Mahindra & Mahindra: The Rise of India's Automotive and Agricultural Pioneer

I. Introduction & Episode Roadmap

Picture this: It's 2024, and in the dusty fields of Punjab, a farmer starts his tractor at dawn. The machine roars to life with a familiar red logo gleaming in the morning sun. Meanwhile, 1,500 kilometers away in Mumbai, a young executive climbs into her new Thar, ready to escape the city for a weekend adventure. And in a Formula E paddock in Monaco, engineers huddle over telemetry data from an electric race car pushing the boundaries of sustainable speed. What connects these three scenes? They're all powered by Mahindra & Mahindra—a company that began as a steel trading firm in pre-independence India and transformed into a $23 billion conglomerate that dominates tractors globally and SUVs domestically.

How does a company founded in the chaos of partition, with a name they couldn't afford to change, become the world's largest tractor manufacturer by volume? How does it maintain 42.9% market share in Indian tractors for 35 consecutive years while simultaneously becoming India's SUV king? The answer lies in a uniquely Indian playbook of frugal innovation, strategic patience, and an uncanny ability to understand what mobility means in a nation of 1.4 billion people.

This is the story of Mahindra & Mahindra—abbreviated as M&M, trading on the NSE with the same symbol. It's a tale of partition-era entrepreneurship, license raj navigation, global ambitions meeting local realities, and the audacious belief that an Indian company could build world-class vehicles. We'll explore how the Mahindra brothers turned adversity into opportunity, why tractors became their unexpected goldmine, how they cracked the SUV code before anyone else in India, and what their electric vehicle journey reveals about the future of mobility.

Over the next few hours, we'll dissect the major inflection points: the Willys Jeep gamble of 1947, the tractor revolution of the 1960s, the Scorpio breakthrough of 2002, and the recent electric pivot. We'll analyze their acquisition strategy—from the triumph of Swaraj to the painful exit from SsangYong. And we'll examine how Anand Mahindra transformed not just a company but created a philosophy—"Rise"—that resonates across India's aspirational middle class.

What makes Mahindra fascinating isn't just its scale—it's the contradictions it embodies. A conglomerate that spans 20+ industries yet maintains focus. A company rooted in rural India that races in Formula E. A firm that builds both $6,000 tractors and $3 million Pininfarina hypercars. Understanding Mahindra means understanding India's economic evolution itself.

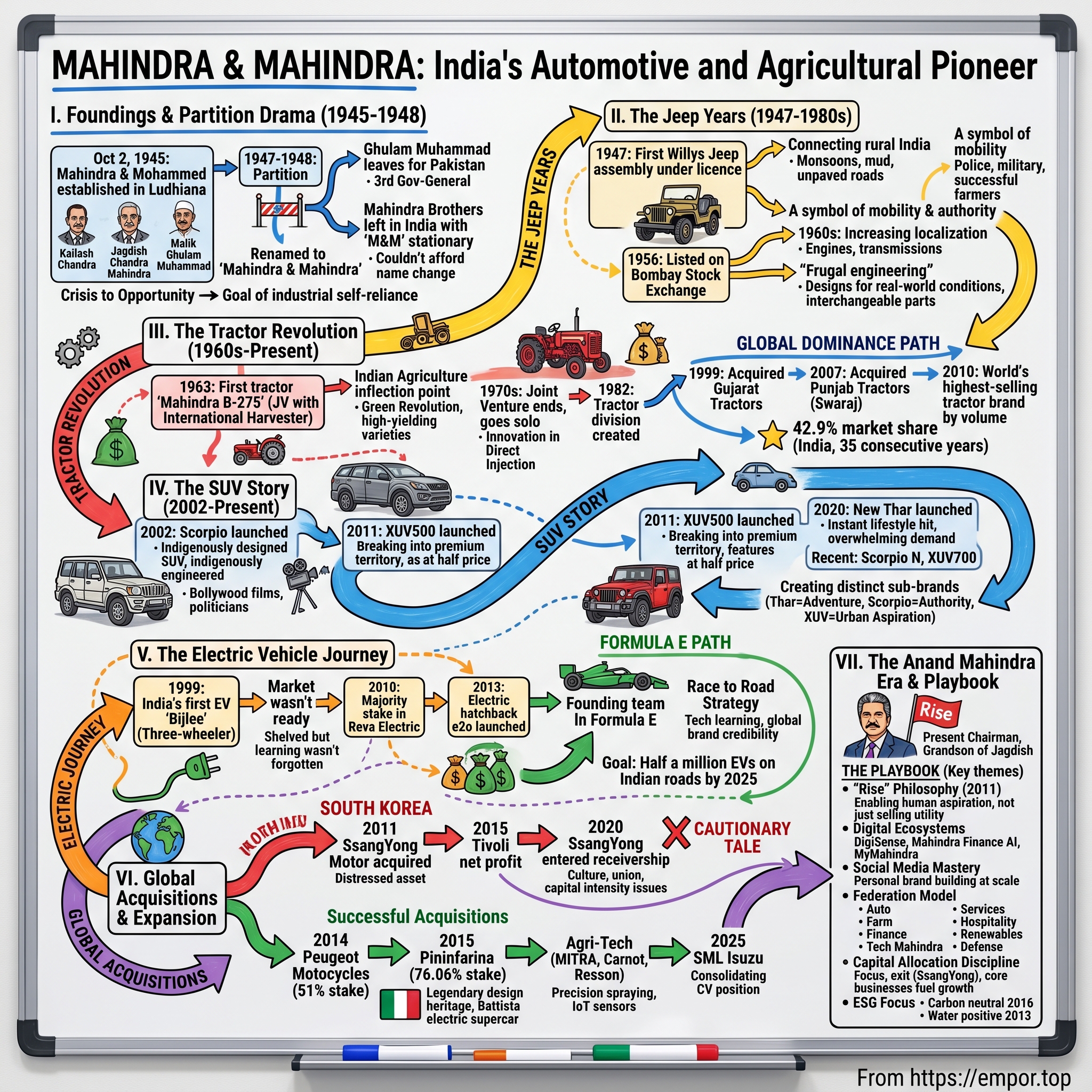

II. The Founding Story & Partition Drama

The date was October 2, 1945—Gandhi's birthday, though India was still two years away from independence. In Ludhiana, Punjab, two brothers—Kailash Chandra Mahindra and Jagdish Chandra Mahindra—sat with their business partner Malik Ghulam Muhammad, signing papers to establish "Mahindra & Mohammed." The irony wasn't lost on them: launching a company amid the death throes of the British Raj, when the future map of India itself was uncertain.

The Mahindra brothers came from a prosperous Punjabi family with interests in steel trading. Ghulam Muhammad brought capital and connections. Together, they saw opportunity in the post-World War II reconstruction boom. Steel was the backbone of rebuilding nations, and India—whatever form it would take—would need massive amounts of it. Their initial business model was straightforward: import steel, distribute it across North India, and build relationships with emerging industrialists.

But history had other plans. In August 1947, India gained independence—and was immediately cleaved in two. The partition of India and Pakistan triggered one of the largest mass migrations in human history. Twelve million people crossed borders; a million died in communal violence. For Mahindra & Mohammed, the political became deeply personal. By 1948, history caught up with the partnership. Ghulam Mohammed decided to move to the newly formed Pakistan, where he would eventually become the third governor-general of Pakistan from 1951 to 1955 and play a controversial role in that nation's early political development. The Mahindra brothers faced a peculiar problem: they were left with stationary and company stamp that said M&M. They did not have the financial resources to change the name.

Here's where pragmatism met serendipity. Since there were two Mahindra brothers in the business they decided to change the company name to Mahindra & Mahindra. The ampersand remained; only the meaning changed. What started as a symbol of Hindu-Muslim partnership became a family enterprise—though the brothers kept the familiar "M&M" abbreviation that customers already knew.

The partition story reveals something fundamental about Mahindra's DNA: the ability to transform crisis into opportunity. Losing a founding partner and significant capital in 1948 could have killed the young company. Instead, the brothers pivoted. They looked at post-independence India with fresh eyes. What did this new nation need? Not just steel trading, but manufacturing capability. Not just imported goods, but domestic production. The partition didn't just divide a country—it crystallized Mahindra's vision of industrial self-reliance.

The timing of their founding—October 2, 1945, Gandhi's birthday—wasn't coincidental but prophetic. Just as Gandhi envisioned political independence, the Mahindras envisioned economic independence. They understood that India's future lay not in remaining a market for foreign goods but in becoming a manufacturer for its own people and eventually the world. This philosophy would drive every major decision for the next eight decades.

III. The Jeep Years: Building India's Mobility (1947–1980s)

The year was 1947. While India celebrated independence and mourned partition simultaneously, the Mahindra brothers stood in a Bombay warehouse looking at knocked-down kits of Willys Jeeps. The American military had left behind these vehicles after World War II, and Willys-Overland was eager to find new markets for their rugged machines. The brothers saw what others missed: in a country with barely any paved roads, where bullock carts were still the primary transport, these all-terrain vehicles weren't just products—they were perfect infrastructure.

M&M saw a business opportunity in expanding into manufacturing and selling larger multi utility vehicles (MUVs) and started assembling under the licence of Willys Jeep in India. The first Mahindra Jeep rolled off their makeshift assembly line in 1947, the same year India gained independence. The symbolism was powerful: a new nation and a new kind of mobility, both finding their feet together.

Consider the context. Post-independence India had inherited 400,000 kilometers of roads, but only 65,000 were paved. The monsoons turned dirt tracks into rivers of mud. Villages remained cut off for months. Government officials, police, military personnel, farmers with produce—everyone needed vehicles that could handle this reality. The Willys Jeep, battle-tested in World War II, was engineered for exactly these conditions.

The early years were brutal. In 1949, Mahindra assembled just 75 vehicles. By 1953, they had scaled to 1,200 units annually—still tiny numbers, but each vehicle represented a small revolution in its district. A single Jeep could transform a village's access to markets, hospitals, and schools. Mahindra wasn't just selling vehicles; they were selling connectivity in a disconnected nation.

The License Raj era (1947-1991) created unique challenges and opportunities. Foreign companies couldn't easily enter India. Import duties were prohibitive. Government permits were needed for everything from capacity expansion to pricing decisions. While these restrictions strangled many businesses, Mahindra turned them into moats. Their early license to manufacture Willys Jeeps became increasingly valuable as competitors found entry blocked by bureaucratic walls.

Soon, M&M was established as the Jeep manufacturer in India and later commenced manufacturing light commercial vehicles (LCVs) and agricultural tractors. By 1956, the company had grown confident enough to list on the Bombay Stock Exchange. The IPO wasn't just about raising capital—it was a statement that an Indian manufacturing company could stand alongside the established trading houses and textile mills that dominated the exchange.

The 1960s marked a crucial evolution. Mahindra began increasing local content in their vehicles, partly due to government mandates but mainly from necessity. Importing components was expensive and slow. They started with simple parts—seats, tires, batteries—then moved to engines and transmissions. Each localization reduced costs and built capabilities. By 1969, Mahindra had transformed from an assembler to a manufacturer, becoming an exporter of utility vehicles and spare parts.

The numbers tell the story of steady, unglamorous growth. From 1,200 units in 1953, production climbed to 5,000 by 1965, 10,000 by 1975, and 21,000 by the early 1980s. These weren't Silicon Valley growth rates, but in the context of License Raj India, they represented remarkable expansion. Each production increase required government approval, each new model needed permits, each price change faced scrutiny.

What's fascinating about the Jeep years is how Mahindra built a brand without modern marketing. There was one television channel, Doordarshan, with limited reach. Print advertising was expensive and ineffective in reaching rural customers. Instead, Mahindra's Jeeps marketed themselves. When a district collector arrived in a village in his Mahindra Jeep, it projected authority. When a successful farmer drove one to the market, it signaled prosperity. The vehicle became a symbol of upward mobility in an India where mobility—social and physical—was heavily constrained.

The company also pioneered what would later be called "frugal engineering." Indian customers couldn't afford American prices or American maintenance costs. Mahindra simplified designs, used locally available materials, and built vehicles that village mechanics could repair with basic tools. A Mahindra Jeep from the 1960s could run on kerosene mixed with diesel when pure diesel wasn't available. Parts were interchangeable across models. This wasn't cost-cutting—it was designing for reality.

By 1980, Mahindra faced a crossroads. The Jeep market was saturating. Urban India was slowly emerging with different transportation needs. Agricultural mechanization was accelerating. The company had built formidable manufacturing capabilities and distribution networks, but needed new products to feed them. The answer would come from an unexpected direction: tractors. But before that transformation, Mahindra had established something crucial—proof that an Indian company could take foreign technology, adapt it for local conditions, and build a sustainable manufacturing business. The Jeep years weren't just about vehicles; they were about building the confidence and capability for everything that would follow.

IV. The Tractor Revolution & Global Dominance (1960s–Present)

In 1961, a Mahindra engineer stood in a Punjab wheat field watching farmers struggle with traditional plowing methods. Bullocks were slow, unreliable, and couldn't handle the increasing farm sizes created by land reforms. That engineer's report would trigger one of the most successful pivots in Indian corporate history. Two years later, in 1963, the company introduced its first tractor, the Mahindra B-275, as part of a joint venture with International Harvester.

The B-275 wasn't just a tractor—it was a 35-horsepower revolution on wheels. Priced at ₹18,000 (roughly $3,800 then), it cost more than most farmers' annual income. Yet Mahindra understood something profound: Indian agriculture was at an inflection point. The Green Revolution was beginning. High-yielding varieties of wheat and rice needed precise timing for planting and harvesting. A delayed harvest could mean crop loss. A tractor could cover in hours what bullocks needed days to accomplish.

Initially, sales were modest—just 253 tractors in the first year. But Mahindra played a long game. They established training centers where farmers could learn to operate and maintain tractors. They created innovative financing schemes, including harvest-based payment plans. Most importantly, they designed tractors specifically for Indian conditions: smaller than American models but more powerful than European ones, with high ground clearance for flooded fields and engines that could run on variable-quality diesel.

The 1970s brought challenges and opportunities. International Harvester wanted to increase prices and reduce localization. Mahindra wanted the opposite. The partnership grew strained. Meanwhile, Indian agriculture was transforming. The Green Revolution had succeeded beyond expectations. Punjab and Haryana were producing wheat surpluses. Farmers had money and needed mechanization. In 1977, Mahindra made a bold decision: they ended the International Harvester joint venture and went solo.

Going independent was risky but liberating. Mahindra could now innovate freely. They introduced the 265 DI in 1978—"DI" standing for direct injection, a technology that improved fuel efficiency by 20%. In an era of oil shocks and diesel shortages, this mattered immensely. They also pioneered the concept of "right-sized" tractors. While international manufacturers pushed larger, more powerful machines, Mahindra realized most Indian farms needed 30-40 horsepower tractors that were affordable, efficient, and maneuverable in small fields.

Mahindra & Mahindra created a tractor division in 1982, signaling that tractors weren't just another product line but a core business deserving dedicated resources and leadership. This organizational change coincided with agricultural liberalization. The government eased restrictions on tractor manufacturing, allowed new players to enter, and removed price controls. Competition intensified, but so did the market opportunity.

The 1990s marked Mahindra's transformation from domestic leader to global force. Economic liberalization opened India to foreign brands like John Deere and New Holland. Instead of retreating, Mahindra accelerated. They acquired Gujarat Tractors Limited in 1999, gaining access to the Shaktimaan and Bhoomiputra brands popular in western India. The real masterstroke came in 2007 with the acquisition of Punjab Tractors Limited, makers of Swaraj tractors. Swaraj held 14% market share and brought advanced technology plus a fanatically loyal customer base in Punjab. In 2010, Mahindra became the world's highest-selling tractor brand by volume. This wasn't just a milestone—it was validation of a 47-year journey from licensed manufacturer to global leader. Having rolled out its first tractor in 1963 through a partnership with International Harvester Inc. of the U.S., Mahindra Tractors surpassed the 1-Million-unit production mark in 2004 and then went on to claim the title of the world's highest-selling farm tractor manufacturer by volume in 2009.

The numbers are staggering. Mahindra reached the 2-Million-unit production milestone in 2013, followed by the 3-Million mark in 2019. Mahindra Tractors achieved a milestone by selling the brand's 40th Lakh tractor, inclusive of exports in March 2024. That's 4 million tractors—enough to mechanize agriculture across continents.

But the real story isn't in the numbers—it's in the market position. For more than three remarkable decades, Mahindra has proudly held the title of India's unrivalled No. 1 tractor brand and the world's largest manufacturer of tractors by volume. Currently holding 42.9% market share in the Indian tractor industry, Mahindra hasn't just led—it has dominated for 35 consecutive years.

How does a company maintain such dominance? The answer lies in understanding that in India, a tractor isn't just farm equipment—it's a multipurpose economic asset. Farmers use tractors for plowing, yes, but also for transportation, running water pumps, powering mills, and even as wedding vehicles. Mahindra designed for this reality, creating tractors that were Swiss Army knives on wheels.

The global expansion strategy was methodical. Mahindra tractors are available in 40 countries, including India, the United States, China, Australia, New Zealand, Africa, Latin America, South Asia, the Middle East and Eastern Europe. Each market required different approaches. In the US, Mahindra focused on compact tractors for hobby farmers and landscapers. In Africa, they emphasized durability and serviceability. In Europe, they stressed emissions compliance and precision farming capabilities.

Recent acquisitions have strengthened their position further. Beyond Gujarat Tractors and Swaraj, Mahindra acquired stakes in Mitsubishi Agricultural Machinery (33.33% in 2015), Finland's Sampo Rosenlew (35% in 2016, increased to 49.04% in 2019), and Turkish companies Hisarlar and Erkunt in 2017. Each acquisition brought technology, market access, or manufacturing capabilities that enhanced Mahindra's global competitiveness.

The tractor business also demonstrates Mahindra's ability to create platforms, not just products. Their dealer network spans 1,200+ touchpoints in India alone. Service centers employ 25,000+ tractor experts. Financing arms provide credit to farmers who banks won't touch. This ecosystem—not just the metal machines—explains the market dominance.

What's remarkable is how tractors transformed from a side business to the crown jewel. Today, the Farm Equipment Sector contributes significantly to Mahindra's profitability with higher margins than automotive. It's recession-resistant (farmers need tractors regardless of economic cycles), enjoys pricing power (brand loyalty is fierce), and generates steady cash flows that fund other ventures. The tractor revolution didn't just build a business—it built the financial foundation for Mahindra's entire conglomerate ambitions.

V. The SUV Story: Scorpio, XUV500, and Thar

In 2002, Anand Mahindra stood before his board with a proposal that seemed insane. He wanted to invest ₹500 crores to develop India's first indigenously designed SUV. The automotive establishment scoffed. Indians bought Maruti 800s for efficiency or imported Toyotas for prestige. Who would buy a homegrown SUV? The board approved the project by a single vote. That one vote would reshape Indian automotive history.

The Scorpio project, codenamed internally as the "Car of the Century," was born from a simple insight: India's rising middle class wanted more than transportation—they wanted to project success. But they couldn't afford Land Cruisers or Pajeros. There was a gaping hole in the market between utilitarian Jeeps and luxury imports. Mahindra would fill it with something uniquely Indian.

The development was chaotic and exhilarating. Mahindra assembled a team of young engineers, many fresh from college, and gave them unprecedented freedom. They worked in a converted warehouse in Mumbai, using jugaad innovation when budgets ran thin. When they couldn't afford expensive crash test facilities abroad, they built their own. When Italian designers quoted astronomical fees, they partnered with lesser-known but talented Korean studios. Ramkripa Ananthan and her team designed the most popular Mahindra cars like the Bolero, Xylo, and Scorpio. She joined Mahindra & Mahindra as an interior designer in 1997, working on the interiors of the Bolero, Scorpio and the Xylo cars, bringing a fresh perspective to automotive design in a male-dominated industry.

The Scorpio launched in October 2002 at ₹5.4 lakhs—half the price of competing imports but with 80% of the features. The gamble paid off spectacularly. Within months, Mahindra had 15,000 bookings. The Scorpio wasn't just a product success; it was a cultural phenomenon. It appeared in Bollywood films, became the vehicle of choice for politicians and businessmen, and established Mahindra as a serious player in passenger vehicles, not just utility workhorses. The XUV500 (2011): Breaking into premium territory. First launched in 2011, the Mahindra XUV500 played a significant role in shaping the brand's presence in the Indian market. Priced starting at ₹10.80 lakhs (ex-showroom Delhi), it offered features previously seen only in vehicles twice its price: touchscreen infotainment, GPS navigation, six airbags, and electronic stability control. The development team had surveyed 1,500 people across different countries about their SUV expectations, then delivered beyond them.

The XUV500 wasn't just a product—it was a statement that Mahindra could compete in premium segments. By 2014, Mahindra had already sold more than 1.5 lakh units of the XUV500, a record accomplishment for any Indian premium SUV. It proved that customers would pay premium prices for Indian-designed vehicles if they delivered on quality and features. But the real cultural phenomenon came with the Thar. The launch of the new Mahindra Thar in 2020—known for its off-road capabilities, received a modern makeover while retaining its iconic design, became an instant hit with overwhelming demand. Within just five days of its launch on October 2, 2020, Mahindra received over 9,000 bookings. By 18 days, that number exceeded 15,000, with 57% of buyers being first-time car buyers—an unprecedented statistic for a 4x4 vehicle.

The Thar story reveals something profound about product-market fit. Mahindra didn't try to make the Thar more civilized or urban-friendly. They celebrated its ruggedness while adding just enough modern features—touchscreen infotainment, automatic transmission options—to make it livable. The result? By October 2021, bookings had hit 75,000 units in a year. The Thar became more than a vehicle—it became a lifestyle statement, spawning Instagram communities, off-road clubs, and a subculture of weekend adventurers.

Recent launches continue this momentum. The Scorpio N (2022) and XUV700 (2021) have reinforced Mahindra's position as India's SUV specialist. Each model demonstrates the company's evolved capability: sophisticated design, advanced features like ADAS (Advanced Driver Assistance Systems), and pricing that undercuts international competitors while matching their quality.

What's remarkable about Mahindra's SUV journey is how they've created distinct sub-brands within SUVs. The Thar owns adventure. The Scorpio owns authority. The XUV series owns urban aspiration. This segmentation allows Mahindra to compete across price points without cannibalizing their own products—a feat few automakers achieve.

VI. The Electric Vehicle Journey & Formula E

In 1999, while the world was worried about Y2K, Mahindra was quietly building India's first electric vehicle. Called "Bijlee" (Hindi for electricity), this experimental three-wheeler was ahead of its time—so far ahead that the market wasn't ready. India's electric vehicles journey had an early start with the aptly named Bijlee, made by Mahindra & Mahindra way back in 1999 - this first leap of faith didn't take M&M too far on the EV journey. The vehicle was shelved, but the learning wasn't forgotten.A decade later, Mahindra took a different approach. Rather than building from scratch, they looked globally for existing technology. After a global search for EV technology, M&M acquired a 55 per cent stake in Reva Electric Vehicle Company in 2010. Mahindra & Mahindra Ltd. strengthened its position in the electric vehicles domain with the acquisition of a majority stake in REVA Electric Car Co Ltd. Bangalore, with M&M owning 55.2% equity in Mahindra REVA by a combination of equity purchase from the promoters and a fresh equity infusion of over Rs 45 crores (approx US $10 million) into the company.

Reva wasn't just any EV company. Founded by Chetan Maini, a Stanford-educated engineer, it had sold 3,500+ vehicles across 24 countries—arguably the largest EV fleet globally at the time. But Reva had hit a ceiling. It lacked capital for expansion and the manufacturing expertise to scale. Mahindra provided both, while gaining crucial EV technology and talent.

After the acquisition, the company launched the electric hatchback e2o in 2013. The market launch was delayed while awaiting a decision from the Indian government on whether it would provide consumer tax benefits for electric car buyers. Although the incentives were not included in the 2013-14 Indian government budget, the company decided to proceed with the market launch. The e2o was innovative—app-controlled features, battery-as-a-service models—but commercially disappointing. The market wasn't ready, charging infrastructure didn't exist, and consumers remained skeptical.

In 2014, M&M became part of Formula E as one of the ten founding teams. This investment underlined M&M's 'race to road' strategy to be at the cutting edge of technology and applying the knowledge for mobility solutions across the board. Mahindra Racing was the 1st Formula E team to receive highest level (3 Star) sustainability accreditation.

Formula E seems like an odd choice for a company known for tractors and SUVs. Why race electric cars in Monaco when your core customers are in Mumbai? The answer reveals Mahindra's strategic thinking. Formula E provided three things money couldn't buy: technological learning at racing speeds, global brand credibility, and recruitment of world-class engineering talent. Every race pushed battery management, motor efficiency, and thermal dynamics to extremes—lessons directly applicable to road cars.

The Formula E investment also signaled intent. While competitors dismissed EVs as a distant future, Mahindra was racing them at 280 km/h. This commitment attracted partnerships, government support, and most importantly, changed internal culture. Engineers who might have joined Maruti or Tata now saw Mahindra as the place for cutting-edge technology.

M&M today leads India's EV push with goal of putting half a million electric vehicles on Indian roads by 2025. Around INR 1,700 crore has already been invested in the business in India, and another INR 500 crore has been set aside for a new research and development (R&D) centre. The recent launch of the BE 6 and XEV 9e electric SUVs signals a new phase—not retrofitting ICE platforms for batteries, but purpose-built EVs designed from the ground up.

What's fascinating about Mahindra's EV journey is its patience. Twenty-five years elapsed between Bijlee and their current EV push. Most companies would have given up after the first failure. Mahindra kept learning, acquiring capabilities, waiting for the market to mature. This long-term thinking—rare in quarterly earnings-driven corporate India—defines their approach to strategic bets.

VII. Global Acquisitions & Expansion Strategy

In 2010, Mahindra executives sat in a Seoul boardroom, finalizing the acquisition of SsangYong Motor Company. The Korean automaker was in court receivership, bleeding cash, with a poisoned brand. Mahindra paid $463 million for a 70% stake. Investment bankers called it brave. Competitors called it foolish. The journey that followed would be both. In 2011 Mahindra acquired a majority stake of South Korea's SsangYong Motor. The acquisition was completed in February 2011 and cost Mahindra US$463.6 million. Initially, the acquisition showed promise. In 2015, SsangYong launched the Tivoli, its first car after Mahindra acquisition. Within a year of Tivoli's launch, the company reported its first net profit in 9 years.

The Tivoli success was real—in 2017, SsangYong sold 106,677 units in domestic sales and 37,008 units in exports, setting a record high in 14 years. More importantly, the Tivoli platform became the basis for Mahindra's XUV300, sharing many parts including several metal sheets. Technology transfer was happening both ways.

But underneath the surface, problems festered. SsangYong's dealer network resented Indian ownership. Korean unions remained hostile despite initial agreements. The company needed massive investment to develop new models, but Mahindra was stretched funding its Indian operations. By 2020, COVID-19 delivered the final blow. After Mahindra stopped funding it in December 2020, SsangYong entered receivership. By November 2022, when a KG Group-led consortium completed the acquisition procedures for a controlling stake, Mahindra's Korean dream officially ended.

The SsangYong story is a cautionary tale about cross-border M&A. Mahindra gained valuable technology—the XUV300 platform alone justified much of the investment. But they underestimated cultural barriers, union dynamics, and the capital intensity of keeping a troubled automaker competitive. The lesson wasn't to avoid international acquisitions but to be more selective.

This selectivity showed in subsequent deals. In October 2014, Mahindra acquired a 51% controlling stake in Peugeot Motocycles and a 100% controlling stake in October 2019. This wasn't about cars but two-wheelers—a logical adjacency to their existing businesses. The brand carried heritage value, the business was manageable in size, and European regulations provided a testing ground for electric two-wheelers. The crown jewel acquisition came in December 2015. Mahindra and its affiliate Tech Mahindra, through a special purpose vehicle (SPV), agreed to buy a 76.06% stake in Italian car designer Pininfarina, for €168 million. This wasn't just buying a company—it was acquiring 90 years of design heritage. Pininfarina had designed some of the most beautiful Ferraris, Alfa Romeos, and Peugeots ever made.

Since 2018, Mahindra owns legendary design firm Pininfarina, and under its ownership, the Italian firm has developed the Battista electric supercar. The Battista represents something profound: an Indian-owned company building a $2.2 million hypercar that accelerates from 0-100 km/h in less than 2 seconds. It's faster than a Formula 1 car, produces 1,400 kW (1,877 hp), and represents the pinnacle of electric vehicle technology.

The strategic logic of Pininfarina is subtle but powerful. It's not about selling Battistas—only 150 will ever be made. It's about capability acquisition, brand halo, and technology transfer. The battery management systems, motor controllers, and thermal solutions developed for a hypercar eventually cascade down to mass-market EVs. The design language influences everything from tractors to SUVs. The brand association elevates Mahindra from "Indian automaker" to "owner of Italian design royalty."

Agricultural technology acquisitions reveal another dimension of Mahindra's strategy. Stakes in MITRA Agro Equipments (26% in 2018, increased to 39% in 2020), Carnot Technologies (22.9% in 2018), Resson Aerospace (10% in 2018), and Switzerland's Gamaya (11.25% in 2019) weren't random. Each brought specific capabilities: precision spraying, IoT sensors, aerial imaging, and AI-powered crop analytics. Mahindra isn't just selling tractors anymore—they're building an agricultural technology ecosystem. Mahindra's most recent acquisition is SML Isuzu, acquired in April 2025 for ₹555Cr with 58.96% stake. The acquisition involves M&M purchasing shares from SML Isuzu's existing promoters—43.96% from Sumitomo Corporation for ₹413.55 crore and 15% from Isuzu Motors Ltd for approximately ₹141.10 crore. This wasn't about entering a new market but consolidating position in commercial vehicles where Mahindra held just 3% market share in the >3.5T segment despite dominating the <3.5T segment with 54.2% share.

The global footprint today is impressive: manufacturing in India, the US, Brazil, Mexico, Finland, Turkey, and Japan. Assembly operations span 100+ countries. But it's not about planting flags—it's about building capabilities where they matter. US operations focus on compact tractors for lifestyle farmers. European facilities develop emission-compliant vehicles. Asian partnerships bring technology transfer. Each location serves a strategic purpose beyond mere market access.

VIII. The Anand Mahindra Era & Modern Transformation

Anand Mahindra, the present Chairman of Mahindra Group, is the grandson of Jagdish Chandra Mahindra. When he took over executive responsibilities in 1991, Mahindra was a $500 million company known for Jeeps and tractors. Today, it's a $23 billion federation spanning 20+ industries. But the transformation isn't just about scale—it's about reimagining what an Indian conglomerate could be.

Anand brought something different: a Harvard MBA, yes, but more importantly, a global perspective married to deep Indian roots. He understood that Mahindra couldn't compete on cost alone—Chinese manufacturers would always be cheaper. It couldn't compete on technology alone—German and Japanese firms had decades of advantage. Mahindra needed a different playbook.

The "Rise" philosophy, launched in 2011, wasn't just a marketing campaign—it was organizational therapy. For decades, Mahindra had sold utility, function, value. "Rise" said something different: we enable human aspiration. A tractor isn't just farm equipment—it's a tool for prosperity. An SUV isn't just transport—it's a statement of arrival. This shift from product features to human outcomes transformed how Mahindra designed, marketed, and thought about its role.

Digital transformation under Anand has been remarkable, but not in the conventional sense. While competitors built apps and websites, Mahindra built ecosystems. DigiSense connects tractors to smartphones, providing real-time diagnostics. Mahindra Finance uses AI for rural credit scoring where traditional banks see only risk. The MyMahindra app doesn't just book services—it creates communities of owners who share routes, modifications, and stories.

Anand's social media mastery deserves study. With 11+ million Twitter followers, he doesn't just promote products—he shapes conversations. When he tweets about a customer's innovative use of a Mahindra vehicle, it gets more engagement than million-dollar ad campaigns. When he responds personally to complaints, it builds more trust than customer service protocols. This isn't corporate communication—it's relationship building at scale.

The federation model—Present in over 20+ industries across Auto, Farm and Services including SUVs, LCVs, electric 3-wheelers, trucks & buses, motorcycles, Mahindra Finance, Tech Mahindra, hospitality, real estate, renewables, logistics, steel manufacturing, auto recycling, defence and aerospace—seems sprawling but follows logic. Each business either supports the core (Mahindra Finance enables vehicle sales), extends capabilities (Tech Mahindra brings IT expertise), or explores adjacencies (renewable energy aligns with sustainability goals).

Capital allocation under Anand reveals strategic discipline beneath apparent diversification. Core businesses (automotive, farm equipment) get steady investment. Growth businesses (EVs, aerospace) get patient capital with long-term horizons. Experimental ventures get limited resources with clear milestones. Failing businesses get fixed or exited—the SsangYong withdrawal, painful as it was, showed willingness to cut losses.

The ESG focus isn't greenwashing. Mahindra became carbon neutral in 2016—not through offsets but actual reduction. Water positive since 2013. 100% renewable energy at major facilities. These aren't CSR initiatives—they're business strategy. Rural customers facing climate change appreciate water conservation. Urban millennials choosing SUVs value sustainability credentials. Investors pricing climate risk reward genuine action.

What's most impressive about Anand's era is the cultural transformation. From a hierarchical, family-controlled firm to a professional, performance-driven organization. From domestic focus to global ambition. From manufacturing mindset to innovation culture. This isn't easy in a 75-year-old company with deep traditions. It requires balancing respect for heritage with hunger for change—a balance Anand has largely achieved.

IX. Playbook: Business & Investing Lessons

The Power of Frugal Innovation Mahindra's success challenges Silicon Valley's "move fast and break things" philosophy. Instead, they perfect slowly and build for decades. The Bolero, launched in 2000, still sells 10,000+ units monthly with minimal changes. Why? Because Mahindra understood that rural customers value reliability over novelty, repairability over features. Frugal innovation isn't about being cheap—it's about maximizing value within constraints. Every Mahindra product embodies this: good enough performance, exceptional durability, accessible maintenance.

Balancing Conglomerate Complexity with Focus Conventional wisdom says conglomerates destroy value through complexity. Mahindra proves otherwise by maintaining clear boundaries. Each business must either strengthen the core, share customers, or bring unique capabilities. Real estate seems random until you realize it helps attract talent to Mumbai headquarters. Hospitality seems odd until you understand it showcases Mahindra vehicles at resorts. The federation structure allows entrepreneurship within disciplines—business heads run their units like CEOs but within group-wide capital allocation frameworks.

Strategic Patience: The Long Game Mahindra waited 17 years between launching the Scorpio (2002) and Thar (2020)—their two biggest SUV successes. They spent 25 years in electric vehicles before launching competitive products. This isn't slowness—it's strategic patience. Each major move comes after capabilities are built, markets mature, and timing aligns. In businesses with 10-year product cycles and 20-year investment horizons, rushing destroys more value than waiting.

The Acquisition Playbook Mahindra's M&A track record teaches clear lessons. Successful acquisitions (Swaraj, Pininfarina) bring specific capabilities to strengthen existing businesses. Failed ones (SsangYong) attempt to enter new markets through distressed assets. The pattern is consistent: buy technology and talent, not market share. Integrate carefully—Swaraj kept its brand and dealer network. Exit decisively—when SsangYong failed, Mahindra didn't throw good money after bad.

Building Brands with National Identity Mahindra vehicles aren't just products—they're symbols of Indian aspiration. The Scorpio projected new Indian confidence. The Thar represents adventure-seeking youth. This isn't jingoism but authentic connection to customer identity. In markets where foreign brands carry prestige, Mahindra makes Indian-ness itself prestigious. This works because it's genuine—Mahindra vehicles are designed for Indian conditions, built by Indian engineers, solving Indian problems.

Capital Allocation in Capital-Scarce Markets Operating in India means capital is expensive and scarce. Mahindra's response: generate cash from mature businesses (tractors), reinvest in growth areas (EVs), and use debt sparingly. Return on capital employed (ROCE) drives decisions more than growth rates. This discipline means missing some opportunities but avoiding existential risks. In volatile emerging markets, survival precedes success.

The Tractor-to-Tech Diversification Model Mahindra's evolution from tractors to technology seems random but follows logic. Tractors taught manufacturing excellence. Jeeps brought automotive capability. IT services (through Tech Mahindra) added software skills. EVs combine all three. Each phase built on previous capabilities while adding new ones. This isn't diversification—it's capability accumulation. Today's electric SUVs exist because of competencies built over 75 years.

X. Analysis & Bear vs. Bull Case

Bull Case: The Structural Advantages

Mahindra isn't just the world's largest tractor company by volume—it owns a market structure that's nearly impossible to attack. With 42.9% market share maintained for 35 consecutive years, the company has built moats that deepen with time. The 1,200+ dealer network in India can't be replicated without decades and billions in investment. The financing arm knows rural credit patterns that no algorithm can match. Brand loyalty spans generations—farmers buy Mahindra because their fathers did.

The SUV position is equally formidable but different. While not market leader by volume, Mahindra owns the most profitable segments: lifestyle SUVs (Thar), aspirational SUVs (XUV700), and workhorse SUVs (Bolero). These aren't commodity products competing on price but differentiated offerings with pricing power. The Thar commands waiting periods despite premium pricing. The Scorpio N saw 100,000 bookings within 30 minutes of opening. This is brand power, not market share.

Early mover advantage in Indian EVs matters more than it appears. While Tesla and Chinese brands dominate global EV headlines, India's market will develop differently. Local manufacturing requirements, price sensitivity, and infrastructure challenges favor domestic players. Mahindra's BE 6 and XEV 9e aren't just EVs—they're EVs designed for Indian conditions, priced for Indian wallets, serviceable by Indian mechanics. The Formula E experience and Pininfarina ownership provide technology credibility that pure-play EV startups lack.

Diversified revenue streams provide resilience that focused players lack. When COVID-19 crushed automotive sales, tractors boomed as agriculture continued. When chip shortages constrained production, Mahindra Finance kept generating returns. When commodity prices spike, the steel business benefits. This isn't the random diversification that destroys value—it's strategic hedging that ensures survival through cycles.

Bear Case: The Structural Challenges

The SsangYong failure wasn't an aberration—it reveals structural weaknesses in Mahindra's global ambitions. Despite spending $1+ billion over a decade, Mahindra couldn't make a Korean acquisition work. The cultural challenges, union dynamics, and capital requirements overwhelmed potential synergies. If Mahindra can't succeed in Korea, how can it compete globally against Toyota, Volkswagen, or emerging Chinese giants?

Competition from global players entering India intensifies yearly. Kia and MG have grabbed significant SUV share within years of entry. Chinese brands are preparing India entries. Tesla will eventually arrive. These aren't capital-constrained local competitors but global giants with deep pockets and proven products. Mahindra's domestic moats matter less when competitors can spend billions to build networks and brands.

The EV transition poses existential questions. Mahindra must invest billions in EV development while maintaining ICE businesses that generate current cash flows. But EVs have fundamentally different economics: lower margins, higher capital intensity, faster obsolescence. The capabilities that made Mahindra successful in mechanical vehicles—frugal engineering, local manufacturing, distributed service—matter less in software-defined vehicles where batteries and chips determine competitiveness.

Conglomerate discount concerns are real and persistent. Tech Mahindra trades separately but at lower multiples than pure-play IT services firms. The automotive business gets valued like a cyclical manufacturer despite SUV premiumization. The sum of parts exceeds market capitalization by most estimates. This isn't just market inefficiency—it reflects genuine complexity in understanding and valuing such diverse businesses.

Dependence on rural and agricultural economy creates vulnerability. Climate change makes monsoons more variable. Farm income volatility affects tractor demand. Rural consumption patterns are shifting as youth migrate to cities. The core customer base that drove Mahindra's growth for 75 years is changing in fundamental ways. Urbanization helps SUV sales but hurts tractor volumes. This transition requires different capabilities, channels, and capital allocation.

The Net Assessment

The bull and bear cases aren't mutually exclusive—they're simultaneously true. Mahindra dominates profitable niches but faces structural challenges. It has unassailable positions in some markets but failed global ambitions in others. The company generates enormous cash from mature businesses but needs enormous investment for future ones.

The key question isn't whether Mahindra will survive—the balance sheet strength and market positions ensure that. It's whether Mahindra can transition from an Indian champion to a global player, from a mechanical manufacturer to a technology company, from a conglomerate to a focused corporation. The answer determines whether Mahindra trades at 15x earnings (respectable industrial) or 25x earnings (growth platform).

XI. Epilogue & "If We Were CEOs"

The recent BE 6 and XEV 9e electric SUV launches in November 2024 represent more than new products—they signal Mahindra's vision for the next 75 years. These aren't converted ICE platforms with batteries stuffed underneath but ground-up EVs with radical designs, sophisticated software, and genuine innovation. The BE 6 starts at ₹18.90 lakhs—aggressive pricing that could catalyze mass EV adoption. The XEV 9e's coupe-SUV design language wouldn't look out of place in Munich or California. This is Mahindra saying: we're not just participating in the EV transition, we're leading it.

The future of mobility in India won't mirror the West or China—it will be uniquely Indian. Personal vehicles for aspirational urban families. Shared mobility for cost-conscious commuters. Electric three-wheelers for last-mile delivery. Autonomous tractors for precision farming. Mahindra is positioned across all these segments, but position doesn't guarantee success. Execution, capital allocation, and timing will determine outcomes.

Balancing heritage with innovation is Mahindra's perpetual challenge. The Thar succeeded by modernizing an icon without losing its soul. The XUV700 succeeded by being genuinely innovative while remaining accessible. But for every success, there's a KUV100 (trying too hard to be different) or Marazzo (solid product, confused positioning). The lesson: innovation must solve real problems, not just showcase capability.

If We Were CEOs, here's what we'd do differently:

First, we'd dramatically simplify the portfolio. The commercial vehicle business needs either full commitment or exit—the current middle ground destroys value. Pick five core automotive platforms and build everything else from them. Kill sub-scale ventures that distract management and confuse investors.

Second, we'd separate and potentially IPO Mahindra Finance and Tech Mahindra at maximum valuations. Use proceeds to fund the EV transition without diluting automotive ownership. These businesses have proven they can thrive independently—let them.

Third, we'd be more aggressive on the EV timeline. The current approach is prudent but risks missing the inflection point. Take bigger bets on battery technology, charging infrastructure, and software capabilities. Partner with global technology leaders rather than trying to build everything internally.

Fourth, we'd clarify the global strategy. Either commit to becoming a global player with the requisite investment, or focus on dominating South Asia and Africa where Mahindra's value proposition resonates. The current approach of opportunistic international expansion wastes resources without building scale.

Fifth, we'd invest heavily in software and services. The future automotive profit pool shifts from manufacturing to software, services, and data. Mahindra's engineering heritage is necessary but not sufficient. Acquire or build genuine software capabilities before tech companies make hardware commodities.

Final Reflections

Mahindra's story is ultimately about transformation—from trading to manufacturing, from utility to aspiration, from local to global, from mechanical to digital. Each transformation required abandoning comfortable competencies for uncertain capabilities. The next transformation—to sustainable, intelligent mobility—will be the most challenging yet.

What makes Mahindra fascinating isn't its size or scope but its contradictions. A company that builds $6,000 tractors and $3 million hypercars. That dominates in India but struggles globally. That spans 20 industries yet maintains focus. That honors 75 years of heritage while embracing radical change. These contradictions aren't weaknesses—they're the source of resilience and optionality.

Building an enduring Indian multinational requires different strategies than building an American or European one. Capital is scarcer, so frugality matters more. Markets are volatile, so diversification helps. Customers are diverse, so portfolio breadth makes sense. Infrastructure is developing, so self-reliance becomes necessary. Mahindra embodies these adaptations—not always successfully, but always authentically.

The ultimate test comes in the next decade. Can Mahindra navigate the EV transition while maintaining ICE profitability? Can it compete with Chinese scale and Silicon Valley software? Can it remain Indian while becoming global? Can it honor heritage while embracing transformation? The answers will determine whether Mahindra's next 75 years match the first 75.

For investors, Mahindra represents a complex but compelling opportunity. It trades at reasonable valuations with hidden assets (brand value, real estate, subsidiary stakes) providing downside protection. The core businesses generate cash to fund transformation. The EV initiatives provide optionality for massive value creation. But this isn't a simple growth story or value play—it requires understanding India, believing in management, and patience for transformation.

The Mahindra story continues to be written. From partition-era entrepreneurship to potential EV leadership, from Ludhiana steel trading to global manufacturing, from family firm to professional corporation—each chapter brought challenges that seemed insurmountable until they were surmounted. That history suggests betting against Mahindra is unwise. But betting on Mahindra requires understanding that the journey will be neither straight nor simple—much like India itself.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube