ISGEC Heavy Engineering: India's 90-Year Industrial Power Play

I. Introduction & Episode Roadmap

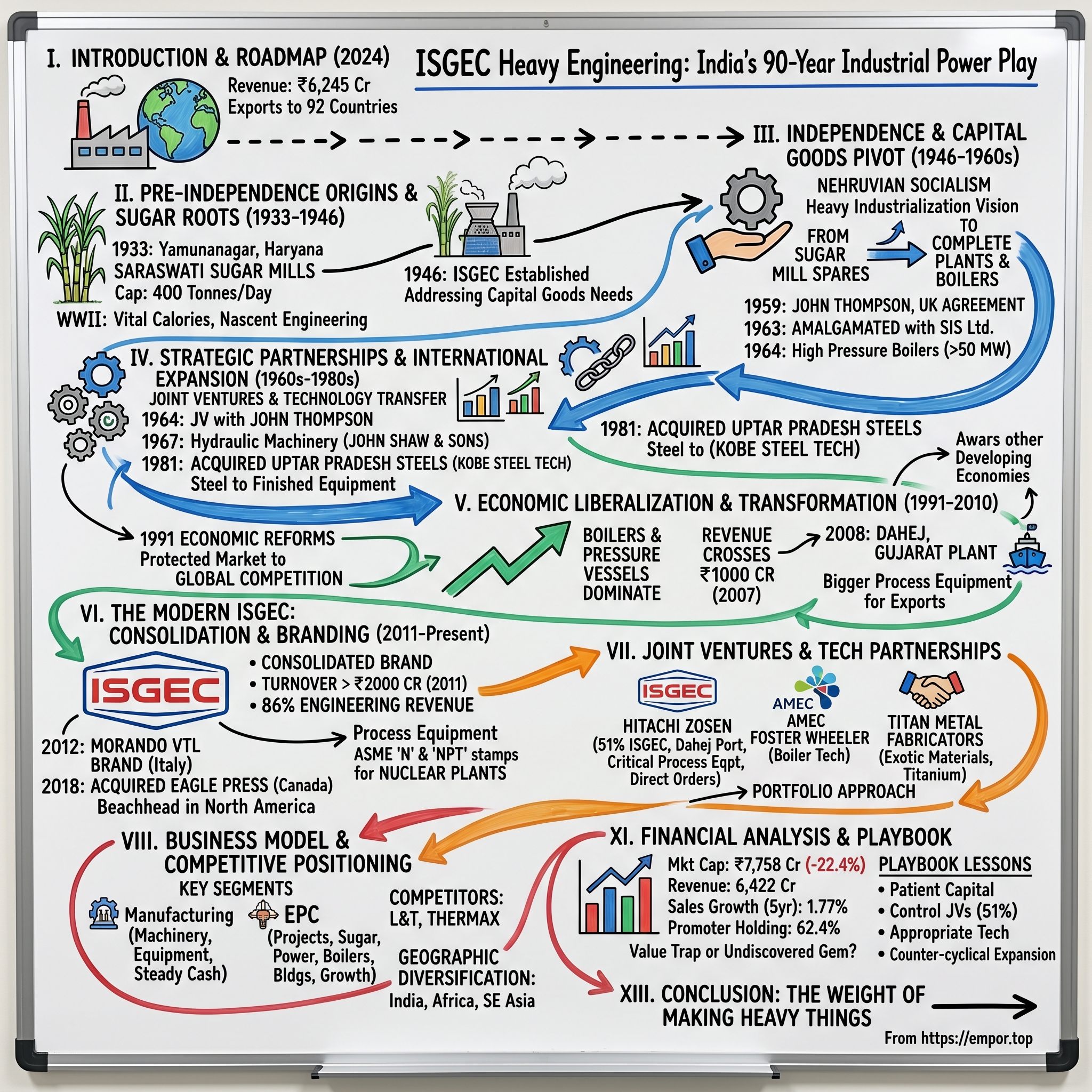

The year is 2024. In a nondescript industrial corridor outside Delhi, massive steel structures take shape—boilers the size of buildings, pressure vessels that will power chemical plants across continents, sugar mills that will process thousands of tonnes daily. This is ISGEC Heavy Engineering at work, generating ₹6,245 crore in revenue, exporting to 92 countries, employing thousands. Yet most investors have never heard of it.

Here's the paradox: How did a company that started making spare parts for sugar mills in pre-independence India transform into a diversified heavy engineering powerhouse? How does a firm ranked 252 in the ET 500 and 253 in the Fortune India 500 remain so under the radar? And perhaps most intriguingly—in an era of asset-light business models and software eating the world—what's the enduring power of making really, really heavy things?

The ISGEC story isn't just corporate history; it's a lens into India's industrial evolution. From the final years of the British Raj through Nehruvian socialism, from the License Raj through liberalization, from Make in India to competing with China—ISGEC has navigated every twist. Along the way, it's partnered with John Thompson of the UK, Hitachi Zosen of Japan, and Foster Wheeler of the US, absorbing technology while maintaining control. It's survived sugar crashes, steel crises, and economic liberalization that killed countless protected industries.

What makes this story particularly fascinating for students of business strategy is the sheer audacity of the pivot. Imagine Apple deciding tomorrow to manufacture jet engines, or Microsoft pivoting to steel production. That's essentially what ISGEC's predecessors did—leveraging sugar mill expertise to enter heavy engineering, then systematically building capabilities in boilers, process equipment, and turnkey projects. Today, 86% of consolidated revenues come from engineering products and projects, with the original sugar business a profitable but small sideshow.

The company trades at 2.84 times book value with a market cap around ₹7,758 crore—down 22.4% over the past year despite India's infrastructure boom. Sales growth has been anemic at 1.77% over five years. The promoter family holds 62.4%, providing stability but raising governance questions. Is this a value trap in a cyclical industry, or an undiscovered gem positioned for India's infrastructure buildout?

Over the next several hours, we'll unpack nine decades of industrial evolution, strategic pivots, and engineering excellence. We'll explore how a sugar mill supplier became a heavy engineering conglomerate, why family control might be a feature not a bug in capital-intensive industries, and what ISGEC's journey tells us about building industrial capabilities in emerging markets. We'll analyze the joint ventures, dissect the financials, and debate whether slow-and-steady industrial companies can create value in a world obsessed with disruption.

But first, let's go back to 1933, to a small town in North India, where sugar was king and independence was still a dream.

II. Pre-Independence Origins & Sugar Roots (1933–1946)

Picture a small town in North India in 1933—Yamunanagar, in what would later become Haryana state. The air is thick with the sweet smell of sugarcane harvest, ox-carts loaded with fresh cane lumber toward a new industrial facility. Established in 1933, it is located at Yamunanagar in Haryana, India. This is Saraswati Sugar Mills, beginning operations with a crushing capacity of just 400 tonnes of sugarcane per day—modest by any standard, revolutionary for its time.

The 1930s were a peculiar moment in Indian industrial history. The Great Depression had devastated global commodity prices, yet paradoxically created opportunities for import substitution. British colonial policy, while generally extractive, had begun tolerating—even encouraging—certain local industries that didn't directly compete with Manchester textiles or Birmingham steel. Sugar was perfect: a local crop for local consumption, requiring industrial processing that couldn't be shipped from Britain.

Some pieces of equipment installed way back in 1933 are still working in tandem with the latest equipment. This detail reveals something profound about the company's DNA—a respect for what works, an engineering culture that values maintenance and incremental improvement over wholesale replacement. In an era where planned obsolescence drives profits, ISGEC's sugar mills still operate machinery from the Roosevelt administration.

The founding family—whose names remain frustratingly elusive in corporate documents, typical of old Indian business houses that valued discretion—understood something crucial: sugar wasn't just about sugar. It was about building industrial capability. Every broken roller that needed replacement, every boiler that required repair, every pump that failed during crushing season was a learning opportunity. They weren't just making sugar; they were inadvertently creating an engineering knowledge base.

By the late 1930s, as Europe descended into war, the sugar business was thriving. The mills had expanded capacity, local farmers had increased acreage, and critically, the company had begun manufacturing its own spare parts. This vertical integration wasn't strategic planning—it was survival. When you're 7,000 miles from the nearest industrial supplier and shipping takes months, you learn to make things yourself or watch your mill grind to a halt.

World War II transformed everything. Suddenly, India became the "arsenal of the East" for the Allied war effort. Sugar production was deemed essential—troops needed calories, industrial alcohol was required for munitions. The Saraswati mills ran round the clock, pushing equipment to its limits. Every breakdown became urgent, every repair critical. The company's nascent engineering capabilities, born of necessity, suddenly became strategic assets.

Indian Sugar & General Engineering Corporation (Isgec Heavy Engineering Limited) is established to address the need for the Indian Capital Goods Industry. As 1946 approached and independence loomed, the family made a pivotal decision. Rather than simply continuing as sugar producers with some engineering capability, they would formalize their engineering expertise into a separate entity. The timing was deliberate—they could sense that independent India would need capital goods, and they had spent thirteen years learning how to make them.

The transformation from agricultural processor to industrial engineer wasn't sudden—it was evolutionary, almost organic. By 1946, they had mechanics who understood steam pressure, fabricators who could work with specialized steels, and engineers who grasped the thermodynamics of industrial processes. The sugar mill hadn't just processed cane; it had processed knowledge, transforming agricultural India's raw materials into industrial India's human capital.

As midnight approached on August 14, 1947, and India prepared for independence, the Saraswati Industrial Syndicate was ready for a new chapter. The company that began making sugar would help build the machines that would build the nation.

III. Independence & The Capital Goods Pivot (1946–1960s)

The partition of India in 1947 threw industrial planning into chaos. Isgec shifts Registered Office from Lahore, (undivided India) to Abdullapur (now Yamunanagar in Haryana, India)—a single line in corporate history that masks enormous upheaval. Imagine the scramble: machinery abandoned, supply chains severed, skilled workers scattered across new borders. Yet this crisis became catalyst. At the time of the nation's independence, the need for an Indian capital goods industry was recognized and ISGEC was established in 1946.

The timing wasn't coincidental. Jawaharlal Nehru's vision for India centered on heavy industrialization—steel plants, dams, power stations—what he famously called the "temples of modern India." But who would build these temples? Not the British, who were leaving. Not the Americans or Soviets, locked in their Cold War. India needed its own capital goods industry, and The initial activity was the manufacture of spares for sugar mills.

Think about the audacity here. A company making replacement parts for sugar mills deciding it could manufacture the industrial equipment for a newly independent nation. It's like a garage mechanic deciding to build Formula One engines. Yet the logic was sound: they understood mechanical systems, worked with specialized steels, and critically, they understood Indian conditions—the heat, the monsoons, the inconsistent power supply, the maintenance challenges.

The 1950s were the crucible years. India's first Five Year Plan (1951-56) focused on agriculture, but the second plan (1956-61) pivoted hard toward heavy industry. The Industrial Policy Resolution of 1956 reserved seventeen industries for the public sector, but capital goods manufacturing remained open to private enterprise. This was ISGEC's opportunity window.

In the course of its history, the company diversified into a range of engineering products. The progression was logical but bold. From sugar mill spares, they moved to complete sugar plants. From repairing boilers, they began manufacturing them. Each step built on previous capabilities while stretching into new territory. By the late 1950s, they were ready for their first major international partnership.

Agreement with John Thompson Ltd., UK for manufacture of Boilers in 1959 marked a watershed. John Thompson wasn't just any partner—they were one of Britain's premier boiler manufacturers, with technology that powered the Industrial Revolution. For a twelve-year-old Indian company to secure this partnership was remarkable. It suggests ISGEC had already demonstrated serious engineering capability.

The License Raj, often maligned for stifling competition, actually helped companies like ISGEC. With imports restricted and licenses required for expansion, established players with technical capabilities had protected markets. The challenge wasn't competition but execution—could you actually build what India needed? The Saraswati Sugar Syndicate Ltd. name changed to Saraswati Industrial Syndicate Ltd. (SIS Ltd.) and Isgec is amalgamated with SIS Ltd. in 1963, formally consolidating the sugar and engineering businesses.

By 1964 Collaboration agreement with John Thompson Water Tube Boilers Ltd. for the manufacture of high pressure boilers having output in excess of 50 MW. This wasn't incremental improvement—50 MW boilers could power entire cities. The technology transfer involved wasn't just blueprints but tacit knowledge: welding techniques for high-pressure vessels, quality control for critical components, project management for complex installations.

The same year, First Ton Container is manufactured. This diversification into liquefied gas containers showed strategic thinking. India's industrialization would need energy infrastructure, and LPG was becoming crucial for both industrial and domestic use. The company was positioning itself across the industrial value chain.

What's striking about this period is the patient capability building. Unlike today's startups that pivot quarterly, ISGEC spent eighteen years (1946-1964) methodically climbing the technology ladder. They didn't try to leap from sugar mill spares to nuclear reactors. Each product line built on previous expertise while adding new capabilities that would enable the next advance.

The social contract of the era mattered too. In Nehruvian India, industrialists weren't just businessmen but nation-builders. Profit was acceptable, even necessary, but the larger purpose was industrial self-reliance. This alignment between corporate strategy and national purpose provided both protection and purpose. ISGEC wasn't just making boilers; they were building India's industrial capacity.

As the 1960s progressed, India faced wars with China (1962) and Pakistan (1965), foreign exchange crises, and political upheaval. Yet these challenges reinforced the importance of domestic industrial capability. Every imported component that couldn't be sourced, every foreign technician who couldn't arrive, strengthened the case for companies like ISGEC. The path from sugar to steel was set, but the journey would require navigating both technological complexity and geopolitical reality.

IV. Strategic Partnerships & International Expansion (1960s–1980s)

The 1960s opened with India still finding its industrial feet, but ISGEC was ready to accelerate. In 1964, it established a joint venture with John Thompson of the UK to form ISGEC John Thompson—not just a licensing agreement but a true joint venture, suggesting both technological sophistication and negotiating prowess. John Thompson brought world-class boiler technology; ISGEC brought local manufacturing capability and market access. It was a marriage of equals, rare for that era.

The timing was fortuitous. India's Third Five Year Plan (1961-66) had allocated massive resources for power generation. Every new thermal power plant needed boilers, and ISGEC John Thompson was positioned to supply them. The venture wasn't just about technology transfer—it was about learning project management, quality systems, and the discipline of executing large-scale industrial projects.

Through the 1960s and 70s, ISGEC methodically expanded its technological repertoire. Licenses received for manufacture of Hydraulic Machinery in collaboration with John Shaw and Sons in 1967. Production of Mechanical Presses started with technical knowhow from Rovetta Presse Spa, Italy in 1985. Each partnership was carefully chosen, each technology absorbed and indigenized. This wasn't passive licensing—it was active learning.

The 1970s brought new challenges. The oil crisis of 1973 sent energy prices soaring. Mrs. Gandhi's socialist turn meant more regulations, more controls. The Foreign Exchange Regulation Act (FERA) of 1973 forced many multinationals to dilute their Indian holdings. Yet ISGEC navigated these waters skillfully, maintaining its foreign partnerships while staying firmly Indian-controlled.

Then came the masterstroke: In 1981, it acquired majority shares in Uttar Pradesh Steels. This wasn't just any acquisition. UP Steels had been set up by Kobe Steel Group of Japan at Muzaffarnagar in 1966—a greenfield project with Japanese technology and standards. By acquiring it, ISGEC gained not just steel-making capacity but Japanese manufacturing philosophy: kaizen, just-in-time, total quality management.

The acquisition timing was brilliant. The early 1980s saw India beginning to liberalize tentatively under Rajiv Gandhi's technology missions. Having steel production capacity meant ISGEC could control its raw material quality for critical components. Both units were subsequently absorbed into the parent company, creating integrated manufacturing capabilities from steel to finished equipment.

What's remarkable about this period is the strategic patience. While American companies focused on quarterly earnings and European firms consolidated at home, ISGEC spent two decades (1960-1980) building a web of technological partnerships. Each venture taught something: British project management from John Thompson, Italian mechanical engineering from Rovetta, Japanese quality systems from the UP Steels acquisition.

The company also began its international expansion during this period. By the late 1970s, ISGEC equipment was finding its way to Africa and Southeast Asia—markets where Indian technology was appropriate, Indian prices competitive, and Indian engineers understood the operating conditions. This wasn't competing with Siemens or GE in Frankfurt or New York; it was serving Nairobi and Dhaka, markets the global giants ignored.

The social dynamics mattered too. In the License Raj, relationships were everything. ISGEC's promoter family, with roots going back to 1933, had built trust with bureaucrats, politicians, and competitors alike. When licenses were scarce, when foreign exchange was rationed, when government approval was needed for expansion, these relationships proved invaluable.

By 1980, ISGEC had transformed from a sugar mill equipment manufacturer into a diversified engineering conglomerate with capabilities in boilers, presses, steel production, and turnkey project execution. The company that started by fixing broken sugar mill rollers was now building power plants. The question was: could they maintain this momentum as India began opening up to global competition?

V. Economic Liberalization & Transformation (1991–2010)

July 1991. India's foreign exchange reserves had dwindled to barely two weeks of imports. The government literally airlifted gold to secure emergency IMF loans. For ISGEC, watching from their Yamunanagar factories, this wasn't just macroeconomic drama—it was existential threat. India's foreign exchange reserves fell to dangerously low levels, covering less than three weeks of imports. The country had to airlift gold to secure emergency loans.

The liberalization that followed wasn't ideology but desperation. In the 1990s, the government gradually opened up the economy, abolishing industrial and import licensing, freeing foreign exchange regulations, gradually reducing import tariffs and direct tax rates, reforming capital and financial markets, and generally cutting red tape. For four decades, ISGEC had thrived in a protected market. Now, suddenly, global giants could enter India. Siemens, ABB, GE—companies with revenues larger than India's defense budget—were eyeing the same contracts ISGEC had considered theirs by birthright.

The initial response was panic, then pragmatism. If you can't beat them, partner with them—but on your terms. The 1990s and 2000s became ISGEC's partnership decade. Unlike the 1960s partnerships which were about learning, these were about competing. The company systematically identified technology gaps and filled them through targeted alliances.

The economy responded with a surge in growth, which averaged 6.3 percent annually in the 1990s and the early 2000s, and ISGEC rode this wave skillfully. Infrastructure spending exploded. Power generation capacity targets doubled, then tripled. Every power plant needed boilers, every refinery needed pressure vessels, every steel plant needed equipment. The market was growing faster than foreign competitors could establish themselves.

The company's response was counterintuitive: instead of defending their home turf, they went global. By the late 1990s, ISGEC equipment was being installed in Nigeria, Vietnam, and the Middle East. The logic was beautiful—in India, they competed with global giants; abroad, they were the global giant, especially in markets where European equipment was too expensive and Chinese quality still suspect.

Technology absorption accelerated. Where earlier partnerships involved learning to manufacture under license, now ISGEC was co-developing products. The shift from follower to partner was subtle but profound. When negotiating with Foster Wheeler for CFBC boiler technology, ISGEC brought their own innovations to the table—modifications for high-ash Indian coal, designs for extreme temperature variations.

The dot-com bust of 2001 and global recession should have hurt, but India's infrastructure deficit provided insulation. Soon after came two droughts (in 2000 and 2002), the dot-com collapse and global recession of 2001, and the huge global uncertainty created in the run-up to the invasion of Iraq in 2003. While Silicon Valley imploded, India needed power plants, roads, ports. ISGEC's order books remained full.

By 2007, the transformation was complete. Company turnover crossed Rs.1000 Crores—a psychological barrier that marked arrival in the big leagues. More importantly, the revenue mix had shifted. Sugar equipment, once the core, was now a small fraction. Boilers, pressure vessels, and EPC projects dominated. The company that began making spare parts was now executing turnkey power plants.

The 2008 financial crisis tested this transformation. Global capital froze, projects stalled, customers delayed payments. Yet ISGEC survived, even thrived. Their conservative financial management—a legacy of the License Raj when capital was scarce—meant minimal debt. Their diversified portfolio—sugar to steel, domestic to export—provided resilience.

New plant at Dahej, Gujarat commenced production in 2008, Set up to manufacture heavier and bigger process plant equipment for the overseas market. This wasn't just capacity expansion but capability enhancement. Dahej could handle equipment sizes that Yamunanagar couldn't—massive vessels for refineries, huge boilers for power plants. Location mattered too: proximity to ports reduced logistics costs for export orders.

What's remarkable about this period is how ISGEC navigated the identity crisis of liberalization. Many Indian companies either sold out to multinationals or retreated to protected niches. ISGEC did neither. They embraced competition while maintaining independence, adopted global technology while preserving Indian ownership, expanded internationally while staying rooted in India.

The social contract had changed too. In the socialist era, companies provided lifetime employment, subsidized housing, cradle-to-grave security. Post-liberalization, the deal was different: market salaries, performance bonuses, but also market discipline. ISGEC managed this transition without major labor unrest, suggesting sophisticated stakeholder management.

By 2010, ISGEC was unrecognizable from its 1991 avatar. Revenue had grown 10x, technology capabilities had transformed, market presence had globalized. Yet the ownership remained with the same family, the headquarters remained in India, the engineering DNA remained intact. As India entered its second decade of liberalization, ISGEC was ready for its next transformation.

VI. The Modern ISGEC: Consolidation & Brand Building (2011–Present)

The year 2011 marked a corporate coming-of-age. In 2011, the company name was changed from Saraswati Industrial Syndicate Ltd. to ISGEC Heavy Engineering Ltd. with all businesses consolidated and now marketed under a common brand name – ISGEC. After 78 years, the company finally shed its colonial-era name. "Syndicate" suggested a loose confederation; "Heavy Engineering" declared exactly what they were. The rebranding wasn't cosmetic—it signaled transformation from a holding company with various businesses to an integrated engineering powerhouse.

The timing was deliberate. 2011 Company turnover crosses Rs.2000 Crores, double what it had been just four years earlier. The company had critical mass, technological depth, and most importantly, clarity of purpose. Over the years, it has transformed into a diversified heavy engineering company with 86% Consolidated Revenues from Engineering Products and Projects. Sugar, the original business, was now a profitable footnote.

The decade that followed was about systematic capability building through targeted acquisitions and partnerships. Company buys drawings and the brand Morando for manufacture of Vertical Turning Lathes (VTL) from an Italian Company in 2012. This wasn't just buying technology—it was acquiring a brand with decades of reputation in precision machining. Company acquires technology to manufacture Electrostatic Precipitators (ESP) from a German company, Envirotherm GmbH. As India tightened pollution norms, ESP technology became critical for power plants and cement factories.

The joint venture strategy evolved too. Earlier partnerships were about learning; now they were about market access and specialized capabilities. Company forms a new joint venture with Hitachi Zosen Corporation, Japan for manufacturing specialized and critical process equipment. Shareholding pattern: 51% (Isgec) to 49% (Hitachi Zosen Corp.). Note the shareholding—ISGEC maintained control while accessing Japanese technology for high-margin specialized equipment.

Process Equipment business vertical receives "N" and "NPT" stamps from ASME for manufacture of equipment for Nuclear Plants. These certifications weren't just regulatory compliance—they were tickets to the global nuclear supply chain. An Indian company manufacturing for nuclear plants worldwide would have been unthinkable in 1991.

Then came the boldest move yet. ISGEC Heavy Engineering announced that its subsidiary, Isgec Canada Inc. has on 18 September 2018, acquired 100% stake in Eagle Press and Equipment Co., Canada and its group companies. This wasn't just international expansion—it was a reversal of historical flows. An Indian company acquiring a North American manufacturer, bringing 60 years of Canadian engineering under Indian ownership.

This company manufactures Mechanical Presses and related equipment, and sells its machines to customers in USA, Canada and Mexico. The turnover of Eagle Press and Equipment Co in the year 2017 has been about Canadian Dollars 30 million. The strategic logic was compelling: access to North American automotive customers, advanced press technology, and critically, a beachhead in NAFTA markets.

The initial Purchase Price paid is Canadian Dollars 14.35 million (approximately Rs.79 crore). An additional Purchase Price of up to Canadian Dollars 6 million (approximately Rs.33 crore) may have to be paid on the basis of performance of the acquired entity in the next two years. The earnout structure showed sophisticated deal-making—ISGEC wasn't overpaying for potential but linking payment to performance.

The modern ISGEC operates at scale. Isgec Heavy Engineering Ltd. is a multi-product, multi-location public company that has been providing engineering solutions to customers across 92 countries for the past 90 years. Manufacturing facilities span Haryana, Uttar Pradesh, Gujarat, Tamil Nadu and Maharashtra. The product portfolio reads like an industrial catalog: process equipment, EPC projects, industrial boilers, sugar plants, distilleries, mechanical and hydraulic presses, steel and iron castings, air pollution control equipment and contract manufacturing.

Yet challenges persist. Mkt Cap: 7,758 Crore (down -22.4% in 1 year) · Revenue: 6,422 Cr · Profit: 356 Cr The market cap decline despite record revenues suggests investor skepticism. The company has delivered a poor sales growth of 1.77% over past five years. In a decade where Indian infrastructure spending exploded, this anemic growth raises questions.

Stock is trading at 2.84 times book value—not cheap for a capital-intensive business with single-digit growth. Promoter Holding: 62.4% provides stability but limits float, potentially explaining the valuation disconnect.

The company's joint venture portfolio has become increasingly sophisticated. Beyond Hitachi Zosen, there's A Joint Venture Company along with Amec Foster Wheeler North America Corp., U.S.A has been incorporated in the name of "Isgec Foster Wheeler Boilers" and Isgec and TITAN Metal Fabricators create joint venture manufacturing operation. Each partnership targets specific technologies or markets, creating a web of capabilities that would be impossible to build organically.

What's remarkable about the modern ISGEC is how it has navigated the transition from protected domestic player to global competitor. They've acquired when necessary (Eagle Press), partnered when beneficial (Hitachi Zosen), and built organically when possible. The company that once made sugar mill spares now manufactures equipment for nuclear plants. As India pushes toward $5 trillion GDP, the question is whether ISGEC can accelerate growth to match the opportunity.

VII. Joint Ventures & Technology Partnerships

The architecture of ISGEC's joint ventures reveals sophisticated strategic thinking rarely seen in Indian engineering companies. Each partnership isn't just technology acquisition but carefully structured value creation.

Isgec Hitachi Zosen is a joint venture of lsgec Heavy Engineering Limited, India (Isgec) & Hitachi Zosen Corporation, Japan (HITZ) located at the port town of Dahej, Gujarat on the west coast of India. The location choice—Dahej port—wasn't random. Export-oriented manufacturing needs port proximity to be competitive. The new company has a shareholding pattern of 51% (Isgec) to 49% (Hitachi Zosen Corp.). That 51% matters enormously—ISGEC maintains control while accessing world-class Japanese technology.

Hitachi Zosen is a 135-year-old company, based out of Osaka, Japan with interests in Process Equipment, Environmental Systems, Industrial Plants, Industrial Machinery, Precision Machinery, Steel Structure, Construction Machinery, and Disaster Prevention Systems. This wasn't partnering with a startup but with Japanese industrial royalty. HITZ are one of the leading fabricators of Process Equipment with a global track record of fabricating Reactors, Pressure Vessels, Ammonia Converters, Converter Internals, Tall Columns & other critical equipment. Isgec Hitachi Zosen Limited has been successfully operating since 2012 & has since created global footprint in supplying critical Process Equipment.

The financial structure is revealing. It's authorized share capital is INR 110.00 cr and the total paid-up capital is INR 100.00 cr. Isgec Hitachi Zosen Limited's operating revenue range is Over INR 500 cr for the financial year ending on 31 March, 2023. Within a decade, the JV generates revenue approaching ISGEC's historical turnover levels—this isn't a side project but a core growth driver.

The governance structure shows careful balance. Directors of ISGEC HITACHI ZOSEN LIMITED are TANUPRIYA PURI, KEIICHIRO NAGAO, ASHA RANI, TETSUYA KANASAKA, TAKASHI IBE, SHALABH SINGH, SHAILESH KUMAR, SANJAY GULATI, TOSHIYA TAKENAKA, and ADITYA PURI. Indian and Japanese directors intermixed, suggesting genuine partnership rather than technology licensing disguised as joint venture.

The 2021 amendment to the JV agreement reveals evolving dynamics. The Amendment of Joint Venture Agreement will enable the Joint Venture Company (JVC) for direct booking of orders in case both ISGEC and HITZ agree in addition to orders from government undertakings. Initially, the JV could only execute orders routed through parent companies; now it can bid directly. This operational independence suggests the venture has matured beyond technology transfer to become a standalone competitive entity.

A Joint Venture Company along with Amec Foster Wheeler North America Corp., U.S.A has been incorporated in the name of "Isgec Foster Wheeler Boilers" with a paid up capital of Rupees Two crore only. The modest capital suggests this JV focuses on engineering and design rather than manufacturing—accessing Foster Wheeler's boiler technology without massive capital investment.

The strategic logic becomes clear when examining the portfolio. Isgec Redecam Enviro Solutions Pvt. Ltd. (a joint venture with Redecam, Italy) Isgec Hitachi Zosen Ltd. (a joint venture with Hitachi Zosen Corp., Japan) Isgec SFW Boilers Pvt. Ltd. (a joint venture with Sumitomo SHI FW Energia Oy, Finland) Isgec TITAN Metal Fabricators Pvt. Ltd. (a joint venture with TITAN Metal Fabricators, USA) Each partnership targets specific technology: Italian pollution control, Japanese process equipment, Finnish boiler design, American specialty fabrication.

Isgec and TITAN Metal Fabricators create joint venture manufacturing operation. TITAN brings expertise in exotic materials—titanium, hastelloy, inconel—critical for chemical and petrochemical industries where standard steel won't survive.

What's sophisticated here is the portfolio approach. Rather than depending on a single technology partner who might impose restrictions, ISGEC has created a web of partnerships, each focused on specific capabilities. If one partner becomes difficult, others provide alternatives. If one market slows, others compensate.

The commercial arrangements are equally clever. In view of the above amendment, in case JVC is awarded order directly, ISGEC or HITZ shall claim the Retains directly from JVC or deduct the Retains from the value of the orders. Earlier, on award of orders to ISGEC and HITZ, as the case may be, ISGEC or HITZ will place the order on JVC after reducing the Retains payable to ISGEC or HITZ. In addition to sales commission, such other amount, as may be agreed between ISGEC, HITZ and JVC, will be payable. Earlier, in case of award of orders to JVC, sales commission @2% of FOB Price or FAS Price or Ex-Works Price (as the case may be) shall be paid by JVC only to ISGEC. These aren't just manufacturing arrangements but sophisticated profit-sharing mechanisms that align incentives across partners.

The human element matters too. The joint venture, manned by personnel from India and Japan, is actively supported by both Isgec and Hitachi Zosen, in all its activities, including design and marketing. Knowledge transfer happens through people, not just blueprints. Japanese engineers working alongside Indian counterparts create tacit knowledge transfer impossible through licensing agreements.

Yet questions remain. Why hasn't this sophisticated JV portfolio driven faster growth? With world-class technology partners and global market access, why is ISGEC growing at under 2% annually? The answer may lie not in the partnerships themselves but in execution—having technology is different from deploying it profitably at scale.

VIII. Business Model & Competitive Positioning

ISGEC's business model is deceptively simple yet operationally complex. It operates through two segments: Manufacturing of Machinery & Equipment; and Engineering, Procurement & Construction. The Engineering, Procurement & Construction segment which derives maximum revenue, generates it based on contract manufacturing and execution of projects for setting up sugar plants, power plants, boilers, buildings, factories, and others. The Manufacturing of Machinery & Equipment segment generates revenue based on orders for process plant equipment, presses, castings, boiler components, and liquified gas containers.

This two-segment structure reveals strategic insight. Manufacturing provides steady cash flow and margins; EPC drives growth but with higher working capital needs and execution risks. 86% Consolidated Revenues from Engineering Products and Projects—the company has decisively shifted from product to solutions.

The product portfolio reads like an industrial encyclopedia: The company deals with process equipment, EPC projects, industrial boilers, sugar plants, distilleries, mechanical and hydraulic presses, steel and iron castings, air pollution control equipment and contract manufacturing. Each product line represents decades of capability building, each serving different industries with different cycles.

Geographic diversification provides resilience. The company earns the larger part of its revenue in India and the rest from international markets through countries like Nigeria, Vietnam, Morocco, Bangladesh, and others. These aren't random export markets—they're carefully chosen developing economies where Indian engineering is cost-competitive yet quality-superior to local alternatives.

The order book dynamics are crucial. Heavy engineering isn't retail—you don't wake up and decide to buy a boiler. Sales cycles stretch months, execution years. Working capital gets tied up in project advances, retention money, performance guarantees. Cash conversion cycles can exceed 200 days. This capital intensity creates barriers to entry but also limits return on equity.

Competitive positioning reveals both strength and vulnerability. In India, ISGEC competes with L&T (market cap ₹4 lakh crore), Thermax (₹50,000 crore), and numerous smaller players. L&T operates at a different scale—mega infrastructure projects, defense contracts, technology ventures. Thermax focuses on energy and environment solutions with higher margins but narrower scope. ISGEC sits uncomfortably in between—too small for mega projects, too diversified for specialization premiums.

The international competitive landscape is more favorable. In African and Southeast Asian markets, European competitors are expensive, Chinese quality remains suspect, and ISGEC's India-tested solutions fit perfectly. A boiler designed for Indian coal—high ash, variable quality—works in Nigeria. Equipment built for Indian heat and humidity survives Vietnam's climate.

Technology positioning is nuanced. ISGEC doesn't compete on cutting-edge innovation but on appropriate technology—equipment that's sophisticated enough to be efficient but simple enough for developing-country maintenance. The Company commissioned a 1250T press hardening line in India manufactured in technical collaboration with AP&T of Sweden, as well as 2 nos. 1250T robotic tandem press line in South-East Asia in 2023. This isn't buying technology but adapting it for emerging markets.

Recent developments show continued evolution. The worlds largest Cement Waste Heat Recovery Boiler commissioned in Rajasthan. 7500 TCD complete double sulphitation sugar plant with 120 KLPD distillery and 25 TPH incineration boiler and power plant on turnkey in Uttar Pradesh. These aren't just equipment sales but integrated solutions—ISGEC as systems integrator, not component supplier.

The financial model reflects this complexity. Sales rose 4.89% to Rs 1119.20 crore in the quarter ended December 2024 as against Rs 1066.98 crore during the previous quarter ended December 2023. Net profit of ISGEC Heavy Engineering rose 32.84% to Rs 58.66 crore. Profit growth exceeding revenue growth suggests improving margins—either better pricing power, operational efficiency, or favorable mix.

Yet structural challenges persist. The company has delivered a poor sales growth of 1.77% over past five years. In an era of India's infrastructure boom, this anemic growth is puzzling. Several hypotheses emerge: execution constraints, working capital limitations, conservative bidding, or simply missing the right opportunities.

The contract manufacturing element adds another dimension. It manufactures process plant equipment, presses, Iron & Steel castings & Boiler pressure parts. It also undertakes turnkey projects for setting-up boilers, power plants, sugar plants, distilleries, factories and others. This isn't just making things but solving problems—understanding customer needs, designing solutions, managing execution.

Risk management becomes critical in this model. Every large project carries execution risk—delays mean penalties, cost overruns destroy margins. Currency risk matters with significant exports. Commodity price volatility impacts both input costs and customer demand. Political risk in emerging markets can derail projects overnight.

The moat, such as it exists, comes from accumulated capabilities rather than any single advantage. Ninety years of engineering experience, relationships across industries, proven execution track record, joint venture technology access—individually replicable, collectively formidable. It's the difference between knowing how to make a boiler and knowing how to commission a power plant in rural Bihar during monsoon season.

As India pushes toward developed-country status, ISGEC faces an identity crisis. The capabilities that served well in the protection era—diversification, self-reliance, relationship focus—may not suit the globalized future. The question isn't whether ISGEC can make world-class equipment—they clearly can. It's whether they can build a world-class business around that capability.

IX. Financial Analysis & Performance

Looking at ISGEC's financial metrics reveals a paradox: solid fundamentals undermined by sluggish growth. Mkt Cap: 7,758 Crore (down -22.4% in 1 year) · Revenue: 6,422 Cr · Profit: 356 Cr. The market clearly isn't impressed—a 22% decline while broader indices hit records suggests specific concerns rather than sector rotation.

The valuation multiple tells its own story. Stock is trading at 2.84 times book value—neither cheap enough for value investors nor growth-justified for momentum players. For context, L&T trades at 4-5x book with superior ROE, while struggling PSU engineering companies trade below book. ISGEC sits in no-man's land—too expensive for its growth, too cheap for its quality.

The growth trajectory is particularly troubling. The company has delivered a poor sales growth of 1.77% over past five years. This isn't just below inflation—it's negative in real terms. During the same period, India's infrastructure spending doubled, manufacturing PMI stayed robust, and competitors like L&T grew at double digits. What went wrong?

Working capital management provides clues. Heavy engineering is inherently working capital intensive—you buy steel today, fabricate for months, deliver equipment, then wait for payment. ISGEC's cash conversion cycle often exceeds 200 days. With limited debt capacity and conservative financial management, working capital becomes the growth bottleneck. They can only take projects they can fund.

Profitability metrics show improvement but from a low base. Recent quarters show net margins around 5-6%, respectable for heavy engineering but below best-in-class players. EBITDA margins hover around 10-12%, suggesting reasonable operational efficiency but limited pricing power. The recent 32.84% profit growth on 4.89% revenue growth indicates either one-time gains or mix improvement rather than structural change.

Promoter Holding: 62.4% provides stability but raises governance questions. The high promoter stake means limited float, potentially explaining poor liquidity and valuation disconnect. It also suggests the family views current valuations as undervalued—why else hold such concentration? Yet it limits institutional participation and index inclusion.

Capital allocation has been conservative to a fault. Despite strong cash generation, dividends remain modest, growth capex limited, and acquisitions rare (Eagle Press being the exception). The company seems content with steady-state rather than aggressive expansion. This conservatism protected them during downturns but may be costing growth during booms.

Segment analysis reveals interesting dynamics. The sugar business, while small, generates steady cash with minimal capex needs—essentially funding the engineering business's working capital. The manufacturing segment provides predictable margins, while EPC drives lumpy growth. This portfolio approach provides stability but may prevent focus.

Return metrics disappoint. ROE struggles to exceed 15% despite minimal leverage—suggesting either asset intensity or margin pressure. ROCE similarly underwhelms given the capital employed. For a company with supposed competitive advantages and technology partnerships, these returns suggest execution issues rather than strategic problems.

The order book provides forward visibility but also volatility. Large project wins create revenue spikes; completion creates troughs. Unlike software companies with recurring revenue or FMCG with daily sales, ISGEC's revenue recognition depends on project milestones. This lumpiness makes quarterly comparisons misleading and annual trends more relevant.

Debt levels remain comfortable—one positive from conservative management. Debt-to-equity below 0.5x provides flexibility for growth investment or downturn survival. Interest coverage remains healthy. The balance sheet could support more aggressive growth, but management seems unwilling to lever up.

Geographic revenue mix adds complexity. Export revenues provide dollar denomination, helping during rupee depreciation but adding currency risk. Emerging market exposure means payment delays, political risk, and economic volatility. The developed market presence (through Eagle Press) provides stability but at lower margins.

The cash flow statement reveals operational strength but growth weakness. Operating cash flow remains positive, supporting the business quality thesis. But growth capex remains minimal, acquisition spending rare, and dividend policy conservative. The company generates cash but doesn't deploy it aggressively.

Quarterly volatility reflects project business reality. One quarter might show 30% growth, the next 10% decline—not from operational changes but project timing. This volatility frustrates investors seeking predictability and may partially explain the valuation discount.

The financial picture that emerges is of a solid but unexciting business. Strong fundamentals, conservative management, decent profitability—but missing the growth catalyst that would rerate the stock. The numbers suggest a company capable of much more but unwilling or unable to achieve it.

X. Playbook: Lessons from ISGEC's Journey

ISGEC's nine-decade journey offers a masterclass in building industrial capabilities in emerging markets—lessons particularly relevant as manufacturing shifts from China and countries worldwide attempt industrial policy.

First, the power of patient capital cannot be overstated. The same family controlling ISGEC since 1933 enabled multi-decade capability building impossible under quarterly earnings pressure. When building technical competence in boilers took a decade, when customer relationships spanned generations, when technology absorption required years—patient capital wasn't just helpful but essential. Modern private equity's five-year horizons would never permit such gradual evolution.

The strategic use of joint ventures deserves its own business school case. Unlike many Indian companies that became subordinate partners or mere toll manufacturers, ISGEC consistently maintained 51% control while accessing world-class technology. Each JV targeted specific capabilities—Japanese quality systems, European design, American materials expertise. This portfolio approach prevented dependence while accelerating learning.

The diversification versus focus debate finds nuanced resolution here. Conventional wisdom suggests focus drives returns, yet ISGEC's diversification provided resilience through India's economic cycles. When power projects stalled, sugar equipment sold. When domestic markets slowed, exports compensated. The key was related diversification—everything involved heavy engineering capabilities, even if end markets differed.

Timing economic cycles proved more important than strategy. ISGEC's major moves—the 1946 engineering pivot, 1964 John Thompson JV, 1981 UP Steels acquisition, 2018 Eagle Press purchase—coincided with inflection points. They expanded during downturns when assets were cheap and consolidated during upturns when cash flow was strong. This countercyclical approach required patience and capital most companies lack.

Building industrial capabilities in developing economies follows different rules than Silicon Valley disruption. You can't "move fast and break things" with boilers—failure means explosions, not error messages. Quality takes precedence over speed, reliability over innovation. ISGEC understood that emerging markets need appropriate technology—sophisticated enough to be efficient, simple enough to maintain locally.

The human capital dimension often gets overlooked. ISGEC didn't just transfer technology but built engineering talent. Thousands of engineers trained at ISGEC went on to other companies, spreading industrial knowledge across India. This talent ecosystem, more than any single product, may be ISGEC's greatest contribution to Indian industrialization.

Managing stakeholder complexity in family businesses requires delicate balance. ISGEC navigated between family control and professional management, between worker welfare and market discipline, between government relations and competitive markets. The 62.4% promoter holding that frustrates investors also enabled long-term thinking that created value.

The export development strategy offers lessons for emerging market companies. Rather than competing in developed markets where brand and technology matter most, ISGEC focused on other emerging markets where Indian conditions provided advantage. Equipment designed for Indian infrastructure—unreliable power, extreme weather, limited maintenance—found natural markets in Africa and Southeast Asia.

Technology absorption versus innovation presents a false choice. ISGEC shows you can do both—absorb foreign technology through JVs while innovating for local conditions. Their boilers work with high-ash Indian coal, their sugar plants handle variable quality cane, their equipment survives monsoons. This adaptive innovation, less glamorous than breakthrough invention, creates real competitive advantage.

The working capital challenge in project businesses remains unsolved. ISGEC's growth constraints stem largely from funding limitations—they can only take projects they can finance. Modern supply chain finance, better payment terms, or innovative structures could unlock growth. Yet the company seems stuck in traditional approaches, suggesting organizational inertia.

Government relations in regulated industries require sophistication. ISGEC thrived through License Raj, survived liberalization, and adapted to modern India. This wasn't just lobbying but understanding policy direction, aligning with national priorities, and building trust across political changes. In industries where government remains the largest customer, these relationships matter enormously.

The brand building challenge for B2B companies gets illustrated here. Despite 90 years of operation and presence in 92 countries, ISGEC remains largely unknown. Unlike consumer brands, industrial reputation builds slowly through project execution, technical capability, and word-of-mouth. The 2011 rebranding to ISGEC Heavy Engineering was necessary but insufficient—building industrial brands requires different muscles than consumer marketing.

The succession challenge in family businesses looms large. ISGEC has managed generational transitions while maintaining continuity—rare in Indian business where family feuds often destroy companies. Yet questions remain about whether family management can navigate modern complexity or if professional leadership would unlock value.

Risk management in cyclical industries requires portfolio thinking. ISGEC's diversification across products, geographies, and industries provides resilience individual business lines lack. When evaluating industrial companies, portfolio risk often matters more than individual segment performance.

The ultimate lesson might be that building industrial capabilities is a marathon, not a sprint. In an era obsessed with unicorns and disruption, ISGEC reminds us that making physical things—boilers that don't explode, sugar plants that run decades, equipment that powers nations—requires patience, persistence, and profound technical competence. These capabilities, once built, become national assets transcending corporate boundaries.

XI. Bull vs Bear Case & Future Outlook

Bull Case:

The infrastructure boom thesis starts with simple math. India needs $1.4 trillion in infrastructure investment by 2025 to sustain growth. Every kilometer of highway needs equipment, every power plant needs boilers, every factory needs industrial machinery. ISGEC, with 90 years of experience and established capabilities, sits directly in this spending path.

Make in India and Production Linked Incentive (PLI) schemes fundamentally alter competitive dynamics. Global companies must now manufacture locally, creating demand for industrial equipment. ISGEC's local presence, cost structure, and engineering capabilities position them as natural partners. When Apple suppliers build factories, when semiconductor fabs get established, when battery plants emerge—all need industrial equipment ISGEC provides.

The strong order book provides near-term visibility. Unlike speculative businesses dependent on future demand, ISGEC has confirmed orders stretching years. Large projects already won but not yet executed provide revenue certainty. The lumpy nature of project business means one mega-win could transform growth trajectory.

Technology partnerships provide competitive moat. The Hitachi Zosen JV brings Japanese quality, Foster Wheeler provides boiler technology, Eagle Press opens North American markets. Competitors would need decades to replicate this partnership network. As environmental regulations tighten, ISGEC's pollution control equipment becomes mandatory, not optional.

Export growth potential remains undertapped. With presence in 92 countries but minimal market share, expansion opportunities abound. As China becomes politically complicated, emerging markets seek alternatives. Indian engineering, proven in challenging conditions, offers compelling value proposition. The weak rupee enhances export competitiveness.

The energy transition creates new opportunities. While fossil fuel plants decline, renewable energy needs different equipment—biomass boilers, waste-to-energy plants, grid infrastructure. ISGEC's engineering capabilities translate across energy sources. Industrial decarbonization requires retrofitting existing plants—a massive replacement cycle favoring established players.

Valuation provides margin of safety. Trading at 2.84x book value for a company with real assets, minimal debt, and profitable operations suggests limited downside. If growth accelerates even modestly, rerating potential exists. The 62.4% promoter holding indicates insider confidence.

Bear Case:

The cyclical nature of capital goods creates perpetual uncertainty. When capex cycles turn, orders dry up instantly. Unlike consumer businesses with daily demand, industrial equipment purchases can be postponed indefinitely. ISGEC's exposure to multiple cyclical industries—steel, power, sugar—amplifies rather than diversifies risk.

Working capital intensity limits growth potential. Every project requires upfront investment, tying up capital for months. With conservative financial management and limited debt appetite, ISGEC can only grow as fast as internal cash generation permits. This structural constraint explains the 1.77% five-year CAGR despite India's boom.

Competition from Chinese manufacturers intensifies annually. Chinese companies offer similar equipment at 30-40% lower prices, forcing margin compression. While quality concerns persist, Chinese engineering improves continuously. In price-sensitive emerging markets where ISGEC operates, cost often trumps quality.

Execution risks in large projects threaten profitability. One delayed project, one cost overrun, one technical failure can wipe out years of profits. As projects become larger and more complex, execution risk multiplies. ISGEC's conservative growth might reflect management's risk awareness rather than lack of ambition.

The slow historical growth rate suggests structural issues. Growing at 1.77% during India's infrastructure boom indicates either execution constraints, market share loss, or strategic mistakes. If they couldn't grow during favorable conditions, what happens during downturns?

Technology disruption threatens traditional engineering. 3D printing could eliminate casting businesses, modular construction could bypass traditional equipment, AI-driven design could commoditize engineering. While physical equipment won't disappear, value might shift from manufacturing to software and design.

Governance concerns around family control persist. The 62.4% promoter holding limits institutional participation, reduces liquidity, and raises minority shareholder concerns. Family businesses often prioritize continuity over growth, relationships over returns. Professional management might unlock value but seems unlikely.

Future Outlook:

The next decade presents both ISGEC's greatest opportunity and existential challenge. India's infrastructure build-out is real, massive, and accelerating. Yet competition has never been fiercer, technology evolution faster, or customer demands higher.

The company's strategic choices will determine outcomes. Can they leverage joint ventures for growth rather than just technology? Will they invest aggressively to capture cycle upside or maintain conservative approach? Can family management adapt to institutional governance demands?

Macro trends favor industrial companies. Deglobalization means local manufacturing, energy transition requires equipment replacement, environmental regulations create retrofit demand. Yet micro execution determines who captures value. ISGEC has capabilities and positioning but needs growth catalyst.

The realistic scenario sees continued steady performance—5-7% revenue growth, stable margins, modest returns. This isn't exciting but provides decent risk-adjusted returns given infrastructure exposure. The optimistic case requires management change, aggressive investment, or strategic transformation—possible but requiring different DNA.

The key monitorables become order book growth, margin trends, and capital allocation. If orders accelerate, margins expand, and capital deploys aggressively, rerating follows. If status quo continues, the stock remains a steady but unexciting infrastructure play.

For investors, ISGEC represents a bet on execution rather than concept. The opportunity is clear, capabilities proven, positioning favorable. Whether management can capitalize remains the billion-rupee question.

XII. Power & Reflections

What type of power does ISGEC truly possess? In the Acquired.fm framework, power means persistent differential returns—the ability to generate profits that competition can't erode. ISGEC's power, such as it exists, comes not from any single advantage but from accumulated capabilities that would take decades to replicate.

The most obvious power is switching costs. Once ISGEC equipment is installed in a plant, replacing it requires shutdowns, retraining, and risk. Customers return not from loyalty but from practicality—they know ISGEC understands their operations, can service equipment, and will exist tomorrow. This isn't sexy but it's stable.

Process power emerges from 90 years of learning. ISGEC knows how to execute projects in India's challenging environment—managing labor, navigating regulations, dealing with infrastructure limitations. A foreign competitor might have better technology but would struggle with execution. This tacit knowledge, encoded in organizational routines, can't be purchased or transferred.

Counter-positioning provides subtle advantage. Global giants like GE or Siemens won't compete for small emerging market projects—the overhead doesn't justify it. Chinese companies face quality perception issues. ISGEC occupies a sweet spot—good enough quality at acceptable prices for markets others ignore or can't serve profitably.

Yet ISGEC lacks the strongest forms of power. No network effects—one customer using ISGEC doesn't make it more valuable for others. No cornered resource—their technology comes from partnerships anyone could theoretically access. Brand power remains minimal—industrial customers buy based on specifications and price, not brand preference.

The role of industrial companies in nation-building transcends financial returns. ISGEC built India's industrial infrastructure—literally. Their boilers power cities, their equipment processes food, their sugar plants support rural economies. This social value, while real, doesn't necessarily translate to shareholder returns.

For entrepreneurs in capital-intensive industries, ISGEC offers sobering lessons. Building industrial capabilities requires patient capital, decades of learning, and ability to survive cycles. The financial returns rarely match the effort invested. Yet for those with multigenerational horizons, industrial businesses provide stability and purpose that software startups can't match.

The India story through an engineering lens looks different than through IT or consumer perspectives. While software companies captured headlines and consumer brands captured wallets, companies like ISGEC built the physical infrastructure enabling both. This invisible backbone of industrial capacity determines whether India can manufacture its way to prosperity or remains perpetually dependent on imports.

Key takeaways challenge conventional wisdom. Diversification, typically value-destructive, provided resilience through India's volatile economy. Family control, usually problematic, enabled long-term capability building. Slow growth, seemingly failure, might reflect prudent risk management rather than missed opportunities.

The surprising insight is how little 90 years of experience matters in public markets. ISGEC's deep capabilities, established relationships, and proven execution generate minimal valuation premium. Markets value growth over stability, disruption over continuation, stories over substance. This misalignment between economic value and market value creates both opportunity and frustration.

The greatest lesson might be about time horizons. ISGEC spent decades building capabilities that generate modest returns. A software company could achieve similar market cap in years with minimal assets. Yet when the next crisis hits, when supply chains break, when physical infrastructure needs building—industrial capabilities matter more than apps.

The reflections lead to uncomfortable questions. Has ISGEC been too conservative, missing growth opportunities while protecting downside? Would aggressive expansion have led to spectacular success or spectacular failure? Can traditional industrial companies create shareholder value in modern markets, or are they destined to remain valuable but unprofitable?

Perhaps the answer lies in recognizing different types of success. ISGEC succeeded in building industrial capabilities, survived economic cycles, and contributed to national development. That it hasn't created spectacular shareholder returns might say more about market expectations than company execution.

The power ISGEC possesses is ultimately the power of persistence. In a world of quarterly earnings and instant gratification, they represent something different—the slow accumulation of capability, the patient building of infrastructure, the unglamorous but essential work of making things that make modern life possible.

XIII. Conclusion: The Weight of Making Heavy Things

After nine decades, ISGEC Heavy Engineering stands as a testament to a different era of business building—one where companies measured progress in decades, not quarters; where building meant actual construction, not software development; where value creation involved making things that could crush you if dropped on your foot.

The company that began maintaining sugar mill equipment in 1933 now manufactures nuclear plant components, exports to 92 countries, and partners with global engineering giants. This transformation from agricultural processor to industrial powerhouse parallels India's own journey from colony to emerging power. Yet the market values ISGEC at just ₹7,758 crore—less than some loss-making startups that have never manufactured anything heavier than a smartphone app.

This valuation disconnect reveals profound truths about modern capital markets. We've entered an era where narrative trumps numbers, where potential outweighs performance, where asset-light is automatically considered superior to asset-heavy. ISGEC, with its factories, inventory, and industrial equipment, seems almost anachronistic—a relic from when business meant making physical products rather than capturing user attention.

Yet the COVID-19 pandemic and subsequent supply chain crises reminded us that physical infrastructure still matters. You can't download a boiler, can't digitize a pressure vessel, can't virtualize a sugar plant. Someone, somewhere, needs to make the equipment that powers hospitals, processes food, and generates electricity. In India, that someone is often ISGEC.

The company's strategic evolution—from sugar to steel, from domestic to global, from manufacturing to solutions—shows remarkable adaptability across nine decades. Few companies survive such transitions. Fewer still maintain family control while accessing global technology. ISGEC did both, creating a unique position in India's industrial landscape.

The joint venture strategy deserves particular recognition. While many emerging market companies became subordinate partners to global giants, ISGEC consistently maintained control while accessing technology. The Hitachi Zosen partnership, Foster Wheeler collaboration, and Eagle Press acquisition show sophisticated deal-making that balances autonomy with capability building.

Financial performance, however, tells a more complex story. The 1.77% five-year CAGR during India's infrastructure boom is inexcusable. Either management has been excessively conservative, execution has been problematic, or structural issues limit growth. The contrast with L&T's aggressive expansion or Thermax's margin improvement highlights ISGEC's underperformance.

The 62.4% promoter holding provides stability but limits institutional participation. The family seems content with steady returns rather than spectacular growth. This conservatism protected the company through multiple crises but may be preventing it from capitalizing on India's infrastructure opportunity.

Looking forward, ISGEC faces an identity crisis. Can a 90-year-old family-controlled heavy engineering company adapt to modern market demands? Should it leverage its balance sheet for aggressive growth or maintain conservative stability? Can it attract professional management while preserving family control?

The bull case remains compelling. India needs massive infrastructure investment, environmental regulations create replacement demand, and deglobalization favors local manufacturing. ISGEC's capabilities, partnerships, and track record position it well for these trends. If management becomes more aggressive, growth could accelerate dramatically.

The bear case is equally valid. Chinese competition intensifies, technology disrupts traditional engineering, and working capital constraints limit growth. The slow historical growth suggests structural rather than cyclical issues. Without dramatic change, ISGEC might remain perpetually undervalued.

For investors, ISGEC represents a philosophical choice as much as a financial one. Do you believe in the enduring value of industrial capabilities? Can patience be a virtue in impatient markets? Will making heavy things matter in an increasingly digital world?

The answer depends on time horizon. Over quarters, ISGEC will likely disappoint—lumpy revenues, cyclical demand, and conservative management ensure volatility without excitement. Over decades, however, the company that survived the License Raj, weathered liberalization, and adapted to globalization might surprise again.

The broader lesson transcends ISGEC. In our fascination with disruption, we've forgotten that someone needs to build the infrastructure enabling digital revolution. Data centers need cooling equipment, electric vehicles need charging stations, renewable energy needs grid infrastructure. Companies like ISGEC, unglamorous but essential, make modern life possible.

Perhaps ISGEC's greatest achievement isn't financial returns but industrial capability. They've trained thousands of engineers, built critical infrastructure, and proved that Indian companies can compete globally in complex engineering. This social value, while hard to quantify, might exceed any shareholder return.

As India pushes toward developed country status, it will need many more ISGECs—companies that can design, manufacture, and install the equipment powering economic growth. Whether ISGEC itself captures this opportunity or becomes a case study in missed potential remains to be seen.

The story of ISGEC Heavy Engineering is ultimately a story about time—the time it takes to build capabilities, the time it takes to establish trust, the time it takes to create industrial infrastructure. In a world accelerating toward instant everything, ISGEC reminds us that some things can't be rushed. Making heavy things—things that matter, things that last, things that build nations—still takes time.

And perhaps, for those willing to wait, that's exactly the opportunity.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube