Royalty Pharma: The Quiet Giant Funding Biopharma Innovation

Introduction: The Company That Owns a Piece of Everything

Picture yourself in a Manhattan boardroom in early 2020. The world teeters on the edge of a pandemic that will reshape global healthcare, and pharmaceutical investment banker after pharmaceutical investment banker warns that the IPO window is slammed shut. Into this chaos walks a company most investors have never heard of—Royalty Pharma—seeking to raise over $2 billion in what would become the largest U.S. initial public offering of the year.

On June 15, 2020, the company went public on the Nasdaq stock market under the ticker RPRX. At $28 per share, they sold 77.7 million shares, raising $2.2 billion and valuing Royalty Pharma at $16.7 billion. Royalty Pharma made its stock market debut at $44 per share, valuing the company at a whopping $26.2 billion—the market pushed the stock more than 60% higher during its first day of trading.

How did a former Lazard investment banker from Mexico City create an entirely new asset class and build a company that now owns a piece of a quarter of all blockbuster drugs? To date, Royalty Pharma has deployed more than $25 billion of capital to advance innovation in the biopharmaceutical industry.

The answer lies in a deceptively simple insight that took decades to fully unfold. Royalty Pharma occupies an unusual position—somewhere between the National Institutes of Health and a hedge fund. The company doesn't discover drugs. It doesn't manufacture them. It doesn't market them. Instead, it provides the financial fuel that makes modern pharmaceutical innovation possible—and clips a quiet toll on some of the world's most important medicines in perpetuity.

Founded in 1996, Royalty Pharma is the largest buyer of biopharmaceutical royalties and a leading funder of innovation across the biopharmaceutical industry, collaborating with innovators from academic institutions, research hospitals and non-profits through small and mid-cap biotechnology companies to leading global pharmaceutical companies.

This episode explores the story of how one visionary founder created a new financial model that has become essential to biopharma's capital structure, the landmark deals that transformed the company from boutique investor to industry giant, and the competitive moat that has kept Royalty Pharma at the top of a market it essentially invented.

The Founder's Insight: Pablo Legorreta and the Birth of an Industry (1996)

The Accidental Discovery

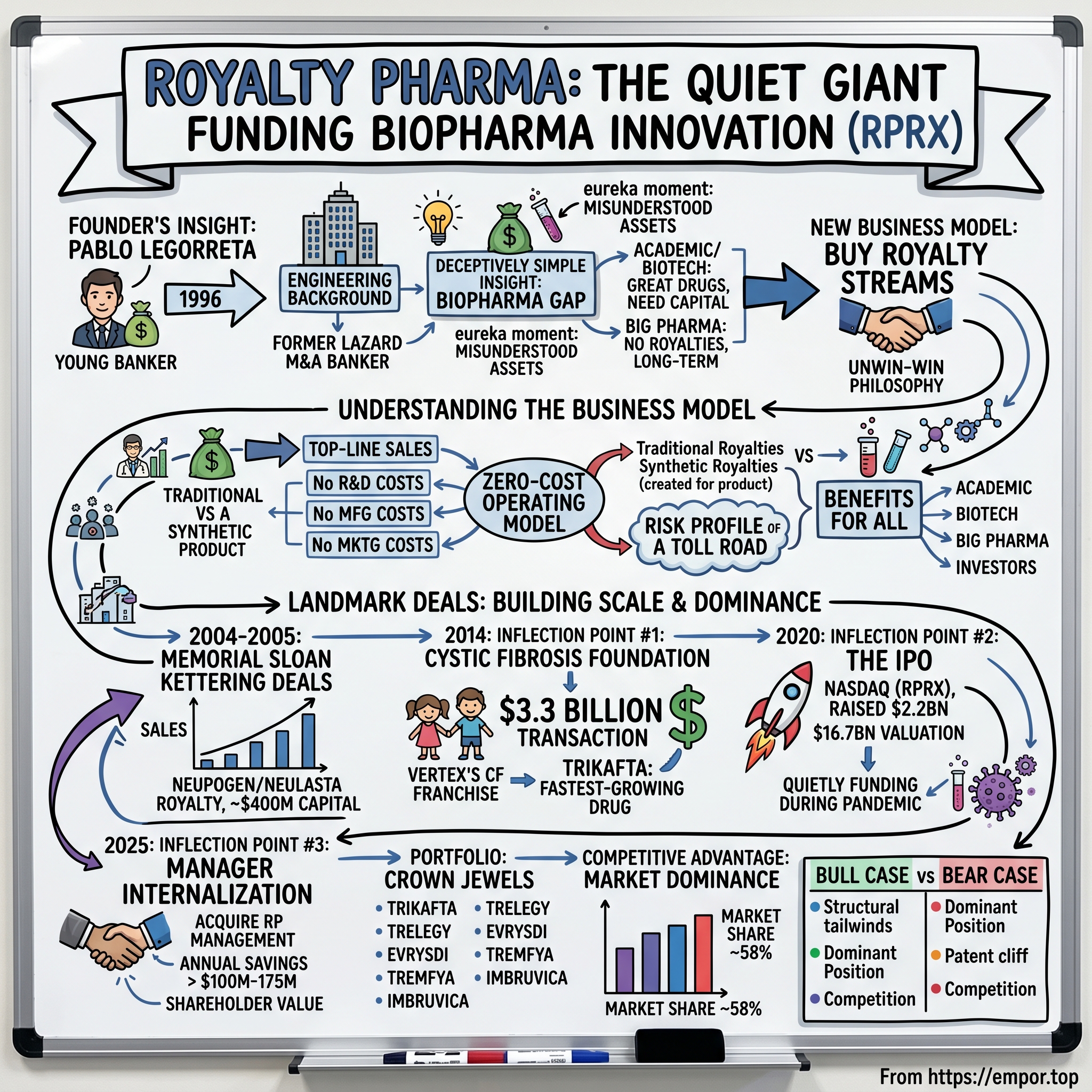

Pablo Legorreta (born in 1963/1964) is a Mexican-American billionaire businessman, and the founder of Royalty Pharma PLC, the "world's biggest acquirer of pharmaceutical royalty streams."

To understand Royalty Pharma, you must first understand its founder—an engineer by training who became one of Wall Street's most creative financial architects. Prior to Royalty Pharma, Legorreta had a 10-year career as an M&A banker at Lazard Frères—from 1987 to 1990 at Lazard Frères et Cie in Paris and from 1990 to 1996 at Lazard Frères & Co. in New York.

Legorreta earned a Bachelor of Science in Engineering from Universidad Iberoamericana. This technical background proved crucial—it gave him a framework for analyzing pharmaceutical development that pure financiers lacked. He understood probabilities, systems, and most importantly, the concept of risk-adjusted returns.

The eureka moment came not in a laboratory, but in a Lazard conference room. While he was still working at Lazard Frères, Legorreta saw how clients of PaineWebber made an investment in rights to a chemotherapy drug back in 1987. This innovative scheme pioneered by Paine Webber bankers encouraged smaller firms to raise money through private investors rather than selling their innovations to big pharma companies outright.

During his time as an investment banker, Legorreta was exposed to the biopharmaceutical industry and identified a market inefficiency: the gap between the long, expensive process of drug development and the need for capital. In 1996, Legorreta founded Royalty Pharma with a groundbreaking idea: instead of trying to discover new drugs, the company would buy royalty streams on future sales of already-approved, blockbuster drugs from pharmaceutical companies, research institutions, and inventors.

The Insight That Changed Everything

The pharmaceutical industry had a structural problem. Academic institutions, research hospitals, and small biotechs often discovered compounds that became blockbuster drugs—but they didn't have the capital, infrastructure, or expertise to commercialize them. They licensed their discoveries to big pharma companies in exchange for royalty payments. But those royalties were uncertain, spread over decades, and difficult to value. Meanwhile, these institutions needed capital now to fund their next generation of research.

Legorreta recognized that these royalty streams were essentially misunderstood financial assets. To the universities and research hospitals that owned them, they were speculative windfalls—nice to have, but impossible to budget around. To someone who could model pharmaceutical markets and build a diversified portfolio, they represented predictable cash flows with tremendous upside potential.

This provided immediate, non-dilutive capital to the sellers and gave Royalty Pharma a diverse portfolio of income streams from some of the world's best-selling medicines. This innovative model de-risked pharmaceutical investing and proved to be immensely successful. Legorreta has since grown the company into the largest buyer of biopharmaceutical royalties in the world.

Building the Foundation

The company began modestly. Since its founding in 1996, Royalty Pharma has been the pioneer and market leader in royalty funding of life science innovation. The company's collaborations span the entire research and development ecosystem, from academic institutions, research hospitals and not-for-profits to small- and mid-cap biotechnology companies and global pharmaceutical companies.

Legorreta's engineering mindset shaped the firm's culture. He approached pharmaceutical royalties not as speculative bets but as assets requiring rigorous scientific due diligence, actuarial analysis, and portfolio construction. Royalty Pharma funds innovation in life sciences, indirectly, when it acquires existing royalties from the original innovators (academic institutions, research hospitals, foundations and inventors) or, directly, when it partners with biopharmaceutical companies to co-develop and co-fund products in late-stage human clinical trials.

The founder also built a network of relationships that would become the company's greatest asset. Legorreta serves on the Boards of the New York Academy of Sciences, Rockefeller University, the Hospital for Special Surgery, and the Pasteur Foundation. He founded and is current Chairman of Alianza Médica para la Salud (AMSA), a privately-funded, not-for-profit foundation that provides scholarships to study abroad to Latin American doctors and healthcare providers.

Beyond building relationships with potential sellers, Legorreta innovated a "win-win" philosophy that would become central to Royalty Pharma's value proposition. He began allowing the inventors, hospitals, and academic institutions from which he acquired royalties to reinvest some of their proceeds back into Royalty Pharma—effectively securing access to a more diversified portfolio of pharmaceutical royalties while maintaining ongoing relationships with the innovator community.

Understanding the Business Model: How Royalties Work

The Mechanics of a Pharmaceutical Royalty

Before diving deeper into Royalty Pharma's history, it's essential to understand the financial plumbing that makes the entire model work. Pharmaceutical royalties exist because of the complicated, collaborative nature of drug development.

Typically, a biotech developing a new drug may partner with a large pharma company, who assumes responsibility for the development, commercialization, and marketing of a promising drug candidate—investing much larger sums than the smaller biotech could on its own. In exchange, the big pharma company makes milestone payments to the biotech as it hits development and commercialization targets, and agrees to give the biotech a portion of all future global sales—usually in the mid-teen percentages—known as a royalty.

Typical royalty deals run between 4-10% of sales based on publicly disclosed agreements by Royalty Pharma in their S-1. However, in some cases biopharma companies can be tied into forking over astonishing sums every year. For example, Royalty Pharma is entitled to 18% of annual net global sales of Biogen's Tysabri up to $2 billion, and 25% of any global sales above that cap, in perpetuity.

It is these royalty streams that Royalty Pharma purchases from the biotechs or original innovators, in exchange for an upfront payment. The genius of the model is its simplicity for everyone involved.

The Zero-Cost Operating Model

What makes Royalty Pharma such an unusual investment vehicle is what it doesn't have to do. Royalty Pharma has assembled a portfolio of royalties which entitles it to payments based directly on the top-line sales of many of the industry's leading therapies. Royalty Pharma funds innovation in the biopharmaceutical industry both directly and indirectly—directly when it partners with companies to co-fund late-stage clinical trials and new product launches in exchange for future royalties, and indirectly when it acquires existing royalties from the original innovators.

The company operates as the largest acquirer of biopharmaceutical royalties in the world. Instead of developing drugs itself, Royalty Pharma purchases royalty rights from innovators such as academic institutions, hospitals, biotech firms, and pharmaceutical companies. These royalties entitle Royalty Pharma to a percentage of top-line sales of specific therapies, allowing it to benefit from the success of leading drugs without incurring the costs or risks associated with research, development, manufacturing, or marketing.

No costs associated with development. No costs for manufacturing. No costs for marketing. Consider the implications: when you buy shares in Pfizer or Merck, you're exposed to the full cost structure of pharmaceutical development—the failed clinical trials, the manufacturing plants, the thousands of sales representatives, the regulatory compliance teams. When you invest in Royalty Pharma, you participate only in the successful outcomes. It's pharmaceutical exposure with the risk profile of a toll road.

Traditional vs. Synthetic Royalties

Royalty monetization typically takes one of two forms: Investors buy or finance against royalties from an existing license or collaboration agreement (a "traditional" royalty), or they buy or finance against a product's future revenue stream (a "synthetic" royalty). While these deals include covenant packages that provide guardrails for what companies can and can't do with the product assets and related operations, the obligations are typically less onerous than traditional debt, and afford companies up-front capital without the dilution of an equity raise.

In a traditional royalty, the royalty already exists organically from a prior business deal. In contrast, a synthetic royalty is artificially created. The company doesn't have a royalty stream to sell because it's commercializing the drug itself. Instead, it crafts a new revenue-sharing agreement from scratch.

This distinction matters because synthetic royalties have become increasingly important to Royalty Pharma's growth strategy. 2024 was a record year for synthetic royalty transactions for Royalty Pharma with $925 million announced. The company's ability to structure these creative financing solutions has become a core competitive advantage, allowing it to partner with companies that don't have traditional royalty streams to sell.

Why This Appeals to Everyone

The model creates genuine value for all participants:

For academic institutions and research hospitals, it converts uncertain, long-duration assets into immediate capital they can deploy for new research or facility expansion.

For biotechs, it provides non-dilutive funding—they get cash without giving up equity or taking on debt covenants that restrict operations.

For big pharma, it creates a robust ecosystem of innovation partners who can fund themselves independently, increasing the pipeline of licensable drug candidates.

For investors, it offers exposure to pharmaceutical upside with a dramatically simplified risk profile—diversified, professionally managed, and focused exclusively on proven or late-stage assets.

According to Deloitte's 2025 market study, 87% of surveyed biopharma executives would consider royalties as part of their capital raising plans over the next three years. The report underscores the vital role royalties play in fueling the biopharma ecosystem—supporting life sciences innovation and commercial success while offering flexible, non-dilutive capital at scale.

Building Scale: Early Deals and the Road to Dominance (1996–2013)

The Memorial Sloan Kettering Deals: Proving the Concept

Royalty Pharma's transformation from boutique investor to industry leader came through a series of increasingly ambitious deals that validated its model and built its reputation.

Notable early successes included two back-to-back transactions with Memorial Sloan Kettering Cancer Centre in 2004 and 2005, whereby MSKCC sold 80% of its Neupogen/Neulasta royalty for $400 million.

Royalty Pharma's $405 million royalty acquisition of Neupogen/Neulasta, a stimulant of white blood cell production that is used to reduce the risk of infection for cancer patients receiving various forms of chemotherapy, provided capital to MSKCC to reinvest in cancer research, expand its footprint and build one of the largest research centers in New York. "The net proceeds from this sale will be used to reinvest in MSKCC's basic and translational research programs and facilities, which we hope will produce new discoveries that will benefit our patients and cancer patients elsewhere."

The Memorial Sloan Kettering transaction exemplified Royalty Pharma's value proposition. Sloan-Kettering ranked fifth among teaching hospitals and research institutes in research expenditures, reporting $224 million in research expenditures. In total, Royalty Pharma purchased royalty interest in Neupogen and Neulasta worldwide except for China, Japan, South and North Korea and Taiwan. The two drugs were "certainly our biggest royalty position," according to hospital officials.

While there are currently several universities and smaller drug companies looking to monetize their patent royalty streams to capture cash early, the impetus behind the Sloan Kettering transaction was risk avoidance. "As the royalty grows, it becomes a huge risk. [Sloan-Kettering] wants to reduce their risk from an asset allocation and diversification standpoint. You can't sell the drug short, but you can sell the royalty or monetize it in some way."

Building the Portfolio of Crown Jewels

Following the Memorial Sloan Kettering success, Royalty Pharma executed a series of landmark acquisitions that built its portfolio of royalties on blockbuster drugs. With royalty interests in 30 approved products (including Abbott's Humira, Johnson and Johnson's Remicade, Merck's Januvia, Gilead's Atripla, Truvada, and Emtriva, Pfizer's Lyrica, Amgen's Neupogen and Neulasta), Royalty Pharma had a fifteen-year history of providing value to holders of royalty interests, including its $400 million purchase of 80% of Memorial Sloan-Kettering Cancer Center's Neupogen/Neulasta royalty, its $700 million acquisition of AstraZeneca's Humira royalty.

These weren't just any drugs—they were the backbone of modern pharmaceutical therapy. Humira would become the world's best-selling drug. Januvia revolutionized diabetes treatment. Lyrica became ubiquitous in pain management. By methodically acquiring royalties on these foundational medicines, Royalty Pharma was building a portfolio that would generate cash flows for decades.

The Dublin Strategy

A critical strategic decision came in 2003, when the company relocated its headquarters to Dublin, Ireland. The move reflected both the tax advantages that Ireland offered to asset management businesses and the increasingly global nature of pharmaceutical royalties.

Since 2003, Ireland's competitive 12.5% corporate tax rate—well below the global average of 23.51%—has been a major draw for multinational investment. Nine of the world's top 10 pharmaceutical companies have established significant operations in Ireland, drawn by the country's deep talent pool and strategic advantages. As one of the only English-speaking nations in the European Union, Ireland offers seamless access to the wider EU market, making it an ideal base for international operations.

This move wasn't just about tax optimization—it positioned Royalty Pharma at the center of the global pharmaceutical ecosystem. Dublin had become a hub for pharma operations, and having a presence there enhanced relationships with potential counterparties.

The External Management Structure

One distinctive feature of Royalty Pharma during this period was its external management structure. Since its founding in 1996, Royalty Pharma had operated under an external management model, relying on a separate Manager, owned by Pablo Legorreta and other members of senior management, for all operations and personnel. The company paid quarterly fees to the Manager equal to 6.5% of Portfolio Receipts and 0.25% of the value of security investments.

This structure—common in the hedge fund world but unusual for what would become a publicly traded company—allowed Legorreta to maintain tight control over the business while aligning the management team's interests with long-term performance. However, it would later become a point of contention with investors who viewed it as a drag on shareholder returns.

Inflection Point #1: The Cystic Fibrosis Foundation Deal (2014)

The Venture Philanthropy Model

The transaction that transformed Royalty Pharma from successful investor to industry titan began not in a Wall Street boardroom, but in a research laboratory funded by parents desperate to save their children.

The Cystic Fibrosis (CF) Foundation has sold royalty rights to treatments developed with support from its "venture philanthropy" model. The venture philanthropy model, adopted in the late 1990s, sees the foundation provide upfront funding for pharmaceutical companies to help reduce the financial risk of developing drugs to treat CF. It gave a total of $150 million to Vertex to support the company's CF drug development program.

The CF Foundation had pioneered a revolutionary approach to disease research. Rather than simply funding academic studies and hoping pharmaceutical companies would eventually develop treatments, the foundation invested directly in drug development—taking equity-like positions and receiving royalties in exchange for its risk capital.

In 2000, the Foundation made its first large investment: $40 million with Aurora Biosciences (now Vertex Pharmaceuticals) to discover compounds that might correct the malfunctioning protein in people with CF. Aurora specialized in high throughput screening, a then-novel technology that uses robots to test the therapeutic properties of thousands of chemical compounds per day in cells in laboratory dishes. It became clear that the venture strategy was a success in 2012, when the U.S. Food and Drug Administration approved the first drug to address the underlying cause of cystic fibrosis: ivacaftor (Kalydeco).

The Landmark Transaction

By 2014, the CF Foundation's bet had paid off spectacularly. Vertex's cystic fibrosis drugs were generating hundreds of millions in revenue, with much larger blockbusters in the pipeline. The foundation faced a dilemma: its royalty stake was now worth billions, but the funds were locked up in a single asset. It needed capital to accelerate its mission.

In November 2014, Royalty Pharma announced its acquisition of royalties on Vertex Pharmaceuticals' cystic fibrosis treatments owned by Cystic Fibrosis Foundation Therapeutics for a cash payment of $3.3 billion. "We are honored to work with the Cystic Fibrosis Foundation on this extraordinary royalty transaction," said Pablo Legorreta. "Our goal is to be the premier provider of innovative capital to enable the life sciences industry to accelerate development of important novel therapies. Furthermore, this transaction represents an important validation of the Foundation's bold vision under Dr. Beall's leadership to fund new drug development as part of its successful venture philanthropy model."

The scale of the deal was unprecedented. As well as this $3.3 billion, reportedly 20 times the foundation's budget for the previous year, the foundation stood to receive additional royalties on other CF therapies Vertex produces.

The Financing Structure

Bank of America Merrill Lynch acted as financial advisors to Royalty Pharma in this transaction and Goodwin Procter acted as legal advisor. Royalty Pharma financed this acquisition with cash on hand and a $2.7 billion unsecured term loan provided by Bank of America Merrill Lynch.

This financing structure demonstrated a key aspect of Royalty Pharma's competitive advantage: its ability to deploy massive capital quickly while maintaining financial flexibility. Few other royalty investors could write a $3.3 billion check with debt financing at attractive rates.

Transformational Impact

"This is a transformational moment for people with CF and the CF community that will enable us to accelerate our mission as never before," said Robert J. Beall, Ph.D., president and CEO of the Cystic Fibrosis Foundation.

The deal proved transformational for both parties. For the CF Foundation, $3.3 billion in immediate capital allowed it to fund an entirely new generation of research—including work on gene therapy approaches that could potentially cure cystic fibrosis entirely. For Royalty Pharma, it provided exposure to what would become the company's crown jewel asset.

In 2014, Royalty Pharma paid $3.3 billion for the stake held by the Cystic Fibrosis Foundation in Vertex's cystic fibrosis portfolio which would become their biggest source of royalty revenues.

The wisdom of this investment became clear as Vertex's CF franchise expanded. In the fourth quarter 2023, Vertex's CF combo therapy Trikafta raked in $2.33 billion in sales, bringing its 2023 haul to $8.9 billion, a 16% increase from 2022. Trikafta, approved in 2019, had become one of the fastest-growing drugs in pharmaceutical history—and Royalty Pharma owned a meaningful royalty on every dollar of sales.

Inflection Point #2: The 2020 IPO—Going Public in a Pandemic

The Boldest Timing in IPO History

In early 2020, as COVID-19 began spreading globally and financial markets cratered, most companies postponed their public offerings indefinitely. Ernst & Young noted in a quarterly IPO trends report that global IPO activity declined sharply between April and May—48% and 67%, respectively—compared to the previous year, mostly due to the impact of the COVID-19 pandemic. However, there was a rebound in IPO activity across all regions in June, with a third of the total IPOs for the year occurring in the month.

Royalty Pharma saw opportunity in chaos. The pandemic highlighted the importance of pharmaceutical innovation—and exposed the industry's capital constraints. Biotechs racing to develop vaccines and treatments needed funding. Academic institutions saw their endowments hammered by market volatility.

Swedish biotech Calliditas raised $90 million with its IPO, the latest in a series of oversubscribed launches as the sector was seen as a safe haven for investment during the COVID-19 pandemic. Royalty Pharma was planning the biggest IPO of the year as the market's appetite for biotech stocks remained strong. The company said in a filing with the US financial regulator that it plans to raise up to $1.96 billion on the Nasdaq using the ticker RPRX.

Execution Excellence

On June 8, Royalty Pharma announced it was looking to raise up to $1.96 billion in an initial public offering, planning to offer 70 million Class A ordinary shares at a target price range of $25-$28 per share. Even at this initially estimated valuation, it would be the U.S.' largest IPO of 2020 so far, leaving behind the recent Warner Music Group's $1.9 billion deal. On Monday June 15, the company revealed the pricing of its IPO at $28 per share. The size of the IPO was increased to 77,681,670 shares. JP Morgan, Goldman Sachs, Citigroup, Morgan Stanley, and BofA Securities were among the IPO's lead book-running managers and underwriters.

New York-based pharmaceutical company Royalty Pharma priced its IPO at $28 per share, with the second-highest per-share price for the quarter. The company, which operates as a buyer of biopharmaceutical royalties, was also the only company to have crossed the $1 billion mark in proceeds raised, enabling the total amount generated for the quarter to beat the previous years. The company's shares saw a significant jump from the initial price in their debut, closing at $44.50 on June 16.

IPO Boutique, a research and advisory firm, said the Royalty Pharma IPO 2020 was "multiple times oversubscribed," meaning that the demand for shares from institutional investors was greater than the supply on offer. Apart from being the biggest IPO of the year, it was the second-largest pharmaceutical public listing ever, just behind Zoetis' $2.2 billion IPO in 2013.

Why Investors Loved It

The IPO's success reflected several factors that resonated with institutional investors:

First, the business model was inherently pandemic-resilient. Royalty Pharma's cash flows came from pharmaceutical sales—and people continued taking their medications regardless of economic conditions. Unlike hospitality or retail businesses getting hammered by lockdowns, pharmaceutical royalties were essentially pandemic-proof.

Second, the timing positioned Royalty Pharma to capitalize on the post-pandemic pharmaceutical boom. Widely respected in the industry for the sheer scale of its operations, Royalty Pharma's decision to go public would undoubtedly provide more liquidity for the company to capitalize on the current global health crisis. When the IPO materialized, the group immediately confirmed that the lion's share of the capital raised from its issuance of stocks would go towards acquiring more royalty rights. Fundamentally, the current pandemic exposed systemic problems in the healthcare and pharmaceutical industries—issues that must be addressed with significant amounts of capital to meet these most pressing of medical needs.

Third, the financial profile was remarkably clean. According to the company's financial reports, Royalty Pharma's net income rose from $581 million in 2015 to $2.35 billion in 2019.

The Follow-On CF Foundation Deal

The IPO's success immediately enabled Royalty Pharma to expand its most valuable asset position. In November 2020, Royalty Pharma announced an agreement to acquire the residual royalty interest in Vertex Pharmaceuticals' cystic fibrosis treatments owned by the Cystic Fibrosis Foundation. The agreement includes an upfront payment of $575 million and a potential milestone payment of $75 million.

As part of previous agreements with the CF Foundation, Royalty Pharma purchased all of the CF Foundation's royalty interests on Vertex's CF franchise. Under the terms of those agreements, Royalty Pharma was obligated to pay the CF Foundation 50% of royalties attributable to revenue over $5.8 billion in any calendar year. This new agreement eliminated this obligation and entitled Royalty Pharma to all royalties above the previous revenue threshold. The Vertex CF franchise generated net revenues totaling over $4.0 billion in 2019. The royalties under this agreement are perpetual and not tied to patent expirations.

This follow-on deal exemplified Royalty Pharma's strategy of deepening relationships with existing partners—and its willingness to invest additional capital when the risk/reward profile was attractive.

Inflection Point #3: Manager Internalization (2025)

The External Management Structure's Limitations

For nearly three decades, Royalty Pharma operated under an external management structure that served the company well during its private years but increasingly drew criticism from public market investors.

Royalty Pharma received feedback from investors that its externally managed structure was an impediment to investing in Royalty Pharma. Internalizing the Manager, with all the benefits described above, had the potential to expand Royalty Pharma's shareholder base and enhance the company's valuation over time.

The concerns were straightforward: the management fee structure—6.5% of Portfolio Receipts plus 0.25% of security investments—represented a significant expense that grew alongside the portfolio. Institutional investors accustomed to internally managed structures viewed this as a permanent drag on returns that benefited management at shareholders' expense.

The Announcement

In January 2025, Royalty Pharma announced two major steps to enhance shareholder value: becoming an integrated company by acquiring its external manager, RP Management, LLC, with significant annual cash savings of greater than $100 million in 2026 growing to over $175 million in 2030, with cumulative savings of more than $1.6 billion over ten years.

Henry Fernandez, lead independent director of Royalty Pharma's Board of Directors and Chairman and Chief Executive Officer of MSCI Inc., said "the Board of Directors of Royalty Pharma is pleased to announce this transaction which it believes increases shareholder alignment and enhances corporate governance. Coupled with the new $3 billion share repurchase authorization, we expect these actions to drive shareholder value creation over the long-term." Pablo Legorreta commented, "We see the internalization of RP Management as a highly compelling next step in the evolution of our business which will yield many financial and strategic benefits to shareholders."

The Transaction Structure

Royalty Pharma will acquire the Manager for approximately 24.5 million shares of Royalty Pharma equity that will vest over 5 to 9 years, approximately $100 million in cash, and the assumption of $380 million of existing Manager debt. The total transaction value of approximately $1.1 billion (based on the closing price of Royalty Pharma plc common stock of $26.20 on January 8, 2025), with the majority paid in long-term deferred equity, is expected to be more than offset by cumulative cash savings of greater than $1.6 billion over the next ten years. The equity component will represent approximately 4% of shares outstanding, assuming all shares vest.

Shareholder Approval and Succession Planning

In May 2025, Royalty Pharma announced that it had successfully closed the acquisition of its external manager, RP Management, LLC. The acquisition received overwhelming support from Royalty Pharma's shareholders, with 99.9% of votes cast in favor of the transaction.

"The completion of the internalization marks an exciting new chapter for Royalty Pharma," said Pablo Legorreta. "It reinforces our commitment to transparency, accountability and long-term growth, while better positioning us to fund the significant capital needs and exciting innovation happening in the life sciences industry."

The transaction also addressed succession planning concerns. Prior to 2024, Pablo Legorreta was the sole owner of the Manager. In early 2024, equity interests in the Manager were granted to 35 team members to support long-term succession planning and enhance alignment; these shares will vest over 10 years.

Following the closing of the internalization transaction, Royalty Pharma is no longer externally managed, and all employees of the Manager have become employees of Royalty Pharma.

The Portfolio: Crown Jewels and Diversification

The Cystic Fibrosis Franchise

At the heart of Royalty Pharma's portfolio lies its royalty interest in Vertex's cystic fibrosis franchise—a position that has grown far beyond what even the most optimistic projections suggested in 2014.

Vertex's marketed CF franchise includes Kalydeco (ivacaftor), Orkambi (lumacaftor and ivacaftor), Symdeko/Symkevi (tezacaftor/ivacaftor and ivacaftor), and Trikafta/Kaftrio (ivacaftor/tezacaftor/elexacaftor and ivacaftor), which are currently the only U.S. Food and Drug Administration (FDA)-approved disease-modifying therapies for CF patients.

Trikafta quickly became a blockbuster, and last year it generated $8.9 billion in revenue for Vertex. The company's other CFTR modulators made up the rest, for a total of $9.8 billion in annual revenue.

The royalty rate on Vertex's CF portfolio is a bit less than 10%; the company says the rate for the next-generation vanza triple will be in the single digits and "meaningfully lower." Even at these rates, the absolute dollar amounts are extraordinary.

Royalty Pharma estimates royalty duration of 2039-2041 due to expected Alyftrek patent expiration and potential generic entry thereafter. Royalty Pharma estimates expected Trikafta patent expiration in 2037 and potential generic entry thereafter leading to sales decline.

Portfolio Breadth and Diversification

Royalty Pharma's current portfolio includes royalties on more than 35 commercial products, including Vertex's Trikafta, GSK's Trelegy, Roche's Evrysdi, Johnson & Johnson's Tremfya, Biogen's Tysabri and Spinraza, AbbVie and Johnson & Johnson's Imbruvica, Astellas and Pfizer's Xtandi, Novartis' Promacta, Pfizer's Nurtec ODT and Gilead's Trodelvy, and 14 development-stage product candidates.

The portfolio spans multiple therapeutic areas—rare diseases, cancer, neuroscience, immunology, and cardiovascular health—reducing concentration risk while maintaining exposure to some of the most important medicines in the world.

Recent Deal Activity

The company continues to execute at scale. Royalty Receipts grew 12% to $729 million in the fourth quarter and 13% to $2,771 million for full year 2024, driven by strong performance from Evrysdi, the CF franchise, Trelegy, Tremfya and new royalty acquisitions. Capital Deployment of $2.8 billion in 2024 with royalties on eight new therapies added to the portfolio. Significantly expanded development-stage portfolio by acquiring royalties on four potential new therapies.

In June 2025, Royalty Pharma announced a $2 billion funding arrangement with Revolution Medicines, consisting of a synthetic royalty of up to $1.25 billion on daraxonrasib and a senior secured loan of up to $750 million.

In November 2025, Royalty Pharma acquired Blackstone's 1% royalty on worldwide net sales of AMVUTTRA in exchange for an upfront payment of $310 million. AMVUTTRA sales reached approximately $1 billion in 2024, which represented 74% year-over-year growth, and are projected to exceed $6 billion by 2028 based on analyst consensus.

Competitive Landscape and Market Dominance

Unmatched Scale

Royalty Pharma is "the largest and most active buyer of royalty streams." In its latest 10K filing, Royalty Pharma reported that from 2012 through 2023, it has executed transactions with an aggregate announced value of $26.4 billion, which represents an estimated market share of approximately 58% of all royalty transactions during this period.

The company continues to be the clear leader in the market for large royalty transactions. Of the 26 royalty transactions to date valued at $500 million or more, Royalty Pharma has executed 20 with a market share of 77%. Half of those transactions have taken place in the four years since the IPO. This reflects an important competitive advantage—scale and rapid access to substantial capital.

The Competitive Field

Three firms are responsible for 71% of royalty origination deal value in the past decade: Royalty Pharma with $4.2 billion (36% of total value), Healthcare Royalty Partners with $2.3 billion (19%) and Blackstone Life Sciences with $1.8 billion (16%). In the past few years, however, new players have entered the market, hinting at growing interest in royalty investments.

KKR acquired a majority stake in HealthCare Royalty Partners (HCRx), enhancing KKR's exposure to the high-growth biopharma royalties market. With this deal, KKR enters direct competition with other royalty investment leaders such as Royalty Pharma and Blackstone Life Sciences, underscoring rising demand for non-dilutive capital in a challenging biopharma funding environment. Founded in 2006 and headquartered in Stamford, Connecticut, HCRx has committed over US$7 billion across more than 55 biopharmaceutical products in 10 therapeutic areas.

Other players are opening up new areas of the market. XOMA, which pivoted in 2017 to become a self-styled "royalty aggregator that thinks like a biotech," is amassing earlier-stage royalties. It has built a diverse portfolio of candidates in early-stage development by the likes of Bayer, Takeda, Roche, Merck, Janssen and Novartis. Shanghai-based Zai Labs is a commercial-stage biotech company acquiring royalties and rights to sell drugs in China.

Market Trends

In the five years from 2020 to 2024, the biopharma royalty market has averaged $6.2 billion in announced transaction value per year, more than double the average of $2.7 billion over the preceding five years. This rapid expansion reflects growing recognition in the life sciences industry of the benefits of royalty funding.

Industry data confirms the trend: From 2020 through 2024, royalty financings in biopharma totaled approximately $29.4 billion, more than double the amount raised between 2015 and 2019, with synthetic royalty structures gaining prominence within this trend.

Synthetic royalties have been gaining traction among biopharma executives in recent years marking a sizable shift. Such evolving perspectives underscore the growing recognition and importance of royalties in meeting the industry's capital needs.

Porter's Five Forces & Hamilton's Seven Powers Analysis

Porter's Five Forces

1. Threat of New Entrants: LOW-MODERATE

The barriers to entry in royalty financing are more substantial than they first appear. While the basic business model is replicable, the execution requires:

- Deep scientific expertise: Evaluating pharmaceutical royalties requires understanding regulatory pathways, competitive dynamics, patent law, and medical science—expertise that takes years to develop.

- Massive capital base: This reflects an important competitive advantage—scale and rapid access to substantial capital. Smaller entrants simply cannot compete for the largest, most attractive deals.

- Relationships built over decades: Royalty Pharma has cultivated relationships with academic institutions, research hospitals, and pharmaceutical companies since 1996. These relationships provide proprietary deal flow.

Royalty Pharma has provided a roadmap for other financiers to follow. New entrants like KKR-backed HCRx are competing, but they're primarily targeting different segments of the market rather than directly challenging Royalty Pharma's dominance in large transactions.

2. Bargaining Power of Suppliers (Royalty Sellers): MODERATE

Royalty holders—biotechs, universities, foundations—have alternatives, but Royalty Pharma's scale and reputation provide significant advantages. The company can close larger deals faster than competitors, and its track record of fair dealing encourages repeat business.

The company has a strong track record over nearly two decades of completing multiple transactions with partners. Recently, it completed its second transaction with Agios and its third transaction with Cytokinetics and PTC.

3. Bargaining Power of Buyers: N/A

Royalty Pharma occupies an unusual position—it IS the buyer. Once it owns a royalty, it collects payments from drug marketers who have no choice but to pay their contractual obligations. There's no negotiation on royalty rates after the fact.

4. Threat of Substitutes: MODERATE

Alternative financing options exist—traditional equity, debt, venture capital, big pharma partnerships. Biopharma has shown growing interest in royalty financing to fund clinical development and drug product launches. Royalty transactions offer an alternative to traditional equity financing and non-dilutive partnership deals, as this strategy avoids equity ownership dilution, helping founders maintain stable control of their companies. For the investor, this asset class offers a hedge against macroeconomic volatility.

However, depressed equity valuations have prompted more companies to seek non-dilutive capital including royalty financing—actually expanding the addressable market.

5. Competitive Rivalry: MODERATE AND INCREASING

In late 2022, HealthCare Royalty Partners struck a deal with Atara Biotherapeutics to take royalties in exchange for $31 million upfront cash to support the launch of Ebvallo in Europe. Similarly, HealthCare Royalty Partners' deal with Atara signifies growing confidence to expand portfolios beyond traditional oral small molecules and biologics.

In April 2020, Blackstone Life Sciences led a $2 billion strategic collaboration with Alnylam anchored around the acquisition of a royalty interest in inclisiran (Leqvio), an innovative product.

Competition is intensifying, but Royalty Pharma's dominance in large transactions remains unchallenged.

Hamilton's Seven Powers

1. Scale Economies: STRONG

Royalty Pharma's scale creates multiple advantages. The company can negotiate better terms on its debt financing, deploy capital on transactions too large for competitors, and spread its modest fixed costs across a growing revenue base. Since 2020, Royalty Pharma has announced transactions of approximately $15.5 billion, including approximately $2.8 billion in 2024.

2. Network Economies: MODERATE

Reputation attracts deal flow; successful deals breed more opportunities. The company's collaborative approach—providing fair value and maintaining long-term relationships—has created a virtuous cycle where institutions prefer to work with Royalty Pharma.

3. Counter-Positioning: STRONG (historically)

Royalty Pharma, founded in 1996, has an unusual business model, somewhere between the National Institutes of Health and a hedge fund. The company essentially created an entirely new asset class that traditional pharma and financial institutions couldn't easily replicate. While competition has emerged, Royalty Pharma's first-mover advantage in building relationships and expertise remains significant.

4. Switching Costs: LOW

Royalty sellers can choose any buyer—there's no lock-in once a transaction is complete. However, long-term relationships and track record matter for repeat business, creating soft switching costs.

5. Branding: STRONG

Founded in 1996, Royalty Pharma is the largest buyer of biopharmaceutical royalties and a leading funder of innovation across the biopharmaceutical industry. The company's pioneer status and 25+ year track record provide significant credibility when competing for transactions.

6. Cornered Resource: MODERATE

Deep scientific expertise and relationships built over decades represent difficult-to-replicate resources. The team's specialized due diligence capabilities and understanding of pharmaceutical development create sustainable advantages.

7. Process Power: MODERATE

Royalty Pharma has developed proprietary processes for evaluating, structuring, and monitoring royalty investments that competitors have struggled to replicate at scale.

Financial Performance and Key Metrics

2024 Performance

"We had an incredibly successful 2024, delivering double-digit growth in Royalty Receipts, which was significantly above our initial guidance, and deploying $2.8 billion of capital on value-enhancing royalties," said Pablo Legorreta, Royalty Pharma's founder and Chief Executive Officer.

Portfolio Receipts of $742 million in Q4 2024 and $2,801 million for FY 2024. Royalty Receipts growth of 12% in Q4 2024 and 13% for FY 2024.

2025 Guidance and Outlook

Royalty Pharma expects 2025 Portfolio Receipts to be between $2,900 million and $3,050 million, representing expected growth of 4% to 9%.

Royalty Pharma expects to benefit in 2025 from new product launches, including Servier's Voranigo, Bristol Myers Squibb's Cobenfy, Ascendis' Yorvipath, Syndax and Incyte's Niktimvo and Geron's Rytelo.

Long-Term Targets

Royalty Pharma expects to deliver at least a mid-teens average total shareholder return (TSR) over 2025-2030, driven by double-digit growth in Portfolio Cash Flow and its growing dividend. Furthermore, Royalty Pharma sees the potential for significant upside beyond a mid-teens total shareholder return as the value of its unique intellectual capital and investment platform are recognized following the completion of the Manager internalization.

The company aims to deliver Portfolio Receipts of $4.7 billion or more by 2030, exceeding consensus expectations.

Key Risks and Considerations

Patent Expirations and Generic Competition

The most significant risk facing Royalty Pharma is the inevitable expiration of patents protecting the drugs in its portfolio. When patents expire, generic competitors quickly erode sales, drastically reducing royalty revenues. Successful royalty investors proactively manage this risk by constructing diversified portfolios with staggered patent expirations.

In May 2025, Camber Pharmaceuticals announced the U.S. launch of eltrombopag (the first AB-rated generic for Promacta). As a result, Royalty Pharma expects Royalty Receipts from Promacta to decline.

Concentration Risk

While Royalty Pharma has diversified its portfolio, the cystic fibrosis franchise remains its largest revenue contributor. Any unexpected developments affecting Vertex's CF drugs—regulatory issues, competitive threats, or manufacturing problems—could materially impact results.

Regulatory and Clinical Risks

Investments in earlier-stage products carry heightened regulatory and clinical risk. As Royalty Pharma has expanded its development-stage portfolio, it has taken on more clinical trial risk than its historical business model.

Competition for Deals

Competition from well-capitalized players, including larger platforms like Royalty Pharma and Blackstone, can compress yields and make sourcing attractive transactions more challenging.

Balance Sheet Leverage

As of December 31, 2024, Royalty Pharma had cash and cash equivalents of $929 million and total debt with principal value of $7.8 billion. The company uses significant leverage to fund acquisitions, which amplifies both returns and risks.

Bull vs. Bear Case

Bull Case

-

Structural tailwinds: "As capital demands grow and global innovation accelerates, the biopharma industry is evolving towards a more diversified funding model, with royalties gaining prominence as a tailored funding solution capable of supporting biopharma's significant capital requirements."

-

Management internalization: The 2025 internalization removes the external management fee drag, adds over $1.6 billion in cumulative savings over ten years, and could attract investors who previously avoided the stock due to its structure.

-

Development-stage optionality: The company has significantly expanded its development-stage portfolio, creating potential upside from drug approvals that isn't fully reflected in current consensus estimates.

-

Capital return: Royalty Pharma's Board authorized a $3 billion share repurchase program, with $2 billion intended to be repurchased in 2025.

-

Dominant market position: With 77% market share in large transactions and repeat business from key partners, Royalty Pharma's competitive moat remains formidable.

Bear Case

-

Patent cliff concerns: Key royalties including Trikafta face patent expirations in the late 2030s, and the company must continuously deploy capital to replace declining assets.

-

Increasing competition: KKR's acquisition of Healthcare Royalty Partners and Blackstone's growing life sciences platform could compress returns on new deals and make attractive acquisitions harder to source.

-

Concentration risk: Despite diversification efforts, the CF franchise remains dominant, creating single-asset risk.

-

Regulatory uncertainty: Drug pricing legislation, accelerated generic competition, and changes to patent law could impact the value of pharmaceutical royalties broadly.

-

Returns on new capital: As the market grows more competitive, Royalty Pharma's returns on newly deployed capital may compress relative to historical investments.

Key Metrics to Watch

For investors monitoring Royalty Pharma, three KPIs stand out as the most important indicators of business performance:

1. Royalty Receipts Growth Rate This metric captures the organic growth of the existing portfolio, excluding milestone payments and other non-recurring items. Double-digit Royalty Receipts growth indicates that the underlying drug assets are performing well and that new royalty acquisitions are contributing meaningfully to revenue.

2. Capital Deployment vs. Returns Watch the relationship between capital deployed annually and the company's stated return targets (mid-teens IRRs for approved products, higher for development-stage). If deployment accelerates while returns compress, it may signal increased competition for deals. The company targets $10-12 billion in capital deployment over the five years from 2022.

3. Portfolio Diversification Metrics Monitor the revenue contribution from the top royalty (currently CF franchise) and the number of royalties contributing more than 5% of receipts. Improving diversification reduces single-asset risk and suggests successful portfolio construction.

Conclusion: The Quiet Revolution in Biopharma Finance

Royalty Pharma's story is fundamentally about the power of a simple insight, relentlessly executed over three decades. Pablo Legorreta recognized that pharmaceutical royalties were misunderstood assets—valued inappropriately by their owners and ignored by traditional investors. He built a platform to correct that inefficiency, and in doing so, helped revolutionize how biopharma innovation gets funded.

"We're witnessing the emergence of a new funding paradigm in biopharma," said Pablo Legorreta. "As highlighted in Deloitte's publication, royalties are increasingly recognized as a vital component of a diversified capital structure to help fund innovation and advance scientific breakthroughs."

The company's trajectory—from boutique royalty investor to the largest player in a market it essentially created—illustrates several timeless investment themes. First, financial innovation often comes not from complex engineering but from recognizing simple inefficiencies that others overlook. Second, relationships and reputation compound over time, creating advantages that are nearly impossible for competitors to replicate quickly. Third, patient capital deployed with expertise can generate extraordinary returns.

For investors, Royalty Pharma presents a distinctive proposition: exposure to pharmaceutical success without the full burden of pharmaceutical risk. The company collects a toll on some of the world's most important medicines—drugs that treat cancer, rare diseases, neurological conditions, and infections. When those drugs succeed, Royalty Pharma succeeds. When they fail, the diversified portfolio provides protection.

The 2025 manager internalization marks a new chapter in this story. With simplified structure, enhanced governance, and significant cost savings, Royalty Pharma enters its fourth decade better positioned than ever to capitalize on the growing demand for royalty financing. The question for investors is whether the company's historical dominance can persist as competition intensifies and the market matures.

What remains unchanged is the fundamental thesis that made Royalty Pharma successful in the first place: the pharmaceutical industry will continue to innovate, that innovation will continue to require capital, and someone will continue to collect royalties on the medicines that result. For nearly thirty years, that someone has been Royalty Pharma. The market is betting that won't change anytime soon.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube