Jupiter Life Line Hospitals: Building India's Healthcare Infrastructure

I. Introduction & Episode Thesis

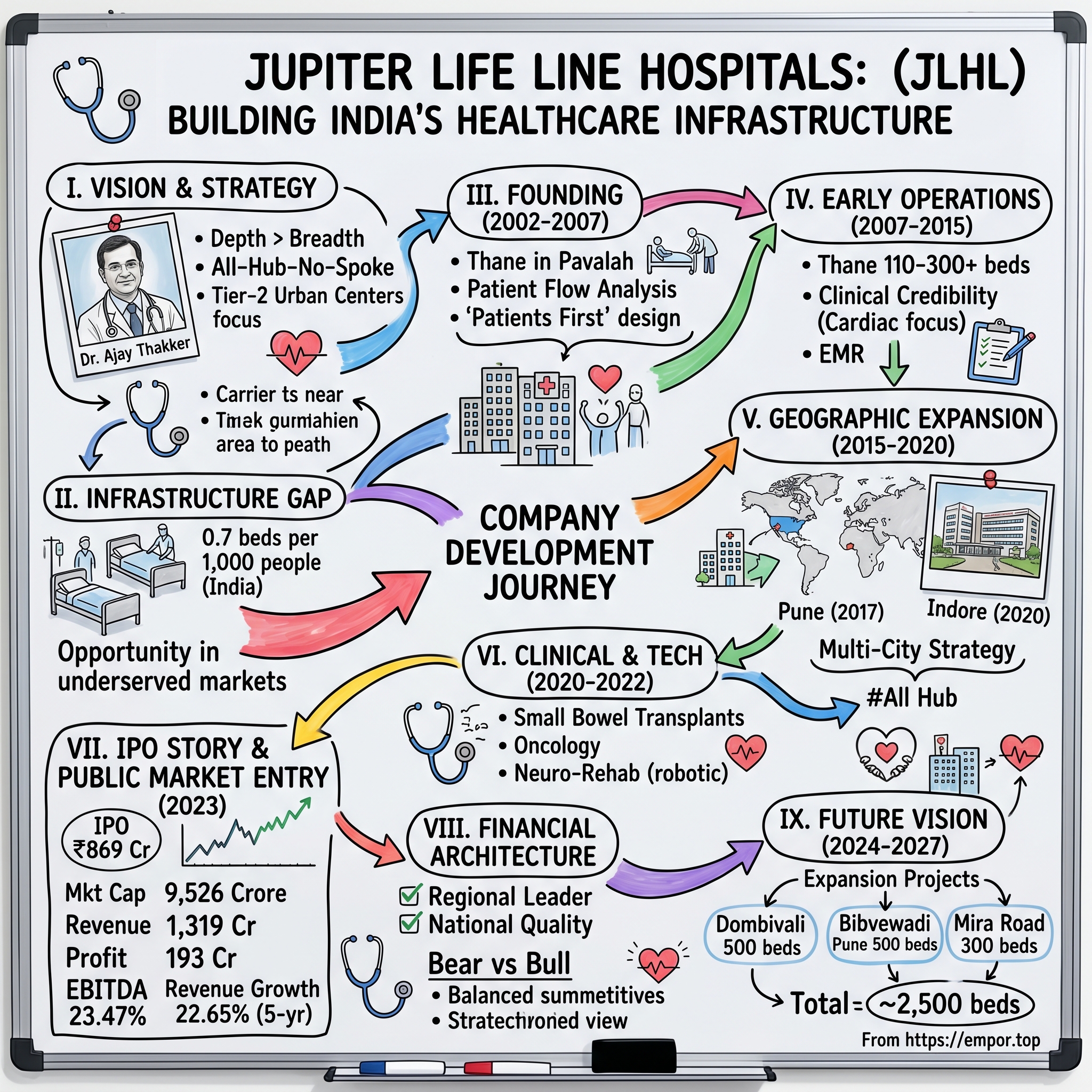

The fluorescent lights of Jupiter Hospital's emergency room in Thane never switch off. At 2 AM on a humid Mumbai night in 2007, Dr. Ajay Thakker walked through the corridors of his newly opened 110-bed facility, checking on patients, adjusting equipment, obsessing over details that larger hospital chains might delegate to operations managers. This wasn't just another hospital launch—it was the manifestation of a five-year preparation, a bet that India's healthcare infrastructure needed a different model: not the hub-and-spoke efficiency of Apollo, not the premium positioning of Fortis, but something uniquely calibrated for the dense, aspirational populations of India's tier-2 urban centers.

Today, seventeen years later, Jupiter Life Line Hospitals Limited commands a ₹9,500 crore market capitalization, operates 1,061 beds across three cities, and has treated over 750,000 patients. The company that started with a single hospital in Thane—Mumbai's often-overlooked satellite city—now runs facilities in Pune and Indore, with ambitious expansion plans that could more than double its capacity by 2027.

But here's what makes Jupiter fascinating for students of business strategy: while national giants like Apollo and Fortis pursued aggressive pan-India expansion, Jupiter chose depth over breadth, betting that Western India's unique demographics—high population density, rising incomes, severe infrastructure gaps—created a defensible regional moat. The company's "all-hub-no-spoke" model, where each hospital operates as a full-service tertiary care center rather than a feeder to a flagship facility, reflects a contrarian view on healthcare delivery.

The numbers tell a compelling story: revenue has grown at 22.65% annually over the past five years, nearly double the industry average of 12.93%. EBITDA margins hover around 23-24%, impressive for a capital-intensive business competing against both established nationals and nimble regional players. The stock has doubled from its September 2023 IPO price of ₹735 to current levels around ₹1,450.

Yet Jupiter's journey raises fundamental questions about healthcare infrastructure in emerging markets. Can regional focus triumph over national scale? How does a healthcare provider balance the contradictions of Indian healthcare—world-class clinical capabilities serving a price-sensitive market? And most intriguingly: in a sector where trust takes decades to build but seconds to destroy, how did a relatively young hospital group convince patients to choose them over century-old institutions?

This is the story of how Jupiter Life Line Hospitals transformed from a single hospital in Thane into Western India's emerging healthcare powerhouse—a tale of calculated bets, operational excellence, and the peculiar dynamics of building critical infrastructure in the world's most populous nation.

II. The Healthcare Context & India's Infrastructure Gap

Picture this: India has 0.7 hospital beds per 1,000 people. Japan has 13. The United States has 2.9. Even China manages 4.3. For a nation of 1.4 billion people, this isn't just a statistic—it's a humanitarian crisis playing out in slow motion, where families camp outside government hospitals for days hoping for admission, where private healthcare remains a luxury for most, and where a medical emergency can instantly transform middle-class families into poverty statistics.

The Mumbai Metropolitan Region, home to over 25 million people, embodies these contradictions at their sharpest. Here, gleaming towers housing global banks stand alongside sprawling slums. Tech workers earning Silicon Valley salaries live kilometers away from daily wage laborers. The region generates nearly 5% of India's GDP, yet its public healthcare infrastructure remains woefully inadequate. Private hospitals have emerged to fill this gap, but they've created their own paradox: world-class facilities that most residents can't afford.

This was the landscape Dr. Ajay Thakker surveyed in 2002. The post-liberalization boom had created India's first genuine middle class—families with stable incomes, health insurance coverage through employers, and aspirations for quality healthcare. Yet the supply side hadn't kept pace. Apollo Hospitals, founded in 1983, had proven that private healthcare could work in India, but their focus on metro cities and premium positioning left vast swathes of the market underserved.

The tiered nature of Indian healthcare added another layer of complexity. Primary care happens at neighborhood clinics. Secondary care—routine surgeries, basic specializations—occurs at nursing homes and small hospitals. But tertiary and quaternary care—complex cardiac procedures, neurosurgery, organ transplants—remained concentrated in a handful of institutions in major cities. Patients from Thane, Pune, or Indore requiring sophisticated treatment had to travel to Mumbai or Delhi, adding cost, complexity, and often fatal delays to their care. The statistics are stark: India currently has just 0.79 government hospital beds per 1,000 population—far below the two beds per 1,000 population recommended by the National Health Policy 2017 and the global average of 2.7 beds per 1,000 population. When including private healthcare, India's current hospital bed-to-population ratio stands at 1.3 beds per 1,000 people, with the country short by approximately 2.4 million hospital beds.

The competitive landscape in 2007 resembled a chess board with clear territories. Apollo Hospitals, with its 25-year head start, dominated South India and maintained flagship facilities in metros. Fortis Healthcare, backed by the Singh brothers' pharmaceutical fortune, was aggressively expanding through acquisitions. Max Healthcare focused on North India, particularly Delhi-NCR. Regional players like Narayana Health in Karnataka and Ruby Hall Clinic in Pune controlled local markets through deep community ties.

But Western India presented unique opportunities. Maharashtra alone accounts for 13% of India's GDP, hosts the financial capital Mumbai, and contains multiple tier-2 cities with populations exceeding 3 million. The state's relatively high insurance penetration—driven by Mumbai's corporate sector—created a paying customer base. Yet outside South Mumbai's premium facilities, quality tertiary care remained scarce.

The insurance revolution quietly reshaping Indian healthcare added another dimension. Between 2000 and 2010, health insurance coverage expanded from virtually zero to covering nearly 200 million Indians through various schemes. Corporate employees expected cashless hospitalization. Government schemes like RSBY (Rashtriya Swasthya Bima Yojana) began covering below-poverty-line families. This wasn't just about ability to pay—it fundamentally changed how hospitals could plan capacity, invest in equipment, and project revenues.

Technology evolution played its part too. Medical equipment that cost millions of dollars in the 1990s became accessible at fraction of the price by 2007. Indian doctors trained at premier institutions like AIIMS, many with international experience, were returning home, drawn by entrepreneurial opportunities and lifestyle considerations. The ingredients for a healthcare infrastructure boom were aligning.

Yet challenges remained formidable. Healthcare is perhaps India's most regulated sector after banking. Hospitals need dozens of licenses—from local municipal corporations, state health departments, pollution control boards, fire departments, atomic energy commissions (for radiation equipment). Land acquisition in urban areas consumed massive capital. Building trust in a new hospital brand could take years, while a single medical negligence case could destroy reputation overnight.

This complex matrix of opportunity and challenge would shape Jupiter's strategy: instead of competing head-on with established nationals, they would build deep roots in underserved urban markets, focusing on clinical excellence over geographic spread, creating what Dr. Thakker would later call "centers of healing, not just hospitals."

III. The Founding Story: Dr. Ajay Thakker's Vision (2002-2007)

The conference room at the Registrar of Companies office in Mumbai was unremarkable—government-issue furniture, fluorescent lighting, the November heat of 2002 barely held at bay by a struggling air conditioner. But for Dr. Ajay Thakker, receiving the Certificate of Incorporation for Jupiter Life Line Hospitals Limited on November 18, 2002, represented the culmination of years of planning and the beginning of an even longer journey.

Dr. Thakker wasn't your typical hospital entrepreneur. Unlike the cardiologists who founded Apollo or the pharmaceutical magnates behind Fortis, Thakker came from the operational side of healthcare. He had spent years observing the inefficiencies, the gaps between capability and delivery, the thousands of small decisions that determined whether a hospital saved lives or merely processed patients. His vision wasn't revolutionary—it was evolutionary, grounded in the belief that Indian healthcare needed better execution more than grand innovation.

The five years between incorporation and the first hospital's opening in 2007 reveal the methodical nature of Jupiter's approach. While competitors rushed to announce new facilities and capture headlines, Thakker's team focused on foundational elements that would later become competitive advantages. They studied patient flow patterns in Western India, analyzing where people traveled for tertiary care, which procedures they sought, and crucially, what made them choose one hospital over another.

The philosophy that would define Jupiter crystallized during these preparation years: "patients first in everything we do." This wasn't marketing speak—it translated into specific operational decisions. While other hospitals maximized bed density to improve per-square-foot economics, Jupiter planned wider corridors for patient comfort. When designing ICUs, they prioritized sight lines that allowed nurses to monitor multiple patients simultaneously, even if it meant fewer total beds.

Capital raising proved challenging. Healthcare infrastructure requires massive upfront investment with long gestation periods—a tough sell to investors accustomed to software's quick returns or retail's predictable cash flows. Banks remained skeptical of hospital ventures after several high-profile failures in the late 1990s. Private equity was still nascent in Indian healthcare. Thakker cobbled together funding from multiple sources: personal savings, loans against property, investments from doctors who would later join as consultants, and strategic partners who understood the long-term thesis.

The decision to locate the first hospital in Thane rather than Mumbai proper seemed counterintuitive. Mumbai real estate commanded premium valuations, attracted the best medical talent, and housed patients with the highest paying capacity. But Thakker saw what others missed: Thane's population of 1.8 million was larger than most state capitals, yet it lacked a single tertiary care facility of scale. Residents traveled to Mumbai for anything beyond basic surgery, adding cost and complexity to their healthcare journey. More critically, Thane's population according to the 2011 census was 1,886,941, but in 2007, it was already approaching 1.5 million—a massive, underserved market on Mumbai's doorstep. The satellite city offered lower real estate costs, easier regulatory navigation (being outside Mumbai's complex municipal structure), and paradoxically, less competition from established players who viewed it as peripheral.

Building the founding team required a delicate balance. Dr. Thakker needed senior doctors with established reputations to provide clinical credibility, but also young specialists hungry to build something new. The recruitment pitch was unconventional: join not for immediate monetary rewards (which Jupiter couldn't match against established hospitals) but for the opportunity to shape departments from scratch, to implement best practices without legacy constraints, to be part of building an institution.

The technology decisions made during this period would prove prescient. While competitors debated digital investments, Jupiter committed to electronic medical records from day one—unusual for Indian hospitals in 2007. They invested in a biomedical department, becoming one of the few hospitals to have full in-house equipment maintenance capabilities. This wasn't just about cost savings; it was about ensuring that a CT scanner breakdown wouldn't force patient transfers to Mumbai.

Regulatory approvals consumed enormous energy. Healthcare in Maharashtra requires clearances from multiple authorities: clinical establishment registration, biomedical waste management authorization, fire safety certificates, radiation safety permits for imaging equipment. Each approval involved multiple visits, documentation, follow-ups. Dr. Thakker personally managed much of this process, understanding that regulatory compliance would be crucial for long-term sustainability.

The financial structure evolved through trial and error. Initial plans for venture capital funding fell through—investors couldn't understand why building one hospital would take five years. Bank loans required personal guarantees that put founders' assets at risk. Eventually, Jupiter adopted a hybrid model: term loans for infrastructure, working capital facilities for operations, and strategic investments from doctor-partners who brought both capital and clinical expertise.

By late 2006, construction was underway on the Thane facility. The 110-bed hospital might seem modest compared to Apollo's 500-bed flagships, but every design element reflected careful thought. Wide corridors accommodated Indian families' tendency to accompany patients in large numbers. The emergency department sat adjacent to the main road for quick access. Operating theaters were oversized to accommodate teaching and observation—Jupiter planned to be an academic center from inception.

As 2007 approached, with concrete structures rising and equipment being installed, Dr. Thakker's five-year preparation was about to be tested. The question wasn't whether Thane needed a tertiary care hospital—that was obvious. The question was whether patients would trust a new institution with their lives, whether doctors would stake their reputations on an unproven platform, whether Jupiter could deliver on its "patient first" promise when the first ambulance arrived at their emergency room door.

IV. Building the First Hospital & Early Operations (2007-2015)

The first patient arrived at Jupiter Hospital Thane at 6:47 AM on opening day in 2007—a construction worker who had fallen from scaffolding, rushed in by colleagues who didn't know where else to go. The emergency team's response would set the template for Jupiter's operational philosophy: stabilize first, paperwork later. The worker received immediate treatment, surgery within hours, and a payment plan that acknowledged his daily-wage reality. Word spread through Thane's construction sites that the new hospital didn't turn away emergencies over payment concerns.

Those early months tested every assumption. The 110 beds filled quickly, but not with the planned mix of cases. Instead of complex cardiac procedures and neurosurgeries that generated higher revenues, Jupiter saw diabetes complications, road accidents, pregnancy-related emergencies—the real health burden of urban India. Dr. Thakker made a crucial decision: rather than cherry-pick profitable cases, Jupiter would serve the community's actual needs while gradually building capabilities for specialized care.

The "patient first" philosophy translated into hundreds of operational decisions. When families complained about visiting hour restrictions—standard practice at most hospitals—Jupiter extended them, training staff to work around family presence rather than excluding it. When patients struggled with discharge summaries written in medical jargon, Jupiter pioneered simplified, vernacular documentation. These seem like small changes, but in Indian healthcare, where patients often feel processed rather than cared for, they created powerful differentiation.

Building clinical credibility required strategic focus. Rather than attempting everything, Jupiter concentrated on a few specialties where they could excel. Cardiac care became the first center of excellence. In 2011, Jupiter inaugurated a specialized cardiac unit with catheterization labs, cardiac ICUs, and a dedicated surgical team. The investment was massive for a hospital generating limited cash flow, but the logic was clear: cardiac disease was exploding in urban India, and establishing expertise in heart care would create a reputation halo effect across all specialties.

The cardiac bet paid off faster than expected. By 2012, Jupiter was performing complex procedures—bypass surgeries, valve replacements, pediatric cardiac interventions—that most hospitals outside major metros couldn't attempt. Patients began traveling from across Maharashtra, even neighboring states, specifically for cardiac care. The ARPOB (Average Revenue Per Occupied Bed) for cardiac patients was nearly double the hospital average, validating the specialized focus strategy.

Technology investments during this period reflected both ambition and pragmatism. Jupiter couldn't afford the latest MRI machines or robotic surgery systems that Apollo showcased, but they invested strategically in equipment that would differentiate their care. The neuro-rehabilitation center, established in 2013, represented this approach perfectly. Rather than competing in acute neurosurgery, Jupiter built South Asia's first Neuro Rehab Centre, spread over 2000 sq. ft. with all the advanced rehabilitation technologies. This served patients after strokes or accidents—a massive, underserved need requiring specialized equipment and expertise but less capital than acute care.

The biomedical department decision proved prescient. While other hospitals faced equipment downtime waiting for vendor technicians, Jupiter's in-house team ensured near-100% uptime for critical equipment. This reliability became a selling point for doctors considering joining Jupiter—they knew their surgeries wouldn't be canceled due to equipment failures.

Financial management during these early years resembled a high-wire act. Hospital economics are brutal: high fixed costs (salaries, equipment EMIs, facility maintenance) against variable revenues dependent on patient flow. Occupancy below 60% meant losses; above 70% generated decent margins. Jupiter oscillated between 55% and 75% occupancy in those early years, with seasonal variations (lower during monsoons, higher in winter) adding complexity.

The 2008 global financial crisis hit just as Jupiter was gaining momentum. Corporate health insurance claims slowed, patients deferred elective procedures, and banks tightened lending. Jupiter responded by introducing innovative payment schemes: interest-free EMIs for procedures, package pricing for common surgeries, partnerships with employers for employee health programs. These innovations, born from necessity, later became competitive advantages.

Human capital emerged as the crucial differentiator. Dr. Thakker personally interviewed every senior doctor, looking beyond credentials for alignment with Jupiter's values. The nursing staff underwent six-month training programs, unusual in India where nurses often receive minimal orientation. Jupiter introduced performance bonuses for entire departments rather than individuals, fostering collaboration over competition.

By 2015, the Thane hospital had grown from 110 to over 300 beds through phased expansion. Occupancy stabilized around 72%, ARPOB exceeded ₹35,000, and most importantly, clinical outcomes matched or exceeded national benchmarks. Jupiter had successfully performed its first kidney transplant in 2014, a milestone requiring sophisticated coordination between multiple departments. The hospital was profitable, generating cash for expansion, and most critically, had built a reputation that would support geographic growth.

The foundation was set, but Dr. Thakker understood that single-hospital economics would never achieve his vision of transforming Western India's healthcare infrastructure. The next phase would test whether Jupiter's model could replicate, whether the culture could scale, whether the "patient first" philosophy would survive the pressures of rapid expansion.

V. Geographic Expansion: The Multi-City Strategy (2015-2020)

The boardroom presentation in early 2015 sparked heated debate. Dr. Thakker proposed not one but two new hospitals—Pune and Indore—requiring over ₹800 crore in capital. Board members, including several doctor-investors who had seen single hospitals consume founders, questioned the aggressive timeline. Why not consolidate Thane's success first? Why venture outside Maharashtra when the state itself offered numerous expansion opportunities? Dr. Thakker's response revealed the strategic thinking that would define Jupiter's next phase: "We're not building hospitals, we're building healthcare infrastructure. And infrastructure requires scale."

The Pune decision seemed obvious on paper. Pune operational since 2017, 375 beds, Maharashtra's second-largest city, educational hub, IT capital with young, insured populations—the demographics screamed opportunity. But Pune also hosted Ruby Hall Clinic, Sahyadri Hospitals, and other entrenched players with decades-old relationships. Jupiter's entry strategy reflected lessons from Thane: rather than competing head-on in central Pune, they chose a location in the developing periphery where the city was expanding, where new residential complexes housed middle-class families underserved by existing healthcare infrastructure.

The Pune hospital construction revealed Jupiter's evolved operational model. Unlike Thane's phased, organic growth, Pune was planned as a 300+ bed facility from day one. Every department—emergency, ICU, operation theaters, diagnostics—was sized for optimal efficiency at 70% occupancy. The layout incorporated eight years of Thane learnings: wider nursing stations for better patient monitoring, dedicated family waiting areas to manage India's extended-family dynamics, modular ICUs that could flex between general and specialized care based on demand.

Simultaneously, Jupiter made a bolder bet: Indore. Indore operational since 2020, 231 beds. If Pune tested Jupiter's ability to compete in a saturated market, Indore examined whether their model could work outside Maharashtra's relatively developed healthcare ecosystem. Madhya Pradesh's largest city, Indore had 2 million residents but limited tertiary care infrastructure. Patients routinely traveled to Mumbai or Delhi for complex procedures. The opportunity was massive, but so were the challenges: different regulatory environment, distinct cultural expectations, limited local medical talent pool.

The "all-hub-no-spoke" model that emerged during this expansion phase differentiated Jupiter from competitors' hub-and-spoke strategies. While Apollo or Fortis might build a flagship hospital surrounded by smaller feeder clinics, Jupiter built each facility as a comprehensive tertiary care center. The Pune hospital wasn't a satellite of Thane; it was a complete hospital with its own cardiac unit, neurology department, cancer center. This required higher capital investment but created stronger local brand presence and avoided the patient shuttle logistics that plagued hub-and-spoke models.

Operational challenges multiplied with geographic spread. Maintaining consistent quality across locations required systematic processes that Jupiter had previously managed through Dr. Thakker's personal oversight. They invested heavily in standard operating procedures (SOPs), clinical protocols, and technology systems that could ensure a patient in Indore received the same care quality as one in Thane. Video conferencing connected ICUs across hospitals, allowing Thane specialists to consult on Indore cases in real-time.

The human capital challenge proved most acute. Pune had adequate medical talent, but convincing specialists to join a new hospital over established institutions required creative approaches. Jupiter offered partnership models where senior doctors received equity stakes in the Pune facility, aligning their interests with the hospital's success. They funded international training programs, conference attendance, and research projects—benefits that established hospitals often restricted to very senior staff.

Indore presented different challenges. The local medical talent pool was limited, requiring Jupiter to relocate doctors from Maharashtra. But asking Mumbai-trained specialists to move to Indore—perceived as a tier-2 city—required substantial incentives. Jupiter created a rotation program where doctors spent time across all three hospitals, positioning Indore assignments as career development rather than exile. They built residential complexes, ensured quality schools for doctors' children, and created a professional ecosystem that made relocation palatable.

Financial engineering became increasingly sophisticated during this phase. Each hospital was structured as a separate entity under the parent company, allowing focused performance tracking and location-specific financing. Jupiter tapped diverse funding sources: term loans from banks familiar with their Thane track record, equipment financing from medical device companies eager for new accounts, and working capital facilities structured around insurance receivables.

The insurance payor mix evolution during this period proved crucial. In 2015, Thane's revenue was 60% cash, 30% insurance, 10% government schemes. By 2020, insurance had grown to 45-50% across all facilities. This wasn't just about payment security; insurance relationships drove patient volumes through network effects. Being empaneled with major insurers meant corporate employees chose Jupiter by default, creating predictable patient flow.

Technology investments accelerated, but with careful prioritization. While competitors showcased robotic surgery systems, Jupiter focused on technologies with broader impact. They implemented integrated Hospital Information Systems (HIS) connecting all three facilities, enabling seamless patient transfers and unified medical records. They invested in tele-radiology, allowing expert radiologists in Thane to read scans from Indore within minutes. These weren't headline-grabbing innovations, but they meaningfully improved patient outcomes.

By early 2020, the expansion results were mixed but promising. Pune's average occupancy rate of 67.0%, and ARPOB of ₹55,000 showed strong performance for a three-year-old facility. Indore's average occupancy rate of 59.0%, and ARPOB of ₹44,700 reflected both the challenges of a new market and the opportunity for growth. Combined, Jupiter now operated over 900 beds, employed more than 5,000 people, and had treated over 500,000 patients.

Then COVID-19 arrived, transforming every assumption about healthcare delivery, hospital economics, and expansion strategies. But that crisis would also demonstrate the resilience of Jupiter's distributed model and accelerate changes that might have taken years to implement.

VI. Clinical Excellence & Technology Leadership

The heart transplant surgery at Jupiter Thane in 2022 lasted fourteen hours. The patient, a 42-year-old schoolteacher from Nashik, had been rejected by three Mumbai hospitals as too high-risk. The surgical team, led by a cardiac surgeon who had trained at Cleveland Clinic but chose Jupiter over more prestigious options, worked through the night. When the patient walked out six weeks later, word spread through medical circles: Jupiter wasn't just running hospitals, they were pushing clinical boundaries.

This commitment to clinical excellence hadn't emerged overnight. It grew from a deliberate strategy that began in 2011 with that first cardiac unit, evolved through systematic capability building, and culminated in Jupiter performing procedures that many hospitals twice their size wouldn't attempt. The company's Thane and Indore hospitals are amongst the few hospitals in the western region of India to provide neuro-rehabilitation services through a dedicated robotic and computer-assisted neuro-rehabilitation center.

The journey toward clinical leadership required careful orchestration. Rather than attempting excellence across all specialties simultaneously—a common mistake that dilutes resources—Jupiter identified focus areas based on community need, competitive gaps, and return on investment. Cardiac care came first, driven by the explosion of heart disease in urban India. Neurology followed, addressing the stroke epidemic accompanying India's aging demographics. Oncology emerged as the third pillar, serving cancer patients who previously traveled to Mumbai's Tata Memorial Hospital.

Building centers of excellence meant more than acquiring equipment or hiring specialists. It required creating ecosystems where complex care could thrive. The cardiac center integrated interventional cardiology, cardiac surgery, cardiac anesthesia, specialized nursing, rehabilitation, and preventive cardiology into a seamless continuum. Patients entering with chest pain received immediate ECG, troponin testing, and echocardiography. Those requiring intervention moved directly to catheterization labs without bureaucratic delays. Post-procedure rehabilitation began before discharge, with structured follow-up protocols ensuring long-term outcomes.

The technology strategy reflected pragmatic innovation rather than prestige purchases. While competitors marketed robotic surgery systems costing crores but used for limited procedures, Jupiter invested in technologies with broader impact. The neuro-rehabilitation center exemplified this approach. The robotic rehabilitation equipment—exoskeletons for gait training, robotic arms for upper limb therapy, virtual reality systems for cognitive rehabilitation—served hundreds of stroke and accident victims rather than showcase surgeries for a select few.

In 2021, the Company carried out small bowel intestine transplant surgery at Thane Hospital—a procedure so complex that only a handful of Indian centers attempt it. The surgery required coordination between twelve departments, from transplant surgery to immunology to intensive care. Success depended not on any single superstar surgeon but on institutional capability—protocols, teamwork, infrastructure—that Jupiter had methodically built over years.

Quality accreditation became both a goal and a tool for improvement. NABH (National Accreditation Board for Hospitals) certification required documenting and standardizing hundreds of processes, from hand hygiene protocols to medication error prevention systems. The accreditation process, often viewed as bureaucratic burden, became a framework for systematic improvement. Infection rates dropped by 60%, medication errors decreased by 75%, and patient satisfaction scores improved across all parameters.

The diagnostic capabilities evolved to support clinical excellence. NABL (National Accreditation Board for Testing and Calibration Laboratories) accreditation for laboratories ensured test results met international standards. Advanced imaging—256-slice CT scanners, 3-Tesla MRI machines, PET-CT for cancer diagnosis—provided clinicians with precise diagnostic information. But technology alone wasn't enough; Jupiter invested equally in training radiologists and technicians to extract maximum value from these tools.

Clinical research emerged as an unexpected strength. Most Indian hospitals focus on service delivery, viewing research as academic luxury. Jupiter integrated research into clinical practice, participating in international trials, publishing case studies, and encouraging doctors to pursue academic activities. This created a virtuous cycle: research participation attracted quality doctors, improved clinical protocols, and enhanced reputation, which in turn attracted more complex cases suitable for research.

The biomedical department evolution deserves special mention. What began as a cost-saving measure—maintaining equipment in-house rather than depending on vendors—became a competitive advantage. Jupiter's biomedical engineers didn't just fix broken machines; they optimized equipment performance, customized devices for specific procedures, and even developed innovative solutions. When COVID-19 created ventilator shortages, Jupiter's team retrofitted anesthesia machines for ICU ventilation, saving lives when equipment wasn't available for purchase at any price.

Training and skill development underpinned clinical excellence. Jupiter established simulation labs where doctors practiced complex procedures on mannequins before attempting them on patients. Nurses underwent specialty certifications in critical care, emergency medicine, and operation theater management. Even support staff—ward boys, technicians, housekeeping—received training in their roles in clinical care. This comprehensive skill development created a culture where everyone understood their contribution to patient outcomes.

The clinical information system integration represented a quiet revolution. Unlike many Indian hospitals where departments operate in silos, Jupiter's systems connected seamlessly. A blood test ordered in emergency appeared immediately in the laboratory system, results flowed automatically to the treating physician's screen, and relevant findings triggered alerts to specialists. This integration eliminated delays, reduced errors, and improved clinical decision-making.

Patient outcomes data, rarely published by Indian hospitals, became a transparency tool. Jupiter began publishing surgical success rates, infection rates, and patient satisfaction scores—initially internally for improvement, later publicly for accountability. When their cardiac surgery mortality rates matched international benchmarks despite serving sicker, less affluent patients than Western hospitals, it validated their clinical model.

The technology roadmap balanced aspiration with pragmatism. Plans included AI-powered diagnostic tools, precision medicine capabilities, and integrated telemedicine platforms. But each investment underwent rigorous evaluation: Would it improve patient outcomes? Could staff be trained to use it effectively? Would it generate returns to fund further improvements? This disciplined approach avoided the technology graveyards littering many Indian hospitals—expensive equipment gathering dust because no one knew how to use it effectively.

By 2023, Jupiter's clinical capabilities had transformed from basic tertiary care to quaternary care—the most complex procedures requiring the highest expertise. They weren't just treating disease; they were setting new standards for what Indian healthcare could achieve. The next challenge would be maintaining this excellence while scaling rapidly, ensuring that clinical quality wouldn't be sacrificed for growth.

VII. The IPO Story & Public Market Entry (2023)

The investment bankers' first valuation model for Jupiter Life Line Hospitals came back at ₹600 crores—significantly below Dr. Thakker's expectations. It was late 2022, and the IPO preparation had exposed every weakness in Jupiter's financial structure: complex holding patterns from years of incremental fundraising, inconsistent accounting across facilities, and the messy reality of Indian healthcare economics. The bankers suggested waiting, cleaning up further, perhaps showing another year of growth. Dr. Thakker pushed back: "The market won't wait for us to be perfect. We go now, or someone else captures the opportunity."

The pre-IPO preparation revealed the gap between running hospitals and running a public company. Jupiter had always focused on clinical metrics—patient outcomes, occupancy rates, doctor satisfaction. Now they needed to speak the language of capital markets: EBITDA margins, return on capital employed, same-store sales growth. The CFO, recruited from a pharmaceutical major, introduced financial discipline that initially frustrated operators but ultimately strengthened the business.

Cleaning up the corporate structure consumed months. Various expansion phases had created a complex web of subsidiaries, joint ventures with doctor partners, and equipment leasing arrangements that made sense operationally but confused financial analysis. Lawyers and accountants worked through nights, simplifying structures, buying out minority stakes, and creating clean lines of ownership that public market investors could understand.

The governance transformation went beyond structure. Jupiter inducted independent directors with healthcare, finance, and regulatory expertise. Board meetings shifted from operational discussions to strategic oversight. Audit committees, risk management frameworks, and compliance systems—previously managed informally through trust and relationships—became formalized processes with documentation trails.

Positioning Jupiter's equity story required careful crafting. In a market familiar with Apollo's national footprint and Fortis's premium positioning, how should investors value a regional player? The answer emerged from Jupiter's unique strengths: dominant position in underserved Western India markets, superior clinical outcomes despite lower price points, and massive expansion potential in tier-2 cities where healthcare infrastructure remained inadequate.

Jupiter Life Line Hospitals IPO is a book build issue of ₹869.08 crores. The issue is a combination of fresh issue of 0.74 crore shares aggregating to ₹542.00 crores and offer for sale of 0.45 crore shares aggregating to ₹327.08 crores. The fresh issue proceeds would fund expansion—new hospitals in Dombivali and other locations. The offer for sale allowed early investors, including doctor partners who had supported Jupiter through difficult years, to partially exit while retaining meaningful stakes.

The roadshow tested Jupiter's story against sophisticated investors' scrutiny. Fund managers questioned everything: Why was Pune occupancy below 60%? How would Jupiter compete against digital health startups? What happened if insurance companies squeezed reimbursement rates? Each question forced sharper thinking, better articulation of strategy, and occasionally, acknowledgment of challenges that needed addressing.

Pricing emerged as the crucial decision. Investment bankers, scarred by recent IPO failures, pushed for conservative pricing around ₹650-700 per share. Dr. Thakker and the board believed Jupiter deserved premium valuation given its growth trajectory and clinical capabilities. They settled at ₹735, the upper end of the price band—aggressive but not unrealistic.

Jupiter Life Line Hospitals IPO bidding started from Sep 6, 2023 and ended on Sep 8, 2023. Those three days revealed intense market interest. Institutional investors, particularly healthcare-focused funds and insurance companies understanding the sector's long-term dynamics, oversubscribed their portion within hours. Retail investors, attracted by Jupiter's brand recognition in Maharashtra, participated enthusiastically. The issue was oversubscribed 1.5 times, modest by hot IPO standards but solid for a healthcare infrastructure company.

The shares got listed on BSE, NSE on Sep 18, 2023. The first day's trading would set perceptions for years. Jupiter opened at ₹755, a modest premium, then volatility struck. Profit booking pushed prices down to ₹720 before recovering to close at ₹748. Not the explosive debut some hoped for, but sustainable—avoiding the pump-and-dump dynamics that plagued other recent listings.

The immediate post-IPO period tested management's public market readiness. Quarterly earnings calls required explaining seasonal variations in hospital occupancy. Stock price volatility, previously irrelevant to private company operations, now affected employee morale and doctor recruitment. Media coverage intensified, with every clinical incident potentially becoming market-moving news.

Capital allocation post-IPO reflected newfound discipline. The ₹542 crore fresh issue proceeds were earmarked specifically: ₹300 crores for the Dombivali hospital, ₹150 crores for equipment upgrades across facilities, ₹92 crores for working capital and general corporate purposes. This specificity, unusual for Indian IPOs that often use vague "general corporate purposes" allocations, built investor confidence.

The stock performance trajectory revealed market education in process. Initial months saw volatility as traders searched for quick gains. But as quarterly results demonstrated consistent execution—occupancy improvements, ARPOB growth, successful new service launches—longer-term investors accumulated positions. Healthcare mutual funds, insurance companies, and family offices began building stakes, providing stability to the shareholder base.

Public market disciplines improved operations in unexpected ways. The quarterly scrutiny forced faster decision-making—equipment purchases that previously took months now closed in weeks. Transparency requirements meant publishing data that competitors could analyze, but also forced internal accountability that improved performance. The employee stock option plan, now linked to public market valuations, aligned entire organizations toward common goals.

By March 2024, six months post-listing, Jupiter's stock had appreciated to ₹950-1000 levels, validating the IPO pricing. More importantly, the company had successfully transitioned from entrepreneur-driven to institutionally-governed, from relationship-based to process-driven, from private to public—without losing the clinical focus and patient-first culture that defined its success.

The IPO wasn't just a financing event; it was a transformation that prepared Jupiter for its next growth phase. Access to capital markets meant expansion could accelerate. Public visibility attracted talent that might previously have chosen established brands. The governance structures and financial disciplines would prove crucial as Jupiter pursued its ambitious goal of operating 2,500 beds by 2027.

VIII. Financial Architecture & Unit Economics

The spreadsheet on the CFO's screen told a story of operational leverage finally kicking in. Q3 FY2024 results showed Thane operating at 76% occupancy with EBITDA margins touching 28%, while Pune had crossed the crucial 65% threshold where hospitals turn meaningfully profitable. But the real insight lay deeper in the unit economics—the intricate machinery that transforms patient admissions into sustainable returns.

Mkt Cap: 9,526 Crore · Revenue: 1,319 Cr · Profit: 193 Cr—the headline numbers that catch investors' attention. But understanding Jupiter's financial architecture requires dissecting how a patient journey translates into revenue, how costs layer across that journey, and why small improvements in operational metrics create disproportionate value.

The revenue model starts with patient mix. A cardiac surgery generates ₹3-5 lakhs but requires expensive infrastructure and specialized teams. A maternity case brings ₹50,000-80,000 with predictable resource needs and shorter stays. Emergency trauma cases, while less profitable, drive volumes that improve overall utilization. Jupiter's revenue optimization doesn't mean cherry-picking high-value procedures; it means architecting the right mix across specialties to maximize both clinical impact and financial returns.

The company's inpatient and outpatient revenue is diversified across hospitals with Thane, Pune, and Indore hospitals accounting for 54.18%, 34.03%, and 11.79%, respectively, of the revenue from operations in Fiscal 2023. This geographic distribution reveals both concentration risk—Thane still dominates—and opportunity, as newer facilities have substantial room for growth.

ARPOB (Average Revenue Per Occupied Bed) serves as the crucial profitability metric. Thane's ARPOB of ₹48,000 reflects its mature operations and complex case mix. Pune at ₹55,000 benefits from higher insurance penetration and affluent demographics. Indore's ₹44,700 shows both lower reimbursement rates in tier-2 markets and opportunity for improvement as the facility matures and attracts more complex cases. The cost structure reveals healthcare's fundamental challenge: high fixed costs with variable demand. Staff salaries consume 35-40% of revenues—unavoidable given healthcare's human-intensive nature. Doctors typically receive fixed retainers plus variable components linked to procedures performed, aligning incentives while managing costs. Nursing staff, the backbone of patient care, represents the largest employee expense but also the most critical quality determinant.

Material costs—pharmaceuticals, consumables, implants—account for 25-30% of revenues. Jupiter's centralized procurement across three hospitals provides negotiating leverage, though not to the scale advantages Apollo or Fortis enjoy. The company maintains strategic inventory levels: 15-20 days for regular consumables, just-in-time for expensive implants, emergency stockpiles for critical drugs.

For the full year, net profit rose 10.31% to Rs 193.20 crore in the year ended March 2025 as against Rs 175.14 crore during the previous year ended March 2024. Sales rose 17.52% to Rs 1261.55 crore in the year ended March 2025 as against Rs 1073.44 crore during the previous year ended March 2024. These results demonstrate solid execution despite the challenges of managing multiple facilities at different maturity stages.

Over the last 5 years, revenue has grown at a yearly rate of 22.65%, vs industry avg of 12.93%—nearly double the sector growth rate. This outperformance reflects both organic growth in existing facilities and successful new hospital ramps. But the real story lies in margin expansion: JUPITER LIFE LINE HOSP L EBITDA is ₹2.92 B INR, and current EBITDA margin is 23.47%.

The working capital cycle in healthcare creates unique challenges. Insurance claims take 45-60 days for settlement, government scheme reimbursements can stretch to 90 days, while expenses—salaries, rent, utilities—require immediate payment. Jupiter manages this through sophisticated cash flow management: negotiating advance payments from cash patients, factoring insurance receivables, and maintaining credit lines specifically structured around healthcare payment cycles.

Capital allocation decisions reveal strategic priorities. Of every rupee of operating cash flow, approximately 40% goes toward capacity expansion (new beds, equipment upgrades), 30% services debt, 20% funds working capital, and 10% provides cushion for opportunistic investments. This disciplined allocation ensures growth doesn't compromise financial stability.

The return on capital employed (ROCE) tells the efficiency story. At 18-20%, Jupiter's ROCE trails Apollo's 25%+ but exceeds most regional players. The gap reflects Apollo's scale advantages and mature facility mix, but Jupiter's trajectory shows steady improvement as newer facilities mature and occupancy improves.

Depreciation deserves special attention in hospital economics. Medical equipment typically depreciates over 10-13 years, building infrastructure over 30 years. But technological obsolescence means equipment often requires replacement before full depreciation. Jupiter's conservative depreciation policies and regular equipment refresh cycles ensure book values reflect economic reality.

The unit economics at procedure level reveal profitability drivers. A cardiac bypass surgery generates ₹3-4 lakhs revenue with 25-30% EBITDA margins. A normal delivery yields ₹50,000 with 20% margins. Diagnostics—MRI, CT scans, lab tests—generate 40-50% margins but require expensive equipment. Emergency services often lose money but drive admissions that generate profitable inpatient stays. Understanding these dynamics allows Jupiter to optimize service mix without compromising clinical care.

Looking forward, the path to improved economics is clear: occupancy improvement in newer facilities, case mix enhancement toward higher-acuity procedures, and operational leverage as fixed costs spread across larger revenue base. The company is strategically expanding its hospital network in western India, with new facilities planned in Dombivli and Pune, aimed at enhancing operational capacity and addressing clinical challenges. However, occupancy rates in newly expanded facilities have been lower than anticipated, prompting a cautious approach to further growth until optimal utilization is achieved.

The financial architecture Jupiter has built—disciplined capital allocation, sophisticated working capital management, transparent reporting—provides the foundation for sustainable growth. As new facilities mature and operational leverage kicks in, the economics should only improve, validating the infrastructure investment thesis that underpins Jupiter's strategy.

IX. Current Expansion & Future Vision (2024-2027)

The construction site in Dombivali buzzes with controlled chaos—concrete mixers, steel frameworks rising, architects huddled over blueprints. But this isn't just another hospital under construction; it's the physical manifestation of Jupiter's next evolutionary leap. The Company is constructing a new multispeciality hospital in Dombivali, Maharashtra with potential capacity of 500 beds, representing their largest single facility and a bet that Mumbai's extended suburbs hold the key to Indian healthcare's future.

The expansion strategy that emerged post-IPO reflects both ambition and learning. The group is constructing two new multispeciality hospitals in Dombivli, Thane (Maharashtra) and Bibvewadi, Pune (Maharashtra) with potential capacity of 500 beds each and It has also purchased land for setting up a new hospital in Mira Road, Thane (Maharashtra) with potential capacity of 300 beds. These aren't random locations—each represents careful analysis of demographics, competition, and infrastructure development.

Dombivali's selection reveals the sophistication of Jupiter's site selection. This Mumbai suburb, often dismissed as a distant bedroom community, houses over 1.2 million residents with virtually no tertiary care infrastructure. The upcoming metro connectivity will reduce travel time to central Mumbai from 90 to 35 minutes, but more importantly, it will position Dombivali as a healthcare hub for surrounding areas like Kalyan, Ulhasnagar, and Ambarnath—a catchment of nearly 5 million people.

The Bibvewadi, Pune facility targets a different opportunity. While Jupiter already operates in Pune, Bibvewadi serves South Pune—an affluent area with established communities but aging healthcare infrastructure. Rather than competing with their existing Pune facility, Bibvewadi will complement it, creating a network effect where doctors can practice at both locations and patients can access the nearest facility for follow-up care.

Mira Road represents the most ambitious bet. This rapidly developing area between Mumbai and Thane will house 300 beds in what Jupiter envisions as their technology showcase—AI-assisted diagnostics, automated pharmacy systems, smart patient rooms. It's designed for the next generation of healthcare consumers who expect digital integration alongside clinical excellence.

These expansions will raise the total bed capacity to ~2,500 beds, more than doubling current capacity. But the strategic intent goes beyond mere bed addition. Jupiter is creating dense clusters in specific geographies rather than scattered presence across multiple states. This clustering enables shared resources—specialists rotating between facilities, centralized diagnostics serving multiple hospitals, unified emergency response systems.

Jupiter Life Line Hospitals announced that an additional 78 beds at Indore Hospital have become operational as of 01 January 2025. As a result, the current capacity of the Company and its subsidiary now stands at 1,061 beds. This incremental expansion at existing facilities parallels the new hospital construction, extracting more value from established infrastructure.

The ₹600 crore expansion financing plan reveals financial sophistication. Rather than diluting equity immediately post-IPO, Jupiter is using a combination of internal accruals (₹200 crores), debt financing (₹300 crores), and equipment leasing (₹100 crores). This maintains the debt-to-equity ratio around 1:1 while preserving financial flexibility for opportunistic acquisitions.

The phased commissioning strategy learned from past expansions will be applied here. Rather than opening all 500 beds simultaneously in Dombivali, Jupiter will commission 200 beds initially, focusing on core departments—emergency, ICU, medicine, surgery, obstetrics. As these departments stabilize and generate cash flow, specialized services—cardiac surgery, neurosurgery, oncology—will be added incrementally.

Technology integration in new facilities goes beyond medical equipment. Jupiter is implementing "smart hospital" concepts: IoT sensors tracking equipment utilization, AI algorithms predicting patient flow, automated inventory management systems. These aren't gimmicks but operational tools that can improve efficiency by 15-20% based on international benchmarks.

The human capital strategy for expansion has evolved from earlier approaches. Instead of relocating entire teams, Jupiter is creating "seed teams"—small groups of experienced staff who establish culture and processes, then train locally recruited talent. This reduces relocation costs while ensuring consistent care standards across facilities.

Competition dynamics in expansion markets vary significantly. In Dombivali, Jupiter will be the first mover in tertiary care, allowing premium pricing and rapid market capture. In Bibvewadi, they'll compete against established players, requiring differentiation through service quality and clinical outcomes. Mira Road sits between these extremes—emerging competition but no dominant player.

The expansion timeline reflects operational realism rather than market promises. Dombivali is scheduled for Q3 FY2026 opening, but Jupiter is planning for Q4 to avoid the over-promising that plagued other hospital IPOs. Construction milestones are tracked weekly, equipment orders placed 12 months in advance, and recruitment begun 6 months before opening.

Regulatory approvals, often the hidden bottleneck in hospital expansion, are being managed proactively. Jupiter has dedicated teams working with municipal corporations, pollution control boards, and fire departments, ensuring permits are obtained sequentially rather than discovering gaps at commissioning time.

The operational playbook for new hospitals has been codified from Pune and Indore experiences. Day 1 readiness includes not just clinical capabilities but also empanelment with major insurance companies, tie-ups with local general practitioners for referrals, and community health camps to build awareness. The goal is 30% occupancy within 3 months, 50% within 12 months, and 65%+ by year two.

Risk mitigation strategies acknowledge expansion challenges. Each new hospital is legally structured as a separate entity, limiting parent company liability. Performance milestones trigger additional funding, preventing good money chasing bad. Exit clauses in equipment leases provide flexibility if a facility underperforms.

The long-term vision extends beyond 2027. Jupiter envisions a network of 15-20 hospitals across Western India, each serving as a complete tertiary care center while benefiting from network effects. They're exploring asset-light models—managing hospitals without owning real estate—to accelerate expansion without proportional capital requirements.

Digital health integration represents the next frontier. While maintaining focus on physical infrastructure, Jupiter is developing telemedicine capabilities, remote monitoring systems, and digital health records that could eventually serve patients beyond hospital walls. This isn't abandoning their infrastructure focus but extending it into digital realms.

The expansion strategy reveals Jupiter's evolution from a single-hospital operator to a healthcare infrastructure company. They're not just adding beds but building an integrated delivery network that can serve Western India's growing healthcare needs while generating attractive returns for shareholders. Success isn't guaranteed—healthcare expansion is littered with failures—but Jupiter's methodical approach, learned from both successes and mistakes, positions them well for the challenge ahead.

X. Competitive Dynamics & Market Position

The battle for Western India's healthcare market resembles a complex chess match where Jupiter plays black against multiple opponents simultaneously. Apollo, the grandmaster with 40 years of experience, controls key squares across India. Fortis, despite corporate turmoil, maintains premium positioning in metros. Regional players like Ruby Hall in Pune and Kokilaben Dhirubhai Ambani in Mumbai defend home territories fiercely. Yet Jupiter has carved out a distinctive position: the middle-market specialist delivering tertiary care at accessible price points.

Market share data reveals Jupiter's steady ascent. Over the last 5 years, market share increased from 1.09% to 1.62% in Western India's organized healthcare sector. This 50% relative growth occurred while larger players also expanded, indicating Jupiter is capturing more than its fair share of market growth. The gains come primarily from unorganized sector conversion—patients choosing Jupiter over nursing homes and single-specialty facilities.

The competitive positioning matrix shows interesting dynamics. On one axis lies clinical capability—from basic secondary care to quaternary procedures. On another lies price positioning—from government rates to international patient pricing. Apollo and Fortis occupy the high-capability, high-price quadrant. Government hospitals provide high-capability at low prices but with quality concerns. Jupiter has positioned itself in the sweet spot: high clinical capability at middle-market prices, accessible to India's growing middle class.

Doctor ecosystem management represents a critical competitive battlefield. Apollo attracts top talent through brand prestige and research opportunities. Fortis offers lucrative packages to star surgeons. Jupiter competes through a different model: partnership opportunities where senior doctors receive equity stakes, creating alignment between clinical excellence and financial returns. This approach has attracted accomplished doctors who value entrepreneurial opportunity over corporate hierarchy.

The referral network architecture reveals competitive advantages. While national chains rely on brand marketing to drive patient flow, Jupiter has cultivated deep relationships with general practitioners in its catchment areas. Regular CME programs, referral acknowledgment systems, and transparent communication build loyalty among referring physicians. In Thane alone, Jupiter works with over 500 GP clinics, creating a patient funnel that expensive advertising couldn't replicate.

Insurance empanelment strategies differentiate players significantly. Apollo's national presence gives them leverage with insurance companies, commanding premium rates. Regional players often accept whatever rates insurers offer. Jupiter has taken a middle path: accepting standard rates for routine procedures while negotiating premium rates for specialized services where they demonstrate superior outcomes. This selective approach maintains volumes while protecting margins.

Technology adoption varies dramatically across competitors. Max Healthcare showcases robotic surgery and AI diagnostics. Narayana Health, conversely, focuses on frugal innovation—delivering quality care at minimal cost. Jupiter's approach is pragmatically selective: adopting technologies that demonstrably improve outcomes or efficiency while avoiding prestige purchases that drain capital without proportional benefit.

The talent retention battle intensifies as healthcare professionals become increasingly mobile. Apollo loses doctors to international opportunities. Fortis faces exodus during corporate upheavals. Jupiter's retention rate exceeds 85% for senior doctors and 75% for nursing staff—superior to industry averages. The secret: career development paths that don't require relocating to metros, equity participation for senior staff, and a culture that values clinical decision-making over corporate bureaucracy.

Geographic strategy reveals fundamental differences in competitive approach. Apollo follows a hub-and-spoke model with flagship hospitals in metros supported by smaller facilities. Fortis clusters hospitals in affluent urban areas. Manipal has a strong presence in South India. Jupiter's "deep rather than wide" strategy—multiple full-service hospitals in selected geographies—creates local density that nationals can't match.

Pricing strategy remains the most visible competitive dimension. For a cardiac bypass surgery, Apollo Mumbai might charge ₹5-6 lakhs, Fortis ₹4-5 lakhs, while Jupiter delivers comparable outcomes at ₹3-4 lakhs. This isn't about being cheap—it's about value optimization. Jupiter achieves lower prices through operational efficiency, lower real estate costs in satellite cities, and acceptance of reasonable rather than maximum margins.

Quality metrics increasingly shape competition as patients become informed consumers. Jupiter publishes infection rates, surgical success rates, and patient satisfaction scores—transparency that many competitors avoid. When Jupiter's cardiac surgery mortality rate of 1.8% matches Apollo's despite serving less affluent patients who often present later in disease progression, it builds credibility that marketing can't buy.

The digital health disruption threat looms over traditional hospitals. Startups promise to deliver healthcare without expensive infrastructure. Telemedicine platforms offer consultations at fraction of hospital costs. Jupiter's response is selective integration rather than resistance: partnering with digital platforms for initial consultations, using telemedicine for follow-ups, but emphasizing that complex care requires physical infrastructure and human expertise that apps can't replace.

Corporate healthcare contracts represent a growing competitive arena. IT companies, manufacturing units, and service organizations seek healthcare partners for employee health management. Jupiter wins these contracts not through lowest pricing but through comprehensive service—onsite health camps, preventive care programs, seamless insurance processing, and most importantly, quality outcomes that reduce employee sick days.

Medical tourism, while not Jupiter's focus, influences competitive dynamics. Apollo and Fortis attract international patients seeking quality care at lower costs than Western countries. Jupiter participates selectively, serving Non-Resident Indians visiting family who need medical care, but doesn't pursue medical tourism aggressively. This focus on local markets provides stability that international patient flows can't guarantee.

The consolidation wave reshaping Indian healthcare creates both opportunity and threat. Private equity firms acquire hospital chains, seeking to build scale for eventual exits. Larger players acquire smaller ones to eliminate competition. Jupiter remains strategically independent, preferring organic growth over acquisition-led expansion. This patience may sacrifice short-term growth but preserves culture and operational excellence.

Regulatory changes affect competitive dynamics unpredictably. Price caps on procedures like knee replacements and cardiac stents compress margins for all players. Clinical establishment acts increase compliance costs. Jupiter's response has been to diversify service mix, reducing dependence on any single procedure or specialty that regulators might target.

Looking ahead, competitive dynamics will likely intensify. National chains will expand into tier-2 cities, Jupiter's stronghold. Digital health platforms will mature, potentially disrupting traditional models. Government insurance schemes will expand coverage but potentially squeeze reimbursement rates. Success will require continuous adaptation—maintaining clinical excellence while improving efficiency, building brand while managing costs, expanding capacity while preserving culture.

Jupiter's competitive position—regional leader with national-quality healthcare at accessible prices—remains defensible but not impregnable. The moat lies not in any single advantage but in the integration of multiple strengths: clinical capabilities that match national chains, local market knowledge that nationals can't replicate, operational efficiency that delivers sustainable margins, and most importantly, a culture that puts patient outcomes above all else.

XI. Playbook: Lessons in Healthcare Infrastructure

The conference room whiteboard captured fifteen years of hard-won wisdom in simple phrases: "Trust compounds daily, breaks instantly." "Occupancy before capability." "Doctors aren't employees, they're partners." These weren't MBA frameworks but operational insights that transformed Jupiter from a single hospital to a healthcare infrastructure platform. Each lesson emerged from specific challenges, mistakes, and occasional triumphs that define the reality of building hospitals in India.

Building trust in healthcare operates by different rules than other industries. A software bug frustrates users; a medical error destroys families. A restaurant's bad meal gets forgotten; a hospital's negligence gets litigated. Jupiter's "patient first" philosophy isn't marketing—it's risk management. Every operational decision filters through this lens: Will it improve patient outcomes? Will it build or erode trust? The accumulated trust from successfully treating 750,000 patients creates a moat that capital alone can't build.

Geographic expansion timing remains more art than science. Conventional wisdom suggests consolidating one market before entering another. Jupiter violated this by opening Pune while Thane was still ramping up, then adding Indore before Pune stabilized. The logic: healthcare infrastructure has long gestation periods. Waiting for perfect timing means perpetually waiting. Better to plant seeds early and nurture them patiently than to rush when opportunity becomes obvious to everyone.

The 65-70% occupancy sweet spot emerged from painful experience. Below 60%, fixed costs crush margins. Above 75%, quality suffers as staff gets stretched, equipment gets overutilized, and patient experience deteriorates. The target isn't maximum occupancy but optimal occupancy—the level that balances profitability with sustainable quality. This means turning away patients during peak periods, a counterintuitive decision that preserves long-term reputation over short-term revenue.

Capital allocation in capital-intensive businesses requires exceptional discipline. Every rupee spent on a fancy lobby can't be spent on medical equipment. Every crore invested in land can't fund doctor training. Jupiter's capital allocation framework prioritizes: first, life-saving equipment; second, clinical talent; third, patient comfort; fourth, operational efficiency; last, aesthetic improvements. This hierarchy, consistently applied, ensures resources flow toward clinical capability rather than cosmetic enhancements.

Managing regulatory complexity across states taught Jupiter to view compliance as competitive advantage rather than burden. While competitors complain about bureaucracy, Jupiter maintains dedicated regulatory teams that proactively engage with authorities. They participate in policy consultations, implement regulations ahead of deadlines, and maintain relationships that ensure smooth approvals. When new regulations emerge, Jupiter is prepared while competitors scramble.

The importance of clinical outcomes in brand building cannot be overstated. Jupiter publishes outcome data that many hospitals hide—infection rates, readmission rates, mortality statistics. Initially, this transparency seemed risky. What if rates were higher than competitors? But transparency forced continuous improvement. When infection rates exceeded benchmarks, Jupiter implemented stringent protocols. When certain procedures showed poor outcomes, they stopped offering them until capabilities improved. This ruthless focus on outcomes built credibility that advertising couldn't achieve.

Doctor partnership models evolved through trial and error. Initial attempts at pure employment models failed—talented doctors valued autonomy over salary. Pure fee-for-service created misaligned incentives. The hybrid model that emerged—base salaries plus procedure-based incentives plus equity participation—aligns clinical excellence with financial success. Senior doctors think like owners because they are owners.

Technology adoption requires careful evaluation beyond vendor promises. For every successful implementation like Jupiter's integrated hospital information system, there are cautionary tales of expensive equipment gathering dust. The evaluation framework: Does it improve clinical outcomes? Can staff be trained effectively? Will patients accept it? Can we maintain it in-house? Will it generate ROI within three years? This disciplined approach avoids technology graveyards while ensuring meaningful innovation.

Scaling culture remains the hardest challenge. The patient-first philosophy that Dr. Thakker personally embodied must somehow transfer to thousands of employees across multiple locations. Jupiter achieves this through systematic onboarding, continuous training, and most importantly, operational processes that make doing the right thing easier than cutting corners. When systems support culture rather than depending on individual initiative, values scale with growth.

Insurance relationship management evolved from transactional to strategic. Initially, Jupiter accepted whatever rates insurers offered, grateful for patient volumes. As capabilities grew, they began selective negotiation—accepting standard rates for routine procedures while demanding premiums for complex ones. The key insight: insurers need quality hospitals as much as hospitals need patient volumes. This mutual dependence, properly managed, creates win-win partnerships.

The nursing talent crisis forced innovative solutions. With nursing schools producing insufficient graduates and international markets attracting Indian nurses with higher salaries, Jupiter faced perpetual shortages. Their response: establishing nursing training partnerships with colleges, offering education sponsorships with service bonds, creating career progression paths that don't require leaving bedside care, and most importantly, treating nurses as professionals rather than support staff.

Equipment lifecycle management balances clinical needs with financial reality. Medical technology evolves rapidly—today's cutting-edge MRI becomes obsolete in five years. Jupiter's approach: buy proven rather than newest technology, maintain equipment meticulously to extend life, upgrade incrementally rather than wholesale replacement, and most importantly, ensure utilization justifies investment. A 256-slice CT scanner means nothing if it performs ten scans daily.

Patient flow optimization resembles industrial engineering more than medicine. How long does registration take? Where do bottlenecks occur? Why do some doctors always run late while others finish early? Jupiter applies systematic process improvement—time-motion studies, queue management systems, standard operating procedures—to minimize patient waiting without compromising care quality. Small improvements—reducing average consultation delay from 45 to 30 minutes—dramatically improve patient satisfaction.

The hub-and-spoke versus all-hub debate continues across healthcare. Jupiter's all-hub model—each hospital offering comprehensive services—requires higher investment but provides better patient experience. Patients receive complete care at one location rather than shuttling between facilities. Doctors practice at one hospital rather than commuting between multiple sites. This operational simplicity, despite higher capital requirements, creates superior outcomes for all stakeholders.

Financial communication with public markets requires careful balance. Healthcare investors understand that occupancy fluctuates seasonally, that new facilities take time to ramp, that clinical quality sometimes requires financial sacrifice. But they also demand predictability, growth, and returns. Jupiter navigates this by setting conservative guidance, explaining variances thoroughly, and maintaining consistent strategic direction even when quarterly results disappoint.

The playbook continues evolving as Jupiter faces new challenges. How to integrate digital health without abandoning infrastructure advantages? How to attract Generation Z healthcare workers with different career expectations? How to manage climate change impacts on hospital operations? Each challenge adds new pages to the playbook, new lessons that future healthcare infrastructure builders will study.

The meta-lesson transcending specific insights: healthcare infrastructure isn't just about building hospitals. It's about creating systems that deliver consistent clinical outcomes across geographies, economic strata, and disease conditions. It's about balancing multiple stakeholders—patients, doctors, nurses, investors, regulators, communities—whose interests often conflict. Most fundamentally, it's about remembering that behind every statistic lies a human being seeking healing, and every operational decision ultimately affects whether that healing occurs.

XII. Bear vs. Bull Case Analysis

The investment committee debate stretched past midnight, spreadsheets competing with strategic arguments, optimism clashing with skepticism. On one side, the bulls saw Jupiter as India's next healthcare giant, perfectly positioned to capture the infrastructure gap. On the other, bears pointed to sobering realities—mediocre occupancy at new facilities, dangerous concentration in one hospital, and competition that grows fiercer daily. Both sides had merit, and understanding each perspective is crucial for long-term investors.

The Bear Case: Why Jupiter Might Stumble

The occupancy challenge at newer facilities represents more than teething troubles. Pune at 54.9% occupancy after six years of operations suggests fundamental issues. Either Jupiter misjudged market demand, failed to build adequate referral networks, or faces stronger competition than anticipated. If established Pune struggles, what hope for Dombivali or Mira Road? The capital invested in underutilized facilities destroys returns—expensive equipment depreciating, staff salaries burning cash, maintenance costs continuing regardless of patient volumes.

The concentration risk cannot be ignored. Thane, Pune, and Indore hospitals accounting for 54.18%, 34.03%, and 11.79%, respectively, of the revenue from operations in Fiscal 2023 reveals dangerous dependence on the original Thane facility. Any disruption—a quality incident, regulatory action, key doctor departures—could devastate financial performance. This concentration also suggests that Jupiter's replication model isn't working as smoothly as management claims.

High capital intensity with long payback periods creates a cash trap. Each new 500-bed hospital requires ₹400-500 crores investment, taking 7-10 years to generate acceptable returns. In a rapidly evolving healthcare landscape, will physical hospitals remain relevant long enough to justify these investments? Digital health platforms offer consultations at 1/10th the cost without any infrastructure. While complex procedures require hospitals today, technology evolution might change this equation faster than Jupiter anticipates.

Intense competition from both national chains and new regional players squeezes margins from both sides. Apollo and Fortis have deeper pockets, better brand recognition, and economies of scale Jupiter can't match. Meanwhile, new doctor-entrepreneur ventures pop up constantly, cherry-picking profitable procedures without bearing full hospital infrastructure costs. Jupiter sits in an uncomfortable middle—too small for national scale advantages, too large for nimble entrepreneur agility.

Regulatory risks loom large over Indian healthcare. Government price caps on procedures have already hit cardiac stents and knee replacements. What if regulators extend price controls to other procedures? What if insurance companies, gaining negotiating power through consolidation, squeeze reimbursement rates? What if clinical establishment acts impose additional compliance costs? Each regulatory change potentially disrupts Jupiter's carefully balanced unit economics.

The doctor dependence problem intensifies with growth. Healthcare ultimately depends on individual physicians' skills and relationships. Key doctors leaving can devastate departments—patients follow trusted physicians, not hospital brands. As Jupiter expands, maintaining quality becomes harder. One bad surgeon in Indore can destroy reputation built over years in Thane. The company lacks the brand strength of Apollo to weather such incidents.

Execution risk multiplies with ambitious expansion. Managing three hospitals already stretches management bandwidth. Adding three more facilities simultaneously while maintaining quality seems unrealistic. Construction delays, equipment procurement issues, staff recruitment challenges—any could derail timelines and escalate costs. The history of Indian healthcare is littered with expansion plans that destroyed previously successful hospitals.

The Bull Case: Why Jupiter Could Soar

The massive under-penetration in Indian healthcare represents generational opportunity. India needs 2.4 million additional hospital beds just to reach global averages. Western India, Jupiter's focus market, has 250 million people with healthcare infrastructure designed for 100 million. Demographics—aging population, rising chronic diseases, increasing insurance coverage—create inexorable demand growth. Jupiter doesn't need to capture market share from competitors; they need only serve the unserved.