KEC International: The Infrastructure Giant's Journey

I. Introduction & Episode Roadmap

Picture this: A massive transmission tower rising from the desert sands of Saudi Arabia, its steel lattice structure gleaming under the harsh sun. Another stands sentinel in the Brazilian rainforest, power lines stretching across impossible terrain. A third emerges from the frozen tundra of Canada. All bear the same maker's mark—KEC International, a company that began in the chaos of post-independence India and transformed into a global infrastructure colossus.

The question that drives this story isn't just how a transmission tower manufacturer survived multiple near-death experiences to become a $3 billion infrastructure powerhouse. It's how a company founded to electrify a newly independent nation became the unlikely protagonist in the global infrastructure story, operating across 110 countries and competing with giants ten times its size.

KEC International today stands as the flagship infrastructure company of the RPG Group, but that descriptor barely captures the journey. This is a company that manufactures transmission towers in Mexico, builds railway lines in Ethiopia, constructs solar farms in the Middle East, and lays pipelines in Southeast Asia. It's a vertically integrated infrastructure player that designs, manufactures, and executes projects from concept to commissioning—a rare capability in the fragmented world of engineering, procurement, and construction (EPC).

The company's evolution mirrors India's own economic transformation: from import substitution to global ambitions, from government contractor to multinational competitor, from survival mode to strategic expansion. Along the way, KEC accumulated lessons in crisis management, global expansion, and the delicate art of infrastructure finance that read like a masterclass in industrial strategy.

What makes KEC particularly fascinating for students of business history is how many times the company could have—should have—died. The oil crises of the 1970s. The debt spiral of the early 1980s. The Asian financial crisis. The 2008 global meltdown. Each time, through a combination of strategic pivots, timely acquisitions, and sheer execution capability, the company emerged stronger.

This episode traces that arc through distinct phases: the founding vision of Ramjibhai Kamani and the post-independence industrial boom; the spectacular international expansion followed by near-bankruptcy; the RPG acquisition and methodical turnaround; the global expansion through strategic acquisitions; and the modern diversification into railways, civil infrastructure, and renewable energy. We'll examine how a company with relatively modest financial metrics—₹22,358 crore in revenue, 2.61% net margins, and an 8.82% ROE—commands respect in boardrooms from Lagos to Lima.

We'll also explore the strategic questions facing KEC today: How does a traditional infrastructure company navigate the energy transition? Can execution excellence overcome the inherent challenges of low-margin, capital-intensive businesses? And in a world where software eats everything, what's the moat for a company that bends steel and pours concrete?

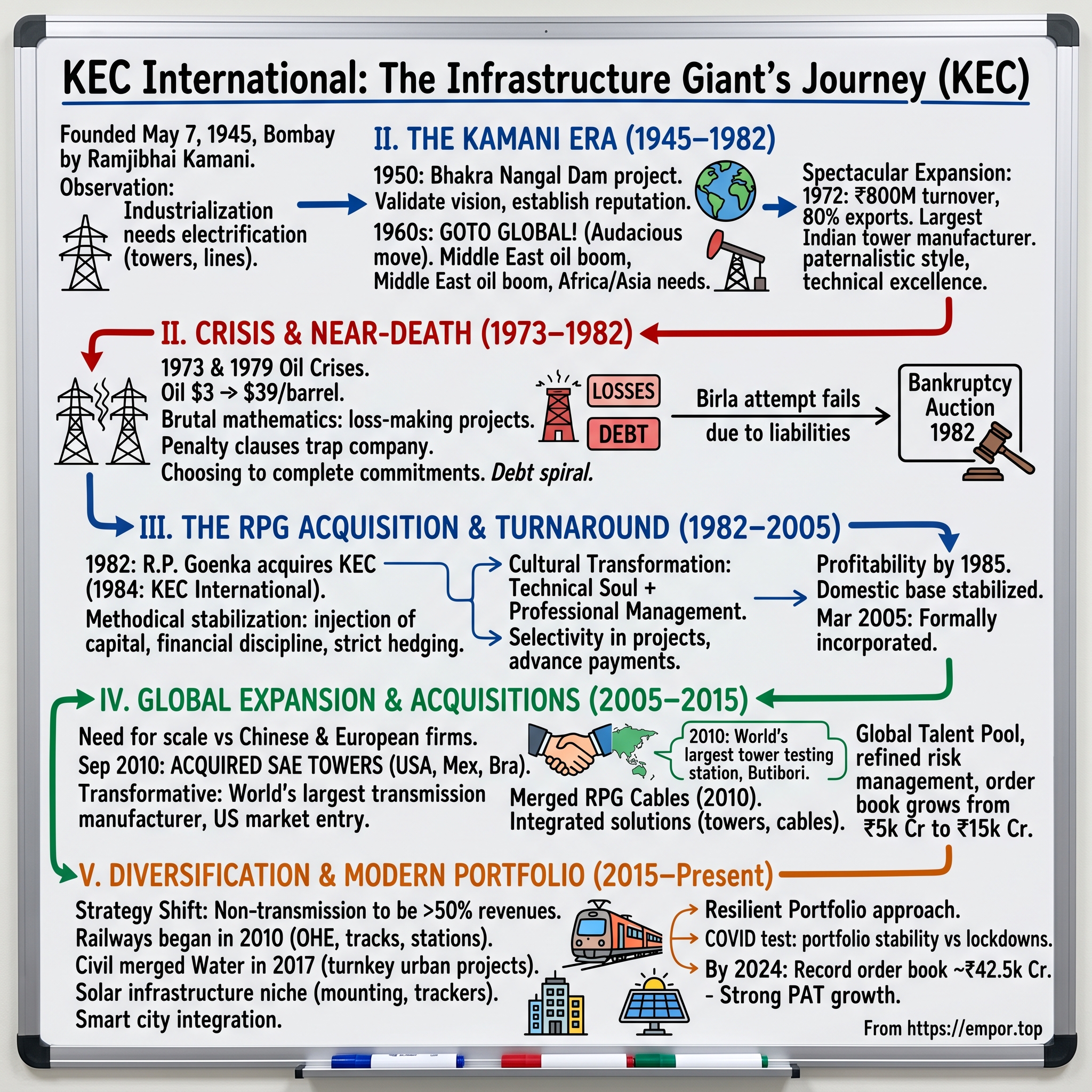

II. Founding & The Kamani Era (1945–1982)

The date was May 7, 1945. World War II was ending in Europe, India was two years from independence, and in Bombay, Ramjibhai Kamani was founding what would become Asia's first electric power transmission company. The timing wasn't coincidental—Kamani understood that the infrastructure of empire would soon become the backbone of a nation.

Kamani Engineering Corporation, as it was originally known, began with a simple observation: India's industrialization would require massive electrification, and someone needed to build the physical infrastructure to carry that power. While others focused on generating electricity or manufacturing equipment, Kamani saw opportunity in the unglamorous middle—the towers, lines, and substations that would connect power plants to cities and factories.

The early years were defined by nation-building projects that read like a roster of India's industrial ambitions. In 1950, just three years after independence, KEC received what would prove to be a transformational order: supplying transmission towers for the Bhakra Nangal Dam project. This wasn't just any infrastructure project—Bhakra Nangal was Nehru's "temple of modern India," a symbol of the young nation's technological aspirations. For KEC to be chosen as the transmission partner validated Kamani's vision and established the company's reputation as a serious player in India's industrialization story.

What distinguished Kamani's approach was his early recognition that transmission technology wasn't just about steel fabrication—it was about engineering solutions for diverse terrains and climates. India, with its mountains, deserts, forests, and flood plains, served as a perfect laboratory. Every project taught KEC something new: how to design towers that could withstand Himalayan winds, how to string lines across the Thar Desert, how to protect equipment from monsoon corrosion.

By the 1960s, Kamani made a decision that would define KEC's trajectory for the next decade: go global. This wasn't the obvious move it might seem in retrospect. Indian companies in the 1960s were largely focused on the protected domestic market. Foreign exchange was scarce, international competition was fierce, and the very idea of an Indian engineering company competing globally seemed audacious.

But Kamani saw opportunity where others saw obstacles. Many newly independent nations in Africa and Asia faced the same infrastructure challenges as India but lacked the technical expertise. Middle Eastern countries, flush with oil revenues, were building modern power grids from scratch. KEC's experience in challenging Indian conditions—combined with cost advantages and engineering ingenuity—made it uniquely positioned to serve these markets.

The international expansion was nothing short of spectacular. By the early 1970s, KEC had executed turnkey power transmission projects across an improbable geographic spread: Iran, Iraq, Kuwait, Saudi Arabia, Sudan, Egypt, Nigeria, Algeria, Mauritius, Indonesia, Malaysia, Thailand, the Philippines, Australia, New Zealand, Brazil, the United States, and Canada. The company was stringing power lines across six continents, adapting its designs for everything from Arabian sandstorms to Canadian blizzards.

The numbers told a remarkable story. By 1972, KEC's turnover had reached nearly ₹800 million, with an astounding 80% coming from exports. The company had become the largest manufacturer of transmission towers in India and the second largest globally, trailing only SAE of Italy. For a company founded just 27 years earlier in a country that had barely begun industrializing, this was an extraordinary achievement.

The Kamani management style was quintessentially that of a family business of its era—paternalistic, hands-on, and deeply personal. Ramjibhai Kamani knew his engineers by name, visited project sites personally, and maintained relationships with key customers that went beyond business. The company culture emphasized technical excellence and customer relationships over financial engineering or strategic planning. This approach worked brilliantly during the expansion phase when opportunities exceeded capacity and relationships drove business.

KEC's technology capabilities evolved rapidly during this period. The company wasn't just fabricating towers to foreign specifications—it was developing its own designs, testing new materials, and pioneering construction techniques. The establishment of one of Asia's first tower testing stations allowed KEC to validate designs for extreme conditions, giving it credibility with international clients who might otherwise hesitate to work with an Indian company.

The project execution capabilities KEC developed during this era would prove to be its most enduring competitive advantage. Building transmission infrastructure in remote locations required not just engineering skills but logistical mastery. How do you transport massive steel structures to a desert site with no roads? How do you string high-voltage lines across a tropical forest during monsoon season? How do you coordinate hundreds of workers speaking different languages across multiple time zones? KEC developed playbooks for all these scenarios, accumulated through trial and error across hundreds of projects.

By 1973, KEC stood at the pinnacle of its international success. The company had projects running simultaneously on multiple continents, a bulging order book, and a reputation as one of the few companies capable of executing complex transmission projects anywhere in the world. Ramjibhai Kamani's vision of building a global infrastructure company from India had been spectacularly vindicated.

But this success contained the seeds of near-catastrophe. The very factors that drove KEC's international expansion—ambitious projects in challenging locations, contracts denominated in foreign currencies, long execution cycles, and heavy capital requirements—would soon combine with external shocks to push the company to the brink of collapse.

III. Crisis & Near-Death Experience (1973–1982)

October 1973. As KEC engineers celebrated Diwali in transmission line camps from Nigeria to Indonesia, oil ministers in Kuwait were making decisions that would quadruple global crude prices overnight. The Yom Kippur War had triggered an oil embargo, and the first oil crisis was about to detonate across the global economy. For KEC, with 80% of revenues coming from international projects priced in dollars, this was the beginning of a nine-year fight for survival.

The mathematics of disaster were elegantly simple and brutally unforgiving. KEC had bid for projects when oil was $3 per barrel. By the time these projects were being executed, oil had hit $12. Since most international infrastructure projects involved substantial transportation costs, equipment imports, and energy-intensive construction processes, KEC's carefully calculated margins evaporated overnight. A project bid at 15% margins could suddenly be losing money before the first tower was erected.

But here's what made KEC's situation particularly precarious: the company couldn't simply walk away from unprofitable contracts. Infrastructure projects, especially those involving national power grids, came with massive performance bonds and penalty clauses. Abandoning a half-completed transmission line in Saudi Arabia or Nigeria wouldn't just mean losing money—it would trigger penalties that could bankrupt the company and destroy its reputation permanently. KEC was trapped in a spider's web of its own success.

The company's response revealed both the strength and weakness of the Kamani-era management philosophy. True to their engineering roots and customer-first approach, KEC chose to complete every single project commitment, regardless of the financial hemorrhaging. Teams in the field were told to maintain quality and meet deadlines. The company's reputation for reliable execution, built over decades, would be preserved at any cost.

By 1976, as the company struggled to complete loss-making projects while bidding for new ones just to maintain cash flow, a second crisis emerged from an unexpected quarter. Indian financial institutions, particularly the Industrial Development Bank of India (IDBI), had invested approximately ₹230 million in KEC through various instruments. As the company's losses mounted and debt servicing became erratic, these institutions grew increasingly nervous. What had seemed like a solid investment in India's most successful transmission company suddenly looked like a potential write-off.

The situation attracted the attention of one of India's most powerful business houses. K.K. Birla, part of the legendary Birla family and owner of Texmaco (a heavy engineering company), saw opportunity in KEC's distress. Here was a company with incredible international relationships, proven execution capabilities, and a global footprint—available at a distressed valuation. Birla began accumulating shares and maneuvering for control. The battle for control took an unexpected turn. Rather than pushing through with a hostile takeover, Birla retreated—reportedly after discovering the true extent of KEC's financial obligations and the complexity of its international contract commitments. The very global footprint that made KEC attractive also made it a minefield of contingent liabilities and performance guarantees that could trigger cascading defaults across multiple jurisdictions.

Then came 1979, and with it, a second oil shock. The Iranian Revolution disrupted global oil supplies once again, and oil prices more than doubled to $39.50 per barrel within twelve months. For KEC, already struggling to complete loss-making projects from the first crisis, this was potentially fatal. The company was now executing projects bid at $3 oil with costs based on $39 oil—a thirteen-fold increase that no amount of efficiency could overcome.

KEC accumulated heavy financial debt during the 1973 oil crisis and the 1979 energy crisis, both of which adversely affected international transactions conducted in US Dollars as world crude oil prices quadrupled. The company struggled but was bound to completing its project commitments. This resulted in the company incurring heavy losses.

The endgame approached with inexorable logic. By 1981, KEC's financial reports showed losses that shocked even the battle-hardened financial institutions. The company's debt servicing had become erratic, working capital had evaporated, and new projects were being bid just to generate cash flow to complete old ones—a classic death spiral. International clients began withholding payments, concerned about KEC's ability to complete projects. Equipment suppliers demanded cash upfront. The company that had once commanded respect in boardrooms from Riyadh to Rio was now struggling to maintain basic operations.

In 1982, the inevitable happened. Unable to clear its mounting debts and with financial institutions unwilling to extend further support, KEC was put up for auction by the Maharashtra government for recovery of dues. The company that Ramjibhai Kamani had built over 37 years, that had electrified nations and competed with global giants, was being sold to the highest bidder to satisfy creditors.

The lessons from this near-death experience would resonate through Indian corporate history. First, international expansion without adequate currency hedging in volatile times was potentially fatal. Second, the pursuit of engineering excellence and customer satisfaction, while admirable, needed to be balanced with financial prudence. Third, long-cycle infrastructure projects required not just technical capability but sophisticated risk management. And finally, sometimes the very factors that drive spectacular growth—ambitious projects, global reach, reputation-driven commitment—can become the anchors that drag a company under when external conditions shift.

But even as the auctioneer's gavel was about to fall, another player was watching carefully from the sidelines. R.P. Goenka, chairman of the RPG Group, saw in KEC's distress not just a company in crisis but an infrastructure platform with capabilities that money couldn't easily buy. The stage was set for one of Indian corporate history's most dramatic turnarounds.

IV. The RPG Acquisition & Turnaround (1982–2005)

R.P. Goenka sat in his Bombay office studying KEC's auction documents with the intensity of a chess grandmaster analyzing an endgame. Where others saw insurmountable debt and operational chaos, Goenka saw something different: a company with engineering DNA that had taken four decades to build, relationships across six continents, and a brand that still commanded respect despite its financial distress. The question wasn't whether KEC was worth saving—it was how to acquire it without inheriting the very problems that had destroyed the Kamanis and deterred the Birlas.

Goenka's approach to the KEC acquisition revealed a strategic sophistication that would become the hallmark of RPG's turnaround. Rather than bidding directly in the government auction, he began a careful campaign of relationship building and tactical positioning. Even after financial institutions stepped in, some members of the Kamani family continued to hold a small number of shares in the company. Goenka carefully maneuvered to purchase these shares, making sure that he did not get trapped in the same pitfalls that had defeated the Birla's attempts to take over KEC.

The strategy was multi-pronged. First, Goenka negotiated with financial institutions, not just about price but about post-acquisition support. He understood that KEC would need working capital, guarantees for ongoing projects, and breathing room to restructure. Second, he engaged with key customers, particularly in the Middle East, assuring them that under RPG management, their projects would be completed. Third, and perhaps most importantly, he identified and courted KEC's senior technical leadership, recognizing that the company's true value lay not in its factories or equipment but in its accumulated engineering knowledge.

In 1982, the RPG Group successfully acquired KEC, and by 1984, the company was renamed KEC International—a signal of Goenka's global ambitions for the firm. The immediate challenge was stabilizing operations while maintaining the company's technical capabilities. Goenka's first moves were telling: rather than massive layoffs or asset sales, he focused on completing existing projects, even the loss-making ones. This decision, while costly in the short term, preserved KEC's reputation and kept its technical teams intact.

The financial restructuring was methodical rather than dramatic. RPG injected fresh capital, but more importantly, it brought financial discipline that had been absent during the Kamani era. Project bidding now required multiple levels of approval. Currency exposures were hedged. Working capital was managed with military precision. The company that had once operated on engineering excellence and customer relationships now added a third pillar: financial rigor.

The cultural transformation under RPG was profound yet respectful of KEC's heritage. The Kamani-era focus on technical excellence remained, but it was now paired with professional management practices. Goenka brought in managers from other RPG companies, creating a cross-pollination of ideas and practices. Performance management systems were introduced. Cost centers were established. The family business transformed into a professionally managed corporation, though one that retained its engineering soul.

By 1985, just three years after acquisition, KEC was profitable again. The turnaround wasn't based on any single dramatic intervention but rather on hundreds of small improvements: better project selection, tighter cost control, improved collection processes, strategic hedging of currency exposures. The company's revenue, which had stagnated at around ₹550 million during the crisis years, began growing again.

The international strategy under RPG was markedly different from the Kamani era. Rather than chasing projects across the globe, KEC became selective. Projects were evaluated not just on technical feasibility but on payment terms, currency risks, and execution complexity. The company began insisting on advance payments and letters of credit. The cowboy internationalism of the 1970s gave way to calculated global expansion.

A crucial element of the turnaround was the integration with the broader RPG Group. KEC could now leverage the group's financial strength for performance guarantees. It could tap into RPG's relationships with Indian financial institutions for working capital. Perhaps most importantly, it became part of a diversified conglomerate, reducing its vulnerability to sector-specific shocks.

The 1990s brought new challenges and opportunities. India's economic liberalization opened domestic markets but also brought international competition. KEC's response was to modernize its manufacturing facilities and expand its product range. The company invested in galvanizing plants, upgraded its tower testing facilities, and began manufacturing higher-capacity transmission towers for the emerging 400kV and 765kV lines.

Project execution capabilities were systematically enhanced. KEC developed specialized teams for different terrains—desert specialists for Middle Eastern projects, mountain teams for Himalayan assignments, forest experts for South American ventures. The company created detailed execution playbooks, documenting lessons from hundreds of projects. What had been tribal knowledge in the Kamani era became institutionalized expertise under RPG.

The relationship with government and public sector undertakings was carefully cultivated. As India embarked on massive power sector expansion in the 1990s, KEC positioned itself as the domestic player with proven international experience. The company won major contracts from Power Grid Corporation, state electricity boards, and the railways. The home market, somewhat neglected during the international expansion of the 1970s, became a stable foundation for growth.

By the late 1990s, KEC had emerged as a different company. Revenue had crossed ₹2,000 million. The company was profitable, growing, and financially stable. It had preserved its engineering excellence while adding professional management. It maintained its international presence while building a strong domestic base. The near-death experience of 1982 seemed like ancient history.

On 18 March 2005, KEC International Limited was incorporated in the Ministry of Corporate Affairs, India, marking a formal milestone in the company's transformation. This wasn't just a legal reorganization—it was the culmination of a 23-year journey from bankruptcy to stability, from family business to professional corporation, from crisis to opportunity.

The RPG turnaround of KEC offers several lessons for distressed asset investing. First, the true value of an engineering company lies in its capabilities and relationships, not its physical assets. Second, cultural transformation must respect organizational heritage while introducing new practices. Third, financial discipline and engineering excellence aren't mutually exclusive—they're mutually reinforcing. Finally, sometimes the best acquisitions are the ones where others have already tried and failed, leaving valuable lessons about what not to do.

As KEC entered the new millennium, it stood ready for its next transformation: from domestic champion to global infrastructure major. The foundation laid during the RPG turnaround would prove crucial for the ambitious expansion that lay ahead.

V. Global Expansion & Strategic Acquisitions (2005–2015)

The boardroom at KEC's Mumbai headquarters buzzed with tension in September 2010. On the table was a decision that would either catapult KEC into the global infrastructure elite or saddle it with debt and complexity that could trigger another crisis. The target: SAE Towers, the American transmission tower giant with operations across the Americas. The price: undisclosed but substantial. The stakes: nothing less than KEC's future as a global infrastructure player.

The pursuit of SAE Towers represented a strategic inflection point that had been years in the making. By 2005, KEC had fully recovered from its near-death experience and was generating steady profits from its India and Middle East operations. But the global infrastructure landscape was consolidating rapidly. Chinese companies, backed by state support, were bidding aggressively for international projects. European firms were leveraging technology advantages. In this environment, scale wasn't just an advantage—it was survival.

The SAE acquisition strategy began not in boardrooms but on project sites. KEC engineers working in South America kept encountering SAE's footprint—well-run factories in Brazil, efficient operations in Mexico, strong customer relationships in the United States. Unlike KEC's previous international forays, which involved building capabilities from scratch, SAE offered existing infrastructure, local knowledge, and most crucially, a ticket into the highly regulated U.S. transmission market.

But before KEC could pursue external acquisitions, it needed to consolidate internally. In March 2010, RPG Cables was merged with KEC International, adding a vertical that would prove increasingly valuable as transmission projects became more integrated. The cable business brought different dynamics—shorter project cycles, different working capital requirements, more standardized products—but also synergies with the transmission business. Customers increasingly wanted integrated solutions: towers, cables, and complete transmission systems from a single vendor.

The approach to the SAE acquisition revealed how much KEC had learned from its history. Due diligence teams spent months analyzing not just financial statements but currency exposures, contract obligations, and contingent liabilities—the very issues that had nearly destroyed KEC in the 1970s. Legal teams scrutinized environmental obligations, especially in the U.S., where cleanup costs could dwarf acquisition prices. Operations teams evaluated manufacturing efficiency, looking for synergies and redundancies.

In September 2010, KEC International acquired Houston, Texas based SAE Towers, a group of operating companies incorporated in the United States, Mexico and Brazil consolidated through SAE Towers Holdings, LLC. The acquisition was transformative in multiple dimensions. First, it created the world's largest transmission tower manufacturer with approximately 300,000 tons of annual production capacity. Second, it gave KEC manufacturing facilities in strategic locations across the Americas. Third, and perhaps most importantly, it provided entry into markets where being a local manufacturer was either legally required or commercially essential.

The integration of SAE revealed the sophistication KEC had developed in managing global operations. Rather than imposing Indian management practices on American operations, KEC adopted a federal structure. SAE's U.S. operations retained their leadership and practices while adopting KEC's project execution methodologies. The Brazilian operations, which served the booming South American infrastructure market, became a hub for regional expansion. The Mexican facilities, with their proximity to the U.S. and lower costs, became strategic manufacturing centers for North American projects.

Technology upgradation was a parallel priority. In April 2010, KEC International set up the world's largest tower testing station at Butibori, in Nagpur. This wasn't just about size—it was about capability. The facility could test towers for 1200kV transmission lines, voltages that didn't yet exist commercially but were being planned for India's power evacuation needs. The testing station became a statement of intent: KEC wasn't just executing today's projects but preparing for tomorrow's challenges.

The global manufacturing footprint that emerged by 2012 was strategically elegant. India remained the hub for engineering and design, leveraging its cost advantages and technical talent. The Middle East facility in Dubai served the Gulf markets and Africa, providing local content for projects requiring it. Brazil manufactured for South America, Mexico for North America, and specialized products were shipped globally from the most efficient location. This wasn't just about cost optimization—it was about speed, local content requirements, and risk distribution.

The acquisition strategy extended beyond manufacturing assets. KEC began acquiring specialized capabilities through smaller, targeted deals. A concrete pole manufacturing company was acquired to serve the distribution segment. A Belgian engineering firm was brought in for its expertise in offshore transmission structures. Each acquisition was modest in size but strategic in intent, adding capabilities that would be expensive and time-consuming to develop organically.

The evolution toward becoming a complete EPC player was gradual but deliberate. Initially, KEC manufactured towers and strung lines. Then it added substation construction. Cable laying capabilities were integrated. By 2015, KEC could take a transmission project from conception to commissioning—designing the route, manufacturing the towers, laying the cables, building the substations, and handing over a functioning system to the customer. This full-stack capability became a significant competitive advantage, especially in emerging markets where clients preferred single-point accountability.

Financial management during this expansion phase showed how far KEC had evolved from its 1970s crisis. Each acquisition was carefully structured to minimize currency risks. Debt was raised in the currencies where revenues would be generated. Natural hedges were created by matching costs and revenues in the same currency. The company that had once been brought down by dollar-denominated debt now managed a complex multi-currency operation with sophisticated hedging strategies.

The market response was validating. KEC's order book grew from ₹5,000 crore in 2005 to over ₹15,000 crore by 2015. The company was executing projects simultaneously in over 30 countries. Its client list read like a who's who of global utilities: PowerGrid in India, Transco in the UAE, Eletrobras in Brazil, CFE in Mexico. The company that had once desperately completed loss-making projects to preserve its reputation now had customers queuing up for its services.

The human capital strategy evolved in parallel with geographic expansion. KEC created a global talent pool, rotating engineers between geographies to build broad expertise. An Indian engineer might spend two years in Brazil learning about Amazon basin projects, then move to Dubai for desert assignments. This cross-pollination created a cadre of engineers who could execute projects anywhere, understanding not just technical requirements but local regulations, cultural nuances, and logistical challenges.

By 2015, KEC had transformed from an Indian company with international operations to a truly global infrastructure firm. It designed towers in India for manufacture in Mexico for installation in the United States. It bid for projects as part of international consortiums, partnering with Japanese trading houses, European equipment manufacturers, and local construction firms. The company operated with the complexity of a multinational while retaining the agility of its entrepreneurial roots.

The decade of global expansion validated several strategic insights. First, in infrastructure, local presence matters as much as technical capability. Second, acquisitions in the infrastructure space are as much about acquiring market access and relationships as physical assets. Third, managing a global manufacturing footprint requires federal structures that balance global standardization with local adaptation. Finally, the evolution from equipment supplier to EPC contractor is a natural progression that clients value and competitors struggle to replicate.

As KEC entered 2015, it faced a new challenge: how to diversify beyond transmission while leveraging its core infrastructure capabilities. The answer would reshape the company yet again.

VI. Business Diversification & Modern Portfolio (2015–Present)

The strategy presentation at RPG's annual leadership conference in 2015 contained a slide that would have seemed heretical just a decade earlier. It showed KEC's revenue projections for 2025 with transmission contributing less than 50% of total revenues. For a company that had built its identity around transmission towers for seven decades, this was a profound shift. But the logic was compelling: infrastructure spending was shifting toward urban development, railways modernization, and renewable energy. KEC could either remain a transmission specialist and watch these opportunities pass by, or leverage its capabilities to capture emerging growth markets.

The railways diversification began almost by accident. In 2010, KEC had bid for a transmission line project that happened to run parallel to a railway track. The railways department, impressed by KEC's execution, asked if the company could also handle railway electrification. The technical capabilities were similar—steel structures, high-voltage systems, complex logistics—but the domain was entirely different. KEC said yes, completed the project successfully, and discovered a market growing even faster than power transmission.

By 2016, KEC's railways business had evolved far beyond overhead electrification. The company's diverse portfolio of projects in railways included overhead electrification (OHE), laying of new railway lines, doubling and tripling of tracks, tunnel ventilation, speed upgradation, and construction of railway stations, platforms and bridges. Each capability was built incrementally, leveraging existing strengths while acquiring new competencies. The tower manufacturing expertise translated into OHE structures. Project management capabilities developed for transmission lines applied to track laying. The ability to work in difficult terrains, honed over decades of transmission projects, proved invaluable for railway projects in mountainous regions.

The railway sector's dynamics differed markedly from transmission. Projects were more visible to the public, timelines were often political, and safety requirements were stringent. A delayed transmission line might affect industrial customers; a delayed railway project could disrupt millions of commuters. KEC adapted by creating specialized railway teams, developing new project management protocols, and investing in railway-specific equipment and training.

The civil infrastructure diversification followed a different path—through integration rather than expansion. In 2017, the Company's Water Business was merged with the Civil Business. The Civil Business now undertakes turnkey construction for Residential, Industrial and Commercial projects, including workshops. This wasn't just organizational restructuring—it reflected a strategic insight. Urban infrastructure projects increasingly required integrated capabilities: a metro project might need stations (civil), electrification (railways), and power supply (transmission). By combining these capabilities, KEC could bid for complex urban infrastructure projects that pure-play competitors couldn't handle.

The solar pivot arrived as the renewable energy revolution gained momentum. Here, KEC's approach was particularly clever. Rather than competing in solar panel manufacturing, where Chinese companies had unassailable cost advantages, or project development, where different skills were needed, KEC focused on solar infrastructure—the mounting structures, trackers, and balance of systems that comprised 40% of a solar project's cost. The company's steel fabrication expertise, project execution capabilities, and global presence made this a natural adjacency.

By 2020, KEC was executing solar projects across the Middle East and India, providing complete EPC services minus the panels themselves. A typical project might involve KEC designing the layout, manufacturing the mounting structures, installing the panels (sourced from others), and connecting the plant to the grid. The company had found a profitable niche in the solar value chain without the capital intensity of manufacturing or the development risk of project ownership.

The smart infrastructure initiative represented KEC's attempt to future-proof its portfolio. As cities became smarter and grids became digital, traditional infrastructure needed to incorporate technology. KEC began integrating smart meters into distribution projects, sensors into transmission towers, and automation into substations. This wasn't a separate business but an enhancement of existing ones—a recognition that infrastructure and technology were converging.

Geographic expansion continued but with a different character. Rather than chasing projects globally, KEC focused on building deep presence in select high-growth markets. In Africa, the company established subsidiaries and local partnerships, recognizing that the continent's infrastructure deficit represented a multi-decade opportunity. In the Americas, the SAE platform was leveraged for expansion into renewable transmission infrastructure. The Middle East operation evolved from project execution to long-term maintenance contracts, providing recurring revenues.

The order book composition by 2020 told the diversification story clearly. Transmission and distribution, while still the largest segment, contributed about 60% of orders. Railways had grown to 25%, civil infrastructure to 10%, and others including solar to 5%. More importantly, the margin profile had improved—newer businesses, with less competition and more differentiation, commanded better prices than commodity transmission towers.

The working capital challenge of diversification required innovative solutions. Different businesses had different cash cycles—railways projects had better payment terms but longer execution periods, solar had upfront payments but thin margins, civil had milestone-based payments but higher retention amounts. KEC developed sophisticated cash flow management systems, using advances from one business to fund execution in another, creating internal capital efficiency that improved overall returns.

Technology adoption accelerated across all verticals. Drones surveyed transmission routes and railway alignments. Building Information Modeling (BIM) optimized civil projects. Predictive analytics improved project planning. The company that had once relied on manual drawings and physical site inspections now operated with digital twins and satellite imagery. This wasn't just efficiency improvement—it was competitive differentiation, especially in markets where KEC competed against local players with lower costs but less sophistication.

The COVID-19 pandemic tested the resilience of KEC's diversified model. When industrial power demand collapsed, affecting transmission projects, railways and civil projects continued as governments used infrastructure spending for economic stimulus. When international projects faced travel restrictions, domestic operations compensated. The portfolio approach that had seemed risky to some analysts proved its value in crisis—diversification provided resilience. By 2024, KEC's transformation into a diversified infrastructure player was complete. The company delivered robust performance with revenue growing by 14% in Q2 and 10% in H1 FY25, with PAT growing by 53% in Q2 and 76% in H1. More importantly, the YTD order intake reached Rs. 13,482 crore, showing stellar growth of 50% YoY, with the YTD Order Book at Rs. 34,088 crore and L1 position of approximately Rs. 8,500 crore. The combined order book and L1 position exceeded Rs. 42,500 crore—a record high that provided multi-year revenue visibility.

The strategic logic of diversification had been validated. KEC was no longer dependent on any single sector, geography, or customer segment. It had evolved from a transmission tower manufacturer to an integrated infrastructure solutions provider, capable of conceptualizing, designing, manufacturing, and executing complex projects across multiple verticals. The company that had nearly died from over-specialization in the 1970s had learned to thrive through calculated diversification in the 2020s.

VII. Financial Performance & Market Position

The numbers tell a story of resilience rather than explosive growth. KEC International's market capitalization stands at ₹21,361 crore, with revenue of ₹22,358 crore and profit of ₹608 crore. For a company operating in capital-intensive infrastructure sectors across 110 countries, these metrics reveal both the opportunities and constraints of the business model. The return on equity of 8.82% over the last three years might disappoint growth investors, but it reflects the realities of infrastructure: thin margins, high capital requirements, and long execution cycles.

Understanding KEC's financial performance requires appreciating the infrastructure EPC business model's inherent tensions. Unlike product companies that can scale revenues without proportional capital increases, or service companies with asset-light models, infrastructure EPC exists in a challenging middle ground. Every project requires significant working capital—performance guarantees, mobilization advances, retention money. Equipment and materials must be procured months before payment milestones. Execution spans years, during which costs can escalate but contract prices remain fixed.

KEC's net profit margin of 2.61% seems razor-thin until you consider the industry context. Global infrastructure giants like Fluor, Bechtel, and Larsen & Toubro operate with similar margins. In the infrastructure EPC world, the game isn't about margins—it's about scale, execution reliability, and capital efficiency. A 2.6% margin on ₹22,000 crore of revenue still generates ₹600 crore in profits, enough to service debt, fund growth, and reward shareholders.

The debt situation reveals both progress and continuing challenges. Net debt including acceptances stands at Rs. 5,265 crore as of September 30, 2024, a reduction of Rs. 1,074 crore versus September 30, 2023, despite revenue growth of approximately Rs. 2,000 crore (12%) in trailing twelve months. This debt reduction while growing revenues demonstrates improving working capital management—a critical metric in infrastructure businesses where cash conversion cycles can stretch beyond 180 days.

The order book dynamics provide the clearest picture of KEC's competitive position. The company's order book plus L1 position stands at a record high of over Rs. 42,500 crore. This represents nearly two years of revenue visibility—remarkable in an industry where order books can evaporate during economic downturns. The order book composition is equally important: roughly 60% domestic and 40% international, providing geographic diversification; spread across transmission, railways, civil, and other verticals, reducing sector concentration; and a mix of government and private clients, balancing payment security with margin potential.

Competition analysis reveals KEC's unique positioning. In transmission, the company competes with global giants like ABB and Siemens on technology, Chinese companies on price, and domestic players like Kalpataru Power on local execution. KEC's strategy has been to avoid direct competition on any single parameter—it's not the cheapest, the most technologically advanced, or the largest. Instead, it positions itself as the reliable middle ground: good technology at reasonable prices with proven execution.

The railways vertical faces different competitive dynamics. Here, KEC competes with infrastructure majors like L&T and specialized railway contractors like IRCON. The competitive advantage comes from KEC's ability to handle complex, integrated projects—electrification plus signaling plus station construction—that pure-play competitors struggle with. The civil business operates in an even more fragmented market, where KEC's financial strength and execution track record provide differentiation.

KEC International reported a net profit of Rs. 87.6 crore in Q1FY25, from Rs. 42 crore a year ago (Q1FY24), while revenue soared 6.3% annually to Rs. 4,512 crore. This doubling of profits on modest revenue growth indicates improving operational efficiency and better project selection—critical factors in a business where a single bad project can wipe out a quarter's profits.

The working capital story deserves particular attention. Infrastructure EPC is fundamentally a working capital business—companies must fund project execution for months before receiving payment. KEC's working capital days have fluctuated between 120 and 150 days over the past five years, better than the industry average of 180+ days but still representing billions in locked capital. The company has addressed this through innovative financing structures: supplier credit programs, bill discounting arrangements, and milestone-based payment negotiations.

Return on capital employed (ROCE) metrics reveal the challenge of the infrastructure business. With ROCE hovering around 12%, KEC generates returns above its cost of capital but below what investors might expect from industrial companies. This reflects the fundamental trade-off in infrastructure: stable, predictable returns rather than explosive growth; essential services that economies need regardless of cycles; and competitive moats based on execution capability rather than technology or brands.

International operations add another layer of complexity to financial performance. Currency fluctuations can significantly impact reported results—a 5% movement in the dollar can swing profits by tens of crores. KEC has developed sophisticated hedging strategies, but perfect hedging is impossible when projects span multiple years and involve multiple currencies. The company typically hedges 60-70% of its foreign currency exposure, accepting some volatility in exchange for avoiding the cost of full hedging.

The segmental performance reveals interesting patterns. Transmission and distribution, despite being the largest segment, often has the lowest margins due to intense competition. Railways, with its complexity and execution challenges, commands better margins. Civil infrastructure projects, particularly in urban areas, can be highly profitable but also carry higher risks. The solar business, while growing rapidly, operates on thin margins due to Chinese competition in equipment supply.

Looking at peer comparison, KEC trades at interesting valuations. At roughly 1x book value and 35x earnings, it's neither cheap nor expensive relative to infrastructure peers. L&T trades at premium valuations given its size and diversification. Kalpataru Power, a more direct competitor, trades at similar multiples. Chinese competitors trade at lower valuations but carry different risk profiles. Global giants trade at higher multiples but operate in more stable markets.

The capital allocation framework has evolved significantly. Historically, KEC reinvested most profits into growth, funding working capital and capacity expansion. Today, the company balances growth investment with debt reduction and dividends. The dividend payout of 20-30% of profits signals confidence in cash generation while retaining capital for growth. Maintenance capex runs at 1-2% of revenues, while growth capex varies with expansion plans.

Financial risk management has become increasingly sophisticated. Beyond currency hedging, KEC manages commodity price risks (steel and aluminum constitute 40% of project costs), interest rate risks (with a mix of fixed and floating debt), and credit risks (through letters of credit and payment guarantees). The company that nearly collapsed from financial risks in 1982 now runs one of the more sophisticated risk management operations in Indian infrastructure.

The financial performance trajectory suggests a company in transition. The focus has shifted from pure revenue growth to profitable growth. Margins are expanding slowly but steadily as operational efficiency improves. Debt levels are declining despite business growth. The order book provides multi-year visibility. These aren't the metrics of a high-growth technology company, but they represent solid, sustainable performance in a challenging industry—exactly what long-term infrastructure investors seek.

VIII. The RPG Synergy & Management Philosophy

Inside RPG House in Mumbai's Worli district, the annual leadership meeting brings together CEOs from across the group's diverse businesses. The head of CEAT Tyres discusses rubber prices with the chief of RPG Life Sciences. The IT services leader shares digital transformation insights with the infrastructure team. This cross-pollination of ideas, seemingly routine, represents one of KEC's most underappreciated competitive advantages—being part of a $5.2 billion conglomerate that operates across infrastructure, tyres, pharmaceuticals, information technology, and innovation ventures.

The RPG Group, one of India's fastest-growing business conglomerates with a turnover of US$5.2 billion, has diverse business interests spanning infrastructure, tyres, pharmaceuticals, information technology, speciality businesses, and emerging innovation-driven technology ventures. For KEC, being the infrastructure flagship of this group provides advantages that go beyond financial strength.

The leadership philosophy under Harsh Goenka, who took over as Chairman of RPG Enterprises after his father R.P. Goenka, represents a fascinating blend of entrepreneurial aggression and professional management. Unlike the patriarchal style of traditional Indian business houses, Goenka operates more like a private equity owner—setting strategic direction, demanding performance, but giving operational autonomy to professional managers. This approach has been particularly beneficial for KEC, where technical expertise and execution capabilities matter more than corporate politics.

Vimal Kejriwal, MD & CEO of KEC International since 2001, embodies this professional management culture. An engineer by training who rose through the ranks, Kejriwal understands both the technical complexities of infrastructure projects and the financial disciplines required for sustainable growth. His quarterly earnings calls reveal a leader comfortable discussing everything from transformer technology to working capital cycles, from railway signaling systems to currency hedging strategies. This technical-financial bilingualism is rare in infrastructure companies, where leaders typically skew toward one or the other.

The cultural transformation at KEC under RPG management has been deliberate and systematic. The company states: "At KEC, we constantly strive to promote a culture that aims at nurturing an environment of mutual care & respect, with a focus on personal & professional progress for every employee. We believe in building our leadership pipeline by nurturing, empowering and enabling our internal talent." This isn't just corporate speak—it represents a fundamental shift from the family business culture of the Kamani era to a meritocratic professional environment.

The "RPG Talent First!" philosophy ensures that internal talent gets first preference for opportunities within RPG Group companies. For KEC employees, this means career paths that can span across industries—an engineer might move to CEAT's manufacturing operations, a finance professional could transfer to RPG Life Sciences, a digital specialist might work across group companies on transformation initiatives. This mobility creates a breadth of experience that's particularly valuable in infrastructure, where projects increasingly require multi-disciplinary expertise.

Group synergies manifest in unexpected ways. When KEC bids for smart city projects, it can leverage the IT expertise of RPG's technology businesses. When executing projects in remote locations, the logistics expertise from CEAT's distribution network proves valuable. The pharmaceutical business's experience with regulatory compliance helps navigate complex environmental clearances. These aren't transformative advantages individually, but collectively they create a capability set that pure-play infrastructure companies lack.

The financial synergies are more obvious but equally important. The group's combined balance sheet strength helps KEC secure performance guarantees for large projects. Treasury operations are centralized, providing better rates for foreign exchange hedging and working capital financing. The group's relationships with financial institutions, built over decades across multiple businesses, translate into better terms for project financing. During the COVID-19 crisis, when standalone infrastructure companies struggled with liquidity, KEC could tap into group resources to maintain operations.

Risk management benefits from group-level perspectives. The RPG board includes independent directors with experience across industries and geographies. Their insights help KEC navigate risks that might blindside a company with a narrower perspective. When entering new markets or sectors, the group's collective experience helps identify potential pitfalls. The disasters avoided through this collective wisdom don't show up in financial statements but are invaluable nonetheless.

The innovation agenda at KEC is influenced by RPG's broader push toward new-age businesses. The group has invested in electric vehicles, artificial intelligence, and sustainable technologies—areas that seem distant from transmission towers but increasingly intersect with infrastructure. KEC's smart infrastructure initiatives, its push into renewable energy infrastructure, and its experiments with construction technology all benefit from the group's innovation ecosystem.

Governance structures reflect RPG's evolution toward institutional practices. Independent directors constitute a majority of KEC's board. Audit, risk, and compensation committees operate with genuine independence. Related party transactions are scrutinized and conducted at arm's length. For a company that's 50.1% owned by a promoter group, the governance standards exceed what's typically seen in Indian family-owned businesses.

The performance management system combines RPG-wide frameworks with KEC-specific metrics. Every employee has clear KPIs linked to company performance. Variable compensation can be significant for high performers. Long-term incentives align management with shareholder interests. The company that once operated on personal relationships now runs on systematic performance management—though relationships still matter in winning and executing projects.

Sustainability initiatives reflect both RPG's corporate philosophy and infrastructure sector requirements. KEC's ESG (Environmental, Social, and Governance) efforts go beyond compliance—they're increasingly becoming competitive advantages in international bids where sustainability credentials matter. The group's commitment to carbon neutrality by 2050 pushes KEC to innovate in construction techniques, material usage, and project execution.

The talent development approach is particularly noteworthy. KEC runs extensive training programs, from technical skills for engineers to leadership development for managers. The company's training center in Nagpur doesn't just teach tower design—it covers project management, financial analysis, cultural sensitivity for international projects, and safety protocols. The investment in human capital, often overlooked in financial analysis, creates the execution capability that ultimately drives performance.

Communication culture has evolved dramatically from the hierarchical structure of traditional Indian companies. Town halls, skip-level meetings, and open-door policies create information flow that speeds decision-making. Project teams in remote locations can escalate issues directly to senior management. This transparency and speed are crucial in infrastructure, where delays compound quickly and small problems can become project-threatening if not addressed promptly.

The RPG connection also provides intangible benefits that are hard to quantify but very real. The group's reputation opens doors with government officials and international clients. The Goenka name carries weight in Indian business circles. The perception of stability from being part of an established conglomerate helps in winning projects where clients care about contractor longevity. These soft factors matter enormously in infrastructure, where relationships and reputation drive business as much as technical capabilities.

Looking at management philosophy, KEC under RPG represents a fascinating case study in balancing multiple tensions: entrepreneurial agility with corporate governance, technical excellence with financial discipline, global ambitions with local execution, growth with sustainability, and autonomy with group synergy. The company has managed these balances not through elaborate frameworks but through cultural evolution—creating an organization that thinks globally while acting locally, that pursues growth while managing risk, that leverages group strengths while maintaining its distinct identity.

IX. Playbook: Infrastructure EPC Lessons

The conference room in KEC's Mumbai headquarters has witnessed every crisis and triumph in the company's modern history. If these walls could talk, they'd reveal a masterclass in infrastructure EPC management—lessons written not in MBA textbooks but in the scar tissue of near-bankruptcy, the exhaustion of completing impossible projects, and the satisfaction of building infrastructure that powers nations. This playbook, extracted from eight decades of KEC's journey, offers insights that transcend the company itself.

Lesson 1: Surviving Near-Death Makes You Stronger (If It Doesn't Kill You)

KEC's 1982 crisis wasn't just a financial near-death experience—it was an organizational crucible that forged capabilities that still drive the company today. The discipline of completing loss-making projects to preserve reputation created an execution culture that prioritizes delivery over everything. The trauma of currency-induced losses led to sophisticated hedging strategies that now protect against volatility. The experience of being abandoned by stakeholders built a conservatism about leverage that persists despite market pressures for aggressive growth.

The survival playbook has specific tactics: maintain liquidity buffers even when they seem unnecessary (cash is oxygen when crisis hits); diversify funding sources before you need them (banking relationships are built in good times, tested in bad); keep technical capabilities intact even during financial stress (infrastructure companies are only as good as their engineering talent); and preserve reputation at any cost (in infrastructure, reputation takes decades to build, moments to destroy).

Lesson 2: Building Global Manufacturing and Execution Capabilities

KEC's evolution from an Indian manufacturer to a global infrastructure player required capabilities that went far beyond setting up factories in different countries. The real challenge was creating execution systems that could deliver consistent quality whether the project was in the Amazon rainforest or the Arabian desert, whether the team was Indian, Brazilian, or Mexican.

The global capability playbook includes several key elements. First, standardize what can be standardized, localize what must be localized. Tower designs are globally standardized, but construction techniques adapt to local conditions. Second, create centers of excellence that serve globally—engineering in India, manufacturing optimization in Mexico, project management in Dubai. Third, rotate talent religiously. Engineers who've worked across geographies bring perspectives that no training can provide. Fourth, invest in technology that enables global coordination—project management systems that work across time zones, design platforms that enable collaboration, communication tools that bridge language barriers.

Lesson 3: Managing Complex Multi-Year Projects

Infrastructure projects are unique beasts—they span years, involve hundreds of stakeholders, face countless uncertainties, and yet must be delivered on fixed timelines and budgets. KEC's ability to consistently deliver such projects comes from systematic approaches developed over decades.

The project management playbook starts with ruthless front-end planning. Spend months on design and planning to save years in execution. Map every risk, plan every contingency, identify every stakeholder. Create detailed work breakdown structures that decompose massive projects into manageable chunks. Build schedule buffers into critical paths—delays are inevitable, the question is whether you've planned for them.

Stakeholder management is equally critical. Infrastructure projects touch everyone—government officials, local communities, environmental groups, labor unions. KEC learned to invest heavily in stakeholder engagement before breaking ground. Community liaison officers who speak local languages, grievance redress mechanisms that actually work, benefit-sharing programs that give communities stakes in project success—these soft elements often determine project outcomes more than technical execution.

Lesson 4: Balancing Diversification with Core Competence

KEC's diversification from transmission into railways, civil, and solar worked because it followed a disciplined approach: leverage existing capabilities into adjacent markets, don't venture into completely unrelated areas, and build new capabilities incrementally rather than through dramatic leaps.

The diversification playbook has clear principles. Adjacent diversification works; random diversification doesn't. Railways leveraged electrical expertise, civil leveraged project management capabilities, solar leveraged structural engineering skills. Each new vertical built on existing strengths while adding new ones. Build or buy capabilities depending on urgency and availability—KEC acquired SAE for immediate American market access but built railway capabilities organically. Maintain focus even while diversifying—KEC still derives majority revenues from transmission, its core competence. New ventures supplement but don't replace the core.

Lesson 5: Working Capital Management in Infrastructure

Infrastructure EPC is fundamentally a working capital business. Companies must fund material procurement, labor costs, and equipment deployment months before receiving payment. KEC's evolution from working capital crisis to sophisticated management offers crucial lessons.

The working capital playbook requires multiple interventions. Negotiate advance payments religiously—even 10% advance dramatically improves cash flows. Structure contracts with regular milestone payments rather than back-ended completion payments. Use supply chain financing creatively—let suppliers with lower capital costs fund inventory. Implement zero-tolerance policies for collection delays—in infrastructure, payment delays compound quickly into crisis. Create natural hedges between businesses—use advances from one project to fund another's working capital needs.

Lesson 6: Government Relations and Policy Navigation

Infrastructure is inherently political. Governments are usually the largest customers, regulators set the rules, and policy changes can make or break business models. KEC's ability to navigate this landscape—from Indian bureaucracy to Middle Eastern monarchies to American regulatory frameworks—provides valuable lessons.

The government relations playbook emphasizes several principles. Invest in understanding regulatory frameworks before entering markets—compliance is cheaper than penalties. Build relationships at multiple levels—political leadership changes, but bureaucracies endure. Maintain strict ethical standards—corruption might win projects but destroys companies. Participate actively in policy formation—industry associations, standard-setting bodies, regulatory consultations. Create local value beyond project execution—employment, supplier development, skill training build political capital.

Lesson 7: Technology Adoption in Traditional Infrastructure

Infrastructure seems like the antithesis of technology—it's about steel and concrete, not software and algorithms. But KEC's selective adoption of technology shows how traditional industries can benefit from digital transformation without losing their core identity.

The technology adoption playbook is pragmatic rather than revolutionary. Adopt technology where it clearly adds value—drones for site surveys, BIM for design optimization, IoT for equipment monitoring. Don't digitize for the sake of digitization. Build versus buy decisions should favor buying—infrastructure companies should focus on infrastructure, not software development. Create digital layers on physical assets—smart towers that monitor their own health, predictive maintenance systems that prevent failures. Train traditional workers in new technologies gradually—revolution causes resistance, evolution enables adoption.

The risk management playbook, refined through multiple crises, is comprehensive. Identify risks systematically—technical, financial, political, environmental, social. Quantify risks wherever possible—probabilistic models beat intuition. Create multiple mitigation layers—hedging, insurance, contractual protections, operational buffers. Monitor continuously—risk profiles change throughout project lifecycles. Learn from every failure—post-project reviews that capture lessons, risk databases that inform future decisions.

These lessons, extracted from KEC's journey, apply beyond the company and even beyond infrastructure. They speak to fundamental challenges of building and sustaining industrial enterprises: How do you balance growth with stability? How do you expand globally while maintaining local relevance? How do you adopt new technologies without abandoning core competencies? How do you serve public infrastructure needs while generating private returns? KEC's playbook doesn't provide perfect answers, but it offers tested approaches—wisdom earned through decades of building the infrastructure that powers modern life.

X. Analysis & Investment Perspective

The investment case for KEC International presents a fascinating study in contrasts. Here's a company executing critical infrastructure projects across 110 countries, holding a record order book exceeding ₹42,500 crore, yet trading at modest valuations with an ROE that would make growth investors yawn. Understanding KEC requires looking beyond simple metrics to grasp the deeper dynamics of infrastructure investing—where stability matters more than growth, execution capability trumps innovation, and long-term value creation happens slowly but steadily.

The Bull Case: Riding the Infrastructure Supercycle

The optimistic view starts with a simple observation: the world needs massive infrastructure investment. The Global Infrastructure Hub estimates a $15 trillion infrastructure investment gap by 2040. India alone plans to spend $1.4 trillion on infrastructure by 2025. Every developed economy is upgrading aging infrastructure while every emerging market is building new capacity. This isn't a cyclical opportunity—it's a multi-decade structural trend.

KEC sits perfectly positioned to capture this opportunity. The company's diversified portfolio addresses multiple infrastructure needs—power transmission for renewable energy integration, railway electrification for sustainable transport, urban infrastructure for growing cities. As Vimal Kejriwal noted, "our Y-T-D order intake stands at about Rs 13,500 crore, reflecting a robust growth of over about 50 per cent compared to last year". This isn't just order book growth—it's validation of KEC's competitive positioning.

The execution track record provides the foundation for the bull case. Over 75 years, KEC has completed projects in terrains ranging from Amazon rainforests to Arabian deserts. This isn't easily replicable—Chinese competitors might offer lower prices, European firms might have better technology, but few match KEC's combination of cost competitiveness and execution reliability. In infrastructure, track record is everything. Clients choose contractors who've successfully completed similar projects, creating a virtuous cycle where past success drives future opportunities.

Geographic diversification offers another positive. With operations across India, Middle East, Africa, and the Americas, KEC isn't dependent on any single market. When oil prices collapsed in 2014-2016, affecting Middle Eastern projects, Indian operations compensated. When COVID-19 hit India hard in 2021, international operations continued. This portfolio effect smooths revenues and reduces vulnerability to regional downturns.

The renewable energy transition presents a particularly compelling opportunity. Every gigawatt of renewable capacity requires transmission infrastructure to evacuate power. Solar and wind farms are often located far from consumption centers, necessitating extensive transmission networks. KEC's capabilities in both transmission and solar infrastructure position it perfectly for this transition. The company isn't betting on which renewable technology wins—it builds the infrastructure all of them need.

Government focus on infrastructure spending provides a powerful tailwind. Post-COVID, governments worldwide have embraced infrastructure investment as economic stimulus. India's Gati Shakti program, America's Infrastructure Investment Act, Middle East's Vision 2030 programs—all represent multi-year spending commitments that benefit companies like KEC. Unlike consumer demand which can evaporate quickly, government infrastructure spending tends to be steady and countercyclical.

The Bear Case: Structural Challenges and Persistent Concerns

The skeptical view starts with the numbers that concern investors. An 8.82% ROE over three years is barely above the cost of capital. Net margins of 2.61% leave no room for error—a single project gone wrong can wipe out quarterly profits. The debt-to-equity ratio of 74% seems high for a cyclical business. These aren't metrics that excite investors seeking growth or value.

The infrastructure EPC business model has inherent limitations. It's fundamentally a services business that requires significant capital, combining the worst aspects of both models. Unlike product companies that can achieve operating leverage, every project requires proportional resources. Unlike asset-light services, significant working capital is locked up in project execution. The result is a business that struggles to generate returns significantly above capital costs.

Competition is intensifying from multiple directions. Chinese companies, backed by state support and cheap financing, are aggressively bidding for international projects. Local competitors in each market are upgrading capabilities. Technology companies are entering infrastructure with digital solutions. The competitive landscape that allowed KEC to thrive in the 1990s and 2000s no longer exists—margins are compressed, and differentiation is harder.

The cyclical nature of infrastructure spending poses risks. While the current environment is supportive, infrastructure spending is inherently cyclical. Economic downturns lead to project postponements. Government fiscal pressures result in spending cuts. The order book that looks robust today can evaporate quickly when conditions change. KEC survived the 1970s oil crisis and 2008 financial crisis, but each survival came at significant cost.

Working capital intensity remains a persistent challenge. Despite improvements, KEC still has significant capital locked in project execution. In an environment of rising interest rates, the cost of this working capital increases, pressuring margins further. The company has limited ability to pass on these costs to customers, who typically fix prices at contract signing.

Execution risks are ever-present in infrastructure. Projects in difficult terrains face weather delays, labor shortages, and logistical challenges. Regulatory changes can affect project economics mid-execution. Environmental and social issues can cause shutdowns. While KEC has strong risk management, the nature of infrastructure means surprises are inevitable.

Valuation Perspectives and Peer Comparison

At current valuations, KEC trades at approximately 35x trailing earnings and 1x book value. Compared to Larsen & Toubro, India's infrastructure giant trading at premium valuations, KEC seems reasonable. Against Kalpataru Power, a direct transmission competitor, valuations are similar. International comparisons are harder—Fluor trades at lower multiples but operates in different markets, while European infrastructure firms command premiums for perceived stability.

The valuation reflects the market's mixed view—not cheap enough to be a value play, not expensive enough to suggest excessive optimism. This middle ground perhaps accurately captures KEC's position: a solid infrastructure company with decent growth prospects but structural limitations on returns.

ESG Considerations and Sustainability

Environmental, Social, and Governance factors increasingly influence infrastructure investment decisions. KEC's role in building renewable energy infrastructure positions it well from an environmental perspective. The company's transmission lines enable clean energy integration, railway projects support sustainable transport, and smart infrastructure initiatives improve resource efficiency.

Social factors are more complex. Infrastructure projects often face community opposition, land acquisition challenges, and displacement concerns. KEC's track record is generally positive, but every project carries social risks. The company's investment in local employment and community development helps, but tensions are inherent in infrastructure development.

Governance has improved significantly under RPG management. Independent directors, transparent reporting, and systematic risk management represent major advances from the family business era. However, 50.1% promoter ownership means minority shareholders have limited influence on major decisions.

Future Growth Drivers

Several factors could drive future growth. Energy transition acceleration could boost demand for transmission infrastructure. Government infrastructure spending might exceed current projections. New technologies like hydrogen might require entirely new infrastructure. Urban infrastructure needs in emerging markets are just beginning to be addressed.

The international expansion potential remains significant. Africa's infrastructure deficit represents decades of opportunity. Southeast Asian countries are beginning major infrastructure upgrades. Even developed markets need infrastructure renewal. KEC's proven ability to execute projects globally positions it to capture these opportunities.

Investment Conclusion: Steady Infrastructure Play

KEC International represents a classic infrastructure investment—steady rather than spectacular, resilient rather than rapidly growing. For investors seeking exposure to the global infrastructure buildout, KEC offers proven execution capability, diversified operations, and reasonable valuations. The company won't deliver venture capital-like returns, but it should provide steady value creation aligned with global infrastructure spending.

The investment case ultimately depends on one's view of infrastructure spending sustainability. Bulls who believe in a multi-decade infrastructure supercycle will find KEC attractively positioned. Bears who worry about execution risks and low returns will remain skeptical. For long-term investors comfortable with the infrastructure sector's characteristics—long cycles, steady returns, execution risks—KEC offers a vehicle to participate in building the physical backbone of economic growth.

The company that nearly died in 1982 has evolved into a resilient infrastructure player. It's not the most exciting investment story, but infrastructure rarely is. What KEC offers is something perhaps more valuable: the capability to execute complex projects that keep lights on, trains running, and economies functioning. In a world increasingly focused on digital transformation, there's investment merit in companies that build the physical infrastructure that makes everything else possible.

XI. Looking Forward & Strategic Questions

The strategy presentation to KEC's board in early 2024 contained a slide that would define the company's next decade: "From Infrastructure Builder to Infrastructure Solutions Provider." This wasn't just semantic evolution—it represented a fundamental question about KEC's future identity. Should the company that built its reputation on executing complex physical infrastructure projects evolve into something more? And if so, what would that transformation look like without losing the engineering DNA that defines its competitive advantage?

The Energy Transition Opportunity

The global energy transition represents both KEC's greatest opportunity and most complex challenge. The International Energy Agency estimates $4 trillion annual investment in clean energy infrastructure by 2030. But this isn't simply about building more transmission lines. The grid of the future requires intelligence—dynamic load balancing, bi-directional power flows, integration of distributed generation, real-time optimization. KEC must decide whether to remain a pure infrastructure builder or develop capabilities in grid intelligence and energy management.

The hydrogen economy presents another strategic question. As countries pivot toward hydrogen as an energy carrier, entirely new infrastructure will be needed—production facilities, transportation networks, storage systems. Should KEC proactively develop hydrogen infrastructure capabilities, or wait for the market to mature? Early entry offers first-mover advantages but requires investment in unproven technologies. Waiting reduces risk but might mean missing the opportunity window.

Battery storage infrastructure is another emerging opportunity. Grid-scale storage is essential for renewable integration, but it requires different capabilities than traditional transmission. Should KEC partner with battery manufacturers, develop independent storage infrastructure expertise, or avoid this technically complex area? The decision will significantly impact the company's position in the renewable energy value chain.

Infrastructure Spending Cycles Globally

Understanding and predicting infrastructure spending cycles has become more complex. Traditional patterns—government spending increasing during downturns, private investment following economic growth—are being disrupted. Climate change is driving emergency infrastructure spending regardless of economic cycles. Geopolitical tensions are spurring infrastructure nationalism. Technology obsolescence is accelerating infrastructure replacement cycles.