Dr. Agarwal's Health Care: The Eye Care Empire That Changed Indian Healthcare

I. Introduction & Cold Open

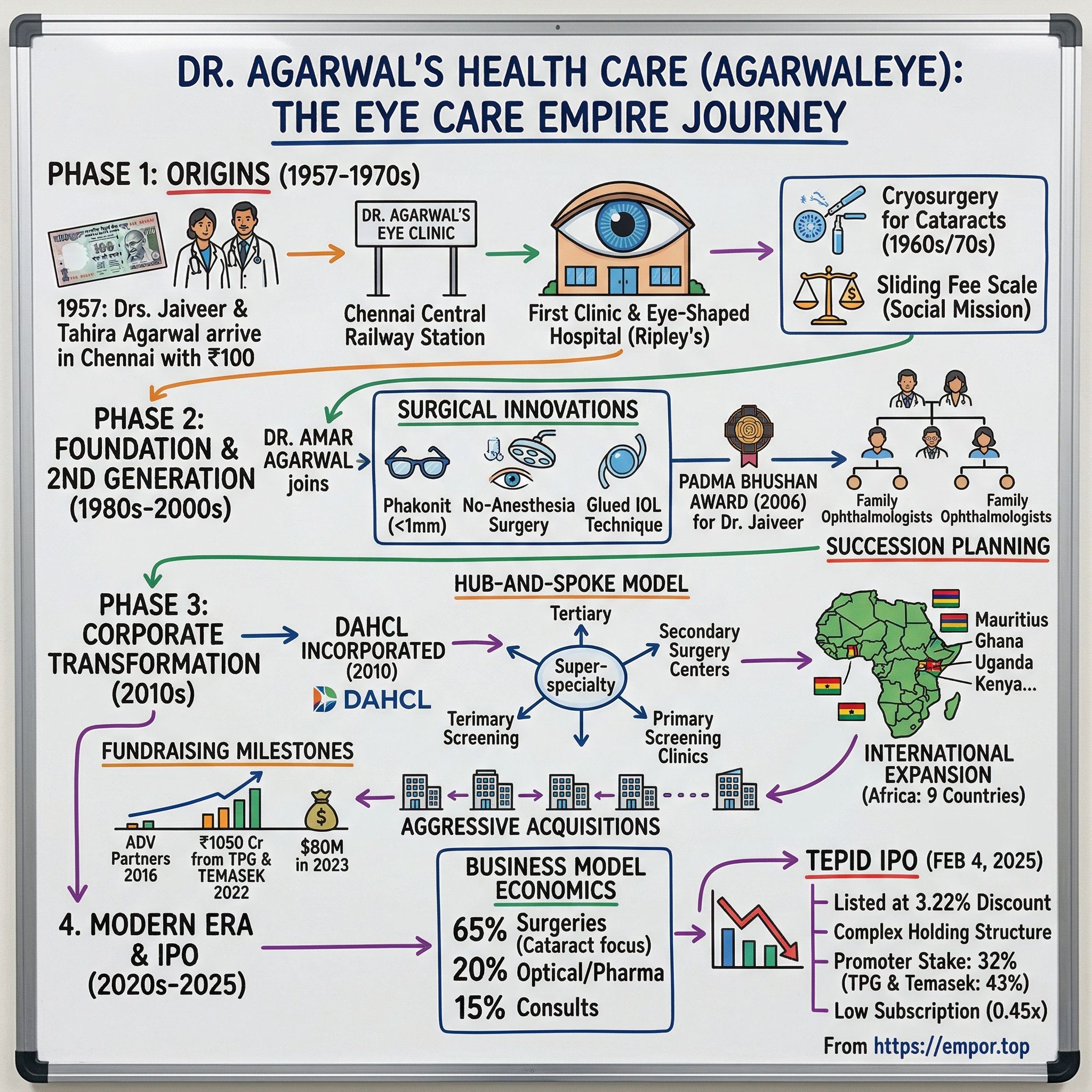

Picture this: It's 1957, and a young medical couple stands at Chennai Central Railway Station with exactly 100 rupees between them. They'd left Jaipur for a spiritual retreat at an ashram in Pondicherry, but something about the humid Chennai air, the bustle of Marina Beach, the energy of this southern metropolis captured their imagination. Dr. Jaiveer Agarwal turns to his wife, Dr. Tahira, and makes a decision that would reshape Indian healthcare: "Let's make this our home."

From that hundred-rupee moment would emerge India's largest eye care empire—a ₹14,000+ crore colossus that today commands 25% of the organized eye care market, operates across 13 Indian states and 9 African countries, and treats over 2 million patients annually. This is the story of Dr. Agarwal's Health Care Limited, a tale that weaves together medical innovation, family legacy, aggressive expansion, and the complex financial engineering that characterizes modern Indian healthcare.

What makes this story particularly fascinating isn't just the scale achieved—though performing 280,000+ surgeries annually is remarkable—but how a mission-driven medical practice transformed into a sophisticated healthcare platform that attracted TPG and Temasek as investors, executed a complex IPO structure with a listed subsidiary, and pioneered the hub-and-spoke model that's now become the playbook for healthcare delivery in emerging markets.

Over the next several hours, we'll unpack how the Agarwal family built this empire brick by brick, innovation by innovation. We'll explore the surgical breakthroughs that put them on the global map, the strategic decisions that enabled national scale, the international expansion that defied conventional wisdom, and yes, the curious case of why their IPO—despite the company's dominant position—received such a tepid market reception, listing at a 3.22% discount on February 4, 2025.

But more than a business story, this is a masterclass in building healthcare infrastructure in developing economies, balancing social mission with commercial viability, and navigating the transition from family-run institution to professionally managed corporation while somehow maintaining the original vision that started with two doctors and a hundred rupees.

II. The Origins: A Love Story Meets Medical Mission (1957-1970s)

The genesis of Dr. Agarwal's reads like a Bollywood script, except it's all true. Dr. Jaiveer Agarwal and Dr. Tahira first met at SMS Medical College in Jaipur—he, the son of renowned ophthalmologist Dr. R.S. Agarwal whose textbook on eye diseases carried a foreword by Prime Minister Lal Bahadur Shastri; she, a brilliant medical student with a passion for pediatric care. Their courtship unfolded between anatomy lectures and clinical rotations, culminating in a marriage that would become both a personal and professional partnership.

The spiritual journey to Pondicherry in 1957 was meant to be temporary—a young couple seeking guidance at Sri Aurobindo Ashram. But Chennai, then Madras, cast its spell during their transit. The city was experiencing a cultural and economic renaissance, positioning itself as the healthcare capital of South India. With their modest savings of 100 rupees and medical degrees as their only assets, they rented a small space on Nungambakkam High Road and hung a simple board: "Dr. Agarwal's Eye Clinic."

What distinguished their practice from dozens of other clinics wasn't just clinical excellence—it was their revolutionary approach to eye care accessibility. While established hospitals catered to the elite, the Agarwals instituted a sliding fee scale: full price for those who could afford it, subsidized rates for the middle class, and completely free treatment for the poor. This wasn't charity; it was a sustainable model where paying patients effectively sponsored free surgeries. The technical breakthroughs came early and decisively. Dr. Jaiveer introduced refractive keratoplasty with the Cryolathe and was the first to start cryoextraction in India in the 1960s—revolutionary techniques when most Indian surgeons were still using conventional methods. Think about the audacity: importing cutting-edge cryogenic equipment to Chennai when most hospitals couldn't afford basic surgical tools. Dr. Tahira wasn't far behind, becoming the first to introduce cryosurgery in the treatment of cataracts in India in 1967, establishing the couple as pioneers who brought Western surgical innovations to Indian shores before anyone else.

But the masterstroke—the moment that transformed them from respected doctors to medical celebrities—came on December 15, 1976. It was Dr. Jaiveer's concept of having an eye hospital in a human eye shape, and his wife Mrs. T. Agarwal transformed the concept into existence, which got recognized in the Ripley's Believe It or Not. The building itself became a tourist attraction, a marketing genius that predated modern healthcare branding by decades. Foreign delegations visited not just to learn surgical techniques but to photograph this architectural marvel. The establishment of the Eye Research Center (ERC) in 1978 represented a formalization of their social mission. The ERC conducted over 60 eye camps per month, performing approximately 1,000 cataract surgeries for low-income individuals. Patients from remote villages were provided transportation, accommodation, and meals as part of the initiative. This wasn't just charity—it was a sophisticated system where urban hospitals subsidized rural care, creating what would later become the template for healthcare delivery in developing nations.

The couple's complementary skills were crucial. Dr. Jaiveer introduced refractive keratoplasty with the Cryolathe and was the first to start cryoextraction in India in the 1960s, while Dr. Tahira was the first to introduce cryosurgery in the treatment of cataracts in India in 1967. Together, they weren't just practicing medicine; they were revolutionizing it, bringing techniques from London's Moorfields and American institutes to Chennai's humid streets.

By the late 1970s, the Agarwals had built something unprecedented: a medical institution that was simultaneously cutting-edge and accessible, profitable yet philanthropic, local but with global recognition. The foundation was set for what would become one of India's most remarkable healthcare expansion stories.

III. Building the Foundation: Second Generation Takes Charge (1980s-2000s)

The transition from founders to second generation is where most family businesses falter, but for the Agarwals, it marked an acceleration. Dr. Amar Agarwal, born in 1960, didn't just inherit a hospital—he inherited a mission and transformed it into a movement. After completing his MBBS from Madras Medical College and MS from Ahmedabad, he pursued FRCS from Edinburgh and F.R.C.Ophth from London, returning with not just degrees but a vision to make Dr. Agarwal's a global name in ophthalmology.

The 1980s and 1990s saw the organization evolve from a Chennai-centric institution to a regional powerhouse. But expansion wasn't just about opening new centers—it was about pushing surgical boundaries. The family developed what would become their signature innovations: phakonit sub-1-mm cataract surgery, no-anesthesia cataract surgery, and the glued intraocular lens (IOL) technique. Each innovation addressed specific challenges in the Indian context—smaller incisions meant faster recovery for patients who couldn't afford extended hospital stays; no-anesthesia procedures reduced costs and complications.

Dr. Jaiveer's leadership positions included President of the All India Ophthalmological Society (AIOS) in 1992, President of the Tamil Nadu Ophthalmic Association, and President of the Madras City Ophthalmological Association. These weren't ceremonial roles—they positioned the Agarwals at the center of Indian ophthalmology's policy and practice evolution.

The institutional recognition started pouring in. Dr. Jaiveer received the Padma Bhushan in 2006, awarded by A.P.J. Abdul Kalam for his outstanding service in the field of medicine. But personal accolades were secondary to systemic impact. During his tenure at AIOS, he advocated for custom duty exemptions on ophthalmic instruments, making advanced eye care technologies more accessible to doctors across India.

What made this period remarkable wasn't just growth—it was the maintenance of quality at scale. While competitors either remained boutique practices or diluted quality for volume, the Agarwals found a third way: standardized excellence. They developed protocols that could be replicated, training programs that could scale, and a brand that meant the same thing whether you walked into their Chennai flagship or a satellite center in rural Tamil Nadu.

The family structure itself evolved during this period. Dr. Amar married Dr. Athiya Agarwal, also an ophthalmologist trained at Moorfields. Their sons—Dr. Adil and Dr. Anosh—along with Dr. Amar's adopted nephews Dr. Ashvin and Dr. Ashar (sons of his sister Dr. Sunita), all became ophthalmologists. This wasn't nepotism; it was strategic succession planning. Each family member brought specialized expertise: cornea, retina, refractive surgery, creating an internal brain trust that could tackle any ophthalmological challenge.

In April 2009, Dr. Tahira Agarwal died. Following her death, Dr. Jaiveer's health declined, and he died on November 15, 2009, at the age of 79. His corneas were donated, restoring sight to two individuals, in line with his lifelong advocacy for eye donation. The founders' passing marked not an end but a transformation—from a founder-led institution to a professionally managed healthcare platform ready for its next phase of growth.

IV. The Modern Transformation: From Family Business to Corporate Healthcare (2010-2020)

The incorporation of Dr. Agarwal's Health Care Limited in 2010 wasn't just a legal formality—it was a strategic inflection point. The family recognized that to achieve their vision of accessible eye care across India and beyond, they needed institutional capital, professional management, and scalable systems. What followed was one of the most ambitious healthcare expansions in Indian history.

The international expansion strategy was counterintuitive. While peers targeted wealthy Middle Eastern markets or developed Western countries, Dr. Agarwal's went to Africa. Starting with Mauritius in 2012, they expanded to Ghana, Uganda, Kenya, Madagascar, Tanzania, Rwanda, Zambia, and Mozambique. The logic was compelling: these markets had similar disease profiles to India, comparable price sensitivity, and massive unmet demand. More importantly, the Indian medical degree carried prestige in these markets, and the Agarwal name already had recognition through medical journals and conferences. The hub-and-spoke model became their signature innovation. Instead of building expensive super-specialty hospitals everywhere, they created a network of primary facilities for diagnosis, secondary facilities for routine surgeries like cataracts, and tertiary facilities as super-specialty centers. This wasn't just cost-effective—it was revolutionary for healthcare delivery in India, where 70% of the population lives in tier-2 and tier-3 cities without access to quality eye care.

The funding journey tells a story of increasing institutional sophistication. After the first round in July 2012, the company attracted ADV Partners in 2016, which committed $45 million. But the game-changer came in May 2022 when Dr. Agarwal's Health Care Ltd. (DAHCL) closed a landmark fund raise of ₹1,050 crore from TPG Growth and Temasek. This was followed by another $80 million from existing investors Singapore's Temasek and U.S.-based TPG in August 2023.

What attracted these blue-chip investors wasn't just the numbers—though the company notched a revenue of over ₹700 crores in FY22—but the scalability of the model. The new investments will enable us to double our network in the next 3 years and we will be pursuing acquisitions in key markets such as Maharashtra, Gujarat, Punjab, Karnataka, AP, Telangana, Dr. Adil Agarwal announced, signaling aggressive expansion plans.

The acquisition strategy was surgical in its precision. Instead of random opportunistic buys, they targeted specific geographies where they lacked presence, acquiring established players with local brand equity. The 2017 acquisition in Maharashtra, 2022 in Gujarat, Punjab Eye Hospital in 2023, and the eye care business in Varanasi and Dr Thind Eye Care Private Limited in Punjab in 2024 weren't just about adding facilities—they were about acquiring local knowledge, relationships, and regulatory clearances that would have taken years to build organically.

Technology adoption during this period was transformative. They weren't just buying equipment; they were pioneering techniques. The development of glued IOL technique, where an intraocular lens is fixated using tissue glue instead of sutures, addressed a critical challenge in developing markets where follow-up care is difficult. Similarly, their no-anesthesia cataract surgery reduced both costs and risks, crucial for elderly patients with multiple comorbidities.

The African expansion deserves special attention. Africa is another important geography for us where we have an existing network presence of 15 hospitals. Operating in countries like Kenya, Uganda, and Ghana presented unique challenges—currency volatility, regulatory complexity, infrastructure deficits. But it also offered massive opportunities: untapped markets, minimal competition, and the ability to charge premium prices for Indian medical expertise.

By 2020, Dr. Agarwal's had transformed from a regional player to a national champion with international presence. The company was treating over 2 million patients annually, performing 280,000+ surgeries, and had built a brand that meant quality eye care across socioeconomic strata. The stage was set for the next phase: going public.

V. The Financial Engineering & IPO Story (2024-2025)

The path to the IPO reveals the complex financial architecture that modern healthcare companies must navigate. When Dr. Agarwal's Health Care Limited filed its draft red herring prospectus in September 2024, it unveiled a structure that would puzzle even seasoned investors: a holding company going public while its subsidiary, Dr. Agarwal's Eye Hospital, was already listed on the BSE with a market cap of ₹2,250 crore. The IPO structure itself was telling: ₹3,027.26 crore consisting of fresh issue of ₹300 crore and OFS of ₹2,727.26 crore. In other words, 90% of the proceeds would go to selling shareholders—primarily TPG and Temasek looking to partially exit—rather than to the company for growth. This immediately raised eyebrows among institutional investors who prefer IPOs where capital goes toward expansion rather than exits.

The pre-IPO shareholding structure revealed the transformation from family business to institutionally owned entity. Promoter holding of only 38% pre-IPO dropping to 32% post-IPO signaled that the founding family had already ceded control to financial investors. TPG and Temasek together held 43% of the company, making them the effective controllers. This wasn't necessarily negative—professional investors often bring discipline and governance—but it meant the company was already operating more like a private equity portfolio company than a founder-led enterprise.

The subsidiary conundrum added another layer of complexity. Dr. Agarwal's Eye Hospital, already listed on BSE with market cap of ₹2,250 crore, was contributing 70% of the parent's H1FY25 PAT. The subsidiary was trading at PE of 40x while the parent IPO was priced at double that PE multiple—around 91x forward earnings. Investors struggled to understand why they should pay twice the valuation for essentially the same underlying business wrapped in a holding company structure. The market debut on February 4, 2025, validated the skeptics. Dr Agarwal's Health Care shares listed at Rs 396.90 apiece on the BSE, a discount of Rs 5.10 or 1.27 per cent against its allotment price of Rs 402. On the National Stock Exchange (NSE), the company's shares listed flat at Rs 402, the same as the IPO allotment price. The tepid reception wasn't surprising given the subscription data: the IPO was subscribed only 0.45 times overall, with QIBs—the smart money—showing only 1.01 times subscription.

What went wrong? The timing was partly to blame—healthcare stocks were trading at elevated valuations, and investors were becoming selective. But the fundamental issue was the structure. With 90% of proceeds going to selling shareholders, investors saw limited upside for the company itself. The high valuation multiple of 91x forward PE versus 44-55x for hospital peers made it even harder to justify, especially when the simpler, cleaner subsidiary was available at half the valuation.

The post-IPO shareholding pattern revealed the new reality: promoters holding just 32%, TPG and Temasek with 43%, and public shareholders with 25%. This wasn't the founder-led growth story that Indian markets typically reward with premium valuations. It was a mature, institutionally controlled business being offered at growth-stage prices.

The IPO's failure to generate excitement marked a turning point in how markets view complex healthcare structures. Investors had become sophisticated enough to see through financial engineering and demand clarity, growth capital deployment, and reasonable valuations. Dr. Agarwal's, despite its operational excellence and market leadership, learned that even the best businesses need the right financial structure to succeed in public markets.

VI. Business Model Deep Dive: The Economics of Eye Care

Understanding Dr. Agarwal's business model requires appreciating the unique economics of eye care in India. Unlike general hospitals that require massive infrastructure and diverse specializations, eye care offers focused, high-volume, predictable procedures with excellent margins—if executed correctly. The company's position as India's largest eye care service chain with 25% market share wasn't accidental but the result of deliberate strategic choices in how they structured operations.

The network scale is staggering: 209 facilities as of September 2024, serving 1.15 million patients and performing 140,787 surgeries in just six months. But raw numbers don't tell the story—it's the hub-and-spoke architecture that creates the economic moat. Primary facilities handle initial diagnosis and clinical investigations with minimal capital investment. Secondary facilities focus on high-volume cataract surgeries—the bread and butter of Indian ophthalmology. Tertiary facilities serve as super-specialty centers for complex procedures, training, and research.

The revenue mix reveals the business priorities: 65% from surgeries (mainly cataract), 20% from optical and pharma products, and the balance from consultations. Cataract surgery dominates because it combines massive demand (India has the world's largest backlog of cataract cases), standardized procedures (enabling efficiency), insurance coverage (making it accessible), and good margins (especially with premium intraocular lenses).

But here's where the model gets interesting: the company doesn't just perform surgeries—it controls the entire value chain. Patients diagnosed at primary centers are referred to secondary facilities for surgery, then purchase post-operative medications and follow-up care from the same network. This isn't predatory; it ensures continuity of care, a critical factor in surgical outcomes. The optical retail business, often dismissed as low-margin, actually serves as a customer acquisition channel, bringing in patients who might need surgical intervention later.

The three-tier facility structure deserves deeper analysis. Primary facilities are essentially screening centers—low capex, high footfall locations in residential areas that identify patients needing intervention. These feed into secondary facilities optimized for volume: standardized operating theaters, assembly-line efficiency, economies of scale in procurement. Tertiary facilities handle complex cases but more importantly, they build the brand. When Dr. Agarwal's performs a complex retinal surgery that others can't, it enhances the reputation of even the smallest primary center in the network.

Financial performance tells a story of scale meeting efficiency challenges. FY24 revenue of ₹1,332.15 crore with net profit of ₹95.05 crore seems healthy until you examine the margins. The 7.1% net margin significantly lags competitors like Narayana Hrudayalaya (12-14%) or Apollo Hospitals (8-10%). The culprit? Depreciation and lease costs of ₹266 crore—20% of revenue versus 8% for other hospital chains.

This margin pressure isn't just about real estate costs. The hub-and-spoke model requires significant infrastructure investment upfront, with utilization building gradually. A new secondary facility might operate at 30% capacity in year one, 50% in year two, only reaching optimal utilization by year three. During this ramp-up, fixed costs remain constant while revenues grow slowly, pressuring margins.

The company's response has been to accelerate utilization through aggressive pricing and package deals. A cataract surgery package including pre-operative assessment, surgery, lens, medications, and follow-up might be priced at ₹25,000—competitive enough to attract volume while maintaining gross margins. But this strategy has limits; beyond a point, price competition erodes brand premium and attracts less desirable patient segments who might default on payments or require more intensive post-operative care.

The international operations add another dimension to the economic model. African facilities operate on different economics: higher prices (2-3x Indian rates), lower volumes, but better margins due to less competition and premium positioning. These operations contribute disproportionately to profitability despite representing less than 10% of facilities. More importantly, they provide a natural hedge against Indian regulatory changes or economic downturns.

Technology adoption represents both opportunity and challenge. Advanced diagnostic equipment like OCT scanners or surgical systems like femtosecond lasers require significant capital investment but enable premium pricing. The company's strategy has been selective adoption—tertiary centers get cutting-edge technology to maintain clinical leadership, while secondary centers focus on proven, cost-effective solutions.

The human capital model is perhaps the most underappreciated aspect. Unlike general hospitals that need diverse specialists, eye hospitals can focus recruitment and training on a single specialty. The company operates its own training programs, creating a pipeline of ophthalmologists and optometrists aligned with its protocols and culture. This reduces recruitment costs, ensures quality control, and creates switching costs for doctors who've been trained in proprietary techniques.

But the model has inherent limitations. Eye care, while essential, is often postponable—patients can delay cataract surgery for months or years. This makes demand elastic to economic conditions. The elective nature of many procedures also means competition from smaller players who can cherry-pick profitable procedures without maintaining the full infrastructure.

VII. The Competitive Landscape & Market Dynamics

The Indian eye care market presents a paradox: massive unmet need alongside intense competition. With the market projected to reach ₹550-650 billion by FY28, growing at 12-14% CAGR, every player from neighborhood clinics to international chains wants a piece. Yet Dr. Agarwal's 25% market share in organized eye care makes them the undisputed leader—a position that's both enviable and precarious.

The competitive landscape resembles a pyramid. At the base are thousands of individual practitioners and small clinics, handling routine cases and referrals. The middle tier includes regional chains like Centre for Sight, Eye-Q, and ASG Eye Hospitals—focused players with 10-50 centers each. At the apex sit integrated healthcare providers like Apollo and Fortis, for whom ophthalmology is one specialty among many. Dr. Agarwal's unique position—the scale of Apollo with the focus of a specialty chain—gives them advantages neither pure-play specialists nor diversified hospitals can match.

Centre for Sight, their closest competitor, operates on a franchise model that enables rapid expansion but sacrifices quality control. Eye-Q focuses on tier-2 and tier-3 cities with a low-cost model but lacks the clinical credibility for complex procedures. ASG Eye Hospitals, backed by private equity, is aggressively acquiring regional players but faces integration challenges. Each competitor has chosen a different vector to compete—geography, price, or specialty focus—but none match Dr. Agarwal's comprehensive approach.

The geographic distribution tells its own story. While competitors cluster in metro cities where patients can pay premium prices, Dr. Agarwal's has systematically built presence across Tamil Nadu, Karnataka, Kerala, Andhra Pradesh, Telangana, and beyond. This isn't just about capturing market share; it's about building density. In Tamil Nadu, they operate 85 facilities—enough that most residents are within 30 minutes of a Dr. Agarwal's center. This density creates network effects: brand recognition, referral patterns, operational efficiencies that new entrants can't replicate. The market dynamics are equally compelling. In May 2022, India's Union Health Minister stated the country requires 49 lakh surgeries to clear the backlog of blindness due to cataract and 53.63 lakh surgeries are needed to clear the backlog of severe visual impairment due to cataract. This represents not just unmet demand but a moral imperative that shapes government policy and funding. The National Programme for Control of Blindness channels significant resources toward eye care, creating a dual market: government-funded mass programs and private-pay premium services.

Technology disruption looms large but hasn't materialized as quickly as predicted. Telemedicine for initial consultations, AI-powered diagnostics, and robot-assisted surgery all promise to reshape the landscape. Yet adoption remains slow. The reason? Eye care, particularly surgery, remains intensely personal. Patients want to look their surgeon in the eye (pun intended) before trusting them with their vision. Dr. Agarwal's has navigated this by adopting technology selectively—using AI for screening in rural camps while maintaining the human touch in surgical consultations.

The insurance penetration story adds another layer. Currently, less than 30% of eye surgeries are insurance-covered, keeping the market largely cash-based. This has advantages—no insurance delays, no claim rejections, immediate treatment decisions. But as insurance penetration increases, especially through government schemes like Ayushman Bharat, the dynamics will shift. Hospitals will need to manage insurance relationships, accept lower negotiated rates, and handle longer payment cycles.

International competition hasn't materialized as feared. Despite India's reputation for medical tourism, international chains have struggled to establish meaningful presence in eye care. The reasons are instructive: eye care doesn't lend itself to medical tourism (patients want follow-up care close to home), the procedures are already affordable in India, and local players have world-class capabilities. Dr. Agarwal's international expansion into Africa flips this dynamic—they're the ones taking Indian expertise abroad.

The rise of specialty segments creates new competitive vectors. While cataract remains the volume driver, growth areas like refractive surgery (LASIK), glaucoma management, and diabetic retinopathy treatment offer higher margins and patient stickiness. Dr. Agarwal's comprehensive approach allows them to capture patients across the spectrum, but focused competitors can cherry-pick profitable segments without the overhead of full-service infrastructure.

Perhaps most interesting is the emergence of new business models. Subscription-based eye care (annual fees for unlimited consultations), corporate wellness programs, and preventive screening packages are reshaping how eye care is packaged and sold. Dr. Agarwal's, with its vast network, is well-positioned to capitalize on these trends, but nimbler startups might move faster in specific niches.

VIII. Playbook: Lessons in Healthcare Empire Building

The Dr. Agarwal's story offers a masterclass in building healthcare empires in emerging markets, with lessons that transcend ophthalmology or even healthcare. The playbook they've written—consciously or through evolution—provides a template for ambitious healthcare entrepreneurs worldwide.

Lesson One: Start with Mission, Scale with Systems

The founding vision of affordable, accessible eye care wasn't just marketing—it became the organizing principle that guided every decision. When you're clear on mission, choices become easier: enter underserved markets even if less profitable initially, maintain free surgery quotas even during expansion phases, invest in training programs that benefit competitors. This mission-first approach paradoxically enabled massive scale because it built trust, attracted talent, and justified premium pricing for those who could afford it.

Lesson Two: The Hub-and-Spoke Model as Competitive Advantage

While others built monolithic hospitals, Dr. Agarwal's distributed model created multiple advantages. Capital efficiency (smaller investments per location), market penetration (presence in neighborhoods), operational flexibility (easy to close underperforming units), and risk distribution (no single point of failure). The model also enabled rapid expansion—opening a primary center requires 1/10th the investment of a full hospital but captures similar patient flow.

Lesson Three: Family Business to Professional Management—The Delicate Transition

The evolution from Dr. Jaiveer's personal practice to institutionally-backed corporation required careful navigation. The family retained clinical leadership and brand custodianship while ceding operational control to professionals. Having multiple family members as doctors helped—they could maintain influence through expertise rather than just ownership. The key was recognizing that different growth stages require different leadership styles and being willing to adapt.

Lesson Four: International Expansion into Similar Markets

While peers chased developed markets for prestige, Dr. Agarwal's went to Africa—markets with similar disease profiles, price sensitivity, and infrastructure challenges. This wasn't just easier; it was smarter. The learnings from serving rural Tamil Nadu translated directly to Kenya or Uganda. The clinical protocols developed for high-volume, low-cost surgery in India worked perfectly in African markets starved for quality healthcare.

Lesson Five: Acquisition as Capability Building, Not Just Expansion

Each acquisition brought something beyond facilities: Maharashtra brought corporate relationships, Gujarat brought insurance expertise, Punjab brought agricultural community connections. This wasn't random M&A but strategic capability acquisition. The lesson: in fragmented markets, consolidation isn't just about scale but about acquiring local knowledge, relationships, and market positions that would take years to build organically.

Lesson Six: Managing High-Skill Workforce at Scale

With over 400 ophthalmologists across the network, talent management becomes critical. The company's approach—internal training programs, standardized protocols, performance-based incentives, and career progression paths—created a system where individual excellence could thrive within institutional frameworks. The creation of centers of excellence where complex cases are handled by super-specialists while routine procedures are standardized across the network balanced quality with efficiency.

Lesson Seven: Technology as Enabler, Not Replacement

Despite pioneering surgical techniques, the company resisted the temptation to over-technologize. They understood that in healthcare, especially in emerging markets, technology must enhance human capability, not replace it. The group has developed globally-adopted procedures like glued intraocular lenses (IOL), pinhole pupilloplasty, and PDEK—pre-Descemet's endothelial keratoplasty. "PDEK allows us to use just 25 microns of corneal tissue instead of the full 600 microns," Dr. Agarwal explains. This philosophy guided selective adoption: AI for screening where doctor availability is limited, but maintaining human interface for surgical consultations.

Lesson Eight: Building Moats in Commodity Businesses

Cataract surgery could be commoditized—standardized procedure, predictable outcomes, price-based competition. Dr. Agarwal's built moats through brand (trust in eye care), network effects (referral patterns once established are hard to break), operational excellence (lower costs through scale), and clinical innovation (proprietary techniques that differentiate outcomes). The lesson: even in seemingly commoditized healthcare segments, sustainable differentiation is possible through systematic excellence.

IX. Bear vs. Bull Case Analysis

The Bull Case: Demographic Destiny Meets Operational Excellence

The optimistic view starts with undeniable demographic trends. India's aging population will double by 2040, and with age comes cataracts—it's not if but when. With the current backlog of 49 lakh cataract surgeries, plus annual additions, the demand pipeline stretches decades into the future. Dr. Agarwal's, with 25% market share and unmatched distribution, stands to capture disproportionate value from this growth.

Scale advantages compound over time. Each new facility makes the next one cheaper to open (standardized designs, bulk procurement, trained staff pipeline). Each additional surgery improves protocols and reduces costs. The network effects are powerful: more locations mean more convenience for patients, more referrals between facilities, better negotiating power with suppliers, and stronger brand recognition. Competitors starting today would need decades to replicate this infrastructure.

The international opportunity remains vastly underpenetrated. With a population of 1.5 billion and healthcare access challenges similar to India's, the continent has emerged as a key focus area for the group's international growth. "Africa and India together represent half the world's population," he notes. If they can achieve even 5% of their Indian scale in Africa, it would double the company's addressable market.

Technology adoption could drive margin expansion. As AI-powered diagnostics reduce the need for ophthalmologists in routine screening, and surgical robots improve precision while reducing training requirements, the company's vast network becomes a platform for deploying these innovations at scale. They have the patient volume to justify investments that smaller players cannot make.

The brand value, built over 67 years, cannot be replicated quickly. In healthcare, trust is everything. When three generations of a family have been treated at Dr. Agarwal's, that relationship represents switching costs that no amount of marketing spend can overcome. This brand equity enables premium pricing for advanced procedures while maintaining volume through trust-based referrals.

The Bear Case: Structural Challenges in a Fragmenting Market

The pessimistic view starts with valuation. Trading at 91x forward PE versus 44-55x for hospital peers prices in perfection. Any execution stumble, regulatory change, or competitive pressure could trigger significant multiple compression. The complex holding structure with a listed subsidiary adds governance concerns and limits institutional investor interest.

Low promoter holding (32% post-IPO) creates overhang risk. TPG and Temasek, sitting on significant gains, might look to exit as lock-ups expire, creating sustained selling pressure. Without founder control, the company becomes vulnerable to competing visions between financial investors focused on returns and the founding family focused on legacy.

The margin structure remains concerning. Revenue from operations increased from Rs 696.08 crore in FY22 to Rs 1,017.98 crore in FY23 to Rs 1,332.15 crore in FY24. But PAT margins of 5-7% versus mid-teens for competitors suggest structural inefficiencies. High lease costs from rapid expansion, depreciation from equipment investments, and the burden of maintaining presence in unprofitable locations for network completeness all pressure profitability.

Competition is intensifying from unexpected directions. Pharmacy chains like Apollo Pharmacy are adding eye care services. E-commerce players enable price comparison and direct-to-consumer sales of optical products. Telemedicine platforms offer consultations without physical infrastructure. While none threaten the core surgical business immediately, they erode the peripheral revenues that support network economics.

The human capital challenge grows acute with scale. The 12.52% attrition rate in FY24 signals difficulty retaining skilled workforce. As the company grows from 200 to targeted 500 facilities, finding, training, and retaining qualified ophthalmologists becomes exponentially harder. Salary inflation in healthcare professionals consistently exceeds revenue growth, pressuring margins.

Regulatory risks loom large. Government price caps on procedures or implants could devastate margins. Changes in medical device import duties affect cost structures. Clinical establishment act compliance adds bureaucracy and costs. Any adverse event leading to regulatory scrutiny could damage the carefully built brand.

The technology disruption threat is real, even if timeline uncertain. If AI-powered home diagnostics become reliable, if telemedicine regulations liberalize, if international players enter through digital platforms, the vast physical infrastructure becomes a liability rather than asset. The company's measured technology adoption, while prudent, might leave them vulnerable to digital-native disruptors.

Geographic concentration remains problematic despite expansion. Over 60% of revenues still come from South India, creating vulnerability to regional economic downturns, competitive intensity, or regulatory changes. Expanding north and west requires different strategies, relationships, and potentially lower margins as these markets have different competitive dynamics.

X. Epilogue: The Future of Indian Healthcare

The Dr. Agarwal's story is more than a business case study—it's a window into the transformation of Indian healthcare from charity-driven service to professionally managed industry. The questions their journey raises will define the next decade of healthcare investing in emerging markets.

The Consolidation Imperative

India's healthcare remains incredibly fragmented. If eye care, a relatively simple specialty, has 99 active competitors for a ₹378 billion market, imagine the fragmentation in multi-specialty healthcare. The rollup opportunity is massive, but Dr. Agarwal's experience shows consolidation is harder than it appears. Cultural integration, system standardization, and maintaining quality at scale all pose challenges that financial engineering cannot solve.

The next wave of consolidation might look different—platform models where independent hospitals share backend services, purchasing cooperatives that maintain individual identity while achieving scale benefits, or technology platforms that unite fragmented providers virtually. Dr. Agarwal's might evolve from an operator to a platform provider, leveraging their systems and expertise across affiliated but not owned facilities.

Technology's Inevitable March

We're at the tip of the iceberg. AI can help correct misdiagnoses and expand access in ways we couldn't have imagined before. Looking ahead, artificial intelligence is central to Dr. Agarwal's strategy for scalable, quality care. But the timeline remains uncertain. Healthcare adoption of technology historically lags other industries by 5-10 years due to regulatory caution, patient conservatism, and provider resistance.

The real disruption might come not from replacing doctors but augmenting them. AI that helps a junior ophthalmologist perform like a senior consultant, surgical robots that eliminate hand tremor, diagnostic tools that catch conditions earlier—these enhancements multiply human capability rather than replacing it. Dr. Agarwal's, with its vast clinical database and procedure volume, could become the training ground for these AI systems.

The Insurance Question

As insurance penetration increases from current 30% to potentially 70% over the next decade, the entire economics of healthcare delivery changes. Hospitals must invest in billing systems, manage working capital differently, and accept lower negotiated rates. But insurance also expands the addressable market dramatically—procedures that patients postponed due to cost become accessible.

Dr. Agarwal's will need to navigate this transition carefully. Their current cash-dominant model provides pricing flexibility and immediate cash flows. Moving to insurance-based revenues might pressure margins initially but could unlock massive volume growth. The key will be maintaining a dual-track system—premium cash services for those who can afford them, insurance-based volume services for the mass market.

Can Family Healthcare Businesses Survive Institutionalization?

The transition from second to third generation, from family to institutional ownership, tests whether the original mission survives. Many global examples suggest difficulty—as professional managers optimize for metrics, the intangible elements that made the institution special often erode. Yet healthcare might be different. The clinical credibility that comes from having doctors in leadership, the trust that comes from family legacy, the mission orientation that attracts talent—these might prove sustainable competitive advantages even under institutional ownership.

Dr. Agarwal's represents a test case. With family members still in clinical leadership but financial investors controlling ownership, they're attempting a hybrid model. Success would provide a template for other family healthcare businesses navigating similar transitions.

The Tepid IPO Reception: Broader Implications

The market's lukewarm response to Dr. Agarwal's IPO—listing at a 3.22% discount despite market leadership—sends important signals. Investors have become sophisticated enough to see through complex structures, demand growth capital deployment over exits, and penalize excessive valuations regardless of business quality.

This might force a rethink of how healthcare companies approach public markets. Simple structures, reasonable valuations, and clear growth capital use might matter more than size or market position. The era of financial engineering creating value might be ending, replaced by focus on operational excellence and sustainable growth.

Future healthcare IPOs will need to learn these lessons. The market wants to invest in India's healthcare growth story but not at any price or structure. Companies that offer transparency, reasonable valuations, and clear growth strategies will find receptive investors. Those relying on complexity or hype might face Dr. Agarwal's fate—operational excellence undermined by financial structure.

What This Means for Healthcare Entrepreneurs

The playbook is clear but execution remains challenging. Start with genuine mission, build systems that can scale, maintain quality while growing, navigate the family-to-professional transition thoughtfully, expand internationally into similar markets, use technology to augment rather than replace human capability, and approach capital markets with transparency and reasonable expectations.

But the biggest lesson might be patience. Dr. Agarwal's took 67 years to build their empire. In an era of unicorn obsession and rapid scaling, their steady, mission-driven growth seems anachronistic. Yet they've built something sustainable—a healthcare institution that serves millions, employs thousands, and advances medical practice. That's a different kind of success than a quick flip to financial buyers.

The future of Indian healthcare will be written by entrepreneurs who learn from Dr. Agarwal's journey—both its successes and struggles. The opportunity is massive: a billion people needing quality healthcare, rising incomes making it affordable, technology making it accessible. But success requires more than spotting opportunity. It requires building institutions that balance mission with margins, scale with quality, innovation with accessibility.

As we close this analysis, Dr. Agarwal's stands at an inflection point. Public company pressures might force short-term thinking that undermines long-term value. Or institutional capital might provide resources for transformation that family ownership couldn't enable. The next chapter of their story will be written by how well they navigate these tensions.

For investors, the question isn't whether Indian healthcare represents opportunity—it clearly does. The question is identifying companies that can execute the complex balance required for sustainable success. Dr. Agarwal's, despite its IPO stumbles, remains a formidable player with unique advantages. Whether those advantages translate to superior returns depends on execution in an increasingly complex competitive and regulatory environment.

The hundred rupees that Dr. Jaiveer and Dr. Tahira brought to Chennai in 1957 has multiplied into a ₹14,000+ crore enterprise. That's a compelling return by any measure. But the real return might be immeasurable: millions of people who can see because of surgeries performed, thousands of professionals trained in life-changing skills, and a template for building healthcare infrastructure in developing economies. That's a legacy that transcends financial metrics—and perhaps that's the most important lesson of all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube