NAVA Limited: The Ferro Alloy to African Power Play

I. Introduction & Episode Setup

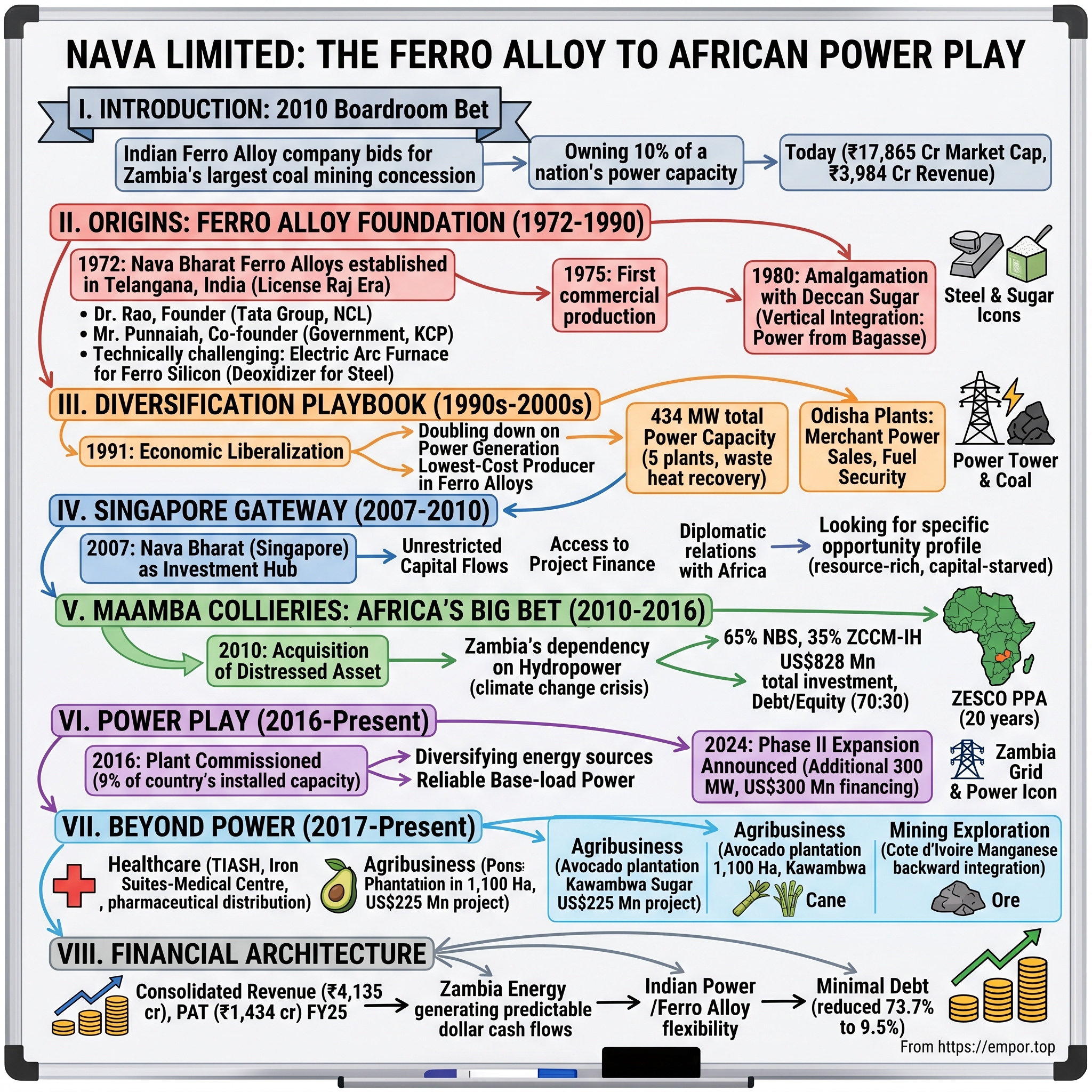

Picture this: It's 2010, and in a boardroom in Singapore, executives from an Indian ferro alloy company are about to make the most audacious bet in their 38-year history. They're bidding for Zambia's largest coal mining concession—a move that would eventually see them owning 10% of an entire nation's power generation capacity. The company? NAVA Limited, a name most Indian investors associate with mundane ferro alloys, not African infrastructure adventures. Today, NAVA trades at a market cap of ₹17,865 Crore with revenue of ₹3,984 Cr, a testament to a journey that began in the humblest of circumstances. This isn't your typical conglomerate story—it's about how a company born in India's License Raj era transformed itself into a player controlling critical infrastructure thousands of miles away in Africa.

Walk through any industrial zone in Telangana, and you'll find ferro alloy plants humming away, producing essential inputs for steel. But NAVA's plants tell a different story. They're connected to a web that stretches from Indian power grids to Zambian copper mines, from Singapore boardrooms to Ivorian manganese fields. The question that fascinates: How did a company that started making ferro silicon—a commodity so unglamorous that most investors can't even describe what it does—end up becoming indispensable to Zambia's electrical grid?

The answer lies in a series of calculated bets, each more audacious than the last. While Indian conglomerates were rushing to acquire assets in developed markets during the 2000s boom, NAVA looked to Africa—specifically to Zambia, a landlocked nation where 96% of electricity came from hydropower and climate change was turning that dependency into a national crisis. In 2010, they saw what others missed: an opportunity to solve a nation's energy problem while building a business moat so deep it would be nearly impossible to replicate.

The company operates 5 power plants in Telangana, Odisha, and AP, with a total installed capacity of 434 MW. It also manages Zambia's sole integrated thermal power plant of 300 MW, with plans to add another 300 MW for $400 Mn. But these numbers only scratch the surface of what's really happening here. This is a story about understanding the intersection of commodities, power, and emerging market politics—and playing that game better than anyone else.

The themes we'll explore resonate far beyond NAVA: How do you build lasting competitive advantages in frontier markets? What happens when a company's success becomes intertwined with a nation's development? And perhaps most intriguingly, how does a traditional industrial company reinvent itself for a world where the old playbooks no longer work?

II. Origins: The Ferro Alloy Foundation (1972-1990)

The year was 1972. India had just won its war with Pakistan, Indira Gandhi was consolidating power, and the License Raj controlled every aspect of industrial production. Into this environment stepped a group of entrepreneurs in Telangana with a simple plan: build a ferro silicon smelter. They called it Nava Bharat Ferro Alloys Limited—"Nava Bharat" meaning "New India" in Hindi, a name that captured the post-independence industrial optimism of the era. Established in 1972 with a single smelter for Ferro Silicon Alloys in Telangana, India, the company was founded by Dr. Rao, who had returned to India after making significant contributions to organizations including the Tata Group and National Chemical Laboratory in Pune. The founding location—Paloncha, a small town on the banks of the Godavari River in what was then Andhra Pradesh—was chosen for its proximity to both water resources crucial for cooling and railway connectivity for raw material transport.

But what exactly is ferro silicon, and why did it matter so much in 1970s India? Ferro silicon is an alloy of iron and silicon used primarily in steel manufacturing to deoxidize the steel and improve its quality. In the controlled economy of the License Raj, where every ton of steel production was planned by bureaucrats in Delhi, securing a license to produce ferro alloys was like getting permission to print money—assuming you could navigate the technical challenges.

The founding team also included Mr. Punnaiah, who brought unique government connections, having started his career as an Employment Exchange Officer with the Government of India in 1947. The British government had even sent him to the U.K. for an in-depth study of employment exchange practices. He later took leadership roles at prominent manufacturing firms like KCP Limited and Jeypore Sugar Company Limited before co-founding NAVA.

The technical challenges were immense. Building a ferro alloy smelter required mastering electric arc furnace technology—essentially creating miniature lightning bolts to melt iron ore and silica at temperatures exceeding 2,000°C. The electricity consumption was staggering: producing one ton of ferro silicon consumed about 8,500 kWh of power, enough to power an average Indian household for nearly four years at that time.

By 1975, they achieved first commercial production of Ferro Silicon Alloys at Paloncha. The timing was fortuitous. India's steel production was ramping up as part of the government's heavy industrialization push, and domestic ferro alloy production was seen as critical to reducing import dependence. NAVA's early customers included the steel plants of SAIL (Steel Authority of India Limited), and the company quickly established a reputation for quality that would become its calling card.

But the real stroke of genius came in 1980 with the amalgamation of Deccan Sugar & Abkhari Company Ltd., instantly transforming NBFAL into a diversified entity producing sugar, rectified spirit, and extra neutral alcohol. This wasn't random diversification—it was strategic vertical integration before anyone called it that. The sugar business came with captive power generation from bagasse (sugarcane waste), providing a hedge against the massive electricity costs of ferro alloy production.

Think about the elegance of this move: sugar mills operate seasonally, typically for 150-180 days when sugarcane is harvested. The rest of the year, their power generation capacity sits idle. By combining sugar and ferro alloys, NAVA could use the sugar mill's power plant year-round, dramatically improving capital efficiency. When sugar prices were high, they could sell sugar and buy power from the grid for ferro alloys. When power prices spiked, they could reduce ferro alloy production and sell power to the grid. It was a real options strategy executed through industrial assets.

The 1980s saw further consolidation as NBFAL acquired 76% equity in Andhra Foundry and Machine Company Ltd. (AFML), eventually leading to its full amalgamation in 1990. This brought engineering capabilities in-house, allowing NAVA to maintain and upgrade its furnaces without depending on expensive foreign consultants—a critical advantage when foreign exchange was scarce and heavily regulated.

The scale of ambition was remarkable for the time. While most Indian industrial houses were content with single-plant operations, NAVA was already thinking about integrated industrial complexes. By the late 1980s, the Paloncha complex had grown to include multiple furnaces producing different grades of ferro alloys, a captive power plant, and even employee townships—a self-contained industrial ecosystem in rural Telangana.

But perhaps the most prescient move was the company's early focus on power generation. While others saw electricity as merely an input cost to be minimized, NAVA's founders recognized that in a power-deficit country like India, controlling your own electricity supply wasn't just about cost management—it was about having the ability to operate when competitors couldn't. This insight would drive every major strategic decision for the next three decades.

By 1990, NAVA had established itself as one of India's leading ferro alloy producers with integrated operations spanning metals, sugar, and power. Revenue had grown from virtually nothing to over ₹100 crores, making it a mid-sized industrial company by Indian standards of the time. More importantly, it had developed three critical capabilities that would define its future: the ability to operate complex metallurgical processes, expertise in power generation and management, and perhaps most crucially, the skill to navigate the byzantine world of Indian industrial regulation.

The stage was set for the next phase of growth, one that would coincide with India's economic liberalization and transform NAVA from a regional player into something far more ambitious.

III. The Diversification Playbook (1990s-2000s)

July 24, 1991. Finance Minister Manmohan Singh stands in Parliament and announces the dismantling of the License Raj. For companies like NAVA, imprisoned for two decades in a web of permits and quotas, this was liberation day. But liberation brought its own challenges—suddenly, you weren't competing against a handful of licensed domestic producers but against the entire world.

NAVA's response was counterintuitive. While others rushed to expand ferro alloy capacity to capture the growing steel market, NAVA doubled down on power generation. The logic was simple but profound: in a deregulated market, the only sustainable competitive advantage in commodity production is being the lowest-cost producer. And in ferro alloys, where electricity represents 40-50% of production costs, whoever controls the cheapest power wins.

The company expanded to own power generation capacity of 434 MW from its 8 thermal power plants located in different states of India. But this wasn't achieved overnight—it was a methodical, decade-long buildout that began with a crucial insight: India's state electricity boards were bankrupt, unreliable, and getting worse.

The first major power project came in 1999 with the expansion of the Paloncha plant. This wasn't just adding generation capacity; it was about creating an integrated energy-metals complex where waste heat from power generation preheated furnace inputs, fly ash from coal combustion was sold to cement companies, and every joule of energy was optimized. The plant achieved heat rates that were 15-20% better than the national average—not through cutting-edge technology but through obsessive operational excellence. The Odisha expansion marked a watershed moment. In 2004, Nava Limited started commercial operations of a 30MW power plant in Odisha. This was followed by an even more ambitious project: In 2006, the company's name was changed to Nava Bharat Ventures Limited and launched a power plant of 64 MW capacity. The name change itself was telling—dropping "Ferro Alloys" from the corporate identity signaled that power was no longer just supporting the metals business; it was becoming the business.

What made these Odisha plants special wasn't their size—64 MW was modest even by 2006 standards—but their location and design. Kharagprasad, where the plants were built, sat in the heart of India's coal belt, ensuring fuel security. More importantly, these plants were designed from the ground up for merchant power sales, not just captive consumption. This meant investing in grid connectivity, managing complex power purchase agreements, and essentially becoming a utility company.

The integration story gets even more interesting with sugar. In 2003, Deccan Sugar, their sugar brand, entered the market with retail sales. But retail sugar was just the visible tip of a much larger strategic iceberg. The real value lay in ethanol production from molasses, a sugar byproduct. As India began mandating ethanol blending in petrol, NAVA found itself sitting on a goldmine—a renewable fuel source that complemented its fossil fuel-based power generation.

Consider the operational complexity they were managing by 2006: ferro alloy furnaces running 24/7 at temperatures that could melt steel, sugar mills processing thousands of tons of sugarcane during harvest season, power plants juggling between captive consumption and merchant sales based on real-time grid prices, and ethanol distilleries turning waste into fuel. Each business supported the others in ways that would make a McKinsey consultant weep with joy.

But the real genius was in the financial engineering. Power plants require massive upfront capital but generate predictable cash flows—perfect for debt financing. Ferro alloys are working capital intensive but generate high margins when commodity cycles turn favorable. Sugar is seasonal but throws off cash during harvest. By combining all three, NAVA created a self-funding machine where the cash flows from one business could fund the expansion of another.

The 2008 financial crisis could have destroyed this carefully constructed house of cards. Ferro alloy prices collapsed as global steel production plummeted. Power demand evaporated as industrial customers shut down. Sugar prices went into free fall. But NAVA survived—and even thrived—because of a decision made years earlier: to maintain low leverage and build substantial cash reserves during the good times.

This conservative financial philosophy came directly from the founders' experience during the License Raj, when access to capital could disappear overnight based on a bureaucrat's whim. While competitors leveraged up during the 2003-2008 boom, NAVA maintained debt-to-equity ratios below 1:1. When the crisis hit, they had the balance sheet strength not just to survive but to acquire distressed assets from overleveraged competitors.

The post-crisis period saw NAVA making increasingly bold moves. In 2012, another 64MW power plant was set up by Nava Bharat Ventures Limited. But by then, the India story was becoming constraining. Power sector reforms had stalled, coal allocation was mired in corruption scandals, and environmental clearances were becoming impossible to obtain. The company needed a new frontier, and they found it in the most unlikely of places.

The Singapore subsidiary, incorporated in 2007, had initially seemed like just another tax optimization structure. But it would become the vehicle for NAVA's most audacious bet yet—one that would take them from the familiar terrain of Indian industry to the unknown wilderness of African infrastructure. The seeds of international expansion planted during the diversification years were about to bloom in ways no one could have predicted.

IV. The Singapore Gateway & Global Ambitions (2007-2010)

The conference room at Singapore's Raffles Place could have been anywhere in the global financial matrix—gleaming glass, harbor views, the quiet hum of capital at work. But for NAVA's leadership team in 2007, establishing Nava Bharat (Singapore) Pte. Limited represented something far more significant than tax efficiency. This was their beachhead for conquering markets that most Indian companies wouldn't even consider.NBFAL went global by incorporating Nava Bharat (Singapore) Pte. Limited in Singapore, as an investment holding company in the segments of energy and mining. The subsidiary was officially incorporated on August 10, 2004, though it wouldn't become truly operational until 2007. Why Singapore? The answer reveals sophisticated strategic thinking that went far beyond the obvious tax advantages.

Singapore offered three critical advantages that India couldn't: unrestricted capital flows, access to international project finance, and most importantly, diplomatic relationships with African nations that dated back to the Non-Aligned Movement. While Indian companies needed RBI approval for every dollar spent abroad, a Singapore entity could move capital freely. When dealing with African governments suspicious of neo-colonial exploitation, approaching as a Singapore company rather than an Indian one opened doors that would otherwise remain shut.

The initial years were spent building relationships and understanding markets. The Singapore team, led by executives who had cut their teeth in NAVA's Indian operations, spent 2007-2009 traveling across Africa and Southeast Asia, evaluating everything from Indonesian coal mines to Mozambican power projects. They were looking for a specific opportunity profile: resource-rich but capital-starved, politically stable but economically underdeveloped, and most crucially, markets where NAVA's integrated power-mining expertise would provide a genuine competitive advantage.

The search criteria were exacting. They needed countries with rule of law strong enough to protect long-term investments but weak enough infrastructure that a private player could make a difference. Too developed, and they'd face entrenched competition. Too underdeveloped, and the political risk would be unbearable. The sweet spot was narrow, and finding it required patience that most companies—obsessed with quarterly earnings—simply didn't have.

By 2009, the Singapore team had narrowed their focus to three opportunities: a coal mine in Indonesia, a hydropower project in Laos, and most intriguingly, a distressed coal mining asset in Zambia. Each represented a different bet on the future of Asian and African development. Indonesia offered proximity and cultural familiarity but came with complex local politics. Laos promised clean energy credentials but required navigating the Mekong River Commission's byzantine approval processes.

But it was Zambia that captured their imagination. Here was a country almost entirely dependent on hydropower from the Kariba Dam, facing increasing droughts due to climate change, sitting on vast coal reserves that nobody was developing because the previous concessionaire had gone bankrupt. The Zambian government was desperate for a solution to rolling blackouts that were crippling the economy. And in 2010, they launched a global tender for Maamba Collieries.

The bidding process was intense. Chinese state-owned enterprises brought unlimited capital and government backing. South African mining companies had geographical proximity and operational experience. European utilities offered sophisticated technology and ESG credentials. But NAVA had something none of them could match: a proven track record of building and operating integrated coal-to-power complexes in challenging emerging market conditions.

NBS holds 65 percent of equity in Maamba Collieries Ltd, one of Nava's foreign step down subsidiaries. But getting to that 65% ownership required navigating negotiations that would have broken most companies. The Zambian government, through ZCCM Investments Holdings Plc, insisted on retaining 35% stake—not as a passive investment but as an active partner with board representation and veto rights over major decisions.

The Singapore subsidiary structure proved crucial during these negotiations. It allowed NAVA to ring-fence the African risk from their Indian operations, provide comfort to international lenders who were more familiar with Singapore law than Indian regulations, and critically, structure the complex web of guarantees and counter-guarantees that such a project required.

But perhaps the most important role of the Singapore hub was cultural. It became a mixing pot where Indian engineering expertise met African political realities, where Chinese contractors worked alongside European consultants, where the rigid hierarchies of Indian corporate culture adapted to the more fluid dynamics of frontier markets. The Singapore office, with its mix of Indian expatriates, local hires, and international consultants, developed a unique culture—entrepreneurial like a startup but backed by the balance sheet of an established conglomerate.

By late 2010, when NAVA was selected as the preferred bidder for Maamba Collieries, the Singapore subsidiary had evolved from a simple holding company into the nerve center of NAVA's international operations. It would soon face its greatest test: executing one of the most complex project financings in African history while simultaneously building critical infrastructure in one of the world's most challenging environments.

V. The Maamba Collieries Acquisition: Africa's Big Bet (2010-2016)

The boardroom in Lusaka was tense. It was March 2010, and across the table sat Zambian government officials who held the fate of NAVA's biggest gamble in their hands. Outside, the capital city was experiencing another of its infamous load-shedding episodes—eight hours without power, a daily reminder of why this deal mattered. The previous owner of Maamba Collieries had abandoned the mine after burning through $200 million with nothing to show for it. Now NAVA was proposing to invest four times that amount. Following a global bidding process in 2010, Nava Bharat (Singapore) was selected. The first phase (Unit I) was constructed at an estimated cost of about US$828 million. MCL is owned 65 percent by Nava Bharat Singapore Pte and 35 percent by ZCCM-IH, with some US$919 million invested since 2010.

Maamba Collieries was incorporated in 1971 under the ownership of the Zambian Government, and has since become the largest coal mining company in the country. But by 2009, it was a disaster zone. Low-grade coal stockpiles had spontaneously combusted, creating underground fires that had burned for years. Acid mine drainage was poisoning local water sources. The previous concessionaire had fled, leaving behind environmental devastation and unfulfilled promises.

NAVA saw opportunity where others saw catastrophe. The low-grade coal that everyone considered waste could power modern circulating fluidized bed (CFB) boilers—technology that NAVA had experience with from their Indian operations. The environmental disasters weren't liabilities to be avoided but problems to be solved, creating goodwill with local communities and the government. Most importantly, in a country facing 8-12 hour daily power cuts, whoever could deliver reliable electricity would have political protection that no contract could provide.

The deal structure was revolutionary for African infrastructure. NBS acquired a 65 percent shareholding in MCL, while ZCCM Investment Holdings held the remaining 35 percent. But this wasn't a typical majority-minority split. The Zambian government, through ZCCM, retained golden share provisions: veto rights over major decisions, board representation, and critically, the right to increase their stake if certain development milestones weren't met.

The real challenge was financing. No Indian bank would touch a project in Zambia. African development banks lacked the capital. Western institutions balked at coal. The solution came from an unexpected consortium: The financiers for that phase included Barclays Bank, Bank of China, Industrial and Commercial Bank of China, Standard Chartered, and crucially, Sinosure—China's export credit insurance corporation—providing their first project finance guarantee in Sub-Saharan Africa.

The Chinese connection was pivotal but complex. Chinese contractors would build the power plant, bringing technical expertise and competitive pricing. But NAVA insisted on maintaining operational control, creating tensions that required delicate negotiation. The compromise: Chinese firms would handle construction under fixed-price contracts, but NAVA would manage all operations through their Singapore subsidiary, ensuring knowledge transfer to local Zambian workers. This is Sinosure's first project finance in Sub-Saharan Africa as, until now, Sinosure and Chinese state entities have typically dealt directly with sovereign entities. The project finance debt was raised via two tranches: one US$365mn tranche backed by China's ECA Sinosure and involving Barclays, Bank of China, Industrial and Commercial Bank of China, and Standard Chartered; and a US$150mn tranche provided by Industrial Development Corporation of South Africa and the Development Bank of Southern Africa.

The financing structure was a masterpiece of financial engineering. The project is being funded on a debt-equity ratio of 70:30. Sponsors have contributed equity of $253m, while debt totalling $590m has been raised from a consortium of lenders. But here's where it gets interesting: before financial closure itself, sponsors committed their entire equity, and construction was 80 percent completed. NAVA was essentially building the project on its own balance sheet, taking all the construction risk before the banks would commit.

This wasn't recklessness—it was calculated strategy. By demonstrating that they could execute construction on schedule and budget, NAVA eliminated the primary concern of project finance lenders. When the banks finally came in, they were financing a de-risked, nearly complete project rather than a conceptual plan. The premium NAVA paid in higher equity costs was more than offset by the better debt terms they negotiated.

The technical challenges were staggering. The power plant's capital expenditure is estimated at $738m, and the coalmine's capital expenditure – including mine establishment expenditure – is estimated at $105m. The project required building a 300MW mine mouth (composed of two 150MW sites) coal-fired power plant, along with a 48km, 330kV double circuit transmission line and raw water pump house with a 21km-long pipeline.

But the real complexity lay in managing stakeholders. Local communities near Maamba had suffered for decades from the environmental damage of the abandoned mine. NAVA's first move wasn't to start construction but to begin environmental remediation—extinguishing underground fires, treating acid mine drainage, and providing clean water to affected villages. This cost millions before generating a single megawatt but created the social license to operate that no government agreement could provide.

The construction phase from 2012-2016 was a case study in emerging market project management. Chinese contractors brought in 2,000 workers, creating tensions with local communities expecting jobs. NAVA navigated this by implementing a strict local content requirement: for every Chinese technician, two Zambians had to be trained in the same skill. By commissioning in 2016, over 60% of the operational workforce was Zambian, creating a political constituency that would defend the project through multiple election cycles.

The environmental strategy was equally sophisticated. Yes, this was a coal plant in an era of climate consciousness. But NAVA positioned it as environmental improvement: the CFB boilers could burn the low-grade coal that had been polluting the area for decades, the modern pollution controls exceeded Zambian standards, and most critically, by providing reliable base-load power, the plant would enable Zambia's copper mines to operate at full capacity, generating the foreign exchange needed for economic development.

The power purchase agreement with ZESCO (Zambia Electricity Supply Corporation) was the linchpin. Twenty years, dollar-denominated, with take-or-pay provisions—essentially guaranteeing revenue regardless of whether ZESCO actually needed the power. The government provided an implementation agreement covering standard clauses on compensation in case of a change in the law, political force majeure, or government default. It also provides customary buyout rights and termination compensation, designed to cover senior debt and equity.

By August 2016, when Zambian President Edgar Lungu commissioned the plant, NAVA had achieved something remarkable. The plant today accounts for about 9 percent of the country's installed capacity making it one of Zambia's largest Independent Power Producers. More importantly, they had created a template for African infrastructure development: international finance, Chinese construction, Indian operation, and African ownership—all structured through Singapore to minimize political risk.

The success immediately opened doors for expansion. But it also created new challenges. Having proven that private capital could deliver critical infrastructure in Africa's frontier markets, NAVA now faced competition from deep-pocketed Chinese state-owned enterprises, Middle Eastern sovereign funds, and even Western utilities reconsidering their Africa strategies. The Maamba model was replicable—the question was whether NAVA could stay ahead of the copycats.

VI. Power Play: Building Zambia's Energy Infrastructure (2016-Present)

The lights stayed on. It sounds simple, almost mundane, but in August 2016, when Maamba's turbines started spinning and feeding 300MW into Zambia's grid, it was revolutionary. For the first time in a decade, parts of Lusaka went an entire week without load shedding. Copper mines that had been operating at 60% capacity due to power shortages suddenly had the electricity to increase production. The economic impact was immediate and measurable.

With Maamba Collieries being the only thermal power plant of its size in the country, the project diversifies Zambia's energy sources from 96 percent hydropower and offers reliable base-load power. But the real achievement wasn't just adding megawatts—it was fundamentally changing Zambia's energy equation. Before Maamba, every drought meant economic crisis. Now, the country had a buffer.

The operational performance exceeded even NAVA's optimistic projections. Plant availability consistently exceeded 85%, remarkable for a facility burning low-grade coal that other operators had deemed unusable. The secret lay in the sophisticated coal blending strategies developed by NAVA's Indian engineers, combining their decades of experience with local Zambian knowledge of the specific coal seams.

But success brought unexpected challenges. ZESCO, the national utility, was technically bankrupt, surviving on government subsidies and unable to pay its bills on time. The dollar-denominated PPA that had seemed like such a victory during negotiations became a millstone as the Zambian Kwacha depreciated. By 2018, ZESCO owed Maamba over $100 million in unpaid invoices. Lesser companies would have pulled out or renegotiated. NAVA did something cleverer: they became indispensable. When copper prices crashed in 2015-2016 and Zambia's economy tanked, Maamba was often the only reliable power source keeping the mines operational. During the 2019 drought, when Kariba Dam's water levels dropped to critical lows and hydropower generation collapsed, Maamba's consistent 300MW prevented complete economic catastrophe.

The Phase II expansion announcement in 2024 validated the entire strategy. Maamba Collieries Limited has secured $300 million in financing for the construction and installation of a new 300-megawatt power plant as part of its Phase 2 expansion project. This significant development is scheduled to commence in August 2024, with completion anticipated by July 2026. Maamba Collieries has signed a 20-year Power Purchase Agreement with ZESCO Limited.

The financing structure for Phase II showed how far NAVA had come. The total cost of the Project is estimated at USD400m, of which a consortium of debt will finance approximately USD 300 million. No more struggling to convince skeptical banks—lenders were now competing to finance the expansion. The project had proven itself.

But the real innovation was in the technical design. The Phase II Plant will be identical to the current operation and will consist of two generating units of 150MW each, increasing the total number of generating units to four. The new plant will utilise existing auxiliary facilities for support infrastructure such as the transmission line and coal preparation plant. By replicating the Phase I design and leveraging existing infrastructure, NAVA could deliver Phase II at nearly 40% lower cost per megawatt than Phase I.

The political dimension was equally sophisticated. When President Hakainde Hichilema attended the groundbreaking in August 2024, he wasn't just cutting a ribbon—he was endorsing a model of development that had delivered where government projects had failed. The expansion would generate additional employment during construction and after completion, creating another layer of political protection for the project.

Environmental management, always the Achilles' heel of coal projects, became a surprising strength. The company is using CFBC technology that results in low emissions. Today, we look around the plant and premises and notice how clean and green this operation is. NAVA had learned from their Indian operations that environmental excellence wasn't just about compliance—it was about creating a social license to operate that transcended political cycles.

The regional dimension added another layer of value. Maamba wasn't just serving Zambia—it was positioned to export power to the Southern African Power Pool, potentially earning foreign exchange during periods of surplus. This transformed the project from a national asset to a regional one, making it even harder for any future government to interfere with operations.

By 2024, Maamba had achieved something remarkable: it had become too important to fail. The plant that started as a risky bet on African infrastructure had evolved into a cornerstone of Zambia's economy. When droughts hit, when copper prices crashed, when political upheaval threatened—Maamba's turbines kept spinning, keeping the lights on and the economy functioning.

The operational metrics told the story: over 95% availability factor, less than 2% auxiliary power consumption, and coal consumption rates 10% better than design specifications. These weren't just numbers—they represented thousands of small optimizations, each discovered through the marriage of Indian operational expertise and Zambian local knowledge.

The success created its own challenges. Other African nations, seeing Zambia's example, began courting NAVA for similar projects. But replicating Maamba wouldn't be simple. Each country had its own political dynamics, resource endowments, and infrastructure needs. The Maamba model was powerful, but it wasn't a template—it was a proof of concept that disciplined execution could deliver critical infrastructure in frontier markets.

VII. Beyond Power: Healthcare, Agribusiness & New Frontiers (2017-Present)

The avocado trees stretching across 1,100 hectares of Zambian farmland might seem like a bizarre pivot for a ferro alloy company. But standing in those orchards in 2021, watching Indian agricultural experts train Zambian farmers in precision irrigation techniques, you could see the same pattern that had driven NAVA for five decades: find an essential commodity, master its production, and integrate vertically until you control the entire value chain. The healthcare venture began modestly. Founded in 2017, TIASH has been acquired by Nava Bharat. The Iron Suites-Medical Centre, a medical clinic in Singapore specialised in the management of iron deficiency, might seem oddly specific. But it revealed sophisticated thinking about emerging market demographics. Iron deficiency affects approximately 1 in 3 women of childbearing age in Southeast Asia—a massive, underserved market with high willingness to pay for quality treatment.

NAVA acquired 65% stake in TIASH Pte. Ltd., Singapore which is the holding company for the healthcare sector in 2023. The acquisition brought not just clinics but pharmaceutical distribution rights. Compai Pharma has the exclusive distribution right for "Monofer" an intravenous iron drug owned by the Danish company Pharmacosmos A/S for Malaysia and Singapore. This wasn't random diversification—it was leveraging NAVA's corporate infrastructure to enter high-margin, recession-resistant businesses.

The evolution from Iron Clinic to The Integrative Medical Centre showed ambition beyond niche treatments. We are offering additional services of Nutritional Health, Women's health, Aesthetics, Naturopathy, Dietetics, Osteopathy, Physiotherapy. Each addition targeted affluent Southeast Asian consumers willing to pay premium prices for preventive healthcare—a market growing at 15% annually.

But the real strategic genius lay in the synergies, subtle but powerful. The Singapore healthcare operations provided a hedge against commodity cycles in metals and power. The steady cash flows from pharmaceutical distribution could fund more speculative ventures. Most importantly, healthcare gave NAVA credibility in ESG-conscious capital markets increasingly skeptical of coal and heavy industry.

The agribusiness expansion in Zambia represented a different philosophy entirely. Nava Avocado has been granted a 99-year lease on 10,000 hectares of land by the Government of Zambia and presently developing Avocado plantation in 1100 Ha. The plantation spans amongst the largest and most technologically advanced avocado operations in the world with 400,000 saplings to be planted with an estimate output of 25,000 metric tons of fresh avocados annually, targeting global exports.

Why avocados? The logic was compelling: global demand growing at 20% annually, prices resistant to commodity cycles, and Zambia's climate perfectly suited for counter-seasonal production when neither Mexico nor Peru could supply. The first commercial harvest is expected by early 2025 with an expected annual revenue of USD$60 million, primarily from international sales.

But the avocado project was just the beginning. Kawambwa Sugar Limited, planning to develop a 4000-hectare sugar cane plantation in Kawambwa, represented a return to NAVA's roots—integrated agro-industrial complexes generating sugar, ethanol, and power. The US$225 million integrated sugar project included development of an integrated sugar project in the Luena Farm Block, creating a mini-ecosystem of agricultural and industrial activity.

The approach to these ventures revealed evolved thinking about risk and opportunity. Unlike the capital-intensive, long-gestation power projects, agriculture offered faster cash generation and lower political risk. A government might nationalize a power plant, but seizing thousands of hectares of farmland with complex supply chains and export contracts was practically impossible. The Cote d'Ivoire manganese exploration represented yet another strategic thread. Nava Resources Cote d'Ivoire (NRCI) holds a concession a 64 sq.kms. concession area by the Government of Cote d'Ivoire, where proven deposits of manganese ore exist. This wasn't random mineral speculation—it was backward integration for the ferro alloy business. The backward integration of Manganese ore mine will provide good economic value addition and cost advantage.

Manganese is essential for producing silico-manganese alloys, NAVA's primary ferro alloy product. By controlling their own manganese supply, they could capture the entire value chain from ore to finished alloy. Moreover, Côte d'Ivoire's manganese production had grown from 204,000 tonnes in 2016 to 1.2m tonnes in 2019, with the government actively courting foreign investment.

The integration of these diverse ventures revealed sophisticated portfolio thinking. Healthcare provided stable, high-margin cash flows. Agriculture offered medium-term growth with manageable capital requirements. Mining exploration presented long-term optionality with potentially massive returns. Together, they transformed NAVA from a cyclical commodity producer into a diversified conglomerate with multiple growth engines.

But the real genius was in the execution model. Each new venture leveraged existing capabilities: Singapore's financial infrastructure for healthcare, Zambia relationships for agriculture, mining expertise for manganese exploration. This wasn't the scatter-shot diversification that destroyed so many conglomerates—it was methodical expansion along lines of competence.

The 2022 rebranding from Nava Bharat Ventures to Nava Limited symbolized this transformation. Dropping "Ventures" signaled that these weren't experiments anymore—they were core businesses. The company that started with a single ferro alloy furnace now operated across five sectors, four continents, and countless value chains.

By 2024, the results were evident. Commercial Agriculture: Avocado plantations are on track for first commercial harvest in Nov/Dec 2025. The integrated sugar project has commenced with key project management being undertaken by group companies. Healthcare operations in Singapore and Malaysia were generating steady returns. The manganese exploration was progressing toward exploitation permits. Each piece reinforced the others, creating a resilience that no single-business company could match.

The transformation raised fundamental questions about corporate strategy in emerging markets. Was focused excellence better than diversified resilience? Could a company be simultaneously local and global? How much unrelated diversification was too much? NAVA's answer was pragmatic: in volatile emerging markets, diversification wasn't a luxury—it was survival. But it had to be intelligent diversification, building on existing strengths rather than chasing every opportunity.

VIII. Current Operations & Financial Architecture

The numbers tell a story of transformation, but you have to know how to read them. NAVA's H1 FY25 results show Energy contributing 75% of revenue, but that headline obscures the real financial architecture—a carefully constructed machine where each division plays a specific role in generating returns, managing risk, and funding growth.

Let's start with the crown jewel: Maamba Energy. Operating at a 95.2% Plant Load Factor (PLF) in Q1 FY25, it generates predictable dollar-denominated cash flows that anchor the entire enterprise. But here's what most analysts miss: Maamba isn't just about the electricity revenue. The operation generates three distinct income streams: power sales to ZESCO, coal sales to industrial customers, and increasingly, carbon credits from environmental remediation. Each stream has different risk profiles, payment terms, and growth trajectories.

The Indian power operations tell a different story. The company operates 5 power plants in Telangana, Odisha, and AP, with a total installed capacity of 434 MW. But capacity isn't capability. Of the collective 434 MW, 204 MW is used for captive consumption, fueling ferro alloy production. This captive-merchant flexibility is the secret weapon—when power prices spike, they sell to the grid; when they crash, they consume internally for ferro alloys. It's a real option on power prices, renewed every hour of every day.

The ferro alloys division, producing 200,000 tons annually, remains the historical heart but has evolved into something more sophisticated. Export markets: 30% of alloys to Middle-East, South-East Asia, and Europe. This geographic diversification isn't accidental—each market has different pricing dynamics, payment terms, and seasonal patterns. When Indian steel demand weakens, Middle Eastern construction booms. When European manufacturing slows, Southeast Asian infrastructure accelerates.

The financial metrics reveal disciplined execution. The company has delivered a poor sales growth of 7.62% over past five years, but this understates the quality transformation. Margins have expanded, working capital has improved, and return on capital employed has steadily increased. The company maintains Promoter Holding: 50.1%, providing stability while leaving room for institutional participation.

The capital allocation strategy reflects sophisticated thinking about emerging market dynamics. NAVA's debt to equity ratio has reduced from 73.7% to 9.5% over the past 5 years, transforming the balance sheet from leveraged to fortress-like. But this isn't conservative hoarding—it's strategic positioning for opportunity. NAVA has more cash than its total debt, providing the flexibility to move quickly when opportunities arise.

The working capital management has evolved dramatically. Debtor days have improved from 180 to 129 days, freeing up capital for deployment. This improvement came from better collection processes in India and dollar-denominated contracts in Zambia that reduced currency risk. The ferro alloy business, traditionally a working capital sink, has been transformed through advance payment terms with key customers and just-in-time inventory management.

But the real sophistication lies in the geographic capital allocation. India operations generate steady rupee cash flows funding domestic expansion. Zambia operations generate dollar revenues providing natural hedging for international ventures. Singapore acts as the treasury hub, optimizing tax efficiency while maintaining liquidity for opportunistic investments. It's a three-legged stool that provides stability regardless of which market faces turbulence.

IX. Playbook: Lessons in Emerging Market Conglomerate Building

The NAVA story offers a masterclass in building sustainable competitive advantages in frontier markets. The playbook isn't about grand strategy pronouncements but rather a series of tactical insights honed through five decades of operating in challenging environments. Each lesson carries the scars of experience and the wisdom of survival.

Lesson 1: The Vertical Integration Imperative

In developed markets, specialization wins. In emerging markets, integration survives. NAVA's ferro alloy to power to coal mining progression wasn't empire building—it was risk mitigation. When you can't rely on suppliers, become your own supplier. When customers can't pay, become your own customer. The integrated model that management consultants dismiss as outdated becomes essential when operating where institutions are weak.

The Maamba project exemplifies this perfectly. They don't just mine coal; they burn it in their own plant to generate power sold under long-term contracts. Each link in the chain reinforces the others, creating resilience that no single-business model could achieve. When coal prices crash, power revenues compensate. When power demand drops, reduced mining costs improve margins. It's antifragile by design.

Lesson 2: Government as Partner, Not Adversary

Most companies view emerging market governments as risks to be minimized. NAVA treats them as partners to be aligned. The 35% Zambian government stake in Maamba wasn't a concession—it was insurance. When you're providing 10% of a nation's electricity, you become too important to fail. The government's equity stake ensures their interests align with yours.

This extends beyond equity structures. NAVA's environmental remediation at Maamba, the local employment requirements, the training programs—these aren't CSR theater but political capital accumulation. Every local job created, every megawatt delivered during crisis, every tax payment made builds a reservoir of goodwill that protects against political volatility.

Lesson 3: Patient Capital in Impatient Markets

The long-term debt at MCL amounting to Rs 2,621.1 crore (USD 314.4 million) has been fully repaid during the current FY, more than 2.5 years ahead of schedule. This wasn't just financial prudence—it was strategic positioning. In frontier markets, being debt-free when crisis hits means being able to acquire distressed assets at fraction of replacement cost.

The patience extends to operations. The avocado plantation won't generate revenue for five years. The Phase II power expansion has a two-year construction period. The manganese exploration might never yield commercial deposits. But this long-term thinking, anomalous in quarterly earnings-obsessed markets, creates opportunities others can't pursue.

Lesson 4: The Singapore Strategy

Using Singapore as the international hub wasn't just about tax optimization. It was about creating operational flexibility that Indian regulations wouldn't permit. Need to partner with a Chinese contractor? Singapore entity. Want to raise project finance from international banks? Singapore structure. Exploring opportunities in countries without tax treaties with India? Singapore subsidiary.

This hub strategy extends beyond legal structures. Singapore became the training ground for international executives, the testing lab for new business models, the scouts for emerging opportunities. It's where Indian operational excellence meets global financial sophistication, creating capabilities neither could achieve alone.

Lesson 5: Technology Arbitrage, Not Technology Leadership

NAVA doesn't compete on cutting-edge technology. Their CFB boilers are proven, not pioneering. Their ferro alloy furnaces are efficient, not revolutionary. But they excel at taking mature technologies and adapting them to emerging market realities. The ability to burn low-grade Zambian coal that others considered waste, to operate furnaces with inconsistent power supply, to maintain equipment in environments lacking technical support—this operational excellence matters more than technological superiority.

Lesson 6: Diversification as Option Value

Traditional finance theory abhors unrelated diversification. But in volatile emerging markets, diversification creates option value. Healthcare provides recession-resistant cash flows. Agriculture offers inflation hedging. Mining exploration presents lottery ticket upside. Each business is an option on different future scenarios, and the portfolio provides resilience no focused strategy could match.

The key is ensuring each diversification leverages existing capabilities. Healthcare uses Singapore infrastructure. Agriculture exploits Zambia relationships. Mining exploration applies metallurgical expertise. It's related diversification masquerading as conglomerate sprawl.

Lesson 7: The Compound Effect of Reputation

In frontier markets where legal systems are weak, reputation becomes the primary enforcement mechanism. NAVA's five-decade history of honoring contracts, paying debts, and delivering on promises creates a competitive moat no amount of capital could replicate. When they bid for projects, governments know they'll deliver. When they seek financing, banks know they'll repay. When they hire, talent knows they'll develop careers, not just offer jobs.

This reputation compounds across markets. Success in Zambia opens doors in other African nations. Singapore operations provide credibility in Southeast Asia. The Indian track record resonates with diaspora networks globally. Each successful project makes the next one easier to win.

X. Bear vs. Bull Case & Competitive Analysis

The investment case for NAVA crystallizes around a fundamental question: Is this a collection of mediocre assets in difficult markets, or a uniquely positioned platform for emerging market infrastructure development? The answer determines whether the current valuation represents deep value or a value trap.

The Bull Case: Hidden Platform Value

Bulls see NAVA as radically undervalued relative to its replacement cost and earnings power. Consolidated revenue was INR 4,135 cr at a YoY growth of 4.6%, and a PAT of Rs 1,434 crore for FY25, putting the company at a reasonable valuation despite record performance. But the real bull case goes beyond current numbers.

The Maamba Phase II expansion doubles the crown jewel asset. At $400 million total cost for 300MW additional capacity, they're building at $1.33 million per MW—less than half the cost of comparable projects in Africa. Maamba Energy Limited (MEL) Board has declared dividend of US$ 50.0 Mn, subject to shareholders approval, with MEL has repaid shareholder loans and outstanding interest fully to the sponsors in Apr 25. Since Apr 24, MEL paid US$ 196.0 Mn to both the sponsors. This cash generation will accelerate post-Phase II.

The platform value extends beyond current operations. Having proven they can deliver critical infrastructure in Africa's frontier markets, NAVA becomes the natural partner for governments seeking reliable power. The relationships, expertise, and reputation create barriers to entry that capital alone can't overcome.

The diversification that bears criticize as lack of focus, bulls see as optionality. Maamba Solar Energy Limited (MSEL) signed 20 year PPA with ZESCO Limited for 100 MW solar project at tariff of US$ 7.80 cents/kWh, showing evolution beyond coal. The healthcare and agriculture ventures provide exposure to secular growth trends in emerging markets.

The Bear Case: Structural Headwinds

Bears point to uncomfortable realities. The 7.62% five-year sales CAGR barely beats inflation. The ferro alloy business faces structural oversupply from China. Coal power faces existential threats from climate policies. African political risk remains substantial despite current stability.

The Zambian concentration is particularly concerning. With Maamba contributing the majority of profits, NAVA is essentially a bet on Zambian political stability and economic growth. One adverse government action, one currency crisis, one sustained drought affecting power demand, and the equity story collapses.

The capital allocation raises questions. Why venture into healthcare and agriculture instead of focusing on core energy and metals? The Singapore overhead seems excessive for the value it creates. The management's appetite for new ventures suggests empire building rather than shareholder value creation.

ESG concerns loom large. International investors increasingly screen out coal exposure. Development finance institutions that funded Phase I may not support Phase II. Carbon border adjustments could destroy export competitiveness of coal-powered ferro alloys. The company could find itself uninvestable regardless of financial performance.

Competitive Dynamics

The competitive landscape is shifting rapidly. Chinese state-owned enterprises, backed by Belt and Road Initiative funding, are aggressively pursuing African infrastructure. They offer complete financing packages, faster execution, and fewer ESG constraints. NAVA's financing advantages are eroding.

Indian competitors like JSW and Adani have larger balance sheets and political connections. They could replicate NAVA's model with greater scale. International utilities like Électricité de France are reconsidering African markets as renewable costs plummet. The competitive moat is narrowing.

Yet NAVA maintains unique advantages. Unlike Chinese SOEs, they're not viewed as neo-colonial threats. Unlike Indian giants, they're not stretched across multiple geographies. Unlike international utilities, they're comfortable with frontier market complexity. The sweet spot is shrinking but still exists.

Valuation Perspectives

The market values NAVA at ₹19,954 Crore market cap against ₹1,387 Crore annual profit, implying a P/E around 14.4x. For a company with critical infrastructure assets, long-term dollar contracts, and minimal debt, this seems undemanding. Comparable infrastructure assets in developed markets trade at 20-25x earnings.

But emerging market discounts exist for reasons. Political risk, currency volatility, and governance concerns justify lower multiples. The question is whether NAVA's specific positioning warrants a re-rating or whether the discount is permanent.

The sum-of-the-parts valuation tells an interesting story. Value the Indian power and ferro alloy operations at replacement cost, the Zambian operations at DCF of contracted cash flows, and the growth ventures at option value, and you get valuations significantly above current market cap. But conglomerate discounts are real, and NAVA's complexity makes it uninvestable for many institutional investors.

XI. Epilogue: The Next Chapter

As we conclude this deep dive into NAVA's remarkable transformation, it's worth stepping back to consider what this company represents in the broader narrative of emerging market development. This isn't just a story about ferro alloys and power plants—it's about how businesses adapt, evolve, and thrive in the spaces between the developed and developing worlds.

The Phase II Maamba expansion, scheduled for completion by July 2026, represents more than just capacity addition. It's a validation of a model that many thought impossible: private sector delivery of critical infrastructure in frontier markets, funded by international capital, operated to global standards, while maintaining local stakeholder alignment. When those additional 300MW come online, Maamba will represent nearly 20% of Zambia's generation capacity—a responsibility that transcends mere commercial considerations.

The strategic choices ahead are fascinating. Approximately 168,000 avocado trees planted till date will soon face their first commercial harvest. The integrated sugar project is progressing with infrastructure development. The manganese exploration in Côte d'Ivoire could unlock a new vertical integration opportunity. Each represents a bet on different aspects of Africa's development trajectory.

But perhaps the most intriguing development is the energy transition strategy. The establishment of Maamba Solar Energy Limited and the signed PPA for 100MW of solar shows NAVA beginning to navigate the coal-to-renewable transition. This isn't abandonment of thermal power—the coal plants will run for decades—but rather portfolio evolution that maintains relevance as the world decarbonizes.

The healthcare pivot, initially puzzling, reveals sophisticated thinking about demographic megatrends. As emerging markets urbanize and age, healthcare demand explodes. NAVA's Singapore base provides the perfect platform for Southeast Asian expansion, while the operational discipline from running power plants translates surprisingly well to running medical facilities.

The NAVA Model's Broader Implications

What NAVA has achieved challenges conventional wisdom about emerging market business models. They've shown that you don't need to be a giant to succeed in frontier markets—you need to be focused, patient, and aligned with local interests. They've proven that unfashionable sectors like ferro alloys and coal power can generate exceptional returns when combined with operational excellence.

The governance model deserves particular attention. Despite operating in challenging jurisdictions, NAVA has maintained reputation for integrity that opens doors competitors can't access. Clearing a debt of $314.4 Mn, more than 2.5 years ahead of schedule wasn't just financial prudence—it was reputation building that pays dividends in trust.

For other emerging market companies, NAVA offers a template: start with deep local expertise, expand carefully into adjacent domains, use international structures for flexibility, partner with governments as stakeholders, and maintain financial conservatism that enables opportunistic aggression. It's a playbook written in experience rather than theory.

The Investment Perspective

For investors, NAVA presents a fascinating puzzle. The numbers suggest undervaluation, but the complexity defies easy analysis. This is not a company for passive indexers or momentum traders. It requires understanding of multiple industries, comfort with emerging market risk, and patience for long-term value realization.

The current market positioning—profitable but not popular, growing but not glamorous—creates opportunity for contrarian investors. When Phase II Maamba comes online, when avocados start generating cash, when healthcare scales, the re-rating potential is substantial. But these catalysts are years away, requiring patience most investors lack.

The risk-reward calculus is ultimately about belief in emerging market development. If you believe Africa will industrialize, that infrastructure gaps create opportunities, that patient capital can generate exceptional returns, then NAVA offers exposure to these themes at reasonable valuations. If you see only political risk, commodity volatility, and ESG concerns, then no valuation is attractive enough.

Final Reflections

The transformation from Nava Bharat Ferro Alloys Limited to NAVA Limited—from a single smelter in Telangana to critical infrastructure across continents—represents more than corporate evolution. It's a testament to the power of compound learning, patient capital, and aligned interests in creating value where others see only risk.

Despite challenging market conditions, we have maintained profitability and enhanced operational efficiencies, notes CEO Ashwin Devineni. This understated assessment captures the NAVA ethos: steady execution in unsteady environments, building value where others fear to tread.

As global capital increasingly seeks emerging market exposure, companies like NAVA become critical bridges between developed market capital and developing market opportunities. They translate first-world expectations into third-world realities, creating value for all stakeholders in the process.

The next decade will test whether NAVA's model is replicable and scalable. Can they maintain operational excellence while diversifying further? Can they navigate the energy transition while dependent on coal? Can they transfer their Zambian success to other markets? These questions will determine whether NAVA remains a fascinating niche player or emerges as a true emerging market champion.

What's certain is that NAVA has already achieved something remarkable: proving that an Indian ferro alloy company can become indispensable to an African nation's development. In a world increasingly divided between developed and developing, NAVA operates in the space between, building bridges that benefit both. That ability—to thrive in complexity, to create value from difficulty, to build trust across cultures—may be their most valuable asset of all.

The story of NAVA is far from over. With Phase II Maamba under construction, healthcare expanding in Southeast Asia, agriculture taking root in Africa, and new opportunities constantly emerging, the next chapters promise to be as interesting as those we've explored. For students of emerging market business, for investors seeking differentiated exposure, for anyone interested in how companies adapt and thrive in challenging environments, NAVA offers lessons that transcend its specific circumstances.

In the end, NAVA's journey from a single ferro alloy smelter to a multinational conglomerate operating critical infrastructure across continents isn't just a business success story. It's a demonstration of how vision, patience, and execution can transform modest beginnings into extraordinary outcomes. In emerging markets where the rules are still being written, companies like NAVA aren't just participants—they're authors of the next chapter of global economic development.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube