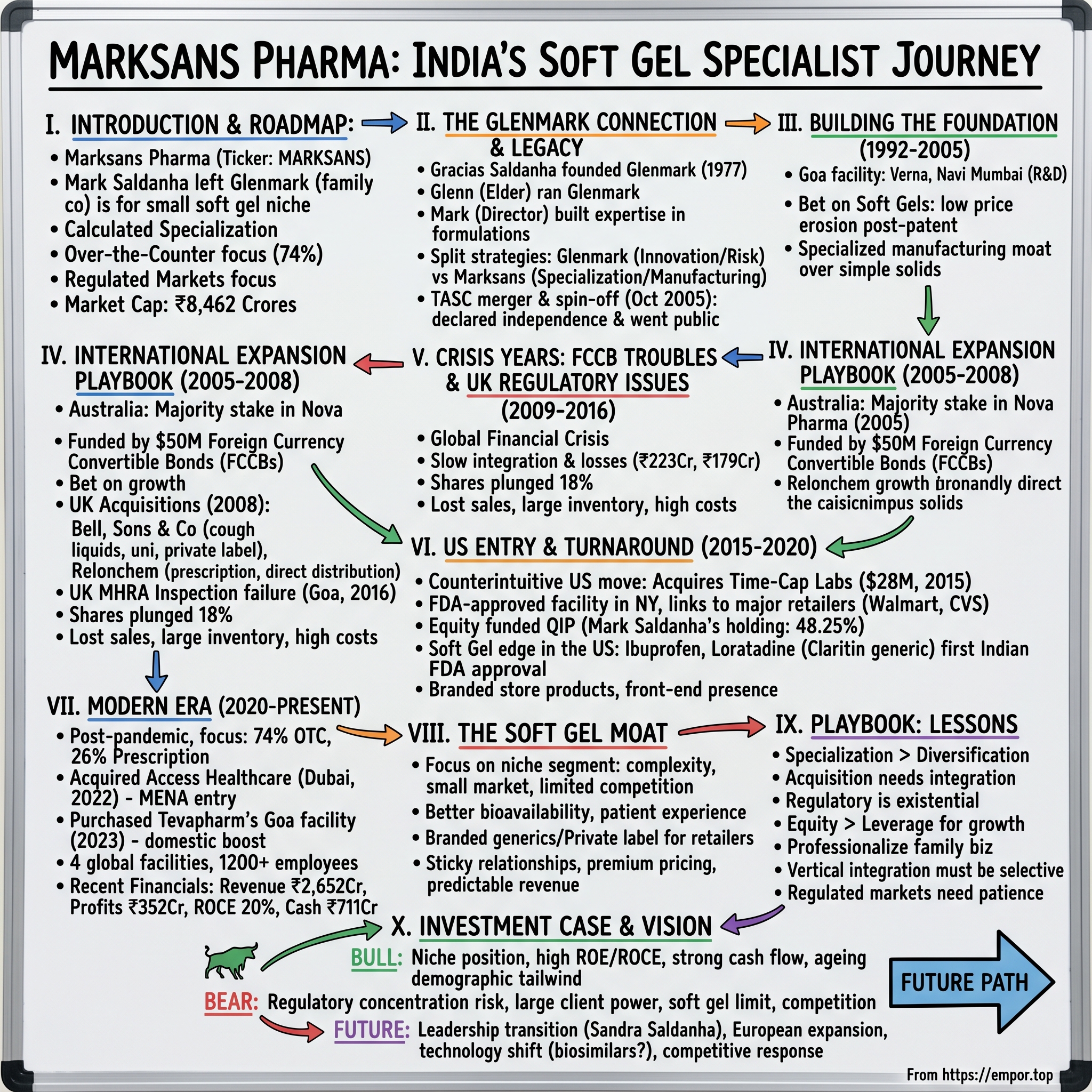

Marksans Pharma: The Story of India's Soft Gel Specialist

I. Introduction & Episode Roadmap

Picture this: A pharmaceutical executive walks away from his family's billion-dollar company to build something of his own. Not because of conflict or ambition alone, but because he sees an opportunity everyone else is ignoring—the unglamorous world of soft gelatin capsules. Mark Saldanha's decision to leave Glenmark Pharmaceuticals, the company his father founded and named after him and his brother Glenn, would lead to the creation of one of India's most specialized pharmaceutical companies.

Today, Marksans Pharma commands a market capitalization of ₹8,462 crores, with 74% of its revenue coming from over-the-counter products sold in the world's most regulated markets. But this isn't just another Indian pharma success story. It's a tale of calculated specialization, near-catastrophic regulatory failures, and a remarkable turnaround that offers lessons for any company attempting international expansion.

The question that drives this narrative: How did a spin-off from Glenmark transform into a global soft gelatin capsule powerhouse, surviving crises that would have destroyed most companies? The answer lies in a combination of family legacy, strategic focus, and the kind of resilience that only comes from betting everything on a single vision.

This journey takes us from the boardrooms of Mumbai to manufacturing facilities in Goa, from regulatory offices in London to distribution centers across America. It's a story about choosing the hard path—building in regulated markets rather than emerging ones—and discovering that sometimes the biggest opportunities lie in the products nobody else wants to make.

II. The Glenmark Connection & Family Legacy

The Saldanha pharmaceutical dynasty began with Gracias Saldanha, a man who understood the power of family legacy so deeply that he literally embedded it in his company's name. When he founded Glenmark Pharmaceuticals in 1977, he combined his sons' names—Glenn and Mark—creating not just a company but a testament to succession.

By the late 1990s, both brothers had proven themselves within Glenmark. Glenn, the elder, had emerged as the natural successor to run the flagship company. Mark, meanwhile, served as Whole Time Director, building deep expertise in formulations and manufacturing. But working in your brother's shadow, even in a company that bears your name, creates its own tensions. In 2001, the pharmaceutical landscape in India was changing rapidly. Generic opportunities were expanding globally, and companies were looking for ways to specialize. Mark Saldanha acquired Glenmark Laboratories Ltd from Glenmark Pharmaceuticals Ltd, a wholly-owned subsidiary that would become his vehicle for independence.

The path to autonomy wasn't immediate. Between 2001 and 2005, Mark built the subsidiary's capabilities while still within the Glenmark umbrella. But the real transformation came with a strategic merger. The company was renamed Marksans Pharma Limited following a Scheme of Amalgamation that took effect on October 10, 2005, when it merged with TASC Pharmaceuticals Limited, a company that had been incorporated in April 1982.

This wasn't just a name change—it was a declaration of independence. The TASC merger provided Mark with a listed entity, public market access, and the foundation to build something distinct from his father's legacy. While Glenn continued to drive Glenmark toward becoming a research-focused pharmaceutical major, Mark chose a different path: specialized manufacturing in formulations, particularly in the unglamorous but profitable world of soft gelatin capsules.

The family dynamic added layers of complexity. Here were two brothers, both accomplished, both with their names literally embedded in pharmaceutical companies, choosing divergent strategies. Glenn's Glenmark would pursue the high-risk, high-reward path of drug discovery. Mark's Marksans would focus on the steady, specialized business of complex formulations for regulated markets. It was a split that reflected not just business strategy but personal philosophy—one brother chasing pharmaceutical innovation, the other mastering pharmaceutical craftsmanship.

III. Building the Foundation: India Operations (1992-2005)

Mark Saldanha founded Marksans Pharma in 1992, thirteen years before the company would take its current form. Those early years were spent learning the intricacies of pharmaceutical manufacturing, understanding regulatory requirements, and most importantly, identifying market gaps that larger players ignored.

The company's manufacturing heart was established in Goa, a location that offered more than just tax benefits. The Verna facility became the cornerstone of Marksans' manufacturing capabilities, while research and development centers were set up in both Verna and Navi Mumbai. This dual-location R&D strategy wasn't accidental—Goa provided the proximity to manufacturing for process development, while Navi Mumbai offered access to scientific talent and proximity to regulatory bodies.

But the real strategic insight came from Mark's observation of post-patent market dynamics. According to the company, price erosion in the soft gelatin capsule segment was only 50-60% against 80-95% in the tablets and capsules segment following patent expiry. This seemingly small difference represented a massive opportunity. While competitors rushed to manufacture simple tablets where margins would eventually evaporate, Marksans began building expertise in soft gels—a format that required specialized equipment, knowledge, and quality control.

The soft gelatin capsule decision was counterintuitive. The market was smaller, the technology more complex, and the capital requirements higher. But that's exactly what created the moat. Most Indian pharmaceutical companies in the early 2000s were focused on volume plays in simple oral solids. Marksans was betting that in regulated markets, complexity would be rewarded with sustained margins.

By 2005, the company had built capabilities across oral solids and tablets, but soft gelatin capsules had emerged as the differentiator. The formulation expertise developed during these foundation years would prove crucial when Marksans began its international expansion. Unlike companies that expanded first and then figured out their specialization, Marksans had already identified its niche—it just needed to find the right markets to exploit it.

The entrepreneurial years from 1992 to 2005 were marked by careful capability building rather than aggressive expansion. Revenue growth was steady but unspectacular. The real value being created was in the knowledge base, the manufacturing expertise, and the regulatory understanding that would enable the company's next phase. When the TASC merger completed in 2005, Marksans wasn't just ready for international expansion—it had a clear thesis about where and how to compete.

IV. The International Expansion Playbook (2005-2008)

The year 2005 marked a inflection point. Fresh from the TASC merger and now operating as an independent entity, Mark Saldanha moved quickly to execute an ambitious international expansion strategy. The company acquired a majority stake in Nova Pharmaceuticals Australasia Private Limited, marking Marksans' first international acquisition and entry into the Australian market.

Australia represented more than just geographic expansion—it was a proof of concept for Marksans' regulated market strategy. The Australian Therapeutic Goods Administration (TGA) maintained standards comparable to the US FDA and UK MHRA. Success in Australia would validate Marksans' ability to meet the world's highest pharmaceutical standards.

To fund this aggressive expansion, Marksans turned to the capital markets with a then-popular instrument: Foreign Currency Convertible Bonds (FCCBs). The company raised $50 million, betting that future growth would allow for conversion at favorable terms. In the heady days of 2005-2007, when Indian pharmaceutical companies could do no wrong in investors' eyes, this seemed like brilliant financial engineering.

The expansion accelerated in 2008 with two transformative UK acquisitions. Marksans acquired Bell, Sons & Company (Druggists) Limited and Relonchem Limited, instantly establishing a significant presence in the European market. Bell, Sons & Co. brought something special—it was the UK's largest manufacturer of private-label and branded cough liquids, with relationships spanning decades with major UK retailers.

The Relonchem acquisition in August 2008 added another dimension. Relonchem had a high-end prescription portfolio of over 100 products, and Marksans turned around the operation by shifting focus from manufacturing for third parties to directly manufacturing and distributing. This vertical integration strategy would become a hallmark of Marksans' approach—don't just manufacture, but control the entire value chain from production to pharmacy shelf.

The timing of these acquisitions seemed perfect. The global financial crisis was just beginning to unfold, creating opportunities to acquire assets at reasonable valuations. Marksans had positioned itself in three major regulated markets—Australia, UK, and through the UK, access to Europe. The soft gel expertise developed in India could now be leveraged across these markets.

But there was a hidden vulnerability in this rapid expansion. The FCCB funding that seemed so clever would become a millstone if the acquisitions didn't quickly generate cash flows. The UK operations, in particular, needed significant integration efforts. And most critically, Marksans was now exposed to regulatory risks across multiple jurisdictions—a complexity that would soon come back to haunt them.

V. Crisis Years: FCCB Troubles & UK Regulatory Issues (2009-2016)

The global financial crisis of 2008-2009 hit just as Marksans was digesting its ambitious acquisitions. What followed was a perfect storm of operational, financial, and regulatory challenges that would test the company's survival instincts.

The acquisitions that had seemed so strategic began hemorrhaging cash. Slow integration of acquired companies and adverse currency movements led to losses of ₹223 crores in 2011 and ₹179 crores in 2012, eventually forcing the company to be referred to BIFR (Board for Industrial and Financial Reconstruction) in 2011. The FCCB bonds, which investors had expected would convert to equity during good times, now loomed as debt that needed to be repaid in cash.

The UK operations proved particularly problematic. Bell, Sons & Co., despite its market position, wasn't generating the returns anticipated. Relonchem was actively losing money as the integration from contract manufacturing to branded business proved more complex than expected. Currency fluctuations added another layer of pain—the pound's volatility against the rupee made financial planning nearly impossible.

But the real catastrophe struck in January 2016. The UK's Medicines and Healthcare products Regulatory Agency (MHRA) conducted an inspection of Marksans' critical Goa manufacturing facility. The inspection failed. The immediate consequence was devastating—shares plunged 18% in a single day as investors grasped the implications. The UK was Marksans' largest market at the time, and the Goa facility was crucial for supplying products to UK subsidiaries.

The regulatory failure created a cascade of problems. Orders from UK customers dried up. Inventory built up. Fixed costs continued while revenues evaporated. The soft gel expertise that was supposed to be Marksans' competitive advantage became almost worthless if the company couldn't access its most important market.

The company emerged from BIFR in 2013 with reduced liabilities and an improving business outlook, but the UK regulatory issues in 2016 threatened to undo all the recovery work. This wasn't just about losing sales—it was about reputation. In pharmaceutical manufacturing, regulatory failures follow you. Other regulators take note. Customers question your reliability.

Mark Saldanha faced the defining crisis of his entrepreneurial journey. The company he'd built by leaving his family's business, the specialized expertise he'd developed over decades, the international expansion he'd orchestrated—all of it hung in the balance. The response to this crisis would determine whether Marksans would survive as an independent entity or become another cautionary tale of overambitious Indian pharmaceutical expansion.

Management made hard choices. Non-core assets were sold. Costs were cut ruthlessly. Most importantly, massive investments were made in quality systems and regulatory compliance. The Goa facility underwent a complete overhaul of its quality processes. Rather than abandoning the UK market, Marksans doubled down on fixing the problems, knowing that success in regulated markets required absolute commitment to quality.

VI. The US Entry & Turnaround (2015-2020)

Even as Marksans battled the UK regulatory crisis, Mark Saldanha made what seemed like a counterintuitive decision: expand into the United States. In 2015, Marksans acquired Time-Cap Laboratories Inc. for $28 million, entering the world's largest pharmaceutical market just as the company was struggling with its existing international operations.

The Time-Cap acquisition was different from previous deals in crucial ways. The company funded this acquisition through equity dilution via a Qualified Institutional Placement (QIP) rather than debt. The FCCB crisis had taught Marksans hard lessons about leverage. This time, they would expand with permanent capital, even if it meant diluting Mark Saldanha's stake. After the QIP of 2015, Mark Saldanha's holding stood at 48.25%.

Time-Cap brought critical capabilities for US market entry. The Farmingdale, New York facility was already FDA-approved and had established relationships with major American retailers. The company had distribution channels across Walmart, Walgreens, CVS, and Cardinal Health. But more importantly, Time-Cap provided something Marksans desperately needed: a fresh start in a new regulatory jurisdiction.

The US strategy leveraged Marksans' soft gel expertise perfectly. The large soft gel capsule market in the US was under-penetrated, offering higher margins. The company launched Ibuprofen soft gelatin capsules in FY15, which became a key growth driver in the US market. Then came a breakthrough: Marksans became the first Indian company to receive US-FDA approval for Loratadine (generic Claritin) soft gel capsules.

This wasn't just another product approval—it validated Marksans' entire strategic thesis. The US market, notorious for price erosion in simple generics, still offered attractive margins for complex formulations like soft gels. The specialized expertise developed over decades in India could create real value in the world's most competitive pharmaceutical market.

Through Time-Cap, Marksans established front-end presence by selling products under their own brand names, which improved margins and allowed them to apply for US government contracts that required domestic manufacturing. This vertical integration in the US mirrored what Marksans had attempted in the UK, but with better execution.

The US expansion coincided with a gradual recovery in UK operations. The Goa facility eventually cleared MHRA re-inspection. Relonchem returned to profitability. Bell, Sons & Co. stabilized. By 2020, over 80% of revenues came from regulated markets in the UK and US, with the company generating 96% of revenue from regulated-developed markets.

The transformation was remarkable. From near-bankruptcy during the BIFR years to establishing successful operations in the world's most demanding pharmaceutical markets. The soft gel specialization that had seemed like a narrow niche proved to be a sustainable differentiator. By 2021's first quarter, the company had already achieved 41.8% of the previous year's full profit, signaling that the turnaround was complete.

VII. Modern Era: Focus & Specialization (2020-Present)

The post-pandemic era has seen Marksans evolve from a turnaround story to a focused specialty pharmaceutical company. The product portfolio now comprises 74% OTC products and 26% prescription drugs, a mix that provides both stability and growth opportunities.

The OTC dominance isn't accidental—it's a strategic choice that leverages Marksans' manufacturing expertise while reducing regulatory risk. OTC products span pain management, cough and cold, digestive remedies, vitamins and tonics, skin treatments, and allergies. These are products where brand trust matters more than patent protection, where manufacturing quality can be a differentiator, and where soft gel formulations can command premium pricing.

Geographic expansion continued, but with more strategic focus. In 2022, Marksans acquired Access Healthcare in Dubai, marking its entry into the MENA (Middle East and North Africa) region. This wasn't just about adding another market—MENA represents a bridge between Marksans' Indian operations and its Western markets, with regulatory standards that the company could now easily meet.

April 2023 brought another significant acquisition: Tevapharm India's Goa facility, purchased on a slump sale basis. This expanded Marksans' domestic manufacturing capacity while providing additional flexibility for serving global markets. The facility acquisition showed how far Marksans had come—from struggling with regulatory compliance to confidently taking over and upgrading other companies' manufacturing assets.

The modern Marksans operates four manufacturing facilities across India, UK, and US, employing over 1,200 people globally with more than 500 registered products. The company has built a robust portfolio of regulatory approvals including US FDA, UK MHRA, and Australian TGA certifications. Each approval represents years of investment in quality systems, documentation, and process excellence.

In recent earnings calls, Mark Saldanha has expressed ambitions for European expansion through M&A, stating "we are working on M&As, and we are exploring on these possibilities". But this isn't the debt-fueled expansion of 2008. The company now evaluates opportunities through the lens of strategic fit, integration capability, and margin sustainability.

Recent financial performance validates the strategy. Revenue reached ₹2,652 crores with profits of ₹352 crores. The company maintains strong return metrics with 20% ROCE and 16.8% ROE. Perhaps most importantly, as of Q1 FY26, the company holds ₹711 crores in cash, providing flexibility for both organic growth and acquisitions without relying on debt.

VIII. The Soft Gel Moat & Business Model

The soft gelatin capsule isn't just a dosage form for Marksans—it's a business philosophy. Understanding why requires diving into pharmaceutical manufacturing economics that most investors overlook.

Marksans Pharma is mainly focused on manufacturing soft gelatin capsules, which is a niche segment. The company focuses on soft gelatin capsules because of manufacturing complexities, small market size, and limited competition in OTC and prescription drugs. These complexities create barriers that protect margins long after patents expire.

The technical advantages are compelling. Bioavailability—the fraction of medicine that reaches system circulation—is higher for soft gels. This means faster action, better patient outcomes, and the ability to charge premium prices even for generic formulations. For elderly patients or those with swallowing difficulties, soft gels offer superior patient experience compared to large tablets.

Manufacturing soft gels requires specialized equipment—encapsulation machines that can handle liquid fills, precise temperature controls, specialized drying tunnels. The capital investment is significant, but more importantly, the learning curve is steep. It takes years to master the nuances of shell formulation, fill compatibility, and stability. This isn't something a contract manufacturer can easily replicate.

The business model evolution reflects this specialization. Initially, Marksans operated primarily as a contract manufacturer, making products for other companies' brands. But contract manufacturing in pharmaceuticals is a brutal business—customers squeeze margins, switch suppliers for small price differences, and capture most of the value.

The transformation to branded generics and private label changed everything. In the US, Marksans now supplies major retailers with store-brand versions of popular OTC medications. These relationships are sticky—retailers don't switch suppliers of successful products without good reason. In the UK, the Bell, Sons & Co. heritage provides century-old relationships with pharmacies and retailers.

The therapeutic area focus is equally strategic. Pain management, cardiovascular, central nervous system, anti-diabetic, and gastrointestinal products represent large, stable markets where soft gel formulations can differentiate. These aren't areas where breakthrough innovations will suddenly obsolete existing products. They're chronic conditions requiring long-term medication where patient preference and experience matter.

The OTC emphasis further strengthens the moat. Unlike prescription drugs where doctors make decisions, OTC products are chosen by consumers who develop brand preferences. A soft gel ibuprofen that works faster and is easier to swallow can maintain market share even against cheaper tablet alternatives. The 74% OTC mix provides revenue stability and predictability that pure prescription generic companies lack.

Contract manufacturing hasn't been abandoned—it now serves a different purpose. Manufacturing for other companies provides volume for fixed cost absorption, intelligence about market trends, and relationships that can lead to acquisition opportunities. It's a complementary business rather than the core.

The margin differential tells the story. While tablet manufacturers face 80-95% price erosion post-patent, soft gels see only 50-60% decline. Over a product's lifecycle, this difference compounds into dramatically different economic outcomes. It's the difference between a race to the bottom and a sustainable business.

IX. Playbook: Lessons in International Pharma

The Marksans journey offers a masterclass in both what to do and what not to do when building an international pharmaceutical company from India. The lessons are particularly relevant for companies attempting to move beyond simple generic manufacturing to build differentiated positions in global markets.

Lesson 1: Specialization beats diversification in pharmaceuticals. While peers chased every opportunity, Marksans' focus on soft gelatin capsules created a defendable niche. The narrower focus meant deeper expertise, better manufacturing economics, and stronger customer relationships. In pharmaceuticals, being very good at something specific beats being average at everything.

Lesson 2: Acquisition-led growth requires integration excellence. The 2008 UK acquisitions nearly destroyed Marksans because integration was underestimated. Successful pharmaceutical M&A isn't just about buying assets—it's about harmonizing quality systems, merging regulatory filings, and creating unified commercial strategies. The Time-Cap acquisition succeeded because Marksans had learned these lessons.

Lesson 3: Regulatory compliance is existential, not operational. The 2016 MHRA failure showed how quickly regulatory issues can destroy value. In regulated markets, quality isn't a department—it's a culture. The massive investments Marksans made in remediation weren't expenses but survival requirements. Companies entering regulated markets must understand that regulatory compliance is the price of admission, not a competitive advantage.

Lesson 4: Capital structure matters more than growth rate. The FCCB crisis taught Marksans that growing fast with leverage in a cyclical industry is a recipe for disaster. The shift to equity funding for the US expansion showed maturity. In pharmaceuticals, where regulatory issues or integration challenges can quickly destroy cash flows, conservative capital structures provide resilience.

Lesson 5: Family businesses can professionalize without losing entrepreneurial edge. Mark Saldanha maintained 43.87% ownership while bringing in professional management and institutional governance. His daughter Sandra Saldanha serves as Whole-Time Director, well-versed in human resource management, business development, projects, and supply chain management. The family involvement provides continuity while professional managers handle specialized functions.

Lesson 6: Regulated markets reward patience. Building presence in the US, UK, and Australia took decades and survived near-bankruptcy. But once established, these positions generate superior returns. The temptation to focus on easier emerging markets is strong, but Marksans proved that the harder path of regulated markets creates more value long-term.

Lesson 7: Vertical integration in pharmaceuticals must be selective. Not every part of the value chain should be owned. Marksans integrated forward into distribution and branding where it added value but remained focused on formulation manufacturing rather than backward integrating into APIs. Understanding where value creation happens in the chain is crucial.

Lesson 8: Crisis management requires decisive action, not hope. When faced with BIFR proceedings and UK regulatory failures, management took painful but necessary actions—selling assets, cutting costs, and rebuilding quality systems. Many Indian pharmaceutical companies facing similar crises waited too long to act decisively.

X. Analysis & Investment Case

Marksans today trades at a market capitalization of ₹8,462 crores, reflecting both its transformation and future potential. The investment case rests on several pillars, each with supporting evidence and legitimate concerns.

The Bull Case:

The core bull thesis centers on Marksans' unique position in soft gelatin capsules within regulated markets. With 24.2 P/E ratio, 20% ROCE, and 16.8% ROE, the company generates returns well above its cost of capital. The 25.8% profit CAGR over the last five years demonstrates sustained execution beyond just recovery from crisis.

The market opportunity remains substantial. Soft gel penetration in generic OTC products is still growing as consumers prefer the dosage form. The aging demographics in Marksans' core markets—US, UK, and Australia—favor easy-to-swallow formulations. The company's established distribution relationships with Walmart, Walgreens, and CVS provide ready channels for new product launches.

Geographic expansion potential adds another growth vector. The European market remains largely untapped despite the UK presence. The MENA entry through Access Healthcare opens new markets with growing healthcare spending. Even in existing markets, Marksans has a relatively small share of the addressable soft gel opportunity.

The financial position provides flexibility. With ₹711 crores in cash and minimal debt, Marksans can fund both organic growth and acquisitions without dilution or leverage. This financial strength is particularly valuable given the company's history with FCCB troubles.

The Bear Case:

Regulatory concentration risk looms large. Despite diversification across geographies, a single major regulatory failure could devastate the business. The 2016 UK experience showed how quickly regulatory issues cascade. With operations in multiple jurisdictions, the probability of regulatory challenges increases.

Customer concentration presents another concern. While Marksans has relationships with major retailers, these powerful customers can squeeze margins. Walmart and CVS have tremendous negotiating leverage. The shift of pharmacy benefit managers toward preferred supplier lists could exclude Marksans from formularies.

The specialized focus that creates the moat also limits the addressable market. Soft gels represent a small portion of the total pharmaceutical market. Growth beyond a certain point may require moving into tablets and traditional dosage forms where Marksans lacks competitive advantage.

Competition is intensifying. Other Indian companies are building soft gel capabilities. Chinese manufacturers offer lower costs. Big pharma companies are increasingly interested in the OTC space. The margins that attracted Marksans to soft gels will inevitably attract competition.

The Balanced View:

Marksans represents a specific type of pharmaceutical investment—a specialized manufacturer with regulated market focus. It's neither a high-growth API player nor a diversified pharmaceutical giant. The company occupies a profitable niche that generates solid returns but may have natural growth limits.

The valuation reflects this reality. At 24.2 times earnings, Marksans trades at a premium to many Indian pharmaceutical companies but at a discount to specialized players in developed markets. The market seems to be pricing in steady but not spectacular growth.

For investors, Marksans offers exposure to the structural shift toward OTC medications in developed markets, the aging demographic tailwind, and the continued premiumization of consumer healthcare products. These are slow-moving but powerful trends that should support the business for years.

The key monitorables are regulatory compliance (any FDA or MHRA issues), margin trends in soft gels (watching for competitive pressure), acquisition integration (if M&A accelerates), and succession planning as Mark Saldanha ages. These factors will determine whether Marksans can sustain its current trajectory or faces new challenges.

XI. Future Vision & Key Questions

The next chapter of the Marksans story hinges on several critical questions that will determine whether the company can evolve from a successful turnaround to an enduring pharmaceutical franchise.

Leadership Transition: Mark Saldanha built Marksans through force of personality and entrepreneurial vision. The involvement of Sandra Saldanha signals family continuity, but the transition from founder-led to next-generation leadership is never simple. Can the entrepreneurial culture survive institutionalization? Will the next generation maintain the focus on soft gels or diversify into broader opportunities?

Geographic Expansion: Management's stated interest in European expansion through M&A represents both opportunity and risk. The European market is fragmented, highly regulated, and competitive. Can Marksans replicate its UK success in Germany, France, or Italy? Will cultural and regulatory differences prove more challenging than anticipated?

Technology Evolution: The pharmaceutical industry is undergoing technological transformation. Continuous manufacturing, personalized medicine, and digital therapeutics are changing the landscape. How does a company specialized in traditional soft gel manufacturing adapt? Is there opportunity to combine soft gel expertise with novel drug delivery technologies?

Market Dynamics: The OTC market is consolidating globally. Major consumer goods companies are acquiring OTC brands. Pharmacy chains are consolidating. Private label is gaining share. How does Marksans maintain its position as industry structure evolves? Will the company need to develop or acquire branded products to remain relevant?

The Biosimilars Question: Complex generics and biosimilars represent the next frontier in generic pharmaceuticals. These products offer higher margins but require different capabilities than small molecule soft gels. Should Marksans stick to its knitting or expand into these adjacent opportunities?

Capital Allocation: With strong cash generation and a clean balance sheet, Marksans faces choices. Should excess capital go toward acquisitions, dividends, buybacks, or organic expansion? The decision will signal management's confidence in growth prospects and commitment to shareholders.

The Competitive Response: As Marksans succeeds, competition will intensify. Indian peers like Aurobindo and Cipla have resources to enter soft gels. Chinese manufacturers offer cost advantages. How sustainable is the soft gel moat when faced with determined competition?

Regulatory Evolution: Pharmaceutical regulations are becoming more stringent globally. Data integrity, supply chain transparency, and environmental compliance requirements are increasing. Can Marksans maintain compliance across multiple jurisdictions as standards rise? Will regulatory costs erode margins?

These questions don't have easy answers. The Marksans story—from family spin-off to near-bankruptcy to regulated market success—shows both resilience and vulnerability. The company has proven it can survive existential threats and exploit niche opportunities. Whether it can build on this foundation to create lasting value remains to be seen.

What's clear is that Marksans represents a unique experiment in Indian pharmaceuticals—a company that chose specialization over diversification, regulated markets over emerging ones, and manufacturing excellence over research ambition. In an industry often criticized for commoditization and price competition, Marksans found a different path. The next decade will reveal whether that path leads to enduring success or eventual marginalization.

The soft gelatin capsule, that seemingly simple pharmaceutical format, has carried Marksans from a small Indian operation to a global specialty pharmaceutical company. It's a reminder that in business, as in medicine, sometimes the most powerful solutions come in the most unexpected packages.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube