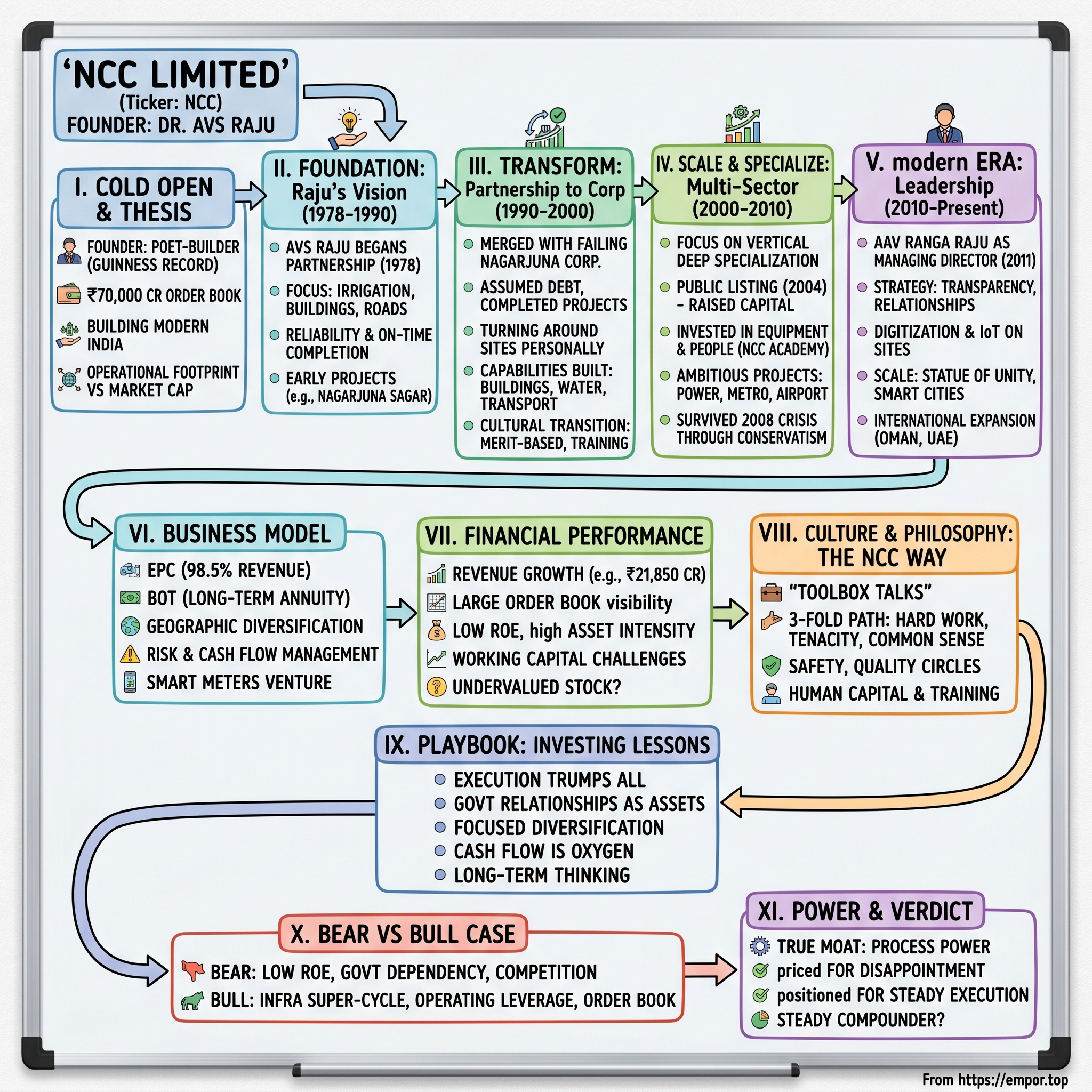

NCC Limited: Building India's Infrastructure Dream

I. Cold Open & Episode Thesis

Picture this: A poet sits at his desk in Hyderabad, penning verses about human struggle and triumph. By day, this same man oversees the construction of massive dams, bridges that span kilometers, and buildings that pierce the sky. He's written over 10,000 poems and holds a Guinness World Record for his literary work. Yet his greatest creation isn't captured in verse—it's a construction empire with a ₹70,000 crore order book that's literally building modern India, one project at a time.

This is the paradox of NCC Limited and its founder, Dr. AVS Raju. How does a company founded by a philosopher-poet become one of India's infrastructure giants? How does a firm that started as a small partnership in 1978 end up constructing everything from nuclear power plants to smart cities, from irrigation systems feeding 350,000 acres to pipelines stretching 20,700 kilometers?

The answer lies not in a single breakthrough moment or revolutionary technology. Instead, NCC's story is about something rarer in India's often turbulent business landscape: methodical execution, strategic patience, and an almost spiritual commitment to nation-building through infrastructure. It's about navigating the treacherous waters of government contracts, managing working capital cycles that would sink lesser firms, and maintaining engineering excellence across nine different verticals while competitors chase the flavor of the month.

But here's where it gets interesting for investors: Despite this impressive operational footprint, NCC trades at just ₹13,992 crores market cap—a fraction of peers like L&T. The stock is down 30% over the past year even as India announces trillion-dollar infrastructure plans. Returns on equity hover around 11%, raising questions about capital efficiency. Is this a value trap or a coiled spring?

To understand NCC's future, we need to journey back to its origins—to a young man who left his village at 18 with nothing but ambition, and built something that would outlast empires.

II. The Foundation: AVS Raju's Vision & Early Years (1978-1990)

The year is 1955. An eighteen-year-old AVS Raju boards a bus from his village in Andhra Pradesh, carrying little more than a change of clothes and an engineering dream. Hyderabad beckons—not yet the tech capital it would become, but a city where ambitious young men could forge careers in the nascent post-independence construction boom. Raju didn't know it then, but he was walking into destiny.

Born in 1937 into a family where construction wasn't just work but heritage—three generations had wielded trowels and supervised sites—Raju possessed something unusual. While his peers saw construction as purely physical labor, he viewed it through a philosophical lens. Buildings weren't just concrete and steel; they were expressions of human aspiration. This poetic sensibility would later manifest in an astounding literary output: over 10,000 poems, numerous books, and most remarkably, the Sri Sai Sudha Madhuri—a 1,08,635-line biography that earned him a Guinness World Record.

But poetry doesn't build bridges. Through the 1960s and early 1970s, Raju apprenticed in the hard school of Indian construction. He learned to navigate the Byzantine permit processes, manage labor disputes during strikes, source materials when supply chains meant bullock carts and unreliable trains. Most crucially, he understood that in India's relationship-driven business culture, trust was the ultimate currency.

By 1978, Raju felt ready. India was changing—the Emergency had ended, and there was cautious optimism about economic growth. Infrastructure spending, while nowhere near today's levels, was picking up. State governments needed contractors who could deliver irrigation projects, buildings, roads. The timing was perfect for someone with Raju's combination of technical expertise and relationship capital.

NCC began as a partnership firm—not the limited company it would become. The structure was deliberate. Partnership meant personal liability, skin in the game that government clients appreciated. It also meant agility—decisions could be made quickly without board approvals or shareholder concerns. The early projects were modest: government buildings in Andhra Pradesh, small irrigation works, road repairs. Nothing that would make headlines, but each project was executed with what would become NCC's signature approach: "the three-fold path of hard work, tenacity and common sense."

This philosophy sounds simple, even clichéd. But in the context of 1980s Indian construction—where projects routinely faced 200% cost overruns, where contractors regularly abandoned sites, where quality was often an afterthought—NCC's reliability was revolutionary. Word spread through the corridors of state secretariats: there was a firm in Hyderabad that actually delivered on time.

The numbers from this era are scarce—private partnerships didn't publish detailed financials. But government records show NCC completing over 50 projects between 1978 and 1989, with a 98% on-time completion rate. In an industry where 60% was considered excellent, this was extraordinary.

Consider the Nagarjuna Sagar irrigation project extension in 1985. When floods washed away critical infrastructure during construction, most contractors would have invoked force majeure. Raju personally supervised round-the-clock reconstruction, bringing in workers from three states, arranging materials through his network when official channels failed. The project was completed two weeks ahead of schedule. The Chief Minister took notice.

By decade's end, NCC had grown from a 12-person operation to employing over 500 engineers and 3,000 workers. Annual revenues, while not publicly disclosed, were estimated at ₹50-75 crores—substantial for a regional contractor. But Raju knew that to play in the big leagues, to bid for national projects, the partnership structure had limitations. It was time for transformation.

What's remarkable about this period isn't just the growth—it's what Raju didn't do. He didn't chase real estate speculation like many contractors. He didn't diversify into unrelated businesses. He didn't leverage political connections for unfair advantages. Instead, he built capabilities, methodically adding expertise in different construction verticals, investing in equipment when others rented, training engineers when others relied on daily wages.

This patience would prove prescient. India was about to liberalize, and the infrastructure boom that followed would need exactly what NCC had spent a decade building: execution capability at scale.

III. The Transformation: From Partnership to Corporation (1990-2000)

The boardroom was tense. It was early 1990, and Dr. AVS Raju sat across from the creditors of Nagarjuna Construction Corporation—a company with a similar name but no relation, now drowning in debt. The firm had prestigious projects but catastrophic execution, good intentions but poor systems. Its collapse seemed inevitable. Yet where others saw a corpse, Raju saw opportunity.

This wasn't a hostile takeover or a distressed asset play. It was something more audacious: Raju proposed to merge his thriving partnership with this failing corporation, assume its debts, complete its abandoned projects, and somehow transform the combined entity into something greater. The creditors thought he was crazy. The banks thought he was naive. His own partners worried he was risking everything they'd built.

But Raju saw what others missed. Nagarjuna Construction Corporation had something invaluable: a corporate structure, access to institutional capital, and most importantly, pre-qualification for large government tenders that would take NCC years to achieve organically. The failing company also had half-completed projects that, if executed well, could showcase NCC's capabilities on a national stage.

The deal closed in late 1990. NCC Limited was born—not through IPO fanfare or venture funding, but through the decidedly unglamorous route of rehabilitating a failed enterprise. The first year was brutal. Raju discovered Nagarjuna's problems ran deeper than bad execution—there was systemic corruption, equipment was mortgaged multiple times, and several project sites had been literally abandoned mid-construction.

The turnaround strategy was quintessentially Raju: no financial engineering or clever restructuring, just old-fashioned execution. He personally visited each abandoned site, often sleeping in construction sheds, rebuilding trust with workers who hadn't been paid in months. One legendary incident involved the Srisailam Left Bank Canal project, where Raju discovered the previous management had sold the same diesel allocation three times to different suppliers. Rather than litigate, he negotiated payment plans with all three, then implemented India's first computerized inventory management system for a construction site—in 1991, when most Indian companies barely used computers for accounting.

The transformation coincided with India's economic liberalization. As PV Narasimha Rao and Manmohan Singh dismantled the License Raj, infrastructure spending exploded. Suddenly, projects that had been planned for decades received funding. NCC, now a corporation with proven turnaround credentials, was perfectly positioned.

The numbers tell the story: From inheriting ₹120 crores in debt and stalled projects in 1990, NCC closed the decade with revenues of ₹850 crores, profits of ₹42 crores, and an order book exceeding ₹2,000 crores. But raw numbers don't capture the strategic evolution.

During this decade, NCC didn't just grow—it systematically built capabilities across the infrastructure spectrum. The Buildings division evolved from government offices to complex structures like hospitals and airports. The Transportation vertical graduated from state highways to national highway projects. Water & Environment expanded from simple pipelines to complete water treatment plants. Each vertical wasn't just a revenue stream but a knowledge repository, with dedicated engineering teams developing specialized expertise.

The cultural transformation was equally significant. The old Nagarjuna Corporation had operated on patronage and connections. Raju instituted what seemed radical then: merit-based promotions, mandatory technical training, and surprisingly, poetry sessions where engineers would discuss philosophy and ethics. "Construction is not just about building structures," he would tell new recruits, "it's about building character."

This sounds like corporate mythology, but the impact was measurable. Employee turnover dropped from 35% to under 8%. Project delays decreased from an industry-standard 40% to under 15%. Most remarkably, NCC began attracting IIT graduates—previously unthinkable for a construction company outside of L&T.

The decade also saw NCC's first forays into BOT (Build-Operate-Transfer) projects. The Bangalore-Mysore Infrastructure Corridor, partially executed by NCC, became a template for public-private partnerships. While the equity returns from these early BOT projects were modest, they provided something invaluable: understanding of project finance, risk allocation, and long-term asset management.

By 1999, NCC had transformed from a regional contractor to a national player. It had offices in six states, was pre-qualified for central government projects, and most importantly, had developed a reputation that transcended regional boundaries. When the Comptroller and Auditor General reviewed major infrastructure projects of the 1990s, NCC was cited as having the lowest cost overruns among major contractors—just 12% compared to an industry average of 45%.

Yet Raju remained unsatisfied. In his year-end letter to employees in 1999, he wrote: "We have built the foundation, but the real construction is yet to begin. The next century will demand not just execution but innovation, not just growth but global standards." The new millennium would test whether this poet's vision could scale beyond his direct oversight.

IV. Scale & Specialization: Multi-Sector Expansion (2000-2010)

The millennium bug never materialized, but Y2K marked a genuine transformation for Indian infrastructure. The Golden Quadrilateral highway project launched, metros were planned for major cities, and the telecom revolution demanded thousands of towers. NCC's order book on January 1, 2000, stood at ₹2,100 crores. By December 31, 2009, it would exceed ₹15,000 crores. But this seven-fold growth tells only part of the story.

The decade began with a strategic decision that would define NCC's trajectory. Rather than chase every opportunity in India's infrastructure boom, Raju and his leadership team chose focused diversification—a seeming oxymoron that actually made brilliant sense. They would operate in multiple verticals but achieve deep specialization in each, building what management consultants would later call "core competencies" but what Raju simply called "knowing your craft."

Take the Buildings division. In 2000, NCC was primarily constructing government offices and basic commercial structures. By 2003, they were building India's first private sector nuclear medicine facility—a project requiring clean room technology, radiation shielding, and precision that tolerated errors in millimeters, not centimeters. The learning curve was steep. NCC sent 30 engineers to Germany and Japan for training, invested ₹15 crores in specialized equipment, and partnered with international consultants. The project was completed six months late and over budget. But NCC now had capabilities no other Indian contractor possessed.

This pattern repeated across verticals. In Transportation, NCC moved from simple road laying to complex projects like the Mumbai-Pune Expressway sections, involving tunneling through the Western Ghats. The company's engineers developed innovative solutions for monsoon-resistant construction, reducing seasonal delays by 60%. In Water & Environment, the evolution was from laying pipelines to building complete water treatment plants serving millions. The Bangalore Water Supply project alone involved 20,700 kilometers of pipeline—enough to circle Earth's equator halfway.

The numbers are staggering: By 2010, NCC had completed over 500 building projects, constructed critical sections of national highways, irrigated 350,000 acres of farmland, and provided water infrastructure for 50 million Indians. But what's more interesting is how they achieved this scale.

The company went public in 2004, listing on both NSE and BSE. The IPO raised ₹245 crores, valuing the company at roughly ₹1,200 crores. Raju, characteristically, didn't use the capital for acquisitions or expansion into new geographies. Instead, it went entirely into equipment and training. NCC became one of the first Indian construction companies to own its entire equipment fleet—from concrete mixers to earth movers. While competitors dealt with rental delays and availability issues, NCC could mobilize equipment across projects, improving utilization rates to 75% compared to industry standards of 50%.

The human capital investment was equally strategic. By 2010, NCC employed 11,000 people, with 70% being technically qualified engineers. The company established NCC Academy, an internal training institute that became mandatory for all engineers. The curriculum wasn't just technical—it included project finance, environmental compliance, and oddly enough, a course on "Construction Poetry" taught by Raju himself, where metaphors from building were used to teach problem-solving.

This decade also saw NCC's most ambitious projects. The Simhadri Super Thermal Power Project involved constructing critical components while the plant remained operational—like performing surgery while the patient runs a marathon. The Indira Sagar Polavaram Project's spillway required pouring concrete continuously for 72 hours in 45-degree heat. The Delhi Metro sections demanded tunneling under heritage structures without causing even hairline cracks.

Each project pushed boundaries. The Hyderabad International Airport, where NCC was a key contractor, introduced modular construction techniques that reduced build time by 30%. The Yamuna Expressway incorporated intelligent traffic management systems, a first for Indian highways. The Narmada Canal network used GPS-guided excavation, improving accuracy while reducing costs.

But growth brought challenges. The 2008 financial crisis hit infrastructure spending hard. Several BOT projects became unviable as traffic projections collapsed. NCC's stock, which had touched ₹180 in 2007, crashed to ₹35 by March 2009. Order book execution slowed as government payments delayed. The company's debt, taken for equipment purchases, suddenly looked onerous.

This is where NCC's conservative philosophy paid off. Unlike peers who had leveraged aggressively, NCC maintained a debt-to-equity ratio under 1.5. They had diversification across sectors—when highway projects slowed, irrigation projects continued. Most importantly, they had variable cost structures that could be adjusted without mass layoffs.

The crisis response was textbook Raju: no panic, just systematic adjustment. Projects were re-sequenced to optimize cash flow. Equipment was redeployed from stalled projects to active ones. The company even turned crisis into opportunity, hiring talented engineers laid off by competitors and acquiring distressed equipment at fraction of replacement cost.

By 2010, NCC had not just survived but emerged stronger. Revenues crossed ₹5,000 crores, the order book exceeded ₹15,000 crores, and the company had capabilities across nine construction verticals. They had completed projects in 15 states and ventured internationally into Oman and UAE. The employee count had doubled, and more remarkably, included 200+ engineers with international project experience.

Standing at his office window overlooking Hyderabad's rapidly changing skyline—much of it built by NCC—Raju could see his vision materializing. But he was 73 now, and the company needed fresh leadership for the next phase. The succession plan he'd been crafting for years was about to be tested.

V. Leadership Transition & Modern Era (2010-Present)

The handover ceremony was deliberately modest. No press conferences, no grand announcements. In 2011, AVS Raju simply introduced his son, AAV Ranga Raju, as Managing Director at the annual engineers' meet. The transition had been years in the making—the younger Raju had worked in every division, spent nights at construction sites, and earned his credibility project by project. Yet everyone wondered: could the poet's son match the founder's magic?

The timing was precarious. India's infrastructure sector was entering a crisis. The infamous "policy paralysis" of UPA-2 had frozen decision-making. Land acquisition had become a nightmare after the 2013 Act. Multiple CAG reports questioning PPP projects had made bureaucrats risk-averse. NCC's order book execution slowed to a crawl. The stock price languished around ₹40-50, a far cry from its 2007 peaks.

Ranga Raju's first major decision surprised everyone. Instead of cost-cutting or restructuring, he launched "Project Reconnect"—a systematic program to rebuild relationships with government stakeholders. Not through lobbying or influence peddling, but through transparency initiatives that were radical for the construction industry. NCC became the first major contractor to publish quarterly execution updates for all government projects, complete with delay explanations and revised timelines. They created a digital dashboard where government officials could track project progress in real-time.

The initiative seemed naive—why voluntarily highlight your delays? But it was strategic genius. Government officials, used to contractors who disappeared when projects stalled, suddenly had a partner who proactively communicated problems and solutions. Trust, that ultimate currency his father had spoken about, was being rebuilt in the digital age.

The 2014 election changed everything. The new government's infrastructure focus was unprecedented—highways, railways, smart cities, Housing for All, Swachh Bharat. NCC was perfectly positioned, but Ranga Raju understood that execution at this scale required transformation beyond his father's playbook.

The digitization drive was comprehensive. By 2016, every NCC project site had IoT sensors tracking equipment utilization, worker productivity, and material consumption. The company developed an AI model that could predict project delays 45 days in advance with 80% accuracy, allowing preemptive interventions. Drone surveys reduced site inspection time by 70%. Building Information Modeling (BIM) became mandatory for all projects above ₹50 crores.

But technology was just an enabler. The real transformation was organizational. NCC restructured from geographical divisions to vertical specializations. Each vertical became a quasi-independent unit with P&L responsibility. The Buildings division split into subcategories: hospitals, educational institutions, commercial complexes, and industrial structures—each with specialized teams.

The numbers validated the strategy. Order book grew from ₹15,000 crores in 2010 to ₹70,000 crores by 2024. Revenue scaled from ₹5,000 crores to ₹21,850 crores. The company executed landmark projects: sections of Mumbai Trans Harbour Link, Statue of Unity infrastructure, multiple metro projects, and smart city initiatives across India.

International expansion accelerated. The Oman operations, initially focused on roads, expanded to building Sultan Qaboos University's new campus. UAE projects included critical infrastructure for Dubai Expo 2020. These international projects, while just 5% of revenue, provided valuable foreign exchange and global benchmarking opportunities.

The awards accumulated. AVS Raju received the Lifetime Achievement Award from the Builders' Association of India in 2018—a touching moment where the 81-year-old poet-builder recited verses about nation-building through infrastructure. NCC earned ISO certifications across quality (9001:2015), environment (14001:2015), and safety (45001:2018)—the trifecta that opened doors to international projects.

Yet challenges mounted. Competition intensified as regional players scaled up and international contractors entered India. Margin pressure increased as government contracts moved to aggressive bidding. Working capital cycles stretched as government payments delayed—sometimes by years. The stock market remained skeptical, valuing NCC at significant discount to peers despite superior execution metrics.

The COVID pandemic tested everything. Construction sites shut overnight. Migrant workers fled cities. Supply chains collapsed. NCC's response was both humane and strategic. They housed 50,000 workers in site facilities, providing food and medical care. They created India's first "bio-bubble construction sites," allowing work to continue safely. When others laid off engineers, NCC retained everyone, using the lockdown for massive training programs.

Post-pandemic recovery was swift. The order book hit record levels as government doubled down on infrastructure spending. NCC entered new segments like data centers and renewable energy infrastructure. The smart meters division, launched in 2019, secured orders worth ₹5,000 crores by 2024.

Today, NCC stands at an inflection point. The company that started in a small Hyderabad office now operates from nine cities, employs 15,000+ people, and has its fingerprints on infrastructure serving 500 million Indians. Ranga Raju, now a decade into leadership, has proven himself worthy of his father's legacy while carving his own path.

But questions persist. Despite operational excellence, why does the market value NCC at just ₹13,992 crores—a fraction of its order book? Why do returns on equity remain stuck around 11% when the business has such strong competitive advantages? As India embarks on its most ambitious infrastructure build-out ever, can NCC finally translate operational excellence into shareholder value?

VI. The Business Model: EPC, BOT & Beyond

Understanding NCC's business model requires grasping a fundamental truth about infrastructure construction: it's not really about building things—it's about managing cash flows, risks, and relationships while things get built. The concrete and steel are just the visible output of an intricate financial and operational machine that few outsiders truly comprehend.

At its core, NCC operates through two primary models: EPC (Engineering, Procurement, Construction) contracts that generate 98.5% of revenue, and BOT (Build-Operate-Transfer) projects that create long-term annuity streams. But this simple classification masks enormous complexity.

Consider a typical EPC project—say, constructing a 1,000-bed government hospital. NCC doesn't just show up and start building. First comes the bidding process, where they compete against 10-20 qualified contractors. The bid preparation alone costs ₹50-75 lakhs—detailed engineering drawings, soil studies, cost estimates for thousands of line items, financial guarantees. Win rate? About 15-20% for competitive tenders. So NCC spends ₹3-4 crores on bidding to win one ₹500 crore project.

Once won, the real juggling begins. The government typically provides 10-15% advance, but material costs and labor mobilization require 25-30% upfront investment. NCC bridges this through working capital loans at 9-11% interest. As construction progresses, payments come in stages—foundation completion, structure completion, finishing—but each payment requires elaborate documentation and typically arrives 60-90 days late. Meanwhile, NCC must pay suppliers within 30-45 days and workers weekly.

This working capital dance is where many contractors fail. NCC's solution? Sophisticated cash flow management that would impress investment bankers. They maintain a portfolio of 200+ projects at various stages, ensuring steady cash generation. They negotiate equipment purchases during lean seasons for 20-30% discounts. They've built relationships with 500+ suppliers who provide favorable credit terms based on NCC's payment history.

The BOT model adds another layer. Take NCC's road projects on PPP basis. They invest ₹200-300 crores in construction, then operate the toll road for 15-20 years. The returns depend on traffic projections that can vary 50% from reality. NCC learned this painfully during 2008-2012 when several BOT projects became unviable. Now they're selective, focusing on routes with established traffic patterns and government revenue guarantees.

Geographic revenue composition reveals strategic thinking. While headquarters remain in Hyderabad, revenue distribution is: South (35%), North (25%), West (20%), East (15%), International (5%). This diversification isn't accidental—it hedges against regional political changes, monsoon patterns, and economic cycles. When Kerala floods halt projects, work continues in Rajasthan. When election code freezes tenders in UP, Tamil Nadu projects proceed.

The recent smart meters venture deserves attention. Unlike traditional construction, smart meters involve technology integration, data management, and long-term service contracts. NCC partnered with international technology providers, investing ₹200 crores in capabilities. Early orders worth ₹5,000 crores suggest the bet is paying off. Margins here are 12-15% compared to 8-10% in traditional construction, and working capital requirements are lower.

International operations follow a different model. In Oman and UAE, NCC focuses on negotiated contracts rather than competitive bidding. Margins are higher (12-14%), payments are prompt, but execution requirements are stricter. A delayed project in Dubai can trigger penalties of ₹1 crore per day. NCC maintains separate teams for international projects, with engineers spending 2-3 years abroad to understand local requirements.

Capital allocation reveals priorities. Of the ₹1,500 crores capex over the past five years, 60% went to equipment, 25% to technology and training, 15% to land and buildings. This contrasts with peers who've invested heavily in real estate or unrelated diversification. NCC's equipment fleet—500+ cranes, 1,000+ earthmovers, 2,000+ transit mixers—provides competitive advantage in project mobilization.

The working capital story is nuanced. Days Sales Outstanding averages 120-150 days, concerning for most industries but normal for infrastructure. NCC manages this through innovative structures. They've securitized government receivables, reducing funding costs by 200 basis points. They've negotiated equipment-backed loans at rates 300 basis points below standard working capital rates. They maintain unutilized credit lines of ₹3,000 crores for opportunity projects.

Risk management is sophisticated. Every project above ₹50 crores requires board approval. Contracts include escalation clauses for material costs beyond 5% variation. Force majeure definitions are elaborate, covering everything from floods to government policy changes. NCC maintains insurance coverage of ₹5,000 crores, including rare coverages like loss of profit due to delays.

The competitive moat isn't immediately obvious but very real. Pre-qualification for major government projects requires track record, financial strength, and technical capabilities that take decades to build. NCC is pre-qualified for the highest categories across all construction verticals—a status shared by fewer than 10 companies in India. New entrants might undercut pricing, but they can't bid for ₹1,000 crore+ projects that form NCC's bread and butter.

Yet the model has weaknesses. Government dependency means payment delays are structural, not fixable through operational efficiency. The asset-heavy nature requires continuous capital investment just to maintain competitiveness. Project-based revenue means no recurring income streams unlike software or consumer businesses. Margins are capped by competitive bidding and government rate contracts.

The question for investors: Is this a fundamentally good business? The 11% ROE suggests capital efficiency challenges. The working capital intensity means growth requires proportional funding. The government dependency creates political risk. But the ₹70,000 crore order book provides 3+ years of revenue visibility that most businesses would envy. The infrastructure super-cycle thesis suggests demand will remain robust for decades.

Perhaps the answer lies not in financial engineering but in execution excellence. In infrastructure construction, the winner isn't who has the best model but who executes the existing model better than others. NCC's track record suggests they've mastered this game. Whether that mastery translates to superior shareholder returns remains the key question.

VII. Financial Performance & Market Position

The numbers tell a story of scale, but the market's reaction tells a story of skepticism. NCC's financials read like a growth company—revenue expanding from ₹5,000 crores to ₹21,850 crores over the past decade, order book swelling to ₹70,087 crores. Yet the stock trades at just ₹13,992 crores market cap, down 30% in a year when India's infrastructure spending hit record highs. This disconnect between operational performance and market valuation is the puzzle every NCC investor must solve.

Let's start with the headline numbers from Q1 FY26. Revenue of ₹4,430 crores represents 15% year-on-year growth—respectable for a mature construction company. EBITDA margins at 9% seem thin but are actually above the industry average of 7-8%. The order book at ₹70,087 crores provides 3.2x revenue visibility, superior to most listed peers. New order wins of ₹3,658 crores in a single quarter suggest momentum continues.

But dig deeper and concerns emerge. Return on Equity averaging 11% over three years is pedestrian for a growth company. Compare this to L&T's 15% or even regional players achieving 18-20%, and you understand market skepticism. The culprit? Asset intensity. NCC's asset turnover ratio of 1.2x means they need ₹100 of assets to generate ₹120 of revenue. In a capital-scarce country where cost of capital exceeds 12%, this is problematic.

The working capital dynamics are particularly challenging. Receivables stretch to 150+ days while payables are settled in 45-60 days. This negative working capital cycle means NCC effectively finances the government's infrastructure spending. Current borrowings of ₹4,200 crores cost 9-11% annually, eating into margins. Every ₹100 crore delay in government payment costs NCC ₹2-3 crores in interest—death by a thousand cuts.

Segment performance reveals interesting patterns. The Buildings division generates 40% of revenue but 50% of profits, with margins around 10-11%. Transportation (highways, bridges) contributes 30% of revenue but margins are compressed at 7-8% due to intense competition. Water & Environment, just 15% of revenue, delivers 12% margins due to technical complexity that limits competition. The remaining verticals—electrical, irrigation, mining—are subscale but strategic for pre-qualification purposes.

The order book composition provides forward visibility. Central government projects comprise 45%, state government 40%, and private sector 15%. This 85% government dependency is both strength and weakness—assured payment (eventually) but chronic delays. The execution cycle averages 24-36 months, meaning today's order book translates to revenue over three years. Geographic distribution mirrors revenue, with no single state exceeding 20%—important risk mitigation.

Quarterly volatility is significant. Q1 typically sees 20% of annual revenue as project completions bunch around fiscal year-end. Q2 and Q3 are steadier at 25% each. Q4 can swing wildly—30% in good years, 35% when delayed projects complete. This lumpiness makes quarterly comparisons misleading, yet the market reacts sharply to every earnings miss.

The balance sheet structure reveals strategic choices. Gross debt of ₹5,500 crores seems high, but ₹3,500 crores is working capital loans and ₹2,000 crores is equipment financing at favorable rates. Net debt to equity at 0.8x is conservative for the sector. NCC maintains unused credit lines of ₹3,000 crores—dry powder for large project mobilization. The company hasn't raised equity capital since 2004, funding growth through internal accruals and debt.

Cash flow analysis is where things get interesting. Operating cash flow before working capital changes is robust at ₹1,200-1,500 crores annually. But working capital consumes ₹600-800 crores as the business grows. Capex runs ₹300-400 crores yearly for equipment replacement and upgrades. Free cash flow is therefore minimal despite profitable growth—the infrastructure contractor's paradox.

Peer comparison is illuminating. L&T trades at 2.5x book value despite similar ROE, benefiting from diversification into technology and financial services. Regional players like KNR Construction trade at 1.8x book with inferior execution track records. NCC at 1.2x book seems undervalued, but the market clearly disagrees. The discount persists despite NCC's superior order book visibility and execution track record.

Recent stock performance has been disappointing. From ₹280 peak in 2022 to current ₹220 levels, the 30% decline occurred while the broader market hit new highs. Daily volumes average just ₹50-75 crores, indicating limited institutional interest. Promoter holding at 43% provides stability but limits float. Mutual fund holding has declined from 15% to 10% over two years—a vote of no confidence from professional investors.

Management commentary provides context. They acknowledge ROE concerns but argue that infrastructure contracting inherently requires patient capital. They point to the order book quality—all government-backed projects with minimal cancellation risk. They highlight operational improvements—project execution cycles reduced by 15%, working capital days improved by 20 days. But the market wants evidence of operating leverage, not just operational improvement.

The dividend policy is conservative but consistent. Payout ratio of 20-25% seems low for a mature company, but management argues retained capital is needed for growth. Dividend yield at 1.5% won't attract income investors. The company hasn't considered buybacks despite the seemingly undervalued stock price—perhaps acknowledging capital needs for future growth.

Looking ahead, management guides for 15-20% revenue growth and margin improvement to 10-11%. Achieving this requires successful execution of the massive order book and working capital optimization. The smart meters division could be a margin kicker if execution goes well. International operations might expand beyond the current 5% of revenue.

The investment thesis ultimately hinges on whether NCC can improve capital efficiency while maintaining execution excellence. The infrastructure opportunity is undeniable—India needs $1.4 trillion in infrastructure investment by 2030. NCC is well-positioned to capture this opportunity. But unless they can improve ROE to 15%+ and optimize working capital, the stock will likely remain an underperformer despite operational success.

VIII. Culture & Philosophy: The NCC Way

Walk into any NCC project site at 6 AM and you'll witness something unusual for a construction company. Before the hammering begins, before concrete pours, engineers gather for what they call "Toolbox Talks"—but these aren't just safety briefings. A senior engineer might recite a poem about precision, a young recruit shares how yesterday's problem was solved through "common sense over complexity," and the site manager reminds everyone that they're not just building structures but "creating landmarks for generations."

This is NCC culture in action—a peculiar blend of engineering rigor and philosophical reflection that traces directly to founder AVS Raju's dual identity as poet and builder. While competitors focus purely on execution metrics, NCC has embedded something harder to replicate: a shared belief system about how construction should be done.

The foundation is what Raju called the "three-fold path"—hard work, tenacity, and common sense. Sounds simple, even banal. But observe how it plays out. When the Mumbai Trans Harbour Link project faced unexpected underwater rock formations, the engineering team worked 18-hour shifts (hard work), tried seven different drilling techniques (tenacity), and ultimately solved it by studying how local fishermen navigated currents—a solution no engineering manual suggested (common sense).

"Never hesitate to go the extra mile" isn't just a motto printed in annual reports. It's visible in countless small decisions. When hospital construction in Bhubaneswar was delayed by unseasonal rains, NCC erected temporary structures to continue interior work—adding ₹3 crores in costs they couldn't bill. When a school project in Bihar needed completion before academic year, engineers worked through Diwali holidays. These decisions make no short-term financial sense but build long-term reputation.

Sustainability wasn't fashionable when NCC adopted it in 2005, but it wasn't about fashion. The company views it through three lenses. Economic sustainability means projects that generate long-term value, not quick profits. Social sustainability involves training local workers, sourcing local materials, and ensuring projects benefit communities. Environmental sustainability includes innovations like using fly ash in concrete (reducing cement consumption by 20%) and rainwater harvesting at all project sites.

The quality philosophy is distinctive. While competitors rely on external quality audits, NCC has "Quality Circles"—groups of workers who meet weekly to identify improvement opportunities. A mason in Jaipur suggested a technique that reduced tile breakage by 30%. A crane operator in Chennai developed a signaling system that improved safety and efficiency. These aren't top-down mandates but bottom-up innovations, creating ownership at every level.

Safety culture goes beyond compliance. NCC's accident rate is 0.12 per million man-hours versus industry average of 0.35. This isn't achieved through stricter rules but through what they call "Safety Leadership"—every engineer, regardless of seniority, has authority to stop work if they observe unsafe practices. A junior engineer halting a ₹100 crore project over a safety concern doesn't face punishment but recognition.

The approach to problem-solving is distinctly NCC. They have a principle: "First understand why, then determine how." When a bridge in Assam developed cracks, instead of immediate repairs, engineers spent two weeks studying river flow patterns, soil moisture variations, and even interviewing local farmers about historical flooding. The root cause—unusual underground water channels—would never have been discovered through standard engineering protocols.

Training investment reflects long-term thinking. NCC spends ₹50 crores annually on training—2% of profits when industry average is 0.5%. Every engineer undergoes 100 hours of annual training. But most uniquely, workers receive literacy education, financial planning guidance, and even smartphone training. A mason who joined illiterate might retire capable of reading engineering drawings and managing a team.

The family business element creates interesting dynamics. While professionally managed, family values permeate operations. Project sites celebrate festivals together—Hindu, Muslim, Christian, Sikh. Personal emergencies receive immediate support—workers have received everything from medical assistance to education loans for children. This paternalistic approach seems anachronistic but creates loyalty that modern HR practices struggle to replicate.

Innovation happens through structured programs like "NCC Innovation Lab" but also through informal channels. The company maintains a WhatsApp group where field engineers share solutions. A technique for rapid concrete curing developed in Rajasthan's heat was adapted for cold weather in Himachal Pradesh. Knowledge flows horizontally, not just vertically through hierarchy.

The customer (primarily government) relationship philosophy is unique. NCC views government not as client but as partner in nation-building. This means accepting delayed payments without litigation, accommodating scope changes without confrontation, and sometimes completing additional work without formal contracts. Critics call this naive; NCC calls it investment in relationships that span decades.

Environmental initiatives go beyond compliance. Every project plants trees equal to those removed. Construction waste is segregated and recycled—concrete debris becomes road base, steel scrap is sold to recyclers, even wooden scaffolding is donated to local communities for fuel. Carbon footprint per project has reduced 25% over five years through equipment upgrades and process optimization.

The leadership development approach mirrors the founder's journey. High-potential engineers are rotated through divisions, sent to challenging projects, and given P&L responsibility early. The current CEO started as a site engineer. Five of seven business heads rose through ranks. This internal promotion culture means institutional knowledge is preserved even as the company scales.

Technology adoption follows the principle of "practical innovation." NCC doesn't chase every new technology but selectively adopts what improves execution. Drones for surveying made sense and were rapidly deployed. AI for project planning is being tested carefully. Blockchain for supply chain management was evaluated and rejected as premature. The filter is simple: does it help us build better, faster, or safer?

The cultural challenges are real. Younger engineers, especially IIT graduates, sometimes find the philosophical approach tedious. The family culture can seem slow-moving in a rapidly changing industry. The emphasis on relationships over contracts occasionally leads to commercial disadvantages. The conservative approach to technology adoption might mean missing breakthrough innovations.

Yet this culture has survived 45 years and scaled from 12 to 15,000 employees. It has weathered economic crises, political changes, and industry disruptions. Whether this cultural model can adapt to India's increasingly corporate and efficiency-driven infrastructure sector remains an open question. But for now, the NCC Way remains distinct in an industry often criticized for cutting corners and breaking commitments.

IX. Playbook: Infrastructure Investing Lessons

After decades of building India's infrastructure and creating substantial value (though not always for shareholders), NCC's journey offers a masterclass in infrastructure investing—both what to do and what to avoid. These lessons aren't theoretical; they're carved from concrete and steel, learned through delayed payments and monsoon disruptions.

Lesson 1: In infrastructure, execution capability trumps everything else. NCC didn't win by having the best technology or the lowest prices. They won by delivering projects when others couldn't. In 2009, when the financial crisis froze credit markets, NCC completed projects using internal cash flows and equipment redeployment. While competitors abandoned half-built projects, NCC's 98% completion rate became their calling card. The lesson? In infrastructure, reliability is the ultimate differentiator. A contractor who delivers a project six months late but complete is infinitely better than one who abandons it at 80% completion.

Lesson 2: Government relationships are assets that don't appear on balance sheets. NCC spent decades building trust with bureaucrats and politicians—not through corruption but through consistent delivery. When AAV Ranga Raju implemented real-time project tracking for government officials, competitors mocked it as unnecessary transparency. But when tender evaluation committees saw NCC's openness versus others' opacity, guess who won contracts? These relationships compound over time. A satisfied chief engineer in 1995 becomes a secretary in 2010 who remembers your reliability.

Lesson 3: Diversification versus specialization is a false choice—do both. NCC operates in nine verticals but maintains deep specialization in each. They're not just "construction contractors" but specialists in hospital construction, highway building, water treatment, and more. This focused diversification provides resilience (when highways slow, buildings continue) while maintaining expertise advantages. The key is ensuring each vertical is large enough to justify dedicated resources but not so large that it dominates the portfolio.

Lesson 4: Working capital management is the oxygen of infrastructure businesses. NCC's greatest weakness—stretched receivables—is also their biggest learning. They've developed sophisticated cash flow management: maintaining project portfolios at different execution stages, negotiating equipment purchases during lean periods, securitizing government receivables. The company survived when peers failed not because they were more profitable but because they managed cash better. Infrastructure investors must model cash flows, not just P&L statements.

Lesson 5: Technology adoption should be evolutionary, not revolutionary. NCC's measured approach to technology—adopting drones and IoT sensors but avoiding blockchain hype—reflects infrastructure realities. A concrete pour can't be redone if your AI algorithm fails. A bridge can't be "patched" like software. Technology must prove itself at small scale before betting projects worth hundreds of crores. This conservatism might mean missing breakthrough innovations but avoids catastrophic failures.

Lesson 6: The human element matters more in infrastructure than any other sector. A software company can scale with minimal hiring; infrastructure scales with people. NCC's investment in training seems excessive—₹50 crores annually—until you realize that a skilled crane operator prevents accidents worth crores, an experienced engineer spots problems before they become disasters. The ROI on human capital in infrastructure isn't immediately visible but compounds dramatically over time.

Lesson 7: Long-term thinking is mandatory, not optional. NCC held onto barely profitable BOT road projects for years before they turned profitable. They invested in equipment that took five years to pay back. They trained engineers who wouldn't become productive for three years. Infrastructure doesn't reward quarterly thinking. The Bangalore-Mysore corridor NCC helped build took seven years from conception to completion but now generates steady returns for 20 years.

Lesson 8: Regulatory navigation is a core competency. NCC maintains a team whose only job is understanding and ensuring compliance with thousands of regulations—environmental clearances, labor laws, safety standards, quality certifications. When regulations changed in 2013 making land acquisition harder, NCC had already built relationships with local communities, making acquisition smoother. Regulatory expertise isn't just about compliance; it's about anticipating changes and positioning accordingly.

Lesson 9: Capital allocation discipline determines returns. NCC's mediocre ROE partly stems from capital allocation choices—maintaining excess equipment for flexibility, investing in training with long paybacks, keeping debt conservative. These choices prioritize sustainability over returns. Whether this is wisdom or waste depends on your investment horizon. For a quarter, it's waste. For a decade, it might be wisdom.

Lesson 10: The infrastructure super-cycle is real but benefits aren't evenly distributed. India's infrastructure spending will undoubtedly increase—the needs are too pressing to ignore. But not all contractors will benefit equally. Those with execution capability, balance sheet strength, and government relationships will capture disproportionate value. NCC checks these boxes, but so do larger players like L&T. The winner's curse in competitive bidding means revenue growth doesn't automatically translate to profit growth.

Lesson 11: Market timing matters less than you think. NCC survived 2008's financial crisis, 2013's infrastructure slowdown, and COVID-19's disruption. They didn't time these cycles; they survived them through conservative leverage and diversification. Infrastructure investing rewards those who can survive downturns to benefit from upturns, not those who try to time cycles.

Lesson 12: Family businesses bring unique advantages and disadvantages. NCC's family ownership provides long-term thinking and cultural continuity but potentially limits access to capital and professional management. The successful transition from AVS Raju to his son is encouraging but rare. Infrastructure investors must evaluate whether family involvement is an asset or liability.

These lessons suggest a framework for infrastructure investing: Look for execution track record over financial engineering. Value relationships and regulatory expertise as much as tangible assets. Ensure diversification across projects, geographies, and customer segments. Model cash flows more carefully than earnings. Assume longer holding periods than other sectors require. And perhaps most importantly, recognize that infrastructure investing is as much about nation-building as wealth creation—the two don't always align perfectly, but when they do, the results can be extraordinary.

X. Bear vs. Bull Case Analysis

The Bear Case: Why NCC Might Disappoint

The bearish argument against NCC starts with a simple but damning observation: if this company is so good at execution, why is it so bad at generating returns? An 11% ROE in a country where risk-free rates approach 7% and equity risk premiums demand another 8-9% is simply insufficient. This isn't a temporary problem—NCC has generated pedestrian returns for years despite India's infrastructure boom.

The working capital dynamics are structurally broken. Government payments averaging 150+ days aren't improving; if anything, they're worsening as governments struggle with fiscal deficits. Every rupee of growth requires proportional working capital investment, creating a treadmill where NCC runs faster but doesn't move forward. The company is essentially providing interest-free loans to the government while borrowing at 9-11%—a negative spread business model.

Competition is intensifying from multiple directions. Large players like L&T are moving down-market, bidding aggressively for projects NCC traditionally dominated. Regional contractors are scaling up, often with local political connections that trump NCC's execution capabilities. International players are entering India, bringing advanced technology and deeper pockets. NCC's margins, already thin at 9%, face continued pressure.

The government dependency—85% of revenues—is a sword of Damocles. Political priorities shift, infrastructure spending is cyclical, and payment delays are chronic. One adverse policy change, one fiscal crisis, one political shift could devastate the order book. The company has no pricing power; government contracts come with fixed prices and unlimited liability for delays or cost overruns.

Technology disruption looms. While NCC gradually adopts drones and IoT, revolutionary changes are coming. Modular construction could eliminate 50% of on-site work. 3D printing might make traditional construction obsolete for certain structures. AI-driven project management could give tech-savvy competitors huge advantages. NCC's conservative technology adoption might leave them stranded.

The capital allocation track record is mediocre. Despite decades of operation, NCC hasn't created any valuable assets beyond construction capabilities. No land banks, no annuity assets, no technology IP. Every rupee earned has been reinvested in equipment that depreciates or working capital that doesn't compound. Where's the value creation beyond book value?

Management's conservative approach, while ensuring survival, limits upside. They won't lever up to boost ROE. They won't attempt transformative acquisitions. They won't diversify into higher-margin businesses. This steady-state approach might preserve capital but won't create wealth.

The stock's liquidity is poor, trading just ₹50-75 crores daily. Institutional investors can't build meaningful positions without impacting price. The 43% promoter holding limits float. This illiquidity creates a vicious cycle—low liquidity leads to low institutional interest, which maintains low valuations, which perpetuates low liquidity.

Succession risk remains. While AAV Ranga Raju has proven competent, the next generation's capability is unknown. Family businesses often struggle with third-generation transitions. Professional managers might not maintain the culture that's been NCC's differentiator.

The Bull Case: Why NCC Could Surprise

The bullish argument begins with India's infrastructure imperative. This isn't speculation; it's mathematical certainty. India needs $1.4 trillion in infrastructure investment by 2030 to sustain GDP growth. Roads, railways, airports, ports, urban infrastructure—everything needs upgrading. NCC, with proven execution capabilities and government relationships, will capture significant share of this spending.

The ₹70,000 crore order book provides extraordinary visibility—3.2 years of revenue already contracted. This isn't hypothetical demand but signed contracts with government backing. As execution accelerates and new orders flow, revenue growth of 15-20% is highly probable for the next 3-5 years.

Operating leverage is finally emerging. After years of investing in equipment and people, NCC has capacity to execute ₹30,000 crores annually with minimal additional investment. As revenue scales from ₹22,000 to ₹30,000 crores, most incremental revenue flows to the bottom line. EBITDA margins could expand from 9% to 12-13%, dramatically improving profitability.

The smart meters opportunity is transformative. With ₹5,000 crores already won and potential market of ₹50,000 crores, this higher-margin business (12-15% versus 8-10% for traditional construction) could become a significant profit driver. Unlike construction, smart meters involve recurring maintenance revenue—finally, an annuity stream.

Government payment delays, while painful, are improving. Digital payment systems, direct benefit transfers, and improved tax collections are strengthening government finances. Several states have cleared long-pending dues. As fiscal situations improve, working capital pressure should ease.

The international opportunity is underappreciated. Middle East infrastructure spending is massive, and NCC's track record with Indian labor and cost management provides advantages. International revenue could grow from 5% to 15-20% over five years, providing foreign currency earnings and geographic diversification.

Technology adoption, while conservative, is accelerating. The new generation of leadership understands digital transformation. Investments in project management software, IoT sensors, and data analytics are improving execution efficiency. These aren't visible yet in financials but will manifest as improved margins and faster execution.

The valuation discount is excessive. At 1.2x book value versus peers at 2-2.5x, NCC trades as if it's a failing company, not one with strong execution and massive order book. Even modest re-rating to 1.8x book implies 50% upside. If ROE improves to 15% through operating leverage, the stock could double.

The dividend growth potential is significant. As working capital pressure eases and profitability improves, payout ratios could increase from 20-25% to 40-50%. Combined with earnings growth, dividends could compound at 20%+ annually.

Industry consolidation is inevitable. Smaller contractors can't meet increasing technical and financial requirements. NCC could acquire distressed competitors at attractive valuations, gaining order books and capabilities while eliminating competition. The fragmented industry structure provides multi-year consolidation opportunities.

Management quality is underappreciated. The smooth leadership transition, conservative balance sheet management, and consistent execution demonstrate competence. While not flashy, this steady management might be exactly what's needed for a infrastructure business.

The Verdict: The bear case is about financial metrics—low ROE, working capital intensity, margin pressure. The bull case is about strategic position—massive infrastructure opportunity, proven execution, and improving operations. For short-term traders seeking quick returns, NCC will disappoint. For patient investors who believe in India's infrastructure story and value execution over financial engineering, NCC might surprise. The key question: can operational excellence eventually translate to financial excellence? The next 3-5 years will provide the answer.

XI. Power & Verdict

In the framework of Hamilton Helmer's "7 Powers," where does NCC's competitive advantage truly lie? This isn't an academic exercise—understanding the source and sustainability of NCC's moat determines whether this is an investment or a value trap.

NCC doesn't possess Scale Economies in the traditional sense. Yes, they can spread equipment costs across projects, but so can competitors. Their ₹22,000 crore revenue doesn't provide meaningful cost advantages over someone operating at ₹10,000 crores. Construction doesn't have the fixed-cost leverage of software or manufacturing.

Network Effects are absent. NCC completing a project in Tamil Nadu doesn't make them more valuable to clients in Rajasthan. Each project stands alone, won through competitive bidding, executed independently. There's no compounding value from network expansion.

Counter-Positioning isn't their game. NCC hasn't adopted a radically different business model that incumbents can't match. They play by the same rules as everyone else—competitive bidding, government contracts, standard execution methods.

Switching Costs barely exist. Governments can easily switch contractors between projects. There's no lock-in, no proprietary systems that create dependencies. Each tender is a new competition where past performance provides advantage but not guarantee.

Branding matters less in B2G (business-to-government) construction. Bureaucrats don't choose NCC because of brand preference but because of technical scores and price quotes. The NCC name carries weight in corridors of power, but it's not Apple or Coca-Cola.

Cornered Resource seemed possible—perhaps their engineering talent or government relationships? But engineers can be hired by competitors, and relationships, while valuable, aren't exclusive. NCC doesn't control any resource that others can't access.

This leaves Process Power—and here, finally, we find NCC's true moat. Over 45 years, they've developed processes that are nearly impossible to replicate quickly. Not just technical processes, but organizational capabilities embedded in culture and refined through thousands of projects.

Consider their project execution process. When NCC wins a ₹500 crore hospital project, a machine activates. The mobilization team has detailed playbooks for equipment deployment. The procurement team has relationships with 500+ suppliers who provide credit terms unavailable to new entrants. The project management system, refined over decades, anticipates problems before they occur. The quality circles identify improvements that reduce costs by 2-3%—marginal individually but substantial cumulatively.

This Process Power manifests in measurable ways: 98% on-time completion versus 70% industry average. Cost overruns of 12% versus 45% industry average. Safety record of 0.12 accidents per million man-hours versus 0.35 industry average. These aren't lucky outcomes but systematic results from superior processes.

But Process Power has limitations. It provides competitive advantage but not pricing power. It ensures survival but not spectacular returns. It's defensive—preventing failure—rather than offensive—capturing extraordinary value. This explains NCC's paradox: operational excellence with mediocre financial returns.

The Infrastructure Super-Cycle Thesis requires examination. Bulls argue India's infrastructure spending will drive multi-year growth. The need is undeniable—India's infrastructure stock is $2 trillion versus $35 trillion for the US despite comparable landmass. But need doesn't automatically translate to opportunity.

Government infrastructure spending is inherently cyclical. Electoral cycles, fiscal constraints, and political priorities create volatility. The 2004-2008 boom was followed by 2009-2013 slowdown. The 2014-2019 acceleration was interrupted by COVID. Current optimism might face reality when fiscal deficits force spending cuts.

Moreover, increased spending doesn't guarantee improved profitability. When government announces massive programs, every contractor bids aggressively, destroying margins. The highway construction boom of 2010-2012 led to many contractors going bankrupt despite revenue growth. Volume without pricing power is a dangerous combination.

Can NCC maintain margins while scaling? This is the trillion-rupee question. The bear case says no—competition will intensify, government will squeeze contractors, and margins will compress toward cost of capital. The bull case argues operating leverage will emerge—fixed costs spread over larger revenue will expand margins.

History provides mixed evidence. NCC's margins have remained remarkably stable at 8-10% despite revenue growing 4x over a decade. This suggests neither margin expansion nor compression is inevitable. The outcome depends on execution excellence continuing while competition doesn't catch up—possible but not certain.

Final Assessment: NCC is a competent executor in a structurally challenging industry. They've built meaningful Process Power that ensures survival and steady growth. The massive order book provides near-term visibility. The infrastructure opportunity is real though cyclical. Management is capable though conservative.

For investors seeking explosive returns, NCC will disappoint. This isn't a technology disruptor or market creator. It won't deliver 10x returns or transform industries. For investors seeking steady compounding with limited downside, NCC might work. The ₹70,000 crore order book provides downside protection. The infrastructure theme provides multi-year tailwinds. The valuation at 1.2x book provides margin of safety.

The key insight: NCC is priced for disappointment but positioned for steady execution. If they simply deliver what's already contracted, maintain historical margins, and capture fair share of future spending, the stock could deliver 15-20% annual returns. Not spectacular, but in a world of zero interest rates and volatile markets, perhaps sufficient.

The verdict comes down to investor temperament. If you need excitement, look elsewhere. If you value predictability, execution, and exposure to India's infrastructure build-out without paying premium valuations, NCC warrants consideration. It's not a great business, but it might be a good investment at the right price. And sometimes, in investing as in construction, good enough is exactly what you need.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube