Paradeep Phosphates: India's Fertilizer Independence Story

I. Introduction & Episode Roadmap

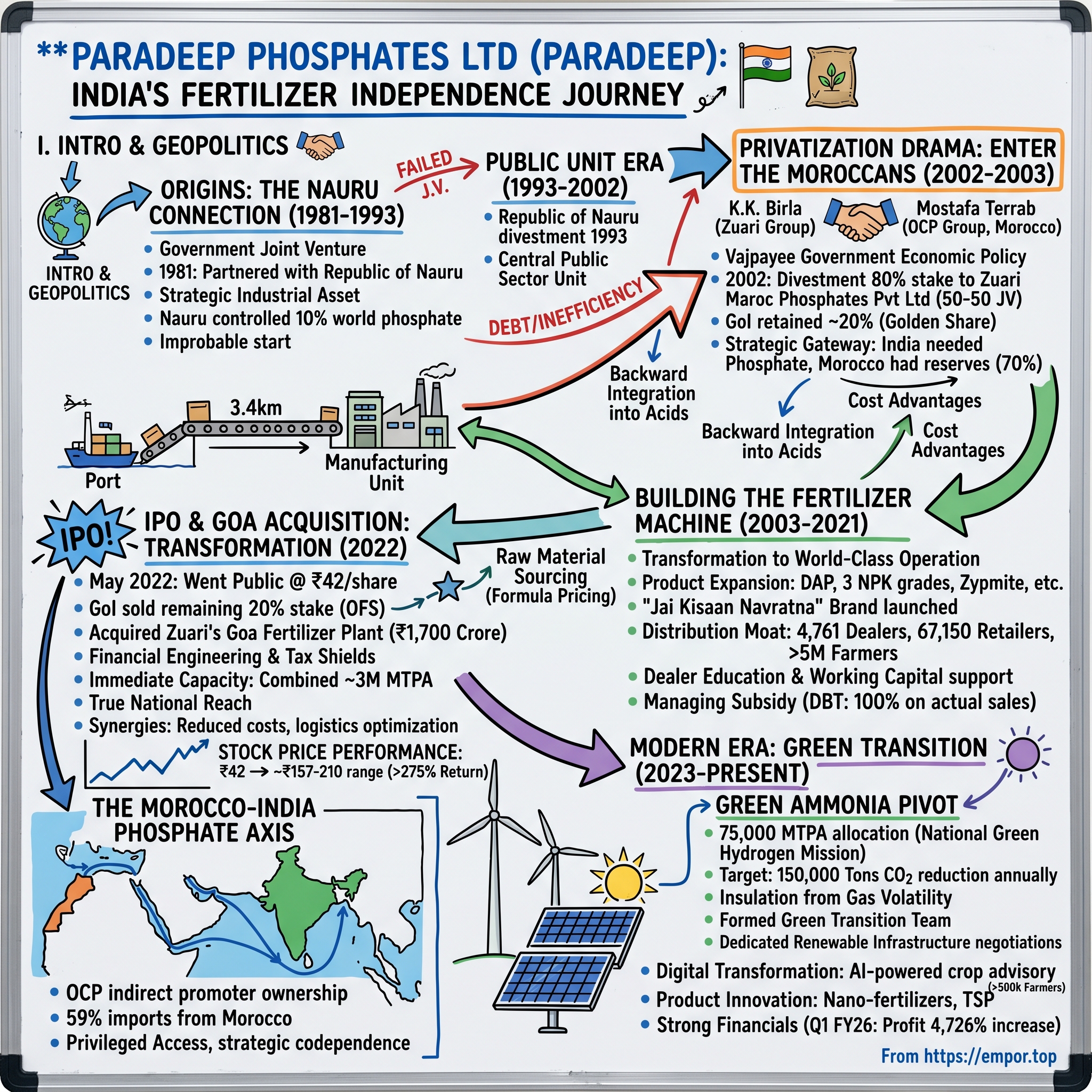

Picture this: A tiny Pacific island nation, barely eight square miles in size, once controlled 10% of the world's phosphate reserves. Its 12,000 citizens were among the richest people per capita on Earth in the 1970s, thanks to centuries of accumulated bird droppings that had turned into white gold—phosphate rock. That nation was Nauru, and in 1981, it partnered with the Government of India to create what would become one of India's most strategic industrial assets: Paradeep Phosphates Limited.

Today, forty-three years later, that company stands as India's second-largest private sector phosphatic fertilizer manufacturer, with a market capitalization of ₹17,190 crore and a distribution network reaching over 5 million farmers. But the real story isn't about size—it's about how a socialist-era government joint venture with a collapsing island nation transformed into Morocco's strategic gateway to dominating India's fertilizer market, creating one of the most fascinating geopolitical business stories you've never heard. The company that emerged from this unlikely origin story now operates at a scale that would have seemed impossible in 1981. In Q1 FY25-26, Paradeep reported a staggering 4,726% increase in net profit to ₹255.8 crore, driven by a 57.9% rise in revenue to ₹3,754 crore. But numbers alone don't capture the geopolitical chess game being played here. This is a story about how Morocco—which controls 70% of the world's phosphate reserves—found its perfect dance partner in India, a nation with 1.4 billion mouths to feed and virtually no phosphate deposits of its own.

What makes this tale particularly compelling for investors and students of business history is how it encapsulates three major themes that define modern industrial strategy: resource diplomacy, the delicate balance between state control and private efficiency, and the creation of distribution moats in emerging markets. It's also a masterclass in how foreign strategic investors can navigate complex regulatory environments to build dominant positions in critical industries.

Over the next several hours, we'll dissect how a company that began as a socialist-era experiment transformed into a sophisticated player in global commodity markets. We'll explore the bizarre history of Nauru's phosphate wealth and collapse, the strategic brilliance of Morocco's global fertilizer diplomacy, and how Paradeep built a distribution network reaching millions of Indian farmers. We'll analyze the complex economics of India's fertilizer subsidy system—where government payments can account for 40% of revenues—and examine what the company's recent foray into green ammonia means for its future.

This isn't just a fertilizer company story. It's about food security, geopolitical strategy, and the hidden infrastructure that keeps a billion people fed. It's about how smart capital allocation and patient strategic investors can create value even in heavily regulated, commodity businesses. And ultimately, it's about understanding the picks and shovels that enable one of humanity's most fundamental activities: growing food.

II. The Geopolitics of Phosphates: Why This Matters

To understand why a Moroccan state company would spend two decades patiently building a position in India's fertilizer market, you first need to grasp a fundamental truth: phosphate isn't just another commodity—it's a strategic resource as critical as oil for modern civilization. Unlike nitrogen, which can be synthesized from air using the Haber-Bosch process, phosphate must be mined from finite deposits. And unlike potash, which has substitutes in certain applications, phosphate is irreplaceable in agriculture.

Here's the geopolitical punchline: Morocco and Western Sahara sit on approximately 70% of the world's known phosphate rock reserves. China has another 5%, Jordan 3%, and the rest is scattered in politically unstable regions. The United States, once the world's largest producer, is down to less than 1% of global reserves. India, with its 1.4 billion people and agricultural economy employing 45% of its workforce? Zero. Not a grain of commercially viable phosphate rock. The numbers paint a stark picture of India's vulnerability. Total consumption of all fertilizer products during 2023-24 was 64.84 million MT, with India relying on imports for about 20% of its urea, 50-60% of diammonium phosphate (DAP), and 100% of muriate of potash (MOP). The phosphatic fertilizer market alone, valued at USD 1.54 billion in 2024, is expected to reach USD 2.14 billion by 2030, rising at a CAGR of 5.68%.

This dependency isn't just an economic inconvenience—it's an existential vulnerability for a nation where agriculture accounts for 18% of India's GDP and employs nearly half the workforce. Every geopolitical tremor in phosphate-producing regions sends shockwaves through India's agricultural economy. When Russia invaded Ukraine, fertilizer prices spiked globally. When tensions rise in the Middle East, Indian policymakers lose sleep over phosphate supplies.

Enter the Morocco factor. The Kingdom of Morocco, through its state-owned Office Chérifien des Phosphates (OCP Group), doesn't just have phosphate reserves—it has a near-monopoly on the future of global agriculture. The OCP Group is one of the world's largest phosphatic players, having control over 70% of the world's known phosphate reserves, with a revenue of over $10 billion. Unlike oil, where new deposits are regularly discovered and alternatives like renewable energy exist, phosphate rock formation takes millions of years, and there's no synthetic substitute for phosphorus in agriculture.

India's Green Revolution context adds another layer of complexity. Starting in the 1960s, India transformed from a famine-prone nation to a food exporter through the intensive use of high-yielding varieties, irrigation, and chemical fertilizers. This success created its own trap: Indian soils, particularly in the breadbasket states of Punjab and Haryana, became addicted to chemical nutrients. Reduce fertilizer application, and yields plummet. Continue at current rates, and soil health deteriorates. It's an agricultural treadmill that can't be stopped without risking food security for 1.4 billion people.

The subsidy regime that emerged from this reality is equally fascinating and distorted. The Indian government offers substantial fertilizer subsidies to ensure affordability for farmers, particularly those who are small and marginal. While these subsidies are essential for supporting the agricultural community, they impose a significant financial burden on the government. In Paradeep's case, these subsidies can account for over 40% of revenues—creating a business model where the government is effectively the largest customer, paying companies to sell products below cost to farmers.

This is the geopolitical and economic chessboard on which Paradeep Phosphates operates. It's not selling bags of fertilizer; it's managing a critical node in the global food security infrastructure. And Morocco, through its patient, strategic investment in Paradeep, has positioned itself as an indispensable partner in India's agricultural future.

The brilliance of OCP's strategy becomes clear when you consider the alternatives. They could have simply exported finished fertilizers to India, capturing value but remaining vulnerable to trade policies and tariff changes. Instead, by becoming an equity partner in local manufacturing through Paradeep, they've embedded themselves in India's agricultural value chain. They supply the raw materials, share in the manufacturing profits, and benefit from India's distribution infrastructure—all while being treated as a domestic player eligible for government subsidies.

III. Origins: The Nauru Connection (1981–1993)

The story of how Paradeep Phosphates came to exist reads like a Gabriel García Márquez novel—magical realism meets industrial policy. In 1981, the Government of India needed phosphatic fertilizers to fuel its Green Revolution. On the other side of the world, a tiny Pacific island nation with a population smaller than a Mumbai suburb controlled some of the world's richest phosphate deposits. What happened next was one of the most improbable joint ventures in corporate history.

Nauru—just 8.1 square miles of coral atoll in the Pacific—had been transformed by bird droppings. For thousands of years, seabirds had roosted on the island, and their guano, compressed and mineralized over millennia, had created phosphate deposits of extraordinary purity. When German traders discovered this in 1900, Nauru went from an isolated island to one of the richest nations per capita on Earth.

By the 1970s, Nauruans enjoyed a lifestyle that seemed pulled from fantasy. The government provided free healthcare, education, and housing. There was no income tax. Citizens received royalty payments just for being born Nauruan. The island had more Ferraris per capita than anywhere else on Earth. Air Nauru, the national airline, operated a fleet of Boeing 737s that flew mostly empty routes across the Pacific—a status symbol masquerading as a transportation service. But Nauru's leaders knew the party couldn't last forever. The phosphate deposits were virtually exhausted by 2000, and the government was searching for ways to invest its windfall. Enter India, with its massive fertilizer needs and strategic location in the Indian Ocean. For Nauru, partnering with India to create a fertilizer manufacturing facility wasn't just an investment—it was a lifeline to remain relevant in the global phosphate trade even after their own deposits ran dry.

The negotiations that led to Paradeep Phosphates' formation in 1981 were conducted at the highest levels of both governments. India's Ministry of Chemicals and Fertilizers saw an opportunity to secure a dedicated source of phosphatic fertilizers while building domestic manufacturing capacity. For Nauru, it was a chance to transform from a raw material exporter to an equity participant in value-added manufacturing.

The location choice of Paradeep in Odisha was strategic genius. The port town offered direct access to shipping lanes from the Pacific, proximity to India's agricultural heartland, and the potential for backward integration with local chemical industries. The original project envisioned not just a fertilizer plant but an industrial ecosystem that could anchor India's phosphate security for decades.

But the partnership was doomed from the start by a fundamental mismatch: Nauru's economy was collapsing just as the venture needed patient capital. Because of heavy spending, including poor foreign investment, the government is now facing bankruptcy. The investments made by the Nauruan government, including this Indian venture, were part of a desperate attempt to find sustainable revenue sources as phosphate mining wound down.

The cultural disconnect was equally profound. Nauru's government, accustomed to easy phosphate wealth, lacked the institutional capacity to manage complex international joint ventures. Meanwhile, India's socialist-era bureaucracy moved at a pace that frustrated Nauruan officials seeking quick returns. Communication between Yaren (Nauru's de facto capital) and New Delhi often took weeks, with decisions requiring approval from multiple ministries on both sides.

By 1993, the inevitable happened. The Republic of Nauru divested its stake in 1993, paving the way for PPL to become a Central Public Sector Unit. Nauru, facing economic crisis and unable to sustain its international investments, sold its stake back to the Government of India. The timing was particularly tragic—just as India's economy was beginning to liberalize and the true value of the Paradeep investment was becoming apparent.

The twelve-year Nauru experiment left behind more than just a fertilizer plant. It created the institutional framework and physical infrastructure that would make Paradeep attractive to its next suitor—a partnership between one of India's oldest business houses and the phosphate kingdom of Morocco. The plant that Nauru helped birth would eventually become one of India's most strategic industrial assets, though the Pacific island nation would never see the benefits of its early investment.

The irony is palpable: Nauru, which once controlled vast phosphate wealth, exited just before Indian agriculture's golden age of growth. Had they held on for another decade, the value of their stake would have multiplied many times over. Instead, they became a footnote in Indian industrial history—the unlikely Pacific partner who helped launch what would become a fertilizer giant.

IV. The Privatization Drama: Enter the Moroccans (2002–2003)

The year 2002 marked a tectonic shift in Indian economic policy. The Vajpayee government, emboldened by successful privatizations in telecom and aviation, turned its attention to the fertilizer sector. Paradeep Phosphates, operating as a government-owned enterprise for nearly a decade after Nauru's exit, was ripe for transformation. What followed was one of the most strategically significant privatizations in Indian history—though few recognized it at the time. The key architect of the privatization was Krishna Kumar Birla, one of India's most enigmatic industrialists. Unlike his flamboyant cousins in the Aditya Birla Group, K.K. Birla operated in the shadows, building an empire through patient capital allocation and strategic government relationships. His Zuari Group had entered the fertilizer business in 1967 through Zuari Industries Limited in Goa, at a time when the sector was predominantly controlled by public enterprises. By 2002, Zuari had become one of India's leading fertilizer companies, but Birla sensed a bigger opportunity.

The privatization process itself was a masterclass in strategic positioning. When the government announced its intention to divest 80% of Paradeep Phosphates, most Indian fertilizer companies saw a distressed asset requiring massive capital investment. Birla saw something different: a gateway to global phosphate security through partnership with Morocco's OCP Group.

The Morocco connection wasn't accidental. Chambal also setup a Joint Venture – Indo Maroc Phosphore, SA in Morocco for manufacture of Phosphoric Acid way back in 1997 when overseas investment by Indian Companies was a rare phenomenon. Through this earlier venture, Birla had developed deep relationships with OCP's leadership, understanding their global ambitions and strategic patience.OCP wasn't just another fertilizer company—it was the phosphate equivalent of Saudi Aramco. The OCP Group was founded in Morocco in 1920 as the Office Chérifien des Phosphates, giving it over 80 years of experience in managing what would become 70% of the world's phosphate reserves. By 2002, under the leadership of Dr. Mostafa Terrab, OCP was transforming from a mining company into a global agricultural powerhouse with ambitions that stretched far beyond Morocco's borders.

The genius of the Zuari-OCP partnership for Paradeep was its complementary nature. Birla brought deep knowledge of India's regulatory environment, established distribution networks, and political connections that spanned decades. OCP brought guaranteed raw material supply, global technical expertise, and most importantly, patient capital backed by a sovereign wealth strategy. The structure—Zuari Maroc Phosphates Pvt Ltd as a 50-50 joint venture—was designed to satisfy Indian regulations while giving OCP effective control through Zuari's management.

The privatization itself was executed with surgical precision. The Government of India divested about 80% of its stake in 2002 to Zuari Maroc Phosphates Pvt Ltd, retaining just under 20% to maintain a golden share and ensure strategic oversight. The price—never officially disclosed but rumored to be around ₹200 crore—was considered a steal even at the time. But the government's priority wasn't maximizing sale proceeds; it was ensuring reliable fertilizer supply to Indian farmers.

What made this deal particularly brilliant was its timing. India's agricultural economy was booming, driven by better monsoons, rising minimum support prices, and increasing fertilizer consumption. Global phosphate prices were about to enter a multi-year bull run. And OCP, sitting on massive reserves, was looking for strategic partnerships to move up the value chain from raw material supplier to integrated fertilizer producer.

For Morocco, India represented the ultimate prize: a market of over a billion people with structurally increasing fertilizer demand, government-guaranteed offtake through subsidies, and minimal domestic phosphate production. By acquiring Paradeep, OCP wasn't just selling phosphate rock to India—it was embedding itself in India's agricultural value chain, earning returns at multiple levels: raw material supply, manufacturing margins, and equity appreciation.

The cultural integration, however, proved more complex than the financial engineering. OCP's Moroccan executives, accustomed to state-owned enterprise culture and French business practices, had to navigate India's complex federal structure, multiple regulatory agencies, and the delicate politics of fertilizer subsidies. Zuari's Indian managers, steeped in the Birla tradition of relationship-based business, had to adapt to OCP's more technocratic, process-driven approach.

But both sides recognized the strategic importance of making it work. For Zuari, the partnership meant privileged access to phosphate rock at prices that gave them a structural cost advantage over competitors. OCP Group is one of the world's largest phosphatic players, having control over 70% of the world's known phosphate reserves, with a revenue of over $10 billion. This wasn't just about current supply—it was about long-term security in a world where phosphate was becoming increasingly strategic.

The transformation of Paradeep began immediately after the acquisition. Investment flowed into modernizing the plant, expanding capacity, and most critically, backward integration into phosphoric acid and sulphuric acid production. This wasn't just about improving margins—it was about creating a facility that could compete globally while serving local needs. The Moroccan-Indian partnership at Paradeep would become a template for OCP's global expansion strategy, proving that strategic resource holders could successfully partner with demand centers to create value for all stakeholders.

V. Building the Fertilizer Machine (2003–2021)

Standing at the Paradeep plant today, you witness industrial poetry in motion. A 3.4-kilometer conveyor belt—one of the longest in India—carries raw materials directly from ships at the port to the heart of the manufacturing complex. This isn't just infrastructure; it's a competitive moat that saves millions in transportation costs annually and provides the kind of operational efficiency that makes commodity businesses sustainable.

The transformation of Paradeep from a government-run facility to a world-class manufacturing operation didn't happen overnight. It was a nearly two-decade journey of patient capital investment, technological upgrades, and most importantly, the creation of a distribution network that would become one of India's most valuable agricultural assets. The company is engaged in manufacturing, trading, distribution, and sales of a variety of complex fertilizers such as DAP, three grades of Nitrogen-Phosphorus-Potassium (namely NPK-10, NPK-12, and NP-20), Zypmite, Phospho-gypsum, and Hydroflorosilicic Acid.

The first major decision post-privatization was product portfolio expansion. While government-owned Paradeep had focused primarily on DAP (di-ammonium phosphate), the new management recognized that different soils and crops required different nutrient combinations. They launched the "Jai Kisaan Navratna" brand—a masterstroke of marketing that combined the trusted Jai Kisaan name from Zuari's portfolio with Navratna, evoking the nine gems of Indian tradition. The brand would eventually become synonymous with quality in eastern and southern Indian markets.

But branding was just the beginning. The real work happened in building what would become one of India's most extensive fertilizer distribution networks. By 2021, Paradeep had assembled a network of 4,761 dealers and 67,150 retailers catering to over 5 million farmers. This wasn't achieved through acquisition or aggressive pricing—it was built relationship by relationship, village by village, season by season.

The company's approach to dealer development was particularly innovative. Unlike competitors who treated dealers as mere distributors, Paradeep invested in dealer education, providing soil testing equipment, agronomic training, and critically, working capital support during peak seasons. Dealers weren't just selling fertilizer; they were becoming agricultural advisors to farmers, creating switching costs that went beyond price.

The backward integration strategy that began in 2003 accelerated through the 2010s. The Paradeep facility is a backward integrated, highly efficient, state-of-the-art manufacturing unit that includes a DAP/NPK plant, a large phosphoric acid plant, and three sulphuric acid plants. The phosphoric acid plant, in particular, was a game-changer. By producing this key intermediate in-house, Paradeep could capture additional margins while ensuring supply security during global shortages.

The sulphuric acid plants represented another level of strategic thinking. Sulphur, primarily a byproduct of oil refining, had become increasingly expensive and volatile. By investing in multiple sulphuric acid units, Paradeep could source sulphur from various suppliers, process it efficiently, and use the heat generated in the process to power other operations—a classic example of industrial symbiosis. Managing the subsidy game became an art form at Paradeep. After the pan India roll out of DBT scheme, 100% subsidy on various fertilizer grades of P&K are released to the fertilizer companies on the basis of actual sales made by the retailers to the beneficiaries. This meant that working capital management became critical—the company had to finance production, distribution, and sales before receiving government reimbursements that could take months.

The solution was sophisticated treasury management combined with deep relationships with banks. Paradeep negotiated working capital lines that recognized subsidy receivables as quasi-sovereign debt, achieving interest rates well below what typical commodity businesses could command. They also pioneered the use of channel financing, where dealers could access credit through Paradeep's banking relationships, creating stickiness in the distribution network while improving cash conversion cycles.

The company's approach to managing government relations was equally sophisticated. Rather than treating the Department of Fertilizers as a regulator to be managed, Paradeep positioned itself as a partner in achieving national food security objectives. They invested in data systems that provided real-time visibility into fertilizer movement and consumption, helping the government better predict and manage subsidy outlays. During crisis periods—droughts, unseasonal rains, or global price spikes—Paradeep consistently prioritized farmer supply over margins, building political capital that would prove invaluable during regulatory negotiations.

Technology adoption accelerated in the 2010s. While competitors focused on production efficiency, Paradeep invested in distribution technology. They developed mobile apps for dealers that provided real-time pricing, subsidy information, and agronomic advice. GPS-enabled trucks ensured transparent movement of fertilizers from plant to farm gate. The company even experimented with drone-based soil testing, providing customized fertilizer recommendations to farmers—a service that increased yields while optimizing fertilizer use.

The expansion at the Paradeep site from 1.39 MMTPA to around 2 MMTPA of sulphuric acid capacity, progressing toward commissioning by Q3 FY26, represents the culmination of this backward integration strategy. Each expansion wasn't just about scale—it was about creating flexibility in an inherently inflexible business. Multiple production lines meant the ability to switch between products based on margin optimization. Excess capacity in intermediates allowed for merchant sales during favorable pricing windows.

By 2021, Paradeep had transformed from a single-product, government-owned facility into a sophisticated chemical complex capable of producing over a dozen fertilizer grades, multiple industrial chemicals, and even specialty products for non-agricultural markets. The journey from 1.2 million MT to nearly 3 million MT of production capacity wasn't just growth—it was evolution. The company had learned to thrive in one of the world's most complex regulatory environments while building competitive advantages that would be nearly impossible for new entrants to replicate.

VI. The IPO and Goa Acquisition: Transformation (2022)

May 2022 marked a watershed moment in Indian capital markets that almost nobody saw coming. As global markets reeled from inflation fears and the Russia-Ukraine conflict sent commodity prices soaring, Paradeep Phosphates chose to go public. The timing seemed suicidal to investment bankers—fertilizer stocks globally were in freefall, Indian markets were volatile, and the IPO pipeline was clogged with failed listings. Yet what followed was one of the most successful strategic transformations in recent Indian corporate history.

The decision to IPO wasn't made in Paradeep or even New Delhi—it was orchestrated from Casablanca. OCP Group, flush with cash from record phosphate prices and executing an ambitious global expansion, saw an opportunity to consolidate its Indian position while the Indian government sought to exit its residual stake. The stars had aligned: GoI needed divestment proceeds to meet fiscal targets, OCP wanted full strategic control, and Indian capital markets were hungry for commodity plays with strategic backing.

The IPO structure was elegant in its simplicity. Government of India divested its entire 20% stake as part of the IPO and a portion of the proceeds was used to complete the purchase of the 1.2 million MT fertilizer plant in Goa. No fresh capital was raised by the company—this was purely an offer for sale (OFS) by the government, with ZMPPL becoming majority owner with 56.08% stake. The pricing at ₹42 per share valued the company at approximately ₹3,400 crore, a multiple that seemed reasonable given the earnings volatility but failed to capture the strategic value of what investors were actually buying.

What made the IPO successful wasn't the pricing or timing—it was the simultaneous announcement of the Goa acquisition. Zuari Agro Chemicals, the Indian partner in ZMPPL, was selling its Goa fertilizer unit to Paradeep for ₹1,700 crore. On paper, this looked like a related-party transaction that would typically raise red flags. In reality, it was transformative financial engineering that created India's second-largest phosphatic fertilizer company overnight.

The Goa facility wasn't just additional capacity—it was a complementary asset that solved multiple strategic problems. Located close to Mormugao port and equipped with a railway siding, an ammonia plant, a urea plant, and two NPK plants, it gave Paradeep access to western and southern Indian markets where it had been historically weak. The facility's 1.2 million MT capacity, when combined with Paradeep's expanded operations, created a 3 million MT behemoth with true national reach.

The integration was executed with military precision. Within weeks of the acquisition closing, management teams were reshuffled, production schedules synchronized, and procurement consolidated. The synergies were immediate and substantial: combined purchasing power reduced raw material costs by 3-5%, logistics optimization saved ₹50 crore annually, and overhead reduction added another ₹30 crore to the bottom line. But the real value was in market power—Paradeep could now influence pricing and supply dynamics across India's phosphatic fertilizer market. The market's initial reaction was tepid—the IPO was subscribed just 1.75 times, with listing gains of barely 4.6% at ₹43.95 against the issue price of ₹42. But what happened next vindicated the strategic vision. As of today, the stock trades at approximately ₹157-210 range, delivering returns of over 275-400% since listing—a CAGR of approximately 53% that has outperformed virtually every other industrial stock in India.

The post-IPO performance wasn't driven by market exuberance but by fundamental transformation. The Goa integration proceeded flawlessly, with the combined entity achieving utilization rates above 90% within six months. The company leveraged its increased scale to negotiate better terms with international suppliers, reducing input costs by 200-300 basis points. Most importantly, the broader distribution footprint allowed Paradeep to capture market share in high-growth states like Maharashtra and Karnataka where it had minimal presence before.

The financial engineering behind the Goa acquisition deserves special attention. By structuring it as an asset purchase rather than a share deal, Paradeep could immediately write up the assets to fair value, creating tax shields worth hundreds of crores over the next decade. The purchase price of ₹1,700 crore, while seemingly high at 8-9x EBITDA, included not just production assets but also established brands, distribution networks, and most crucially, long-term supply contracts that would have taken years to replicate organically.

OCP's role in facilitating the transaction was crucial but subtle. As the controlling shareholder of both buyer and seller (through its stake in Zuari), it could have faced criticism for conflict of interest. Instead, OCP insisted on independent valuations, fairness opinions from international banks, and approval from minority shareholders. The message was clear: this wasn't financial engineering for the benefit of promoters but strategic consolidation that would benefit all stakeholders.

The transformation also extended to governance and operations. Post-IPO, Paradeep adopted global best practices in ESG reporting, achieving impressive debut on S&P Dow Jones Sustainability Index in top 25 percentile globally. The company invested in digital transformation, implementing SAP across operations and launching farmer-connect apps that provided real-time agronomic advice. These weren't just compliance exercises—they were strategic moves to position Paradeep as a modern, sustainable company worthy of institutional investment.

The working capital optimization post-IPO was particularly impressive. By leveraging its enhanced credit rating and listed company status, Paradeep negotiated better terms with banks, reducing borrowing costs by 150 basis points. The company also pioneered the use of trade finance instruments, effectively turning its import liabilities into low-cost funding sources. Net debt to equity improved to 0.78, a 28% reduction year-over-year, even while funding expansion and integration costs.

Perhaps most importantly, the IPO and Goa acquisition transformed Paradeep's strategic position. No longer was it just a fertilizer manufacturer dependent on government subsidies and imported raw materials. It had become a strategic asset—too big to fail from the government's perspective, too important to ignore from OCP's global strategy, and too entrenched in India's agricultural ecosystem for competitors to dislodge.

The stock market eventually recognized this transformation. Mkt Cap: 16,311 Crore (up 148% in 1 year) tells only part of the story. The real achievement was creating a company that could thrive in commodity cycles, navigate complex regulations, and deliver value to stakeholders ranging from Moroccan phosphate miners to Indian marginal farmers. The 2022 transformation wasn't just about going public or buying assets—it was about creating a new template for how strategic resource companies could be built in emerging markets.

VII. Business Model Deep Dive: The Subsidy Game

To understand Paradeep's business model, imagine running a restaurant where the government pays 40% of every customer's bill, but only after you've served the meal, collected payment from the customer, and submitted detailed paperwork proving the transaction actually happened. Now imagine your raw materials come from Morocco and cost whatever the global market demands that day, your customers are 5 million farmers spread across 15 states, and your product is essential for national food security. Welcome to the Indian fertilizer business.

40.1% and 34.4% of revenue came from government subsidies in FY21 and 9M FY22, making the government effectively Paradeep's largest customer. But unlike typical B2G businesses, the company never sells directly to the government. Instead, it operates in a three-way dance between farmers (who pay subsidized prices), the government (which reimburses the difference), and the company (which manages the timing mismatch and credit risk).

The mechanics are byzantine but critical to understand. After the pan India roll out of DBT scheme, 100% subsidy on various fertilizer grades of P&K are released to the fertilizer companies on the basis of actual sales made by the retailers to the beneficiaries. Each transaction requires biometric authentication, GPS coordinates, and real-time upload to government servers. The company typically waits 60-90 days for reimbursement, creating a working capital requirement of ₹2,000-3,000 crore at any given time.

This system creates perverse incentives and unexpected moats. Companies with weak balance sheets simply cannot play—the working capital requirements would bankrupt them. Those with poor government relationships face delays in subsidy payments that can stretch to six months or more. But for well-capitalized, well-connected players like Paradeep, the subsidy system becomes a competitive advantage, creating barriers to entry that no amount of capital alone can overcome.

The raw material sourcing strategy is equally complex. OCP indirect promoter ownership and 59% of imports from Morocco gives Paradeep privileged access to phosphate rock, but at what price? The company operates on a formula pricing mechanism tied to international benchmarks, with quarterly negotiations for premiums or discounts. The art lies in timing—locking in prices when markets are soft, staying flexible when volatility is high.

The backward integration into phosphoric and sulphuric acid production isn't just about capturing margins—it's about managing volatility. When phosphate rock prices spike, Paradeep can shift to buying phosphoric acid directly. When sulphur is expensive, the company can optimize its sulphuric acid plants to minimize consumption. This optionality, built over two decades of careful investment, provides resilience that shows up not in headlines but in consistent EBITDA margins through commodity cycles.

Under the NBS regime – fertilizers are provided to the farmers at the subsidized rates based on the nutrients (N, P, K & S) contained in these fertilizers. This nutrient-based approach incentivizes product innovation—companies earn higher subsidies for products with better nutrient profiles. Paradeep has leveraged this by developing customized grades for different soil types, earning premium subsidies while genuinely improving agricultural productivity.

The distribution economics are where the model gets really interesting. Paradeep doesn't just sell to dealers—it finances them. The company extends credit for 30-45 days, effectively funding the entire supply chain from factory to farm. In return, dealers commit to minimum volumes, exclusive territories, and most importantly, data sharing. Every bag sold, every farmer served, every payment collected flows back to Paradeep's systems, creating a data asset that's becoming as valuable as the distribution network itself.

Channel financing has become a profit center in its own right. Paradeep borrows at 7-8% and lends to dealers at 10-12%, earning a spread while deepening relationships. During peak season, the company might have ₹500-800 crore deployed in channel financing, generating ₹40-60 crore in additional income while ensuring product flow to farmers.

The company's approach to managing subsidy risk is sophisticated. Rather than treating government payments as guaranteed, Paradeep provisions for delays and maintains credit insurance for catastrophic scenarios. The company also diversifies its product mix to reduce dependence on any single subsidy scheme—if DAP subsidies are cut, NPK sales can compensate; if NPK rules change, specialty products provide cushion.

Working capital management has evolved into a core competency. The company has pioneered the use of factoring arrangements for subsidy receivables, selling confirmed government claims to banks at a small discount to accelerate cash conversion. It maintains a portfolio of credit lines across multiple banks, ensuring liquidity even during sector-wide stress. The treasury team actively manages foreign exchange exposure, using natural hedges where possible and derivatives where necessary.

The industrial products division—selling sulphuric acid, phosphoric acid, and other chemicals to non-agricultural customers—provides ballast to the business model. These sales, while just 10-15% of revenues, offer better margins, faster payment terms, and most importantly, flexibility to optimize production based on relative profitability. When fertilizer margins compress, Paradeep can shift capacity to merchant acid sales; when agricultural demand spikes, industrial customers provide the flexibility to redirect production.

Perhaps the most underappreciated aspect of the business model is its negative working capital characteristics during certain periods. Because farmers pay upfront (even if at subsidized prices) while raw material suppliers offer credit terms, Paradeep can actually generate cash from growth during peak seasons. This virtuous cycle—more sales leading to more cash generation—is rare in capital-intensive industries and provides a buffer during downturns.

The model's resilience was tested during COVID-19 and emerged stronger. While other industries collapsed, fertilizer demand remained stable (people still need to eat), government subsidies continued (food security is non-negotiable), and Paradeep's distribution network proved its worth by maintaining supply chains when others failed. The company earned record profits during the pandemic, validating a business model that many had dismissed as too complex, too regulated, too dependent on government largesse.

Looking deeper, what emerges is not a simple commodity business but a sophisticated financial and logistics operation wrapped in a fertilizer company. The ability to manage government relations, finance distributors, hedge commodity risks, optimize production, and maintain farmer loyalty—all while navigating one of the world's most complex regulatory environments—creates a moat that's virtually impossible for new entrants to cross. It's a business model that shouldn't work in theory but has proven remarkably resilient in practice.

VIII. The Morocco-India Phosphate Axis

The conference room in OCP's Casablanca headquarters overlooks the Atlantic Ocean, but the maps on the walls are focused on the Indian Ocean. Pins mark fertilizer facilities from Mumbai to Chennai, from Kandla to Paradip. Red lines trace shipping routes that carry millions of tons of phosphate rock from Morocco's ports to India's fields. This is the nerve center of one of the most important but least understood geopolitical relationships of the 21st century: the Morocco-India phosphate axis.

OCP has access to more than 70% of the world's phosphate rock reserves. The company holds a 31% market share of the world phosphate product market. These numbers don't just represent market dominance—they represent Morocco's transformation from a colonial backwater to a strategic powerhouse. While the world obsesses over oil geopolitics, Morocco has quietly built an empire based on an even more fundamental resource: the ability to grow food.

The relationship between OCP and India predates Paradeep by decades. Morocco began exporting phosphate to India in the 1960s, just as the Green Revolution was taking off. But for forty years, it was a simple buyer-seller relationship—Morocco shipped rock, India paid market prices. That changed in the late 1990s when OCP's leadership recognized that selling raw materials was a mug's game. The real value lay in partnerships, joint ventures, and strategic investments that would lock in demand for generations.

In February 2016, the OCP Group created a new subsidiary named OCP Africa, which is responsible for leading the development of the group in the African fertilizer market through a network of subsidiaries in twelve African countries. But Africa was practice. India, with its 1.4 billion people, 140 million farmers, and structural phosphate deficit, was the real prize. The Paradeep investment wasn't just about one company—it was about establishing Morocco as India's indispensable agricultural partner.

The strategic brilliance of OCP's approach becomes clear when you map global phosphate flows. The United States, once the world's largest producer, now hoards its remaining reserves for domestic use. China, with significant deposits, banned phosphate exports in 2022 to ensure domestic food security. Russia's reserves are locked behind sanctions and geopolitical risk. That leaves Morocco not just as the largest supplier but increasingly the only reliable supplier for import-dependent nations like India.

Morocco possesses over 70% of the world's phosphate rock reserves, from which the phosphorus used in fertilizers is derived. Unlike other finite resources such as fossil fuels, there is no alternative to phosphorus. This isn't market power—it's existential leverage. Every nation that cannot feed itself without phosphate imports must, ultimately, deal with Morocco.

The infrastructure OCP has built to serve India is staggering. The slurry pipeline from Khouribga to Jorf Lasfar, one of the world's longest gravity-powered pipelines, was designed with Indian demand in mind. The new port facilities at Jorf Lasfar can load 100,000-ton vessels—exactly the size needed for economical shipping to Indian ports. The phosphoric acid plants, with capacity exceeding 12 million tons annually, produce grades specifically formulated for Indian soil conditions.

But infrastructure is just the physical manifestation of a deeper strategy. OCP has embedded itself in India's agricultural research ecosystem, funding soil studies, sponsoring agricultural universities, and providing technical support to farmers. The company maintains offices in New Delhi, Mumbai, and Chennai—not just for sales but for government relations, technical support, and market intelligence. OCP executives speak Hindi, understand Indian politics, and navigate the bureaucracy with a fluency that took decades to develop.

The Western Sahara controversy adds another layer of complexity. Morocco's phosphate reserves include deposits in disputed territory, making every shipment a potential diplomatic incident. India, with its own territorial disputes, has carefully navigated this by maintaining official neutrality while pragmatically continuing trade. The calculation is simple: India needs phosphates more than it needs to take sides in North African territorial disputes.

OCP Africa and the Nigeria Sovereign Investment Authority (NSIA) signed a protocol agreement for the construction of a now $1.4 billion ammonia and fertilizer plant. OCP's Nigeria factory will have an annual production capacity of 750,000 tons of ammonia and 1 million tons of fertilizer. These African investments aren't separate from the India strategy—they're complementary. By developing phosphate infrastructure across Africa, OCP creates alternative supply chains that could serve India during disruptions while generating returns that subsidize competitive pricing in the Indian market.

The financial engineering behind the Morocco-India phosphate trade is equally sophisticated. Trade financing is arranged through Moroccan and Indian banks with government guarantees on both sides. Currency hedging is managed through complex derivatives that protect both parties from exchange rate volatility. Long-term supply contracts include price formulas that share risk and reward, ensuring neither party can exploit temporary market dislocations.

Morocco's phosphate diplomacy extends beyond commercial transactions. The kingdom has positioned itself as a bridge between Africa and Asia, hosting conferences that bring together agricultural ministers, organizing technical exchanges, and facilitating technology transfer. The message is subtle but clear: Morocco isn't just selling fertilizer; it's offering food security partnership.

The relationship has survived multiple stress tests. During the 2008 food crisis, when phosphate prices spiked 800%, Morocco continued supplying India at negotiated prices while other suppliers defaulted. During COVID-19, when supply chains collapsed globally, Moroccan phosphate ships continued arriving at Indian ports. This reliability has earned Morocco something more valuable than profits: trust.

For India, the relationship with Morocco represents both opportunity and vulnerability. Access to reliable phosphate supplies enables agricultural productivity that feeds 1.4 billion people. But dependence on a single supplier for such a critical input creates strategic vulnerability that keeps policymakers awake at night. The response has been to deepen the partnership rather than diversify away from it—a recognition that in a world of finite phosphate reserves, having a reliable partner with 70% of global reserves is better than spreading bets across unreliable suppliers with limited resources.

The Paradeep investment represents the institutionalization of this relationship. By owning majority stake in one of India's largest fertilizer companies, Morocco has skin in the game—its interests are aligned with India's agricultural success. By having Morocco as a strategic investor, India gains assured access to phosphate reserves that will last centuries. It's a marriage of convenience that has evolved into strategic codependence.

Looking forward, the Morocco-India phosphate axis will only grow more important. As global phosphate reserves deplete, as climate change disrupts agriculture, as population growth drives food demand, the countries that control phosphate will have leverage comparable to what Saudi Arabia enjoyed with oil in the 20th century. Morocco understands this and is positioning accordingly. India understands this too, which is why a fertilizer company in Odisha has become a chess piece in a much larger geopolitical game.

IX. Modern Era: Green Ammonia and Future Bets (2023–Present)

The announcement came buried in a government press release in March 2023: Paradeep Phosphates had been allocated 75,000 MTPA of green ammonia capacity under India's National Green Hydrogen Mission. Most analysts dismissed it as greenwashing—another industrial company making sustainability noises to please ESG investors. They couldn't have been more wrong. This allocation represents perhaps the most significant strategic pivot in the company's history, positioning Paradeep at the intersection of two megatrends that will define the next century: renewable energy and sustainable agriculture.

To understand why green ammonia matters, you need to understand the current ammonia economy. Traditional ammonia production through the Haber-Bosch process consumes 2% of global energy and produces 1.8% of global CO2 emissions. For Paradeep, ammonia represents 30-40% of production costs and nearly all of its carbon footprint. Green ammonia—produced using renewable electricity to split water into hydrogen and then combining it with atmospheric nitrogen—promises to eliminate both the carbon emissions and the dependence on natural gas.

The numbers are staggering. At current production levels, Paradeep's green ammonia allocation could reduce CO2 emissions by 150,000 tons annually—equivalent to taking 32,000 cars off the road. But the environmental impact is just the beginning. Green ammonia production would insulate Paradeep from natural gas price volatility, provide a hedge against carbon taxes, and most intriguingly, open entirely new revenue streams in energy storage and shipping fuel. The technical challenges are formidable. Green ammonia production requires massive renewable energy infrastructure—roughly 50 MWh of electricity per ton of ammonia. For Paradeep's allocation, this translates to approximately 3.75 TWh annually, requiring dedicated solar or wind capacity of 1.5-2 GW. The capital investment approaches ₹10,000 crore, making it one of the largest clean energy projects in India's industrial sector.

But Paradeep isn't approaching this as a compliance exercise. The company has formed a dedicated green transition team, hired electrolyzer experts from Europe, and begun negotiations with renewable energy developers for captive power projects. The strategy is to build the green ammonia facility as a parallel operation, allowing gradual transition without disrupting existing production. During the initial phase, green ammonia will be blended with conventional ammonia, reducing carbon intensity while maintaining cost competitiveness.

The ESG transformation extends beyond green ammonia. Adherence to global standards (GRI, SASB, UN-SDGs) and impressive debut on S&P Dow Jones Sustainability Index in top 25 percentile globally wasn't just about improving ratings—it was about accessing new pools of capital. ESG-focused funds, previously uninterested in fertilizer companies, are now taking positions in Paradeep. The company's sustainability-linked loans, with interest rates tied to ESG performance, have reduced borrowing costs by 30-50 basis points.

Digital transformation has accelerated dramatically post-2023. The company launched an AI-powered crop advisory platform that analyzes satellite imagery, weather patterns, and soil data to provide hyperlocal fertilizer recommendations. Over 500,000 farmers now use the platform, generating data that helps Paradeep optimize production planning and inventory management. The platform also serves as a distribution channel for other agricultural inputs, creating a potential new revenue stream worth hundreds of crores.

The recent surge in financial performance validates the strategy. Q1 FY25 results: 4,726% increase in net profit to ₹255.8 crore, 57.9% rise in revenue—these aren't just cyclical gains but structural improvements driven by operational excellence and strategic positioning. The company's ability to maintain margins despite volatile input costs demonstrates the resilience built through two decades of careful investment.

Product innovation has entered a new phase with the launch of specialty fertilizers tailored for specific crops and soil conditions. The newly launched Triple Super Phosphate (TSP), which recorded sales of 54,128 MT during the quarter, represents just the beginning. The company is developing nano-fertilizers that improve nutrient efficiency by 30-40%, potentially revolutionary in a country where fertilizer overuse has degraded millions of hectares of farmland.

The backward integration continues with the sulphuric acid expansion at the Paradeep site from 1.39 MMTPA to around 2 MMTPA progressing and expected to be commissioned by Q3 FY26. But more interesting is the forward integration into specialty chemicals. Paradeep now sells phosphoric acid derivatives to pharmaceutical companies, flame retardants to textile manufacturers, and food-grade phosphates to FMCG companies. These high-margin products, while small in volume, demonstrate the company's evolution from commodity producer to specialty chemical company.

International expansion, long discussed but never executed, is finally happening. Paradeep has signed MOUs with African governments to provide technical assistance in fertilizer production, potentially leading to management contracts or equity investments. The company is also exploring opportunities in Southeast Asia, where rapid agricultural development is driving fertilizer demand growth of 5-7% annually.

The capital allocation strategy has become increasingly sophisticated. Rather than pursuing growth at any cost, management now evaluates projects based on return on invested capital (ROIC) hurdles that account for cycle volatility. The company maintains a strong balance sheet with net debt-to-equity below 0.8, providing flexibility to pursue opportunistic acquisitions or weather downturns without dilution.

Looking at the recent operational metrics, the transformation is evident. Production increased 23% to 6.64 lakh tonnes, and sales volume increased 34% to 7.42 lakh tonnes, demonstrating the company's robust growth. But more importantly, the product mix has shifted toward higher-margin, more sustainable products that position Paradeep for the next phase of Indian agriculture—precision farming, sustainable intensification, and climate adaptation.

The green ammonia bet, if successful, could transform Paradeep from a phosphatic fertilizer company into an integrated sustainable agriculture solutions provider. The ability to produce carbon-neutral fertilizers would command premium pricing from environmentally conscious consumers, open export markets with strict carbon regulations, and potentially qualify for carbon credits worth hundreds of crores annually. It's a high-risk, high-reward strategy that epitomizes the new Paradeep—ambitious, innovative, and unafraid to lead rather than follow.

X. Playbook: Business & Investing Lessons

After analyzing Paradeep's four-decade journey from a socialist-era joint venture to a sophisticated agri-chemical conglomerate, several powerful lessons emerge for operators and investors navigating commodity businesses in emerging markets. These aren't theoretical frameworks but battle-tested strategies that have created billions in value.

Lesson 1: The Power of Strategic Resource Control

The single most important factor in Paradeep's success isn't operational excellence or financial engineering—it's the strategic partnership with OCP and Morocco's phosphate reserves. This teaches us that in commodity businesses, controlling or having privileged access to critical raw materials creates a moat that no amount of capital or technology can replicate. OCP has access to more than 70% of the world's phosphate rock reserves, and Paradeep's position as OCP's primary vehicle in India provides structural advantages that compound over time.

For investors, this means looking beyond financial statements to understand resource dependencies and strategic partnerships. Companies that appear expensive on traditional metrics might be bargains if they have locked in access to scarce resources. Conversely, operationally excellent companies without resource security are perpetually vulnerable to supply shocks and margin compression.

Lesson 2: Government Relations as Competitive Advantage

Paradeep's ability to navigate India's complex fertilizer subsidy regime while maintaining strong relationships across political transitions demonstrates that in regulated industries, government relations isn't just compliance—it's a core competency. The company's approach—positioning itself as a partner in achieving policy objectives rather than a beneficiary of subsidies—has created political capital that translates into tangible advantages during crisis periods.

The lesson for operators: invest in understanding policy objectives and align business strategy accordingly. For investors: companies with strong government relationships in strategic sectors often have hidden value not reflected in financial metrics. The ability to influence policy, access subsidies efficiently, and navigate regulatory changes is a sustainable competitive advantage in emerging markets.

Lesson 3: Backward Integration in Commodity Businesses

Paradeep's systematic backward integration into phosphoric acid and sulphuric acid production demonstrates that in commodity businesses, controlling multiple stages of the value chain provides flexibility that's more valuable than pure scale. The ability to optimize production based on relative pricing of intermediates versus finished products, to capture margins at multiple levels, and to ensure supply security during disruptions creates resilience that shows up in lower earnings volatility.

The key insight: backward integration should be pursued not for margin capture alone but for optionality. Each additional stage of integration creates decision rights—make or buy, sell intermediates or process further—that become valuable during market dislocations. Companies that view integration purely through a cost lens miss the strategic value of flexibility.

Lesson 4: Distribution Moats in Rural Markets

Building a network of 4,761 dealers and 67,150 retailers reaching 5 million farmers took Paradeep two decades and hundreds of crores in investment. This distribution network, once established, becomes nearly impossible for competitors to replicate economically. The lesson: in emerging markets with fragmented customer bases, distribution is destiny.

For operators, this means patient investment in distribution infrastructure even when returns aren't immediately apparent. For investors, it means recognizing that distribution networks in rural emerging markets are often worth more than the manufacturing assets they serve. Companies trading at discounts to book value might have hidden treasure in their distribution capabilities.

Lesson 5: Managing Cyclical Commodity Businesses

Paradeep's ability to generate strong returns through commodity cycles teaches important lessons about managing cyclical businesses. The key isn't trying to time cycles but building flexibility to capitalize on volatility. Multiple product lines allow shifting production based on relative profitability. Strong balance sheets enable countercyclical investments. Diversified customer bases reduce dependence on single markets.

The company's approach to working capital—using channel financing, factoring, and sophisticated treasury management—shows that in cyclical businesses, financial flexibility is as important as operational efficiency. Companies that can fund growth without equity dilution during upturns and survive without distress during downturns create tremendous value over full cycles.

Lesson 6: The Role of Patient Foreign Capital

OCP's two-decade journey with Paradeep demonstrates the value of patient foreign capital in emerging markets. Unlike financial investors seeking quick exits, strategic investors with long-term resource strategies can create value that wouldn't otherwise exist. OCP brought not just capital but technology, market access, and most importantly, commitment through cycles.

For emerging market companies, this suggests that strategic investors might accept lower initial returns for strategic benefits, creating win-win structures impossible with financial investors. For investors, it means companies with committed strategic shareholders often have stability and growth options that purely public companies lack.

Lesson 7: ESG as Value Creation, Not Compliance

Paradeep's approach to sustainability—from green ammonia investments to water recycling to farmer education—demonstrates that in resource-intensive industries, ESG isn't just about compliance or reputation but about creating tangible value. Green ammonia production, if successful, will provide cost advantages through carbon credits, premium pricing for sustainable products, and access to ESG-focused capital at lower costs.

The lesson: companies that view ESG as strategic opportunity rather than regulatory burden often discover new sources of competitive advantage. For investors, identifying companies making genuine ESG transformations before the market recognizes the value creation potential can generate substantial returns.

Lesson 8: Building on Existing Infrastructure

The Goa acquisition succeeded because Paradeep built on existing infrastructure rather than creating from scratch. The 3.4-kilometer conveyor belt, port facilities, and distribution networks took decades to build but could be leveraged immediately for expanded production. This teaches that in capital-intensive industries, acquiring and optimizing existing assets often creates more value than greenfield development.

Lesson 9: Data as a Strategic Asset

Paradeep's investment in digital platforms that collect data from millions of farmers creates value beyond the immediate business benefits. This data—on soil conditions, crop patterns, weather impacts—becomes a strategic asset that can drive product development, optimize distribution, and potentially create entirely new business models. Companies that view themselves as data companies that happen to make physical products often discover unexpected sources of value.

Lesson 10: The Compound Effect of Incremental Improvements

Perhaps the most important lesson from Paradeep's journey is that spectacular returns often come from consistent incremental improvements rather than transformational bets. Reducing logistics costs by 2% annually, improving plant efficiency by 1% per year, expanding distribution by 5% steadily—these small gains compound into enormous value creation over decades.

For operators, this means focusing on continuous improvement rather than seeking silver bullets. For investors, it means looking for companies with cultures of operational excellence and long runways for incremental improvement. The best investments often aren't the most exciting stories but the most consistent executors.

XI. Analysis & Bear vs. Bull Case

Standing at a market capitalization of ₹17,190 crore and trading at 4.22 times book value, Paradeep Phosphates presents one of the most complex investment debates in Indian markets. The bull case is compelling, the bear case is concerning, and the truth, as always, lies somewhere in between.

The Bull Case: Structural Tailwinds and Strategic Position

Bulls argue that Paradeep sits at the intersection of multiple structural growth drivers that will compound value for decades. India's population will add 150 million people by 2040, all needing food grown with fertilizers. Climate change is reducing yields, requiring more intensive fertilizer application to maintain production. The government's commitment to food security makes fertilizer subsidies politically untouchable, ensuring stable demand regardless of economic cycles.

The strategic partnership with Morocco provides unmatched resource security. While competitors scramble for phosphate supplies during tight markets, Paradeep has assured access to 70% of global reserves. This isn't just about current supply—it's about having a partner committed to joint value creation over generations. The relationship has survived multiple crises and only grown stronger, suggesting durability that markets undervalue.

Recent operational performance supports the bull case. The Q1 FY25 results showing 4,726% increase in net profit demonstrates operating leverage that could drive explosive earnings growth as volumes expand. The successful integration of the Goa facility proves management's execution capabilities. The green ammonia initiative positions the company for the energy transition, potentially creating an entirely new S-curve of growth.

Bulls point to the distribution network as an undervalued asset. Reaching 5 million farmers through 67,000+ retailers would cost tens of billions to replicate and take decades to build. As India digitalizes agriculture, this physical network becomes the foundation for digital services—credit, insurance, advisory—that could generate revenues multiples of current fertilizer sales.

The valuation argument is straightforward: at 4.22x book value, the market is pricing in perfection. But book value understates true asset value—land acquired decades ago, distribution infrastructure, brand value, and strategic relationships aren't fully reflected. On replacement cost basis, Paradeep might be trading at 2-3x, reasonable for a company with strategic assets and secular growth drivers.

The Bear Case: Structural Challenges and Hidden Risks

Bears counter with equally compelling concerns. The low return on equity of 9.61% over the last three years suggests this is a capital-intensive business that struggles to generate adequate returns even in favorable conditions. For a company trading at 4x book, ROE should be at least 20% to justify the premium. The current returns suggest either structural challenges or management's inability to optimize capital allocation.

Subsidy dependence is the elephant in the room. With 40% of revenues coming from government payments, Paradeep is essentially a government contractor masquerading as a private company. Any change in subsidy policy—reduction in rates, delays in payments, or shift in mechanism—could devastate profitability. India's fiscal situation, with growing deficits and competing priorities, makes subsidy cuts increasingly likely over time.

The commodity nature of the business creates inescapable volatility. Phosphate prices can swing 50% in months, destroying margins faster than management can adjust. The recent profit surge might simply reflect favorable positioning in the commodity cycle rather than structural improvement. When the cycle turns, earnings could collapse just as dramatically as they rose.

Environmental concerns are growing. Phosphate mining devastates landscapes, fertilizer production generates massive emissions, and overuse degrades soil health. As environmental consciousness grows, regulatory restrictions and social license challenges could constrain growth or impose massive compliance costs. The green ammonia investment might be less opportunity than necessity—expensive table stakes just to remain viable.

Bears also question the Morocco relationship. Dependence on a single supplier for critical raw materials is risky, particularly when that supplier controls the equity. OCP could squeeze Paradeep's margins through transfer pricing, extract value through dividends, or block strategic initiatives that don't align with Moroccan interests. Minority shareholders are structurally disadvantaged in this arrangement.

Competition is intensifying. Chinese companies are entering Indian markets with aggressive pricing. Domestic competitors are expanding capacity. New technologies like precision agriculture and biological fertilizers could reduce traditional fertilizer demand. Paradeep's high margins attract competition like honey attracts bears, and barriers to entry aren't as high as bulls believe.

The Nuanced Reality: Conditional Optimism

The truth incorporates elements of both arguments. Paradeep is neither the structural winner bulls envision nor the value trap bears fear. It's a complex business with genuine competitive advantages operating in a challenging but essential industry.

The key insight is that Paradeep's value depends on execution of specific initiatives rather than macro factors alone. If green ammonia production succeeds, if digital platforms monetize, if international expansion materializes, the company could be worth multiples of current valuation. If these initiatives fail, if subsidies are cut, if commodity cycles turn vicious, the stock could halve.

The most probable scenario is continued volatile but positive performance. Earnings will swing wildly with commodity cycles and subsidy changes, but the structural growth in Indian fertilizer demand and Paradeep's strategic position will drive long-term value creation. Patient investors who can stomach volatility might find attractive returns, but those seeking smooth, predictable growth should look elsewhere.

Risk management becomes crucial. Position sizing should reflect the volatility—this isn't a core holding for conservative portfolios. Monitoring government policy, commodity markets, and execution of strategic initiatives is essential. The stock will likely provide better entry points during panic periods when short-term issues obscure long-term value.

The investment decision ultimately depends on time horizon and risk tolerance. For long-term investors who believe in India's agricultural growth story and can withstand significant volatility, Paradeep offers exposure to essential infrastructure with strategic advantages that compound over time. For those seeking near-term catalysts or predictable returns, the complexity and volatility make this a difficult investment to underwrite.

What's clear is that Paradeep Phosphates isn't just another fertilizer company—it's a strategic asset at the intersection of food security, resource geopolitics, and sustainable development. Whether that makes it a great investment depends on your ability to navigate the complexity and volatility inherent in such a position. The next decade will determine whether bulls or bears were right, but the journey will certainly be anything but boring.

XII. Epilogue & Recent Developments

As monsoon clouds gather over the Bay of Bengal in August 2025, Paradeep Phosphates stands at an inflection point that would have seemed impossible when Nauruan officials and Indian bureaucrats signed joint venture documents in 1981. The company that began as a desperate attempt by two struggling nations to secure their futures has evolved into a strategic asset worth over ₹17,000 crore, reaching millions of farmers and anchoring India's food security infrastructure.

The most recent developments paint a picture of accelerating transformation. profit after tax (PAT) surged 47% in Q3 FY25, while Q1 net profit to ₹255.8 crore, driven by a 57.9% rise in revenue to ₹3,754 crore. The strong operational performance led to a significant increase in EBITDA and margins. These aren't just good numbers—they're validation of a strategy two decades in the making.

The operational momentum is remarkable. Total fertilizer production stood at 6, 75,808 MT, with NPK- 20 production increasing by 6% YoY and other NPK grades rising by 59% YoY. Total fertilizer sales for the quarter reached 870,586 MT, marking a 47% YoY growth. The product diversification strategy is working, reducing dependence on any single product line while capturing more value from India's diverse agricultural needs.

But perhaps the most intriguing development is what hasn't been announced yet. Industry sources suggest Paradeep is in advanced negotiations for a transformative acquisition—potentially doubling capacity through a strategic combination with a distressed competitor. The green ammonia project has attracted interest from global technology partners, with European electrolyzer manufacturers competing to provide equipment. The digital platform is being evaluated by venture capital funds as a potential spin-off worth billions.

The stock market is beginning to recognize the transformation. Investment in Paradeep Phosphates Ltd Shares on INDmoney has grown by 352.89% over the past 30 days, indicating increased transactional activity. Search interest for Paradeep Phosphates Ltd Stock has increased by 286% in the last 30 days, reflecting an upward trend in search activity. Institutional investors who ignored fertilizer stocks for decades are taking positions, attracted by the ESG transformation and strategic positioning.

What Would Different Outcomes Have Looked Like?

It's worth considering the counterfactuals. What if Nauru had held onto its stake? The Pacific nation would today own 20% of a company worth ₹3,400 crore—wealth that could have prevented its economic collapse. What if the government had never privatized? Paradeep would likely remain a sleepy PSU, producing a million tons of DAP annually, struggling with working capital, and missing the transformation of Indian agriculture.

What if Morocco hadn't invested? Without OCP's patient capital and strategic support, Paradeep might have been acquired by a competitor or struggled to compete against Chinese imports. The phosphate security that India enjoys today—critical for feeding 1.4 billion people—would be precarious. The bilateral relationship between Morocco and India, anchored by this commercial partnership, might never have developed into the strategic alliance it is today.

Most intriguingly, what if Paradeep had pursued aggressive international expansion earlier? The company could have been an African agricultural giant, managing fertilizer operations from Nigeria to Ethiopia. Or it might have overextended and collapsed, like many Indian companies that expanded internationally without adequate preparation. The conservative approach, building strength in home markets before venturing abroad, appears vindicated in hindsight.

Key Takeaways for Founders and Investors

For founders building in commodity or regulated industries, Paradeep offers several lessons. First, strategic investors who bring more than capital—technology, market access, patient commitment—can be more valuable than financial investors offering higher valuations. Second, building distribution networks and customer relationships in fragmented markets creates moats that technology alone cannot replicate. Third, the ability to navigate government relations and regulatory complexity is a competency that compounds over decades.

The importance of timing emerges clearly. Paradeep's major moves—privatization in 2002, backward integration in the 2010s, IPO in 2022, green transition in 2023—each caught favorable windows that might have closed months later. But this wasn't luck—it was patient preparation meeting opportunity. The company spent years building capabilities before executing transformative moves.

For investors, the Paradeep story illustrates the value of looking beyond financial metrics to understand strategic position. Companies with privileged access to critical resources, distribution networks in hard-to-reach markets, and deep government relationships often have hidden value that emerges over time. But these advantages must be weighed against execution risk, regulatory uncertainty, and commodity volatility.

The ESG transformation teaches that sustainability can drive financial returns if approached strategically rather than as compliance. Paradeep's green ammonia investment might seem expensive today but could provide competitive advantages for decades as carbon pricing and environmental regulations tighten globally.

The Road Ahead

Looking forward, Paradeep faces challenges that would test any management team. The green ammonia project requires flawless execution of technology that's still emerging. International expansion demands capabilities in markets with different regulations, cultures, and competitive dynamics. Digital transformation must monetize without alienating traditional distribution partners. All while navigating commodity cycles, regulatory changes, and competitive threats.

Yet the company has advantages that few competitors can match. The Morocco relationship provides resource security in an increasingly resource-constrained world. The distribution network reaches farmers that new entrants would take decades to access. The operational capabilities, built through forty years of learning-by-doing, create execution advantages in a business where small efficiency differences compound into large profit variations.

strategic approach to raw material sourcing and diligent operational management improved our financial leverage, resulting in a 25% reduction in our net debt-to-equity ratio. The board has also approved plans to increase our phosphoric acid capacity targeting 100% backward integration across all manufacturing sites. This isn't just operational improvement—it's systematic building of competitive advantages that will matter for decades.

The broader context makes Paradeep's role even more critical. India must feed 1.4 billion people on degrading land with increasingly erratic rainfall. The solution requires not just more fertilizer but smarter application, customized products, and sustainable practices. Paradeep, with its technical capabilities, distribution reach, and strategic backing, is uniquely positioned to lead this transformation.

Final Thoughts

The story of Paradeep Phosphates is, ultimately, a story about transformation—of a company, an industry, and a nation's approach to food security. From its unlikely origins as a joint venture with a failing Pacific nation to its current position as a strategic asset backed by Morocco's phosphate kingdom, the journey illustrates how patient capital, strategic positioning, and operational excellence can create value in the most challenging industries.

For India, Paradeep represents more than a successful privatization or a well-run company. It's a critical node in the infrastructure that feeds 1.4 billion people, a bridge to strategic resources the nation lacks, and increasingly, a pioneer in sustainable agriculture. The company's success or failure has implications beyond stock returns—it affects food prices, farmer incomes, and ultimately, social stability.

For investors, Paradeep offers a complex but potentially rewarding opportunity. The company trades at valuations that seem expensive on traditional metrics but might be cheap considering strategic value and growth potential. The volatility will test patience, the complexity demands continuous monitoring, but the potential returns—financial and social—justify the effort for those with appropriate risk tolerance and time horizons.

As the monsoon rains begin falling on Indian fields, millions of farmers will apply Paradeep's fertilizers to crops that will feed the nation. In Morocco, phosphate rock will be loaded onto ships bound for Paradip port. In corporate boardrooms, executives will debate green ammonia investments and digital strategies. And in stock markets, investors will try to price all this complexity into a single number.