Kalpataru Limited: Building Mumbai's Skyline

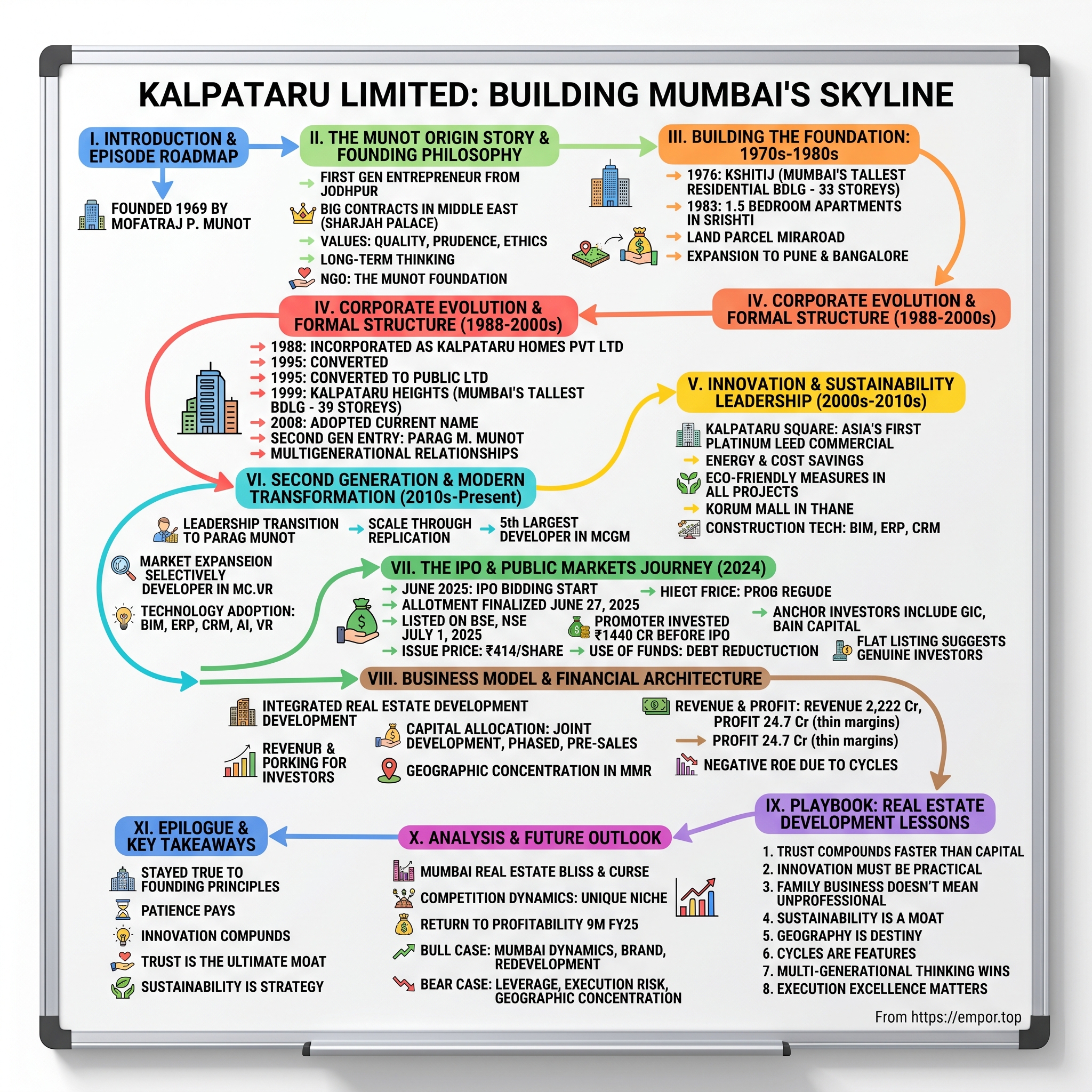

I. Introduction & Episode Roadmap

Picture this scene: It's 1976, and as Mumbai's skyline stretches toward the Arabian Sea, a 33-storey tower rises above everything else in the city. Kshitij became Mumbai's tallest building at 33 storeys, a record that would stand for the next quarter century. This wasn't just another building—it was a statement of ambition from a first-generation entrepreneur who had arrived in Mumbai just seven years earlier with dreams of transforming India's urban landscape.

That entrepreneur was Mofatraj P. Munot, and his company, Kalpataru, would go on to become one of Mumbai's most trusted real estate brands. Today, Kalpataru Limited is an integrated real estate development company with over 113 completed projects across Mumbai, Thane, Panvel, Pune, Hyderabad, Indore, Bengaluru, and Jodhpur. With a market capitalization of ₹8,524.07 Crore, the company stands as a testament to what five decades of patient building can achieve in one of the world's most complex real estate markets.

But here's the fascinating paradox: How did a company that built Mumbai's tallest building in the 1970s—a feat of engineering ambition—also become the developer that built Asia's first, and the world's sixth Platinum LEED certified commercial building? How does a family-run real estate developer maintain trust in an industry notorious for broken promises? And why did it take until 2024 for this 55-year-old institution to tap public markets?

This is the story of Kalpataru Limited—a tale of three generations, hundreds of towers, thousands of families, and one unwavering philosophy: that real estate isn't just about building structures, it's about creating meaningful livelihoods and lasting legacies. It's about understanding that in Mumbai, where every square foot is precious and every family's dream home represents a lifetime of savings, trust isn't just valuable—it's everything.

II. The Munot Origin Story & Founding Philosophy

The year was 1969. India was still finding its feet post-independence, the License Raj controlled every aspect of business, and Mumbai—then Bombay—was transforming from a colonial port city into India's commercial capital. Into this churning metropolis arrived a young man from Jodhpur with an unusual mission.

A first generation entrepreneur Mofatraj started his entrepreneurial foray in the late sixties, inspired by a single point agenda to create meaningful livelihoods for as many people as he could in the difficult economic situation prevalent then. This wasn't the typical motivation of a real estate developer. While others saw land and concrete, Munot saw opportunity to lift entire communities.

After gaining experience while working with his uncle, Mofatraj Munot started to develop real estate himself in 1969. But the timing seemed almost impossibly challenging. India's economy was struggling, capital was scarce, and the real estate industry was fragmented and largely unorganized. Yet Munot saw opportunity where others saw obstacles.

The breakthrough came from an unexpected direction. His Mumbai-based firm Kalpataru saw its first tryst with fortune when Munot bagged big contracts to construct properties in the Middle East during the oil boom of the 1970s. The Gulf states were swimming in petrodollars, ambitious construction projects were everywhere, and they needed reliable contractors who could deliver quality at scale.

But it was one particular project that would establish Munot's reputation forever. The crown jewel among these construction contracts was the palace of the ruler of Sharjah. This established Munot as a leading developer. Imagine the audacity—a first-generation entrepreneur from Jodhpur, barely a few years into his business, building a palace for Middle Eastern royalty. The successful completion of this project didn't just bring capital back to India; it brought something far more valuable: credibility.

The foundation of Kalpataru wasn't built on financial engineering or land banking—it was built on a philosophy that seemed almost quaint in the rough-and-tumble world of Indian real estate. It is this belief that also incorporates into Kalpataru's values along with quality, prudence and business ethics.

He has over 55 years of experience in the real estate business, property development, civil contracting and various other industries, but what set Munot apart wasn't just longevity—it was his approach to the business itself. While competitors focused on quick flips and maximum extraction, Munot was playing an entirely different game.

The philosophy was simple yet radical: Munot is a man who firmly believes in innovation and philanthropy. It is this belief that also incorporates into Kalpataru's values along with quality, prudence and business ethics. In an industry where cutting corners was often seen as smart business, Kalpataru was obsessing over details that wouldn't pay off for years, sometimes decades.

This long-term thinking manifested in unexpected ways. Munot is also a trustee of the NGO named, The Munot Foundation which organizes several initiatives across the country, in the areas of education and healthcare, reaching out to society's least privileged. He believes that good education and good health are the two pillars upon which the future of the country rests. A real estate developer focusing on education and healthcare for the underprivileged? It seemed counterintuitive, but Munot understood something fundamental: sustainable business requires a sustainable society.

By the mid-1970s, the company had accumulated enough capital, credibility, and expertise to attempt something audacious in Mumbai itself. The stage was set for Kalpataru to leave its first major mark on the city's skyline.

III. Building the Foundation: 1970s-1980s

Mumbai in the 1970s was a city bursting at its seams. The textile mills were still running, the stock exchange was finding its feet, and the city's population was exploding as migrants poured in from across India seeking opportunity. The skyline, however, remained largely horizontal—a sprawl of low-rise buildings and chawls stretching from Colaba to the nascent suburbs.

Then came 1976, and with it, a building that would change how Mumbai thought about vertical living. Munot's architectural feats reportedly include building Mumbai's tallest residential building in the 1970s. The building held the record for around 25 years. The 33-storey Kshitij wasn't just tall—it was a statement of possibility. In a city where six-storey buildings were considered high-rises, here was a structure that touched the sky.

But Kalpataru wasn't content with just building tall. The company was systematically reimagining what urban living could be. Swapnalok had unique stepped row houses with private terraces—bringing the concept of private outdoor space to dense urban development. This wasn't just architecture; it was lifestyle innovation.

The real genius, however, lay in understanding Mumbai's unique demographic puzzle. The city had wealthy industrialists who wanted luxury, a growing middle class that needed affordability, and young professionals who fell somewhere in between. In 1983, Kalpataru introduced something that seemed almost absurd: Introduced 1.5 bedroom apartments in Srishti.

Think about the brilliance of this innovation. A one-bedroom was too small for a young couple planning a family. A two-bedroom was often beyond their budget. The 1.5 bedroom—essentially a one-bedroom with a study or small additional room—hit the sweet spot. It was affordable enough for young professionals but spacious enough to grow into. This wasn't just product innovation; it was deep consumer insight translated into concrete and steel.

By 1982, the company was thinking even bigger, Acquired one third rights in a 200 acre land parcel in Mira Road. Mira Road in the early 1980s was considered the absolute periphery of Mumbai—barely connected, poorly developed, almost rural. But Munot saw what others couldn't: Mumbai's inevitable northward expansion. This wasn't speculation; it was patient, strategic positioning for growth that would take decades to fully materialize.

The company also began expanding beyond Mumbai. Kalpataru Apartments revolutionized luxury development Bangalore. Built NABARD staff quarters and Kalpataru Gardens in Pune. Each city taught Kalpataru something new. Bangalore showed them how IT professionals thought about housing. Pune revealed the preferences of manufacturing executives. These weren't just projects; they were market research laboratories.

Kalpataru has very often set new standards in real estate development. From building Mumbai's tallest residential tower in the 70's, a record that stood for the next quarter of a century, to introducing the concept of 1.5 bedroom homes. But setting standards wasn't about showing off—it was about pushing the entire industry forward.

The 1980s also saw Kalpataru developing a unique expertise: working within the constraints of the License Raj while still innovating. Getting approvals for a 33-storey building in the 1970s required navigating a byzantine system of permissions, NOCs, and regulatory requirements. Each project was a masterclass in stakeholder management—keeping regulators satisfied, neighbors appeased, customers happy, and workers motivated.

Kalpataru Limited, one of the largest real estate developers in MMR, was founded in 1969 by the chairman Mr. Mofatraj P. Munot. The company has developed and grown over the years, with an increasing portfolio of projects in numerous micro-markets of MMR. By the end of the 1980s, Kalpataru had built something more valuable than buildings—it had built a reputation.

The company's approach to construction quality was becoming legendary. In an era when buildings often developed cracks within years, started leaking in the first monsoon, or had electrical systems that constantly failed, Kalpataru buildings stood solid. Residents began noticing that Kalpataru buildings commanded premium resale values—not just because of the brand, but because the buildings actually lasted.

IV. Corporate Evolution & Formal Structure (1988-2000s)

The year 1988 marked a pivotal transformation. Kalpataru Limited was originally incorporated as Kalpataru Homes Private Limited on 22 December 1988 under the Companies Act, 1956. It was subsequently converted into a public limited company and renamed Kalpataru Homes Limited on 16 May 1995. The company adopted its current name, Kalpataru Limited, on 1 February 2008 to reflect its broader vision in real estate development.

This wasn't just paperwork—it was a fundamental shift in how the company would operate. The informal, relationship-based business model that had served well in the 1970s and 80s needed structure to scale. The incorporation brought formal governance, standardized processes, and most importantly, the ability to raise institutional capital.

The 1990s arrived with liberalization, and suddenly India was a different country. Foreign investment was flowing in, the middle class was expanding rapidly, and Mumbai was transforming from India's commercial capital to its financial nerve center. The old textile mills were closing, and on their land would rise the glass towers of new India.

1999 At 39-storeys, Kalpataru Heights became Mumbai's tallest building. Twenty-three years after Kshitij, Kalpataru had once again claimed the title. But this time, the context was entirely different. Mumbai now had multiple developers, international architects were working on Indian projects, and customers had become far more sophisticated.

The new millennium brought new challenges and opportunities. 2001 Built Asian Paint's head office, Asian Paints House, in Santacruz. This was significant—Kalpataru was now trusted by India's leading corporations to build their headquarters. Corporate clients brought different demands: stricter timelines, international quality standards, and complex technical requirements. Each corporate project enhanced Kalpataru's capabilities.

Led by Mr. Mofatraj P. Munot, with over five decades of experience, and Mr. Parag M. Munot, with three decades, Kalpataru is known for delivering high-quality projects. The entry of the second generation wasn't abrupt—it was carefully orchestrated. Parag M. Munot, armed with a master's degree in science (in the field of industrial administration) from Carnegie Mellon University, Pennsylvania, brought modern management thinking to a traditional business.

The father-son dynamic was complementary rather than conflicting. While Mofatraj continued to drive the vision and maintain relationships, Parag focused on operations, technology adoption, and systematic expansion. Under his leadership, Kalpataru Limited has emerged amongst the top five largest real estate developer in the Mumbai and Thane region. He has been at the forefront of scaling Kalpataru Limited's expansion in new markets like Hyderabad, Noida and Nagpur.

Kalpataru has been building fine homes and commercial complexes for five decades, partnering with generations of happy customers. This generational continuity of customers—grandparents who bought in the 1970s, parents in the 1990s, and children in the 2010s—created a unique dynamic. Kalpataru wasn't just selling apartments; it was maintaining multi-generational relationships.

The 2000s also saw Kalpataru beginning to think seriously about sustainability—not as a marketing gimmick, but as a fundamental responsibility. The company began experimenting with eco-friendly construction methods that many considered unnecessary expenses at the time. Unlike his counterparts, the builder focuses on incorporating measures like using efficient lighting solutions such as LEDs and CFLs, applying low VOC paints, dual flush toilets, waste water treatment, using solar reflective index material for roofing on top floors to avoid high indoor temperatures and diligent use of construction and demolition waste.

By 2003, these experiments were becoming more ambitious. Kalpataru Habitat introduced a rooftop golf putting green and tennis court. This wasn't just about amenities—it was about reimagining how urban spaces could provide recreational opportunities typically associated with suburban sprawl.

The formal corporate structure also enabled Kalpataru to build institutional capabilities that individual-driven firms struggled with. Systems for project management, quality control, customer service, and financial management were established. The company began hiring professionals from diverse backgrounds—engineers from IITs, MBAs from IIMs, architects from international schools.

V. Innovation & Sustainability Leadership (2000s-2010s)

The year 2008 should have been a disaster. The global financial crisis was decimating real estate markets worldwide. In India, several developers went bankrupt, projects stalled, and customer confidence evaporated. Yet in this chaos, Kalpataru achieved something remarkable.

Kalpataru Square, a prestigious commercial complex developed by Kalpataru Limited, at Andheri, East, in Mumbai has become the first project in Asia to earn the Leadership in Energy and Environment Design (LEED) Platinum Core and Shell certification. This is the highest ever green building standard in the world from the U.S Green Building Council (USGBC).

Let that sink in. While the world's financial system was melting down, while real estate prices were crashing, while competitors were desperately trying to survive, Kalpataru was building Asia's first Platinum LEED certified commercial building. This wasn't just contrarian—it was visionary.

We have got the highest points ever received by any Platinum Green Building under USGBC LEED Core & Shell. The technical achievement was staggering. Energy saving of around 23% over the ASHRAE Budget building during energy simulation studies. In practical terms, this meant tenants would save millions in electricity costs over the building's lifetime.

But why did this matter? Why would a developer invest in expensive green technology during a financial crisis? The answer reveals Kalpataru's fundamental strategy: think in decades, not quarters. The impact of energy costs directly affects the bottom-line of tenants. Energy represents thirty percent of operating expenses in a typical office building and with this achievement; tenants at Kalpataru Square will see the financial benefits from day one.

The sustainability push wasn't limited to one trophy project. By 2013, innovation had become embedded in Kalpataru's DNA. Kalpataru Pinnacle's apartments face west to capitalize on breeze. This seems simple, but in Mumbai's dense urban environment, optimizing natural ventilation could reduce air conditioning costs by 30-40%.

2009 Developed our first independent mall KORUM, Thane. Entering retail development during a global recession seemed counterintuitive, but Kalpataru understood something crucial: Thane was transforming from Mumbai's suburb to a city in its own right. The mall wasn't just retail space—it was social infrastructure for an emerging urban center.

The second generation's influence was becoming more apparent. Under Parag's operational leadership, Kalpataru began adopting technologies that traditional developers ignored. Building Information Modeling (BIM) for design, Enterprise Resource Planning (ERP) for operations, Customer Relationship Management (CRM) for sales—the company was becoming as much a tech company as a real estate developer.

Kalpataru is committed to developing green and sustainable buildings designed for the future, with 47 projects certified by IGBC. By the 2010s, sustainability wasn't an experiment—it was standard operating procedure. But this created an interesting challenge: how do you convince customers to pay premium for green features when the benefits accrue over years?

Kalpataru's solution was elegant: education and demonstration. The company began organizing site visits where potential customers could experience the difference—the natural light, the ventilation, the reduced noise, the lower temperatures. They published actual electricity bills from existing green buildings. They brought in residents to share testimonials about health benefits and cost savings.

2017 Grand Central Park built along the lines of successful global urban parks. This wasn't just about copying Central Park or Hyde Park. It was about understanding that as Indian cities became denser, public spaces became more valuable. A developer who could create genuine community spaces would command premium valuations.

The innovation extended to construction techniques as well. Kalpataru began using precast technology, aluminum formwork, and mechanized construction methods. These weren't just about speed—though projects were completed 20-30% faster. They were about consistency and quality. A precast beam is identical whether it's the first or the thousandth, eliminating the variability that plagued traditional construction.

2018 Parkside Galleria is one of the country's largest real estate experience centres. This was perhaps the most telling innovation. Rather than rely on sample flats and brochures, Kalpataru created an immersive experience center where customers could visualize, customize, and even virtually walk through their future homes. The investment was massive, but the logic was clear: buying a home is the biggest decision most families make—give them the tools to make it confidently.

VI. Second Generation & Modern Transformation (2010s-Present)

The transition of family businesses often becomes their downfall. Harvard Business Review states that only 30% of family businesses survive to the second generation. In Indian real estate, where relationships and trust are paramount, the statistics are even grimmer. Yet Kalpataru's second-generation transition appeared seamless. How?

The answer lay in preparation that began decades earlier. Mr. Parag Munot has over three decades of experience in the real estate sector. This wasn't a son suddenly thrust into leadership—this was a carefully groomed successor who had spent three decades learning every aspect of the business.

The Carnegie Mellon education brought more than just an American degree. It brought exposure to global best practices, analytical frameworks, and most importantly, the confidence to challenge conventional wisdom while respecting traditional values. Parag wasn't trying to revolutionize Kalpataru—he was evolving it.

He is the Managing Director of Kalpataru Limited, one of the prominent real estate developer in India and flagship company of the Kalpataru Group. Under his leadership, Kalpataru Limited has emerged amongst the top five largest real estate developer in the Mumbai and Thane region. The numbers were impressive, but the strategy was more interesting.

While Mofatraj had built Kalpataru through big, iconic projects—the tallest buildings, the greenest complexes—Parag focused on scale through replication. Instead of one 40-storey tower, why not four 20-storey buildings across different micro-markets? The construction risk was lower, the market risk was distributed, and the brand presence multiplied.

He has been at the forefront of scaling Kalpataru Limited's expansion in new markets like Hyderabad, Noida and Nagpur. Each new market was chosen carefully. Hyderabad for its IT boom and young demographics. Noida for its proximity to Delhi and infrastructure development. Nagpur for its emerging status as India's geographic center and logistics hub.

The expansion strategy was notably different from competitors who pursued a "national footprint" by entering every major city. Kalpataru remained selective, entering only markets where it could achieve meaningful scale and maintain quality standards. No Kolkata, no Chennai, no Gurgaon—despite these being major real estate markets.

As of March 31, 2024, the company has 40 ongoing projects and has completed 70 projects. The pipeline revealed ambition tempered with prudence. Forty ongoing projects meant significant execution capability, but it wasn't the 100+ projects some competitors juggled. Quality over quantity remained the mantra.

The modern transformation wasn't just geographic—it was technological. Kalpataru began implementing:

- Virtual Reality for project visualization

- Drone surveys for construction monitoring

- IoT sensors for quality control

- Mobile apps for customer communication

- Artificial Intelligence for demand prediction

But technology was a tool, not the strategy. The strategy remained relationships. He is driving rapid growth plans for Kalpataru Group given his passion for real estate and construction sector. Passion in a second-generation leader isn't guaranteed—it's cultivated through involvement, ownership, and the freedom to innovate.

By 2024, Kalpataru had achieved something remarkable: Kalpataru is the fifth largest developer in the MCGM area in Maharashtra and the fourth largest developer in Thane, Maharashtra in terms of units supplied from the calendar years 2019 to 2023. In Mumbai's hypercompetitive market, where global funds backed mega-developers and political connections determined success, Kalpataru had carved out a sustainable position through sheer execution excellence.

As of March 31, 2024, we have a strong presence across all micro-markets in the Mumbai Metropolitan Region (MMR) and Pune, with a focus on innovation, thoughtful design, and timely delivery, reinforcing the "Kalpataru" brand's legacy of trust and reliability. The presence across "all micro-markets" was strategic brilliance. While competitors focused on premium locations, Kalpataru understood that Mumbai's geography meant every micro-market would eventually gentrify.

VII. The IPO & Public Markets Journey (2024)

For 55 years, Kalpataru had operated as a private company, growing organically, maintaining family control, and avoiding the scrutiny of public markets. So why go public in 2024?

The answer begins with an unusual transaction six months before the IPO. It issued equity shares worth Rs. 1440 cr. to promoters at a price of Rs. 517.25 in March 2025. Wait—the promoters invested ₹1,440 crore of their own money into the company at ₹517.25 per share, just months before offering shares to the public at ₹414?

This was unprecedented. Typically, IPOs see promoters cashing out, not buying in. The signal was unmistakable: the family believed the company was undervalued and was willing to bet their own capital on its future. This wasn't financial engineering—it was the ultimate insider endorsement.

Kalpataru IPO bidding started from June 24, 2025 and ended on June 26, 2025. The allotment for Kalpataru IPO was finalized on Friday, June 27, 2025. The shares got listed on BSE, NSE on July 1, 2025. The timing seemed curious—Indian markets were volatile, real estate sector was under pressure, and interest rates were elevated.

But Kalpataru had specific reasons for going public now. Repayment/pre-payment, in full or in part, of certain borrowings availed by the company and its subsidiaries. General corporate purposes. The primary use of funds was debt reduction—not aggressive expansion. This was balance sheet repair, not growth capital.

The IPO process revealed interesting details about the company's shareholder base. Promoter Holding: 81.3%. Even after the IPO, the family maintained overwhelming control. This wasn't a company looking for new management or strategic investors—it was a family business accessing public markets while maintaining family control.

Kalpataru has already secured Rs 708 crore from anchor investors by allotting over 1.71 crore shares at Rs 414 each. The anchor book includes reputed names such as GIC, Bain Capital, SBI Mutual Fund, ICICI Prudential MF, 360 ONE Group, Aditya Birla Sun Life, and Ayushmat. The anchor investor list was impressive—Singapore's sovereign wealth fund, Bain Capital, and India's largest mutual funds. These weren't momentum investors—they were long-term institutional capital.

The public issue of Kalpataru IPO (KALPATARU,544423) was offered at ₹414.00 per share and was listed at ₹414.00, resulting in an at-par listing. With a minimum lot size of 36 shares, the IPO yielding ₹0 per lot gain or loss on listing. The flat listing was actually positive—in a frothy market where IPOs often list at huge premiums only to crash later, Kalpataru's stable debut suggested realistic pricing and genuine long-term investors.

The IPO also revealed the company's financial challenges. Revenue from operations decline sharply by approximately 46.89 per cent year-on-year (YoY) -- falling from Rs 3,633.1 crore in the financial year ended March 31, 2023, to Rs 1,929.9 crore in FY24. The company also reported a drop in total income, which fell to Rs 2,029.9 crore in FY24 from Rs 3,716.6 crore in FY23 -- a decline of around 45.38 per cent. Despite the fall in revenue and income, Kalpataru managed to reduce its net loss during the year. The company narrowed its net loss to Rs 113.8 crore in FY24 from Rs 226.7 crore in FY23.

The numbers raised questions. Why would a company with declining revenues and losses go public? The answer lay in understanding real estate accounting. FY23's exceptional revenues came from a one-time land transaction. The underlying business was actually improving—losses were narrowing, operations were stabilizing, and the pipeline was strong.

The management is confident of further improvements in its financial performance in coming years considering the projects on hand. Management confidence was backed by tangible metrics: 40 ongoing projects, strong brand value, and improving operational metrics.

VIII. Business Model & Financial Architecture

To understand Kalpataru's business model, imagine you're playing SimCity, but every decision takes three years to materialize, requires hundreds of crores in capital, and affects thousands of families. That's real estate development in Mumbai.

Specializing in luxury, premium, and mid-income residential, commercial, and retail developments, we manage all aspects of real estate development, from land acquisition to design, construction, and sales. The "integrated" model meant Kalpataru controlled every step of the value chain. This wasn't just vertical integration—it was risk management.

Consider the typical real estate development cycle: 1. Land Acquisition: 2-3 years of negotiation, due diligence, and approvals 2. Design & Approvals: 1-2 years of architectural planning and regulatory clearances 3. Construction: 3-4 years of building 4. Sales & Handover: Overlapping with construction, extending 1-2 years post-completion

A single project could span a decade from conception to completion. Capital remained locked for years before generating returns. This is why Company has a low return on equity of -7.75% over last 3 years. The negative ROE wasn't operational failure—it was the nature of the business cycle.

As of March 31, 2024, their ongoing projects comprised approximately 22.02 msf of developable area. Further, as of March 31, 2024, their forthcoming projects comprised approximately 19.93 msf of developable area, and are expected to launch across the financial years 2025, 2026 and 2027 in various phases. The 42 million square feet pipeline represented roughly ₹25,000-30,000 crore in future revenues—but spread over 5-7 years.

The capital allocation strategy was crucial. Unlike manufacturing where you invest in machinery that produces predictable output, real estate capital allocation was more like venture capital—high risk, long gestation, binary outcomes. A single regulatory change could make a project unviable. A market downturn could destroy returns.

Kalpataru's approach to this challenge was distinctive:

Joint Development vs. Outright Purchase: Instead of buying land outright, Kalpataru often entered joint development agreements with landowners. The landowner contributed land, Kalpataru contributed development expertise and capital, and they shared revenues. This reduced capital requirements and aligned interests.

Phased Development: Large projects were broken into phases. Phase 1 revenues funded Phase 2 construction. This reduced capital needs and market risk.

Pre-sales Model: Kalpataru leverages a strong brand to sell projects during construction. Customers paid 20-30% upfront, providing working capital. The brand strength meant customers trusted Kalpataru to deliver, enabling higher pre-sales.

Geographic Concentration: By focusing on Mumbai and select cities, Kalpataru achieved economies of scale in procurement, construction crews, and regulatory relationships.

Revenue: 2,222 Cr · Profit: 24.7 Cr. The thin profit margins revealed the industry's challenge. Real estate appeared high-margin—apartments selling for crores—but after land costs, construction, approvals, marketing, and financing costs, margins were often single-digit.

The financial architecture also revealed interesting patterns:

Debtor days have increased from 98.1 to 128 days. Rising debtor days suggested either collection challenges or more flexible payment terms to attract customers. In a competitive market, payment flexibility became a differentiator.

Earnings include an other income of Rs.110 Cr. Significant other income—likely from interest on customer advances and deposits—showed how financial management was as important as construction management.

IX. Playbook: Real Estate Development Lessons

After 55 years and 113 projects, what's the Kalpataru playbook for real estate development? The lessons are counterintuitive, especially for those who view real estate as a get-rich-quick scheme.

Lesson 1: Trust Compounds Faster Than Capital

The company's brand "Kalpataru" is a well-established brand in the real estate sector and acts as a strategic sales driver enabling the company to sell projects at a premium to competitors. The premium wasn't just pricing power—it was reduced sales and marketing costs, faster sales velocity, and lower financing costs as banks trusted the brand.

Lesson 2: Innovation Must Be Practical

From 1.5 bedroom apartments to west-facing designs for ventilation, Kalpataru's innovations weren't technological marvels—they were practical solutions to real problems. Innovation in real estate isn't about the newest materials or fanciest designs—it's about understanding how people actually live.

Lesson 3: Family Business Doesn't Mean Unprofessional

He has been awarded the "the lifetime achievement award" each at the 22nd Construction World Global Awards 2024, CREDAI - MCHI Golden Pillars Real Estate Awards 2023 and 10th Realty Plus Excellence Awards 2018. Recognition from industry bodies showed that family-run could coexist with professional excellence.

The governance structure balanced family control with professional management. Independent directors, institutional processes, and transparent reporting created trust without diluting family involvement.

Lesson 4: Sustainability Is a Moat

Kalpataru focuses on sustainable, green building practices in development. What started as expensive experimentation became competitive advantage. Green buildings commanded premium prices, attracted quality tenants, and most importantly, created differentiation in a commoditized market.

Lesson 5: Geography Is Destiny

Kalpataru holds over 1,800 acres of land reserves, offering future development potential across key cities. The land bank wasn't randomly accumulated—each parcel was strategically located in the path of urban expansion. Understanding city master plans, infrastructure development, and demographic shifts was more important than financial engineering.

Lesson 6: Cycles Are Features, Not Bugs

Real estate is cyclical—boom, bust, recovery, repeat. Kalpataru survived by: - Never overleveraging during booms - Maintaining cash reserves for downturns - Buying land during busts - Launching projects during recoveries

Lesson 7: Multi-Generational Thinking Wins

Led by Mr. Mofatraj P. Munot, with over five decades of experience, and Mr. Parag M. Munot, with three decades. The combined eight decades of experience meant institutional memory of multiple cycles, regulatory changes, and market shifts. This wasn't replaceable by hiring from competitors.

Lesson 8: Execution Excellence Matters More Than Vision

They have adopted an integrated real estate development model, with capabilities and in-house resources to carry out all key activities associated with real estate development, including identifying and acquiring land (or development rights thereto), planning, designing, executing, sales, and marketing of their projects. As a result of their end-to-end execution capabilities and in-house resources, they are able to develop high-quality projects as well as benefit from economies of scale and supply chain efficiency.

In-house capabilities meant control, consistency, and ultimately, competitive advantage.

X. Analysis & Future Outlook

As we analyze Kalpataru in 2024, we see a company at an inflection point. The IPO has provided capital for balance sheet repair, the second generation has successfully taken operational control, and the pipeline suggests strong growth ahead. But what does the future hold?

The Mumbai Reality

Mumbai real estate is both blessing and curse. For the calendar years 2019 to 2023, the MMR was ranked first among the top seven Indian markets (MMR (Maharashtra), Pune (Maharashtra), Bengaluru (Karnataka), Hyderabad (Telangana), the National Capital Region, Chennai (Tamil Nadu) and Kolkata (West Bengal)) in terms of supply, absorption and average base selling price.

Mumbai's dominance seems unshakeable, but it comes with challenges: - Land scarcity driving prices beyond affordability - Regulatory complexity adding years to project timelines - Infrastructure constraints limiting expansion possibilities - Political interference affecting approvals and policies

Yet Mumbai's strengths remain compelling: - India's financial capital ensuring constant demand - Limited supply creating scarcity value - Infrastructure investments (Metro, Coastal Road, Trans-Harbor Link) opening new micro-markets - Redevelopment opportunities in aging building stock

Competition Dynamics

Godrej Properties Limited: A leading real estate developer in India, with a strong presence in the Mumbai Metropolitan Region (MMR) and Pune. Macrotech Developers Limited: A prominent real estate developer in India, with a significant presence in the MMR and other cities. Oberoi Realty Limited: A well-established real estate developer in India, with a strong presence in the MMR and other cities.

The competitive landscape reveals distinct strategies: - Godrej Properties: Asset-light model, brand leverage, national presence - Macrotech (Lodha): Scale player, affordable housing focus, mega-townships - Oberoi Realty: Ultra-luxury focus, limited projects, high margins

Kalpataru's positioning—premium but not ultra-luxury, selective geographic presence, integrated model—creates a unique niche. The company isn't trying to be the biggest or the most premium—it's trying to be the most trusted.

Financial Trajectory

However, the company reported a net profit of Rs 5.51 crore for the nine-month period ended December 31, 2024, with revenues of Rs 1,624.7 crore. The return to profitability, even if modest, signals operational improvement.

The company has turned the corner for 9M of FY25 and the management is confident of further improvements in its financial performance in coming years considering the projects on hand. Management confidence appears justified given: - 40 ongoing projects providing revenue visibility - Debt reduction improving interest coverage - Pre-sales momentum indicating market acceptance - Cost optimization showing results

The Bear Case

The challenges are real and substantial:

- Leverage Concerns: Despite IPO proceeds for debt reduction, absolute debt levels remain high

- Execution Risk: 40 ongoing projects require flawless execution

- Market Concentration: Heavy Mumbai dependence creates geographic risk

- Regulatory Overhang: Real estate remains heavily regulated with policy uncertainty

- Working Capital Intensity: The business model requires constant capital infusion

- Competition: Well-funded competitors with institutional backing

The Bull Case

Yet the opportunity is equally compelling:

- Mumbai Dynamics: Supply constraints and demand growth create structural opportunity

- Brand Value: Five decades of trust commands premium and ensures sales

- Redevelopment Opportunity: Mumbai's aging building stock needs redevelopment

- Professional Management: Second generation bringing modern practices

- Pipeline Strength: 42 million sq ft provides multi-year growth visibility

- Sustainability Leadership: Green building expertise becoming differentiator

XI. Epilogue & Key Takeaways

As our story of Kalpataru Limited draws to a close, we return to where we began—that 33-storey tower piercing Mumbai's skyline in 1976. Kshitij wasn't just a building; it was a declaration that Indian companies could build as tall, as strong, and as beautiful as anyone in the world.

Today, Mumbai's skyline is unrecognizable from that era. Towers of 50, 60, even 80 floors are becoming common. International architects design signature buildings. Global capital funds mega-projects. Yet in this transformed landscape, Kalpataru hasn't just survived—it has thrived by staying true to its founding principles.

The Munot Foundation which organizes several initiatives across the country, in the areas of education and healthcare, reaching out to society's least privileged. He believes that good education and good health are the two pillars upon which the future of the country rests. The philanthropy isn't corporate social responsibility mandated by law—it's philosophy embedded in DNA.

What can investors and entrepreneurs learn from Kalpataru's journey?

First, patience pays. In an era of quarterly earnings and instant gratification, Kalpataru played a 55-year game. Buildings designed in the 1970s still generate rental income. Relationships built in the 1980s still drive sales. Reputation earned in the 1990s still commands premiums.

Second, innovation doesn't require disruption. Kalpataru never "disrupted" real estate. Instead, it consistently innovated within the framework—1.5 bedrooms, green buildings, west-facing apartments. Small innovations, compounded over decades, created sustainable differentiation.

Third, family businesses can modernize without losing soul. The transition from Mofatraj to Parag wasn't just succession—it was evolution. The values remained constant while practices modernized. This isn't easy, which is why it's valuable.

Fourth, trust is the ultimate moat. In real estate, where purchases are infrequent and expensive, trust matters more than technology, financial engineering, or even location. Kalpataru's multigenerational customer relationships prove that trust, carefully built and maintained, becomes unassailable competitive advantage.

Fifth, sustainability is strategy, not marketing. Kalpataru's early bet on green buildings seemed expensive and unnecessary. Today, it's a differentiator that competitors struggle to replicate because it requires not just investment but belief.

As we look ahead, Kalpataru faces a fascinating future. The company must navigate: - Mumbai's evolution into a global city - Climate change affecting coastal construction - Technology transforming customer expectations - Generational shifts in housing preferences - Regulatory evolution in real estate

Yet if history is any guide, Kalpataru will navigate these challenges the same way it always has—patiently, thoughtfully, and with an eye on the next 50 years rather than the next quarter.

The story of Kalpataru Limited isn't just about real estate. It's about how businesses can create value across generations, how trust can be built and maintained in low-trust industries, and how thinking long-term remains the ultimate competitive advantage.

In Mumbai, where every square foot tells a story of ambition, struggle, and dreams, Kalpataru has written its story in concrete and steel, in glass and green spaces, in the homes of thousands of families who trusted a first-generation entrepreneur from Jodhpur to help them build their dreams.

That trust, more than any building, may be Kalpataru's tallest achievement.

XII. Recent News

-

Q1 FY26 Performance: Kalpataru reports Q1 FY26 consolidated loss of Rs 56.37 Cr; standalone loss Rs 15.56 Cr; auditor review unmodified... ESOP granted; IPO proceeds utilized

-

Strong Pre-sales Growth: Kalpataru reports Q1 FY26 pre-sales up 83% to ₹1,249cr, collections up 37%, net debt reduced to ₹7,939cr

-

FY25 Full Year Results: Real estate firm Kalpataru Ltd announced on Sunday that it has registered a 41 per cent growth in its pre-sales to ₹4,531 crore in FY25, driven by higher demand for residential properties... For the full FY25, pre-sales were at ₹4,531 crore, up 41 per cent year-on-year (YoY)... In FY24, the company sold properties worth ₹3,202 crore

-

Post-IPO Debt Reduction: Kalpataru Ltd raised ₹1,590 crore in equity through the IPO in June 2025. Of this, ₹1,192.5 crore has been utilised for debt repayment to date, in line with the objects of the issue. As a result, the net debt-to-equity ratio has further improved

XIII. Links & Resources

Company Resources: - [Official Website: www.kalpataru.com] - [Annual Reports and Investor Presentations] - [SEBI Filings and RHP Documents]

Industry Research: - [ANAROCK Property Reports - Mumbai Real Estate] - [Knight Frank India Real Estate Reports] - [CREDAI Maharashtra Publications] - [JLL India City Momentum Index]

Books on Indian Real Estate: - "The Indian Real Estate" by Ashwinder Raj Singh - "Mumbai Fables" by Gyan Prakash - "Maximum City: Bombay Lost and Found" by Suketu Mehta

Mumbai Development History: - [Mumbai Metropolitan Region Development Authority (MMRDA)] - [Municipal Corporation of Greater Mumbai Archives] - [Urban Design Research Institute (UDRI) Publications]

Academic Papers: - "The Political Economy of Urban Land in India's Metro Cities" - EPW - "Sustainable Urban Development: Case Study of Mumbai" - IIM Ahmedabad - "Family Businesses in Indian Real Estate" - ISB Hyderabad

Green Building Resources: - [Indian Green Building Council (IGBC)] - [US Green Building Council - LEED Certification] - [TERI - Green Rating for Integrated Habitat Assessment (GRIHA)]

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube