Pace Digitek: The Story of India's Telecom Infrastructure Powerhouse

I. Cold Open & Episode Setup

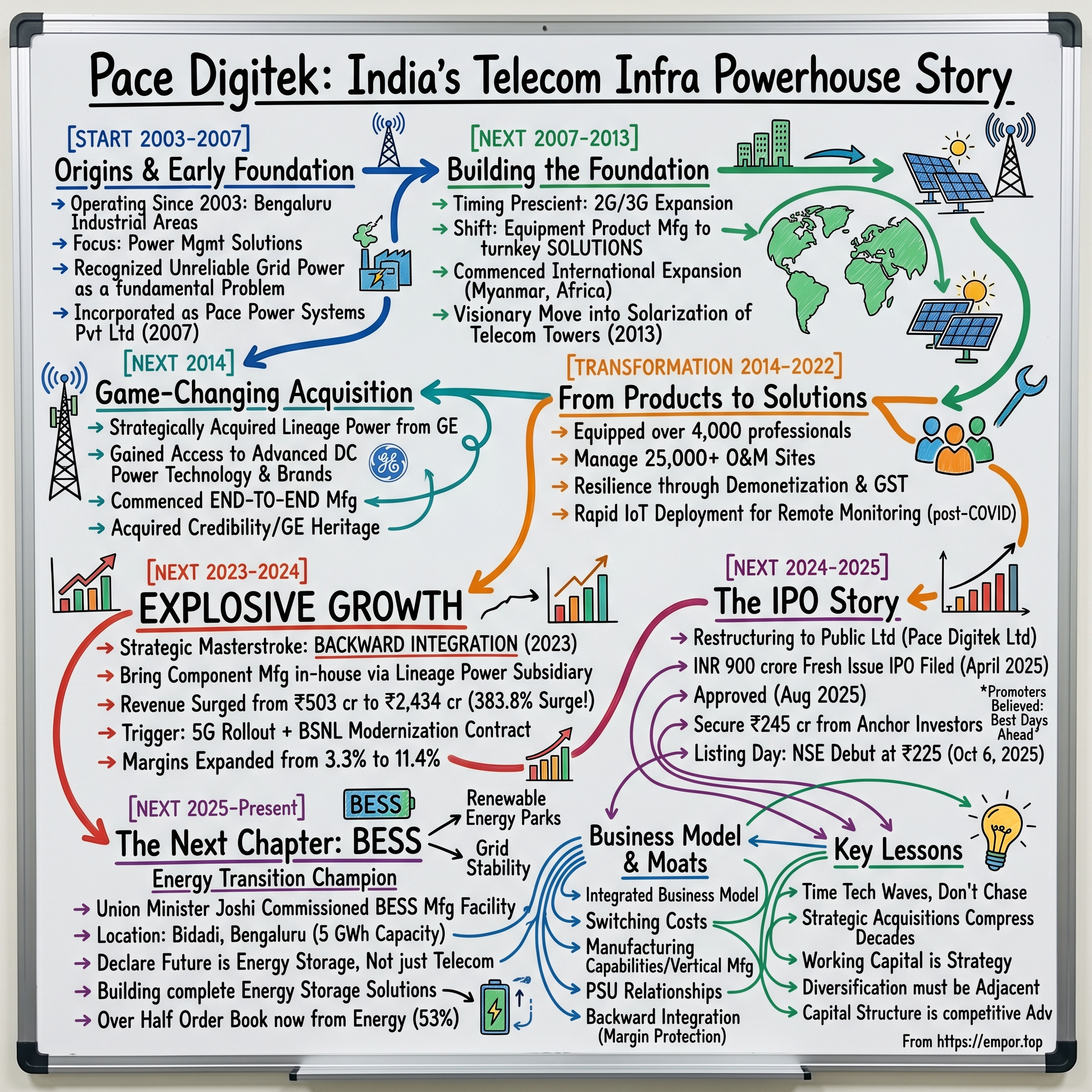

Picture this paradox: a company incorporated as Pace Power Systems Private Limited on March 1, 2007, in a nondescript industrial area of Bengaluru. Yet behind closed doors, the founders had been quietly operating since 2003, building power management solutions for an industry that barely existed in India at the time. The paperwork said 2007, but the sweat equity started four years earlier—a peculiar beginning for what would become one of India's most dramatic infrastructure transformation stories.

Now fast forward to fiscal year 2024. Revenue from operations increased from Rs 503.20 crore in FY23 to Rs 2,434.49 crore in FY24—a staggering 383.8% surge that most companies don't see in a decade, let alone twelve months. This wasn't just growth; it was metamorphosis. From a modest power equipment manufacturer to India's telecom backbone builder, Pace Digitek's journey reads like a playbook on timing, transformation, and tenacity.

What makes this story particularly fascinating isn't just the numbers—though a PAT surged from ₹16.5 crore to ₹229.9 crore (+1,290%) certainly catches attention. It's how a company founded by technocrats in Bengaluru's industrial outskirts managed to position itself at the intersection of every major infrastructure wave that swept through India: the 2G boom, 3G rollout, 4G revolution, fiber expansion, and now the 5G and renewable energy transitions.

Maddisetty Venugopal Rao, Padma Venugopal Maddisetty, Rajiv Maddisetty and Lahari Maddisetty are the company promoters—a family that saw opportunity where others saw complexity. They didn't just ride the waves; they anticipated them, positioning their surfboard before the swells even formed on the horizon.

This is the story of how a company with three manufacturing facilities totaling 200,000 square feet became the silent enabler of India's digital revolution. It's about strategic acquisitions that changed destinies, backward integrations that expanded margins, and a pivot to energy storage that might define the next chapter of India's infrastructure story. It's about Pace Digitek—a company you've probably never heard of, but whose handiwork touches every call you make, every video you stream, and increasingly, every watt of renewable energy stored for the grid.

II. Origins and Early Foundation (2003-2007)

The monsoons of 2003 brought more than just rain to Bengaluru. In the industrial corridors of Kumbalgodu, along the Bengaluru-Mysore highway, a small operation was taking shape. At the core of Pace Digitek's extraordinary journey lies a legacy of innovation and commitment dating back to 2003. The founders weren't waiting for perfect paperwork or ideal conditions—they were already manufacturing electrical equipment for an industry that was about to explode.

India's telecom sector in 2003 was a paradox of its own. Mobile subscribers numbered just 13 million in a country of over a billion people. Towers were scarce, power was unreliable, and the infrastructure needed to support a telecom revolution simply didn't exist. While multinational giants debated market entry strategies from air-conditioned boardrooms, Venugopalrao Maddisetty and Rajiv Maddisetty were getting their hands dirty in workshop floors, figuring out how to keep telecom towers running when the grid failed—which in India, happened with clockwork regularity.

Pace Digitek Limited was originally incorporated as Pace Power Systems Private Limited, at Bengaluru as a private limited company on March 1, 2007. But this formal incorporation was merely the legitimization of what had been brewing for four years. The founders had spent 2003 to 2007 understanding a fundamental problem: India's power infrastructure couldn't support its telecom ambitions. Every tower needed reliable backup power, every base station required sophisticated power management, and nobody was building these solutions specifically for Indian conditions—extreme heat, monsoon humidity, dust storms, and frequent power cuts.

At first, the company concentrated on power electronics solutions, particularly in the telecom sector, where the need for dependable power backup systems was growing swiftly. This wasn't glamorous work. While software startups in Bengaluru were making headlines, Pace was designing rectifiers and power supplies that could survive 45-degree heat in Rajasthan and torrential rain in the Northeast.

The timing was prescient. India was on the cusp of its 2G expansion, with players like Bharti Airtel, Vodafone (then Hutch), and Reliance Communications racing to build networks. Every operator needed thousands of towers, and every tower needed power management systems. The gold rush wasn't in spectrum or subscribers—it was in the unglamorous business of keeping the lights on.

Pace Power is a privately owned company with manufacturing and headquarters in Bengaluru, India. From day one, the founders insisted on vertical manufacturing—a decision that seemed capital-intensive and risky but would prove transformational. While competitors assembled imported components, Pace built its capabilities from the ground up. Factories are all ISO 9001 and use the most advanced methods and machinery in their vertical manufacturing methodology.

The early customers were skeptical. Why trust a small Bengaluru company when established players existed? The answer came through reliability and customization. Pace's equipment wasn't just built for Indian conditions; it was over-engineered for them. When a tower in Bihar stayed operational through a week-long power outage during floods, word spread. When equipment survived dust storms in Gujarat that knocked out imported alternatives, telecom operators took notice.

By 2007, as the company formalized its incorporation, it had already established credibility with key customers. The order books were thin but growing. The manufacturing facility was modest but expanding. Most importantly, the founders had identified their north star: wherever India's telecom infrastructure went, Pace would be there first, building the power systems that made connectivity possible.

The foundation was set. The electrical equipment manufacturer from Bengaluru was ready to become something more. And India's telecom boom was about to provide the perfect catalyst.

III. The First Decade: Building the Foundation (2007-2013)

The year 2008 should have been a disaster for a young infrastructure company. The global financial crisis was crushing businesses worldwide, credit was frozen, and India's growth story seemed to pause. Yet for Pace Digitek, operating now as a formally incorporated entity, the crisis became an unexpected accelerator. As multinational suppliers retreated and imports became expensive due to rupee depreciation, Indian telecom operators turned to domestic manufacturers. Pace was ready.

The 3G spectrum auctions of 2010 changed everything. The government raised an astronomical ₹67,719 crore, and every rupee of that would translate into infrastructure spending. Operators who had paid billions for spectrum needed to monetize it quickly, which meant rapid network rollouts. PACE was established in 2003 and has since grown into a leading OEM (Original Equipment Manufacturer) supplier, O&M Service provider for Towercos & Opcos. The company's evolution from pure manufacturing to services was beginning.

During these years, Pace made a crucial strategic decision: instead of just selling equipment, they would offer turnkey solutions. A telecom operator in Assam didn't just need a power system; they needed someone to transport it through difficult terrain, install it during monsoon season, and maintain it year-round. Pace said yes to all of it. The company commenced operations as an electrical equipment product manufacturer for the telecom industry, and over the years it has expanded Telecom Infra operations to comprise products, projects, operations & maintenance (O&M), and services and solutions.

The international expansion began almost accidentally. In 2011, Myanmar was opening up after decades of isolation. Its telecom infrastructure was virtually non-existent—the entire country had fewer mobile connections than a single Indian metro city. Pace executives flew to Yangon with a simple pitch: "We've built infrastructure in India's most challenging locations. Myanmar won't be harder." They were right. By 2012, Pace had its first international orders, small but symbolically important.

Africa came next. The continent's telecom boom was following India's trajectory with a five-year lag. The same challenges—unreliable power, harsh weather, difficult logistics—required the same solutions Pace had perfected in India. At present, our footprint spans India with a global presence in Africa, Bangladesh, Myanmar, the Philippines, and Sri Lanka, though the Philippines and Bangladesh expansions would come later.

Company has been undertaking projects for solarization of telecom towers (which comprises supply of solar modules and along with lithium-ion batteries the related passive equipments to telecom towers, installation, commissioning and O&M) since 2013. This early move into solar was visionary. While most telecom infrastructure companies saw solar as an expensive experiment, Pace recognized it as inevitable. Diesel costs were crushing tower operators' margins, and environmental regulations were tightening.

The numbers from this period don't tell the full story—revenues were growing steadily but not spectacularly. What mattered was what happened beneath the surface. Pace was building relationships, accumulating expertise, and creating a reputation for solving problems others wouldn't touch. When Bharat Sanchar Nigam Limited (BSNL) needed towers in Naxalite-affected areas where no contractor would go, Pace went. When private operators needed someone to manage sites in the Sundarbans where tigers were a genuine occupational hazard, Pace raised their hands.

By 2013, the company had operations across multiple Indian states, a growing international presence, and most importantly, trust from both public and private sector operators. The workforce had grown, the manufacturing facilities had expanded, and the service portfolio now included everything from installation to annual maintenance contracts.

But the founders knew something was missing. They were successful but subscale. They had capabilities but lacked cutting-edge technology. They had built a good company, but the opportunity was to build a great one. The telecom infrastructure market was consolidating globally, and Pace needed a game-changer to compete with larger players.

That game-changer would come from an unexpected source: General Electric was looking to exit a business that no longer fit its strategy. And Pace was ready to make the boldest move in its history.

IV. The Game-Changing Acquisition: Lineage Power from GE (2014)

The conference room in GE's Gurgaon office was intimidating even for seasoned executives. Across the table sat representatives of one of the world's most powerful corporations, a company with a market cap larger than many countries' GDPs. On the other side: the Maddisetty family from Bengaluru, running a company most people had never heard of. It was David meeting Goliath, except this time, David was trying to buy Goliath's slingshot.

In 2014, Pace Digitek strategically acquired Lineage Power from General Electric Company. But the story of how this happened is far more intricate than a simple M&A transaction. GE had acquired Lineage Power Holdings in 2011 for $540 million from The Gores Group, seeing it as strategic to their industrial internet ambitions. By 2014, new CEO Jeff Immelt was reshaping GE's portfolio, focusing on core industrial businesses. The Indian operations of Lineage Power—sophisticated but subscale—no longer fit the strategy.

For Pace, this was the opportunity of a lifetime. Lineage Power wasn't just a brand; it was a technology treasure trove. The company had developed some of the most advanced DC power systems in the world, with patents, certifications, and customer relationships that would take decades to build organically. The acquisition not only granted us access to avant-garde energy management technology but also allowed... Lineage Power's role transcends beyond the telecom infrastructure.

The negotiation was complex. GE wanted a clean exit but also needed assurance that the Lineage Power brand wouldn't be diluted. Pace wanted the technology but needed to structure the deal in a way that wouldn't overlever their balance sheet. Pace Power also gets the rights to use GE's Lineage Power brand in some of its areas of operation. The companies declined to disclose the value of the deal.

The financing was creative. Instead of a large upfront payment, Pace structured a combination of cash, earnouts, and technology transfer agreements. They convinced Indian banks that this acquisition would transform them from a regional player to a national champion. The banks, seeing the telecom infrastructure boom, agreed.

With the acquisition of the business of GE Power Electronics India and rights over the 'Lineage Power' brand in Fiscal 2014, the company commenced 'end to end' manufacturing of direct current systems which are tailored for telecom tower companies and operators and has helped it enhance market position in the energy management solutions. This wasn't just about buying assets; it was about acquiring capabilities that would typically take decades to develop.

The integration was smoother than anyone expected, perhaps because both companies shared engineering-first cultures. The GE India team, initially skeptical about being acquired by a smaller Indian company, was won over by Pace's commitment to technology and manufacturing excellence. Key personnel were retained, expertise was preserved, and the Lineage Power brand was given new life under Indian ownership.

In 2014, Pace Digitek acquired the business of GE Power Electronics India and the rights to the 'Lineage Power' brand, enabling it to commence end-to-end manufacturing of direct current (DC) systems tailored for telecom towers. The impact was immediate. Contracts that were previously out of reach became winnable. Large telecom operators who wouldn't return Pace's calls were suddenly interested in meetings.

The technology transfer was the real prize. Lineage Power's rectifier modules were 30% more efficient than anything Pace had built before. Their thermal management systems could operate in higher temperatures without derating. Their modular architecture meant systems could be scaled up or down based on site requirements. Currently, Lineage Power has 3 world-class facilities of telecom and power equipment for DC supplies, SMPS, Power Interface Units, AMF Panels, and Rectifier Modules.

But perhaps the most important acquisition was credibility. When Pace's sales team walked into a room and said they owned Lineage Power, doors opened differently. When they bid for international projects, the GE heritage carried weight. The company that started in a Bengaluru workshop now had technology that could compete globally.

The acquisition also brought discipline. GE's systems and processes, from quality control to project management, were integrated into Pace's operations. Six Sigma methodologies were implemented. Supply chain management was revolutionized. What had been an entrepreneurial company became a professionally managed enterprise without losing its entrepreneurial spirit.

By the end of 2014, the transformation was evident. Pace Digitek was no longer just another telecom infrastructure company. They were now technology leaders with manufacturing capabilities, global credentials, and most importantly, the confidence to dream bigger. The acquisition had cost them financially, but it had given them something priceless: the ability to shape India's infrastructure future rather than just participate in it.

V. The Transformation Years: From Products to Solutions (2014-2022)

The integration of Lineage Power was complete, but Venugopal Rao Maddisetty stood in the newly expanded Bengaluru facility with a realization: owning advanced technology was just the beginning. The real transformation would come from reimagining what an infrastructure company could be. Between 2014 and 2022, Pace Digitek would undergo its most fundamental evolution—from a product manufacturer to an end-to-end solutions provider.

The shift began with a simple observation. Telecom operators were drowning in complexity. They had different vendors for tower construction, power systems, fiber laying, and maintenance. Each vendor pointed fingers when something went wrong. Pace decided to become the single throat to choke—one company that could handle everything from site acquisition to steady-state operations.

Equipped with a proficient team of more than 4000 professionals, we've proudly serviced over 100,000 products, managed over 25,000 O&M service sites, and provided energy services to 600 or more sites. This massive scaling didn't happen overnight. Each year brought deliberate capability additions.

2015: The company established its second manufacturing facility, expanding beyond power systems into complete tower infrastructure solutions. The 200,000 square feet of total manufacturing space across Bengaluru became a showcase of vertical integration.

2016: Demonetization hit India like a tsunami. Construction projects stalled, payments delayed, and many infrastructure companies collapsed. Pace survived through a combination of strong relationships with banks, better working capital management than peers, and crucially, long-term contracts with government entities that continued paying despite the chaos.

2017: The Goods and Services Tax (GST) implementation created another disruption. But Pace had learned from demonetization. They had built buffers, diversified their customer base, and most importantly, invested in systems that could handle regulatory complexity. While competitors struggled with compliance, Pace was winning contracts.

2018-2019: These years marked the acceleration of 4G rollouts. Reliance Jio's entry had disrupted the market, forcing all operators to upgrade networks rapidly. Pace was perfectly positioned—they had the products, the execution capability, and the balance sheet to handle large projects. With a resilient workforce of 4000+ experts spread across the Indian, African, Myanmar, and SAARC markets, Lineage Power is recognized for its remarkable operational presence. The company has completed 100,000+ product services and 25,000+ sites of O&M services.

Then came 2020 and COVID-19.

The first lockdown announcement found Pace's teams scattered across hundreds of remote sites. Some were in Ladakh, others in the Andaman Islands. The immediate challenge wasn't strategic but human—how to ensure employee safety while maintaining critical infrastructure that kept India connected during the pandemic.

The company's response revealed its evolution. Within 72 hours, Pace had created bio-bubbles at critical sites, arranged accommodation for workers who couldn't return home, and established testing protocols before they became mandatory. They convinced authorities that telecom infrastructure was essential service, getting movement passes for their teams when entire cities were locked down.

Financially, COVID-19 should have been devastating. Projects were delayed, new orders dried up, and receivables stretched as customers preserved cash. But Pace's transformation into a solutions provider paid off. While product sales plummeted, recurring revenue from O&M contracts continued. Sites needed maintenance whether there was a pandemic or not.

The pandemic also accelerated digital transformation. Remote monitoring systems, previously a nice-to-have, became essential. Pace rapidly deployed IoT sensors across sites, enabling remote diagnostics and predictive maintenance. A control room in Bengaluru could now monitor battery health in Mizoram, fuel levels in Bihar, and temperature readings in Rajasthan—all in real-time.

2021-2022 brought unexpected opportunities. The government's push for digital India had gained urgency post-COVID. BharatNet projects accelerated. Smart city initiatives resumed. Most importantly, the 5G auctions were approaching, and everyone knew the infrastructure requirements would be unprecedented.

PDL also undertakes turnkey projects for renewable energy sector through Subsidiary, Pace Renewable Energies Private Limited. It also undertakes BESS projects in either standalone mode or coupled with solar PV plants, floated through both 'build, own, and operate' and 'engineering, procurement, and construction' models. This diversification into renewable energy, started modestly during these years, would soon become crucial.

By 2022's end, Pace Digitek had transformed completely. They were no longer just selling products or even just executing projects. They were managing the entire lifecycle of infrastructure assets. A telecom operator could give them coordinates and requirements; Pace would handle everything else—from getting permits to laying fiber, from installing equipment to managing operations for decades.

The numbers validated the strategy. Order books were growing, margins were expanding, and most importantly, customer relationships had deepened. When BSNL or Bharti Airtel thought about infrastructure, Pace was no longer a vendor—they were a partner.

But the biggest transformation was yet to come. As 2023 approached, the company was about to execute a strategic masterstroke that would send revenues soaring nearly 6x in a single year.

VI. The Inflection Point: Backward Integration & Explosive Growth (2023-2024)

The board meeting in early 2023 was unusually tense. The Maddisetty family had built Pace Digitek steadily for two decades, but what they were proposing now seemed almost reckless. They wanted to backward integrate through their subsidiary Lineage Power Private Limited, bringing component manufacturing in-house. The investment required was massive, the risks substantial, and the timing—with global supply chains still recovering from COVID—seemed questionable.

But Venugopal Rao had done his homework. Every analysis pointed to the same conclusion: the companies that would win India's infrastructure boom wouldn't be those with the best products or even the best execution. Winners would be those who controlled their supply chains. From Fiscal 2023, it has backward integrated supply of Telecom Infra products through its Subsidiary, Lineage Power Private Limited.

The impact was almost immediate and far more dramatic than even the optimists predicted. Revenues grew nearly 6x from FY23 (INR 503 crore) to FY24 (INR 2,434 crore). This wasn't just growth—it was an explosion. To put this in perspective, most infrastructure companies are thrilled with 20% annual growth. Pace achieved 383.8% in twelve months.

What triggered this extraordinary surge? Three factors converged perfectly:

First, the backward integration immediately expanded margins. Components that Pace previously bought from suppliers at 30-40% markup were now manufactured in-house. On large contracts, this meant millions in additional profit. The EBITDA impact was staggering—margins expanding from 3.3% in FY23 to 11.4% in FY25.

Second, India's 5G rollout had begun in earnest. Every 5G site needed 3-4x more equipment than 4G sites. Power requirements were higher, fiber density greater, and complexity exponentially increased. Pace was one of the few companies that could deliver integrated solutions at scale. When Reliance Jio needed to roll out thousands of sites monthly, Pace could commit because they controlled their supply chain.

Third, and perhaps most importantly, BSNL's massive modernization drive kicked into high gear. The state-owned operator, after years of decline, received government support for a comprehensive network upgrade. Operating Income: ₹2,511.82 crore, a significant increase from ₹516.26 crore in the previous year... including a ₹7,033 crore contract from BSNL. This single contract transformed Pace's trajectory.

The BSNL project wasn't just large; it was complex. It required equipment supply, installation across difficult terrains, and long-term maintenance. Many companies could do one or two of these elements. Pace could do all three, and thanks to backward integration, they could do it profitably.

The operational excellence during this period was remarkable. PAT increased from Rs 16.53 crore in FY23 to Rs 229.87 crore in FY24 and Rs 279.10 crore in FY25—a 1,290% increase that made Pace one of the fastest-growing infrastructure companies globally.

But growth at this pace brings challenges. Working capital requirements exploded. Pace needed to fund raw materials for manufacturing, execute projects before payment, and manage receivables from government entities notorious for delayed payments. The solution came through creative financing—bill discounting, supply chain financing, and most importantly, strong relationships with banks who understood the quality of Pace's order book.

The company also faced execution challenges. Scaling from ₹500 crore to ₹2,400 crore revenue meant hiring aggressively, expanding manufacturing, and managing thousands of concurrent projects. Lesser companies would have broken under the pressure. Pace's two-decade foundation of systems and processes held firm.

International operations also contributed, though India remained the growth engine. Myanmar's digital transformation accelerated post-coup as the military government sought to control communications. African operations expanded as countries like Kenya and Tanzania rolled out 4G networks. These international projects, while smaller, provided better margins and crucial foreign exchange earnings.

By March 2024, as the financial year closed, Pace Digitek had been transformed once again. As of 31 March 2025, the company had an order book worth INR 7,633 crore, entirely from public sector undertakings (PSUs), providing multi-year visibility. The company that had started FY23 as a mid-sized infrastructure player ended FY24 as one of India's largest telecom solutions providers.

The debt-to-equity ratio, despite massive growth, actually improved—falling to 0.13 by FY25. This wasn't leveraged growth; it was profitable expansion. Return on equity hit levels that made software companies envious. The working capital cycle, though extended due to government contracts, was manageable thanks to strong banking relationships.

But perhaps the most important achievement was credibility. When the IPO plans were announced, the market didn't see a company that had gotten lucky with one big contract. They saw an organization that had methodically built capabilities for two decades and was now harvesting the fruits of patient preparation.

As 2024 progressed, the founders began thinking about the next phase. The private company had achieved everything possible within its current structure. To compete for even larger projects, to expand internationally at scale, and to participate in India's renewable energy revolution, they needed capital. It was time to go public.

VII. The IPO Story & Public Market Debut (2024-2025)

The journey to the public markets began not in boardrooms but in a small office where the Maddisetty family confronted a truth: Pace Digitek had outgrown its private company structure. The order book exceeded ₹7,600 crore, expansion plans required massive capital, and most importantly, the opportunity ahead—in 5G, fiber, and renewable energy—was too large for internal funding alone.

The corporate restructuring began in July 2024. The name of the Company was changed to Pace Digitek Infra Private Limited, dated July 24, 2020. The name of Company was changed to Pace Digitek Private Limited, and a fresh certificate of incorporation dated July 29, 2024, was issued. Each name change reflected evolution—from power systems to digital infrastructure to the final avatar as a comprehensive solutions provider.

Subsequently, Company got converted into a public limited and the name was changed to its present name, Pace Digitek Limited, pursuant to a fresh certificate of incorporation dated November 19, 2024. The conversion to a public limited company was smooth, but the real work was just beginning.

The DRHP was submitted earlier on 3 April 2025, with Unistone Capital acting as the lead manager... Pace Digitek filed its DRHP with SEBI on 3 April 2025 and received approval for its INR 900 crore IPO on 29 August 2025. The five-month approval process was relatively quick by SEBI standards, reflecting the quality of documentation and the company's strong fundamentals.

The IPO structure was deliberately clean—Pace Digitek IPO will be a totally fresh issue of INR 900 crore. The issue will be entirely a fresh issue, with no Offer for Sale (OFS). This sent a powerful signal: the promoters weren't cashing out. They believed the best days were ahead.

September 26, 2025, arrived with unusual anticipation. IPO markets had been volatile, with several issues failing to fully subscribe. Pace Digitek's pricing at ₹219 per share valued the company at roughly ₹4,700 crore—aggressive but justified by growth rates and order book visibility.

Prior to the public issue, Pace Digitek secured ₹245.14 crore from anchor investors by allotting 1.12 crore shares at ₹219 each on 25 September 2025. Key investors included Bandhan Small Cap Fund, SBI General Insurance, Samsung India Small & Mid Cap Focus Trust, Compact Structure Fund, Necta Bloom VCC, Rajasthan Global Securities Pvt Ltd, Holani Venture Capital Fund-I, Sunrise Investment Opportunities Fund, and Abundantia Capital VCC. This strong anchor allocation reflected confidence in the company's growth strategy.

The four-day IPO period was nerve-wracking. Day one saw tepid response—just 0.4x subscription. Critics questioned whether the market understood the infrastructure story. Day two improved to 0.8x, but doubts persisted. Then institutional investors arrived. By day three, the issue was oversubscribed. The telecom infra IPO, subscribed 1.59x, secured ₹245.14 Cr from anchor investors.

October 6, 2025—listing day. The Maddisetty family gathered at the NSE, watching as their life's work became a public company. Pace Digitek shares listed at ₹225, a 2.7% premium over the ₹219 issue price. Modest by IPO standards, but the founders weren't concerned. They were building for decades, not days.

The early trading patterns were revealing. Unlike typical IPOs where pre-IPO investors dump shares, Pace saw accumulation. Institutional investors who missed the IPO were buying. The stock found its floor around ₹206 and ceiling near ₹231, establishing a trading range that reflected both potential and uncertainty.

Pace Digitek shares rose 3.47% to ₹216.80 after winning a ₹185.87 Cr O&M contract from Tata Teleservices for five southern states telecom infrastructure... Mr. Rajiv Maddisetty, Whole-time Director of Pace Digitek Limited, stated, "We are immensely proud that Tata Teleservices has entrusted us with this critical O&M contract. This award underscores the trust and value we deliver in the telecom infrastructure space". This contract win, announced just days after listing, validated the growth story.

The capital allocation strategy was clear from day one. Proceeds will primarily fund capex (INR 630 crore) and general corporate purposes. The majority would go toward the BESS manufacturing facility—a bet on India's energy storage future that would define Pace's next chapter.

Post-IPO, the governance structure evolved rapidly. Independent directors were appointed, quarterly reporting began, and the informal family-run culture started adapting to public market scrutiny. The challenge was maintaining entrepreneurial agility while building institutional processes.

Market reception remained mixed but improving. Sell-side analysts struggled to categorize Pace—was it a telecom play, an infrastructure story, or a renewable energy bet? The answer, of course, was all three, but markets prefer simple narratives. The company's investor relations team worked overtime, educating funds about the integrated business model.

By early 2025, patterns emerged. The stock correlated strongly with government infrastructure spending announcements. Every BSNL contract update moved the price. Renewable energy policy changes caused volatility. The market was slowly learning to value Pace not just for what it was, but what it was becoming.

The IPO proceeds were deployed quickly. Construction of the BESS facility accelerated. Working capital for new projects was secured. Most importantly, the public listing provided currency for future acquisitions—though the founders remained selective, having learned from the Lineage Power experience that the right acquisition at the right time could be transformational.

As 2025 progressed, Pace Digitek settled into its new identity as a listed company. The scrutiny was intense, the reporting requirements onerous, but the benefits clear. Access to capital, enhanced credibility, and most importantly, the ability to participate in India's next infrastructure revolution—renewable energy and storage.

VIII. The Next Chapter: BESS and Energy Transition (2025-Present)

June 28, 2025, Bidadi Industrial Area, Bengaluru. Union Minister for New and Renewable Energy Pralhad Joshi cut the ribbon on what might be India's most important manufacturing facility that nobody had heard of. The minister hailed the development as a significant step towards clean energy, improved grid resilience, and India's emergence as a global leader in energy storage... The BESS facility, established by PACE Digitek, boasts an annual manufacturing capacity of 5 GWh, placing it among the country's most advanced energy storage units.

This wasn't just another factory opening. This was Pace Digitek's declaration that it was no longer just a telecom infrastructure company. The future was energy storage, and Pace intended to own it.

The BESS (Battery Energy Storage Systems) opportunity was massive and urgent. India had committed to 500 GW of renewable energy by 2030. Solar and wind power were intermittent—the sun doesn't always shine, the wind doesn't always blow. Without storage, renewable energy remained a promise unfulfilled. The CEA estimates a project requirement of 411.4 GWh (175.18 GWh from PSP and 236.22 GWh from BESS) of energy storage systems by 2032.

The Bidadi facility represented two years of planning and execution. Pace Digitek has commissioned a battery energy storage systems (BESS) manufacturing facility, through its subsidiary Lineage Power Private Limited. The facility is located in the Bidadi industrial area in Bengaluru, Karnataka... The facility has an annual production capacity of 2.5 GWh, extendable to 5 GWh.

The technology inside was cutting-edge. It will feature a fully automated cell-to-pack assembly line. Lithium iron phosphate cells, proven safer than alternatives, were assembled into modules, then racks, then containers. Each container could store megawatt-hours of electricity—enough to power hundreds of homes through the night.

But Pace wasn't just assembling batteries. They were building complete energy storage solutions. These include: (i) liquid cooled battery energy storage containers; (ii) power conversion systems (PCS); and (iii) energy management system (EMS). The liquid cooling was crucial for Indian conditions where ambient temperatures could exceed 45°C. The EMS was the brain, deciding when to charge, when to discharge, optimizing for electricity prices and grid stability.

The market opportunity was staggering. According to the India Energy Storage Alliance, the country's energy storage sector is likely to attract ₹4.79 lakh crore investment by 2032. Every solar park needed storage. Every wind farm required batteries. The grid itself needed massive storage to manage the duck curve—the mismatch between peak renewable generation and peak demand.

Pace's telecom heritage provided unexpected advantages. They understood remote site management, having maintained thousands of telecom towers in difficult locations. They knew battery technology, having deployed backup power systems for two decades. Most importantly, they had relationships with government entities who were now driving renewable energy adoption.

The first major BESS contract came from Maharashtra State Electricity Distribution Company Limited (MSEDCL). The project requirements were daunting—grid-scale storage that could respond in milliseconds to frequency changes, survive monsoons and summer heat, and operate reliably for 20 years. Pace won not because they were cheapest, but because they could deliver.

"Through this facility, PACE Digitek is not just manufacturing batteries—it is helping shape India's energy future. It will foster innovation, create high-value jobs, and strengthen our manufacturing ecosystem in line with the vision of Aatmanirbhar Bharat," the minister said.

The transformation wasn't just about new products; it was about reimagining the business model. In telecom, Pace sold equipment and provided services. In energy storage, they could own and operate assets. A 100 MWh storage facility could generate recurring revenue for decades through capacity charges and energy arbitrage. The financial profile shifted from lumpy project revenue to predictable cash flows.

Competition was intensifying. Global giants like Tesla, Fluence, and Wartsila were entering India. Chinese manufacturers offered lower prices. But Pace had advantages: local manufacturing reduced costs by 30%, understanding of Indian conditions improved reliability, and relationships with utilities accelerated project awards.

The integration with existing businesses created synergies. Telecom towers needed backup power; BESS provided cleaner alternatives to diesel generators. Rural electrification projects required off-grid solutions; solar-plus-storage microgrids were perfect. Smart cities needed grid resilience; distributed storage was the answer.

By late 2025, the transformation was evident. Over half its order book now comes from energy (53% in FY25), showing it is preparing for growth in the renewable space. The company that had started as a telecom power equipment manufacturer was becoming an energy storage champion.

The challenges were real. Battery cell technology was evolving rapidly—lithium iron phosphate today, sodium-ion tomorrow, solid-state eventually. Global supply chains for lithium and other materials were volatile. Competition from Chinese manufacturers with government subsidies was intense. But Pace had navigated disruption before.

As 2025 ended, Pace Digitek stood at another inflection point. The telecom business provided steady cash flows and deep customer relationships. The energy storage business offered explosive growth and transformation potential. The combination—rare globally—positioned Pace uniquely for India's twin transitions: digital and energy.

The Bidadi facility hummed with activity, producing battery systems that would store sunshine for dark nights and wind for still days. It was perhaps the perfect metaphor for Pace Digitek itself—storing potential, waiting for the right moment to release transformational energy.

IX. Business Model & Competitive Moats

Understanding Pace Digitek requires grasping a fundamental truth: this isn't one business but three interconnected engines, each reinforcing the others in ways competitors struggle to replicate. The magic isn't in any single piece but in how they fit together.

The company's top 5 customers accounted for Rs 2,291.78 crore (93.97 percent) of the company's total revenue in FY25. This customer concentration would terrify most investors, but dig deeper and it reveals Pace's first moat: switching costs. When BSNL or Bharti Airtel gives Pace a contract, they're not just buying equipment. They're buying two decades of site knowledge, established maintenance protocols, and teams that know every tower's quirks. Switching providers means retraining thousands of technicians, rebuilding maintenance schedules, and risking network downtime. In telecom, downtime isn't just expensive—it's catastrophic.

The integrated business model creates the second moat. The company undertakes manufacturing, installation and commissioning services of products at the site and undertake operation and maintenance of site including tower erection and optical fiber cable laying as turnkey solution. It generates revenue from operations from 3 verticals i.e., telecommunications, energy, and information and communication technology (ICT). Competitors might match Pace on manufacturing or services individually, but few can offer everything. This integration creates pricing power—Pace can lose money on equipment sales knowing they'll recover it through 20-year maintenance contracts.

Manufacturing capabilities form the third moat. Those three facilities in Bengaluru, spanning 200,000 square feet, aren't just factories—they're fortresses. With certifications including ISO 9001:2015, ISO/IEC 27001:2022, ISO 20000:2018, ISO 14001:2015, and CMMi Level 3, alongside global safety benchmarks such as UL 1973, UL 1642, UL 9540A, and IEC 62619:2022. Each certification took years to obtain and creates barriers for new entrants. When a utility evaluates BESS suppliers, these certifications aren't nice-to-have—they're mandatory.

The backward integration through Lineage Power creates the fourth moat: margin protection. When raw material prices spike or supply chains tighten, Pace continues manufacturing while competitors scramble for components. This reliability premium shows up in contract awards—customers pay more for certainty.

PSU relationships constitute the fifth moat, perhaps the most underappreciated. As of 31 March 2025, the company had an order book worth INR 7,633 crore, entirely from public sector undertakings (PSUs). Government contracts in India aren't just about lowest price. They're about trust, track record, and navigating bureaucracy. Pace has spent two decades learning the unwritten rules—which clauses matter, which officials decide, which certifications open doors. A new entrant with better technology and lower prices would still lose because they don't speak the language.

The working capital dynamics reveal both strength and vulnerability. Company has high debtors of 276 days. In most industries, this would signal distress. In Indian infrastructure, it's normal. Government entities pay slowly but surely. Pace has built its entire financial structure around this reality—credit lines for working capital, relationships with banks that understand the cycle, and most importantly, the balance sheet strength to wait.

The revenue mix tells the strategic story. Telecom contributes ~94% of revenues, but energy is growing fast. ICT remains small at less than 1%, but serves a crucial purpose—it's the innovation sandbox where Pace experiments with new technologies before scaling them. Smart classroom solutions teach them about edge computing. Surveillance systems provide insights into AI and analytics. These small bets today could become major businesses tomorrow.

The competitive landscape is fragmented above and consolidated below. At the top, global giants like Huawei and Ericsson focus on active equipment, viewing passive infrastructure as commodity. At the bottom, thousands of small contractors handle simple installation work. Pace occupies the sweet spot—sophisticated enough to handle complex projects, local enough to provide responsive service.

Pricing power comes from an unexpected source: complexity management. When BSNL needs towers in Naxalite areas, fiber in the Northeast monsoons, and maintenance in Ladakh winters, few companies can deliver. Pace charges premium prices not for products but for problem-solving. The margin expansion from 3.3% to 11.4% reflects this value capture.

The capital efficiency is remarkable for an infrastructure business. Debt-to-Equity Ratio: 0.13 — Minimal debt, strong balance sheet. This isn't because projects don't require capital—they do. It's because Pace has mastered the art of using customer advances and supplier credit to fund growth. They get paid to grow, a rare achievement in capital-intensive industries.

The talent moat is subtle but crucial. Those 4,000 professionals aren't just employees—they're infrastructure specialists who understand both technology and India. Training a tower technician takes months. Creating a project manager who can handle government contracts takes years. Building a team that can execute across India's diverse geography takes decades. Competitors can poach individuals but not the institutional knowledge.

Risk management is embedded in the model. Geographic diversification across Indian states hedges against regional slowdowns. International operations provide currency hedging. The mix of products, projects, and services smooths revenue volatility. Even customer concentration, seemingly a risk, is managed through long-term contracts and deep relationships.

The platform economics are just beginning to emerge. Every tower Pace maintains is a data point. Every battery deployed is a sensor. The company is sitting on operational data that could optimize everything from maintenance schedules to energy trading. They haven't fully monetized this yet, but the potential is enormous.

What makes Pace's moats particularly defensible is their interconnection. Manufacturing supports services. Services generate data. Data improves manufacturing. PSU relationships provide steady revenue. Revenue funds innovation. Innovation wins more PSU contracts. It's a flywheel that accelerates with scale.

X. Playbook: Key Strategic Lessons

The conference room whiteboard in Pace's Bengaluru headquarters bears witness to two decades of strategic decisions. Some proved transformational, others educational. Together, they form a playbook for building infrastructure businesses in emerging markets—lessons written in project delays, payment struggles, and ultimately, remarkable success.

Lesson 1: Time the Technology Waves, Don't Chase Them

Pace's history reads like a masterclass in timing. They entered power management just before the 2G boom. They acquired Lineage Power just before 4G exploded. They backward integrated just before 5G began. Now they're building BESS capacity just as renewable energy takes off. This isn't luck—it's patient observation and aggressive execution when the moment arrives.

The key insight: infrastructure follows consumer adoption by 18-24 months. When Reliance launched Jio in 2016, Pace was already scaling manufacturing. When the government announced renewable targets in 2023, Pace had already broken ground on the Bidadi facility. They watch consumer trends but bet on infrastructure needs.

Lesson 2: Strategic Acquisitions Can Compress Decades into Years

The acquisition was a game-changer for us! It gave us a head start and footprint in DC Power Systems, which helped us become the leading telecom power solution provider it is today. The Lineage Power acquisition wasn't just buying assets—it was buying time. Building GE-level technology would have taken 10-15 years. Acquiring it took 6 months.

But the playbook goes deeper. Pace didn't just acquire technology; they acquired credibility, relationships, and most importantly, the confidence to compete globally. They also retained key personnel, integrated systems carefully, and maintained the acquired brand—mistakes many Indian companies make when buying foreign assets.

Lesson 3: Backward Integration Is About Control, Not Just Cost

The 2023 decision to backward integrate looked like a cost play—eliminate supplier margins, improve profitability. The real value was control. When global supply chains broke during COVID, Pace kept manufacturing. When the 5G rollout created component shortages, Pace had inventory. Control over supply chains is worth more than margin improvement.

The execution matters: Pace didn't integrate everything. They focused on critical components where technology differentiation and supply security mattered. Commodity items are still outsourced. It's strategic integration, not blind vertical expansion.

Lesson 4: Working Capital Is Strategy, Not Treasury

The company's operations are working capital-intensive, with gross current asset days of 239 in FY2024. Most companies would see this as a problem to solve. Pace sees it as competitive advantage. Those 276 debtor days? They're the price of admission to government contracts. Competitors who can't fund this working capital can't compete for the most lucrative projects.

The playbook: Build banking relationships before you need them. Structure contracts with advance payments where possible. Use supply chain financing creatively. Most importantly, educate investors that working capital in infrastructure isn't inefficiency—it's investment.

Lesson 5: Government Relationships Are Built Over Decades

The company generates a major portion of its revenue from public sector customers. This isn't a vulnerability—it's a moat. But building these relationships requires patience most companies lack. Pace started with small BSNL contracts in dangerous areas others avoided. They delivered consistently, building trust over years. Twenty years later, that trust translates into billion-dollar contracts awarded without competitive bidding.

The key: Understand that government contracts aren't just about price. They're about reliability, local presence, and solving problems beyond the contract scope. When floods hit Kerala, Pace fixed towers outside their maintenance contracts. When COVID hit, they kept government networks running despite payment delays. These investments in relationships pay dividends for decades.

Lesson 6: Diversification Must Be Adjacent, Not Random

Pace's evolution from power systems to telecom infrastructure to energy storage seems logical in retrospect, but each expansion was carefully chosen. Telecom towers needed power systems—adjacent. Towers needed fiber connectivity—adjacent. Renewable energy needed storage—adjacent. They never strayed far from their core competency: critical infrastructure that requires high reliability.

The discipline shows in what they didn't do. Despite opportunities, they didn't enter real estate, didn't chase software services, didn't build consumer products. Every diversification leveraged existing capabilities while adding new ones.

Lesson 7: Build for the Future While Serving the Present

The BESS investment is instructive. In 2023, India's battery storage market was tiny. By 2025, when the facility opened, demand was exploding. This requires betting corporate resources on future markets while current businesses fund the investment. It's a difficult balance—too early and you burn cash waiting for demand, too late and competitors establish positions.

Pace's approach: Start small, learn fast, scale aggressively. They began with small solar installations in 2013, learned battery management, understood customer needs, then committed to the 5 GWh facility when the market signals were clear.

Lesson 8: Culture Eats Strategy, Even in Infrastructure

The Maddisetty family's hands-on approach permeates Pace. Executives visit remote sites. Engineers are empowered to solve problems without bureaucracy. Speed matters more than perfection. This culture—unusual in infrastructure—enables Pace to win contracts through execution speed that competitors can't match.

But culture also means knowing when to evolve. The transition to public company required professional management, formal processes, and institutional governance. The family retained influence but brought in professionals. It's controlled evolution, not revolution.

Lesson 9: Capital Structure Is Competitive Advantage

Its debt-to-equity ratio fell to 0.13 times in FY25, showing a stronger balance sheet than peers. This conservative leverage isn't timidity—it's strategy. When opportunities arise—like the BSNL contract or BESS facility—Pace can move quickly without lengthy negotiations with lenders. In infrastructure, speed to deploy capital often matters more than cost of capital.

Lesson 10: Build Platforms, Not Just Projects

Every tower Pace maintains, every battery they deploy, every fiber they lay is a node in a platform. The data from these assets—performance metrics, failure patterns, usage trends—creates insights competitors without operational assets can't access. Pace is transitioning from selling products and services to selling outcomes—uptime, reliability, efficiency.

The playbook continues evolving. As India's infrastructure needs change, so does Pace's strategy. But the core lessons remain: patient capital, strategic timing, operational excellence, and most importantly, solving real problems for customers who matter. It's not complicated, but execution at scale is extraordinarily difficult. That difficulty is itself the moat.

XI. Analysis: Bull vs. Bear Case

The investment committee room is divided. On one side, bulls see Pace Digitek as India's next infrastructure champion, trading at valuations that will seem quaint in five years. On the other, bears see concentrated risks and execution challenges that could derail the story. Both sides have compelling arguments.

The Bull Case: Riding Three Megatrends Simultaneously

The bulls start with market timing. India's infrastructure spending is not just growing—it's exploding. The 5G rollout alone requires $20-30 billion in infrastructure investment. Fiber penetration, currently at 35%, needs to reach 70% for Digital India goals. Passive Telecom Infrastructure market size in India is estimated at ₹ 1.6 lakh crore – 1.7 lakh crore (cumulative) Between Fiscals 2020-2024 and is projected to increase moving forward to ~₹ 2 lakh crore -2.1 lakh crore between fiscal 2023- 2028. Additionally, the optical fibre EPC industry which was estimated at ~ ₹ 8.4 lakh crore as of Fiscal 2024, is expected to grow to ₹ 13.5-14 lakh crore by Fiscal 2028.

The energy transition multiplies the opportunity. India's battery storage demand is projected to reach 236 GWh by 2032. At $150 per kWh, that's a $35 billion market. Pace's 5 GWh facility positions them to capture 10-15% market share in a winner-take-most dynamic where scale, local manufacturing, and government relationships matter more than technology.

Financial performance validates the strategy. Its EBITDA margin at 20.7% is higher than competitors. This isn't just operational efficiency—it's pricing power from integrated solutions. When competitors quote telecom projects, they mark up third-party equipment. Pace manufactures internally, captures those margins, and still wins on price.

The order book provides unusual visibility. ₹7,633 crore worth of confirmed projects in hand (more than 3x its annual revenue). In infrastructure, order books can be misleading—projects get delayed, cancelled, or repriced. But Pace's book is 100% government contracts that, while slow-paying, rarely cancel. This is three years of revenue already locked in.

Valuation remains compelling despite the stock's run. At 17x P/E, Pace trades at a discount to manufacturing companies with similar growth rates and a fraction of the order book visibility. Comparable renewable energy players trade at 25-35x. As the market recognizes Pace's transformation from telecom to energy infrastructure, multiple expansion seems inevitable.

The platform transformation is underestimated. Markets value Pace as a project execution company. But they're becoming a data-driven infrastructure platform. Every battery deployed is a trading node in future energy markets. Every tower maintained provides network optimization data. The recurring revenue potential from software and services could eventually exceed traditional project revenue.

Management execution has been flawless through multiple transitions. They navigated demonetization, GST, COVID, and hypergrowth without missing targets. The backward integration was executed perfectly. The IPO was timed well. This isn't a management team that stumbles.

The Bear Case: Concentration Risks and Execution Challenges

The bears start with customer concentration. 96% revenue comes from just 10 clients; losing even one can hurt results sharply. Worse, these are government clients whose procurement decisions can change with political winds. One policy shift, one budget cut, one bureaucratic delay could crater revenues.

The PSU dependency is particularly concerning. Government contracts mean 276-day receivables, compressed margins from competitive bidding, and payment uncertainty. Private sector telecom operators pay better and faster, but Pace has limited exposure. As government fiscal situations tighten, payment delays could extend further.

Execution risks are multiplying. Managing ₹500 crore revenue is different from ₹2,500 crore, which is different from the ₹5,000+ crore Pace targets. Each scale requires new systems, processes, and people. The infrastructure industry is littered with companies that grew too fast and collapsed under execution failures.

Competition is intensifying everywhere. In telecom infrastructure, Chinese companies offer 30% lower prices. In energy storage, global giants like Tesla and Fluence have better technology and deeper pockets. In services, thousands of small contractors provide local competition. Pace's integrated model is powerful but also makes them vulnerable to specialized competitors in each vertical.

Technology disruption looms. Pace is betting billions on lithium-ion batteries just as sodium-ion and solid-state alternatives emerge. They're building fiber infrastructure as satellite internet proliferates. They're installing 5G equipment as 6G research accelerates. In technology-driven infrastructure, today's assets can become tomorrow's stranded costs.

Working capital requirements could strangle growth. At 276 days receivables and growing revenues, Pace needs hundreds of crores in working capital annually. Banks have been supportive, but credit markets can turn quickly. One liquidity crisis could force Pace to slow growth or accept expensive financing.

The BESS bet might be premature. India's energy storage market is nascent, regulations are unclear, and utility procurement is slow. Pace has built 5 GWh capacity, but demand might take years to materialize. Meanwhile, Chinese manufacturers with 50 GWh facilities have massive scale advantages.

Regulatory risks are underappreciated. Telecom infrastructure regulations change frequently. Energy storage regulations don't really exist yet. Environmental clearances are becoming stricter. One adverse regulatory change could impact multiple business lines simultaneously.

The family-run structure, despite professional management, creates governance concerns. Promoter Holding: 69.5%. While the family has been excellent stewards, minority shareholders have limited influence. Related-party transactions, though disclosed, remain substantial.

The Verdict: Asymmetric Risk-Reward

Both cases have merit, but the risk-reward appears asymmetric. The bull case requires continued execution and market growth—both likely given track records. The bear case requires multiple failures or black swan events—possible but less probable.

The key insight: Pace isn't a pure play on anything, which is both weakness and strength. Telecom struggles? Energy compensates. Energy delays? Services provide cushion. This diversification within related verticals provides resilience that focused competitors lack.

For investors, the decision comes down to time horizon and risk tolerance. Short-term traders should beware—the stock will remain volatile as markets struggle to categorize it. Long-term investors might see opportunity—infrastructure businesses that successfully navigate technology transitions often compound wealth for decades.

The truth likely lies between extremes. Pace will probably face execution challenges, experience customer losses, and navigate technology disruptions. They'll also likely capture meaningful share of India's infrastructure boom, successfully transition to energy storage, and generate substantial cash flows. The question isn't whether challenges will arise, but whether management's two-decade track record of navigating them will continue.

XII. Epilogue & Looking Forward

As the sun sets over the Bidadi facility, casting long shadows across rows of battery containers that will soon store energy for millions of Indians, it's worth reflecting on the journey that brought Pace Digitek here. From a small workshop in 2003 to a ₹4,700 crore public company with infrastructure spanning continents, the transformation has been remarkable. But in many ways, the story is just beginning.

India stands at an infrastructure inflection point unprecedented in its history. The convergence of digital transformation and energy transition creates opportunities measured not in billions but trillions of rupees. 5G networks need 10x the infrastructure density of 4G. Electric vehicles require charging networks that don't exist. Renewable energy needs storage at a scale never before attempted. Smart cities need intelligent infrastructure that hasn't been invented. In each of these transformations, companies like Pace Digitek will play crucial roles.

The near-term milestones are clear. The BESS facility needs to ramp to full utilization, proving Pace can compete in energy storage. The ₹7,633 crore order book needs to be executed flawlessly, demonstrating scale capabilities. Working capital cycles need to be managed as revenues potentially double again. International expansion, particularly in Africa and Southeast Asia, needs acceleration as these markets follow India's infrastructure trajectory.

But the longer-term vision is more ambitious. "I firmly believe that through this facility, PACE Digitek will not be not just building batteries, it will be building India's energy future. It will be creating high-value jobs, nurturing innovation, and strengthening our domestic manufacturing ecosystem in line with Modi ji's vision of Aatmanirbhar Bharat," said the Minister. This isn't just political rhetoric—it's a genuine opportunity to build national champions in critical infrastructure.

The strategic options are multiplying. Pace could acquire distressed assets as infrastructure markets consolidate. They could expand into adjacent areas like EV charging infrastructure or data center power management. They could develop software platforms that optimize infrastructure performance across industries. They could even become an infrastructure investor, owning and operating assets rather than just building them.

The challenges ahead are equally substantial. Managing hypergrowth while maintaining quality is extraordinarily difficult. Competing with global giants requires constant innovation and capital investment. Navigating India's complex regulatory environment demands patience and relationships. Transitioning from family-run to institutionally-governed while maintaining entrepreneurial culture is a delicate balance few achieve.

Yet several factors suggest Pace is well-positioned for the challenges ahead. First, their track record of navigating transitions—from 2G to 3G to 4G to 5G, from products to services to solutions—demonstrates adaptability. Second, their conservative balance sheet provides flexibility to invest counter-cyclically. Third, their deep customer relationships create a revenue floor that enables calculated risks.

The broader implications extend beyond Pace Digitek. India needs dozens of companies like Pace to achieve its infrastructure ambitions. The playbook they've written—patient capital, strategic acquisitions, backward integration, platform building—could be replicated across industries. Their success proves that Indian companies can compete globally in complex infrastructure, not through labor arbitrage or cost advantage, but through innovation and execution.

For investors, Pace represents a fascinating case study in transformation. The company that listed at ₹225 isn't the same one that incorporated in 2007, or even the one that exploded in growth in 2024. It's constantly evolving, adapting to market needs while building on core strengths. This isn't a company you buy and forget—it's one you watch and learn from.

The lessons for entrepreneurs are even more valuable. Pace's journey shows that building infrastructure businesses requires different skills than building software companies. Patient capital matters more than rapid scaling. Relationships matter more than technology. Execution matters more than strategy. Most importantly, solving real problems for real customers matters more than everything else.

As India marches toward its destiny as a $10 trillion economy, infrastructure will be both enabler and beneficiary. Roads, ports, and airports get the attention, but digital and energy infrastructure—Pace's domains—might matter more. Every video streamed, every call made, every kilowatt stored contributes to economic growth. The companies building this invisible infrastructure are building India's future.

The story of Pace Digitek is far from over. The next chapters will be written in 5G towers across rural India, in battery farms storing renewable energy, in fiber cables connecting the last unconnected villages. They'll be written in board rooms where strategic decisions shape decades, in factories where innovation meets manufacturing, in field sites where execution meets ambition.

What makes Pace's story particularly relevant isn't its uniqueness but its replicability. India needs not one but hundreds of Pace Digiteks—companies that can bridge the gap between ambition and execution, between government policy and ground reality, between global technology and local needs. The infrastructure boom isn't just an investment opportunity; it's nation-building in real-time.

Twenty years from now, when India's infrastructure rivals any developed nation, when renewable energy powers prosperity, when digital connectivity enables opportunities in every village, few will remember the companies that built it all. Pace Digitek might be forgotten by consumers, but their handiwork will be everywhere—invisible but essential, unglamorous but fundamental.

That, perhaps, is the ultimate validation for an infrastructure company: to be so successful that your work becomes invisible, so essential that it's taken for granted. Pace Digitek isn't there yet, but the trajectory is clear. From a small Bengaluru workshop to India's infrastructure backbone, from power systems to energy storage, from family enterprise to public company—the transformation continues.

The sun has set over Bidadi, but for Pace Digitek, it's still early morning. The best chapters of this infrastructure story are yet to be written.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube