Mankind Pharma: The Domestic Giant's Quest for Global Relevance

I. Introduction & Episode Roadmap

In the sprawling landscape of Indian pharmaceuticals, where multinational giants and export-focused generics manufacturers dominate headlines, Mankind Pharma stands as a fascinating anomaly. As the fourth largest pharmaceutical company in India by domestic sales, it has built an empire worth over ₹1 lakh crore in market capitalization while deriving an astonishing 97% of its operating revenue from the Indian market alone. This concentration, which would make most global investors nervous, has been precisely the source of Mankind's strength.

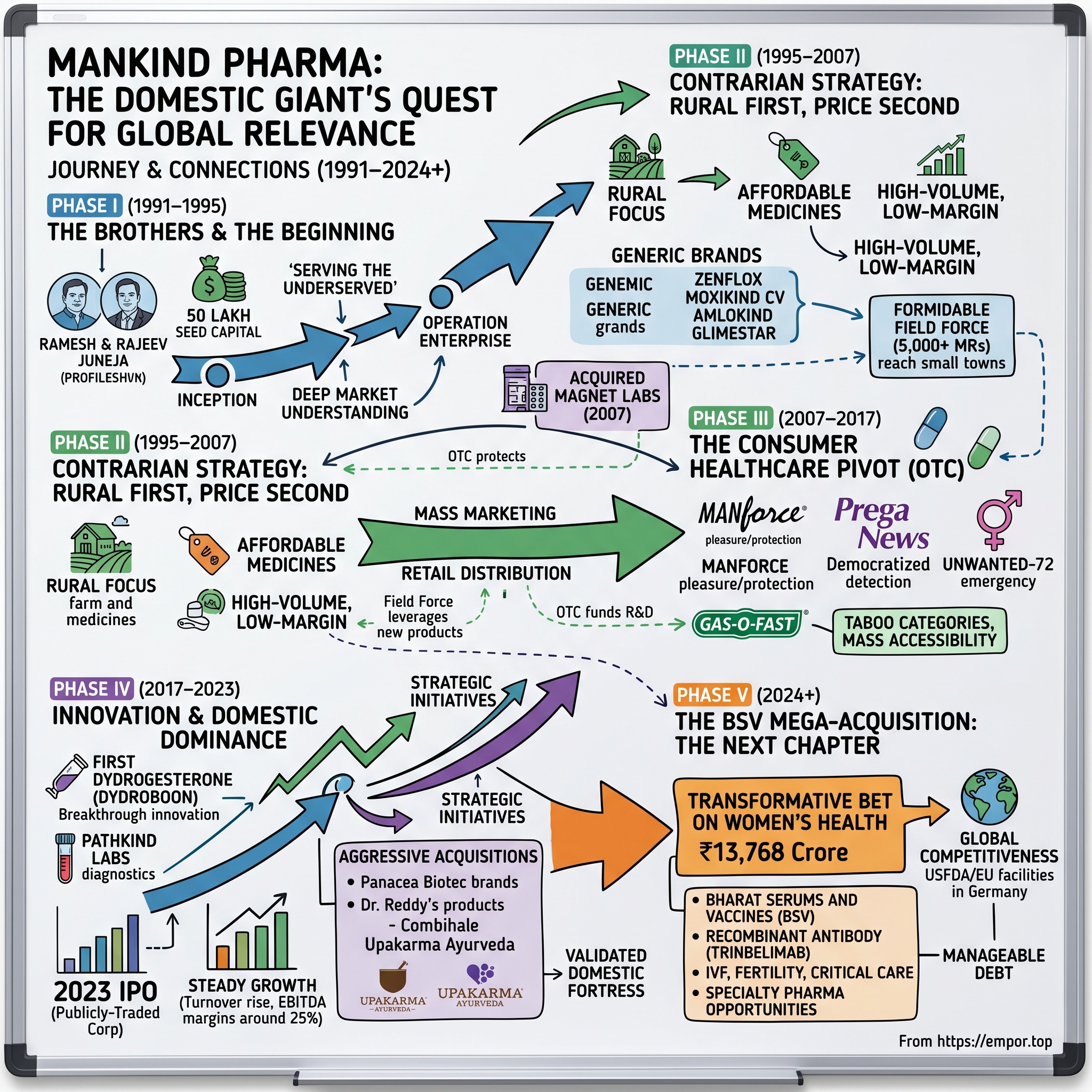

The story of Mankind Pharma is fundamentally the story of two brothers who saw opportunity where others saw limitation. Ramesh and Rajeev Juneja didn't set out to conquer global markets or develop cutting-edge biologics. Instead, they focused relentlessly on a simple but powerful mission: making quality medicines affordable and accessible to every corner of India, particularly the rural heartlands that most pharmaceutical companies ignored.

What makes Mankind's journey particularly compelling is its timing and trajectory. Starting in 1991 with just ₹50 lakhs in seed capital, the company began operations during India's liberalization era, when the pharmaceutical landscape was experiencing seismic shifts. The brothers didn't have the backing of established business houses or access to significant venture capital. What they had was deep industry knowledge, an understanding of India's unique healthcare challenges, and an unwavering belief that serving the underserved could build a sustainable business empire.

This is not just another pharmaceutical success story. It's a masterclass in market segmentation, distribution innovation, and the power of focusing on one geography with laser precision. While peers rushed to capture export markets and compete with global generics giants, Mankind built a fortress in India's domestic market that has proven nearly impregnable. The company's evolution from a prescription drug manufacturer to a consumer healthcare powerhouse, its audacious ₹13,768 crore acquisition of Bharat Serums and Vaccines in 2024, and its journey to public markets in 2023 offer profound lessons for entrepreneurs operating in emerging markets.

The central narrative tension that runs through Mankind's story is this: Can a company built on serving India's masses at affordable prices transform itself into a specialty pharmaceutical player without losing its core identity? And perhaps more importantly, in an increasingly globalized pharmaceutical industry, is extreme domestic focus a strategic advantage or an eventual liability?

II. The Brothers & the Beginning (1991–1995)

The pharmaceutical landscape of early 1990s India was ripe for disruption. The License Raj was finally loosening its grip, economic liberalization was opening new possibilities, and yet healthcare accessibility remained a distant dream for millions of Indians. Into this environment stepped two brothers with complementary skills and a shared vision that would eventually reshape India's pharmaceutical industry.

Ramesh C. Juneja's journey began in 1974 when he started his career with KeePharma Ltd. as a medical representative. In 1975, he joined Lupin Limited and worked there as first line manager for almost 8 years. This wasn't just a job for Ramesh; it was an education in the ground realities of Indian healthcare. Traveling across territories, meeting doctors in small towns, witnessing patients unable to afford basic medications—these experiences would shape the philosophy of the company he would later build.

The younger brother, Rajeev Juneja, took a different but equally instructive path. While details of his early career are less documented, what's clear is that he gained deep market insights working in pharmaceutical sectors before deciding to join forces with his brother. Rajeev actually wanted to join the Indian Army, but he decided to serve mankind in another way. This decision to pivot from military service to healthcare service would prove prophetic, given the company's eventual name and mission.

Thirty-three years ago, the idea of Mankind Pharma became a reality with 20 employees and a seed capital of INR 5,000,000. The timing was deliberate. India's pharmaceutical industry in 1991 was dominated by multinational corporations on one end and established Indian companies focused on exports on the other. The domestic market, particularly for affordable medicines, was underserved. The brothers saw this gap not as a limitation but as an opportunity.

Mankind Pharma was incorporated in 1991, and actively started its operations in 1995, with the contributions of two brothers, Ramesh C. Juneja and Rajeev Juneja, along with their brother-in-law P.K. Arora and nephew Sheetal Arora, making it truly a family enterprise from the start. The four-year gap between incorporation and operations wasn't idle time—it was spent in meticulous planning, understanding regulatory requirements, and most importantly, developing a go-to-market strategy that would differentiate them from established players.

What made the Juneja brothers' approach revolutionary was their fundamental reframing of the pharmaceutical business model. While competitors focused on high-margin specialty drugs or export markets with better pricing power, Mankind chose to focus on high-volume, affordable medications for the Indian masses. This wasn't charity—it was a calculated bet that volume could compensate for lower margins if execution was flawless.

In 1983, he resigned from Lupin and started his own company Bestochem in Partnership. In 1994, he withdrew his ownership from Bestochem, clearing the way for Mankind's launch in 1995. This earlier entrepreneurial venture gave Ramesh crucial insights into running a pharmaceutical business, lessons that would prove invaluable in Mankind's early days.

The brothers brought complementary skills to the venture. Ramesh, with his extensive field experience and deep understanding of doctor-patient dynamics, focused on market strategy and relationships. Rajeev, described as having gained "deep market insights," brought operational expertise and a vision for scaling. Together, they possessed something rare in Indian business at the time: a willingness to play the long game in a market segment that others had written off as unprofitable.

The initial business model was deceptively simple but operationally complex. Instead of setting up expensive research facilities to develop new molecules, Mankind would focus on proven generic formulations. Instead of targeting metro cities where competition was fierce, they would build distribution networks reaching into rural India. Instead of pricing for maximum margin, they would price for maximum accessibility. Every decision reflected a philosophy that Ramesh would later articulate: providing quality life saving drugs at affordable cost.

The seed capital of ₹50 lakhs (₹5 million) was modest even by 1991 standards. Most pharmaceutical startups required significantly more capital for manufacturing facilities, regulatory approvals, and working capital. The brothers made this work through extreme capital efficiency—outsourcing manufacturing initially, keeping overhead low, and reinvesting every rupee of profit back into growth. Mankind Pharma reportedly started with 20 employees and launched in two states in the first year of its operation.

What's remarkable about Mankind's founding story is how un-remarkable it appeared at the time. No venture capital backing, no revolutionary technology, no high-profile board members. Just two brothers who understood the Indian pharmaceutical market's inefficiencies and had the operational discipline to exploit them. They weren't trying to build the next Pfizer or Glaxo; they were trying to ensure that a daily wage laborer in Bihar could afford antibiotics for his child.

The decision to focus on the domestic market exclusively was both brave and controversial. In 1995, the conventional wisdom was that Indian pharmaceutical companies needed to tap export markets for growth and better margins. The domestic market was seen as price-sensitive, highly regulated, and dominated by doctor relationships that took years to build. The Juneja brothers saw these same characteristics and reached the opposite conclusion: these barriers to entry would become moats once they were overcome.

The early months were grueling. Without established relationships, getting doctors to prescribe Mankind's products was an uphill battle. The company's unknown brand meant pharmacists were reluctant to stock their medicines. Distributors demanded higher margins to take on an unproven company's products. Every sale had to be earned through persistent relationship building and consistent product quality.

III. The Contrarian Strategy: Rural First, Price Second (1995–2007)

While established pharmaceutical companies battled for market share in India's metros, Mankind Pharma executed a strategy so contrarian that industry veterans dismissed it as naive. Between 1995 and 2007, the company systematically built what would become one of India's most formidable pharmaceutical distribution networks by focusing on the markets everyone else ignored: rural India, Tier 3 and Tier 4 cities, and price-sensitive therapeutic segments.

Mankind Pharma initially targeted price-sensitive drugs, with a focus on rural market; its early products included antibacterial drug Zenflox and prescription antibiotic Moxikind CV, which were priced at a steep discount to the existing products in the market. These weren't random choices. Zenflox, an antibacterial drug, and Moxikind CV, a prescription antibiotic, addressed two critical needs in underserved markets: treating common infections that, if left untreated, could become life-threatening, and doing so at prices that didn't force families to choose between medicine and meals.

The pricing strategy was radical for its time. While competitors maintained healthy margins of 40-50% on antibiotics, Mankind operated on margins as low as 15-20%. This wasn't sustainable by conventional metrics, but the brothers understood something their competitors didn't: in a country where out-of-pocket healthcare spending dominated, affordability wasn't just a competitive advantage—it was the only way to unlock massive untapped demand.

The field force strategy became Mankind's secret weapon. While multinational companies concentrated their medical representatives in urban areas where doctors saw more patients and had higher prescription values, Mankind deployed teams to small towns and rural districts. By 2000, the company had built one of India's largest medical representative networks, with teams reaching doctors in places where no pharmaceutical representative had visited before. These weren't just salespeople; they were evangelists for affordable healthcare, building relationships one rural clinic at a time.

The company's product selection philosophy reflected deep market understanding. Instead of chasing blockbuster drugs or specialty medications, Mankind focused on high-volume, chronic therapies—the everyday medicines that millions of Indians needed regularly. Antibiotics for infections, antacids for digestive issues, basic pain relievers, and medications for chronic conditions like hypertension and diabetes. These weren't glamorous products, but they represented the bulk of India's pharmaceutical consumption.

Discovery Mankind offers a product-mix ranging from Monotherapy to Combination therapy, and caters to the medical needs of patients with products like Dynaglipt, Glimestar, Glykind-M, & Voglistar. The 2004 launch of Amlokind (for hypertension) and Glimestar (for diabetes) marked a pivotal moment in Mankind's evolution. These weren't just products; they were strategic beachheads in the massive and growing chronic disease market.

The genius of Mankind's approach to chronic therapies lay in understanding the Indian patient's journey. In rural India, medication adherence for chronic conditions was abysmal, primarily due to cost. By pricing Amlokind and Glimestar at 30-40% below competing brands, Mankind didn't just capture market share—they expanded the market itself, bringing treatment to patients who had previously gone without.

The total net worth of Mankind Pharma's products are as follows: Moxikind (Rs. 1984 million), Telmikind (Rs. 1801 million), Amlokind (Rs. 1472 million), Nurokind (Rs. 1123 million), Zenflox (Rs. 888 million), Cefakind (Rs. 788 million). These numbers tell the story of a portfolio strategy that prioritized volume over margin, accessibility over exclusivity.

The rural-first approach required rethinking every aspect of pharmaceutical distribution. In urban areas, stockists and distributors operated on predictable cycles with reliable infrastructure. Rural distribution meant dealing with erratic electricity, poor roads, limited cold chain facilities, and distributors who often doubled as general merchants. Mankind didn't try to force urban models onto rural markets; instead, they built a distribution system designed for rural realities.

This meant smaller, more frequent shipments to prevent stockouts. It meant packaging medicines in smaller strips to match rural purchasing power. It meant educating pharmacists about proper storage in shops without air conditioning. Every operational decision reflected a deep respect for the constraints of rural commerce.

The company acquired Magnet Labs Pvt. Ltd. to enter the antipsychotic segment in 2007. This acquisition wasn't just about adding products; it was about entering a therapeutic area with massive unmet need in India. Mental health medications were expensive and stigmatized, creating a perfect opportunity for Mankind's affordable, accessible approach.

The field force became Mankind's greatest competitive advantage during this period. By 2007, the company had over 5,000 medical representatives, one of the largest forces in Indian pharma. But size alone wasn't the differentiator—it was deployment and training. Mankind's representatives were trained not just in product knowledge but in understanding local healthcare ecosystems. They knew which doctors served the poorest patients, which pharmacies stocked generic alternatives, which distributors could reach the most remote areas.

The company's approach to doctor relationships was equally unconventional. While competitors wooed doctors with international conferences and expensive gifts, Mankind focused on consistent service and reliable product availability. A doctor in rural Bihar might never attend a pharma-sponsored conference in Bangkok, but he knew that when he prescribed a Mankind product, it would be available at the local pharmacy at a price his patients could afford.

The price penetration policy is the driving force behind Discovery Mankind's market success. By keeping profit margins at a minimum, it has extended the benefits to patients by establishing a mutual platform of trust and solidarity between prescribers and products. This wasn't corporate social responsibility dressed up as business strategy—it was a fundamental reimagining of the pharmaceutical value chain.

The "Mankind System," as employees called it, had three pillars: price (always 25-40% below competition), presence (available even in the smallest pharmacy), and persistence (medical representatives who visited regularly, regardless of prescription volumes). This system created a virtuous cycle: lower prices led to higher volumes, which justified continued rural presence, which built doctor trust, which drove more prescriptions.

By 2005, Mankind had achieved something remarkable: brand recognition in markets where brands supposedly didn't matter. Rural patients began asking for "Mankind ki dawai" (Mankind's medicine), trusting the company's products even when they couldn't pronounce the drug names. This brand equity, built painstakingly over a decade, would become invaluable when the company eventually entered the consumer healthcare market.

The contrarian strategy extended to research and development as well. While peers invested heavily in novel drug discovery or complex generics for regulated markets, Mankind focused on reformulation and combination drugs for the Indian market. Creating fixed-dose combinations that improved patient compliance, developing flavored syrups for pediatric medications, making scored tablets for dose flexibility—these incremental innovations might not win scientific awards, but they solved real problems for Indian patients.

The financial discipline during this period was extraordinary. Despite rapid growth, the company remained entirely self-funded, reinvesting profits rather than raising external capital. This wasn't just financial conservatism; it was strategic autonomy. Without external investors demanding quick returns or strategic pivots, the Juneja brothers could maintain their long-term focus on rural markets even when quarterly results disappointed.

By 2007, Mankind had quietly become one of India's top 10 pharmaceutical companies by domestic sales, though few outside the industry noticed. The company didn't feature in business magazines or win industry awards. But in thousands of small towns across India, Mankind had become synonymous with affordable, quality healthcare. The foundation was set for the next phase: taking this trust and extending it beyond prescriptions into consumer healthcare.

IV. The Consumer Healthcare Pivot: From Prescriptions to OTC (2007–2017)

The company ventured into the over-the-counter segment in 2007, focusing primarily on sexual healthcare products. This decision would prove to be one of the most transformative in Mankind's history, catapulting it from a prescription pharmaceutical company to a household name across India. The timing was deliberate and the execution masterful, but the journey into consumer healthcare required Mankind to master entirely new competencies: mass marketing, retail distribution, and most challengingly, navigating the complex cultural sensitivities around sexual health in conservative Indian society.

The entry into OTC wasn't a random diversification. The Juneja brothers recognized that their decade-long investment in distribution infrastructure and brand trust could be leveraged beyond prescription medicines. More importantly, they identified massive gaps in India's consumer healthcare market, particularly in categories that established players avoided due to cultural taboos or perceived limited market potential.

Mankind Pharma's consumer healthcare brands are the largest-selling in their respective categories, including Manforce in condoms, Prega News in pregnancy test kits, and Unwanted-72 in emergency contraception. Each of these brands tells a story of market creation, not just market capture. When Mankind entered the condom market with Manforce, the category was dominated by government programs distributing free condoms and a few premium brands targeting urban consumers. The middle market—affordable but aspirational—barely existed.

Manforce's launch strategy was audacious for a company that had built its reputation on conservative, doctor-focused marketing. The brand didn't just sell protection; it sold pleasure, desire, and modern relationships. The marketing campaigns, featuring Bollywood celebrities and bold imagery, were a radical departure from Mankind's traditional approach. This wasn't the company that quietly sold antibiotics in rural pharmacies anymore.

The genius of Manforce lay in its segmentation strategy. While government condoms were free but associated with family planning programs (and thus unsexy), and premium brands like Durex were expensive and available mainly in urban areas, Manforce positioned itself as the affordable indulgence. Priced at ₹30-40 for a pack of three, compared to ₹60-80 for premium brands, Manforce made protected sex accessible without the stigma of government handouts.

Distribution was equally innovative. Mankind leveraged its pharmaceutical distribution network but added new channels: paan shops, general stores, even roadside vendors. The company understood that condom purchase behavior was different from medicine—it needed to be convenient, discreet, and ubiquitous. By 2010, Manforce was available in over 500,000 outlets across India, many of which had never stocked condoms before.

Manforce Condoms, India's best-selling brand, offers 16 exciting variants to enhance pleasure with protection. The product innovation strategy was relentless. While competitors offered basic variants, Manforce launched flavored condoms (chocolate, strawberry, coffee), dotted and ribbed textures, long-lasting variants, and even condoms with cooling sensations. Each variant addressed specific consumer desires, transforming condoms from a necessary evil to a pleasure enhancer.

The marketing evolution was equally dramatic. Early campaigns focused on safety and responsibility. But as the brand gained traction, messaging shifted to pleasure and intimacy. The tagline evolved from "Protection with Pleasure" to more provocative messaging that pushed cultural boundaries while remaining within acceptable limits. Television commercials, previously unthinkable for condom brands, became regular during late-night slots.

Prega News, launched in 2010, represented a different kind of market creation. Home pregnancy tests existed in India, but they were expensive (₹150-200), available mainly in urban pharmacies, and marketed with clinical coldness. Mankind saw an opportunity to democratize pregnancy detection while addressing the emotional journey of potential motherhood.

Priced at just ₹50, Prega News made home pregnancy testing accessible to middle-class families across India. But pricing was just the beginning. The product design—a simple strip test requiring just a few drops of urine—was foolproof. The packaging included clear instructions in multiple languages with pictorial guides. The marketing emphasized accuracy, privacy, and the emotional moment of discovery.

The distribution strategy for Prega News was particularly innovative. Recognizing that many women in smaller towns might be embarrassed to ask for pregnancy tests, Mankind trained pharmacists to discretely offer the product when women purchased missed-period medications or asked about pregnancy symptoms. The company also pioneered combo packs with sanitary napkins, making purchase less conspicuous.

This is an oral medication, which, if taken within 72 hours of unprotected intercourse, can help eliminate the chances of pregnancy. Unwanted-72, the emergency contraceptive pill, was perhaps Mankind's boldest consumer healthcare launch. Emergency contraception was virtually unknown in India outside of urban gynecology clinics. The product faced multiple challenges: regulatory scrutiny, social stigma, and the need for consumer education about a completely new category.

Mankind's approach to Unwanted-72 was a masterclass in sensitive market development. Instead of mass marketing, which could have triggered backlash, the company focused on education through healthcare professionals. Gynecologists were educated about emergency contraception and encouraged to counsel patients. Pharmacists were trained to provide discreet guidance. The packaging included detailed information about proper use, side effects, and the importance of regular contraception.

The pricing strategy—₹75-100 per pill—balanced accessibility with the need to prevent misuse as regular contraception. The name itself, while direct, addressed the core consumer need without euphemism. Within three years, Unwanted-72 had created a ₹200 crore category that hadn't existed before, potentially preventing thousands of unwanted pregnancies and unsafe abortions.

The success in sexual and reproductive health emboldened Mankind to expand across consumer healthcare. Gas-O-Fast for acidity, launched in flavored sachets at ₹5 each, competed directly with established brands like Eno but at half the price. HealthOK multivitamin tablets targeted the growing health consciousness among middle-class Indians. AcneStar gel addressed teenage skin concerns with prescription-strength ingredients in an OTC format.

Each product launch followed the "Mankind OTC Playbook": identify an underserved need, particularly in Tier 2/3 cities; develop a product that's significantly more affordable than existing options; ensure availability through both pharmaceutical and general trade channels; and market with a mix of aspiration and accessibility. This formula, refined over dozens of launches, transformed Mankind from a pharmaceutical company with some consumer products to a consumer healthcare powerhouse.

Since its inception in 1995, Mankind Pharma has expanded its presence to 34 international markets, supported by a dedicated team of 22,000 employees. It has evolved into the leading pharmaceutical manufacturing and marketing company in India, driven by research and innovation. It ranks No.1* in prescription medicine. Mankind Pharma offers a diverse portfolio of products, including pharmaceuticals, OTC, and FMCG brands. Some notable offerings include Manforce Condoms, Prega News, Unwanted-72 Oral Contraceptive Tablets, Gas-O-Fast, HealthOK Multivitamin Tablets, AcneStar Gel, and more.

The organizational transformation required for OTC success was profound. Mankind had to build new capabilities in brand management, creative advertising, retail merchandising, and consumer research. The company hired talent from FMCG companies, partnered with creative agencies that understood youth culture, and invested in market research to understand rapidly evolving consumer preferences.

The financial impact of the OTC pivot was transformative. By 2017, consumer healthcare contributed nearly 25% of Mankind's domestic revenues but over 35% of profits, thanks to higher margins and lower marketing costs per unit sold. More importantly, OTC products created brand visibility that prescription products never could. Mankind was no longer just known to doctors and patients; it was a household name.

The cultural impact was equally significant. By normalizing conversations around contraception, emergency contraception, and pregnancy testing, Mankind's OTC products contributed to public health in ways that went beyond commercial success. The company's willingness to enter taboo categories with sensitivity and scale helped modernize Indian attitudes toward sexual and reproductive health.

The listing of Mankind Pharma — whose popular products include Manforce condoms and Prega News pregnancy test kits — comes after its IPO, worth up to Rs 4,326 crore, a testament to how these consumer brands had become central to Mankind's identity and valuation. The transformation from a prescription-focused company to a consumer healthcare leader was complete, setting the stage for even more ambitious expansions in the decade ahead.

V. Innovation & Domestic Dominance (2017–2023)

The period from 2017 to 2023 marked Mankind Pharma's most ambitious phase of innovation and consolidation of domestic dominance. This era began with a groundbreaking achievement that would redefine the company's position in the pharmaceutical innovation hierarchy and concluded with strategic acquisitions that expanded its reach into virtually every therapeutic segment.

In 2019, Mankind became the first Indian company and second only in the world to develop and launch Dydrogesterone, a drug used in high-risk pregnancies and infertility by the brand name Dydroboon. This wasn't just another generic launch; it was a statement of technological capability that shattered perceptions about what Indian pharmaceutical companies could achieve. The manufacturing process of Dydrogesterone is very complex as it involves conversion of natural progesterone, requiring sophisticated chemistry and manufacturing expertise that most Indian companies lacked.

The development of Dydroboon took nine years and involved a team of 400 scientists. "We are the first Indian pharmaceutical company to develop this drug and second company in the world," Mankind Group founder and Chairman R C Juneja said. The significance extended beyond technical achievement. Dydrogesterone addressed a critical gap in women's healthcare in India, where pregnancy complications and infertility treatments often required expensive imported medications.

The drug's launch timing was strategic. Abbott's Duphaston, the original dydrogesterone product, dominated the market with limited competition. By developing a generic version, Mankind could offer the medication at significantly lower prices while maintaining quality standards. "The company generated annual sales of approximately ₹250 crores from Dydroboon over four years," said research analysts Tushar Manudhane and Akash Manish Dobhada from Motilal Oswal Financial Services.

In 2017, Mankind Pharma established Pathkind Labs, a provider of diagnostics and healthcare tests. This wasn't a small experiment but a major strategic initiative. "We are foraying into diagnostics space with new venture Pathkind Diagnostics. In the coming 4 years, the company has a plan to invest Rs 305 crore in its new venture, which will start its operation from August 2017," a company statement said.

The diagnostics venture reflected Mankind's understanding of healthcare evolution in India. As chronic diseases became more prevalent and health consciousness grew, diagnostic services were becoming essential to healthcare delivery. "As a part of the strategy, Pathkind would aim to reach out to the masses in tier 2/3 cities in India with the direct approach of providing easily accessible diagnostics services at affordable prices", maintaining Mankind's core philosophy even in this new vertical.

To promote this new venture in the Diagnostics space, Mankind has joined hands with Sanjeev Vashishta. Sanjeev Vashishta has been known for his ability of connecting with people and for his potential to turn around businesses. He was also responsible for the dramatic transformation of SRL's business in just 4 years. This strategic hiring showed Mankind's willingness to bring in external expertise when entering new domains.

The diagnostics business model followed Mankind's proven playbook but adapted for services rather than products. The company is planning to open 12 large labs, 20 rapid response labs and 150 collection centres in 12 months and will operate on a three-tier model, ensuring reach into smaller towns and villages where diagnostic services were virtually non-existent.

The 2022 acquisition spree marked a pivotal shift in Mankind's growth strategy. Panacea Biotec Pharma Ltd. (PBPL) approved the sale of domestic formulations brands of PBPL, for India and Nepal, to Mankind Pharma Limited for Rs 1,872 crore. This acquisition wasn't just about adding products; it was about acquiring established brands with loyal prescriber bases and expanding Mankind's presence in therapeutic areas where it had limited penetration.

The domestic formulations brands being sold have reported revenue from operations of Rs 132 crore for H1 FY2021-22 which is around 42 per cent of the company's consolidated revenue for H1 FY2021-22. The deal structure was particularly clever—Mankind retained Panacea's sales force, instantly adding experienced relationships in new therapeutic areas without the time and cost of building from scratch.

It then acquired a respiratory treatment product, and an infant skincare brand from Dr. Reddy's Laboratories. The acquisition of Combihale and Daffy from Dr. Reddy's demonstrated Mankind's strategic focus on high-growth therapeutic segments. Combihale, a drug used for treating asthma and chronic obstructive pulmonary disease has a category market size of Rs 900 crore which is growing at 14 percent (IQVIA).

It also bought a majority stake in the Ayurvedic and herbal products manufacturer, Upakarma Ayurveda. This acquisition reflected Mankind's recognition of the growing consumer preference for traditional medicine, particularly in preventive healthcare and wellness segments.

In 2022, the company entered agritech and pet care segments. These seemingly unrelated diversifications made strategic sense when viewed through Mankind's distribution lens. The company's vast rural network, built over decades for pharmaceutical distribution, could easily carry adjacent products to the same customer base.

The manufacturing scale achieved during this period was staggering. As of 2023, Mankind Pharma had 25 factories and 6 R&D centres in India. This infrastructure wasn't just about capacity; it represented strategic redundancy, regulatory compliance across multiple standards, and the ability to manufacture everything from simple tablets to complex formulations like Dydrogesterone.

With 6 cutting-edge R&D facilities, we pioneer breakthroughs like Dydrogesterone in pharmaceutical excellence. The R&D investment marked a crucial evolution. Mankind was no longer content being a fast follower; it was investing in creating intellectual property and developing complex generics that few Indian companies could manufacture.

The company's approach to market dominance was methodical. Multiple brands within the same therapeutic area allow us to cater to the requirements of a wide range of patients. This multi-brand strategy in single therapeutic areas allowed Mankind to capture different price points and prescriber preferences without cannibalizing its own products.

Innovation extended beyond products to business processes. The company's investment in digital transformation, while maintaining its traditional field force strength, created a hybrid model that could serve both digitally-savvy urban doctors and relationship-driven rural practitioners. The implementation of data analytics for sales force effectiveness, inventory management, and demand forecasting improved operational efficiency significantly.

The talent strategy during this period was equally important. The second generation of the founding families began taking active roles. Since joining in 2009, he has overseen R&D, manufacturing, supply chain, and IT, leading Mankind's successful IPO in 2023. He spearheaded Mankind Pharma's entry into the US market and secured USFDA approvals for regulated markets. This generational transition brought fresh perspectives while maintaining family control.

The financial discipline remained exceptional despite aggressive expansion. Each acquisition was funded through internal accruals or structured debt, avoiding equity dilution. The company maintained industry-leading working capital management, with cash conversion cycles among the best in Indian pharma.

Mankind Pharma has shown significant growth over the past five years, with turnover rising from ₹6,400 crores to ₹10,550 crores. "The company has shown a consistent double-digit growth rate for the past three years, with a five-year CAGR of 13%," added Sapale. This consistent growth, achieved while maintaining profitability and investing in R&D, demonstrated the sustainability of Mankind's business model.

The domestic fortress strategy proved its worth during this period. While export-focused peers struggled with regulatory issues in developed markets and pricing pressure in generics, Mankind's domestic focus provided stable, predictable growth. The company's deep understanding of Indian prescriber behavior, patient preferences, and distribution dynamics created competitive advantages that multinational competitors couldn't replicate despite superior resources.

By 2023, Mankind had achieved something remarkable: it had become simultaneously the most affordable and one of the most innovative Indian pharmaceutical companies. This apparent contradiction—usually companies are either innovative or cost-focused, not both—was resolved through Mankind's unique approach to innovation. Instead of pursuing novel drug discovery, the company focused on innovative delivery mechanisms, patient-friendly formulations, and manufacturing complex generics that improved patient outcomes while maintaining affordability.

The strategic choices made during this period—building diagnostic capabilities, acquiring established brands, investing in complex manufacturing, and entering adjacent segments—positioned Mankind perfectly for its next phase: going public and making the transformative BSV acquisition that would redefine its future.

VI. Going Public: The 2023 IPO

The decision to go public in 2023 represented a pivotal moment in Mankind Pharma's journey, marking the transition from a closely-held family enterprise to a publicly-traded corporation. After 28 years of bootstrapped growth and careful capital management, the timing of the IPO was strategically perfect, coming at a moment when the company had achieved domestic dominance, diversified revenue streams, and demonstrated consistent profitability.

Mankind Pharma IPO is a bookbuilding of Rs 4,326.36 crores. The issue is entirely an offer for sale of 4.01 crore shares. This structure was significant—no fresh capital was being raised for the company. Instead, existing shareholders, primarily the founding families and private equity investors who had acquired stakes over the years, were partially monetizing their investments.

Mankind Pharma IPO bidding started from April 25, 2023 and ended on April 27, 2023. The allotment for Mankind Pharma IPO was finalized on Wednesday, May 3, 2023. The shares got listed on BSE, NSE on May 9, 2023. The three-day window saw dramatic shifts in investor sentiment, with institutional investors ultimately driving the overwhelming demand.

Mankind Pharma IPO price band is set at ₹1080 per share. The minimum lot size for an application is 13. The minimum amount of investment required by retail investors is ₹13,338. But it is suggested to the investor to bid at the cutoff price to avoid the oversubscription senerio, which is about to ₹14,040. The pricing reflected confidence in Mankind's business model but also acknowledged the complete OFS nature of the issue.

The subscription numbers told a fascinating story of divergent investor perspectives. The Mankind Pharma IPO QIB subscription is 49.16 times till 2023-04-27 19:02:00. The Mankind Pharma IPO is subscribed 15.32 times till 2023-04-27 19:02:00. The Total Number of shares bid are 429512902. The massive institutional oversubscription reflected professional investors' confidence in Mankind's domestic franchise and growth prospects.

The quota reserved for qualified institutional bidders was subscribed 49.16 times, while the portion for non-institutional bidders was booked 3.80 times. The allocation of retail investors was subscribed merely 92 per cent. This divergence was unusual—retail investors, typically enthusiastic about well-known consumer brands, showed lukewarm interest despite Mankind's popular products like Manforce and Prega News.

The retail skepticism had multiple explanations. First, the complete OFS nature meant no growth capital for the company, raising questions about why promoters were selling if prospects were so bright. Second, at the upper price band of ₹1,080, the valuation of 19 times forward earnings seemed rich compared to established pharmaceutical peers. Third, the company's 97% domestic revenue concentration concerned investors worried about growth limits.

The anchor investor allocation provided early validation. On 24th April 2023, Mankind Pharma Ltd did an anchor placement 30% of the IPO size getting absorbed by the anchors. Out of the 4,00,58,844 shares on offer, the anchors picked up 1,20,17,652 shares accounting for 30% of the total IPO size. The quality of anchor investors—including sovereign wealth funds, global pharmaceutical funds, and marquee domestic institutions—signaled sophisticated investor confidence.

The entire anchor allocation was made at the upper price band of Rs1,080. This was significant—anchors paying the maximum price indicated their belief that the stock would trade above IPO levels. Their confidence proved prescient.

The book-building process revealed interesting dynamics. QIB bids typically get bunched on the last day and while the heavy demand for the anchor placement had given an indication of the institutional appetite for the Mankind Pharma Ltd IPO subscription overall, the actual demand did turn to be quite robust for the IPO. The last-day surge in QIB demand suggested that institutional investors had completed their due diligence and decided Mankind's domestic moat justified the valuation.

Macquarie's pre-IPO research note proved influential. "At the upper band price of Rs 1,080, the stock valued at 19 times PER on FY25e EPS of Rs 56. Macquarie initiated coverage with Rs 1,400 target based on 25 times FY25e PER, with an Outperform rating." This bullish view from a respected global brokerage provided institutional investors with analytical support for aggressive bidding.

The listing day, May 9, 2023, delivered spectacular returns for successful allottees. The IPO of Mankind Pharma was open for subscription between April 25-27 in the price range of Rs 1,026-1,080 per share as the company raised 4,326 crore and issue was overall booked 15.32 times. Mankind Pharma share bumper listing: Stock debuts at 20% premium.

On the listing day, the shares of Mankind Pharma opened ₹1,300.00, touching its day's high at ₹1,430.00. The strong debut validated institutional confidence while leaving retail investors who hadn't participated regretting their caution.

The IPO structure revealed interesting details about ownership transition. 4326.36 crores, comprising an offer for sale of 3,705,443 equity shares aggregating to Rs. 400.18 crores by Ramesh Juneja, 3,505,149 equity shares aggregating to Rs. 378.56 crores by Rajeev Juneja, 2,804,119 equity shares aggregating to Rs. 302.85 crores by Sheetal Arora. The founding families were selling roughly equal proportions, maintaining their relative ownership stakes while achieving partial liquidity.

Ramesh Juneja, Rajeev Juneja, Sheetal Arora, Ramesh Juneja Family Trust, Rajeev Juneja Family Trust, and Prem Sheetal Family Trust are the company promoters. The use of family trusts alongside individual holdings showed sophisticated succession planning, ensuring family control would continue across generations while allowing for liquidity events.

The private equity exit was equally noteworthy. 17,405,559 equity shares aggregating to Rs. 1879.80 crores by Cairnhill Cipef Limited, 2,623,863 equity shares aggregating to Rs. 283.38 crores by Cairnhill CGPE Limited, 9,964,711 equity shares aggregating to Rs. 1076.19 crores by Beige Limited. These funds, having invested during Mankind's growth phase, achieved substantial returns, validating the company's value creation over the years.

The IPO prospectus revealed fascinating insights into Mankind's competitive position. According to the IQVIA Medical Audit report of March 2022, 80% of doctors in India have been prescribed medicines by Mankind Pharma. In the last five years, Mankind Pharma has generated the highest share of prescriptions in the Indian Pharmaceutical Market. These statistics underscored Mankind's extraordinary reach and influence in Indian healthcare.

Mankind Pharma is India's fourth largest pharmaceutical company in terms of Domestic Sales and third largest in terms of sales volume for MAT December 2022. The volume leadership despite being fourth in value highlighted Mankind's lower price points—a deliberate strategy that had driven market share gains for decades.

It has one of the largest networks of medical representatives in PAN India. This field force, built painstakingly over decades, represented Mankind's most valuable intangible asset—one that couldn't be replicated quickly regardless of capital availability.

The post-IPO performance validated the institutional thesis. On May 22, 2023, the share price touched its all-time low at ₹1,242.00. Despite this dip, the stock rebounded strongly. By June 21, 2023, Mankind Pharma's shares had surged to a high of ₹1,768.00. The initial volatility gave way to steady appreciation as quarterly results demonstrated continued execution.

They have EBITDA margins of around 25% which is pretty decent. PAT has grown from 1000 Crores in Fy20 to 1400 Crores in Fy22. 9MFy23 PAT is ~1000 Crores, so if we annualise it, the PAT would be ~1300 Crores. EPS would be 32, P/E 34x which looks over valued as compare to median P/E of Pharma Peers at 25x. The premium valuation reflected investor confidence in Mankind's ability to sustain above-industry growth rates.

The IPO proceeds distribution revealed strategic priorities. While the company received no fresh capital, the partial exit by promoters provided them with resources for future investments, both within Mankind and in new ventures. The liquidity also facilitated employee stock options and potential management incentive programs, crucial for attracting and retaining talent in the competitive pharmaceutical industry.

The governance changes post-IPO were minimal but meaningful. Independent directors were strengthened, audit committees formalized, and disclosure standards elevated to listed company requirements. However, with promoters retaining majority stake, the essential family-driven culture and decision-making remained intact.

The market's reception of Mankind's IPO reflected broader themes in Indian capital markets. Investors were willing to pay premiums for companies with strong domestic franchises, consistent execution track records, and exposure to India's consumption story. Mankind's focus on affordable healthcare resonated with the narrative of India's expanding middle class and increasing healthcare spending.

The timing proved fortuitous. The IPO came during a period of strong market sentiment, with pharmaceutical stocks recovering from COVID-era volatility. Global investors were returning to emerging markets, and India's pharmaceutical sector was seen as a defensive play with growth characteristics.

For the Juneja families, the IPO represented validation of their three-decade journey. From ₹50 lakhs in seed capital to a ₹43,000 crore valuation at IPO—a multiplication of nearly 90,000 times—demonstrated the power of patient capital, operational excellence, and deep market understanding.

The successful IPO provided Mankind with currency for acquisitions (through potential future equity issuances), enhanced brand visibility, and the credibility that comes with public market scrutiny. These benefits would prove crucial for the next phase of Mankind's evolution: the transformative BSV acquisition that would redefine its strategic positioning.

VII. The BSV Mega-Acquisition: Betting Big on Women's Health (2024)

The announcement in July 2024 that Mankind would acquire Bharat Serums and Vaccines for ₹13,768 crore sent shockwaves through India's pharmaceutical industry. This wasn't just another acquisition; it was the largest pharmaceutical deal in Indian history by a domestic company, representing a transformative bet on specialty pharmaceuticals and women's healthcare that would fundamentally alter Mankind's strategic trajectory.

Mankind Pharma Limited has completed the transaction to acquire 100% stake in Bharat Serums and Vaccines Limited (BSV), for a purchase consideration of INR 13,768 Crores. This strategic move marks a significant leap for Mankind Pharma, positioning it as a market leader in the Indian women's health and fertility drug market alongside access to other high entry barrier products in critical care segment with established complex R&D tech platforms.

The scale of the acquisition was breathtaking for a company that had started with ₹50 lakhs just three decades earlier. To put it in perspective, the BSV acquisition cost more than three times what Mankind had raised in its IPO just a year earlier. This wasn't incremental growth; it was a quantum leap into a new league of pharmaceutical companies.

BSV reported revenues of Rs 1,723 crore in FY24, delivering robust 20 per cent year-on-year growth with adjusted EBITDA margins of 28 per cent. The business has grown at a 21 per cent revenue compound annual growth rate over the last three years. These financials revealed why Mankind was willing to pay such a premium—BSV wasn't just growing; it was accelerating in high-margin, specialized segments.

The strategic rationale was compelling on multiple levels. The women's health portfolio has products ranging from fertility drugs to post-pregnancy therapies. Amid increasing IVF penetration, this offers growth potential. Around 20 million couples in India alone experience infertility, which affects 60–80 million couples globally. Mankind was buying into a massive, underserved market with structural growth drivers.

Numerous pharmaceutical, biotech, and biological products have been developed since the inception of BSV in 1971. The company's five-decade history meant established relationships, proven products, and regulatory approvals that would take years to replicate organically. The company was set up in 1971 with Vinod Daftary opening a blood bank and eventually launching an injectable for expecting mothers.

The BSV portfolio represented a dramatic departure from Mankind's traditional business. With over five decades of leadership in biopharmaceuticals, BSV has developed recombinant and niche biologic products in-house. It has a strong portfolio across women's health, fertility, and critical care. These weren't simple generic tablets but complex biologics requiring sophisticated manufacturing and deep scientific expertise.

The world's first marketed recombinant Anti Rh(o)-D Immunoglobulin, is a pioneering New Biological Entity (NBE) developed by BSV to prevent sensitization in Rh negative mothers to prevent complications of hemolytic disease in newborn babies. Proudly patented globally, it embodies India's vision of innovating in India, making in India for the world. Since its launch in 2021, Trinbelimab has protected over 2.6 million Rh negative mothers. Winner of Modi Prix Galien 2024 for the Best Biotechnology Product, Trinbelimab sets the global benchmarks in maternal care, reflecting BSV's commitment to improving health worldwide.

This single product exemplified what Mankind was acquiring—not just revenues but genuine innovation capability. Trinbelimab represented the kind of complex, high-barrier product that Mankind had aspired to develop but lacked the technical capabilities to create independently.

The acquisition structure and financing were equally bold. The transaction was funded through internal accruals and external debt, arranged through a combination of non-convertible debentures (NCDs) and commercial papers. "Mankind Pharma may consider retiring a portion of its debt through a potential equity raise, which is already approved by the shareholders," the company added.

This financing approach showed sophisticated capital management. By using debt initially and keeping the option for equity raise later, Mankind could complete the acquisition quickly while maintaining flexibility for optimal capital structure. The pre-approved equity raise from shareholders demonstrated management's foresight and board confidence.

More than 2,500 BSV employees will be joining Mankind. The human capital aspect was crucial. BSV brought specialized expertise in biologics, IVF protocols, and complex manufacturing that Mankind couldn't develop internally without years of investment. BSV has an R&D centre with over 60 scientists and a strong product pipeline.

The seller's perspective added another dimension to the story. Private equity major Advent International was looking to exit BSV four years after it picked up a majority stake in BSV. Advent acquired a 74 per cent stake in BSV in February 2020, providing a complete exit to private equity investors OrbiMed Asia and Kotak PE and a partial exit to the promoter Daftary family.

Advent's transformation of BSV during its ownership was remarkable. The company's consolidated revenue grew 15 per cent in FY23 to Rs 1,435 crore due to significant traction in the women's health and assisted reproductive segments, with the two verticals growing by 42 per cent and 230 per cent, respectively. Advent had professionalized operations, accelerated growth, and positioned BSV perfectly for strategic acquisition.

From the outset, we recognized the strength of BSV's portfolio in Assisted Reproductive Technology (ART) and other areas of women's health. Advent believed the low investment in women's health and fertility in India was coming to a long-awaited end and was now set for decades of growth and investment. In BSV, we identified the kernel of a company with the potential to become a domestic champion, delivering research-driven products to save and improve the lives of millions of women, both in India and across the globe.

The market opportunity in women's health was particularly compelling. BSV has products for conditions like endometriosis, a condition that affects 109 million women worldwide and around 25 million in India. Lifestyle changes, delayed parenthood, and the increase of chronic diseases have seen fertility rates decline by 50% in the last 50 years across the world.

These demographic and lifestyle trends created sustainable demand for BSV's products. Unlike traditional pharmaceuticals where generic competition erodes margins, fertility treatments and specialized women's health products maintained pricing power due to their complexity and critical nature.

The manufacturing capabilities acquired were equally strategic. It has US FDA and EU-approved facilities in Germany and operates in the Philippines through a wholly-owned subsidiary. With 5 dedicated injectable formulation lines and 2 API manufacturing lines, it produces cutting-edge injectables for India and emerging markets. A US FDA approved plant manufacturing Active Pharmaceutical Ingredients (APIs) and fertility hormones.

These international regulatory approvals opened doors that Mankind couldn't easily access independently. The German facility, in particular, provided a beachhead for European market entry with complex biologics—a market Mankind had never seriously contemplated before.

Terming BSV's acquisition a pivotal moment for the company, Rajeev Juneja, vice-chairman and managing director, Mankind Pharma, said BSV's established specialty R&D tech platforms with complex portfolio perfectly aligns with Mankind's vision to expand into a high-entry barrier area. "This strategic move marks a significant leap for Mankind Pharma, positioning us as a market leader in the Indian women's health and fertility drug market," he added.

The cultural fit was surprisingly strong despite the companies' different histories. Our mission at BSV is to preserve, protect, and enhance quality of life while we remain committed to 'Bringing Life to Life'. Our values of Transparency, Agility, Accountability, and Collaboration, hold us in good stead in every step of our patient journey. These values aligned well with Mankind's mission-driven approach to healthcare.

Sheetal Arora, chief executive officer and whole-time director of Mankind Pharma, said BSV's business will be highly synergistic with their comprehensive product portfolio, expansive field force, and doctor coverage. "We are confident this would correspond to the expansion of EBITDA margins and thereby solidify our position as a company known for marketing innovative and specialised offerings," Arora said.

The synergies were multifaceted. Mankind's massive field force of over 12,000 medical representatives could immediately begin promoting BSV's specialized products to gynecologists and fertility specialists. BSV's high-margin products would improve Mankind's overall profitability profile. The combined entity would have unparalleled reach in women's healthcare across India.

The debt gamble was significant but calculated. Taking on nearly ₹14,000 crore in acquisition debt transformed Mankind from a debt-free company to a leveraged one overnight. However, with BSV's 28% EBITDA margins and 20% growth rate, the debt service appeared manageable. The option to raise equity provided a safety valve if needed.

Their established specialty R&D tech platforms with complex portfolios perfectly aligns with the vision of reaching out into the high entry barrier portfolio. "Today, we warmly welcome BSV's 2,500+ members into our Mankind family and add a new chapter to our exciting journey and set the stage for accelerated growth", said Rajeev Juneja, Vice-chairman and Managing Director, Mankind Pharma.

The integration challenges were substantial. Merging a biologics-focused, internationally-oriented company with Mankind's domestic, small-molecule-focused organization required careful management. Different regulatory requirements, manufacturing processes, and go-to-market strategies needed harmonization without destroying what made each company successful.

The competitive implications were profound. Post-acquisition, Mankind would leap from being a domestic generics player to a specialty pharmaceutical company with genuine innovation capabilities. The combined entity would compete not just with Indian peers but with multinational pharmaceutical companies in complex therapeutic areas.

Sanjiv Navangul, CEO and managing director of BSV, said, "We are proud to be one of the few Indian companies that have several first-of-its-kind indigenously developed complex treatments that have delivered better patient outcomes." This innovation heritage was precisely what Mankind needed to transcend its image as an affordable generics manufacturer.

The BSV acquisition represented Mankind's boldest strategic move yet—a ₹13,768 crore bet that specialty pharmaceuticals, particularly in women's health, would drive the next phase of growth. It was a transformative deal that would either establish Mankind as India's leading specialty pharmaceutical company or saddle it with unsustainable debt. The execution of this integration would determine which outcome prevailed.

VIII. Business Model & Competitive Advantages

The business model that has driven Mankind Pharma from a ₹50 lakh startup to a ₹1 lakh crore pharmaceutical giant is deceptively simple in concept but extraordinarily complex in execution. At its core lies a philosophy that has remained unchanged since 1995: "Quality, affordability and accessibility"—three words that encapsulate an entire approach to pharmaceutical business that differs fundamentally from both multinational competitors and export-focused Indian peers.

The field force advantage represents Mankind's most formidable competitive moat. With over 12,000 medical representatives—one of the largest in India—Mankind has achieved something remarkable: presence in virtually every prescribing doctor's clinic across the country. But size alone doesn't capture the strategic brilliance. While competitors concentrate their field forces in metros and Tier 1 cities where doctors see more patients, Mankind has deployed its representatives deep into Tier 2, 3, and even 4 cities where competition is minimal and doctor loyalty, once earned, tends to be sticky.

This distribution strategy creates a virtuous cycle. In smaller cities, a Mankind representative might be the only pharmaceutical company representative a doctor sees regularly. This exclusive mindshare translates into higher prescription shares. The cost per medical representative is lower in smaller cities, improving return on investment. The relationships built over decades become nearly impossible for competitors to dislodge without massive investment.

More than 50% of India's total population resides in villages, making access to medicines difficult. Mankind's pioneering use of supply chains and a company-owned distribution setup bolsters accessibility. The company operates a hybrid distribution model that combines traditional stockist-distributor networks with direct distribution in key markets. This flexibility allows Mankind to maintain availability even in markets where traditional distribution economics don't work.

The portfolio strategy reveals sophisticated market understanding. Multiple brands within the same therapeutic area allow us to cater to the requirements of a wide range of patients. This multi-brand approach in single therapeutic categories isn't redundancy—it's strategic positioning. Different brands target different price points, different doctor segments, and different patient profiles. A cardiologist in Mumbai might prescribe Mankind's premium brand, while a general practitioner in rural Bihar prescribes the economy variant. Both generate margins, both build volume, and together they create market dominance.

Consider the antihypertensive segment where Mankind has multiple brands: Telmikind (premium), Amlokind (mid-market), and several combination products. Each targets specific patient needs and doctor preferences. The premium brand competes with multinationals on quality perception. The mid-market brand captures volume. The combinations improve patient compliance. Together, they give Mankind a 15-20% market share in the segment—impossible to achieve with a single brand.

Manufacturing efficiency represents another crucial advantage. With 25 factories across India, Mankind has achieved remarkable economies of scale while maintaining flexibility. The facilities are strategically located in tax-advantaged zones, near raw material sources, and close to major distribution hubs. This network allows the company to produce over 20 billion tablets and capsules annually at costs 20-30% lower than peers.

But manufacturing excellence goes beyond cost. Mankind has invested heavily in backward integration for key molecules, controlling the entire value chain from API to finished formulation. This integration provides multiple benefits: cost control, quality assurance, supply security, and the ability to quickly scale production when products gain traction. During COVID-19, when supply chains globally were disrupted, Mankind's integrated manufacturing allowed uninterrupted production.

The R&D strategy, often overlooked, is cleverly differentiated. With 6 cutting-edge R&D facilities, we pioneer breakthroughs like Dydrogesterone in pharmaceutical excellence. But Mankind's R&D philosophy differs from peers who chase novel molecules or complex generics for regulated markets. Instead, Mankind focuses on three areas: reformulation for Indian needs (pediatric syrups, scored tablets, combination drugs), complex generics with limited competition (like Dydrogesterone), and patient-centric innovations (taste masking, improved bioavailability, convenient dosing).

This focused R&D approach delivers exceptional returns. Developing Dydrogesterone cost a fraction of what developing a new chemical entity would require, yet it positioned Mankind as an innovation leader. The pediatric formulations, while not scientifically groundbreaking, solve real problems for Indian mothers trying to give medicine to children. These innovations might not win scientific awards, but they win customer loyalty.

The consumer healthcare transformation added another dimension to the business model. A range of consumer healthcare products to meet the non-prescription segment ranging from antacids to condoms to pregnancy test kits. The OTC business leverages Mankind's distribution infrastructure while operating on fundamentally different dynamics. Higher margins, direct consumer marketing, and brand loyalty create a more predictable, profitable revenue stream that balances the prescription business's volatility.

The financial model underlying these operations is remarkably capital efficient. Mankind maintains one of the lowest working capital requirements in Indian pharma—around 60-70 days of sales compared to industry averages of 100-120 days. This efficiency comes from multiple factors: strong distributor relationships allowing favorable payment terms, rapid inventory turnover due to focused SKUs, and disciplined credit management.

Cash generation has been exceptional. Despite continuous expansion and acquisitions, Mankind has maintained strong cash flows, generating over ₹2,000 crore in operating cash flow annually in recent years. This cash generation funded growth without diluting equity or taking excessive debt (until the BSV acquisition), allowing the founding families to maintain control while scaling the business.

The organizational structure, while appearing traditional, contains subtle innovations. Decision-making remains centralized for strategy but is highly decentralized for execution. Division heads have significant autonomy in product selection, marketing spending, and field force deployment. This structure combines entrepreneurial agility with corporate scale—units operate like startups within the larger organization.

Human capital management, often a weakness in family-run businesses, has been a strength at Mankind. The company maintains industry-leading retention rates, with many employees spending entire careers at Mankind. This isn't just about compensation (though Mankind pays competitively) but about culture. The company's promotion from within policy, transparent performance management, and genuine care for employee welfare create loyalty that translates into superior execution.

The technology adoption strategy has been pragmatic rather than cutting-edge. While competitors invested heavily in digital marketing and e-commerce platforms, Mankind focused on basics: ERP systems for supply chain management, CRM systems for field force effectiveness, and data analytics for demand forecasting. This practical approach delivered returns without the massive investments in unproven technologies that plagued some peers.

The regulatory and compliance approach reflects deep understanding of Indian pharmaceutical regulations. Mankind has maintained an excellent compliance record, with minimal regulatory issues despite operating numerous facilities. This isn't luck but systematic investment in quality systems, regular training, and a culture that prioritizes compliance over shortcuts. In an industry where regulatory issues can destroy value overnight, this track record is invaluable.

Why 97% domestic focus might be both strength and weakness deserves careful analysis. The concentration appears risky—exposed to Indian regulatory changes, currency fluctuations, and economic cycles. Yet this focus has been Mankind's greatest strength. Deep market knowledge allows rapid response to opportunities. Concentrated investment creates economies of scale. Avoided distractions of managing multiple regulatory regimes. Protection from global generic pricing pressure that has hurt export-focused peers.

However, the domestic focus also creates limitations. Growth is capped by Indian market expansion. No natural hedge against rupee depreciation. Limited exposure to innovation happening in developed markets. Difficulty attracting global talent and partners. These limitations explain why the BSV acquisition, with its international presence and innovation capabilities, was strategically necessary.

The competitive advantages compound over time. Field force relationships built over decades become harder to displace. Manufacturing scale economics improve with volume. Brand equity in consumer products strengthens with advertising investment. Distribution networks become denser with expansion. Each advantage reinforces others, creating a competitive position that would require massive investment and time to replicate.

The sustainability of these advantages varies. The field force advantage might erode with digital transformation of healthcare. Manufacturing efficiency could be matched by competitors with investment. The domestic focus advantage might become a liability if India's growth slows. However, the integrated nature of Mankind's advantages—where distribution reinforces manufacturing, which enables pricing, which builds brand equity—creates resilience that individual advantages alone wouldn't provide.

The business model has evolved while maintaining core principles. From pure prescription generics to consumer healthcare. From single brands to portfolio strategies. From family management to professional leadership. From domestic focus to selective internationalization through BSV. Each evolution built on existing strengths rather than abandoning them, creating layers of capability that define modern Mankind.

This business model—built on unglamorous but essential principles of affordability, accessibility, and quality—has created extraordinary value. It proves that in pharmaceuticals, as in many industries, perfect execution of a simple strategy beats poor execution of a complex one. Mankind's model might not be revolutionary, but its consistent application over three decades has been nothing short of transformative.

IX. Playbook: Lessons for Emerging Market Entrepreneurs

The Mankind Pharma story offers a masterclass in building billion-dollar businesses in emerging markets, where conventional Silicon Valley wisdom often fails and developed market strategies prove inadequate. The lessons extracted from their journey provide a playbook for entrepreneurs operating in similar environments—markets characterized by price sensitivity, infrastructure challenges, regulatory complexity, and vast underserved populations.

Building in markets with price-sensitive customers requires fundamental rethinking of business models. Mankind's approach wasn't to offer stripped-down versions of premium products but to reimagine the entire value chain for affordability. They understood that in emerging markets, affordability isn't just about price—it's about value perception, purchase convenience, and total cost of treatment. When Mankind priced medicines 30-40% below competitors, they weren't just competing on price; they were expanding the market by bringing treatment to patients who previously went without.

The key insight: in price-sensitive markets, volume economics can more than compensate for lower margins, but only if you achieve sufficient scale. Mankind's patient building of distribution and manufacturing scale over decades before attempting margin expansion shows the discipline required. Too many emerging market entrepreneurs make the mistake of trying to premiumize too early, before achieving the scale that makes the business defensible.

The power of focusing on one geography deeply cannot be overstated. While globalization rhetoric suggests companies should think globally from day one, Mankind's 97% domestic revenue concentration after 30 years suggests otherwise. Deep focus allowed them to understand micromarket nuances—why doctors in Karnataka prescribe differently from those in Bihar, why rural patients prefer syrups to tablets, why certain brands resonate in specific regions.

This geographic focus enabled competitive advantages impossible to achieve with scattered international presence. The cost of acquiring customer insights dropped dramatically. Marketing messages could be precisely tailored. Distribution investments compounds rather than spreading thin. Regulatory compliance became routine rather than complex. The lesson: dominate your home market completely before venturing abroad.

When to pivot from B2B (prescriptions) to B2C (OTC) represents one of the most critical decisions for emerging market companies. Mankind waited 12 years before entering consumer healthcare, using that time to build distribution infrastructure, brand credibility, and cash generation capabilities. The timing was crucial—too early and they would have lacked the resources for consumer marketing; too late and competitors would have captured the opportunity.

The pivot wasn't abandonment of B2B but addition of B2C, leveraging existing capabilities while developing new ones. The prescription business provided steady cash flows that funded consumer brand building. The field force relationships gave credibility to consumer products. The distribution network carried both product types efficiently. This gradual, leveraged transition minimized risk while maximizing synergies.

Managing family businesses at scale presents unique challenges that Mankind navigated skillfully. The company maintained family control while professionalizing operations, bringing in external talent for specialized roles while keeping strategic decisions within the family. The second generation was gradually integrated, working their way up rather than parachuting into senior positions. Clear role definitions prevented the confusion and conflict that often plague family businesses.

The family structure provided advantages often overlooked: patient capital allowing long-term thinking, aligned incentives preventing agency problems, quick decision-making without bureaucracy, and deep commitment beyond financial returns. The key was maintaining these advantages while adding professional management capabilities where needed.

Timing market entry: Why being late can sometimes win contradicts conventional first-mover advantage thinking. Mankind entered established markets—antibiotics, antihypertensives, antidiabetics—where multiple players already competed. But they entered with better understanding of what didn't work, lower cost structures from learning curve benefits, and differentiated positioning when markets were mature enough to segment.

Being late allowed Mankind to avoid expensive market education costs. Pioneer companies educated doctors about new therapeutic categories; Mankind entered once prescription habits were established. Early entrants made costly mistakes in regulation and distribution; Mankind learned from these errors. The lesson: in emerging markets, being first matters less than being best positioned when the market inflects.

Capital efficiency: Bootstrapping to billions might seem impossible in today's venture capital-fueled environment, but Mankind proved otherwise. Starting with ₹50 lakhs and reaching ₹43,000 crore IPO valuation without significant external capital required extreme discipline. Every rupee was reinvested. Growth was organic until cash generation could fund acquisitions. Expansion was sequential rather than simultaneous.

This bootstrapping forced beneficial constraints. Without capital to burn, Mankind had to achieve profitability quickly. Without venture capital pressure, they could focus on sustainable growth over hypergrowth. Without external board members, they could make contrarian long-term bets. The discipline developed through bootstrapping continued even after going public, evident in their careful approach to the debt-funded BSV acquisition.

The approach to innovation in emerging markets differs fundamentally from developed markets. Instead of pursuing breakthrough innovation, Mankind focused on appropriate innovation—solutions that solved local problems within local constraints. Developing scored tablets for flexible dosing in markets where patients often can't afford full doses. Creating flavored syrups for pediatric medications in cultures where medicine compliance is challenging. These innovations might seem trivial to developed market observers but create tremendous value in emerging markets.

Building defensible moats without traditional advantages (technology, patents, network effects) required creativity. Mankind built moats through execution excellence in areas competitors found unglamorous: field force productivity, distribution density, working capital management, and regulatory compliance. These operational moats proved more defensible than technology moats in emerging markets where intellectual property protection is weak and technology can be quickly copied.

The approach to talent in emerging markets required pragmatism. Unable to attract top-tier talent with stock options (being private) or global career opportunities (being domestic), Mankind built talent through internal development. They hired raw talent and trained extensively. They promoted from within, creating loyalty and institutional knowledge. They compensated competitively but not excessively, focusing on job security and growth opportunities over immediate rewards.

Managing stakeholder relationships in emerging markets requires nuance often unappreciated by Western business education. Mankind maintained excellent relationships with regulators through compliance and transparency. They built trust with distributors through consistent policies and fair dealing. They earned doctor loyalty through reliable service over flashy marketing. They gained community support through local employment and social responsibility. These relationships, built over decades, became invaluable intangible assets.

The acquisition strategy for emerging market companies differs from developed market approaches. Mankind's acquisitions—Magnet Labs, Panacea's brands, BSV—weren't about acquiring technology or entering new markets but about consolidating fragmented domestic markets and acquiring established relationships. The focus was on revenue synergies through distribution leverage rather than cost synergies through elimination of redundancies.

Dealing with infrastructure constraints required innovative solutions. Poor cold chain infrastructure led to development of heat-stable formulations. Unreliable power supply prompted investment in captive power generation. Limited banking infrastructure inspired creative credit management systems. Rather than waiting for infrastructure to improve, Mankind built business models that worked within existing constraints.

The approach to competition in emerging markets avoided direct confrontation with stronger players. Instead of competing with multinationals on innovation or with large Indian companies on scale, Mankind competed on dimensions where they could win: reach into underserved markets, relationships in neglected segments, and responsiveness to local needs. This indirect competition strategy allowed them to grow without triggering aggressive competitive responses.

Building brands in emerging markets with limited marketing budgets required creativity. Mankind built brands through consistency rather than big campaigns. Every product delivered on its promise. Every interaction reinforced brand values. Word-of-mouth became the primary marketing vehicle. When they eventually invested in advertising for consumer products, the foundation of trust was already established.