacturing expertise as a trusted partner through this strategic joint venture".

The technology transfer aspect was crucial. This wasn't just contract manufacturing where Givaudan would send formulas and Privi would execute. This was genuine technology transfer, where Privi would learn to manufacture molecules that had previously been made only in Switzerland. The knowledge gained from this partnership would inevitably spillover into Privi's own R&D and manufacturing capabilities.

By 2024, the joint venture had reached operational status. Privi Speciality Chemicals Limited has commenced commercial operations at its greenfield facility in Mahad in the state of Maharashtra by Prigiv Specialties Private Limited, a joint venture with Givaudan SA Switzerland. This greenfield facility is a state-of-the-art manufacturing unit, custom-built to produce smart volume fragrance ingredients of medium to high complexity exclusively for Givaudan.

The facility represented an investment of Rs 178 crore, but the real value wasn't in the capital deployed—it was in the validation. When the world's leading fragrance company chooses you as their manufacturing partner for complex molecules, it sends a powerful signal to every other player in the industry. Suddenly, conversations with IFF, Firmenich, and Symrise became very different. Privi wasn't just another Indian chemical company trying to compete on cost; they were Givaudan's chosen partner.

The joint venture also demonstrated Privi's strategic sophistication. By maintaining 51% control, they ensured that the learnings and capabilities built through the partnership would primarily benefit them. They weren't just a service provider to Givaudan; they were partners who would share in the value creation. This structure would become a template for future partnerships, positioning Privi not as a subordinate supplier but as an equal partner in the global fragrance supply chain.

VII. Product Innovation & The Specialty Story

Innovation in aroma chemicals isn't about eureka moments in pristine laboratories—it's about methodical exploration of chemical pathways, deep understanding of structure-odor relationships, and the ability to scale complex chemistry from milligrams to metric tons. Privi's innovation story exemplifies this reality, transforming from a manufacturer of basic aroma chemicals to a creator of sophisticated molecules that command premium prices. The Galaxmusk story exemplifies Privi's innovation journey. The company had commercialized a plant for Galaxmusk (4800 MTPA)—a polycyclic musk having application in laundry and detergents industry. Musk compounds are among the most valuable in the fragrance industry, often commanding prices of thousands of dollars per kilogram. But creating a new musk that's both olfactorily appealing and commercially viable requires navigating a minefield of technical, regulatory, and market challenges.

Galaxmusk wasn't just another musk variant—it represented Privi's ability to develop and scale complex polycyclic molecules that require sophisticated chemistry. The 4800 MTPA capacity suggests significant market acceptance, as companies don't build multi-thousand-ton plants for niche products. This was a molecule that had found its way into mainstream applications, from laundry detergents to fine fragrances.

But the real innovation crown jewel appears to be Amber Xtreme. Recently developed a woody aroma chemical Amber Xtreme wherein the realizations are highest in the company's product portfolio, with EBITDA margins upwards of 50%. Think about that margin structure—in an industry where 20-25% EBITDA margins are considered healthy, Privi had developed a molecule generating margins north of 50%.The R&D philosophy at Privi reveals sophisticated thinking about innovation in specialty chemicals. The research specialists at in-house R&D center continuously thrive to develop new products and processes. But this isn't blue-sky research—it's targeted innovation focused on building on existing value chains. New products are selected based on market intelligence and are further developed in the R&D facilities by its core technical team.

Privi also develops and produces custom-made aroma chemicals as per specific requirement of the customer. This custom synthesis capability is crucial for building deep customer relationships. When a fragrance house needs a specific molecule for a new perfume—perhaps a variation of an existing compound with slightly different olfactory properties—Privi can develop and scale it. This creates switching costs that go beyond price; the customer becomes dependent on Privi's technical capabilities.

The R&D technical team is also engaged in optimizing the manufacturing processes, which not only improve yields, but also reduce cycle time, cost, effluent, safety and environmental risks, with the focus on a complete sustainable solution. This process innovation is less glamorous than new molecule development but often more valuable. Improving the yield of a high-volume product by even a few percentage points can add millions to the bottom line.

The ESG angle has become increasingly important. Privi achieved 31.8 million safe man hours as on June 30, 2022 and received the "Rotary Water Award" for exemplary work in water conservation. More impressively, "Privi is now Ecovadis Platinum rated" it's amongst the only top 1% companies in the world to have the Platinum rating. For customers increasingly focused on supply chain sustainability, this provides additional differentiation beyond just price and quality.

Green chemistry initiatives aren't just about compliance—they're about competitive advantage. The ability to produce aroma chemicals using renewable feedstocks, reducing water consumption, and minimizing waste creates cost advantages while meeting increasingly stringent environmental regulations. When European customers face pressure to reduce their carbon footprint, having a supplier with strong green credentials becomes a competitive advantage.

The company's innovation pipeline continues to expand. At Privi we are constantly working towards creating new experiences for our customers by creating new fragrances and aroma chemicals that are safe and refreshing. The upcoming products list suggests continued focus on high-value, technically complex molecules where Privi can leverage its manufacturing capabilities and customer relationships.

What's particularly impressive about Privi's innovation strategy is its pragmatism. They're not trying to compete with the basic research capabilities of universities or the blue-sky R&D of pharmaceutical companies. Instead, they focus on applied research—taking known chemistry and making it better, cheaper, or greener. It's innovation that directly translates to customer value and, ultimately, to margins.

VIII. Financial Performance & Unit Economics

The numbers tell a story of transformation. With a market cap of ₹9,491 crores, revenue of ₹2,196 crores, and profit of ₹211 crores, Privi has evolved from a small specialty chemicals company to a significant player in the global aroma chemicals market. But raw numbers don't capture the underlying unit economics that make this business compelling. The recent quarterly performance reveals acceleration in the business. Revenue is up for the last 2 quarters, 493.06 Cr → 628.37 Cr, with an average increase of 21.5% per quarter. More impressively, Privi Speciality Chemicals Ltd's net profit jumped 114.44% since last year same period to ₹66.52Cr in the Q4 2024-2025. The net profit margin jumped 67.88% since last year same period to 10.59% in the Q4 2024-2025.

For the full year, net profit rose 97.03% to Rs 187.00 crore in the year ended March 2025 as against Rs 94.91 crore during the previous year ended March 2024. Sales rose 19.92% to Rs 2101.19 crore in the year ended March 2025 as against Rs 1752.23 crore during the previous year ended March 2024. This isn't just growth—it's profitable growth, with margins expanding even as revenues scale.

The unit economics of the aroma chemicals business are particularly attractive. Unlike commodity chemicals where margins are often in single digits, specialty aroma chemicals can command gross margins of 30-40% or higher. The key is the value-to-weight ratio. A kilogram of a sophisticated musk compound might sell for thousands of dollars, while a kilogram of basic industrial chemicals might fetch only a few dollars.

Capital efficiency metrics tell an interesting story. ROCE stands at 16.4% and ROE at 18.1%—respectable but not spectacular. However, these numbers mask the improving trajectory. As higher-margin products like Amber Xtreme scale up and the Givaudan JV reaches full capacity, these returns should improve significantly.

The working capital management in specialty chemicals is always challenging. Customers—especially large fragrance houses—often demand extended payment terms, while raw material suppliers expect prompt payment. Privi has managed this balance reasonably well, though there's always room for improvement in cash conversion cycles.

CRISIL Ratings has revised its outlook on the long-term bank facilities of Privi Speciality Chemicals Ltd to 'Positive' from 'Stable' while reaffirming the rating at 'CRISIL A+'. The outlook revision factors CRISIL's expectation of improvement in overall credit profile driven by steady growth in revenue, along with sustenance of operating margin and reducing debt levels.

The stock trades at 8.61 times its book value and a PE multiple of 45.1—premium valuations that reflect market expectations of continued growth and margin expansion. Whether these valuations are justified depends on execution of the growth strategy and the ability to maintain margins in an increasingly competitive market.

Comparison with global peers reveals interesting disparities. Western specialty chemical companies often trade at lower multiples despite higher margins, reflecting slower growth expectations. Indian specialty chemical companies command premium valuations based on the "China+1" theme and expectations of market share gains. Privi sits somewhere in between—not as cheap as mature Western players, not as expensive as some high-flying Indian peers.

The financial trajectory suggests a company at an inflection point. After years of building capabilities and relationships, Privi is now harvesting the fruits of those investments. The question for investors is whether the best is behind or ahead—and the recent results suggest there's more room to run.

IX. Competitive Positioning & Moats

In the specialty chemicals industry, competitive advantages aren't built on patents or brand recognition—they're constructed from a complex interplay of technical expertise, customer relationships, and operational excellence. Privi's moats are subtle but substantial, creating barriers that become more formidable with scale.

Technical complexity stands as the first and perhaps most important barrier. The ability to perform critical reactions like Hydrogenation, Condensation, Grignard reactions, as well as unit operations like Pyrolysis, Reactive Distillation, High Vacuum Distillation, Continuous Distillation isn't just about having the equipment—it's about having the accumulated knowledge of how to run these processes at scale, consistently, safely, and profitably.

Consider what it takes to manufacture a complex aroma chemical: You need to source specific raw materials (often from multiple suppliers across different geographies), run multi-step synthesis processes where each step must meet precise specifications, purify the final product to 99%+ purity (because even trace impurities can affect odor), and do all this while meeting stringent environmental and safety regulations. Now imagine doing this for 50+ different products, each with its own complexity. The learning curve is measured not in months but in decades.

Customer relationships in the fragrance industry operate on trust built over years. Nearly 10 of the world's largest and prestigious fragrance companies are its clients, including Givaudan, Firmenich, Symrise, Mane, IFF, P&G, Reckitt Benckiser. These relationships weren't built overnight. When a fragrance house sources a critical ingredient from you, they're not just buying a chemical—they're trusting you with their brand reputation. One contaminated batch that makes it into a global product launch could destroy years of trust.

The stickiness of these relationships is remarkable. Once a fragrance formulation is locked with a specific supplier's ingredient, changing suppliers requires reformulation, stability testing, regulatory reapproval, and market testing. The switching costs aren't just financial—they're temporal and reputational. This creates an annuity-like revenue stream for established suppliers.

Backward integration provides another layer of competitive advantage. Being one of only 4 refineries in the world to process CST, and the single largest refinery globally at a single location, gives Privi control over critical raw materials. Competitors who want to match Privi's cost structure in pine-based chemicals would need to replicate this entire infrastructure—a capital investment of hundreds of crores with uncertain returns.

Scale economics in the fragrance industry are counterintuitive. Unlike commodity chemicals where scale always helps, in specialty chemicals, the optimal scale varies by product. Some molecules are best produced in 10-ton batches, others in 1000-ton continuous processes. Privi's integrated facilities allow them to optimize production scale for each product, switching between batch and continuous processes as needed.

The regulatory compliance moat is often underestimated. All manufacturing units have been re-accredited with ISO 9001:2015, ISO 14001: 2015, and ISO 45001:2018 standards. But beyond certifications, it's about having systems that can satisfy surprise audits from the world's most demanding customers. When a Givaudan or IFF audit team shows up, they're not just checking boxes—they're looking for any sign of risk to their supply chain.

Quality certifications are table stakes, but quality culture is a moat. The ability to deliver consistency in odor and prescribed key parameters in an industry driven by stringent olfaction standards requires more than good equipment—it requires a workforce trained to understand that a slight variation in temperature or pressure can ruin an entire batch worth lakhs of rupees.

The China+1 strategy has become a tailwind rather than a moat itself, but Privi is well-positioned to benefit. As global fragrance companies look to diversify supply chains away from China, India emerges as a natural alternative. But not every Indian company can step into this role—it requires existing relationships, proven capabilities, and scale. Privi checks all these boxes.

Environmental and sustainability credentials increasingly matter. Being "Ecovadis Platinum rated" - amongst the only top 1% companies in the world to have the Platinum rating—provides differentiation in a world where supply chain sustainability is under scrutiny. When a European fragrance house needs to report their Scope 3 emissions, having suppliers with strong environmental credentials becomes a competitive advantage.

The network effects in the aroma chemicals industry are subtle but real. The more products you manufacture, the better you understand the underlying chemistry. The more customers you serve, the more you learn about market needs. The more raw materials you process, the better your procurement becomes. Each element reinforces the others, creating a flywheel effect that's hard for new entrants to replicate.

Geography provides an underappreciated advantage. The Mahad facility sits strategically between Mumbai (India's commercial capital) and Pune (a growing industrial hub), with access to ports for export and a skilled workforce. The Jhagadia facility in Gujarat benefits from the state's pro-business policies and chemical industry cluster effects. These aren't just plants—they're nodes in a carefully constructed supply chain network.

The combination of these moats creates a formidable barrier to entry. A new competitor would need to simultaneously build technical capabilities, earn customer trust, achieve regulatory compliance, create backward integration, and reach efficient scale—all while competing against an incumbent with three decades of experience and established relationships. It's possible, but it's expensive and risky, which is why despite the attractive margins in specialty aroma chemicals, new large-scale entrants are rare.

X. Risks & Bear Case

Every investment thesis needs a pre-mortem—an honest assessment of what could go wrong. For Privi, despite its impressive moats and growth trajectory, several risks lurk beneath the surface that could derail the story.

Raw material volatility presents the most immediate risk. Aroma chemicals are derived from petrochemicals and agricultural products, both subject to significant price swings. When crude oil prices spike or pine resin availability tightens, input costs can surge faster than price increases can be passed to customers. The CST refinery provides some insulation, but it's not immunity. A sustained period of raw material inflation could compress margins significantly.

Customer concentration, while a sign of quality, is also a vulnerability. With nearly all major fragrance houses as clients, losing even one major customer could materially impact revenues. More concerning is the bargaining power these large customers wield. As Givaudan, IFF, and others consolidate, their negotiating leverage increases. They can demand price reductions, extended payment terms, or exclusive supply arrangements that erode profitability.

Environmental regulations represent a sword of Damocles. The chemical industry faces increasingly stringent environmental norms globally. What's compliant today might be banned tomorrow. The EU's REACH regulations, for instance, can suddenly require expensive testing or reformulation. A single environmental incident at a plant could trigger regulatory backlash, production shutdowns, and reputational damage that takes years to recover from.

Competition from Chinese manufacturers remains a constant threat. While the China+1 narrative is compelling, Chinese companies aren't standing still. They're moving up the value chain, improving quality, and competing aggressively on price. If geopolitical tensions ease and supply chain diversification becomes less critical, Chinese competitors could regain market share with their cost advantages.

Technology disruption in synthetic biology could be game-changing. Companies like Gingko Bioworks and Zymergen (before its collapse) have been working on producing fragrance molecules using engineered microorganisms instead of chemical synthesis. While progress has been slower than promised, a breakthrough in bio-manufacturing could obsolete traditional chemical processes, rendering Privi's manufacturing infrastructure less valuable.

The recent decline in promoter holding is worth noting. Promoter holding has decreased over last quarter: -4.16%, bringing total promoter holding to 69.9%. While still substantial, any significant reduction in promoter stake could signal waning confidence or create overhang in the stock.

Valuation concerns are real. Trading at 45.1 times earnings and 8.61 times book value, Privi is priced for perfection. Any disappointment in growth or margins could trigger a sharp correction. The stock has already run up significantly—up 69.3% in one year—potentially limiting near-term upside.

The specialty chemicals sector's cyclicality is often underestimated during good times. The industry has historically experienced cycles of overcapacity followed by consolidation. If multiple players simultaneously expand capacity anticipating demand growth that doesn't materialize, pricing pressure could intensify.

Working capital management remains a persistent challenge. As the company grows, working capital requirements increase proportionally. Any disruption in collections or need to extend credit terms could strain cash flows, potentially requiring additional debt or equity financing at inopportune times.

Integration risks from rapid expansion shouldn't be ignored. As Privi adds new products, facilities, and partnerships like the Givaudan JV, complexity increases exponentially. Managing this complexity while maintaining quality and efficiency requires exceptional operational excellence. Any stumble in execution could impact customer confidence.

Currency fluctuations present ongoing challenges. With significant export revenues but rupee-denominated costs, Privi benefits from rupee depreciation but can be hurt by rupee strength. While hedging can mitigate some risk, it adds cost and complexity.

Succession planning remains opaque. While Mahesh Babani has built an impressive organization, the depth of the next generation of leadership isn't clear. In a relationship-driven business, leadership transition can be particularly challenging.

The bear case essentially boils down to this: Privi is a well-run company in an attractive industry, but it's trading at valuations that assume continued exceptional execution. Any stumble—whether from external shocks or internal mistakes—could lead to significant multiple compression. The company has delivered a poor sales growth of 9.68% over past five years and has a low return on equity of 11.0% over last 3 years, according to historical metrics, suggesting that the recent improvement might not be sustainable.

Market timing risk is real. Specialty chemicals tend to be early-cycle, meaning they peak before the broader economy. If we're late in the economic cycle, Privi might face headwinds just as investor expectations are highest.

The key question for investors is whether these risks are adequately reflected in the current valuation. The market seems to be betting that Privi's competitive advantages and growth prospects outweigh these concerns. Time will tell if this optimism is justified.

XI. Future Strategy & Growth Vectors

The next chapter of Privi's story is being written now, with strategic moves that could either multiply value or destroy it. Understanding where the company is headed requires parsing management commentary, industry trends, and strategic initiatives.

Capacity expansion remains the most visible growth driver. With current capacity of over 40,000 tons per annum spread across multiple product categories, Privi has room to grow within existing facilities, but major expansion will require new investments. The company has guided for 3000 Cr revenue in 3-3.5 years post capex, implying significant capacity additions are planned. The strategic acquisition to invest in Privi Fine Sciences reveals the next growth vector. Privi Speciality Chemicals Limited is exploring a strategic investment in PFSPL by way of subscription to and/or secondary acquisition of such number of equity shares of PFSPL as aggregate upto Rs.298 crore, equivalent to approximately 50.95% of the issued and paid-up share capital of the PFSPL. This isn't just an investment—it's a bet on green chemistry.

Privi Fine Sciences Private Limited (PFSPL) operates in the speciality and aroma chemicals industry, focusing on green science chemistry. The products to be manufactured using green science chemistry have been successfully developed by the Company through research and testing has been completed at a pilot level. This represents a strategic pivot toward sustainability-driven innovation.

The expansion at Privi Fine Sciences is ambitious. The project aims to increase the manufacturing capacity of synthetic organic chemicals from the existing 2160 TPA to 8872 TPA, with an estimated value of Rs 50.91 crore. This four-fold increase in capacity suggests confidence in the green chemistry products' market potential.

Adjacent opportunities in specialty chemicals present another growth avenue. The boundaries between aroma chemicals, flavor chemicals, and other specialty chemicals are increasingly blurred. Privi's technical capabilities—particularly in complex organic synthesis—could be leveraged into adjacent markets where similar chemistry is required but applications differ.

The EV and sustainability tailwind creates unexpected opportunities. As the world shifts toward electric vehicles and sustainable products, demand patterns for chemicals are changing. Some traditional applications may decline, but new ones emerge. Privi's focus on green chemistry positions them to capture these emerging opportunities.

Global versus domestic market dynamics present strategic choices. While exports have driven growth historically, India's domestic market for fragrances and personal care products is expanding rapidly. Rising incomes, urbanization, and premiumization create domestic demand for the same high-quality aroma chemicals Privi exports. Balancing global and domestic opportunities will be crucial.

The digital transformation of the chemical industry, while less visible than capacity expansion, could be equally important. Implementing advanced analytics for process optimization, predictive maintenance for equipment, and AI-driven R&D could provide competitive advantages in an industry where marginal improvements compound over time.

Strategic partnerships beyond Givaudan could accelerate growth. The success of the Givaudan JV demonstrates Privi's ability to be a trusted partner to global leaders. Similar partnerships with other fragrance houses or consumer goods companies could provide access to new technologies, markets, and revenue streams.

The product portfolio evolution toward higher-value molecules continues. As shown with Amber Xtreme's 50%+ EBITDA margins, moving up the value chain dramatically improves economics. The challenge is identifying which molecules to pursue—a decision requiring deep market understanding and technical capabilities.

Backward integration opportunities remain. While Privi has integrated backward into CST refining, further integration into other raw materials could provide additional cost advantages and supply security. However, this must be balanced against capital requirements and the risk of over-integration.

The M&A landscape presents both opportunities and risks. As the Indian specialty chemicals sector consolidates, Privi could be either acquirer or target. Strategic acquisitions could provide new capabilities or market access, but integration challenges and valuation disciplines must be maintained.

Regulatory tailwinds from production-linked incentive (PLI) schemes and China+1 strategies continue to support growth. Government support for the chemical sector, combined with global supply chain diversification, creates a favorable environment for expansion.

The key strategic question is capital allocation. With multiple growth opportunities—capacity expansion, green chemistry, M&A, backward integration—choosing where to invest becomes crucial. The company's track record suggests disciplined capital allocation, but as opportunities multiply, maintaining this discipline becomes harder.

Management's guidance of Rs 3,000 crore revenue in 3-3.5 years implies a CAGR of approximately 15-20% from current levels. Achieving this while maintaining or expanding margins will require flawless execution across multiple initiatives. The building blocks are in place, but execution will determine whether potential becomes performance.

XII. Investment Thesis & Valuation

At a market capitalization of ₹9,491 crores, Privi Speciality Chemicals presents a complex valuation puzzle. The stock trades at 45.1 times earnings and 8.61 times book value—multiples that would make value investors wince but growth investors salivate. The question isn't whether Privi is expensive in absolute terms (it is), but whether the growth trajectory and quality characteristics justify the premium.

The bull case rests on multiple expansion drivers. First, the structural shift in global supply chains favoring India remains in early innings. As fragrance houses continue diversifying away from China, Privi's established relationships and proven capabilities position it as a primary beneficiary. This isn't a temporary arbitrage opportunity but a potential decade-long tailwind.

Second, the product mix shift toward higher-margin specialties like Amber Xtreme could drive margin expansion even without volume growth. If EBITDA margins can expand from current levels to the 25-30% range seen in best-in-class specialty chemical companies, earnings could surprise significantly to the upside.

Third, the Givaudan JV represents just the beginning of potential partnerships. Success here could lead to similar arrangements with other global players, each bringing technology transfer, guaranteed volumes, and validation that supports premium pricing.

The growth-quality-valuation framework suggests Privi scores well on growth (recent quarters showing acceleration) and quality (strong customer relationships, technical moats), but valuation remains the sticking point. However, comparing Privi to global specialty chemical peers reveals interesting disparities. Companies like Givaudan trade at 35-40x earnings despite single-digit growth, suggesting quality commands premiums regardless of geography.

Within the Indian context, specialty chemical companies trade at wide-ranging multiples based on their perceived quality and growth prospects. PI Industries trades at 40-45x, Aarti Industries at 25-30x, while commodity-oriented players trade at 10-15x. Privi's multiple suggests the market views it closer to PI Industries than commodity players—a vote of confidence in its specialty positioning.

The India story premium is real but difficult to quantify. International investors allocating to India often prefer "plays on India's growth" rather than direct consumption stories. Specialty chemicals offer exposure to India's manufacturing prowess, technical talent, and cost advantages without the complexities of consumer markets. This structural demand for quality Indian manufacturing stories supports valuations.

Key metrics to watch going forward include: - Revenue growth sustaining above 20% (validates market opportunity) - EBITDA margins expanding toward 25% (proves mix shift strategy) - ROCE improving toward 20%+ (demonstrates capital efficiency) - Working capital days remaining stable or improving (operational excellence) - New product launches and their contribution to revenue (innovation engine)

The bear case on valuation is straightforward: at 45x earnings, any disappointment could trigger sharp multiple compression. If growth slows to mid-teens or margins compress due to competition, the stock could easily trade at 25-30x, implying 30-40% downside. History suggests specialty chemical valuations are cyclical, and we may be near peak multiples.

The discounted cash flow perspective requires heroic assumptions to justify current valuations. Even assuming 20% revenue CAGR for five years, margin expansion, and a generous terminal multiple, fair value calculations often arrive below current prices. This suggests the market is pricing in either exceptional execution or strategic optionality (like a takeover premium).

Risk-reward analysis at current levels skews negative for new investors. With the stock up 69.3% in one year, much of the easy money has been made. The asymmetry that existed when Privi was undiscovered no longer exists. That said, for existing investors, the business quality and growth trajectory may justify holding despite rich valuations.

The institutional ownership pattern provides mixed signals. Promoter holding at 69.9% remains high, suggesting continued founder confidence. However, the recent 4.16% quarter-on-quarter decline in promoter holding raises questions. Are insiders taking profits at these valuations, or is this portfolio rebalancing?

Relative valuation within the portfolio context matters. For investors overweight financials or traditional industries, Privi offers exposure to structural growth themes. For those already heavy in expensive growth stocks, adding Privi compounds valuation risk. Portfolio construction considerations often trump absolute valuation metrics.

The margin of safety—that bedrock principle of value investing—is largely absent at current prices. This doesn't make Privi a bad investment, but it makes it a different kind of investment. You're betting on continued exceptional execution, favorable industry dynamics, and multiple maintenance or expansion. When everything needs to go right to justify the price, risk management becomes paramount.

Catalysts that could drive rerating include: - Successful commercialization of green chemistry products - New blue-chip customer additions - Margin-accretive acquisitions - Additional strategic partnerships like Givaudan JV - Regulatory approvals for new molecules

Conversely, risks that could trigger derating include: - Margin compression from competition - Loss of key customers - Environmental or safety incidents - Adverse regulatory changes - General market correction in expensive growth stocks

The verdict on valuation is nuanced. Privi isn't cheap by any conventional metric, but neither was Asian Paints at 30x earnings in 2010, or HDFC Bank at 4x book value in 2005. Quality compounds, and paying up for quality often proves wise in hindsight. However, the margin for error is thin, and position sizing should reflect the elevated risk at current valuations.

XIII. Playbook & Lessons

The Privi story offers a masterclass in building a global business from an emerging market, with lessons that extend far beyond specialty chemicals. Each strategic decision, from the initial product selection to the Givaudan partnership, reveals principles applicable across industries and geographies.

Building a global business from India requires a different playbook than serving domestic markets. Privi understood early that competing globally meant matching international quality standards from day one—no "good enough for India" mentality. This meant investing in certifications, quality systems, and processes that seemed excessive for a small company but proved essential for global credibility.

The approach to customer acquisition was methodical. Rather than trying to win everyone, Privi focused on building deep relationships with a few key accounts. Once they proved themselves to Givaudan or IFF, other customers followed. In B2B markets, reference customers matter more than marketing budgets.

The power of focusing on unsexy B2B markets cannot be overstated. While entrepreneurs chase consumer glory and venture capital, B2B markets offer better economics with less competition. Privi's invisibility was its strength—no brand building costs, no consumer fickleness, just technical excellence and consistent delivery.

The company's evolution demonstrates that B2B doesn't mean boring. The chemistry involved in creating new aroma molecules is as innovative as any tech startup, just less visible. The lesson: innovation doesn't require an app store presence.

Timing market cycles in chemicals requires understanding that the industry operates on different rhythms than financial markets. Capacity additions take years, customer qualifications take months, and product development cycles span decades. Privi's patient capital approach—building capacity ahead of demand, investing in R&D during downturns—reflects this reality.

The CST refinery investment exemplified contrarian timing. When others avoided the complexity and capital requirements, Privi jumped in. By the time competitors realized the strategic value, Privi had established an insurmountable lead. The lesson: in cyclical industries, the best investments often feel uncomfortable when made.

Managing complexity in operations becomes exponential as product count grows. Privi's evolution from 2 to 50+ products required systems thinking. Each product has different raw materials, reaction conditions, quality specifications, and customer requirements. Managing this complexity while maintaining quality requires operational excellence that can't be bought—only built over time.

The integration of multiple manufacturing sites adds another layer of complexity. Deciding what to produce where, managing inventory across locations, and ensuring consistent quality regardless of production site requires sophisticated planning systems and experienced management.

Building trust with global MNCs is a gradual process with no shortcuts. These companies have century-old supplier relationships and regulatory requirements that make switching costs enormous. Privi's approach was to start small—perhaps supplying a non-critical ingredient—then gradually earning larger responsibilities.

The Givaudan JV represents the culmination of decades of trust building. Givaudan didn't choose Privi randomly; they chose a partner who had demonstrated reliability over years. The lesson: in B2B markets, trust is built in drops but lost in buckets.

Capital allocation in cyclical industries requires discipline that goes against human nature. When business is good and cash flows are strong, the temptation is to expand aggressively. When downturns hit, the instinct is to conserve. Privi did the opposite—investing during downturns when assets were cheap and competition was retrenching.

The buyback of Fairfax's stake demonstrated sophisticated capital allocation. Rather than using cash for marginal capacity additions, Babani bought back equity, consolidating ownership at what proved to be attractive valuations. This financial engineering created more value than any operational improvement could have.

The India advantage goes beyond labor costs. It includes: - Deep technical talent pool from IITs and other institutions - English language capabilities enabling global business - Reverse engineering expertise from decades of import substitution - Entrepreneurial hunger from a rapidly developing economy - Regulatory expertise from navigating complex domestic requirements

Privi leveraged all these advantages while avoiding the typical pitfalls of Indian manufacturing—inconsistent quality, delayed deliveries, and informal business practices.

Strategic patience emerges as perhaps the most important lesson. Building Privi took three decades. The CST refinery took years to optimize. Customer relationships took decades to mature. In an era of quarterly capitalism, Privi's long-term orientation stands out.

This patience extended to financial markets. Despite being listed since 2015 (through the complex merger history), the company focused on building the business rather than managing stock price. The eventual rerating validated this approach.

The power of focus in an era of conglomerate temptation is remarkable. Despite opportunities to diversify into other chemicals or forward integrate into fragrances, Privi stayed focused on aroma chemicals. This focus enabled deep expertise that diversified competitors couldn't match.

Lessons for investors include: - Look for companies solving complex B2B problems - Value customer stickiness over growth rates - Understand industry-specific moats beyond traditional frameworks - Appreciate the compounding value of incremental improvements - Recognize when backing proven operators despite rich valuations might make sense

Lessons for entrepreneurs include: - Choose markets where India has structural advantages - Build for global standards from day one - Focus on technical excellence over marketing - Be patient with customer acquisition but impatient with quality - Consider B2B markets that VCs ignore

The Privi playbook isn't easily replicable—it required specific industry knowledge, technical capabilities, and decades of relationship building. But the principles—focus, quality, patience, and strategic thinking—apply universally. In a world obsessed with disruption, Privi shows that building slowly and steadily can create enormous value.

XIV. Final Analysis

After thousands of words dissecting Privi Speciality Chemicals, we arrive at the essential question: Is this a specialty chemicals compounder destined for continued outperformance, or a cyclical play approaching its peak? The answer, unsatisfyingly but honestly, is that it could be either—the outcome depends on execution, industry dynamics, and macroeconomic factors largely outside anyone's control.

The bull case rests on solid foundations. India's rise as a global manufacturing hub isn't a narrative—it's happening. The China+1 strategy isn't consultant speak—it's driving real orders. The Givaudan partnership isn't a press release—it's a Rs 178 crore facility producing complex molecules. When narratives align with facts, sustainable value creation often follows.

The quality markers are undeniable. Relationships with every major fragrance house, technical capabilities that take decades to build, backward integration that provides cost advantages—these aren't easily replicable. In industries where switching costs are high and technical requirements are complex, incumbents with proven track records have tremendous staying power.

The growth trajectory, while perhaps not sustainable at recent quarters' pace, has multiple drivers. Capacity expansion, product mix improvement, new customer additions, and emerging applications like green chemistry provide multiple ways to win. Unlike single-product companies or those dependent on one customer, Privi has diversified sources of growth.

The bear case deserves equal consideration. Valuations pricing in perfection leave no room for error. Competition from Chinese manufacturers won't disappear—they're moving up the value chain too. Environmental regulations could impose unexpected costs. The specialty chemicals cycle, dormant for years, could reassert itself.

The recent promoter stake reduction, while small, raises questions. Insiders selling into strength isn't necessarily bearish, but it suggests even management recognizes the rich valuations. The historical metrics showing poor five-year sales growth and low three-year ROE remind us that the recent excellent performance might be exceptional rather than normal.

Key surprises from the research:

The depth of technical complexity required in aroma chemicals exceeded expectations. This isn't just mixing chemicals—it's sophisticated organic synthesis requiring expertise comparable to pharmaceutical manufacturing.

The stickiness of customer relationships was remarkable. Once qualified, suppliers become embedded in formulations that can last decades. This creates an annuity-like quality to revenues that's rare in manufacturing.

The strategic sophistication of management, particularly in capital allocation and partnership structuring, stood out. The Givaudan JV structure (51% Privi, 49% Givaudan) showed negotiating prowess and confidence unusual for Indian companies dealing with global giants.

The importance of backward integration into CST refining was underappreciated. This single investment created a sustainable competitive advantage that competitors struggle to replicate.

The verdict: Privi Speciality Chemicals is a high-quality company in an attractive industry with strong competitive positions and capable management. It's also expensive, with execution risks and exposure to global economic cycles. For investors with long time horizons who believe in the India manufacturing story and can stomach volatility, Privi represents a compelling opportunity to own a potential global champion. For value-conscious investors or those worried about market cycles, waiting for better entry points might be prudent.

The most honest assessment is that Privi is neither a sure thing nor a value trap—it's a quality company at a full price in an uncertain world. In investing, as in chemistry, the reaction depends on conditions. Current conditions favor Privi, but conditions change. The key is not predicting the future but understanding the range of possible outcomes and positioning accordingly.

What's certain is that Privi has built something substantial—a globally competitive Indian manufacturer in a technically complex industry. Whether the stock price appropriately reflects this achievement or overshoots it remains the open question. Time, that ultimate arbiter of investment decisions, will provide the answer.

For those choosing to invest, size positions appropriately for the risk, monitor execution closely, and remember that even the best companies can be poor investments at the wrong price. For those passing, keep Privi on the watchlist—quality companies at reasonable prices are rare, but market volatility occasionally provides opportunities.

The Privi story continues to be written. Whether the next chapters describe continued triumph or cyclical challenges remains unknown. What's known is that this company, started with two products in 1992, now shapes how the world smells. That's an achievement worth acknowledging, regardless of where the stock trades tomorrow.

In the end, Privi Speciality Chemicals embodies both the promise and peril of investing in India's manufacturing renaissance. The promise: world-class companies emerging from unlikely origins to compete globally. The peril: valuations that assume everything goes right in a world where things often go wrong. Navigate accordingly.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube