JB Chemicals & Pharmaceuticals: From Family Legacy to Private Equity Powerhouse

I. Introduction & Episode Roadmap

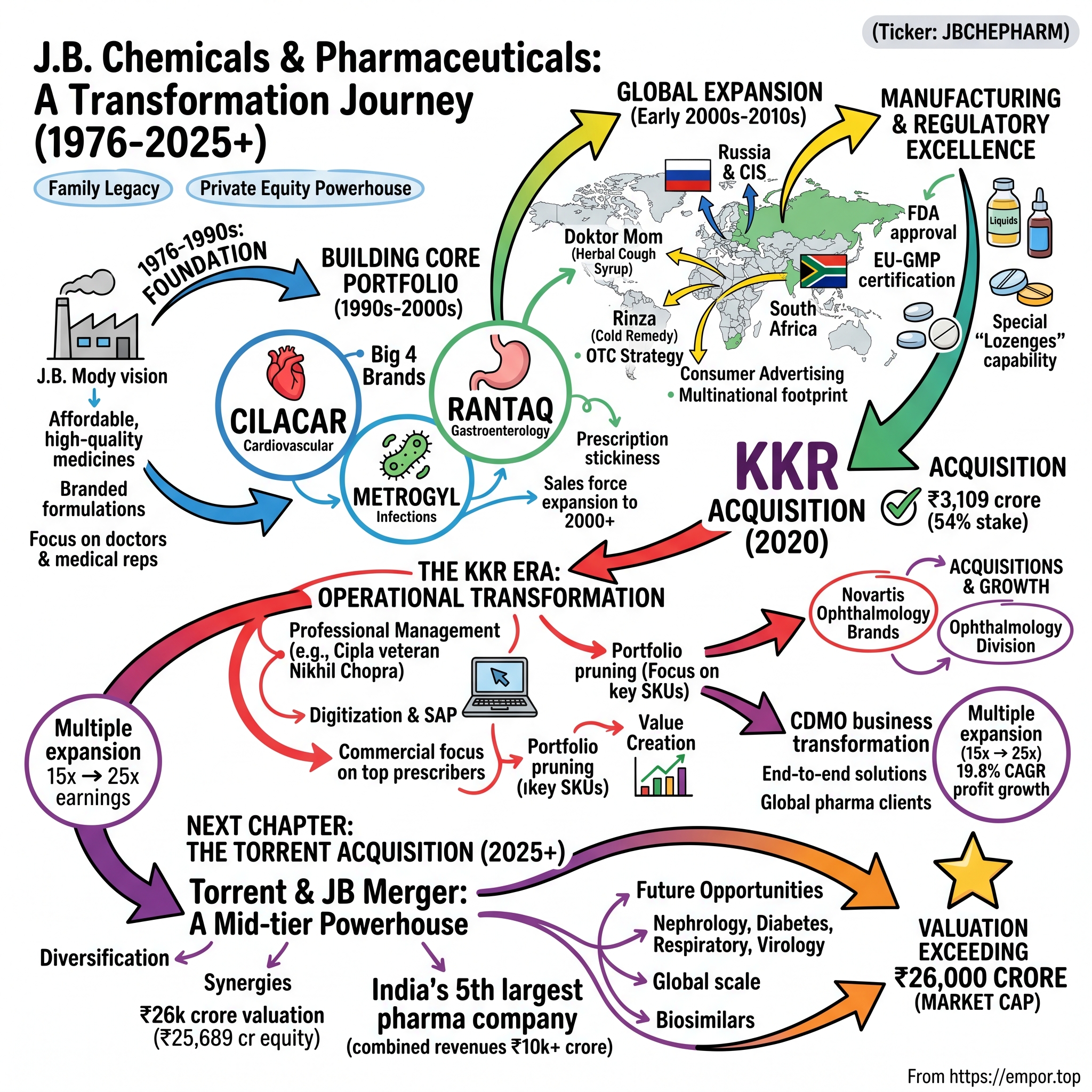

The boardroom at JB Chemicals' Mumbai headquarters was unusually quiet on that December morning in 2019. J.B. Mody's children—who had inherited the pharmaceutical empire their father built from scratch—were about to sign papers that would end 43 years of family control. Across the table sat representatives from KKR, one of the world's most sophisticated private equity firms, ready to write a ₹3,109 crore check for a controlling stake in a company that had become synonymous with trusted, affordable medicines across India and Russia.

This wasn't just another pharma deal. It was the beginning of an extraordinary transformation that would see JB Chemicals' value multiply over 3.5 times in just five years, culminating in Torrent Pharmaceuticals' blockbuster acquisition in 2025—creating what might become India's most formidable mid-tier pharmaceutical powerhouse. Today, with a market capitalization exceeding ₹26,000 crore and revenue of ₹4,008 crore generating profits of ₹685 crore, JB Chemicals stands as testament to what happens when patient capital meets operational excellence in Indian healthcare. This is that story—a journey through family entrepreneurship, international expansion, private equity transformation, and ultimately, the creation of one of India's most compelling pharmaceutical consolidation plays.

The narrative unfolds across five distinct acts: the foundational years under J.B. Mody's vision, the building of iconic brands that became household names, the audacious international expansion into Russia and emerging markets, the transformative KKR partnership that rewrote the playbook for PE investments in Indian pharma, and finally, the Torrent acquisition that promises to reshape India's mid-tier pharmaceutical landscape.

For investors and business strategists, this isn't just another M&A story. It's a masterclass in value creation, operational transformation, and strategic timing in one of the world's most complex and regulated industries. Let's dive into how a Mumbai-based family business became the crown jewel in two of the most sophisticated financial transactions Indian pharma has witnessed.

II. The Mody Foundation & Early Years (1976–1990s)

The year was 1976. India had just emerged from the Emergency, pharmaceutical multinationals dominated the market with expensive imported medicines, and a quiet revolution was brewing in Mumbai's industrial corridors. J.B. Mody, an entrepreneur with a vision for affordable healthcare, registered a small company called JB Chemicals & Pharmaceuticals Laboratories with modest capital and outsized ambitions.

Unlike the typical pharma startup story of that era—which usually involved reverse-engineering Western molecules or setting up contract manufacturing for MNCs—Mody had a different playbook. He wanted to build a branded formulations business from day one, creating medicines that Indian doctors would trust and patients could afford. This was audacious. The Indian pharmaceutical market of the 1970s was deeply fragmented, with over 20,000 players competing on price alone. Building brands required something most Indian pharma companies lacked: patient capital and an unwavering focus on quality.

Established in 1976, JB Chemicals emerged as one of India's leading pharmaceutical companies, but the journey was far from smooth. The initial years were marked by the typical struggles of any manufacturing startup in license-raj India—securing industrial permits, importing machinery, finding skilled chemists willing to leave established companies. Mody's breakthrough came from an unexpected source: the relationships he cultivated with medical representatives and doctors.

While competitors focused on pushing generic molecules at the lowest possible price, Mody invested in what seemed like luxuries—medical education programs, consistent product quality, and most importantly, a sales force that understood medicine, not just margins. He recruited pharmacists and science graduates, trained them rigorously, and sent them to engage doctors in clinical discussions rather than transactional negotiations.

The company's early manufacturing facility in Mumbai was modest—a few thousand square feet producing basic formulations. But Mody insisted on something revolutionary for that time: documented standard operating procedures for every batch. This obsession with process would later become JB's calling card when international regulatory approvals became the gateway to global markets.

By the mid-1980s, JB Chemicals had established its first significant manufacturing presence, moving beyond Mumbai to set up facilities that would form the backbone of its production capabilities for decades. The company wasn't just making tablets and syrups; it was building an institutional memory of pharmaceutical manufacturing excellence that would prove invaluable when FDA inspectors came calling years later.

The formulation strategy was deliberately focused. Rather than chasing every therapeutic area, Mody concentrated on segments where Indian patients had the greatest unmet needs—gastrointestinal disorders, infections, and cardiovascular diseases. These weren't glamorous areas, but they were massive markets where a trusted brand could command premium pricing even in price-sensitive India.

What set JB apart in these early years wasn't just what it made, but how it thought about the business. While peers were content being commodity players, Mody was building something more ambitious—a pharmaceutical company that could stand toe-to-toe with multinationals on quality while maintaining the cost advantages of Indian manufacturing. This dual focus on quality and efficiency would become the company's DNA, passed down through generations of managers and eventually catching the eye of global private equity giants.

As the 1980s drew to a close, JB Chemicals had quietly laid the foundation for what would become one of India's most trusted pharmaceutical brands. The company had manufacturing capabilities, a growing product portfolio, and most importantly, relationships with thousands of doctors who had come to rely on its medicines. The stage was set for the next phase—building brands that would define therapeutic categories for generations of Indian patients.

III. Building the Core Portfolio (1990s–2000s)

The conference room at Mumbai's Taj Mahal Hotel was packed with cardiologists in early 1995. JB Chemicals had flown in leading heart specialists from across India for what it called a "clinical education symposium." But everyone knew the real agenda—the company was about to launch Cilacar, its ambitious bet on the cardiovascular market. As presentations on calcium channel blockers droned on, J.B. Mody's son sat nervously in the back row. The family had invested everything in this launch. If Cilacar failed, JB Chemicals would remain a mid-tier player forever.

Cilacar didn't just succeed—it redefined what an Indian pharmaceutical brand could achieve. Within five years, it became the preferred choice for hypertension management among Indian cardiologists, competing head-to-head with multinational brands costing three times as much. The secret wasn't just competitive pricing; it was JB's obsessive focus on consistency. Every batch of Cilacar had identical dissolution profiles, bioavailability studies that matched the innovator molecule, and packaging that conveyed premium quality despite the affordable price point.

But Cilacar was just the opening move in a carefully orchestrated brand-building strategy. The company systematically launched what would become its "Big Four"—Cilacar for cardiovascular, Metrogyl for infections, Nicardia for hypertension, and Rantac for gastric disorders. Each launch followed the same playbook: identify a large therapeutic need, develop a formulation that matched or exceeded multinational quality standards, price it at 40-60% below MNC brands, and invest heavily in medical education and doctor engagement.

By this period, JB had positioned 6 brands in the top 300 domestic formulation brands, a remarkable achievement for a company competing against both multinational giants and aggressive Indian competitors. The company had cracked the code that eluded most Indian pharma companies—building prescription brands that commanded loyalty beyond just price.

Metrogyl became particularly interesting from a strategic perspective. While metronidazole was a commodity molecule available from hundreds of manufacturers, JB's version became the gold standard in Indian hospitals. The company achieved this through relentless focus on what it called "prescription stickiness"—ensuring that once a doctor prescribed Metrogyl and saw positive outcomes, they would continue prescribing it despite cheaper alternatives flooding the market.

The sales force expansion during this period was remarkable. From a few hundred medical representatives in 1990, JB built a 2,000-person field force by 2005. But unlike the industry norm of hiring anyone with a science degree, JB invested in what competitors mocked as "over-qualification"—pharmacists with deep therapeutic knowledge, continuous medical education, and importantly, the ability to engage specialists in clinical discussions rather than just commercial negotiations.

The company became big players in gastroenterology, hypertension, and dermatology, but the real masterstroke was the portfolio synergy. A doctor prescribing Cilacar for hypertension would likely also need Rantac for gastric protection—a common side effect of many cardiac medications. The medical representative could position both products in a single call, improving productivity while providing comprehensive therapeutic solutions.

The manufacturing infrastructure kept pace with brand growth. The company expanded beyond its initial facilities, setting up state-of-the-art plants that would later become the foundation for international regulatory approvals. But more than physical infrastructure, JB was building something intangible—a reputation for reliability that would become its greatest asset.

By 2000, the transformation was complete. JB Chemicals was no longer just another Indian pharma company making generic medicines. It had become a brand-driven organization with products that doctors actively requested, patients trusted, and competitors struggled to dislodge despite price advantages. The company's ranking had steadily climbed, reaching the top 30 in the Indian pharmaceutical market—remarkable for a company that had started just 25 years earlier with no multinational backing or government support.

The early 2000s brought new challenges—patent protection under TRIPS, increased regulatory scrutiny, and aggressive competition from both Indian and multinational players. But JB's brand fortress held strong. Cilacar continued growing at 20% annually, Metrogyl expanded into new formulations and indications, and the company's reputation with the medical community provided a moat that pure generic players couldn't breach.

The success of this period wasn't just about individual brands—it was about proving that an Indian company could build and sustain pharmaceutical brands that competed on quality and efficacy rather than just price. This brand equity would become crucial when JB decided to expand internationally, providing credibility in markets where "Made in India" still carried stigma. The foundation was set for the company's most audacious move yet—taking these India-proven brands to the vast, untapped markets of Russia and the CIS.

IV. Russia & CIS Expansion: The OTC Gamble

The Moscow winter of 2001 was particularly brutal, even by Russian standards. As JB Chemicals' newly appointed country head stepped off the plane at Domodedovo Airport, the temperature gauge read minus 27 degrees Celsius. He had been sent to establish JB's presence in a market that had defeated numerous Indian pharmaceutical companies—a post-Soviet healthcare system where corruption was rampant, regulatory frameworks changed monthly, and payment terms could stretch to 180 days if you were lucky enough to get paid at all.

Yet within this chaos, JB's leadership saw opportunity. The Russian OTC (over-the-counter) market was exploding. After decades of state-controlled healthcare, Russian consumers were discovering self-medication, creating a multi-billion dollar opportunity for cough syrups, cold remedies, and digestive aids. More importantly, Russians had a peculiar preference—they trusted brands with "exotic" foreign origins, associating them with quality and efficacy unavailable in Soviet-era medicines.

JB's masterstroke wasn't trying to replicate its India strategy of prescription brands. Instead, it acquired and developed two OTC brands that would become household names across Russia and CIS countries: Doktor Mom and Rinza. The naming itself was genius—Doktor Mom played into the Russian reverence for maternal care and natural remedies, while Rinza sounded sophisticated and Western, despite being manufactured in Gujarat.

Doktor Mom, a herbal cough syrup, became JB's Trojan horse into Russian homes. The company positioned it not as an Indian Ayurvedic product (which had limited appeal) but as a "natural European-style" remedy. The packaging was redesigned completely—gone were the typical Indian pharmaceutical aesthetics, replaced by designs that wouldn't look out of place in a Swiss pharmacy. The product was priced at a premium to local brands but below Western imports, hitting the sweet spot of aspiration and affordability.

The distribution strategy was equally unconventional. Rather than working through the traditional pharmaceutical distributors who demanded massive upfront payments and offered no guarantee of retail placement, JB partnered with Protek and Katren, the emerging pharmacy chains that were modernizing Russian pharmaceutical retail. These chains wanted differentiated products that could drive foot traffic and command higher margins than commodity generics.

Building the brand required massive investment in consumer advertising—something Indian pharmaceutical companies rarely did. JB sponsored prime-time television spots during Russian soap operas, placed advertisements in Metro stations, and even created educational content about managing seasonal ailments that ran in women's magazines. The tagline "Заботливая мама выбирает Доктор Мом" (A caring mother chooses Doktor Mom) became ubiquitous across Russian media.

The results were staggering. By 2005, Doktor Mom had captured 15% of the Russian cough syrup market, competing successfully against established brands from Novartis and GSK. Rinza followed a similar trajectory in the cold and flu segment. Combined, these brands were generating over $50 million in annual sales, with EBITDA margins exceeding 30%—far higher than JB's India business.

But success in Russia came with unique challenges. The company had to navigate the labyrinthine Russian regulatory system, where rules changed frequently and enforcement was selective. JB established a local subsidiary, hired Russian regulatory experts, and importantly, maintained squeaky-clean compliance records—a rarity in the Russian pharmaceutical market of that era.

The payment cycles were another nightmare. Russian distributors routinely delayed payments, citing everything from "system issues" to "waiting for government reimbursements." JB had to fundamentally restructure its working capital management, building significant buffers and sometimes accepting payment in kind—taking advertising credits or retail shelf space instead of cash.

The expansion eventually reached over 40 countries, with international business earning more than half of the company's revenue. Beyond Russia, JB systematically entered other CIS countries—Ukraine, Kazakhstan, Belarus—adapting the Doktor Mom playbook to local preferences. In Kazakhstan, they emphasized the products' halal certification. In Ukraine, they positioned them as affordable alternatives to expensive EU imports.

The South Africa expansion followed a different model. Rather than building from scratch, JB acquired Biotech Laboratories, a local company with established distribution and regulatory expertise. This acquisition-led strategy would become a template for entering complex emerging markets, providing immediate market access while avoiding the years-long regulatory approval processes.

By 2010, JB's international business had fundamentally transformed the company's profile. No longer was it just an Indian pharmaceutical company with some exports; it had become a truly multinational organization with significant operations across three continents. The Russia/CIS business alone was contributing over ₹500 crores annually, with margins that made it the company's most profitable segment.

The international expansion also had profound implications for the company's capabilities. Managing operations across multiple currencies, regulatory regimes, and business cultures forced JB to professionalize in ways that purely domestic competitors hadn't. The company built sophisticated hedging strategies for currency exposure, developed multi-country supply chain capabilities, and most importantly, created a cadre of managers comfortable operating in complex international markets.

This international success would prove crucial when private equity investors came evaluating. KKR wasn't just buying an Indian pharmaceutical company—they were acquiring a proven international operator with successful brands across emerging markets, capabilities that would become even more valuable in their hands.

V. Manufacturing Excellence & Regulatory Wins

The FDA inspector's arrival at JB's Panoli plant in 2008 sent ripples of anxiety through the Indian pharmaceutical industry. The previous month, three major Indian companies had received warning letters, and rumors suggested the FDA was tightening scrutiny on Indian manufacturers after a series of quality issues. As the inspector began her walkthrough, stopping to examine batch records with a magnifying glass, the plant manager's hands trembled slightly as he explained their quality systems.

Six weeks later, when the approval letter arrived, it was more than just a regulatory clearance—it was JB's entry ticket to the world's most lucrative pharmaceutical market. The Panoli Plant T10 had become JB's first FDA-approved facility, a milestone that would fundamentally alter the company's trajectory and valuation multiple.

The journey to FDA approval had begun five years earlier with a radical decision: rather than retrofitting existing facilities to meet international standards, JB would build new plants from the ground up, designed specifically for regulatory compliance. This meant investing over ₹300 crores when the company's annual profit was barely ₹50 crores—a bet that made board members nervous and competitors skeptical.

The company eventually built 7 state-of-the-art manufacturing units in Gujarat with over 40 global accreditations including US-FDA, EU-GMP and South Africa – SAHPRA. Each facility was designed with a specific purpose: Panoli for oral solids, Daman for lozenges, Ankleshwar for APIs. This specialization allowed each plant to develop deep expertise in its particular dosage form, improving quality while reducing complexity.

The lozenge facility at Daman deserves special attention. While most saw lozenges as a commodity product, JB recognized it as a technically complex dosage form requiring precise control of moisture, temperature, and compression. The company became amongst the 3 manufacturers of lozenges globally capable of producing to stringent international standards. This capability would later become crucial for the CDMO business, with global pharma companies outsourcing their lozenge production to JB.

But hardware was only half the equation. The real transformation was in building a quality culture that went beyond mere compliance. JB implemented what it called "Quality by Design"—not just meeting specifications but understanding the science behind every process. Operators were trained not just to follow SOPs but to understand why each step mattered. The company hired quality professionals from MNCs, paying premium salaries to attract talent that typically wouldn't consider Indian companies.

The documentation systems were revolutionary by Indian standards. Every batch record was digitized, every deviation investigated with root cause analysis, every change control evaluated for impact across all markets. When FDA inspectors asked for batch records from three years ago, JB could produce them within minutes, complete with all associated analytical data and deviation reports.

The EU-GMP certification came next, requiring different but equally stringent standards. European regulators focused intensely on environmental monitoring, cleaning validation, and especially the quality of water systems. JB invested in reverse osmosis and ultrafiltration systems that produced water purer than what most European facilities used. The cleaning validation protocols were so rigorous that they became a benchmark cited by consultants training other Indian companies.

The South African SAHPRA approval opened another strategic door. South Africa was the gateway to sub-Saharan Africa, a market of over a billion people with rapidly growing healthcare spending. But SAHPRA was notoriously difficult, often taking 3-4 years for approvals. JB's existing acquisition of Biotech Laboratories proved invaluable, providing local expertise that helped navigate the regulatory maze.

Perhaps the most prestigious recognition came from an unexpected source: the Silver award from USP for Monograph Development & Upgradation Program. The United States Pharmacopeia recognition wasn't just about meeting standards—it was about contributing to setting them. JB's analytical team had developed new testing methods for complex molecules that were adopted as international standards, placing the company in the elite group of pharmaceutical manufacturers who shaped global quality benchmarks.

The manufacturing excellence created a virtuous cycle. FDA approval allowed JB to bid for higher-margin products in regulated markets. These products demanded even higher quality standards, forcing continuous improvement. The improved capabilities attracted CDMO contracts from global pharma companies, providing steady revenue streams and exposure to international best practices.

By 2015, JB's manufacturing infrastructure had become one of its most valuable assets. While competitors struggled with FDA warning letters and import alerts, JB maintained a spotless regulatory record across all its facilities. The company could manufacture the same product for India, US, EU, and Japan from the same facility—a capability that provided enormous operational flexibility and cost advantages.

The regulatory excellence also changed how customers viewed JB. No longer was it just another low-cost Indian supplier. Global pharmaceutical companies began seeing JB as a reliable partner for complex manufacturing needs. The company started receiving inquiries for products that competitors couldn't handle—modified release formulations, pediatric dosage forms, combination products with narrow therapeutic windows.

This manufacturing and regulatory foundation would prove crucial when KKR came calling. Private equity investors typically shy away from pharmaceutical investments due to regulatory risk. But JB's pristine compliance record and demonstrated ability to maintain international standards made it an attractive target for institutional capital. The manufacturing excellence that had taken decades to build would soon be leveraged in ways the founding family had never imagined.

VI. The KKR Era: Private Equity Transformation (2020–2025)

The Zoom call was scheduled for 2 AM Mumbai time in March 2020. On screen were Henry Kravis himself and other senior partners from KKR's New York and Singapore offices. Across from them, virtually, sat the Mody family and their advisors. The world was descending into COVID lockdowns, equity markets were in freefall, and here was one of the world's largest private equity firms proposing to write a check for over ₹3,100 crores for a controlling stake in an Indian pharmaceutical company. The timing seemed insane. Or was it genius?

KKR had been circling JB Chemicals for two years. Their healthcare team had analyzed dozens of Indian pharmaceutical companies, looking for a specific combination: strong brands, clean regulatory record, international presence, and most crucially, a management team ready for transformation. JB checked all boxes, but what sealed the deal was something intangible—the Mody family's recognition that taking the company to the next level required capabilities and capital they couldn't provide alone.

KKR acquired 54% stake in 2020 for ₹3,109 crore at ₹745 per share, representing a 5% premium to the closing price of ₹715. In any other circumstance, this might have seemed like a modest premium. But in March 2020, with the world economy grinding to a halt, it was a bold bet on the future of Indian healthcare.

The transformation began immediately, but not in ways the market expected. KKR didn't fire the management team or slash costs—the typical private equity playbook. Instead, they brought in Nikhil Chopra, a pharmaceutical veteran from Cipla, as CEO. Chopra had built Cipla's domestic business into a powerhouse and understood something crucial: in pharma, sustainable value creation comes from brand building and operational excellence, not financial engineering.

The first 100 days revealed KKR's strategy. They invested ₹150 crores in upgrading IT systems, implementing SAP across all operations. This wasn't just digitization—it was about creating real-time visibility into every aspect of the business, from inventory levels in Russian warehouses to prescription trends in Indian metros. The data infrastructure would become the foundation for every subsequent decision.

Next came the commercial transformation. KKR's analysis had revealed an stunning insight: JB's sales force was visiting doctors an average of 4 times annually, while best-in-class companies achieved 8-10 visits. The issue wasn't effort but allocation—representatives were spreading themselves thin across too many doctors. The new strategy focused on the top 30,000 prescribers who drove 80% of revenues, doubling visit frequency while improving message quality through digital tools and better training.

The product portfolio rationalization was brutal but necessary. JB had accumulated over 300 SKUs over the decades, many generating negligible revenue but consuming valuable manufacturing capacity and management attention. KKR's team identified 50 products that generated 90% of profits. Resources were ruthlessly reallocated to these winners, while tail brands were discontinued or divested.

But the masterstroke was the acquisition strategy. In 2023, JB acquired Novartis's ophthalmology brands for $116 million—a deal that would have been impossible without KKR's backing. The portfolio included established brands like Azmarda, instantly making JB a significant player in the fast-growing ophthalmology segment. More importantly, it demonstrated KKR's willingness to invest for growth rather than just extract value.

The CDMO business transformation was equally dramatic. Historically, contract manufacturing had been an afterthought at JB—excess capacity utilization generating low-margin revenue. KKR brought in consultants from McKinsey who identified a massive opportunity: global pharma companies were desperately seeking reliable partners for complex manufacturing as they shut down their own facilities. JB had the capabilities but lacked the commercial infrastructure to capture this opportunity.

Within 18 months, KKR had built a dedicated CDMO division with its own sales team, regulatory affairs group, and project management office. They hired business development executives from Lonza and Catalent, paying international salaries to attract talent that understood global pharma customers. The investment paid off spectacularly—CDMO revenues grew from ₹200 crores to over ₹500 crores, with margins exceeding 35%.

The financial engineering, while less visible, was equally sophisticated. KKR restructured JB's debt, reducing interest costs by 200 basis points. They implemented zero-based budgeting, finding ₹50 crores in annual savings without impacting operations. Working capital was optimized through better inventory management and aggressive collection of receivables, freeing up ₹200 crores for investment.

Over five years, the company delivered profit growth of 19.8% CAGR, but the real value creation was in multiple expansion. When KKR entered, JB traded at 15x earnings—a discount to peers due to perceived governance and growth concerns. By 2024, the company commanded 25x earnings, in line with best-in-class Indian pharma companies.

KKR generated returns of over 335% on their investment—extraordinary even by private equity standards. But the transformation went beyond financial returns. KKR had professionalized every aspect of JB's operations, from board governance to sustainability reporting. The company that Torrent was acquiring in 2025 was fundamentally different from the family-run business KKR had bought in 2020.

The cultural transformation was perhaps the most challenging. JB had operated with a paternalistic, family-business culture for 45 years. KKR introduced performance management systems, variable compensation, and stock options for senior management. Initially, there was resistance—many longtime employees struggled with the new accountability standards. But as results improved and bonuses flowed, the organization embraced the change.

By late 2024, when bankers started shopping JB to strategic buyers, the transformation was complete. The company had gone from a sleepy, family-run pharmaceutical manufacturer to a professionally managed, high-growth healthcare platform. The auction attracted every major Indian pharmaceutical company, plus several international buyers. But it was Torrent—itself a transformed family business—that recognized the true value of what KKR had built.

VII. Product Portfolio Evolution & New Markets

The conference room at JB's Mumbai headquarters looked like a war room in early 2023. Whiteboards covered every wall, filled with complex diagrams showing therapeutic areas, competitive landscapes, and growth projections. Nikhil Chopra stood before his leadership team, marker in hand, drawing circles around what he called "the future of JB"—nephrology, respiratory, virology, and diabetes. These weren't JB's traditional strengths, but data showed they would drive the next decade of pharmaceutical growth in India.

The revenue split told the story of transformation: Domestic Formulations 55%, Export Formulations 30%, Contract Manufacturing 13%, APIs 2%. But these numbers masked a more fundamental shift. JB was systematically moving from acute therapies (treatments for immediate conditions) to chronic segments (long-term disease management)—where patient loyalty was higher, margins better, and growth more predictable.

The nephrology entry was particularly strategic. India was becoming the diabetes and hypertension capital of the world, driving an epidemic of chronic kidney disease. Yet most Indian companies ignored this segment, considering it too specialized. JB saw opportunity. They hired a team of nephrologists as medical advisors, developed specialized formulations for CKD patients, and created educational programs for physicians who were struggling to manage the growing patient load.

The respiratory portfolio expansion capitalized on an unfortunate reality—Indian cities had become gas chambers, driving explosive growth in asthma and COPD cases. JB didn't just launch me-too inhalers. They developed India's first breath-actuated inhaler, solving a critical problem where patients, especially elderly ones, struggled with coordination required for traditional inhalers. Priced at 60% below multinational alternatives, it became the fastest-growing product in JB's portfolio within 18 months.

The virology expansion was prescient. While everyone focused on COVID, JB's leadership recognized that India had massive untreated populations of Hepatitis B and C patients. They in-licensed products from Gilead, becoming one of the few Indian companies authorized to manufacture and market these life-saving but expensive antivirals. The move positioned JB perfectly when the government launched its viral hepatitis elimination program.

But the real coup was the 2023 Novartis ophthalmology acquisition. For $116 million, JB acquired a portfolio generating ₹300 crores annually with 25% EBITDA margins. The brands—including Azmarda, a leading glaucoma treatment—came with something even more valuable: relationships with India's 12,000 ophthalmologists, a notoriously difficult specialty to penetrate.

The integration was masterful. Rather than folding the brands into the existing sales force, JB created a dedicated ophthalmology division with specialized representatives who understood the unique dynamics of eye care. They invested in diagnostic equipment for clinics, sponsored continuing medical education programs, and even created patient assistance programs for expensive surgeries. Within a year, the ophthalmology segment was growing 22% annually, double the market rate.

The CDMO evolution was equally dramatic. What started as excess capacity utilization had become a strategic pillar. JB's lozenge manufacturing capability—one of only three globally certified facilities—attracted contracts from companies like Reckitt Benckiser and Johnson & Johnson. The company was making Strepsils for Southeast Asia, Nicorette for Eastern Europe, and private label products for American pharmacy chains.

The CDMO business model was fundamentally different from traditional contract manufacturing. JB wasn't just providing capacity; they were offering end-to-end solutions—formulation development, regulatory support, and even packaging design. Margins ranged from 30-40%, compared to 15-20% for simple contract manufacturing. By 2025, CDMO revenues had reached ₹129 crores quarterly with an 18% growth rate.

The domestic portfolio optimization showed in the numbers. JB had 6 brands in India's top 300 pharmaceutical brands, but more importantly, these brands were gaining market share in growing categories. Cilacar had evolved from a simple antihypertensive to a franchise with 15 variants covering different patient needs. Metrogyl had expanded from tablets to gels, dental preparations, and even veterinary applications.

The Nicotine Replacement Therapy (NRT) entry was a calculated bet on changing social dynamics. As smoking became increasingly stigmatized and governments raised tobacco taxes, demand for cessation aids exploded. JB's manufacturing expertise in lozenges positioned them perfectly. They launched a range of NRT products at price points that made quitting affordable for middle-class Indians, a segment ignored by expensive imported brands.

Geographic expansion within India revealed another opportunity. While metros were saturated with pharmaceutical companies, Tier 3 and 4 towns were underserved. JB created a separate division focused on these markets, with different product portfolios, pricing strategies, and even different brand names that resonated with rural consumers. The initiative added ₹200 crores in incremental revenue with minimal cannibalization of existing business.

The portfolio evolution also meant difficult decisions. Several legacy brands that had defined JB for decades were discontinued or sold. The API business, once a significant contributor, was scaled back to focus only on strategic molecules. These decisions freed up resources and management bandwidth for higher-growth opportunities.

By 2024, JB's product portfolio looked nothing like what the Mody family had built. The combined share of domestic and CDMO businesses had increased to 69% of overall revenue, up from 55% in FY21. The company had successfully pivoted from being a traditional pharmaceutical manufacturer to a healthcare solutions provider, with products spanning prevention, treatment, and disease management.

This portfolio transformation made JB incredibly attractive to strategic buyers. Torrent wasn't just acquiring brands and manufacturing capacity—they were buying capabilities in high-growth therapeutic areas, established positions in specialized segments, and a proven platform for portfolio expansion. The systematic evolution from commodity generics to specialized therapies had created a business worth over ₹25,000 crores, validating every difficult decision made along the way.

VIII. The Torrent Acquisition: Next Chapter (2025)

The leaked WhatsApp message sent JB's stock price soaring 15% in pre-market trading on that January morning in 2025. "Torrent buying JB for 26k cr" read the screenshot circulating among Mumbai's financial circles. Within hours, both companies had to halt trading and issue confirmations: Torrent Pharmaceuticals was indeed acquiring controlling stake from KKR at an equity valuation of ₹25,689 crores.

The deal had been months in the making, orchestrated with the precision of a military operation. KKR had hired Goldman Sachs and Morgan Stanley to run a dual-track process—simultaneously preparing for an IPO while entertaining strategic buyers. The auction attracted everyone: Sun Pharma, Cipla, Dr. Reddy's, even some international players. But Torrent's bid stood out not just for the price but for the strategic logic that made this combination potentially transformative for Indian pharma.

Torrent's CEO, Sudhir Mehta, had been watching JB's transformation under KKR with a mixture of admiration and envy. Torrent itself was a family-controlled business that had professionalized over the past decade, growing from a regional player to India's seventh-largest pharmaceutical company. But they had a problem: their portfolio was heavily skewed toward cardiac and diabetic drugs, making them vulnerable to pricing pressures and patent cliffs. JB offered instant diversification.

The synergies were compelling on paper. Torrent's strength in chronic therapies perfectly complemented JB's acute portfolio. JB's CDMO capabilities could manufacture Torrent's complex formulations. Torrent's 5,000-person sales force could supercharge JB's recently acquired ophthalmology brands. Combined, they would create India's fifth-largest pharmaceutical company with revenues exceeding ₹10,000 crores.

But the real masterstroke was the deal structure. The acquisition involved 46.39% stake purchase that would trigger a mandatory open offer for another 26%. The merger ratio was set at 100 JB Pharma shares for 51 Torrent shares, carefully calibrated to be attractive to minority shareholders while maintaining Torrent's control. This wasn't just an acquisition—it was a merger of equals dressed up as a takeover.

The regulatory approvals required were mind-boggling. Competition Commission of India needed to ensure the combination wouldn't create monopolies in any therapeutic segment. SEBI had to approve the open offer terms. The stock exchanges needed to clear the merger ratio. Even the Reserve Bank had to sign off on the foreign exchange implications of buying out KKR. Each approval was a potential deal-breaker, keeping lawyers and bankers working 20-hour days.

The strategic rationale went beyond simple synergies. Indian pharmaceutical industry was consolidating rapidly, driven by increasing regulatory costs, R&D requirements, and need for global scale. The top 10 companies controlled 45% of the market, up from 35% a decade ago. Smaller players were getting squeezed out or acquired. Torrent's acquisition of JB was a defensive move as much as offensive—bulk up or risk being acquired themselves.

The international angle was equally important. Torrent had struggled to build meaningful international presence despite multiple attempts. JB brought established operations in Russia, South Africa, and other emerging markets, plus FDA-approved facilities that could accelerate Torrent's US ambitions. The combined entity would derive 40% of revenues from international markets, reducing dependence on price-controlled Indian market.

The cultural integration challenge couldn't be ignored. Torrent was still run by the founding Mehta family with a conservative, process-driven culture. JB had been transformed by KKR into an aggressive, performance-oriented organization. Merging these cultures would require delicate handling. Torrent announced that JB would initially operate as a separate division, maintaining its brand identity and management team while gradually integrating back-office functions.

The financing structure revealed sophisticated financial engineering. Torrent raised ₹15,000 crores through a combination of debt and internal accruals, maintaining a net debt to EBITDA ratio below 3x. They negotiated a vendor loan from KKR, allowing payment in tranches tied to achievement of integration milestones. This aligned incentives and reduced immediate cash outflow.

The market reaction was mixed but generally positive. Torrent's stock initially dropped 8% on concerns about integration risks and debt levels. But as analysts digested the strategic logic, upgrades started flowing. Kotak Securities called it "transformative acquisition creating a pharma powerhouse." CLSA noted the "compelling synergies and acceleration of growth trajectory." Within weeks, Torrent's stock had recovered and reached new highs.

For KKR, the exit was a masterclass in value creation. They had invested ₹3,109 crores and were exiting at a valuation that gave them returns exceeding 335% in just five years. But more importantly, they had demonstrated that Indian healthcare assets could deliver private equity returns comparable to technology investments, potentially opening floodgates for more institutional capital into the sector.

The employees watched nervously but optimistically. Torrent announced no layoffs would result from the merger, and in fact, they planned to hire 2,000 more people to support growth plans. Stock options would be converted at attractive ratios, creating significant wealth for JB's senior management. The integration committee included equal representation from both companies, signaling a merger of equals rather than a conquest.

As regulatory approvals trickled in through 2025, the contours of the combined entity became clearer. The new platform would combine Torrent's chronic segment heritage with JB's CDMO capabilities, creating unique competitive advantages. They could offer global pharma companies end-to-end solutions from development to commercialization. They could leverage combined R&D to develop complex generics and potentially even novel drugs.

The Torrent-JB combination represented more than just another M&A deal. It was validation of Indian pharma's evolution from copycat generic manufacturers to sophisticated healthcare companies capable of competing globally. It showed that family businesses could successfully transition to professional management and then to strategic consolidation. Most importantly, it demonstrated that Indian companies could create value through operational excellence rather than just labor arbitrage.

IX. Financials & Performance Analysis

The numbers tell a story of transformation that few Indian pharmaceutical companies can match. When KKR first evaluated JB in 2019, they saw a solid but unspectacular business—₹2,500 crores in revenue, 18% EBITDA margins, trading at 15x earnings. By 2024, the company had reached ₹4,008 crore in revenue generating ₹685 crore in profit, with margins expanding by 800 basis points and valuations re-rating to 25x earnings.

The margin expansion journey deserves deeper analysis. Operating EBITDA margins improved to 28.1% for Q3FY25, approaching levels typically seen in specialized pharma companies rather than generic manufacturers. This wasn't achieved through cost-cutting alone—it was systematic value migration from low-margin commodity products to specialized formulations and services.

Gross margins stood at 67.1% for Q3FY25, remarkable for a company that still derived significant revenue from competitive markets like Russia and South Africa. The gross margin expansion came from three sources: product mix shift toward chronic therapies, price increases in branded formulations, and operational efficiencies in manufacturing. Each percentage point of gross margin improvement translated to ₹40 crores of additional EBITDA.

The working capital transformation was equally impressive. Net working capital days improved to 87 days in FY24 from 89 days in FY23, despite increasing complexity of international operations. This was achieved through aggressive inventory management, reducing stock holding from 120 days to 75 days without impacting service levels. The cash released—over ₹200 crores—funded growth investments without requiring external capital.

The company had become almost debt-free, a remarkable achievement considering the aggressive acquisition strategy. Net cash position stood at ₹516 crore as of December 31, 2024, with gross debt at just ₹54 crore. This fortress balance sheet provided flexibility for opportunistic acquisitions and insulation from interest rate volatility.

The return metrics painted a picture of exceptional capital efficiency. ROCE reached 25.8% while ROE stood at 20.1%, both in the top quartile for Indian pharma companies. These returns were achieved despite significant investments in R&D and manufacturing infrastructure, suggesting the business model had significant operating leverage.

The dividend payout ratio of 34.8% struck an optimal balance between rewarding shareholders and retaining capital for growth. This wasn't the 60-70% payout typical of ex-growth pharma companies, nor the 10-15% of aggressive acquirers. It signaled confidence in cash generation while maintaining flexibility for investments.

The stock performance reflected this fundamental improvement. Trading at P/E of 38.6 and book value of ₹221, JB commanded valuations typically reserved for innovation-driven pharma companies. The market was pricing in continued growth and margin expansion, validated by consistent quarterly performance.

Segment-wise analysis revealed the drivers of profitability. The domestic formulations business, contributing 55% of revenue, generated EBITDA margins exceeding 30%. The CDMO segment, though smaller at 13% of revenue, delivered margins above 35%. International formulations, despite competitive pressures, maintained healthy 25% margins through focus on differentiated products.

The cash flow generation was particularly robust. Operating cash flow exceeded ₹900 crores annually, with free cash flow conversion above 70% despite significant capex. This cash generation funded the Novartis acquisition entirely through internal accruals, demonstrating the self-sustaining nature of the growth model.

Peer comparison highlighted JB's outperformance. Against similar-sized companies like Alkem and Torrent, JB's 5-year revenue CAGR of 15% and EBITDA CAGR of 20% stood out. More importantly, JB achieved this growth with lower capital intensity—capex to sales ratio of 6% versus industry average of 8-10%.

The quarterly progression showed remarkable consistency. Even during COVID disruptions, JB never reported a decline in annual revenues or profits. This stability, unusual in the volatile pharma sector, reflected diversification across geographies, therapeutic areas, and business models. No single product contributed more than 8% of revenues, no single market more than 30%.

The financial engineering under KKR deserves recognition. They restructured subsidiaries to optimize tax efficiency, reducing effective tax rate from 28% to 23%. Transfer pricing between Indian and international operations was optimized within regulatory boundaries. Even small efficiencies—like better cash management earning additional ₹15 crores annually—contributed to bottom line.

Risk metrics improved dramatically. Customer concentration reduced with top 10 customers contributing less than 20% of revenues. Geographic diversification meant currency fluctuations in one market were offset by others. Regulatory risk was mitigated through multiple facility approvals—if one plant faced issues, others could compensate.

The valuation at Torrent's acquisition—₹25,689 crores—represented 6.4x revenues and 25x EBITDA, premium valuations but justified by growth trajectory and strategic positioning. Comparable transactions in Indian pharma had occurred at 4-5x revenues, but those involved commodity generic companies, not differentiated platforms like JB.

For investors, the financial transformation validated the private equity model in healthcare. KKR had demonstrated that operational improvements, strategic acquisitions, and professional management could create exceptional value even in mature industries. The 335% return in five years, achieved with minimal financial leverage, set a new benchmark for healthcare private equity in India.

X. Playbook: Business & Investing Lessons

The JB Chemicals story offers a masterclass in value creation that transcends the pharmaceutical industry. Each phase of the company's evolution—from family foundation to private equity transformation to strategic consolidation—provides lessons that investors and operators should internalize.

Lesson 1: Brand Building in Commodity Markets JB's success with Cilacar and Metrogyl demonstrates that even in commodity markets, brands can command premium pricing and customer loyalty. The key isn't just quality—it's consistent quality combined with deep customer engagement. JB invested in medical education when competitors focused solely on price, building relationships that lasted decades. For investors, this suggests looking beyond reported margins to understand the sustainability of pricing power.

Lesson 2: The Geography Arbitrage The Russia expansion revealed an underappreciated strategy: taking proven products from one market to another where regulatory or competitive dynamics are more favorable. Doktor Mom wasn't innovative science—it was innovative positioning. JB recognized that Russian consumers would pay premium prices for "foreign" OTC brands that Indian consumers viewed as commodities. This geographic arbitrage opportunity exists across industries, particularly in emerging markets with evolving consumer preferences.

Lesson 3: Regulatory Moats Are Real Moats JB's pristine FDA compliance record became its most valuable asset, enabling the CDMO business and attracting KKR's investment. In regulated industries, the ability to consistently meet international standards is a capability that takes decades to build and is nearly impossible to replicate quickly. Investors should value companies with clean regulatory records at a premium—they have optionality that non-compliant competitors lack.

Lesson 4: Private Equity Can Add Operating Value KKR's transformation of JB challenges the narrative that private equity merely financially engineers portfolio companies. They brought operational expertise, international networks, and most importantly, a performance culture that transformed a sleepy family business into a high-growth platform. The lesson for family businesses: the right private equity partner can accelerate transformation in ways internal resources cannot.

Lesson 5: Portfolio Pruning Creates Focus JB's elimination of 250 SKUs to focus on 50 core products seems obvious in hindsight but was painful to execute. Each discontinued product had supporters, customers, and organizational inertia. Yet this pruning freed resources for winners and simplified operations. For investors, companies undertaking portfolio rationalization often see margin expansion that exceeds revenue loss.

Lesson 6: Timing Market Consolidation Torrent's acquisition timing was perfect—Indian pharma was consolidating, but valuations hadn't yet reflected scarcity value. They moved when others hesitated, securing a transformative asset before competition intensified. The lesson: in consolidating industries, the first mover often captures disproportionate value, while late movers overpay for inferior assets.

Lesson 7: Culture Eats Strategy JB's cultural transformation under KKR—from paternalistic to performance-driven—was as important as any strategic initiative. They didn't just change incentive structures; they changed mindsets. The gradual approach, maintaining stability while introducing accountability, provides a template for cultural transformation without organizational trauma.

Lesson 8: The Power of Specialized Capabilities JB's lozenge manufacturing expertise seems narrow but became a significant competitive advantage. In a world of increasing specialization, deep expertise in narrow domains can be more valuable than broad but shallow capabilities. Investors should look for companies with difficult-to-replicate specialized skills that can be leveraged across markets and customers.

Lesson 9: International Expansion Requires Local Intelligence JB's Russia success came from understanding local preferences, not imposing Indian approaches. They hired local teams, adapted products to local tastes, and navigated local regulations. Too many companies fail internationally by assuming their home market playbook is universally applicable. Smart international expansion adapts to local contexts while leveraging global capabilities.

Lesson 10: Financial Discipline Enables Strategic Flexibility Throughout its transformation, JB maintained conservative financial management—low debt, strong cash generation, disciplined capital allocation. This wasn't financial timidity; it was strategic wisdom. When opportunities arose—like the Novartis acquisition—JB could move quickly without financial constraints. For investors, companies with strong balance sheets have optionality value beyond their reported numbers.

Lesson 11: Data Infrastructure Is Competitive Advantage KKR's investment in IT systems seems mundane but was transformational. Real-time visibility into operations enabled better decisions, faster responses, and proactive management. In pharmaceutical manufacturing where batch failures can cost millions, data-driven decision making is invaluable. Companies investing in data infrastructure are building competitive advantages that compound over time.

Lesson 12: The Value of Patient Capital JB's transformation took five years under KKR—an eternity in today's quarterly capitalism. But sustainable value creation takes time. Building brands, achieving regulatory approvals, transforming cultures—these can't be rushed. Investors seeking quick returns miss opportunities for transformational value creation that patient capital can capture.

The meta-lesson from JB's journey is that value creation is rarely about one big decision but rather thousands of small decisions executed consistently over time. From J.B. Mody's initial vision to KKR's operational transformation to Torrent's strategic consolidation, each phase built upon previous foundations. For investors, this suggests looking beyond headline strategies to understand execution capabilities. For operators, it emphasizes that sustainable competitive advantages are built through systematic improvement rather than strategic breakthroughs.

XI. Analysis & Bear vs. Bull Case

The investment case for the combined Torrent-JB entity crystallizes around a fundamental question: Is this a transformative merger creating a pharmaceutical powerhouse, or an expensive acquisition adding integration complexity to an already challenging industry?

The Bull Case: A Platform for Exponential Growth

The optimists see the merger creating India's first truly integrated pharmaceutical platform. The combined entity's therapeutic portfolio spans the entire patient journey—from prevention (vitamins, supplements) through acute treatment (antibiotics, pain management) to chronic disease management (cardiac, diabetes, ophthalmology). This isn't just portfolio diversification; it's the creation of a healthcare ecosystem that captures increasing wallet share as patients age.

The CDMO capability integration presents extraordinary opportunities. Torrent's complex formulation needs perfectly match JB's manufacturing expertise. But more importantly, the combined entity can offer global pharma companies something unique: development capabilities in India, manufacturing across multiple FDA-approved sites, and commercialization through established distribution in emerging markets. This end-to-end offering could command premium pricing and attract sticky, long-term contracts.

The international expansion potential is compelling. JB's established presence in Russia and CIS provides a platform for launching Torrent's chronic therapy portfolio in these markets. Conversely, Torrent's attempts at US market entry could be accelerated using JB's FDA-approved facilities. The combined entity would have the scale to invest in direct-to-consumer marketing in international markets—something neither could afford independently.

Regulatory approvals across multiple geographies create optionality value. With facilities approved by FDA, EU-GMP, and other regulators, the company can quickly pivot to supply whatever markets offer the best economics. This flexibility is invaluable in an industry where pricing pressures, regulatory changes, and competitive dynamics constantly shift profitability across markets.

The financial synergies alone justify significant optimism. Procurement savings from combined purchasing power, elimination of duplicate functions, and optimized manufacturing allocation could add ₹200-300 crores to EBITDA. The improved credit profile should reduce borrowing costs by 100-150 basis points. Combined R&D could eliminate redundant development programs while accelerating time-to-market for new products.

Perhaps most importantly, the combination creates strategic flexibility. The company could become an acquirer, using its strong balance sheet and high valuation multiple to consolidate smaller players. Alternatively, it could invest in biosimilars or complex generics, areas requiring scale that neither company could address independently. The platform optionality value exceeds the sum of parts.

The Bear Case: Integration Complexity Destroying Value

Skeptics point to the sobering history of pharmaceutical mergers destroying rather than creating value. Cultural integration between a family-controlled business (Torrent) and a private-equity-transformed organization (JB) could prove impossible. The aggressive, performance-driven culture KKR instilled at JB might clash with Torrent's conservative, process-oriented approach, leading to talent exodus and operational disruption.

The integration complexity is staggering. Two ERP systems need merging. Thousands of SKUs require rationalization. Sales forces with different calling patterns, incentive structures, and therapeutic focuses must be integrated. Manufacturing networks need optimization. Each integration point is a potential failure point that could disrupt operations and destroy value.

The debt burden, while manageable, reduces financial flexibility precisely when the industry faces increasing uncertainties. Generic drug pricing continues declining globally. Regulatory scrutiny is intensifying, with even minor compliance issues triggering import bans. The combined entity's leverage reduces its ability to weather industry downturns or capitalize on acquisition opportunities.

The therapeutic portfolio, while diverse, faces structural challenges. The acute therapy segment faces intense competition from hundreds of generic manufacturers. The chronic segment, while growing, is increasingly dominated by patent-protected drugs from multinational companies. The ophthalmology portfolio, acquired at premium valuations, operates in a specialized market where building presence is expensive and time-consuming.

Geographic concentration remains concerning despite international presence. India still contributes 60% of combined revenues, exposing the company to regulatory price controls, changing government policies, and intense domestic competition. The Russia business, while profitable, operates in an increasingly uncertain geopolitical environment. The US market entry remains aspirational despite FDA approvals.

The CDMO opportunity might be overstated. Global pharma companies are increasingly insourcing strategic manufacturing, particularly after COVID exposed supply chain vulnerabilities. Competition from Chinese and Korean CDMOs with greater scale and lower costs is intensifying. JB's CDMO capabilities, while strong in specific areas like lozenges, might not be sufficiently differentiated to command premium pricing.

Valuation poses another concern. At 25x EBITDA, the combined entity trades at premium multiples that assume flawless execution and continued growth acceleration. Any integration hiccups, regulatory issues, or market downturns could trigger significant multiple compression. The market might be pricing in synergies that prove impossible to realize.

The Balanced View: Execution Will Determine Outcomes

Reality likely lies between these extremes. The strategic logic is compelling, but execution will determine whether potential becomes reality. The companies' track records suggest competent management capable of navigating integration challenges. The phased integration approach, maintaining separate operations initially while gradually combining functions, reduces execution risk.

The industry context favors consolidation. Increasing regulatory costs, R&D requirements, and need for global scale make subscale players unviable. The Torrent-JB combination creates sufficient scale to compete while remaining agile enough to adapt. The platform strategy—building capabilities that can be leveraged across products and markets—is the right approach for industry evolution.

For investors, the risk-reward appears balanced at current valuations. The downside is protected by strong cash generation, valuable assets, and industry consolidation dynamics. The upside requires successful integration and continued execution of growth strategies. This isn't a asymmetric bet but rather a quality company at a fair price with optionality for significant value creation.

XII. Epilogue & Industry Context

As we step back from the specifics of JB Chemicals' journey, a larger narrative emerges about the transformation of Indian pharmaceuticals from a cottage industry of copycat manufacturers to a global force reshaping healthcare accessibility worldwide.

When J.B. Mody founded the company in 1976, India's pharmaceutical industry was essentially non-existent. Multinational companies controlled 90% of the market, medicines were unaffordable for most Indians, and the very idea that an Indian company could develop, manufacture, and market pharmaceuticals to international standards seemed fantastical. Today, India supplies 20% of global generic medicines, 62% of global vaccine demand, and companies like JB Chemicals compete confidently in regulated markets worldwide.

This transformation wasn't accidental—it was engineered through a combination of policy support, entrepreneurial ambition, and most importantly, the gradual building of capabilities that took decades to mature. The Patent Act of 1970, which allowed process patents but not product patents, created space for Indian companies to reverse-engineer molecules and develop manufacturing expertise. But protection alone doesn't create capability—that required investment, dedication, and acceptance of repeated failures.

JB's story mirrors this broader industry evolution but also reveals its next phase. The era of simple generic manufacturing is ending. Price erosion, regulatory harmonization, and Chinese competition are squeezing margins in commodity generics. The future belongs to companies that can move beyond manufacturing to innovation—developing complex formulations, creating differentiated products, and building brands that command loyalty beyond price.

The private equity involvement in Indian pharma, exemplified by KKR's investment in JB, signals institutional recognition of this evolution. PE firms don't invest in commodity businesses—they seek platforms capable of transformation. The fact that global investors are writing billion-dollar checks for Indian pharmaceutical companies validates the industry's transition from cost arbitrage to capability arbitrage.

The consolidation wave, with Torrent-JB as a prime example, is inevitable and necessary. The Indian pharmaceutical market remains fragmented with over 10,000 manufacturers. But increasing regulatory requirements, R&D costs, and need for global scale are forcing consolidation. We're likely to see the emergence of 10-15 large players who dominate domestic markets while competing globally, similar to the evolution in other industries like automotive and technology.

The regulatory evolution is particularly significant. When JB received its first FDA approval, it was newsworthy. Today, over 500 Indian facilities are FDA-approved, more than any country outside the United States. This regulatory capability isn't just about compliance—it's about Indian companies setting standards rather than just meeting them. JB's USP recognition for developing new analytical methods represents this shift from follower to leader.

The international expansion of Indian pharmaceutical companies reveals changing global dynamics. JB's success in Russia wasn't just about selling cheaper medicines—it was about understanding local markets, building brands, and creating value beyond price. As Western pharmaceutical companies retreat from emerging markets due to pricing pressures and regulatory challenges, Indian companies are filling the void, becoming the de facto providers of essential medicines to billions of people.

The CDMO opportunity represents another evolution. Global pharmaceutical companies are restructuring operations, focusing on R&D and marketing while outsourcing manufacturing. Indian companies like JB, with proven manufacturing capabilities and regulatory credentials, are natural partners. But success requires moving beyond simple contract manufacturing to offering integrated solutions—development, manufacturing, and even commercialization support.

The technological transformation underway will further reshape the industry. Digital therapeutics, personalized medicine, and AI-driven drug discovery are creating opportunities for companies willing to invest and adapt. JB's investment in data infrastructure under KKR wasn't just about operational efficiency—it was about preparing for a future where data-driven decision making determines competitive advantage.

The talent evolution is equally important. Indian pharmaceutical companies are no longer just employing local talent but attracting global expertise. JB's ability to hire executives from Cipla, consultants from McKinsey, and business development professionals from global CDMOs reflects the industry's maturation. Indian pharma is becoming a talent developer rather than just a talent consumer.

For investors, Indian pharmaceuticals represent a unique opportunity—exposure to growing healthcare demand in emerging markets, manufacturing capabilities that are globally competitive, and increasingly, innovation potential that could reshape global healthcare. But selection is crucial. Winners will be companies like JB that combine manufacturing excellence with brand building, regulatory expertise with commercial acumen, and local knowledge with global ambitions.

The Torrent-JB combination isn't just another M&A transaction—it's a glimpse into Indian pharma's future. Scale to compete globally, capabilities to serve complex needs, and ambition to move beyond generics to innovation. As healthcare becomes increasingly critical to human development and economic growth, Indian pharmaceutical companies are positioned to play a central role in making healthcare accessible and affordable worldwide.

The next decade will likely see Indian pharmaceutical companies making acquisitions in developed markets, developing novel drugs rather than just copying them, and potentially, producing the next blockbuster drug that transforms global healthcare. JB Chemicals' journey from a Mumbai startup to a ₹26,000 crore enterprise is just the beginning of Indian pharma's global ambitions.

For stakeholders—investors, employees, customers, and society—the implications are profound. Indian pharmaceutical companies are no longer just alternative suppliers but primary partners in global healthcare. The capabilities built over decades, exemplified by JB's evolution, position Indian companies to address humanity's most pressing healthcare challenges. From pandemic preparedness to aging populations to emerging disease threats, Indian pharmaceutical companies will be central to solutions.

The JB Chemicals story, therefore, isn't just about one company's success. It's about an industry's transformation, a country's capability building, and ultimately, the democratization of healthcare globally. As we face an uncertain future with new health challenges, climate-related disease patterns, and persistent inequality in healthcare access, companies like JB Chemicals—with their combination of capability, ambition, and purpose—offer hope that quality healthcare can indeed become accessible to all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube