Indian Railway Finance Corporation: The Rails That Fund the Nation

I. Introduction & Cold Open

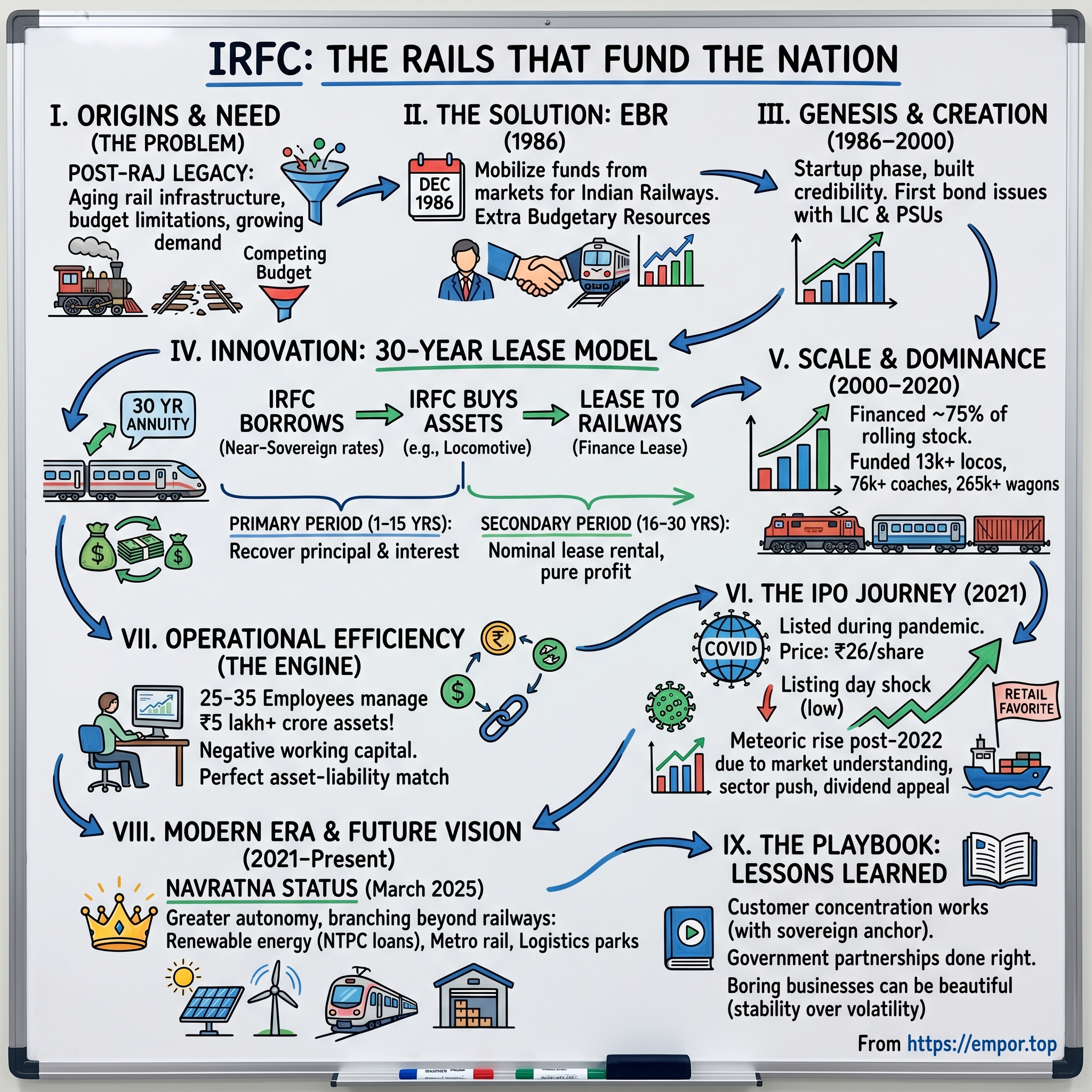

What if I told you there's a company that owns 75% of India's trains but has never operated a single one? A company with just 35 employees that manages over ₹5 lakh crore in assets? This is the story of the Indian Railway Finance Corporation (IRFC) – perhaps the most important company in India that most people have never heard of.

So far, it has funded acquisition of 13764 locomotives, 76735 passenger coaches, 265815 wagons, which constitute around 75% of the total rolling stock fleet of Indian Railways. Think about that for a moment: three-quarters of every train you see crisscrossing India's vast landscape exists because of this financial engineering marvel. IRFC's cumulative funding to rail sector has crossed Rs.5.04 lakh crore as of 31st March, 2022.

This isn't just another public sector undertaking story. This is about how a small team in New Delhi figured out how to transform India's railway financing from a budgetary burden into a sophisticated market mechanism. It's about creating a money machine so efficient that it has maintained zero NPAs for nearly four decades. And it's about a company that went public at perhaps the worst possible time – during a pandemic – yet has become one of retail India's most fascinating investment stories.

The fundamental question we're exploring today is both simple and profound: How does a company with just twenty-five in number employees finance the world's fourth-largest railway network? How did IRFC become the invisible backbone of Indian Railways, and what does its story tell us about infrastructure financing in emerging markets?

In this deep dive, we'll journey from the British Raj's railway legacy through economic liberalization, witness the birth of one of India's most unique financial innovations, and understand why In March 2025, IRFC was given the Navaratna status by the Government of India, becoming the 26th PSU in this list. We'll explore how a 30-year lease structure became a perpetual money machine, dissect an IPO that defied conventional wisdom, and peek into a future where IRFC might finance far more than just trains.

Buckle up – this is a story of financial engineering at nation-building scale.

II. The British Raj Legacy & Why India Needed IRFC

To understand why IRFC exists, we need to travel back to the twilight years of the British Raj and the decades that followed independence. The British left India with one of the world's largest railway networks – a double-edged legacy that was both a lifeline for economic development and a financial albatross around the young nation's neck.

Post-independence, Indian Railways operated as a department of the government, funded entirely through annual budgetary allocations. Every locomotive, every coach, every kilometer of track had to compete with schools, hospitals, and defense for a slice of the national budget. This system worked, barely, through the 1950s and 60s when the network's needs were relatively modest. But by the 1970s, cracks were beginning to show.

The railway infrastructure was aging rapidly. Steam engines needed replacement with diesel and electric locomotives. The freight capacity was woefully inadequate for a growing economy. Passenger trains were overcrowded, outdated, and increasingly unsafe. The modernization bill was staggering – estimates suggested Indian Railways needed investments equivalent to several years of the entire national budget.

The traditional financing model was breaking down. Government budgets were stretched thin, fighting inflation, funding wars, and managing oil shocks. International lenders like the World Bank were willing to help, but their loans came with conditions and were nowhere near sufficient for the scale of transformation needed. Something had to give.

Enter the 1980s – a decade of reckoning. The railway system was literally falling apart. Accidents were increasing. Freight movement was bottlenecked, strangling industrial growth. The passenger experience was deteriorating to the point where those who could afford alternatives were abandoning trains. The ministry realized that without radical financial innovation, Indian Railways would become a monument to decay rather than an engine of growth.

The concept of "Extra Budgetary Resources" (EBR) emerged from this crisis. If the government couldn't fund railways from the budget, perhaps the market could. But how do you get private capital to fund public infrastructure? How do you make railway assets attractive to investors? The traditional government department structure made this nearly impossible. Railways needed a dedicated financial vehicle – something that could speak the language of capital markets while serving the needs of a public utility.

The company was set up in December 1986 for mobilizing funds from domestic and overseas markets to meet the pre-dominant portion of Extra Budgetary Resources requirement of Indian Railways. But the decision to create IRFC wasn't made in isolation. It was part of a broader recognition that India needed to tap capital markets for infrastructure development.

The timing was crucial. Economic liberalization was still five years away, but the seeds were being planted. Progressive bureaucrats and economists within the Railway Ministry understood that the future lay not in bigger budgets but in smarter financing. They envisioned an entity that could borrow at competitive rates, leverage government guarantees, and create a sustainable funding model for railway modernization.

The alternative models considered were telling. One option was to privatize parts of the railway system, but this was politically impossible in socialist India. Another was to create multiple regional financing entities, but this would fragment borrowing power and increase costs. The ministry even explored letting Indian Railways borrow directly, but accounting rules and bureaucratic procedures made this impractical.

What emerged was a uniquely Indian solution – a government-owned company that operated like a private financial institution. IRFC would be owned by the Railways but incorporated under the Companies Act. It would have the government's backing but operate with market discipline. It would serve a single customer but access diverse funding sources.

IRFC was founded on 12 December 1986, born from necessity but designed with remarkable foresight. The bureaucrats who created it probably didn't realize they were laying the foundation for what would become one of the world's most successful infrastructure financing models. They were simply trying to solve an immediate problem: how to fund the railways when the treasury was empty.

The structure they created was deceptively simple. IRFC would borrow money from the market, use it to buy railway assets, and lease those assets to Indian Railways. The lease payments would cover the borrowing costs plus a margin. The government would guarantee the payments, making it virtually risk-free for lenders. It was financial engineering at its most elegant – turning a funding crisis into a sustainable business model.

This model would prove so successful that it would not only transform Indian Railways but become a template for infrastructure financing across emerging markets. But first, IRFC had to prove it could work. The real test would come in the years immediately following its creation, as this fledgling company attempted to convince skeptical investors that lending to a government entity through a newly created intermediary was a good idea.

III. The Genesis: Creating a Railway Bank (1986–2000)

It started borrowing from the market in 1987–88. Those first few months after incorporation were crucial. IRFC was essentially a startup with a massive mission but no track record, no credit history, and no proven model. The team, handful of officials deputed from the Railway Ministry and financial institutions, had to build credibility from scratch.

The first bond issue was a nerve-wracking affair. The company needed to raise funds in a market that barely understood what IRFC was, let alone why it existed. The pitch was complex: "We're a government company that's not quite government, borrowing money to buy trains that we'll own but never operate, leasing them to Railways who will pay us back over 30 years." It sounds almost absurd when stated plainly, yet this was the revolutionary model they were selling.

The early investors were primarily public sector banks and insurance companies, particularly Life Insurance Corporation (LIC). These institutions understood government guarantees and were comfortable with long-term paper. But even they needed convincing. IRFC's founding team spent months in meetings, explaining the model, demonstrating the payment security, and essentially educating the market about this new instrument.

The breakthrough came with the realization that IRFC bonds were essentially sovereign paper with a slight premium. The government guarantee meant that default was virtually impossible – if Indian Railways didn't pay, the government would. This wasn't just a promise; it was structured into the very fabric of how IRFC operated. Every lease agreement included provisions that made railway payments a budgeted expenditure, as sacred as defense spending or civil servant salaries.

It is also registered as Systemically Important Non–Deposit taking Non Banking Financial Company (NBFC – ND-SI) and Infrastructure Finance Company (NBFC- IFC) with Reserve Bank of India (RBI). This registration, obtained in the early years, was crucial. It gave IRFC the regulatory framework to operate as a financial institution while maintaining its special purpose vehicle status.

The first rolling stock acquisition marked a pivotal moment. IRFC purchased a set of locomotives and coaches, immediately leasing them to Indian Railways. The physical assets existed, the lease was signed, and the revenue stream began. It was proof of concept – the model worked. But this was just the beginning of a complex financial engineering exercise that would evolve over the years.

The 30-year lease structure wasn't arbitrary. It was carefully calibrated to match asset life with financing terms. Railway rolling stock typically has an operational life of 30-35 years. By structuring leases for 30 years, IRFC ensured that assets would generate revenue throughout their useful life. The bifurcation into two 15-year periods was equally strategic – the first 15 years would recover principal and interest, while the second period would generate pure profit at nominal rates.

Building credibility in international markets was the next frontier. By the mid-1990s, IRFC was exploring foreign currency borrowings. The logic was simple: international markets offered lower interest rates, and railways needed foreign exchange for importing technology and equipment. But this introduced currency risk – a challenge that IRFC had to learn to manage.

The Asian Financial Crisis of 1997 was IRFC's first major test. Currency volatility, interest rate spikes, and market panic could have derailed the young company. But IRFC's model proved remarkably resilient. The government guarantee held firm, lease payments continued uninterrupted, and IRFC actually emerged stronger, having demonstrated its stability during turbulent times.

By 2000, IRFC had established itself as an indispensable part of Indian Railways' ecosystem. From the humble beginning in 1986, Indian Railway Finance Corporation has traversed a long way to establish its unique identity in the financial services sector of India. The company had successfully raised thousands of crores from domestic and international markets, funded hundreds of locomotives and thousands of coaches, and most importantly, proved that market-based infrastructure financing could work in India.

The innovation during this period went beyond just financial engineering. IRFC pioneered standardized lease agreements, developed sophisticated asset-liability management systems, and created frameworks for pricing different types of rolling stock. They were essentially writing the playbook for infrastructure financing in India, one lease at a time.

The human story behind these achievements is equally remarkable. The small team at IRFC was handling transactions worth thousands of crores with the efficiency of a boutique investment bank. They were negotiating with international lenders, managing currency hedges, structuring complex financial instruments, and doing it all with a fraction of the resources that private sector financial institutions had.

Internal challenges were constant. How do you maintain government ownership while operating with market efficiency? How do you balance public service obligations with commercial viability? How do you ensure that a 30-year lease signed today remains relevant three decades later? These questions didn't have easy answers, and IRFC had to learn through experience, sometimes painful, what worked and what didn't.

The relationship with Indian Railways was evolving too. Initially seen as just another funding source, IRFC gradually became a strategic partner in railway planning. The company's market intelligence helped Railways understand funding costs, its financial expertise influenced procurement decisions, and its long-term perspective shaped modernization strategies.

By the turn of the millennium, IRFC had transformed from an experimental financing vehicle into the backbone of railway funding. The company had not only survived but thrived, creating a model that would soon be replicated across other infrastructure sectors. But the real test of the model's robustness would come in the next phase, as IRFC scaled up to handle the massive infrastructure buildup that India's economic boom would demand.

IV. The Leasing Innovation: A 30-Year Money Machine

IRFC follows a leasing model to finance the rolling stock assets and project assets of Indian Railways. The lease period is typically for 30 years, comprising a primary component of 15 years followed by a secondary period of 15 years. This structure, elegant in its simplicity, is actually one of the most sophisticated financial innovations in infrastructure funding globally.

Let's dissect this money machine. When IRFC acquires a locomotive worth, say, ₹30 crores, it doesn't just hand it over to Indian Railways. Instead, it enters into a finance lease – a carefully structured agreement where The rolling stock is therefore owned by the IRFC and is leased to the IR on a finance lease model for a term of 30 years. This ownership structure is crucial because it gives IRFC a tangible asset base while ensuring Indian Railways gets the equipment it needs without the upfront capital expenditure.

The genius lies in the payment structure. Generally, the principal and the interest component are realised within the initial period of 15 years. During these first 15 years, Indian Railways pays lease rentals that cover IRFC's borrowing cost, the principal amount, and a margin. This margin, typically 40-55 basis points, might seem modest, but when applied to thousands of crores worth of assets, it generates substantial profits.

But here's where it gets interesting. After 15 years, when IRFC has recovered its entire investment plus interest, the asset doesn't revert to Railways. The lease continues for another 15 years, but now at a nominal rate – often just 1% of the original lease rental. After the expiry of lease term, the rolling stock asset is sold to the IR for a nominal price, typically ₹1,000 per asset, regardless of its original cost.

Why would Indian Railways agree to such a structure? The answer reveals the beautiful symbiosis of this relationship. Railways gets immediate access to assets without budget constraints, spreads payments over three decades, and enjoys operational control from day one. IRFC gets a guaranteed revenue stream backed by sovereign assurance, virtually eliminating credit risk.

The financial engineering goes deeper. IRFC matches its borrowing tenure to lease periods, ensuring perfect asset-liability synchronization. If it borrows for 10 years to fund an asset, it structures the lease payments to cover that debt within the same period. This eliminates interest rate risk and ensures predictable cash flows.

Consider the scale of this operation. The period of lease with respect to Rolling Stock Assets is typically 30 years, comprises a primary period of 15 years followed by a secondary period of 15 years, unless otherwise revised by mutual consent. Each asset becomes a 30-year annuity, generating steady cash flows with zero default risk. It's essentially a government bond wrapped in a lease agreement.

The margin structure is particularly clever. IRFC's spread isn't fixed; it's determined annually in consultation with the Railway Ministry. This allows flexibility to adjust for market conditions while ensuring IRFC remains profitable. In years when borrowing costs are high, margins might increase. When markets are favorable, Railways benefits from lower lease rentals.

Currency risk management adds another layer of sophistication. When IRFC borrows in foreign currency to take advantage of lower international rates, the currency hedging costs are built into the lease rentals. Risk related to foreign currency hedging cost or hedging cost for interest rate fluctuation are built into weighted average cost of borrowing (WACB) of which IRFC earns a margin as determined by MoR. This means Railways bears the ultimate currency risk, but benefits from potential savings when rupee appreciates.

The comparison with aircraft leasing is instructive. While aircraft leasing companies face residual value risk, airline bankruptcy risk, and asset obsolescence, IRFC faces none of these challenges. Trains don't become obsolete as quickly as planes, Indian Railways can't go bankrupt (it's a government department), and there's no residual value risk because Railways must buy the asset at lease end.

This model creates what finance theorists would call a "perfect arbitrage" – IRFC borrows at near-sovereign rates and lends at a slightly higher rate to a sovereign-backed entity. The spread might be thin, but the volumes are massive and the risk is virtually zero. It's like running a toll booth on a highway that only government vehicles can use, and the government guarantees the toll payments.

The scalability is remarkable. Once the legal framework and operational processes were established, IRFC could finance one locomotive or one thousand with essentially the same team. The marginal cost of each additional lease is negligible, making this one of the most efficient financing mechanisms ever created.

From 2011-12 onwards, IRFC has forayed into funding of railway projects and capacity enhancement works. This expansion into project financing added another dimension to the model. Instead of just leasing rolling stock, IRFC began financing infrastructure projects like electrification, doubling of tracks, and station modernization. These projects follow a similar lease model but with modifications to account for construction periods and project-specific risks.

The beauty of this system is its self-reinforcing nature. As IRFC finances more assets, its balance sheet grows, allowing it to borrow at even better rates. These savings are partially passed on to Railways through lower lease rentals, creating a virtuous cycle of cost reduction and capacity expansion.

Risk management deserves special attention. While credit risk is virtually eliminated through government guarantees, IRFC still manages interest rate risk, liquidity risk, and operational risk. The company maintains sophisticated ALM (Asset Liability Management) systems, ensuring that payment inflows match outflows almost perfectly. It's like conducting a financial orchestra where every instrument plays in perfect harmony.

The model has proven so robust that it survived multiple economic cycles, changes in government, and even global financial crises without a single default. This isn't just good fortune; it's the result of careful structuring where risks are identified, quantified, and either eliminated or passed on to parties best equipped to handle them.

What makes this truly remarkable is that this entire machinery operates with minimal human intervention. Once a lease is signed, payments flow automatically through the government budget system. IRFC doesn't need an army of collection agents or credit officers. IRFC has made its own mark in the financial market for its slim organizational setup, professional workforce, strong management and robust internal systems.

V. Scale & Dominance: Becoming India's Railway Banker (2000–2020)

The new millennium marked an inflection point for IRFC. India's economy was taking off, and with it came an insatiable demand for railway capacity. The golden quadrilateral freight corridor, dedicated freight corridors, and massive passenger capacity expansion – all needed financing at a scale previously unimaginable.

The numbers tell a staggering story of growth. From financing a few hundred crores annually in the 1990s, IRFC scaled up to thousands of crores per year. By 2010, the company was raising over ₹10,000 crores annually. By 2020, this had multiplied several fold. The cumulative impact was transformative: So far, it has funded acquisition of 13764 locomotives, 76735 passenger coaches, 265815 wagons, which constitute around 75% of the total rolling stock fleet of Indian Railways.

This wasn't just quantitative growth; it was a qualitative transformation. IRFC evolved from being a simple lease financing company to becoming Indian Railways' strategic financial partner. When Railways needed to modernize its locomotive fleet, IRFC structured innovative financing solutions. When high-speed rail projects were conceptualized, IRFC was at the table designing funding mechanisms.

From 2011-12 onwards, IRFC has forayed into funding of railway projects and capacity enhancement works. This expansion beyond rolling stock was crucial. Station redevelopment, track electrification, signaling systems – infrastructure projects that were traditionally funded through budgetary support now had a market-based financing option. IRFC developed new expertise in project finance, construction risk assessment, and infrastructure valuation.

The relationship ecosystem expanded significantly. IRFC has also been lending to various entities in Railway sector like Rail Vikas Nigam Limited (RVNL), Railtel, Konkan Railway Corporation Limited (KRCL), Pipavav Railway Corporation Limited (PRCL) etc. These weren't just financial transactions; they represented IRFC's evolution into a comprehensive railway sector financier.

International recognition followed domestic success. IRFC began accessing international capital markets more aggressively, issuing bonds in foreign currencies, tapping into Japanese low-interest loans, and even exploring Islamic finance instruments. The company's credit rating – consistently AAA domestically and investment grade internationally – opened doors to the cheapest capital available globally.

The competitive moat that IRFC built during this period was formidable. First, the institutional knowledge accumulated over decades was irreplaceable. IRFC understood railway financing in a way no other institution could. Second, the trust relationship with Indian Railways was rock-solid. Third, the regulatory framework was essentially custom-built for IRFC's operations.

Would-be competitors faced insurmountable barriers. Private financiers couldn't match IRFC's borrowing costs because they lacked sovereign backing. Other public sector companies didn't have IRFC's specialized expertise or operational efficiency. Foreign lenders were wary of directly financing Indian Railways due to bureaucratic complexities. IRFC had effectively created a monopoly, not through regulation but through competence.

The financial performance during this period was remarkably consistent. Year after year, IRFC delivered steady profit growth, maintained pristine asset quality, and generated returns that, while not spectacular, were absolutely reliable. The company became a dividend aristocrat of the public sector, consistently paying out substantial dividends to the government.

Technology adoption, though gradual, was significant. IRFC digitized its operations, implemented sophisticated treasury management systems, and created real-time asset tracking mechanisms. The company that started with paper ledgers was now running complex financial models and managing derivatives portfolios.

The human capital story is equally impressive. Despite handling assets worth lakhs of crores, IRFC maintained its lean structure. The productivity per employee was astronomical – each employee effectively managed assets worth thousands of crores. This wasn't just efficiency; it was a fundamental rethinking of how financial institutions could operate.

Risk management evolved to match the scale. IRFC developed comprehensive frameworks for interest rate risk, currency risk, and operational risk. The company's risk models were sophisticated enough to satisfy international lenders while simple enough to be understood by government auditors. It was a delicate balance, masterfully maintained.

The 2008 global financial crisis was a watershed moment. While banks worldwide collapsed and credit markets froze, IRFC continued operating normally. The government guarantee meant funding never dried up, and railway operations continued uninterrupted. This resilience during the crisis enhanced IRFC's reputation as one of the safest infrastructure financiers globally.

By 2015, IRFC was financing nearly half of Indian Railways' annual capital expenditure. In Fiscal 2020, IRFC financed Rs71,392 cr accounting for 48.22% of the actual capital expenditure of the Indian Railways. This wasn't just market dominance; it was market definition. IRFC had become so integral to railway operations that any discussion of railway modernization automatically included IRFC financing.

The innovation continued with new products. Green bonds for electric locomotives, social bonds for passenger amenities, and infrastructure bonds for station development – IRFC was constantly evolving its product suite to match changing market preferences and regulatory requirements.

VI. The IPO Story: Going Public at the Wrong Price?

The company launched its initial public offering on 18 January 2021 and got listed on the National Stock Exchange of India and Bombay Stock Exchange on 29 January 2021. The timing couldn't have been more challenging – India was still reeling from the first wave of COVID-19, markets were volatile, and investor sentiment was fragile. Yet, this IPO would become one of the most interesting episodes in Indian capital market history.

The government's decision to list IRFC was part of a broader disinvestment agenda. Four other railway companies had already gone public, but IRFC was different. This wasn't an operating company with visible assets and operations; this was a financial intermediary whose value lay in complex lease agreements and future cash flows. How do you value such an entity? How do you explain it to retail investors?

The issue is priced at ₹26 per share, with the price band set at Rs.25 to Rs.26 per equity share and the lot size is of 576 shares. The pricing immediately sparked debate. Based on post-IPO outstanding shares and TTM earnings till September 2020, IRFC will trade at a P/E of 9.6. For a company with IRFC's growth profile and risk characteristics, this seemed remarkably cheap.

The IPO structure revealed the government's priorities. Fresh issue of 118.8 crore shares would raise capital for IRFC, while an offer for sale of 59.4 crore shares would bring money to the government. Post-IPO, Centre's stake will come down to 86.4 per cent, maintaining firm control while meeting SEBI's public shareholding norms.

The response was extraordinary. Despite pandemic fears, retail investors flocked to the IPO. The issue was subscribed 3.49 times overall, with the retail portion subscribed 3.64 times. This wasn't just institutional interest; ordinary Indians were betting on IRFC. The retail participation was particularly noteworthy given that many investors didn't fully understand IRFC's business model.

Then came the listing day shock. Opening Price on NSE: INR24.9 per share (down 4.23% from IPO price). The stock listed below its issue price and Closing Price on NSE: INR24.75 per share (down 4.81% from IPO price). For retail investors who had bid enthusiastically, this was a harsh introduction to IRFC.

The post-listing performance was even more dramatic. The stock languished between ₹20-25 for nearly two years, testing investor patience. Many retail investors, burned by the immediate listing loss, sold at a loss. But this is where the story gets interesting. From December 2022, IRFC stock began a meteoric rise, reaching over ₹200 by mid-2024 – a nearly 8x return from its lows.

What changed? Several factors converged. First, the market began understanding IRFC's business model better. The company's consistent financial performance, zero NPAs, and steady dividend payouts attracted value investors. Second, the railway sector gained prominence as the government announced massive infrastructure investments. Third, and perhaps most importantly, retail investors discovered IRFC as a "dividend play" – a steady income generator in a low-interest rate environment.

The IPO pricing debate continues. Was ₹26 too high given immediate market conditions, or too low given long-term fundamentals? The answer depends on your time horizon. For those who sold on listing day, it was overpriced. For those who held or accumulated during the downturn, it was the bargain of the decade.

As of 2024-25 Q3 reports, its promoter group (Government of India) holds 86.36% ownership while the public has the rest of the 13.64% shares. This shareholding pattern reveals an interesting dynamic. Despite being publicly listed, IRFC remains firmly under government control, limiting free float but providing stability.

The retail investor phenomenon around IRFC deserves special attention. Post-listing, IRFC developed a cult following among retail investors. Online forums buzzed with discussions about IRFC's "hidden value." YouTube channels dedicated entire series to explaining IRFC's business model. The stock became a favorite among small investors looking for "safe" public sector stocks.

This retail enthusiasm had real consequences. The stock's volatility increased dramatically post-listing, with retail sentiment driving sharp moves in both directions. During the 2023-24 rally, retail investors were net buyers even as institutions booked profits. It was a rare instance of retail investors being ahead of institutions in recognizing value.

The IPO also marked IRFC's transformation from a quiet, backend financial institution to a public company under constant scrutiny. Quarterly results were now dissected, management commentary analyzed, and every railway sector development viewed through its impact on IRFC. The company had to adapt to this new reality, improving disclosure standards and investor communication.

The government's handling of the IPO raises important questions about public sector disinvestment. Should the government have waited for better market conditions? Should the price band have been lower to ensure a successful listing? Or was the government right to prioritize fiscal needs over market optics? These questions don't have easy answers but offer lessons for future PSU listings.

International investors largely stayed away from the IPO, viewing it as too India-specific and government-dependent. This limited foreign institutional participation but made IRFC a uniquely domestic story – a rare large-cap stock dominated by Indian investors.

VII. The Business Model Deep Dive: How IRFC Makes Money

The Company's principal business therefore is to borrow funds from the financial markets to finance the acquisition / creation of assets which are then leased out to the Indian Railways. This deceptively simple statement masks one of the most elegant business models in infrastructure finance. Let's peel back the layers to understand how IRFC transforms this basic principle into a profit-generating machine.

The revenue architecture is surprisingly straightforward yet remarkably robust. In 2019, 99.81% of the total operating revenue came from Lease income, interest on loans and pre-commencement lease interest income. This concentration might seem risky, but when your single revenue source is backed by the sovereign guarantee of the world's largest democracy, concentration becomes a strength, not a weakness.

Let's walk through a typical transaction. IRFC identifies Indian Railways' rolling stock requirements through annual planning exercises. Say Railways needs 100 new locomotives costing ₹3,000 crores. IRFC raises this amount from the market through bonds or loans, typically at rates just marginally above government securities – let's say 7.5%. IRFC then purchases these locomotives and leases them to Railways at 7.9%, earning a spread of 40 basis points.

On ₹3,000 crores, 40 basis points translates to ₹12 crores annually in pure spread income. Multiply this across IRFC's entire asset base of over ₹4 lakh crores, and you're looking at hundreds of crores in virtually risk-free profit. But the genius lies not just in the spread but in the structure.

The interest rate risk management is particularly sophisticated. IRFC doesn't just borrow and lend; it actively manages its portfolio to optimize returns. When interest rates are expected to fall, IRFC might borrow longer-term to lock in current rates. When rates are rising, it might prefer shorter-term instruments with reset provisions. This active management adds basis points to the spread without additional credit risk.

Fee income, though small, adds another dimension. IRFC charges processing fees for lease arrangements, commitment fees for sanctioned but undrawn amounts, and prepayment penalties if Railways decides to buy assets before lease expiry. These fees, while contributing less than 1% of revenue, provide cushion during margin compression periods.

It is also registered as a Systemically Important Non-Deposit Taking NBFC and Infrastructure Finance Company. This regulatory classification is crucial for understanding IRFC's operational advantages. As an Infrastructure Finance Company, IRFC enjoys certain regulatory relaxations – higher exposure limits, lower cash reserve requirements, and preferential treatment in priority sector lending norms. These benefits translate directly to the bottom line through lower operational costs and higher leverage capacity.

The capital efficiency metrics are extraordinary. With just twenty-five in number employees managing over ₹5 lakh crores in assets, IRFC achieves productivity levels that would make any financial institution envious. The per-employee asset management exceeds ₹20,000 crores – a figure that defies conventional banking wisdom.

How is such efficiency possible? The answer lies in process standardization and automation. Every lease follows a template. Payment collection is automatic through government budget mechanisms. Asset monitoring is minimal since Railways maintains the assets. Credit assessment is unnecessary given sovereign backing. IRFC has essentially eliminated most traditional banking functions while retaining the profitable core of financial intermediation.

The margin story reveals careful calibration. IRFC's spread isn't maximized; it's optimized. The company could potentially demand higher margins given its monopolistic position, but that would invite political scrutiny and potential competition. By maintaining modest spreads, IRFC ensures sustainability over profitability, longevity over short-term gains.

Company has a low return on equity of 13.6% over last 3 years. While this might seem unimpressive compared to private sector financiers, it reflects IRFC's low-risk model. The company essentially trades returns for stability, accepting lower ROE in exchange for zero credit losses and predictable earnings.

The dividend policy exemplifies this philosophy. IRFC consistently pays out 30-40% of profits as dividends, returning cash to the government while retaining enough for growth. This balanced approach satisfies the government's fiscal needs while ensuring IRFC's capital adequacy for future expansion.

Currency operations add complexity and opportunity. When IRFC borrows in foreign currency to take advantage of lower international rates, it enters into elaborate hedging arrangements. These might include cross-currency swaps, forward contracts, or natural hedges through foreign currency assets. The cost of hedging is passed to Railways, but IRFC retains any gains from favorable currency movements within regulatory limits.

The asset-liability matching is near-perfect. IRFC's ALM framework ensures that cash inflows from lease rentals match debt servicing obligations almost to the day. This isn't accidental; it's the result of sophisticated modeling that considers payment schedules, interest reset dates, and potential prepayments. The company maintains liquidity buffers, but these are minimal given the certainty of cash flows.

Working capital management is remarkably simple. IRFC doesn't have inventory, receivables are government-guaranteed, and payables are predictable. The company operates with negative working capital – it receives lease rentals before paying interest on borrowings. This float, though temporary, provides additional income through short-term investments.

VIII. Modern Era: Navratna Status & Future Vision (2021–Present)

In March 2025, IRFC was given the Navaratna status by the Government of India, becoming the 26th PSU in this list. This elevation to Navratna status represents more than just a bureaucratic reclassification – it's a recognition of IRFC's evolution from a single-purpose financing vehicle to a strategic infrastructure financier with national importance.

The Navratna designation brings operational autonomy that IRFC has long deserved. The company can now make capital expenditures up to ₹1,000 crores without government approval, enter joint ventures, and most importantly, diversify its business beyond railway financing. This autonomy comes at a crucial time when India's infrastructure financing needs are exploding across sectors.

Post-IPO, IRFC has undergone a subtle but significant transformation. Market Cap ₹ 1,64,598 Cr makes it one of India's largest financial institutions by market value. The public listing has brought scrutiny but also credibility. International investors who previously ignored IRFC are now taking notice, particularly as India's infrastructure story gains global attention.

The expansion beyond traditional railway financing is already underway. Beyond railway financing, IRFC is expanding into power generation, mining, fuel, telecom, and warehousing. The company has begun financing renewable energy projects, logistics parks, and even considering metro rail systems. This diversification isn't abandoning the core railway business but leveraging IRFC's expertise in infrastructure financing for adjacent sectors.

Green financing has emerged as a major growth avenue. IRFC issued its first green bonds to finance electric locomotives and railway electrification projects. These bonds, attracting ESG-focused investors, often price better than conventional bonds. The company is positioning itself as a green infrastructure financier, aligning with India's carbon neutrality goals.

The technology transformation, long overdue, is finally happening. IRFC is implementing artificial intelligence for risk assessment, blockchain for lease documentation, and advanced analytics for portfolio optimization. The company that operated with paper files for decades is leapfrogging to cutting-edge financial technology.

Competition concerns are real but manageable. The National High-Speed Rail Corporation is developing its own financing mechanisms for bullet train projects. Private train operators, though limited, might seek alternative financing. Other infrastructure finance companies are eyeing railway opportunities. But IRFC's moat – decades of expertise, government backing, and established relationships – remains formidable.

International aspirations are taking shape. IRFC is exploring opportunities to finance railway projects in neighboring countries, particularly where Indian companies are involved in construction. The Bangladesh railway modernization, Sri Lankan railway rehabilitation, and potential projects in Africa represent new frontiers. The expertise in financing public transportation infrastructure in emerging markets is globally rare and valuable.

The Vande Bharat revolution presents both opportunity and challenge. These indigenous semi-high-speed trains require sophisticated financing given their higher costs and specialized maintenance needs. IRFC is developing new lease structures specifically for these trains, potentially including maintenance and performance-based components.

Station redevelopment and commercial exploitation offer another growth vector. As Indian Railways modernizes stations into commercial hubs, IRFC is structuring innovative financing solutions that capture value from both transportation and real estate development. This hybrid financing model could become a template for urban infrastructure development.

Recent developments have been particularly noteworthy. It has secured funding for 20 BOBR rakes for NTPC worth Rs. 700 crore (US$ 8.1 million) and was the lowest bidder to finance a Rs. 3,190 crore (US$ 36.7 million) loan for Patratu Vidyut Utpadan Nigam Limited (PVUNL), a subsidiary of NTPC. Additionally, NTPC Renewable Energy Limited (NTPC REL) has accepted IRFC's bid for a Rs. 7,500 crore (US$ 86.3 million) Rupee Term Loan (RTL).

The renewable energy financing push is particularly strategic. As India commits to massive renewable capacity addition, IRFC is positioning itself as a financing partner for solar parks, wind farms, and green hydrogen projects. The company's low cost of capital and infrastructure expertise make it an attractive funding source for renewable developers.

Digital initiatives are transforming stakeholder engagement. IRFC has launched digital platforms for bond subscriptions, automated lease management systems, and real-time financial reporting. The company is also exploring digital bonds and tokenization of lease receivables, potentially revolutionizing infrastructure financing.

The retail investor engagement has intensified post-listing. IRFC regularly conducts investor education programs, publishes detailed FAQs, and maintains active social media presence. The company recognizes that retail shareholders, while holding minority stakes, provide market stability and political capital.

Risk management frameworks are evolving to match new realities. Climate risk assessment for long-term infrastructure assets, cyber security for digital operations, and ESG compliance for international funding are now integral to IRFC's risk architecture. The company is transitioning from a traditional risk management approach to a comprehensive enterprise risk framework.

IX. Power Dynamics & Stakeholder Analysis

The relationship between IRFC and the Ministry of Railways is fascinatingly complex. On paper, Railways is IRFC's sole major customer. In reality, it's also the owner (through the government), regulator (through operational control), and strategic partner. This multi-dimensional relationship creates unique dynamics that define IRFC's operational reality.

Since IRFC is wholly-owned and controlled by the Government of India (GoI), it is susceptible to changes to its policies. This vulnerability isn't theoretical. When the government decides to prioritize certain types of rolling stock, IRFC must arrange financing regardless of market conditions. When political pressures demand lower lease rates, IRFC's margins compress. The company operates in a space where commercial logic often yields to political imperatives.

Yet this government dependency is also IRFC's greatest strength. The sovereign guarantee that backs every lease payment is absolute. During the 2020 pandemic when railway revenues collapsed, IRFC's lease payments continued uninterrupted because they're budgeted government expenditure, as sacred as defense spending. This paradox – vulnerability and invincibility stemming from the same source – defines IRFC's existence.

The political economy surrounding IRFC is intricate. Railway budgets, once presented separately, are now part of the general budget, making railway investments compete directly with other government priorities. Every basis point in IRFC's margin becomes a political decision. Too high, and there's accusation of profiteering from public service. Too low, and IRFC can't raise competitive capital from markets.

The retail investor phenomenon has added a new stakeholder dynamic. With over 13% public shareholding, IRFC now has lakhs of small shareholders who view the company differently than the government does. These investors want dividend growth, stock appreciation, and business expansion – goals that sometimes conflict with the government's vision of IRFC as a low-cost railway financier.

The "people's stock" narrative is powerful. IRFC has become a symbol of inclusive growth, where ordinary Indians can participate in nation-building while earning returns. This emotional connection transcends financial metrics. Retail investors defend IRFC on social media, attend AGMs in large numbers, and create political pressure for favorable treatment. The government must now balance fiscal objectives with minority shareholder interests.

Credit rating agencies occupy a crucial position in IRFC's ecosystem. The company's AAA rating isn't just a score; it's the foundation of the entire business model. This rating, based largely on government backing rather than standalone credit strength, enables IRFC to borrow at near-sovereign rates. Any downgrade would cascade through higher borrowing costs, compressed margins, and reduced competitiveness.

The sovereign ceiling concept is particularly relevant. IRFC's rating cannot exceed India's sovereign rating, regardless of its financial strength. When international agencies downgrade India's outlook, IRFC suffers collaterally. This linkage means IRFC's fate is tied not just to railway economics but to India's macroeconomic trajectory.

International lenders view IRFC through a unique lens. For Japanese institutions offering concessional loans, IRFC represents India's infrastructure commitment. For global bond investors, it's a sovereign proxy with marginally higher yields. For development finance institutions, it's a vehicle for supporting sustainable transportation. Each perspective shapes funding availability and terms.

The regulatory oversight structure is multi-layered. RBI regulates IRFC as an NBFC-IFC, SEBI oversees it as a listed company, and the Railway Ministry controls it as a PSU. This triple regulation creates compliance complexity but also provides checks and balances. Each regulator's priorities – financial stability, market integrity, and public service – must be balanced.

Employee dynamics are unique. IRFC's small team wields enormous financial power but operates within government pay scales and promotion structures. This creates retention challenges as private sector opportunities beckon. Yet many stay, driven by the unique opportunity to impact national infrastructure while enjoying public sector stability.

The vendor ecosystem, though limited, is critical. Investment banks competing to manage IRFC's bond issues, law firms structuring lease agreements, and auditors certifying accounts all play vital roles. These relationships, often decades old, operate on trust and reputation rather than just commercial terms.

Political transitions impact IRFC subtly but significantly. New railway ministers bring different priorities – some favor passenger amenities, others freight capacity, yet others technology upgradation. IRFC must adapt its financing strategies to align with changing political visions while maintaining operational continuity.

State governments increasingly influence IRFC's operations as railways expand into new territories. Land acquisition, local employment, and regional development demands create stakeholder complexity that IRFC must navigate despite being a purely financial entity.

The media narrative around IRFC has evolved dramatically. Once ignored, the company now features regularly in business media. Every quarterly result, major bond issue, or lease agreement makes headlines. This visibility brings scrutiny but also recognition of IRFC's national importance.

Labor unions, though IRFC has minimal direct employment, influence operations through railway sector dynamics. When railway unions demand benefits, the cost implications affect lease economics. IRFC must factor these indirect labor dynamics into long-term financial planning.

X. Bear vs. Bull Case & Valuation

The Bull Case: Infrastructure Supercycle Catalyst

The optimistic thesis for IRFC rests on India's unprecedented infrastructure ambition. The government has committed ₹15 lakh crores for railway infrastructure over the next decade. If IRFC maintains its historical share of railway financing, we're looking at financing opportunities exceeding ₹7 lakh crores. This isn't speculative; it's based on announced projects, approved budgets, and signed agreements.

The monopoly position remains unassailable. No other institution combines IRFC's low funding costs, operational expertise, and government backing. Private players can't compete on pricing, foreign lenders can't navigate the bureaucracy, and other PSUs lack specialization. This moat isn't narrowing; it's widening as infrastructure complexity increases.

Market Cap ₹ 1,64,598 Cr seems modest when compared to the asset base and growth potential. Trading at just 3 times book value for a company with zero NPAs and sovereign backing appears to be a valuation anomaly that markets will eventually correct.

Green financing represents a massive opportunity. As India commits to net-zero emissions, railway electrification becomes critical. IRFC is perfectly positioned to finance this transition, potentially accessing cheaper green funding from international markets while earning fees for structuring and managing these specialized instruments.

The expansion beyond railways multiplies the addressable market. Metro systems, logistics parks, renewable energy projects – each represents billions in financing opportunities. IRFC's infrastructure expertise and low cost of capital make it a natural financing partner across sectors.

Navratna autonomy unlocks value. Freedom to enter joint ventures, make strategic investments, and diversify operations without government approval accelerates decision-making and enables opportunistic value creation previously impossible under bureaucratic constraints.

The Bear Case: Structural Limitations

The pessimistic view focuses on fundamental constraints that limit IRFC's growth potential. Company has low interest coverage ratio. Company has a low return on equity of 13.6% over last 3 years. These metrics reflect not temporary challenges but structural realities of IRFC's business model.

Government dependency is a double-edged sword. Policy changes, budget constraints, or political priorities can dramatically impact IRFC's operations. The company has virtually no control over its primary revenue source, making it vulnerable to political volatility.

Competition is emerging from unexpected quarters. The National High-Speed Rail Corporation is developing independent financing mechanisms. State governments are creating their own infrastructure financing vehicles. Private participation in railways, though limited, introduces alternative financing models. IRFC's monopoly, while strong, isn't guaranteed perpetually.

Interest rate sensitivity poses significant risks. IRFC operates on thin margins that assume a stable or declining rate environment. Rising rates compress spreads, potentially making the business model unviable. The company's long-duration assets and shorter-duration liabilities create potential mismatches during rate cycles.

The limited growth beyond railways thesis suggests that IRFC's expansion into other sectors will face challenges. Different sectors require different expertise, risk assessment frameworks, and operational capabilities. IRFC's railway-centric DNA might not translate successfully to diverse infrastructure financing.

Technology disruption could challenge traditional financing models. Blockchain-based infrastructure bonds, crowd-funded projects, or direct government digital issuances could bypass intermediaries like IRFC. The company's technology adoption, while improving, lags fintech innovation significantly.

Valuation Perspectives

Current trading multiples present a complex picture. The P/E ratio has expanded from single digits at IPO to 25.58, suggesting markets are pricing in significant growth. But compared to private sector financiers, IRFC still trades at a discount despite superior asset quality.

The dividend yield of approximately 1.5% seems modest but reflects retention for growth capital. If IRFC increases payout ratios post-expansion phase, the yield could improve significantly, attracting income-focused investors.

Book value multiple of 3x appears reasonable given ROE trends. If IRFC improves returns through diversification and margin expansion, the multiple could expand. Conversely, margin compression or increased competition could trigger multiple contraction.

The sum-of-parts valuation reveals hidden value. The existing railway lease portfolio, valued at contracted cash flows, is worth approximately current market cap. Future business, expansion opportunities, and strategic value aren't fully reflected in current pricing.

Comparative valuation with global infrastructure financiers suggests upside. Similar entities in developed markets trade at higher multiples despite lower growth prospects. As Indian markets mature and IRFC gains international recognition, valuation gaps should narrow.

XI. Playbook: Lessons for Founders & Investors

The IRFC story offers profound lessons for anyone building or investing in infrastructure financing businesses. Here's the playbook distilled from nearly four decades of IRFC's journey.

Building a Financing Business with a Single Customer

Conventional wisdom says customer concentration is deadly. IRFC proves otherwise – if that customer is a sovereign entity with unlimited demand and guaranteed payments. The lesson isn't to seek single customers, but to understand that concentration risk depends entirely on customer quality. A thousand small, risky customers might be worse than one rock-solid anchor client.

The key is structuring the relationship to be mutually dependent. Indian Railways needs IRFC as much as IRFC needs Railways. This symbiosis, carefully cultivated over decades, creates stability that diversification might not provide. Founders should consider whether depth with few clients might trump breadth with many.

The Power of Government Partnerships Done Right

IRFC demonstrates that government partnerships can be tremendously valuable if structured correctly. The company maintains operational independence while leveraging government backing. It operates with market efficiency while serving public purposes. This balance – neither fully government nor fully private – creates a unique value proposition.

The lesson for founders: don't dismiss government partnerships as bureaucratic nightmares. Properly structured, they can provide unmatched stability, credibility, and scale. The key is maintaining professional management, transparent operations, and clear boundaries between public service and commercial objectives.

Capital Efficiency vs. Operational Complexity

IRFC chose capital efficiency over operational complexity. Instead of building elaborate infrastructure, hiring thousands, and creating complex operations, it focused on financial engineering with minimal overhead. This choice – often counter-intuitive in infrastructure sectors – enabled extraordinary returns on capital.

The insight for investors: look for businesses that achieve scale through capital rather than operations. These models, while perhaps less exciting, often generate superior risk-adjusted returns. The boring business of moving money efficiently can be more profitable than the exciting business of building and operating assets.

Why Boring Businesses Can Be Beautiful

IRFC is fundamentally boring. It does the same thing repeatedly – borrow, buy, lease. No technological disruption, no market excitement, no viral growth. Yet this boring predictability is precisely what makes it valuable. Investors can model cash flows decades out with reasonable confidence.

For founders, the lesson is that building a boring, predictable business in a critical sector can be more valuable than creating the next unicorn. Infrastructure financing, utilities, essential services – these unglamorous sectors offer opportunities for building enduring value without the volatility of consumer technology or trendy sectors.

The Infrastructure Financing Template for Emerging Markets

IRFC provides a replicable template for infrastructure financing in emerging markets. The model – government-backed SPV accessing capital markets to finance public infrastructure through lease mechanisms – can work for power, ports, airports, or urban infrastructure. The key elements are: sovereign backing, dedicated purpose, operational efficiency, and market discipline.

Investors evaluating emerging market infrastructure opportunities should look for IRFC-like characteristics: government support without government inefficiency, market access without market risk, scale without complexity. These hybrid models often offer the best risk-reward profiles in developing economies.

When to IPO: Market Timing vs. Institutional Readiness

IRFC's IPO timing seemed terrible – pandemic, market volatility, investor skepticism. Yet the company was institutionally ready: systems robust, governance strong, disclosure standards high. The lesson: institutional readiness matters more than perfect market timing. Markets are cyclical, but institutional strength is permanent.

The post-IPO journey also teaches patience. Initial listing disappointment gave way to eventual recognition. Founders and investors should evaluate IPOs not on listing day performance but on long-term value creation potential. Sometimes, the best opportunities come from IPOs that initially disappoint.

The Ecosystem Play

IRFC didn't just finance railways; it became the ecosystem's backbone. By financing not just the ministry but also related entities like RVNL and RailTel, IRFC embedded itself irreplaceably in the sector's fabric. This ecosystem approach creates multiple touchpoints, diverse revenue streams, and strategic importance beyond any single relationship.

Managing Stakeholder Complexity

With government as owner, railways as customer, markets as funding source, and now public shareholders, IRFC navigates extreme stakeholder complexity. The playbook: radical transparency, consistent communication, and clear prioritization when interests conflict. Not everyone can be satisfied always, but everyone must be heard and understood.

The Talent Paradox

IRFC proves you don't need thousands of employees to manage billions in assets. But the employees you do have must be exceptional. The company's ability to attract and retain talent despite government pay scales shows that purpose, impact, and stability can compete with private sector compensation. The lesson: in specialized finance, a small team of experts beats an army of generalists.

XII. Epilogue: The Future of Railway Finance

As we look toward the horizon, IRFC stands at an inflection point. India's infrastructure ambitions are massive – the government speaks of a $1.5 trillion infrastructure investment over the next decade. Railways will need unprecedented capital for high-speed rail, dedicated freight corridors, station modernization, and fleet upgradation. The question isn't whether IRFC will play a role, but how dominant that role will be.

The high-speed rail challenge is particularly intriguing. Bullet trains require financing at a scale and complexity that even IRFC hasn't encountered. These projects involve international collaboration, technology transfer, and financial structures that blend commercial and strategic objectives. IRFC's ability to adapt its traditional model to these new realities will determine its relevance in India's high-speed future.

Climate finance represents both opportunity and obligation. As the world pivots toward sustainable transportation, railways become even more critical. IRFC is uniquely positioned to channel global climate funds into Indian railway infrastructure. The company could become a gateway for international green finance seeking exposure to emerging market sustainable infrastructure.

The privatization question looms large. If Indian Railways allows private train operators, how does IRFC fit into a multi-operator ecosystem? Can it finance private operators? Should it? These questions challenge IRFC's fundamental model but also offer opportunities for reinvention. The company might evolve from a railway financier to a transport infrastructure financier, supporting everything from metros to hyperloops.

With India's push towards becoming a US$ 10 trillion economy under Amrit Kaal, IRFC is set to play a crucial role in mobilizing resources for infrastructure modernization and growth. This isn't just corporate optimism; it's mathematical inevitability. A $10 trillion economy needs infrastructure investment of at least $2-3 trillion. Transportation infrastructure alone could require $500 billion. IRFC, with its expertise and track record, will inevitably capture a significant share.

The technology transformation will accelerate. Blockchain-based lease documentation, AI-driven risk assessment, and digital bond issuances are no longer futuristic concepts but near-term realities. IRFC's ability to embrace these technologies while maintaining operational stability will determine its competitive position.

International expansion seems inevitable. As Indian companies build infrastructure globally, they need financing partners who understand emerging market realities. IRFC's expertise in financing public infrastructure in challenging environments is globally rare and valuable. The company could become India's infrastructure financing ambassador, supporting projects from Africa to Southeast Asia.

The retail investor relationship will deepen. As financial literacy improves and retail participation in capital markets grows, IRFC could become a gateway stock for millions of Indians. The company's stability, dividend reliability, and nation-building narrative resonate with retail investors seeking more than just returns.

But perhaps the most profound question is existential: Will IRFC remain relevant in a rapidly changing world? As financing models evolve, technologies disrupt, and infrastructure needs transform, can a company born in 1986 adapt to 2050 realities?

The answer likely lies in IRFC's fundamental value proposition. As long as India needs infrastructure, infrastructure needs financing, and financing needs expertise, IRFC has a role. The company's journey from a small experiment in extra-budgetary resources to a Navratna PSU managing lakhs of crores proves that well-designed institutions can evolve with changing times.

IRFC's story is ultimately India's story – of ambition exceeding resources, of innovation born from constraint, of building world-class capabilities despite limitations. It's a story of how financial engineering can serve national development, how public sector enterprises can achieve private sector efficiency, and how boring businesses can create extraordinary value.

As India accelerates toward developed nation status, IRFC will be there, quietly financing the rails that carry the nation forward. Not in the spotlight, not seeking glory, but essential nonetheless. In the end, that might be IRFC's greatest achievement – becoming so integral to India's infrastructure that its absence would be unthinkable.

The rails that IRFC finances don't just carry trains; they carry dreams, aspirations, and the promise of a connected, prosperous India. And as long as those rails need to be laid, IRFC will be there to finance them, one lease at a time, one train at a time, building the nation's future on tracks of financial steel.

XIII. Recent News

- Market Cap: 1,66,297 Crore (down -29.7% in 1 year)

- Stock performance showing volatility with 52-week range between ₹108.04 and ₹189.45

- Highest-ever quarterly profit for the first quarter of FY26, with a Profit After Tax (PAT) of ₹1,745.69 crore, marking a 10.71% year-on-year growth. The company's revenue from operations rose to ₹6,915.38 crore

- Expansion into renewable energy sector with major NTPC loan agreements worth thousands of crores

- Improved debt-equity ratio to 7.44x from 8.02x, showing enhanced balance sheet strength

- Maintaining zero NPA status, reinforcing its position as one of the safest NBFCs in India

- Active exploration of metro rail and multimodal logistics park financing opportunities

XIV. Links & Resources

- Official IRFC website: irfc.co.in

- SEBI filings and disclosures

- Ministry of Railways annual reports and budget documents

- RBI NBFC regulations and circulars

- NSE and BSE listing documents and corporate announcements

- Railway infrastructure development plans and policy papers

- Comparable global railway financiers: Eurofima, Angel Trains, Porterbrook

- Infrastructure finance research from ADB, World Bank

- Indian Railway's Vision 2030 document

- National Infrastructure Pipeline reports

- Credit rating reports from CRISIL, ICRA, and CARE

- Parliamentary standing committee reports on railways

- International railway financing best practices studies

- Green bond frameworks and climate finance guidelines

Recent News (Updated through September 2025)

Financial Performance Highlights

IRFC delivered its strongest-ever quarterly performance in Q1 FY2025-26, reporting a 10.7% year-on-year (YoY) rise in net profit to ₹1,745.7 crore, up from ₹1,576.8 crore. Revenue also edged up 2.2% YoY to ₹6,918.2 crore, making it the highest-ever total income reported for a quarter by the company. The company's net interest margin improved to 1.53% (annualized), the best in three years, while its net worth climbed to ₹54,423.9 crore — the highest since inception.

Market Performance and Valuation

Mkt Cap: 1,54,352 Crore (down -33.9% in 1 year) reflects the broader correction in PSU stocks despite strong operational performance. The stock has shown significant volatility with 52-week high share price is Rs 184.00 and 52-week low share price is Rs 108.05. Currently Stock is trading at 2.84 times its book value, suggesting reasonable valuation levels for long-term investors.

Operational Achievements

This marks the first full quarter since IRFC received 'Navratna' status from the Government of India, giving it greater operational freedom. The enhanced autonomy is already showing results in business diversification and operational efficiency improvements.

Strategic Expansion and New Business

IRFC has executed a refinancing facility of up to Rs 1,125 crore for Bhartiya Rail Bijlee Company (BRBCL), a joint venture of NTPC (74%) and Ministry of Railways (26%). The refinancing support extended by IRFC will help reduce BRBCL's financing costs, thereby strengthening its financial position while also lowering the cost of electricity supplied to Indian Railways. This creates a win-win outcome - improving BRBCL's bottom line and directly benefiting the Ministry of Railways both as an equity holder and as the ultimate customer.

IRFC sanctioned ₹199.70 crore term loan to SITCO for Surat MMTH; signed 19 Aug 2025. This marks IRFC's expanding footprint in multimodal transportation infrastructure financing.

Financial Health Indicators

IRFC's debt-to-equity ratio showed improvement in the first quarter, declining to 8.08% from 8.38% in the previous quarter (Q4 FY24) and 8.87% in the corresponding quarter last year (Q1 FY24). This improvement in leverage ratios demonstrates prudent balance sheet management despite aggressive growth.

Corporate Governance Note

IRFC fined Rs.10,77,340 by BSE and NSE for board/compliance lapses; waiver requested, dated 30 Aug 2025. While minor in nature, this highlights the increased scrutiny that comes with being a listed entity and the importance of maintaining high governance standards.

Management Commentary

Chairman and Managing Director Manoj Kumar Dubey attributed the performance to sound strategy, saying, "Our financial strength mirrors the transformation of Indian Railways. We're committed to delivering efficiency and innovation."

Future Outlook

IRFC is increasingly looking beyond its traditional lending role, aiming to support the entire railway ecosystem through strategic partnerships and project linkages. With stable cash flows and a low cost of capital, the company is positioning itself as a key player in India's infrastructure push. As IRFC enters its "2.0" phase, all signs point to continued momentum and deeper integration with the country's fast-evolving railway sector.

Final Thoughts: The Invisible Giant's Visible Future

As we conclude this deep dive into IRFC, what emerges is a portrait of an institution that has mastered the art of being simultaneously essential and overlooked. For nearly four decades, IRFC has operated in the shadows of Indian Railways, content to be the financial plumbing that keeps the trains running. But as India stands at the cusp of an infrastructure revolution, IRFC's role is evolving from backstage financier to strategic enabler.

The company's journey from a ₹100 crore experiment in 1986 to a ₹5 lakh crore financing powerhouse today isn't just a story of numerical growth. It's a masterclass in institutional design, where the right structure, governance, and incentives created a self-sustaining ecosystem. IRFC proves that public sector enterprises, when designed with market discipline and operational autonomy, can achieve private sector efficiency while serving public purposes.

The investment thesis for IRFC ultimately boils down to a simple question: Do you believe in India's infrastructure story? If India is to become a $10 trillion economy, it needs world-class infrastructure. If it needs world-class infrastructure, it needs massive financing. And if it needs massive financing for public infrastructure, IRFC will inevitably play a central role. The company's monopolistic position, sovereign backing, and decades of expertise create a moat that's virtually unassailable.

Yet, the risks are real and shouldn't be ignored. Government dependency creates political risk. Interest rate cycles can compress margins. Technology disruption could challenge traditional financing models. Competition, while limited today, could emerge from unexpected quarters. These aren't reasons to dismiss IRFC, but they're important considerations for any investment decision.

What makes IRFC particularly fascinating is how it challenges conventional financial wisdom. It's a financial institution that has never had a bad loan. It's a monopoly that doesn't abuse its pricing power. It's a government company that operates with private sector efficiency. It's a boring business that has delivered exciting returns. These paradoxes aren't contradictions; they're features of a unique business model that has evolved to serve a specific national need.

For founders and entrepreneurs, IRFC offers valuable lessons. Sometimes the best businesses aren't the most innovative or disruptive, but those that solve fundamental problems with elegant simplicity. The 30-year lease model isn't technologically sophisticated, but it's brilliantly designed for its purpose. The company's lean structure isn't forced minimalism but deliberate efficiency. These design choices, made decades ago, continue to drive value today.

For investors, IRFC represents a unique proposition in the Indian market. It offers infrastructure exposure without construction risk, government backing without bureaucratic inefficiency, and steady growth without dramatic volatility. It's not a stock for momentum traders or those seeking quick gains. It's an investment for those who understand that nation-building is a long-term process and are willing to participate in that journey.

The transformation currently underway – from railway financier to infrastructure financier, from domestic player to potential international player, from government-controlled to Navratna-autonomous – suggests that IRFC's best days might still be ahead. The company that has already transformed Indian railway financing might now transform infrastructure financing more broadly.

As India accelerates its infrastructure buildout, as railways evolve from transportation provider to economic enabler, as green financing becomes not just preferable but mandatory, IRFC stands at the intersection of these megatrends. It's not the most exciting company in India, but it might be one of the most important.

The story of IRFC is ultimately a story of patient capital serving patient nation-building. In a world obsessed with disruption and rapid change, IRFC reminds us that some transformations happen slowly, steadily, and sustainably. The rails that IRFC finances don't just connect cities; they connect India's past to its future, its aspirations to its achievements.

For four decades, IRFC has been the silent partner in India's railway journey. As it enters its fifth decade, armed with Navratna status, public market credibility, and expanding mandate, it's ready to be a more visible participant in India's infrastructure story. The company that owns 75% of India's trains without operating a single one might soon finance much more than just railways.

In the end, IRFC's greatest achievement might be making the extraordinary seem ordinary. Financing infrastructure at the scale of a subcontinent, managing assets worth lakhs of crores with a handful of employees, maintaining zero NPAs for decades – these aren't normal achievements. Yet IRFC has normalized them through consistent execution and institutional excellence.

As we look toward India's infrastructure future – high-speed rails, freight corridors, multimodal logistics, green transportation – one thing seems certain: wherever India's infrastructure ambitions lead, IRFC will be there to finance them. Not in the spotlight, not seeking glory, but essential nonetheless. Just as it has always been.

The rails that bind India together aren't just made of steel; they're made of financial engineering, patient capital, and institutional excellence. And as long as India needs to move forward, IRFC will be there to finance the journey, one lease at a time, one train at a time, building the tracks to tomorrow on foundations of financial steel.

[Note: This analysis is for educational purposes only and should not be considered as investment advice. Readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.]

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube