Jio Financial Services: India's Digital Finance Revolution

I. Introduction & Episode Roadmap

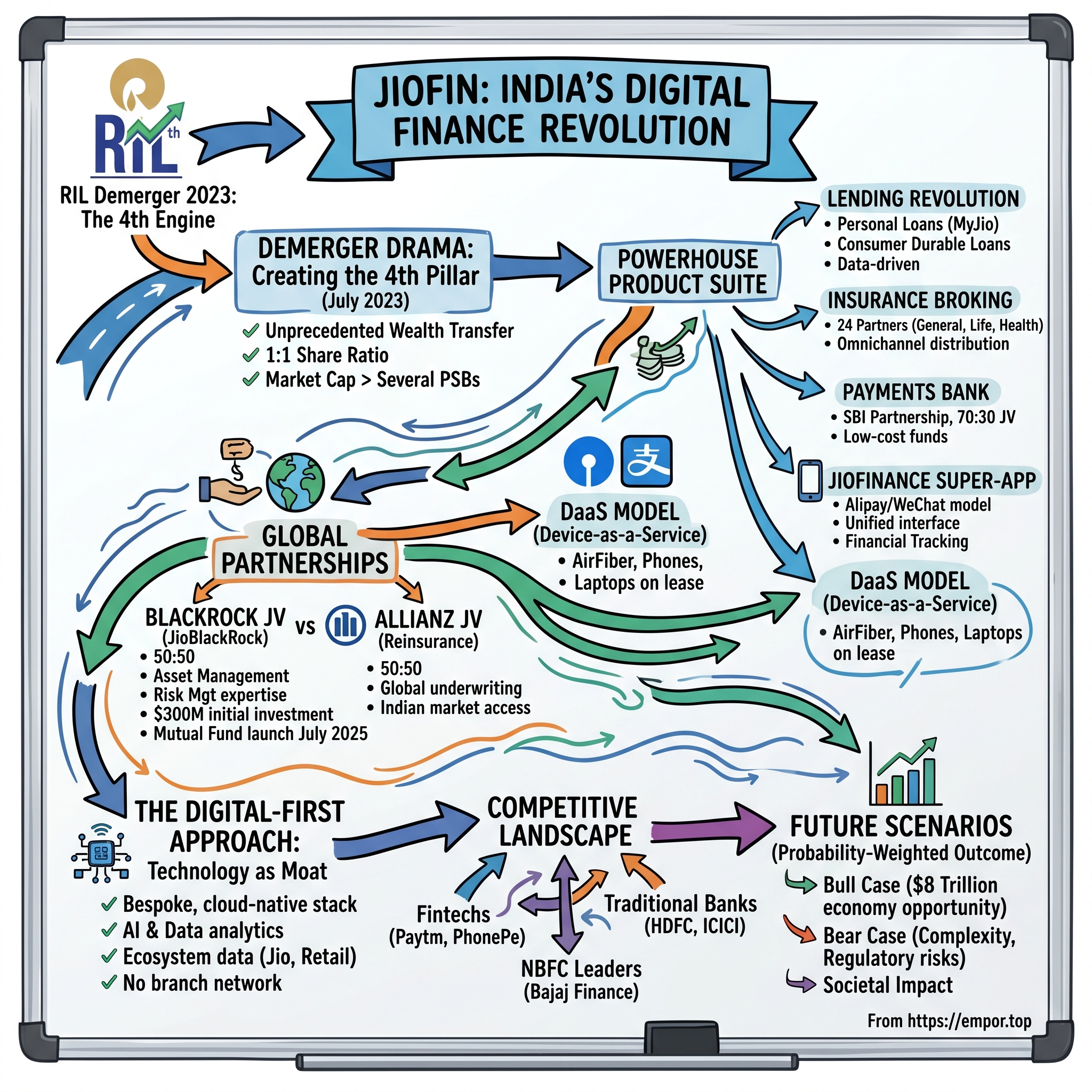

The monsoon season of 2023 marked a seismic shift in India's financial landscape. In July 2023, it was spun-off via a demerger, with shareholders of Reliance Industries receiving one equity share of Jio Financial Services for every share they held in Reliance. This wasn't just another corporate restructuring—it was Mukesh Ambani's audacious bet to transform how 1.4 billion Indians access financial services.

Picture this: A conglomerate that disrupted telecom with free data, revolutionized retail with hyperlocal delivery, and now sets its sights on democratizing finance. The central question isn't whether Jio Financial Services can compete—it's whether India's traditional financial institutions can survive the onslaught of what Mukesh Ambani dubbed Jio Financial Services the group's 'fourth engine' after oil, telecom, and retail.

Reliance Industries transferred Rs 15,500 crore of cash and liquid investments to Jio Financial Services as part of the demerger scheme. This gave Jio Financial Services a liquid asset base of Rs 20,700 crore—a war chest that would make most startups weep with envy and established players lose sleep.

The audacity of the vision becomes clear when you consider the timeline. While fintech startups spend years burning venture capital to acquire customers, Jio Financial Services launched with immediate access to over 450 million Jio telecom subscribers and thousands of Reliance Retail touchpoints. It's not building a financial services company from scratch—it's weaponizing an ecosystem.

What unfolds over the next several hours is a story of calculated disruption, strategic partnerships with global giants, and a playbook that borrows equally from Ant Financial's dominance in China and Reliance's own history of obliterating competition. We'll explore how a telecom-and-retail conglomerate plans to build a financial services superpower, why BlackRock and Allianz rushed to partner with them, and whether this fourth engine can generate the same transformative impact as its predecessors.

II. The Reliance Legacy & Ambani's Financial Services Vision

The story of Jio Financial Services doesn't begin in 2023—it begins in 1986, in the bustling streets of Mumbai where a visionary named Dhirubhai Ambani saw opportunity where others saw obstacles. Reliance Capital Limited was incorporated in 1986 at Ahmedabad in Gujarat as Reliance Capital & Finance Trust Limited. The name Reliance Capital came into effect on 5 January 1995.

Think about the India of 1986. Public sector banks dominated the landscape like monolithic fortresses, loan options were scarce, and financial services were the preserve of the privileged few. Into this environment, Dhirubhai Ambani launched Reliance Capital & Finance Trust with a radical proposition: financial services for the masses. The company's initial revenue streams—lease financing, bill discounting, and corporate deposits—might seem mundane today, but they were revolutionary for their time.

Dhirubhai's approach to financial services mirrored his philosophy in textiles and petrochemicals: identify the underserved, offer them value they couldn't refuse, and scale relentlessly. This wasn't just business—it was nation-building through capitalism. The man who famously said he was "willing to salaam anyone" in government understood that in India, financial services wasn't just about money; it was about access, empowerment, and ultimately, political capital.

But then came the great divide. After suffering a stroke in 1986, he handed over the daily operations of the company to his sons Mukesh Ambani and Anil Ambani. After the death of Dhirubhai Ambani in 2002, the management of the company was taken up by both the brothers. What followed was a Shakespearean drama of sibling rivalry that would reshape Indian business.

The Reliance ADA Group was formed in 2006 after the two brothers Mukesh Ambani and Anil Ambani, split Reliance Industries in December 2005. Anil Ambani got the responsibility of Reliance Infocomm, Reliance Energy, and Reliance Capital. While the world watched the brothers divide their father's empire, few noticed the strategic implications: Mukesh lost financial services to Anil, but he never lost the vision.

Here's where the story becomes fascinating. When Mukesh Ambani first introduced Reliance's telecom service in 2002 under the Reliance Infocomm brand, he had banking services in mind. The telecommunications infrastructure wasn't just about voice and data—it was about building the digital pipes through which financial services would eventually flow. But the split meant that while Mukesh focused on building the distribution highway through telecom, Anil got to drive the financial services vehicle.

The irony is palpable. Anil Ambani, armed with Reliance Capital, tried repeatedly to master the world of finance. He expanded aggressively, acquired companies, launched IPOs that were oversubscribed 73 times. Yet by 2019, he would declare bankruptcy in a UK court, his financial empire in ruins, saved from jail only by his brother's last-minute intervention. Meanwhile, Mukesh, seemingly locked out of financial services, was playing a much longer game.

Ambani established a beachhead in the financial services industry by acquiring a payments bank licence in 2015, two months after the Reserve Bank of India invited applications for this new class of banks. This wasn't a retreat—it was a strategic flanking maneuver. Payments banks might seem limited—they can accept small savings and issue debit cards but not credit cards—but Mukesh saw them differently. They were the trojan horse that would eventually breach the fortress of traditional banking.

The genius of Mukesh's approach becomes clear when you map the timeline. 2015: Payments bank license acquired. 2016: Jio launches with free voice and data, acquiring 428 million customers. 2016-2020: Reliance Retail expands to 17,000+ stores. Each move wasn't isolated—it was creating the infrastructure for financial services at a scale India had never seen.

Consider the strategic patience required. While Paytm burned cash acquiring customers post-demonetization, while PhonePe and Google Pay fought QR code wars with cashbacks, Mukesh Ambani sat quietly, building his ecosystem. Following the 2016 demonetisation, when Vijay Shekhar Sharma's Paytm and Google Pay were amassing payments customers in the QR code frenzy by offering cash backs, Ambani, who had a payments banking licence, kept out of the fray. Jio Payments' senior executives would regularly present a business case in their review meetings. Ambani would listen patiently without uttering a word, perplexing the senior executives.

This silence wasn't indecision—it was calculation. Why fight expensive customer acquisition battles when you already own the customer through telecom and retail? Why subsidize transactions when you can wait for the market to mature and enter with superior infrastructure?

The vision crystallizes when you examine India's financial landscape through Ambani's lens. A nation with 1.4 billion people but chronic under-penetration of financial services. Hundreds of millions who have phones but not bank accounts, who shop but don't invest, who need credit but can't access it. This wasn't just a market opportunity—it was what consultants call a "whitespace," virgin territory waiting to be conquered.

And unlike his father, who had to genuflect to obtain licenses, Mukesh Ambani had something more powerful than political connections: he had data. Every Jio subscriber's calling patterns, every Reliance Retail transaction, every digital interaction—petabytes of behavioral information that could be transformed into credit scores, risk profiles, and personalized financial products.

The stage was set. The infrastructure was built. The customers were captured. All that remained was to pull the trigger on what would become the group's 'fourth engine' after oil, telecom, and retail. The demerger wasn't the beginning of Jio Financial Services—it was the culmination of a two-decade strategy to reclaim what was lost in 2005 and build something far greater than what was originally envisioned.

III. The Demerger Drama: Creating the Fourth Pillar

July 20, 2023, will be remembered as the day Indian capital markets witnessed one of the most complex and ambitious corporate restructurings in history. But the drama began months earlier, in boardrooms where the decision to carve out financial services from Reliance Industries wasn't just strategic—it was revolutionary.

The mechanics of the demerger reveal Ambani's meticulous planning. Mukesh Ambani-led Reliance Industries Ltd (RIL) demerged its financial unit, Jio Financial Services (JSFL) on 20 July. Reliance had fixed 20 July as the record date to identify eligible shareholders for the allotment of shares of the demerged entity. This wasn't a simple spin-off—it was a surgical separation designed to unlock value while maintaining control.

The numbers tell a story of unprecedented wealth transfer. Reliance Industries transferred Rs 15,500 crore of cash and liquid investments to Jio Financial Services as part of the demerger scheme. To put this in perspective, this initial capital injection was larger than the market capitalization of most Indian NBFCs. It wasn't seed funding—it was a war chest designed to signal serious intent to the market.

But the real drama unfolded in the pre-market hours of July 20. The share price of RIL ex-JFSL has been discovered at Rs 2,580 per share while Jio Financial Services is valued at Rs 261.85 per share after the pre-opening session on the NSE and BSE. The market's price discovery mechanism was stress-tested like never before.

As RIL has derivatives contracts, the National Stock Exchange will conduct a special pre-open session for Reliance Industries on July 20 to determine the equilibrium price, as the conglomerate is set to demerge its financial services business. Picture the tension in trading rooms across Mumbai. Algorithms recalibrating, traders frantically updating models, and the entire market holding its breath as India's largest company essentially split itself in two.

The market's verdict was stunning. The market discovered price of Rs 261.85 per share of Jio Financial Services has come much higher than most brokerages' estimates. This high price is a reflection of the market's assessment of Jio Financials' potential. Analysts who had projected modest valuations were left scrambling to explain why the market valued a company with no operational history at such a premium.

The demerger ratio was elegantly simple: The ratio for demerger is fixed at 1:1. Every Reliance shareholder would wake up owning a piece of the financial services future. Under the Reliance-JFSL demerger, shareholders of Reliance will get one share of the demerged entity for every share owned by them in the oil-to-telecom conglomerate. So, if an investor owns 100 RIL shares on 20 July, he/she will be eligible to receive 100 Jio Financial Services shares.

But simplicity in structure masked complexity in execution. The derivatives market faced an unprecedented challenge. All existing contracts with expiry dates July 27, 2023, August 31, 2023 and September 28, 2023, will expire on July 19, 2023. The methodology of settlement shall be separately intimated by respective Clearing Corporations. The entire F&O ecosystem had to be recalibrated overnight.

The tax implications added another layer of sophistication. According to a statement by Reliance, the post-demerger cost of acquisition of RIL shares is 95.32 per cent and that of JFSL shares is 4.68 per cent. For example, if you had purchased the Reliance share on 19 July at Rs 2,840 then value of your Reliance holding would be 2,707 and Rs 133 for JSFL holding. This wasn't just accounting—it was financial engineering designed to minimize tax impact while maximizing value creation.

The strategic rationale for the demerger reveals Ambani's deeper thinking. The nature and competition involved in the financial services business is distinct from the other businesses, and it is capable of attracting a different set of investors, strategic partners, lenders and other stakeholders. This wasn't just about unlocking value—it was about creating a pure-play financial services entity that could attract specialized capital and partnerships.

The governance structure post-demerger sent clear signals about ambitions. On July 8, 2023, a week after Jio Financial Services was demerged from the financial services business of Reliance Industries, JFS announced that Ambani's daughter Isha had joined its board. The inclusion of the next generation wasn't ceremonial—it was a declaration that JFS would be central to Reliance's future for decades to come.

The listing journey itself became a spectacle. JFSL was listed on the stock exchanges on 21 August 2023. Between demerger and listing, the stock remained in a unique suspended animation—included in indices but not actively traded, creating a month-long buildup of market anticipation.

Following the demerger and listing, JFSL was briefly a part of Nifty 50, BSE SENSEX and FTSE indices, but was removed from these indices over the following weeks as it did not meet their inclusion criteria. The index inclusion and subsequent exclusion wasn't a setback—it was expected. The company needed operational history to qualify for index inclusion, but the brief appearance in India's premier indices had already achieved its purpose: putting JFS on every institutional investor's radar.

The market capitalization at listing told its own story. After the demerger and subsequent listing of JFS on the stock exchanges, the fledgling JFS commands a market capitalisation of around Rs 1.6 lakh crore- bigger than several public sector banks and next only to that of State Bank of India (SBI). A company with no operational history was valued higher than banks with decades of operations. The market wasn't buying the present—it was betting on the future.

Dr. V.K. Vijayakumar, Chief Investment Strategist at Geojit Financial Services, captured the market sentiment: The wide reach of JFSL through RIL's other business segments like Reliance Retail has the potential to grow the company at a fast pace for many years to come. The market is discounting this potential.

The demerger achieved something remarkable: it created a financial services giant with the capital strength of an established player, the agility of a startup, and the ecosystem advantages of a conglomerate. The fourth pillar wasn't just erected—it was architected to be load-bearing for Reliance's next phase of growth.

IV. Building the Financial Services Empire: Product by Product

The architecture of Jio Financial Services reveals a carefully orchestrated financial ecosystem, not a random collection of services. Typical of Ambani, JFS wants the lion's share of the fast-growing financial services market via organic and inorganic growth—grabbing products, geographies and licences. It has a modular framework with independent CEOs for each business.

The corporate structure itself tells a story of strategic compartmentalization. The company operates as a holding entity with tentacles reaching into every corner of financial services. JFS is a holding company that operates its financial services business through entities such as Jio Finance, Jio Insurance Broking, Jio Payment Solutions, Jio Payments Bank, Jio Leasing, and Jio-BlackRock. Each subsidiary isn't just a business unit—it's a specialized assault vehicle designed to capture specific segments of the financial services market.

The Lending Revolution

The lending business represents JFS's most direct assault on traditional banking. JFS said it has already launched personal loans service for salaried and self-employed individuals in Mumbai via its MyJio app and consumer durable loans across 300 stores pan India. But this isn't just another NBFC offering loans—it's a data-driven lending machine leveraging the entire Reliance ecosystem.

Consider the consumer durable loans across 300 stores. These aren't standalone Jio Financial outlets—they're integrated into Reliance Digital and Reliance Retail stores where millions of Indians already shop for electronics and appliances. The customer doesn't need to visit a bank branch or fill out lengthy applications. The loan approval happens at the point of purchase, using data from their Jio telecom account, previous Reliance Retail purchases, and digital payment history.

The personal loans through MyJio app represent an even more radical departure from traditional lending. With over 450 million Jio subscribers, the app doesn't need to acquire customers—it already owns them. The credit underwriting doesn't rely solely on CIBIL scores or salary slips—it incorporates alternative data like mobile recharge patterns, data consumption, and payment regularity.

Get a loan against mutual funds or property without selling your assets. Also, make your dream home possible with our home loans at attractive rates. Need capital for your business? Try our corporate loans. Plus, go green with special solar financing options. The product suite isn't random—each offering targets a specific customer need while maximizing the use of existing collateral or relationships.

Insurance Broking: The Distribution Powerhouse

The insurance broking business showcases JFS's platform approach to financial services. Rather than seeking insurance licenses immediately, JFS positioned itself as the ultimate distribution partner. The company has established partnerships with 24 insurance companies across general, life, and health insurance segments—essentially becoming a financial supermarket.

The breadth is staggering: Life – 5, General – 15, Health – 4 insurance partners offering everything from term life and health insurance to auto coverage and embedded insurance products. But the real innovation lies in distribution. Through the MyJio app, Reliance Retail stores, and JioMart, the company can offer contextual insurance at the moment of need—travel insurance when booking tickets, device insurance when purchasing electronics, health insurance during medical consultations on JioHealth.

The Payments Bank Play

On 19-August-2015 Reliance Industries received a license to run a payments bank from the Reserve Bank of India under Section 22 (1) of the Banking Regulation Act, 1949. It then partnered with the State Bank of India and incorporated Jio Payments Bank Limited in November 2016. The 70:30 joint venture with SBI wasn't just about regulatory compliance—it was about combining Jio's digital reach with SBI's banking expertise.

Jio's payments bank licence allows it to offer current accounts and savings accounts (the so-called CASA combo of cheap funds) but doesn't allow lending activity. While this might seem limiting, it provides JFS with something invaluable: a low-cost source of funds that can be deployed through its NBFC arms for lending.

The payments infrastructure extends beyond traditional banking. Entities of Jio Financial Services offer loans, payments bank savings accounts, digital insurance, UPI money transfers, bill payments, and recharges. Every transaction generates data, deepens customer relationships, and creates cross-selling opportunities.

JioFinance: The Super-App Strategy

In May 2024, JFSL launched JioFinance, an app with digital payments, loans and insurance offerings. This isn't just another fintech app—it's JFS's answer to Alipay and WeChat Pay, a super-app designed to be the single interface for all financial needs.

All the services are offered through a full-stack app called JioFinance, which also doubles up as a financial tracking and money management tool. The app doesn't just facilitate transactions—it becomes the customer's financial command center, tracking spending, managing investments, and recommending products based on financial behavior.

The integration with the broader Jio ecosystem is seamless. Pay bills, buy insurance, plan for the future, and handle emergencies — all in the Finance tab on MyJio. Track your earnings, spending, and savings - all in one place with MyMoney. The boundaries between telecom, retail, and financial services dissolve in the customer experience.

Device-as-a-Service: The Trojan Horse

Perhaps the most innovative offering is the Device-as-a-Service (DaaS) model. It has also started its operating lease business with AirFiber devices. The company's DaaS (device as a service) model for consumer devices (AirFiber, phone, laptop) is expected to create an altogether new market as it is not something large NBFCs or banks have done so far.

Think about the implications. Instead of selling a JioPhone or AirFiber device outright, JFS leases it to the customer. This accomplishes multiple objectives: it makes devices affordable through small monthly payments, creates a recurring revenue stream, deepens customer lock-in, and generates consistent data on payment behavior. It's consumer finance disguised as telecom service.

In 2024, Jio Financial Services established a subsidiary called Jio Leasing Services Ltd, an unrelated leasing services business. The leasing subsidiary isn't just about consumer devices—it's positioning JFS to enter equipment leasing, vehicle leasing, and potentially even real estate leasing.

The Technology Infrastructure

Underpinning all these services is a technology stack that rivals any global fintech. the company has implemented a modern, bespoke technology stack across each business unit. This isn't legacy banking technology with digital lipstick—it's cloud-native, AI-powered infrastructure built for scale.

The technology advantage becomes clear in execution. While traditional banks struggle with core banking system upgrades, JFS launches new products in weeks. While NBFCs grapple with manual underwriting, JFS uses AI to make instant credit decisions. While insurance companies rely on agents, JFS deploys chatbots and automated claim processing.

Each product in the JFS portfolio isn't just a revenue stream—it's a data generator, a customer touchpoint, and a cross-selling opportunity. The company isn't building a financial services business—it's constructing a financial services ecosystem where each element reinforces and amplifies the others. The empire isn't just being built product by product—it's being architected for exponential network effects.

V. The BlackRock Partnership: Global Meets Local

The announcement on July 26, 2023, sent shockwaves through global financial markets. BlackRock, the world's largest asset manager with $11.5 trillion under management, was entering India not through acquisition or organic growth, but through a 50:50 joint venture with a company that had just been demerged days earlier. This wasn't just a partnership—it was a validation of Jio Financial Services' ambitions at the highest level of global finance.

BlackRock [NYSE: BLK] and Jio Financial Services Limited (JFS) today announced an agreement to form Jio BlackRock. The structure of the deal reveals sophisticated thinking on both sides. Jio BlackRock was launched with an initial investment of $150 million from each partner, bringing the total to $300 million. This equal commitment wasn't just about capital—it was about signaling equal partnership in a venture that would fundamentally reshape India's asset management industry.

The timing was no coincidence. This move followed the demerger of Jio Financial Services from Reliance Industries in July 2023, laying the groundwork for the new venture. Ambani had orchestrated the sequence perfectly: first, create an independent financial services entity, then immediately validate it with a partnership with the world's most powerful asset manager.

But why would BlackRock, with its pick of partners globally, choose JFS? The answer lies in the complementary capabilities each brought. The partnership will leverage BlackRock's deep expertise in investment and risk management along with the technology capability and deep market expertise of JFS to drive digital delivery of products. BlackRock brought global investment expertise, sophisticated risk management systems, and the credibility that comes from managing money for the world's largest institutions. JFS brought something BlackRock couldn't buy: direct access to 450 million Jio customers and the digital infrastructure to reach them at near-zero marginal cost.

Larry Fink, BlackRock's CEO, had been eyeing India for years. The country represented the last great untapped market for asset management—a rapidly growing economy with a 35% household savings rate but minimal penetration of mutual funds and investment products. But BlackRock's previous attempts to enter India through traditional routes had yielded limited results. The JFS partnership offered something different: not just market entry, but market transformation.

On 26 May 2025, SEBI issued its final approval and registration certificate to JioBlackRock Mutual Fund to begin operations. Following the authorisation, Jio BlackRock rolled out its first New Fund Offers (NFOs) in early July 2025. The speed from announcement to operation—less than two years—was unprecedented for a venture of this scale and complexity.

The initial product launch revealed the venture's ambitions. the Overnight, Liquid, and Money Market Funds, which together raised around ₹17,800 cr. Starting with debt funds wasn't just conservative—it was strategic. These products established credibility, built operational capabilities, and created a base of assets that could fund more aggressive expansion.

But the real disruption came in the business model. The zero-cost launch offer and digital delivery through the Jio ecosystem target first-time investors, leveraging India's 1.2 billion internet users. Zero-cost wasn't just pricing—it was a declaration of war on the traditional mutual fund industry's distribution-heavy, commission-driven model.

The technology integration revealed the partnership's sophistication. it integrates BlackRock's Aladdin platform, a powerful risk and portfolio management tool, bringing institutional-grade technology to retail investors. Aladdin, BlackRock's proprietary risk management system used to manage trillions globally, was being deployed for Indian retail investors. This wasn't technology transfer—it was technology transformation.

Speaking on this transaction, Mr. Hitesh Sethia, President and CEO, JFS, said: "This is an exciting partnership between JFS and BlackRock, one of the largest and most respected asset management companies globally". Sethia's background—decades at ICICI Bank including international operations—signaled that this wasn't just about domestic ambitions. JFS was thinking globally from day one.

The expansion beyond asset management came swiftly. Ltd. to establish a 50:50 joint venture. The joint venture agreement will also involve setting up a wealth management company and a brokerage firm in India. This wasn't just about mutual funds—it was about building a comprehensive wealth management ecosystem that could serve everyone from first-time investors to ultra-high-net-worth individuals.

The expansion of BlackRock and Jio Financial's partnership underscores Reliance's growing ambitions in the financial services sector. The $237 billion Indian firm already leads the nation's refinery, retail and telecom sectors. For BlackRock, this wasn't just another emerging market partnership—it was a bet on India becoming the next China in terms of wealth creation and asset management opportunity.

The implications for India's asset management industry are profound. With mutual fund penetration still low (16% AUM-to-GDP ratio versus a global 63%), Jio BlackRock's approach backed by recent data showing a 35.46% year-over-year AUM growth to ₹53.40 lakh crore by March 2024 aims to bring financial inclusion to the forefront. The partnership isn't just entering a market—it's expanding it.

The distribution strategy leverages every element of the Jio ecosystem. The venture uses Jio's extensive digital ecosystem, especially the JioFinance app, to distribute its products cutting out traditional intermediaries. Imagine: a rural customer walks into a JioMart store to buy groceries, opens a Jio Payments Bank account, and invests in a Jio BlackRock mutual fund—all in one visit, all through one ecosystem.

But perhaps most significantly, this partnership changes the competitive dynamics fundamentally. Since BlackRock is a global asset management responsible for managing roughly $11 trillion in assets, the partnership will bring tremendous operational knowledge into the business but will limit Ambani's input. Unlike Jio Telecom or Reliance Retail where Ambani called all the shots, this was a true partnership between equals.

The market's response was immediate and dramatic. JioBlackRock Mutual Fund on 7th July, 2025, said it has closed its first New Fund Offer (NFO), raising ₹17,800 crore (about USD 2.1 billion) across three cash and debt schemes. For context, this was one of the largest NFO collections in Indian mutual fund history—and this was just the beginning.

The BlackRock partnership represents something beyond business metrics. It's the marriage of global sophistication with local distribution, of institutional capability with retail reach, of patient capital with aggressive expansion. It transforms JFS from a domestic financial services player into a global force, and gives BlackRock the keys to what could become the world's largest wealth creation opportunity over the next decade. The question isn't whether this partnership will disrupt Indian asset management—it's whether the disruption will spread globally.

VI. The Allianz Partnership & Insurance Play

Lightning struck twice. Just as the market was digesting the BlackRock partnership, Jio Financial Services unveiled another blockbuster alliance that would reshape India's insurance landscape. Jio Financial Services Limited (JFSL) and Allianz Group (Allianz), through its wholly-owned subsidiary Allianz Europe B.V., today entered into a binding agreement to form a 50:50 domestic reinsurance joint venture to serve the dynamic and high-growth insurance market in India.

The Allianz partnership wasn't just about insurance—it was about building the entire insurance value chain from the ground up. The two companies also entered into a non-binding agreement for setting up equally owned joint ventures for both general and life insurance businesses in India. The potential partnership for insurance will see two trusted financial services brands – JFSL and Allianz – coming together to deliver innovative and holistic protection solutions to the people of India.

To understand the significance, consider India's insurance landscape. Despite being the world's most populous nation, India's insurance penetration stands at a mere 3.7% of GDP, compared to 10%+ in developed markets. The protection gap—the difference between economic losses and insured losses—runs into hundreds of billions of dollars. This wasn't just a market opportunity; it was a societal imperative.

The structure of the partnership reveals strategic sophistication. Starting with reinsurance wasn't the obvious move—most players begin with direct insurance—but it was brilliant. The reinsurance JV between JFSL and Allianz will help insurers manage risks more effectively by providing access to strong underwriting capabilities and competitive capacity – ultimately strengthening the resilience of the entire insurance ecosystem. By providing reinsurance, JFS wouldn't just be competing with insurers; it would be enabling them, learning from them, and positioning itself at the center of the insurance ecosystem.

The JV will leverage Allianz's existing Allianz Re and Allianz Commercial portfolios and activities in India. It will also benefit from Allianz's global setup, including its pricing, risk selection and portfolio management expertise. Allianz Re has been reinsuring risk in India for over 25 years. This wasn't Allianz's first rodeo in India—they brought decades of experience and relationships that JFS could leverage immediately.

The timing of the partnership was particularly intriguing. Allianz was the JV partner with Bajaj Finserv for more than 20 years and had two insurance JVs — Bajaj Allianz Life and Bajaj Allianz General. Allianz had a 26 per cent stake in both the insurance companies. In October last year, Allianz expressed its intention to split with Bajaj Finserv, and in March this year, Bajaj Finserv announced that it will buy Allianz's stake in both the JVs for ₹24,180 crore.

Allianz's exit from Bajaj and immediate entry with JFS wasn't coincidental—it was strategic realignment. With Bajaj, Allianz was a minority partner in mature businesses. With JFS, they were equal partners in ventures that could define India's insurance future. The German insurer wasn't just changing partners; it was changing its entire India strategy.

Isha M. Ambani, Non-executive Director, Jio Financial Services Limited, says: "India is witnessing a transformative surge in insurance demand, driven by rising prosperity, growing financial awareness, and rapid digital adoption. This partnership, combining Allianz's global reinsurance expertise with JFSL's deep understanding of the Indian market and strong digital infrastructure, aims to deliver innovative and customized reinsurance solutions.

The involvement of Isha Ambani sends a clear signal—this wasn't just another business venture for Reliance. The next generation was taking ownership of building India's insurance future. Her presence on the board alongside global insurance executives created a bridge between Silicon Valley-style disruption and European insurance sophistication.

The reinsurance joint venture addresses a critical market gap. Currently, India's insurance sector has one state-owned reinsurer — General Insurance Corporation (GIC Re). Valueattics Reinsurance, backed by Prem Watsa and Kamesh Goyal, has recently received the insurance regulator's nod for a reinsurance company. Additionally, there are 13 foreign reinsurance branches (FRBs) set up by global reinsurance companies, including Munich Re, Swiss Re, and Lloyd's of London, operating in India.

Despite these players, India's reinsurance market remains underpenetrated and dominated by the state-owned GIC Re. The JFS-Allianz venture wouldn't just be another competitor—it would bring global best practices, sophisticated risk modeling, and crucially, capacity to take on large, complex risks that Indian insurers currently struggle to place.

The life and general insurance ventures, while still non-binding, represent even larger opportunities. India's life insurance market, dominated by LIC's quasi-monopoly and a handful of private players, is ripe for disruption. The general insurance market, fragmented among dozens of players with minimal differentiation, needs innovation in products, distribution, and claims processing.

JFS's distribution advantage in insurance is even more pronounced than in asset management. Insurance, unlike mutual funds, requires trust, explanation, and often, hand-holding. The combination of Jio's digital reach and Reliance Retail's physical presence creates an omnichannel distribution network that no existing insurer can match.

Consider the possibilities: Parametric crop insurance distributed through JioKrishi to farmers, with claims automatically triggered by weather data. Health insurance embedded in JioHealth consultations, with AI-powered underwriting based on health records. Auto insurance offered at Reliance petrol pumps, with telematics-based pricing using JioThings IoT devices. Each product leverages the ecosystem in ways traditional insurers cannot replicate.

Oliver Bäte, Chief Executive Officer, Allianz SE, says: "We are proud to partner with Jio Financial Services to support the democratization of access to world-class financial services for the people of India, with the opportunity to serve a growing number of consumers who are seeking the right protection for themselves, their families, and their businesses. Allianz and Jio Financial Services are two trusted brands distinguished for customer excellence, and we are very much looking forward to actively contributing to and participating in this exciting journey of change".

The broader vision extends beyond traditional insurance. The partnership aims to support India's national vision of "Insurance for All by 2047"—ensuring every Indian has access to basic insurance protection by India's 100th independence anniversary. This isn't corporate social responsibility—it's building a market that could become one of the world's largest.

The competitive implications are severe. Existing insurers, already struggling with distribution costs and low penetration, now face a competitor with unmatched distribution, global expertise, and patient capital. The reinsurance venture means JFS will have intimate knowledge of every major insurer's risk profile and pricing strategies. The life and general insurance ventures will leverage this intelligence to cherry-pick profitable segments while avoiding the mistakes of incumbents.

The Allianz partnership completes JFS's insurance ecosystem. Insurance broking provides distribution and customer relationships. Reinsurance provides risk management capability and industry intelligence. Direct insurance will provide the products and profitability. It's not just vertical integration—it's strategic encirclement of the entire insurance value chain.

For Allianz, India represents the future of global insurance growth. With developed markets saturated and facing demographic headwinds, India's young population, growing middle class, and increasing risk awareness offer decades of growth potential. The partnership with JFS isn't just market entry—it's securing pole position in what could become the world's largest insurance market by 2050.

The insurance play reveals Ambani's ultimate ambition: not just to participate in financial services, but to fundamentally restructure how Indians think about and access financial protection. Insurance isn't just another product in the JFS portfolio—it's the cornerstone of financial inclusion, the gateway to resilience, and potentially, the most profitable business in the entire Reliance empire.

VII. The Digital-First Approach: Technology as the Moat

In the gleaming towers of Mumbai's Bandra Kurla Complex, where India's financial elite make decisions that move markets, Jio Financial Services was building something radically different. Not another marble-clad bank branch or glass-walled trading floor, but a technology platform that would make both obsolete.

the company has implemented a modern, bespoke technology stack across each business unit. The word "bespoke" is crucial here. While traditional financial institutions struggle with decades-old core banking systems held together by digital band-aids, JFS built its technology from scratch, designed for the smartphone age.

The technology philosophy permeates every aspect of operations. "We have developed a cutting-edge, scalable, cloud-native technology stack, incorporating Artificial Intelligence (AI) and data driven capabilities to deliver optimal performance and cost efficiency," says Sethia. Cloud-native isn't just a buzzword—it means JFS can scale from thousands to millions of customers without the infrastructure investments that cripple traditional banks.

The JioFinance super-app represents the culmination of this digital-first approach. Together, they offer loans, banking services, bill payments, insurance, and more through the JioFinance mobile app. Entities of Jio Financial Services offer loans, payments bank savings accounts, digital insurance, UPI money transfers, bill payments, and recharges. All the services are offered through a full-stack app called JioFinance, which also doubles up as a financial tracking and money management tool.

But JioFinance isn't trying to be another Paytm or PhonePe. The ambition is far grander—to become India's answer to Alipay, a financial operating system for daily life. The app doesn't just process transactions; it anticipates needs, recommends products, and manages financial health proactively.

The data advantage cannot be overstated. Every Jio subscriber generates approximately 2GB of data daily—browsing patterns, app usage, location data, communication patterns. Every Reliance Retail transaction adds purchase history, brand preferences, and spending patterns. Every JioMart order reveals household composition, consumption habits, and price sensitivity. This isn't big data—it's intimate data, the kind that traditional banks spend billions trying to acquire and still fail to obtain.

The similarities with Ma's model are hard to ignore, as the key is the proprietary payments or retail transaction data that will help Jio create a business model around lending, asset management, insurance, and stock broking. Jack Ma built Ant Financial on Alibaba's e-commerce data. Ambani is building JFS on something even more powerful—the digital exhaust of an entire nation.

Consider how this plays out in practice. Traditional banks rely on credit bureau scores based on loan repayment history—backward-looking data that excludes millions of Indians who've never had formal credit. JFS can assess creditworthiness based on mobile recharge patterns—someone who consistently recharges before their plan expires is likely more creditworthy than someone who lets their phone go dead for days. Someone who shops at Reliance Fresh every week has stable household income. Someone who upgrades their JioFiber plan has increasing disposable income.

The AI and machine learning capabilities transform this data into actionable intelligence. Fraud detection systems trained on billions of transactions can identify suspicious patterns in milliseconds. Credit models can approve loans in seconds, not days. Insurance claims can be processed automatically using image recognition and natural language processing. Customer service chatbots can resolve queries without human intervention.

The API-first architecture enables ecosystem integration at unprecedented scale. Every Reliance business becomes a distribution channel, every partner becomes a data source, every transaction becomes a learning opportunity. When a customer buys a television at Reliance Digital, JioFinance can offer consumer durable loans in real-time. When someone books a flight on JioMart, travel insurance appears seamlessly. When a small business uses JioMart for procurement, working capital loans are pre-approved based on purchase patterns.

The technology moat extends beyond consumer-facing applications. The back-end infrastructure leverages the same cloud capabilities that power Jio's telecom network—handling millions of concurrent transactions, petabytes of data, and real-time analytics at scale. While competitors struggle with system outages during peak times, JFS's infrastructure is built to handle Jio's scale—450 million users generating billions of daily interactions.

Security and privacy, often afterthoughts in India's digital rush, are foundational to JFS's architecture. Biometric authentication, tokenization, end-to-end encryption—technologies that are optional extras for many Indian financial institutions are baseline requirements for JFS. The company can afford to be paranoid about security because a single breach could undermine the entire ecosystem's trust.

The platform approach creates powerful network effects. Every user makes the platform more valuable for other users. Every merchant increases consumer utility. Every financial product provider enhances customer choice. Every transaction improves AI models. It's a virtuous cycle that becomes increasingly difficult for competitors to break.

The cost advantages of this digital-first approach are staggering. Traditional banks spend 60-70% of revenues on operating expenses—branches, staff, paper, processing. JFS can operate at a fraction of this cost. No branches to maintain, minimal staff requirements, zero paper processing. These savings can be passed to customers as lower interest rates, higher deposit rates, and better product features—or retained as super-normal profits.

The technology platform also enables rapid experimentation and innovation. While traditional banks take years to launch new products—navigating legacy systems, regulatory approvals, and organizational inertia—JFS can go from idea to market in weeks. A/B testing, rapid iteration, fail-fast mentality—Silicon Valley principles applied to Indian financial services.

But perhaps the most powerful aspect of JFS's technology moat is its invisibility. Customers don't see the AI models, the cloud infrastructure, or the data analytics. They see instant loan approvals, seamless payments, personalized recommendations. They experience financial services that just work, without forms, without queues, without friction. Technology isn't the product—it's the enabler of experiences that traditional financial institutions simply cannot deliver.

The digital-first approach isn't just a competitive advantage—it's a generational leap. While competitors digitize analog processes, JFS builds digital-native solutions. While banks add mobile apps to branch-based models, JFS builds branch-less banking. While insurers automate paper forms, JFS eliminates forms entirely. It's not disruption—it's displacement, making traditional financial services models not just inefficient but irrelevant.

VIII. Competitive Landscape & Market Dynamics

The Indian financial services battlefield in 2024 resembles a multi-front war where traditional banks, nimble fintechs, global tech giants, and now Jio Financial Services converge in a winner-take-all combat. Understanding this landscape requires mapping not just who the players are, but how the rules of engagement are changing.

The fintech explosion has created a fascinating paradox. putting the conglomerate on a collision course with hundreds of startups as well as Google and Walmart's PhonePe vying for a piece of the action. Companies like Paytm, PhonePe, and Google Pay have spent billions educating Indians about digital payments, building QR code acceptance, and creating behavioral change. They've done the hard work of market creation—and now JFS arrives to harvest what they've sown.

Consider the payments landscape. PhonePe processes over 5 billion monthly transactions. Google Pay serves 150 million users. Paytm, despite regulatory challenges, remains a force in merchant payments. These players fought bloody battles for market share, burning venture capital to acquire customers with cashbacks and rewards. JFS enters this market not as another warrior but as an emperor with an existing empire—450 million Jio users who don't need to be acquired, just activated.

The traditional banking giants face an existential crisis. He will have to face tough competition from existing banks like HDFC Bank, ICICI Bank, Kotak Mahindra Bank and others. These institutions, built over decades with thousands of branches and millions of customers, suddenly find their moats evaporating. Their branch networks, once assets, become liabilities in a digital world. Their process-heavy operations, designed for risk management, become competitive disadvantages against algorithm-driven lending.

HDFC Bank, India's largest private bank with a market cap exceeding $150 billion, epitomizes the incumbent's dilemma. Profitable, well-run, and technologically competent, yet constrained by legacy systems, regulatory obligations, and organizational inertia. When JFS can approve a loan in seconds using AI, HDFC's three-day process looks antiquated. When JioFinance offers zero-fee banking, HDFC's fee structure looks exploitative.

The NBFC sector presents a different challenge. Jio Financial Services has entered the highly competitive NBFC lending space, where Bajaj Finance is the leader. Shriram Finance, Tata Capital, Cholamandalam Investment and Finance Aditya Birla Capital are other top NBFCs from corporate houses. These players have mastered the art of non-bank lending—faster decisions, flexible products, aggressive distribution. But they lack what JFS has: a captive customer base and zero customer acquisition cost.

Bajaj Finance, the crown jewel of Indian NBFCs with over 50 million customers, built its empire through consumer durable financing and personal loans. But Bajaj needs to partner with retailers, share economics, and spend heavily on customer acquisition. JFS owns the retailers (Reliance Digital), owns the customers (Jio subscribers), and owns the data (transaction history). It's not a fair fight.

The China parallel looms large over this landscape. In 2004, Jack Ma, the Co-founder of China's Alibaba, an e-commerce business then just five years old and yet to become a world-beater, launched payments platform Alipay for its retail customers and merchants. In a decade, Alipay (later reborn as Ant Financial) became China's leading financial services giant, offering a digital wallet, consumer credit, money market funds, wealth management, and a digital-only bank for small enterprises. Ant Financial soon had $600 billion in assets under management as it layered various financial services atop the e-commerce platform. What also worked was China's underserved and unbanked population, with an aspirational middle class—and a surge in smartphone use.

India in 2024 mirrors China in 2004—massive unbanked population, smartphone adoption reaching critical mass, regulatory environment becoming conducive to digital finance. If JFS follows Ant Financial's playbook, traditional financial institutions face not just disruption but potential irrelevance.

The regulatory environment adds another dimension to the competitive dynamics. The Reserve Bank of India, unlike China's initially permissive regulators, maintains strict oversight. "Banking is a more tightly regulated industry compared to others," said Rishi Gupta, managing director and CEO of Fino Payments Bank. This regulation is both a barrier and an opportunity for JFS. Barrier because it cannot move as fast as unregulated fintechs. Opportunity because once licensed, regulatory compliance becomes a moat against new entrants.

The recent regulatory crackdowns on Paytm Payments Bank for KYC violations and on NBFCs for aggressive lending practices show that the RBI won't tolerate growth at any cost. JFS's approach—partnering with SBI for payments banking, securing proper licenses before launching products, maintaining conservative leverage—suggests learning from competitors' mistakes.

(India's central bank doesn't permit tycoons to receive the banking license.) This regulatory stance explains JFS's partnership-heavy approach. Unable to get a full banking license directly, Ambani creates a banking ecosystem through partnerships, subsidiaries, and joint ventures—achieving banking outcomes without a banking license.

The competitive response has been swift but scattered. HDFC Bank accelerates digital initiatives but can't abandon its branch network. Bajaj Finance expands into new products but lacks ecosystem advantages. Paytm pivots from payments to lending but faces regulatory headwinds. PhonePe and Google Pay dominate payments but struggle to monetize beyond transaction fees. Each competitor fights on a narrow front while JFS attacks across the entire battlefield.

The market dynamics favor platforms over products. In financial services, customer acquisition costs are high, switching costs are low, and margins are thin. The winner isn't who has the best product but who owns the customer relationship. JFS doesn't need the best loan product if it's the most convenient. It doesn't need the highest deposit rates if it's the most accessible. It doesn't need the cheapest insurance if it's the most trusted.

Network effects accelerate these dynamics. "Forget telecom or retail; when they started growing mangoes at the Jamnagar refinery complex, they quickly became Asia's largest mango exporter," says a banker. This quote, while seemingly tangential, captures a crucial truth: Reliance doesn't just enter markets, it dominates them through scale, integration, and relentless execution.

The competitive landscape isn't static—it's evolving rapidly toward consolidation. Smaller fintechs will run out of capital or get acquired. Traditional banks will merge to achieve scale. NBFCs will specialize or perish. In this consolidation, JFS's integrated model, patient capital, and ecosystem advantages position it not just as a survivor but as a likely acquirer of distressed assets and struggling competitors.

The ultimate competitive dynamic is time. Every day JFS operates, it gathers more data, deepens customer relationships, and strengthens network effects. Every day competitors delay responding, they fall further behind. The question isn't whether JFS will disrupt Indian financial services—it's whether anyone can stop it.

IX. The Ambani Playbook: Lessons from Telecom and Retail

To understand Jio Financial Services' trajectory, we must first decode the Ambani playbook—a devastating combination of patient capital, predatory pricing, and ecosystem leverage that has repeatedly transformed Indian industries. The patterns are unmistakable, the execution ruthless, and the outcomes, thus far, inevitable.

The Jio telecom disruption remains the most audacious corporate assault in Indian business history. When it entered telecom with Jio in 2016, it bled the leaders with its low pricing. But "low pricing" understates the violence of the strategy. Jio offered free voice calls forever and 1GB of 4G data for less than the price of a coffee. Competitors weren't just undercut—they were eviscerated.

The numbers tell the story of corporate carnage. The Indian telecom industry went from 12 operators to effectively 3. Aircel, Reliance Communications (ironically, Anil Ambani's company), Telenor, Videocon—bankruptcy or exit. Vodafone and Idea, forced to merge to survive. Airtel, the market leader, saw its stock price halve and margins evaporate. In less than two years, Jio went from zero to 280 million subscribers. It wasn't competition—it was conquest.

But the genius wasn't in the pricing—it was in the preparation. Mukesh Ambani: We've always taken big risks because, for us, scale is important. The biggest risk we have taken so far was Jio. At the time, it was our own money that we were investing, and l was the majority shareholder. Between 2010 and 2016, while competitors were milking 2G and 3G for profits, Ambani spent $35 billion building a 4G-only network. When Jio launched, competitors were still upgrading to 4G. They were fighting the last war while Ambani had already won the next one.

The philosophical underpinning reveals Ambani's thinking: Our worst-case scenario was that it might not work out financially because some analysts thought India wasn't ready for the most advanced digital technology. But l told my board, "In the worst case, we will not earn much return. That's okay because it's our own money. But then, as Reliance, this will be the best philanthropy that we will have ever done in India because we will have digitized India, and thereby completely transformed India".

This wasn't corporate speak—it was strategy disguised as patriotism. By framing Jio as national service, Ambani transformed a competitive assault into a nation-building exercise. Competitors couldn't attack Jio without appearing anti-progress, anti-poor, anti-India.

The Reliance Retail story follows a similar arc but with different weapons. Launched in 2006, Reliance Retail didn't just compete with existing retailers—it reimagined retail itself. While others focused on modern retail formats for urban elites, Reliance built for India—local languages, regional products, price points for the masses.

The acquisition strategy was surgical. Instead of building stores, Reliance acquired struggling retail chains—Future Group's assets, Hamleys, Netmeds—integrating them into an omnichannel behemoth. Each acquisition brought customers, locations, and capabilities that would take decades to build organically.

JioMart's launch during COVID-19 lockdowns showcased the ecosystem advantage. While standalone e-commerce players struggled with logistics, JioMart leveraged Reliance Retail stores as fulfillment centers, Jio's telecom network for customer acquisition, and WhatsApp for ordering. It wasn't just entering e-commerce—it was redefining it through integration.

The capital allocation philosophy underlying both disruptions is crucial. Forget telecom or retail; when they started growing mangoes at the Jamnagar refinery complex, they quickly became Asia's largest mango exporter. This mango anecdote isn't trivial—it reveals a crucial principle: Reliance doesn't do anything small. When they enter a market, they plan to dominate it, regardless of how peripheral it might seem.

The pattern is consistent: Enter with overwhelming force, accept massive initial losses, drive out weak competitors, consolidate the market, then monetize the monopoly or oligopoly position. It's predatory, it's effective, and it's now being deployed in financial services.

The cross-ecosystem synergies multiply the impact. Jio subscribers become Reliance Retail customers become JioMart users become JioFinance account holders. Each business feeds the others, creating a virtuous cycle that competitors cannot replicate. A Bajaj Finance customer is just a lending customer. A JioFinance customer is embedded in an ecosystem that touches every aspect of their life.

The data advantage compounds over time. Every transaction, every call, every purchase adds to a customer profile that becomes increasingly valuable and impossible to replicate. Traditional banks spend millions on customer analytics. JFS inherits petabytes of behavioral data from day one.

The patience is perhaps most remarkable. Following the 2016 demonetisation, when Vijay Shekhar Sharma's Paytm and Google Pay were amassing payments customers in the QR code frenzy by offering cash backs, Ambani, who had a payments banking licence, kept out of the fray. Jio Payments' senior executives would regularly present a business case in their review meetings. Ambani would listen patiently without uttering a word, perplexing the senior executives.

This patience isn't indecision—it's strategic timing. Why compete when the market is nascent and unit economics are terrible? Wait for competitors to educate the market, burn capital on customer acquisition, and establish behavioral change. Then enter with superior infrastructure and ecosystem advantages. It's the corporate equivalent of letting others clear the minefield before advancing.

The organizational structure enables this playbook. It has a modular framework with independent CEOs for each business. So Vinod Easwaran is the CEO of Reliance Payments Bank, and A.R. Ramesh heads Reliance Payment Solutions Ltd. Each unit operates independently but coordinates strategically—competing where necessary, collaborating where beneficial.

The financial philosophy is equally crucial. Unlike venture-funded startups that depend on external capital and face pressure for quick returns, Reliance uses its own capital. This patient capital, generated from cash-cow businesses like refining and petrochemicals, funds long-term bets without quarterly earnings pressure.

The talent strategy mirrors the ambition. With over two decades of experience, Sethia played a key role in expanding ICICI Bank's presence globally, being a founding member of the bank's Canadian and German operations. He was also assigned senior roles in the UK and Hong Kong branches of the private bank. In his last role with the Mumbai-headquartered bank, Sethia led the transaction banking division. JFS isn't hiring startup talent—it's recruiting senior executives from established institutions who understand scale operations.

Applying this playbook to financial services, the strategy becomes clear:

Phase 1 (Current): Build infrastructure, secure licenses, establish partnerships. Accept losses while creating ecosystem integration.

Phase 2 (Next 2-3 years): Aggressive customer acquisition using ecosystem advantages. Undercut competitors on pricing while leveraging data for superior risk management.

Phase 3 (3-5 years): Drive consolidation as weak players exit or seek buyers. Acquire distressed assets at favorable valuations.

Phase 4 (5-10 years): Monetize dominant position through repricing, cross-selling, and new product introduction.

The playbook isn't secret—everyone can see it coming. But like watching an avalanche from the valley floor, seeing it and stopping it are very different things. The Ambani playbook works not because it's surprising but because it's unstoppable—a combination of capital, patience, and execution that overwhelms any defense.

The lessons from telecom and retail aren't just precedents—they're promises. JFS isn't experimenting with financial services disruption. It's executing a proven playbook with a track record of destroying industries and rebuilding them in Reliance's image. The question for competitors isn't whether this will happen in financial services, but whether they'll survive it.

X. Power Analysis & Future Scenarios

The evaluation of Jio Financial Services requires us to think in scenarios, not certainties. The company exists at the intersection of massive opportunities and significant risks, where small variations in execution or regulation could lead to vastly different outcomes.

The Bull Case: The $8 Trillion Opportunity

On August 21, at the listing ceremony of JFS, Kamath, now its Chairman, said, "It's possible to predict that within the next eight to nine years, our GDP could double, reaching around $8 trillion. This presents a tremendous opportunity for India". This isn't just macroeconomic optimism—it's the foundation of JFS's strategy.

Consider the mathematics of financial inclusion. India's credit-to-GDP ratio stands at roughly 55%, compared to 150%+ in developed markets. If India reaches even 100% credit-to-GDP by 2035, it represents $4 trillion in additional lending opportunity. JFS, with its ecosystem advantages, could capture 10-15% market share, representing a $400-600 billion loan book—larger than any Indian bank today.

The insurance opportunity is equally staggering. India's insurance penetration — the ratio of premiums to gross domestic product — is about 3.7 per cent, well below other Asian countries including Japan, South Korea and Thailand. Reaching even Thailand's 5% penetration would double the market size. Achieving developed market levels of 8-10% would create a $500 billion annual premium market.

The wealth management potential might be greatest of all. With mutual fund penetration still low (16% AUM-to-GDP ratio versus a global 63%), the opportunity for growth is exponential. As India's middle class expands from 300 million to 600 million over the next decade, the demand for investment products will explode. JFS-BlackRock could become India's largest asset manager within five years.

The demographic dividend amplifies these opportunities. India adds 10 million people to the workforce annually. These digital natives don't want branch banking—they want smartphone finance. They don't trust agents—they trust apps. They don't have legacy relationships—they're available for acquisition. JFS's digital-first model perfectly matches this generational shift.

The ecosystem network effects create exponential, not linear, growth potential. Every Jio subscriber who becomes a JioFinance user makes the platform more valuable for merchants. Every merchant increases the value for consumers. Every transaction improves risk models. Every improved risk model enables better pricing. Better pricing attracts more customers. It's a flywheel that, once spinning, becomes nearly impossible to stop.

The Bear Case: Execution Complexity and Regulatory Risks

However, financial services are certainly not low-hanging fruit. This understated warning from a banker who watched Reliance dominate mangoes contains profound truth. Financial services isn't commerce or telecom—it's trust, and trust is fragile.

The execution complexity is staggering. JFS isn't building one business but multiple interconnected businesses, each with different regulations, capital requirements, and risk profiles. Lending requires credit assessment capabilities that take decades to build. Insurance requires actuarial expertise and claims management infrastructure. Asset management requires investment expertise and trust. Doing all simultaneously multiplies complexity exponentially.

The regulatory environment presents constant challenges. The RBI's recent crackdowns on Paytm Payments Bank and various NBFCs show zero tolerance for regulatory violations. One KYC failure, one money laundering incident, one systemic risk event could trigger regulatory action that cripples growth for years. Unlike telecom where regulations were stable, financial services regulations evolve constantly, often in response to political or economic pressures.

The partnership dependencies create vulnerabilities. Since BlackRock is a global asset management responsible for managing roughly $11 trillion in assets, the partnership will bring tremendous operational knowledge into the business but will limit Ambani's input. Unlike Jio Telecom or Reliance Retail where Ambani had complete control, JFS depends on partners who might have different priorities, risk appetites, or strategic visions.

The competitive response won't be passive. HDFC Bank has $200 billion in assets and decades of relationships. Bajaj Finance has mastered consumer lending with sophisticated risk models. Global tech giants have unlimited capital and technology advantages. Unlike telecom where competitors were complacent, financial services incumbents are alert to the threat and mobilizing defenses.

The technology risks are real and growing. One cybersecurity breach could destroy customer trust instantly. One algorithmic bias in credit decisions could trigger regulatory action and public backlash. One system outage during critical transactions could cause customer exodus. The same technology that enables scale also creates systemic vulnerabilities.

The Organizational Culture Challenge

Each of our business units is tasked with upholding our foundational principles, encapsulated in the 4Rs—Reputation above all, Regulatory adherence, Return of Capital, and Return on Capital. These principles sound prudent but executing them while pursuing aggressive growth is extraordinarily difficult.

Financial services requires a different organizational DNA than Reliance's other businesses. Oil refining tolerates no mistakes—processes must be perfect. Retail thrives on experimentation—fail fast and iterate. Telecom demands standardization—same service for millions. Financial services requires personalization at scale—unique solutions for each customer while maintaining systemic stability.

The talent challenge is acute. India produces thousands of engineers but few risk managers. Many coders but few underwriters. Plenty of salespeople but few wealth advisors. JFS needs specialized talent that's scarce and expensive, competing against global banks and tech giants for the same people.

Network Effects and Winner-Take-All Dynamics

The crucial question is whether financial services exhibits winner-take-all dynamics like technology platforms or remains fragmented like traditional banking. The evidence suggests a hybrid: certain segments (payments, basic banking) tend toward concentration while others (specialized lending, wealth management) support multiple players.

JFS's strategy appears designed for both scenarios. In commoditized services (payments, basic accounts), leverage ecosystem advantages for market share. In specialized services (wealth management, corporate lending), partner with global leaders for expertise. It's not betting on winner-take-all—it's positioning to win regardless of market structure.

The Probability-Weighted Outcome

Synthesizing these scenarios, the most likely outcome is neither complete dominance nor failure, but significant market share with varying success across segments:

- Payments and Basic Banking: 25-30% market share within 5 years (High Probability)

- Consumer Lending: 10-15% market share within 7 years (Medium-High Probability)

- Insurance Distribution: 20-25% market share within 7 years (Medium-High Probability)

- Insurance Underwriting: 5-10% market share within 10 years (Medium Probability)

- Asset Management: 10-15% market share within 7 years (Medium Probability)

- Wealth Management: 5-10% market share among HNIs within 10 years (Medium-Low Probability)

The aggregate outcome: JFS becomes one of India's top 5 financial services providers within a decade, but doesn't achieve the complete dominance seen in telecom. The ecosystem advantages ensure significant market share, but regulatory constraints and competitive responses prevent monopolistic outcomes.

The societal impact might be most significant. Even partial success means hundreds of millions gaining access to formal financial services, trillions in capital allocated more efficiently, and India's savings channeled into productive investments. JFS might not dominate financial services, but it will fundamentally transform it.

XI. Epilogue: The Next Decade

As the monsoon clouds gather over Mumbai in 2034, Jio Financial Services will either be remembered as the company that democratized finance for a billion Indians or as the cautionary tale of imperial overreach. The next decade will determine which narrative prevails.

India's trajectory toward an $8 trillion economy isn't just an economic projection—it's the canvas on which JFS is painting its ambitions. Every percentage point of GDP growth creates exponential opportunities in financial services. Every million Indians entering the middle class expands the addressable market. Every smartphone sold deepens digital engagement. JFS isn't just betting on India's growth—it's positioning itself as the financial infrastructure for that growth.

The question of whether JFS can become India's first true financial super-app transcends technology. WeChat Pay and Alipay succeeded in China through a unique combination of regulatory forbearance, market timing, and cultural acceptance. India presents different challenges: democratic governance means slower regulatory changes, multiple languages complicate user interfaces, and diverse financial behaviors resist standardization. Yet India also offers unique advantages: English-speaking talent pool, robust legal system, and diaspora connections that could make JFS a global player.

The global expansion question looms intriguingly. With 30 million Indians abroad controlling over $1 trillion in assets, JFS could leverage diaspora connections for international growth. Imagine JioFinance enabling remittances, cross-border investments, and global banking for Indians worldwide. The partnerships with BlackRock and Allianz provide global capabilities. The technology platform enables borderless operations. The ambition certainly exists.

But the ultimate measure of success won't be market share or profitability—it will be societal impact. If JFS succeeds in its stated mission, hundreds of millions of Indians will gain access to credit, insurance, and investment products previously reserved for the privileged. Small businesses will access working capital. Farmers will get crop insurance. Families will build wealth through systematic investment. This isn't corporate rhetoric—it's the logical outcome of JFS's business model, where profitability aligns with inclusion.

The challenges ahead remain formidable. Regulatory scrutiny will intensify as JFS grows. Competitive responses will become more sophisticated. Technology risks will multiply with scale. Partnership tensions will emerge as interests diverge. Execution complexity will increase exponentially. Any of these could derail the journey.

Yet betting against Mukesh Ambani has historically been unprofitable. The man who transformed Indian telecom from expensive luxury to free utility, who built the world's largest refinery in a Gujarat coastal village, who created India's largest retail network during e-commerce disruption—this man doesn't enter markets to participate. He enters to dominate, to transform, to redefine the possible.

The next decade will witness an epic battle for India's financial future. Traditional banks defending their fortresses. Fintech startups fighting guerrilla wars. Global giants deploying unlimited capital. And at the center, Jio Financial Services—armed with ecosystem advantages, patient capital, and the Ambani playbook—advancing inexorably toward its vision of financial services domination.

The outcome isn't predetermined. Market forces, regulatory decisions, technological shifts, and competitive responses will shape the trajectory. But one thing is certain: Indian financial services will look fundamentally different in 2034 than it does today. And Jio Financial Services will be either the primary architect of that transformation or the catalyst that forced others to transform.

As we conclude this analysis, the words of Dhirubhai Ambani echo across the decades: "Think big, think fast, think ahead. Ideas are no one's monopoly." His son has taken these words and weaponized them into a business strategy that has repeatedly redefined Indian industries. Financial services is next. The fourth engine has been ignited. The journey toward India's financial future has begun.

Whether JFS achieves its audacious ambitions or falls short, its mere existence has already changed Indian financial services forever. Incumbents are accelerating digital transformation. Regulators are reconsidering frameworks. Consumers are expecting more. Competitors are consolidating. The industry has been put on notice: the Reliance juggernaut has arrived, and business as usual is no longer an option.

The story of Jio Financial Services isn't just about one company's ambitions—it's about India's transformation from a nation of savers to a nation of investors, from financial exclusion to inclusion, from analog processes to digital experiences. It's about the democratization of finance in the world's most populous nation. And regardless of who ultimately wins this battle, 1.4 billion Indians will benefit from the war.

The fourth engine isn't just running—it's accelerating. The next decade will determine whether it powers India's financial transformation or overheats attempting the impossible. Either way, it will be spectacular to watch.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube