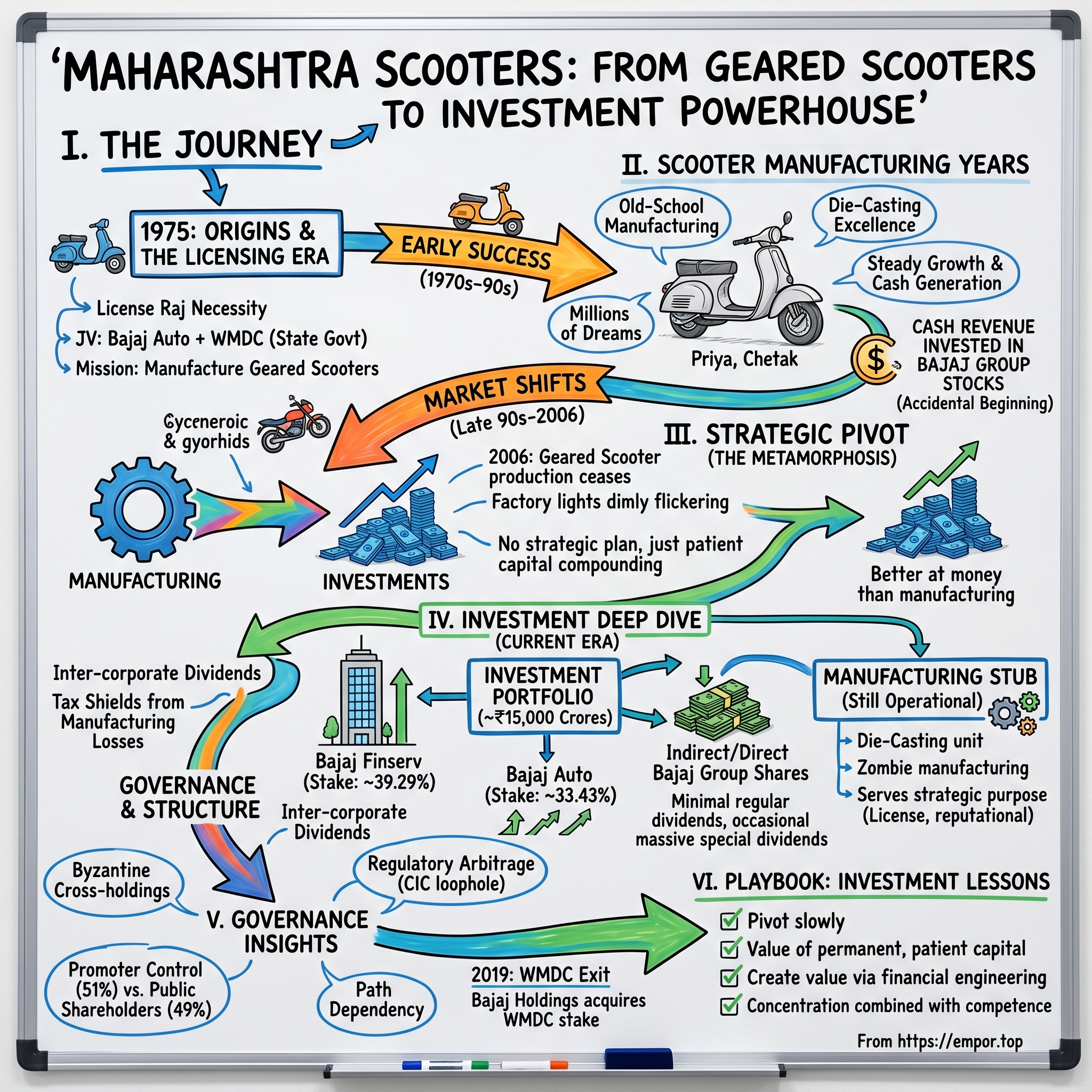

Maharashtra Scooters: From Geared Scooters to Investment Powerhouse

I. Introduction & Episode Roadmap

Picture this: A company with a market capitalization of ₹16,738 crores that generates just ₹205 crores in revenue—yet somehow produces ₹241 crores in profit. The math seems impossible, a violation of basic business physics. Welcome to the enigma of Maharashtra Scooters Limited, perhaps India's most peculiar transformation story.

In the labyrinthine world of Indian conglomerates, where cross-holdings create Russian doll-like ownership structures, Maharashtra Scooters stands as a monument to strategic pivoting. This isn't your typical Silicon Valley "pivot or die" narrative. This is something far more Byzantine—a state-backed manufacturing venture that morphed into a sophisticated investment vehicle, all while keeping its factory lights dimly flickering as if preserving a relic from another era.

The company's stock ticker, MAHSCOOTER, hints at its industrial past, but today it's essentially a treasury operation masquerading as a manufacturer. It's a Core Investment Company that still maintains some manufacturing operations—like keeping your childhood bedroom intact decades after moving out. The real business? Holding strategic stakes in the Bajaj empire's crown jewels: Bajaj Auto and Bajaj Finserv.

What makes this story particularly fascinating is how it encapsulates three distinct eras of Indian capitalism. First, the License Raj period when government partnerships were mandatory for scale. Second, the liberalization era when Indian manufacturing had to compete globally. And third, the financialization phase where holding companies became wealth preservation vehicles for business dynasties.

The protagonist in our drama isn't a visionary founder or a turnaround CEO—it's the inexorable force of market evolution. When Indian consumers abandoned geared scooters for motorcycles in the early 2000s, Maharashtra Scooters faced an existential crisis. Most companies would have shuttered. Instead, it discovered that its investment portfolio, accumulated almost accidentally, was worth far more than its manufacturing operations ever were.

Today, Maharashtra Scooters is a financial engineering marvel that would make Warren Buffett's Berkshire Hathaway structure look straightforward. Through its parent Bajaj Holdings & Investment Limited (BHIL), it owns 33.43% of Bajaj Auto and 39.29% of Bajaj Finserv—stakes worth thousands of crores. The manufacturing business that gave it birth? It limps along with operating losses, a vestigial organ that nobody seems willing to amputate.

This is a story about adaptation in slow motion, about value hiding in plain sight, and about how India's unique corporate governance environment creates these fascinating anomalies. It's about a company that succeeded by failing at its original purpose, and in doing so, became something far more valuable.

II. The Bajaj Dynasty & Origins (1975)

The year was 1975. India was emerging from the trauma of the Emergency, inflation was rampant, and the country's industrial policy was a maze of licenses and permits. Into this environment stepped an unlikely partnership: Bajaj Auto Limited, the two-wheeler giant run by the formidable Rahul Bajaj, and Western Maharashtra Development Corporation (WMDC), a state government undertaking with grand ambitions for regional industrialization.

The joint venture wasn't born from strategic vision—it was regulatory necessity dressed up as public-private partnership. Under the License Raj, scaling manufacturing required government blessing, and what better way to secure it than making the government your partner? WMDC brought political cover and land access; Bajaj brought technology and market knowledge. The equity split reflected this arranged marriage: Bajaj Auto held the majority, WMDC took 27%, and public shareholders got the rest.

The stated mission was audacious for its time: manufacture geared scooters to complement Bajaj Auto's product line without cannibalizing it. Think of it as Procter & Gamble creating a separate company to make a slightly different shampoo—seemingly redundant, but in the License Raj, such corporate contortions were routine. The government got to claim job creation in Maharashtra; Bajaj got additional manufacturing capacity without regulatory headaches.

The location chosen was strategic—close enough to Bajaj Auto's Pune operations for synergy, far enough to justify separate existence. The initial product lineup read like a love letter to middle-class Indian aspirations: the "Priya" (Sanskrit for beloved), the "Bajaj Super" (because everything needed "Super" in its name in the 1970s), and later, the legendary "Bajaj Chetak"—named after Maharana Pratap's faithful horse, a masterstroke of cultural branding.

What made these scooters special wasn't innovation—it was accessibility. Geared scooters were easier to maintain, more fuel-efficient, and crucially, easier to ride for first-time two-wheeler owners. In a country where a scooter wasn't just transportation but a family's first major asset after a home, reliability mattered more than speed.

The manufacturing setup was deliberately old-school. While the world was moving toward automation, Maharashtra Scooters invested in dies, jigs, fixtures—the mechanical craftsmanship that Indian workers excelled at. The die-casting operation, in particular, became a center of excellence, producing components not just for their scooters but for the broader Bajaj ecosystem.

Rahul Bajaj, never one to miss an opportunity for vertical integration, saw Maharashtra Scooters as more than just additional capacity. It was a hedge against regulatory changes, a training ground for managers, and importantly, a separate profit center that could pay dividends to the parent. The financial engineering was already beginning, hidden beneath the grease and grime of manufacturing.

The early years were marked by steady growth. India's middle class was expanding, urbanization was accelerating, and the waiting list for scooters stretched for years. Maharashtra Scooters rode this wave, its order books full, its factories humming. By the early 1980s, it had established itself as a credible player, not just another government joint venture destined for mediocrity.

But even in these golden years, there were signs of the transformation to come. The company's annual reports, dry documents that they were, revealed an interesting pattern: investment income was growing faster than manufacturing profits. The treasury department, meant to park surplus cash, was quietly building a portfolio of Bajaj Group stocks. Nobody called it strategic—it was just prudent cash management. Or so they said.

The WMDC representatives on the board, political appointees who rotated frequently, seemed content with employment numbers and dividend checks. They didn't probe why a scooter company needed such an elaborate investment strategy. This benign neglect would later become crucial when the company's very purpose came into question.

As the 1980s dawned, Maharashtra Scooters looked like a textbook success of mixed economy planning. It was profitable, growing, and serving a social purpose. But underneath this comfortable narrative, tectonic shifts were beginning. Japanese motorcycle technology was arriving in India. Consumer preferences were evolving. And somewhere in Honda's headquarters, plans were being drawn that would revolutionize Indian two-wheeler market.

The company that was born to make scooters accessible was about to discover that its greatest asset wasn't its factories or its technology—it was the patient capital it had accumulated, almost by accident, over years of steady operations.

III. The Scooter Manufacturing Years (1975–2006)

The Bajaj Chetak production line at Maharashtra Scooters' factory floor in 1985 was a symphony of coordinated chaos. Sparks flew from welding stations, the rhythmic thud of stamping machines provided bass notes, and the acrid smell of industrial paint hung in the air. Workers in blue overalls moved with practiced precision, each scooter taking shape through hundreds of small human interventions. This was manufacturing at its most visceral—not the antiseptic automation of Japanese factories, but the muscular, hands-on production that built India's industrial base.

For three decades, this scene repeated daily, producing millions of scooters that became part of India's cultural fabric. The geared scooter wasn't just transportation; it was a rite of passage. The first family vehicle. The dowry essential. The small business enabler. Maharashtra Scooters didn't just manufacture products—it manufactured middle-class dreams, one gear shift at a time.

The company's engineering prowess lay not in breakthrough innovation but in incremental refinement. The Priya scooter, their flagship through the 1980s, was a masterclass in frugal engineering. Every component was designed for two objectives: durability and repairability. In an India where authorized service centers were sparse and roadside mechanics abundant, a scooter that could be fixed with basic tools wasn't just practical—it was essential.

The die-casting division, initially a support function, evolved into a competitive advantage. Maharashtra Scooters produced engine blocks, transmission housings, and dozens of other components with tolerances that impressed even Bajaj Auto's Japanese partners. The precision achieved through manual skill rather than computerized machinery became a point of pride. Old-timers still talk about the master craftsmen who could detect a two-micron deviation by touch.

Through the 1980s and early 1990s, the numbers told a story of steady success. Production ramped from 50,000 units annually to over 200,000. Market share in the geared scooter segment touched 30%. Revenue grew at double digits. But more interesting than these headline figures were the margins—consistently higher than industry average, thanks to the captive component manufacturing and lower overhead from the government partnership.

The financial model was elegantly simple. WMDC's presence meant easier land acquisition, fewer labor issues, and occasional state government orders. Bajaj Auto provided technology transfer at favorable terms and guaranteed component purchases. The public shareholders got steady dividends. Everyone was happy. The surplus cash, growing year by year, was prudently invested in fixed deposits and, increasingly, equity shares of group companies.

Then came 1991—liberalization. Suddenly, the moats that protected Indian manufacturers began draining. Honda, Yamaha, and Suzuki entered through joint ventures. They brought not just better technology but different technology. The motorcycle—faster, more fuel-efficient, more masculine in its marketing—began its assault on the scooter's dominance.

Maharashtra Scooters' response was textbook incumbent behavior: denial, then incremental improvement, then desperate innovation. The Bajaj Super got a facelift. The Chetak received electronic ignition. New models were launched with increasingly optimistic names. But the market had spoken, and it was speaking in the language of four-stroke engines and sleek designs that Maharashtra Scooters' aging infrastructure couldn't replicate.

The late 1990s witnessed a curious phenomenon. Even as scooter sales declined, the company's profits held steady. How? The investment portfolio, built over two decades, was generating returns that offset manufacturing losses. The treasury department, once a sleepy backwater, became the de facto profit center. Board meetings spent less time discussing production targets and more time debating portfolio allocation.

By 2003, the writing wasn't just on the wall—it was in neon lights. Motorcycle sales had overtaken scooters three-to-one. The geared scooter segment, Maharashtra Scooters' only product category, was shrinking 15% annually. The factory that once ran three shifts was down to one. The workforce, protected by labor laws and political considerations, couldn't be reduced proportionally. Fixed costs were eating into margins like rust through metal.

The end came not with a bang but with a whimper. In 2006, the last Bajaj Chetak rolled off the production line. No fanfare, no media coverage—just a quiet acknowledgment that an era had ended. The workers were retained, reassigned to the die-casting division or given voluntary retirement. The assembly lines were mothballed, not dismantled—as if the company couldn't quite let go.

But here's where the story takes its fascinating turn. Any other company would have shut down, liquidated assets, and returned capital to shareholders. Maharashtra Scooters did something far more interesting: it pivoted without announcing a pivot. The manufacturing license was retained. The die-casting operation continued, now serving external customers. And the investment portfolio, that accidental treasure chest, became the primary business.

The transformation wasn't strategic—it was existential. The company literally backed into becoming an investment vehicle. No McKinsey presentation, no board retreat in Goa, no vision statement. Just the gradual recognition that they were better at managing money than making scooters. The very Indian talent for jugaad—making do with what you have—had created an entirely new business model.

Looking back, the manufacturing years weren't a failure—they were an extended gestation period for what Maharashtra Scooters would become. Every scooter sold, every component manufactured, had generated cash that was carefully invested. The real product wasn't vehicles; it was patient capital, compounding quietly while the factory floor gradually fell silent.

IV. The Strategic Pivot: From Manufacturing to Investment (2006–2019)

The December 2006 board meeting of Maharashtra Scooters must have been surreal. The agenda item read "Future Strategic Direction," but everyone knew what it really meant: what do we do now that we don't make scooters anymore? The WMDC representative, a bureaucrat more concerned with employment figures than profit margins, argued for diversification into motorcycles. The independent directors pushed for liquidation. But Rahul Bajaj, representing the promoter's interest, had a different idea—do nothing dramatic, let the investments compound.

This wasn't pivoting; it was metamorphosis in slow motion. While Silicon Valley startups pride themselves on rapid pivots executed in weeks, Maharashtra Scooters took thirteen years to complete its transformation. The company became a study in corporate patience, or perhaps corporate paralysis—depending on your perspective.

The immediate post-2006 period was awkward, like attending your high school reunion years after dropping out. The company still called itself Maharashtra Scooters, still maintained its NSE listing under MAHSCOOTER, still filed manufacturing company returns. But the factory was essentially a Potemkin village. The die-casting unit limped along, generating roughly ₹200 crores in revenue but operating at a loss once you factored in overheads. The real action was happening in a small office where two fund managers quietly managed a portfolio worth thousands of crores.

The numbers from this period tell a fascinating story of a business model in transition. In 2007, manufacturing revenue was ₹189 crores with an operating loss of ₹12 crores. Investment income? ₹145 crores. By 2010, manufacturing had shrunk to ₹156 crores with losses widening to ₹23 crores. Investment income had grown to ₹234 crores. The company was literally making money by losing money—the operating losses provided tax shields while the investments compounded tax-efficiently.

The investment strategy, if you could call it that, was beautifully simple: buy and hold Bajaj Group stocks. Through the parent BHIL, Maharashtra Scooters held significant stakes in Bajaj Auto and Bajaj Finserv. Directly, it owned shares in Bajaj Finance, Bajaj Allianz, and other group companies. The remaining 10% of the portfolio went into debt instruments—not for returns but for liquidity management.

What made this strategy brilliant wasn't its sophistication but its timing. The 2006-2019 period saw Bajaj Auto transform from a scooter company into India's most profitable two-wheeler manufacturer. Bajaj Finance went from a small NBFC to India's most valuable financial services company outside banks. Bajaj Finserv became a financial conglomerate worth more than most banks. Maharashtra Scooters, by doing absolutely nothing except holding these stocks, saw its investment portfolio value multiply twenty-fold.

The WMDC situation during this period deserves its own business school case study. Here was a government entity owning 27% of a company that had abandoned its original purpose. The rational response would be to exit, take the cash, and redeploy it in actual development projects. Instead, WMDC held on, paralyzed by bureaucratic inertia and perhaps mesmerized by the growing dividend income.

Every year, the dance repeated. WMDC would make noises about the company not fulfilling its manufacturing mandate. The Bajaj representatives would point to the die-casting unit still operating. The independent directors would suggest the investment income was creating value for all shareholders. And nothing would change. The status quo, that most powerful force in Indian corporate governance, prevailed.

The regulatory classification added another layer of complexity. In 2015, Maharashtra Scooters was classified as a Core Investment Company (CIC) by RBI definitions—holding more than 90% of assets in group company investments. But it didn't register as an NBFC-CIC because it wasn't taking public deposits. It was a manufacturing company that didn't manufacture, an investment company that didn't want to be called one.

The dividend policy during this period was conservative to the point of being miserly. Despite sitting on thousands of crores of liquid investments, the company paid out minimal dividends. The stated reason was maintaining reserves for future manufacturing investments. The real reason? Nobody could agree on what to do with the cash. The Bajaj team wanted to preserve capital for a potential buyout. WMDC wanted higher dividends for the state treasury. Public shareholders wanted special dividends. Paralysis won.

Market participants weren't fooled. The stock traded at a massive discount to its investment value—sometimes as much as 60%. Analysts called it the "holding company discount," but it was really a "confusion discount." Nobody knew what Maharashtra Scooters actually was anymore. The company had transformed from a manufacturer to an investment vehicle, but it refused to acknowledge its own transformation.

By 2018, the absurdity had reached peak levels. The company's annual report devoted pages to its manufacturing heritage, included photos of the defunct production lines, and discussed future manufacturing plans that everyone knew would never materialize. Meanwhile, the investment portfolio, mentioned almost as an afterthought, had crossed ₹15,000 crores in value.

The transformation was complete, but nobody wanted to admit it. Maharashtra Scooters had become a zombie manufacturer and an accidental investment genius. It was generating returns that most fund managers would kill for, simply by holding onto stocks it had accumulated when it actually made things. The strategic pivot that wasn't a strategy had somehow worked brilliantly.

V. The WMDC Exit & Bajaj Holdings Takeover (2019)

The mahogany conference room at Bajaj Holdings' headquarters in Pune had seen many negotiations, but none quite like this. On one side sat representatives of Western Maharashtra Development Corporation, clutching feasibility studies and valuation reports. On the other, the Bajaj team, armed with spreadsheets showing why WMDC's stake was worth exactly what they were offering—not a rupee more. Between them lay the question nobody wanted to ask aloud: why had it taken thirteen years to have this conversation?

June 17, 2019, marked the end of one of Indian corporate history's most prolonged unwinding. WMDC finally sold its 27% stake in Maharashtra Scooters to Bajaj Holdings & Investment Limited for ₹228.5 crores. The price tag seemed almost insultingly low for a stake in a company with a market cap of over ₹6,000 crores, but the negotiations revealed the bizarre dynamics at play.

WMDC's initial asking price, according to sources familiar with the discussions, was based on the proportional value of the investment portfolio—roughly ₹1,800 crores. The Bajaj team countered with a valuation based on the manufacturing business's book value, conveniently ignoring the investments. The final price of ₹228.5 crores represented a peculiar compromise: higher than book value, dramatically lower than investment value, justified through creative math involving "illiquidity discounts" and "holding company considerations."

The irony was delicious. WMDC, which had entered the venture to promote manufacturing in Maharashtra, was exiting just as the company had completely abandoned manufacturing. The development corporation had inadvertently become a passive investor in financial markets, generating returns that had nothing to do with regional development. The quarterly dividend checks were nice, but explaining to the state legislature why a development corporation owned stakes in a non-manufacturing manufacturer was becoming increasingly awkward.

The negotiation dynamics revealed the power asymmetry inherent in such transactions. WMDC needed to exit—political pressure was mounting, and the optics were terrible. Bajaj Holdings wanted to consolidate control but wasn't desperate. They had operational control anyway; buying out WMDC was about cleaning up the capital structure, not gaining power. In negotiations, the party that needs the deal always pays the price, and WMDC needed this deal.

What made the transaction particularly complex was determining what exactly was being sold. Was it 27% of a manufacturing company with accumulated losses? Or 27% of an investment portfolio worth thousands of crores? The sale agreement, a masterpiece of legal ambiguity, somehow managed to describe it as both and neither. The warranties and representations section ran longer than the actual business description, each side protecting against different interpretations of reality.

The minority shareholders watched this drama with a mixture of hope and resignation. Hope that the exit of WMDC would finally allow the company to acknowledge its transformation and unlock value. Resignation because they knew the Bajaj group's history of prioritizing control over minority returns. The stock price reaction was telling—a brief 15% spike on announcement, then a gradual drift back as reality set in.

Post-acquisition, Bajaj Holdings owned 51% of Maharashtra Scooters, making it a subsidiary. The consolidation brought interesting accounting implications. Maharashtra Scooters' investments in Bajaj companies, which were already circular, became even more incestuous. The company now owned stakes in companies that owned stakes in its parent that owned it—a structure that would make M.C. Escher dizzy.

The integration, such as it was, was minimal. No employees were transferred, no operations were merged, no synergies were captured—because there were none to capture. Maharashtra Scooters continued operating exactly as before, except now the board meetings were shorter without WMDC representatives asking uncomfortable questions about manufacturing revival.

The strategic implications were more subtle. With full control, Bajaj Holdings could theoretically merge Maharashtra Scooters, simplifying the structure and eliminating the holding company discount. But they didn't. The separate listing provided optionality—for tax planning, for regulatory arbitrage, for future financial engineering. In Indian conglomerates, complexity isn't a bug; it's a feature.

The WMDC exit also marked a generational transition in thinking. The old guard, represented by Rahul Bajaj, saw corporate structures as permanent fixtures. The younger generation, including Sanjiv Bajaj and Rajiv Bajaj, understood that structures should serve strategy, not constrain it. The purchase of WMDC's stake was the first step in what many expected would be a broader simplification of the Bajaj group structure.

But eighteen months later, Maharashtra Scooters remained unchanged—still listed, still maintaining the fiction of manufacturing, still trading at a discount. The transformational moment had come and gone, and transformation hadn't occurred. Or perhaps it had, just not in the way anyone expected. The company had transformed from a joint venture constrained by government partnership to a fully controlled subsidiary constrained by... what exactly?

The answer, as with many things in Indian corporate life, was path dependency. Maharashtra Scooters had traveled so far from its origins that nobody quite knew how to get it back to something coherent. It was easier to let it continue existing in its strange twilight zone—not quite a manufacturer, not quite an investment company, but somehow, profitably, both and neither.

VI. The Investment Portfolio Deep Dive

The Excel spreadsheet displaying Maharashtra Scooters' investment portfolio looks like someone accidentally copied Bajaj Holdings' holdings and forgot to change the header. Through multiple layers of ownership, the company controls approximately ₹15,000 crores worth of Indian financial services and automotive excellence. But the real fascination isn't the what—it's the how and why of this peculiar structure.

Let's start with the crown jewels held indirectly through parent BHIL: a 33.43% stake in Bajaj Auto, India's most profitable two-wheeler manufacturer, and 39.29% of Bajaj Finserv, the financial services behemoth. These aren't just investments; they're dynastic stakes, the kind of holdings that families go to war over. The combined value of just these two positions exceeds ₹12,000 crores, yet Maharashtra Scooters' entire market cap hovers around ₹16,738 crores—a discount that would make value investors weep.

The direct holdings tell a different story. Maharashtra Scooters owns shares in Bajaj Finance, purchased at prices that today look like computational errors. Shares bought at ₹50 now trade at ₹7,000. The unrealized gains are so large that realizing them would create a tax bill that would make the finance minister smile. So they sit, these paper profits, compounding at rates that make venture capital returns look pedestrian.

The debt portfolio—roughly ₹189 crores in debentures, commercial papers, and certificates of deposit—seems almost quaint by comparison. This isn't sophisticated fixed-income investing; it's parking money in Bajaj Finance debentures at 9% because, well, why not keep it in the family? The mutual fund investments are similarly unsophisticated: liquid funds for treasury management, nothing exotic. This is investment management as practiced by a company that stumbled into investing.

The dividend income stream from these holdings is where things get interesting. In FY2023, Maharashtra Scooters received approximately ₹180 crores in dividends, primarily from Bajaj Auto and Bajaj Finserv. The beauty of this model is its simplicity: own shares in profitable companies, receive dividends, pay minimal tax due to dividend distribution tax exemptions for inter-corporate holdings, repeat. It's passive income at its most passive.

But here's where the structure becomes truly Byzantine. Maharashtra Scooters owns shares in companies that own shares in its parent, which owns shares in it. The circular holdings create a situation where dividend payments bounce around the group like a pinball, each iteration creating tax efficiency and capital allocation flexibility. It's financial engineering that would make a Wall Street structurer jealous, achieved not through design but through decades of accidental accumulation.

The valuation methodology for these holdings is deliberately conservative. Everything is marked at cost or market value, whichever is lower. This means the balance sheet shows investments at a fraction of their market value. The footnotes to the financial statements, where truth traditionally hides in corporate reports, reveal the gap: book value of investments at ₹2,456 crores, market value at ₹15,234 crores. That ₹12,778 crore difference? It doesn't appear anywhere except in the dreams of value investors.

The concentration risk would terrify modern portfolio theorists. Over 90% of the portfolio in group companies. Zero international diversification. No sectoral spread beyond financial services and automotive. By every measure of portfolio construction, this is wrong. Yet it's produced returns that most diversified portfolios would envy. Sometimes, concentration combined with competence beats diversification.

The tax efficiency of this structure deserves special mention. Inter-corporate dividends are largely tax-free. Capital gains can be deferred indefinitely by simply not selling. The holding company structure allows for tax-efficient extraction of value through buybacks rather than dividends. It's a structure that minimizes tax leakage at every level, designed by accident but maintained by intention.

What's remarkable is what's missing from this portfolio. No start-up investments despite India's booming venture ecosystem. No international holdings despite globalization. No gold, no real estate, no commodities. This isn't a portfolio constructed by modern portfolio theory—it's a collection of historical accidents that happened to work out spectacularly.

The management of this portfolio is refreshingly simple. There's no trading, no rebalancing, no tactical asset allocation. The investment committee meets quarterly, reviews the dividend income, checks if any debt instruments are maturing, and then goes for lunch. The entire investment operation could be managed by a competent CA with an Excel spreadsheet, and probably is.

The opportunity cost of this approach is enormous but unquantifiable. Could active management have produced better returns? Could diversification have reduced risk? Could international investments have provided growth? These questions are academic because Maharashtra Scooters isn't really an investment company—it's a holding vehicle that happens to be publicly listed, managing family wealth with public market transparency requirements.

Looking forward, the portfolio's evolution seems predetermined. Continue holding the Bajaj stakes, collect dividends, occasionally buy more Bajaj Finance shares if prices correct, maintain enough debt instruments for liquidity. It's not exciting, but excitement isn't the point. This is wealth preservation masquerading as a public company, and by that measure, it's succeeding brilliantly.

VII. Financial Engineering & Market Performance

The stock chart of Maharashtra Scooters over the past five years looks like an electrocardiogram of someone watching a thriller—long periods of flatline interrupted by violent spikes. The 57.6% surge in market cap over the past year alone took the company's valuation to ₹16,738 crores, a number that makes sense only when you stop trying to value it as a manufacturing company and start treating it as a publicly-traded family office.

The price-to-earnings ratio of 72.20 would typically signal either explosive growth or irrational exuberance. Maharashtra Scooters offers neither. Revenue has actually declined 2.71% over five years. What you're really seeing is the market's confused attempt to price an investment holding company that reports manufacturing revenues. The earnings come from dividends and capital gains, not operations, making traditional P/E analysis about as useful as a chocolate teapot.

The price-to-book ratio tells a more interesting story. At 0.57, the market values the company at roughly half its book value. But remember, the book value itself understates reality because investments are carried at historical cost. The real price-to-book, if you marked investments to market, would be closer to 0.15. This isn't just a discount; it's a clearance sale that's been running for fifteen years.

The volatility metrics reveal the company's split personality. Daily volatility at 3.03% is surprisingly high for what's essentially a portfolio of stable, dividend-paying stocks. The beta of 0.95 suggests it moves roughly in line with the market, but this masks the reality. On days when Bajaj Finance or Bajaj Auto announce results, Maharashtra Scooters moves violently. The rest of the time, it trades like a government bond—steady, boring, predictable.

The trading patterns are particularly revealing. Average daily volume of around 15,000 shares means you could buy every share traded in a day for about ₹30 crores. For context, the company's investment portfolio generates that much in dividends every two months. The float is so thin that a single institutional order can move the price 5%. This isn't a market; it's a negotiation between a handful of participants who probably know each other by name.

The dividend policy, or lack thereof, represents financial engineering at its most conservative. Despite sitting on thousands of crores of liquid investments and generating hundreds of crores in dividend income, Maharashtra Scooters pays out minimal dividends to shareholders. The five-year average dividend yield is under 1%, a number that would make even the stingiest companies blush. The retained earnings pile up, invested back into more Bajaj stocks, creating a compounding machine that benefits primarily the controlling shareholders.

But then came the special dividends—irregular, unexpected, and massive. When they happen, they're typically 5-10 times the regular dividend, as if the company suddenly remembered it had public shareholders. These windfalls are impossible to predict, turning dividend investing in Maharashtra Scooters into a lottery where you know you'll win eventually, you just don't know when or how much.

The capital allocation strategy, if you can call it that, is fascinatingly primitive. No buybacks despite the massive discount to intrinsic value. No special situations investing despite the cash pile. No debt despite the tax benefits. It's as if modern finance theory never reached the treasurer's office. The entire strategy can be summarized in four words: buy Bajaj, hold forever.

The working capital management adds another layer of absurdity. The company maintains negative working capital—it collects money from customers faster than it pays suppliers. This would be impressive for a manufacturing company if it actually manufactured anything substantial. Instead, it's just an artifact of the die-casting unit's payment terms, a tail wagging a very large investment dog.

Return on equity metrics are where traditional analysis completely breaks down. The three-year average ROE of 0.78% would suggest a dying business. But this is calculated on the book value of equity, which includes investments at historical cost. The real ROE, based on market values, would be respectable if anyone could agree on how to calculate it. The accounting standards weren't designed for companies that accidentally became investment vehicles.

The market's attempts to value Maharashtra Scooters have produced some entertaining sell-side research. One analyst valued it as a sum-of-parts, meticulously calculating the stake values, then applied a 60% holding company discount because "that's what the market does." Another tried discounted cash flow analysis, projecting dividend income for ten years, as if the company's strategy might suddenly change in year eleven. A third gave up and simply said "buy below book value, sell above," which might be the most honest advice.

The foreign institutional investor participation, or lack thereof, is telling. FII holding is negligible, probably because explaining this structure to an investment committee in New York or London would require PowerPoint slides that violate the laws of logic. Domestic institutions hold small stakes, mostly index funds that have to own it because it's in the index, suffering in silence.

What we're witnessing is financial engineering by inertia. No clever structures, no innovative instruments, no strategic initiatives. Just a company that discovered it could generate superior returns by doing absolutely nothing with its investment portfolio except collecting dividends. It's either the most brilliant strategy ever devised or no strategy at all, and after studying it extensively, I'm still not sure which.

VIII. The Manufacturing Stub: Still Operational

Walk into the die-casting unit of Maharashtra Scooters today, and you'd be forgiven for thinking you've traveled back in time. The same machines that produced components for the Bajaj Chetak in the 1980s are still running, maintained with the dedication usually reserved for vintage cars. The workforce, grayed but proud, operates equipment that predates most of India's IT industry. It's industrial archaeology masquerading as active manufacturing.

The numbers tell a story of deliberate downsizing without closure. Current manufacturing revenue hovers around ₹200 crores annually, a fraction of the glory days. The product mix has shifted from complete scooter assembly to specialized components: pressure die-casting dies, jigs, fixtures, and precision components for the two and three-wheeler industry. Think of it as moving from making entire watches to just producing the tiny screws—less glamorous, but surprisingly sticky as a business.

The operating losses—roughly ₹20-30 crores annually—are treated with the kind of accounting creativity that would make Silicon Valley jealous. They're not losses; they're "investments in maintaining manufacturing capability." The tax benefits from these losses offset dividend income, creating a perverse incentive to keep losing money. It's the only manufacturing unit in India where breaking even would actually be bad news.

The customer concentration is extreme even by Indian standards. Bajaj Auto accounts for over 70% of orders, paying prices that generously could be called "fair" and realistically could be called "subsidized." The remaining customers are tier-2 automotive suppliers who value the Maharashtra Scooters name on their vendor list more than the actual components. It's reputation arbitrage—associating with a listed company provides credibility worth more than the price premium.

The workforce situation defies economic logic. Approximately 300 employees maintain operations that could be managed by 50. But labor laws, union agreements, and political considerations make downsizing impossible. Instead, there's a bizarre arrangement where employees are paid to maintain skills that might be needed someday, like keeping a fire department in a city that switched to fireproof buildings. The average employee age is 52, and recruitment is essentially frozen—the unit is demographically downsizing, waiting for biology to solve what economics cannot.

The technology in use is fascinatingly obsolete. While the world has moved to 3D printing and automated manufacturing, Maharashtra Scooters still uses manual lathes and analog measurement tools. The justification? These components require "craftsman's touch" that machines can't replicate. The reality? Nobody wants to invest in upgrading equipment for a business everyone pretends might close tomorrow.

Yet somehow, this zombie manufacturing operation serves crucial strategic purposes. First, it maintains the manufacturing license—a valuable regulatory asset in India where getting new industrial permits is harder than explaining cryptocurrency to your grandmother. Second, it provides the legal fiction that Maharashtra Scooters is still a manufacturing company, avoiding awkward questions about why an investment company is listed on the stock exchange.

The quality certifications tell their own story. The unit maintains ISO 9001, TS 16949, and various other automotive standards—not because customers demand them, but because letting them lapse would signal surrender. The quality control department, staffed by engineers who could probably rebuild a Chetak blindfolded, maintains documentation standards that would impress German auditors. It's excellence in service of inertia.

The real estate occupied by the manufacturing unit is worth multiples of the business itself. Located in what's now prime industrial land near Pune, developers circle like vultures, offering prices that would make the stock price double overnight. But selling would mean acknowledging what everyone already knows—Maharashtra Scooters is no longer a manufacturing company. So the land sits, worth hundreds of crores, hosting an operation that loses tens of crores, because admitting reality is apparently more expensive than maintaining fiction.

The supply chain relationships reveal unexpected value. Decades-old vendor relationships, credit terms negotiated when Indira Gandhi was prime minister, and a reputation for paying on time even during losses create a network effect. Small suppliers stay loyal not for the business volume but for the stability. In India's volatile manufacturing sector, a customer that's been ordering for forty years, even small quantities, is worth keeping.

The R&D department, such as it is, consists of three engineers who spend their time improving processes that won't be replaced and designing components for products that won't be launched. They file patents occasionally—not for commercial value but to justify their existence. It's innovation theater, performed for an audience that stopped watching years ago.

The environmental compliance is exemplary, mainly because doing nothing is environmentally friendly. The unit produces minimal waste, uses no hazardous chemicals, and has energy consumption that would make Greta Thunberg smile. It's probably India's greenest manufacturing unit by default—hard to pollute when you're barely producing.

Looking forward, the manufacturing stub will likely continue its slow-motion wind-down. No dramatic closure, no grand restructuring, just gradual attrition as workers retire and machines finally break beyond repair. It's the corporate equivalent of hospice care—keeping comfortable something that everyone knows is dying but nobody wants to officially pronounce dead.

IX. Governance, Ownership & Corporate Structure

The annual general meeting of Maharashtra Scooters resembles a family wedding where everyone knows there's drama but maintains polite conversation. The promoter group, sitting at 51% ownership through Bajaj Holdings, occupies the head table. Public shareholders, holding 49%, fill the remaining seats, knowing they're guests at someone else's party. It's corporate democracy in theory, family control in practice.

The board composition reads like a who's who of Indian corporate governance—and that's both a compliment and a concern. Independent directors with impeccable credentials share the table with Bajaj family members and nominees. The board meetings, according to sources, are cordial affairs where real decisions have already been made in Pune before anyone reaches Mumbai. The independent directors provide oversight in the way that traffic lights control Formula 1 races—present, blinking, but largely irrelevant to the outcome.

The Core Investment Company (CIC) status adds regulatory intrigue. Maharashtra Scooters qualifies as a CIC under RBI guidelines—more than 90% of assets in financial investments, no public deposits. But it hasn't registered as an NBFC-CIC because of a beautiful loophole: it's still technically a manufacturing company. This regulatory arbitrage means avoiding RBI oversight while enjoying the flexibility of an investment company. It's like claiming you're a vegetarian while running a steakhouse because you also serve salad.

Related party transactions are where things get genuinely Byzantine. Maharashtra Scooters buys components from Bajaj Auto at "arm's length prices"—if your arm is short and the length is measured in millimeters. It invests surplus funds in Bajaj Finance debentures at market rates that happen to be set by Bajaj Finance. The audit committee approves these transactions with the diligence of someone checking their own homework.

The minority shareholder protection mechanisms exist in the same way that smoke detectors exist in submarines—technically present but practically useless. The company follows all regulations, files all reports, maintains all committees. But when the promoter owns 51% and the investment portfolio consists entirely of promoter group companies, minority shareholders are essentially along for whatever ride the Bajaj family chooses to provide.

The dividend policy, or lack thereof, exemplifies the governance challenge. Despite generating hundreds of crores in dividend income, Maharashtra Scooters pays out peanuts to its shareholders. The board minutes probably record discussions about "maintaining reserves for future opportunities," but everyone knows the real reason: why share wealth when you don't have to? The occasional special dividend feels less like strategic capital allocation and more like throwing breadcrumbs to keep the pigeons from getting too restless.

Information asymmetry is built into the structure. The real value creation happens at Bajaj Auto and Bajaj Finance, but Maharashtra Scooters shareholders only get quarterly glimpses through investment income reporting. It's like watching a movie through a keyhole—you can see something's happening, but you're missing most of the action. The parent company knows everything; public shareholders know what they're told.

The auditor rotation policy follows regulations precisely, but the same audit firm that audits Bajaj Holdings also audits Maharashtra Scooters. Independence is maintained through Chinese walls that are probably more like Japanese screens—technically separating spaces while everyone can hear everything. The audit reports are clean, as they should be when your main activity is receiving dividends and banking them.

Board committees function with bureaucratic precision. The audit committee meets quarterly to review finances that could be understood by a first-year commerce student. The nomination committee considers directors pre-selected by the promoters. The CSR committee allocates the mandatory 2% to causes that, coincidentally, align with Bajaj Foundation priorities. It's governance theater performed for regulatory audiences.

The institutional investor engagement is particularly revealing. Proxy advisory firms regularly recommend voting against resolutions, citing related party concerns and board independence issues. These recommendations are routinely ignored because, with 51% voting power, the promoter doesn't need anyone's agreement. The voting results are foregone conclusions announced with the solemnity of election results in single-party states.

Succession planning, that great governance buzzword, is straightforward here. The company will be run by whoever runs Bajaj Holdings, which will be run by whoever the Bajaj family designates. The independent directors might provide input, but it's like suggesting baby names to parents who've already filled out the birth certificate.

The whistleblower policy exists, properly documented and communicated. What exactly someone would blow the whistle about in a company that primarily banks dividend checks remains unclear. "Alert! They deposited the Bajaj Auto dividend in the same bank account as last quarter!" The vigil mechanism is like a security system for a bank vault containing other bank vaults.

Environmental, Social, and Governance (ESG) reporting has recently been introduced, creating the amusing situation of rating the sustainability of not manufacturing. The carbon footprint is exemplary—hard to pollute when your main activity is receiving electronic fund transfers. The social impact is measured in maintaining employment for workers who might otherwise be unemployed. The governance scores depend on whether you consider family control a bug or a feature.

Looking at the shareholding pattern over time reveals steady consolidation. The public float has gradually decreased as the promoter group accumulated shares during periodic downturns. It's a slow-motion privatization, executed through market purchases rather than delisting offers. At the current pace, Maharashtra Scooters might become a closely-held company by 2040, assuming regulations still permit public listing by then.

X. Playbook: Investment Company Lessons

The Maharashtra Scooters story offers a masterclass in corporate transformation through inaction—a playbook written not in strategy documents but in the accumulated sediment of quarterly results. For investors and operators alike, the lessons are counterintuitive, occasionally absurd, but undeniably effective in the specific context of Indian capital markets.

When to Pivot vs. When to Shut Down

The conventional wisdom says: pivot fast or die faster. Maharashtra Scooters suggests another option: pivot so slowly that nobody notices you've pivoted at all. When scooter manufacturing became unviable in 2006, the rational response would have been closure. Instead, the company discovered that maintaining the fiction of manufacturing while becoming a de facto investment company was more valuable than either pure option.

The lesson isn't to avoid hard decisions—it's to recognize when avoiding a decision is itself a strategic choice. In markets with high closure costs (regulatory, labor, political), sometimes the best pivot is to let the old business atrophy while the new one grows around it, like a hermit crab gradually transitioning shells.

The Value of Patient Capital in Emerging Markets

Maharashtra Scooters' investment portfolio turned ₹500 crores into ₹15,000 crores not through brilliant stock picking but through the radical strategy of never selling. In emerging markets, where the best companies compound at 20-25% annually for decades, the biggest risk isn't volatility—it's premature profit-taking.

The portfolio concentration that would horrify modern portfolio theorists—90% in group companies—worked because the investor had information advantages and alignment that diversified investors lack. When you know the management, understand the business, and have board representation, concentration isn't risky—it's logical.

Managing Government JV Partners

The thirteen-year dance with WMDC before their exit teaches a crucial lesson: government partners in India don't respond to economic logic; they respond to political pressure. WMDC held onto their stake long after the JV's purpose was fulfilled, not because it made sense but because nobody wanted to make the decision to exit.

The playbook for managing such partners is patience combined with subtle pressure. Make their position increasingly untenable (an investment company doesn't fulfill regional development mandates) while providing face-saving exits (the purchase price, while low, was presented as a "win" for the state). Never force the issue; let political evolution solve what negotiation cannot.

Creating Value Through Financial Engineering vs. Operations

The traditional view holds that financial engineering is inferior to operational excellence. Maharashtra Scooters proves that in certain contexts, financial engineering IS operational excellence. The company created more value through tax-efficient dividend collection and compound investing than it ever did through manufacturing.

The key insight: in markets with complex tax codes and holding company structures, the CFO can create more value than the CEO. Understanding inter-corporate dividend taxation, capital gains deferrals, and regulatory arbitrage opportunities becomes the core competency. It's not sexy, but it's incredibly effective.

The Holding Company Structure as Wealth Preservation

Indian business families have perfected the art of using holding companies to maintain control while accessing public capital. Maharashtra Scooters shows how this works in practice: layer upon layer of ownership that makes hostile takeovers impossible and minority squeeze-outs difficult.

The structure serves multiple purposes: tax efficiency (dividends flow tax-free between group companies), control preservation (51% at each level maintains absolute control), and optionality (each entity can be leveraged, sold, or merged independently). It's complexity as a defensive moat.

Tax Efficiency and Dividend Distribution Strategies

The company's approach to dividend distribution—minimal regular dividends punctuated by irregular special dividends—might seem arbitrary, but it's actually sophisticated tax planning. Regular dividends set expectations; special dividends provide flexibility. The timing often coincides with tax law changes or when shareholders need to realize gains for their own tax planning.

The manufacturing losses, maintained deliberately, provide tax shields against dividend income. It's the corporate equivalent of wealthy individuals maintaining loss-making farms for tax benefits. The loss is real, but so are the tax savings, and the net effect is positive.

The Option Value of Maintaining Licenses and Registrations

Why keep a manufacturing license for a business you've abandoned? Because in India, getting new licenses is exponentially harder than maintaining old ones. Maharashtra Scooters' manufacturing registration, land permits, and environmental clearances have option value—they could be activated if needed or, more likely, sold to someone who needs them.

This extends to the stock exchange listing itself. Maintaining a listed entity, even one that does nothing, provides a vehicle for future financial engineering. It's like keeping a shell company, except it's not a shell—it's a fully operational company that happens to operate very little.

Managing Stakeholder Expectations in Transformation

The genius of Maharashtra Scooters' transformation was never announcing it. No "pivot to fintech" press releases, no "strategic transformation initiatives," no consultants brought in to bless the obvious. The company just quietly changed what it did while maintaining the appearance of continuity.

This works in markets where dramatic announcements trigger regulatory scrutiny, tax reassessments, and stakeholder resistance. Sometimes the best way to change everything is to insist nothing has changed while filing quarterly results that tell a different story.

The Permanent Capital Advantage

Unlike private equity funds with ten-year horizons or mutual funds with quarterly redemptions, Maharashtra Scooters has permanent capital. This allows investment strategies impossible for conventional fund managers: holding through multiple cycles, ignoring mark-to-market volatility, and benefiting from compound effects that only manifest over decades.

The lesson for investors: structure matters as much as strategy. The same investment approach that would get a fund manager fired for underperformance can create enormous wealth in a permanent capital vehicle. Time horizon isn't just an investment parameter—it's the ultimate competitive advantage.

XI. Bear vs. Bull Case Analysis

The Bull Case: Hidden Value in Plain Sight

The optimists see Maharashtra Scooters as a cigar butt with several puffs left—Warren Buffett's classic value investment selling at a fraction of its intrinsic worth. The math is compelling: a market cap of ₹16,738 crores for a company holding investments worth over ₹15,000 crores, plus a manufacturing business, plus real estate, plus the option value of its licenses and registrations.

The indirect exposure to Bajaj Group's crown jewels offers a discounted entry point into two of India's best-performing companies. Bajaj Finance has compounded at over 30% annually for a decade. Bajaj Auto has consistently delivered industry-leading margins. Buying Maharashtra Scooters at a 60% discount to its holding value is like buying these champions at 40 cents on the dollar.

The company is essentially debt-free, with a clean balance sheet that would make conservative investors swoon. In an era of leveraged growth stories and aggressive accounting, Maharashtra Scooters' simplicity is refreshing. The investment portfolio is liquid, marked conservatively, and generating predictable dividend income. What you see is what you get, and what you get is worth significantly more than what you pay.

The potential for corporate simplification offers massive upside. If Bajaj Holdings ever decides to merge Maharashtra Scooters, minority shareholders would likely receive shares in the parent at closer to NAV. The holding company discount could evaporate overnight, creating a 50-100% return without any change in underlying business performance. It's not a question of if, but when the Bajaj family decides to clean up the structure.

Special dividends provide periodic windfall gains. While unpredictable in timing, they're inevitable given the cash generation. The company literally cannot reinvest all its dividend income productively, so eventually, it must return cash to shareholders. Each special dividend is like a lottery ticket you know will eventually win—you just don't know when.

The manufacturing stub, while currently loss-making, has option value in India's growing automotive market. If two-wheeler demand explodes again, if electric vehicles require specialized components, if Bajaj Auto needs additional capacity—the infrastructure is there, ready to be activated. It's a free call option on India's manufacturing renaissance.

The Bear Case: Value Trap in Perpetuity

The pessimists see a corporate structure designed to benefit promoters at the expense of minorities. The 51% control means public shareholders are permanent guests at someone else's party, hoping for scraps from the head table. No amount of discount makes a bad governance structure a good investment.

The five-year revenue decline of 2.71% tells the real story—this is a dying manufacturing business propped up by legacy investments. The operational losses aren't temporary; they're structural. The company lacks the will to shut down manufacturing and lacks the capability to revive it. It's corporate purgatory, neither living nor dead.

The return on equity of 0.78% over three years is abysmal by any standard. Yes, the book value understates market value, but even adjusting for that, the returns are mediocre. The company generates returns below the risk-free rate while taking equity risk. You could buy government bonds and sleep better.

The holding company discount isn't a temporary market inefficiency—it's a permanent feature reflecting genuine governance concerns. Markets aren't stupid; they're pricing in the probability that minority shareholders will never receive fair value. The discount has persisted for fifteen years and will likely persist for fifteen more.

The complexity of the structure makes it uninvestible for most institutions. Foreign investors can't understand it, domestic institutions can't justify it, and retail investors can't analyze it. Without natural buyers, the stock will continue trading at massive discounts regardless of intrinsic value. It's cheap for a reason, and the reason isn't going away.

The lack of growth catalysts means the investment case relies entirely on multiple expansion—hoping someone will pay more for the same assets tomorrow. But why would they? The company isn't growing, isn't improving operations, isn't simplifying structure. It's a value trap where the value is real but permanently inaccessible.

The ESG concerns are mounting. A company that exists primarily to hold stakes in other companies while maintaining a loss-making manufacturing operation fails on environmental efficiency, social purpose, and governance standards. As ESG investing becomes mandatory, Maharashtra Scooters becomes increasingly uninvestible.

The opportunity cost is enormous. While investors wait for value realization that may never come, Indian markets offer dozens of companies growing at 15-20% annually with clean structures and aligned management. Why tie up capital in a governance quagmire when better opportunities abound?

The Verdict: A Rorschach Test for Value Investors

Maharashtra Scooters is ultimately a Rorschach test for investment philosophy. Value investors see a dollar selling for fifty cents. Growth investors see a dying business with no future. Governance advocates see a structure designed to preserve family control. Tax experts see a brilliantly efficient capital structure.

The truth encompasses all these perspectives. It's simultaneously undervalued and likely to remain so, profitable but not growing, well-managed for the promoters but not for minorities. It's an investment that makes perfect sense on spreadsheets and no sense in reality.

For patient investors with a twenty-year horizon and no need for liquidity, it might work. For anyone else, it's probably better admired as a case study than owned as an investment. The bull case is mathematically correct; the bear case is practically correct. In the conflict between math and reality, reality usually wins, but occasionally, very occasionally, patience rewards those who bet on the numbers.

XII. Epilogue: The Future of Indian Holding Companies

The boardroom at Bajaj Holdings' headquarters has witnessed countless strategic decisions, but the question that lingers unresolved is perhaps the simplest: what exactly is Maharashtra Scooters supposed to be? Six years after becoming a subsidiary, five years after the last meaningful merger speculation, the company continues its existence as a corporate paradox—generating returns that would make fund managers envious while maintaining the pretense of being a manufacturer.

The logic for consolidation seems obvious. As one analyst noted, "Post-exit of WMDCL, the merger of MSL & BHIL should happen as there is no commercial rationale to have two holding companies in the group." Yet here we are in 2025, with Maharashtra Scooters still independently listed, still filing separate results, still confusing investors who can't decide if they're buying a manufacturer with investments or an investment company with a factory.

The potential merger math is tantalizing. If consolidation were to happen based on current market prices, the shareholding restructuring would be complex but manageable, with various options including buybacks or preference shares to maintain promoter control levels. The holding company discount—that persistent 40-60% gap between price and underlying value—could theoretically evaporate overnight. It's the kind of value unlock that makes investment bankers salivate and minority shareholders dream.

But the Bajaj Group operates on geological time scales when it comes to corporate restructuring. The WMDC exit took sixteen years from initial offer to completion. The transformation from manufacturer to investment company took thirteen years to acknowledge. At this pace, Maharashtra Scooters might merge with its parent sometime around 2040, assuming the concept of public companies still exists by then.

The recent corporate actions tell a story of gradual unwinding rather than dramatic transformation. In July 2025, both the CEO and Company Secretary resigned, with the CEO accepting a Voluntary Separation Scheme. It's the corporate equivalent of slowly turning off lights in an empty building—not quite abandonment, but certainly not expansion.

The financial performance continues to baffle traditional analysis. For Q4 FY2025, net profit surged an astronomical 51,530% to ₹51.63 crores despite sales of just ₹6.65 crores. For the full year, net profit rose 7.55% to ₹214.35 crores even as sales declined 17.69% to ₹183.33 crores. These aren't business results; they're the financial equivalent of a magic trick where the rabbit appears without anyone pulling it from the hat.

The dividend policy has finally shown signs of generosity. The board recommended a final dividend of ₹30 per share plus a special dividend of ₹30 per share for FY2025, with June 27, 2025 as the record date. It's as if management suddenly remembered that public shareholders exist and deserve more than token returns on their patience.

The broader Indian holding company landscape is evolving rapidly around Maharashtra Scooters. SEBI's new regulations on related party transactions, enhanced disclosure requirements, and pressure on governance standards are making complex structures increasingly difficult to maintain. The old ways of circular holdings and opaque transactions are giving way to demands for simplification and transparency.

Yet Maharashtra Scooters persists in its twilight existence, neither fully alive as a manufacturer nor fully acknowledged as an investment company. It continues as an unregistered Core Investment Company with 90% of assets in Bajaj group companies and the balance in debt instruments. The regulatory arbitrage of being technically a manufacturer while functionally an investment company can't last forever, but apparently it can last longer than anyone expected.

The international investment community remains bewildered. Foreign institutional ownership is negligible—explaining this structure to a portfolio manager in London or New York requires PowerPoint slides that violate the laws of both finance and common sense. "So it's a company that makes losses manufacturing but profits from investments?" "Yes." "And it trades at a massive discount to its holdings?" "Yes." "And nothing is being done about this?" "Correct." "I'll pass."

The next generation of Bajaj leadership, represented by Sanjiv Bajaj and his cousins, supposedly brings a more modern approach to corporate structure. But actions speak louder than intentions, and so far, the actions have been minimal. Maharashtra Scooters remains a monument to path dependency—a structure that exists because it has always existed, continuing because stopping would require decisions nobody wants to make.

Looking ahead, three scenarios seem possible. First, the status quo continues indefinitely—Maharashtra Scooters remains a listed curiosity, generating returns for patient shareholders while frustrating anyone seeking strategic clarity. Second, a gradual privatization through creeping acquisitions until the free float becomes so small that delisting becomes feasible. Third, and least likely but most value-accretive, a genuine merger with Bajaj Holdings that unlocks value for all shareholders.

The smart money is betting on scenario one. In Indian corporate life, inertia is the most powerful force, stronger than logic, strategy, or shareholder activism. Maharashtra Scooters will likely continue its existence as a zombie manufacturer and accidental investment genius, a corporate Schrödinger's cat that is simultaneously dead and alive, manufacturing and investing, valuable and cheap.

What Maharashtra Scooters ultimately represents is the unique nature of Indian capitalism—where family control matters more than market efficiency, where complexity provides safety, and where patient capital can generate extraordinary returns despite, not because of, corporate strategy. It's a business model that shouldn't work but does, a governance structure that shouldn't exist but persists.

For investors, Maharashtra Scooters remains what it has always been: a test of patience and philosophy. Those who see a dollar trading for fifty cents will continue to accumulate, waiting for the inevitable value realization. Those who see a governance nightmare will stay away, refusing to participate regardless of the discount. Both are right, both are wrong, and both will probably maintain their positions for years to come.

The future of Indian holding companies isn't Maharashtra Scooters—it's too peculiar, too specific to its circumstances to be replicated. But its continued existence proves that in Indian markets, the exceptional can become routine, the temporary can become permanent, and sometimes the best strategy is having no strategy at all. As we witness the gradual evolution of Indian corporate governance, Maharashtra Scooters stands as a reminder that evolution doesn't always mean progress—sometimes it just means surviving long enough for everyone to forget what you were supposed to be in the first place.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube