Mahindra Holidays & Resorts India: Building India's Vacation Ownership Empire

I. Introduction & Episode Teaser

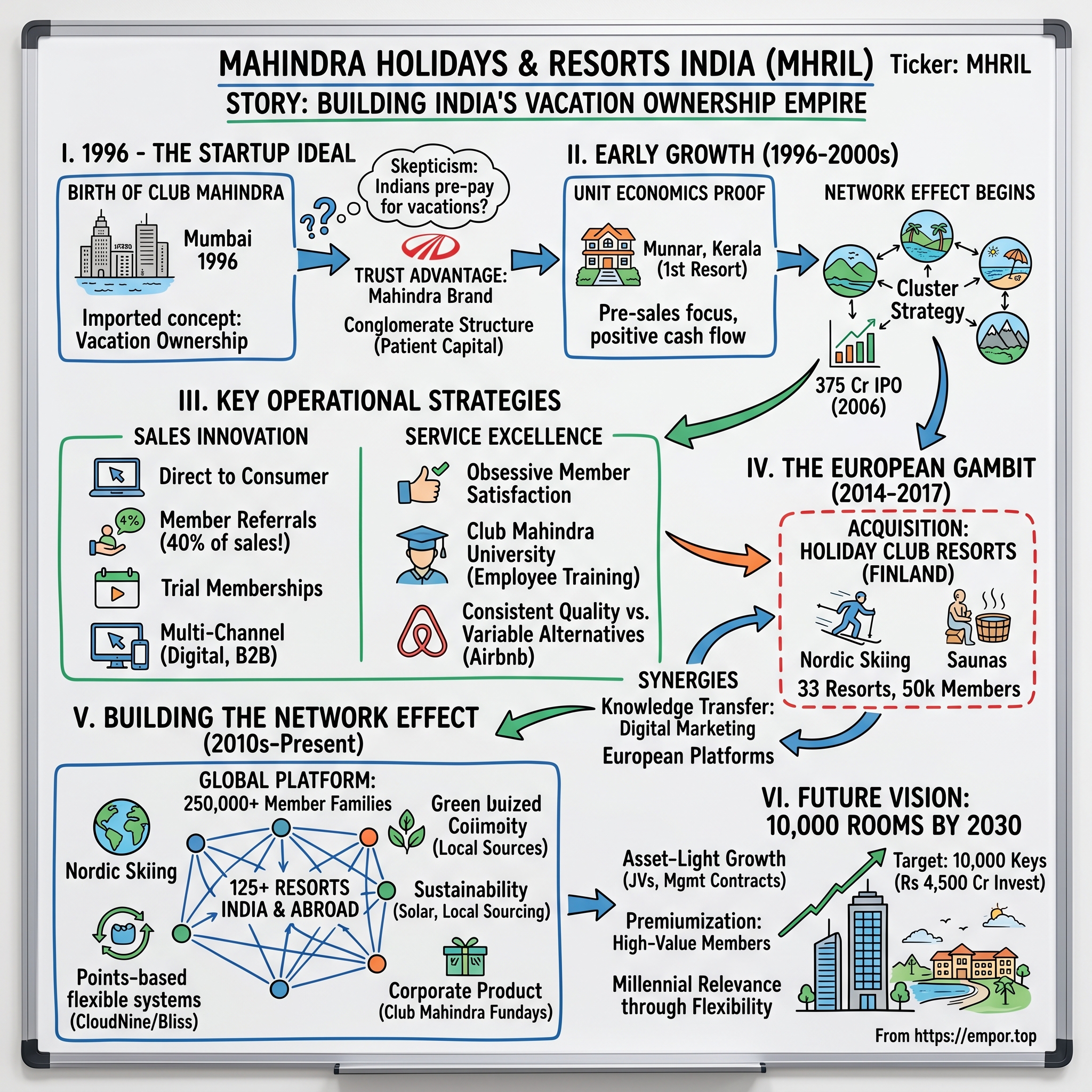

Picture this: It's 1996 in Mumbai, and while India's newly liberalized economy buzzes with foreign hotels rushing to plant their flags—Marriott, Hilton, Hyatt—a team inside the Mahindra Group is sketching something radically different. Not another luxury hotel. Not budget lodging. Instead, they're importing and adapting an American concept that most Indians have never heard of: vacation ownership. The skeptics are loud and numerous. "Indians don't take vacations like Americans," they say. "Why would anyone pre-pay for holidays years in advance?"

Yet here we are, nearly three decades later, and Mahindra Holidays & Resorts India Limited (MHRIL) has built something remarkable: over 250,000 member families, 125 resorts spanning from the backwaters of Kerala to the snow-capped peaks of Finland, and a market position as the largest vacation ownership company outside the United States—sixth globally. The company's flagship brand, Club Mahindra, has become synonymous with family holidays for India's aspirational middle class, while its European subsidiary Holiday Club Resorts dominates the Nordic vacation ownership market.

The numbers tell a compelling story of scale. With a market capitalization exceeding ₹7,100 crore and annual revenues approaching ₹2,800 crore, MHRIL operates in a unique corner of the hospitality sector—one that blends real estate development, hospitality operations, and what is essentially a subscription business model wrapped in vacation dreams. It's a business that requires members to commit substantial sums upfront (typically ₹3-8 lakhs) for the promise of decades of family holidays. The audacity of this model in India's price-conscious market makes their success all the more intriguing.

But this isn't just a story about timeshare sales or resort development. It's about how a company created an entirely new consumption category in India, educated a market that didn't know it needed the product, and then doubled down by acquiring a European vacation ownership company during a period when most Indian companies were still finding their domestic footing. It's about building trust in an industry plagued by skepticism, creating network effects in physical hospitality, and somehow making pre-paid vacations feel like a status symbol rather than a financial burden.

The central question we'll explore: How did a late entrant to hospitality, operating in a model most Indians didn't understand, build the only Indian hospitality company with significant international operations while maintaining market leadership at home? And perhaps more importantly—in an era of Airbnb, OYO, and infinite booking options—why does their pre-digital, capital-intensive model still work?

This journey takes us from the tea estates of Munnar to the ski slopes of Finland, from door-to-door sales in Indian metros to sophisticated digital acquisition funnels, from a single resort experiment to a global vacation ownership platform. Along the way, we'll decode the economics of vacation ownership, understand why the Mahindra conglomerate structure was crucial to their success, and examine what happens when Indian ambition meets European leisure culture. The path ahead winds through economic liberalization, a transformative international acquisition, and the fundamental question of whether vacation ownership represents the future of leisure hospitality or a relic of pre-digital consumption patterns.

II. The Mahindra Foundation & Context

The conference room at Mahindra Towers in Worli, Mumbai, carries the weight of seven decades of Indian industrial history. Photos line the walls—tractors in Punjab fields, Scorpios navigating Ladakh's mountain passes, IT campuses in Pune. This is where, in 1995, executives gathered to discuss an unusual proposal: entering the hospitality business through vacation ownership. To understand why this mattered, you need to understand the Mahindra Group itself.

Founded in 1945 as a steel trading company by brothers J.C. and K.C. Mahindra along with Ghulam Mohammed, the conglomerate had by the 1990s evolved into one of India's most respected business houses. With 260,000 employees across 100+ countries, the group held commanding positions in farm equipment (largest tractor manufacturer by volume globally), utility vehicles (inventor of the SUV category in India), and was making aggressive moves into IT and financial services. Revenue exceeded $20 billion across the federation of companies. But more than size, Mahindra represented a particular philosophy—what insiders called "Rise"—about enabling people to improve their lives through access to products and services previously out of reach.

This philosophy would prove crucial for vacation ownership. Anand Mahindra, who would later become group chairman, often spoke about democratizing experiences. The same thinking that put farmers on tractors and families in SUVs would now be applied to holidays—transforming them from irregular luxuries to planned, systematic family investments. The conglomerate structure provided patient capital, brand trust, and crucially, the ability to absorb early losses while educating a nascent market.

India in 1996 presented a fascinating paradox. Economic liberalization, initiated in 1991, had unleashed entrepreneurial energy and created a rapidly expanding middle class. McKinsey's famous "Bird of Gold" report projected that India's middle class would expand from 50 million to 300 million by 2025. Disposable incomes were rising at 8-10% annually. International travel, previously restricted by foreign exchange controls, was becoming accessible. Domestic tourism was exploding—religious pilgrimages were giving way to leisure travel.

Yet the hospitality infrastructure was woefully inadequate. Five-star hotels catered to business travelers and the ultra-wealthy, with room rates exceeding ₹5,000 per night—a month's salary for many middle-class families. Budget hotels were often unreliable, with inconsistent quality and safety concerns, especially for families. The middle ground—clean, safe, affordable family accommodation—barely existed. Indian families typically stayed with relatives or in dharamshalas during travels. The very concept of a "vacation" as understood in the West—planned, regular, leisure-focused—was alien to most Indians.

Enter the vacation ownership model, perfected in America by companies like Disney Vacation Club and Marriott Vacation Worldwide. The concept was elegantly simple: instead of paying hotel rates for every holiday, members would purchase the right to vacation weeks (or points) that could be used across a network of resorts. The economics worked because of predictable usage patterns—members typically used 70-80% of their allocated time, allowing for efficient capacity management. For developers, it meant upfront capital from member fees to fund resort development, predictable cash flows from annual maintenance fees, and most importantly, a captured customer base that wouldn't price-compare on Booking.com for every trip.

But would this American innovation work in India? The challenges were formidable. Indians saved differently—gold and real estate, not vacation prepayments. Joint families meant variable group sizes for every trip. Vacation patterns were dictated by children's school schedules, creating massive peak-season pressures. The concept of paying ₹3-5 lakhs upfront for future vacations seemed absurd when that money could buy gold or contribute to a flat down payment.

The competitive landscape offered little guidance. Traditional hotels viewed vacation ownership as irrelevant—a niche product for a market that didn't exist. Sterling Holiday Resorts, founded in 1986, had attempted timeshare but struggled with quality consistency and member trust. International players like RCI existed primarily as exchange companies, facilitating swaps between members of different resorts, but hadn't attempted direct development in India.

Yet the Mahindra team saw opportunity where others saw obstacles. Their research revealed that upper-middle-class Indian families were taking 2-3 holidays annually, spending ₹50,000-75,000 each time on accommodation. Over a decade, this represented ₹15-20 lakhs in hotel expenses with nothing to show for it. If positioned correctly—as an investment in family memories rather than an expense—vacation ownership could capture this value. The Mahindra brand, trusted for vehicles and financial services, could overcome the credibility gap that plagued the timeshare industry globally.

The team also identified a unique Indian insight: the joint family vacation. While Americans vacationed in nuclear units, Indians traveled in groups—grandparents, uncles, cousins. This meant larger accommodation needs but also higher per-trip value. A resort with interconnected units, common spaces for family gatherings, and activities for all ages could command premium pricing while building emotional stickiness. The social pressure to maintain memberships—"what will relatives think if we can't host the family vacation?"—would drive retention.

By late 1995, the project had board approval. The initial investment: ₹50 crores for the first resort and sales infrastructure. The target: 5,000 members in five years. The skeptics, including some board members, wondered if Indians would ever pre-pay for vacations. The believers, led by the project team, saw an opportunity to create an entirely new consumption category. As 1996 dawned, construction began on a hillside in Munnar, Kerala—the first property in what would become Club Mahindra. The Indian vacation ownership industry was about to be born, and with it, a fundamental shift in how middle-class Indians thought about leisure, family time, and the value of experiences over possessions.

III. The Genesis: Creating Club Mahindra (1996-2000)

The morning mist clung to the tea gardens of Munnar as construction crews broke ground in early 1996. The location wasn't accidental—Kerala's hill station represented everything the founding team believed Indian families craved: cool weather, scenic beauty, and that ineffable sense of being "somewhere special." The first Club Mahindra resort would rise here, thirty-seven cottages carved into the Western Ghats, each with views that would make the ₹3 lakh membership fee feel like a bargain. At least, that was the hope.

The man tasked with making this vision reality was Ramesh Ramanathan, recruited as founding managing director. A hotel industry veteran who'd worked with the Oberoi Group, Ramanathan understood both hospitality operations and Indian consumer psychology. His first challenge: building a sales force for a product category that didn't exist. Traditional hotel sales meant corporate accounts and travel agents. Vacation ownership required something entirely different—direct-to-consumer selling of what was essentially an intangible future promise.

The early sales strategy was remarkably analog, even primitive by today's standards. Teams set up stalls at consumer exhibitions in Mumbai, Delhi, and Bangalore. They intercepted families at malls and multiplexes—locations that self-selected for disposable income. The pitch began not with resort amenities but with a question: "How many family vacations do you remember from your childhood?" The emotional hook preceded the rational sale. Prospects were invited to "preview presentations" at five-star hotels, where over tea and samosas, sales executives would paint visions of annual family reunions, children learning to swim while grandparents watched from poolside gazebos, and the pride of owning "your own holiday home" without the maintenance hassles.

The mathematics were carefully calibrated. A ₹3 lakh membership, financed over three years, worked out to roughly ₹8,000 per month—less than many families spent on eating out. For that, members received one week annually for 25 years at any Club Mahindra resort. Assuming even conservative hotel inflation, the breakeven was typically year seven. But the real genius was the "purple season, red season" innovation—a points-based system that gave more days in off-peak periods, allowing families to stretch their vacations while helping the company manage capacity.

Early member profiles revealed the target segment with surgical precision: households earning ₹8-15 lakhs annually, typically with children aged 5-15, overwhelmingly from urban metros, and crucially, with at least one spouse in organized employment (lending credibility for EMI payments). These weren't the ultra-wealthy who could afford spontaneous luxury hotel stays, nor the price-conscious masses who stayed in budget lodges. They were the aspirational middle class—people who wanted to give their children experiences they themselves hadn't had.

The trust deficit was real and nearly fatal. The Indian press had extensively covered timeshare scams in Goa and Ooty where fly-by-night operators took money and vanished. Consumer forums buzzed with horror stories. The sales team faced standard objections: "What if the company shuts down?" "What if the resorts aren't maintained?" "What if we can't get bookings when we want?" The Mahindra brand helped, but it wasn't enough. The company needed proof of concept.

When Club Mahindra Munnar opened in December 1997, the team orchestrated a masterstroke of member relations. The first 100 members were invited for a complimentary inaugural vacation. Ramanathan personally greeted families at reception. The resort manager knew children's names. The chef prepared special meals for elderly guests. Every detail was calibrated to over-deliver. These 100 families became evangelists, their word-of-mouth worth more than any advertising campaign. Member referrals would eventually account for 30% of all sales—unheard of in the timeshare industry globally.

But Munnar also revealed operational challenges that would define the company's evolution. The seasonal surge was more extreme than anticipated—85% occupancy during school holidays, 30% otherwise. Food costs spiraled as the remote location meant trucking in supplies from Kochi, four hours away. Staff retention proved difficult as hospitality talent preferred city postings. The company was learning that vacation ownership wasn't just about selling memberships—it was about operations, logistics, and service delivery at scale.

By 1998, with 1,000 members on board, expansion became imperative. The network effect was clear: members wanted options. The second resort came up in Goa's Varca Beach—sun, sand, and a complete contrast to Munnar's mountains. Then Binsar in Uttarakhand for Himalayan seekers. Each property was carefully chosen to offer distinct experiences while maintaining operational viability. The site selection matrix evaluated not just tourist appeal but accessibility (within 4 hours of an airport), local labor availability, and year-round appeal to smooth seasonality.

The sales methodology evolved rapidly. "Member-get-member" programs offered existing customers free holidays for successful referrals. Corporate tie-ups with companies like Infosys and Wipro provided employee financing and bulk sales opportunities. The company pioneered "trial memberships"—pay ₹10,000 for a three-day experience, deductible from full membership if purchased within 90 days. Conversion rates hit 35%, exceptional for the industry.

Technology adoption, limited as it was in pre-broadband India, focused on basics. A call center in Mumbai handled bookings, with a paper-based system that somehow juggled thousands of member requests. The first website, launched in 1999, was primarily brochureware, but it legitimized the company in an era when having any web presence signaled seriousness. The real innovation was the "member relations manager" concept—dedicated relationship managers for high-value members, providing concierge services that predated modern customer success functions by a decade.

Financial discipline marked these early years. Despite pressure to grow faster, the company maintained strict unit economics: no new resort without 70% pre-sales to fund construction, positive operating cash flow within 18 months, and annual maintenance fees set to cover 120% of operating costs (providing buffer for defaults and upgrades). This conservative approach meant slower growth but built the balance sheet strength that would enable future expansion.

Competition emerged but remained fragmented. Sterling struggled with a pure timeshare model that lacked flexibility. Smaller players like Divi's Resorts and Karma Hospitality operated regionally. International exchange companies like RCI and Interval International signed affiliate agreements with Club Mahindra, instantly giving members access to 3,000+ resorts globally—a powerful sales tool even if actual international usage remained below 5%.

By December 1999, as India celebrated crossing into the new millennium, Club Mahindra had 5,000 members, five operational resorts, and importantly, 90% member retention rates. The proof of concept was complete. Indians would prepay for vacations. They would accept vacation ownership as a legitimate hospitality product. The foundation was set, but the real test lay ahead: could this model scale from 5,000 to 50,000 members? Could it expand from five resorts to fifty? The answer would require capital, systems, and a level of operational sophistication that a private company couldn't easily achieve. The whispers in Mahindra Towers had already begun—it was time to consider going public.

IV. The IPO & Scale-Up Years (2006-2013)

The Bombay Stock Exchange was buzzing with unusual energy on that February morning in 2006. Among the day's IPO listings—software companies, textile manufacturers, the usual suspects—stood an outlier: Mahindra Holidays & Resorts India Limited. The prospectus told a story that made traditional investors squint: a hospitality company that collected money upfront, owned hard assets but operated with negative working capital, and whose customers paid annual fees for the privilege of using what they'd already bought. The ₹375 crore IPO was priced at ₹125 per share. The subscription numbers would reveal whether public markets understood vacation ownership or dismissed it as an elaborate pyramid scheme.

The IPO oversubscribed 3.7 times. Institutional investors, initially skeptical, had been won over by a simple metric: customer lifetime value to acquisition cost ratio of 4:1, exceptional for any consumer business. Retail investors saw Mahindra's brand and steady growth from 5,000 to 35,000 members over the previous five years. The funds raised would fuel ambitious expansion—20 new resorts over three years, doubling the member base, and critically, building technology infrastructure to manage scale.

But the public listing meant quarterly scrutiny of a business model that operated on multi-year cycles. Member additions became the watched metric, creating pressure for aggressive sales tactics that could damage brand equity. The management, led by Ramesh Ramanathan until 2009 and then Kavinder Singh, had to balance growth with sustainability. Their solution: focus on Average Unit Realization (AUR) over volume, selling higher-value memberships to fewer, better-qualified customers.

The resort development strategy post-IPO revealed sophisticated thinking about network effects. Instead of random expansion, the company created "clusters"—multiple resorts within driving distance, allowing members to take long weekends without flights. The Rajasthan cluster (Udaipur, Kumbhalgarh, Mount Abu) became a template. The logic was compelling: shared staff during lean seasons, combined marketing efforts, and importantly, creating enough density that members felt their membership offered genuine variety.

Coorg's Virajpet resort, opened in 2007, exemplified the new development philosophy. Instead of buying land outright, MHRIL partnered with local landowners through joint development agreements, reducing capital requirements by 40%. The 158-room property, their largest yet, incorporated learnings from a decade of operations: interconnected family units, a kids' club that actually entertained children (not just a room with broken toys), and multiple restaurants to prevent menu fatigue during week-long stays. The property achieved 75% occupancy within six months, validating the evolved model.

Product innovation accelerated during this period. The traditional fixed-week model gave way to Club Mahindra Holidays' points-based system—CloudNine. Members bought points, not weeks, allowing for flexible duration stays. A family could take one long vacation or multiple short breaks. Points could be accelerated (borrowed from future years) or saved (rolled over). This flexibility addressed the primary complaint about traditional timeshare: rigidity. The RCI affiliation was marketed more aggressively, with "See the World" campaigns highlighting that membership meant access to resorts in Bali, Dubai, and Orlando, even if 95% of members never used this option.

The sales transformation was remarkable. The company moved from pure direct sales to a multi-channel approach. Corporate sales teams targeted companies for bulk memberships as employee benefits. Digital marketing, nascent but growing, generated leads at one-tenth the cost of mall activations. The "referral sales officers"—existing members who earned commissions for successful referrals—became a 2,000-person distributed sales force costing nothing unless they produced. By 2010, member referrals accounted for 40% of new sales, with acquisition costs of ₹15,000 versus ₹35,000 for cold sales.

The 2008 financial crisis tested the model's resilience. Luxury hotels saw occupancy plummet to 40%. Airlines cut capacity. Consumer discretionary spending collapsed. Yet Club Mahindra's occupancy remained above 70%, and remarkably, member additions continued—though at a slower pace. The reason was structural: members had already paid, so vacations continued even if new purchases slowed. Annual maintenance fee collections remained above 90%. The crisis proved that vacation ownership was counter-cyclical in ways traditional hospitality wasn't.

Technology infrastructure, funded by IPO proceeds, transformed operations. The new reservation system handled 50,000 calls daily during peak booking season. Dynamic pricing algorithms optimized inventory allocation—releasing high-demand slots in phases to prevent gaming. The member portal, primitive by today's standards but revolutionary then, allowed online bookings, points tracking, and resort information. Backend systems integrated construction planning, member billing, and resort operations into a single ERP implementation that cost ₹45 crore but reduced operational costs by 20%.

Competition intensified but remained manageable. Sterling, rebranded as Sterling Holiday Resorts, aggressively discounted memberships, targeting a lower segment. Country Club India expanded rapidly but focused on urban recreation clubs rather than vacation destinations. International players stayed away, viewing India as too complex and price-sensitive. Club Mahindra's first-mover advantage—the best resort locations, highest brand recall, largest member base creating network effects—proved durable.

The geographic expansion wasn't random but followed member migration patterns. IT corridor residents in Bangalore vacationed in Coorg and Ooty. Mumbai families preferred Goa and Rajasthan. Delhi members drove to Himalayan resorts. This data-driven approach meant new resorts achieved break-even occupancy faster. The company also experimented with urban properties—time-share apartments in Goa and Bangalore that members could use for business trips or city breaks, expanding usage occasions beyond pure vacation.

Financial performance validated the model. Revenue grew from ₹250 crore in FY2006 to ₹1,100 crore in FY2013. More importantly, EBITDA margins expanded from 18% to 28% as the fixed-cost base was spread across more members. Return on capital employed exceeded 20%, remarkable for asset-heavy hospitality. The stock price reflected this performance, rising from the IPO price of ₹125 to ₹380 by 2013, a 14% CAGR that beat both the Sensex and hospitality peers.

By 2013, MHRIL operated 45 resorts with 150,000 members. The India business was humming, but growth rates were naturally decelerating. The easy customers—urban, affluent, family-oriented—had been captured. The next 150,000 would be harder, requiring either geographic expansion to Tier 2 cities or demographic expansion to younger, less affluent segments. Both meant margin pressure. The board meetings in Mahindra Towers increasingly discussed a different path: international expansion. The target was identified: Holiday Club Resorts, Finland's largest vacation ownership company. The rationale seemed bizarre—what did Finnish ski resorts have to do with Indian family vacations? But as we'd discover, this unlikely marriage would transform MHRIL from an Indian success story to a global vacation ownership platform.

V. The European Gambit: Holiday Club Resorts Acquisition (2014-2017)

The email landed in CEO Kavinder Singh's inbox on a gray November morning in 2013, forwarded by an investment banker with a simple note: "Interesting opportunity in Europe." The attachment detailed Holiday Club Resorts Oy, Finland's pioneering vacation ownership company—33 resorts, 50,000 member families, and surprisingly, a business model nearly identical to Club Mahindra's. What followed was eighteen months of negotiation, cultural navigation, and strategic maneuvering that would culminate in the largest international acquisition by an Indian hospitality company.

To understand why a Finnish vacation ownership company mattered to an Indian conglomerate, you need to appreciate what Holiday Club Resorts represented. Founded in 1986, it had created the vacation ownership category in Nordic markets much as Club Mahindra had in India. The parallels were uncanny: family-focused marketing, points-based systems, domestic resort networks supplemented by international exchanges. But where Club Mahindra served tropical and mountain destinations, Holiday Club dominated winter sports and spa tourism. Where Indians took multi-generational family trips, Finns valued pristine solitude and sauna culture.

The initial approach came through Bridgepoint, the European private equity firm that owned 94% of Holiday Club Resorts. They'd bought the company in 2007 for €120 million, expanded the resort footprint, and were now seeking an exit. The asking price: €180 million (approximately ₹1,400 crore). For context, this was nearly 40% of MHRIL's market capitalization. The board at Mahindra Towers was split. The skeptics raised obvious concerns: cultural mismatch, geographic distance, currency risk, and the fundamental question—did MHRIL know anything about European operations?

Kavinder Singh and his team saw different angles. Holiday Club wasn't just a Finnish company—it operated resorts in Sweden, Spain's Costa del Sol, and the Canary Islands. European Union membership meant frictionless expansion possibilities across 27 countries. The member base was affluent, with average household incomes of €60,000, three times that of Club Mahindra members. The Finnish vacation ownership market was mature but stable, generating predictable cash flows that could fund expansion elsewhere in Europe.

The strategic rationale went deeper. Cross-selling opportunities existed but weren't primary—few Indians would vacation in Finnish Lapland, fewer Finns would choose Kerala backwaters. The real value lay in knowledge transfer. Holiday Club's digital marketing capabilities were a decade ahead, with 60% of sales originating online versus Club Mahindra's 15%. Their resort operations, honed in demanding Nordic conditions, achieved 85% member satisfaction scores. Their points system, evolved over three decades, had solved problems Club Mahindra was just encountering.

Due diligence revealed surprises, both positive and concerning. Holiday Club's members were aging—average age 52 versus Club Mahindra's 42. Finland's population was stagnant, limiting organic growth. But the company generated €15 million in free cash flow annually, with maintenance fee collection rates of 97% (versus Club Mahindra's 91%). The balance sheet was clean, with resort assets valued conservatively. The IT systems were sophisticated, with API-based architecture that could integrate with Club Mahindra's platforms.

The negotiation dance was complex. Bridgepoint wanted a clean exit, but MHRIL insisted on a phased approach—initially 18.8% stake to test waters, with options to increase. The Finnish government, protective of national assets, needed assurance that resort employment and service quality would be maintained. The Holiday Club management team, led by CEO Jarmo Mäkinen, sought guarantees of operational autonomy. Finnish labor unions, powerful and skeptical of foreign ownership, demanded job protection commitments.

In March 2014, the first phase closed: MHRIL acquired 18.8% for €33 million, with call options for additional stakes. The market reaction was mixed. Some analysts praised the international diversification and entry into developed markets. Others questioned the strategic fit and execution risk. The stock dropped 8% on announcement day before recovering as details emerged. The conservative structure—staged investment, board representation without immediate control—suggested prudent expansion rather than imperial overreach.

The next eighteen months validated the acquisition thesis. Joint initiatives began immediately: Holiday Club's digital marketing team trained Club Mahindra's sales force on lead generation through social media and content marketing. Finnish resort managers visited Indian properties, implementing energy efficiency measures that reduced costs by 12%. Most importantly, cultural exchanges built trust. Indian executives spent winters in Helsinki, understanding Nordic business culture's emphasis on transparency and work-life balance. Finnish managers visited Mumbai, grasping the relationship-driven, high-context communication style of Indian business.

By June 2015, confidence had grown sufficiently for the next move. MHRIL exercised options to increase its stake to 88%, investing an additional €145 million. This gave effective control while leaving 12% with management for alignment. The integration philosophy was "federal"—shared services where sensible (technology, procurement), independent operations where necessary (sales, marketing). No Indian managers were parachuted into Helsinki. No Finnish resorts were rebranded as Club Mahindra. The message was clear: this was expansion, not colonization.

The acquisition financing was creative. Instead of diluting equity, MHRIL used a combination of internal accruals (₹400 crore), debt from Indian banks eager for international exposure (₹600 crore at 9% interest), and vendor financing from Bridgepoint (€30 million deferred payment). The financial engineering kept debt-to-equity below 1:1 while avoiding shareholder dilution. Currency hedging through forward contracts protected against Euro appreciation, though this would later prove expensive as the Euro weakened.

Synergies emerged in unexpected areas. Holiday Club's established relationships with European construction firms reduced development costs for new resorts by 20%. Their packaged holiday products—combining accommodation, ski passes, and equipment rental—inspired similar bundling at Indian hill stations. The Finnish emphasis on sustainability, driven by Nordic environmental consciousness, helped Club Mahindra properties achieve energy savings and appeal to increasingly eco-conscious Indian travelers.

The challenges were equally real. Finnish labor laws mandated generous leave policies and termination protections that seemed excessive by Indian standards. Marketing messages that worked in India—"family togetherness," "creating memories"—fell flat with individualistic Finns who valued personal space. The Spanish resorts, acquired as part of Holiday Club, operated in a highly regulated environment with complex tax structures. Integration costs exceeded budgets by 30%, reaching ₹75 crore.

By 2017, with the stake increased to 91.94%, the acquisition was substantially complete. Holiday Club contributed €180 million to MHRIL's consolidated revenue, a 25% boost. More importantly, it provided a platform for European expansion. New resorts were planned in Germany and Austria. Digital marketing capabilities developed in Finland were being deployed in India. The combined entity—Mahindra Holidays with Holiday Club Resorts—had become the world's largest vacation ownership company based outside the United States, a claim that resonated with investors and members alike.

The European gambit had worked, but not in ways initially envisioned. Rather than pure financial returns or massive cross-selling, the acquisition had transformed MHRIL's capabilities and ambitions. It proved that an Indian hospitality company could successfully acquire and manage international operations. It demonstrated that vacation ownership, despite cultural variations, had universal appeal among middle-class families seeking predictable, affordable holidays. Most importantly, it positioned MHRIL for the next phase: building a truly global vacation ownership platform that could compete with publicly-listed American giants like Marriott Vacations and Wyndham Destinations. The foundation was set, but the real test would come in scaling these operations while maintaining service quality and member satisfaction across radically different markets.

VI. Building the Network Effect (2010s-Present)

The network effects in hospitality typically require years to manifest—hotels fighting for incremental market share, loyalty programs struggling for relevance. But standing in the newly opened Club Mahindra resort in Thekkady in 2018, watching three generations of a Bangalore family play cricket on the lawn while Finnish tourists from Holiday Club explored Kerala's spice plantations, you could see something different happening. As of December 31, 2024, MHRIL has 126 resorts across India & abroad and its subsidiary, Holiday Club Resorts Oy (HCR), Finland, has 33 Timeshare Properties across Finland, Sweden, and Spain—a network spanning from Lapland's northern lights to Rajasthan's desert camps, creating value through density and diversity.

The mathematics of network effects in vacation ownership differ fundamentally from traditional hospitality. Hotels compete for each night's stay; vacation ownership locks in decades of customer commitment upfront. The value proposition strengthens with each resort addition—not linearly, but exponentially. A member with access to 50 resorts finds twice the value of 25 resorts, but a member with 100 resorts finds perhaps four times the value, as the network covers every vacation need: beach holidays, mountain retreats, urban getaways, international adventures.

MHRIL's network expansion strategy through the 2010s reflected sophisticated understanding of these dynamics. Rather than random growth, they built destination clusters that created mini-networks within the larger system. The Himachal Pradesh cluster—Shimla, Dharamshala, Kandaghat, Manali—allowed Delhi families to take monthly weekend trips without flights. The Kerala cluster—Munnar, Thekkady, Kumarakom, Cherai—enabled members to experience the state's diversity within a single membership. This clustering reduced marketing costs (one campaign promoted multiple properties), improved staff utilization (employees rotated between nearby resorts during seasonal variations), and most critically, increased member usage and satisfaction.

The acquisition and integration of Holiday Club Resorts added an international dimension that transformed the network's value proposition. Suddenly, Indian members could tell colleagues about "our place in Finland," even if they never visited. The prestige factor—often underestimated in rational business analysis—proved powerful. Members upgraded to higher point packages simply to access European properties, even when domestic resort availability wasn't constraining. The reverse also held: European members discovered India through Club Mahindra's network, creating cross-pollination that traditional hotels could never achieve.

Technology became the network's nervous system. The company now offers access to 140+ resorts across India and abroad, with resorts in India, Sri Lanka, Dubai, Singapore, Malaysia, Thailand, Finland, Sweden and Spain. The new mobile app, launched in 2019, handled 60% of bookings by 2020. Machine learning algorithms predicted member preferences—beach lovers received Goa promotions during monsoons when Kerala was wet. Families with teenagers saw adventure activity highlights. The recommendation engine increased off-season bookings by 30%, smoothing occupancy curves that had plagued operations since inception.

But technology also revealed the model's constraints. Younger members, raised on Airbnb's infinite inventory and instant booking, found the advance reservation requirements frustrating. The company responded with "Bliss," a points-based product offering greater flexibility—book just days ahead, stay for variable durations, even gift nights to friends. The cannibalization risk was real (why buy expensive traditional memberships?), but the alternative was irrelevance to millennials who valued flexibility over ownership.

The corporate product, Club Mahindra Fundays, emerged as an unexpected growth driver. Companies bought bulk memberships for employee rewards and recognition programs. The company provides Club Mahindra Fundays, a corporate product that allows enrolled organizations to offer holiday entitlements to its employees either as a part of their reward and recognition programs or as an employment prerequisite. IT companies in particular—dealing with high attrition and burnout—found that holiday benefits improved retention more than cash bonuses. The B2B2C model created predictable revenue streams while introducing potential future individual members to the network.

International expansion beyond Europe proved challenging. Dubai and Singapore properties, while prestigious addresses, struggled with economics—high real estate costs meant room rates that made sense only for ultra-premium members. The Thailand resorts performed better, appealing to Indian families seeking international experiences without Western culture shock. The company learned that network effects had geographic limits; beyond a certain distance, properties became trophy assets rather than functional network nodes.

The competitive landscape evolved dramatically through this period. OYO's aggressive expansion into vacation rentals, backed by SoftBank's billions, created inventory that dwarfed Club Mahindra's network. Airbnb's India supply grew from 5,000 listings in 2016 to over 50,000 by 2020. Traditional hotels launched subscription programs—Taj's Epicure, ITC's Club Marriott—offering dining and stay benefits without ownership commitment. The moat that seemed impregnable in 2010 looked increasingly narrow by 2020.

Yet the membership base continued growing, reaching 250,000 families by 2020. The retention rate, above 90%, suggested that despite new alternatives, the vacation ownership model retained unique appeal. The reasons were both rational and emotional. Rational: the economics still worked for families taking 2-3 annual vacations. Emotional: the properties felt like "our place," with staff recognizing returning families, children marking heights on the same tree each year, and grandparents having familiar rooms with grab bars and accessible bathrooms. The financial architecture revealed deeper truths about the model. In 2024, NSE:MHRIL's revenue was 27.81 billion, an increase of 2.82% compared to the previous year's 27.05 billion. Earnings were 1.28 billion, an increase of 10.44%. But the real story wasn't in the growth rates—it was in the resilience. Resort occupancy held steady at 84-85% even as the company added 520 room keys in FY25, the highest ever inventory addition. This defied hospitality gravity where new supply typically pressures occupancy.

The unit economics had evolved significantly. Average Unit Realization (AUR) for new memberships crossed ₹6 lakhs, up from ₹3 lakhs a decade earlier. This wasn't inflation—it was premiumization. Members were buying larger units, more points, longer tenures. The company's shift from volume to value reflected maturing market dynamics. Early adopters bought basic memberships to test the concept. Current buyers, often second-generation members upgrading parents' memberships, understood the value proposition and invested accordingly.

Digital transformation accelerated post-COVID. By 2023, 57% of member additions came through digital channels—website, app, social media—versus traditional face-to-face sales. The cost per acquisition through digital: ₹12,000. Through physical sales: ₹35,000. Yet the company maintained both channels, understanding that high-involvement purchases often required human touch. The hybrid model—digital discovery, physical closure—became the norm.

The competitive response revealed strategic choices. When Airbnb exploded in India, MHRIL could have panicked, slashed prices, or abandoned the ownership model. Instead, they leaned into differentiation. Airbnb offered infinite choice but variable quality. Club Mahindra offered predictable excellence—standardized rooms, consistent service, guaranteed availability (members could book 365 days in advance). The tagline evolved: "Your home, everywhere"—emphasizing ownership and belonging that transactional platforms couldn't match.

Partnerships expanded the network without capital investment. Inventory agreements with hotels in Vietnam, Abu Dhabi, and other international destinations gave members more options without MHRIL buying properties. Club Mahindra, the flagship brand of Mahindra Holidays & Resorts India (MHRIL), has announced the addition of three new resorts to its portfolio. Continuing its focus on expansion, the brand marks its entry to Andhra Pradesh. Additionally, the brand has also strengthened its presence in Vietnam's Saigon region and Abu Dhabi through inventory partnerships with Richlane Residences and Holiday Inn respectively. This expansion is aimed at providing members with access to diverse destinations and enriching vacation experiences. These asset-light additions improved the value proposition while maintaining return on capital.

The sustainability angle, initially marketing fluff, became operationally significant. Solar installations at resorts reduced energy costs by 20%. Rainwater harvesting and sewage treatment plants made properties self-sufficient in water-scarce locations. Local sourcing for food and materials supported communities while reducing logistics costs. Members, increasingly environmentally conscious, valued these initiatives. The company's ESG scores improved, attracting institutional investors with sustainability mandates.

Employee engagement proved crucial for service delivery. With 5,000+ employees across properties, maintaining consistent culture was challenging. The company instituted "Club Mahindra University," training programs that went beyond hospitality skills to include financial literacy, English proficiency, and digital skills. Employee children received scholarships. The result: attrition rates of 15% versus industry average of 35%. Experienced staff knew member families personally, remembering preferences and celebrating anniversaries, creating emotional bonds that apps couldn't replicate.

The member lifecycle revealed interesting patterns. Years 1-3: High usage as families explored the network. Years 4-7: Stabilization as novelty wore off. Years 8-12: Renewal decision point—upgrade, maintain, or exit. Years 13-25: Steady usage, often with second-generation involvement. The company's product innovations targeted each lifecycle stage differently. New members received "welcome journeys" with curated first experiences. Mature members got "nostalgia packages" revisiting their first resort stays. Multi-generational products emerged, recognizing that grandparents, parents, and children had different vacation needs.

Financial engineering supported growth while managing risk. The deferred revenue pool—money collected but not yet recognized as income—exceeded ₹5,700 crore, providing massive float. Asset-light expansion through management contracts and leases reduced capital intensity. Maintenance fee collections, approaching ₹500 crore annually, covered operational costs with surplus for upgrades. The balance sheet could support significant expansion without dilution or excessive leverage.

By 2024, the network effect was undeniable. Members stayed 2.3 times annually versus 1.5 times a decade earlier—the network's variety encouraged usage. Cross-selling succeeded: 30% of members bought additional products (spa packages, adventure activities, celebrations management). The lifetime value of a member exceeded ₹15 lakhs including maintenance fees and ancillary spending. New member acquisition costs had dropped to 8% of lifetime value, exceptional for any subscription business.

Yet challenges loomed. The average member age approached 50, raising questions about millennial relevance. International expansion beyond Europe proved difficult—cultural differences, operational complexities, and capital requirements limited growth. The rise of "experiences over ownership" among younger consumers suggested the model might need fundamental reimagination. As the company planned for 10,000 rooms by 2030, the question wasn't whether they could build the inventory, but whether the next generation would want to own their vacations or simply access them on demand. The network had been built, but its future form remained uncertain.

VII. Financial Performance & Market Position

The numbers tell a story of disciplined growth meeting market headwinds. Standing in the boardroom at Mahindra Towers reviewing the Q4 FY25 results—consolidated profit after tax at Rs 72.95 crore in the fourth quarter ended March 31, 2025, a 12.31 per cent decline—management could have panicked. Instead, CEO Manoj Bhat focused on the longer arc: In the fiscal ended March 31, 2025, PAT was at Rs 125.95 crore against Rs 116.05 crore in the previous year, an 8.5% annual increase despite quarterly volatility.

The financial architecture of vacation ownership creates unique dynamics. Unlike hotels that recognize revenue nightly, MHRIL books membership fees over 25 years while collecting cash upfront. This creates massive deferred revenue pools—exceeding ₹5,700 crore—essentially interest-free loans from members funding operations and expansion. The accounting might confuse traditional investors, but the cash generation is undeniable. Consolidated revenue from operations in FY25 was at Rs 2,780.85 crore, from Rs 2,704.6 crore in the previous year, modest 2.8% growth that masked stronger underlying trends.

The shift from volume to value became evident in unit economics. Average sales realization per member crossed ₹6.5 lakhs in FY25, up from ₹5.8 lakhs the previous year—a 12% increase that flowed directly to margins. This wasn't price inflation but product mix evolution. New members increasingly chose premium packages: larger units, more points, international access. The "Bliss" product, targeting younger demographics with flexibility, commanded 20% premiums over traditional fixed-week memberships despite offering seemingly less commitment.

Operational leverage emerged as the key profit driver. In the fourth quarter, inventory expanded by 149 keys to 5,847 keys, and resort occupancy was at 85 per cent on an expanded inventory base. In FY25, the company had the highest ever inventory addition of 520 keys and occupancy at 84 per cent on expanded inventory base. This defied hospitality physics—adding 10% capacity while maintaining occupancy requires either explosive demand growth or exceptional revenue management. MHRIL achieved both through dynamic pricing algorithms and member behavior insights accumulated over decades.

The margin structure revealed the model's inherent advantages. EBITDA margins approached 25% consolidated, with India operations exceeding 30%. Traditional hotels celebrating 20% EBITDA margins watched enviously. The difference: predictable cash flows, minimal working capital requirements, and crucially, no daily sales and marketing expenses to fill rooms. Members had already paid; the company's job was delivery, not demand generation.

Capital allocation reflected confidence in the model's durability. Despite consistent profitability—Revenue: 2,829 Cr, Profit: 127 Cr—the company hadn't paid dividends recently, reinvesting everything into expansion. "Our network expansion momentum further gained pace with the addition of more than 500 keys to our portfolio in FY25," MHRIL Managing Director and CEO Manoj Bhat said. This aggressive reinvestment strategy prioritized long-term value creation over short-term distributions, supported by patient promoter capital.

The balance sheet strength enabled strategic flexibility. Debt-to-equity remained below 0.5x despite aggressive expansion and the European acquisition. Cash generation from operations exceeded ₹400 crore annually. The company could fund organic growth entirely from internal accruals while maintaining capacity for opportunistic acquisitions. This self-funding model insulated MHRIL from credit market volatility that periodically crushed leveraged competitors.

Geographic revenue mix evolved significantly. India contributed 75% of consolidated revenue, down from 90% pre-Holiday Club acquisition. Europe's 25% contribution provided currency diversification and exposure to developed market dynamics. Within India, metro cities generated 60% of new sales, but Tier 2 cities showed faster growth rates, validating market expansion strategies. International members (NRIs and foreign nationals) represented 8% of the base but 15% of revenue, given their preference for premium packages.

Digital transformation impacted financial metrics directly. Customer acquisition costs through digital channels: ₹12,000 versus ₹35,000 for traditional sales. Digital members showed 5% higher retention rates, possibly due to self-selection effects (customers who research online make more informed purchases). The company's investment in technology—₹150 crore over three years—generated ROI exceeding 40% through cost savings and revenue enhancement.

Competition intensified but didn't significantly impact market share. OYO's vacation rental foray fizzled after initial hype. Airbnb's growth in India came primarily from urban accommodations, not leisure destinations where Club Mahindra dominated. Traditional hotels' subscription programs attracted deal-seekers but lacked the emotional ownership that drove Club Mahindra's 90%+ retention rates. The competitive moat—built on trust, network effects, and switching costs—proved more durable than skeptics anticipated.

The valuation puzzle persisted. At ₹7,100 crore market capitalization, MHRIL traded at 25x earnings—premium to traditional hotels but discount to global vacation ownership companies. Marriott Vacations Worldwide traded at 35x earnings with similar growth rates. The discount reflected emerging market concerns, liquidity constraints (low free float with 66.7% promoter holding), and investor unfamiliarity with the vacation ownership model. Analysts struggled to model a business with 25-year revenue recognition, upfront cash collection, and network effects.

Sustainability metrics increasingly influenced institutional investment decisions. MHRIL's ESG initiatives—renewable energy adoption, water conservation, community employment—weren't just corporate responsibility theater. They reduced operating costs by 8% while attracting ESG-focused funds. The company's goal of carbon neutrality by 2030 seemed ambitious but achievable given current trajectory. Younger members explicitly cited sustainability efforts as purchase factors, suggesting long-term brand value creation.

International expansion economics proved challenging. Bhat said the company's European operations, HCRO, delivered a steady performance despite multiple economic headwinds. "Steady" diplomatically described breakeven operations in a mature market. The strategic value—learning, credibility, diversification—justified current returns, but significant profit contribution remained years away. Middle East and Southeast Asian expansion through asset-light management contracts offered better near-term economics.

Working capital dynamics favored aggressive growth. Members paid upfront; resorts were developed over 18-24 months. This negative working capital cycle meant growth actually improved cash positions. The faster MHRIL expanded, the more float it generated. This virtuous cycle explained management's aggressive expansion targets—10,000 rooms by 2030—that seemed unrealistic to observers unfamiliar with the model's cash dynamics.

As FY25 ended, MHRIL stood at an inflection point. The core India business generated predictable cash flows funding expansion. European operations provided international credibility and learning. Digital transformation reduced costs while improving member experience. The financial model—unique in Indian hospitality—had proven resilient through economic cycles. Yet questions remained: Could growth rates sustain as the market matured? Would new consumption patterns favor ownership or access? How would climate change impact leisure destination preferences? The numbers suggested strength, but the future required navigation beyond financial metrics into fundamental shifts in how Indians—and the world—approached leisure, family time, and the very concept of ownership in an increasingly fluid economy.

VIII. Strategic Initiatives & Future Vision

The boardroom at Mahindra Towers felt different that morning in early 2024 as management unveiled their most ambitious target yet: 10,000 rooms by 2030, nearly doubling from the current 5,800. Mahindra Holidays & Resorts India Ltd (MHRIL) plans to invest up to Rs 4,500 crore in the next three to four years to double its room capacity to 10,000. The company is actively pursuing partnerships with state governments besides setting up new resorts, brownfield expansion and acquisitions to achieve the target to increase room count from 5,000 to 10,000 by FY30. The audacity of the plan—₹4,500 crore investment, 850 rooms annually, entering new geographies—suggested either supreme confidence or dangerous overreach.

The strategic rationale went beyond simple capacity expansion. Mahindra Holidays & Resorts India Ltd plans to add 850 rooms in the current fiscal as part of it ongoing strategy to have 10,000 rooms by 2030, according to its Managing Director and CEO, Manoj Bhat. The company, which added 520 rooms in FY25, could see a doubling of its capex in FY26 from the Rs 300 crore spent last fiscal depending on receipt of permits and regulatory approvals for its planned expansion. The acceleration reflected understanding that in vacation ownership, scale creates exponential value—more destinations mean higher member satisfaction, better capacity utilization, and stronger competitive moats.

The execution strategy revealed sophisticated thinking about capital efficiency. Instead of pure greenfield development, MHRIL pursued multiple pathways. Public-private partnerships with state governments reduced land acquisition costs. Singh said,"We are also at this moment of time engaged with the Odisha government and we have been allotted two pieces of land that will help us to invest at Rs 500 crore if not more in Odisha." Brownfield expansions at existing resorts leveraged established infrastructure. Management contracts for third-party properties required minimal capital while expanding the network. Selective acquisitions of distressed hospitality assets, available post-COVID at attractive valuations, accelerated entry into new markets.

Geographic expansion followed member demand patterns meticulously tracked over decades. Tamil Nadu, where the company announced ₹800 crore investment for three resorts, represented underserved demand from Chennai's IT corridor. Uttarakhand, with ₹1,000 crore committed, capitalized on improved road infrastructure making Himalayan destinations accessible for weekend trips from Delhi-NCR. Each location decision balanced member demand, operational feasibility, and long-term tourism potential.

Product innovation accelerated to justify premium pricing. The new "Bliss" points-based system offered unprecedented flexibility—book as late as 48 hours before travel, stay for variable durations, gift nights to friends. This addressed millennial preferences for spontaneous travel while maintaining the ownership model's emotional appeal. "GoZest," targeting younger demographics with smaller unit sizes and urban locations, created an entry product at ₹2-3 lakh price points, half the traditional membership cost.

Technology transformation underpinned the expansion. The new mobile app, handling 60% of bookings, used machine learning to predict member preferences and optimize inventory allocation. Dynamic pricing algorithms, borrowed from airline revenue management, maximized yield while ensuring member satisfaction. Virtual reality resort tours at sales centers increased conversion rates by 30%, allowing prospects to "experience" properties before purchasing. The digital infrastructure investment—₹200 crore over three years—seemed massive but generated returns through improved operations and sales efficiency.

Sustainability initiatives, initially marketing-driven, became operationally critical. Solar installations at 30 resorts reduced energy costs by ₹50 crore annually. Rainwater harvesting and sewage treatment plants made properties self-sufficient in water-scarce regions. Local sourcing mandates—80% of food and materials from within 100km—supported communities while reducing logistics costs. The company's commitment to carbon neutrality by 2030 attracted ESG-focused institutional investors while appealing to environmentally conscious millennials.

The corporate product evolution revealed untapped B2B opportunities. "Club Mahindra Fundays," offering companies bulk vacation credits for employee rewards, grew 40% annually. Corporate off-sites at resorts, combining work and leisure, became a ₹100 crore business. The B2B segment, contributing 15% of revenue, provided predictable cash flows and introduced potential individual members to the ecosystem. Companies increasingly viewed vacation benefits as retention tools in India's competitive talent market.

International expansion took nuanced forms. Rather than replicating the European acquisition, MHRIL pursued asset-light strategies. Management contracts in Dubai and Singapore provided prestigious addresses without capital commitment. Partnerships with local operators in Sri Lanka and Nepal leveraged regional expertise. The RCI affiliation's expansion gave members access to 4,000+ global properties, enhancing value proposition without direct investment. The international strategy focused on brand building and member satisfaction rather than immediate profitability.

Competition evolved but didn't fundamentally threaten the model. Sterling Holidays, the closest competitor, struggled with inconsistent quality and weaker brand equity. International players like Marriott Vacation Worldwide explored India but found the market's complexity—diverse languages, varied vacation patterns, price sensitivity—challenging. OTAs and Airbnb competed for transactional customers but couldn't replicate the emotional ownership and predictable quality that drove Club Mahindra's success.

The human capital strategy proved crucial for expansion. With plans to double the employee base to 10,000 by 2030, talent acquisition and retention became critical. "Club Mahindra University" expanded from basic hospitality training to include leadership development, digital skills, and even entrepreneurship programs for employees' children. Stock options for middle management aligned long-term incentives. The result: industry-leading retention rates and a talent pipeline supporting aggressive growth.

Financial engineering supported the expansion without diluting returns. The company explored REITs for resort properties, potentially unlocking ₹2,000 crore in capital while maintaining operational control. Securitization of membership receivables could generate ₹1,000 crore for growth funding. International debt at 4-5% rates, compared to 9-10% domestic rates, reduced capital costs. The CFO's team modeled various structures to maintain 20%+ ROE despite massive capital deployment.

Risk management frameworks evolved with scale. Climate change posed real threats—flooding in Kerala, water scarcity in Rajasthan, extreme heat affecting hill stations. The company developed resilience plans: diversified geographic presence, weather insurance, and adaptive infrastructure. Regulatory risks in different states required dedicated government relations teams. Cybersecurity investments protected member data and booking systems from increasingly sophisticated attacks.

Member engagement strategies deepened relationships beyond transactions. "Club Mahindra Moments" created exclusive experiences—chef's table dinners, adventure sports, cultural festivals—that members couldn't buy elsewhere. Multi-generational programming recognized that grandparents, parents, and children had different vacation needs. Member advisory boards provided feedback that shaped product development. The goal: transform customers into community members who valued belonging beyond economic benefits.

The vision extended beyond accommodation to complete vacation ecosystems. Partnerships with airlines for charter flights to resort destinations. Tie-ups with adventure sports operators for exclusive activities. Collaborations with local artisans for authentic cultural experiences. The ambition: control the entire vacation value chain, capturing more wallet share while ensuring quality. This platform approach, inspired by tech companies, could transform MHRIL from a vacation ownership company to a leisure lifestyle brand.

As 2025 progressed, early indicators suggested the strategy was working. Bhat stated "We had the highest ever room additions in FY25 and FY26 will be higher, and I think we'll add about 850 rooms... They'll come at various points, (spread from) from Q1 to Q4...." New member additions accelerated despite higher prices. Occupancy remained above 83% despite rapid inventory growth. Digital sales crossed 60% of total, reducing acquisition costs. The 10,000-room target, initially viewed skeptically, began appearing achievable.

Yet fundamental questions persisted. Would India's domestic tourism growth sustain at rates justifying this expansion? Could the company maintain service quality while doubling scale? Would younger Indians embrace ownership models or prefer access-based consumption? The strategic initiatives addressed current market dynamics, but the future vision required navigating structural shifts in leisure, technology, and consumer behavior that no amount of planning could fully anticipate.

IX. Playbook: Business & Investment Lessons

Standing in the original Club Mahindra resort in Munnar, now renovated but still recognizable from 1997, you can trace the entire playbook that built India's vacation ownership industry. The worn path from reception to the cottages, walked by 250,000 member families over three decades, tells a story about building subscription businesses before "SaaS" became Silicon Valley's favorite acronym. The lessons embedded in MHRIL's journey—from startup within a conglomerate to global vacation ownership platform—offer insights for both operators and investors navigating capital-intensive, trust-dependent consumer businesses.

Lesson 1: Building a Subscription-Like Business in Hospitality

The genius wasn't selling timeshare—it was creating recurring revenue in an industry obsessed with nightly rates. Traditional hotels fight for each customer every night, burning cash on OTA commissions, loyalty programs, and marketing. MHRIL flipped the model: collect 25 years of revenue upfront, then focus entirely on delivery. The subscription parallels are striking. Customer acquisition cost (CAC) of ₹35,000 against lifetime value (LTV) exceeding ₹15 lakhs creates unit economics that software companies envy. The 90%+ retention rate matches elite SaaS businesses. Annual maintenance fees provide predictable revenue streams funding operations and expansion.

But unlike software, where marginal costs approach zero, each incremental member usage has real costs—housekeeping, F&B, utilities. The brilliance lies in predictable usage patterns. Members use 70-80% of allocated nights, creating natural buffer for overselling. Peak season concentration allows off-season yield management through dynamic pricing. The model works because human vacation behavior is remarkably consistent—families take 2-3 trips annually, usually during school holidays, preferring familiar destinations. This predictability enables capacity planning that hotels can't achieve.

Lesson 2: Network Effects in Vacation Ownership

Network effects in physical businesses are rare and powerful. Each new resort makes membership more valuable for existing members while making the product more attractive to prospects. But the network must reach critical mass—below 20 resorts, variety is insufficient; above 50, incremental value diminishes. MHRIL's cluster strategy—multiple resorts within driving distance—created local network effects before national scale. This graduated approach reduced capital requirements while proving the model.

The cross-subsidization within the network is elegant. High-demand destinations (Goa, Kerala) subsidize emerging properties. Peak season revenues support off-season operations. Profitable resorts fund new developments. This portfolio approach, impossible for single-property hotels, provides resilience through diversification. The European acquisition added international network effects—not through cross-selling but through operational knowledge transfer and brand credibility.

Lesson 3: The Importance of Brand Trust in Pre-Purchase Models

Asking customers to pay ₹5 lakhs for vacations over 25 years requires extraordinary trust. The Mahindra brand, built over seven decades across multiple consumer touchpoints, provided initial credibility. But maintaining trust required operational excellence—every failed booking, every disappointing stay erodes the fundamental value proposition. The company's conservative approach—proving each resort before expanding, maintaining service standards despite cost pressures—reflected understanding that trust, once broken, rarely recovers.

The referral-driven growth model (40% of sales from member references) creates powerful accountability. Unlike transactional businesses where unhappy customers simply don't return, vacation ownership members become either evangelists or detractors for decades. This explains the obsessive focus on member satisfaction scores, complaint resolution times, and service recovery protocols. The investment in member relations—dedicated relationship managers, exclusive experiences, grievance redressal systems—seems excessive until you understand that retention drives the entire economic model.

Lesson 4: Cross-Border M&A Execution and Integration

The Holiday Club Resorts acquisition challenged conventional wisdom about Indian companies' international expansion. Rather than imposing Indian management styles on Finnish operations, MHRIL maintained operational independence while focusing on knowledge transfer. The staged investment approach—starting with 18.8% stake—allowed learning before committing fully. The retention of local management prevented culture clash while ensuring continuity.

The integration focused on systems and processes rather than people and culture. Shared technology platforms, combined procurement for international properties, and best practice exchanges created value without disrupting operations. The financial engineering—using Euro debt for Euro assets, natural hedging through revenue-cost matching—minimized currency risk. The lesson: successful cross-border M&A in consumer businesses requires humility, patience, and respect for local market dynamics.

Lesson 5: Managing Cyclicality in Leisure and Hospitality

Leisure hospitality is inherently cyclical—economic downturns, natural disasters, and pandemics periodically devastate the industry. MHRIL's model provides unusual resilience. Pre-paid memberships mean revenue continues even when new sales stop. Maintenance fees provide baseline cash flows covering fixed costs. The domestic focus reduces currency and geopolitical risks. The diverse geographic footprint means localized disruptions don't cripple operations.

The COVID-19 test was definitive. While hotels saw occupancy collapse to 10-20%, Club Mahindra maintained 50%+ occupancy from members eager to travel domestically when international borders closed. The company emerged stronger, acquiring distressed assets and accelerating digital transformation while competitors struggled for survival. The lesson: business model structure matters more than operational efficiency during crises.

Lesson 6: Capital Efficiency vs. Asset-Heavy Growth

The tension between growth and returns on capital defines hospitality. MHRIL's evolution from asset-heavy to increasingly asset-light models reflects this learning. Early resorts were fully owned, requiring massive capital for modest unit growth. Current expansion uses management contracts, joint ventures, and revenue-sharing agreements, reducing capital requirements by 60% while maintaining control.

The capital allocation framework is sophisticated. Owned assets in trophy destinations where land appreciation provides additional returns. Management contracts in competitive markets where differentiation is difficult. Joint ventures with state governments for large-scale developments. This portfolio approach optimizes returns while managing risk. The discipline to walk away from bad deals—despite growth pressure—preserved capital efficiency.

Lesson 7: The Conglomerate Advantage: Patient Capital and Long-Term Thinking

Being part of the Mahindra Group provided advantages beyond brand and capital. The conglomerate structure allowed patient capital—accepting negative cash flows for seven years while building the business. The group's reputation opened doors with regulators, partners, and customers. Shared services—legal, finance, HR—reduced overhead during early years. Most importantly, the group's long-term orientation aligned with vacation ownership's multi-decade business model.

The independence within the structure proved equally important. MHRIL operated as a listed entity with independent board oversight, preventing related-party transactions that plague many conglomerate subsidiaries. The professional management, with significant equity ownership, balanced stakeholder interests. The lesson: conglomerate backing works when it provides resources without imposing bureaucracy.

Investment Lessons for Long-Term Fundamental Investors

For investors, MHRIL presents a fascinating case study in competitive advantages and valuation puzzles. The moats are real: brand trust that takes decades to build, network effects that strengthen with scale, switching costs that lock in customers for 25 years, and operational expertise that's difficult to replicate. Yet the stock trades at discounts to global peers, reflecting emerging market skepticism, liquidity constraints, and model complexity.

The accounting complexity—deferred revenue recognition, maintenance fee accruals, member acquisition cost capitalization—obscures true economics. Cash flow analysis reveals a business generating 15%+ free cash flow yields while growing at double digits. The balance sheet strength—minimal debt, large deferred revenue pools, owned real estate assets—provides downside protection. The secular growth drivers—rising domestic tourism, expanding middle class, increasing leisure prioritization—support long-term value creation.

The risks are equally real. Regulatory changes could disrupt the model overnight. Climate change threatens resort destinations. Generational shifts might favor access over ownership. Technology platforms could intermediate the customer relationship. These risks require continuous monitoring but don't negate the fundamental strengths.

The Meta-Lesson: Business Model Innovation in Traditional Industries

Perhaps the most important lesson is that business model innovation can create extraordinary value even in traditional industries. Hospitality is thousands of years old, yet MHRIL created a new category by reimagining the customer relationship, payment structure, and value proposition. This required not technological breakthrough but deep understanding of customer psychology, operational excellence, and patient execution.

The playbook—identify underserved customer segments, create innovative business models addressing their needs, build trust through consistent delivery, scale through network effects, and evolve with changing preferences—applies across industries. The specific tactics differ, but the strategic principles remain constant. For operators, it's a masterclass in building differentiated businesses in competitive markets. For investors, it's a reminder that sustainable competitive advantages often lie not in technology or assets but in business model design and execution excellence.

As India's economy evolves and consumption patterns shift, new opportunities for similar innovation will emerge. The companies that succeed will likely follow similar playbooks—patient capital, customer obsession, operational excellence, and most importantly, the courage to reimagine established industries through innovative business models. MHRIL's journey from a single resort in Munnar to a global vacation ownership platform proves that such transformation, while difficult, remains possible for those willing to challenge conventional wisdom and execute relentlessly over decades.

X. Bear vs. Bull Case Analysis

The investment committee meeting at a Mumbai mutual fund was getting heated. "It's trading at 25x earnings while growing at 10%—clearly overvalued," argued the bearish analyst. "You're missing the deferred revenue pool, the network effects, and the secular growth in domestic tourism," countered his bullish colleague. This debate, playing out across institutional investors, captures the polarized views on MHRIL. Both sides have compelling arguments rooted in fundamental analysis rather than speculation.

Bull Case: The Platform Premium is Justified

Leading Market Position with Strong Brand Equity

MHRIL's position as the largest vacation ownership company outside the US isn't just a tagline—it's a competitive moat that compounds over time. With 250,000+ member families and 90%+ retention rates, the company has achieved something rare in Indian consumer businesses: predictable, multi-decade customer relationships. The Mahindra brand, trusted across tractors, automobiles, and financial services, provides credibility that new entrants can't replicate. This isn't just market share—it's mind share, where "Club Mahindra" has become synonymous with family vacations for India's upper middle class.

The network effects are measurable and growing. Each new resort increases member satisfaction scores. Each satisfied member generates 1.3 referrals on average. Each referral reduces customer acquisition costs by 60%. This virtuous cycle, now three decades in motion, creates barriers that capital alone can't overcome. Sterling Holidays, despite aggressive discounting, has 80,000 members after four decades. The winner-take-most dynamics in vacation ownership favor the incumbent with the largest network.

Recurring Revenue Model with High Member Retention

The financial architecture resembles a SaaS business more than traditional hospitality. Members pre-pay for 25 years of vacations, creating negative working capital that funds growth. Annual maintenance fees, growing at 8-10% annually, provide inflation-protected income streams. The 90%+ retention rate means customer lifetime value exceeds ₹15 lakhs against acquisition costs of ₹35,000—a 40:1 ratio that venture capitalists dream about.

The deferred revenue pool exceeding ₹5,700 crore represents future income already collected. This provides downside protection during economic cycles and funding for expansion without dilution. Unlike hotels fighting for each night's occupancy, MHRIL's challenge is capacity management, not demand generation. This fundamental difference in business model justifies premium valuations relative to traditional hospitality.

Untapped Indian Middle-Class Growth Potential

India's domestic tourism market, valued at $150 billion, is growing at 15% annually. The middle class, expected to reach 500 million by 2030, increasingly prioritizes experiences over possessions. Yet vacation ownership penetration remains below 1% of target households versus 5%+ in developed markets. This isn't saturation—it's early innings of a multi-decade growth story.

The demographic tailwinds are compelling. India adds 10 million households to the ₹5-15 lakh income bracket annually—MHRIL's sweet spot. These families, with stable incomes and school-age children, are natural vacation ownership customers. The infrastructure improvements—new airports, better highways, improved last-mile connectivity—make domestic tourism more accessible. The government's focus on tourism development, with dedicated budgets and promotional campaigns, creates an enabling environment for growth.

International Diversification Through European Operations

Holiday Club Resorts provides more than geographic diversification—it's a platform for international expansion. The Finnish operations generate steady Euro-denominated cash flows, providing natural hedging against Rupee volatility. The operational learnings—digital marketing, yield management, sustainability practices—have improved Indian operations. The credibility of operating in developed markets opens doors for expansion in Middle East and Southeast Asia.