NTPC Green Energy: India's Renewable Power Giant

I. Introduction & Opening

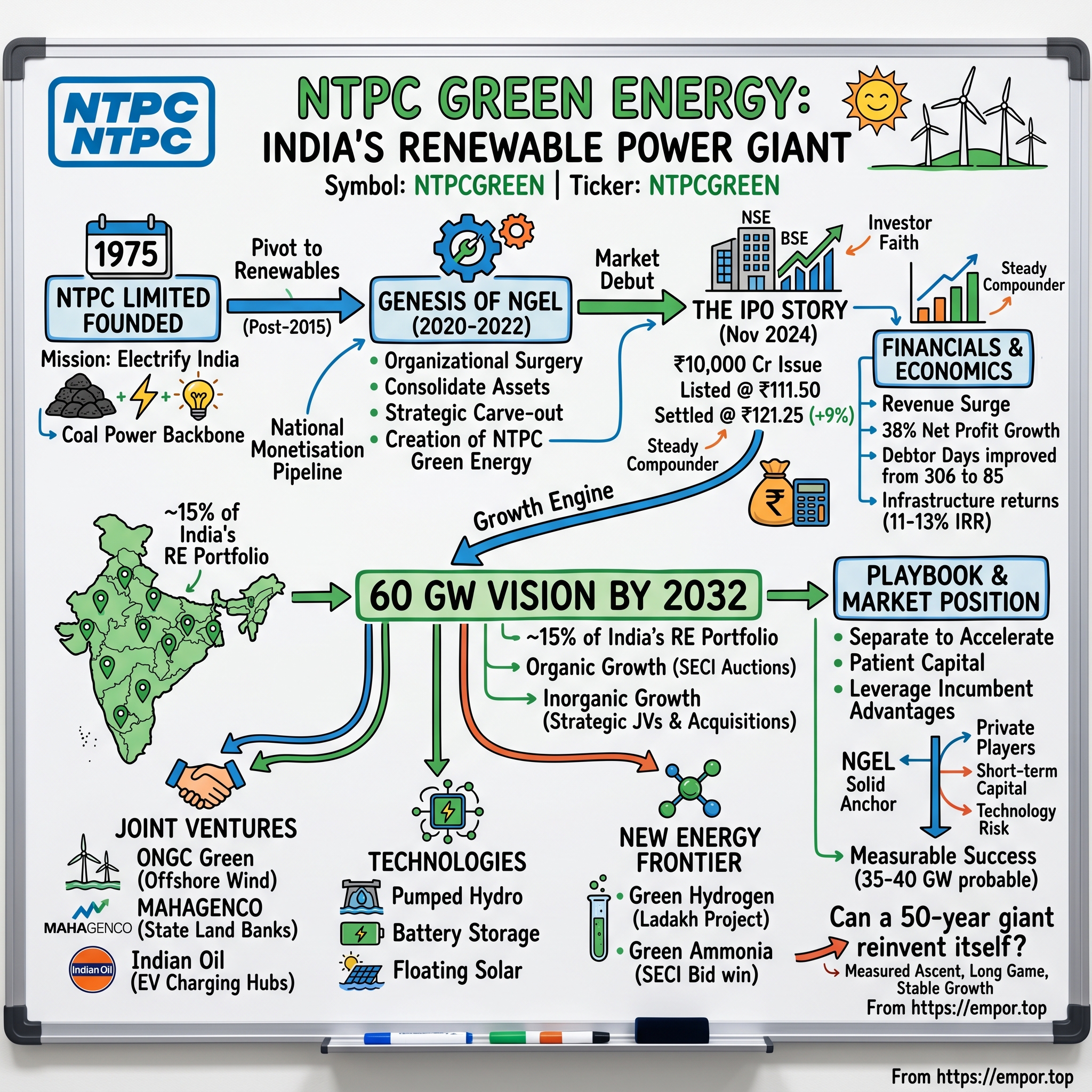

Picture this: November 27, 2024, 9:15 AM at the National Stock Exchange in Mumbai. The trading floor buzzes with anticipation as NTPC Green Energy Limited—symbol NTPCGREEN—makes its market debut. The stock opens at ₹111.50, a modest 3.24% premium to its IPO price of ₹108. By day's end, it would settle at ₹121.25, up nearly 9%. Not the explosive "pop" that retail investors dream of, but for India's largest renewable energy public sector enterprise, this measured ascent felt perfectly appropriate. After all, this wasn't some speculative startup—this was the renewable energy arm of NTPC, India's power generation behemoth, carrying five decades of institutional memory into the clean energy future.

The numbers tell one story: ₹85,814 crore market capitalization, 3,171 MW of operational capacity, 60 GW targeted by 2032. But the real story—the one that matters for understanding India's energy transition—is far more nuanced. How does a state-owned enterprise, built on coal-fired power plants, transform itself into a renewable energy champion? How does it compete with nimble private players while navigating the labyrinth of government bureaucracy? And perhaps most intriguingly: why should global investors care about a PSU in India's renewable sector when Adani Green and ReNew Power grab all the headlines?

This is the story of institutional evolution at massive scale. It's about patient capital meeting urgent climate needs, about engineering excellence pivoting from thermal turbines to solar panels, about a company that generates 25% of India's electricity despite owning just 16% of capacity now betting its future on wind and sun. At its core, this is a case study in how incumbents—especially state-owned incumbents—can successfully navigate technological disruption.

The central question we're exploring isn't whether renewable energy will dominate India's future—that's already decided by physics, economics, and policy. The question is whether a 50-year-old thermal power giant can reinvent itself fast enough to capture that future. Can NTPC Green Energy leverage its parent's advantages—land banks, transmission access, government relationships, AAA credit rating—while moving with the speed and innovation the renewable sector demands?

As we'll see, the answer lies not in dramatic pivots or moonshot bets, but in methodical execution, strategic patience, and an almost boring commitment to operational excellence. In the venture capital world, this would be death. In infrastructure, it might just be the winning formula.

II. NTPC Legacy & The Energy Context

The year was 1975. India, still finding its economic footing post-Emergency, desperately needed power—literally. The country's installed capacity stood at a mere 16,664 MW, chronic shortages darkened cities, and industrial growth stuttered for want of electricity. Into this crisis stepped the National Thermal Power Corporation, established on November 7, 1975, with an audacious mandate: build massive coal-fired power plants and electrify a nation.

Fast forward five decades, and NTPC Limited stands as a colossus—80,154.50 MW of installed capacity spanning coal, gas, hydro, and renewables. The company's thermal plants, engineering marvels in their own right, achieve availability factors above 85% and plant load factors that consistently outperform private sector peers. When you flip a switch anywhere in India, there's a one-in-four chance that electricity flows from an NTPC plant. This isn't just market share; it's the backbone of a $3.7 trillion economy.

But here's where the story gets interesting. Around 2015, something fundamental shifted in global energy markets. Solar module prices crashed 90% in a decade. Wind turbine efficiency doubled. Battery costs plummeted. Suddenly, renewable energy wasn't just clean—it was cheap. In India, solar tariffs dropped from ₹17 per unit in 2010 to ₹2.44 by 2017, undercutting new coal plants. The economics that built NTPC's empire were inverting before their eyes.

Then came Paris. The 2015 Climate Agreement saw India commit to 40% non-fossil fuel capacity by 2030. Prime Minister Modi, never one for modest targets, upped the ante: 450 GW of renewable capacity by 2030, later revised to 500 GW. For context, that's more renewable capacity than the entire U.S. grid today. These weren't aspirational targets—they became national policy, embedded in five-year plans, state procurement mandates, and regulatory frameworks. For NTPC's management, the writing was on the wall. ESG investors started excluding coal-heavy portfolios. International financing dried up for thermal projects. Young engineering talent gravitated toward clean tech startups. The company that epitomized India's industrial might suddenly looked like a relic. Board meetings in 2016-2017 must have been sobering affairs—how do you tell 20,000 employees that everything they've mastered might become obsolete?

Yet NTPC possessed unique advantages that pure-play renewable developers could only dream of. Land banks across India, painstakingly acquired over decades. Transmission infrastructure connecting to every major load center. Relationships with state electricity boards, forged through decades of reliable power delivery. An AAA credit rating that meant borrowing at government rates. And perhaps most critically: operational DNA that understood how to build, run, and maintain massive infrastructure projects in India's complex regulatory environment. The strategic pivot began quietly in 2016 with NTPC setting up its first 10 MW solar plant in Anantapur. By 2020, the company announced its ambitious target: 50% non-fossil based capacity by 2032. This wasn't incrementalism—it was a fundamental reimagining of what NTPC could become. The board recognized that renewable energy wasn't a side business or CSR initiative. It would become the core growth engine, eventually overshadowing the thermal legacy that built the company.

The transformation required more than targets and press releases. It demanded organizational surgery—carving out renewable assets, creating new subsidiaries, hiring different talent, and most painfully, admitting that the future looked nothing like the past. For a PSU accustomed to five-year construction timelines and 25-year PPAs, the renewable world's pace—six-month installations, rapidly evolving technology, aggressive auction-based pricing—felt alien. Yet NTPC's leadership understood a fundamental truth: in infrastructure transitions, the incumbent's advantages often outweigh the insurgent's agility.

So what for investors? The NTPC story demonstrates that successful energy transitions aren't about abandoning legacy assets overnight but leveraging them strategically. The company's thermal cash flows fund renewable expansion, its operational expertise ensures superior project execution, and its government backing provides patient capital that private players can't match. For long-term investors, this suggests that well-managed incumbents might actually be better positioned for the energy transition than pure-play disruptors—a contrarian view worth considering.

III. The Genesis: Creating NTPC Green Energy (2020–2022)

The boardroom at NTPC's headquarters in Dwarka, New Delhi, had seen many pivotal moments since 1975. But the discussions in early 2022 carried unusual weight. The renewable energy portfolio, scattered across various NTPC subsidiaries and joint ventures, had grown organically but chaotically—a solar project here, a wind farm there, no unified strategy or operational synergy. Chairman and Managing Director Gurdeep Singh knew that competing with Adani Green's aggressive expansion and ReNew Power's Wall Street backing required structural transformation, not incremental adjustments.

The business model centered on development, construction, and operation of renewable energy projects (solar and wind), supported by long-term Power Purchase Agreements (PPAs). But executing this model through NTPC's traditional structure was like racing a Formula One car with truck tires. The company needed a dedicated vehicle—nimble enough to compete in reverse auctions, sophisticated enough to attract international capital, yet robust enough to leverage NTPC's institutional strengths.

Enter NTPC Green Energy Limited, incorporated in April 2022 as a wholly-owned subsidiary. The creation wasn't just administrative paperwork—it represented a fundamental reorganization of how India's largest power producer would approach the next three decades. Through a business transfer agreement dated July 8, 2022, NTPC consolidated its entire renewable portfolio under this new entity, with the transfer completing on February 28, 2023. Every solar panel, wind turbine, and power purchase agreement moved under one roof.

The National Monetisation Pipeline, announced by Finance Minister Nirmala Sitharaman in 2021, provided the strategic trigger. The government's push to unlock value from public assets aligned perfectly with NTPC's need to restructure. Rather than selling assets to private players—politically sensitive and strategically questionable—NTPC could monetize through capital markets while retaining control. The IPO path wasn't just about raising money; it was about creating a market-valued entity that could compete for talent, partnerships, and international capital.

NTPC Renewable Energy Limited (NREL), established as NGEL's primary operating subsidiary, became the organic growth vehicle. While NGEL would handle strategy, capital allocation, and stakeholder management, NREL would execute—bidding for projects, managing construction, operating assets. This two-tier structure might seem bureaucratic, but it served a crucial purpose: separating financial engineering from operational execution, allowing each entity to optimize for its core competency.

The initial portfolio transferred to NGEL told its own story of evolution. As of August 31, 2024, operational capacity stood at 3,071 MW of solar projects and 100 MW of wind projects. These weren't greenfield developments but operating assets with established track records, generating steady cash flows from long-term PPAs. The portfolio spanned seven states—from Rajasthan's desert solar parks to Tamil Nadu's wind corridors—providing both geographic diversification and operational learning across different regulatory regimes.

But the real asset wasn't the installed capacity—it was the pipeline. 31 renewable energy projects under construction in seven states, accounting for 11,771 MW, represented one of India's largest renewable construction portfolios. These weren't speculative land banks or MoUs but contracted projects with secured PPAs, financing arranged, and construction underway. For investors evaluating the IPO, this pipeline visibility mattered more than historical financials.

The organizational culture shift proved more challenging than asset transfers. NTPC's thermal engineers, accustomed to complex thermodynamics and massive boiler operations, had to embrace silicon chemistry and wind patterns. The procurement team, experts in coal logistics and turbine specifications, needed to understand module degradation rates and inverter efficiencies. HR had to compete for talent not with BHEL or L&T but with renewable startups offering ESOPs and Silicon Valley culture.

Yet NTPC Green Energy inherited invaluable intangibles. The parent's AAA credit rating meant accessing debt at near-sovereign rates—a 200-300 basis point advantage over private competitors. Land acquisition capabilities, honed over decades of power plant development, translated directly to renewable projects. Most crucially, relationships with state governments and distribution companies, built on decades of reliable power supply, opened doors that money couldn't buy.

The governance structure reflected this dual heritage. The board combined NTPC veterans who understood government processes with renewable energy specialists who brought technological expertise. The management team blended thermal power operators who knew how to run large infrastructure with young engineers who understood solar economics and grid integration. This wasn't just succession planning—it was institutional knowledge transfer at scale.

So what for investors? The genesis story reveals NGEL as neither a startup nor a spin-off but a strategic carve-out designed to capture specific advantages while shedding legacy constraints. The company inherits NTPC's strengths—credit rating, government relationships, operational excellence—while gaining autonomy to move at market speed. For investors, this hybrid model offers an intriguing proposition: startup-like growth potential backed by PSU-like stability. The question isn't whether this model can work but whether management can balance these dual identities without compromising either.

IV. The Business Model & Strategy

Standing inside NTPC Green Energy's 600 MW solar park in Nokh, Rajasthan, the scale becomes visceral. Row upon row of photovoltaic panels stretch to the horizon, tracking the sun's arc with mechanical precision. Each panel generates data—temperature, voltage, current—streaming to control rooms where algorithms optimize output in real-time. This isn't your grandfather's power plant with turbines and boilers. Yet fundamentally, the business model remains beautifully simple: convert photons to electrons, sell electrons for rupees, repeat at massive scale.

The revenue model centers on long-term Power Purchase Agreements—25-year contracts with state distribution companies, typically at fixed or escalating tariffs. As of June 30, 2024, servicing 15 off-takers through 37 solar and 9 wind projects, NGEL's customer concentration seems manageable, though the top five account for significant revenue share. These aren't market-price contracts subject to merchant risk but regulated agreements with sovereign-backed counterparties. Think of it as infrastructure-as-a-service with 25-year SaaS-like recurring revenue—except the churn rate is essentially zero.

The unit economics tell a compelling story. Solar projects commissioned in 2024 achieve leveled tariffs around ₹2.50-3.00 per kWh, with capital costs of ₹3.5-4 crore per MW. At 20-22% capacity utilization factors (CUFs) typical for Indian solar, each MW generates roughly 1.75 million units annually. Simple math: ₹43-52 lakh annual revenue per MW against ₹25-30 lakh in operating expenses and debt service. The projects turn cash-positive from year one, achieving unlevered IRRs of 11-13%—not spectacular by venture standards but exceptional for infrastructure.

Wind economics prove trickier. Higher capital costs (₹6-7 crore per MW) and variable generation profiles compress returns. But NGEL's strategic focus remains solar, with wind serving as portfolio diversification and hybrid project enabler. The real innovation lies in hybrid projects—combining solar and wind at single locations, sharing transmission infrastructure and providing steadier generation profiles. These projects command premium tariffs and better grid stability, attractive to distribution companies struggling with renewable intermittency. The financial performance validates the model's resilience. Revenue stood at ₹2,311 crore with profit of ₹556 crore for the recent period, while net profit rose 38% to ₹474.12 crore in FY25, compared with ₹342.86 crore in FY24, with total income growing 21% year-on-year to ₹2,465.70 crore. More impressively, debtor days improved from 306 to 85.3 days—critical in a sector notorious for payment delays. This working capital efficiency translates directly to cash generation, funding growth without constant equity dilution.

The strategic focus on utility-scale projects over distributed generation reflects deep understanding of Indian market dynamics. Rooftop solar might grab headlines, but utility-scale delivers economics. A 100 MW solar park achieves 30-40% lower leveled costs than equivalent distributed capacity. Standardized designs, bulk procurement, optimized O&M—boring advantages that compound over 25 years. NGEL doesn't chase residential customers or C&I contracts; it builds infrastructure that utilities need, at prices they can afford.

Geographic diversification provides natural hedging. Solar irradiation varies by region—Rajasthan's deserts receive 20% more sunlight than Kerala's coast. Wind patterns differ dramatically—Tamil Nadu's monsoons, Gujarat's coastal breezes, Karnataka's plateau winds. By spreading projects across states, NGEL reduces weather risk while navigating India's complex state-level regulatory frameworks. Each state has different land policies, grid codes, banking regulations—institutional knowledge that takes years to develop.

The technology strategy emphasizes proven over cutting-edge. While startups experiment with perovskite cells or concentrated solar power, NGEL deploys crystalline silicon panels and horizontal-axis turbines—technologies with 20-year track records. Module suppliers include Tier-1 manufacturers like Jinko, Trina, and LONGi, with warranties extending to 25 years. Inverter partners—ABB, Siemens, Sungrow—provide global support networks. This isn't technological conservatism but risk management. When you're building ₹400 crore projects with 25-year lifespans, beta testing isn't an option.

The operations and maintenance (O&M) capabilities deserve special attention. Unlike pure developers who flip projects post-commissioning, NGEL operates assets throughout their lifecycle. In-house teams handle everything from module cleaning (critical in dusty Rajasthan) to inverter maintenance to grid synchronization. Predictive maintenance algorithms, developed over millions of operating hours, identify failures before they occur. This operational excellence translates to superior availability factors—98%+ for solar, competitive with thermal plants.

Securing PPAs in India's complex market requires both technical competence and political navigation. The recent success in SECI's auction for 70,000 Metric Tonnes Per Annum of Green Ammonia demonstrates evolving capabilities beyond traditional electricity generation. These aren't just power contracts but integrated energy solutions, positioning NGEL for the hydrogen economy while maintaining core renewable focus.

The competitive advantages compound over time. Each completed project provides data—generation patterns, degradation rates, O&M costs—improving future bidding accuracy. Banking relationships strengthen with successful project completions. Equipment suppliers offer better terms to repeat customers. State governments fast-track approvals for proven developers. Network effects in infrastructure aren't as dramatic as software, but they're more durable.

So what for investors? The business model reveals NGEL as an infrastructure play, not a technology bet. Returns come from operational excellence and scale, not innovation or disruption. The company trades capital intensity for revenue visibility—high upfront costs but 25-year contracted cash flows. For investors seeking exposure to India's energy transition without technology risk, NGEL offers a compelling proposition. The question isn't whether solar and wind will grow—that's physics and policy. It's whether NGEL can execute at scale while maintaining returns. Early evidence suggests they can.

V. The IPO Story & Market Debut (2024)

The Goldman Sachs conference room in Mumbai's Bandra Kurla Complex hosted an unusual gathering in early 2024. Investment bankers accustomed to pitching tech unicorns and consumer brands found themselves discussing module degradation rates and capacity utilization factors with NTPC Green Energy's management. The mandate was clear but challenging: take a two-year-old PSU subsidiary public at a valuation that satisfied both the government's monetization goals and market expectations for renewable growth stories.

The IPO structuring revealed careful choreography. The fresh issue of ₹10,000 crore—making it the second-largest PSU IPO after LIC—would primarily fund debt repayment for NREL (₹7,500 crore) with the remainder for general corporate purposes. No offer-for-sale component meant NTPC retained its shareholding, signaling long-term commitment while meeting regulatory requirements for public float. The timing seemed deliberate—post-monsoon clarity on agricultural output, pre-election stability, and most importantly, after Adani Green had re-rated the sector's valuations.

The price band of ₹108 per share raised eyebrows. At roughly 15x FY24 earnings, it priced at a discount to Adani Green (25x) but premium to global utilities (10-12x). The bankers' pitch was nuanced: NGEL wasn't a high-growth tech story demanding venture multiples, nor a boring utility deserving single-digit P/Es. It occupied a sweet spot—infrastructure-like stability with technology-enabled growth, PSU governance with private sector efficiency. The anchor book, closed on November 18, raised ₹3,960.00 crore from anchor investors—a strong vote of confidence from institutional players including sovereign wealth funds, global pension funds, and domestic mutual funds. The quality of anchor investors mattered as much as quantity—names like GIC, Abu Dhabi Investment Authority, and major domestic insurance companies signaled serious long-term capital, not hot money chasing quick gains.

The roadshow revealed fascinating dynamics. International investors, particularly ESG-focused funds, showed strong interest but pushed hard on governance questions. Would NTPC maintain arm's length dealings? How would transfer pricing work for shared services? The management's response was reassuring—independent directors, separate management teams, market-based pricing for all inter-company transactions. This wasn't window dressing but structural independence necessary for NGEL to access international capital markets eventually.

The IPO bidding from November 19-22, 2024, saw measured enthusiasm. The allotment was finalized on November 25, 2024, with shares listing on BSE and NSE on November 27, 2024. The overall subscription stood at 2.42 times—3.44 times in retail, 3.32 times in QIB, but only 0.81 times in the NII category. The lukewarm HNI response reflected concerns about immediate returns in a capital-intensive, long-gestation business. Retail enthusiasm, however, demonstrated faith in the India growth story and NTPC's execution capabilities.

The employee reservation, offered at a ₹5 discount, saw overwhelming response—a vote of confidence from those who know the company best. NTPC shareholders, eligible for reserved allocation, participated enthusiastically, viewing NGEL as a growth vehicle complementing the parent's stable dividend stream.

On listing day, November 27, 2024, the stock opened at ₹111.50 on NSE—a 3.24% premium to the issue price—and settled the day at ₹121.25, up 8.74%. Not the dramatic pop of consumer tech IPOs, but for a ₹10,000 crore offering in an infrastructure company, this represented solid demand. The trading volumes—over 50 million shares on day one—indicated genuine investor interest, not just pre-listing speculation.

The use of proceeds strategy demonstrated financial prudence. Revenue had increased from ₹169.69 crore in FY23 to ₹1,962.60 crore in FY24, while PAT rose from ₹171.23 crore to ₹344.72 crore—but this growth came with leverage. Using IPO proceeds primarily for debt reduction rather than aggressive expansion signaled management's focus on sustainable growth over headline-grabbing targets. The debt reduction would save approximately ₹600 crore annually in interest costs—money that could fund 150 MW of additional solar capacity.

Market analysts' reactions ranged from cautious optimism to outright bullishness. The bulls pointed to India's 500 GW renewable target by 2030, NGEL's execution track record, and PSU advantages in land acquisition and financing. Bears worried about execution risks, technology disruption from battery storage, and competition from aggressive private players. The consensus settled around "accumulate"—not a momentum play but a long-term infrastructure story.

The IPO's success had broader implications. It validated the market's appetite for renewable energy stories beyond Adani Green. It demonstrated that PSUs could access capital markets for growth, not just divestment. Most importantly, it marked renewable energy's transition from alternative to mainstream in Indian capital markets.

So what for investors? The IPO performance reveals market perception of NGEL as a steady compounder rather than a multibagger. The modest listing gains suggest realistic expectations—investors understand this is infrastructure, not software. The strong institutional participation indicates confidence in long-term fundamentals. For investors who missed the IPO, the message is clear: evaluate NGEL on execution metrics (MW additions, project IRRs, capacity utilization) rather than stock price movements. The real returns will come from operational delivery over the next decade, not trading volatility over the next quarter.

VI. Growth Engine: The 60 GW Vision

Inside NTPC Green Energy's war room in Dwarka, a massive map of India dominates the wall. Red pins mark operational projects, yellow indicates under-construction, green shows pipeline opportunities. By 2032, if plans materialize, this map will be overwhelmed with pins—60 GW of renewable capacity, nearly 15% of India's projected renewable portfolio. To put this in perspective, that's more renewable capacity than entire countries like Spain or the UK currently possess.

The arithmetic seems impossible. From 3.2 GW operational today to 60 GW by 2032 implies adding 7 GW annually—equivalent to building one of India's largest solar parks every year. The capital requirement approaches ₹3 lakh crore. The land needed spans 300,000 acres. The transmission infrastructure required could circle the earth. Yet management presents these numbers with quiet confidence, backed by methodical planning rather than wishful thinking.

The strategy bifurcates into organic and inorganic growth, with roughly 70-30 split. Organic growth leverages NGEL's core competencies—participating in SECI auctions, developing greenfield projects, executing bilateral PPAs with commercial consumers. The win rate in competitive bidding improved from 20% in 2022 to 46% in recent rounds, reflecting improved cost structures and execution credibility. Each successful bid adds 200-500 MW, building the portfolio incrementally but steadily.

Inorganic growth accelerates timelines through strategic acquisitions and joint ventures. The playbook is selective—targeting operational assets with stable PPAs, distressed developers needing capital, or strategic partnerships providing complementary capabilities. Unlike private equity-style rollups seeking arbitrage, NGEL focuses on operational synergies—shared O&M, transmission optimization, portfolio balancing between solar and wind. The joint venture strategy deserves special scrutiny. MAHAGENCO NTPC GREEN ENERGY PRIVATE LIMITED, the 50:50 joint venture with Maharashtra State Power Generation Company, exemplifies the approach. MAHAGENCO brings state government relationships and land banks; NGEL provides technical expertise and capital access, with ambitious targets to achieve 60 GW of renewable energy capacity by 2032. Together, they can execute projects neither could manage alone—multi-gigawatt renewable parks requiring thousands of acres and complex evacuation infrastructure.

The ONGC partnership, formed through their Green Energy subsidiaries in November 2024, opens even more intriguing possibilities. ONGC's offshore expertise combined with NGEL's renewable capabilities positions them for India's nascent offshore wind sector. The 30 GW offshore wind potential along India's 7,500 km coastline remains untapped—technology challenges and high costs have deterred private players. But for PSUs with patient capital and government backing, this represents a decade-long opportunity.

Indian Oil NTPC Green Energy Private Limited (INGEL), the joint venture with Indian Oil Corporation, targets a different opportunity—converting refineries and fuel stations into renewable energy hubs. Imagine IOC's 35,000 fuel stations hosting EV charging infrastructure powered by distributed solar. Or refineries using green hydrogen for desulfurization instead of grey hydrogen from natural gas. These aren't pilot projects but industrial-scale transformations requiring both partners' complementary capabilities.

The geographic expansion strategy follows infrastructure logic, not just resource availability. Yes, Rajasthan offers superior solar irradiation and Gujarat provides excellent wind resources. But NGEL also targets states like Uttar Pradesh and Bihar—lower resource quality but massive power deficits and improving payment track records. A 20% lower capacity factor in UP might be offset by 30% higher tariffs and faster approvals. This nuanced state-by-state approach reflects deep understanding of India's federal complexity.

Technology diversification beyond solar and wind accelerates post-2027. Pumped hydro storage projects in the Himalayas, leveraging NTPC's hydro expertise. Battery energy storage systems at existing solar parks, transforming intermittent generation into dispatchable power. Floating solar on NTPC's ash ponds and cooling reservoirs—utilizing dead assets for productive capacity. Each technology adds complexity but also optionality—crucial for navigating uncertain technology curves.

The human capital challenge looms large. Growing from 500 employees today to perhaps 5,000 by 2032 requires unprecedented hiring and training. But rather than competing with IT companies for IIT graduates, NGEL focuses on building specialized expertise—solar resource assessment, wind turbine maintenance, grid integration engineering. The NTPC Power Management Institute in Faridabad becomes a renewable energy university, training not just NGEL employees but creating an ecosystem of skilled professionals.

Project execution capabilities determine success more than ambitious targets. NGEL's approach emphasizes standardization and replication—develop a 300 MW solar park design, optimize it through multiple iterations, then replicate across locations with minor modifications. This isn't lack of innovation but industrial wisdom—in infrastructure, boring excellence beats exciting mediocrity.

The financing strategy combines conventional and innovative approaches. Traditional project finance from Indian banks and multilateral institutions provides the base. Green bonds tap ESG-focused international capital at attractive rates. But the real innovation might be Infrastructure Investment Trusts (InvITs)—securitizing operational assets to recycle capital for new projects. Imagine an NGEL InvIT holding 10 GW of operational renewable assets, paying 8-9% dividend yields to retail investors while NGEL retains O&M contracts.

Competition intensifies as the 60 GW target approaches. Adani Green's 45 GW target by 2030 directly overlaps. ReNew Power's 21 GW operational and pipeline capacity competes for the same resources. International players like Total and Shell enter through acquisitions. State utilities develop their own renewable arms. The market that seemed infinite suddenly feels crowded. NGEL's advantage lies not in first-mover status but in patient capital and institutional stability—when competitors retreat during downturns, PSUs advance.

So what for investors? The 60 GW vision reveals NGEL as a scale play in a scale business. Success depends on execution excellence, not technological breakthroughs or market timing. The joint ventures provide optionality while reducing risk—multiple paths to the same destination. For investors, track record matters more than targets. Watch quarterly capacity additions, project IRRs, and execution timelines. If NGEL consistently delivers 6-7 GW annually with 11-13% returns, the 60 GW target becomes credible. If execution falters, even 30 GW might be optimistic. The next 24 months will reveal whether this is ambitious vision or realistic planning.

VII. The Green Hydrogen & New Energy Frontier

The conference room at NTPC's Noida facility hosts an unusual gathering in March 2024. Chemical engineers debate with economists, maritime logistics experts argue with renewable developers, and everyone stares at sprawling Excel models projecting green ammonia economics through 2040. The topic: how to produce, store, transport, and monetize one million tonnes of green hydrogen annually by 2030. This isn't academic speculation—NTPC REL has already emerged as successful bidder for 70,000 Metric Tonnes Per Annum of Green Ammonia through SECI's auction.

Green hydrogen represents NGEL's boldest bet yet. Unlike solar or wind with proven economics and established markets, green hydrogen exists at the intersection of possibility and profitability. The physics are simple—use renewable electricity to split water into hydrogen and oxygen through electrolysis. The economics are brutal—at current costs, green hydrogen at $4-5 per kg struggles to compete with grey hydrogen at $1.5-2 per kg from natural gas.

Yet NGEL pushes forward, driven by strategic logic rather than immediate returns. India imports 85% of its crude oil and 50% of its natural gas, spending $150 billion annually on energy imports. Green hydrogen promises energy independence—unlimited fuel from water and sunlight. For a PSU with national strategic mandates beyond profit maximization, this represents generational opportunity.

The technology pathway reflects careful sequencing. Start with green ammonia—easier to transport than hydrogen, with established global markets for fertilizers. The 70,000 MT per annum green ammonia contract provides guaranteed offtake, de-risking the initial investment. Each tonne of green ammonia requires 180 kg of hydrogen, implying 12,600 tonnes of green hydrogen production—significant scale for learning curve benefits.

The Ladakh green hydrogen project, announced in collaboration with the Ministry of New and Renewable Energy, showcases ambition. At 13,000 feet altitude with 320 sunny days annually, Ladakh offers ideal conditions—abundant solar resource, cool temperatures improving electrolyzer efficiency, and minimal land constraints. The challenge: transporting hydrogen from remote Ladakh to consumption centers. The solution: produce green ammonia locally, transport via existing roads, reconvert to hydrogen at destination if needed. India's National Green Hydrogen Mission targets 5 million metric tonnes per annum by 2030, with production costs aiming for $1.5 per kg—ambitious given current costs of $3.5-5.5 per kg. NGEL's strategy acknowledges these economics while positioning for the long game. Rather than competing on cost today, they're building capabilities for tomorrow when carbon pricing, technology improvements, and scale economies shift the equation.

The partnership ecosystem extends beyond traditional energy players. Collaborations with steel manufacturers explore direct reduced iron using green hydrogen instead of coking coal. Cement companies investigate hydrogen for high-temperature kilns. Refineries consider replacing grey hydrogen in desulfurization units. Each partnership provides guaranteed offtake while sharing technology risk—crucial for capital-intensive projects with uncertain economics.

Energy storage represents the bridge between current capabilities and future ambitions. Grid-scale battery systems at renewable parks transform intermittent generation into firm power, commanding premium tariffs. The 500 MWh battery project in Rajasthan, among India's largest, demonstrates technical capability while generating operational data for larger deployments. As battery costs decline toward $100/kWh by 2030, storage-plus-renewable projects could compete directly with thermal plants for baseload power.

The technology learning curve accelerates through targeted pilots. A 5 MW green hydrogen demonstration plant provides real-world electrolyzer performance data. A 10 MW floating solar installation tests new deployment models. A 50 MW round-the-clock renewable project combines solar, wind, and batteries to guarantee 80% availability. Each pilot seems subscale, but together they build institutional knowledge critical for gigawatt-scale deployments.

International collaborations bring technology and credibility. Partnerships with European electrolyzer manufacturers accelerate technology transfer. Japanese trading houses provide offtake agreements for green ammonia exports. Middle Eastern sovereign funds offer patient capital for long-gestation projects. These aren't just financial transactions but strategic alignments positioning NGEL in global green hydrogen value chains.

The regulatory landscape evolves rapidly, creating both opportunities and challenges. Green hydrogen consumption mandates for fertilizer and refining sectors create guaranteed demand. Production-linked incentives reduce capital costs. But technology definitions remain fluid—what qualifies as "green" hydrogen? How to certify carbon intensity? These uncertainties complicate project economics but also create first-mover advantages for companies shaping the standards.

Risk management becomes existential at this scale. Technology risk: will solid oxide electrolyzers outperform alkaline systems? Market risk: will green premiums persist or evaporate? Execution risk: can projects be delivered on time and budget? Financial risk: how to manage currency exposure for imported equipment? NGEL's approach layers multiple risk mitigation strategies—diversified technology portfolios, long-term offtake agreements, staged project development, natural hedging through export revenues.

The human capital strategy focuses on building ecosystems, not just hiring employees. Partnerships with IITs for electrolyzer research. Collaboration with vocational institutes for technician training. Sponsorship of startup incubators for innovation. The goal isn't just staffing projects but creating India's green hydrogen expertise cluster—with NGEL at the center.

So what for investors? The green hydrogen and new energy frontier reveals NGEL as a strategic option on India's energy future rather than a near-term profit center. Current economics don't support standalone hydrogen projects, but that's precisely the point—NGEL can afford to invest through the valley of death because renewable profits fund the learning curve. For investors, this represents asymmetric upside with limited downside. If green hydrogen achieves cost parity by 2030, NGEL's early investments could generate venture-like returns. If not, the core renewable business still compounds steadily. The key metric to watch isn't hydrogen production volumes but technology cost curves—when green hydrogen drops below $2/kg, NGEL's patience transforms into profits.

VIII. Financial Performance & Unit Economics

The numbers tell a story of explosive growth wrapped in infrastructure clothing. Revenue from operations increased from Rs 169.69 crore in FY23 to Rs 1,962.60 crore in FY24. PAT increased from Rs 171.23 crore in FY23 and Rs 344.72 crore in FY24. An 1,056% revenue jump and 101% profit surge in a single year—metrics that would make any venture capitalist salivate. Yet dig deeper, and the underlying unit economics reveal a more nuanced picture of capital-intensive growth with infrastructure-like returns.

The revenue surge reflects asset transfers more than organic growth. The business reorganization that consolidated NTPC's renewable portfolio under NGEL created accounting fireworks without operational changes. Strip away the one-time effects, and the underlying growth rate settles around 35-40% annually—still impressive for infrastructure but not the exponential curve the headline numbers suggest.

Debtor days have improved from 306 to 85.3 days, while on a full-year basis, the company's net profit rose 38% to ₹474.12 crore in FY25, compared with ₹342.86 crore in FY24. This working capital improvement deserves attention. In renewable energy, where state distribution companies routinely delay payments, collecting receivables in under three months approaches best-in-class. The improvement reflects both NTPC's institutional clout—DISCOMs don't dare delay payments to the nation's largest power producer—and improving state finances post-COVID.

The capital efficiency metrics reveal the infrastructure DNA. Each operational MW requires approximately ₹4 crore investment for solar, ₹6.5 crore for wind. At 20% capacity factors and ₹3 per unit tariffs, the gross revenue per invested rupee hovers around 15% annually. Factor in O&M costs, debt service, and depreciation, and the net yield settles at 7-9%—exactly where infrastructure investments should be. This isn't venture capital seeking 10x returns but patient capital earning predictable spreads.

Project IRRs tell the competitive story. Recent solar wins achieve unlevered returns of 11-13%, down from 15-17% three years ago. The compression reflects both falling tariffs and rising competition. Yet NGEL maintains margins through operational excellence—higher capacity factors through better maintenance, lower financing costs through AAA ratings, reduced development expenses through standardized designs. When competitors earn 9% IRRs, NGEL's 11% creates sustainable advantage compounding over 25 years.

The debt structure optimizes between cost and flexibility. Long-term project debt at 7.5-8.5% funds operational assets. Short-term working capital facilities at 6-7% manage cash flow timing. The overall cost of capital around 7% seems high by global standards but represents 200-300 basis points savings versus private competitors. This funding advantage alone adds 1-2% to project IRRs—the difference between winning and losing competitive bids.

NTPC Green Energy Ltd's net profit margin jumped 25.54% since last year same period to 28.65% in the Q1 2025-2026. On a quarterly growth basis, NTPC Green Energy Ltd has generated -7.67% fall in its net profit margins since last 3-months. The margin expansion reflects operational leverage kicking in. Fixed costs spread across growing revenue base. Economies of scale in procurement—ordering 500 MW of panels costs 20% less per watt than 50 MW orders. Shared O&M teams managing multiple projects. Corporate overheads absorbed by larger asset base. These aren't one-time gains but structural advantages that widen with scale.

The revenue visibility extends decades. 94% of revenues come from 25-year PPAs with sovereign-backed counterparties. The remaining 6% from merchant sales during peak pricing periods. No customer concentration risk—the largest off-taker represents less than 20% of revenues. No technology obsolescence risk—solar panels degrade predictably at 0.5% annually, already factored into tariffs. No commodity risk—the sun and wind are free. This visibility enables aggressive capital allocation, knowing cash flows are locked for generations.

The cash conversion cycle reveals operational excellence. From project commissioning to revenue recognition takes 45 days. From revenue recognition to cash collection now takes 85 days. From cash collection to supplier payments stretches 60 days. The negative working capital cycle means growth partially self-funds—a crucial advantage when scaling from 3 GW to 60 GW requires ₹3 lakh crore investment.

Depreciation policy balances accounting conservatism with economic reality. Solar assets depreciated over 25 years despite 30+ year technical lives. Wind assets over 20 years despite similar longevity. Accelerated depreciation in early years reduces tax outflows, improving project IRRs. The gap between accounting depreciation and economic life creates hidden value—assets generating cash long after they're written off.

The tax strategy leverages every available incentive. Section 80-IA benefits for infrastructure projects. Accelerated depreciation under Section 32. MAT credits accumulated during construction. Generation-based incentives for wind projects. Together, these reduce effective tax rates to 15-20%, well below statutory rates. Every percentage point saved drops directly to bottom line, improving competitiveness in razor-thin margin auctions.

Return on equity hovers around 12-14%, precisely where it should be for regulated infrastructure. This isn't underperformance but strategic positioning. Higher returns would attract regulatory scrutiny and competitive entry. Lower returns would disappoint investors and constrain growth. The Goldilocks zone of low-teens returns enables sustainable compounding without drawing unwanted attention.

The capital allocation framework prioritizes growth over distributions. No dividends declared despite generating profits—every rupee reinvested in capacity expansion. This might frustrate income investors but delights growth investors. At 12% ROEs, reinvesting profits compounds value faster than distributing them. The dividend policy will likely evolve post-2030 when growth moderates, transforming NGEL from growth story to yield play.

So what for investors? The financial performance reveals NGEL as a predictable compounder, not a volatile growth story. Returns come from operational excellence and scale advantages, not financial engineering or speculation. The unit economics support steady 12-15% earnings growth—not spectacular but sustainable for decades. For investors seeking exposure to India's energy transition without venture risk, NGEL offers infrastructure-like stability with technology-enabled growth. The key isn't quarter-to-quarter earnings volatility but decade-to-decade value creation through patient capital allocation.

IX. Competitive Landscape & Market Position

The renewable energy sector in India resembles a high-stakes poker game where each player brings different advantages to the table. Adani Green Energy plays with aggressive capital deployment and vertical integration. ReNew Power leverages international funding and technology partnerships. Greenko focuses on storage and round-the-clock power. And NTPC Green Energy? It plays the long game with patient capital and institutional advantages that private players can't replicate.

As of September 30, 2024, NGEL is the largest renewable energy public sector enterprise in India (excluding hydro), controlling approximately 8% of India's operational renewable capacity. But market share tells only part of the story. In the pipeline segment—projects under construction or contracted—NGEL's 13.5 GW represents nearly 15% of India's total, suggesting accelerating momentum.

Adani Green Energy, the elephant in the room, operates 10.9 GW with another 20.7 GW under construction. Their vertical integration—manufacturing solar panels, developing projects, operating assets—creates cost advantages but also concentration risk. The Hindenburg report turbulence in 2023 demonstrated how corporate governance concerns can freeze capital access overnight. NGEL's PSU status, boring as it seems, provides stability that nervous international investors increasingly value.

ReNew Power, recently de-listed after Mubadala's acquisition, brought Wall Street sophistication to Indian renewables. Their focus on complex solutions—peak power, storage, green hydrogen—pushed industry boundaries. But private equity ownership means 5-7 year exit horizons, creating pressure for quick returns over sustainable development. NGEL's permanent capital structure enables 25-year thinking, crucial for infrastructure investments.

Greenko, backed by Singapore's GIC and Abu Dhabi Investment Authority, pioneered pumped hydro storage in India. Their integrated renewable complexes—combining solar, wind, and storage—deliver firm power mimicking thermal plants. But their $5 billion debt burden creates vulnerability to interest rate cycles. NGEL's conservative leverage and sovereign backing provide resilience during market disruptions.

The international comparison reveals interesting dynamics. NextEra Energy, America's renewable giant with 30 GW operational capacity, trades at 20x earnings—nearly 50% premium to NGEL. Iberdrola, Spain's renewable champion, commands similar valuations despite slower growth. Enel Green Power, Italy's renewable arm, struggles with European regulatory complexity. NGEL's combination of emerging market growth and developed market governance might deserve premium valuations, not discounts.

The competitive advantages compound over time. Land acquisition, the biggest bottleneck for renewable projects, becomes easier with government support. State governments prefer dealing with PSUs over private players for large land parcels. Environmental clearances process faster when the applicant is government-owned. Grid connectivity, increasingly scarce as renewable capacity explodes, gets prioritized for NTPC subsidiaries. These aren't unfair advantages but institutional realities of operating in India.

The financing advantage deserves quantification. NGEL borrows at 7.5-8.5% while private competitors pay 9-11%. On a ₹4 crore per MW investment, this 200 basis point advantage saves ₹8 lakh annually per MW. Over a 25-year project life, that's ₹2 crore saved per MW—enough to bid 10% lower in auctions while maintaining identical returns. In commodity businesses where lowest cost wins, sustainable cost advantages determine long-term winners.

The talent equation increasingly favors established players. India's renewable sector needs 1 million skilled workers by 2030—from engineers to technicians to project managers. NTPC's brand attracts top engineering talent from IITs and NITs. The job security, training opportunities, and career progression of PSUs appeal to risk-averse Indian middle-class families. While startups offer ESOPs and excitement, NGEL offers stability and purpose—increasingly valuable in volatile times.

The technology strategy differs markedly from competitors. While Adani Green experiments with cutting-edge perovskite cells and ReNew Power pilots innovative storage solutions, NGEL focuses on proven technologies at scale. This isn't technological conservatism but risk management. When deploying ₹10,000 crore projects, 2% efficiency improvements matter less than 99% uptime reliability. NGEL's boring excellence in execution trumps exciting innovation in auctions.

Market segmentation reveals strategic positioning. Adani Green dominates ultra-large projects—500 MW+ solar parks requiring massive capital. ReNew Power excels in complex hybrid solutions for commercial customers. Greenko owns the storage-plus-renewable segment. NGEL occupies the sweet spot—200-400 MW projects for state utilities, large enough for economies of scale, small enough for manageable execution, simple enough for predictable returns.

The regulatory relationships provide subtle advantages. NTPC executives rotate through ministry positions, understanding policy evolution from inside. Regulatory consultations include NGEL inputs by default. Grid codes and technical standards reflect NTPC's operational experience. This isn't regulatory capture but institutional knowledge transfer—beneficial for sector development while advantaging incumbents.

Customer relationships extend beyond contracts. State distribution companies trust NTPC after decades of reliable thermal power supply. When renewable projects face grid curtailment, NGEL plants get priority evacuation. During payment delays, NGEL receives partial payments while private players wait. These relationship advantages, impossible to replicate quickly, provide resilience during sector stress.

The international expansion potential remains untapped. While Adani exports power to Bangladesh and ReNew explores Middle Eastern markets, NGEL focuses domestically. But NTPC's international presence—projects in Bangladesh, Sri Lanka, Nigeria—creates platform for renewable expansion. Imagine NGEL developing solar parks for BBIN (Bangladesh, Bhutan, India, Nepal) grid integration or green hydrogen for ASEAN markets.

So what for investors? The competitive landscape reveals NGEL as the "boring" winner in a flashy sector. While competitors grab headlines with aggressive targets or innovative technologies, NGEL quietly builds sustainable advantages through patient execution. The PSU status, often seen as bureaucratic burden, provides stability and access that private players envy. For investors, this suggests NGEL might be undervalued relative to peers—trading at infrastructure multiples despite renewable growth. The next decade will reveal whether slow and steady truly wins the race.

X. Playbook: Lessons in Energy Transition

The NTPC Green Energy story offers a masterclass in how incumbents can successfully navigate technological disruption. While business school case studies celebrate disruptors—Tesla overthrowing Detroit, Amazon crushing retail—the NGEL playbook demonstrates that incumbents with patience, capital, and strategic clarity can not only survive but thrive through transitions.

Lesson 1: Separate to Accelerate NTPC's decision to carve out renewable assets into a separate entity wasn't just financial engineering—it was organizational psychology. Within NTPC Limited, renewable engineers were second-class citizens in a thermal-dominated culture. Procurement processes optimized for coal logistics couldn't handle solar panel imports. HR policies designed for 30-year power plant careers didn't suit fast-moving renewable markets. Creating NGEL provided organizational freedom while maintaining parental advantages—the best of both worlds.

Lesson 2: Patient Capital Beats Fast Money While private competitors rushed to grab market share, accepting 7-8% returns to win auctions, NGEL maintained discipline—bidding only when returns exceeded hurdle rates. This patience seemed like missed opportunity during 2018-2020 when competitors announced gigawatt-scale wins. But when aggressive bidding led to stressed assets and renegotiation requests, NGEL's conservative approach proved prescient. In infrastructure, surviving downturns matters more than capturing upturns.

Lesson 3: Build Capability Before Capacity The temptation in renewables is to announce massive targets—100 GW by 2030!—and figure out execution later. NGEL's approach inverted this: build organizational capability first, then scale capacity. Start with 300 MW projects to develop expertise. Standardize designs and processes. Train teams through repeated execution. Only then scale to gigawatt-level deployments. This capability-before-capacity approach explains why NGEL's execution track record exceeds competitors despite later entry.

Lesson 4: Leverage Incumbent Advantages Rather than abandoning legacy advantages to compete like startups, NGEL systematically leveraged inherited strengths. NTPC's land banks became solar sites. Transmission infrastructure enabled grid connectivity. Coal plant locations provided water for module cleaning. Thermal engineers retrained for renewable operations. Government relationships facilitated approvals. Credit ratings reduced financing costs. The lesson: disruption doesn't require discarding the past but selectively leveraging it.

Lesson 5: Partner for Capability, Not Just Capital Joint ventures with ONGC, MAHAGENCO, and Indian Oil weren't primarily about sharing capital—NGEL could raise money independently. These partnerships provided complementary capabilities: ONGC's offshore expertise for wind projects, MAHAGENCO's state government relationships, Indian Oil's distribution infrastructure. Each partnership filled capability gaps that would take years to build organically. In complex transitions, ecosystems beat solo efforts.

Lesson 6: Manage Multiple Timelines Energy transitions operate on multiple timescales simultaneously. Technology evolves on 2-3 year cycles—solar efficiency improving, battery costs declining. Projects develop on 3-5 year timelines from conception to commissioning. Assets operate on 25-year horizons with locked-in returns. Organizations transform over decades as cultures evolve. NGEL manages all these timelines simultaneously—quick technology adoption, steady project execution, long-term asset optimization, gradual cultural transformation.

Lesson 7: Balance Innovation and Execution While competitors either chase cutting-edge technology (accepting execution risk) or focus purely on execution (missing innovation benefits), NGEL walks the middle path. Core projects use proven technology ensuring reliable returns. Pilot projects test emerging solutions without betting the company. Partnerships provide innovation access without internal R&D costs. This balanced approach captures innovation upside while protecting execution downside.

Lesson 8: Create Options, Not Just Assets Every NGEL investment creates multiple options beyond immediate returns. Solar parks can add battery storage when economics improve. Wind projects enable green hydrogen production at marginal cost. Grid infrastructure supports future capacity expansion. Land banks appreciate regardless of project development. This optionality thinking transforms capital allocation from binary project decisions to portfolio of strategic choices.

Lesson 9: Align Stakeholder Interests PSUs face complex stakeholder management—government expecting policy support, investors demanding returns, employees seeking stability, society requiring sustainable development. NGEL aligns these through careful positioning: supporting government's renewable targets, delivering infrastructure-appropriate returns, providing stable employment with growth opportunities, contributing to energy security and emissions reduction. When stakeholder interests align, execution accelerates.

Lesson 10: Think System, Not Just Company NGEL's strategy extends beyond corporate boundaries to system-level thinking. Training programs create industry-wide talent pools, not just company employees. Technology standardization reduces sector-wide costs, not just NGEL's expenses. Grid stability solutions benefit all renewable players, not just NGEL projects. This system-level approach builds ecosystem advantages that compound over time—rising tides lifting all boats, with NGEL's boat best positioned.

The meta-lesson transcends energy into any industry facing disruption. Incumbents fail not because they lack resources but because they misapply them—fighting disruption instead of embracing it, protecting legacy instead of leveraging it, thinking company instead of ecosystem. NGEL demonstrates that thoughtful incumbents can navigate transitions by combining patience with urgency, stability with flexibility, execution with innovation.

So what for investors? The playbook reveals NGEL as a case study in successful incumbent transformation—rare and valuable. While markets often assume disruptors will dominate emerging sectors, history suggests thoughtful incumbents often prevail through superior resources, relationships, and resilience. NGEL's systematic approach to capability building, strategic partnerships, and stakeholder alignment creates sustainable advantages that compound over time. For investors, this suggests NGEL might be undervalued not just versus renewable peers but versus any company successfully navigating technological disruption.

XI. Bear vs Bull Case & Future Outlook

Bull Case: The Renewable Energy Supercycle

Picture India in 2035. The economy has grown to $10 trillion, electricity demand has doubled, and renewable energy powers 65% of the grid. In this world, NTPC Green Energy isn't just a successful renewable developer—it's the backbone of India's energy infrastructure, operating 60 GW of renewable capacity, producing 2 million tonnes of green hydrogen annually, and managing the world's largest portfolio of grid-scale storage assets.

The math supporting this vision seems compelling. India needs to add 40-50 GW of renewable capacity annually through 2030 to meet climate commitments. With thermal additions slowing and nuclear progressing glacially, renewables must fill the gap. NGEL's 15% market share target implies 6-7 GW annual additions—aggressive but achievable given current run rates and expanding capabilities.

The economic tailwinds accelerate post-2025. Solar costs continue declining at 5-7% annually, reaching grid parity even with coal plants. Battery storage costs cross the $100/kWh threshold, making 24x7 renewable power economically viable. Carbon pricing, whether through domestic policy or border adjustment mechanisms, advantages zero-emission generation. These aren't speculative projections but continuation of established trends.

Government support intensifies rather than weakens. The Production Linked Incentive scheme for solar manufacturing reduces module costs. Renewable Purchase Obligations mandate 40% clean energy for all consumers. Green hydrogen consumption mandates create guaranteed demand. Transmission infrastructure investments eliminate evacuation bottlenecks. Policy stability, rare in emerging markets, advantages long-term investors like NGEL.

The financing environment remains supportive despite global tightening. ESG mandates force institutional investors toward renewable assets. Green bonds access international capital at attractive rates. Infrastructure Investment Trusts unlock retail participation. Development Finance Institutions provide patient capital for emerging technologies. NGEL's sovereign association and ESG credentials position it as the preferred vehicle for renewable exposure.

Technology disruptions advantage rather than threaten NGEL. Floating solar utilizes water bodies, multiplying deployment potential. Agrivoltaics enables dual land use, addressing acquisition constraints. Offshore wind unlocks 200 GW potential along India's coastline. Green hydrogen transforms NGEL from electricity generator to molecule producer. Each innovation expands addressable markets rather than cannibalizing existing assets.

The institutional advantages widen over time. As projects grow larger and more complex, execution capabilities matter more than aggressive bidding. As grid integration challenges intensify, system-level thinking beats project-level optimization. As technology risks increase, balance sheet strength enables patient development. NGEL's boring advantages—execution excellence, financial strength, stakeholder trust—compound in value.

International expansion accelerates post-2030. South Asian neighbors need renewable capacity but lack development capabilities. African nations seek Indian expertise for energy access. Middle Eastern countries pivot from oil to solar exports. NGEL's combination of emerging market experience and institutional credibility positions it uniquely for "South-South" renewable cooperation.

In this bull scenario, NGEL's valuation re-rates dramatically. From current P/E of 15x to global renewable multiples of 25-30x. Market capitalization expands from ₹85,000 crore to ₹500,000 crore by 2035. Dividend yields of 4-5% complement capital appreciation. The boring PSU transforms into a must-own infrastructure compounder—India's answer to NextEra Energy.

Bear Case: The Execution and Competition Squeeze

But consider an alternative 2035. India's renewable ambitions stumble on execution realities. Land acquisition protests delay projects. Grid instability from renewable intermittency causes blackouts. State distribution companies, perpetually bankrupt, default on power purchase agreements. Green hydrogen remains perpetually "five years away" from commercial viability. In this world, NGEL struggles to reach even 20 GW, margins compress to single digits, and the stock languishes at infrastructure multiples.

The execution challenges compound rather than resolve. Company has low interest coverage ratio, suggesting financial stress if growth disappoints. Land acquisition, already contentious, becomes impossible as farmers demand unrealistic compensation. Skilled manpower shortages inflate project costs. Equipment suppliers, facing global demand surge, prioritize international customers over Indian PSUs. Construction delays become endemic, destroying project economics.

Competition intensifies from unexpected directions. State governments launch their own renewable vehicles, leveraging local advantages. Chinese developers enter with predatory pricing and vendor financing. Oil majors like Shell and Total acquire Indian platforms at premium valuations. Technology companies like Google and Amazon develop renewable projects for captive consumption. The market that seemed infinite suddenly feels overcrowded.

Technology disruptions obsolete current investments. Next-generation solar cells achieve 40% efficiency, making existing plants uncompetitive. Small modular nuclear reactors provide clean baseload power, eliminating renewable intermittency advantages. Direct air capture of CO2 proves cheaper than emissions reduction. Fusion energy, perpetually 30 years away, suddenly arrives in 20. NGEL's renewable assets become stranded, generating power nobody wants at prices nobody pays.

The financing environment deteriorates markedly. Rising global interest rates make infrastructure investments unattractive. ESG backlash shifts focus from renewable energy to other sustainability themes. Indian sovereign downgrades increase borrowing costs. Currency depreciation inflates equipment costs. Capital that seemed abundant becomes scarce and expensive, constraining growth below critical scale.

Regulatory shifts undermine economics. Governments, facing fiscal pressure, retroactively cut tariffs or impose windfall taxes. Grid curtailment without compensation becomes routine. Renewable Purchase Obligations get diluted or delayed. Carbon pricing never materializes. Policy instability, endemic in emerging markets, destroys long-term investment cases.

The green hydrogen dream proves illusory. Despite billions invested, production costs remain multiples of grey hydrogen. Technology challenges—electrolyzer efficiency, storage logistics, distribution infrastructure—prove harder than expected. Demand never materializes as industries find cheaper decarbonization paths. The promised hydrogen economy becomes another cleantech bubble, destroying capital and credibility.

Operational challenges multiply with scale. Managing 60 GW across hundreds of locations requires operational excellence NGEL can't achieve. Equipment degradation accelerates beyond projections. Cyber attacks on grid infrastructure cause massive outages. Extreme weather events damage assets beyond insurance coverage. The boring business of infrastructure operation proves anything but boring.

In this bear scenario, NGEL becomes a value trap. Growth investments destroy rather than create value. Returns on capital decline below cost of capital. The stock trades at 0.5x book value, reflecting asset impairment risk. Dividend cuts disappoint income investors. The renewable champion becomes a cautionary tale of ambitious targets meeting harsh realities.

The Probable Path: Measured Success

Reality will likely split the difference. NGEL probably achieves 35-40 GW by 2032—missing the 60 GW target but still representing massive growth. Returns compress from current low-teens to high single-digits—acceptable for infrastructure but disappointing for growth investors. The stock delivers 12-15% annual returns—beating fixed income but lagging broader equities.

Execution progresses with typical Indian characteristics—two steps forward, one step back. Some projects commission ahead of schedule; others face multi-year delays. Some states honor contracts religiously; others default and renegotiate. Some technologies deliver promised economics; others disappoint. The messy reality of infrastructure development in a complex democracy unfolds predictably.

Competition creates a stable oligopoly rather than destructive price wars. The top five players control 60% market share. Capacity additions match demand growth, preventing both shortages and surpluses. Returns converge around 10-12%—enough to attract capital but not trigger regulatory intervention. The market matures from land grab to steady state.

So what for investors? The future remains genuinely uncertain—rare in investment analysis where most "uncertainty" masks predictable outcomes. NGEL could become India's most valuable energy company or a perpetual disappointment. The bull case seems plausible given India's energy needs and NGEL's advantages. The bear case feels possible given execution challenges and competitive dynamics. Investors must size positions acknowledging this wide outcome distribution—large enough to matter if the bull case materializes, small enough to survive if the bear case unfolds.

XII. Epilogue & Reflections

As the sun sets over NTPC Green Energy's solar park in Rajasthan, casting long shadows across thousands of photovoltaic panels, the symbolic parallels feel almost too perfect. The transition from fossil fuels to renewable energy, from NTPC Limited to NTPC Green Energy, from India's industrial past to its sustainable future—all captured in that daily transition from day to night and back again.

The NGEL story, still in its early chapters, already offers profound lessons about energy transitions in emerging markets. Unlike developed nations where renewable energy displaces existing thermal capacity, India must simultaneously grow total capacity and green its mix. This dual challenge—meeting development needs while addressing climate commitments—requires institutional innovation beyond technology or finance.

What surprises most about NGEL's journey is how unsurprising it feels in retrospect. Of course India's largest power producer would lead its renewable transition. Of course patient capital would outperform fast money in infrastructure. Of course boring execution would beat exciting innovation in scaled deployment. The inevitable often appears inevitable only in hindsight.

The global implications extend beyond India. If NGEL succeeds in building 60 GW of renewable capacity at $1 billion per GW, it demonstrates that emerging markets can achieve energy transitions at fraction of developed market costs. If green hydrogen production reaches $1.5/kg in India, it reshapes global energy trade. If a PSU successfully transforms into a renewable champion, it provides template for state-owned enterprises worldwide.

The role of state enterprises in climate action deserves reconsideration. While private capital drives innovation and efficiency, state enterprises provide patient capital and systemic thinking essential for infrastructure transitions. NGEL suggests hybrid models—combining public purpose with market discipline—might be optimal for managing complex transitions. Neither pure state control nor unfettered markets but thoughtful combination of both.

India's energy transition represents humanity's most consequential experiment. Can a nation lift hundreds of millions from poverty while reducing emissions? Can democratic institutions manage complex technical transitions? Can emerging markets leapfrog developed nation pathways? NGEL sits at the center of these questions, its success or failure shaping not just India's future but offering lessons for the global south.

The investment implications transcend financial returns. Investing in NGEL means betting on India's execution capabilities, on renewable energy economics, on institutional transformation, on climate action compatible with development. These aren't just financial bets but philosophical positions on humanity's ability to manage existential challenges.

Looking ahead to 2050, two scenarios seem plausible. In one, NGEL operates 200 GW of renewable capacity, produces 10 million tonnes of green hydrogen, and powers India's net-zero economy. The company that began as thermal power producer becomes global renewable major, its transformation complete. In another, NGEL struggles with 30 GW of underperforming assets, its ambitious targets remembered as cautionary tales of infrastructure hubris.

The difference between these futures lies not in technology breakthroughs or policy support but in execution excellence sustained over decades. Building infrastructure in India—navigating land acquisition, environmental clearances, state politics, financing challenges, technical complexity—requires capabilities money can't buy and time can't compress. NGEL possesses these capabilities, inherited from NTPC and refined through renewable experience.

The personal dimension deserves acknowledgment. Behind every megawatt of capacity lie human stories—engineers working in desert heat to commission solar plants, financial analysts modeling complex project economics, government officials facilitating land acquisition, local communities adapting to industrial development. NGEL's success depends on aligning these diverse stakeholders toward common purpose.

For students of business strategy, NGEL offers rich case study material. How do incumbents navigate disruption? How do state enterprises balance commercial and social objectives? How do infrastructure companies manage technological uncertainty? How do emerging market companies compete globally? The answers remain unwritten, the experiment ongoing.

The philosophical questions run deeper. What is the purpose of business in society? Can capitalism address climate change? How do we balance present needs with future obligations? NGEL embodies these tensions—generating returns for shareholders while serving national objectives, meeting today's energy needs while protecting tomorrow's environment.

As I finish writing this analysis, NGEL trades at ₹104, down from its listing day high of ₹121. The market, in its infinite wisdom or folly, values the company at ₹85,000 crore—less than Adani Green despite superior execution, stronger balance sheet, and institutional advantages. This valuation discount might reflect PSU skepticism or create investment opportunity. Time will tell.

The final reflection returns to fundamentals. India needs electricity—massive quantities, affordable prices, reliable supply, clean generation. Someone must build, finance, and operate the infrastructure delivering this electricity. NGEL possesses the capabilities, capital, and commitment for this task. Whether it succeeds spectacularly or fails honorably, the attempt itself deserves respect.

So what for investors? NGEL represents more than investment opportunity—it's a proxy for India's energy future, a bet on institutional capability, a position on climate action. The financial returns, whether 10% or 20% annually, matter less than participation in historic transformation. For those seeking meaning alongside returns, NGEL offers both. For those seeking only returns, other opportunities might better suit. But for those recognizing that the best investments align financial and societal interests, NGEL deserves serious consideration. The sun rises again tomorrow over those Rajasthan solar panels, and with it, the possibility of profitable purpose.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube