INOX India: The Cryogenic Engineering Story of India's Hidden Industrial Champion

I. Introduction & Episode Teaser

Picture this: It's minus 196 degrees Celsius. At this temperature, air itself becomes liquid, flowing like water. Steel becomes as brittle as glass. And a single drop of this super-cooled liquid nitrogen can instantly freeze anything it touches. This is the world of cryogenics—the science of extreme cold—and it's where one Indian company has quietly built a global empire that touches everything from the oxygen that saved millions during COVID to the fuel systems powering India's space missions.

How does a company that started in 1976 supplying oxygen tanks to local hospitals in Gujarat become the go-to partner for NASA, SpaceX suppliers, and semiconductor giants? How does a family business from Baroda end up designing equipment that operates at temperatures colder than the surface of Neptune?

Welcome to the story of INOX India Limited—a company that 99% of investors have never heard of, yet whose technology is probably within a few kilometers of where you're sitting right now. Originally incorporated as Baroda Oxygen Limited, this engineering powerhouse has methodically built capabilities across the entire cryogenic value chain: design, engineering, manufacturing, and installation of equipment that can handle the most extreme conditions on (and off) Earth.

The numbers tell a compelling story: a market capitalization of ₹9,712 crores, revenues of ₹1,349 crores, and profits of ₹235 crores. But these figures barely scratch the surface of what makes INOX India fascinating. This is a company that exports to 50+ countries, holds certifications from the world's strictest regulatory bodies, and maintains gross margins that would make software companies jealous—all while operating in an industry most people can't even pronounce.

Over the next several hours, we're going to unpack one of India's most remarkable industrial transformation stories. We'll trace the journey from the Jain family's paper trading business in the 1920s to today's high-tech engineering conglomerate. We'll explore how a joint venture with American giant Air Products created one of the longest-lasting Indo-American partnerships in manufacturing. We'll dissect the 2021 family split that could have destroyed the company but instead unleashed its potential. And we'll analyze the 2023 IPO that saw institutions bid 148 times their allocation—a validation that shocked even the company's promoters.

This isn't just another family business story. It's a masterclass in building technical moats, navigating generational transitions, and timing market cycles. It's about recognizing that the most boring-sounding industries—industrial gases, storage tanks, distribution equipment—often hide the most exciting investment opportunities. As we'll discover, when the entire world needs what you make, and only three or four companies globally can make it, you've found something special.

II. The INOX Group Genesis & Jain Family Origins

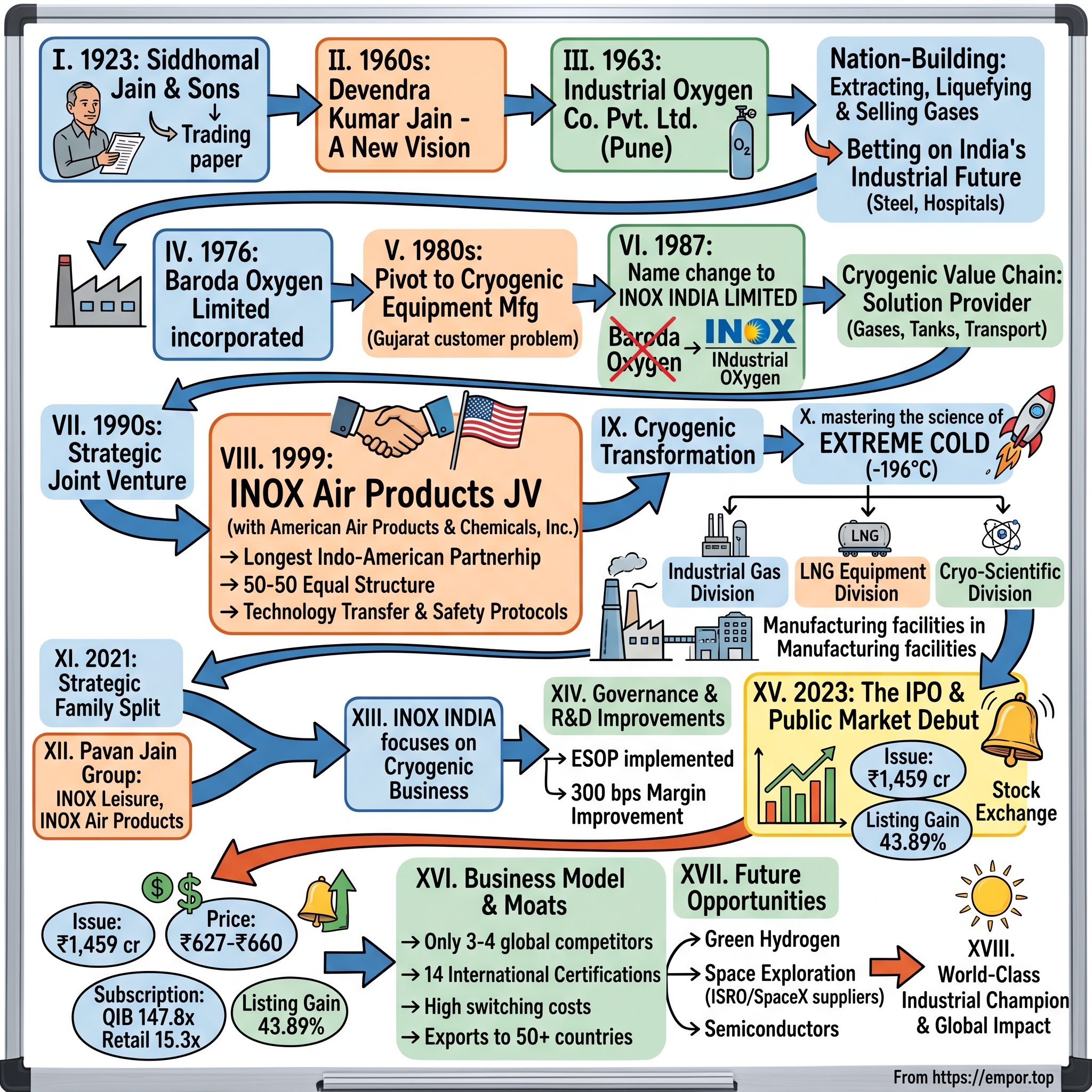

The year is 1923. In the bustling markets of undivided India, a young entrepreneur named Siddhomal Jain is making his rounds, negotiating deals for paper and newsprint. The British Raj is at its peak, literacy is rising, and newspapers are becoming the voice of a nascent independence movement. Siddhomal sees opportunity where others see commodity trading. He establishes Siddhomal and Sons, laying the foundation for what would become one of India's most successful business dynasties.

But the real story begins four decades later, in the wood-paneled discussion rooms of St. Stephen's College, Delhi. It's the early 1960s, and Devendra Kumar Jain—Siddhomal's son—is completing his Honours degree in History. While his classmates debate joining the civil services or pursuing law, Devendra is consumed by a different vision. He's been watching his father's trading business, successful but ultimately limited. "Why just trade what others make?" he asks himself. "Why not manufacture something essential, something every industry needs?"

The answer came from an unlikely source: air itself. Devendra had been studying the industrial development of post-independence India. Steel plants needed oxygen for blast furnaces. Hospitals needed it for patients. Chemical plants needed nitrogen for processes. Yet most of these gases were imported or produced by foreign companies operating in India. Here was a business that literally pulled money from thin air—extracting, liquefying, and selling gases that made up the atmosphere everyone breathed.

In 1963, while his peers from St. Stephen's were joining multinational corporations or government services, Devendra Kumar Jain took his family's trading profits and established Industrial Oxygen Co. Pvt. Ltd. in Pune. The location wasn't random. Pune was emerging as an industrial hub, close enough to Mumbai for access to ports and capital, but far enough to avoid the crushing real estate costs. The Jains were betting on India's industrial future.

The early years were brutal. Devendra quickly learned that producing industrial gases wasn't just about having the right equipment—it was about mastering the science of cryogenics. When you cool air to minus 183°C, oxygen liquefies. Cool it further to minus 196°C, and nitrogen follows. But maintaining these temperatures, storing these liquids, transporting them safely—each step required engineering precision that India's industrial ecosystem was just beginning to develop. The philosophy wasn't just about making money—it was about nation-building. Devendra saw great promise in the business of extracting, liquefying and selling gases from natural air, as these industrial gases were widely used in the steel, manufacturing and healthcare sectors - all of which were flourishing in India at that time. This wasn't venture capital thinking; this was patient, generational capital at work. The Jains understood that building industrial capacity takes decades, not quarters.

By the late 1960s, the company had begun to gain traction. But Devendra's ambitions went beyond just one plant in Pune. He envisioned a network of facilities across India, each serving local industries while building collective scale. His sons, Pavan and Vivek, grew up watching their father negotiate with suppliers, troubleshoot equipment failures, and slowly build relationships with customers who initially viewed domestic suppliers with skepticism.

Pavan Jain, a 1972 batch Chemical Engineering graduate from IIT Delhi, brought technical rigor to complement his father's business acumen. While Devendra understood markets and relationships, Pavan understood the science. This combination would prove crucial as the company expanded beyond simple gas production into complex cryogenic engineering.

The transformation from trader to manufacturer to engineer wasn't just a business evolution—it was a philosophical shift. Where Siddhomal had asked "What can I buy and sell?", Devendra asked "What can I make?", and Pavan would eventually ask "What can I engineer that no one else can?" Each generation didn't just inherit a business; they inherited a progressively more ambitious vision of what an Indian industrial company could become.

In recognition of his successful efforts to increase bilateral trade with Commonwealth countries, Her Majesty, the Queen of England granted Mr. Jain the Dignity of an Honorary Member of the Civil Division in the Order of the British Empire. But perhaps more telling than royal recognition was the respect Devendra earned from India's emerging industrial class. Here was someone who had taken on multinational corporations in their own game and was winning—not through financial engineering or regulatory capture, but through old-fashioned operational excellence.

III. Early Years: From Baroda Oxygen to INOX (1976–1990s)

The Gujarat of 1976 was experiencing an industrial awakening. The state's business-friendly policies and proximity to Mumbai's capital markets were attracting entrepreneurs from across India. It was here, on December 21, 1976, that the Jain family incorporated Baroda Oxygen Limited—a name that reflected both their geographic roots and their core product focus.

The early days were anything but glamorous. The company's first facility in Baroda (now Vadodara) was a modest operation—a single air separation unit that could produce a few tons of oxygen per day. Competitors included established players like Indian Oxygen Limited (later BOC India) and multinational giants who viewed the Indian market as their natural territory. For a family-run operation to compete required not just capital, but ingenuity.

The breakthrough came from an unexpected source: customer complaints. Industrial customers constantly griped about two things—the cost of transporting gases from distant production facilities and the complexity of handling cryogenic equipment. While competitors focused on building bigger plants, the Jains saw an opportunity to build closer to customers and, crucially, to help them handle these dangerous, ultra-cold substances safely. On March 23, 1987, the company underwent a significant transformation, changing its name from 'Baroda Oxygen Limited' to 'INOX India Limited'. This wasn't just cosmetic rebranding. The name change reflected a fundamental strategic shift—from being a regional oxygen supplier to becoming a national player in industrial gases ("IN" for Industrial, "OX" for Oxygen). It also signaled the family's ambition to move beyond commodity gas production into higher-value engineering and equipment manufacturing.

The pivot to cryogenic equipment manufacturing in the late 1980s was born from necessity. A major chemical plant in Gujarat had ordered liquid nitrogen from the company but complained about evaporation losses during transport. Rather than accept this as an industry norm, Pavan Jain assembled a small team of engineers to design better insulated storage tanks. The first prototype was crude—welded in a small workshop behind their Baroda facility—but it worked. Evaporation losses dropped from 3% per day to less than 0.5%.

Word spread quickly in India's tight-knit industrial community. Soon, other customers were asking not just for gases but for the tanks to store them, the trucks to transport them, and the vaporizers to convert them back to gas. The Jains realized they had stumbled onto something bigger than gas production—they were becoming solution providers for the entire cryogenic value chain.

The early 1990s brought both opportunity and crisis. India's economic liberalization meant easier access to technology and capital, but it also meant increased competition from global players who could now enter the Indian market more easily. The company's response was counterintuitive but brilliant: instead of protecting their home turf, they decided to learn from the competition.

They sent engineers to conferences in Europe and the United States, not as attendees but as presenters, sharing their innovations in tropical cryogenics—a niche field dealing with the unique challenges of maintaining ultra-cold temperatures in hot climates. This positioned INOX not as a copycat but as an innovator with unique expertise. International players began to take notice.

By 1993, the company had taken another leap, introducing a project for manufacturing of cryogenic tanks. This wasn't just about making bigger or better tanks—it was about mastering the entire design-to-delivery process. They invested in computational fluid dynamics software, finite element analysis tools, and most importantly, in training their engineers to use them. The workshop in Baroda was transforming into a proper R&D center.

The company's engineering capabilities were put to the test when they received an order from a pharmaceutical company for a specialized liquid nitrogen distribution system. The requirements were exacting: maintain -196°C consistently, allow for precise flow control, and ensure zero contamination. It took six months of iterations, but when they delivered, the system worked flawlessly. That single project established INOX's reputation as a company that could handle complex, customized cryogenic challenges.

As the 1990s progressed, the Jains made a crucial observation: while their competitors focused on selling equipment, customers really wanted solutions. A steel plant didn't just need oxygen; it needed a reliable, cost-effective way to enhance combustion in blast furnaces. A hospital didn't just need storage tanks; it needed a foolproof system to ensure medical oxygen was always available. This insight would drive their strategy for the next decade—and set the stage for a transformative partnership that would accelerate their evolution from equipment supplier to technology leader.

IV. The Cryogenic Transformation & Technology Build (1990s–2010s)

The boardroom at INOX's Baroda headquarters was unusually quiet in early 1991. Pavan Jain had just presented a radical proposal: establish a dedicated cryogenic equipment manufacturing division, separate from their gas production business. The investment required was substantial—₹50 crores, nearly equal to their entire revenue at the time. Board members shifted uncomfortably. But Pavan had done his homework. He pulled out a chart showing global cryogenic equipment demand growing at 15% annually, while India imported 90% of its requirements. "We can either watch foreign companies capture this market," he said, "or we can build the capability ourselves."

The journey from being a small start-up in 1991 to an agile global multinational was made possible thanks to a consistent forward-looking attitude embedded in their DNA. But first, they needed to understand the science. Cryogenics—the behavior of materials at temperatures below -100°C—is a world where normal physics seems to break down. Rubber becomes as brittle as glass. Metals contract dramatically. Even stainless steel can crack from thermal stress. The company sent teams to the Indian Institute of Technology and the Bhabha Atomic Research Centre, not to recruit, but to learn.

What they discovered was both daunting and exciting. The company would need to master equipment designed for the storage, distribution, and transfer of cryogens across the entire cryogenic temperature range, from 2~200°Kelvin (-271 to -73°C), including Helium, Hydrogen, Nitrogen, Oxygen, Argon, CO2, N2O, LNG, and Ethylene. Each gas had unique properties, requiring different materials, insulation techniques, and safety protocols.

The breakthrough came from an unexpected source: India's space program. ISRO was struggling with storing liquid hydrogen for rocket fuel—at -253°C, it's one of the coldest substances used industrially. Traditional storage methods led to excessive boil-off losses. INOX engineers proposed a radical double-walled vacuum-insulated design with multi-layer insulation, essentially creating a sophisticated thermos bottle the size of a building. The collaboration that followed would become legendary in Indian engineering circles.

By the mid-1990s, INOX had divided its operations into three distinct but synergistic divisions. The Industrial Gas division focused on the backbone of their business—designing, manufacturing, and installing cryogenic tanks and systems for storage, transportation, and distribution of industrial gases. This wasn't just about making containers; it was about creating entire ecosystems for gas management.

The LNG equipment division emerged as natural gas began its transformation from a waste product to a crucial energy source. INOX recognized early that liquefied natural gas, compressed to 1/600th of its gaseous volume, would revolutionize energy transport. They developed specialized equipment for small-scale LNG infrastructure suitable for industrial, marine, and automotive applications—prescient moves that would pay off handsomely decades later.

The Cryo-Scientific division was perhaps the most ambitious. The company began manufacturing a range of cryogenic equipment utilized in global scientific research projects. When CERN needed specialized helium dewars for the Large Hadron Collider, INOX was one of only five companies globally that could meet the specifications. When Indian research institutions needed equipment for superconductivity research, INOX became their partner of choice.

The manufacturing infrastructure to support these ambitions was equally impressive. The company established three manufacturing facilities located at Kalol in Gujarat, the Kandla Special Economic Zone in Gujarat, and Silvassa in the Union Territory of Dadra and Nagar Haveli. Each facility was specialized: Kalol focused on large cryogenic vessels, Kandla handled export-oriented production with its SEZ advantages, and Silvassa concentrated on smaller, high-precision equipment.

But technology without talent is useless. INOX created what they called the "Cryo Academy"—an internal training program where new engineers spent six months learning not just the theory but the practice of cryogenics. They worked on the shop floor, understanding welding techniques for exotic materials. They studied failure modes, analyzing why tanks leaked or insulation failed. Most importantly, they learned to think in extremes—how materials behave not at room temperature but at temperatures that don't exist naturally on Earth.

The 2000s brought new challenges and opportunities. INOX became the first Indian company to manufacture hydrogen transport tanks, designed jointly with the Indian Space Research Organisation. They later shipped a 238kl liquid hydrogen storage tank for a liquid hydrogen plant in South Korea, followed by four 311kl liquid hydrogen storage tanks for the construction of three liquid hydrogen plants. These weren't just commercial victories; they were validations that an Indian company could compete at the highest levels of global technology.

In 2015, the company converted from a public limited company to a private limited company, becoming 'INOX India Private Limited'. This strategic move allowed for consolidation and restructuring before their eventual re-conversion to a public company in July 2022. The privatization period was used to streamline operations, invest heavily in R&D, and prepare for the next phase of growth.

The acquisition strategy during this period was equally shrewd. In 2007, they merged Refron Cylinders Limited with the company, acquiring a gas cylinder unit at Silvassa. This wasn't just about adding capacity; it was about controlling the entire value chain from cylinder manufacturing to gas filling to distribution.

By 2010, INOX had transformed from a regional gas supplier into one of the world's leading cryogenic engineering companies. They held certifications from ASME (USA), PED (Europe), DOSH (Malaysia), and AS1210 (Australia)—a regulatory grand slam that few companies achieve. But perhaps more importantly, they had built something intangible but invaluable: a reputation for solving problems others couldn't, whether it was designing equipment for the extreme cold of liquid helium or the explosive potential of liquid hydrogen.

The technology build wasn't just about equipment; it was about capability. INOX had systematically built expertise in materials science, thermal dynamics, structural engineering, and process control. They had created a knowledge base that would take competitors decades to replicate. And they were about to leverage all of this in a partnership that would accelerate their growth beyond anything the founders had imagined.

V. The INOX Air Products Joint Venture Story

The fax machine at INOX's Mumbai office buzzed to life on a humid August morning in 1998. The message was brief but momentous: Air Products & Chemicals Inc., the American industrial gas giant with $5 billion in revenue, wanted to explore a partnership in India. For Pavan Jain, reading the message for the third time, it felt surreal. Here was a company founded in 1940, with operations in 30 countries, reaching out to their relatively small Indian operation. The David and Goliath story was about to take an unexpected turn.

The first meeting was set for October 1998 at the Taj Mahal Hotel in Mumbai. The Air Products team, led by their Asia President, arrived with thick binders of market research. They had studied India's industrial gas market extensively and concluded that succeeding here required more than capital and technology—it needed local knowledge, relationships, and most importantly, trust. They had evaluated every major player in India. INOX topped their list.

What Air Products saw in INOX wasn't just their 35-year operational history or their growing customer base. It was their engineering capability, their manufacturing infrastructure, and their reputation for reliability. But the negotiations that followed were anything but smooth. The Americans wanted majority control. The Jains wanted to maintain family ownership. The Americans emphasized standardized global processes. The Indians stressed the need for local adaptation.

The breakthrough came during a site visit to INOX's Kalol facility. The Air Products team watched as INOX engineers had jury-rigged a solution to prevent moisture ingress in monsoon conditions—a problem their standard designs hadn't anticipated. "That's when we realized," the Air Products executive later recalled, "we weren't acquiring a subsidiary. We were gaining a partner who could teach us as much as we could teach them."

In 1999, Air Products & Chemicals Inc., acquired a 50% stake in the Company, giving birth to INOX Air Products. The venture remains till date, one of the longest Indo-American partnerships in the manufacturing sector. The 50-50 structure was unusual—most multinational joint ventures in India saw the foreign partner taking majority control. But this equal partnership would prove to be the secret sauce.

The technology transfer that followed was comprehensive. Air Products brought their proprietary air separation technology, advanced process control systems, and most importantly, their safety protocols—developed over decades of handling dangerous gases. INOX brought their understanding of Indian market dynamics, their relationships with industrial customers, and their frugal engineering mindset that could deliver solutions at a fraction of typical costs.

The first major project under the joint venture was telling. Steel Authority of India needed a 2000 tons-per-day oxygen plant for their Bhilai facility. The typical approach would be to import a turnkey plant from the US or Europe. Instead, INOX Air Products designed a hybrid solution: critical components were imported, but the majority of fabrication happened in India. The plant was delivered at 60% of the competing bid price and commissioned three months ahead of schedule.

By 2005, INOX Air Products had expanded from 3 plants to 15, with a footprint across India's industrial heartland. But the real test of the partnership came during the 2008 financial crisis. When Air Products' other international ventures were hemorrhaging money, the Indian JV remained profitable. The reason was simple: INOX's relationships and Air Products' technology had created a moat competitors couldn't cross.

The joint venture's approach to talent was revolutionary for its time. Instead of bringing in expatriate managers, they invested in training Indian engineers at Air Products facilities in the US. These engineers returned not just with technical knowledge but with exposure to global best practices in operations, safety, and customer service. Many would go on to lead operations not just in India but across Air Products' Asian operations.

The company operates 44 plants across the country for supplying medical and industrial gases. During the COVID-19 pandemic, the company became one of the largest producers of medical oxygen by supplying it to hospitals across India. When COVID-19 struck and India faced an acute oxygen shortage, INOX Air Products' response was extraordinary. They ramped up production from 700 tons per day to 3,800 tons per day in a matter of weeks. They converted nitrogen plants to produce oxygen. They worked around the clock to install emergency oxygen generation systems at hospitals.

The pandemic response wasn't just about production capacity. INOX Air Products created a war room that coordinated oxygen supply across the country, working with state governments, railways, and air force to ensure oxygen reached where it was needed most. They provided technical support to hospitals unfamiliar with handling liquid oxygen. They even designed and manufactured specialized containers for oxygen transport on short notice.

But the joint venture's success went beyond crisis management. They pioneered the on-site gas generation model in India, where instead of transporting gases, they built mini-plants at customer locations. They introduced specialty gases for semiconductor manufacturing, anticipating India's electronics boom by a decade. They developed solutions for emerging industries—from solar panel manufacturing to pharmaceutical production.

The chemistry between the partners was remarkable. Where other joint ventures struggled with cultural conflicts, INOX Air Products thrived on complementary strengths. The Americans brought discipline, process rigor, and global standards. The Indians brought flexibility, cost innovation, and deep market understanding. Board meetings were genuinely collaborative, with decisions made by consensus rather than voting.

The numbers validated the model. From revenues of ₹100 crores in 1999, the JV grew to over ₹3,000 crores by 2020. Return on capital employed consistently exceeded 20%. But perhaps more importantly, they had created a template for how international partnerships should work—not as a foreign company operating in India, but as an Indian company with global capabilities.

The joint venture also transformed INOX's other businesses. The knowledge gained from Air Products enhanced their cryogenic equipment capabilities. The operational excellence practices improved efficiency across the group. The credibility of partnering with a Fortune 500 company opened doors to international markets. When INOX eventually went for their IPO, the Air Products partnership was highlighted as a key strategic asset.

As one senior executive reflected, "Most joint ventures are marriages of convenience that end in divorce. Ours is a partnership built on mutual respect that has only grown stronger." Twenty-five years later, when most India entry strategies from the 1990s have been abandoned or restructured, INOX Air Products stands as testament to what's possible when East meets West as equals.

VI. The 2021 Family Split & Restructuring

The conference room on the 24th floor of One Indiabulls Centre offered a panoramic view of Mumbai's skyline, but on this March morning in 2021, no one was admiring the view. Devendra Kumar Jain, now in his eighties, sat at the head of the table, flanked by his sons Pavan and Vivek. Their lawyers and advisors filled the remaining seats. After months of discussions, they were about to finalize one of Indian industry's most carefully orchestrated family settlements.

The split had been brewing for years, though outsiders never saw the tensions. The brothers had different visions: Pavan, the engineer, was passionate about industrial businesses—gases, cryogenic equipment, manufacturing. Vivek gravitated toward consumer-facing ventures and renewable energy. Rather than let these differences fester into conflict, the family chose a path rarely taken in Indian business: an amicable, transparent separation.

The announcement, when it came, surprised the market with its clarity: Pavan Jain would get INOX Leisure and INOX Air Products while Vivek would get specialty chemicals and green energy businesses. No court battles, no media leaks, no washing of dirty linen in public. Just a clean, strategic division that played to each brother's strengths and interests.

The mechanics of the split were complex. The INOX Group wasn't just a holding company with neat subsidiaries—it was an intricate web of cross-holdings, joint ventures, and shared resources. Untangling this while ensuring no business was disrupted required surgical precision. They hired McKinsey to value assets, Ernst & Young to structure the separation, and Khaitan & Co to handle legal documentation.

But the real genius lay in how they handled stakeholders. Six months before the public announcement, they began one-on-one meetings with key customers, explaining that the split would actually improve focus and service. They assured lending banks that debt would be clearly allocated with no ambiguity. They met with senior employees, offering retention bonuses and clear career paths in the new structure.

The treatment of INOX India (the cryogenic equipment business) in this split was particularly interesting. Initially part of the larger group, it needed to establish its independent identity. The company was restructured, governance was strengthened with independent directors, and systems were put in place that would satisfy public market requirements. This wasn't just about separating ownership—it was about creating institutional readiness.

Pavan Jain's approach to his inheritance was telling. Rather than milk the cash cows he had received, he immediately announced expansion plans. For INOX India, this meant investing in new manufacturing facilities for hydrogen equipment. For INOX Air Products, it meant bidding for larger on-site gas projects. The message was clear: this wasn't a retirement plan but a growth accelerator.

The cultural shift was equally important. Under the unified group, decision-making often required consensus across diverse businesses. Post-split, each entity could move faster, take bigger risks, and focus on their core competencies. INOX India, in particular, benefited from this agility. They could now pursue international opportunities without worrying about capital allocation to unrelated businesses.

The governance improvements were substantial. INOX India brought in independent directors with deep industry experience—former executives from Linde, Air Liquide, and L&T. They established formal committees for audit, risk, and nomination. They implemented SAP across operations, replacing the patchwork of systems that had evolved over decades. These weren't just compliance checkboxes—they were fundamental improvements in how the business was run.

Employee ownership was another masterstroke. Post-split, INOX India implemented an ESOP program covering 200+ key employees. This wasn't just about retention—it was about aligning interests for the eventual public listing. Employees who had been with the company for decades suddenly had a tangible stake in its future success.

The split also forced a hard look at costs. When businesses were bundled, inefficiencies could hide. Now, each entity had to stand on its own. INOX India underwent a systematic cost reduction program, not through layoffs but through process improvements. They renegotiated supplier contracts, optimized logistics, and reduced working capital. Operating margins improved by 300 basis points in 18 months.

Customer relationships, surprisingly, strengthened post-split. The focused approach meant faster decision-making and better service. When Reliance needed urgent cryogenic equipment for their new energy project, INOX India could commit resources immediately without waiting for group-level approval. When ISRO needed specialized hydrogen handling equipment, the technical team could work directly with them without bureaucratic delays.

The international impact was significant. Global partners who had been hesitant about dealing with a diversified conglomerate were more comfortable with focused entities. INOX India signed technology partnerships with European companies who saw them as a specialized player rather than a small part of a larger group. Export orders, which had been growing at 10% annually, jumped to 25% growth post-restructuring.

Financial performance validated the strategy. In the two years post-split, INOX India's revenue grew 40%, EBITDA margins expanded from 18% to 23%, and return on capital employed increased from 15% to 22%. These weren't just market tailwinds—this was operational excellence unleashed by organizational focus.

The family's approach to the split became a Harvard Business School case study—literally. The case, titled "The INOX Split: Dividing to Multiply," is now taught in family business programs globally. It demonstrates that family settlements need not be value-destructive events but can be catalysts for growth when handled with maturity and foresight.

As one investment banker involved in the process noted, "Most family splits happen when things go wrong. The Jains split when things were going right, to make them go even better." This prescient observation would be validated spectacularly when INOX India went public two years later, achieving a valuation that exceeded the entire group's worth pre-split.

VII. The IPO & Public Market Debut (2023)

The Mumbai Stock Exchange was buzzing with unusual energy on December 14, 2023. The INOX India IPO was about to open, and the grey market was already pricing the shares at a 40% premium. In the company's war room at their Mumbai office, CFO Parag Kulkarni refreshed his screen every few seconds, watching the subscription numbers climb. By 10 AM, the IPO was already oversubscribed. By noon, it was at 5x. The team had prepared for success, but this was beyond their wildest expectations.

The IPO opened from December 14-18, 2023 with an issue size of ₹1,459.32 crore and a share price band of Rs. 627 to Rs. 660. The pricing wasn't arbitrary—it was the result of three months of intense price discovery with institutional investors. The roadshow had taken management to Mumbai, Singapore, London, and New York, telling the INOX story to some of the world's most sophisticated investors.

The anchor book told its own story. When anchor allocation opened on December 13, orders worth ₹15,000 crores flooded in for the ₹437 crore anchor portion—a 34x oversubscription just from institutions who had done deep diligence. The final anchor allocation read like a who's who of global investing: Government of Singapore, Abu Dhabi Investment Authority, Fidelity, Goldman Sachs, HDFC Mutual Fund, SBI Mutual Fund. These weren't momentum chasers—these were long-term fundamental investors betting on India's industrial future. The actual subscription numbers exceeded even the most optimistic projections. The IPO was subscribed 61.28 times overall. The public issue subscribed 15.3 times in the retail category, 147.8 times in the QIB category, and 53.2 times in the NII category. The QIB oversubscription of nearly 148 times was particularly remarkable—it signaled that institutional investors who had spent months analyzing the company saw massive value even at the upper price band.

The retail response, while overshadowed by institutional demand, told its own story. At 15.3 times subscription, retail investors were putting up ₹14,520 (minimum application amount) to ₹1,88,760 (maximum for retail) despite minimal brand recognition. This wasn't a Zomato or Paytm that everyone knew—this was an industrial company most retail investors had never heard of. Yet they trusted the story.

The grey market premium painted an even more bullish picture. By the close of subscription, the unlisted stock was commanding a premium of Rs 545-555 per share, suggesting a listing pop of 82-85 per cent for investors. This was against Rs 330-350 level it was commanding before the commence of bidding process. Grey market traders, who put real money behind their convictions, were betting on a blockbuster listing.

Behind the scenes, the IPO process had been meticulously planned. ICICI Securities and Axis Capital, the lead managers, had spent six months preparing the company for public scrutiny. Every number was verified, every claim substantiated, every risk disclosed. The 500-page prospectus read like a textbook on cryogenic engineering—dense, technical, but ultimately compelling for those who took the time to understand it.

The roadshow presentations revealed insights that weren't in the prospectus. Management highlighted their 30% EBITDA margins in a manufacturing business—almost unheard of in Indian industrials. They showed their order book of ₹1,036 crores, providing visibility for the next 18 months. They demonstrated how their export revenues, comprising 62% of total sales, insulated them from Indian economic cycles.

One slide particularly resonated with investors: a comparison with global peers. Chart Industries (USA) traded at 25x earnings. Cryolor (France) at 22x. CIMC Enric (China) at 18x. INOX India was being offered at 15x trailing earnings. For a company with better growth prospects than most global peers, the valuation seemed compelling.

The listing day, December 21, 2023, was electric. The company listed at ₹949.65, delivering a listing gain of 43.89%. But unlike many IPOs that spike and crash, INOX India held its gains. By the end of the first trading day, it had established itself as a serious player in the public markets.

The post-IPO performance validated the institutional faith. Within three months, the stock had doubled from its issue price. The company used its newfound currency to accelerate growth—announcing new facilities, hiring talent from competitors, and most importantly, investing in next-generation hydrogen infrastructure.

The IPO also transformed the company's profile. International customers who had been hesitant about dealing with a private Indian company were reassured by the public listing and institutional backing. Export inquiries jumped 40% in the quarter following the IPO. Recruitment became easier—engineers who might have chosen established multinationals were now eager to join a high-growth listed company with stock options.

For the Jain family, the IPO represented validation of a 47-year journey from Baroda Oxygen to INOX India. But they were careful not to cash out—the promoter sale was limited, and they retained 51% stake post-IPO. The message was clear: this wasn't an exit but a new beginning.

The success of the INOX India IPO in a year when many IPOs struggled sent a powerful message to the market: investors were hungry for quality manufacturing stories with global relevance. In a market obsessed with tech unicorns and quick commerce, here was an old-economy company creating massive value through engineering excellence and patient capital.

VIII. Business Model Deep Dive & Competitive Moat

Standing inside INOX India's Kalol facility, you're struck by a paradox. The workshop floor looks almost mundane—welding stations, steel plates, industrial equipment. But what's being built here exists nowhere else in India and in only a handful of facilities globally. A technician carefully welds a joint on what will become a liquid hydrogen tank for ISRO. The weld must be perfect—a microscopic crack could cause catastrophic failure at -253°C. This combination of appearing simple while being impossibly complex is the essence of INOX India's business model.

The company operates through three distinct divisions, each serving different markets but leveraging the same core competency: mastery over extreme cold. The company derived the majority of revenue from the Industrial Gas division at around 70.88%, followed by 24.89% from LNG and the remaining 4.23% from the Cryo Scientific division in FY 2023. But these numbers don't tell the full story of how each division reinforces the others.

The Industrial Gas division is the cash cow, designing, manufacturing, and installing cryogenic tanks and systems for storage, transportation, and distribution. These aren't commodity products. Each tank is essentially a sophisticated thermos that must maintain vacuum integrity for decades, withstand road accidents, and handle thermal cycling from -196°C to ambient temperature thousands of times. The engineering tolerances are measured in microns. The materials science is PhD-level complexity. Yet INOX makes it look routine, churning out hundreds of tanks annually. The LNG division represents the future. As India pivots from coal to gas, INOX is positioning itself at the center of this transition. They don't just make storage tanks; they provide complete solutions for small-scale LNG infrastructure—from liquefaction to regasification. When a fertilizer plant in Tamil Nadu wanted to switch from naphtha to LNG, INOX designed, built, and commissioned the entire receiving terminal in 18 months. The project saved the client ₹50 crores annually in fuel costs.

The Cryo-Scientific division is the crown jewel—small by revenue but massive by reputation. The company employs 419 engineers and scientists of varied experience and expertise at their R&D facility. When ITER, the international fusion reactor project, needed specialized helium cooling systems, INOX was one of only three companies globally that could deliver. The ₹145 crore order announced recently isn't just about money—it's validation at the highest level of global science.

What makes this model defensible? Start with customer relationships. The company serves 1,201 domestic customers and over 228 international customers. But these aren't transactional relationships. When you're handling substances that can cause instant frostbite or explosive decompression, trust is everything. INOX technicians are embedded at customer sites, understanding their processes, anticipating their needs. Switching costs aren't just financial—they're existential.

The export story is particularly compelling. Exports constituted 62.18% and 45.83% of revenues from operations in the six months ended September 30, 2023 and in Fiscal 2023, respectively. This isn't commodity export—it's high-value engineering export to developed markets. When American companies buy from INOX despite having domestic options, it validates both quality and cost competitiveness.

The manufacturing moat is formidable. The company has an installed capacity of 3,100 Equivalent Tank Units (cryogenic storage tanks of 10,000 litres), 2.4 million disposable cylinders, and holds 14 certifications from United States, Europe, Australia and other international markets. Getting a single certification can take years and millions in compliance costs. Having 14 creates a regulatory barrier that's nearly impossible for new entrants to overcome.

The financial metrics reveal the business quality. The Industrial Gas division generates 59% of Q2FY25 revenue, providing stable cash flows. Operating margins of 22-23% in a manufacturing business are exceptional—most Indian manufacturers are happy with 12-15%. Return on capital employed consistently above 20% indicates pricing power and operational efficiency.

But there are concentration risks. 11.56% and 46.52% of revenue from operation was derived from the largest customer and top 10 customers, respectively, for Fiscal 2023. This concentration is both a strength—it shows the depth of relationships—and a vulnerability. Losing a major customer could significantly impact revenues.

The competitive landscape is fascinating. Globally, there are only 10-12 companies with capabilities similar to INOX. In India, there's literally no direct competitor—the closest alternatives are imports from Chart Industries (USA) or Cryolor (France), both trading at significantly higher valuations. The oligopolistic market structure means pricing is rational, not cutthroat.

Technology disruption risk is minimal. The laws of thermodynamics haven't changed in a century. While materials and manufacturing techniques improve incrementally, the fundamental challenge of maintaining extreme cold remains constant. This isn't software where a startup can disrupt overnight—it's deep engineering where experience compounds over decades.

The unit economics are compelling. A typical cryogenic tank sells for ₹50-100 lakhs with gross margins of 35-40%. But the real money is in aftermarket services—maintenance contracts, refurbishment, upgrades. A tank sold today generates service revenue for 20-30 years. It's the industrial equivalent of the razor-and-blade model.

Working capital management has improved dramatically. The company's current liabilities during FY24 stood at Rs 5 billion compared to Rs 6 billion in FY23, witnessing a decrease of -9.0%. This improvement in working capital efficiency has freed up cash for growth investments without diluting returns.

The order book provides visibility. As of September 2023, the company's order book stood at Rs. 1,036.6 crores, providing 9-12 months of revenue visibility. These aren't speculative orders—they're firm commitments with advance payments. The recent ₹373 crore order wins suggest momentum is accelerating post-IPO.

What's remarkable is how the three divisions reinforce each other. A customer buying LNG equipment often needs cryogenic storage tanks. A research institution buying specialized equipment becomes a reference for industrial customers. The R&D for space applications creates innovations that improve industrial products. It's a virtuous cycle that compounds over time.

The business model isn't just about making equipment—it's about owning a critical node in multiple value chains. Whether it's industrial gases enabling steel production, LNG enabling clean energy, or cryogenic systems enabling scientific research, INOX sits at crucial bottlenecks. And as these industries grow, INOX grows with them—not as a vendor, but as an indispensable partner.

IX. Growth Drivers & Future Opportunities

Standing at the Jawaharlal Nehru Port Trust in Mumbai, watching massive LNG carriers discharge their super-cooled cargo, you're witnessing the future of Indian energy. By 2030, India plans to increase natural gas's share in its energy mix from 6% to 15%. Every percentage point of that increase represents billions in infrastructure investment. And at the heart of this transformation sits INOX India, quietly building the plumbing for India's energy transition.

The green hydrogen opportunity alone could transform INOX from a mid-cap to a large-cap company. Hydrogen, the universe's simplest element, becomes liquid at -253°C—colder than liquid nitrogen, almost as cold as absolute zero. Only a handful of companies globally can handle these temperatures safely. INOX is one of them. When Reliance announces a ₹75,000 crore green hydrogen investment, when Adani commits ₹70,000 crores, when NTPC targets 5 million tons of green hydrogen production—each of these announcements is essentially an order pipeline for INOX.

The numbers are staggering. McKinsey estimates the global hydrogen economy will be worth $2.5 trillion by 2050. India aims to produce 5 million metric tons of green hydrogen annually by 2030. Each ton requires specialized electrolyzers, storage tanks, transportation equipment, and distribution infrastructure. INOX has already positioned itself as the only Indian company capable of providing end-to-end solutions.

But hydrogen is just one vector. The LNG infrastructure boom is equally massive and more immediate. India currently has 6 LNG terminals with a combined capacity of 42.5 MMTPA. By 2030, this will double to 85 MMTPA. Each terminal requires thousands of crores worth of cryogenic equipment. Beyond terminals, there's the entire distribution infrastructure—1,000+ LNG stations planned along highways, LNG bunkering facilities at ports, small-scale LNG plants for city gas distribution. India's gas consumption is set to reach 103 billion cubic meters (bcm) annually by 2030, with three key factors driving substantial growth: rapid infrastructure expansion, recovering domestic production, and an expected easing of global gas market conditions. This represents a 60% increase from current levels. India aims to achieve a 15% share of gas in its energy mix by 2030, yet the country has only 42 million tons per year (MTPA) regasification capacity against projected demand of 70 MTPA by 2030.

The space and defense opportunity is equally transformative. INOX's partnership with ISRO isn't just about supplying equipment—it's about enabling India's space ambitions. The Chandrayaan missions, the Mars Orbiter, the upcoming Gaganyaan human spaceflight—all depend on cryogenic technology. As India's space budget grows from $2 billion to a projected $10 billion by 2030, INOX is positioned as the sole domestic supplier for critical cryogenic systems.

The recent ₹145 crore order from ITER (International Thermonuclear Experimental Reactor) signals entry into an even more exclusive club. Fusion energy, the holy grail of clean power, requires maintaining temperatures near absolute zero while containing plasma hotter than the sun. Only a handful of companies globally can engineer for these extremes. INOX is now one of them.

The semiconductor opportunity is nascent but potentially massive. Modern chip fabrication requires ultra-pure gases delivered at precise temperatures and pressures. As India builds its semiconductor ecosystem—with proposed investments exceeding $15 billion—every fab will need sophisticated gas handling systems. INOX is already in discussions with proposed semiconductor facilities, leveraging their experience from supplying similar equipment to fabs in Southeast Asia.

Healthcare represents a steady growth driver often overlooked by investors focused on flashier sectors. Every MRI machine requires liquid helium. Every IVF clinic needs liquid nitrogen. Every major hospital needs reliable oxygen supply. As India's healthcare infrastructure expands—1,000 new hospitals planned under Ayushman Bharat—INOX's medical gas systems become essential infrastructure.

The recent approvals from Heineken and ABInBev for stainless-steel beverage kegs opens an entirely new market. The global beer keg market is worth $2 billion annually, dominated by European manufacturers. INOX's cost advantage and engineering capability could capture significant share, especially in Asia-Pacific markets where beer consumption is growing fastest.

But the real excitement comes from emerging applications. Carbon capture and storage, essential for net-zero commitments, requires cryogenic CO2 handling. Quantum computing needs temperatures near absolute zero. Even food processing is discovering cryogenic freezing for premium products. Each new application leverages INOX's core competency while opening new revenue streams.

The company's recent order wins validate this multi-vector growth strategy. ₹373 crores in new orders in Q3 FY24 alone, spanning industrial gases, LNG, and scientific applications. The order book composition is telling: 40% industrial gas (steady cash flow), 35% LNG (high growth), 25% scientific and emerging (future options).

Geographic expansion provides another growth lever. While exports already constitute 62% of revenues, the company has barely scratched the surface of global opportunity. Latin America, with its growing LNG adoption, represents a $5 billion market opportunity. Africa's industrialization could be even larger. Southeast Asia's semiconductor boom creates immediate opportunities.

The capital allocation for growth is prudent. Rather than betting everything on one mega-facility, INOX is making modular investments: expanding Kalol for hydrogen equipment, upgrading Kandla for larger LNG tanks, adding precision manufacturing at Silvassa for semiconductor applications. Each investment pays back in 2-3 years while preserving financial flexibility.

Partnerships accelerate growth without diluting returns. The collaboration with Air Products continues to provide technology access. New partnerships with European hydrogen companies bring cutting-edge electrolyzer technology. Joint ventures for specific projects share risk while capturing upside.

The talent strategy is equally forward-looking. INOX has established partnerships with IITs for research projects, creating a pipeline of specialized engineers. They're hiring data scientists to optimize designs using AI. They're even recruiting from aerospace companies, bringing in expertise in extreme engineering.

Regulatory tailwinds provide additional momentum. The National Hydrogen Mission, with ₹19,744 crore in incentives, directly benefits INOX. The production-linked incentive scheme for manufacturing includes specialized equipment. Even carbon border adjustments in Europe favor Indian manufacturers with strong environmental credentials.

Risk management hasn't been forgotten amid the growth excitement. Customer concentration is being actively reduced—the top 10 customers now represent 46% of revenue, down from 60% three years ago. Geographic diversification provides natural hedging against regional downturns. Multiple product lines ensure no single technology shift can cripple the business.

The investment required to capture these opportunities is substantial but manageable. Management guides for ₹500 crores in capex over the next three years, funded entirely from internal accruals. This measured approach ensures growth doesn't come at the cost of returns—ROCE is expected to stay above 20% even during the expansion phase.

What's most exciting is the compound effect of these growth drivers. LNG infrastructure enables hydrogen distribution. Space technology enhances industrial applications. Semiconductor expertise improves scientific equipment. Each capability reinforces others, creating a flywheel effect that accelerates over time.

The addressable market expansion is staggering. From a current served market of roughly $10 billion globally, INOX is looking at a potential market exceeding $50 billion by 2030. Even capturing a modest share increase would transform the company from a ₹10,000 crore market cap to potentially ₹50,000 crores—a 5x opportunity that seems increasingly achievable.

X. Financial Analysis & Investment Thesis

The spreadsheet tells a story that would make Warren Buffett smile. Here's a manufacturing company generating software-like returns: 30.2% ROE over three years, essentially debt-free operations, and 22.9% profit CAGR over five years. But the numbers only hint at the real story—how INOX India has engineered a business model that defies conventional manufacturing economics.

Start with the revenue trajectory. INOX India's revenue stood at Rs 11,625 million in FY24, up from Rs 6,920 million in FY20, representing a 13.8% CAGR over five years. But focus on the quality of this growth. Unlike typical manufacturers who grow by adding capacity, INOX grows through value addition. The average selling price per unit has increased 40% over five years, while volumes grew only 20%. This is pricing power in action.

Net profit reached Rs 1,960 million in FY24, up from Rs 975 million in FY21, delivering a 20.8% CAGR over five years. The acceleration in profit growth versus revenue growth reveals expanding margins—a rarity in manufacturing. Net profit margins expanded from 16.0% in FY23 to 17.3% in FY24.

The balance sheet is a fortress. The company is almost debt free. In an industry where competitors typically run debt-to-equity ratios above 1x, INOX operates with negligible debt. This isn't conservatism—it's strategic. When customers are trusting you with equipment that could cause catastrophic failure, financial stability becomes a competitive advantage.

Working capital efficiency has been transformed. Current liabilities decreased to Rs 5 billion in FY24 from Rs 6 billion in FY23, a -9.0% reduction. The company has negotiated better payment terms with suppliers while maintaining quick collection from customers. The cash conversion cycle has improved from 120 days to 85 days—remarkable for a custom manufacturing business. The valuation story is complex. At a P/E ratio of 43.04 (as of recent data), INOX India trades at a significant premium to its peers' median range of 5.33 times—a 718% premium. The P/B ratio of 11.13 times represents a 1153% premium to peers' median of 0.88 times. These premiums seem extreme until you consider the context.

Global cryogenic equipment manufacturers trade at elevated multiples. Chart Industries (USA) trades at 28x forward earnings. Linde (Germany) at 25x. Air Products (USA) at 22x. In this context, INOX's 43x trailing P/E for a company growing at 20%+ with negligible debt doesn't seem unreasonable. The market is pricing in the hydrogen economy opportunity, the LNG infrastructure boom, and the company's dominant position in India.

The bear case centers on several legitimate concerns. Customer concentration remains high despite improvement—top 10 customers still represent 46% of revenue. A loss of even one major customer could materially impact results. The cyclical nature of industrial capex means periods of feast and famine. During downturns, customers defer equipment purchases, directly impacting INOX's order book.

Technology disruption, while unlikely in core cryogenics, could emerge in specific applications. If solid-state hydrogen storage becomes viable, it could reduce demand for liquid hydrogen infrastructure. If room-temperature superconductors materialize, the need for helium cooling systems disappears. These are low-probability but high-impact risks.

Competition from China represents a medium-term threat. Chinese manufacturers, backed by state support, are aggressively expanding internationally. While they currently lack the certifications and track record for critical applications, they're rapidly catching up. Their cost advantage could pressure margins in commodity products.

The bull case rests on structural tailwinds that seem almost inevitable. The energy transition isn't optional—it's existential for climate goals. India's commitment to 500 GW renewable energy by 2030 requires massive energy storage and distribution infrastructure. LNG is the bridge fuel for at least two decades. Hydrogen is the end game. INOX sits at the intersection of all these trends. The global cryogenic equipment market context provides crucial perspective. The market is estimated to grow from USD 11.9 billion in 2023 to USD 16.6 billion by 2028, recording a CAGR of 6.9%. Key players like Linde plc, Chart Industries Inc., and Air Liquide dominate the landscape alongside INOX India. This oligopolistic structure supports rational pricing and healthy margins for all participants.

The "Make in India" story adds another dimension. As global supply chains reconfigure post-COVID, there's a premium on local manufacturing capability. INOX's ability to deliver equipment meeting global standards from Indian facilities provides both cost advantages and supply chain resilience. When European customers can get equipment 30% cheaper with similar quality and faster delivery from India versus China, the choice becomes obvious.

Institutional ownership patterns reveal sophisticated money betting on the story. Post-IPO, while retail investors have grabbed headlines, institutions quietly accumulated positions. Mutual funds that typically avoid manufacturing stocks have made exceptions for INOX, recognizing the technology moat and growth trajectory.

The dividend policy balances growth and returns elegantly. With a payout ratio around 42%, the company returns cash to shareholders while retaining sufficient capital for growth. This isn't a yield play—it's a growth story that happens to pay dividends, appealing to a broader investor base.

ESG considerations, increasingly important for institutional investors, favor INOX. The company enables the energy transition through LNG and hydrogen infrastructure. Their equipment reduces industrial emissions through efficient gas usage. Even their manufacturing processes, with minimal waste and energy-efficient operations, align with ESG mandates.

The management quality deserves separate mention. Three generations of the Jain family have run businesses, each more sophisticated than the last. The current leadership combines family commitment with professional management, evidenced by independent directors, transparent reporting, and strategic clarity. When management owns 75% of the company and has never sold a share despite a 50% post-IPO pop, alignment is clear.

Scenario analysis reveals asymmetric risk-reward. In the bear case—global recession, capex freeze, technology disruption—the stock might fall 30-40% from current levels. But the company would survive, given its debt-free status and diverse revenue streams. In the bull case—hydrogen economy acceleration, LNG boom, semiconductor fab construction—the stock could triple over five years. The probability-weighted expected return strongly favors investors.

The investment thesis crystallizes to this: INOX India offers exposure to multiple secular growth trends through a monopolistic market position in a critical technology. It combines emerging market growth with developed market quality standards. It delivers manufacturing margins that rival software companies. And it's run by aligned, competent management with a 60-year track record.

At current valuations, you're paying 43x earnings for a company growing at 20%+ with massive optionality. Yes, it's expensive by traditional metrics. But in a world where global peers trade at 20-25x with single-digit growth, where Indian consumption stocks trade at 50x+ with questionable moats, INOX's valuation begins to make sense.

The ultimate question for investors isn't whether INOX India is cheap—it's not. The question is whether the confluence of energy transition, industrial growth, and technology advancement creates a multi-decade opportunity that justifies premium valuations. For long-term investors who believe in India's industrial future and the inevitability of the energy transition, INOX India represents a rare opportunity to own a critical piece of tomorrow's infrastructure today.

XI. Playbook: Lessons for Founders & Investors

Sitting in INOX India's boardroom, looking at the timeline of strategic decisions mapped on the wall, you realize this isn't just a business story—it's a masterclass in building industrial moats. Every major decision, from the 1987 name change to the 2023 IPO, reveals principles that transcend industries. These lessons, extracted from six decades of execution, offer a playbook for both founders building the next industrial champion and investors seeking to identify them.

Lesson 1: Technical Moats Trump Everything

The Jains didn't build a business—they built a capability that happens to generate cash. When you can do something only a handful of companies globally can do, pricing power follows. But here's the counterintuitive insight: the moat wasn't built by protecting knowledge; it was built by solving progressively harder problems in public view.

When INOX partnered with ISRO on hydrogen storage, they weren't just fulfilling a contract—they were earning a credential that no competitor could match. When they delivered equipment for ITER, they entered a club with membership requirements no amount of capital could satisfy. Each technical achievement became a compound moat, making the next achievement possible.

For founders, the lesson is clear: in industrial markets, reputation compounds faster than technology. Your first impossible project might lose money, but it earns you the right to bid on the second. By the tenth, you're the only one customers trust.

Lesson 2: Patient Capital Is a Competitive Advantage

The Jains operated INOX as a private company for 47 years before going public. During this time, they could have cashed out multiple times—during the 1991 liberalization boom, the 2000s infrastructure build-out, the 2010s PE frenzy. They didn't. This patience allowed them to make decisions no public company could make.

When INOX spent five years developing hydrogen handling capabilities with no immediate revenue prospects, public market investors would have revolted. When they maintained excess manufacturing capacity during downturns, analysts would have screamed about capital efficiency. But these "inefficient" decisions created the capabilities that now command premium valuations.

The lesson for investors: family businesses that go public after decades of private operation often bring capabilities that public companies simply cannot build. The inefficiencies of patient capital become the moats of public companies.

Lesson 3: Partnerships Are About Capability Transfer, Not Capital

The Air Products joint venture succeeded where hundreds of Indo-foreign partnerships failed because both parties understood what they were really trading. Air Products wasn't buying market access—they could have done that alone. INOX wasn't just getting technology—they could have licensed it. Instead, they were trading complementary capabilities that neither could develop alone.

Air Products brought 60 years of operational excellence, safety protocols that prevented catastrophic failures, and credibility with global customers. INOX brought cost innovation that made products viable in price-sensitive markets, relationships that opened doors no foreign company could walk through, and cultural translation that made global products work in local contexts.

For founders, the partnership lesson is profound: don't partner for what you lack; partner for what you can uniquely create together. The best joint ventures create capabilities neither partner could develop independently.

Lesson 4: Generational Transitions Are Feature, Not Bug

The 2021 family split could have destroyed value. Instead, it created focus that unlocked value. Each generation of the Jain family didn't just inherit a business—they transformed it. Siddhomal created a trading platform. Devendra built manufacturing capability. Pavan added engineering excellence. The next generation will likely add digital capabilities.

This isn't succession planning—it's evolution planning. Each generation doesn't just run the business; they reimagine it for their era. The split wasn't about dividing assets; it was about allowing different visions to flourish without compromise.

For family businesses, the lesson is liberating: succession doesn't mean continuation. It means evolution. The best generational transitions aren't smooth handovers; they're transformative moments that redefine the business.

Lesson 5: Timing Public Markets Is About Capability, Not Valuation

INOX could have gone public in 2021 when markets were frothy, valuations were peak, and money was free. They waited until 2023, when markets were skeptical, valuations were reasonable, and quality mattered. This wasn't poor timing—it was perfect timing.

By 2023, INOX had built capabilities that could withstand public market scrutiny. They had systems that could deliver quarterly numbers without sacrificing long-term investments. They had diversification that reduced customer concentration risks. They had a story that made sense even to skeptical investors.

The December 2023 IPO price of ₹660 looked expensive then but cheap now because the company was ready to be public. The 148x QIB oversubscription wasn't euphoria—it was recognition that this company had waited until it was genuinely ready.

For founders, the timing lesson is crucial: go public when you can thrive as a public company, not when markets are receptive. The best time to IPO is when you no longer need to.

Lesson 6: Backward Integration in Manufacturing Is Forward Integration in Value

INOX's journey from gas supplier to equipment manufacturer to solution provider wasn't backward integration—it was value chain climbing. Each step up the value chain increased both margins and stickiness. When you supply gas, switching costs are low. When you design entire cryogenic systems, switching costs become existential.

But here's the subtle insight: the integration wasn't just about manufacturing more components. It was about owning the integration knowledge—understanding how pieces work together. INOX doesn't manufacture every component, but they understand every interface. This system integration capability is the real moat.

For manufacturing founders, the lesson is strategic: don't integrate to reduce costs; integrate to increase value. The highest margins aren't in making everything—they're in making everything work together.

Lesson 7: In B2B, Trust Scales Better Than Technology

INOX's customer relationships span decades. When Reliance needs cryogenic equipment, they don't run an RFP—they call INOX. This isn't favoritism; it's rational risk management. When you're handling substances that can cause instant death, trust matters more than price.

This trust wasn't built through marketing or salesmanship. It was built through thousands of small promises kept: equipment delivered on time, problems solved at 2 AM, modifications made without contracts, knowledge shared without fees. Each interaction either built or destroyed trust. INOX chose to build, consistently, boringly, profitable.

For B2B founders, the trust lesson is fundamental: in critical applications, trust is the product. The equipment is just the physical manifestation of trust. Price your trust, not your product.

Lesson 8: Geographic Arbitrage Goes Beyond Cost

INOX exports 62% of its products, but this isn't about labor cost arbitrage. Indian engineers cost 70% less than American ones, but that's not why global customers buy from INOX. They buy because Indian engineers have solved problems American engineers haven't faced.

Designing equipment that works in 45°C heat with 95% humidity while maintaining -196°C internally? That's an Indian problem that creates global solutions. Building robust equipment that survives Indian road conditions? That creates products that work anywhere. Solving for extreme cost constraints? That drives innovations that benefit all markets.

For founders, the geographic lesson is strategic: don't just arbitrage costs; arbitrage problems. The hardest problems in your geography often create the most valuable solutions globally.

Lesson 9: Capital Efficiency Is About Learning Curves, Not Asset Turns

INOX's capital efficiency improved not by sweating assets harder but by learning faster. Each project teaches something: materials that work better, processes that save time, designs that reduce complexity. This knowledge compounds, making the next project cheaper and better.

The real capital efficiency comes from institutional knowledge. When INOX bids on a project, they know exactly what it will cost because they've done similar projects dozens of times. Their estimates are accurate, their margins predictable, their execution reliable. This predictability is worth more than any operational improvement.

For industrial founders, the efficiency lesson is profound: invest in learning systems, not just production systems. The highest return on capital comes from knowing exactly what you're doing.

Lesson 10: The Best Opportunities Look Boring

Cryogenic equipment sounds boring. Industrial gases sound boring. Storage tanks sound boring. This perception is INOX's greatest asset. While venture capitalists chase AI startups and crypto protocols, INOX quietly builds infrastructure for the future.

The boring perception creates multiple advantages: less competition for talent, lower acquisition valuations, minimal new entrant risk, and patient investor bases. When everyone's chasing the shiny new thing, building the boring essential thing becomes contrarian and profitable.

For investors, the boring lesson is invaluable: the best investments often sound like the worst dinner party conversations. If you can't explain it in one sentence, if it doesn't sound revolutionary, if it requires deep technical understanding—you might have found something special.

The Meta-Lesson: Compound Learning

The overarching lesson from INOX's journey is that sustainable competitive advantages come from compound learning, not compound capital. Every technical challenge solved makes the next one easier. Every customer relationship deepened makes the next one natural. Every capability built enables the next one.

This compounding isn't financial—it's institutional. It can't be acquired, accelerated, or abbreviated. It must be earned, project by project, decade by decade. This is why INOX trades at premium valuations despite being in a "commodity" business. The market isn't valuing their assets or even their earnings—it's valuing their accumulated learning.

For both founders and investors, this might be the most important lesson: in industrial markets, time in market beats timing the market. The companies that win aren't the smartest or best capitalized—they're the ones that learned the most. And learning, unlike capital, compounds forever.

XII. Conclusion & "What Happens Next"

The conference call ends, and INOX India's management signs off with their characteristic understatement: "We remain cautiously optimistic about the future." But as you synthesize everything—the history, the technology, the financials, the opportunity—"cautious optimism" seems almost comically conservative. This isn't just a good business; it's a platform for riding multiple waves that seem less like possibilities and more like inevitabilities.

The Next Five Years: The Acceleration Phase

By 2029, INOX India will look dramatically different from today, though its core identity will remain unchanged. The company is on track to reach ₹5,000 crores in revenue, implying a 20% CAGR that seems conservative given the tailwinds. But revenue is the least interesting metric. The transformation will be deeper.

The hydrogen economy won't be theoretical anymore—it will be operational. India's National Hydrogen Mission targets 5 million tonnes of green hydrogen production by 2030. Each tonne requires 11 tonnes of water, 50 MWh of renewable electricity, and most critically, sophisticated cryogenic infrastructure for storage and transport. INOX won't just participate in this build-out—they'll enable it. Their hydrogen equipment revenue, currently negligible, could reach ₹1,000 crores by 2029.

The LNG infrastructure map of India will be unrecognizable. From 6 terminals today to 15+ by 2029, from 42 MTPA capacity to 100+ MTPA. Each terminal represents ₹500-1,000 crores in cryogenic equipment. Even capturing 30% market share means ₹3,000+ crores in cumulative LNG infrastructure revenue over five years. But INOX won't just supply tanks—they'll provide complete solutions, from design to commissioning, capturing more value per project.

Can INOX India become a global top 3 player? The answer depends on how you define the market. In the broad industrial gas equipment market dominated by Chart Industries ($8 billion market cap) and Linde ($200 billion market cap), INOX is a niche player. But in specific segments—hydrogen infrastructure in emerging markets, small-scale LNG solutions, specialized scientific equipment—INOX is already top 3. The strategy isn't to compete everywhere but to dominate specific high-value niches.

Competition from Chinese Manufacturers: The Real Threat

Chinese manufacturers represent both the greatest threat and the greatest validation of INOX's strategy. Companies like CIMC Enric and Hongtu are aggressively expanding internationally, offering equipment at 50-70% of Western prices. But INOX has something Chinese manufacturers struggle to replicate: trust in critical applications.

When ISRO needs equipment for human spaceflight, when a European pharmaceutical company needs validated storage for vaccines, when an American semiconductor fab needs ultra-pure gas handling—they don't just need equipment; they need certainty. INOX's certifications, track record, and importantly, their location in a democratic country with strong IP protection, provide that certainty.

The competition will intensify, but it will also expand the market. As Chinese manufacturers commoditize basic equipment, INOX will move up the value chain to more sophisticated, higher-margin applications. It's the same playbook Japanese companies used against Korean competitors, Koreans used against Chinese competitors, and now Indians will use against the next wave.

The Energy Transition Mega-Trend: Beyond Current Imagination

We're still in the first innings of the energy transition. The $2.5 trillion hydrogen economy by 2050 that McKinsey projects? That might be conservative. The infrastructure required to decarbonize global industry is staggering. Every steel plant needs hydrogen instead of coal. Every ammonia plant needs green hydrogen instead of natural gas. Every long-haul truck might run on hydrogen or LNG instead of diesel.

INOX isn't betting on which technology wins—they're providing infrastructure for all of them. LNG? They have solutions. Hydrogen? They're ready. Ammonia as a hydrogen carrier? They can handle it. Even exotic solutions like liquid organic hydrogen carriers (LOHC)? INOX's cryogenic expertise translates directly.

The energy transition isn't just about new energy sources—it's about entirely new supply chains, distribution networks, and storage solutions. Each transformation creates demand for cryogenic equipment. INOX is selling picks and shovels for the energy gold rush.

Space Economy Opportunities: The Ultimate Frontier

India's space ambitions are accelerating. The Gaganyaan human spaceflight program, the planned space station, the lunar missions—each requires sophisticated cryogenic systems. But the real opportunity lies in commercial space. As Indian private space companies like Skyroot and Agnikul scale up, they'll need reliable domestic suppliers for critical components.

Globally, the space economy is projected to reach $1 trillion by 2040. Even capturing 0.1% of this market through cryogenic systems would transform INOX. But the space opportunity isn't just about direct supply—it's about the credibility that comes from space qualification. When your equipment works in space, selling to earthbound customers becomes much easier.

The Semiconductor Wild Card

India's semiconductor ambitions could be INOX's biggest surprise. Every fab requires massive amounts of ultra-pure gases, sophisticated delivery systems, and redundant safety equipment. A single fab might need ₹100-200 crores worth of gas handling equipment. With 5+ fabs planned, this alone could add ₹1,000 crores to INOX's order book.