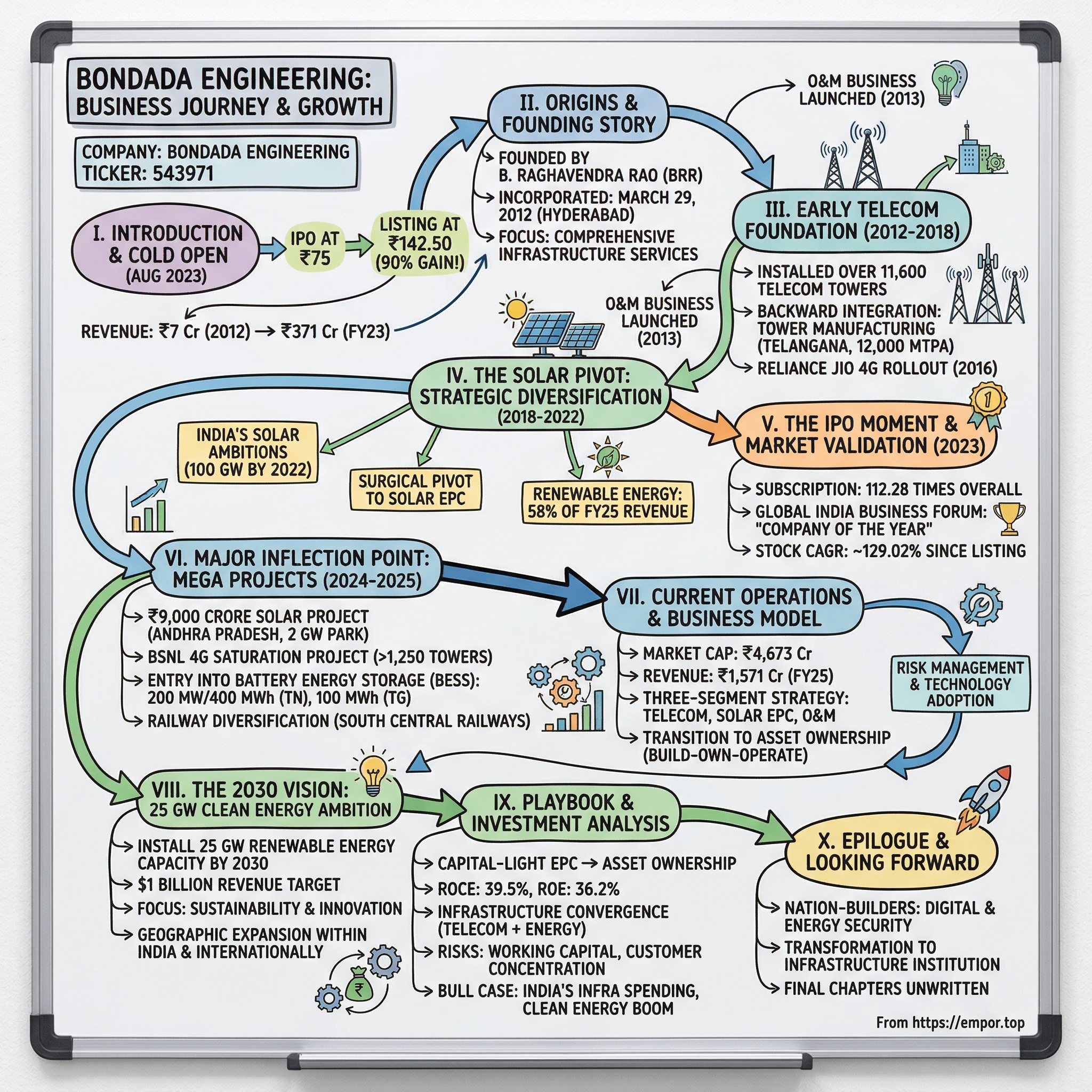

Bondada Engineering: From Telecom Towers to Solar Powerhouse

I. Introduction & Cold Open

Picture this: August 2023, the BSE SME platform. A relatively unknown engineering company from Hyderabad launches its IPO at ₹75 per share. What happens next defies all market logic—the IPO gets subscribed 112.28 times, with non-institutional investors fighting for every available share. The stock lists at ₹142.50, delivering a stunning 90% listing gain and returning ₹108,000 per lot to investors who managed to get an allocation.

But here's what makes this story even more remarkable: This company had started with just ₹7 crore in revenue in 2012 and reached ₹371 crore by FY22-23—a classic David-versus-Goliath tale in India's infrastructure sector. Today, Bondada Engineering commands a market capitalization of ₹4,673 crore with revenues of ₹1,571 crore, having transformed from a modest telecom infrastructure player into one of India's most promising renewable energy EPC contractors.

How does a company founded in the aftermath of India's telecom boom navigate the treacherous waters of infrastructure development, pivot into solar energy at precisely the right moment, and emerge as a key player in the nation's clean energy transition? This is the story of Bondada Engineering—a company that built its foundation installing cell towers during India's 4G revolution and is now positioning itself to install 25 gigawatts of renewable energy capacity by 2030.

The numbers tell only part of the story. Behind this meteoric rise lies a fascinating narrative of strategic pivots, government tailwinds, and the vision of a founder who spent nearly three decades understanding the pulse of India's infrastructure needs before striking out on his own. From erecting telecom towers in remote villages to securing ₹9,000 crore solar projects from state governments, Bondada's journey mirrors India's own infrastructure evolution—messy, ambitious, and ultimately transformative.

II. Origins & Founding Story (2012)

The monsoons had just retreated from Hyderabad in late 2012 when Bondada Raghavendra Rao—known as BRR in industry circles—walked away from his corner office as COO and Executive Director at Aster Private Limited. After 28 years of experience in the telecom and power industries, he wasn't leaving to retire. He was leaving to build something of his own.

At Aster, BRR had handled massive operations—peak revenue volumes of ₹690 crore in telecom projects, ₹580 crore in transmission and distribution, ₹120 crore in pre-engineered buildings, and ₹180 crore in international operations. But scale alone wasn't enough. He'd seen firsthand how India's infrastructure companies were struggling to adapt to the post-License Raj reality—bureaucratic, slow-moving behemoths trying to serve a nation desperate for connectivity and power.

On March 29, 2012, Bondada Engineering Private Limited was incorporated by the Assistant Registrar of Companies, Andhra Pradesh. The timing was deliberate. India's telecom sector was on the cusp of a massive transformation. The 3G auctions had concluded, 4G was on the horizon, and telecom operators needed thousands of towers erected across the country—fast.

BRR's approach was radically different from the established players. While large infrastructure companies moved with the speed of government tenders, he built Bondada to be nimble, execution-focused, and obsessively customer-centric. The company would provide what he called "comprehensive services to the infrastructure industry"—not just building towers but handling everything from site surveys to long-term maintenance.

The founding team wasn't just BRR alone. His wife Neelima Bondada and colleague Satyanarayana Baratam joined as co-promoters. Satyanarayana, a chartered accountant with two decades of experience, would prove instrumental in creating the financial architecture that would later enable the company's rapid scaling. The trio understood something fundamental: India's infrastructure boom wouldn't wait for perfect conditions or pristine business plans. It needed companies that could execute in chaos.

BRR's management philosophy, forged over nearly three decades, was simple but effective. He became renowned for his perseverance, target achievement, and ability to get the best from his team. In an industry notorious for project delays and cost overruns, he insisted on what would become Bondada's calling card: on-time delivery with quality standards.

The initial months were spent building relationships rather than towers. BRR leveraged his decades of connections, but more importantly, he offered something different—a partnership approach. While competitors treated telecom operators as clients, Bondada positioned itself as an extension of their teams. This wasn't just marketing speak. When a tower needed to be erected in a remote village in Telangana, it was often BRR himself who would drive out to inspect the site.

The company's first office in Hyderabad's Kapra area was modest—a far cry from the glass towers housing their competitors. But what it lacked in glamour, it made up for in intensity. Engineers worked around the clock, project managers slept at construction sites, and BRR's phone was never switched off. This wasn't sustainable, but it didn't need to be. It just needed to work long enough to establish credibility.

By late 2012, as India's telecom operators began their aggressive infrastructure rollout, Bondada had positioned itself perfectly. The company wasn't the biggest, didn't have the most capital, and certainly didn't have government connections. What it had was something more valuable in India's emerging economy: the ability to execute when everyone else was still planning.

The foundation was set, but the real test was about to begin. India's telecom sector was entering what would be remembered as one of the most aggressive infrastructure buildouts in global history. And a small company from Hyderabad was about to play a much bigger role than anyone could have imagined.

III. Early Telecom Foundation (2012-2018)

The call came at 2 AM on a humid October night in 2013. A telecom operator needed emergency repairs on a tower in rural Andhra Pradesh—monsoon damage had left an entire district without mobile coverage. While larger contractors would have cited force majeure and waited for daylight, BRR's team was already loading equipment into trucks. By dawn, the tower was operational. Word spread quickly through the tight-knit community of telecom infrastructure managers: Bondada delivered when others made excuses.

The company's telecom infrastructure services expanded rapidly to include turnkey services for cell site construction, erection, operation and maintenance of telecom towers with civil, electrical, and mechanical works, eventually installing over 11,600 telecom towers. But these weren't just metal structures erected in fields. Each tower represented a complex engineering challenge—land acquisition disputes, power availability issues, and the eternal Indian problem of last-mile connectivity.

The real breakthrough came with the decision to backward integrate. Rather than depending on third-party suppliers with unpredictable delivery schedules, Bondada established its own tower manufacturing facility in Telangana with an installed capacity of 12,000 MTPA for tower fabrication. This wasn't just about controlling costs—it was about controlling destiny. When Reliance Jio began its historic 4G rollout in 2016, demanding thousands of towers in impossibly short timeframes, Bondada's manufacturing facility ran three shifts continuously for months.

By fiscal 2023, the company had manufactured 34,945 telecom towers and offered EPC services for 4,400 towers at different locations across India. These numbers tell a story of scale, but they hide the granular complexity. Each tower required navigating local politics, managing armies of contract workers, and ensuring quality standards that would withstand everything from Kashmir's winters to Kerala's monsoons.

The 4G revolution transformed Bondada from a contractor into a critical infrastructure partner. The company delivered passive telecom infrastructure solutions encompassing comprehensive services including optical fiber cable laying and upkeep, power equipment provisioning, and other related services. When Airtel needed towers in Northeast India's challenging terrain, when BSNL required urgent capacity additions in underserved rural areas, Bondada's teams were there.

The operations and maintenance (O&M) business, launched in October 2013, became an unexpected profit center. While competitors saw O&M as a low-margin afterthought, BRR recognized it as a relationship builder. By maintaining thousands of towers across multiple states, Bondada gained invaluable data on equipment performance, site conditions, and operator needs—intelligence that would inform every future business decision.

The company's customer concentration was both a strength and a vulnerability. By March 31, 2023, 54.09% of outstanding book value came from their largest customer and 92.49% from their top five customers. This wasn't unusual in Indian infrastructure, but it meant that Bondada's fortunes were tied to a handful of relationships. BRR managed these relationships personally, understanding that in India's relationship-driven business environment, trust was currency.

The numbers validated the strategy. From starting with just ₹7 crore in revenue in their first year, the company reported a topline of ₹335 crore for FY22 on a consolidation basis. But growth came with growing pains. The business was manpower intensive, and if the company couldn't pool contract laborers, projects faced delays. Managing thousands of workers across hundreds of sites required military-style logistics and constant firefighting.

Recognition followed results. In 2021, the Economic Times named Bondada "Telecom Infrastructure Services Provider" of the year—validation from an industry that had initially viewed the Hyderabad upstart with skepticism. But BRR wasn't celebrating. He could see the writing on the wall: telecom tower installation was becoming commoditized, margins were compressing, and the next wave of growth would come from elsewhere.

By 2018, as the telecom tower market began to consolidate and mature, Bondada had built something valuable: a reputation for execution, a manufacturing base, and most importantly, the financial strength to pivot. The question wasn't whether to diversify, but where. The answer would come from an unlikely source—India's ambitious renewable energy targets and a government desperate to show progress on climate commitments. The telecom foundation was solid, but Bondada's next chapter would be written under the sun.

IV. The Solar Pivot: Strategic Diversification (2018-2022)

The meeting that changed everything happened in a nondescript government office in Amaravati in early 2018. Andhra Pradesh's energy secretary was explaining the state's renewable energy targets to a room full of contractors when he mentioned something that made BRR sit up: "We need players who can execute at the speed of telecom but with the complexity of power infrastructure." It was as if the bureaucrat was speaking directly to him.

India's solar ambitions were staggering—100 GW by 2022—but ground reality was sobering. Traditional power infrastructure companies moved at geological pace, solar specialists lacked execution muscle, and international players didn't understand India's unique challenges. Bondada occupied a unique position: they had the execution DNA from telecom, manufacturing capabilities, and critically, the balance sheet strength to take on large projects.

The pivot wasn't sudden—it was surgical. Bondada began offering end-to-end solar EPC services covering site surveys, land preparation, system design, installation, and performance monitoring, including solar module mounting structures (MMS), battery energy storage systems (BESS), and large-scale solar power plants. The company didn't abandon telecom; instead, it ran a parallel track, using telecom's steady cash flows to fund solar's working capital requirements.

The first major solar project was a disaster—at least initially. A 50 MW installation in Rajasthan faced everything from land acquisition delays to module delivery issues. The project was three months behind schedule and bleeding money. Lesser companies might have retreated, but BRR saw it as tuition fees. The team worked eighteen-hour days, flew in experts from across the country, and delivered the project just two weeks late. More importantly, they documented every lesson learned.

By 2020, as COVID-19 brought most infrastructure projects to a standstill, Bondada's dual-track strategy proved prescient. While telecom work continued as an essential service, the company used the lockdown to retool its solar capabilities. Engineers underwent training on the latest inverter technologies, project managers studied global best practices, and the company quietly built one of India's most comprehensive solar execution playbooks.

Renewable energy now represents 58% of FY25 revenue—a remarkable transformation for a company that had zero solar revenue just seven years earlier. But this wasn't just portfolio diversification; it was strategic positioning for India's energy transition. Every state government was now mandating renewable purchase obligations, discoms needed to green their energy mix, and corporate India was making net-zero commitments.

The solar business brought unexpected synergies with telecom. The same project management systems that coordinated tower installations across hundreds of sites could manage solar farms. The vendor relationships built over years in telecom provided leverage in solar procurement. Most importantly, the reputation for on-time delivery in telecom opened doors with solar developers who were tired of EPC contractors who overpromised and underdelivered.

Government policy became a massive tailwind. Production-linked incentives, viability gap funding, and accelerated depreciation benefits made solar projects financially attractive. But Bondada's edge wasn't in financial engineering—it was in execution engineering. When a large IPP needed 200 MW commissioned in six months, Bondada was one of the few contractors who didn't blink.

The working capital challenge in solar was more severe than telecom. Solar projects required massive upfront investments in modules and equipment, with payments typically coming 60-90 days after commissioning. This is where Satyanarayana Baratam's financial acumen proved invaluable. The company structured its contracts to minimize working capital cycles, negotiated better payment terms with module suppliers, and critically, maintained the discipline to walk away from projects with unfavorable terms.

Competition in solar EPC was fierce—Sterling & Wilson, L&T, Tata Power Solar—these were formidable players with deeper pockets and longer track records. But Bondada competed on speed and flexibility. While larger players took months to mobilize, Bondada could have teams on-site within weeks. While others insisted on standard designs, Bondada customized solutions for each project's unique challenges.

The transformation wasn't without casualties. Several senior managers from the telecom days, uncomfortable with solar's complexity, left the company. The company's culture had to evolve from the "cowboy" mentality of telecom tower installation to the precision required for solar plants generating power for 25 years. BRR personally led this cultural transformation, spending weeks at solar sites, learning alongside his engineers.

By 2022, Bondada wasn't just another solar EPC contractor—it was becoming a renewable energy solutions provider. The company was now bidding for projects that combined solar with battery storage, exploring hybrid renewable projects, and even evaluating manufacturing opportunities in the solar value chain. The telecom business remained strong, but it was clear that solar would drive the next phase of growth.

The strategic diversification was complete, but the real validation would come from the public markets. As Bondada prepared for its IPO in 2023, it had a story that resonated with India's dual infrastructure needs—digital connectivity through telecom and energy security through renewables. The market's response would exceed even BRR's optimistic projections.

V. The IPO Moment & Market Validation (2023)

The red herring prospectus dropped on June 3, 2023, into a market that was decidedly skeptical of SME IPOs. Too many companies had listed with grand promises only to disappoint investors. But Bondada's DRHP told a different story—real revenues, actual profits, and a business model that aligned perfectly with India's infrastructure priorities. Still, nobody expected what happened next.

The IPO roadshow was unconventional. Instead of Mumbai's five-star hotels and Delhi's power corridors, BRR insisted on meeting investors at project sites. Fund managers found themselves wearing hard hats, walking through solar installations, climbing telecom towers, and most importantly, talking to customers who couldn't stop praising Bondada's execution capabilities. One mutual fund manager later remarked, "It was the first IPO roadshow where I saw the product being built in real-time."

The IPO was priced at ₹75 per share with a minimum investment of ₹120,000, scheduled to open on August 18-22, 2023, with allotment on August 25 and listing on August 30. The pricing was aggressive for an SME listing—at nearly 20 times earnings—but the investment bankers argued that the company's growth trajectory justified the premium. They had no idea how right they were.

When subscription opened on that Friday morning in August, the response was immediate and overwhelming. By day three, the IPO was subscribed 112.28 times overall, with NIIs subscribing 115.46 times and retail investors 100.05 times. The grey market premium shot up to ₹43, indicating a listing around ₹118—nearly 60% above the issue price. But even the grey market underestimated investor enthusiasm.

The oversubscription wasn't just about the numbers. It reflected a deeper recognition—India's infrastructure story was entering a new phase, and companies like Bondada were perfectly positioned to benefit. The retail investor in Chennai who applied for one lot saw the same opportunity as the HNI in Mumbai who put in ₹50 lakhs—a company that could execute India's twin infrastructure dreams of universal connectivity and clean energy.

August 30, 2023, listing day, began with unusual activity. The pre-open session saw orders at prices that seemed impossible. When trading began, the stock opened at ₹142.50—a 90% premium to the issue price. The first day saw 18.75 lakh shares traded in over 1,000 trades, with the stock hitting an intraday high of ₹149.62. Investors who had received allotment were sitting on returns that usually took years to achieve.

The validation extended beyond just financial markets. In 2023, the Global India Business Forum named Bondada "Company of the Year"—recognition that the company had graduated from promising upstart to established player. But what truly mattered was the signal it sent to customers: Bondada now had the credibility and capital to take on even larger projects.

The post-IPO performance was even more remarkable. From the listing price to current levels, the stock has delivered a CAGR of approximately 129.02%. The stock reached its all-time high of ₹754 on August 28, 2024, before settling into a trading range that still represented massive wealth creation for early investors.

What explained this extraordinary market reception? Part of it was timing—the IPO came just as India's renewable energy sector was hitting an inflection point. Part of it was execution—the company had demonstrated an ability to grow revenues at 50% annually while maintaining profitability. But mostly, it was the story—a company that had started with telecom towers and successfully pivoted to solar, proving it could adapt to India's changing infrastructure needs.

The IPO proceeds of ₹42.72 crore might seem modest by mainboard standards, but for Bondada, it was transformative. ₹35 crore was earmarked for long-term working capital requirements, with ₹5.41 crore for general corporate purposes. More than the money, the listing provided credibility with banks for larger credit lines, with customers for bigger projects, and with employees for talent retention.

The market's message was clear: Bondada wasn't just another infrastructure company. It represented a new breed of Indian enterprise—nimble enough to pivot, large enough to scale, and ambitious enough to dream big. The IPO had provided validation, but the real test was converting this momentum into sustainable growth. The opportunity would come sooner than expected, and it would be bigger than anyone imagined.

VI. Major Inflection Point: The 2 GW Solar Park & Mega Projects (2024-2025)

The call from the Andhra Pradesh Energy Department came on an ordinary Tuesday in May 2024. What followed was anything but ordinary. The state government was awarding Bondada a ₹9,000 crore solar power project through its wholly-owned subsidiary, Bondada Renewable Energy. In one stroke, the company's order book swelled to over ₹14,000 crore, transforming Bondada from a mid-sized EPC player to a renewable energy powerhouse.

But this wasn't just about one large order. FY 2024-25 would prove to be Bondada's annus mirabilis—a year when every strategic bet placed over the previous decade would pay off simultaneously. The company wasn't just growing; it was metamorphosing from a contractor into something far more ambitious: an integrated energy solutions provider.

The BSNL 4G Saturation Project saw Bondada executing more than 1,250 telecom towers, representing about 10% of the nationwide rollout that was dedicated to the nation by the Prime Minister on September 28, 2025. Each tower was a feat of logistics and engineering, often erected in locations where roads were suggestions and electricity was a luxury. The BSNL project alone, valued at over ₹1,156 crore, would have been a company-defining achievement in earlier years. Now it was just one of several mega-projects running simultaneously.

The transformation went deeper than just project size. Bondada evolved from a solar EPC contractor into a renewable energy developer, initiating a 2 GW solar park under its subsidiary GreenBond RE Park Pvt. Ltd. and making significant progress in battery energy storage with the execution of a 200 MW/400 MWh project in Tamil Nadu. This wasn't just service delivery—it was asset creation, a fundamental shift in business model that would provide annuity revenues for decades.

The TGGENCO battery storage project marked another milestone—Bondada's entry into the BESS segment with a 100 MWh (50 MW x 2 hours) system at Shankarpally, Telangana, near the 400/220 kV TGTRANSCO substation. Valued at ₹204.20 crore with an 18-month execution timeline, the project positioned Bondada at the forefront of India's energy storage revolution—a market expected to grow 50-fold by 2030.

The railway diversification added another dimension. Securing an order from South Central Railways covering 452 sites across 1,500 kilometers wasn't just geographical expansion—it was sectoral expansion into one of India's largest infrastructure spenders. Railways brought different challenges—stricter safety standards, complex signaling requirements, and the need to work without disrupting operations on one of the world's busiest rail networks.

Managing this explosive growth required a complete organizational transformation. The company's headcount grew from 1,050 to over 2,500 professionals, but hiring was just the beginning. Bondada had to build systems that could handle multiple mega-projects simultaneously—project management offices that tracked thousands of activities daily, supply chain systems that managed inventory worth hundreds of crores, and quality systems that ensured every installation met specifications that would be tested over 25-year asset lives.

The financial performance reflected this operational excellence. FY 2024-25 saw revenues of ₹1,571 crore (up 96% year-on-year) and net profit of ₹115 crore (up 149% year-on-year). The company's credit rating was upgraded to CRISIL A (Stable)—crucial for a business where bank guarantees and working capital lines determined project capability.

The Andhra Pradesh solar project deserved special attention. The phased implementation planned 250 MW for FY 2026, 750 MW in FY 2027 generating ₹145 crore revenue, and 1,000 MW in FY 2028 with projected revenue of ₹580 crore, eventually generating ₹1,160 crore annually from FY 2029 onwards. This wasn't just project execution—it was building a revenue stream that would flow for the next quarter-century.

The challenge of managing ₹14,000 crore of projects over three years would break most mid-sized companies. Module procurement alone required relationships with global suppliers, hedging strategies for currency and commodity risks, and working capital management that would make CFOs lose sleep. But Bondada had spent a decade preparing for exactly this moment—building the systems, relationships, and financial strength to handle complexity at scale.

What made FY 2024-25 truly transformative wasn't just the quantum of orders but their strategic significance. Each project—whether BSNL towers enabling digital India, solar parks powering energy transition, or battery storage enabling grid stability—positioned Bondada at the intersection of India's most critical infrastructure needs. The company wasn't just riding waves; it was creating them.

VII. Current Operations & Business Model

Inside Bondada's war room in Hyderabad, twenty screens display real-time data from project sites across India. A solar installation in Tamil Nadu is running two days ahead of schedule. A telecom tower cluster in Bihar needs additional generators due to extended power cuts. A battery storage system in Telangana is undergoing pre-commissioning tests. This is the nerve center of an operation that has grown far beyond what anyone imagined when BRR started with that modest office in Kapra.

The company now operates with a market capitalization of ₹4,673 crore, generating revenues of ₹1,571 crore with a profit of ₹115 crore. But these headline numbers obscure the complexity underneath. The three-segment strategy encompasses telecom infrastructure (still contributing steady cash flows), solar EPC (now 58% of FY25 revenue), and O&M services spanning the entire portfolio.

The telecom business, while no longer the growth driver, remains the ballast. With contracts from BSNL, Reliance Jio, Airtel, and other operators, it provides predictable revenues and relationships that often lead to solar opportunities. The manufacturing facility in Telangana continues to produce towers, but it's also been retooled to manufacture solar module mounting structures—a clever synergy that improves asset utilization.

The solar business operates on multiple models. Pure EPC contracts where Bondada builds and hands over. Build-Own-Operate projects where the company retains assets and sells power. Hybrid models involving battery storage, increasingly important as renewable energy penetration creates grid stability challenges. Each model requires different capabilities—EPC needs execution excellence, BOO needs asset management skills, and hybrid projects need technology integration expertise.

Operating revenue of ₹1,947.63 crore on a trailing twelve-month basis with 97% annual revenue growth suggests momentum, but also masks operational challenges. Solar projects have massive working capital requirements—modules must be procured months before revenue recognition, labor costs are front-loaded, and customer payments often lag by quarters. The company maintains credit lines exceeding ₹800 crore, but even this feels stretched during peak execution periods.

The employee base tells its own story of transformation. From engineers who cut their teeth on telecom towers to solar specialists recruited from leading renewable energy companies, from financial analysts managing complex project economics to sustainability experts ensuring ESG compliance—Bondada's workforce reflects India's infrastructure evolution. The company employs 2,500 professionals with an order book of ₹15,000 crore, implying ₹6 crore of order book per employee—exceptional productivity by industry standards.

Customer concentration remains a strategic vulnerability: 54.09% of revenue from the largest customer, 92.49% from the top five. In infrastructure contracting, this is both inevitable and dangerous. Large projects come from large customers, but dependency creates risks—payment delays can cripple cash flows, relationship deterioration can destroy order books. Bondada manages this through deep, multi-level customer relationships and by gradually diversifying its customer base.

The margin profile reveals the business model's evolution. Telecom EPC operates at 8-10% EBITDA margins—competitive but not spectacular. Solar EPC manages 10-12%, benefiting from Bondada's execution efficiency. But the real margin expansion comes from value-added services—design engineering, technology integration, and O&M contracts that can deliver 15-20% margins over multi-year periods. The strategic shift toward BOO projects in solar and battery storage promises even better returns, albeit with higher capital requirements.

Technology adoption has been selective but effective. Project management software tracks thousands of activities across hundreds of sites. Drone surveys reduce site assessment time from days to hours. Predictive maintenance algorithms minimize O&M costs. But Bondada hasn't fallen for technology theater—every digital initiative must demonstrate clear ROI within twelve months or it's terminated.

Risk management has evolved from informal to institutional. Currency hedging for imported solar modules. Performance guarantees backed by insurance. Contractual structures that share risks appropriately between Bondada and customers. The company learned expensive lessons from early projects where enthusiasm exceeded prudence. Today, a risk committee reviews every contract above ₹50 crore, sometimes killing deals that would have added to top line but destroyed bottom line.

Geographic expansion beyond India remains exploratory. While international revenues contributed significantly during the Aster days, Bondada has consciously focused on the domestic market where it understands the terrain—literally and figuratively. But with Indian EPC companies increasingly winning international contracts, particularly in Africa and Southeast Asia, international expansion might become inevitable rather than optional.

The business model is transitioning from pure services to a hybrid of services and assets. This requires different skills—asset management rather than just project management, power market understanding rather than just construction expertise, financial structuring capabilities rather than just execution excellence. It's a complex transition that many EPC companies attempt but few successfully navigate.

VIII. The 2030 Vision: 25 GW Clean Energy Ambition

The auditorium at Bondada's annual general meeting in October 2025 was packed beyond capacity. Shareholders who had seen their investments multiply were eager to hear what came next. When BRR took the stage, his opening statement sent ripples through the room: "By 2030, Bondada will install 25 gigawatts of renewable energy capacity". To put that in perspective, that's roughly equivalent to Gujarat's entire power generation capacity—from a company that didn't exist in the solar space seven years ago.

The roadmap was audacious but specific: double revenue by FY 2026, triple it by FY 2027, and achieve a seven-fold increase by FY 2030. These weren't random multipliers pulled from air—each target aligned with India's infrastructure spending trajectory, state renewable energy policies, and global climate commitments that would drive trillions in clean energy investment.

The 25 GW target breaks down into multiple vectors. Utility-scale solar parks leveraging relationships with state governments. Distributed solar for commercial and industrial customers facing net-zero pressure. Wind-solar hybrid projects maximizing land utilization. Battery storage systems essential for grid stability. Green hydrogen projects, still nascent but potentially transformative. Each vector requires different capabilities, but all build on Bondada's core strength—execution at scale.

The company aims to achieve $1 billion in revenue and 25 GW of renewable energy capacity by 2030, emphasizing sustainability and innovation. This isn't just about installing panels and turbines. It's about creating an ecosystem—manufacturing capabilities for critical components, technology partnerships for next-generation solutions, financial structures that make projects viable, and operational excellence that ensures 25-year asset performance.

Competition is intensifying from every direction. Global giants like Adani Green and ReNew Power have deeper pockets and larger project pipelines. Chinese EPC contractors offer lower prices backed by cheap equipment financing. Technology companies like Tata Power Solar bring innovation and brand strength. In this environment, Bondada's strategy is to be the fastest and most flexible—winning projects that need rapid execution, complex sites that deter larger players, and hybrid solutions that require technical creativity.

The battery storage opportunity alone could transform the company. India needs 200 GWh of storage by 2030 to manage renewable energy intermittency. Bondada's Tamil Nadu project—valued at ₹836 crore and executed under Build-Own-Operate model—provides a template for capturing this market. Unlike solar where competition is fierce, battery storage requires sophisticated understanding of grid dynamics, technology selection, and power market operations—capabilities Bondada is systematically building.

Geographic expansion within India is accelerating. The company recently signed an MoU with Assam for a 100 MW hybrid wind-solar plant, marking entry into the Northeast—a region with massive renewable potential but challenging execution conditions. Each new state brings different regulations, political dynamics, and environmental challenges, but also diversifies risk and creates new growth avenues.

The railway electrification opportunity represents another multi-year growth driver. Indian Railways plans to electrify 40,000 route kilometers by 2030, requiring thousands of substations, overhead equipment installations, and signaling upgrades. Bondada's South Central Railway project is essentially a qualification test—successful execution opens doors to contracts worth tens of thousands of crores.

As BRR stated at the AGM: "From telecom and renewable energy to railways and storage, we have proven our ability to deliver at scale while creating long-term value". But proving ability and sustaining it at 10x scale are different challenges. The company needs to institutionalize capabilities currently dependent on individual heroes, build systems that can handle complexity without compromising speed, and maintain culture while growing from 2,500 to potentially 25,000 employees.

The financial implications are staggering. Achieving 25 GW would require managing projects worth ₹100,000 crore over five years—more than most Indian infrastructure companies handle in a lifetime. This needs credit lines in thousands of crores, relationships with dozens of financial institutions, and working capital management that would challenge even established giants. The company's investment banker privately admits, "If they pull this off, it's a case study for business schools. If they don't, it's still a case study."

Technology will be critical but not sufficient. Digital project management, AI-powered predictive maintenance, blockchain-based supply chain tracking—all are being evaluated or implemented. But technology is an enabler, not a differentiator. The real edge comes from combining technology with execution excellence, financial innovation with engineering rigor, ambition with discipline.

The international expansion question looms large. While the company plans to expand its footprint to international markets in renewable energy, the timing and approach remain undefined. Africa's massive infrastructure deficit offers opportunities but also risks. Middle Eastern countries' renewable ambitions align with Bondada's capabilities but require navigating complex business environments. For now, the focus remains India—large enough to support ambitious growth, familiar enough to execute with confidence.

IX. Playbook & Investment Analysis

The spreadsheet on the analyst's screen tells a compelling story, but like all financial models, it captures only part of reality. With a market cap of ₹4,673 crore, P/E ratio of 42.4, ROCE of 39.5%, and ROE of 36.2%, Bondada trades at premium valuations that suggest the market believes the growth story. The question for investors isn't whether Bondada can grow—it's whether it can grow profitably while managing the inherent risks of infrastructure contracting.

The capital-light model that served Bondada well in telecom EPC is evolving toward asset ownership in solar and battery storage. This transition fundamentally changes the investment thesis. EPC businesses generate cash quickly but must constantly win new projects. Asset ownership provides predictable long-term cash flows but requires massive upfront capital. Bondada is attempting something rarely successful—maintaining EPC velocity while building an asset base.

The financial trajectory validates the strategy: profit after tax rising from ₹17.13 crore to ₹46.31 crore between FY23 and FY24. But profitability metrics only tell part of the story. Cash flow patterns reveal the real challenge—massive working capital requirements during project execution followed by lumpy collections that can make quarterly results volatile. Investors who focus on quarterly earnings will be perpetually disappointed or delighted, missing the longer-term value creation.

The infrastructure convergence thesis—telecom plus energy—is Bondada's unique selling proposition. While pure-play renewable companies struggle during sector downturns and telecom infrastructure players face market saturation, Bondada can dynamically allocate resources between sectors. When solar module prices spike, focus shifts to telecom. When telecom spending slows, solar projects fill the gap. This optionality has value that traditional valuation metrics struggle to capture.

The balance sheet reveals both strength and stress. Total assets grew to ₹504.53 crore from ₹250.72 crore between FY23 and FY24, but this expansion was funded by both equity and debt. The debt-to-equity ratio remains comfortable at under 0.5x, but executing the ₹15,000 crore order book will require significant leverage expansion. Management's ability to fund growth without diluting equity or overleveraging will determine long-term returns.

Working capital intensity remains the Achilles heel. Solar projects require purchasing modules worth crores months before revenue recognition. Customer payment cycles average 60-90 days after commissioning. Meanwhile, suppliers demand faster payments, and labor costs can't be deferred. The company generated positive operating cash flow of ₹54 crore in FY24 versus negative ₹32 crore in FY23, but this improvement might reverse as mega-projects enter execution phase.

Competitive advantages are real but replicable. Execution excellence can be copied by hiring Bondada's people. Manufacturing facilities can be built by anyone with capital. Government relationships can be cultivated by competitors with patience. The true moat lies in the combination—the ability to execute complex projects reliably, backed by manufacturing capabilities, supported by relationships, and funded by a balance sheet that can withstand project delays and payment uncertainties.

The customer concentration risk cuts both ways. With 54.09% of revenue from the largest customer and 92.49% from top five customers, a single relationship deterioration could devastate the business. But these aren't ordinary customers—they're government entities and large corporations with multi-decade infrastructure needs. The risk isn't customer bankruptcy but project delays, scope changes, and payment delays that strain working capital.

Valuation presents a paradox. At 42x P/E, the stock appears expensive versus traditional infrastructure companies trading at 15-20x. But compared to renewable energy pure-plays trading at 50-100x, Bondada seems reasonable. The right comparison might be neither—Bondada is creating a new category combining EPC execution with asset ownership, telecom infrastructure with renewable energy, Indian ambition with global opportunity.

The bear case writes itself: customer concentration creates vulnerability, working capital intensity limits growth, competition from larger players with deeper pockets, execution risks in managing multiple mega-projects simultaneously, technology disruption making current capabilities obsolete, and regulatory changes affecting project economics. Any of these could derail the growth story.

But the bull case is equally compelling: India's infrastructure spending approaching $2 trillion this decade, renewable energy investment accelerating globally, telecom 5G rollout requiring massive infrastructure upgrades, battery storage market exploding from nearly zero to hundreds of gigawatts, proven execution creating competitive advantages, and management with skin in the game and a track record of delivery. With promoters holding 62.4% equity, alignment with minority shareholders is clear.

X. Epilogue & Looking Forward

As the sun sets over Bondada's manufacturing facility in Telangana, workers are loading the last telecom tower of the day onto trucks bound for a BSNL site in Madhya Pradesh. In the adjacent facility, solar mounting structures are being packaged for shipment to Tamil Nadu. This daily rhythm—steel transformed into infrastructure, infrastructure enabling connectivity and clean energy—represents something larger than quarterly earnings or stock price movements.

Each megawatt commissioned, each tower erected contributes to powering Bharat's growth story. When a village in Bihar gets 4G connectivity through a Bondada tower, it's not just about data speeds—it's about a farmer accessing weather information, a student attending online classes, a woman entrepreneur reaching customers through e-commerce. When a solar park in Andhra Pradesh starts generating power, it's not just about renewable energy targets—it's about reducing carbon emissions, creating energy security, and building industrial competitiveness.

The next five years will test every assumption underlying Bondada's ambitions. Can a company that started with ₹7 crore in revenue really install 25 gigawatts of renewable energy? Can an organization built on entrepreneurial hustle transform into an institution capable of managing complexity at scale? Can the infrastructure convergence thesis survive technology disruption, regulatory changes, and competitive pressure?

Market signals suggest optimism but also embed skepticism. The stock's 129% CAGR since listing reflects belief in the growth story, but volatility reveals uncertainty about execution. Days when the stock rises 10% on order announcements are followed by drops on working capital concerns. This volatility isn't noise—it's the market's way of processing the fundamental uncertainty of Bondada's transformation.

Dr. Bondada Raghavendra Rao's vision is clear: "From telecom and renewable energy to railways and storage, we have proven our ability to deliver at scale... our 2030 vision of becoming a 25 GW clean energy powerhouse, reinforcing India's digital and energy security". But visions don't build infrastructure—execution does. And execution at this scale requires capabilities Bondada is still building.

The broader context matters enormously. India's infrastructure needs aren't optional—they're existential. Without reliable power, manufacturing can't compete globally. Without digital connectivity, services can't scale. Without sustainable infrastructure, climate commitments become empty promises. Companies like Bondada aren't just contractors; they're nation-builders, even if their day-to-day reality involves mundane struggles with equipment procurement and project delays.

Key metrics to watch going forward aren't just financial. Order book conversion rates will reveal execution capability. Employee attrition in critical roles will indicate organizational health. Working capital cycles will determine growth sustainability. Customer diversification progress will show risk management maturity. Technology adoption success will indicate future competitiveness. Each metric tells part of a story that's still being written.

The international opportunity remains tantalizing but undefined. Indian infrastructure companies have historically struggled globally, lacking the financial muscle of Chinese competitors and the technology edge of Western firms. But as India's domestic market creates scale and capability, companies like Bondada might emerge as credible global players—particularly in markets like Africa that need infrastructure but can't afford developed-world prices.

The risks are escalating with scale. A single project failure at current sizes could wipe out years of profit. A key customer relationship souring could crater the order book. A technology shift making current capabilities obsolete could strand investments. These aren't theoretical risks—they're real possibilities that keep management awake and should concern investors.

Yet the opportunity is equally unprecedented. Growing from a ₹4,700 crore enterprise to $1 billion revenue with 25 GW renewable capacity would create enormous value for all stakeholders. More importantly, it would contribute meaningfully to India's infrastructure transformation—enabling the digital economy through telecom infrastructure and powering sustainable growth through renewable energy.

The story of Bondada Engineering is still being written. Whether it becomes a case study in successful transformation or ambitious overreach won't be known for years. But what's already clear is that this company—started in 2012 with modest ambitions and telecom relationships—has positioned itself at the intersection of India's most critical infrastructure needs. The execution challenges are immense, the competition is fierce, and the risks are multiplying. But then again, building a nation's infrastructure was never meant to be easy.

As we look toward 2030, the question isn't whether India needs companies like Bondada—it clearly does. The question is whether Bondada can evolve from an impressive executor to an infrastructure institution, from a successful SME listing to a large-cap infrastructure major, from installing towers and panels to powering India's growth story. The early chapters suggest it's possible. The final chapters remain unwritten.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube