Bank of Baroda: The Nation-Building Bank Goes Global

I. Introduction & Episode Roadmap

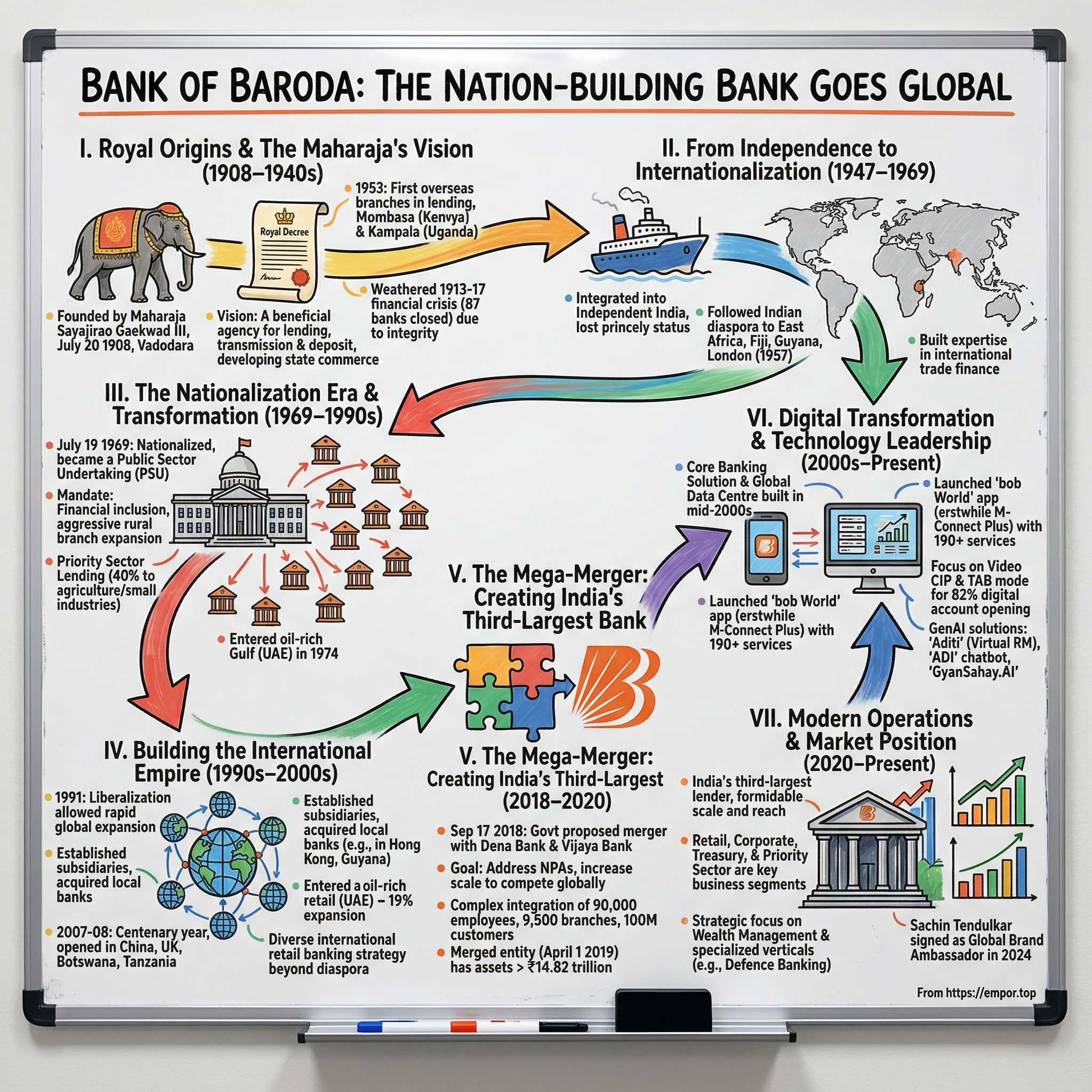

In the heart of Vadodara, Gujarat, on a monsoon morning in July 1908, something extraordinary happened. The bank was founded by the Maharaja of Baroda, Maharaja Sayajirao Gaekwad III on 20 July 1908, marking the beginning of what would become one of India's most storied financial institutions. Unlike the typical colonial-era banks established by British interests, this was different—a princely state bank with a vision that transcended mere commerce.

The central question that drives our exploration today is profound: How did a regional bank founded by a progressive maharaja in a princely state transform into India's third-largest lender, navigating colonialism, independence, nationalization, and ultimately orchestrating one of the most audacious mergers in global banking history?

This is not merely a story of balance sheets and branch expansions. It's a narrative of nation-building through banking, of weathering economic storms that destroyed dozens of competitors, of bold international expansion when others feared to venture beyond borders, and of a 2019 mega-merger that created a banking behemoth with assets exceeding ₹14.82 trillion. It's about an institution that served as both witness and participant in India's economic transformation—from princely state to independence, from socialist controls to liberalization, from domestic focus to global ambitions.

What makes Bank of Baroda's journey particularly fascinating is its ability to maintain relevance across three distinct centuries. Founded in the twilight of the British Raj, it thrived through independence, survived nationalization, embraced technology, and continues to compete in an era of fintech disruption and digital banking. This adaptability, combined with its unwavering commitment to both commercial success and social responsibility, offers profound lessons for understanding how institutions can endure and evolve.

As we embark on this deep dive, we'll explore themes that resonate far beyond banking: the role of visionary leadership in institutional building, the delicate balance between government ownership and commercial autonomy, the challenges of cultural integration in massive mergers, and the transformation of a traditional bank into a digital powerhouse. We'll examine how Bank of Baroda navigated the treacherous waters of non-performing assets, regulatory changes, and intense competition while maintaining its position as a trusted financial partner for millions.

II. Royal Origins & The Maharaja's Vision (1908–1940s)

The story of Bank of Baroda begins not in a boardroom or financial district, but in the progressive court of one of India's most enlightened rulers. Maharaja Sayajirao Gaekwad III not only spearheaded educational and social reforms but also played a pivotal role in the economic development of Baroda State. Among his notable economic enterprises, the establishment of a railroad and the founding of the Bank of Baroda in 1908 stand out prominently.

The Maharaja's vision for the bank was remarkably prescient and comprehensive. The founder strongly believed that, "a bank of this nature would prove to be a beneficial agency for lending, transmission and deposit of money and a powerful factor in the development of art, industries and commerce of the state as also of adjoining territories". This wasn't just about creating a financial institution; it was about catalyzing economic development across an entire region and beyond.

The formal establishment came with careful legal grounding. The Bank of Baroda, established in July 1908 under the Companies Act of 1887, has since grown and expanded successfully. The founding wasn't a solitary effort but involved a constellation of prominent business leaders. In 1908, Sayajirao Gaekwad III, set up the Bank of Baroda (BoB), with other stalwarts of industry such as Sampatrao Gaekwad, Ralph Whitenack, Vithaldas Thakersey, Lallubhai Samaldas, Tulsidas Kilachand and NM Chokshi.

The early days of the bank were marked by a ceremonial beginning that reflected both tradition and ambition. It was founded by the great visionary the late Maharaja of Baroda – Sir Sayajirao Gaekwad-III. On 18 July 1908, an auspicious day, the Maharaja took an elephant ride to a small rented office in the heart of the city. He arrived before 11 am, and deposited a silver plate filled with 101 gold coins – Bank of Baroda's first deposit. This symbolic act, blending royal patronage with modern banking, set the tone for an institution that would bridge traditional values with progressive finance.

The bank's early expansion strategy was methodical and strategic. Two years later, BoB established its first branch in Ahmedabad. This move beyond Baroda's borders signaled ambitions that extended far beyond serving just the princely state. Ahmedabad, as Gujarat's commercial hub, provided the perfect launching pad for wider expansion.

The true test of the bank's resilience came early in its existence. During the years 1913 to 1917, a financial crisis led to the closure of 87 banks in India. Despite these challenges, the Bank of Baroda weathered the storm due to its steadfast financial integrity, a legacy that continues to define its ethos today. This survival, when so many others perished, wasn't mere luck—it was the result of conservative lending practices, strong capital reserves, and the confidence inspired by royal backing.

The princely state of Baroda itself provided a unique context for the bank's founding. Under Sayajirao Gaekwad III's rule, Baroda was one of India's most progressive states, with initiatives in education (including free and compulsory primary education), social reform (including measures against untouchability), and economic development. The bank was part of a broader modernization agenda that included establishing libraries, universities, and industrial enterprises. This ecosystem of progress created fertile ground for the bank's growth.

The Maharaja's approach to banking was influenced by his extensive travels abroad, where he observed modern financial systems in Europe and America. He understood that economic development required not just capital but also efficient mechanisms for its deployment. The bank was envisioned as a catalyst for entrepreneurship, enabling local merchants and industrialists to access credit for expanding their businesses.

During the 1920s and 1930s, the bank continued its steady expansion across Gujarat and into neighboring regions. Each new branch was carefully selected based on commercial potential and strategic importance. The bank developed a reputation for reliability and prudent management, attracting deposits from both the wealthy elite and emerging middle class. Its loan portfolio supported everything from textile mills to agricultural enterprises, playing a crucial role in the region's economic development.

The philosophy of "banking with a purpose" was embedded from the beginning. While commercial viability was important, the bank never lost sight of its broader mission to facilitate economic progress. This included supporting small traders and artisans, not just large industrialists. The bank pioneered several customer-friendly practices, including vernacular banking (conducting business in local languages) and flexible repayment schedules for seasonal businesses.

The governance structure established by the Maharaja balanced professional management with strategic oversight. While the royal family maintained influence, day-to-day operations were handled by experienced bankers recruited from across India. This separation of ownership and management was progressive for its time and helped establish professional banking standards that would serve the institution well in coming decades.

III. From Independence to Internationalization (1947–1969)

The end of British rule and the integration of princely states into independent India marked a pivotal transformation for Bank of Baroda. The bank, which had thrived under royal patronage, now had to navigate the complexities of a newly independent nation with its own economic priorities and regulatory framework. Yet, rather than retreating into a defensive posture, Bank of Baroda embarked on one of the most ambitious international expansion strategies ever undertaken by an Indian bank.

The post-independence period brought both challenges and opportunities. With the integration of Baroda state into Bombay State (and later Gujarat), the bank lost its special status as a state-sponsored institution. However, this also freed it from geographic constraints and allowed it to think nationally and internationally. The leadership recognized that India's diaspora, particularly in East Africa and other British colonies, represented an underserved market with significant potential.

The bank grew domestically until after World War II. Then in 1953 it crossed the Indian Ocean to serve the communities of Indians in Kenya and Indians in Uganda by establishing a branch each in Mombasa and Kampala. This move to East Africa wasn't random—it followed the trails of Indian merchants and traders who had established thriving businesses across the region during the colonial period.

The decision to open the first overseas branch in Mombasa in 1953 was strategic on multiple levels. East Africa had a substantial Indian population engaged in trade, commerce, and industry, but they were largely underserved by local banks. These communities maintained strong ties to India, regularly remitting money home and seeking financial services that understood their unique needs. Bank of Baroda positioned itself as the bridge between their adopted homes and their motherland.

The expansion continued systematically across East Africa. The next year it opened a second branch in Kenya, in Nairobi, and in 1956 it opened a branch in Tanzania at Dar-es-Salaam. Each new branch served as a hub for Indian businesses, facilitating trade finance, remittances, and providing banking services tailored to the diaspora's needs. The bank's understanding of Indian business culture and practices gave it a significant competitive advantage over local and international banks.

But Bank of Baroda's international ambitions extended beyond Africa. In 1957, the bank made a bold move that would establish its credentials as a truly international institution. During the period 1953-1969, the Bank opened three branches in Fiji, five branches in Kenya, three branches in Uganda and one each in London and Guyana. Between 1969 to 1974, we established three branches in Mauritius, two branches in UK and one branch in Fiji.

The London branch, established in 1957, was particularly significant. It placed Bank of Baroda in the heart of global finance, enabling it to facilitate trade between India and Britain, serve the growing Indian community in the UK, and learn from one of the world's most sophisticated banking markets. This presence in London also enhanced the bank's international credibility and opened doors for correspondent banking relationships worldwide.

The strategy of following the Indian diaspora proved remarkably successful. In Fiji, where Indians comprised a significant portion of the population and dominated retail trade and agriculture, Bank of Baroda became an integral part of the economic landscape. Similarly, in Guyana, the bank served the substantial Indo-Guyanese community descended from indentured laborers.

During this period, the bank also developed sophisticated capabilities in international trade finance. It became an expert in letters of credit, foreign exchange, and cross-border transactions—skills that would prove invaluable as India's economy gradually opened up in later decades. The international network also provided valuable foreign exchange earnings, which were crucial for India during a period of foreign exchange scarcity.

The management structure evolved to handle this international complexity. The bank established an International Division at its head office, staffed with specialists in foreign exchange, international law, and cross-border banking. It also began recruiting and training staff specifically for overseas postings, creating a cadre of internationally experienced bankers who understood both Indian and global banking practices.

Technology adoption during this period, while primitive by today's standards, was progressive for its time. The bank invested in telex machines for international communication, implemented standardized procedures across branches, and developed systems for reconciling accounts across different currencies and time zones. These investments in infrastructure and processes laid the groundwork for future expansion.

The relationship with host country regulators required careful navigation. Each country had its own banking regulations, cultural norms, and business practices. Bank of Baroda developed expertise in regulatory compliance across multiple jurisdictions—a capability that would become increasingly valuable as banking regulations grew more complex globally.

The bank also played a crucial role in facilitating trade between India and its host countries. It financed imports of Indian goods, from textiles to spices, and helped local businesses export commodities back to India. This two-way flow of trade, supported by the bank's financial services, strengthened economic ties between India and these nations.

Risk management during international expansion was a constant concern. Political instability in some African countries, currency fluctuations, and varying regulatory environments all posed challenges. The bank developed robust risk assessment frameworks and maintained conservative lending practices, which helped it navigate through various crises including political upheavals in Uganda and Kenya.

The period also saw the bank building strong relationships with correspondent banks worldwide. These relationships were crucial for facilitating international transactions, providing credit lines, and accessing global financial markets. The network of correspondent banks became a valuable asset, enabling Bank of Baroda to offer comprehensive international banking services to its clients.

As the 1960s progressed, the bank's international operations became increasingly sophisticated. It began offering specialized services like export credit, project finance for overseas Indian businesses, and treasury services for managing foreign exchange risk. The international division became a significant profit center, contributing both to the bottom line and to the bank's reputation as India's most international bank.

IV. The Nationalization Era & Transformation (1969–1990s)

The nationalization of Bank of Baroda marked one of the most dramatic turns in its history. The Government of India nationalized the Bank of Baroda, along with 13 other major commercial banks of India, on 19 July 1969 and the bank was designated as a profit-making public sector undertaking (PSU). This event, occurring just one day before the bank's 61st anniversary, fundamentally altered its ownership structure, mandate, and operational philosophy.

Prime Minister Indira Gandhi's decision to nationalize the major banks was driven by a socialist vision of using banking as a tool for economic development and social justice. For Bank of Baroda, this meant transitioning from a commercially focused institution with royal origins to a government-owned entity with explicit social responsibilities. The transformation was profound and multifaceted.

The immediate impact of nationalization was a dramatic shift in the bank's priorities. While maintaining commercial viability remained important, the bank now had to pursue aggressive branch expansion into rural and semi-urban areas, implement priority sector lending targets, and participate in government-sponsored poverty alleviation programs. The mandate expanded from serving profitable customer segments to achieving financial inclusion for all Indians.

Branch expansion during the 1970s and 1980s was unprecedented. The bank opened hundreds of branches in remote villages, often in locations where banking services had never existed before. These branches were frequently unprofitable from a purely commercial perspective, but they served a crucial social function by bringing formal financial services to previously unbanked populations. The bank's staff had to adapt to working in challenging conditions, often without basic infrastructure like electricity or proper roads.

The priority sector lending requirements mandated that 40% of lending go to agriculture, small-scale industries, and other designated sectors. This forced the bank to develop new competencies in agricultural lending, microfinance, and small business credit. Loan officers who had previously focused on large corporate clients now had to understand crop cycles, assess the creditworthiness of small farmers, and manage portfolios of tiny loans spread across thousands of borrowers.

Despite these social obligations, Bank of Baroda managed to maintain its international expansion momentum. A significant development in the sphere of overseas operations was the entry of the Bank in the oil rich Gulf countries in 1974 when two branches were opened in UAE, one at Dubai and another at Abu Dhabi. This expansion into the Gulf was particularly strategic, as these countries were experiencing an oil boom and attracting large numbers of Indian workers who needed banking services for remittances.

The 1980s brought new challenges and opportunities. The bank had to navigate India's complex regulatory environment while maintaining profitability. It developed innovative products for different customer segments, from savings schemes for rural households to working capital facilities for small industries. The bank also began computerization efforts, though these were limited by government policies that restricted technology adoption to protect employment.

An important development during this period was the evolution of the bank's organizational culture. The transition from private to public sector brought in new employees through competitive examinations, creating a more diverse workforce. The bank had to balance the entrepreneurial culture inherited from its private sector days with the procedural requirements and social obligations of a government-owned institution.

The bank also played a crucial role in implementing government schemes. Whether it was financing the Green Revolution through agricultural loans, supporting small-scale industries under various government programs, or implementing loan melas for political purposes, Bank of Baroda became an instrument of state policy. This sometimes led to deterioration in asset quality, as political considerations occasionally overrode commercial prudence.

Training and development became increasingly important as the bank's role expanded. The bank established training centers to prepare staff for diverse responsibilities, from agricultural lending to international banking. It also began recruiting specialists in areas like agricultural economics, rural development, and small business management to support its expanded mandate.

The late 1980s and early 1990s saw the beginning of financial sector reforms in India. The bank had to prepare for a more competitive environment while still carrying the burden of its social obligations. It began focusing on improving operational efficiency, adopting new technologies where permitted, and strengthening its risk management systems.

In 1999, BoB merged in Bareilly Corporation Bank in another rescue. At the time, Bareilly had 64 branches, including four in Delhi. These mergers and acquisitions during the nationalization era served dual purposes: they prevented banking failures that could have hurt depositors, and they helped Bank of Baroda expand its network and customer base.

The international operations during this period continued to flourish, providing valuable foreign exchange earnings and maintaining the bank's global presence. In 1997, BoB opened a branch in Durban. The next year BoB bought out its partners in IUB International Finance in Hong Kong. The Hong Kong acquisition was particularly significant as it gave the bank a foothold in one of Asia's most important financial centers.

Asset quality management became increasingly challenging during the late 1980s and early 1990s. The directed lending programs, combined with economic downturns and political interference, led to mounting non-performing assets. The bank had to balance the need for recovery with political sensitivities and social considerations. This period taught valuable lessons about credit risk management that would influence the bank's policies in subsequent decades.

The employees' union played a significant role during the nationalization era. Wage negotiations, service conditions, and technology adoption were all subjects of intense discussions between management and unions. The bank had to navigate these labor relations carefully while trying to improve productivity and efficiency.

V. Building the International Empire (1990s–2000s)

The liberalization of India's economy in 1991 opened new horizons for Bank of Baroda's international operations. With foreign exchange controls relaxing and Indian businesses going global, the bank found itself uniquely positioned to leverage its decades of international experience. The period from the 1990s to the 2000s witnessed an unprecedented expansion of its global footprint, transforming it into India's most international bank.

The strategic approach to international expansion during this period was remarkably sophisticated. Rather than simply opening branches, the bank began establishing subsidiaries, acquiring local banks, and forming joint ventures in different markets. Apparently this was a response to regulatory changes following Hong Kong's reversion to the People's Republic of China. The now wholly owned subsidiary became Bank of Baroda (Hong Kong), a restricted license bank.

In Guyana, BoB incorporated its branch as a subsidiary, Bank of Baroda Guyana. BoB added a branch in Mauritius and closed its Harrow Branch in London. This shift from branches to subsidiaries reflected a more nuanced understanding of international banking regulations and the benefits of local incorporation in certain jurisdictions.

The new millennium brought accelerated expansion. In 2000 BoB established Bank of Baroda (Botswana). The bank has three banking offices, two in Gaborone and one in Francistown. The African expansion continued to follow the Indian diaspora but also began serving local populations and businesses, demonstrating the bank's evolution from a diaspora-focused institution to a truly international bank.

Technology became a crucial enabler of international operations during this period. The bank invested heavily in connecting its international network through modern communication systems, implemented SWIFT for international transfers, and developed centralized processing capabilities for foreign exchange and trade finance operations. These technological investments were essential for providing seamless service across time zones and currencies.

The acquisition strategy gained momentum in the 2000s. In 2002 BoB acquired Benares State Bank (BSB) at the Reserve Bank of India's request. BSB had been established in 1946 but traced its origins back to 1871 and its function as the treasury office of the Benares state. The acquisition of BSB brought BoB 105 new branches. While this was a domestic acquisition, it demonstrated the bank's growing capability to integrate other institutions—a skill that would prove crucial in later years.

The bank's centenary year in 2007-2008 marked a high point in its international expansion. In 2007, its centenary year, BoB's total business crossed 2.09 trillion (short scale), its branches crossed 2000, and its global customer base 29 million people. The celebration of 100 years coincided with an aggressive push into new markets.

China, with its rapidly growing economy and increasing trade with India, became a priority market. In 2008 BoB opened a branch in Guangzhou, China (02/08/2008) and in Kenton, Harrow United Kingdom. The Guangzhou branch was strategically located in China's manufacturing hub, facilitating trade finance for Indian importers sourcing from Chinese suppliers.

The bank also began offering sophisticated products and services internationally. Treasury operations expanded to include complex foreign exchange derivatives, interest rate swaps, and structured trade finance products. The bank developed expertise in project finance for overseas Indian businesses, syndicated lending for large international transactions, and cash management services for multinational corporations.

BoB also returned to Tanzania by establishing a subsidiary in Dar-es-Salaam. BoB also opened a representative office each in Kuala Lumpur, Malaysia, and Guangdong, China. Representative offices, while not able to conduct banking business directly, served as important listening posts and relationship-building centers in markets where full banking licenses were difficult to obtain.

The international retail banking strategy evolved significantly during this period. Beyond serving the diaspora, the bank began targeting local customers in its host countries. Products were customized for local markets—Islamic banking products in the Gulf, mortgage products tailored to local regulations in the UK, and trade finance solutions designed for Africa's commodity exporters.

In 2009 Bank of Baroda (New Zealand) was registered. As of 2017 BoB (NZ) has 3 branches: two in Auckland, one in Wellington. The expansion into developed markets like New Zealand demonstrated the bank's confidence in competing with sophisticated international banks in highly regulated environments.

Risk management for international operations became increasingly sophisticated. The bank developed country risk assessment frameworks, implemented limits for exposure to different markets, and created specialized units for managing regulatory compliance across multiple jurisdictions. The lessons learned from operating in diverse markets—from the volatile African countries to highly regulated developed markets—created a robust risk management culture.

The bank also pioneered innovative delivery channels for international customers. Internet banking for NRIs (Non-Resident Indians) was launched early, allowing diaspora customers to manage their accounts in India from anywhere in the world. Mobile banking services were introduced in select international markets, and the bank experimented with agent banking models in Africa to extend its reach beyond traditional branches.

Partnerships and alliances became an important part of the international strategy. In 2010 Malaysia awarded a commercial banking licence to a locally incorporated bank to be jointly owned by Bank of Baroda, Indian Overseas Bank and Andhra Bank. Such collaborative approaches helped overcome regulatory barriers and share risks in new markets.

The global financial crisis of 2008 tested the bank's international operations but also validated its conservative approach to international expansion. While many global banks retreated from international markets, Bank of Baroda maintained its presence and even found opportunities to expand as competitors withdrew. The crisis reinforced the importance of maintaining strong capital buffers, diversified revenue streams, and robust risk management systems.

Human resource management for international operations evolved into a sophisticated function. The bank developed specialized career paths for international banking, created cultural orientation programs for staff posted overseas, and implemented succession planning for key international positions. The ability to deploy experienced Indian bankers globally while also recruiting and developing local talent became a key competitive advantage.

The contribution of international operations to the bank's overall performance grew steadily. Foreign branches generated significant fee income from trade finance and remittances, provided valuable foreign currency resources, and enhanced the bank's ability to serve Indian corporates expanding globally. The international network also provided diversification benefits, as economic cycles in different countries offset each other.

VI. The Mega-Merger: Creating India's Third-Largest Bank (2018–2020)

The announcement on September 17, 2018, sent shockwaves through India's banking sector. On 17 September 2018, the government of India proposed the merger of Dena Bank and Vijaya Bank with the Bank of Baroda, pending approval from the boards of the three banks, effectively creating the third largest lender in the country. This wasn't just another consolidation—it was India's first three-way amalgamation of banks, a complex undertaking that would test the limits of integration capabilities in the banking sector.

The strategic rationale behind this mega-merger was multifaceted. The Indian banking sector was grappling with mounting non-performing assets (NPAs), intense competition from private banks, and the need for scale to compete globally. Some of the main stated reasons for the merger were to help the weaker banks improve their operational efficiency, increase their customer base and market reach, and to help them raise capital without depending on government funds at all.

The three banks brought different strengths and challenges to the merger. Bank of Baroda, with its international presence and technological capabilities, was the natural anchor. Vijaya Bank, though smaller, had relatively better asset quality and strong presence in South India. Dena Bank, however, was the weak link. Earlier that year, Dena Bank had been brought under the Prompt Corrective Action (PCA) framework due to its high non-performing loans. At the time of the proposal to merge, the gross NPA ratios of Bank of Baroda, Vijaya Bank and Dena Bank were 12.4%, 6.9% and 22% respectively, and Dena Bank was the weakest among the three in terms of its total business size.

The government's decision to proceed with this ambitious merger reflected a broader strategy of creating fewer but stronger public sector banks. The timing was crucial—the banking sector needed consolidation to address systemic weaknesses, and the government wanted to reduce its capital infusion burden. Bank of Baroda, with its relatively stronger balance sheet and proven track record of absorbing other banks, was chosen as the vehicle for this transformation.

The merger was approved by the Union Cabinet and the boards of the banks on 2 January 2019. The speed of approval reflected the urgency felt by policymakers to address the banking sector's challenges. However, the real work was just beginning.

The share swap ratios were carefully calculated to be fair to all shareholders while reflecting the relative strengths of each bank. Under the terms of the merger, Dena Bank and Vijaya Bank shareholders received 110 and 402 equity shares of the Bank of Baroda, respectively, of face value ₹2 for every 1,000 shares they held. These ratios reflected not just the book values but also factors like asset quality, market position, and future potential.

The merger came into effect on 1 April 2019. This date marked the beginning of one of the most complex integration exercises in Indian banking history. The combined entity that emerged was impressive in scale. The amalgamation is the first-ever three-way consolidation of banks in the country, with a combined business of Rs 14.82 trillion (short scale), making it the third largest bank after State Bank of India (SBI) and ICICI Bank.

The human dimension of the merger was enormous. In the present case, post-merger, Bank of Baroda shall become an employer of over 90,000 employees working across 9,500 branches throughout the country. Further, it will also have to integrate data of more than 100 million customers as well. Managing this massive workforce integration while maintaining employee morale and productivity was a herculean task.

The cultural integration posed significant challenges. Each bank had its own organizational culture, work practices, and employee expectations. As part of the alignment, BoB had sent out notices to employees at administrative offices of these two banks that their working hours will change from 10am-5pm to 9am-4pm from 1 May, 2019. "Presently, working hours of administrative offices of Bank of Baroda are 9am to 4pm while that of erstwhile Vijaya Bank and erstwhile Dena Bank are 10am to 5pm. Consequent to amalgamation, it is imperative to bring uniformity in working hours of administrative offices across the bank to ensure smooth integration of the amalgamated entity," the notice had said.

The bank offered voluntary retirement schemes to manage redundancies and provide options for employees who didn't want to continue with the merged entity. According to the second person cited above, employees of these two banks were given the option to either opt for a voluntary retirement (VRS) and retire on 31 March, 2019 or join the merged bank. He said that around 260 employees from Dena Bank chose to retire instead of joining BoB.

The technology integration was one of the most complex aspects of the merger. Three different core banking systems had to be merged, customer data had to be migrated without any loss or disruption, and thousands of ATMs, point-of-sale terminals, and digital banking platforms had to be integrated. The bank took a phased approach to minimize disruption.

The Bank has completed the integration of 1770 erstwhile Dena Bank Branches in December 2020 and had earlier completed the integration of 2128 erstwhile Vijaya Bank Branches in September 2020. This staggered integration allowed the bank to learn from each phase and refine its processes.

The scale of customer account migration was unprecedented in Indian banking. Over 5 crore customer accounts were migrated. Each account had to be carefully mapped, customer credentials verified, and services seamlessly transitioned. The bank invested heavily in customer communication to ensure smooth transition and maintain confidence.

The post-merger integration went beyond just systems and processes. The bank had to rationalize its branch network, eliminating overlaps while ensuring no customer was left underserved. Product portfolios had to be harmonized, with the best products from each bank retained and redundant ones phased out. Credit policies had to be standardized, risk management frameworks integrated, and treasury operations consolidated.

Post the successful integration, all customers now have access to a total of 8248 domestic branches and 10318 ATMs Pan India, which will provide them complete access to the entire suite of products and service offerings of Bank of Baroda. This expanded network created significant convenience for customers, who could now access services from a much larger number of touchpoints.

The financial impact of the merger was substantial. Post-consolidation, Bank of Baroda will have business of around Rs 15.4 trillion and advances and deposits market share of 6.9% and 7.4%, respectively. Further, considering the regional widespread presence of Vijaya Banka and Dena Bank, the Bank of Baroda will have pan India presence.

The bank's leadership, led by MD & CEO Sanjiv Chadha during the crucial integration period, demonstrated remarkable execution capabilities. Shri. Sanjiv Chadha, MD & CEO said, "We are pleased to inform that we have successfully completed fully Integration of erstwhile Banks with Bank of Baroda amidst the challenges faced under the COVID environment. With the successful integration, the Bank is well poised to derive and consolidate the benefits arising from this amalgamation of the three Banks, apart from driving synergies".

The merger also created opportunities for operational efficiency and cost optimization. Duplicate branches were consolidated, back-office operations were centralized, and procurement was leveraged for better pricing. The bank estimated significant cost savings from these synergies, which would improve profitability over time.

The asset quality challenge from Dena Bank's portfolio required careful management. The bank had to provision for the higher NPAs while working on recovery strategies. Special teams were created to focus on recovering bad loans, and the bank leveraged new regulations like the Insolvency and Bankruptcy Code to expedite resolutions.

VII. Digital Transformation & Technology Leadership (2000s–Present)

The digital transformation journey of Bank of Baroda represents one of the most comprehensive technology modernization efforts undertaken by any Indian public sector bank. From its early investments in core banking solutions to its current position as a leader in digital banking innovation, the bank has consistently demonstrated that traditional institutions can successfully reinvent themselves for the digital age.

The foundation for digital transformation was laid in the mid-2000s. Launched Core Banking Solution and Internet Banking · Established India's First SME Loan Factory built around assembly line production principle - An innovative Sales & Delivery Model. The implementation of core banking solution (CBS) was a watershed moment, connecting all branches in real-time and enabling customers to access their accounts from any branch.

A critical infrastructure investment came in 2005. The bank built a Global Data Centre in Mumbai for running its centralized banking solution, providing the backbone for all digital initiatives that would follow. This data center, with its disaster recovery capabilities and high availability architecture, became the nerve center of the bank's technology operations.

The bank's approach to digital transformation was comprehensive and strategic. Rather than treating technology as merely a support function, Bank of Baroda recognized it as a fundamental driver of business transformation. The "Baroda Next" initiative represented this shift in thinking, focusing on next-generation banking technology that would revolutionize customer experience.

The launch of mobile banking marked a crucial milestone in the bank's digital journey. The evolution from basic SMS banking to sophisticated mobile applications reflected the bank's ability to adapt to changing customer preferences. The M-Connect Plus application, which would later evolve into bob World, became a cornerstone of the bank's digital strategy.

The transformation of M-Connect Plus into bob World represented more than just a rebranding—it was a complete reimagining of digital banking. From the Best technology bank 2021*, presenting to you bob World, the official Bank of Baroda's revamped Mobile Banking application erstwhile known as M-Connect Plus. We unveil to you a new world of endless possibilities which has grown from a smaller to a bigger passion encompassing an all new digital experience. The metamorphosis from M-Connect Plus to bob world has been crafted intuitively to provide a fresh look and feel that is so seamless, contactless and effortless.

The bob World platform has achieved remarkable adoption and usage metrics. During FY 2024, the bob World app achieved 28.48 lakh activations, bringing the total to 306 lakh activations, and facilitated 17.09 crore financial and 228.64 crore non-financial transactions. These numbers demonstrate not just adoption but active engagement, with customers using the platform for a wide range of banking needs.

The breadth of services offered through bob World is impressive. bob World is Bank of Baroda's state-of-the-art, feature rich mobile banking application. This app brings 190+ services of banking world at your fingertips - right from simple balance enquiry to cardless cash withdrawal facility. The platform has evolved from basic banking transactions to become a comprehensive financial services ecosystem.

Infrastructure modernization has been crucial to supporting digital initiatives. To further improve connectivity and service quality, the Bank implemented SD-WAN technology across 7,100+ branches, optimized bandwidth usage, and transitioned VSAT branches to MPLS networks where feasible. This network upgrade ensures reliable, high-speed connectivity essential for real-time digital services.

The bank's approach to customer acquisition has been revolutionized through digital channels. Leveraging digital channels like Video Customer Identification Process (VCIP) and TAB mode, the Bank achieved remarkable client acquisition, opening 1,02,299 VCIP SB accounts, 33,799 B3-digital accounts, and 2,44,582 current accounts in FY 2024, with 82.11 percent of these accounts opened through TAB mode. Additionally, 66.92 percent of the 55,93,991 Non-FI Savings Bank accounts were opened digitally.

The integration with government platforms has streamlined business account opening. Integration with the Ministry of Corporate Affairs Portal facilitated the seamless opening of 5,186 current accounts for newly formed companies. This integration demonstrates the bank's ability to leverage ecosystem partnerships for customer convenience.

In 2024, Bank of Baroda made a bold leap into artificial intelligence with the launch of three GenAI-powered solutions. Bank of Baroda (BoB), a public-sector bank, on Tuesday announced the launch of GenAI -powered Virtual Relationship Manager, Aditi, GenAI-enabled knowledge management platform, GyanSahay.AI for its employees, and GenAI chatbot, ADI, for digital customer experience.

The Aditi virtual relationship manager represents a significant innovation in customer service. These human-like interface(https://www.bankofbaroda.in/contact-us/vrm) presented in the form of digital avatars, offer conversational banking across a range of services. Available on the Bank's web portal, the capability supports audio, video, and chat-based assistance, ensuring 24×7 banking services with multilingual support, thereby augmenting the overall customer experience.

GyanSahay.AI addresses the critical challenge of knowledge management in a large organization. In addition to customer-facing innovations, the Bank of Baroda has also launched a GenAI-enabled knowledge management platform, 'GyanSahay.AI' for its employees. Trained in the Bank's product policies and processes, this platform provides employees with instant and accurate answers, enabling them to seamlessly handle customer queries and access key operational details more efficiently. It aids employees to work smarter and faster, ultimately enhancing customer satisfaction and service delivery.

The bank's leadership recognizes the transformative potential of AI. Mr. Debadatta Chand, Managing Director & Chief Executive Officer, Bank of Baroda, said, "We at Bank of Baroda have been closely following the rapid advancement of GenAI and are convinced that it has the power to transform banking operations as we know it today. The Bank will continue to enhance these GenAI use cases with incremental sales and service features driving customer self-service and immediate fulfillment. Additionally, our GenAI enabled knowledge management platform is an endeavor to empower the Bank's large customer facing workforce with the right information on products, policies and processes so that there is improved service delivery".

Security and ethical considerations have been paramount in the digital transformation journey. Executive Director of Bank of Baroda, Sanjay Mudaliar said "While the first set of GenAI use cases are pioneering large scale implementations, the Bank has also setup the necessary technology architecture and guardrails to ensure security and ethical AI".

The bank has also focused on building partnerships with technology firms to accelerate innovation. Partnerships with tech firms like Zopper and Optimum Solution enabled the launch of SmartInsure and SmartInvest, delivering tailored digital insurance and investment solutions. These partnerships allow the bank to quickly deploy new capabilities without having to build everything in-house.

Digital transformation has also extended to internal operations. Project Navoday, with its three pillars of transforming the core business, building next-generation capabilities, and nurturing the organization, represents a holistic approach to modernization. The project encompasses not just technology but also process reengineering, capability building, and cultural transformation.

The bank's investment in analytics and data-driven decision-making has been substantial. Advanced analytics are now used for credit risk assessment, customer segmentation, fraud detection, and personalized product recommendations. The ability to leverage data effectively has become a key competitive advantage.

VIII. Modern Operations & Market Position (2020–Present)

The post-merger Bank of Baroda that emerged in 2020 represents a formidable force in Indian banking, combining scale, reach, and technological sophistication. The successful integration of three banks during a global pandemic demonstrated exceptional operational resilience and management capability, setting the stage for the next phase of growth and transformation.

The current operational footprint of Bank of Baroda is impressive by any measure. The Bank's distribution network includes 8,200+ branches, 10,000+ ATMs, 1,200+ self-service e-lobbies and 20,000 Business Correspondents. The Bank has a significant international presence with a network of 100 branches/offices of subsidiaries, spanning 20 countries. This extensive network provides unparalleled reach and convenience to customers across India and globally.

The bank's business model has evolved to encompass four key segments, each contributing to overall performance. Retail Banking has emerged as the fastest-growing segment, driven by digital acquisition strategies and innovative products. The retail loan book has expanded significantly, with a focus on home loans, auto loans, and personal loans—all supported by digital origination and quick processing.

Corporate Banking remains a cornerstone of the bank's operations, leveraging deep relationships with India's largest companies and growing mid-market enterprises. The bank has developed specialized capabilities in project finance, working capital management, and trade finance. Its international network provides a unique advantage in serving Indian corporates with global operations.

Treasury Operations have become increasingly sophisticated, managing not just the bank's liquidity but also providing complex financial solutions to clients. The treasury team handles foreign exchange trading, interest rate risk management, and investment in government securities, contributing significantly to non-interest income.

The Priority Sector segment, while mandated by regulation, has been transformed into a viable business through innovative approaches. The bank has developed specialized products for agriculture, micro, small and medium enterprises (MSMEs), and other priority sectors, using technology to reduce costs and improve risk assessment.

Wealth management has emerged as a strategic focus area. The bank has recognized the growing affluent segment in India and developed comprehensive wealth management services. From portfolio management to estate planning, the bank now competes with private banks and specialized wealth managers for high-net-worth clients.

The appointment of Sachin Tendulkar as Global Brand Ambassador in 2024 marked a significant step in brand building. Public sector lender Bank of Baroda (BoB) has signed cricketing legend Sachin Tendulkar as the bank's global brand ambassador. The three-year deal involving a strategic partnership between the ace cricketer and the bank was announced ahead of the launch of its first campaign featuring Sachin, called "Play the Masterstroke." The bank has introduced the 'bob Masterstroke Savings Account,' designed especially for clients desiring premium services. BoB said in a statement that Sachin, a Bharat Ratna awardee, will be positioned as brand ambassador, featuring in all the bank's branding campaigns, consumer education and awareness programmes on financial literacy and fraud prevention, as well as customer and employee engagement programmes.

The strategic rationale behind this partnership goes beyond mere celebrity endorsement. Sachin represents the epitome of Leadership, Excellence, Trust, Consistency and a Legacy that transcends generations – values that form the bedrock of Bank of Baroda's century-long journey. The strategic partnership between Sachin Tendulkar and Bank of Baroda is built on a profound alignment of core values like excellence & trust. Bank is proud to have this iconic partnership with Shri Sachin Ramesh Tendulkar as Global Brand Ambassador of Bank of Baroda.

Financial performance in recent years has been strong, validating the merger strategy and operational improvements. The bank has shown consistent profit growth, improving asset quality, and strong capital adequacy ratios. BANK OF BARODA's capital adequacy ratio (CAR) was at 16.3% as on 31 March 2024 as compared to 16.2% a year ago. The net NPA ratio of BANK OF BARODA was 0.7% in financial year 2024. This compared with 0.9% a year ago.

The bank's market position has strengthened considerably. The bank is among India's top five banks by asset size and total deposits with a 6% market share as of FY24. This scale provides significant advantages in terms of operational efficiency, bargaining power with vendors, and ability to invest in technology and innovation.

Government ownership remains a defining characteristic, with implications for both strategy and operations. The Government of India continues to be the largest shareholder, owning approximately 64% of the bank's equity. This provides stability and implicit government backing but also means the bank must balance commercial objectives with policy priorities.

The competitive landscape presents both challenges and opportunities. Private sector banks continue to gain market share with their customer service and innovation, while fintech companies are disrupting traditional banking models. However, Bank of Baroda's scale, trust factor, and improving digital capabilities position it well to compete effectively.

The bank has also focused on building specialized verticals for key customer segments. Bank of Baroda, which has around 165 million customers across 17 countries, established a dedicated Defence Banking Vertical led by a retired Lieutenant General as Chief Defence Banking Advisor, supported by Deputy Advisors at key locations to serve the defence segment effectively. Such specialized approaches help deepen relationships and capture greater wallet share.

Employee engagement and capability building remain priorities. The bank has invested in training programs, leadership development, and creating career paths that motivate and retain talent. The integration of three different organizational cultures into one cohesive unit has been largely successful, though challenges remain in fully harmonizing work practices and mindsets.

The bank's approach to corporate social responsibility reflects its heritage as a nation-building institution. Beyond regulatory requirements, the bank actively participates in financial inclusion initiatives, supports education and healthcare projects, and contributes to environmental sustainability efforts.

Risk management has evolved to address modern challenges. Beyond traditional credit risk, the bank now actively manages operational risk, cyber risk, and reputational risk. The three-way merger provided valuable lessons in integration risk management that have strengthened overall risk capabilities.

IX. Playbook: Business & Investing Lessons

The Bank of Baroda journey offers profound lessons that extend far beyond banking, providing insights into institutional resilience, transformation management, and long-term value creation. These lessons are particularly relevant in an era where businesses must balance stakeholder interests, navigate regulatory complexity, and manage digital disruption.

The "Patient Capital" Approach: Long-term Thinking in a Short-term World

Bank of Baroda's 116-year history demonstrates the power of patient capital and long-term thinking. Unlike quarterly earnings-obsessed institutions, the bank has consistently taken decisions with multi-decade horizons. The international expansion that began in 1953 didn't show significant returns for years but eventually became a crucial differentiator. The investment in technology infrastructure in the 2000s, when many PSU banks hesitated, positioned the bank for digital leadership. This patient approach to capital allocation—whether in branch expansion, technology, or human resources—has created compound value over time. The lesson for modern businesses is clear: while short-term pressures are real, building enduring institutions requires the courage to invest for the long term, even when immediate returns aren't visible.

Managing Complexity: From Princely State Bank to Global Conglomerate

The evolution from a single-state bank to a global financial conglomerate offers masterclasses in complexity management. The bank has successfully navigated multiple transformations: from private to public ownership, from domestic to international operations, from traditional to digital banking, and through numerous mergers and acquisitions. Each transformation added layers of complexity—regulatory, operational, technological, and cultural. The bank's approach has been to build strong foundational systems, invest in middle management capabilities, and maintain clear communication channels across the organization. The ability to manage complexity without losing operational efficiency or customer focus is particularly relevant for modern businesses operating in interconnected, regulated environments.

Merger Integration Excellence: Lessons from the 2019 Amalgamation

The successful integration of Dena Bank and Vijaya Bank provides a textbook case in merger management. The bank's systematic approach—from careful due diligence to phased integration to cultural harmonization—offers valuable lessons. Key success factors included: clear communication to all stakeholders from day one, offering voluntary exit options to manage redundancies compassionately, maintaining service continuity during integration to retain customer confidence, leveraging technology for faster integration while managing risk, and celebrating quick wins while maintaining focus on long-term integration goals. The ability to execute such a complex merger during the COVID-19 pandemic demonstrates that with proper planning and execution, even the most challenging integrations can succeed.

Balancing Social Responsibility with Commercial Objectives

As a public sector bank, Bank of Baroda has masterfully balanced social mandates with commercial viability. The bank has fulfilled priority sector lending requirements, participated in government schemes, and maintained branches in unprofitable locations while still delivering shareholder returns. This balance was achieved through cross-subsidization strategies, innovative approaches to make social banking profitable, leveraging technology to reduce the cost of financial inclusion, and viewing social responsibility as a long-term investment in market development. This approach offers lessons for modern businesses grappling with ESG pressures and stakeholder capitalism.

Technology Adoption in a Traditional Organization

The transformation of a century-old institution into a digital leader offers insights into managing technological change in traditional organizations. The bank's approach included: starting with infrastructure before applications, focusing on employee training and change management, partnering with fintechs rather than viewing them as threats, maintaining legacy systems while building new capabilities, and using technology to enhance rather than replace human interaction. The recent adoption of GenAI shows that age is no barrier to innovation when there's organizational will and systematic execution.

Building Trust Across Cultures and Geographies

Operating successfully across 20 countries requires deep cultural intelligence. Bank of Baroda's international success stems from: hiring local talent while maintaining Indian leadership, adapting products to local needs while maintaining global standards, building relationships with regulators and community leaders, serving diaspora communities while expanding to local customers, and maintaining consistent service quality across diverse markets. These lessons are invaluable for any business pursuing international expansion.

Capital Allocation in a Government-Controlled Entity

Despite government ownership constraints, the bank has demonstrated shrewd capital allocation. Priority decisions have balanced: regulatory requirements with business opportunities, social mandates with profitability targets, technology investments with immediate business needs, geographic expansion with risk management, and shareholder returns with capital conservation. The ability to optimize capital allocation within constraints offers lessons for businesses operating in regulated or restricted environments.

Creating Institutional Memory and Knowledge Management

Over 116 years, the bank has built tremendous institutional knowledge. The recent implementation of GyanSahay.AI represents a modern approach to capturing and disseminating this knowledge. Key lessons include: documenting not just policies but also tacit knowledge, creating systems for knowledge transfer across generations, using technology to democratize access to expertise, building learning cultures that value experience while embracing change, and maintaining historical perspective while driving innovation.

Managing Stakeholder Relationships

The bank's success in managing diverse stakeholders—government, regulators, employees, unions, customers, and shareholders—provides valuable lessons. Strategies have included: transparent communication even when delivering difficult messages, building coalition support for major initiatives, balancing competing interests through creative solutions, maintaining independence while respecting ownership structures, and building trust through consistent delivery over time.

Risk Management Evolution

From surviving the 1913-1917 banking crisis to managing modern cyber risks, the bank's risk management evolution offers important lessons: building risk management into business processes rather than treating it as a separate function, learning from crises to strengthen systems, balancing risk-taking with prudence, diversifying risks across geographies and businesses, and investing in risk management capabilities before crises hit. The bank's relatively strong asset quality compared to peers validates this approach.

X. Analysis & Bear vs. Bull Case

The investment case for Bank of Baroda presents a fascinating study in contrasts, with compelling arguments on both sides reflecting the complex dynamics of Indian public sector banking in an era of rapid technological and economic change.

Bull Case: The Optimistic Perspective

The scale advantages achieved post-merger cannot be overstated. With assets exceeding ₹14.82 trillion and a network spanning 8,200+ branches, Bank of Baroda enjoys economies of scale that few Indian banks can match. This scale translates into lower per-unit costs, stronger negotiating power with vendors and partners, and the ability to invest in technology and innovation that smaller banks cannot afford. The bank's 6% market share in deposits provides a stable, low-cost funding base crucial for maintaining healthy net interest margins.

The government backing provides an implicit guarantee that significantly reduces perceived risk. With the Government of India owning 64% of equity, depositors and creditors have confidence that the bank will receive support during stress periods. This "too big to fail" status provides competitive advantages in attracting deposits, particularly from risk-averse savers who form the backbone of India's deposit base. During times of financial stress, flight-to-safety behaviors often benefit large PSU banks at the expense of smaller private players.

The international presence spanning 20 countries is a unique differentiator. Few Indian banks have Bank of Baroda's global footprint and experience in international banking. This network provides multiple revenue streams, natural hedging against domestic economic cycles, and the ability to serve Indian corporates expanding globally. As Indian businesses increasingly go global and the Indian diaspora grows, this international network becomes increasingly valuable.

The digital transformation momentum is particularly impressive for a public sector bank. With 306 lakh bob World app activations and 82% of new accounts opened digitally, the bank has demonstrated that traditional institutions can successfully compete in digital banking. The recent GenAI implementations show continued innovation leadership. The combination of digital capabilities with physical presence creates an omnichannel advantage that pure digital players cannot replicate.

Rural and semi-urban market dominance provides a moat that's difficult for private banks to replicate. With decades of presence in these markets, deep customer relationships, and understanding of local dynamics, Bank of Baroda has built trust that cannot be easily displaced. As rural India's economy grows and digitalizes, this embedded presence becomes increasingly valuable. The bank is well-positioned to capture the financial services opportunity in India's next billion consumers.

The improving asset quality trajectory validates management's execution capabilities. With net NPAs at 0.7% in FY24, down from 0.9% a year ago, the bank has demonstrated effective risk management and recovery capabilities. The successful absorption of Dena Bank's troubled assets while improving overall asset quality shows sophisticated credit management capabilities.

Bear Case: The Skeptical View

The PSU bank inefficiencies and bureaucracy remain structural challenges. Government ownership brings political interference in lending decisions, constraints on executive compensation that make talent retention difficult, and bureaucratic decision-making that slows innovation. The requirement to participate in government schemes, regardless of commercial viability, can impact profitability. Labor unions' resistance to change can impede necessary restructuring and efficiency improvements.

Competition from nimble private banks and fintechs is intensifying. Private banks like HDFC and ICICI continue to gain market share with superior customer service and innovation. Fintech companies are unbundling banking, cherry-picking profitable segments like payments and lending while avoiding regulatory burdens. New-age digital banks are attracting younger customers with user-friendly interfaces and innovative products. The bank's size and government ownership make it difficult to match the agility of these competitors.

Asset quality concerns persist despite recent improvements. The bank's exposure to stressed sectors like infrastructure and power remains significant. The true extent of COVID-19's impact on asset quality may not be fully visible yet. Priority sector lending requirements force exposure to inherently riskier segments. The integration of Dena Bank's weak assets could still create future problems if economic conditions deteriorate.

Government interference in decision-making remains a significant risk. Political pressures for loan melas and debt waivers can impact asset quality. Forced mergers with weaker banks, as happened with Dena Bank, can destroy value. Constraints on branch rationalization and staff reduction limit operational efficiency. The inability to freely price products and services based on market conditions impacts profitability.

Talent retention challenges are becoming acute. The bank cannot match private sector compensation, particularly for specialized roles in technology and risk management. Younger talent increasingly prefers private banks and fintechs with their entrepreneurial cultures. The hierarchical, seniority-based promotion system frustrates high performers. Brain drain to private sector reduces institutional capabilities over time.

The technology debt from legacy systems remains substantial. Despite digital progress, core systems are still antiquated compared to new-age banks. The cost and complexity of modernizing legacy infrastructure are enormous. Integration challenges from multiple mergers have created technical complexity. Cybersecurity risks are elevated due to aging infrastructure and the large attack surface.

Balanced Assessment

The reality likely lies between these extremes. Bank of Baroda possesses genuine competitive advantages—scale, trust, international presence, and improving digital capabilities. The successful merger integration and digital transformation demonstrate execution capabilities often underestimated in PSU banks. However, structural challenges from government ownership, intensifying competition, and legacy burdens are equally real.

The bank's future likely depends on its ability to leverage strengths while addressing weaknesses. This means accelerating digital transformation while maintaining the human touch valued by traditional customers, improving operational efficiency within government ownership constraints, attracting and retaining talent through non-monetary incentives and culture, managing asset quality through economic cycles, and balancing social responsibilities with commercial objectives.

The investment case ultimately depends on one's view of India's economic trajectory and the role of public sector banks within it. Bulls see Bank of Baroda as a play on India's economic growth, financial inclusion, and the modernization of public sector banking. Bears see structural challenges that cannot be overcome regardless of management efforts. The truth, as often happens, likely involves elements of both narratives.

XI. Epilogue & "If We Were CEOs"

Standing at the helm of Bank of Baroda today would mean commanding one of India's most storied financial institutions at a crucial inflection point. The next decade will determine whether this 116-year-old institution remains relevant in an age of digital disruption, or becomes another casualty of technological change. If we were CEOs, here's how we would navigate these turbulent waters.

Strategic Priorities for the Next Decade

The first priority would be completing the digital transformation—not as a technology project, but as a fundamental business model reinvention. This means moving beyond digitizing existing processes to reimagining banking from first principles. We would create a separate digital bank within the bank, free from legacy constraints, to compete directly with neobanks. This "Bank of Baroda Neo" would have its own technology stack, agile culture, and innovation mandate, while leveraging the parent's trust and capital.

The second strategic imperative would be talent transformation. We would launch "Project Phoenix"—a comprehensive program to rebuild the bank's human capital. This would include recruiting top technology and data science talent through market-competitive compensation structures (working within government constraints through performance bonuses and ESOPs where possible), creating a parallel career track for specialists that doesn't require them to become generalist managers, establishing innovation labs in tech hubs like Bangalore and Hyderabad to tap into India's tech talent, and partnering with premier institutions for continuous leadership development.

The third priority would be portfolio optimization. We would conduct a zero-based review of all business lines, branches, and products. Unprofitable branches would be converted to digital service points. Non-core businesses would be divested or shut down. Resources would be reallocated to high-growth, high-return areas like wealth management, transaction banking, and digital lending.

Navigating the Fintech Disruption

Rather than viewing fintechs as threats, we would embrace them as partners and teachers. We would launch a ₹1,000 crore fintech investment fund to take strategic stakes in promising startups, create an accelerator program to incubate fintech solutions for specific banking challenges, establish API banking infrastructure to enable seamless fintech partnerships, and acquire select fintechs to rapidly build capabilities in areas like digital lending and wealth management.

We would also create an internal fintech—a separate subsidiary with startup culture and compensation—to build innovative solutions that could be white-labeled to other banks. This would transform Bank of Baroda from just a bank to a banking technology provider.

International Expansion Opportunities

The international strategy would shift from following the diaspora to building a global digital bank. We would leverage India's UPI success to build payment solutions for emerging markets, create digital banking platforms for countries with underdeveloped financial systems, and position Bank of Baroda as the gateway bank for businesses trading with India.

Specific opportunities would include expanding in Africa through mobile-first banking solutions, building trade finance platforms connecting India with Southeast Asia and Africa, creating specialized NRI banking solutions that go beyond basic remittances, and establishing innovation centers in global tech hubs to access talent and ideas.

Building a Performance Culture in a PSU

Cultural transformation would be the hardest but most important challenge. We would implement "Mission 2030"—a cultural transformation program with clear, measurable goals. This would include introducing objective performance metrics tied to customer satisfaction and digital adoption, creating internal competition through gamification and recognition programs, establishing innovation time (like Google's 20% time) for employees to work on new ideas, and breaking down hierarchical barriers through cross-functional teams and reverse mentoring.

We would also reshape the narrative around public sector banking—from a job to a mission of nation-building through financial inclusion and innovation. This purpose-driven approach would attract idealistic young talent who want to make a difference.

The Role of Public Sector Banks in India's Growth Story

We would redefine Bank of Baroda's role from being just a commercial bank to being a catalyst for India's economic transformation. This means becoming the primary banker for India's transition to renewable energy, supporting the formalization of the informal economy through digital solutions, financing the infrastructure needed for India's manufacturing ambitions, and enabling financial inclusion through innovative products for the next billion users.

We would position the bank as a "development bank with commercial principles"—pursuing profits while catalyzing economic development. This unique positioning would differentiate us from both private banks (purely commercial) and traditional PSU banks (often uncommercial).

Technology and Innovation Roadmap

The technology strategy would be radical: we would announce a plan to shut down all physical branches by 2035, replacing them with digital channels and partnership networks. This would force digital transformation while giving sufficient time for customer transition. We would build India's first fully AI-powered bank where AI handles all routine decisions and humans focus on complex, high-value interactions, implement blockchain for trade finance and cross-border payments, create voice-first banking for India's vernacular speakers, and pioneer quantum-resistant security systems preparing for the post-quantum era.

Risk Management in a New Era

Modern risk management would go beyond credit risk to encompass cyber risk, climate risk, and model risk from AI systems. We would establish a "Risk Innovation Lab" to simulate emerging risks and develop mitigation strategies, implement real-time risk monitoring using AI and alternative data, create scenario planning capabilities for black swan events, and build resilience through diversification across geographies, sectors, and products.

Stakeholder Management

Managing government expectations while pursuing commercial objectives would require sophisticated stakeholder management. We would propose a "performance contract" with the government clearly defining social and commercial objectives, create transparent reporting on both financial and social impact metrics, build coalition support for necessary reforms through industry associations, and demonstrate that commercial success and social impact are not mutually exclusive.

The Path Forward

If we were CEOs, we would set an audacious goal: make Bank of Baroda one of the world's top 50 banks by market capitalization by 2035. This would require growing profits at 15% annually, achieving return on assets above 1.5%, maintaining asset quality with net NPAs below 0.5%, and building a market capitalization exceeding $50 billion.

The path would be challenging, requiring navigation through government constraints, union resistance, technological disruption, and intense competition. But the opportunity is equally massive—serving India's growth story, leveraging digital to leapfrog traditional banking models, and building a global Indian financial champion.

The story of Bank of Baroda over the next decade will be written by bold decisions made today. The institution has survived and thrived through colonialism, independence, nationalization, and liberalization. With the right vision, strategy, and execution, it can master the digital age too, emerging as a model for how traditional institutions can reinvent themselves for the future.

The question isn't whether Bank of Baroda can transform—its history proves its adaptability. The question is whether it will have the leadership courage to make the bold moves necessary for transformation. If we were CEOs, we would bet on transformation, knowing that the alternative—gradual irrelevance—is far riskier than bold change.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube