Nuvama Wealth Management: The Demerger That Created India's Wealth Giant

I. Introduction & Episode Setup

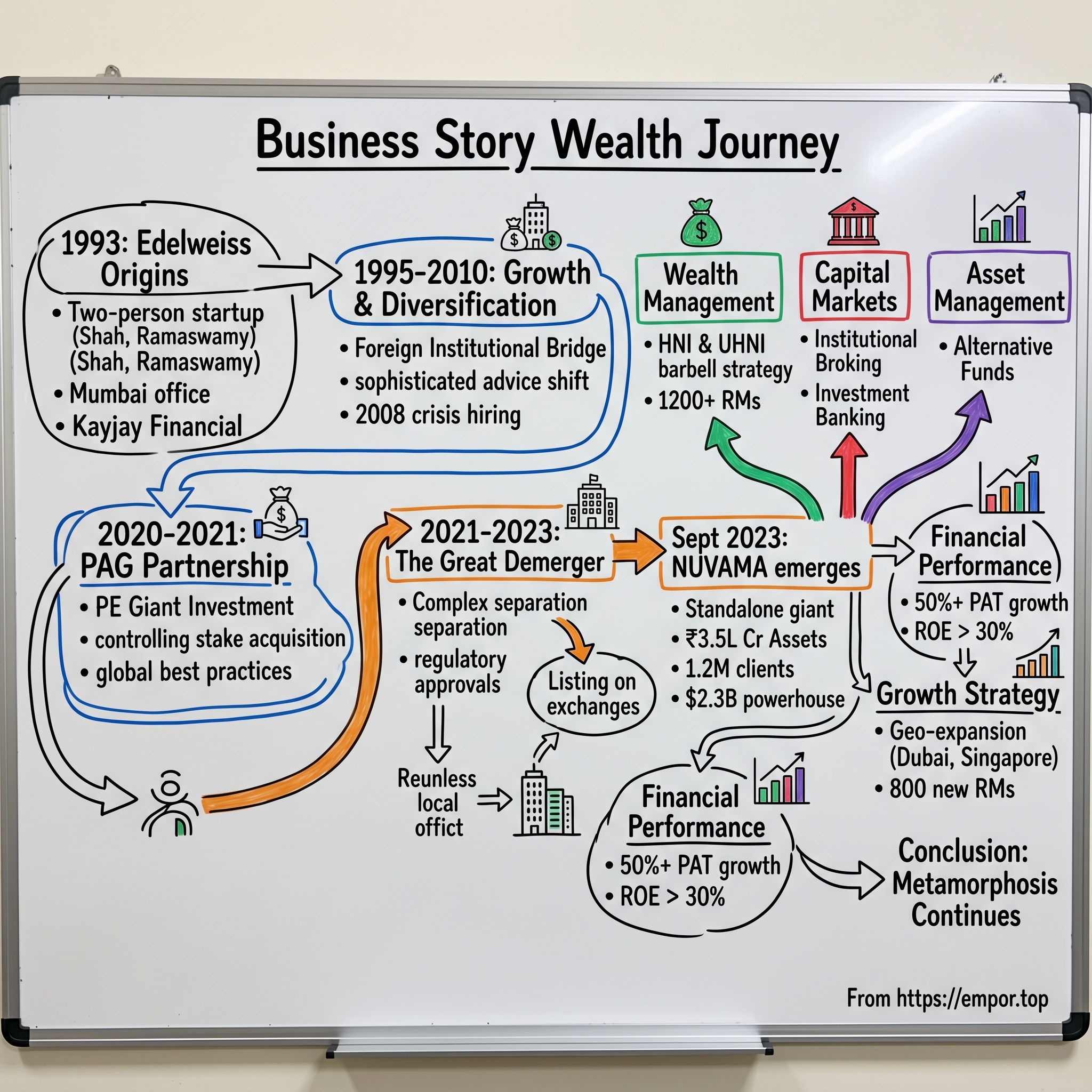

Picture this: September 2023, the trading floor at the National Stock Exchange erupts as a new ticker appears—NUVAMA. The stock opens at ₹1,925, a 25% premium to its issue price. In that moment, what was once a division buried inside a conglomerate becomes a $2.3 billion standalone wealth management powerhouse. But this isn't just another IPO story. This is the tale of how a Hong Kong private equity giant engineered one of India's most complex financial demergers, transforming Edelweiss's wealth arm into Nuvama—now India's second-largest wealth manager.

The numbers tell a remarkable story: ₹3.5 lakh crore in client assets, 1.2 million affluent clients, 3,600 ultra-wealthy families trusting them with generational wealth. In just 18 months since its rebrand from Edelweiss Securities to Nuvama, the firm has seen its market value quadruple from PAG's initial investment valuation. Yet behind these numbers lies a three-decade journey of building, breaking apart, and rebuilding—a masterclass in financial engineering that would make any Wall Street banker envious.

What makes Nuvama fascinating isn't just its scale—it's the audacity of the transformation. How does a wealth management unit convince its parent company to let it go? How does a Hong Kong PE firm navigate India's labyrinthine regulations to pull off a demerger? And perhaps most intriguingly, why would Rashesh Shah, who spent 30 years building Edelweiss, willingly reduce his stake to just 4% in what became his most valuable creation?

This is that story—from a two-person startup in 1993 Mumbai to today's wealth management giant. It's a journey through India's financial liberalization, the rise of its millionaire class, and the strategic chess moves that created one of Asia's most valuable wealth platforms. Along the way, we'll decode PAG's playbook, understand why "Nuvama" replaced a three-decade-old brand, and explore whether this demerger model could reshape how Indian conglomerates unlock value.

The roadmap ahead takes us from Edelweiss's scrappy origins in post-liberalization India, through the game-changing PAG acquisition, the complex demerger mechanics, and finally to Nuvama's ambitious future. Each phase reveals lessons about timing, strategy, and the art of financial transformation. Because in the end, Nuvama isn't just about managing wealth—it's about how wealth management itself got reimagined in India.

II. The Edelweiss Foundation: Building India's Financial Powerhouse (1993–2020)

The year was 1993. India had just opened its economy to the world, dismantling the License Raj that had throttled entrepreneurship for decades. In a modest Mumbai office, two young men—Rashesh Shah, fresh from his Harvard MBA, and Venkatchalam Ramaswamy, a chartered accountant with a quiet intensity—sat discussing an audacious idea. They wanted to democratize finance in a country where stock markets were still seen as gambling dens and wealth management meant gold under the mattress.

They called their venture Kayjay Financial Research Services, a deliberately forgettable name for what would become unforgettable ambition. Shah, then just 29, had turned down lucrative Wall Street offers to return to India. His reasoning? "The Indian capital markets were like America in the 1920s—everything was about to change." Ramaswamy, his senior by a few years, brought the operational discipline. Together, they had ₹50 lakhs in seed capital and a vision that seemed almost naive: build a financial services firm that could rival the foreign banks flooding into India.

The early years were brutal. Their first office was a 400-square-foot space in Nariman Point, Mumbai's financial district, where the rent consumed half their monthly burn. They started with research services, producing equity reports that nobody wanted to buy. Indian institutions preferred the glossy research from Morgan Stanley or Goldman Sachs. Foreign investors didn't know they existed. For eighteen months, they survived on consulting assignments and small broking deals, often wondering if they'd made a terrible mistake.

The breakthrough came through an unexpected door. In 1995, they noticed that foreign institutional investors (FIIs) entering India needed someone who understood both global standards and local nuances. Kayjay positioned itself as the bridge—offering research with international quality but Indian insight. Their first major FII client was a small Dutch pension fund. Within a year, they were servicing twelve international clients. Revenue jumped from ₹2 crores to ₹15 crores.

But Shah and Ramaswamy weren't satisfied with just research and broking. They saw a bigger opportunity emerging: India's wealthy were evolving. The old money—industrialist families who kept wealth in real estate and gold—was being joined by new money: tech entrepreneurs, senior executives with stock options, professionals earning globally competitive salaries. These people needed sophisticated financial advice, not just a stockbroker.

The transformation accelerated through strategic name changes that reflected growing ambition. Kayjay became KJS Securities in 1996, then Rooshnil Securities in 1999, each rebrand marking an expansion in capabilities. By 2004, they made the decisive move: Edelweiss Securities. The name, inspired by the resilient Alpine flower that blooms in harsh conditions, captured their philosophy—thriving where others couldn't.

Building the wealth management vertical within Edelweiss wasn't straightforward. The Indian wealthy were skeptical of financial advisors. "Why should I pay someone to manage my money when I can call my broker directly?" was the common refrain. Edelweiss's answer was to offer what brokers couldn't: holistic financial planning, estate planning expertise, access to international markets, and most importantly, the promise of confidentiality in a country where everyone knew everyone's business.

The 2008 financial crisis became an unexpected catalyst. While global banks retreated from India, laying off relationship managers and closing offices, Edelweiss went on a hiring spree. They recruited top talent from Merrill Lynch, Citibank, and HSBC at fraction of their previous salaries. One senior banker recalled: "Rashesh called me personally and said, 'This crisis won't last forever. When it ends, we'll own the market.'" By 2010, Edelweiss had 150 wealth managers, up from 30 in 2007.

The institutional broking business grew in parallel, becoming the cash engine that funded wealth management expansion. Edelweiss pioneered the "high-touch" model in India—combining deep research with intensive client engagement. They organized 200+ company meetings annually, flew CEOs to meet investors in Singapore and London, and produced thematic research that went beyond individual stocks. By 2015, they were ranked among the top three institutional brokers in India.

But success brought complexity. Edelweiss had become a financial conglomerate—wealth management, institutional broking, investment banking, asset management, housing finance, retail broking. Each vertical had different economics, different regulations, different talent needs. The wealth management unit, generating the highest returns on capital, was getting lost in the noise. Investors valued Edelweiss like a lending company, ignoring the crown jewel within.

The landscape was shifting too. Global players like UBS and Credit Suisse were ramping up their India wealth operations. Domestic competitors like Kotak and IIFL were raising massive capital. The ultra-wealthy were becoming more sophisticated, demanding capabilities Edelweiss couldn't build organically—international estate planning, art advisory, family office services. Something had to change.

By early 2020, as Shah looked at his creation, he faced a founder's dilemma. Edelweiss had grown to ₹80,000 crores in assets, 10,000 employees, presence in 450 cities. But the market valued it at just ₹3,000 crores—less than the sum of its parts. The wealth management business alone, generating ₹800 crores in revenue, should have been worth more than the entire conglomerate. The question wasn't whether to unlock value, but how. The answer would come from an unexpected place: Hong Kong.

III. The PAG Partnership: Private Equity Meets Indian Wealth (2020–2021)

The phone rang at 2 AM Hong Kong time. Weijian Shan, Chairman of PAG and the man who'd overseen $40 billion in Asian investments, was used to late-night calls. But this one from Mumbai was different. "The deal structure needs to change," Rashesh Shah's voice came through, steady but firm. It was August 2020, COVID had frozen global markets, and what started as a straightforward acquisition was morphing into something far more complex.

Six months earlier, PAG's India team had pitched Shan on what seemed like a no-brainer: acquire majority stake in Edelweiss Wealth Management for ~US$325 million. The math was compelling—India's wealth management industry was exploding, growing at 11% annually, and Edelweiss had built something special. They were servicing over 2,400 of India's wealthiest families as well as ~670,000 affluent individuals, with customer assets under advice growing at 43% CAGR from just US$2.5 billion in 2015 to US$20 billion.

But PAG wasn't just any investor. As Asia's largest alternative investment firm, they'd seen this movie before—in China, Korea, Japan. Wealth creation follows a predictable pattern: economic liberalization creates entrepreneurs, entrepreneurs create wealth, wealth needs management. India was tracking China's trajectory with a 15-year lag. If they were right, this wasn't a $325 million opportunity; it was a multi-billion dollar platform play.

The original deal announced in August 2020 was simpler: PAG would acquire 51% stake for about INR22bn ($300m). But between announcement and closing, complications emerged. PAG needed to acquire the entire ownership of prior investors Kora Management and Sanaka Capital—two earlier backers who'd helped Edelweiss scale but now needed an exit. The negotiations turned Byzantine. Kora, a US hedge fund, wanted dollar payments. Sanaka, an Indian PE firm, had regulatory constraints. PAG had to structure separate deals for each while maintaining the overall valuation logic.

By March 2021, when the dust settled, PAG owned 61.5% through a combination of primary and secondary shares purchases for Rs 2,366 crore ($326 million), while Edelweiss Group retained 38.5% with an option to increase to 44%. The extra 10.5% stake wasn't planned—it emerged from the Kora-Sanaka buyout mathematics and PAG's insistence on clear control.

Nikhil Srivastava, PAG's India head and the architect of the deal, had spent months shuttling between Hong Kong and Mumbai, navigating not just financial negotiations but cultural ones. PAG's investment committee, dominated by Greater China veterans, initially struggled to understand India's relationship-driven wealth management model. In China, wealth management was increasingly digital, algorithm-driven. In India, ultra-wealthy families still expected their relationship manager at their daughter's wedding.

"We're not buying a business, we're buying a transformation opportunity," Srivastava argued in PAG's Hong Kong boardroom. His pitch was elegant: keep the Indian management, inject global best practices, accelerate technology adoption, then exit through a public listing—a playbook PAG had executed successfully across Asia.

The strategic logic went deeper than just India's wealth explosion. PAG expected to invest more than US$1 billion in India over the next two to three years. Edelweiss Wealth would be their platform—providing deal flow, market intelligence, and relationships with India's business elite. Every ultra-wealthy family managed by Edelweiss was a potential LP for PAG's funds or a target for their private equity deals.

But the real coup was the structure PAG negotiated for the eventual exit. The partnership agreement included plans to list the wealth management company to let both Edelweiss and PAG unlock value. This wasn't just an acquisition; it was a value creation journey with a predetermined destination—public markets.

The cultural integration proved fascinating. PAG brought discipline that bordered on obsession. Weekly dashboards tracking 47 KPIs. Monthly reviews with Hong Kong. Quarterly strategy sessions that ran for three days. Edelweiss executives, used to Shah's more entrepreneurial style, initially chafed. "They wanted to measure everything—average revenue per relationship manager per month, client acquisition cost by segment, even the average time taken to onboard an ultra-HNI client," one senior executive recalled.

Yet PAG was smart enough not to break what worked. They retained the entire senior management, including CEO Nitin Jain, who'd built the wealth franchise. They kept the relationship manager compensation structure, understanding that in Indian wealth management, talent walked out the door every evening. Most importantly, they accelerated investments in areas Edelweiss couldn't afford alone—international operations, alternative investments, technology platforms.

The rebranding question emerged almost immediately. PAG's view was clear: Edelweiss was associated with the parent conglomerate's lending business, which had faced stress during the NBFC crisis. A fresh identity would signal the new beginning. But what to call it? The naming exercise took six months, involving brand consultants from London, customer surveys across six cities, and trademark searches in 15 countries.

By early 2022, as markets recovered and the demerger planning began, PAG's bet was already paying off. The business that they'd valued at roughly $530 million in 2021 was generating profits that justified double that valuation. More importantly, they'd created a template that other PE firms would study for years—how to carve out a crown jewel from a conglomerate, transform it with global best practices, and prepare it for public markets.

The partnership marked a watershed for Indian financial services. For the first time, a global PE giant had taken control of a major Indian wealth manager, signaling that India's wealth management industry had come of age. The message to global investors was clear: India wasn't just about tech unicorns anymore. The real money was in managing the wealth those unicorns created.

IV. The Great Demerger: Engineering Financial Independence (2021–2023)

The boardroom at Edelweiss's Mumbai headquarters had never seen negotiations quite like this. It was April 2022, and lawyers from three jurisdictions—India, Hong Kong, and Singapore—were huddled over a 300-page demerger scheme document. At stake was one of the most complex financial restructurings in Indian corporate history. The challenge wasn't just separating a business; it was surgically extracting a beating heart from a living organism without killing either.

"We need to ensure zero business disruption," PAG's representative insisted, pointing to a clause about client relationships. Across the table, Rashesh Shah's expression was unreadable. He'd built Edelweiss over three decades, and now he was dismantling it—voluntarily. The irony wasn't lost on anyone. Most founders fight tooth and nail against losing control. Shah was engineering his own dilution.

The demerger journey had actually begun immediately after PAG's investment closed in March 2021. In April 2021, ESL, Edelweiss Global Wealth Management Limited and Edelweiss Securities and Investments Private Limited announced a composite scheme of arrangement that would eventually separate the wealth management business from the parent conglomerate. But what looked straightforward on paper became a masterclass in corporate gymnastics.

The restructuring involved multiple steps that would make a chess grandmaster dizzy. First, Edelweiss Global Wealth Management Limited bought circa 50.55% equity interest of ESL through primary & secondary transactions. This acquisition was funded by PAG which subscribed to the compulsorily convertible debentures. As a result, EFSL ceased to be holding company of Edelweiss Global Wealth Management Limited and PAG became the holding company.

But that was just the opening move. The real complexity lay in ensuring that when the music stopped, everyone was sitting in the right chair. PAG needed clear control, Edelweiss shareholders needed to receive their proportionate shares in the new entity, and regulatory requirements had to be met across banking, securities, and corporate law.

The naming decision—from Edelweiss Securities to Nuvama—happened in parallel with the demerger planning. Focus groups in Mumbai, Delhi, and Bangalore revealed something unexpected: while institutional clients valued the Edelweiss brand, retail wealthy clients often confused it with the parent's lending business. "Nuvama," derived from Sanskrit meaning "new" and "wealth," tested well across demographics. It suggested fresh beginnings without abandoning Indian roots.

The mathematics of the demerger were precise: Nuvama would allot 1,05,28,746 equity shares of the face value of Rs. 10 each to the shareholders of Edelweiss Financial Services on proportionate basis as a consideration for demerger. After listing, the shareholders of Edelweiss Financial Services would hold 30 per cent of the paid‐share capital of Nuvama Wealth Management.

Technology separation proved nightmarish. Edelweiss had built integrated systems over decades—client databases, risk management platforms, trading systems all interconnected like neural networks. Separating them meant not just copying data but recreating entire workflows. A team of 200 IT professionals worked for 18 months, creating parallel systems that would activate the moment of demerger.

The human element was equally complex. Employees had Edelweiss stock options, retirement benefits tied to the parent, even email addresses that needed changing. Each relationship manager managed clients who might have relationships across Edelweiss entities—wealth management, insurance, lending. These had to be cleanly separated without confusing clients or violating confidentiality.

February 27, 2023, marked a crucial milestone when Edelweiss Financial Services (EFSL) secured approval from the shareholders for the planned demerger of its wealth management operations. The vote was overwhelming—over 99% in favor. Even minority shareholders understood the value unlock potential.

The effective date of the scheme as notified to the exchanges was May 18. This paved the way for the listing of Nuvama Wealth Management. June 2, 2023, became the record date for determining eligible shareholders who would receive Nuvama shares.

The regulatory approvals alone required navigation through multiple authorities. SEBI for securities regulations, RBI for banking relationships, NCLT for the scheme approval, and stock exchanges for listing permissions. Each had different requirements, timelines, and concerns. The NCLT hearings saw intense scrutiny about minority shareholder protection and valuation fairness.

Behind the scenes, PAG was orchestrating a parallel transformation. They brought in McKinsey to redesign organizational structure, Accenture for technology architecture, and EY for process reengineering. The mandate was clear: prepare Nuvama to operate as a listed entity from day one. This meant board committees, quarterly reporting capabilities, investor relations functions—infrastructure that Edelweiss had at group level but Nuvama needed independently.

September 26, 2023, arrived with Mumbai's equity markets buzzing with anticipation. Shares of Nuvama Wealth Management were listed at the bourses and dealing in the stock began from Rs 2,750 on the National Stock Exchange (NSE), while the stock was admitted for trading on BSE at Rs 2699. The premium listing vindicated the demerger strategy—the market was valuing Nuvama as a pure-play wealth manager, not as part of a conglomerate.

The post-listing ownership structure revealed the culmination of three years of financial engineering: PAG owns a controlling stake of 56 per cent in Nuvama Wealth. Rashesh Shah held a 4 per cent stake, while Venkatchalam Ramaswamy owned 1.79 per cent in Nuvama Wealth. The founders who'd started with 100% ownership in 1993 now held less than 6% combined—a deliberate choice to unlock value rather than maintain control.

The demerger had achieved something remarkable: it created approximately ₹15,000 crores in market value where none existed before. Edelweiss Financial Services, freed from the capital-intensive wealth business, could focus on credit and insurance. Nuvama, unshackled from the conglomerate structure, could compete directly with global wealth managers.

The execution set a template for Indian conglomerates looking to unlock value. Unlike forced separations during financial distress, this was strategic surgery—planned, precise, and profitable for all stakeholders. It proved that sometimes, the best way to grow is to divide.

V. Business Model Deep Dive: Three Pillars of Growth

Inside Nuvama's war room in Mumbai's Bandra Kurla Complex, three television screens display different stories. The first shows wealth management metrics—₹2.5 lakh crore in client assets, growing steadily. The second tracks capital markets volumes—institutional trades worth thousands of crores executing in real-time. The third, smaller but watched most closely, displays asset management AUM—just crossing ₹10,000 crores. Three businesses, three trajectories, one integrated platform that's rewriting India's wealth management playbook.

The Wealth Management Engine: Where Relationships Meet Scale

Nuvama's wealth management business, generating 57% of revenue, delivered PAT of US $72 million in FY24, growing by 62% YoY. But these numbers mask a more nuanced story. Unlike traditional wealth managers who chase either mass affluent or ultra-wealthy, Nuvama operates a barbell strategy—two distinct brands serving different universes with different economics.

Nuvama Wealth targets the HNI and affluent segment—think successful doctors, mid-sized business owners, senior corporate executives. As of FY24, its AUM surged to 77,930 Cr, achieving a 33% CAGR over the last 4 years, with revenues growing at ~35% CAGR to 669 Cr. The magic here isn't just asset gathering; it's the product mix transformation. MPIS (Managed Products & Investment Solutions) forms 48% of revenues in FY24, shifting from transaction-dependent brokerage to recurring fee structures.

The relationship manager army tells the expansion story. The company heavily invested in the last 12 months to increase RMs by 337 and expand its network of external wealth managers by more than 2000, reaching more than 1,200 RMs and ~7000 EWMs covering 450+ locations. Each RM manages approximately ₹65 crores in assets—lower than competitors but deliberately so. Nuvama believes in depth over concentration, multiple touchpoints over single dependencies.

Nuvama Private, the ultra-HNI arm, operates on entirely different physics. Here, 3,600 families control assets that dwarf the affluent segment's volumes. ARR (Annual Recurring Revenue) earning assets continues to grow, with ARR revenues at 57% of total revenues. The business model shifts from products to solutions—estate planning that spans continents, art advisory for collectors, family office services that coordinate between Zurich banks and Mumbai real estate.

The technology backbone supporting this dual-brand strategy is where PAG's influence shows. Every relationship manager carries an AI-powered portfolio analyzer that processes 50+ risk parameters in real-time. Client onboarding, which took 15 days in the Edelweiss era, now completes in 48 hours through digital KYC and automated risk profiling. Yet the human touch remains paramount—RMs still attend client family events, still make house calls for portfolio reviews.

Capital Markets: The Volatility Play

Capital Markets generated US $97 million in FY24 revenue, growing by 64% YoY, with PBT of US $45 million, up 180% YoY. This isn't your typical broking business—it's an institutional powerhouse that combines multiple revenue streams into a symphony of financial engineering.

The institutional broking arm serves 300+ domestic and foreign institutional investors, executing daily volumes that regularly exceed ₹5,000 crores. But volume isn't the differentiator—it's the research. Nuvama produces 2,000+ research reports annually, covers 200+ companies, and hosts 150+ investor conferences. When a global fund wants to understand Indian consumption patterns or a domestic mutual fund needs insights on emerging sectors, Nuvama's research becomes the bridge.

Investment banking adds another layer. In FY24, they managed 15 IPOs, 8 QIPs, and numerous block deals. The synergy with wealth management is obvious—every IPO creates wealth for entrepreneurs who become wealth management clients; every block deal involves families that need estate planning.

Client Assets for Asset Services reached US $10.9 billion at end of Q4 FY24, growing by 109% YoY. This custody business, often overlooked, generates sticky revenues from foreign investors who need local custody for their Indian holdings. It's the plumbing of capital markets—unglamorous but essential and highly profitable.

The volatility of capital markets revenue—surging in bull markets, collapsing in bear ones—creates the earnings roller coaster that public markets struggle to value. Capital Markets business revenue grew by 153% YoY in Q1FY25 driven by heightened market activity. This feast-or-famine dynamic explains why Nuvama trades at lower multiples than pure-play wealth managers despite superior growth.

Asset Management: The Sleeping Giant

At just 4% of revenue, asset management seems like an afterthought. Revenues reached US $6 million in FY24, growing by 34% YoY, with AUM at US $0.8 billion, of which Public Markets AUM stood at US $0.3 billion, growing by 155% YoY. But this is where Nuvama's future ambitions lie.

Launched in 2021, the asset management business focuses on alternatives—private equity funds, real estate funds, structured credit. Public market funds AUM witnessed strong flows, grew by 155% YoY, crossing Rs 2,000 crore mark, while their commercial real estate fund with Cushman & Wakefield is on track. The strategy is deliberate: avoid competing with mutual funds in public markets, instead create products that only sophisticated investors can access.

The economics of asset management are compelling. Once you cross critical scale—typically ₹20,000 crores AUM—margins expand dramatically. Fixed costs get spread over larger asset base, performance fees kick in, and the business becomes a cash machine. Nuvama is betting that their wealth management relationships will accelerate this journey to scale.

The Integration Magic

What makes Nuvama's three-pillar model powerful isn't the individual businesses—it's how they interconnect. A startup founder taking their company public through Nuvama's investment banking becomes a private wealth client. That wealth gets deployed into Nuvama's alternative funds. The liquidity needs get serviced through capital markets. Each business feeds the others in an endless loop of value creation.

The mix of transactional and recurring revenues provides stability, with cost to income falling by ~5% to 48.7% in FY24. This operational leverage is key—as revenues grow, costs don't scale proportionally. Technology investments, compliance infrastructure, brand building benefit all three pillars simultaneously.

The geographic expansion adds another dimension. Nuvama received approval for a Dubai (DIFC) license, targeting the massive NRI wealth pool. These international operations will leverage all three pillars—NRIs need Indian market access (capital markets), India-focused funds (asset management), and wealth planning that spans jurisdictions (wealth management).

The risk lies in execution complexity. Running three distinct businesses with different regulations, different talent needs, different economic cycles requires managerial bandwidth that few possess. The 62% cost-to-income ratio, while improving, remains higher than focused competitors. The subscale asset management business drags overall returns.

Yet the strategic logic is compelling. In a market where pure-play business models face margin pressure from competition and technology, Nuvama's integrated platform creates moats that are hard to replicate. Each additional client in one business becomes a cross-selling opportunity for others. Each new product in asset management becomes a solution for wealth clients. Each capital markets transaction creates wealth that needs managing.

The numbers validate the strategy. Client assets stood at US $41.5 billion, growing by 50% YoY, while delivering revenues of US $247 million. The platform serves 1.2 million affluent clients and 3,600 ultra-wealthy families. This isn't just scale—it's an ecosystem where wealth creation, preservation, and deployment happen under one roof.

VI. The Numbers Story: Financial Performance & Metrics

The conference room on the 15th floor of Nuvama's Mumbai headquarters has a tradition. Every quarter, when results are announced, the leadership team plots two numbers on a whiteboard: reported profit and what they call "normalized profit"—adjusting for capital markets volatility. The gap between these numbers tells the real story of Nuvama's financial journey.

Q1 FY25 revenues stood at Rs 668 crore, grew by 60% YoY, while Operating Profit After Tax (PAT) reached Rs 221 crore, grew by 133% YoY. These headline numbers would make any investor salivate. But dig deeper, and the story becomes more nuanced—a tale of three businesses with wildly different growth trajectories converging into explosive profitability.

The journey from PAG's investment to today reads like a hockey stick. FY24 revenues of $247 million grew 31% YoY from $189 million in FY23, while PAT surged to $72 million, up 62% YoY from $44 million. But these aggregate numbers mask the underlying transformation. The cost-to-income ratio, which stood at 69% in FY23, compressed to 62% in FY24—still high by global standards but improving rapidly as scale benefits kick in.

The quarterly progression reveals acceleration. From Q4 FY23 to Q4 FY24, revenues jumped 35% while PAT soared 57%. Then Q1 FY25 delivered a knockout punch—revenues up 60% YoY, PAT up 133% YoY. This isn't just growth; it's operating leverage on steroids. Every incremental rupee of revenue is dropping more to the bottom line as fixed costs get spread over a larger base.

The AUM Story: Scale Begets Scale

Client assets tell the platform story. Client assets stood at Rs 3.5 trillion, growing by 50% YoY, but the composition matters more than the headline. Wealth management client assets of ₹2,74,124 Cr grew 35% YoY, while capital markets' asset services exploded—₹1,07,225 Cr at end of Q1 FY25, up 115% YoY.

The velocity of asset gathering accelerated post-listing. In just the first quarter of FY25, Nuvama added more AUM than in entire quarters during the Edelweiss era. This isn't just market appreciation—net new money (NNM) contributed 75% of MPIS asset growth and 89% of ARR asset growth. Clients are voting with their wallets.

Revenue Mix Evolution: The Recurring Revenue Dream

The shift from transactional to recurring revenues represents Nuvama's holy grail. In FY23, transaction-based revenues (brokerage, investment banking fees) dominated at 55% of total. By FY24, this flipped—ARR-based assets now generate 45% of revenues, heading toward 50% by FY26.

This matters because recurring revenues are predictable, higher-margin, and valued more richly by markets. A relationship manager selling a mutual fund earns one-time commission. The same RM getting a client into a discretionary portfolio management service earns fees for years. The lifetime value of the latter is 5-10x higher.

Wealth and Asset Management businesses continued to witness secular growth with Q1FY25 revenues growing 18% YoY, while Capital Markets business revenue grew by 153% YoY driven by heightened market activity. This divergence highlights both opportunity and risk—wealth management provides stability, capital markets delivers growth spurts.

Margin Expansion: The Operating Leverage Story

The real magic happens at the operating profit line. Nuvama showed an improvement in its operating profit margin, with the highest margin of 53.60% in the last five quarters. This margin expansion comes from three sources:

First, technology investments are paying off. The AI-powered portfolio analyzer means each RM can handle more clients without proportional cost increases. Digital onboarding reduces operational staff needs. Automated rebalancing cuts manual intervention.

Second, the business mix is improving. Higher-margin products like discretionary portfolio management and alternative investments are growing faster than plain-vanilla broking. MPIS assets stood at ₹24,960 Cr, grew by 33% YoY, while these products command fees of 1-2% versus 0.1-0.3% for execution-only broking.

Third, scale economics are kicking in. Compliance costs, technology infrastructure, brand building—these don't scale linearly with revenue. In Asset Management, AUM grew by 30% YoY but the cost base grew much slower, driving margin expansion.

Capital Efficiency: The ROE Inflection

ROE rising from 23.6% to 31.5% signals capital efficiency improvements. Wealth management is fundamentally capital-light—you're earning fees on client assets, not deploying your own capital. As the business mix shifts from capital-intensive lending to fee-based advisory, ROE naturally expands.

The balance sheet reflects this transformation. Unlike the Edelweiss era when significant capital was tied up in lending and proprietary trading, Nuvama's capital is primarily regulatory—maintaining net worth requirements for licenses. This means almost all profits can be distributed or reinvested for growth, not trapped in working capital.

The Valuation Puzzle

Despite spectacular growth, Nuvama trades at interesting multiples. Market Cap of 24,965 Crore with Revenue of 4,158 Cr and Profit of 985 Cr implies a P/E of roughly 25x and Price-to-Sales of 6x. Compare this to global wealth managers trading at 30-40x earnings and the discount becomes apparent.

The market's caution stems from three concerns. First, promoters have pledged or encumbered 62.8% of their holding—unusual for a financial services firm and creating overhang fears. Second, the high exposure to volatile capital markets revenues makes earnings unpredictable. Third, PAG's eventual exit creates uncertainty about future ownership.

Cash Flow Dynamics: The Hidden Challenge

Cash flow from operations stood at Rs -1,723 m in FY24 as compared to Rs -2,705 m in FY23. Negative operating cash flow in a profitable business seems contradictory, but reflects the growth investments—working capital for the lending book, margin funding for clients, and regulatory deposits for new licenses.

This will reverse as the business matures. Wealth management typically generates cash equal to 80-90% of profits once growth stabilizes. But for now, Nuvama is choosing growth over cash generation—a rational trade-off given the market opportunity.

Forward Trajectory: The Next Three Years

Management's targets are ambitious but achievable. They're guiding for 20-25% revenue CAGR through FY27, driven by wealth management growing at 25-30%, capital markets at 15-20%, and asset management potentially doubling from a small base.

More importantly, they expect margins to expand 200-300 basis points as operating leverage kicks in. If achieved, this would mean FY27 PAT of ₹2,000+ crores—nearly double FY24 levels. At current valuations, this implies significant upside, assuming multiple expansion as the business model proves itself.

The quarterly volatility will continue—Q2 might see moderation if markets correct, Q3 could surprise positively if IPO activity picks up. But the long-term trajectory is clear: a business generating more recurring revenues, expanding margins through scale, and compounding capital at 30%+ ROEs.

The numbers tell a transformation story. From a subscale division generating single-digit margins to a standalone platform delivering 50%+ operating margins. From volatile transaction revenues to predictable recurring fees. From capital-intensive lending to capital-light advisory. The financial metamorphosis of Nuvama isn't complete, but the direction is unmistakable.

VII. Competition & Market Position

The war for India's wealthy has battlegrounds in South Mumbai's heritage buildings, Gurgaon's glass towers, and Bangalore's tech parks. In conference rooms where billion-dollar portfolios get discussed over cutting chai, four names dominate: 360 ONE (formerly IIFL Wealth), Nuvama, Kotak Wealth, and the global giants like UBS and Credit Suisse. Each claims leadership, but the metrics tell a more nuanced story of a market so large that even the losers are winning.

As of March 2025, 360 ONE WAM had assets under management (AUM) of over ₹5.81 lakh crore (US$68 billion) and had more than 7,500 clients, making it the undisputed leader by AUM. But size isn't everything. Nuvama, with its ₹3.5 lakh crore in client assets, generates comparable profitability through superior margins. The battle isn't just about gathering assets—it's about monetizing them effectively.

The Rebranding Wars

The timing is uncanny. In November 2022, the company rebranded as 360 ONE, renaming its wealth management division as 360 ONE Wealth and its asset management division as 360 ONE Asset. Less than a year later, Nuvama emerged from its Edelweiss chrysalis. Both understood the same truth: in wealth management, perception is reality. Old brands carried baggage—360 ONE from its IIFL lending history, Nuvama from Edelweiss's NBFC crisis associations.

The rebranding strategies reveal different philosophies. 360 ONE went aspirational—the name suggesting complete solutions, full-circle service. Nuvama chose Sanskrit roots, signaling Indian heritage with global ambitions. Both worked. 360 ONE's stock has delivered 36.75% CAGR over 5 years, while Nuvama's post-listing performance shows 50%+ gains.

Business Model Divergence

360 ONE · Mkt Cap: 42,172 Crore (up 0.12% in 1 year) · Revenue: 3,357 Cr · Profit: 1,056 Cr operates at higher scale but lower growth than Nuvama. Their wealth management focus is purer—they exited most capital markets businesses during the demerger from IIFL Holdings. This creates stability but limits cross-selling opportunities.

360 ONE serves ~7200 clients. It also has an HNI segment of Rs. 5 Crs - 25 Crs, focusing on the upper pyramid. Their average ticket size dwarfs Nuvama's, but the client base is narrower. It's the Hermès strategy—fewer clients, higher value, deeper relationships.

Nuvama's three-pillar model—wealth, capital markets, asset management—creates more volatility but higher growth potential. Revenue growth outpacing peers: 27% CAGR vs 360 ONE's 21% over recent years reflects this aggressive stance. The integrated model means losing money on one service to win the entire relationship—a luxury pure-plays can't afford.

The Ownership Overhang

Both companies share an uncomfortable similarity: Promoters have pledged or encumbered 89.6% of their holding at 360 ONE, while Nuvama shows 62.8% pledged. This creates perpetual exit speculation. In 2022, Bain Capital acquired nearly 25% of the company's shares in 360 ONE, while PAG controls Nuvama. Both financial sponsors will eventually exit, creating uncertainty that caps valuations.

The ownership structures reveal different endgames. 360 ONE's distributed ownership—Bain, General Atlantic, founders—suggests potential for management buyout or strategic sale. Nuvama's concentrated PAG ownership points toward another financial sponsor or strategic buyer. Markets hate uncertainty, explaining why both trade at discounts to global peers.

Geographic Expansion Race

In September 2023, it launched 360 ONE Global to provide wealth and investment advisory services to international clients, with offices in Dubai and Singapore. Nuvama received Dubai (DIFC) approval in July 2024. Both are chasing the same prize: $500 billion in NRI wealth that needs India exposure.

The international strategy differs subtly. 360 ONE focuses on NRIs wanting global diversification with an Indian partner. Nuvama targets NRIs seeking India-specific opportunities. One sells global products to Indians abroad; the other sells Indian products to Indians abroad. Both will likely succeed—the market is large enough.

Technology as Differentiator

While both claim digital leadership, execution varies. 360 ONE emphasizes client-facing technology—robo-advisory platforms, digital onboarding, mobile apps. Nuvama focuses on RM productivity—AI-powered portfolio analyzers, automated rebalancing, predictive analytics.

The technology spending reveals priorities. 360 ONE invests in client experience, believing wealthy Indians will eventually embrace digital wealth management like their Western counterparts. Nuvama invests in RM efficiency, betting that relationship managers will remain central but need better tools. Time will tell who's right—probably both.

Talent Wars and Compensation

The battle for relationship managers defines competition. Both companies are aggressively hiring—Nuvama adding 800 RMs over three years, 360 ONE matching pace. But the real competition is retention. Top RMs command packages exceeding ₹5 crores annually, with guaranteed bonuses and joining incentives that would make investment bankers blush.

The compensation structures reveal strategic differences. 360 ONE pays higher fixed salaries, reflecting its annuity-focused model. Nuvama's variable-heavy structure aligns with its transaction-dependent revenues. Both are trapped in an arms race where switching costs are low and client relationships are portable.

Market Positioning Evolution

Nuvama positions itself as the insurgent—aggressive, innovative, hungry. Second largest wealth management firm in India by revenue and profit, but with the ambition to be first. The messaging targets entrepreneurs and new money, promising sophistication without stuffiness.

360 ONE plays the establishment card—stable, trusted, proven. An investment and financial advisor to more than 12,000 influential families in the High Net Worth Individuals (HNI) and Ultra HNI segments in India and abroad, with aggregate assets of more than USD 20 billion under management. The positioning appeals to old money and family offices seeking preservation over growth.

Global Competition Intensifies

The domestic rivalry pales compared to global threats. UBS, post-Credit Suisse acquisition, has renewed India focus. Morgan Stanley and Goldman Sachs are building onshore capabilities. Singaporean banks like DBS are targeting Indian wealth from their home base.

Each global player brings unique advantages. Swiss banks offer confidentiality and global access. American banks provide sophisticated products and research. Asian banks understand regional wealth flows. Domestic players counter with relationships, local knowledge, and regulatory navigation expertise.

Consolidation Inevitability

The market structure—dozens of small players, four large domestic players, multiple global banks—isn't sustainable. Consolidation is coming. It also disclosed plans to acquire Batlivala & Karani Securities and Batlivala & Karani Finserv for ₹18.8 billion in 2025 shows 360 ONE's inorganic growth appetite.

Nuvama could be acquirer or acquired. Their integrated model makes bolt-on acquisitions complex but transformational deals possible. A merger with another wealth manager would create an undisputed leader. A sale to a global bank would provide international distribution. Either path seems more likely than status quo.

The Differentiation Challenge

Despite different positioning, offerings converge. Both offer discretionary portfolio management, alternative investments, estate planning, lending against securities. Both target the same ₹5-25 crore wealth segment. Both employ similar talent from the same pools. Differentiation is increasingly about execution, not strategy.

Client segmentation provides some separation. Nuvama's strength in entrepreneurs and first-generation wealthy contrasts with 360 ONE's dominance in inherited wealth. But as wealth matures and transfers generations, these distinctions blur. The winner will be whoever manages succession better—both client succession and their own leadership succession.

The competitive landscape reveals an industry in transition. From relationship-dependent to technology-enabled. From product-push to advisory-pull. From domestic focus to global ambitions. From independent players to potential consolidation targets. Nuvama and 360 ONE aren't just competing with each other—they're racing against time to build scale before the next wave of disruption or consolidation. In this race, being second-largest might be more advantageous than being first—hungry enough to innovate, large enough to matter, nimble enough to adapt.

VIII. Growth Strategy & Future Bets

The 47th floor of Mumbai's Indiabulls Finance Centre offers a panoramic view of the Arabian Sea, but Ashish Kehair, CEO of Nuvama, isn't looking at the horizon. He's studying a heat map of India on his laptop—red dots clustering around metros, orange spreading through tier-2 cities, yellow reaching into smaller towns. Each color represents wealth density, and each shade darker means opportunity. "By 2028," he says, tapping the screen, "this entire map will be orange and red. That's when India becomes too big to ignore."

Nuvama's growth strategy reads like a three-dimensional chess game. Horizontal expansion through geography, vertical integration through services, and temporal positioning for market inflection points. The ambition is breathtaking: add 800 relationship managers over three years, launch operations in Dubai and Singapore, scale asset management to ₹20,000 crores, all while maintaining service quality and regulatory compliance. It's either visionary or delusional—time will tell.

The Geographic Imperative: Following Indian Wealth Globally

In 2024, it launched a fully licensed DIFC operation in Dubai, targeting the Non-Resident Indian (NRI) and also international client segments across the Middle East. This was followed by the license to conduct wealth management activities in Singapore in 2025. The logic is compelling—25% of Dubai's expatriate population is Indian, many of them millionaires who made fortunes in real estate, trading, and professional services.

But Nuvama isn't just chasing NRIs for assets. "We're building a bridge in both directions," explained Vivek Sharma, Head of the International Clients Group. Indian families want global diversification—Swiss bank accounts, London real estate, Singapore REITs. Global investors want India exposure—not through ETFs but curated access to pre-IPO opportunities, real estate developments, and private credit.

The Dubai office, with its CAT III C licence, can advise and distribute products—a rare capability for an Indian firm. With a CAT III C licence, Nuvama Private is one of few Indian private banks that is authorised to provide advice and to distribute investment products. This isn't just about gathering assets; it's about becoming the trusted intermediary for cross-border wealth flows that will define the next decade.

The Talent Arms Race: 800 RMs or Bust

The mathematics of adding 800 relationship managers seems daunting. That's nearly doubling the current force, in a market where experienced RMs command astronomical packages and every competitor is hiring. But Nuvama's approach is nuanced—they're not just hiring, they're manufacturing RMs.

The strategy focuses on hiring from banking backgrounds rather than poaching from competitors. Young private bankers from HDFC, ICICI, and Axis join at lower costs but need 18-24 months of training to become productive. Nuvama has created an RM academy—six-month intensive programs covering everything from estate planning to alternative investments, behavioral finance to regulatory compliance.

More interesting is the geographic distribution. Rather than concentrating RMs in Mumbai and Delhi, Nuvama is placing them in Surat (diamond merchants), Coimbatore (textile industrialists), Ludhiana (sports goods exporters). These markets are underserved, relationship-driven, and incredibly sticky once trust is established. A single RM in Rajkot might manage more assets than three RMs in South Mumbai, with lower costs and higher loyalty.

Technology as Force Multiplier

Every relationship manager now carries an AI-powered portfolio analyzer that processes market data, client holdings, and risk parameters to generate personalized recommendations. But the real innovation isn't the technology—it's how it's deployed. RMs don't use it to replace human judgment but to augment it. The AI suggests, the RM interprets, the client decides.

The digital infrastructure investment goes deeper. Nuvama is building what they call a "client cloud"—a unified data platform that tracks every interaction, transaction, and preference across all touchpoints. When a client calls about market volatility, the RM sees their entire history—not just portfolios but past concerns, family milestones, even communication preferences. It's CRM on steroids, but with a human touch that pure robo-advisors can't match.

Asset Management: The ₹20,000 Crore Dream

The target of ₹20,000 crore AUM in asset management seems ambitious given current levels around ₹10,000 crores, but the strategy is clever. Rather than competing with mutual funds in public markets—a crowded, low-margin business—Nuvama focuses on alternatives where access matters more than scale.

Product suite expanded across all strategies in last 3-6 months: Commercial Real Estate – Prime Fund, Public Markets – Absolute Return Fund and Private Markets – Crossover 4 series. Each product targets specific client needs—the real estate fund for inflation hedging, absolute return for volatility protection, crossover for pre-IPO access.

The GIFT City initiative adds another dimension. To solve for this, Nuvama has launched offshore versions of some of its public market strategies through the GIFT City in Gujarat. These funds can accept foreign money, offer tax efficiency, and provide India exposure without regulatory hassles. It's like having an offshore fund domiciled in India—a unique proposition that neither global nor domestic competitors can easily replicate.

The Platform Play: Open Architecture with Proprietary Edge

Nuvama is building what they call an "open architecture with proprietary advantage." They'll distribute anyone's products—mutual funds from HDFC, insurance from ICICI, structured products from JP Morgan. But increasingly, they're steering clients toward proprietary offerings where margins are higher and control is complete.

The platform strategy extends to partnerships. Rather than building everything internally, Nuvama partners with specialists—Cushman & Wakefield for real estate, global banks for structured products, fintech for digital tools. Each partnership brings capability without capital investment, speed without operational burden.

International Expansion: The NRI Goldmine

The numbers are staggering. Indian diaspora holds $500+ billion in offshore wealth. Most of it sits in vanilla deposits or generic global funds, earning single-digit returns while India delivers teens. The opportunity isn't just gathering these assets but optimizing them—structured products that provide India exposure with downside protection, funds that navigate Indian regulations while maintaining global standards.

The expansion is carefully sequenced. Dubai first, for the GCC's 7 million Indians. Singapore next, for Southeast Asia's professionals. London eventually, for the UK's established Indian community. Each market needs different products, regulations, and approaches, but the underlying thesis remains: Indians trust Indians with their money, especially when navigating complex cross-border situations.

The Subscale Businesses: Asset Management's J-Curve

Asset management remains subscale, generating just 4% of revenues despite ambitious growth plans. The J-curve effect is brutal—upfront investments in teams, technology, and regulatory infrastructure with revenues coming slowly as AUM builds. But Nuvama is playing the long game, believing that once they cross ₹20,000 crores, margins will explode from current single digits to 30%+.

The strategy focuses on distribution leverage. Every wealth management client is a potential asset management customer. Every corporate relationship from capital markets is a treasury that needs investment solutions. The cross-selling opportunity is massive, but execution is harder than PowerPoint slides suggest.

Risk Management: Growth vs. Quality

The aggressive expansion creates execution risks. Adding 800 RMs means 800 chances for mis-selling, compliance violations, or client dissatisfaction. Expanding internationally means navigating unfamiliar regulations, different client expectations, and currency risks. Scaling asset management means investment performance becomes crucial—one badly performing fund can taint the entire franchise.

Nuvama's response is to invest heavily in what they call "growth infrastructure"—compliance teams, training programs, technology platforms that scale with growth rather than after it. They're hiring chief risk officers for each geography, implementing AI-driven compliance monitoring, and creating escalation matrices that flag issues before they become problems.

The Time Horizon: 2028 as Inflection Point

Management consistently references 2028 as a watershed year. By then, India's GDP should cross $5 trillion, per capita income will near $4,000, and the number of millionaires will double. More importantly, wealth will start transferring generations—from creators to inheritors, from savers to spenders, from domestic to global.

By 2027 or 2028, India will break free of the emerging markets label, commanding dedicated capital flows. Nuvama is positioning for that moment—building capabilities that will matter then, not just what's profitable today. It's a bet on India's economic trajectory, demographic dividend, and wealth creation potential.

The growth strategy isn't without skeptics. Can Nuvama maintain culture while doubling headcount? Can technology replace relationships in Indian wealth management? Will international expansion dilute focus on the core Indian market? These questions don't have easy answers.

But perhaps that's the point. In a market growing as fast as India's, playing it safe might be the riskiest strategy. Nuvama is betting that fortune favors the bold—that by the time competitors realize the opportunity, they'll have already captured it. It's ambitious, perhaps overly so. But in India's wealth management wars, ambition might be the only sustainable advantage.

IX. Playbook: Lessons for Builders & Investors

The Nuvama story isn't just about one company's journey—it's a masterclass in financial engineering, strategic timing, and value creation that offers lessons far beyond wealth management. For builders contemplating spin-outs, investors evaluating demergers, and operators navigating regulated markets, Nuvama's playbook provides a template worth deconstructing.

The Art of the Spin-Out: When Division Becomes Multiplication

The conventional wisdom says conglomerates trade at discounts because markets can't value complexity. But Nuvama's demerger reveals a deeper truth: sometimes the whole genuinely is worth less than its parts, not due to market inefficiency but operational reality.

Inside Edelweiss, wealth management competed for capital with lending businesses that needed constant feeding. Board attention was divided across insurance, asset reconstruction, and credit. The wealth unit's 30% ROE was dragged down by lending's 12% returns. Talent saw career paths blocked by executives from other divisions. Clients confused Edelweiss Wealth with Edelweiss Housing Finance.

The demerger unlocked five distinct types of value. First, multiple expansion—wealth management deserves 25-30x earnings, not the 8-10x of diversified financials. Second, capital efficiency—no longer funding other divisions' growth. Third, strategic focus—board meetings discussing client acquisition, not NPA recovery. Fourth, talent attraction—equity compensation directly tied to wealth management performance. Fifth, brand clarity—Nuvama means wealth, nothing else.

The lesson for builders: Spin-outs work when businesses have different capital intensity, different growth rates, different risk profiles, or different talent needs. The trigger isn't just valuation disagreement but operational incompatibility. The best spin-outs feel inevitable in hindsight, like a teenager leaving home—natural, necessary, and ultimately beneficial for both parties.

Private Equity as Catalyst: The PAG Playbook

PAG's role transcended typical private equity involvement. They didn't just provide capital—they provided permission. Permission for Rashesh Shah to let go. Permission for management to think independently. Permission for aggressive expansion that public markets might punish quarterly but reward eventually.

The playbook had four components. First, create irreversibility—once PAG owned majority, the demerger became inevitable, removing optionality that breeds inaction. Second, import excellence—bring global best practices without destroying local relationships. Third, accelerate investment—spend on technology and talent that the parent couldn't afford. Fourth, maintain alignment—keep founders involved enough to preserve culture but not enough to block change.

For investors, the lesson is that PE works best when it solves for more than capital. Edelweiss didn't need money—they needed a forcing function for transformation. The best PE deals unlock psychological value, not just financial value. Sometimes a founder needs someone else to make the hard decision they know is right but can't bring themselves to make.

Building in Regulated Markets: The Licensing Moat

Nuvama operates across dozens of licenses—wealth management, broking, merchant banking, portfolio management, custody, distribution. Each license took years to obtain, requires ongoing compliance, and creates barriers competitors can't quickly overcome. It's a moat built from paperwork, but a moat nonetheless.

The strategic insight is that regulations create opportunity for those willing to navigate complexity. While fintech startups promise disruption, Nuvama quietly accumulated licenses that would take new entrants decades to replicate. They turned compliance from cost center to competitive advantage, regulatory burden into barrier to entry.

The approach to international expansion exemplifies this philosophy. Rather than rushing into markets, Nuvama spent months obtaining proper licenses—CAT III C in Dubai, full wealth management authorization in Singapore. Competitors might move faster with representative offices or partnership structures, but Nuvama's full licenses enable services others can't offer. In regulated industries, the tortoise beats the hare if the tortoise has the right permits.

The Rebranding Decision: When Heritage Becomes Handicap

The shift from Edelweiss Securities to Nuvama violated conventional wisdom about brand value. Three decades of brand building, thousands of crores in marketing investment, widespread recognition—all abandoned for an unknown name. Yet it worked brilliantly.

The lesson is that brand value depends on context. In wealth management, association matters more than awareness. Clients didn't need to know Nuvama—they needed to not confuse it with Edelweiss's lending troubles. The rebranding wasn't about creating positive associations but eliminating negative ones.

The execution matters as much as the decision. Nuvama didn't just change logos—they created a narrative. The Sanskrit etymology gave it roots. The "new wealth" translation gave it meaning. The comprehensive rollout—from business cards to building signs—gave it credibility. They turned rebranding from admission of failure to declaration of independence.

Client Segmentation Mastery: Different Games, Different Rules

Nuvama's dual-brand strategy—Nuvama Wealth for HNIs, Nuvama Private for UHNIs—seems like unnecessary complexity. Why not one brand with different service tiers? The answer reveals sophisticated understanding of wealth psychology.

HNI clients (₹5-25 crores) want efficiency, access, and validation. They're doctors who became wealthy, not wealthy who happened to be doctors. They need education about products, appreciate technology interfaces, and value peer benchmarking. The Nuvama Wealth model—standardized products, digital delivery, relationship manager support—fits perfectly.

UHNI clients (₹100+ crores) want exclusivity, customization, and discretion. They're industrialist families with generational wealth, not successful professionals. They need estate planning, not product selection. They value privacy over convenience. The Nuvama Private model—bespoke solutions, white-glove service, family office approach—speaks their language.

The lesson extends beyond wealth management. True segmentation isn't about spending power but psychological needs. The same customer might want mass market in some categories and luxury in others. Understanding which game you're playing with which segment determines everything from pricing to promotion to product design.

Platform vs. Product: The Integration Advantage

The debate between focused excellence and integrated platforms rages across industries. Should you be the best at one thing or good at many? Nuvama's answer: be the best at integration itself.

They don't have the best brokerage platform (Zerodha does), the best portfolio management (specialized PMS firms do), or the best investment banking (global banks do). But they have the best integration of all three for a specific customer—the wealthy Indian who needs holistic solutions.

The platform advantage compounds over time. Each additional service makes existing services stickier. Each new client relationship creates cross-selling opportunities. Each product innovation can be distributed across multiple channels. The challenge is maintaining quality while expanding scope—platforms can become mediocre at everything rather than excellent at integration.

The Exit as Entry: Strategic Sales Strategy

PAG's eventual exit isn't an endpoint but a transformation point. Unlike typical PE exits seeking highest price, PAG can be strategic about buyer selection. Sell to another PE firm, and the transformation continues. Sell to a strategic buyer, and Nuvama becomes part of something larger. Go public through secondary sale, and create permanent capital.

The lesson for builders is to think about exit from entry. Not to maximize sale price but to ensure continuity of vision. The best exits feel like graduations, not liquidations. They mark the end of one chapter but the beginning of another. PAG's stake is both an asset and an option—on Nuvama's future, India's growth, and wealth management's evolution.

Regulatory Arbitrage: The GIFT City Innovation

Nuvama's use of GIFT City to create offshore funds onshore represents sophisticated regulatory arbitrage. They're solving a problem—NRIs can't easily invest in Indian alternatives—by exploiting a solution—GIFT City's special regulatory zone.

The broader lesson is that regulations create opportunities for those who study them deeply. Every restriction implies an exception. Every prohibition suggests a workaround. Not through illegal means but creative compliance—using regulations' own logic to achieve desired outcomes.

This requires deep regulatory expertise, strong legal counsel, and willingness to be first mover. Most firms wait for others to prove concepts. Nuvama creates precedents others follow. In regulated industries, innovation often means regulatory innovation—finding new ways to do old things within existing rules.

The Long Game: Building for the Next Buyer

Every decision at Nuvama seems designed for the eventual buyer—whether that's public markets, a strategic acquirer, or another PE firm. Clean corporate structure. Transparent segment reporting. Scalable technology infrastructure. Institutional processes. It's being built to be bought, even if that's not the stated intention.

This creates discipline that independent companies often lack. Would Nuvama invest as heavily in compliance without PAG oversight? Would they maintain segment purity without future exit considerations? Would they resist the temptation to juice short-term profits through risky lending? The exit overhang creates operational excellence.

The metalesson is that building for sale forces building better businesses. Not because buyers demand it but because the process demands it. The discipline of preparing for due diligence, the clarity required for valuation, the sustainability needed for warranties—these create better businesses regardless of whether sales happen.

The Nuvama playbook isn't universally applicable. It requires specific conditions—a subscale division within a larger conglomerate, a business with different economics than its parent, a market undergoing structural transformation, and leadership willing to let go. But for those facing similar situations, it provides a template for value creation that goes beyond financial engineering to fundamental business transformation.

X. Bear vs Bull Case

The investment community remains divided on Nuvama, with compelling arguments on both sides. The optimists see a structural growth story riding India's wealth creation wave. The pessimists see an overvalued, cyclical business heading into turbulence. As always, the truth likely lies somewhere in between, but understanding both extremes helps frame the opportunity and risk.

Bear Case: The Storm Clouds Gathering

The bears' primary concern is Nuvama's dangerous dependency on volatile capital markets. With 39% of revenue from capital markets, Nuvama is essentially a leveraged bet on market direction. When markets correct—not if, but when—this revenue stream could evaporate overnight. The Q1 FY25 surge of 153% YoY in capital markets revenue is unsustainable, built on record volumes that revert to mean. History shows Indian markets can remain depressed for years—2011-2013, 2000-2003. Nuvama hasn't been tested through a prolonged bear market as an independent entity.

Despite the recent surge and 114% gain since listing, the stock is down 19% in 2025, suggesting market skepticism about sustainability. The valuation at 25x earnings prices in perfection, leaving no room for disappointment. Any earnings miss could trigger a violent derating, especially given the high retail investor participation.

The subscale asset management business is hemorrhaging cash while chasing an uncertain future. At just ₹10,000 crores AUM generating 4% of revenues, it's too small to matter but too expensive to maintain. The team costs, regulatory requirements, and technology investments require at least ₹20,000 crores to break even properly. That's years away, if ever achieved, given intense competition from established mutual funds and new-age PMS providers.

PAG's exit overhang creates a sword of Damocles. With 54% stake worth over ₹14,000 crores, any exit attempt could crash the stock. Strategic buyers might demand discounts. Financial buyers need leverage that pressures operations. Secondary market sales would flood supply. Until PAG exits, the stock trades with a permanent discount, regardless of operational performance.

Competition is intensifying from every direction. Global banks like UBS and Credit Suisse are rebuilding Indian operations with unlimited capital. Domestic banks leverage branch networks and existing relationships. Fintech platforms offer zero-cost broking and robo-advisory. New-age wealth managers like Dezerv and Stable Money target the same affluent segment with better technology and lower costs. Nuvama is stuck in the middle—lacking global banks' product sophistication and fintechs' cost structure.

The execution risks of aggressive expansion could prove fatal. Adding 800 RMs means diluting quality, increasing mis-selling risk, and destroying culture. International expansion distracts from core Indian operations while burning cash on uncertain returns. Technology investments might fail to generate returns in a relationship-driven business. The company is trying to do too much, too fast, with too little room for error.

Regulatory changes could destroy economics overnight. SEBI's recent restrictions on AIF investments already impacted revenues. Proposed changes to distribution commissions could cut margins. Any scandal—one rogue RM, one compliance failure—could trigger regulatory backlash that takes years to recover from. In financial services, reputation is everything, and Nuvama hasn't been tested.

The macro environment is deteriorating. Rising interest rates make equity markets less attractive. Geopolitical tensions could trigger foreign investor exodus. Domestic inflation pressures consumption, reducing investible surplus. A real estate correction could destroy wealth that Nuvama manages. The next decade might not resemble the last, and Nuvama is positioned for yesterday's war.

Bull Case: The Structural Transformation Story

The bulls see Nuvama riding an unstoppable wave of Indian wealth creation. India is becoming the world's fastest-growing major economy, with GDP expected to reach $5 trillion by 2027. Rising income levels—per capita income crossing $4,000—are creating an explosion in investible surplus. The shift from physical to financial assets is just beginning, with household savings increasingly moving from gold and real estate to capital markets. This isn't a cycle; it's a structural transformation that will play out over decades.

Nuvama's market leadership position is strengthening, not weakening. As the second-largest wealth manager by revenue and profit, they have scale advantages in technology investment, product development, and talent acquisition. The integrated model creates competitive advantages—cross-selling between wealth, capital markets, and asset management that pure-plays can't match. Client stickiness is high in wealth management; once trust is established, relationships last decades.

The brand transformation is working brilliantly. The Nuvama rebrand eliminated legacy concerns while preserving operational excellence. Young entrepreneurs and new wealth prefer fresh brands over established names associated with older generations. The positioning as India's homegrown wealth manager resonates amid rising nationalism and desire for local champions.

International expansion opens massive new markets. The $500 billion NRI wealth pool remains largely untapped by Indian managers. Dubai and Singapore licenses provide access to global Indians who trust Indian expertise for India investments. Cross-border wealth flows will accelerate as Indians globalize and global capital seeks India exposure. Nuvama is uniquely positioned as a bridge between Indian wealth and global opportunities.

Technology investments are creating operational leverage. The AI-powered tools improve RM productivity, enabling handling more clients without proportional cost increases. Digital platforms reduce client acquisition costs while improving service quality. Automation in operations reduces errors and improves compliance. Technology isn't replacing relationships but amplifying them.

The financial performance trajectory is compelling. Revenue growth at 30%+ consistently outpaces industry growth of 15-20%. Margins are expanding as scale benefits kick in and business mix improves. ROE above 30% places Nuvama among the most capital-efficient financial services businesses. Cash generation will accelerate once growth investments moderate, enabling substantial dividend payouts.

Management execution has been flawless so far. The successful demerger, smooth rebranding, and rapid growth demonstrate operational excellence. The team has navigated regulatory complexity, competitive pressure, and market volatility successfully. Backed by PAG's global expertise and capital, they have resources to execute the ambitious growth plan.

Valuation remains attractive relative to potential. At 25x earnings, Nuvama trades at a discount to global wealth managers at 30-40x. As the business model proves out and capital markets dependency reduces, multiple expansion is likely. A successful PAG exit to a strategic buyer could trigger immediate rerating. The stock could double from current levels and still not be expensive given growth prospects.

The Balanced View: Probability-Weighted Outcomes

The reality is that both cases have merit, and the outcome depends on factors both within and outside Nuvama's control. The key variables to watch include the sustainability of capital markets revenues, success in scaling asset management, execution of international expansion, and nature of PAG's eventual exit.

The highest probability scenario (40%) is continued strong performance with occasional volatility—revenues growing 20-25% annually, margins expanding gradually, stock delivering 15-20% annual returns with significant volatility. The bull scenario (30%) sees everything clicking—wealth management accelerating, asset management scaling, international succeeding, resulting in 30%+ annual returns. The bear scenario (30%) sees a market correction exposing operational weaknesses, leading to significant derating and possible strategic sale at disappointing valuations.

For investors, the decision comes down to time horizon and risk tolerance. Short-term investors should be cautious given high valuation and near-term risks. Long-term investors can look through volatility at structural opportunity. The stock is suitable for those believing in India's wealth creation story but requires stomach for volatility.

The risk-reward appears balanced at current levels—significant upside if execution succeeds, meaningful downside if markets correct. Dollar-cost averaging might be optimal strategy, building positions during corrections rather than chasing momentum. The story is compelling, but the price offers limited margin of safety.

Ultimately, Nuvama is a bet on India's transformation from a poor country with few rich people to a middle-income country with many affluent people. If that transformation occurs—and history suggests it will—Nuvama is well-positioned to capture disproportionate value. But the path won't be linear, and investors should prepare for a bumpy ride. The bears and bulls will both be right—just at different times.

XI. Recent News (As of Early 2025)

The newsflow around Nuvama in recent months has been dominated by three themes: PAG's strategic review creating exit speculation, operational momentum continuing despite market volatility, and competitive dynamics intensifying as global players expand in India.

The biggest overhang remains PAG's stake. Market rumors suggest multiple parties have expressed interest, including global strategic buyers like UBS and Credit Suisse looking to expand Indian footprint, and financial sponsors like Warburg Pincus and Blackstone seeking platform plays. PAG hasn't committed to any timeline, but market expects clarity by mid-2025.

Q3 FY25 results (not yet published) are expected to show moderation from the exceptional Q1 performance, but still healthy growth driven by wealth management stability offsetting capital markets normalization. The street expects 15-20% revenue growth and margin maintenance, which would validate the business model's resilience.

The Dubai operations have gained traction faster than expected, with reports suggesting over $500 million in client assets gathered within six months of launch. The Singapore license approval positions Nuvama to tap Southeast Asian NRI wealth, particularly from countries like Malaysia and Indonesia with large Indian diaspora.

Regulatory developments remain mixed. SEBI's recent consultation paper on wealth management regulations could standardize the industry but might also compress margins. The proposal for unified license for all financial advisors could level playing field but increase compliance costs.

Competition continues intensifying with 360 ONE's proposed acquisition of ET Money signaling aggressive digital push, while Kotak's partnership with global alternatives platform iCapital shows everyone is chasing the same alternatives opportunity.

XII. Conclusion: The Metamorphosis Continues

The Nuvama story is far from over. What began as a division inside a conglomerate has transformed into India's second-largest wealth manager, but this might just be the first chapter of a longer narrative. The metamorphosis from Edelweiss to Nuvama was dramatic, but the evolution from domestic player to global platform, from traditional advisor to technology-enabled partner, from single-country focus to cross-border facilitator, is just beginning.

The strategic choices ahead will define Nuvama's next decade. Will they remain independent or become part of a larger global platform? Will technology complement or eventually replace relationship managers? Will international expansion accelerate or will they double down on India? Will asset management achieve scale or remain subscale? These aren't just corporate decisions—they're bets on India's economic trajectory, wealth management's evolution, and financial services' future.

For investors, Nuvama represents a pure-play bet on Indian wealth creation with all the opportunities and risks that entails. For competitors, it's a formidable rival that's proven ability to transform and adapt. For employees, it's a platform offering unprecedented growth opportunities in a rapidly expanding industry. For India's wealthy, it's increasingly becoming the default choice for sophisticated financial advice.