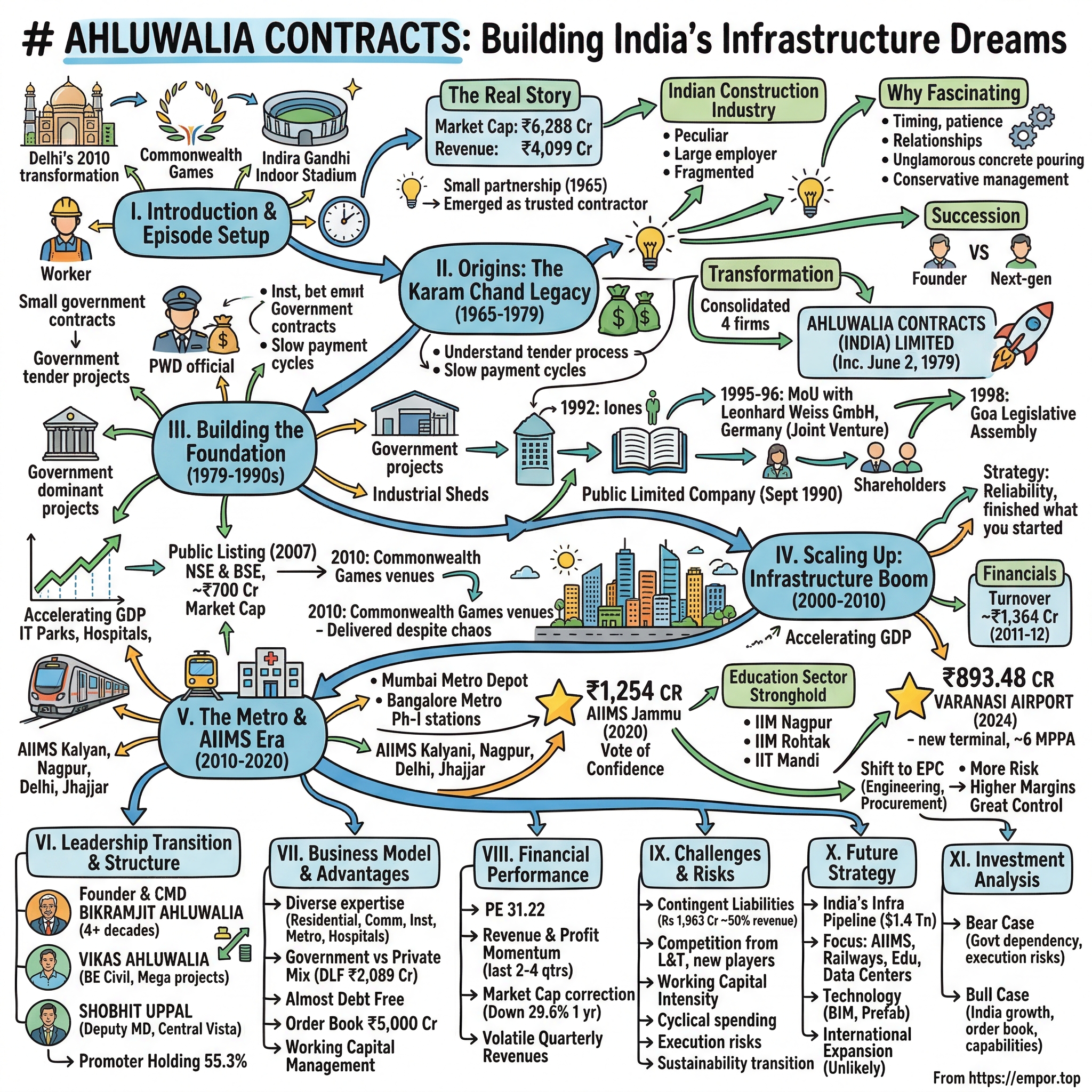

Ahluwalia Contracts: Building India's Infrastructure Dreams

I. Introduction & Episode Setup

Picture this: It's 2010, and Delhi is transforming at breakneck speed. The Commonwealth Games are months away, and across the capital, construction sites buzz with urgency. At the Indira Gandhi Indoor Stadium, workers are racing against time to complete what will become one of the Games' centerpiece venues. The contractor behind this massive project? A company most Indians have never heard of, yet one that has quietly shaped the nation's skyline for nearly half a century—Ahluwalia Contracts.

Today, Ahluwalia Contracts commands a market capitalization of ₹6,288 crore with annual revenues touching ₹4,099 crore. But the real story isn't in these numbers—it's in how a small partnership firm founded in 1965 navigated the treacherous waters of India's License Raj, survived economic liberalization, and emerged as one of the country's most trusted infrastructure contractors. This is a story of patience, relationships, and the unglamorous art of pouring concrete at scale.

The construction industry in India is peculiar. It's simultaneously one of the largest employers and one of the most fragmented sectors. While tech unicorns grab headlines, companies like Ahluwalia have been literally building the foundation of modern India—from AIIMS hospitals to Metro stations, from IITs to international airports. They operate in a world where a single project can take years, where government relationships matter more than marketing budgets, and where your reputation is built one perfectly executed project at a time.

What makes Ahluwalia's journey particularly fascinating is its timing. The company formalized its operations just as India was beginning to dream bigger about infrastructure. It went public just before the great infrastructure boom. And it's now positioning itself for India's next phase of growth—smart cities, modern airports, and world-class hospitals. But unlike the flashy infrastructure plays that dominate business news, Ahluwalia has chosen a different path: conservative financial management, deep government relationships, and an almost obsessive focus on execution.

This is also a story about succession in Indian family businesses. How does a founder who's been at the helm for over four decades prepare the next generation? How do you maintain entrepreneurial spirit while building institutional capabilities? And perhaps most importantly, how do you stay relevant in an industry where yesterday's relationships might not win tomorrow's contracts?

II. Origins: The Karam Chand Legacy (1965-1979)

The year is 1965. India is barely two decades into independence, still reeling from wars with China and Pakistan. In this environment of scarcity and nation-building, a man named Karam Chand Ahluwalia sees opportunity where others see chaos. The country needs everything—roads, buildings, bridges, hospitals. The government is the only entity with money to spend, and it needs contractors who can deliver. Not flashy architects or grand visionaries, but reliable executors who understand the unglamorous reality of moving earth and pouring concrete.

Karam Chand doesn't start with grand ambitions of building monuments. He begins with small government contracts—perhaps a government office here, a small residential complex there. In those days, construction in India was less about engineering prowess and more about navigating the labyrinthine government procurement process. You needed to understand tender documents, maintain relationships with PWD officials, and most crucially, have the working capital to survive the government's notoriously slow payment cycles. What actually happened in those early years from 1965 to 1979 remains somewhat shrouded in the mists of pre-digital India. The company traces its roots to Late Sh. Karam Chand Ahluwalia, father of Mr. Bikramjit Ahluwalia, who founded the business in 1965. But this wasn't a single entity—it was a collection of partnership firms, the standard structure for Indian businesses in that era. Partnership firms had advantages: minimal regulatory oversight, flexibility in operations, and the ability to bid for multiple government contracts simultaneously through different entities.

The transformation from informal partnerships to a formal corporate structure tells us something important about the evolution of Indian business. On June 2, 1979, Ahluwalia Contracts (India) Limited was incorporated, acquiring the business of four partnership firms engaged in construction in July 1979. This wasn't just paperwork—it was a fundamental shift in ambition. Incorporation meant audit requirements, regulatory compliance, and transparency. But it also meant the ability to raise capital, bid for larger projects, and build an institution that could outlive its founders.

Bikramjit Ahluwalia, who would have been in his early thirties at the time of incorporation, represented the bridge between old and new India. His father had built relationships and understood the construction business; Bikramjit understood that those relationships needed to be institutionalized. The timing was crucial—1979 was just before India's slow march toward economic liberalization would begin, but late enough that the most restrictive aspects of the License Raj were starting to crack.

The decision to consolidate four partnership firms into one entity suggests that by 1979, the Ahluwalia operations had reached a scale where informal structures were becoming a constraint. Government contracts were getting larger, competition was intensifying, and clients wanted to work with organized entities, not loose partnerships. The construction industry was professionalizing, and Ahluwalia was positioning itself for what would come next.

III. Building the Foundation (1979-1990s)

The company became a Public Limited Company in September 1990, a move that coincided with India's economic awakening. The timing was either prescient or fortuitous—just months before P.V. Narasimha Rao and Manmohan Singh would unleash economic reforms that would transform India. But before we get to that inflection point, let's understand what Ahluwalia was building in the 1980s.

The 1980s in Indian construction were characterized by government dominance. Private sector construction was limited to small residential projects and industrial sheds. The real money—and the real challenges—were in government contracts. These projects had their own peculiar dynamics: lengthy tender processes, elaborate technical specifications written by government engineers who'd never built anything themselves, and payment cycles that could stretch for months or even years.

Ahluwalia's strategy during this period appears to have been methodical rather than meteoric. They weren't trying to be the biggest; they were trying to be the most reliable. In an industry plagued by abandoned projects and contractor defaults, simply finishing what you started was a competitive advantage.

The transition to public limited company status in 1990 was more than administrative—it was a declaration of intent. Going public meant opening your books, having independent directors, and being accountable to shareholders beyond the family. For a company that had operated as a closely-held family business for 25 years, this was a cultural revolution. The 1992 milestone deserves attention: completing the Chancery building for the High Commission of India, Delhi. This wasn't just another government building—it was a diplomatic facility, requiring higher security clearances, more stringent quality standards, and the ability to work with multiple stakeholders including the Ministry of External Affairs. For a company still finding its feet as a public entity, this was validation at the highest level.

The international ambitions materialized in 1995-96 when the company signed a MoU with Leonhard Weiss GmbH & Co, Germany for a joint venture. This was classic 1990s India—everyone wanted foreign collaboration, whether they needed it or not. German engineering had cachet, and for government tenders, having an international partner could be the difference between winning and losing. Whether this partnership yielded significant technological transfer or was merely a marketing exercise remains unclear, but it signaled that Ahluwalia was thinking beyond traditional boundaries.

In 1998, the company completed the construction of Goa legislative assembly project, establishing its credentials in institutional buildings. Legislative assemblies are peculiar projects—they combine the complexity of modern construction with the sensitivities of political symbolism. Every detail matters because it will be scrutinized by politicians who, while they may not understand construction, certainly understand finding fault.

The 1990s also saw the beginning of India's IT boom, though Ahluwalia wouldn't fully capitalize on this until later. The company was still primarily focused on government and institutional projects, a segment that was steady if not spectacular. While software companies were promising to change the world, Ahluwalia was content to build the physical infrastructure that world would need.

IV. Scaling Up: The Infrastructure Boom Years (2000-2010)

The turning point came in the late 1990s and early 2000s when it expanded its operations to include large government contracts, contributing significantly to urban infrastructure projects. This wasn't coincidence—India was changing. The GDP growth was accelerating, foreign investment was flowing in, and there was finally political consensus that infrastructure was holding the country back. Roads, airports, metros, hospitals—everything needed to be built, and built fast.

The company's public listing arrived in 2007, a moment of perfect timing or spectacular luck. The company had established itself as a publicly traded entity on the National Stock Exchange (NSE) and the Bombay Stock Exchange (BSE), with a market capitalization of approximately ₹700 crores at its initial listing. This was peak India optimism—the Sensex was roaring, real estate was booming, and everyone believed the India story. Going public gave Ahluwalia the capital to bid for larger projects and the credibility that came with regulatory oversight.

But the real transformation was in the type of projects Ahluwalia was winning. The company mentions completing projects like IFCI Tower New Delhi, NDMC City Centre, and South Asian University. These weren't just buildings; they were statements of India's ambition. South Asian University, for instance, was meant to be a symbol of regional cooperation, funded by SAARC nations. The construction quality couldn't just be good—it had to be exemplary.

The Commonwealth Games of 2010 deserve special attention. For India, this was supposed to be what the Beijing Olympics were for China—a coming-out party on the global stage. The preparation was chaotic, marked by corruption scandals, delays, and last-minute panic. Yet when the games finally happened, the infrastructure held up. Companies like Ahluwalia, working behind the scenes, had delivered. While politicians and organizing committee members made headlines for all the wrong reasons, the contractors who actually built the venues remained largely anonymous.

What's interesting about this period is how Ahluwalia navigated the chaos. The Commonwealth Games projects were notorious for payment delays, scope changes, and political interference. Many contractors who took on these projects ended up in financial distress. Ahluwalia not only survived but emerged stronger, suggesting either exceptional project management or, more likely, the deep relationships and financial cushion needed to weather such storms.

The 2000s also saw Ahluwalia diversifying its portfolio. IT parks started appearing in the mix, a recognition that India's economy was shifting. Hospitals became a major focus, as India belatedly realized its healthcare infrastructure was woefully inadequate. Educational institutions—IITs, IIMs, universities—became regular clients. Each segment had its own requirements, its own decision-makers, its own payment cycles. Managing this complexity required evolution from a construction company to something more sophisticated.

The financial metrics from this period tell a story of steady growth rather than explosive expansion. By 2011-2012, the company's turnover had reached Rs. 1364 Crores, a respectable figure but not earth-shattering. This was deliberate—Ahluwalia was choosing profitability over growth, relationships over transactions.

V. The Metro & AIIMS Era: National Scale Projects (2010-2020)

If the 2000s were about establishing credibility, the 2010s were about executing at national scale. The projects from this era read like a roster of India's infrastructure ambitions: Mumbai Metro Depot, Bangalore Metro Rail Corporation Phase-I stations, AIIMS expansions across multiple cities. These weren't just large projects; they were complex, multi-year endeavors that required sophisticated project management and deep pockets to handle working capital requirements.

The Metro projects deserve particular attention. Urban rail in India is a peculiar beast—technically complex, politically sensitive, and invariably delayed. The Mumbai Metro Depot project for Mumbai Metro One Pvt. Ltd. wasn't just about laying tracks; it was about creating maintenance infrastructure that would keep the city's lifeline running for decades. Similarly, the Bangalore Metro Rail Corporation Phase-I stations required not just construction expertise but the ability to work in dense urban environments while minimizing disruption.

But it's the AIIMS projects that truly defined this era for Ahluwalia. The All India Institute of Medical Sciences represents the pinnacle of Indian healthcare—where presidents and paupers theoretically receive the same treatment. Expanding AIIMS to new cities was a political priority, and the construction requirements were stringent. Hospitals aren't just buildings; they're complex organisms with specialized requirements for everything from operating theater ventilation to radiation shielding.

The AIIMS projects in Kalyani, Nagpur, Delhi, and Jhajjar each presented unique challenges. Then came the big one: the ₹1,254 crore AIIMS Jammu contract in 2020, involving construction of a hospital, medical college, and hostels. This wasn't just Ahluwalia's largest single contract; it was a vote of confidence from the government in the company's ability to deliver nationally important infrastructure.

The education sector became another stronghold. IIM Nagpur, IIM Rohtak, IIT Mandi—these weren't just construction projects but institution-building exercises. An IIM campus isn't just classrooms and hostels; it's about creating an environment that will shape India's future business leaders. The architecture matters, the quality matters, the timeline matters because each delay means another batch of students starts their education in temporary facilities. The recent win of the Varanasi Airport's new terminal for Rs. 893.48 crore in 2024 continues this tradition of landing marquee projects. Airports Authority of India issued LOA and awarded Varanasi Airport new terminal's Rs. 893.48 crore construction contract to Ahluwalia Contracts. The project involves a new terminal building spread across an area of 75,220 sqm, equipped with 8 aerobridges, 72 check-in counters, 14 security check counters and 6 baggage claim belts, with an ultimate design capacity of handling 6 MPPA and capable of handling 5000 peak hour passengers. What's particularly noteworthy is that Ahluwalia's bid of Rs. 893.48 crore was well below AAI's Rs. 995.08 crore estimate, suggesting either exceptional efficiency or a strategic decision to bid aggressively for a high-profile project.

The evolution into complex EPC (Engineering, Procurement, Construction) capabilities marked a fundamental shift in Ahluwalia's business model. EPC contracts transfer more risk to the contractor but also offer higher margins and greater control over project execution. It requires not just construction skills but engineering expertise, procurement networks, and project management sophistication. The fact that Ahluwalia could win and execute EPC contracts for critical infrastructure like airports and hospitals demonstrated how far the company had evolved from its roots as a simple construction contractor.

VI. Leadership Transition & Modern Structure

The leadership structure of Ahluwalia tells a story that's quintessentially Indian—a family business trying to professionalize while maintaining founder control. Bikramjit Ahluwalia, the Founder, Promoter and Managing Director of the company, has been appointed as Managing Director since 1979 and designated as Chairman and Managing Director, aged 84 years, having been involved in construction activity for more than 56 years. Think about that—the same person has been running the company for over four decades, through economic liberalization, multiple boom-bust cycles, and technological revolutions.

The second generation is already deeply involved. Vikas Ahluwalia, aged 49 years, son of Sh. Bikramjit Ahluwalia, is BE (Civil) and has more than 20 years of experience in multifarious activities relating to infrastructure. His involvement since 1996 and role in the award and execution of many mega projects by the Company suggests a gradual transition is underway.

What's interesting is the inclusion of professional management alongside family members. Shobhit Uppal as Deputy Managing Director, aged 56 years, an Electrical Engineering graduate from National Institute of Technology, Kurukshetra, has over three decades of experience and has been involved in various prestigious projects such as Central Vista Projects, New Delhi, AIIMS Kalyani, IIM Nagpur, IIM Rohtak. The Central Vista Projects mention is particularly significant—this is the controversial redevelopment of India's parliamentary complex, one of the most politically sensitive construction projects in the country.

The promoter holding at 55.3% gives the family firm control while still having meaningful public shareholding. This balance is delicate—enough control to drive long-term strategy, enough public float to ensure liquidity and institutional interest. The low dividend payout of just 1.42% of profits over the last 3 years suggests the family is more interested in reinvesting for growth than extracting cash, a positive signal for minority shareholders.

The board structure includes independent directors with relevant expertise, including retired government officials who understand the byzantine world of government contracting. This isn't just about governance compliance; it's about having people who can navigate the corridors of power, who understand how decisions are really made in government departments.

VII. Business Model & Competitive Advantages

Ahluwalia's business model is deceptively simple: win government and institutional contracts, execute them well, and use that track record to win more contracts. But the execution of this model requires capabilities that take decades to build.

The company's expertise spans residential, commercial, institutional, corporate offices, power plants, hospitals, hotels, IT parks, Metro stations and depots, and automated car parking lots for Government as well as private clients. This isn't diversification for its own sake—each segment requires different technical capabilities, different relationship networks, different working capital cycles. A company that can handle this complexity has built something valuable.

The government versus private sector mix is crucial. Government contracts offer scale and prestige but come with payment delays and bureaucratic hassles. Private sector projects, particularly from developers like DLF (as evidenced by the recent Rs. 2089 Cr residential project order from DLF for 44 months), offer better payment terms but require different capabilities and relationships.

The "almost debt free" strategy is particularly interesting in a capital-intensive business like construction. Most construction companies lever up to grow faster, but this creates vulnerability during downturns. Ahluwalia's conservative approach means slower growth but also means they can survive when others can't.

The order book strength of approximately ₹5,000 crore provides visibility for the next 2-3 years. In construction, order book is everything—it's not just future revenue but a validation of the company's capabilities and relationships. The quality of the order book matters as much as its size; projects from AAI, AIIMS, and IITs come with their own credibility.

Working capital management in construction is an art form. You need to fund projects upfront, manage retention money, handle variations and change orders, and somehow maintain cash flow while clients take their own sweet time to pay. Ahluwalia's ability to maintain growth while staying debt-free suggests exceptional working capital management or very selective project choice—probably both.

The quality certifications (ISO 14001:2004, OHSAS 18001:2007, ISO 9001:2008) might seem like bureaucratic box-ticking, but in government contracts, they're table stakes. More importantly, they suggest systematic processes, which is crucial when you're managing multiple complex projects simultaneously.

VIII. Financial Performance & Market Position

The numbers tell a story of steady execution rather than explosive growth. Current revenue of ₹4,099 Cr and profit of ₹202 Cr represent solid but not spectacular margins. The PE ratio of 31.22 suggests the market is pricing in growth, but the stock performance tells a different story.

The momentum metrics are encouraging. Revenue has been up for the last 2 quarters with an average increase of 21.7% per quarter, while net profit has been up for the last 4 quarters with an average increase of 27.8% per quarter. This acceleration suggests either better project mix, improved execution, or operating leverage kicking in—probably all three.

The quarterly volatility is worth noting. On a consolidated basis, Ahluwalia reported a profit of Rs 83.33 crore on total income of Rs 1,233.98 crore for the quarter ended 2025, while for the year ended 2024, it posted a profit of Rs 374.83 crore on total income of Rs 3,855.30 crore. Construction revenues are inherently lumpy, depending on project milestones and completion certificates.

The market cap of ₹6,288 Crore being down 29.6% in 1 year despite improving fundamentals suggests either market skepticism about sustainability or broader sector derating. The 52-week high of Rs 1,439.95 versus current levels around Rs 1,000 represents a significant correction.

The comparison with peers reveals Ahluwalia's positioning. Unlike pure-play developers who take development risk, or EPC giants like L&T that compete for mega projects, Ahluwalia occupies a sweet spot—large enough to handle complex projects, small enough to be nimble, focused enough to maintain quality.

IX. Challenges & Risk Factors

Contingent liabilities of Rs.1,963 Cr represent a significant overhang. In construction, contingent liabilities are par for the course—disputes over variations, delays, quality issues. But at nearly 50% of revenue, this number bears watching. These aren't necessarily losses waiting to happen, but they represent uncertainty.

Competition is intensifying from multiple directions. Large players like L&T are moving down-market as mega projects become scarce. New entrants with political connections are winning projects that Ahluwalia might have won in the past. Regional players are becoming more sophisticated. The moat that existed from relationships and track record is eroding.

Working capital intensity remains a structural challenge. Even with excellent management, construction requires funding gaps between expenditure and collection. As projects become larger and more complex, this intensity increases. The government's tendency to delay payments, especially at fiscal year-ends, exacerbates this.

The cyclical nature of infrastructure spending creates volatility. When the government tightens spending, orders dry up quickly. When spending resumes, everyone bids aggressively, crushing margins. Navigating these cycles requires financial strength and strategic patience.

Execution risks in complex projects are ever-present. A single project gone wrong can wipe out years of profits. Technical challenges, weather delays, labor issues, material price escalations—the list of what can go wrong is endless. Ahluwalia's track record suggests good risk management, but past performance doesn't guarantee future results.

The sustainability transition presents both opportunity and challenge. The company reported that around 30% of its projects now incorporate eco-friendly materials and construction processes. This is necessary for winning modern contracts but requires new capabilities and often higher costs.

X. Future Strategy & Growth Drivers

India's infrastructure pipeline is massive. The government has committed to spending over $1.4 trillion on infrastructure by 2025. Airports need modernization, metros are being built in tier-2 cities, hospitals are being upgraded, smart cities are being developed. The opportunity is undeniable; the challenge is converting opportunity into profitable growth.

The focus areas align well with government priorities. AIIMS projects will continue as healthcare infrastructure gets attention post-COVID. Railway station redevelopment is a priority project for the current government. Universities and educational infrastructure will see continued investment as India tries to build human capital. Data centers represent a new opportunity as digitization accelerates.

Technology adoption in construction is no longer optional. Building Information Modeling (BIM), project management software, drone surveys, prefabrication—these aren't just buzzwords but necessary tools for competitive advantage. Ahluwalia's investment in technology will determine whether it remains relevant or becomes obsolete.

International expansion remains a possibility but seems unlikely given the domestic opportunity and the company's traditional conservatism. The failed international ventures of many Indian construction companies serve as cautionary tales.

Next-generation leadership development is crucial. As Bikramjit Ahluwalia approaches his mid-80s, succession planning becomes critical. The involvement of Vikas Ahluwalia suggests continuity, but the transition needs to be managed carefully to maintain relationships and culture.

Capital allocation priorities will determine long-term value creation. The low dividend payout suggests growth is prioritized, but as the company matures, shareholders might demand higher returns. Balancing growth investment with shareholder returns while maintaining financial conservatism will be the key challenge.

XI. Investment Analysis & Valuation

The bear case is straightforward. Government dependency creates political risk—a change in government priorities could quickly impact order flow. Execution risks remain ever-present in complex projects. The contingent liabilities could crystallize into real losses. Competition is intensifying, potentially pressuring margins. The stock's recent underperformance might reflect fundamental concerns rather than temporary pessimism.

The bull case rests on India's infrastructure imperative. The country needs to build, and companies like Ahluwalia with proven execution capabilities will benefit. The order book provides near-term visibility, the balance sheet provides resilience, and the track record provides competitive advantage. If India grows at 6-7% annually, infrastructure spending must follow, and Ahluwalia is well-positioned to capture this.

The valuation puzzle is interesting. At current levels, the market seems to be pricing in significant risks or limited growth. The PE of 31 seems high for a construction company but reasonable for one with Ahluwalia's quality and growth profile. The price-to-book ratio and return metrics suggest the market isn't giving credit for the company's execution capabilities.

The 29.6% decline in market cap over one year despite improving operational metrics suggests either the market knows something the numbers don't show, or there's a genuine opportunity. The disconnect between fundamental performance and stock performance often creates opportunities for patient investors.

Long-term value creation in construction comes from three sources: volume growth as the market expands, margin improvement through better execution and mix, and multiple expansion as the company proves its sustainability. Ahluwalia has potential on all three fronts, but execution will determine outcomes.

XII. Lessons & Takeaways

Building trust over five decades in a relationship-driven business is perhaps Ahluwalia's greatest achievement. In an industry where contracts are won as much on reputation as on price, this trust is invaluable. Every project completed on time, every quality standard met, every payment dispute resolved fairly—these compound over decades into a moat that's hard to replicate.

Managing government contracts requires a special skill set. It's not just about technical execution but understanding bureaucratic processes, managing political sensitivities, and having the patience to deal with delayed payments and changing requirements. Ahluwalia's longevity suggests they've mastered this art.

Family business succession in a professional environment is one of the hardest challenges in business. How do you maintain entrepreneurial drive while building institutional capabilities? How do you ensure the next generation is competent, not just connected? Ahluwalia's approach—gradual transition, professional management alongside family, conservative financial management—offers a template.

Capital efficiency in a capital-intensive business seems like an oxymoron, but Ahluwalia proves it's possible. By choosing projects carefully, managing working capital aggressively, and maintaining financial discipline, they've generated returns without excessive leverage.

The importance of reputation in B2B/B2G markets cannot be overstated. Unlike consumer businesses where marketing can drive perception, in construction, reputation is built project by project over decades. One failed project can undo years of relationship building. Ahluwalia's steady growth suggests they understand this dynamic.

The story of Ahluwalia Contracts is ultimately a story about the unglamorous but essential work of building a nation's infrastructure. While tech unicorns capture imagination and headlines, companies like Ahluwalia literally build the foundations on which modern India stands. Their journey from a small partnership firm to a ₹6,000+ crore public company mirrors India's own infrastructure evolution. Whether they can navigate the next phase of growth while maintaining their core strengths will determine if this is a story of continued success or a cautionary tale about the challenges of generational transition and market evolution.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube