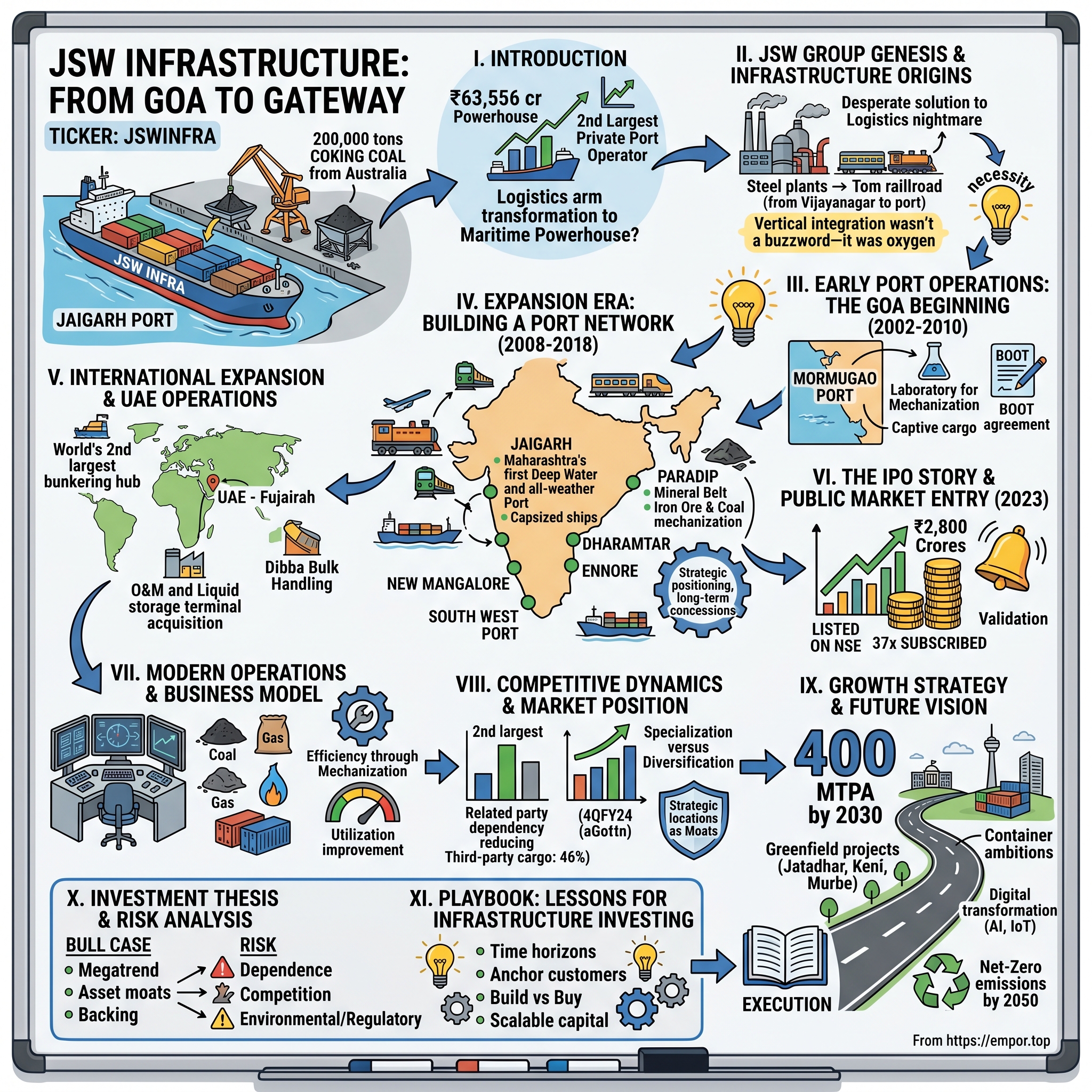

JSW Infrastructure: From Goa to Gateway - Building India's Port Empire

I. Introduction & Episode Framework

Picture this: A massive cargo vessel, the size of three football fields, glides into Jaigarh Port on India's western coast. Its hull sits deep in the water, carrying 200,000 tons of coking coal from Australia. The port's mechanized unloaders—towering steel giants—spring to life, their grabbers descending like mechanical birds of prey. Within hours, what would have taken days at traditional ports is complete. The coal begins its journey inland, destined for blast furnaces that will transform it into steel for India's infrastructure boom.

This is JSW Infrastructure in action—a company that has quietly become India's second-largest commercial port operator while most investors were watching its flashier competitors. With 170 million tons per annum of cargo handling capacity spread across ten strategic locations, JSW Infrastructure represents a fascinating paradox: a ports company born not from maritime ambition, but from a steel manufacturer's desperate need to control its own destiny.

The central question isn't just how a steel conglomerate's logistics arm transformed into a ₹63,556 crore maritime infrastructure powerhouse. It's why this transformation matters for understanding India's next decade of growth—and what it reveals about the hidden moats in supposedly commoditized businesses.

Founded in 1999 and freshly listed on the NSE in October 2023, JSW Infrastructure's story intersects with India's economic liberalization, the rise of private infrastructure, and the strategic chess game between industrial houses for control of the country's trade gateways. It's a narrative that challenges conventional wisdom about related-party transactions, vertical integration, and what constitutes a competitive advantage in capital-intensive industries.

II. The JSW Group Genesis & Infrastructure Origins

The year was 1982. India was still two decades away from its economic awakening, operating under the License Raj system where private enterprise required government permission for nearly everything. In this constrained environment, a young entrepreneur named O.P. Jindal saw opportunity where others saw obstacles. He acquired a struggling re-rolling mill in Tarapur, Maharashtra—a facility so distressed that banks had written it off. Jindal renamed it Jindal Iron and Steel Company (JISCO), marking the birth of what would become the JSW Group.

But the real story begins with succession planning done right. When O.P. Jindal died in a helicopter crash in 2005, his four sons had already divided the empire with surgical precision—no messy battles, no courtroom drama. Sajjan Jindal, the youngest, inherited the steel business. While his brothers got power, stainless steel, and pipes, Sajjan got what seemed like the commodity play. Yet he had a different vision: vertical integration so complete it would redefine what it meant to be a steel company.

By 1997, before JSW Infrastructure formally existed, the seeds were already planted. South West Port Limited was incorporated—not as a standalone port venture, but as a desperate solution to a logistics nightmare. JSW's Vijayanagar steel plant in Karnataka, landlocked and 340 kilometers from the nearest major port, was hemorrhaging money on transportation costs. Every ton of iron ore imported, every ton of steel exported, meant dealing with congested government ports, unpredictable turnaround times, and a transport mafia that controlled inland logistics. The formation of JSW Infrastructure in 1999 wasn't a grand announcement or strategic pivot—it was born of necessity. Operating since 1999, the company was founded in Mumbai, initially as JSW Infrastructure & Logistics Limited, changing its name to JSW Infrastructure Limited on March 25, 2008. The company's mandate was ambitious yet vague: developing world class airports, shipyards, townships, roads and rail connectivity, inland waterways, water treatment plants, special economic zones and other infrastructural facilities.

But infrastructure without purpose is just concrete and steel. The real catalyst came from the Vijayanagar plant's logistical nightmare. Every day, trains carrying iron ore would queue for kilometers outside government ports. Ships would wait weeks for berths. Demurrage charges alone were eating into margins that were already razor-thin in the commodity steel business.

Sajjan Jindal's solution was characteristically bold: if you can't beat the system, build around it. The South West Port Limited venture wasn't just about owning a port—it was about controlling time, cost, and reliability in a supply chain where delays meant death. This wasn't empire-building; it was survival engineering.

The strategic rationale went deeper than cost-cutting. In the late 1990s, India's infrastructure was a contradiction—massive potential strangled by inadequate execution. Government ports operated at 60-70% efficiency on good days. Private participation in ports was still experimental. The 1997 New Economic Policy had just opened doors for private operators, but nobody quite knew how to walk through them.

For JSW, vertical integration wasn't a buzzword—it was oxygen. The steel business is brutally simple: your costs are largely fixed, your prices are set by global markets, and your only real lever is efficiency. By controlling ports, JSW could guarantee evacuation of finished products, ensure steady raw material supply, and most critically, decouple its operations from the inefficiencies of state-run infrastructure.

This infrastructure genesis would set a pattern that defined JSW's next two decades: identify bottlenecks in your core business, then systematically own and operate the solutions. It was infrastructure as competitive advantage, not as diversification. The foundation was set for what would become one of India's most ambitious port expansion stories.

III. Early Port Operations: The Goa Beginning (2002-2010)

The morning of April 15, 2002, marked a turning point that few recognized at the time. A small team from JSW stood at the edge of Mormugao Port in Goa, watching as construction crews began work on what would become their first dedicated bulk cargo berths. The Arabian Sea stretched endlessly before them, cargo ships dotting the horizon like chess pieces waiting to move. The challenge wasn't just building berths—it was reimagining how Indian ports could operate. The South West Port was acquired by the JSW Group in 2002 when they acquired ABG Goa Port Private Ltd and renamed it to South West Port Limited (SWPL). But acquisition was just paperwork—transformation required vision and sweat. SWPL started operations at Mormugao in 2004 with 2 berths to handle coal and steel products.

The Mormugao operation wasn't just another port terminal—it was JSW's laboratory for mechanization. The company operated two bulk cargo berths at Mormugao Port Authority at Goa, on a Build, Own, Operate and Transfer (BOOT) license agreement. The 30-year concession gave JSW the long-term stability needed to justify heavy capital investment in mechanization.

The numbers tell the efficiency story: Berth 1 for coal handling using 2x2000 TPH ship grab uploaders including covered back-up conveying systems, and Berth 2 for other bulk, break-bulk cargo using 2 mobile harbor cranes 2x1200 TPH. This wasn't just equipment—it was a statement of intent. While government ports still relied on manual labor and outdated cranes, JSW was building for scale.

The strategic location was no accident. South West Port provided vital logistic support to the JSW Steel plant at Vijayanagar, Karnataka, being the closest port to the steel industry cluster of Bellary-Hospet in Karnataka. The 340-kilometer distance that had once been a liability became manageable with dedicated rail connectivity and mechanized loading systems.

Early challenges came in waves. Environmental concerns plagued operations from day one. Local fishing communities protested coal dust pollution. The solution wasn't to fight but to innovate: Lower dust pollution because of dust suppression systems, closed transport rail wagons and sprinkler arrangements became standard operating procedure, setting benchmarks that government ports would later struggle to match.

Competition was fierce and personal. Berths 5a and 6a, operated by JSW, were directly northwest of berth 7, operated by Adani. In 2016-17, JSW was the main importer with 10.11 million tonnes, followed by Adani with 1.9 million tonnes. The proximity wasn't coincidental—both groups were eyeing the same cargo, the same customers, the same future.

But the real achievement wasn't in tonnage—it was in reliability. The terminal handled around 70 MMT and 19,000 rakes since its inception, creating a track record that would become JSW's calling card. In an industry where a single day's delay could cost millions, JSW was delivering predictability.

The Goa operations also revealed a critical insight: captive cargo wasn't enough. At 4 lakh tonnes per month, South West Port was able to handle only 3.6 mt of coal a year or half the requirement of the steel plant. This limitation would drive JSW's next phase of expansion—the search for scale that could match their industrial ambitions.

IV. Expansion Era: Building a Port Network (2008-2018)

The boardroom at JSW's Mumbai headquarters in early 2007 was electric with tension. Sajjan Jindal stood before a massive map of India's coastline, red pins marking existing ports, blue ones showing opportunities. "We're thinking too small," he said, his finger tracing the western coast. "One port makes us dependent. Ten ports make us indispensable. "The transformation began with name change from JSW Infrastructure & Logistics Limited to JSW Infrastructure Limited on March 25, 2008—a signal that logistics was no longer the tail but the dog. That same year marked the beginning of JSW's most ambitious project yet: Jaigarh Port.

JSW Infrastructure signs a lease with Maharashtra Maritime Board to develop a greenfield facility at Jaigarh Port in 2007 was just the beginning. The concession agreement between the Maharashtra Maritime Board (MMB) and JSW Jaigarh Port Limited was signed on June 24, 2008, with a licence period of 50 years. Fifty years—not the typical 30-year BOOT model, but a half-century bet on India's infrastructure future.

The Jaigad port (JSW) was established in 2006 to support the coal import requirements directly adjacent to the thermal power plant. The port was officially inaugurated in August 2009. But this wasn't just another port—It is Maharashtra's first deep water and all-weather port for berthing of capsized ships.

The engineering marvel of Jaigarh deserves pause. The construction of JSW Jaigarh Port was completed in 20 months—a timeline that made international port developers question if corners were cut. They weren't. Instead, JSW had pioneered modular construction techniques, pre-fabricating components while site preparation continued in parallel.

The depth advantage was game-changing. With 17.5 meters draft depth (later expanded to 18 meters), Jaigarh could handle Capesize vessels—the giants of bulk shipping that most Indian ports couldn't accommodate. This meant direct shipments from Australia and Brazil, eliminating transshipment costs that plagued competitors.

Strategic location wasn't accidental. Located strategically between the two major ports of Mumbai (365 km) and Goa (250 km), Jaigarh port's existing cargo handling capacity is about 50 million tonnes per annum (mtpa). The port served as a gateway to its primary hinterland of south Maharashtra, north Karnataka and north west Andhra Pradesh.

But ports without connectivity are islands. JSW understood this viscerally. The company didn't just build berths; it engineered ecosystems. Signs concession agreement with Konkan Railway to construct 33.7km of rail line connecting Jaigarh Port. This wasn't just track-laying—it was threading a needle through the Western Ghats, one of India's most challenging terrains.

The multi-modal strategy extended beyond Jaigarh. In 2012, JSW Infrastructure signs a long-term operations and maintenance contract for handling cargo at Dharamtar jetty for JSW Dolvi Steel Works (Maharashtra). Each addition to the network wasn't random accumulation but strategic positioning—creating a web of ports that could serve different cargo types, vessel sizes, and industrial clusters. The eastern expansion was equally strategic. The Iron Ore terminal located in Paradip Port is a mechanized terminal having a capacity of 10 MTPA (later expanded to 18 MTPA). The terminal is strategically situated 210 nautical miles south of Kolkata and 260 nautical miles north of Visakhapatnam. This wasn't just geography—it was positioning at the heart of India's mineral belt.

But JSW's masterstroke at Paradip came with coal. Paradip East Quay Coal Terminal Private Limited has secured the contract for mechanization of EQ1, EQ2 and EQ3 berths of Paradip Port and operates a mechanized terminal having a capacity of 30 MTPA. This single facility could handle 30 MTPA of cargo for exporting / coastal movement of domestic coal.

The technical specifications revealed ambition: JSW's iron ore terminal at Paradip comprises two ship-loaders, each with a capacity of 7,000 metric tonnes per hour. It also has 800,000 metric tonnes cargo storage yard with Rotary & Tandem Wagon tipplers to enable fast rake unloading. These weren't just numbers—they represented the ability to load a Capesize vessel in under 24 hours, a feat that took competitors days.

Meanwhile, on the west coast, Ennore Terminal's closeness to the hinterland has growth opportunities. The cargo handling capabilities of the New Mangalore terminal set it apart. Each terminal was selected not for immediate returns but for strategic positioning in India's evolving industrial geography.

The long-term concession strategy was revolutionary in Indian infrastructure. While competitors fought for quick returns on 15-20 year contracts, JSW was signing 30-50 year agreements. The math was counterintuitive but powerful: longer concessions meant lower annual payments to port authorities, allowing for heavier upfront mechanization investment that would pay dividends over decades.

Building relationships beyond the JSW Group became critical. JSW Infrastructure has gradually reduced its dependence on the group. From accounting for just 25% of cargo volume in 2021, it makes up 35% today. Third-party customers weren't just revenue diversification—they were validation that JSW's ports could compete on merit, not just captive demand.

The expansion philosophy was clear: be everywhere that mattered, but only where you could dominate. By 2018, JSW Infrastructure had transformed from a single-port operator serving one steel plant into a network spanning both coasts, handling everything from coal to containers, serving customers from cement manufacturers to power plants.

V. International Expansion & UAE Operations

The phone call came at 2 AM Dubai time in March 2015. Arun Maheshwari, then head of JSW Infrastructure's business development, was in his hotel room overlooking the Fujairah coast when the news arrived: "The Arabs want to meet. Tomorrow. They're interested in an Indian operator for their terminals."

The Middle East wasn't on JSW's roadmap. The company had its hands full with Indian expansion. But Fujairah represented something different—a chance to prove that Indian port operators could compete globally, not just in protected home markets. Fujairah wasn't just any port—it was the world's second-largest bunkering hub, strategically positioned outside the Strait of Hormuz. JSW Infrastructure signed an agreement with Port of Fujairah (UAE) for management of mechanised bulk cargo handling terminals in December 2016. The port handles around 100 million tons per annum (MTPA), which is poised to increase to 150 MTPA.

The O&M (Operations & Maintenance) model was different from JSW's Indian playbook. Instead of long-term concessions, they would manage existing infrastructure—proving operational excellence without capital deployment. We have an O&M contract for two berths in this terminal which has a cargo handling capacity of 24 MTPA.

But operational management was just the entry ticket. The real prize came later. JSW Infrastructure through its subsidiary JSW Terminal (Middle East) FZE, successfully completed the acquisition of Marine Oil Terminal Corp (MROTC) for an Enterprise Value of $187mn from the Mercuria Group. Marine Oil Terminal Corp operates a liquid storage terminal with a capacity of 465,000 cbm situated at Fujairah Oil Industry Zone (FOIZ).

This wasn't just geographic diversification—it was cargo diversification. The state-of-the-art liquid tank storage facility with 465,000 cubic meters capacity represented JSW's entry into the lucrative oil storage business. In a world where oil traders needed flexible storage to arbitrage price differentials, JSW was positioning itself as the infrastructure backbone of energy trading.

The Dibba expansion followed naturally. We entered into an international agreement with the Port of Fujairah for operations and maintenance of Dibba Bulk Handling Terminal – Dibba, Fujairah (UAE) which came into effect in Fiscal 2023. The transport of aggregates from the stockyard to port shall be made via a 4.2 km conveyor system—mechanization at its finest.

Strategic location was everything. Fujairah Terminal's strategic location near India's western coast leads to greater utilities for the cement and steel companies for limestone and aggregate imports. It provides great distance advantage, continuously being used by top Indian steel and cement producing companies. This wasn't just serving Indian demand—it was creating a bridge between Middle Eastern resources and Indian industry.

The UAE operations proved something crucial: JSW could compete without the safety net of captive cargo or government relationships. At this port, container terminals are managed by DP World and henceforth JSW will manage mechanised bulk cargo terminals—putting them in direct competition with one of the world's largest port operators.

"This foray will strengthen business and trade ties between India and the GCC region, especially UAE. The inking of this pact opens new opportunities for us in global arena putting us in the league of the world's best port operating companies," Captain BVJK Sharma, then Joint Managing Director and CEO, had said.

The Middle East strategy wasn't about empire-building—it was about capability demonstration. Every ton handled in Fujairah was proof that Indian infrastructure companies could operate at global standards. This credibility would prove invaluable when JSW returned to Indian capital markets.

VI. The IPO Story & Public Market Entry (2023)

September 15, 2023. The conference room on the 27th floor of JSW Centre in Mumbai's Bandra Kurla Complex was packed with investment bankers, lawyers, and company executives. After months of preparation, road shows, and regulatory filings, the final IPO pricing meeting was underway. The debate was intense: price it high to maximize proceeds, or conservative to ensure a successful listing? The decision was made: ₹2,800 crores entirely through fresh issue—no offer for sale, no promoter dilution. The issue comprised 23,52,94,117 equity shares of the face value of ₹2 aggregating up to ₹2,800.00 Crores. The price band was set at ₹119 per share.

This wasn't just fundraising—it was validation. After 24 years of building in relative obscurity, JSW Infrastructure was stepping into the spotlight. The roadshows had been grueling. Arun Maheshwari and the management team had crisscrossed from Mumbai to Singapore, London to New York, explaining to global investors why Indian ports mattered, why JSW was different, why this wasn't just another infrastructure play riding the India story.

The anchor book told the real story. JSW Infrastructure IPO raises ₹1,260.00 crore from anchor investors on September 22, 2023. Half the IPO was already spoken for before retail investors could even apply. The names were impressive—global funds that rarely participated in Indian infrastructure offerings were writing large checks.

JSW Infrastructure IPO bidding started from September 25, 2023 and ended on September 27, 2023. Those three days felt like three years. The subscription numbers started trickling in: Day 1 ended at 2.5x, respectable but not spectacular. Day 2 jumped to 12x. By the final day, the momentum was unstoppable.

The final tally was staggering: The JSW Infrastructure Ltd IPO is subscribed 37.37 times. The public issue subscribed 10.32 times in the retail category, 57.09 times in the QIB category, and 15.99 times in the NII category. The QIB (Qualified Institutional Buyers) oversubscription of 57x was particularly telling—smart money was betting big on ports.

October 3, 2023. The listing day. The JSW team gathered at the BSE building for the ceremonial bell ringing. Sajjan Jindal, usually stoic, allowed himself a smile. The shares got listed on BSE, NSE on October 3, 2023. The public issue was offered at ₹119.00 per share and was listed at ₹143, delivering a listing gain of 20.17%.

The remarkable 37.37x oversubscription of the IPO demonstrates the unwavering faith the public has in our vision and performance, the company would later state. But the numbers told a deeper story. At listing, JSW Infrastructure commanded a market capitalization of over ₹33,000 crores—making it larger than many established infrastructure companies that had been public for decades.

The capital allocation strategy was clear and conservative. The proceeds would go toward prepayment or repayment of certain outstanding borrowings through investment in wholly owned subsidiaries JSW Dharamtar Port Private Limited and JSW Jaigarh Port Limited, and financing capital expenditure for proposed expansion/upgradation works at Jaigarh Port including expansion of LPG terminal.

The PE ratio at IPO of 28.88 seemed reasonable compared to Adani Ports trading at 40x. But valuation wasn't the story—credibility was. After more than 13 years, JSW Group is reopening with an IPO. JIL is the second-largest commercial port operator in India in terms of cargo handling capacity.

The post-IPO performance would validate the enthusiasm. Within months, the stock would touch ₹200, delivering nearly 70% returns to IPO investors. The public market entry wasn't just about capital—it was about transparency, governance, and the discipline that comes with quarterly scrutiny. For a company that had operated in the shadows of its steel parent for two decades, the spotlight was both challenge and opportunity.

VII. Modern Operations & Business Model

Inside JSW Infrastructure's command center at Jaigarh Port, dozens of screens display real-time data: vessel positions, crane productivity, truck movements, weather patterns. A ship carrying 180,000 tons of coal is being unloaded at 4,000 tons per hour—twice the speed of a government port just 50 kilometers away. This operational excellence isn't accident; it's architecture.

JSW Infrastructure Limited stands as the second-largest private port operator in India, boasting significant cargo handling capacity of 170 MTPA. But capacity without efficiency is just concrete and steel. The real story lies in utilization and mechanization.

The cargo portfolio reads like a catalog of India's economy: dry bulk, break bulk, liquid bulk, gases, and containers, including thermal coal, coal (other than thermal coal), iron ore, sugar, urea, steel products, rock phosphate, molasses, gypsum, barites, laterites, edible oil, LNG, LPG, and containers. This isn't diversification for its own sake—each cargo type represents a customer relationship, a supply chain solution, a revenue stream immune to single-commodity volatility.

The mechanization story deserves special attention. At Paradip, twin ship-loaders each handling 7,000 tons per hour can load a Capesize vessel in under 24 hours—a task that takes manual ports three to four days. At Jaigarh, covered conveyor systems move coal from ship to rail without a single grain of dust escaping into the atmosphere. These aren't just machines; they're competitive weapons.

Revenue architecture reveals sophisticated financial engineering. Long-term contracts with anchor customers, some of which include take-or-pay provisions, provide baseline revenue regardless of cargo volumes. Take-or-pay means customers pay for minimum guaranteed capacity whether they use it or not—transforming a cyclical business into something approaching an annuity.

The numbers validate the model: Market cap of ₹62,412 Crore, Revenue of ₹4,690 Cr, Profit of ₹1,614 Cr. The EBITDA margins hovering around 55% would make software companies envious. How does a capital-intensive infrastructure business generate such margins?

The answer lies in operational leverage. Once a port is built and mechanized, the marginal cost of handling additional cargo is minimal. A crane operator managing automated systems can handle 10x the cargo of manual operations. A single control room manages operations that once required hundreds of supervisors. This is the infrastructure paradox: massive upfront investment, near-zero marginal costs. The growth trajectory validates the model: JSW Infrastructure's installed cargo handling capacity in India experienced a CAGR of 15.27%, increasing from 153.43 MTPA as of March 31, 2021, to 158.43 MTPA as of March 31, 2023. Simultaneously, the cargo volume in India witnessed an CAGR of 42.76%, growing from 2021 to 2023. Volume growing nearly 3x faster than capacity—that's utilization improvement at scale.

The multi-modal evacuation story sets JSW apart. While competitors rely on trucks and congested highways, JSW operates an integrated logistics network: dedicated rail sidings at every major terminal, a fleet of mini-bulk carriers for coastal shipping, and covered conveyor systems eliminating intermediate handling. Higher utilization rates at Paradip Iron Ore Terminal, Paradip Coal Terminal, and Mangalore Coal Terminal contributed to volume growth.

Container operations reveal the next growth vector. The Mangalore Container Terminal saw cargo volume expand 33% versus last year, with third-party volume rising 47%. Containers generate 3-4x the revenue per ton of bulk cargo—a margin multiplier that transforms port economics.

The financial metrics tell the efficiency story: Higher volumes translated into a 21% increase in consolidated revenue to Rs. 1,018 crore. Thanks to operating leverage and cost control efforts, EBITDA jumped 33% to Rs. 558 crore while EBITDA margin held firm at 54.8%.

Value-added services represent the hidden revenue stream. Beyond basic loading and unloading, JSW provides cargo blending (mixing different grades of coal to customer specifications), bagging and packaging, warehousing, and even financing solutions. Each service adds 5-10% to base tariffs while creating switching costs that lock in customers.

The technology backbone deserves attention. Automated gate systems reduce truck turnaround from hours to minutes. IoT sensors on cranes provide real-time productivity metrics. Predictive maintenance algorithms prevent breakdowns before they occur. This isn't digitization theater—it's operational excellence through technology.

Comprehensive maritime services encompass cargo handling, storage solutions, logistics services, and value-added offerings—each layer adding margin while deepening customer relationships. The evolution from port operator to logistics solutions provider isn't just semantic—it's strategic positioning for India's next decade of growth.

VIII. Competitive Dynamics & Market Position

The numbers are stark and sobering: Adani commands a 24% volume share whereas JSW Infrastructure is a mere 6%. In any other industry, this gap would signal an also-ran destined for irrelevance. But ports aren't like other industries—geography is destiny, and JSW has chosen its geography wisely.

Adani Ports' dominance is undeniable. From Mundra to Krishnapatnam, they've built an empire that handles everything from containers to cars. Their integrated logistics play through Adani Logistics creates end-to-end solutions that JSW can't match. Yet JSW isn't trying to be Adani—they're playing a different game entirely.

JSW Infrastructure, a part of JSW Group, is the second largest commercial port operator in India in terms of cargo handling capacity. Second place in infrastructure isn't failure—it's positioning. While Adani chases scale everywhere, JSW focuses on strategic locations tied to industrial clusters. This isn't David versus Goliath; it's specialization versus diversification.

The related party conundrum requires honest examination. The share of third-party cargo increased to 46% in 4QFY24 from 37% in 4QFY23. Critics point to the 54% captive cargo as weakness—dependence on the JSW Group that limits growth potential. But this misses the strategic value of anchor customers. Guaranteed baseline volumes allow for infrastructure investments that wouldn't be viable on merchant cargo alone.

Promoter Holding: 83.6%—a number that signals both commitment and concern. The high promoter stake ensures aligned interests but limits free float, potentially impacting valuations. Yet this concentration also enables quick decision-making and long-term thinking rare in widely-held companies.

Strategic locations near industrial clusters represent JSW's true moat. Jaigarh serves Maharashtra's industrial belt. Paradip sits at the heart of Odisha's mineral wealth. Ennore connects to Tamil Nadu's manufacturing corridor. These aren't just ports—they're industrial infrastructure integrated into supply chains that would take decades to replicate.

Multi-modal evacuation advantage goes beyond having rail and road connections. JSW's ports are designed as logistics hubs, not just transfer points. The ability to store, blend, package, and forward cargo creates value that pure transshipment can't match. While Adani builds bigger ports, JSW builds stickier ones.

The private versus government port dynamics favor JSW's model. Government ports, constrained by bureaucracy and labor unions, operate at 70% efficiency on good days. JSW's mechanized operations run at 90%+ efficiency consistently. This 20-percentage point gap is pure competitive advantage monetized through premium pricing for reliability.

But competitive dynamics are shifting. The Adani Group on the other hand has been focusing on growing their container shipping business. You know, when folks like Amazon or Hyundai want to ship stuff, they stuff it into these massive containers. That kind. And from 32% of revenues in FY16, it has inched up to 38% in FY23. As India's trade shifts from bulk commodities to manufactured goods, container capacity becomes critical.

JSW's response has been measured but strategic. Rather than compete head-on in containers, they're partnering with global operators, providing port infrastructure while letting specialists handle operations. It's acknowledgment that not every battle needs to be fought to win the war.

The market position reveals a sustainable niche: not the biggest, but among the most efficient; not the most diversified, but the most integrated; not purely independent, but not entirely captive. In infrastructure, being indispensable to a few often beats being optional to many.

IX. Growth Strategy & Future Vision

"300 MTPA by 2030"—the number hangs in the air during every investor call, every analyst meeting. It's not just a target; it's a statement of intent that JSW Infrastructure plans to nearly double capacity in six years. But the real story isn't the number—it's how they plan to get there. The revised target is even more ambitious: JSW Infrastructure has announced a Rs 300 billion capital expenditure plan to boost its cargo-handling capacity to 400 million tonnes per annum (MTPA) by FY30. From 170 MTPA today to 400 MTPA—a 135% increase that would require perfect execution.

The growth strategy reveals sophistication: a mix of greenfield and brownfield projects at key strategic locations across India. Brownfield expansion at existing ports in Jaigarh, Dharamtar, and Goa leverages existing infrastructure. Greenfield development at Jatadhar, Keni, and Murbe targets emerging industrial clusters.

Upgrading Salav Port, building two greenfield ports at Nangaon and Keni—each project carefully selected for strategic value rather than size. The Board approved a total capacity expansion plan of 36 MTPA (15 MTPA at Jaigarh and 21 MTPA at Dharamtar), with construction anticipated to be completed by March 2027.

The container terminal ambitions mark a strategic shift. JSW Infrastructure incorporated wholly owned subsidiary for Kolkata port container terminal project. This isn't just adding capacity—it's entering higher-margin segments where Adani has dominated.

December 2023: Plans to acquire majority stake in PNP Port for ₹270 crore signals the inorganic growth playbook. Why build when strategic assets can be acquired at reasonable valuations? The acquisition strategy focuses on operational ports with existing customer relationships—immediate revenue, no construction risk.

Digital transformation represents the hidden accelerator. Port automation, IoT-enabled tracking, blockchain for documentation—each innovation shaves minutes off turnaround times, reduces errors, improves safety. In infrastructure, small efficiencies compound into competitive advantages.

ESG initiatives aren't greenwashing—they're business strategy. The company has committed to reducing its greenhouse gas emissions and achieving net-zero emissions by 2050. Green ports attract ESG-conscious customers, qualify for sustainability-linked financing, and preempt regulatory challenges.

The financial foundation enables ambition: With zero net debt as of September 30, 2024, JSWIL is well-positioned for aggressive expansion and value-driven acquisitions. Zero net debt in a capital-intensive business—that's not conservatism, it's optionality.

The logistics integration deserves special attention. Plans to enhance its logistics network through acquisitions, including Navkar Corporation, and a slurry pipeline project transform JSW from port operator to supply chain orchestrator. When you control the nodes and the connections, you control the network.

Customer diversification continues: third-party cargo now accounting for 48% of total volumes in H1 FY25, compared to just 5% in FY19. The company aims for a 50-50 split between group and third-party customers to ensure stability and profitability.

"Our goal is to create an efficient, integrated ports and logistics ecosystem that will support India's economic growth. This expansion will deliver long-term value to our stakeholders," said Rinkesh Roy, Joint MD and CEO. The vision isn't just about tonnage—it's about becoming indispensable to India's supply chains.

X. Investment Thesis & Risk Analysis

The investment case for JSW Infrastructure rests on a fundamental bet: that India's infrastructure needs will grow faster than its ability to build government-owned capacity. It's a bet on privatization by necessity rather than ideology.

The Bull Case:

India's infrastructure megatrend is undeniable. The government's National Infrastructure Pipeline targets ₹111 trillion investment by 2025. Maritime infrastructure alone requires ₹1.5 trillion. Government coffers can't fund this alone—private capital is essential, and JSW is positioned to capture this opportunity.

Strategic asset locations with long-term concessions create moats measured in decades. A 50-year port concession isn't just a contract—it's a multi-generational monopoly on specific trade routes. Once industries build around your port, switching costs become prohibitive.

The diversified cargo and geographic mix provides resilience. Coal down? Iron ore might be up. West coast congested? East coast operations compensate. This isn't diversification for its own sake—it's portfolio theory applied to infrastructure.

Strong parent backing and anchor customers solve the chicken-and-egg problem plaguing independent port operators. JSW Steel's cargo provides baseline utilization allowing for infrastructure investments that pure merchant ports can't justify.

High barriers to entry protect returns. Building a greenfield port requires environmental clearances that take years, capital that runs into thousands of crores, and operational expertise that can't be hired overnight. By the time a competitor builds capacity, JSW has moved on to the next expansion.

The valuation remains reasonable. Trading at P/E of 28.88 versus Adani Ports at 40x, despite superior margins and comparable growth. The discount for related-party dependence may be excessive given improving third-party mix.

The Bear Case:

High dependence on JSW Group remains concerning. Despite improvements, over 50% of cargo still comes from related parties. What happens if JSW Steel's fortunes reverse? Can the ports survive independently?

Competition from Adani Ports is intensifying. Adani's scale advantages in procurement, financing, and operations create cost structures JSW struggles to match. In commodity businesses, the lowest-cost producer eventually wins.

Regulatory and environmental risks are escalating. Coastal Regulation Zone rules, environmental clearances, land acquisition challenges—each can delay projects by years and inflate costs by multiples.

The capital intensive business model limits flexibility. Once you've spent ₹5,000 crores on a port, you're committed regardless of market conditions. High fixed costs mean utilization drops translate directly to margin compression.

Global trade volatility impacts volumes immediately. Trade wars, pandemic disruptions, commodity cycles—factors beyond JSW's control determine cargo flows. Being efficient doesn't help if ships aren't sailing.

The governance concerns around high promoter holding (83.6%) limit institutional investment. Low free float creates liquidity issues and valuation discounts that may persist regardless of operational performance.

The Balanced View:

JSW Infrastructure represents a specific type of infrastructure bet: not the largest or fastest-growing, but possibly the most sustainable. The company has chosen to be the strong #2 rather than chase unprofitable growth.

The strategy of focusing on industrial clusters rather than pure transshipment creates stickier revenue streams. Serving steel plants and power stations generates predictable, long-term cargo flows that pure merchant ports can't access.

Recent operational metrics validate the model. Revenue growth of 20%+, EBITDA margins of 55%, ROCE approaching 20%—these aren't accidents but the result of disciplined capital allocation and operational excellence.

The risk-reward appears favorable for patient capital. Near-term volatility from commodity cycles and related-party concerns may create entry opportunities for investors with 5-10 year horizons.

Key Monitorables:

- Third-party cargo mix reaching 50%+ (reduces related-party risk)

- Capacity utilization above 65% (operational leverage kicks in)

- Container terminal success (higher-margin validation)

- Debt-to-equity maintaining below 1x (financial flexibility)

- Greenfield project execution on time and budget (execution credibility)

XI. Playbook: Lessons for Infrastructure Investing

The JSW Infrastructure story offers a masterclass in building infrastructure businesses in emerging markets. The lessons extend beyond ports to any capital-intensive, long-gestation sector where patient capital meets operational excellence.

Lesson 1: Long-term concession models create predictable moats

The 30-50 year port concessions JSW secures aren't just contracts—they're options on India's growth. In infrastructure, time horizons determine competitive advantages. While markets obsess over quarterly earnings, infrastructure returns compound over decades.

Lesson 2: Vertical integration in industrial groups isn't weakness—it's strategy

Critics dismiss captive cargo as dependence, missing the strategic value. Anchor customers de-risk the initial investment, provide baseline utilization for mechanization, and create demonstration effects that attract third parties. Independence is earned, not declared.

Lesson 3: Building versus buying infrastructure assets requires nuanced thinking

JSW's mixed approach—greenfield where strategic, acquisitions where opportunistic—reveals sophistication. Build when you need specific configurations or locations. Buy when operational assets are mispriced. The discipline is knowing which and when.

Lesson 4: Government relations in infrastructure aren't corruption—they're capability

Managing relationships with port authorities, customs, railways, environmental regulators—this coordination capability is as important as operational efficiency. Infrastructure operates at the intersection of public and private, requiring skills MBA programs don't teach.

Lesson 5: Scaling capital-intensive businesses requires creative financing

JSW's journey from private funding to IPO to potential infrastructure investment trusts shows evolution in capital strategy. Each growth phase requires different capital structures. The ability to tap multiple funding sources determines growth potential.

Lesson 6: Anchor customers in infrastructure are features, not bugs

The stability provided by long-term contracts with take-or-pay provisions creates the foundation for infrastructure investment. Merchant capacity comes later, built on the backbone of committed volumes. Security enables ambition.

Lesson 7: Operational excellence in infrastructure compounds

Small improvements in turnaround time, crane productivity, or fuel efficiency compound into competitive advantages. JSW's focus on mechanization and automation shows that infrastructure isn't just about concrete and steel—it's about systems and processes.

Lesson 8: Geographic diversification in infrastructure requires strategic coherence

JSW's port locations aren't random dots on a map but strategic positions serving industrial clusters. Each port reinforces the network effect. Random diversification destroys value; strategic positioning creates it.

The playbook reveals a deeper truth: infrastructure investing isn't about finding the next hot sector but about identifying long-term structural shifts and positioning assets to capture value over decades. It requires patience private markets understand but public markets struggle to price.

XII. Epilogue & Future Outlook

As the sun sets over the Arabian Sea, casting long shadows across Jaigarh Port's massive cranes, the next chapter of JSW Infrastructure's story is being written. The company stands at an inflection point where three powerful forces converge: India's infrastructure ambitions, global supply chain realignment, and the energy transition.

India's maritime ambitions under the Sagarmala program envision $120 billion investment in port modernization by 2035. The program targets reducing logistics costs from 14% to 10% of GDP—a shift that would add $300 billion to India's economy. JSW Infrastructure, with its strategic port locations and operational expertise, is positioned to capture a meaningful share of this transformation.

Technology disruption in ports is accelerating. Automation reduces labor costs by 50% while improving safety and productivity. AI-powered predictive maintenance prevents breakdowns before they occur. IoT sensors track every container, every truck, every ship in real-time. JSW's greenfield projects incorporate these technologies from day one, while brownfield expansions systematically upgrade existing infrastructure.

But the real revolution may come from green shipping and sustainability imperatives. The International Maritime Organization's 2050 net-zero target will reshape global shipping. Ports that can provide green hydrogen bunkering, shore power for docked vessels, and carbon-neutral operations will command premiums. JSW's commitment to net-zero by 2050 isn't just environmental responsibility—it's competitive positioning for a decarbonizing world.

What would success look like in 2030?

Success would mean 400 MTPA capacity fully utilized, generating ₹15,000 crores revenue at 60% EBITDA margins. It would mean container operations contributing 20% of revenues at 2x the margins of bulk cargo. It would mean third-party cargo at 60%, definitively proving independence from the JSW Group.

But true success goes beyond numbers. It would mean JSW Infrastructure recognized not as "JSW's ports business" but as India's most efficient port operator. It would mean becoming the partner of choice for manufacturing companies setting up operations in India. It would mean creating a replicable model for infrastructure development that balances private returns with public benefit.

Key metrics for investors to watch:

The traditional metrics—revenue, EBITDA, capacity—tell only part of the story. Watch instead for: - Average turnaround time per vessel (efficiency indicator) - Revenue per ton handled (pricing power metric) - Third-party customer additions (market validation) - Technology adoption rate (future competitiveness) - Green cargo percentage (ESG positioning) - Employee productivity ratios (operational excellence)

The Broader Context:

JSW Infrastructure's journey from captive logistics provider to public infrastructure company mirrors India's own evolution. As India aims to become a $10 trillion economy by 2035, infrastructure will determine whether this ambition becomes reality or remains aspiration.

The company's success or failure won't just affect shareholders. It will influence whether Indian manufacturing can compete globally, whether supply chains can handle growing trade volumes, whether infrastructure can be built sustainably. In this sense, JSW Infrastructure isn't just a company—it's a test case for India's infrastructure ambitions.

Final Thoughts:

The story of JSW Infrastructure teaches us that in infrastructure, the race doesn't always go to the swiftest or largest. Sometimes it goes to those who understand that infrastructure isn't about building monuments but about enabling commerce, that operational excellence beats financial engineering, that patience and persistence can overcome scale disadvantages.

As India writes its next chapter of growth, companies like JSW Infrastructure will determine the plot. They're building not just ports but possibilities, not just handling cargo but enabling commerce, not just creating shareholder value but national competitiveness.

The next decade will reveal whether JSW Infrastructure can transcend its origins to become a truly independent infrastructure champion. The foundations are strong, the strategy is clear, and the opportunity is massive. What remains is execution—the mundane, difficult, daily work of moving millions of tons of cargo efficiently, safely, and profitably.

In infrastructure, that's everything.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube