Medanta: India's Healthcare Revolution - From Cardiac Surgeon to Hospital Empire

I. Introduction & Cold Open

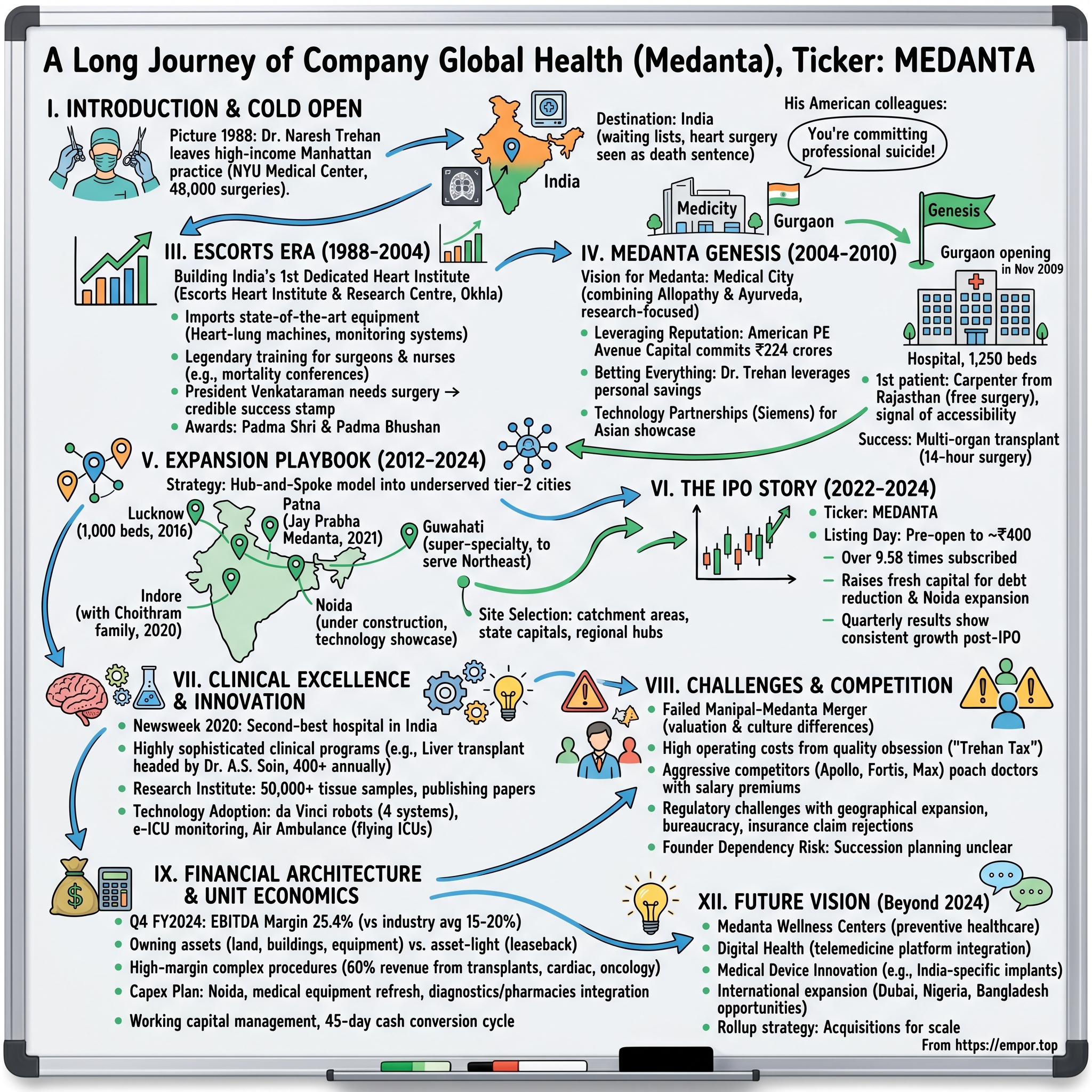

Picture this: It's 1988, and one of America's most successful cardiac surgeons is packing up his Manhattan practice. Dr. Naresh Trehan has just performed his 48,000th successful heart surgery at New York University Medical Center. His patients include Wall Street titans and UN diplomats. His income places him among the highest-earning physicians in America. And he's walking away from all of it.

The destination? India—a country where, at the time, getting a CT scan meant a three-month waiting list, where heart surgery was considered a death sentence by most, and where the very idea of world-class healthcare seemed like an oxymoron. His American colleagues thought he'd lost his mind. "You're committing professional suicide," one told him bluntly over drinks at the Yale Club.

Fast forward to today: Global Health Limited, the company built from Dr. Trehan's vision, commands a ₹37,094 crore market capitalization on the NSE. The flagship Medanta hospitals treat everyone from Bihar farmers to Fortune 500 CEOs flying in from Singapore. With ₹3,862 crores in revenue and ₹534 crores in profit, it's become one of India's healthcare crown jewels—a testament to what happens when surgical precision meets entrepreneurial ambition.

But here's what makes this story truly remarkable: While Apollo's Prathap Reddy built India's first corporate hospital chain through pure business acumen, and Fortis emerged from the financial engineering of the Singh brothers, Medanta represents something different—a third way. It's what happens when a doctor refuses to choose between clinical excellence and commercial scale, between serving the elite and reaching the masses, between Western standards and Indian affordability.

The company that trades under the symbol MEDANTA isn't just another hospital operator. It's a vertically integrated healthcare ecosystem spanning hospitals, pathology labs, medical services, and R&D for drugs and devices. It's simultaneously India's second-best hospital according to Newsweek and one of its most aggressive expanders into tier-2 cities. It's a place where robots perform surgeries while traditional Ayurvedic healers work down the hall.

How does a cardiovascular surgeon's personal mission become a publicly-traded healthcare platform? How do you maintain surgical standards when you're operating at Indian price points? And what happens when the founder who is the brand approaches his ninth decade?

This is the story of how one man's return ticket to India sparked a healthcare revolution—and why the next chapter might be even more audacious than the first.

II. The Architect: Origins & American Journey

The year was 1963, and a young man from a middle-class Delhi family had just secured admission to King George's Medical College in Lucknow—one of India's oldest medical institutions, where the corridors still echoed with colonial-era formality and where becoming a doctor meant memorizing British medical texts that were already decades old. Naresh Trehan wasn't born into medicine; his father ran a small business, his mother managed the household. But something about the precision of surgery, the immediate impact of healing, captured his imagination.

Six years later, fresh MBBS degree in hand, Trehan made a decision that would define not just his career but eventually India's healthcare landscape: he boarded a Pan Am flight to New York City with $8 in his pocket and a residency offer from Thomas Jefferson University Hospital in Philadelphia. It was 1969—Neil Armstrong had just walked on the moon, Woodstock was redefining American culture, and a 23-year-old Indian doctor was about to enter the pressure cooker of American medical training.

The residency years were brutal. Hundred-hour weeks were standard. Foreign medical graduates faced an additional layer of scrutiny—every procedure double-checked, every diagnosis questioned. Trehan responded by becoming technically flawless. His hands, colleagues would later say, had an almost musical quality during surgery—swift, precise, never a wasted movement. By 1971, he'd earned a position at NYU Medical Center, one of Manhattan's most prestigious hospitals.

This is where the mythology begins to build. In the operating theaters of NYU, Trehan didn't just perform heart surgeries—he pioneered techniques. He became known for taking cases others wouldn't touch: the 400-pound patient whose heart was barely accessible, the infant with multiple congenital defects, the Wall Street executive who needed a triple bypass but couldn't afford more than three days away from the trading floor. His success rate climbed to 99.5%—astronomical in an era when a 90% survival rate was considered excellent.

The same year he started at NYU, Trehan married Madhu—a journalist who would later become one of India's media pioneers with her show "The Last Word." Their life in Manhattan was everything an immigrant success story should be: a brownstone in the Upper East Side, two daughters attending private schools, dinner parties with New York's medical and media elite. By the mid-1980s, Trehan was performing over 3,000 coronary surgeries annually, his patient list reading like a Who's Who of global power brokers.

But success in America came with a growing dissonance. During visits back to India, Trehan saw patients dying from conditions he could fix in his sleep. He watched families sell ancestral land to afford substandard cardiac care. He met brilliant Indian doctors whose skills were wasted due to lack of proper equipment and training. The contrast became unbearable.

The breaking point came during a 1987 trip to Delhi. Trehan was visiting his parents when a family friend—a retired army colonel—mentioned needing heart surgery. The options were grim: fly to America (unaffordable), try the government hospital (six-month wait, 50% survival rate), or accept fate. Trehan operated on the colonel at a private nursing home, improvising with limited equipment. The surgery succeeded, but the experience haunted him. "I realized I was treating American investment bankers while Indian school teachers were dying from the same conditions," he'd later tell an interviewer.

His American colleagues couldn't understand the decision to return. At a farewell dinner at the Four Seasons, the chief of cardiac surgery at NYU pulled him aside: "Naresh, you're at the peak of your powers. You have everything here—resources, reputation, wealth. India has nothing. Why throw it away?" Trehan's response was cryptic then, clearer in hindsight: "Because India has 800 million people who deserve what Americans take for granted."

The personal dynamics added another layer of complexity. Madhu, his wife, was building her own media career. Their daughters were thoroughly American teenagers—one dreaming of Columbia journalism school, the other eyeing pre-med at Cornell. Yet the family agreed to uproot everything. As Madhu would later write in her column: "We weren't just moving countries; we were moving from the first world to what felt like the nineteenth century of medicine."

In early 1988, Trehan performed his last surgery at NYU—a complex valve replacement on a Broadway producer. Two weeks later, he was in Delhi, negotiating with Rajan Nanda of the Escorts Group to create India's first dedicated heart institute. The surgeon who'd conquered Manhattan was about to face his greatest challenge: revolutionizing healthcare in a country that many considered beyond repair.

The American years hadn't just made Trehan a world-class surgeon; they'd given him something more valuable—a template for what excellence looked like, and the unshakeable belief that India deserved nothing less.

III. Escorts Era: Building India's First World-Class Heart Institute

The Delhi that Dr. Trehan returned to in 1988 bore little resemblance to the Manhattan he'd left behind. At Escorts Hospital in Okhla, where he'd agreed to establish the Escorts Heart Institute and Research Centre, the contrasts were jarring. The hospital's main building looked modern enough from the outside, but inside, the infrastructure told a different story. Power cuts were routine—imagine performing open-heart surgery when the lights could fail at any moment. The "sterile" operating theaters had windows that opened onto Delhi's polluted streets. The blood bank refrigeration was temperamental. Even basic supplies like surgical gloves had to be washed and reused.

Trehan's first surgery at Escorts nearly ended in disaster. Midway through a coronary bypass, the power failed. The backup generator took forty-five seconds to kick in—an eternity when a patient's heart is stopped. Trehan continued operating by the light of a flashlight held by a trembling junior doctor, his hands never wavering. The patient survived, but Trehan walked out of that OR with a singular determination: never again.

What followed was less a renovation than a revolution. Trehan didn't just want to upgrade Escorts' cardiac unit—he wanted to create a template for Indian healthcare. Using his American connections, he imported equipment that most Indian hospitals had never seen: heart-lung machines that could maintain circulation for hours, monitoring systems that tracked seventeen vital parameters simultaneously, surgical instruments precise to the millimeter. The cost was staggering—over ₹50 crores in 1988 rupees—but Rajan Nanda, Escorts' chairman, backed every purchase. "Dr. Trehan doesn't think in half-measures," Nanda told his board when they questioned the expenses.

But equipment was the easy part. The harder challenge was human: how do you create a culture of excellence in an environment accustomed to "chalta hai"? Trehan's approach was part drill sergeant, part professor. He instituted protocols that seemed obsessive to Indian medical staff: hand-washing procedures that took three full minutes, surgical checklists with forty-seven items, mortality and morbidity conferences where every death was dissected without mercy.

The training regimen he created was legendary in its intensity. Young cardiac surgeons would assist in over 500 procedures before being allowed to make their first incision. Nurses underwent six months of specialized cardiac training. Even the cleaning staff received lectures on infection control. "We're not just changing how we operate," Trehan told his team. "We're changing how India thinks about healthcare."

The results spoke louder than any mission statement. Within eighteen months, Escorts' cardiac surgery mortality rate dropped from 8% to under 2%—comparable to the best American centers. Word spread through Delhi's elite circles: there was finally a place in India where heart surgery wasn't a gamble with death. Industrialists who'd been planning trips to Cleveland Clinic started coming to Okhla instead.

Then came the call that changed everything. In 1991, President R. Venkataraman needed cardiac surgery. The protocol was to fly him to America or bring in foreign surgeons. Instead, the president's office asked: "What about Dr. Trehan?" The surgery's success didn't just save a president—it gave Escorts, and Indian healthcare, a stamp of credibility that no marketing campaign could have achieved. Trehan became the official cardiac surgeon to Rashtrapati Bhavan, a position he'd hold through multiple presidents.

The awards followed inevitably: Padma Shri in 1991, Padma Bhushan in 2001. But Trehan seemed almost indifferent to the honors. What excited him were the numbers: by 1995, Escorts was performing 4,000 cardiac surgeries annually with a 98.5% success rate. The institute had trained over 200 cardiac surgeons who were spreading Trehan's protocols across India. International patients—initially skeptical NRIs, then Europeans seeking affordable care—began arriving.

Yet even as Escorts became India's cardiac care destination, Trehan grew increasingly frustrated. The relationship with Escorts leadership became strained over vision. Trehan wanted to expand into other specialties, to create a true multi-specialty medical city. Escorts saw the heart institute as sufficient—profitable, prestigious, why rock the boat? Trehan pushed for a medical college, for research facilities, for partnerships with international institutions. The board pushed back, citing costs and complexity.

The breaking point came during a 2003 board meeting. Trehan had prepared a presentation on creating "Escorts Medical City"—a 100-acre campus that would rival Mayo Clinic. The board's response was tepid. "We're a heart hospital, Doctor, not a real estate company," one member said. Trehan walked out of that meeting knowing his time at Escorts was ending. He'd built India's premier cardiac center, trained a generation of heart surgeons, and proven that Indian healthcare could match global standards. But the Escorts experience had also taught him a crucial lesson: to truly transform healthcare, you needed complete control.

By 2004, after two decades of association that had redefined Indian cardiac care, Trehan resigned from Escorts. He was 58 years old, at the peak of his surgical career, having personally performed over 48,000 successful heart surgeries. Most surgeons would have coasted toward a comfortable retirement, perhaps taking emeritus positions and board seats.

But Trehan had a different plan brewing—one that would require him to transform from surgeon to entrepreneur, from medical practitioner to institution builder. The blueprint in his mind wasn't just for another hospital. It was for something India had never seen: a medical city that would make even his achievements at Escorts look like a rehearsal.

IV. The Medanta Genesis: Vision to Reality

The land in Gurgaon was nothing special in 2004—43 acres of scrubland on the outskirts of a city that was itself just beginning its transformation from a Delhi suburb to India's millennium city. Property developers saw future shopping malls and office complexes. Dr. Naresh Trehan saw something entirely different: India's answer to Mayo Clinic, Johns Hopkins, and Cleveland Clinic rolled into one. He called it Medanta—a portmanteau of "medical" and "Vedanta," the ancient Indian philosophy of holistic knowledge.

The first person Trehan called wasn't a banker or a builder—it was Sunil Sachdeva, a healthcare administrator who'd worked with him at Escorts. "I'm building something that's never been attempted in India," Trehan told him over coffee at the Oberoi. "Not just a hospital, but a medical city. Multi-specialty, research-focused, combining allopathy with Ayurveda, serving both the diplomat and the daily wage worker." Sachdeva's response captured what many thought: "Dr. Trehan, with respect, you're describing a ₹1,500 crore project. Where's the money coming from?"

The funding journey was a masterclass in leveraging reputation. Trehan didn't just pitch a hospital; he sold a vision of transforming Indian healthcare. His first major breakthrough came from an unexpected source: Avenue Capital, the American private equity firm run by Marc Lasry. Lasry had met Trehan through a patient—a hedge fund manager whose life Trehan had saved at Escorts. In 2006, Avenue committed ₹224 crores, not just for the returns but because, as Lasry told his partners, "This guy doesn't think in singles; he swings for home runs."

But even with Avenue's backing, the capital requirements were staggering. Trehan took a decision that would have been unthinkable for most doctors: he leveraged everything. His savings from two decades in America, his Escorts earnings, property, even his wife Madhu's media company shares—everything went into Medanta. "My accountant thought I'd gone mad," Trehan later recalled. "But I knew that if I didn't bet everything on this, why should anyone else?"

The design phase revealed Trehan's obsessive attention to detail. He hired architects from Singapore who'd designed hospitals in earthquake zones, infection control specialists from Sweden, and equipment consultants from Germany. Every aspect was rethought from first principles. Why did Indian hospitals smell like phenyl? Because they used cheap disinfectants—Medanta would use the same enzymatic cleaners as Swiss hospitals. Why did patients' families camp in corridors? Because Indian hospitals ignored attendants—Medanta would have dedicated family zones with sleeping facilities.

The infection control measures seemed paranoid to Indian contractors. Trehan mandated negative pressure isolation rooms, HEPA filters in every operating theater, and antimicrobial copper surfaces on all high-touch areas. The construction team was baffled when he insisted on separate elevators for waste disposal, different pathways for clean and dirty materials, and UV sterilization systems in the air conditioning. "We're not building a hospital," he told them. "We're building a fortress against infection."

The technology partnerships were equally ambitious. Trehan flew to Munich to negotiate directly with Siemens for imaging equipment that wasn't even commercially available yet. He convinced them to make Medanta their showcase facility for Asia—installing PET-CT scanners, 3-Tesla MRI machines, and a CyberKnife system that only twenty hospitals worldwide possessed. The Siemens CEO asked him point-blank: "Dr. Trehan, this equipment is for populations of millions in Western cities. Gurgaon has what, 200,000 people?" Trehan's response: "Build it, and they will come."

But perhaps the most radical decision was integrating traditional medicine into a super-specialty hospital. Trehan created an entire floor dedicated to Ayurveda, Yoga, and naturopathy—not as token additions but as serious therapeutic options. Harvard-trained cardiologists would work three floors above practitioners of 5,000-year-old healing arts. The medical establishment was skeptical, even scandalized. At a medical conference, a senior Apollo doctor publicly questioned whether Trehan was "diluting scientific medicine with mumbo-jumbo." Trehan's response was characteristically sharp: "Western medicine treats disease; Eastern medicine treats the person. Why should Indians choose when they can have both?"

November 2009 marked the moment of truth. Medanta – The Medicity opened with 1,250 beds spread across 1.7 million square feet, making it one of the largest private hospitals in India. The inauguration was deliberately low-key—Trehan rejected suggestions for a Bollywood celebrity or political heavyweight to cut the ribbon. Instead, the first official patient was a carpenter from Rajasthan who needed heart surgery but couldn't afford it. Trehan operated on him for free, sending a clear message: excellence didn't mean exclusivity.

The early months were brutal. The daily cash burn was over ₹2 crores. The occupancy rate hovered around 30%. Insurance companies were reluctant to empanel a new hospital, even one with Trehan's name. Corporate clients wanted to see a track record. The sprawling campus felt empty, the state-of-the-art equipment underutilized. One financial advisor told Trehan bluntly: "You've built a Rolls-Royce in a market that wants Maruti Suzukis."

Then, six months after opening, Medanta handled its first major crisis: a multi-organ transplant requiring simultaneous coordination between cardiac, liver, and kidney teams. The 14-hour surgery succeeded. The patient—a prominent industrialist—became Medanta's most vocal ambassador. Word spread through Delhi's power corridors: Medanta wasn't just another hospital; it was a medical destination where the impossible became routine.

By the end of 2010, Medanta was performing surgeries that were firsts not just for India but for Asia: bloodless cardiac surgeries for Jehovah's Witnesses, robotic surgeries for prostate cancer, stem cell therapies for spinal injuries. The hospital that industry watchers had dubbed "Trehan's Folly" was suddenly being studied by McKinsey as a case study in healthcare innovation.

The foundation was set, but Trehan knew Medanta couldn't remain a single-location marvel. The real test would be whether this model—capital-intensive, technology-heavy, uncompromisingly excellent—could be replicated across India's heartland.

V. Expansion Playbook: Building a Healthcare Network

The conference room at Medanta Gurgaon in early 2012 looked like a war room. Maps of India covered every wall, marked with colored pins—red for Apollo hospitals, blue for Fortis, green for Max, and yellow for potential Medanta sites. Dr. Trehan stood before his leadership team with a simple question that would define the company's next decade: "Do we go deep in metros or wide in tier-2 cities?"

The conventional wisdom was clear: stick to metros where patients could pay, where insurance penetration was higher, where the Medanta brand already resonated. Apollo had conquered Chennai, Mumbai, and Delhi. Fortis dominated the satellite cities around the capital. But Trehan's analysis led to a contrarian conclusion. "The metros are bloodbaths of competition," he told his team. "But look at Lucknow—1.5 million people, not a single hospital with a liver transplant program. Look at Patna—every serious patient travels to Delhi or Vellore. That's where India's healthcare emergency really is."

The expansion strategy that emerged was counterintuitive: target state capitals of India's most underserved states, build massive facilities that could serve as regional hubs, and create centers of excellence that would make patient travel unnecessary. It wasn't about following the money; it was about following the mortality data.

Lucknow became the test case. The city of nawabs and kebabs had plenty of nursing homes and government hospitals, but nothing approaching international standards. In 2016, Trehan announced a 1,000-bed facility with a ₹1,000 crore investment—larger than many metros' biggest hospitals. Local competitors scoffed. "He's building a five-star hotel in a two-star market," one Lucknow hospital owner told the Times of India.

The Lucknow facility, which opened in 2019, wasn't just big—it was transformative. Trehan insisted on replicating every capability from Gurgaon: organ transplants, cardiac surgery, oncology, even a nuclear medicine department. But he also added something new: a partnership with local Unani medicine practitioners, acknowledging Lucknow's cultural heritage. The first month saw 40% occupancy. By month six, there were waiting lists for cardiac procedures.

The Patna expansion told a different story. Bihar, India's third-most populous state, had some of the country's worst health indicators. The Jay Prabha Medanta Super Specialty Hospital, inaugurated in 2021, represented a ₹500 crore bet that Biharis deserved the same healthcare as Mumbaikars. The 500-bed facility included Bihar's first comprehensive cancer center and its only pediatric cardiac surgery program.

But Patna also revealed the challenges of tier-2 expansion. Attracting talent was brutal—specialists commanded 40% premiums to relocate from metros. The payer mix was challenging, with 70% patients paying out-of-pocket versus 40% in Gurgaon. Supply chains were inefficient; critical equipment parts that took two days to reach Gurgaon took two weeks to reach Patna. Yet Trehan persisted, personally visiting Patna monthly, operating on complex cases to demonstrate that excellence was location-agnostic.

The Indore facility, opened in 2020, represented another strategic pivot: partnering with local business houses. The Choithram family, Indore's industrial dynasty, co-invested in the 1,000-bed hospital, providing not just capital but local credibility. This became the template for future expansions—find local partners who brought more than money.

Then came the most audacious announcement yet: a super-specialty hospital in Guwahati to serve the entire Northeast. The numbers seemed impossible—₹500 crores for 400 beds targeting a population that included some of India's poorest states. But Trehan's math was different. "Fifty million people in the Northeast currently fly to Mumbai or Delhi for tertiary care. If we capture just 5% of that, we're profitable from day one."

The Noida project, currently under construction, represents the evolution of Trehan's thinking. Located in India's most densely populated state, it's designed as Medanta's technology showcase: AI-powered diagnostics, robotic surgery suites, and India's first proton therapy center for cancer. The ₹2,000 crore investment makes it Medanta's most expensive project, but also potentially its most profitable, targeting the Delhi-NCR overflow and medical tourism from Nepal and Bangladesh.

Each expansion refined the playbook. Site selection followed a formula: state capital or major city, minimum catchment of 20 million people within 200 kilometers, weak existing competition, and state government support. The hub-and-spoke model emerged organically—each major hospital surrounded by diagnostic centers and clinics that could refer complex cases. By 2024, Medanta operated five major hospitals with 3,008 beds, supported by over 30 clinics.

But the expansion wasn't without casualties. A planned Ranchi facility faced land acquisition issues that delayed it by three years. The Nagpur project was scrapped after local political opposition. An ambitious plan for South India—starting with Bengaluru—was shelved after feasibility studies showed the market was already oversupplied.

The financial discipline behind the expansion was remarkable. Unlike Fortis's debt-fueled growth or Apollo's asset-light model, Medanta maintained a conservative debt-to-equity ratio, never exceeding 1.5x. Each new hospital was required to achieve operational break-even within 18 months and EBITDA positivity within three years. Those that didn't meet targets saw capital allocation frozen until performance improved.

By 2022, the network effects were becoming visible. A patient diagnosed with cancer at a Medanta clinic in Meerut could seamlessly transfer to Gurgaon for surgery, recover in Noida, and receive follow-up care back in Meerut—all within the same medical record system, under the same protocols, with the same quality standards. The company that started as one doctor's vision had become a healthcare network serving 100 million Indians.

VI. The IPO Story: Going Public in Turbulent Times

The Morgan Stanley presentation deck was compelling: 46 slides showcasing Medanta's journey from a single hospital to a healthcare network, revenue growth trending steadily upward, EBITDA margins that made investors salivate. It was early 2022, and Dr. Trehan sat across from investment bankers who were painting a rosy picture of the public markets. "This is your moment, Dr. Trehan," the lead banker said. "Healthcare IPOs are hot. The COVID bump in valuations is still there. You could raise ₹3,000 crores easily."

But 2022's market was anything but easy. The Russia-Ukraine war had just erupted. The Federal Reserve was hiking rates. Indian markets had corrected 15% from their peaks. Tech IPOs like Paytm and Zomato had burned investors. The window that looked wide open in January was rapidly closing by March. Yet Trehan, now 76, knew this wasn't really about market timing. It was about succession, about institutionalizing Medanta beyond its founder, about creating permanent capital for expansion.

The decision to go public triggered intense internal debates. The old guard—doctors and administrators who'd been with Trehan since Escorts—worried about quarterly pressures corrupting clinical decisions. Would they have to justify every expensive surgery to analysts? Would profit margins matter more than patient outcomes? Trehan's son-in-law, Pankaj Sahni, who'd married his daughter and joined as CEO, became the bridge between medical excellence and market expectations. "We're not changing who we are," Sahni told the medical staff. "We're just adding transparency to what we've always done."

The structuring of the IPO revealed careful thought. Of the ₹2,206 crores to be raised, only ₹500 crores was fresh capital for the company—earmarked for debt reduction and the Noida expansion. The remaining ₹1,706 crores was an offer for sale (OFS) by existing investors, including Avenue Capital's long-awaited exit and partial stakes from the Trehan family. This wasn't a desperate capital raise; it was a measured transition to public ownership.

The roadshow in October 2022 was unlike typical IPO presentations. While most healthcare companies led with financial metrics, Trehan insisted on starting with patient outcomes—survival rates, infection rates, readmission statistics. In a memorable moment at the Mumbai roadshow, when a fund manager asked about competition from Apollo, Trehan responded: "Apollo has 10,000 beds. We have 3,000. But check how many liver transplants we do versus them. Scale without excellence is just a bigger problem."

The price band of ₹319-336 per share valued Medanta at roughly ₹9,000 crores—rich but not unreasonable given ₹3,800 crores in revenue and 16% net margins. The institutional response was encouraging but cautious. Foreign investors loved the story but worried about single-founder risk. Domestic institutions appreciated the financials but questioned the tier-2 city strategy. The retail portion was where the real drama unfolded.

November 3, 2022—listing day. The pre-open session showed bids clustering around ₹380-390, nearly 20% above the issue price. When trading began at 9:15 AM, the first tick was ₹401—a 19.35% premium. Within minutes, volume exploded. The stock touched ₹425 before settling around ₹410. Market capitalization had jumped to ₹10,754 crores. In the Medanta boardroom, there was relief but not celebration. "The real test," Trehan told his team, "starts now."

The subscription data told the real story. The issue was oversubscribed 9.58 times overall—institutional portion 13.33 times, HNI portion 8.74 times, retail 3.29 times. Total bids received were for 44.79 crore shares against 4.67 crore offered. The message was clear: institutional investors saw Medanta as a long-term play on India's healthcare transformation.

What the IPO proceeds enabled was immediate and tangible. The ₹300 crores allocated for debt reduction dropped Medanta's interest costs by 40%, improving margins instantly. The ₹200 crores for Noida accelerated construction by six months. But more importantly, the public listing enforced discipline that even Trehan admitted was overdue—standardized procurement processes, formal board committees, quarterly medical audits that went beyond financial metrics.

The post-IPO performance validated the timing. Despite broader market volatility, Medanta's stock held steady, trading between ₹380-450 in its first year. Quarterly results showed consistent improvement—Q4 FY2023 saw 13% revenue growth and EBITDA margins expanding to 25.4%. The company announced a ₹4,000 crore capex plan for the next five years, funded entirely through internal accruals.

But the IPO also brought unexpected scrutiny. Analysts questioned why Medanta's revenue per bed was lower than Apollo's. Financial media dissected every quarterly variance. Short-sellers circulated reports about related-party transactions with the Trehan family's other ventures. The company that had operated in relative privacy for thirteen years was now under a microscope.

The institutional changes were profound. The board, previously dominated by Trehan loyalists, added three independent directors with deep healthcare and financial expertise. Quarterly earnings calls became tutorials in healthcare economics, with Pankaj Sahni patiently explaining why occupancy rates were less important than case mix, why ARPOB (average revenue per occupied bed) varied by geography, why medical equipment depreciation wasn't comparable to manufacturing assets.

By late 2024, with the stock trading at ₹850—up 150% from IPO—the public market experiment had clearly succeeded. Medanta had raised capital, achieved liquidity for early investors, and maintained its clinical standards. But more subtly, it had proven something important: Indian public markets were ready to value healthcare beyond just financial metrics, to appreciate the long-term nature of hospital investments, to back founders who prioritized purpose alongside profit.

VII. Clinical Excellence & Innovation Engine

The letter from Newsweek arrived on a humid August morning in 2020, when Medanta's leadership was deep in COVID crisis management. "Congratulations," it read. "Medanta has been ranked the second-best hospital in India and 132nd globally." In the Gurgaon boardroom, the reaction was mixed. Pride, certainly, but also classic Trehan perfectionism: "Who's first, and what are they doing that we're not?"

The rankings validated what insiders knew: Medanta had quietly built one of Asia's most sophisticated clinical programs. The cardiac unit, Trehan's obvious crown jewel, was performing procedures that most Indian hospitals wouldn't attempt—bloodless heart surgeries, pediatric heart transplants, minimally invasive valve repairs. But it was the other departments that truly showcased institutional depth.

Take the liver transplant program, headed by Dr. A.S. Soin, who Trehan had recruited from Sir Ganga Ram Hospital with an offer that included not just money but complete autonomy and unlimited investment in his department. By 2023, Medanta was performing 400+ liver transplants annually with survival rates exceeding 95%—better than most American centers. The program's innovation wasn't just clinical; Soin pioneered swap transplants, where incompatible donor-recipient pairs exchanged organs, effectively doubling the donor pool.

The cancer institute represented another leap. While Apollo and Fortis offered oncology services, Medanta built what Trehan called "cancer care without borders"—medical, surgical, and radiation oncology under one roof, with India's first CyberKnife for non-invasive tumor destruction. The institute's protocol was radical: every cancer patient's case was discussed by a tumor board of twelve specialists before treatment began. "We don't treat cancer," the marketing accurately claimed. "We treat cancer patients."

But clinical excellence at Medanta went beyond just advanced procedures. The infection control statistics were staggering: central line infection rates of 0.9 per 1,000 catheter days versus the Indian average of 7.2, surgical site infections at 0.8% versus 4.2% nationally. These weren't accidents but the result of obsessive protocols—UV robots disinfecting operating rooms between procedures, copper-infused surfaces that killed bacteria on contact, mandatory hand hygiene audits where even Trehan's compliance was tracked and posted publicly.

The research infrastructure set Medanta apart from pure clinical players. The Medanta Institute of Education and Research wasn't a token addition but a serious scientific enterprise. The tissue repository alone contained 50,000+ samples, enabling genomic studies that were yielding insights into why Indians developed diabetes and heart disease differently than Caucasians. By 2024, Medanta researchers had published 300+ papers in peer-reviewed journals—more than most Indian medical colleges.

Technology adoption at Medanta followed a simple principle: if it improved outcomes or patient experience, cost was secondary. The ₹40 crore spent on a 3-Tesla MRI seemed excessive until it enabled detection of brain tumors 2mm in size. The robotic surgery program—with four da Vinci systems costing ₹15 crores each—performed 2,000+ procedures annually with lower blood loss, faster recovery, and minimal scarring. The e-ICU system, monitoring 300 beds remotely from a central command center, reduced ICU mortality by 22%.

Medical tourism became an unexpected validator of clinical quality. By 2023, international patients—primarily from Africa, the Middle East, and Central Asia—contributed 18% of Medanta's revenues. These weren't price-sensitive medical tourists but outcome-focused patients who could afford treatment anywhere. The Nigerian oil executive who chose Medanta over Johns Hopkins for his liver transplant, the Kazakh minister who flew in for robotic cardiac surgery, the SAARC country heads of state who made Medanta their default medical destination—each was a testimony to clinical credibility.

The integration of traditional medicine, initially seen as Trehan's quirk, evolved into a differentiator. The Ayurveda and Integrative Medicine Centre wasn't offering token yoga classes but running serious clinical trials on traditional interventions. When their research showed that certain Ayurvedic preparations reduced chemotherapy side effects by 35%, it was published in the Journal of Clinical Oncology. Harvard Medical School sent residents to study Medanta's East-meets-West model.

Telemedicine, accelerated by COVID, became a permanent capability. Medanta's e-clinics reached 100,000+ patients annually across 15 states. But unlike basic teleconsultations, these were sophisticated interactions—radiologists reading scans in real-time, surgeons guiding procedures remotely, psychiatrists managing complex cases through video. The technology enabled Medanta quality to reach patients who'd never travel to their physical hospitals.

The air ambulance service, launched in 2019, epitomized Medanta's approach to innovation. While competitors outsourced medical evacuations, Medanta bought and retrofitted two aircraft as flying ICUs, staffed by critical care teams trained in aviation medicine. The service handled 500+ evacuations annually, from bringing accident victims to Gurgaon to transporting organs for transplant. Each flight lost money, but as Trehan noted, "It's not about profit; it's about completing the care continuum."

Quality metrics were obsessively tracked and transparently reported. Medanta published annual quality reports that most Indian hospitals wouldn't dare share—30-day mortality rates by procedure, hospital-acquired infection rates by department, patient satisfaction scores by doctor. The data sometimes showed Medanta trailing international benchmarks, but the transparency itself became a competitive advantage. "Patients trust us," Pankaj Sahni explained, "because we're honest about where we stand."

By 2024, Medanta's clinical programs weren't just matching international standards—they were setting them. The cardiac surgery program's bloodless surgery protocols were being studied at Mayo Clinic. The liver transplant program's swap model was being replicated across Asia. The infection control standards became the template for India's National Accreditation Board. The boy from Lucknow who'd gone to America to learn medicine was now teaching the world how healthcare could work in resource-constrained environments.

VIII. Challenges, Controversies & Competition

The news broke on a Sunday evening in December 2019, catching even Medanta insiders off guard. "Manipal-Medanta Merger Called Off," screamed the Economic Times headline. The deal—₹5,800 crores for Manipal Hospitals to acquire Medanta—would have created India's largest hospital chain, overtaking Apollo. For six months, investment bankers had worked eighteen-hour days, due diligence teams had camped in Gurgaon, and integration committees had mapped out synergies. Then, suddenly, it was dead.

The official reason was "valuation differences," but insiders knew the real story was more complex. Trehan, even at 73, couldn't stomach the idea of Medanta becoming just another division of a larger chain. During final negotiations, when Manipal executives presented plans to "standardize" Medanta's protocols with their other hospitals, Trehan reportedly stood up and said, "Gentlemen, you don't standardize excellence downward." The deal collapsed within 48 hours.

The failed merger highlighted Medanta's perpetual challenge: how to scale while maintaining standards that were, frankly, economically irrational. Competitors privately called Medanta's quality obsession "the Trehan Tax"—the 15-20% higher operating costs from protocols that seemed excessive. Did you really need to change surgical gloves between every procedure? Did infection control require UV robots that cost ₹50 lakhs each? Apollo and Fortis achieved 90% of Medanta's outcomes at 75% of the cost.

Competition had evolved from respectful rivalry to open warfare. Apollo, with 10,000+ beds, used scale to negotiate better insurance rates and equipment prices. Fortis, despite its promoter controversies, had rebuilt itself as the value-for-money option. Max Healthcare, post its private equity makeover, was aggressively poaching Medanta's doctors with 50% salary premiums. Even startups like Pristyn Care were nibbling at margins, offering simple surgeries at 40% of Medanta's prices.

The talent wars were particularly brutal. In 2021, Medanta lost its head of neurosurgery and three senior surgeons to Max in a single week. The packages offered were eye-watering—₹4 crores base salary plus performance bonuses that could double that. Medanta's response was hamstrung by its compensation philosophy: doctors were well-paid but not excessively so. "We want surgeons who are here for the mission, not the money," Trehan insisted. But missions don't pay for children's foreign education or Delhi farmhouses.

Then there were the controversies that came with scale. In 2020, during COVID's peak, a patient's family alleged negligence after their father died despite a ₹45 lakh bill. The video of relatives crying outside Medanta's gates went viral, with #MedantaMurder trending for three days. Investigations cleared Medanta of wrongdoing—the patient had arrived in critical condition—but the reputational damage was done. The incident exposed healthcare's uncomfortable truth: even the best hospitals can't save everyone, but social media doesn't do nuance.

Regulatory challenges multiplied with geographic expansion. Each state had different rules for hospital licensing, medical equipment imports, and doctor registrations. The Lucknow hospital faced a six-month delay because local authorities questioned why a private hospital needed a nuclear medicine department. The Patna facility was forced to reserve 40% beds for below-poverty-line patients at government rates—noble in principle, devastating for unit economics. Navigating India's healthcare bureaucracy required a full-time team of fifty people just for compliance.

The insurance ecosystem presented another battleground. Insurance companies, squeezed by COVID claims, turned aggressive on hospital billing. Medanta's claims rejection rate jumped from 5% to 15% between 2021-2023. Insurers questioned everything: why did a cardiac patient need a private room, why were antibiotics prescribed preventively, why did surgeries take longer than "standard" times? Each rejection meant either writing off lakhs in treatment costs or fighting patients' families for payment—both terrible options.

New-age competition was perhaps most threatening. Digital health platforms like Practo and Pharmeasy were commoditizing basic healthcare. Wellness chains like Cult.fit were redefining preventive care. International players were eyeing India—Cleveland Clinic was scouting locations, Johns Hopkins was exploring partnerships. Most ominously, corporate giants were entering healthcare. Reliance's announcement of Jio Health, promising "healthcare for every Indian," sent hospital stocks tumbling 10% in a day.

Internal challenges compounded external pressures. The founder's shadow loomed large—every major decision still needed Trehan's approval, creating bottlenecks. Succession planning was murky; while CEO Pankaj Sahni was competent, he lacked Trehan's gravitational pull. The second generation of leadership—department heads hired in Medanta's early days—were approaching retirement themselves. The culture that Trehan had painstakingly built showed signs of dilution as the organization grew from 1,000 to 10,000 employees.

Quality control at scale proved increasingly difficult. The Gurgaon flagship maintained exceptional standards, but newer facilities struggled. Patna's infection rates were double Gurgaon's. Lucknow's patient satisfaction scores lagged by 15 percentage points. The very protocols that defined Medanta were harder to enforce when Trehan couldn't personally oversee every department. "We're becoming what we swore we'd never be," one senior doctor confided, "just another hospital chain."

The competitive response was evolving. Trehan and his team recognized that Medanta couldn't compete on scale with Apollo or on price with Fortis. The strategy crystallized around "depth over breadth"—becoming so exceptional in select specialties that patients would travel any distance. The liver transplant program already achieved this. Could oncology, neurosurgery, and pediatrics follow? It was a high-risk strategy in a market increasingly dominated by generalists, but it was perhaps the only way to preserve what made Medanta special.

IX. Financial Architecture & Unit Economics

The spreadsheet on CFO Sanjeev Kumar's screen told a story of disciplined growth. Q4 FY2024 had just closed with ₹37,714 million in operating income—a 13% jump year-over-year. But the number that made investment bankers salivate was buried three rows down: EBITDA margin of 25.4%. In an industry where 15% was considered healthy and 20% exceptional, Medanta was printing money like a software company while running capital-intensive hospitals.

The margin magic wasn't accidental but architectural. Unlike Apollo's asset-light franchise model or Fortis's sale-and-leaseback financial engineering, Medanta owned everything—land, buildings, equipment. This meant massive upfront capital but also complete control over costs. "When you're paying ₹30 crores annually just in rent for a hospital, that's ₹30 crores that could go toward better doctors or equipment," Trehan had argued in early board meetings. The strategy required patience—Medanta's return on capital employed took five years to exceed 15%—but once the flywheel started spinning, the economics were compelling.

Revenue per bed told the real story. At ₹52 lakhs annually per bed, Medanta trailed Apollo's ₹65 lakhs and Max's ₹58 lakhs. But the composition mattered more than the quantum. Medanta's revenue came 60% from complex procedures—transplants, cardiac surgeries, cancer treatments—versus 40% for competitors. These procedures had 40-50% gross margins compared to 20-25% for routine operations. "We're not in the volume business," Sanjeev explained to analysts. "We're in the complexity business."

The payer mix was evolving fascinatingly. In 2019, the split was 50% cash, 30% insurance, 20% government schemes. By 2024, insurance had jumped to 45%, but the cash segment remained stubbornly high at 40%. The reason? International patients and wealthy Indians who preferred paying cash for privacy and priority. These cash patients, paying full rack rates, generated 60% margins. One Nigerian patient's liver transplant generated more profit than fifty insurance-covered appendectomies.

The ₹4,000 crore capex announcement in late 2023 raised eyebrows. In an era of asset-light everything, Medanta was doubling down on owned infrastructure. But the allocation revealed strategic thinking. ₹1,500 crores for the Noida facility—expected to generate ₹800 crores in annual revenue at maturity. ₹800 crores for medical equipment refresh—maintaining the technology edge. ₹700 crores for expansion at existing facilities—adding 500 beds without new hospitals. ₹1,000 crores for digital infrastructure and backward integration into diagnostics and pharmacies.

The unit economics of each hospital told different stories. Gurgaon, the flagship, operated at 85% occupancy with EBITDA margins exceeding 30%—essentially funding the entire network's expansion. Lucknow had turned EBITDA positive in month 14, ahead of the 18-month target. Patna struggled, with 55% occupancy and 12% margins, but was improving quarterly. The portfolio approach meant winners could subsidize investments in future winners.

Working capital management was a masterclass in healthcare finance. Despite the industry's notorious 90-day payment cycles from insurance companies, Medanta maintained a cash conversion cycle of 45 days. How? Aggressive follow-up on insurance claims, upfront deposits from international patients, and innovative financing schemes for cash patients. The company even launched its own medical credit card with HDFC Bank, offering zero-interest EMIs for procedures above ₹2 lakhs.

The procurement strategy balanced scale with quality. Medanta centralized purchasing for commodities—syringes, gloves, basic medicines—achieving 20-30% cost savings through bulk negotiations. But for critical equipment and specialized drugs, quality trumped cost. The pharmacy ran at just 8% margins, deliberately kept low to ensure doctors prescribed optimal rather than profitable medications. "Every percentage point of pharmacy margin comes from patient pockets," Trehan reminded finance teams pushing for higher markups.

Physician compensation models were uniquely structured. Unlike competitors who offered revenue shares or per-procedure payments, creating incentives for unnecessary treatments, Medanta doctors received fixed salaries plus quality-based bonuses. A cardiac surgeon earned bonuses for low infection rates, not high surgery volumes. This meant higher fixed costs—salary expenses were 35% of revenues versus 25% at competitors—but also aligned incentives with patient outcomes.

The digital investments, initially questioned by board members, were yielding unexpected returns. The ₹200 crore spent on electronic medical records and clinical decision support systems reduced medical errors by 30%, directly impacting malpractice insurance costs. The telemedicine platform, built for ₹50 crores, generated ₹180 crores in annual revenue with 70% margins. The e-ICU system, monitoring patients remotely, reduced ICU length of stay by 1.2 days, improving both outcomes and economics.

International operations contributed 18% of revenues but 28% of profits. These patients—African politicians, Middle Eastern businessmen, Central Asian elites—paid premium rates for guaranteed outcomes. Medanta maintained separate international patient wings with hotel-like amenities, Arabic and Russian translators, and dedicated relationship managers. The lifetime value of an international patient exceeded ₹50 lakhs, including initial treatment and follow-ups.

The balance sheet strength enabled strategic flexibility. With debt-to-EBITDA at 1.8x and interest coverage at 8x, Medanta could fund expansion through internal accruals while maintaining an acquisition war chest. The company held ₹800 crores in cash, earning criticism from aggressive investors but providing what Trehan called "the ability to move fast when opportunities arise."

By early 2024, with the stock trading at 28x P/E—premium to Apollo's 24x but discount to Max's 32x—markets were valuing Medanta's unique position: the quality of a boutique hospital with the scale of a chain, the margins of a specialty player with the resilience of a diversified portfolio. The financial architecture that seemed conservative in boom times proved antifragile in volatility.

X. Playbook: Lessons in Healthcare Entrepreneurship

The Harvard Business School case study on Medanta, published in 2023, opened with a provocative question: "Can excellence scale, or does scale inevitably dilute excellence?" The 40-page analysis dissected how Medanta had seemingly squared this circle, maintaining Mayo Clinic standards while expanding into Bihar. But the real insights came from the practices that weren't immediately visible—the organizational choices that compounded over decades.

Trust in healthcare, Trehan understood, wasn't built through advertising but through what he called "accumulated credibility." Every successful surgery created ambassadors. Every failed surgery, handled with transparency and compassion, paradoxically strengthened trust. When a minister's surgery went wrong in 2018, Medanta publicly released the entire case file, acknowledged the error, and implemented protocol changes. The minister's family, instead of suing, became vocal supporters. "We don't hide from failures," Trehan told his team. "We learn from them louder than anyone else."

The doctor-led versus corporate-led model debate raged across Indian healthcare. Apollo succeeded with professional managers. Fortis thrived (until it didn't) with financial engineers at the helm. Medanta chose a third path: doctor-leaders supported by professional management. Every major division was headed by a practicing clinician who spent 50% of their time seeing patients. "The moment our leaders stop being doctors," Trehan warned, "we become a real estate company with surgical facilities."

Geographic expansion strategy revealed sophisticated thinking about Indian healthcare consumption. While competitors fought over the eight metros, Medanta targeted what internal documents called "medical capitals"—cities that surrounding populations trusted for serious healthcare. Lucknow for Eastern UP, Patna for Bihar, Indore for Central India, Guwahati for the Northeast. Each location could draw from 100+ million people within a day's journey. The strategy required patience—these markets took longer to develop—but created regional monopolies in complex care.

The balance between clinical excellence and commercial viability was maintained through what Medanta called "portfolio theory." Every department didn't need to be profitable; the hospital needed to be profitable. Pediatric cardiac surgery lost money on every procedure, but parents whose children were saved became lifetime customers for the entire family. The liver transplant program was marginally profitable, but it attracted international patients who paid premium rates for everything else.

Technology adoption followed a counterintuitive principle: implement slowly but completely. While Apollo announced AI initiatives monthly, Medanta spent two years customizing a single clinical decision support system. But once implemented, adoption was mandatory, training was comprehensive, and results were measured obsessively. The robotic surgery program took eighteen months to launch but achieved 90% utilization within six months—versus industry averages of 40%.

The founder's reputation, typically a depreciating asset, was systematically institutionalized. Trehan's surgical videos became training materials. His patient interaction style was codified into communication protocols. His decision-making framework was documented in case studies. Young doctors didn't just work at Medanta; they were enrolled in the "Trehan School"—a formal mentorship program where senior surgeons transmitted not just technical skills but philosophical approaches to medicine.

Talent development went beyond conventional medical education. Medanta University, launched in 2021, wasn't another medical college but an innovation lab. Students—ranging from fresh graduates to senior doctors—worked on projects like reducing ICU costs by 30% without compromising outcomes, or designing surgical instruments for Indian body types. The best innovations were patented, with inventors receiving royalties. By 2024, Medanta held 47 patents, generating ₹12 crores in annual licensing fees.

The cultural architecture was deliberately designed. Every new employee, from surgeons to security guards, underwent a three-day orientation that included shadowing patient families, understanding treatment costs, and discussing medical ethics. The cafeteria, where Trehan ate daily, was deliberately designed to force interaction between departments. The monthly "mortality and morbidity" conferences, where failures were dissected, were mandatory for everyone, including administrators and board members.

Competitive differentiation evolved from claiming superiority to demonstrating specificity. Medanta didn't say it was better than Apollo; it published outcome data letting patients decide. The marketing tagline—"When it matters most"—acknowledged that routine healthcare could happen anywhere, but when lives hung in balance, expertise mattered. This positioning allowed premium pricing for complex procedures while avoiding price wars in commoditized services.

The financing innovation extended beyond traditional models. Medanta launched India's first "outcome-based pricing" for certain procedures—patients paid only if specific success metrics were met. The liver transplant program offered "success fee" structures where 30% of payment depended on one-year survival. Insurance companies initially resisted, then embraced these models as they aligned everyone's incentives.

Partnerships were selective and strategic. While competitors signed dozens of international collaborations for marketing value, Medanta maintained just three deep partnerships—with University of Southern California for liver transplants, with Duke for cardiac care, and with MD Anderson for oncology. Each partnership involved actual physician exchanges, joint research, and protocol development. "We don't collect logos," Pankaj Sahni explained. "We build capabilities."

The backward integration strategy was surgical in its precision. Medanta didn't try to manufacture everything but focused on critical dependencies. The pathology lab, processing 10,000 samples daily, ensured test results in hours not days. The pharmacy, stocking 8,000+ SKUs, guaranteed medication availability. The blood bank, with 500+ units always available, eliminated surgery delays. Each integration solved a specific bottleneck in patient care.

By 2024, the Medanta playbook had become required reading at healthcare conferences. But as Trehan reminded audiences, playbooks weren't recipes. "You can copy our protocols, buy our equipment, hire our people," he said at a recent conference. "But culture isn't copied; it's cultivated. And that takes decades, not quarters."

XI. Bear vs. Bull Case

The debate at the Morgan Stanley healthcare conference in Singapore was getting heated. On one side, a fund manager from Temasek argued Medanta was India's most undervalued healthcare asset. On the other, an analyst from a prominent short-seller made the case that Medanta was a "vanity project" that would struggle post-founder. The moderator turned to the audience: "Show of hands—who's bullish on Medanta?" The room split almost evenly.

The Bull Case: A Generational Opportunity

The demographics alone made bulls salivate. India's population over 60 would double to 300 million by 2050. Diabetes affected 77 million Indians, heart disease killed 2.5 million annually, cancer incidences were rising 8% yearly. Against this tsunami of demand, India had 0.65 doctors per 1,000 people versus WHO's recommended 2.5. The supply-demand imbalance wasn't closing; it was widening. Medanta, with its established brand and expanding footprint, was positioned to capture disproportionate value.

The insurance penetration story was even more compelling. Health insurance coverage had jumped from 15% in 2015 to 35% in 2024, still far below China's 95% or even Brazil's 70%. Every percentage point increase in insurance penetration meant ₹10,000 crores in additional healthcare spending. Government schemes like Ayushman Bharat, covering 500 million Indians, were game-changers. Medanta's early investments in insurance infrastructure—dedicated claim processing teams, standardized billing systems—positioned it to benefit more than competitors still dependent on cash patients.

Investment activity told its own story. Over the past 30 days, institutional investment in Medanta had surged 159.85%, indicating smart money's conviction. The investors weren't momentum traders but long-term players like Singapore's GIC, Canada's CPPIB, and Norway's sovereign wealth fund. These institutions had done deep diligence, met management multiple times, and stress-tested the business model. Their conclusion: Medanta at 28x P/E was cheaper than regional peers like IHH Healthcare (32x) or Bangkok Dusit (35x).

The moat was deepening, not shrinking. Training a liver transplant surgeon took 15 years. Building Medanta's reputation took 20 years. Replicating its protocols and culture would take a generation. Meanwhile, Medanta's medical outcomes data—50 million patient records—fed machine learning models that improved diagnosis and treatment. Every patient treated made Medanta smarter. This wasn't a business that internet startups could disrupt with an app and venture capital.

Geographic expansion into underserved markets was masterful positioning. While competitors fought over saturated metros, Medanta was building regional monopolies. In Lucknow, Patna, and soon Guwahati, Medanta wasn't competing; it was category-defining. These markets, with 200+ million people combined, had nowhere else to go for complex care. As income levels rose—UP's per capita income was growing 8% annually—these captive markets would generate decades of growth.

The international opportunity remained untapped. Medical tourism to India was worth $9 billion in 2024, projected to reach $20 billion by 2030. Medanta's 18% revenue from international patients could easily double. The weak rupee made Indian healthcare incredibly attractive—a liver transplant costing $200,000 in America cost $40,000 at Medanta with equal or better outcomes. As word spread through diaspora networks and government partnerships, Medanta could become the Mayo Clinic for emerging markets.

The Bear Case: Structural Challenges Ahead

The bear thesis started with an uncomfortable truth: hospitals were terrible businesses. Capital intensity was crushing—₹1,500 crores for a single hospital that took five years to reach full utilization. Return on capital averaged 12-15%, barely above India's cost of capital. Technology obsolescence was accelerating; the ₹40 crore MRI machine bought today would be outdated in seven years. Unlike software or pharmaceuticals, hospitals couldn't scale without proportional capital investment.

Regulatory risks were mounting, not declining. Government price controls on stents had decimated cardiac surgery margins. Similar controls on cancer drugs, joint implants, and dialysis were coming. State governments, facing budget pressures, were forcing private hospitals to treat subsidized patients at below-cost rates. The regulatory pendulum, having swung toward private healthcare for two decades, was swinging back toward populism.

Competition was intensifying from every direction. At the premium end, Cleveland Clinic and Johns Hopkins were entering India. At the value end, single-specialty chains like Narayana Health were performing cardiac surgeries at 20% of Medanta's cost. Digital health platforms were keeping patients away from hospitals entirely. Corporate hospitals faced the classic "stuck in the middle" problem—too expensive for mass market, not exclusive enough for ultra-wealthy.

Geographic concentration made Medanta vulnerable. With 60% of revenues from North India, any regional disruption—environmental crisis in Delhi, economic slowdown in UP, or political instability—would disproportionately impact Medanta. The South Indian expansion, critical for diversification, had been repeatedly postponed. Meanwhile, competitors were going national, spreading risk across geographies.

The founder dependency was existential. At 78, Dr. Trehan remained actively involved in major decisions. His reputation drove international patients. His relationships secured government contracts. His presence attracted top doctors. The succession plan, while existing on paper, hadn't been tested. CEO Pankaj Sahni was competent but lacked Trehan's gravitas. When Trehan eventually stepped back, would Medanta remain Medanta?

The talent crisis was structural, not cyclical. India produced 50,000 doctors annually, but only 5,000 specialists Medanta needed. These specialists had global options—America offered 10x salaries, Dubai provided tax-free income, Singapore promised better quality of life. Medanta's mission-over-money philosophy worked for Trehan's generation, but millennials doctors were different. The recent exodus to Max Healthcare was symptomatic of a deeper problem.

The numbers, while impressive, showed deceleration. Revenue growth had slowed from 18% (FY2021) to 13% (FY2024). New hospital ramp-ups were taking longer—Patna at 55% occupancy after three years versus Lucknow at 70% after two. EBITDA margins, while high at 25%, had plateaued. The core Gurgaon hospital, generating 40% of profits, was at maximum capacity. Future growth required massive capital investment with uncertain returns.

The Verdict

Both cases had merit, but the balance was shifting. The bull story of demographic tailwinds and insurance penetration was macroeconomically sound but would benefit all healthcare players. The bear concerns about capital intensity and competition were immediate and specific to Medanta. The investment decision ultimately came down to time horizon and risk tolerance. For patient capital seeking 15-20% IRRs over a decade, Medanta was compelling. For investors seeking quick returns or unable to stomach regulatory volatility, better opportunities existed elsewhere.

The most honest assessment came from Trehan himself at the last earnings call: "We're not building for the next quarter or even the next year. We're building for the next generation of Indians who'll need world-class healthcare. If you share that vision and patience, welcome aboard. If not, there are easier ways to make money."

XII. Future Vision & Strategic Options

The whiteboard in Medanta's strategy room was covered with arrows, boxes, and question marks. It was January 2024, and the leadership team was mapping out what they called "Medanta 3.0"—the next evolution beyond hospitals. Pankaj Sahni stood before the board, marker in hand: "We've mastered acute care. We've proven the model scales. The question isn't what we do next, but what we don't do. Every healthcare company eventually faces this choice: remain focused and risk irrelevance, or diversify and risk losing what makes you special."

Digital health represented the most obvious opportunity—and the most dangerous trap. The telemedicine platform, accelerated by COVID, was generating ₹180 crores annually with minimal capital investment. The temptation was to build "Medanta Digital"—a comprehensive health app offering everything from consultation to medicine delivery. But Trehan's skepticism was sharp: "We're doctors, not technologists. The moment we compete with Practo on their terms, we've lost." The compromise: selective digital investments that enhanced physical hospitals rather than replacing them. The AI-powered diagnostic tool that helped radiologists detect cancers 30% faster. The remote monitoring system that let Gurgaon specialists guide procedures in Patna. Digital as an amplifier, not an alternative.

The medical device opportunity was more intriguing. Medanta's surgeons constantly complained about equipment designed for Western body types—hip implants too large for Indian frames, stents optimized for Caucasian arteries. The biomedical engineering team had already developed seventeen innovations, from a low-cost ventilator during COVID to surgical instruments for minimally invasive procedures. The proposal: a ₹500 crore investment in Medanta MedTech, developing India-specific medical devices. The market was massive—₹90,000 crores and growing 15% annually. But it meant competing with Johnson & Johnson, Medtronic, and Siemens. "We'll start small," Sahni proposed. "Five products where we have unique insights. Build credibility before scaling."

Pharmaceuticals presented another adjacent opportunity. Medanta's pharmacy already formulated specialized compounds for organ transplants. The research team had identified three drug candidates from their tissue repository studies. But drug development meant 10-year timelines, ₹1,000 crore investments, and 90% failure rates. The board was split. The pragmatists wanted to license discoveries to pharmaceutical companies. The visionaries saw an opportunity to build India's first hospital-integrated pharmaceutical company. The decision was postponed, but the debate revealed fundamental tensions about Medanta's identity.

International expansion had reached an inflection point. The options were stark: build hospitals abroad, acquire existing facilities, or remain India-focused. Dubai had offered land for a 500-bed hospital catering to medical tourists. Nigeria's government wanted Medanta to manage three public hospitals. Bangladesh proposed a joint venture for Dhaka's first quaternary care center. Each opportunity was attractive individually but collectively would stretch management bandwidth and capital resources. Trehan's view was clear: "We haven't finished our work in India. Forty percent of Indians still lack access to basic healthcare, and we're dreaming of Dubai?"

The consolidation opportunity was heating up. India's hospital sector remained fragmented—the top ten chains controlled just 15% of beds. Smaller hospitals, struggling with COVID debt and competitive pressures, were seeking buyers. Medanta had identified twelve acquisition targets, from 200-bed specialty hospitals to 500-bed multi-specialty facilities. The rollup strategy was tempting: buy at 8-10x EBITDA, integrate operations, and achieve 15-20% returns. But acquisitions meant inheriting cultures, managing egos, and diluting the Medanta way. "We're builders, not buyers," Trehan insisted, though the board increasingly questioned whether organic growth alone was sufficient.

The preventive healthcare pivot was philosophical as much as strategic. Hospitals, by definition, treated sickness. But India's disease burden was increasingly preventable—diabetes from lifestyle, heart disease from diet, cancers from environment. The proposal: Medanta Wellness Centers offering comprehensive health assessments, lifestyle interventions, and preventive treatments. The economics were attractive—60% margins, asset-light, subscription-based revenues. But it meant competing with Cult.fit and traditional wellness players. More fundamentally, it challenged Medanta's identity as a tertiary care provider.

Succession planning loomed over every strategic discussion. Trehan, approaching 80, remained sharp but recognized his mortality. The transition plan had three phases: Trehan as Executive Chairman (current), Trehan as Non-Executive Chairman (2025-2027), and Trehan as Chairman Emeritus (2028 onwards). Pankaj Sahni would continue as CEO, but the real question was clinical leadership. The solution being crafted was innovative: a Council of Chiefs, where department heads collectively provided clinical governance. No single successor to Trehan, but a system that outlived any individual.

The next generation leadership was being systematically developed. Forty doctors under 40 had been identified as future leaders, enrolled in management programs at ISB and Wharton, and given P&L responsibility for departments. The Medanta Leadership Academy, launched in 2023, combined clinical excellence training with business education. The goal: create doctor-leaders who thought like entrepreneurs without losing clinical focus.

Technology infrastructure investment was accelerating. The ₹1,000 crore allocated for digital systems wasn't just IT spending but foundational capability building. Electronic health records that could integrate with any system. AI models that improved with every patient. Robotic systems that could be operated remotely. The vision: make Medanta's technology infrastructure so advanced that physical location became less relevant. A surgeon in Gurgaon operating on a patient in Guwahati through robotic systems. An AI diagnosing conditions before symptoms appeared. Healthcare delivered independent of geography.

The partnership strategy was evolving from bilateral to multilateral. Instead of one-off collaborations with international hospitals, Medanta was creating a Global Centers of Excellence Network—twenty hospitals worldwide sharing protocols, research, and talent. The network effect: a breakthrough in liver transplants at USC immediately benefited Medanta patients. A Medanta innovation in infection control helped hospitals in Vietnam and Kenya. Knowledge flowing multidirectionally, value created collectively.

By mid-2024, the strategic options had crystallized into three scenarios. The "Focus" scenario: double down on Indian hospitals, achieve 20% market share in complex care, and become India's undisputed clinical leader. The "Platform" scenario: build adjacent businesses leveraging Medanta's brand, from devices to digital, creating a healthcare conglomerate. The "Network" scenario: remain asset-light but orchestrate a global alliance of excellence-focused hospitals. Each path had different capital requirements, risk profiles, and cultural implications.

The decision wouldn't be made in boardrooms but in operating theaters, where Medanta's mission lived. As Trehan reminded his team: "Strategy is what we choose not to do. Our choices must honor why we exist—to save lives that others can't, to bring hope where none existed, to prove that excellence and accessibility aren't mutually exclusive. Everything else is just tactics."

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube