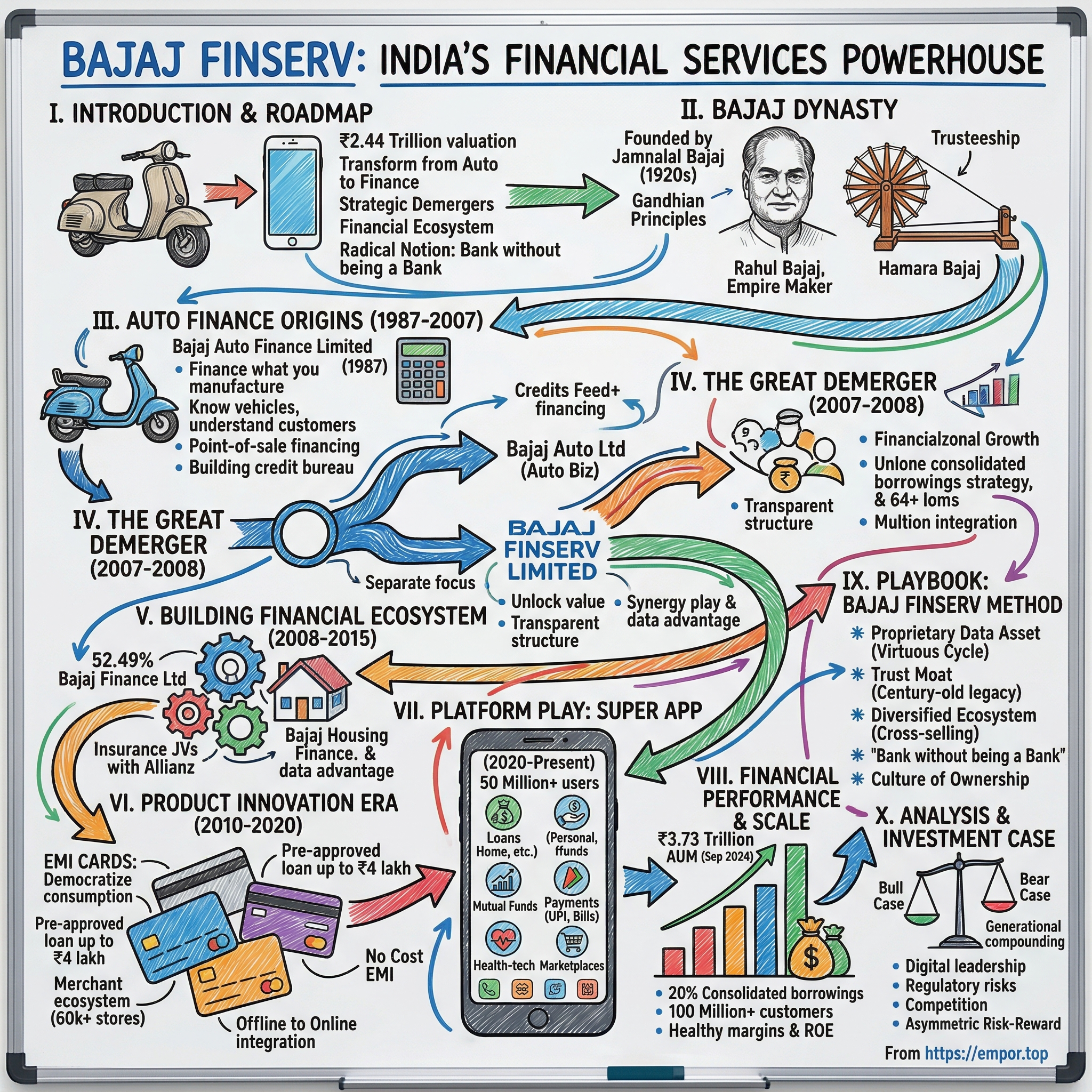

Bajaj Finserv: India's Financial Services Powerhouse

I. Introduction & Episode Roadmap

The story of Bajaj Finserv begins not in the gleaming towers of Mumbai's financial district, but in the dusty workshops of post-independence India where scooters were assembled and dreams of financial inclusion were just beginning to take shape. Today, with a staggering ₹2.44 trillion market valuation, Bajaj Finserv stands as India's financial services colossus—a testament to what happens when industrial DNA meets financial innovation.

How does a company born from the demerger of an auto manufacturer become one of India's most valuable financial services enterprises? The answer lies in a uniquely Indian playbook of patient capital, ecosystem thinking, and the radical notion that you can build a bank without actually being one. This is the story of transformation on an epic scale—from financing two-wheelers in small Indian towns to managing assets worth hundreds of thousands of crores, from simple loan products to a super-app serving over 100 million customers.

The Bajaj Finserv journey illuminates three critical themes that define modern Indian capitalism: the power of strategic demergers to unlock value, the creation of financial ecosystems that transcend traditional banking boundaries, and the democratization of credit in a country where formal financial services were once the privilege of the few. At its core, this is a story about reimagining what a financial services company can be in the world's most populous nation.

The fundamental question that Bajaj Finserv poses—and arguably answers—is whether you can capture the economics and customer relationships of a bank while avoiding the regulatory constraints and capital requirements that traditional banks face. Their answer has created a blueprint that fintech startups worldwide are now trying to replicate, though few have matched the scale and profitability that Bajaj has achieved.

As we unpack this remarkable transformation, we'll explore how a company rooted in Gandhian principles of self-reliance evolved into a sophisticated financial powerhouse, how strategic partnerships with global players like Allianz created competitive moats, and how early bets on digitization positioned Bajaj to compete with both established banks and nimble fintech challengers. This is not just a business story—it's a masterclass in building enduring value in one of the world's most complex and rapidly evolving markets.

II. The Bajaj Dynasty: From Gandhi to Global Finance

The year was 1889 when Jamnalal Bajaj was born into a poor farming family in the dusty village of Kashi Ka Bas near Sikar in Rajasthan. His father Kaniram was a struggling farmer, his mother Birdibai a housewife managing their meager household. But destiny had extraordinary plans for this third son of theirs. In 1894, when young Jamnalal was merely five years old, Seth Bachhraj Bajaj, a wealthy merchant from Wardha, happened to pass through the village. Something about the boy caught his attention—perhaps it was his bright eyes, his confident demeanor, or simply the inexplicable pull of fate. After much persuasion and negotiation, including Bachhraj's promise to install a well for the village, Jamnalal was adopted as Seth Bajaj's grandson and heir.

Jamnalal founded the Bajaj Group of companies in the 1920s, and the group now has 24 companies. He was also a close and beloved associate of Mahatma Gandhi, who is known to have often declared that Jamnalal was his fifth son. This relationship would define not just Jamnalal's life but the entire ethos of what would become one of India's largest business conglomerates.

The transformation from village boy to business magnate began under Seth Bachhraj's careful tutelage. Jamnalal learned the arts of commerce—maintaining meticulous accounts, understanding commodity trading, building relationships with traders and customers. By the time Seth Bachhraj passed away, Jamnalal had not just inherited wealth but had absorbed the disciplines of ethical business practice that would become his hallmark. He strongly believed that "common good was more important than individual gain"—a philosophy that would permeate through generations of Bajaj leadership.

The convergence with Gandhi's movement marked the true awakening of Jamnalal's purpose. When Gandhi returned from South Africa, Jamnalal found in him not just a political leader but a spiritual guide whose vision of self-reliance resonated deeply. The relationship transcended the typical patron-leader dynamic. He donated 20 acres of land to Mahatma Gandhi to establish what would become the center of the freedom movement in Wardha. Gandhi's influence was so profound that Jamnalal publicly burned his silk clothes and Western garments, pledging to wear only khadi for the rest of his life.

He gave up the title of Rai Bahadur conferred on him by the British government and joined the non-cooperation movement in 1921. This wasn't merely symbolic—for a businessman of his stature to renounce British honors meant risking commercial relationships and inviting government scrutiny. But Jamnalal understood that building a nation required sacrifice, and business success without national dignity was meaningless.

The philosophy of trusteeship that Gandhi advocated found its most ardent practitioner in Jamnalal. He viewed his inherited and earned wealth not as personal property but as a sacred trust to be deployed for society's benefit. This wasn't charity in the conventional sense but a fundamental reimagining of the relationship between capital and community. When Gandhi called for funds for the Tilak Swarajya Fund in 1921, Jamnalal contributed Rs. 1 crore—an astronomical sum at the time—for the promotion of khadi and village industries.

His business philosophy was revolutionary for its time. While other industrialists focused on maximizing profits through cost-cutting and exploitation, Jamnalal insisted on quality products, fair wages, and ethical practices. He understood that sustainable business success came not from extracting maximum value but from creating it—for customers, employees, and society at large. This approach laid the foundation for what would become the Bajaj Group's enduring competitive advantage: trust.

The sugar mills that Jamnalal established weren't just industrial ventures but instruments of Gandhi's vision for self-reliance. At Gandhi's insistence, he was among the pioneers who initiated India's sugar industry, establishing one of the thirty mills that would free India from dependence on imported sugar. Each business decision was filtered through the lens of national interest—could this enterprise contribute to India's economic independence? Would it provide dignified employment to Indians? Could it demonstrate that Indian entrepreneurship could match and exceed colonial enterprises?

When Jamnalal passed away in 1942, just as India's freedom struggle was reaching its crescendo, he left behind more than a business empire. Gandhi wrote, "Whenever I wrote of wealthy men becoming trustees of their wealth for the common good I always had this merchant prince principally in mind." The mantle passed to his son Kamalnayan Bajaj, who had returned from Cambridge University with modern management ideas but retained his father's commitment to ethical business.

Kamalnayan faced the tumultuous decades of the 1940s, 50s, and 60s—the upheaval of partition, the challenges of building a new nation, the License Raj that strangled entrepreneurship, chronic shortages of power, raw materials, and foreign exchange. Yet he expanded the group's footprint, diversifying into scooters, three-wheelers, cement, alloy casting, and electricals. The expansion wasn't random but strategic—each new venture addressed a critical need in India's development journey. When he took over active management in 1954, he understood that the Bajaj Group's destiny was intertwined with India's.

The real transformation came when Rahul Bajaj took control in 1965. If Jamnalal was the philosopher-entrepreneur and Kamalnayan the builder, Rahul was the empire-maker. Under his leadership, Bajaj Auto became synonymous with Indian mobility. The Bajaj scooter wasn't just a product—it was a social revolution on two wheels, enabling middle-class aspirations, connecting villages to cities, and creating what would become one of India's most beloved brands: "Hamara Bajaj" (Our Bajaj).

Bajaj Auto was established on 29 November 1945, initially importing and selling two- and three-wheelers, obtaining a license in 1959 to manufacture in collaboration with Piaggio for Vespa scooters. But Rahul Bajaj's vision extended far beyond manufacturing. He recognized that as India's economy evolved, financial services would become as critical as physical products. The seeds of what would become Bajaj Finserv were being planted even as the scooters rolled off assembly lines.

The Bajaj Group today stands as a testament to this multi-generational vision. With a market capitalization exceeding Rs. 14 lakh crores (approximately US$ 167 billion), encompassing 40 group companies and employing roughly 100,000 people, it represents one of India's most successful business transformations. But more than numbers, it embodies a philosophy—that business success and social responsibility aren't contradictory but complementary, that patient capital and ethical practices create more enduring value than short-term profit maximization.

The journey from Jamnalal's adoption by Seth Bachhraj to today's financial services powerhouse illuminates a uniquely Indian model of capitalism—one rooted in Gandhian principles of trusteeship, shaped by the challenges of nation-building, and adapted to the opportunities of a globalizing economy. The DNA of service, self-reliance, and social responsibility that Jamnalal embedded in the organization's culture would prove crucial when the group made its boldest move yet—the demerger that would create Bajaj Finserv and unlock value that even the visionary founder might not have imagined.

This philosophical foundation—the belief that business exists to serve society, that trust is the ultimate currency, that long-term thinking trumps quarterly earnings—would prove invaluable as Bajaj ventured into financial services. In an industry where trust is everything and reputation can be destroyed in moments, the century-old legacy of ethical business practice would become Bajaj Finserv's greatest asset. The stage was set for the next chapter in this remarkable saga—the transformation from industrial conglomerate to financial services innovator.

III. The Auto Finance Origins: Building the Foundation (1987–2007)

The year 1987 marked a pivotal moment in the Bajaj story, though few recognized it at the time. On March 25th, Bajaj Auto Finance Limited was incorporated as a non-banking financial company, ostensibly to provide financing for two and three-wheelers. But this seemingly modest subsidiary would become the cornerstone of one of India's most successful financial services enterprises. The decision to enter financial services wasn't accidental—it emerged from a profound understanding of India's economic transformation and the recognition that selling vehicles was only half the equation; enabling purchases was equally critical.

The India of the late 1980s was a nation on the cusp of change. The rigid socialist economy was showing cracks, middle-class aspirations were rising, but access to formal credit remained a privilege of the wealthy. Banks were bureaucratic fortresses, demanding collateral that most Indians couldn't provide, processing applications through labyrinthine procedures that could take months. For a schoolteacher dreaming of a scooter or a small businessman needing a three-wheeler for his enterprise, the formal financial system might as well have been on another planet.

Bajaj Auto Finance started with a simple insight: the company knew its vehicles, understood its customers, and had a distribution network that reached into India's smallest towns. Why shouldn't it finance what it manufactured? The initial model was elegantly straightforward—leverage the parent company's dealer network, use knowledge of vehicle values for risk assessment, and create simple, transparent loan products that ordinary Indians could understand and access.

The early years were about building fundamental capabilities that would later prove invaluable. Credit assessment in an economy where most applicants had no credit history required innovation. The company developed proprietary scorecards that went beyond traditional metrics, considering factors like employment stability, community standing, and even behavioral indicators during the application process. Field officers became anthropologists of credit, understanding local economies, seasonal income patterns, and the subtle signals that distinguished good borrowers from risky ones.

By 1998, after eleven years of quiet building, the company was ready for its next leap. The initial public offering and listing on the BSE and NSE wasn't just about raising capital—it was a statement of intent. The financial services business was no longer an adjunct to vehicle manufacturing but a standalone enterprise with its own growth trajectory. The market's enthusiastic response validated what insiders already knew: Bajaj had cracked the code of retail lending in India.

The turn of the millennium brought new opportunities and challenges. India's economy was liberalizing rapidly, consumer aspirations were exploding, and the concept of EMI (Equated Monthly Installment) was beginning to reshape purchasing behavior. Bajaj Auto Finance, with characteristic foresight, began venturing beyond vehicle finance into consumer durables and small-ticket personal loans. This wasn't diversification for its own sake but a recognition that the capabilities built for vehicle finance—risk assessment, collection infrastructure, customer relationships—could be leveraged across multiple products.

The consumer durables financing business revealed something profound about Indian consumption patterns. A television wasn't just an electronic device but a window to the world, a refrigerator not just an appliance but a symbol of progress, a washing machine not just a convenience but liberation for millions of women from drudgery. By financing these purchases, Bajaj wasn't just earning interest—it was democratizing prosperity, making middle-class life accessible to millions who had the income but not the capital.

The distribution strategy during this period was masterful in its simplicity. Rather than building expensive branch networks like banks, Bajaj embedded itself in the retail ecosystem. Loan officers were stationed at dealerships and electronics stores, applications were processed on-site, and approvals often came within hours, not weeks. This point-of-sale financing model would later be recognized as revolutionary, but at the time it was simply practical—go where the customers are, make it easy, make it fast.

Risk management evolved from art to science during these years. The company built one of India's most sophisticated credit bureaus before formal credit information companies existed, tracking repayment behaviors across millions of customers. Machine learning before it was fashionable, pattern recognition before it became buzzword—Bajaj was quietly building a data advantage that would prove insurmountable for later competitors. Every loan, every payment, every default added to an ever-growing repository of intelligence about Indian consumers' financial behavior.

The small-ticket loan business, launched in the early 2000s, was particularly revealing. These loans, often just a few thousand rupees, were uneconomical for traditional banks but perfect for Bajaj's lean operating model. They served customers during emergencies—medical expenses, school fees, family obligations—building loyalty that transcended the transactional. A customer who received a Rs. 5,000 loan for their child's school admission would remember Bajaj when they were ready for a Rs. 500,000 home loan years later.

Technology adoption during this period was pragmatic rather than flashy. While banks struggled with legacy systems, Bajaj built its technology infrastructure from scratch, designed for scale and efficiency. Handheld devices for field officers, automated credit scoring, SMS-based payment reminders—these innovations seem ordinary now but were revolutionary in an industry still dependent on paper ledgers and manual processes. The technology investments weren't about being cutting-edge but about being effective, reducing costs while improving customer experience.

The relationship with Bajaj Auto provided unique advantages during these formative years. Beyond the obvious synergies of financing parent company products, there was knowledge transfer, brand leverage, and most importantly, patient capital. While independent finance companies struggled with funding and credibility, Bajaj Auto Finance could tap into the parent's reputation and resources, allowing it to take long-term bets that venture-funded startups couldn't afford.

The human capital strategy was equally thoughtful. Rather than poaching expensive talent from banks, Bajaj recruited fresh graduates and trained them in their unique model. These young professionals, unburdened by traditional banking orthodoxies, became evangelists for a new way of financial services—customer-centric, technology-enabled, and relentlessly focused on execution. Many of today's senior leaders in Indian financial services cut their teeth at Bajaj during these years.

By 2007, on the eve of the great demerger, Bajaj Auto Finance had transformed from a captive finance unit into a full-fledged financial services company. The loan book had expanded from simple vehicle loans to a diversified portfolio spanning consumer durables, personal loans, and small business credit. The distribution network stretched across thousands of locations, the customer base numbered in millions, and the brand had become synonymous with accessible, transparent credit.

But perhaps the most valuable asset built during these twenty years wasn't on the balance sheet. It was the deep understanding of Indian consumers—their needs, aspirations, and behaviors. The insight that credit wasn't just about money but about dignity, that speed mattered as much as rates, that trust was built through thousands of small interactions rather than grand gestures. This customer intelligence would prove invaluable as Bajaj prepared for its next transformation.

The organizational culture that evolved during this period was distinctive. Unlike the hierarchical, process-driven culture of banks, Bajaj fostered entrepreneurship at every level. Branch managers were mini-CEOs, empowered to make decisions and held accountable for results. Field officers were relationship managers, not just collection agents. The head office was a support function, not a control tower. This decentralized, empowered culture would become a competitive advantage as the company scaled.

The seeds of future innovation were already visible. Experiments with co-branded credit cards, partnerships with retailers for exclusive financing offers, early forays into digital applications—these initiatives, while small, showed an organization constantly pushing boundaries. The EMI culture that Bajaj helped create was reshaping Indian consumption, making everything from smartphones to vacations accessible through affordable installments.

As 2007 drew to a close, the stage was set for transformation. The financial services business had proven its viability, the market opportunity was enormous, and the organization had the capabilities to capture it. But success had also brought complexity. The financial services business needed capital, regulatory flexibility, and strategic focus that was difficult to achieve as a subsidiary of a manufacturing company. The solution would be radical—a demerger that would create two focused entities from one conglomerate. It was a bet-the-company move that would either unlock tremendous value or destroy a carefully built enterprise. As history would show, it became one of the most successful corporate restructurings in Indian business history.

IV. The Great Demerger: Birth of Bajaj Finserv (2007–2008)

The boardroom at Bajaj Auto's headquarters in Pune was unusually quiet on May 17, 2007. Rahul Bajaj, the patriarch who had built the company into India's mobility giant, was about to propose the most radical restructuring in the group's 80-year history. The board was being asked to approve a demerger that would split the monolithic Bajaj Auto into three distinct entities—a move that would either unlock tremendous value or destroy decades of carefully built synergies. The tension was palpable because everyone understood this wasn't just a corporate restructuring; it was a reimagining of what Bajaj could become in the 21st century.

The financial services and wind energy businesses were transferred to Bajaj Finserv Limited (BFL) as part of the concluded demerger from Bajaj Auto Limited, approved by the High Court of Judicature at Bombay by its order dated 18 December 2007. But the story of this demerger began much earlier, rooted in the fundamental question of how a conglomerate creates value in an era of specialization.

The strategic rationale was compelling yet controversial. Bajaj Auto had become an unwieldy giant—manufacturing vehicles, financing purchases, selling insurance, generating wind power, and making strategic investments. Each business had different capital requirements, regulatory environments, and growth trajectories. Vehicle manufacturing needed heavy capital expenditure and dealt with cyclical demand. Financial services required regulatory capital but could scale with minimal physical infrastructure. Insurance was a long-gestation business with J-curves that confused investors focused on quarterly earnings. Wind energy was capital-intensive with predictable returns. Trying to manage and value this complexity under one roof was becoming increasingly difficult.

In April 2007, Bajaj Finserv was established following its separation from Bajaj Auto Limited. This structural change was initiated to enable Bajaj Finserv to exclusively focus on the group's financial services business. The preparation had been meticulous. Before the formal announcement, Bajaj Auto had quietly incorporated two subsidiaries—Bajaj Holdings & Investment Limited (BHIL) and Bajaj Finserv Limited (BFS). The company subscribed to 43.5 million shares of Rs. 10 each in BHIL and 43.5 million shares of Rs. 5 each in BFS. These weren't random numbers but carefully calculated to ensure the right capital structure for each entity post-demerger.

The demerger scheme was elegant in its simplicity yet complex in its implications. The entire two-wheeler and auto business of BAL would be transferred to BHIL, along with Rs.1500 crores cash and equivalents. The entire wind energy, insurance and auto finance business would be transferred to BFL, along with Rs.800 crores cash and equivalents. For every share held in the original Bajaj Auto, shareholders would receive one share each in the new Bajaj Auto (the renamed BHIL would later rename back), Bajaj Finserv, and Bajaj Holdings & Investment Limited.

The market's initial reaction was skepticism bordering on hostility. Investors who had bought into Bajaj Auto for its manufacturing prowess suddenly found themselves holding financial services and investment companies they hadn't asked for. The complexity of the structure—three companies with cross-holdings and different business models—confused analysts accustomed to simpler stories. Some saw it as financial engineering designed to benefit promoters at the expense of minority shareholders. The criticism was particularly sharp regarding the effective increase in promoter control in the financial services business without triggering open offer requirements.

Post demerger, the promoter group will hold 63% (promoter group+BAL) in Bajaj Finserv Ltd. Currently, they hold only 47% in Bajaj Auto Ltd. as a single entity. The incremental 16% holding has been bought at merely Rs.21.75 crores. Critics argued this was a clever maneuver to gain control without paying a control premium, though the company maintained it was a legitimate restructuring to unlock value for all shareholders.

The execution timeline revealed the meticulous planning behind the demerger. The key events unfolded in sequence: Board approval on 17.05.2007, Shareholder/Creditor approval on 18.08.2007, Court approval on 18.12.2007, Effective Date when filed with RoC, Pune on 20.02.2008, Record date for allotment on 25.03.2008, and finally Listing Date of the 2 demerged companies on 26.05.2008. Each step was carefully orchestrated to ensure regulatory compliance while minimizing market disruption.

The allocation of assets revealed the strategic thinking behind the restructuring. The auto business, with its established brand, manufacturing facilities, and export operations, would focus on what it did best—building and selling vehicles globally. The financial services business would house the rapidly growing finance and insurance operations, freed from the capital allocation conflicts of being part of a manufacturing company. The holding company would manage investments and incubate new businesses, providing patient capital without the pressure of quarterly earnings expectations.

Regarding 'Financing India' and 'De-Risking India', the de-merger that occurred in the course of 2007-08, and the consequent formation of Bajaj FinServ Limited, should enable the group to unlock greater value by widening its financial reach and portfolio. This vision, articulated by Rahul Bajaj himself, captured the transformative ambition behind what seemed like mere corporate restructuring.

The financial engineering aspects were sophisticated. The cost basis for taxation would be split among the three entities based on net worth proportions—56.5% to BHIL, 22.1% to the new BAL, and 21.4% to BFS. This meant shareholders could benefit from long-term capital gains tax exemptions if they held for over a year, making the restructuring tax-efficient. The company had essentially created a tax-free value unlock for patient shareholders while maintaining family control across the group.

The wind energy business, often overlooked in discussions of the demerger, was strategically important. Apart from financial services, it is also active in wind energy generation with an installed capacity of 65.2 MW. This provided Bajaj Finserv with a steady, predictable cash flow stream that could support the more volatile financial services businesses during their growth phase. It was patient capital generating its own returns—a masterstroke in capital allocation.

The insurance joint ventures with Allianz added another layer of complexity and opportunity. The partnerships in both life and general insurance, established in 2001, were now housed under Bajaj Finserv, creating clear ownership and strategic focus. The demerger also clarified the economics of these ventures, making it easier for investors to value them appropriately. The subsequent negotiations with Allianz about stake adjustments would be simpler with a dedicated financial services holding company as counterparty.

The demerger aimed to allow each entity to focus on its core businesses, unlock shareholder value, and facilitate benchmarking against industry peers. It created transparent structure and allowed investors to hold separate focused stocks. This transparency would prove crucial as each entity began competing for capital and talent in their respective sectors.

The cultural implications of the demerger were profound. Bajaj Auto had been a monolithic organization with a manufacturing DNA. Suddenly, the financial services team had their own company, their own board, their own destiny. This liberation unleashed entrepreneurial energy that had been constrained within the larger conglomerate. Executives who had been running "divisions" were now CEOs of substantial businesses. The change in mindset from cost center to profit center, from subsidiary to standalone, was transformative.

Risk management post-demerger became more sophisticated. Each entity could now maintain capital structures optimized for their specific businesses. The auto company could leverage up for capacity expansion during growth cycles. The financial services company could maintain regulatory capital ratios without being constrained by manufacturing investment needs. The holding company could take long-term bets without worrying about quarterly earnings volatility.

The competitive dynamics changed dramatically post-demerger. Bajaj Auto could now compete with Hero Honda and TVS without the distraction of financial services. Bajaj Finserv could compete with HDFC and ICICI without being seen as merely a captive finance unit. Each business could attract specialized talent, form focused partnerships, and make strategic acquisitions without complex internal negotiations about capital allocation.

The combined market capitalisation of the three entities stood at Rs. 4,18,220 crore as on 30th April 2023 compared to just Rs. 24,542 crore as on 31 March 2007 of erstwhile Bajaj Auto Ltd. – an increase to almost seventeen times in sixteen years. This spectacular value creation vindicated the demerger strategy, though it took years for the market to fully appreciate the wisdom of the restructuring.

The governance improvements post-demerger were substantial. Each company now had independent boards with relevant expertise. Financial services experts governed Bajaj Finserv, automotive specialists oversaw Bajaj Auto, and investment professionals guided the holding company. This specialization in governance improved decision-making speed and quality, crucial advantages in rapidly evolving markets.

Looking back, the 2007-2008 demerger was a masterclass in corporate restructuring. It demonstrated that value creation isn't just about growing revenues or cutting costs—it's about organizing businesses in ways that maximize their potential. The courage to break apart a successful conglomerate, the vision to see three focused companies where others saw one diversified giant, and the execution excellence to manage the complexity—all these elements came together in one of Indian corporate history's most successful restructurings.

The demerger also set a template for other Indian conglomerates grappling with similar challenges. The message was clear: in an era of specialization, focused companies with clear strategies and appropriate capital structures create more value than diversified conglomerates with competing priorities. The Bajaj demerger wasn't just about unlocking value—it was about unlocking potential, freeing each business to pursue its destiny unencumbered by the constraints of being part of a larger, more complex whole. As Bajaj Finserv embarked on its independent journey, it carried with it the manufacturing discipline of its parent but was now free to write its own rules in the dynamic world of financial services.

V. Building the Financial Ecosystem (2008–2015)

The post-demerger years from 2008 to 2015 marked Bajaj Finserv's transformation from a holding company with inherited assets into a sophisticated financial ecosystem. This wasn't just growth—it was the deliberate construction of interconnected financial services that would create network effects, cross-selling opportunities, and competitive moats that traditional banks couldn't replicate. The strategy was audacious: build the capabilities of a universal bank without the regulatory constraints, create the reach of a fintech without sacrificing profitability, and maintain the trust of a century-old institution while innovating like a startup.

The core architecture of this ecosystem rested on four pillars, each carefully chosen for its strategic value. 52.49% stake in Bajaj Finance Ltd., a listed non-bank with the strategy and structure of a bank, represented the lending engine—the profit generator that would fund expansion into other areas. The insurance joint ventures with Allianz SE provided long-term value creation and customer stickiness. Bajaj Allianz Life Insurance received the IRDA certificate on 3 August 2001, while Bajaj Allianz General Insurance, another joint venture with Allianz SE, was established in 2001. These partnerships brought global expertise and capital to India's underpenetrated insurance market.

The lending portfolio's evolution during this period was remarkable in its breadth and depth. The company deals in consumer lending, SME lending, commercial lending, rural lending, deposits, and wealth management. Each vertical wasn't just a product line but a gateway to understanding different customer segments, building specialized capabilities, and creating multiple touchpoints for cross-selling. The consumer lending business taught them about individual behavior, SME lending about business cycles, commercial lending about corporate relationships, and rural lending about India's vast hinterland.

The geographic expansion was equally strategic. Across 3800 towns, it has 294 consumer branches and 497 rural locations with over 33,000+ distribution points and 1,50,000+ stores. This wasn't just about physical presence but about creating a distribution advantage that digital-only players couldn't match. Each branch was a data collection point, each rural location a beachhead in underserved markets, each distribution point a node in an ever-expanding network.

Bajaj Housing Finance emerged as a critical component of the ecosystem during this period. Bajaj Housing Finance, as a wholly owned subsidiary of Bajaj Finance, provides various housing finance products, including home loans, loans against property, and lease rental discounting. Housing finance wasn't just another product—it was a gateway to long-term customer relationships, cross-selling opportunities for insurance, and a hedge against the volatility of unsecured lending. The mortgage business provided stable, secured assets that improved the overall risk profile while generating predictable cash flows.

The synergy play between these entities was where the real magic happened. A customer taking a two-wheeler loan from Bajaj Finance would be offered vehicle insurance from Bajaj Allianz General. As their income grew and they bought a home, Bajaj Housing Finance would provide the mortgage while Bajaj Allianz Life would offer life cover. The same customer's parents might invest in Bajaj Finance fixed deposits, their children might use EMI cards for consumer purchases. This wasn't just cross-selling—it was lifecycle value capture at its finest.

Technology investments during this period laid the foundation for future digital dominance. While competitors were still debating whether to invest in technology, Bajaj was building core banking systems, credit scoring algorithms, and digital interfaces. The technology wasn't flashy—no blockchain announcements or AI buzzwords—but it was effective. Loan applications could be processed in hours instead of days, credit decisions automated for standard products, and customer data integrated across business lines.

The partnership with Allianz brought more than just capital and brand value. It brought global best practices in risk management, actuarial expertise, and product innovation. The Germans' methodical approach to process and documentation complemented the Indians' entrepreneurial energy and market knowledge. This cultural fusion created insurance products tailored for Indian needs but with international standards of service and risk management.

The data advantage that emerged during this period would prove to be one of Bajaj's most enduring moats. Every loan application, every insurance claim, every payment collected added to a growing repository of customer intelligence. This wasn't just big data—it was relevant data, behavioral data, longitudinal data that captured how Indians' financial lives evolved over time. While banks had account information and fintechs had transaction data, Bajaj had the complete picture—assets, liabilities, insurance, investments, and most importantly, the connections between them.

The organizational structure evolved to support this ecosystem approach. Each business maintained operational independence while sharing critical resources—data, technology platforms, regulatory expertise, and crucially, customer relationships. The holding company structure allowed for optimal capital allocation, with profitable businesses funding growth initiatives, mature businesses providing stability, and new ventures getting patient capital to achieve scale.

Risk management in this interconnected ecosystem required sophisticated approaches. Concentration risk was managed by diversifying across products, geographies, and customer segments. Credit risk was mitigated through secured lending products like housing finance balancing unsecured consumer loans. Operational risk was controlled through standardized processes and technology. Regulatory risk was managed by maintaining conservative capital buffers and proactive compliance. The interconnected nature of the businesses actually reduced overall risk through diversification while maintaining the benefits of integration.

The human capital strategy during this period focused on building specialized expertise while maintaining cultural coherence. Insurance professionals from the joint ventures brought technical expertise, bankers hired from traditional institutions brought credit skills, and technology talent from IT services companies brought digital capabilities. But everyone was indoctrinated in the Bajaj way—customer first, long-term thinking, ethical practices, and relentless execution.

The competitive response to Bajaj's ecosystem play was fragmented and ineffective. Banks couldn't match the agility and customer focus. Insurance companies lacked the distribution reach. NBFCs didn't have the product breadth. New fintech startups had innovation but lacked trust and patient capital. By building an ecosystem rather than a single business, Bajaj had created competitive advantages that were nearly impossible to replicate.

Customer acquisition costs in this ecosystem model were dramatically lower than standalone businesses. A customer acquired for one product became a lead for multiple products. The lifetime value of customers increased exponentially as they used more services. The data from one product improved risk assessment for others. The trust built through one successful interaction reduced acquisition friction for subsequent products. This virtuous cycle of lower costs and higher values created economic advantages that compounded over time.

The regulatory navigation during this period was masterful. By maintaining separate entities for different regulated activities—NBFC for lending, insurance through joint ventures, housing finance as a subsidiary—Bajaj could optimize regulatory capital while maintaining operational synergies. The company built strong relationships with regulators, often going beyond compliance requirements, understanding that regulatory trust was as valuable as customer trust in financial services.

The capital allocation strategy reflected long-term thinking. Profits from mature businesses like consumer finance funded investments in nascent areas like rural lending. The insurance businesses, despite long gestation periods, received patient capital because the strategic value exceeded near-term returns. Technology investments were made not for immediate ROI but for building capabilities that would matter in the future. This patient capital approach, possible only because of the promoter's long-term vision and the holding company structure, created advantages that quarterly-earnings-focused competitors couldn't match.

By 2015, the ecosystem was fully operational. Millions of customers were using multiple Bajaj services. The data advantage was insurmountable. The distribution network reached into every corner of India. The brand had evolved from a two-wheeler financier to a comprehensive financial services provider. The technology infrastructure could handle millions of transactions daily. The risk management systems had been tested through economic cycles. Most importantly, the organizational capability to manage this complexity while maintaining growth and profitability had been proven.

The ecosystem wasn't just about financial metrics—it was about creating a new model for financial services in emerging markets. Unlike developed markets where specialized players dominated, or China where super-apps controlled everything, India needed a hybrid model—physical presence with digital capability, product breadth with specialized expertise, global standards with local customization. Bajaj Finserv had created this model, and the next phase would be about leveraging this ecosystem for exponential growth through product innovation and digital disruption.

VI. The Product Innovation Era: EMI Cards & Digital Disruption (2010–2020)

The conference room at Bajaj Finance's Pune headquarters buzzed with nervous energy in early 2010. The team was about to launch a product that would either revolutionize Indian retail finance or become an expensive failure. The EMI Card—a simple plastic card that would allow customers to convert any purchase into easy monthly installments—seemed almost too simple to be revolutionary. Yet this unassuming piece of plastic would democratize consumption for millions of Indians and establish Bajaj as the master of product innovation in financial services.

The insight behind the EMI Card was profound in its simplicity. Middle-class Indians wanted to buy aspirational products—smartphones, refrigerators, air conditioners—but lacked the lump sum capital. Credit cards existed but penetration was abysmal, approval rates were low, and the revolving credit model was alien to Indian sensibilities. Indians understood loans, they understood EMIs, but they were wary of credit card debt. What if you could give them the convenience of a card with the predictability of an installment loan?

The EMI Network Card comes with a pre-approved loan of up to Rs.4 lakh that customers can use across any of Bajaj Finserv's 60,000+ partner stores in more than 1,300 cities. It comes with features like flexible tenors ranging from 3 – 24 months, nil foreclosure charges, and one time document submission to allow shopping favourite products on EMI from top e-commerce platforms. The execution was brilliant—customers received pre-approved limits based on their credit profiles, could walk into any partner store, swipe the card, and convert their purchase into EMIs instantly.

The merchant ecosystem building was as important as the product itself. Bajaj didn't just issue cards and hope merchants would accept them. They built an entire infrastructure—point-of-sale machines, merchant training programs, instant settlement systems, and co-marketing initiatives. Electronics retailers were the first targets, then mobile phone stores, then furniture shops, eventually expanding to categories no one had imagined financing—gym memberships, salon treatments, even restaurant bills. The 9.8 million EMI card users will have an access to over 10,000 more retail partners added by Bajaj Finance in last one year. Company's partner network grew from 40,000 to 50,000 in 12 months, representing explosive growth in merchant acceptance. But numbers alone don't capture the revolution—this was about changing how Indians thought about consumption, credit, and financial planning.

The genius of the EMI Card wasn't technological innovation but behavioral insight. Indians had always understood installment payments—the local kirana store's "udhar khata" (credit ledger) was essentially an EMI system. Bajaj formalized this informal credit culture, added technology and scale, and made it respectable. The psychology was perfect: it wasn't debt, it was smart financial planning; it wasn't spending beyond means, it was managing cash flows efficiently.

The merchant acquisition strategy was methodical and brilliant. Rather than trying to convince all retailers simultaneously, Bajaj focused on categories with high aspirational value and moderate ticket sizes—smartphones, laptops, televisions. These products had clear upgrade cycles, strong brand preferences, and price points that made EMI financing attractive. Once consumers experienced the convenience in these categories, expansion into others became natural.

The economics for merchants were compelling. Today, Bajaj Finserv is the market leader in consumer finance, with a market share of over 50% of all goods purchased through finance in India. Merchants saw immediate sales uplift—customers who might have delayed purchases or bought cheaper alternatives could now afford premium products. The average ticket size increased, conversion rates improved, and customer satisfaction rose. Bajaj handled all credit risk, provided instant approval, and settled with merchants quickly.

The average ticket size for an EMI purchase in Tier-I town is Rs 34,000, whereas for a tier II and III market it goes up to Rs 39,000. This counterintuitive pattern revealed something profound about aspirational consumption in smaller cities. Without EMI options, Tier-II and Tier-III consumers often had to save for months or years for big purchases. With EMI cards, they could finally buy the products they wanted, often choosing better models than their metro counterparts who had more financing options.

The digital transformation of the EMI Card happened gradually then suddenly. Initially, the card was purely physical, used at offline stores. But as e-commerce exploded in India, Bajaj quickly adapted. Bajaj Finserv has tie-up with all leading e-tailers like Amazon and Flipkart, as well as partnerships with all the leading manufacturers, brands and retailers across categories. The online integration wasn't just about technology—it required building trust with e-commerce platforms, integrating with their checkout systems, and ensuring seamless customer experience.

The Bajaj Finserv EMI Store, launched during this period, represented the next evolution. Rather than being just a financing provider, Bajaj became a marketplace itself. Financing over 2.5 million transactions in FY2022 with 48% growth, onboarding 140 online partners for total of 210 partners, with 13 on Bajaj Finserv App. This wasn't just about disintermediation but about owning the complete customer journey—discovery, selection, financing, and purchase.

The data advantage from EMI Cards was extraordinary. Every transaction provided insights into consumer behavior—what products they bought, at what price points, in which seasons, after how many store visits. This wasn't just transaction data but intent data, aspiration data, lifecycle data. A customer buying a Rs. 15,000 phone on EMI was likely to buy a Rs. 30,000 phone three years later. Someone financing furniture was probably newly married or moving homes—perfect timing for insurance products.

The risk management for EMI Cards required sophisticated approaches. Unlike traditional loans with single large disbursements, EMI Cards involved continuous exposure as customers made multiple purchases. Bajaj developed dynamic limit management systems, adjusting available credit based on repayment behavior, income changes, and macro-economic conditions. The ability to instantly block cards, adjust limits, and modify terms gave them control that traditional credit products lacked.

The competitive response from banks was initially dismissive, then panicked, then imitative. Banks launched their own EMI programs but struggled with execution. Their systems weren't designed for point-of-sale financing, their approval processes were slow, their merchant relationships were weak. By the time banks recognized the threat, Bajaj had locked up exclusive partnerships with key retailers and built insurmountable scale advantages.

The No Cost EMI innovation was particularly brilliant. While technically the cost was borne by merchants through subvention, consumers perceived it as interest-free credit. The EMI Card comes with no hidden charges, and most importantly, payment is through 'No Cost EMIs'—which means no more exorbitant interest. This perception drove adoption among middle-class consumers who were interest-rate sensitive but aspired to premium products.

The process simplification was relentless. Simply walk into any store and share basic documents like address proof, income proof and a cancelled cheque. The company representative will check the customer's eligibility online and the loan is approved instantly, with immediate disbursal. What traditionally took weeks in banking now happened in minutes. This speed wasn't just convenience—it was essential for capturing impulse purchases and competing with cash transactions.

The omnichannel strategy that emerged during this period was sophisticated. Online and offline weren't separate channels but complementary parts of the customer journey. A customer might research online, visit a store to experience the product, check prices on the app, and finally purchase online with store pickup. The EMI Card worked seamlessly across all touchpoints, with consistent offers and instant approvals.

Four proprietary marketplaces emerged during this era: EMI Store, Insurance Marketplace, Investment Marketplace, and Broking App. Each marketplace wasn't just a distribution channel but a data collection engine, customer engagement platform, and cross-selling opportunity. The marketplaces created a virtuous cycle—more customers attracted more merchants, which attracted more customers.

The partnership ecosystem expanded beyond traditional retail. Bajaj Pay wallet with UPI, EMI card, credit card options and Triple Reward system, creating payments solution for 120,000 merchant partners. This wasn't just about payments but about embedding Bajaj into daily transaction flows. Every UPI payment was a touchpoint, every wallet transaction a data point, every reward redemption an engagement opportunity.

The technology infrastructure built during this period was remarkable in its ambition and execution. By 2020, 60% of workload on cloud, expanding to create super-app integrating five proprietary marketplaces. This wasn't just lift-and-shift cloud migration but fundamental re-architecture for scale, flexibility, and innovation. The cloud infrastructure enabled rapid product launches, instant scaling during sales events, and sophisticated analytics that wouldn't have been possible with traditional systems.

The customer acquisition cost economics were transformed by the EMI Card model. Traditional lending required expensive marketing, complex applications, and high rejection rates. With EMI Cards, customers were acquired at point of purchase when motivation was highest. The card itself became a marketing tool—every use reminded customers of Bajaj's value proposition. Word-of-mouth from satisfied customers was more powerful than any advertising campaign.

The regulatory navigation during this period was complex. EMI Cards occupied a grey area—not quite credit cards, not traditional loans. Bajaj worked closely with regulators to ensure compliance while maintaining product innovation. They proactively implemented consumer protection measures, transparent pricing, and responsible lending practices, building regulatory trust that would prove valuable when rules eventually formalized.

The cultural impact of EMI Cards extended beyond finance. They democratized consumption in India, making middle-class lifestyle accessible to millions. The teenager in Tier-III city could own the same iPhone as their Mumbai cousin. The young professional could furnish their apartment without waiting years to save. The small business owner could upgrade equipment without depleting working capital. This wasn't just financial inclusion—it was social inclusion.

By 2020, the EMI Card had evolved from a simple payment instrument to a platform for financial services innovation. The Insta EMI Card with instant digital issuance, the co-branded cards with partners like Airtel, the category-specific cards for healthcare and education—each innovation expanded the addressable market and deepened customer relationships. The foundation was set for the next phase—building a super-app that would consolidate all these innovations into a single, powerful platform.

VII. The Platform Play: Super App & Ecosystem Expansion (2020–Present)

The year 2020 marked an inflection point in Bajaj Finserv's evolution. As the pandemic forced India into lockdown, digital became not just important but essential. While traditional financial institutions scrambled to adapt, Bajaj was ready. The Bajaj Finserv App is trusted by 50 million+ customers across India for their financial & payment needs—a number that seemed impossible just years earlier. But this wasn't just about downloads or user counts; it was about fundamentally reimagining financial services as a platform play.

The super-app strategy emerged from a simple insight: customers didn't want multiple apps for different financial needs. They wanted one trusted platform for everything—loans, investments, insurance, payments, shopping. Initially dubbed a 'Super App', the Bajaj Finserv App is your all-in-one application for shopping and finance-related matters. The ambition was audacious: compete with specialized players in each vertical while maintaining the coherence of a unified platform.

The app architecture was deliberately comprehensive. You can apply for loans including personal loan, home loan, gold loan, business loan, etc. You can shop offline from 1 million+ products on Easy EMIs, invest in Fixed deposit, get insurance & do much more. You can also easily pay electricity bill, recharge your mobile, DTH service & transfer money using BHIM UPI. Each feature wasn't just bolted on but integrated into a seamless experience where data and insights from one service enhanced others.

The marketplace strategy within the app created powerful network effects. Shop from 1 million+ products at 1.5 lakh+ stores across India. From electronics to sports equipment to smartphones to furniture - shop everything on No-cost EMIs. This wasn't just e-commerce but "phygital" commerce—bridging online discovery with offline fulfillment, digital payments with physical experiences. The app became a discovery platform, financing enabler, and transaction facilitator rolled into one.

Bajaj Finserv Direct, operating as Bajaj Markets, emerged as the digital-first avatar of the company's distribution strategy. It serves as a registered Corporate Agent under Insurance Regulatory and Development Authority, a registered Investment Adviser under Securities and Exchange Board of India, a registered third-party app provider for Unified Payments Interface payments, and a digital lending platform for its partner institutions. This regulatory compliance across multiple verticals gave Bajaj the license to operate as a true financial super-app.

The health-tech venture represented a bold expansion beyond traditional financial services. Bajaj Finserv Health Ltd wasn't just about health insurance but about reimagining healthcare delivery itself. Bajaj Finserv Health Digital with over 120,000 doctors, 6,000+ lab touchpoints, and 1,800+ hospitals created an integrated healthcare ecosystem. The vision was clear: healthcare and financial services were converging, and Bajaj would be at the intersection.

The integration with health services revealed sophisticated platform thinking. A customer searching for doctors on the health platform was likely to need health insurance. Someone booking regular health checkups might be interested in wellness products financed through EMI. Health emergencies often required instant loans. By owning the healthcare discovery and delivery platform, Bajaj could anticipate and fulfill financial needs proactively rather than reactively.

The mutual fund business launch demonstrated Bajaj's ambition to be a comprehensive wealth platform. Bajaj Finserv Asset Management commencing mutual fund operations in March 2023, with ₹16,293 crore AAUM for quarter ending September 2024, showed rapid scale achievement. The integration with the existing customer base provided instant distribution, while the app platform enabled seamless investment experiences.

The technology transformation underpinning the super-app was massive. Creating your unique Bajaj Pay UPI ID, enjoy UPI offers & send/receive money, or pay bills by scanning any QR code & authorize your UPI payments by entering the UPI PIN. This wasn't just about adding UPI but about making payments the engagement layer for all other services. Every payment was an opportunity for cross-sell, every transaction a data point for better credit decisions.

The merchant ecosystem expanded dramatically through the platform approach. Bajaj Finserv for Business became the B2B counterpart to the consumer app. Accept payments for your business and boost your sales whether you are a merchant, a small business or a start-up owner, a freelancer, a retail manager, or a delivery service provider. By serving both consumers and merchants, Bajaj created a two-sided platform with powerful network effects.

The data integration across services created unprecedented customer intelligence. A user's loan repayment history informed insurance pricing. Investment patterns influenced credit limits. Shopping behavior predicted loan demand. Payment frequency indicated income stability. This 360-degree view enabled personalized offerings that seemed almost prescient—the right product at the right time through the right channel.

The user experience design philosophy prioritized simplicity despite complexity. With dozens of products and hundreds of features, the app could have been overwhelming. Instead, intelligent personalization ensured users saw relevant options. First-time users might see personal loans prominently, while existing customers saw investment options. Young professionals saw education loans, while families saw insurance products. The app adapted to user needs rather than forcing users to navigate complexity.

The Allianz partnership evolution during this period was significant. In October 2024 stock filing, Bajaj Finserv announced that Allianz is considering exiting their life and general insurance joint ventures due to its strategic priorities. The subsequent announcement of acquiring stakes for ₹10,400 crore demonstrated Bajaj's confidence in the insurance business and financial strength to make large acquisitions.

The ecosystem expansion through strategic acquisitions accelerated. In early 2024, the company acquired Bangalore-based Vidal Healthcare Services and its two subsidiaries as part of its pan-India expansion of outpatient delivery services. Each acquisition wasn't just about adding capabilities but about filling gaps in the ecosystem, creating more touchpoints for customer engagement, and generating more data for intelligent services.

The regulatory compliance across multiple verticals within a single platform was a masterclass in navigation. Different financial services had different regulators, rules, and requirements. The app had to ensure data privacy while enabling cross-sell, maintain service boundaries while creating seamless experiences, follow lending norms while innovating on products. This regulatory juggling act required sophisticated governance and technology architecture.

The competitive dynamics in the super-app space intensified. While global players like Google Pay and Amazon Pay focused on payments, and vertical specialists like PolicyBazaar dominated insurance distribution, Bajaj's integrated approach created unique advantages. The combination of lending capabilities, insurance underwriting, investment products, and payment infrastructure in one platform was difficult to replicate.

The customer acquisition through the platform model transformed economics. Traditional customer acquisition costs in financial services ranged from thousands to tens of thousands of rupees. Through the app, customers often onboarded themselves for free services like bill payments or UPI, then gradually adopted paid products. The platform became a customer acquisition engine with negative acquisition costs—customers paid to join through service usage.

The risk management in a platform model required new approaches. Concentration risk increased as customers used multiple products. A customer defaulting on a loan might also stop insurance premiums and withdraw investments. But the platform also provided early warning signals—changes in payment patterns, app usage frequency, or service cancellations could predict credit problems before they materialized.

The partnership ecosystem expanded beyond traditional boundaries. Choose from 100+ brand partners that offer a diverse range of products and services. These weren't just distribution partnerships but deep integrations where partner services became native platform features. The boundaries between Bajaj services and partner services blurred, creating a seamless experience ecosystem.

The investment marketplace strategy demonstrated platform leverage. Instead of building every capability internally, Bajaj became an aggregator and curator. Invest in any Mutual Fund via monthly SIPs or pay a lumpsum. Make the most of your investment by paying 0% distributor commission. By aggregating demand and negotiating better terms, Bajaj could offer superior value while earning platform fees.

The BYTE program for technology talent acquisition reflected the platform's technical complexity. Offering 260 engineers from seven campuses, the program wasn't just about hiring but about building a technology-first culture. These engineers weren't maintaining systems but building the future—AI-driven credit decisions, real-time personalization engines, blockchain-based verification systems.

The international expansion possibilities through the platform model became apparent. Unlike physical banking that required licenses and branches in each country, the digital platform could potentially serve Indian diaspora globally, then expand to local populations. The technology stack, risk models, and product innovations developed for India could be adapted for other emerging markets.

Looking at the platform's evolution from 2020 to present, the transformation has been remarkable. What started as a digital channel for existing services became a ecosystem platform rivaling global tech giants. The Bajaj Finserv app serving 35.5 million customers wasn't just a number but represented millions of Indians whose financial lives were being transformed through technology. The platform play wasn't complete—new services, partnerships, and innovations continued to expand the ecosystem. But the foundation was solid: a trusted brand, comprehensive services, superior technology, and most importantly, deep customer relationships that would power growth for decades to come.

VIII. Financial Performance & Scale Economics

The numbers tell a story of extraordinary scale and efficiency. Its assets under management (AUM) grew by 29 per cent to Rs 3.73 trillion as of September 30, 2024, from Rs 2.9 trillion as of September 30, 2023. Bajaj Finance Ltd. holding massive ₹247,379 crore AUM represents an asset base larger than many mid-sized banks, achieved without the regulatory capital requirements or branch infrastructure of traditional banking. But the real story isn't the absolute numbers—it's the economics behind them.

The unit economics of Bajaj's model reveal why financial services, executed properly, can be one of the best businesses in the world. Deposits contributed to 20 per cent of consolidated borrowings as of September 30, 2024. This deposit franchise, built without being a bank, provides stable, relatively cheap funding that enhances margins. The cost of funds advantage compounds over time—better margins enable competitive pricing, which drives volume, which improves operational leverage, which further enhances margins.

Serving over 100 million customers isn't just a vanity metric—it's a moat. New loans booked were up 14 per cent to 9.69 million in Q2, compared with 8.53 million in Q2 FY24. The customer acquisition machine runs continuously, with each new customer representing not just immediate revenue but lifetime value across multiple products. The network effects are powerful: more customers attract more merchants, who attract more customers, creating a virtuous cycle that competitors struggle to break.

The insurance subsidiaries demonstrate the power of patient capital in financial services. ₹90,584 crore AUM of Bajaj Allianz Life Insurance Company represents premiums collected and invested over decades, generating float that can be deployed profitably while waiting for claims. The general insurance business, having successfully sold over 28 million policies through Bajaj Allianz General Insurance, provides both underwriting profits and investment income, a double engine of value creation.

The diversification across business lines creates remarkable stability. Overall, the AUM surged by 34%, from ₹247,379 crore in FY 2023 to ₹330,615 in FY 2024. In FY24 Q4, the net interest income swelled by 28%, reaching ₹8,013 crore compared to ₹6,254 crore recorded in the same quarter in FY23. When consumer lending slows, commercial picks up. When urban markets saturate, rural provides growth. When credit cycles turn negative, insurance and fee income provide cushion. This isn't random diversification but strategic portfolio construction designed to smooth earnings volatility.

The margin dynamics reveal sophisticated pricing power. Despite intense competition from banks, fintechs, and other NBFCs, Bajaj maintains healthy margins through superior risk assessment, operational efficiency, and value-added services. The company estimates that COF has peaked as of Q2 and net interest margin has stabilised in Q2Fy25, Bajaj Finance said in an analyst presentation. The ability to maintain margins while growing rapidly demonstrates pricing discipline rare in financial services.

The operational leverage in the model is extraordinary. Technology investments create high fixed costs initially but marginal costs approaching zero for additional transactions. A loan processing system that costs crores to build can handle millions of applications with minimal incremental expense. This operating leverage means that revenue growth drops disproportionately to the bottom line, creating expanding margins as scale increases.

The ROE dynamics deserve special attention. Its capital adequacy ratio (CAR) stood at 21.69 per cent with Tier I of 20.90 per cent as of September 30, 2024. While maintaining conservative capital ratios for stability, Bajaj generates returns on equity that most banks can only dream of. The secret lies in the business mix—high-yielding unsecured loans balanced with secured mortgages, fee-generating insurance products complementing spread-based lending, and efficient capital allocation across businesses.

The wind energy generation with installed capacity of 65.2 MW might seem like an oddity in a financial services company, but it reveals sophisticated thinking about capital allocation. These assets provide stable, predictable cash flows uncorrelated with financial markets, acting as a natural hedge while generating returns above the cost of capital. It's patient capital generating its own returns while waiting for deployment opportunities.

The deposit franchise evolution has been remarkable. The deposit book grew by 21 per cent year-on-year and stood at Rs 66,131 crore as of September 30, 2024. Without bank branch networks or government guarantees, Bajaj built a deposit base through trust, superior service, and competitive rates. These deposits provide stable funding reducing dependence on wholesale markets and improving margins.

The fee income streams demonstrate the platform's monetization potential. The company in a statement said its fees and commission income rose nine per cent year-on-year to Rs 1,426 crore in Q1 FY25. Beyond traditional interest income, Bajaj earns processing fees, insurance commissions, distribution fees, and platform charges. These fee streams are typically more stable than interest income and require minimal capital, improving overall return metrics.

Comparative analysis with traditional banks reveals Bajaj's advantages. While banks struggle with legacy technology, regulatory constraints, and bureaucratic decision-making, Bajaj operates with startup agility at massive scale. The cost-to-income ratios are superior, customer acquisition costs lower, and time-to-market for new products measured in weeks not years. Yet unlike fintech startups, Bajaj has the balance sheet strength and regulatory relationships to weather economic storms.

The comparison with HDFC and ICICI is particularly instructive. While these banking giants have broader product suites and regulatory advantages, Bajaj's focused approach generates superior returns. Without the drag of priority sector lending, CRR/SLR requirements, or legacy branch networks, Bajaj can optimize capital allocation purely for returns. The market recognizes this efficiency, often valuing Bajaj at premium multiples despite lacking a banking license.

International comparisons are even more revealing. The blueprint envisages your Company to become a dominant payments and financial services company in India over the medium term. To be a leading payments and financial services company in India with a customer franchise of over 150 million, market share of 3% of payments Gross Merchandise Value (GMV), 3%-4% of total This ambition puts Bajaj in league with global financial services giants, but with the growth tailwinds of an emerging market.

The credit quality metrics demonstrate sophisticated risk management. Bajaj Finance in a statement said net loan losses and provisions for Q2FY25 were Rs 1,909 crore, up from Rs 1,077 crore in Q2FY24. Loan losses and provisions remained elevated in Q2. While provisions have increased, they remain manageable relative to the book size and pricing power. The ability to maintain profitability despite elevated provisions shows the robustness of the business model.

The growth trajectory remains compelling. For FY25, it predicts a growth of 26-28%, boosted by new secure businesses introduced in FY24 like LAP, new car financing, and tractor finance. This isn't growth for growth's sake but strategic expansion into adjacencies where existing capabilities provide competitive advantages. Each new product line leverages existing infrastructure while adding incremental revenue streams.

The technology investments impact on margins is becoming apparent. Since inception, the Company has leveraged technology to launch 26 product lines and 51 product variants for retail, MSME and commercial consumers, with major product innovations such as the EMI card and Flexi. The ability to launch new products rapidly and efficiently creates first-mover advantages in emerging segments while the technology platform enables superior customer experience at lower costs.

The capital allocation framework demonstrates long-term thinking. Rather than maximizing short-term earnings, Bajaj invests in new businesses that might be dilutive initially but create long-term value. New lines of businesses have started contributing 2-3 per cent of AUM growth, it said. These nascent businesses, nurtured with patient capital, become tomorrow's growth engines.

The ecosystem economics multiply standalone business values. A customer acquired for personal loans generates revenue through insurance premiums, investment products, and payment fees. The lifetime value of an ecosystem customer can be 5-10x that of a single-product customer, fundamentally changing acquisition economics. This ecosystem premium is reflected in valuation multiples that exceed pure-play comparables.

The resilience of the model was tested during COVID-19 and proved robust. While credit costs spiked temporarily, the diversified business model, conservative underwriting, and strong capital position enabled Bajaj to not just survive but gain market share. The crisis accelerated digital adoption, playing to Bajaj's strengths and widening the competitive moat.

Looking at the financial architecture holistically, Bajaj has created something unique—the profitability of a focused lender, the stability of a diversified financial conglomerate, the growth of a fintech startup, and the trust of a century-old institution. The financial performance isn't just about past success but demonstrates a model that can compound value for decades. The scale economics ensure that competitive advantages strengthen rather than erode with size, a rare achievement in any industry but particularly impressive in the competitive landscape of financial services.

IX. Playbook: The Bajaj Finserv Method

The Bajaj Finserv playbook isn't written in any manual or taught in any business school. It's a living methodology, evolved over decades through trial, error, and relentless iteration. Understanding this playbook means decoding how a company builds competitive moats in financial services—an industry where products are commodities, regulations are stringent, and competition is fierce. The Bajaj method demonstrates that sustainable competitive advantage comes not from any single factor but from the intricate interweaving of multiple reinforcing elements.

The proprietary intelligence asset that Bajaj has built represents one of the most underappreciated moats in Indian business. Every loan application, insurance claim, payment transaction, and investment decision feeds into a vast data repository that becomes more valuable with each passing day. This isn't just big data—it's longitudinal, behavioral, interconnected data that captures the complete financial lifecycle of Indian consumers. When a customer applies for a loan, Bajaj doesn't just see their current income and credit score; they see their insurance premium payment history, their EMI card usage patterns, their investment behaviors, their payment regularity across multiple products. This 360-degree view enables risk assessment and pricing decisions that competitors using fragmented data simply cannot match.

The data moat creates a virtuous cycle that accelerates with scale. Better data enables better risk assessment, which reduces losses, which improves pricing, which attracts more customers, which generates more data. This flywheel effect means that Bajaj's competitive advantage actually strengthens as the company grows—a rare dynamic in business where scale often breeds complacency. The artificial intelligence and machine learning models trained on this data become more accurate with each iteration, creating predictive capabilities that seem almost prescient to customers receiving perfectly timed product offers.

The brand moat in financial services is particularly powerful because trust, once earned, creates switching costs that go beyond mere inconvenience. The Bajaj name, built over a century, carries weight in Indian households that no amount of advertising can buy. When a family has financed their scooter, insured their home, and invested their savings with Bajaj across generations, the relationship transcends commercial transaction. This emotional equity manifests in lower acquisition costs, higher retention rates, and powerful word-of-mouth marketing that no digital-first competitor can replicate.

The diversified financial ecosystem creates cross-selling opportunities that dramatically improve unit economics. A customer acquired for a two-wheeler loan at a marginal profit becomes highly profitable when they subsequently take home loans, buy insurance, invest in fixed deposits, and use payment services. The ecosystem ensures that Bajaj captures an increasing share of wallet over the customer's lifetime, turning the traditional banking model of 3-4 products per customer into 8-10 products or more. This isn't aggressive selling but intelligent orchestration—using data to identify life moments when specific products become relevant and presenting them through the customer's preferred channel at the optimal time.

The distribution advantage that Bajaj has built represents a masterclass in channel strategy. The hybrid model—combining digital efficiency with physical presence—provides reach and richness that pure-play digital or traditional players cannot match. In metros, the digital app might be the primary interface, while in smaller towns, the local Bajaj Finance office provides the trust and hand-holding that customers need. The 33,000+ distribution points aren't just locations but nodes in a network that provides market intelligence, customer support, and local relationship management that algorithms alone cannot deliver.

The "Bank without being a Bank" strategy reveals sophisticated regulatory arbitrage. By operating as an NBFC rather than a bank, Bajaj avoids priority sector lending requirements, CRR/SLR obligations, and the bureaucratic oversight that constrains traditional banks. Yet through deposits, payments, and comprehensive financial services, Bajaj captures most of the value that banks create. This regulatory positioning provides flexibility to enter new businesses quickly, experiment with products, and optimize capital allocation purely for returns rather than regulatory compliance.

Managing complexity as a conglomerate requires organizational capabilities that take decades to build. Each business—lending, insurance, investments, payments—has different dynamics, regulations, and success factors. Yet Bajaj manages this complexity through a combination of operational autonomy and strategic integration. Business units operate independently day-to-day but share critical resources like technology platforms, risk management systems, and customer data. This federated structure provides the agility of smaller firms with the resources of a conglomerate.