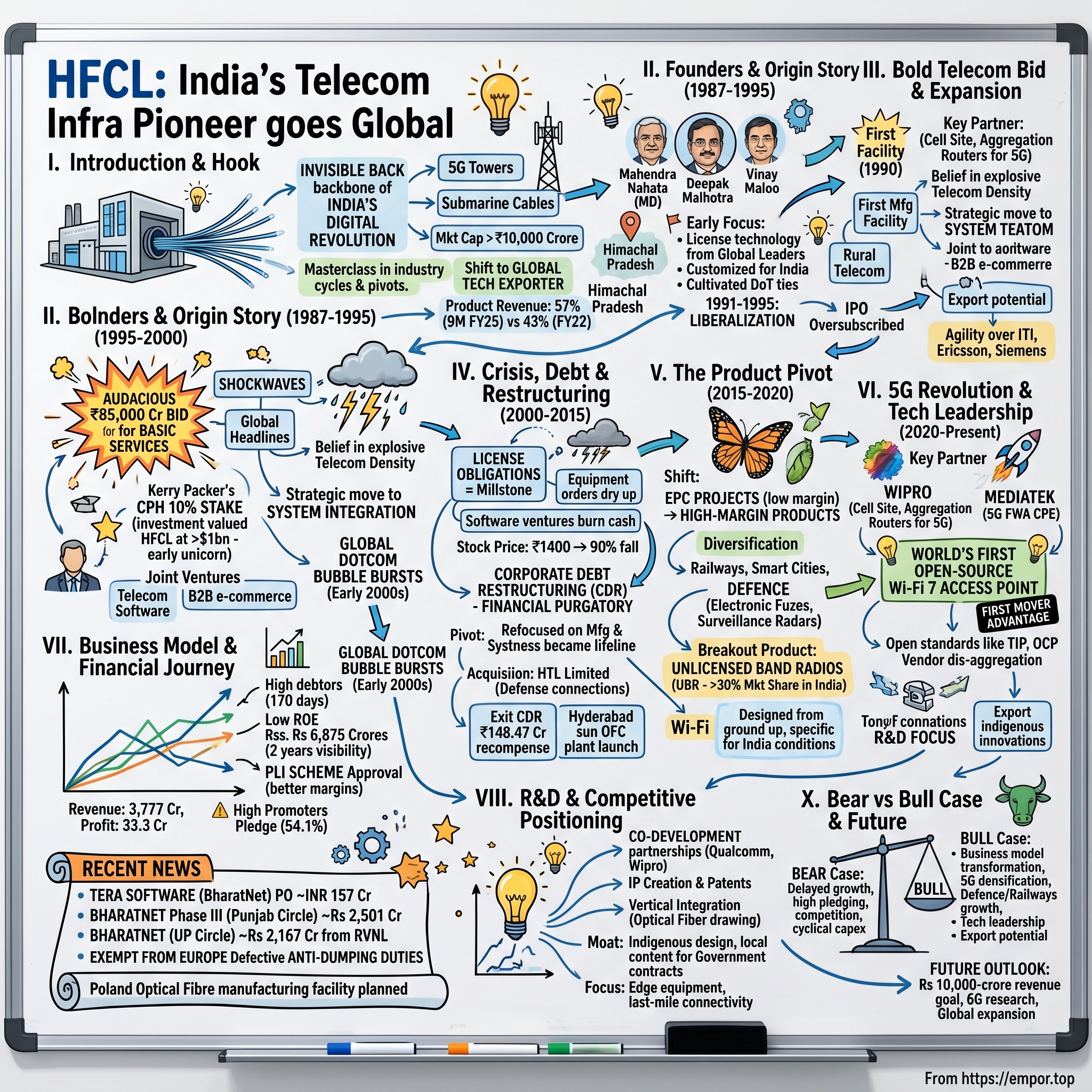

HFCL: India's Telecom Infrastructure Pioneer Goes Global

I. Introduction & Episode Hook

The year is 2024. In a nondescript industrial facility in Hyderabad, machines hum as they spin hair-thin strands of glass that will carry terabytes of data across continents. These optical fibers, manufactured by HFCL Limited, form the invisible backbone of India's digital revolution—from 5G towers in metropolitan cities to submarine cables connecting Chennai to Singapore. Yet few know the story of how a company founded in the mountain state of Himachal Pradesh, far from India's tech hubs, became the nation's optical fiber champion with a market capitalization exceeding ₹10,000 crore.

The paradox is striking: HFCL began in 1987 when India's telecom network consisted of creaky landlines and months-long waiting lists for phone connections. Today, it manufactures cutting-edge 5G equipment, defense electronics, and supplies optical fiber to global telecom giants. The journey between these two points reads like a thriller—featuring an audacious ₹85,000 crore bid that shook India's telecom industry, a near-death experience during the dotcom bust, intervention by Australian media mogul Kerry Packer, and a phoenix-like resurrection as a technology powerhouse. What makes HFCL's story particularly compelling for investors is how it embodies India's transformation from a telecom importer to a global technology exporter. The company's revenue composition has shifted dramatically, with Telecom Products now representing 57% of revenues in 9M FY25 versus 43% in FY22, driven by offerings including UBR radios, Wi-Fi 5/6 access points, AI-driven network management systems, and optical fiber cables where it holds the largest market share in OFC supplies. This isn't just another infrastructure play—it's a masterclass in how to survive industry cycles, pivot business models, and emerge stronger from near-catastrophic setbacks.

II. The Founders & Origin Story (1987-1995)

Picture India in 1987: Rajiv Gandhi is Prime Minister, mobile phones are science fiction, and getting a landline connection requires bribing officials and waiting up to five years. In this analog world, three entrepreneurs—Mahendra Nahata, Deepak Malhotra, and Vinay Maloo—saw a digital future that few could imagine. They incorporated Himachal Futuristic Communications Limited on May 11, 1987, in what seemed like an unlikely birthplace for a telecom revolution: the hill state of Himachal Pradesh, better known for apples than electronics.

The choice of Himachal Pradesh wasn't romantic idealism—it was strategic financial engineering. The state offered tax incentives for industries, lower land costs, and most importantly, a way to differentiate from the established players concentrated in Delhi, Mumbai, and Bangalore. Nahata, who would emerge as the driving force and is still Managing Director today, brought an engineer's precision to the business. An alumnus of IIT Delhi, he understood that India's telecom infrastructure desperately needed modernization, and whoever could bridge the technology gap would capture enormous value.

The early years were about survival through partnerships. HFCL didn't try to reinvent the wheel—they licensed technology from global leaders and adapted it for Indian conditions. Their first major breakthrough came with transmission equipment for the Department of Telecommunications (DoT). In an era when Indian manufacturing meant Ambassador cars and heavy machinery, HFCL was assembling sophisticated digital switching equipment. They weren't just importing and reselling; they were learning, absorbing technology, and building local capabilities that would prove crucial decades later.

The founders displayed remarkable foresight in two areas. First, they recognized that India's geography—vast distances, difficult terrain, poor road infrastructure—made optical fiber essential for telecommunications, not optional. While others focused on copper cables and microwave towers, HFCL began investing in fiber optic technology knowledge. Second, they understood that government relationships would make or break telecom companies in India. The company cultivated deep ties with the DoT, positioning itself as the reliable Indian alternative to foreign suppliers.

By 1990, HFCL had established its first manufacturing facility and was supplying equipment to the government's ambitious rural telecommunication projects. The quality was good enough that they began exploring international markets, a audacious move for an Indian tech company at the time. Revenue grew from virtually nothing to several crores, validating the founders' vision but also attracting competition. Companies like ITI Limited had government backing, while multinationals like Ericsson and Siemens had technology advantages. HFCL's edge was agility—they could customize solutions for Indian conditions faster than foreign companies and deliver better technology than government enterprises.

The period from 1991 to 1995 transformed everything. India's economic liberalization under Finance Minister Manmohan Singh opened telecom to private players. Suddenly, the addressable market wasn't just government departments but potentially hundreds of millions of Indians. HFCL went public in this period, raising capital from investors who bought into the India telecom story. The IPO was oversubscribed, reflecting market confidence in both the sector and the company's execution capabilities.

What distinguished HFCL in these formative years was their willingness to think beyond manufacturing boxes. While competitors focused on hardware, Nahata pushed the company toward system integration—not just selling equipment but designing and implementing entire networks. This approach required deeper technical expertise but offered higher margins and stronger customer relationships. By 1995, HFCL had transformed from a small manufacturer in Himachal Pradesh to a serious player in India's telecom equipment market, setting the stage for the audacious move that would define its next chapter and nearly destroy it.

III. The Bold Telecom Bid & Early Expansion (1995-2000)

The year 1995 marked a watershed moment in Indian telecom history, and HFCL placed itself at the epicenter of the revolution. When the government invited bids for basic telephony services licenses—essentially the right to provide landline services in competition with the monopoly MTNL and DoT—most industry observers expected conservative bids from established players. What happened instead sent shockwaves through corporate India and made global headlines.

HFCL, in consortium with other partners, submitted a bid of ₹85,000 crore (approximately $25 billion at 1995 exchange rates) for basic services licenses across multiple circles. To put this in perspective, this was larger than many state government budgets and exceeded the market capitalization of most Indian companies at the time. The number was so astronomical that competitors accused HFCL of market manipulation, regulators questioned the bid's seriousness, and financial analysts scrambled to understand the logic.

Nahata's strategy was both brilliant and dangerous. He believed that India's telecom density—then less than 2%—would explode to global averages within a decade. If you assumed 200 million subscribers paying ₹500 monthly, the revenue potential was staggering. The bid wasn't meant to be paid upfront but over the license period, making it theoretically manageable with projected cash flows. More importantly, the aggressive bid would deter competitors and potentially give HFCL dominant market position in the world's second-most populous nation.

The immediate impact was electric. HFCL's stock price soared as investors bought into the vision of a company controlling significant telecom infrastructure. International partners came calling—everyone from equipment vendors offering financing to foreign telecom operators seeking joint ventures. The company leveraged this momentum to diversify rapidly. They entered IT services, seeing convergence between telecom and computing. They launched software development centers, targeting the Y2K opportunity and telecom billing systems. For a brief moment, HFCL looked like it might become India's first integrated telecom-to-technology conglomerate.

The year 2000 brought an unexpected validator: Kerry Packer, the Australian media mogul who had revolutionized cricket with World Series Cricket, acquired a 10% stake in HFCL through his company Consolidated Press Holdings (CPH). Packer wasn't known for technology investments—his empire was built on television and gambling—but he saw parallels between media and telecom convergence. The investment valued HFCL at over $1 billion, making it one of India's first unicorns before the term existed.

CPH and HFCL established two joint ventures that reflected the zeitgeist of the dotcom era. The first focused on software products and services, attempting to build India's answer to Oracle in telecom software. The second, even more ambitious, aimed to create a B2B e-commerce platform for telecom equipment—imagine Amazon Business but exclusively for network gear. Both ventures had strong business logic: software offered 70% gross margins versus 30% for equipment, while B2B e-commerce could disintermediate distributors and capture value in a $10 billion annual market. But the expansion came at a terrible cost. The telecom license obligations required massive capital expenditure that HFCL couldn't fund from operations. The software ventures burned cash without achieving scale. Most critically, the global telecom bubble was already showing cracks. Equipment vendors worldwide were sitting on massive inventory as telecom operators, drowning in debt from spectrum auctions, slashed capital spending. HFCL's stock price, which had touched ₹1,400 in early 2000, began its descent. By year-end, it had fallen 90%, wiping out thousands of crores in market value and setting the stage for a crisis that would test the very survival of the company.

IV. Crisis, Debt & Restructuring Era (2000-2015)

The telecom bubble didn't burst—it imploded. By 2001, HFCL found itself in a perfect storm: the basic services license had become a millstone around its neck with mounting annual fees, equipment orders dried up as operators canceled expansion plans, and the software ventures hemorrhaged cash without achieving product-market fit. The company that had bid ₹85,000 crore with such confidence now struggled to service even routine working capital requirements.

The numbers were brutal. HFCL's debts were restructured under the Corporate Debt Restructuring (CDR) mechanism, and the company submitted a proposal to exit the program. With improved financial performance, HFCL was able to repay ₹148.47 crore as part of the recompense deal, enabling its exit from the CDR mechanism. But this exit wouldn't come until 2017—the company would spend over a decade under CDR, a financial purgatory that constrained every strategic decision.

Corporate Debt Restructuring ("CDR") mechanism is a voluntary non statutory mechanism under which financial institutions and banks come together to restructure the debt of companies facing financial difficulties due to internal or external factors, in order to provide timely support to such companies. The intention behind the mechanism is to revive such companies and also safeguard the interests of the lending institutions and other stakeholders. For HFCL, CDR meant survival but at the cost of growth—every investment needed lender approval, expansion was virtually impossible, and the company operated under constant scrutiny.

Yet even in crisis, HFCL displayed remarkable resilience through strategic pivots. Recognizing that the telecom services dream was over, management refocused on what they knew best: manufacturing and system integration. The optical fiber cable business, almost an afterthought during the boom years, became the lifeline. India's telecom networks still needed fiber backbone, and HFCL had the manufacturing capability. Orders from BSNL, though delayed and often disputed over payments, kept the factories running.

The company also made a crucial strategic acquisition during this period, taking a stake in HTL Limited (Hindustan Teleprinters Limited), a Chennai-based PSU with manufacturing capabilities. While the market questioned why a debt-laden company was acquiring assets, Nahata saw opportunity—HTL had land, factory infrastructure, and most importantly, relationships with defense establishments. This would prove prescient when defense electronics emerged as a growth driver years later.

The period from 2005 to 2010 was particularly challenging. India's telecom sector exploded with the entry of new players like Reliance Communications and Aircel, but HFCL couldn't capitalize—the CDR restrictions meant it couldn't bid aggressively for contracts or invest in new product development. Competitors like Sterlite Technologies, unencumbered by legacy debt, captured market share in optical fiber. Chinese vendors like Huawei and ZTE entered India with aggressive pricing and vendor financing that HFCL couldn't match.

Innovation, however, continued despite financial constraints. The R&D team, working on shoestring budgets, began developing products for the future—software-defined radios, early wireless broadband equipment, and specialized defense communication systems. These weren't generating significant revenue yet, but they kept HFCL technologically relevant. The company also started exploring international markets more seriously, particularly in Africa and Southeast Asia where Indian vendors had cost advantages over European suppliers.

With the improved financial performance, the company submitted its proposal for exit from CDR mechanism to Monitoring Institution (MI) i.e. IDBI Bank Limited. The MI has recommended recompense amount of Rs 148.47 Crore on term and working capital loans. The same has been approved by CDR - Empowered Group vide their order dated 22 March 2016 subject to the approval from company's lenders. Subsequent to CDR-EG's approval, the recompense amount has been approved by some of the lenders and approval from remaining lenders is expected soon. Accordingly, the Board of Directors of HFCL at their meeting held on 10 May 2016 approved the recompense amount of Rs 148.47 Crore to exit from CDR mechanism.

By 2015, the worst was behind them. India's telecom sector was consolidating, creating opportunities for vendors. The government's Digital India initiative promised massive infrastructure spending. Most importantly, HFCL had survived when many peers hadn't—companies like Shyam Telecom and Kavveri Telecom had either shut down or been acquired for pennies on the dollar. HFCL's persistence through the crisis, while painful, had preserved its manufacturing capabilities, customer relationships, and technological knowledge base. In 2018, a crucial milestone validated this persistence: HFCL launched its optical fibre manufacturing unit in Hyderabad, marking its transformation from an OFC manufacturer to a fully integrated optical fiber producer—a capability that would prove invaluable in the 5G era that was about to dawn.

V. The Product Pivot: From Projects to Products (2015-2020)

The exit from CDR in 2017 marked more than financial freedom—it represented a fundamental strategic transformation. For the first time in over a decade, HFCL could make decisions without seeking permission from a consortium of bankers. Nahata and his team had spent years planning for this moment, and they executed with precision.

The strategic shift was clear: move from low-margin, working-capital-intensive EPC (Engineering, Procurement, and Construction) projects to high-margin product manufacturing. The segment revenue grew 24% YoY in 9M FY25, driven by a strategic shift from project-based to product-based revenue, to facilitate lower working capital needs, faster realizations, and improved margins. This wasn't just about changing the revenue mix—it required reimagining HFCL's entire business model, from R&D to sales to working capital management.

In 2017, HFCL expanded into new business verticals, including Railways, Smart Cities, and Defence. The company secured contracts worth ₹113 crore for railway telecom systems and signed a ₹95 crore contract with Larsen & Toubro Ltd for the Western Dedicated Freight Corridor. The railway vertical was particularly strategic—Indian Railways was modernizing its communication infrastructure, moving from analog to digital systems, and needed vendors who understood both telecom and the unique requirements of railway signaling.

The defense vertical represented an even bigger opportunity. It is a prominent player in India's defence sector, offering products like electronic fuzes, thermal weapon sights, and surveillance radars. India's push for defense indigenization under "Make in India" created a massive addressable market for local manufacturers. HFCL leveraged its subsidiary HTL's existing relationships and clearances to win contracts for specialized communication equipment, electronic warfare systems, and surveillance solutions. The margins in defense were attractive—often 30-40% gross margins versus 15-20% in commercial telecom.

But the real transformation was in telecom products. The company offers UBR radios, Wi-Fi 5/6 access points, AI-driven network management, home mesh routers, etc. It is a top manufacturer of Wi-Fi access points and UBR radios in India. Unlicensed Band Radios (UBRs) became HFCL's breakout product category. These devices, which enable point-to-point wireless connectivity without expensive spectrum licenses, found applications in enterprise connectivity, smart city projects, and telecom backhaul. HFCL captured over 30% market share in India, competing successfully against established players like Cambium Networks and Ubiquiti.

The development of Wi-Fi products showcased HFCL's evolved R&D capabilities. Rather than simply assembling imported components, the company designed products from the ground up, creating intellectual property and differentiation. Their Wi-Fi access points incorporated features specifically for Indian conditions—enhanced heat dissipation for tropical climates, power surge protection for unreliable electricity grids, and software optimized for high-density deployments common in Indian cities.

Smart Cities emerged as another growth vertical. The government's Smart Cities Mission, covering 100 cities with proposed investments of ₹2 lakh crore, required massive deployment of surveillance cameras, sensors, and networking equipment. HFCL positioned itself as an end-to-end solution provider, offering not just equipment but system integration and managed services. Projects in Gurugram, Nagpur, and other cities demonstrated HFCL's ability to handle complex, multi-stakeholder deployments.

The optical fiber business also evolved significantly. Rather than competing solely on price in commodity fiber, HFCL focused on specialized products—ribbon cables for data centers, micro cables for congested urban ducts, and armored cables for harsh environments. It manufactures optical fibers, micro cables, ribbon cables, and IBR cables, holding the largest market share in OFC supplies. The Hyderabad optical fiber plant, commissioned in 2018, incorporated the latest technology for producing bend-insensitive fiber, critical for 5G and FTTH deployments.

R&D investment increased substantially during this period. In this age of technological advancements and digitalisation, it is imperative for organisations to ramp up their R&D investments to ensure that they are able to stay ahead of their peers. Aware of this reality, we have substantially increased our R&D focus over the years, to ensure that we are able to position ourselves as a technology-driven company. The company established development centers in Gurgaon and Bengaluru, hiring engineers from India's top institutions. Unlike the earlier era when R&D meant adapting foreign technology, HFCL now developed products from scratch, filing patents and creating genuine IP.

By 2020, the transformation was evident in the numbers. Product revenue as a percentage of total revenue had increased from less than 30% to over 50%. Working capital cycles improved as product sales meant faster cash conversion than project execution. Most importantly, HFCL had built capabilities in emerging technologies—5G equipment, Wi-Fi 6, software-defined networking—that positioned it perfectly for the next wave of telecom investment that was about to sweep across India and the world.

VI. The 5G Revolution & Technology Leadership (2020-Present)

The COVID-19 pandemic, paradoxically, accelerated HFCL's transformation into a technology leader. As the world shifted online overnight, demand for connectivity equipment exploded. HFCL's products—Wi-Fi access points for work-from-home setups, UBRs for rapid network expansion, optical fiber for data center interconnects—were suddenly mission-critical. But the real opportunity lay in 5G, where India was preparing for one of the world's largest network rollouts.

Wipro Limited and HFCL Limited announced that they have entered into a partnership to engineer a variety of 5G transport products that include Cell Site Router, DU (Distributed Unit) Aggregation Router, and CU (Centralized Unit) Aggregation Router. This partnership with Wipro wasn't just another vendor relationship—it represented HFCL's arrival as a serious player in 5G infrastructure. Wipro is a key partner for HFCL because of its world-class engineering and in-depth experience on hardware design, embedded software and its in-house certification and compliance labs (Tarang). HFCL's comprehensive portfolio of 5G transport products (which are under development), that include Cell Site Router, DU Aggregation Router and CU Aggregation Router, will enable CSPs to modernize their backhaul networks and make them ready for 5G services.

The 5G product portfolio expanded rapidly. HFCL Limited, a leading technology enterprise and integrated next-gen communications product and solution provider, has entered into a partnership with MediaTek to integrate the class-leading MediaTek T750 chipset onboard its HFCL 5G FWA Indoor CPE. MediaTek, a renowned innovator in systems-on-chip (SoC) for mobile, home entertainment, connectivity, and IoT products, is known globally for cutting-edge technological advancements. HFCL's 5G FWA Indoor CPE stands out with features like ultra-compact form factor and minimal power consumption, courtesy of its onboard MediaTek chipset. The 5G Fixed Wireless Access (FWA) products addressed a critical need—providing fiber-like speeds without the cost and complexity of laying physical cables, perfect for India's last-mile connectivity challenges.

But the real technological leap came with Wi-Fi 7. HFCL Limited, the leading high-tech enterprise and integrated next-gen communication product and solution provider in collaboration with Qualcomm Technologies, Inc. launches world's first Open source Wi-Fi 7 Access Points under its IO product line at India Mobile Congress, Pragati Maidan, New Delhi on 01 October 2022. HFCL becomes the first OEM to launch Open source Wi-Fi 7 Access Points, based on the IEEE 802.11be - a revolutionary Wi-Fi technology that is designed to deliver Extremely High Throughput (EHT), higher spectral efficiency, better interference mitigation, and Real Time Applications (RTA) support. Being first globally with open-source Wi-Fi 7 wasn't just a technical achievement—it positioned HFCL as an innovation leader, not a fast follower.

With the launch of open-source Wi-Fi 7 Access Point, HFCL has become the first original equipment manufacturer in India to design and launch this Wi-Fi technology to complement the indoor 5G coverage. The strategic importance of this achievement cannot be overstated. While 5G provides outdoor coverage and mobility, Wi-Fi handles indoor traffic where 80% of data consumption occurs. By offering both 5G and Wi-Fi 7 solutions, HFCL could address the entire connectivity stack.

The technology partnerships reveal HFCL's evolved strategy. Working with Qualcomm for Wi-Fi 7, MediaTek for 5G CPE, and specialized partners like CommAgility for small cells, HFCL assembled best-in-class components while adding its own software and system integration expertise. This approach allowed rapid product development without the massive R&D investment required to develop chipsets from scratch.

The company's in-house R&D Centres located at Gurgaon and Bengaluru along with invested R&D houses and other R&D collaborators at different locations in India and abroad, innovate a futuristic range of technology products and solutions. HFCL has developed capabilities to provide premium quality Optical Fiber and Optical Fiber Cables, state-of-the-art telecom products including 5G Radio Access Network (RAN) products, 5G Transport Products, Wi-Fi Systems (Wi-Fi 6, Wi-Fi 7), Unlicensed Band Radios, Switches, Routers and Software Defined Radios.

The focus on open standards and open-source became a key differentiator. HFCL's 5G Transport products are based on merchant silicon, network dis-aggregated architecture, and on open standards like TIP (Telecom Infra Project), and OCP (Open Compute Project). While competitors offered proprietary solutions that locked in customers, HFCL embraced openness, allowing operators to mix and match vendors and avoid vendor lock-in—a crucial consideration for cost-conscious Indian operators.

HFCL has partnered with Qualcomm Technologies for design and development of their 5G outdoor small cell products that will enable faster rollout of 5G network. Learn how HFCL & Qualcomm together develop a portfolio of 5G outdoor small cell products for both sub-6Ghz and mmWave to address India and the global market. Small cells represent another strategic bet. As 5G frequencies don't propagate as far as 4G, networks need many more cell sites. Traditional macro towers are expensive and face right-of-way challenges. Small cells—compact, low-power base stations—can be deployed on street furniture, building facades, and indoor locations, enabling dense 5G coverage.

The results of this technology leadership are already visible. The increasing demand for our 5G Fixed Wireless Access (FWA) Customer Premises Equipment, Point-to-Point Unlicensed Band Radio (UBR), routers, switches, and other telecom and networking products eligible for PLI benefits is solidifying HFCL's position as a leading supplier in key markets. We firmly believe that these products will make a substantial contribution to our revenue and profitability. HFCL has successfully positioned itself not just as an equipment vendor but as a technology partner capable of designing, developing, and deploying next-generation network solutions.

The global recognition is equally important. Speaking on this development, Jitendra Chaudhary, Executive President, HFCL said, "We are immensely proud to be the first Indian enterprise that enables the deployment of WBA's OpenRoaming across our Wi-Fi portfolio. We are currently working with telecom operators and large ISPs in India and in few other countries to deploy OpenRoaming. We aim to make the most of this first mover advantage and make the internet more accessible for all globally. From a company that once licensed foreign technology, HFCL now exports its indigenous innovations to global markets—a complete reversal of India's traditional technology trade flow.

VII. Business Model Evolution & Financial Journey

The transformation of HFCL's business model from a project-heavy EPC contractor to a product-focused technology company represents one of the most successful pivots in Indian corporate history. The numbers tell a compelling story: Telecom Products (57% in 9M FY25 vs 43% in FY22), with the segment growing at 24% year-over-year, fundamentally altering the company's financial dynamics.

This shift wasn't merely about changing the revenue mix—it required reimagining every aspect of operations. Project businesses are inherently working capital intensive. You win a contract, deploy capital for equipment and installation, and then wait months or sometimes years for milestone payments. Product businesses operate on different dynamics: faster inventory turns, immediate payment upon delivery, and crucially, the ability to scale without proportional working capital increases.

The three-segment strategy that emerged—Telecom Products, Turnkey Contracts, and Services—represents a sophisticated balance. Telecom Products provide growth and margins. Turnkey Contracts, while lower margin, offer steady cash flow and deep customer relationships that often lead to product sales. Services, the smallest but fastest-growing segment, includes managed services and annual maintenance contracts that provide recurring revenue and customer stickiness.

Working capital management has been the Achilles' heel for many Indian infrastructure companies, and HFCL was no exception. Company has high debtors of 170 days. This remains a challenge, but the shift to products is gradually improving the situation. Product sales typically have 30-60 day payment terms versus 180+ days for projects. The company has also become more selective about projects, focusing on government contracts with assured payment mechanisms rather than private operators with stretched balance sheets.

The export story deserves special attention. International revenue now constitutes approximately 20% of total revenue, up from virtually nothing a decade ago. This isn't just about finding new markets—it's about validation. When European operators buy HFCL's optical fiber or African telcos deploy their Wi-Fi equipment, it demonstrates that Indian manufacturing can compete globally on quality, not just price. The company has established relationships across geographies, from Southeast Asia to Middle East to Africa, reducing dependence on the cyclical Indian market.

Revenue: 3,777 Cr · Profit: 33.3 Cr The current financial position reflects both achievements and challenges. Revenue has grown, but profitability remains under pressure from global optical fiber oversupply and competitive intensity in the Indian market. Company has a low return on equity of 7.66% over last 3 years. This low ROE reflects the capital intensity of manufacturing and the competitive market dynamics, but management expects improvement as the product mix shifts further and 5G deployments accelerate.

The order book provides visibility and confidence. We closed the year with an outstanding order book of Rs. 6,875 crores. This substantial backlog, equivalent to nearly two years of current revenue, provides cushion against market volatility. The order book composition is also improving, with a higher proportion of product orders versus projects, suggesting better margin realization going forward.

Capital allocation has become more disciplined post-CDR. Instead of pursuing growth at any cost, management focuses on return on capital employed (ROCE) improvement. Investments are directed toward high-margin products and technologies where HFCL has competitive advantages. The company has also been selective about acquisitions, preferring partnerships and joint ventures that don't strain the balance sheet.

The Production Linked Incentive (PLI) scheme has emerged as a game-changer. HFCL has received approval from the Small Industries Development Bank of India (SIDBI), the Project Management Agency (PMA) and Competent Authority designated by the Centre on its application for participation in the PLI Scheme. The scheme provides financial incentives for domestic manufacturing of telecom equipment, improving economics for local production versus imports. For HFCL, this means better margins on eligible products and a competitive advantage against importers.

However, challenges remain substantial. Promoters have pledged or encumbered 54.1% of their holding. This high promoter pledge raises governance concerns and limits financial flexibility. The company also faces the perennial challenge of Indian infrastructure companies—delayed payments from government contracts, though the situation has improved with better payment discipline from agencies like BSNL and Railways.

The company has delivered a poor sales growth of 1.15% over past five years. This seemingly poor historical growth rate is misleading—it reflects the deliberate shift away from low-margin projects toward higher-margin products. Revenue quality has improved even if headline growth has been modest. The focus now is on profitable growth rather than growth at any cost, a lesson learned painfully during the aggressive expansion of the late 1990s.

Looking at cash flow generation, the picture is mixed. HFCL's cash flow from operating activities (CFO) during FY24 stood at Rs -449 million on a YoY basis. Cash flow from investing activities (CFI) during FY24 stood at Rs -4 billion, an improvement of 917.7% on a YoY basis. Cash flow from financial activities (CFF) during FY24 stood at Rs 5 billion, an improvement of 414% on a YoY basis. Overall, net cash flows for the company during FY24 stood at Rs -396 million from the Rs 462 million net cash flows seen during FY23. The negative operating cash flow reflects working capital investments for growth, while investing activities show commitment to capacity expansion and R&D.

The financial evolution of HFCL mirrors India's broader economic transformation—from a protected, license-raj economy to a competitive, globalized marketplace. The company that once depended on government orders and borrowed technology now competes with global giants, exports indigenous products, and generates intellectual property. The financial metrics may not yet fully reflect this transformation, but the trajectory is clear: HFCL is becoming a technology company that happens to be in telecom, not a telecom company trying to do technology.

VIII. R&D, Innovation & Competitive Positioning

The transformation of HFCL from a technology licensee to an innovation leader represents a masterclass in capability building under resource constraints. We opened a new R&D Centre at Bengaluru. We empowered ourselves with various collaborative arrangements to co-innovate future technologies. These R&D centers in Gurgaon and Bengaluru aren't just cost centers—they're the engines driving HFCL's competitive differentiation in an industry dominated by giants like Huawei, Nokia, and Ericsson.

The product development strategy reveals sophisticated thinking about where to compete. Rather than attempting to build complete 5G base stations—a market dominated by companies with 100x HFCL's R&D budget—the company focused on specific niches where it could achieve leadership. Unlicensed Band Radios (UBRs) exemplify this approach. Over half a million successful deployment serving global customers is a testimony to the rising demand for the Unlicensed Band Radios to meet the connectivity requirements. By focusing on this specific category, HFCL achieved scale, expertise, and market recognition that would have been impossible trying to compete across the entire equipment spectrum.

The innovation in Wi-Fi technology showcases indigenous capability development. Speaking about the launch of this revolutionary product line, Mr. Mahendra Nahata, MD, HFCL said, "We are immensely proud to be the first Indian company to launch Wi-Fi 7 product line in market and the first in the world to offer an Open source Wi-Fi 7 portfolio. Our Wi-Fi 7 portfolio is based on the latest Wi-Fi 7 Qualcomm® Networking Pro Series Platforms and offers better features than any commercial products available in market today. We are really thankful to the Qualcomm Technologies teams for working closely with us and supporting us to make this possible. This wasn't about being first for the sake of it—early mover advantage in Wi-Fi 7 means setting standards, influencing specifications, and building customer relationships before competitors enter.

The collaborative innovation model deserves examination. Unlike the old model of licensing finished products, HFCL now engages in co-development partnerships. The Qualcomm partnership for Wi-Fi products involves HFCL engineers working alongside Qualcomm's teams, gaining deep understanding of chip-level functionality. The Wipro partnership for 5G transport products combines HFCL's telecom domain expertise with Wipro's software engineering capabilities. We will leverage our strong experience in network equipment engineering, expertise in 5G/LTE and VLSI (Very-Large-Scale Integration) system design, engineering design services and embedded software.

IP creation has become a strategic priority. While specific patent numbers aren't disclosed, the company has filed multiple patents in areas like antenna design, thermal management for outdoor equipment, and software algorithms for network optimization. This IP serves multiple purposes: differentiation from competitors, protection against litigation, and increasingly, licensing revenue from other manufacturers.

The focus on "Make in India" aligned perfectly with government policy and created competitive advantages. When the government mandates local content for government purchases, HFCL's indigenous design and manufacturing capabilities become a moat. Chinese vendors, despite cost advantages, face restrictions in government contracts. Global vendors often struggle to meet local content requirements without significant investment. HFCL, with established local manufacturing and R&D, is perfectly positioned.

Defense R&D represents a different innovation paradigm. HFCL also entered into a strategic partnership with General Atomics Aeronautical Systems Incorporated (GA-ASI), US, to develop critical sub-systems for one of the world's most sophisticated unmanned aerial vehicles (UAVs).This partnership underscores our capabilities in the defense sector and opens more export opportunities for us. We are also in advanced stage of discussions for export of our indigenously designed and developed Electronics Fuzes in the global market. Defense products require different capabilities—ruggedization for extreme environments, encryption for security, and most importantly, reliability where failure isn't an option. The partnership with GA-ASI for UAV subsystems demonstrates HFCL's ability to meet global defense standards.

The competitive positioning against global giants follows classic disruption theory. HFCL doesn't compete with Nokia or Ericsson in high-end core network equipment. Instead, it focuses on edge equipment, last-mile connectivity, and specialized solutions where local knowledge and customization matter more than scale. Against Chinese vendors, HFCL leverages trust and security concerns, positioning itself as the secure alternative for critical infrastructure.

In the Indian market, HFCL's competitive advantages are multifaceted. Deep relationships with government agencies built over decades provide insider knowledge of requirements and procurement processes. Local manufacturing enables rapid customization and support—when BSNL needs equipment modified for Indian conditions, HFCL can respond in weeks while foreign vendors take months. The ability to provide end-to-end solutions, from fiber to wireless to services, creates stickiness that pure product vendors can't match.

The technology roadmap reveals ambition tempered with realism. There is a suite of products under development, which include Software Defined Radios, Routers, PON, 5G Transport and Radio products, Wi-Fi 7 access points, Home mesh router, Point-to-multipoint Radios and Ground Surveillance Radars among others. Each product category represents a calculated bet on market growth, competitive dynamics, and HFCL's ability to differentiate.

Software is becoming increasingly important in HFCL's innovation strategy. Modern telecom equipment is essentially software running on commodity hardware. HFCL's investment in software capabilities—network management systems, AI-driven optimization, and automation tools—transforms commodity hardware into differentiated solutions. This software layer also enables recurring revenue through licenses and upgrades, improving the business model.

The innovation culture within HFCL has evolved dramatically. From an engineering culture focused on meeting specifications, the company now encourages experimentation and accepts failure as part of innovation. Engineers are incentivized not just for successful products but for patents filed, papers published, and standards contributions. Regular hackathons and innovation challenges create energy and identify new ideas. Partnerships with IITs and other premier institutions bring fresh thinking and access to cutting-edge research.

IX. Playbook: Lessons in Resilience & Transformation

HFCL's journey from near-bankruptcy to technology leadership offers a masterclass in corporate resilience that transcends industry boundaries. The playbook that emerges isn't about avoiding crises—it's about surviving them and emerging stronger.

Surviving Technology Transitions: HFCL has navigated every generation of telecom technology from analog to 5G. Each transition killed companies—equipment vendors who couldn't adapt from circuit-switched to packet-switched networks, cable manufacturers who missed the fiber optic revolution, 2G leaders who failed in 3G. HFCL survived by maintaining technology agnosticism. Instead of betting everything on one technology, they maintained capabilities across the stack. When 2G equipment demand collapsed, fiber optic cables provided revenue. When fiber faced oversupply, wireless products grew. This portfolio approach to technology provided resilience that single-product companies lacked.

Building in India for the World: The reverse innovation model HFCL pioneered challenges conventional wisdom about emerging market companies. Instead of adapting developed market products for India (the traditional approach), HFCL designs for Indian conditions and then exports globally. Products designed to work in India's challenging environment—extreme heat, unreliable power, limited maintenance—excel in other emerging markets. A Wi-Fi access point that survives Mumbai's monsoons and Delhi's summer performs brilliantly in Southeast Asia or Africa. This approach creates genuine differentiation versus products designed for benign developed market conditions.

Managing Cyclical Capex: Telecom capital expenditure is notoriously cyclical. Operators spend billions during network upgrades, then slash spending to digest capacity. Many equipment vendors fail during these down cycles. HFCL developed multiple strategies to manage cyclicality. Diversification across customer segments—telecom, railways, defense—ensures some segments are always investing. Geographic diversification means when Indian operators pause spending, international markets may be investing. The shift to products from projects reduces the amplitude of cycles—product demand is steadier than project awards. Most importantly, the company learned to manage costs variably, scaling up during booms and retrenching during busts without losing core capabilities.

Vertical Integration in Optical Fiber: The decision to backward integrate from cable manufacturing to fiber drawing seemed risky when optical fiber faced global oversupply. But vertical integration provided strategic benefits beyond cost. It enabled product differentiation—HFCL could create specialized fibers for specific applications rather than depending on commodity fiber. It provided supply security during shortages. It captured more value chain margin during upturns. Most importantly, it created technical knowledge that improved cable design and customer solutions. The Hyderabad fiber plant isn't just a manufacturing facility—it's a capability that differentiates HFCL from cable-only competitors.

Balancing Products vs Projects: The tension between products and projects is existential for companies like HFCL. Projects provide large revenue chunks and deep customer relationships but consume working capital and deliver thin margins. Products offer better margins and capital efficiency but require continuous innovation and face fierce competition. HFCL's solution is strategic balance. They maintain project capabilities for strategic customers and large opportunities but are increasingly selective, focusing on projects that complement product sales or provide technology learning. The gradual shift from 70% projects to 60% products didn't happen overnight—it required patience, discipline, and willingness to sacrifice revenue for quality.

Government Relationships and Policy Navigation: In infrastructure sectors, government isn't just a customer—it's a stakeholder, regulator, and often competitor. HFCL mastered the art of government relations without becoming dependent. They participate in policy formation through industry associations, providing technical input that shapes standards and specifications. They maintain relationships across political parties and bureaucratic levels, ensuring continuity despite political changes. Most importantly, they've learned to read policy signals—understanding when "Make in India" or "Digital India" represents real opportunity versus rhetoric. The recent BharatNet order wins are a testament to our expertise in strengthening India's digital infrastructure, reinforcing our position as a trusted technology partner in the Country's broadband revolution. Additionally, the establishment of our new defense manufacturing unit in Hosur marks a significant milestone in our journey towards self-reliance in critical defense technologies. This step not only aligns with the 'Make in India' and 'Atmanirbhar Bharat' initiatives but also enhances our capability to contribute to national security.

Crisis as Catalyst: The CDR years could have destroyed HFCL. Instead, crisis became catalyst for transformation. Financial constraints forced innovation—when you can't buy technology, you develop it. Limited resources demanded focus—HFCL couldn't pursue every opportunity, so they chose carefully. Creditor oversight instilled discipline—every investment needed justification, creating rigor that persists today. Most importantly, surviving existential crisis created organizational confidence. Having survived near-death, the company developed resilience and risk appetite that enables bold moves like being first with Wi-Fi 7.

Talent and Culture: Transforming from equipment assembler to technology innovator required fundamental culture change. HFCL attracted talent by offering something multinationals couldn't—the opportunity to build products from scratch, to see innovations reach market quickly, to impact India's digital transformation. They retained talent through crisis by maintaining R&D investment even during financial stress, signaling commitment to technology. The culture evolved from hierarchical to entrepreneurial, from risk-averse to innovation-oriented, from domestic-focused to globally ambitious.

Patient Capital and Long-term Thinking: Despite public market pressures, HFCL maintained long-term orientation. Investments in R&D, manufacturing capacity, and market development often took years to pay off. The optical fiber plant investment looked questionable during oversupply but proved prescient when 5G drove demand. The defense vertical took years of capability building before generating significant revenue. This patience isn't financial luxury—it's strategic necessity in industries with long development cycles and relationship-based selling.

X. Bear vs Bull Case & Future Outlook

Bear Case: The Structural Challenges

The bear case for HFCL starts with sobering financial realities. The company has delivered a poor sales growth of 1.15% over past five years. Company has a low return on equity of 7.66% over last 3 years. These metrics suggest a company struggling to generate growth and returns in a supposedly high-growth industry. For investors seeking explosive growth stories, HFCL's modest financial performance raises questions about execution and market positioning.

The promoter pledge issue creates a sword of Damocles. Promoters have pledged or encumbered 54.1% of their holding. High promoter pledging often precedes distress selling during market downturns, creating cascading price pressure. It also raises questions about the promoters' financial position outside the company and limits their ability to participate in fund-raising if needed.

Competition from Chinese vendors remains an existential threat despite government restrictions. Chinese companies like Huawei and ZTE have scale advantages that enable R&D investments HFCL cannot match. They offer vendor financing that cash-strapped operators find attractive. While banned from some government contracts, Chinese vendors remain active in private networks. As geopolitical tensions potentially ease, these competitors could re-enter restricted segments, pressuring prices and margins.

Global technology giants pose different but equally serious challenges. Companies like Nokia, Ericsson, and Samsung have decades of 5G experience, vast patent portfolios, and established operator relationships globally. As Indian operators mature and demand sophisticated core network equipment, HFCL's edge-focused product portfolio may limit addressable market. These giants also have financial strength to sustain losses while gaining market share—a luxury HFCL doesn't enjoy.

The global optical fiber cable market is currently experiencing a slowdown. However, it is anticipated that the market will begin to see growth again from the last quarter of current financial year 2024-25. The optical fiber market faces structural oversupply. Chinese manufacturers expanded capacity aggressively, creating global glut. Prices have fallen 40-50% from peaks, pressuring margins across the industry. While demand will eventually absorb supply, the timeline remains uncertain. HFCL's backward integration into fiber manufacturing, while strategically sound, exposes it to commodity cycle volatility.

Telecom capex cyclicality creates earnings volatility that markets dislike. Indian operators completed initial 5G rollout faster than expected, potentially creating an air pocket in equipment demand. The next investment cycle—5G densification and advanced features—may take years to materialize. Government infrastructure spending, while substantial, faces execution delays and payment issues that stress working capital.

Bull Case: The Transformation Story

The bull case rests on fundamental transformation that metrics haven't fully captured. The shift from projects to products isn't just mix change—it's business model revolution. Telecom Products (57% in 9M FY25 vs 43% in FY22) with 24% growth demonstrates momentum in the right direction. As this shift continues, margins should expand, working capital should improve, and returns should increase. The company is essentially transforming from a construction contractor to a technology manufacturer—a transition that takes time but creates substantial value.

The 5G opportunity in India remains early innings. While initial rollout focused on coverage, the real investment comes from densification, enterprise networks, and advanced use cases. India's 5G subscriber base is projected to reach 800 million by 2030, requiring massive network investment. HFCL's product portfolio—small cells, FWA equipment, transport products—addresses exactly these requirements. Unlike 2G/3G/4G where foreign vendors dominated, 5G's open architecture and government support for local manufacturing create unprecedented opportunity for Indian vendors.

Defense and railways diversification provides secular growth independent of telecom cycles. India's defense modernization, with emphasis on indigenous equipment, creates a $10+ billion annual addressable market. Railways' signaling modernization and network expansion require specialized communication equipment where HFCL has established credibility. These segments offer better payment terms, higher margins, and longer-term contracts than traditional telecom.

Technology leadership in specific niches creates defensible moats. With the launch of open-source Wi-Fi 7 Access Point, HFCL has become the first original equipment manufacturer in India to design and launch this Wi-Fi technology to complement the indoor 5G coverage. Being first with Wi-Fi 7 globally isn't just PR—it demonstrates R&D capability, attracts talent, and builds customer confidence. Leadership in UBRs, with over 500,000 deployments, creates scale advantages competitors struggle to match.

BharatNet and government infrastructure push provide multi-year revenue visibility. The government's commitment to connecting all gram panchayats with optical fiber creates steady demand for HFCL's cables and equipment. Smart Cities, despite implementation challenges, require extensive networking infrastructure. These government programs, while slow, provide base demand that private capex supplements rather than replaces.

Export potential offers the biggest upside surprise. International revenue at 20% of total could double as HFCL's products gain global acceptance. The company's focus on emerging markets—Africa, Southeast Asia, Latin America—addresses the next wave of digital infrastructure investment. Products designed for Indian conditions resonate in these markets, providing competitive advantage versus developed market vendors.

The PLI scheme fundamentally alters economics. Government incentives for local manufacturing improve margins by 4-6% for eligible products. This transforms marginally viable products into profitable ones and enables price competition with imports. As HFCL scales PLI-eligible production, margin expansion could surprise positively.

Management quality and execution track record inspire confidence. Navigating from near-bankruptcy to technology leadership demonstrates exceptional strategic thinking and execution. The team that survived CDR and transformed the business model has earned credibility. Their conservative guidance and focus on profitable growth over revenue suggests lessons learned from past excess.

Future Outlook: The Next Chapter

The next five years will determine whether HFCL becomes India's telecom equipment champion or remains a niche player. The pieces are in place—technology capabilities, manufacturing infrastructure, customer relationships, and financial stability. But execution in a rapidly evolving market will determine outcomes.

The immediate focus is completing the business model transformation. Achieving 70% product revenue mix would fundamentally alter financial characteristics. Working capital days should decline from 170 to below 120. ROE should improve from high single digits to mid-teens. These aren't aggressive targets—they're natural outcomes of mix shift and operational improvement.

Technology evolution continues accelerating. 6G research has begun globally, with commercial deployment expected by 2030. HFCL must balance current product development with future technology investment. The company's approach—partnering for core technology while developing applications and solutions—seems sustainable. But maintaining technology relevance requires continuous investment that pressures near-term margins.

Consolidation in the telecom equipment industry seems inevitable. Smaller players lack scale for R&D investment. Larger players seek market share and technology. HFCL could be acquirer, target, or merger partner. The company's valuable assets—manufacturing facilities, customer relationships, product portfolio—make it attractive. But cultural fit and valuation expectations will determine outcomes.

The India opportunity remains compelling despite near-term challenges. Digital transformation isn't optional—it's existential for economic growth. The government understands this, evidenced by consistent infrastructure investment despite fiscal constraints. Private operators, after 5G investment digestion, will resume spending on densification and enterprise solutions. HFCL, as one of the few credible Indian vendors, should capture disproportionate share.

XI. Recent News

The momentum in HFCL's business is accelerating, with recent developments validating the strategic transformation. HFCL Limited bags Purchase Order aggregating to ~INR 157 Crores from Tera Software Limited, a consortium partner of ITI Limited for BharatNet Project, demonstrating continued traction in government infrastructure projects. More significantly, In the December quarter, the company bagged an advance work order worth about Rs 2,501.30 crore for the design, supply, construction, installation, upgrade, operation, and maintenance of the middle-mile network of BharatNet Phase III in the Punjab Telecom Circle. In addition, the company has also secured advance purchase orders worth Rs 2,167.65 crore from Rail Vikas Nigam Ltd for the supply and maintenance of optical fibre cables, telecom gears for BharatNet Phase III in Uttar Pradesh (East) Telecom Circle, and Uttar Pradesh (West) Telecom Circle.

These BharatNet wins are transformative—over ₹4,600 crore in orders from a single government program validates HFCL's positioning as the partner of choice for India's digital infrastructure buildout. The scope includes not just equipment supply but design, installation, and multi-year maintenance, providing revenue visibility and recurring income streams.

The 5G momentum continues building. HFCL Limited...has secured a purchase order of Rs 623 crore for the supply of indigenously manufactured 5G networking equipment. This is the first such large order for 5G networking equipment placed on any Indian company by any telecom service provider. Being the first Indian company to win such a large 5G order marks a watershed moment—it proves that indigenous manufacturers can compete with global vendors in cutting-edge technology.

International expansion is gaining traction. Our goal is to achieve a substantial rise in export revenue from our optic fibre segment, with a significant portion of revenue coming from international markets in the coming years. Additionally, we aim for a considerable share of our telecom segment revenue to be export-driven. The company is executing on this vision with the company's board has granted approval for a strategic expansion into Europe by way of setting up an optical fibre cable manufacturing facility in Poland.

The European expansion is particularly strategic. The European Commission on December 16, 2024 announced the imposition of definitive anti-dumping duty on all other Indian OFC manufacturers, reaffirming HFCL's exemption. This exemption from anti-dumping duties gives HFCL a massive competitive advantage—while other Indian manufacturers face tariff barriers, HFCL can compete on level terms with European producers.

Defense orders are materializing after years of capability building. the company has received a letter of intent for defence orders worth Rs 800 crore that has been delayed due to the approval process and is making efforts to complete it by April or May this year. Defense contracts, while slow to materialize, offer multi-year revenue visibility and higher margins than commercial telecom.

Financial performance shows mixed signals reflecting the transition phase. The company's consolidated net profit declined 10.4% to Rs 73.65 crore on a 2% fall in revenue to Rs 1,011.95 crore in Q3 December 2024 over Q3 December 2023. However, order book strength provides confidence. the firm had an order book of Rs 10,000 crore as on December 31, 2024—nearly three years of revenue visibility at current run rates.

Management's ambitious vision is clear. Domestic telecom gear maker HFCL is betting big on growth from overseas sales and uptake of defence supplies as the company looks to become a Rs 10,000-crore revenue enterprise. Achieving ₹10,000 crore revenue would represent nearly 3x growth from current levels—ambitious but achievable given the order book and market opportunities.

The strategic priorities are evolving. our strategic focus on new products, global expansion, focus on building both capacities and capabilities backward and horizontal integration has begun to yield positive results. Our commitment to strengthening market share and technology leadership positions remain steadfast as we continue to invest in innovation for both cost and performance benefits.

Recent earnings calls reveal management confidence despite near-term challenges. Nahata said HFCL is likely to add a revenue of Rs 350-400 crore in the current quarter but may not achieve the target of Rs 2,000 crore set for the fiscal year due to shortfall in supply of some equipment on account of delay in customer readiness, trials, etc. This transparency about execution challenges while maintaining long-term optimism reflects mature management that has learned from past over-promises.

The BharatNet opportunity deserves special attention. BharatNet is a large opportunity for everybody, all tele companies involved. It's about INR 1.4 lakh crores, out of which, but let me be clear, out of which roughly about INR 40,000 crores to INR 50,000 crores would be CapEx rest would be OpEx, which would incur over 10 years. HFCL's early wins position it to capture significant share of this massive program.

XII. Links & Resources

Company Resources: - Investor Presentations: Available on www.hfcl.com/investors - Annual Reports: BSE and NSE filings sections - Quarterly Results: Published within 45 days of quarter end - Corporate Announcements: Stock exchange websites

Industry Research: - Telecom Equipment Manufacturers Association (TEMA) reports - COAI (Cellular Operators Association of India) industry updates - TRAI (Telecom Regulatory Authority of India) sector reports - Department of Telecommunications policy documents

Technology Resources: - 5G India Forum whitepapers - TIP (Telecom Infra Project) specifications - IEEE standards for Wi-Fi 7 and optical communications - Open RAN Alliance documentation

Government Programs: - BharatNet official portal for project updates - PLI scheme guidelines from Ministry of Electronics - Digital India initiative progress reports - Defense procurement portal for tender tracking

Financial Analysis: - Rating agency reports from CARE, ICRA - Broker research (where available publicly) - Stock exchange filings for detailed financials - Corporate debt market updates

The HFCL story is far from over. From a regional manufacturer in Himachal Pradesh to a global technology player, the company has demonstrated remarkable resilience and transformation capability. The challenges are real—competitive intensity, working capital management, and execution risks. But the opportunities—5G densification, BharatNet implementation, defense modernization, and global expansion—are equally substantial.

For investors, HFCL represents a bet on India's digital transformation and the broader theme of technology indigenization. It's not without risks, but for those who believe in India's technology future and appreciate companies that have survived existential crises to emerge stronger, HFCL offers a compelling narrative. The next chapter—whether HFCL becomes India's Huawei or remains a niche player—is being written now, shaped by technology transitions, government policies, and management execution.

The company that once bid ₹85,000 crore in audacious ambition and nearly died from the hubris has been reborn as a disciplined, technology-focused enterprise. That transformation, more than any financial metric, might be HFCL's greatest achievement and the best indicator of its future potential.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube