Power Finance Corporation: India's Power Sector Backbone

I. Introduction & Episode Roadmap

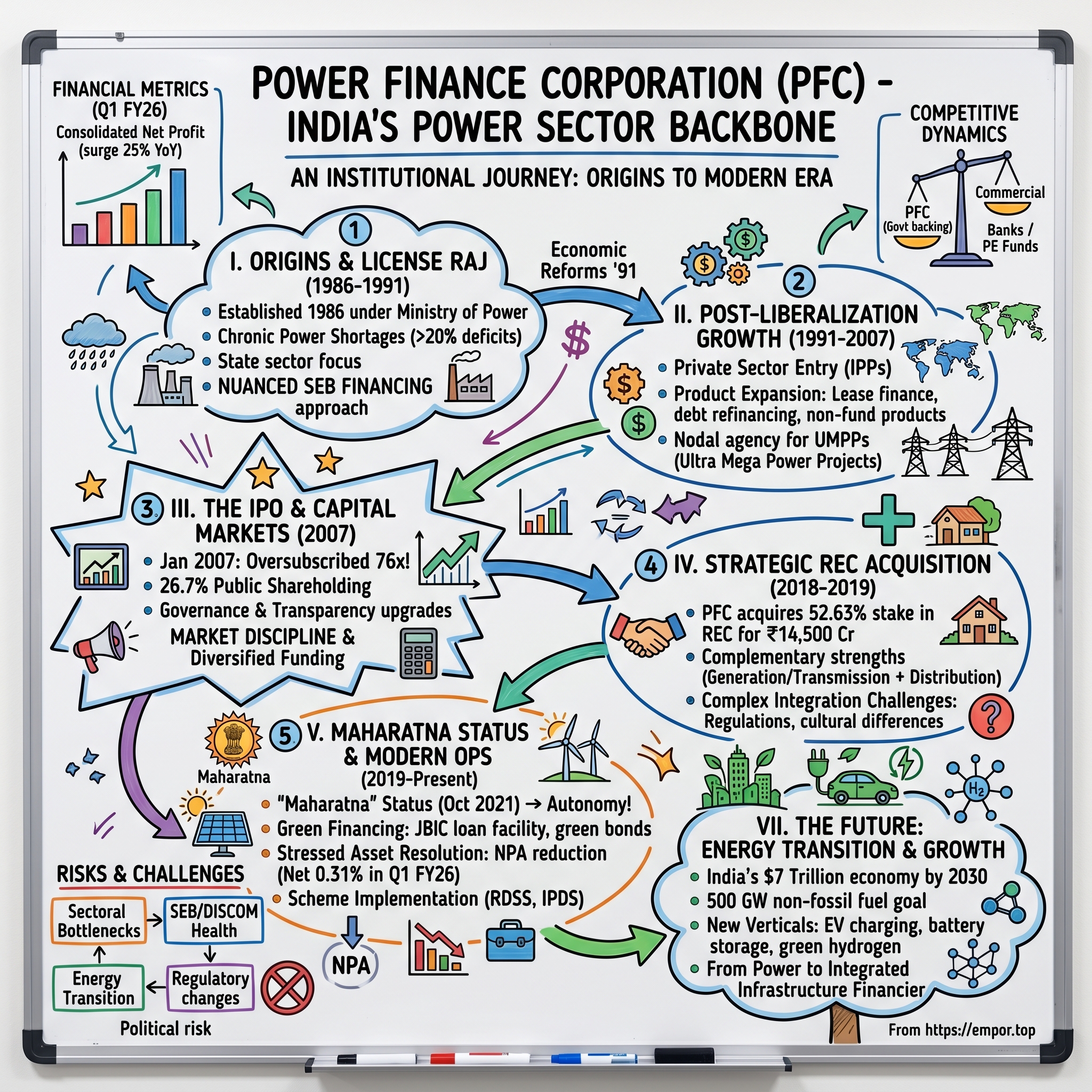

Power Finance Corporation stands as one of India's most critical yet underappreciated financial institutions, a government-owned giant that has quietly powered the nation's electrification journey for nearly four decades. Established in 1986 under the Ministry of Power, PFC achieved the prestigious "Maharatna" status in October 2021, joining an elite club of just twelve central public sector enterprises granted maximum operational and financial autonomy by the government.

As a Systemically Important Non-Deposit taking Non-Banking Financial Company (SI-ND-NBFC) registered with the Reserve Bank of India as an Infrastructure Finance Company, PFC operates at the intersection of finance and infrastructure development. The company extends financial assistance across the entire power sector value chain—from generation to transmission and distribution—serving Central sector power utilities, State Electricity Boards, private sector companies, and increasingly, renewable energy developers.

The question that drives our exploration today is compelling: How did a government-owned NBFC, born in the twilight years of India's socialist economy, transform into the financial backbone of the world's third-largest electricity system? It's a story that mirrors India's own economic transformation—from state control to liberalization, from chronic power shortages to energy surplus, from coal dominance to renewable energy transition.

The numbers tell a remarkable story of scale: Market cap of ₹1,34,877 Crore, Revenue of ₹1,10,324 Cr, and Profit of ₹32,314 Cr. Yet behind these figures lies a more nuanced narrative of institutional evolution, policy implementation, and the delicate balance between commercial operations and developmental mandate.

Our journey through PFC's history will traverse multiple epochs of Indian economic development. We'll explore the company's origins during the License Raj era when chronic power shortages threatened agricultural productivity and industrial growth. We'll examine how economic liberalization in 1991 fundamentally altered PFC's role, expanding its mandate from financing state utilities to supporting private power producers. The 2007 IPO marked a watershed moment, transforming PFC from a wholly government-owned entity to a listed company accountable to public shareholders.

The strategic acquisition of Rural Electrification Corporation in 2019 represents perhaps the most ambitious move in PFC's history, with the government approving the takeover on December 6, 2018, and the acquisition completing on March 28, 2019, with PFC acquiring the government's 52.63% stake in REC. This ₹14,500 crore deal created India's largest power financing entity but also raised complex questions about market concentration and operational integration that continue to shape the company's trajectory.

Today, PFC stands at a fascinating inflection point. The company must navigate India's energy transition while managing legacy thermal assets, support renewable energy expansion while maintaining financial prudence, and balance its developmental role with shareholder returns. With approximately 550 employees managing a loan book exceeding ₹11 lakh crore, PFC exemplifies the leverage and efficiency possible in specialized infrastructure financing.

II. Origins & The License Raj Era (1986–1991)

The mid-1980s painted a grim picture of India's power sector. Chronic electricity shortages plagued the nation, with peak deficits routinely exceeding 20 percent. State Electricity Boards, the monopolistic utilities responsible for power generation and distribution, teetered on the brink of financial collapse. Industrial production suffered frequent disruptions, agricultural pump sets remained unenergized, and vast swathes of rural India lived in darkness. The monsoon failures of the early 1980s had exposed the critical link between electricity access and agricultural productivity, making power sector development a national priority.

Into this crisis stepped the Government of India with a bold institutional innovation. In July 1986, Power Finance Corporation was established as a wholly government-owned financial institution under the administrative control of the Ministry of Power. Unlike commercial banks that viewed power projects as risky long-gestation investments, PFC was conceived as a specialized development finance institution with deep sectoral expertise and patient capital.

The initial mandate was deliberately narrow but critically important: provide financial assistance to State Electricity Boards and state sector power utilities for generation, transmission, and distribution projects. This focus reflected the reality of India's controlled economy where the state monopolized the power sector. Private participation was virtually non-existent, foreign investment prohibited, and market mechanisms subordinated to central planning.

PFC's early operations were shaped by the peculiar dynamics of the License Raj era. Every power project required multiple clearances from various ministries, environmental approvals were nascent, and land acquisition proceeded under colonial-era laws. Interest rates were administered rather than market-determined, and credit allocation followed government priorities rather than commercial logic. In this environment, PFC functioned less as a commercial lender and more as a financial arm of the government's power development policy.

The institution's founding leadership understood that building credibility required more than just disbursing government funds. They invested heavily in developing project appraisal capabilities, creating standardized lending norms, and establishing monitoring mechanisms for funded projects. Engineers and financial analysts were recruited from premier institutions, training programs initiated with international development agencies, and systematic documentation processes established.

A critical early innovation was PFC's approach to State Electricity Board financing. Unlike commercial banks that evaluated SEBs based on conventional financial metrics—most would have failed any prudent credit assessment—PFC developed a nuanced understanding of the political economy of state utilities. They recognized that while SEBs might be commercially unviable, they enjoyed implicit state government guarantees and played essential developmental roles. This insight allowed PFC to continue lending even as SEB finances deteriorated, maintaining power sector investments during a critical period.

The relationship with the Ministry of Power proved both enabling and constraining. On one hand, ministerial backing ensured PFC's loans carried quasi-sovereign comfort, facilitating resource mobilization from domestic financial institutions. The company became the nodal agency for implementing various government schemes, from rural electrification programs to system improvement initiatives. On the other hand, lending decisions often reflected political priorities rather than commercial merit, and recovery mechanisms remained weak given the sovereign nature of borrowers.

By 1991, PFC had established itself as the undisputed leader in power sector financing, with a loan portfolio approaching ₹5,000 crore. The institution had funded major thermal and hydro projects across states, supported transmission line construction, and financed distribution network expansion. More importantly, it had developed invaluable institutional knowledge about India's complex power sector—understanding of fuel linkages, appreciation of regional grid dynamics, and relationships with state utilities that would prove crucial in the liberalized era ahead.

The controlled economy environment also shaped PFC's organizational culture in profound ways. Decision-making was hierarchical, following government protocols and procedures. Risk assessment focused more on policy alignment than commercial viability. The compensation structure mirrored government pay scales, attracting professionals motivated by nation-building rather than financial rewards. This public sector ethos—emphasizing developmental impact over profitability—would remain embedded in PFC's DNA even as India's economy transformed.

III. Post-Liberalization Growth & Expansion (1991–2007)

The economic reforms of 1991 fundamentally transformed India's power sector landscape, and with it, Power Finance Corporation's role and operations. The dismantling of the License Raj, opening up of the economy to private investment, and the Electricity Act amendments created unprecedented opportunities and challenges for PFC. The institution that had operated as a captive lender to state utilities suddenly found itself navigating a complex multi-stakeholder environment with private developers, independent power producers, and international investors.

The most significant change was the entry of private sector players into power generation. The government's policy to encourage Independent Power Producers (IPPs) meant PFC had to develop entirely new capabilities. Evaluating private sector projects required sophisticated financial modeling, understanding of power purchase agreements, assessment of fuel supply arrangements, and analysis of sponsor creditworthiness. The infamous Enron-Dabhol controversy of the mid-1990s underscored the risks of private power development, making rigorous due diligence essential.

PFC responded by dramatically expanding its product portfolio. Beyond traditional project term loans, the company introduced lease financing for equipment purchases, allowing utilities and private developers to optimize their capital structure. Short and medium-term loans to equipment manufacturers addressed working capital needs in the power equipment ecosystem. The innovation of debt refinancing products helped operational projects optimize their cost of capital as interest rates declined through the decade. Deferred payment guarantees and letters of comfort enabled equipment suppliers to offer competitive terms to power developers.

The institutional transformation required to support this expanded mandate was remarkable. From a staff of barely 200 in 1991, PFC grew to approximately 550 employees by 2007. New departments were created for private sector lending, structured finance, and risk management. Professionals with private sector experience were recruited, bringing expertise in project finance, derivative products, and international banking practices. Training programs with multilateral institutions like the World Bank and Asian Development Bank exposed PFC staff to global best practices in infrastructure financing.

A defining moment came in 2005 when PFC was designated as the nodal agency for Ultra Mega Power Projects (UMPPs), massive 4,000 MW coal-based plants developed through international competitive bidding. This role went beyond mere financing—PFC was responsible for project development, bid process management, and hand-holding successful developers through implementation. The Sasan and Krishnapatnam UMPPs demonstrated PFC's evolution from a lender to a comprehensive project development institution.

The federal structure of India's power sector created unique challenges that PFC learned to navigate skillfully. While generation was increasingly opened to private investment, transmission remained largely with state and central utilities, and distribution continued as state monopolies. This meant a private power plant's viability depended on power purchase agreements with often financially distressed state distribution companies. PFC developed innovative structures like tripartite agreements involving state governments, creating comfort for private developers while managing its own exposure.

Product innovation accelerated through this period. Recognizing that fuel security was critical for thermal power projects, PFC began financing coal mine development and fuel transportation infrastructure. The introduction of non-fund based products like performance guarantees and credit enhancement facilities helped developers optimize their balance sheets. Special schemes for renovation and modernization of aging power plants addressed efficiency improvement without requiring new capacity addition.

The company's approach to risk management evolved significantly during this period. Sectoral exposure limits were introduced to prevent over-concentration in particular states or fuel types. Asset-liability management practices were strengthened to manage interest rate and maturity risks. Credit rating mechanisms were institutionalized, with regular reviews and early warning systems. The establishment of a dedicated stressed assets management vertical reflected the growing complexity of the portfolio.

Building institutional capabilities extended beyond internal processes to ecosystem development. PFC played a crucial role in developing standardized documentation for power project financing, creating model concession agreements, and establishing industry benchmarks for construction costs and operating parameters. The company's technical standards for project appraisal became industry norms, adopted by commercial banks entering power sector lending.

The relationship with government evolved into a more arms-length arrangement while maintaining strategic alignment. Though wholly government-owned, PFC increasingly operated on commercial principles. Lending decisions were based on project viability rather than political directives. Market-based transfer pricing was introduced for government-sponsored schemes. Performance metrics shifted from merely disbursement targets to profitability, asset quality, and return ratios.

This period also witnessed PFC's growing influence in policy formulation. The company's ground-level experience in project financing provided valuable inputs for regulatory reforms. PFC executives participated in government committees on power sector restructuring, tariff rationalization, and open access implementation. The institutional knowledge accumulated over two decades made PFC an indispensable advisor to both central and state governments on power sector issues.

By 2007, PFC had transformed from a development finance institution to a sophisticated infrastructure financier. The loan book had grown to over ₹50,000 crore, with private sector exposure exceeding 30 percent. The company was profitable, well-capitalized, and ready for its next transformation—accessing public capital markets. The journey from a government department dispensing budgetary support to a commercial institution competing with private banks represented a remarkable institutional evolution, one that would be tested in the public markets ahead.

IV. The IPO & Capital Markets Entry (2007)

The decision to take Power Finance Corporation public in 2007 represented a watershed moment, not just for the company but for India's broader public sector reform agenda. The timing was propitious—India's economy was growing at over 9 percent, infrastructure investment was booming, and capital markets were witnessing unprecedented enthusiasm. The power sector, long considered a laggard, was suddenly attractive as electricity demand growth outpaced GDP expansion and massive capacity addition programs were announced.

The genesis of the IPO decision lay in multiple converging factors. PFC's capital requirements were expanding rapidly as power sector investment accelerated. The Eleventh Five Year Plan projected power sector investment needs of over ₹10 lakh crore, and PFC aimed to maintain its market share of approximately 20 percent. Accessing capital markets would diversify funding sources beyond government budgetary support and institutional borrowings. Moreover, the government's disinvestment program sought to unlock value in profitable PSUs while retaining strategic control.

The IPO preparation process, beginning in early 2006, forced PFC to undergo rigorous institutional transformation. Years of accumulated practices were scrutinized through the lens of public market expectations. Accounting policies were aligned with international standards, requiring detailed provisioning norms and mark-to-market requirements. Governance structures were strengthened with the induction of independent directors and establishment of board committees for audit, risk management, and stakeholder relations. Internal audit mechanisms were revamped, and compliance frameworks strengthened to meet listing regulations.

The roadshow for the IPO became PFC's introduction to global institutional investors. Management teams traveled across financial capitals—Mumbai, Singapore, Hong Kong, London, New York—articulating PFC's unique value proposition. The pitch was compelling: exposure to India's infrastructure growth story, quasi-sovereign comfort from government ownership, sectoral expertise accumulated over two decades, and a profitable track record with improving asset quality. International investors, seeking entry into India's power sector without direct project risks, found PFC an attractive vehicle.

January 2007 witnessed extraordinary market enthusiasm for the PFC offering. The issue, priced at ₹85-90 per share, was oversubscribed 76 times, generating bids worth over ₹2 lakh crore. Retail investors, institutional buyers, and high net worth individuals competed for allocation. The quantum of oversubscription surprised even optimistic market observers, reflecting both specific interest in PFC and broader bullishness about India's infrastructure story. The listing day saw the stock open at a significant premium, validating market confidence.

The successful IPO fundamentally altered PFC's institutional character. From a wholly government-owned entity, the company now had 26.7 percent public shareholding, including foreign institutional investors, mutual funds, and retail shareholders. This diverse shareholder base brought new expectations—quarterly earnings visibility, transparent communication, and shareholder value creation. The comfortable monopolistic position of earlier decades gave way to market scrutiny and competitive pressures.

Listing on the National Stock Exchange and Bombay Stock Exchange integrated PFC into India's capital market ecosystem. The stock's inclusion in major indices like Nifty and Sensex ensured automatic investment from passive funds. Sell-side analyst coverage proliferated, with detailed research reports dissecting PFC's business model, growth prospects, and risks. The financial media began tracking PFC's quarterly results, loan growth, and asset quality metrics with the same intensity as private sector banks.

The transformation from government ownership to partial privatization created interesting dynamics. While the government retained 73.3 percent stake, ensuring continued strategic control, public shareholders demanded commercial orientation. This dual accountability—to government for developmental objectives and to shareholders for returns—required delicate balancing. Lending decisions had to satisfy both commercial viability and policy priorities. Dividend distribution needed to meet government's fiscal needs while retaining capital for growth.

Governance improvements accelerated post-listing. Independent directors brought diverse expertise from banking, infrastructure, and regulatory domains. Board discussions became more substantive, with detailed deliberations on strategy, risk management, and capital allocation. The audit committee's oversight strengthened, with quarterly reviews of financial statements, internal audit reports, and compliance status. Stakeholder engagement expanded beyond government to include regular investor calls, analyst meets, and annual general meetings with active shareholder participation.

Access to capital markets fundamentally transformed PFC's funding strategy. Beyond the initial equity raised, the listing enabled efficient debt capital access. The company's bonds became benchmark instruments in Indian debt markets, with regular issuances across maturities. The ability to raise subordinated debt for tier-II capital strengthened the balance sheet. International bond issuances followed, with PFC's debut green bond in 2017 attracting strong investor interest. The diversified funding mix reduced dependence on any single source while optimizing cost of capital.

The market discipline imposed by listing proved beneficial for operational efficiency. Quarterly results pressure drove focus on asset quality, with systematic monitoring of early warning signals and proactive restructuring of stressed accounts. Cost consciousness increased, with operating expense ratios benchmarked against peers. Technology investments accelerated to improve productivity and customer service. Human resource practices evolved with performance-linked compensation and employee stock options.

The IPO's success had broader implications for public sector reform. PFC demonstrated that government companies could successfully access capital markets while maintaining strategic control. The model of partial privatization through minority stake sale became a template for other PSU disinvestments. The governance improvements and operational efficiencies achieved post-listing provided evidence that market discipline could enhance public sector performance without full privatization.

V. The Strategic REC Acquisition (2018–2019)

The acquisition of Rural Electrification Corporation by Power Finance Corporation in 2019 stands as one of the most significant consolidation moves in India's financial sector, creating a power financing behemoth while raising complex questions about market concentration and operational integration. The story began with the Cabinet Committee for Economic Affairs approving the strategic sale in December 2018, followed by PFC's acquisition of the government's 52.63 percent stake in REC at a cash purchase consideration of Rs 14,500 crore in March 2019.

The strategic rationale appeared compelling on paper. Both institutions operated in the same sector with complementary strengths—PFC focused on generation and transmission while REC specialized in distribution and rural electrification. Consolidation promised synergies through elimination of duplicative operations, unified lending strategies, and stronger balance sheet capacity for large-ticket infrastructure projects. The government, facing fiscal pressures and disinvestment targets, saw an opportunity to raise substantial resources while retaining indirect control through PFC.

The transaction mechanics were carefully orchestrated. PFC bought REC shares at Rs 139.50 per piece, with the entire consideration of Rs 14,500 crore transferred through RTGS mode on March 28, 2019. The funding structure relied heavily on debt, with PFC raising resources through a combination of domestic bonds, bank loans, and its first major international issuance post-acquisition—a landmark $1 billion dual-tranche bond in June 2019.

However, the acquisition's implications proved far more complex than anticipated. A major obstacle emerged as several global lenders to both PFC and REC raised alarms over the delay in merger and the structure of the combined entity. The Reserve Bank of India's regulations for NBFCs posed a particularly thorny challenge. Under existing norms, NBFCs could lend up to 25 percent of their net worth to a single borrower and 40 percent to a group. As separate entities, PFC and REC could each extend these limits to the same project, effectively providing 50 percent of project funding between them.

Post-merger, this capacity would be halved, potentially impacting the combined entity's ability to finance large power projects. PFC management argued that considering their present net worth, there was "enough cushion" to lend to the private sector, but market participants remained concerned about reduced financing flexibility. The regulatory arithmetic was unforgiving—two institutions with combined lending capacity of ₹100,000 crore to a single project would see this reduced to ₹50,000 crore post-merger.

The integration challenges extended beyond regulatory issues. Both organizations had developed distinct cultures over decades—PFC with its focus on large generation projects and private sector lending, REC with its rural distribution emphasis and government scheme implementation. Harmonizing lending policies, risk assessment frameworks, and operational procedures required delicate management. Employee concerns about role redundancy and career progression needed careful handling to prevent talent attrition.

The merger timeline proved particularly contentious. While PFC initially announced intentions to merge with REC in 2020, REC subsequently maintained that merging was no longer an option. This ambiguity created uncertainty for stakeholders, with investors unable to properly value the combined entity's prospects and borrowers uncertain about future lending capacity. The absence of a clear integration roadmap suggested that what was initially envisioned as a merger had effectively become a holding company structure.

The financial impact on PFC was substantial. The ₹14,500 crore acquisition cost, largely debt-funded, significantly increased PFC's leverage ratios. Interest costs on acquisition debt impacted profitability margins in subsequent quarters. The company's debt-to-equity ratio deteriorated, constraining future borrowing capacity. Credit rating agencies expressed concerns about asset-liability mismatches and the sustainability of dividend payments given the increased debt burden.

Market reaction reflected these concerns. While PFC's stock initially rallied on acquisition announcement, suggesting investor optimism about consolidation benefits, subsequent quarters saw volatility as integration challenges became apparent. Foreign institutional investors particularly questioned the strategic logic of two government-owned entities operating independently despite common ownership. The promised synergies of ₹500 crore annually seemed modest relative to the acquisition cost and integration risks.

The government's perspective added another layer of complexity. While the transaction helped achieve disinvestment targets and raised ₹14,500 crore for the exchequer, the government retained control of both entities—directly in PFC and indirectly in REC through PFC. This structure satisfied political objectives of maintaining public sector control over critical infrastructure financing while accessing immediate fiscal resources.

The broader implications for India's power sector were significant. The creation of a dominant power financier raised questions about competitive dynamics. Private sector banks and NBFCs found it harder to compete with the combined entity's scale and government backing. Some argued this concentration could reduce innovation and efficiency in power sector lending. Others contended that a larger, stronger institution was necessary to finance India's massive infrastructure requirements.

International precedents offered mixed lessons. Global trends showed financial sector consolidation creating institutions with greater lending capacity and operational efficiency. However, the specific challenge of merging two government-owned entities with similar mandates and overlapping portfolios was relatively unique. The absence of clear international benchmarks made it harder to assess whether the acquisition strategy would ultimately succeed.

Operational integration proceeded gradually despite merger uncertainty. Joint lending programs were initiated for large projects, leveraging combined expertise. Common technology platforms were explored to reduce operational costs. Shared training programs and knowledge exchange initiatives were launched. However, maintaining separate corporate structures, boards, and regulatory reporting limited the extent of achievable synergies.

The REC acquisition highlighted fundamental tensions in India's public sector reform approach. The transaction represented financial engineering to meet fiscal objectives rather than strategic consolidation for operational efficiency. The reluctance to fully merge despite common ownership suggested political economy constraints that prevented optimal corporate structures. The episode underscored that ownership consolidation without operational integration might satisfy immediate fiscal needs but fail to create long-term value.

VI. Maharatna Status & Modern Operations (2019–Present)

The conferment of "Maharatna" status on Power Finance Corporation on October 12, 2021, marked the culmination of its transformation from a sectoral lender to a comprehensive infrastructure financier. This prestigious designation, granted to only twelve central public sector enterprises, provided PFC with enhanced operational and financial autonomy—the ability to make investments up to ₹5,000 crore without government approval, form joint ventures, establish overseas offices, and restructure organizations independently.

The Maharatna status arrived at a pivotal moment as PFC was expanding beyond traditional power sector boundaries. The company's financing portfolio had evolved to encompass coal mine development, addressing fuel security concerns for thermal plants. Fuel transportation infrastructure, including coal handling facilities and railway sidings, became integral to ensuring operational efficiency of power projects. Oil and gas pipeline financing recognized the growing importance of gas-based power generation and city gas distribution networks. This diversification reflected understanding that infrastructure sectors were increasingly interconnected, requiring holistic financing approaches.

The green financing transformation represented perhaps the most significant strategic shift. PFC's landmark agreement with Japan Bank for International Cooperation (JBIC) in January 2025 for JPY 120 billion, marking JBIC's largest green financing deal with any Indian company, signaled serious commitment to renewable energy transition. The November 2017 Green Bond issue for US$400 million had already established PFC's credentials in sustainable finance, attracting international ESG-focused investors.

The renewable energy portfolio expansion has been remarkable, growing by 36% year-on-year in Q1 FY26, demonstrating PFC's successful pivot toward clean energy financing. This shift required developing new competencies—understanding solar radiation patterns, wind resource assessment, battery storage technologies, and grid integration challenges. The technical teams that once evaluated coal plant efficiencies now analyzed module degradation rates and capacity utilization factors for renewable projects.

International capital raising capabilities expanded dramatically during this period. The FY2020 milestone of raising US$1.3 billion from international markets, including US$1 billion in June 2019—the first dual and largest USD bonds transaction for a government-owned Indian NBFC after the REC acquisition—demonstrated global investor confidence. These international issuances not only diversified funding sources but also subjected PFC to global governance standards and ESG scrutiny.

The modern operational framework reflects sophisticated risk management evolution. Net NPA reached its lowest level at 0.31% in Q1 FY26 from 0.84% in Q1 FY25, while Gross NPA significantly declined by 150 basis points from 2.97% to 1.47%. This improvement occurred despite power sector stress, demonstrating effective resolution mechanisms and proactive asset management. The establishment of dedicated stressed asset resolution teams, early warning systems, and sector-specific monitoring frameworks contributed to this achievement.

The role in government scheme implementation became increasingly sophisticated. Beyond traditional rural electrification programs, PFC emerged as the key financier for complex initiatives like the Revamped Distribution Sector Scheme (RDSS), focusing on distribution infrastructure modernization and smart metering deployment. The Integrated Power Development Scheme (IPDS) implementation required coordinating with multiple stakeholders—state utilities, technology providers, and urban local bodies—showcasing PFC's project management capabilities beyond mere lending.

Strategic focus on renewable energy financing aligned with national commitments to achieve 500 GW non-fossil fuel capacity by 2030. The JBIC loan facility specifically targets financing renewable energy portfolios, advancing India's transition to non-fossil-fuel-based energy sources. This involved developing specialized products for solar parks, wind-solar hybrid projects, battery storage systems, and green hydrogen initiatives. The technical expertise accumulated in conventional power was reimagined for distributed generation, mini-grids, and prosumer models.

The organizational transformation to support expanded operations was comprehensive. New verticals were created for sustainable finance, international business, and innovation funding. Partnerships with multilateral agencies like World Bank, ADB, and KfW provided not just capital but technical assistance for capability building. Digital transformation initiatives modernized loan origination, credit assessment, and portfolio monitoring processes. Artificial intelligence and machine learning applications were piloted for early stress detection and customer service enhancement.

Leadership under Chairman and Managing Director Parminder Chopra has emphasized this strategic evolution: "PFC has once again delivered a strong financial performance... These results reaffirm PFC's position as a leading financier in the power and infrastructure sectors and reflect our strategic focus on sustainable growth and energy transition".

Managing the transition from thermal to renewable financing required delicate balancing. While renewable energy represented the future, existing thermal assets needed continued support to prevent stranded investments and maintain grid stability. PFC developed transition financing products helping coal plants improve efficiency and reduce emissions while gradually shifting capital allocation toward clean energy. This pragmatic approach recognized that energy transition would be gradual, requiring careful management of legacy assets.

The expansion into new infrastructure sectors brought fresh challenges. Electric vehicle charging infrastructure financing required understanding utilization patterns, technology standards, and business model viability. Smart city projects involved complex stakeholder management across urban local bodies, technology providers, and citizen groups. Metro rail and urban transport financing demanded expertise in ridership projection and fare box recovery. Each sector expansion stretched organizational capabilities while offering portfolio diversification benefits.

Regulatory compliance became increasingly complex with expanded operations. Different infrastructure sectors were governed by distinct regulatory frameworks—electricity regulation, petroleum and natural gas rules, urban development guidelines. Managing these multiple compliance requirements while maintaining operational efficiency required sophisticated governance mechanisms. The establishment of specialized compliance teams, regular regulatory updates, and proactive engagement with regulators became essential.

The financial performance validated this strategic evolution. Q1 FY26 witnessed consolidated net profit of ₹6,866.26 crore, marking 24% year-on-year growth and 8.7% sequential quarter improvement. These results demonstrated that expanding beyond traditional power sector boundaries while maintaining asset quality discipline could deliver sustainable growth. The ability to generate strong returns while supporting infrastructure development validated PFC's hybrid model combining commercial operations with developmental objectives.

VII. Business Model & Competitive Dynamics

Power Finance Corporation's business model represents a sophisticated blend of development banking principles and commercial financial operations, creating a unique position in India's infrastructure financing landscape. The core revenue generation mechanism remains elegantly simple—borrowing at lower rates leveraging quasi-sovereign status and lending at higher rates to power and infrastructure projects—but the execution complexity has evolved dramatically over four decades.

The fund-based products constitute PFC's primary business, with project term loans forming the backbone. These loans, typically tenure of 10-15 years with moratorium periods aligned to project construction schedules, are structured to match project cash flows. The pricing mechanism incorporates base rates linked to government securities, credit spreads based on borrower ratings, and sector-specific risk premiums. Lease financing for equipment purchases offers utilities capital efficiency benefits, allowing off-balance-sheet financing while PFC retains asset ownership. Short and medium-term loans address working capital requirements of equipment manufacturers, creating ecosystem liquidity essential for project execution.

The non-fund based products portfolio includes deferred payment guarantees, letters of comfort, and guarantees for performance of contracts/obligations with regards to fuel supply agreements, along with credit enhancement facilities. These products generate fee income while optimizing capital utilization, as they don't require immediate fund deployment but create contingent liabilities. The sophistication of structuring these products—determining guarantee fees, managing counter-party risks, establishing recourse mechanisms—reflects PFC's evolved risk management capabilities.

The funding strategy leverages PFC's unique position with most funds raised through rupee-denominated bonds carrying the highest credit rating in the Indian market, while also being eligible for raising funds through capital gain tax bonds under section 54EC of the Income Tax Act, 1961. This special status provides access to retail investors seeking tax-efficient investment options, creating a stable funding source at competitive rates. The ability to raise 54EC bonds gives PFC a structural advantage over private sector competitors who cannot access this funding pool.

The competitive landscape has transformed dramatically from PFC's monopolistic early decades. Commercial banks, initially hesitant about power sector exposure, now compete aggressively for quality assets. Private sector NBFCs like L&T Finance and Tata Capital have developed specialized infrastructure financing capabilities. International lenders, including Japanese banks and multilateral institutions, offer competitive terms for renewable energy projects. Yet PFC maintains distinctive advantages that preserve its market leadership.

Government ownership at 56.0% represents both strength and constraint. The sovereign comfort enables lower borrowing costs, approximately 50-75 basis points below comparable private NBFCs. Government backing provides implicit guarantee comfort to lenders and bondholders, reducing risk premiums. Access to government schemes and nodal agency roles creates captive business opportunities. However, government ownership also imposes constraints—lending decisions sometimes reflect policy priorities over commercial merit, dividend payments must satisfy fiscal needs, and operational flexibility remains limited compared to private competitors.

The relationship with REC post-acquisition creates interesting competitive dynamics. While both entities operate independently, common ownership enables coordinated lending for large projects. The combined entity can finance up to ₹50,000 crore for a single project, unmatched by any competitor. Joint appraisal processes leverage complementary expertise while maintaining separate risk assessments. However, the inability to fully merge limits operational synergies and maintains cost duplications.

The dividend philosophy reflects balancing stakeholder interests, with PFC declaring dividend of ₹2.05 per share in March 2025, translating to a dividend yield of 3.80%. This consistent dividend payment attracts income-focused investors while retaining sufficient capital for growth. The dividend payout ratio of approximately 30-35% demonstrates prudent capital allocation, maintaining balance sheet strength while rewarding shareholders.

Technology adoption increasingly differentiates PFC's operational efficiency. Digital loan origination platforms reduce processing time from weeks to days. Automated credit scoring models incorporate hundreds of variables for risk assessment. Blockchain pilots for documentation management promise reduced fraud and faster disbursements. Artificial intelligence applications for early warning systems identify stress signals before traditional metrics. These technology investments, while requiring significant capital expenditure, enhance productivity and risk management capabilities.

The advisory and consultancy services leverage PFC's sectoral expertise for fee income generation. These services span financial, regulatory, and capacity building domains, positioning PFC as more than just a lender. Project structuring advice for state governments, tariff determination support for regulatory commissions, and capacity building programs for utility officials create value beyond financing. These activities strengthen relationships, generate insights for lending decisions, and establish PFC as a knowledge institution rather than mere financial intermediary.

Human capital strategy reflects the specialized nature of infrastructure financing. With approximately 550 employees managing assets exceeding ₹11 lakh crore, PFC demonstrates remarkable operational leverage. The workforce combines engineers understanding technical aspects, financial analysts evaluating commercial viability, and legal experts navigating regulatory complexity. Continuous learning programs, including international training and industry certifications, maintain competency currency. Performance-linked compensation, while constrained by public sector guidelines, increasingly rewards individual contribution.

The geographic diversification strategy balances concentration risks with operational efficiency. While maintaining strong presence in power-surplus states like Gujarat and Tamil Nadu, PFC actively develops portfolios in power-deficit regions like Bihar and Uttar Pradesh. International financing remains limited, focusing on Indian companies' overseas acquisitions rather than direct international exposure. This domestic focus reflects both regulatory constraints and strategic choice to leverage local expertise.

Margin management in a declining interest rate environment poses ongoing challenges. As MOSL analysis indicates, PFC has reaffirmed loan growth guidance of 10-11% for FY26, with expectations of healthy Return on Assets (RoA) of 3% and Return on Equity (RoE) of 18% by FY27, coupled with dividend yield of ~4.4%. The ability to maintain spreads requires careful asset-liability management, dynamic pricing strategies, and operational efficiency improvements.

The business model evolution from simple government-directed lending to sophisticated structured financing demonstrates remarkable institutional adaptation. The ability to compete with private sector institutions while maintaining developmental mandate, generate commercial returns while supporting policy objectives, and embrace innovation while preserving stability represents the unique balance PFC has achieved. This hybrid model—neither purely commercial nor entirely developmental—positions PFC distinctively in India's financial landscape.

VIII. Challenges & Risk Factors

The structural challenges facing Power Finance Corporation are starkly evident in its financial metrics, with the company showing low interest coverage ratio and delivering poor sales growth of 11.4% over the past five years. These headline numbers mask deeper systemic issues that threaten PFC's traditional business model and require fundamental strategic recalibration.

The sectoral challenges in India's power ecosystem create cascading risks for PFC's portfolio. Land acquisition for power projects remains a persistent bottleneck, with projects delayed months or years due to farmer protests, litigation, and compensation disputes. The Land Acquisition Act of 2013, while addressing social concerns, significantly increased project costs and timelines. PFC's exposure to stalled projects due to land issues exceeds ₹15,000 crore, requiring constant restructuring and provision coverage.

Delays in Power Purchase Agreement execution compound project viability concerns. State distribution companies, wary of long-term commitments amid rapidly declining renewable energy tariffs, hesitate to sign PPAs for new thermal capacity. This reluctance leaves completed projects without assured off-take, transforming performing assets into potential NPAs. The phenomenon of "stranded assets"—completed power plants unable to find buyers for their electricity—represents an existential threat to traditional project finance models.

The financial health of State Electricity Boards and distribution companies remains PFC's Achilles heel. Despite multiple bailout schemes, including UDAY and the recent Revamped Distribution Sector Scheme, state DISCOMs continue hemorrhaging losses exceeding ₹90,000 crore annually. Political pressure for free or subsidized power, inefficient operations, and high transmission and distribution losses perpetuate the vicious cycle. PFC's exposure to state utilities exceeds ₹4 lakh crore, creating concentration risk that no amount of diversification can fully mitigate.

The energy transition presents both obsolescence risk and opportunity cost challenges. India's commitment to 500 GW renewable capacity by 2030 implies dramatic reduction in thermal capacity addition. PFC's legacy thermal portfolio, accumulated over decades, faces declining utilization rates as renewable energy receives dispatch priority. Plant load factors for coal-based plants have declined from 78% in 2010 to barely 55% currently, impacting project economics and debt servicing ability. The ₹2 lakh crore exposure to coal-based generation could transform from performing assets to stranded investments if energy transition accelerates beyond current projections.

Renewable energy, while representing the future, brings its own financing challenges. The intermittent nature of solar and wind generation creates grid stability issues, requiring expensive battery storage or gas-based backup. Aggressive tariff competition has driven renewable energy prices below ₹2.50 per unit, raising questions about project viability and developer sustainability. The sector's dependence on imported solar panels and wind turbines creates currency and supply chain risks. PFC's renewable portfolio, while growing rapidly, requires different risk assessment frameworks that are still evolving.

The regulatory environment adds another layer of complexity, with moderating loan growth expectations to 10-11% reflecting these sectoral challenges. The Reserve Bank of India's tightening norms for NBFCs—including asset quality recognition, provisioning requirements, and exposure limits—constrain operational flexibility. The inability to fully merge with REC due to regulatory restrictions limits synergy realization and maintains operational inefficiencies. Periodic regulatory changes in the power sector, from tariff determination mechanisms to renewable purchase obligations, create policy uncertainty affecting project viability.

Political risk remains embedded in PFC's operating model. Government ownership means lending decisions sometimes reflect political priorities rather than commercial merit. Pressure to fund unviable projects in politically sensitive regions, maintain exposure to struggling state utilities, and support government schemes regardless of economics compromises portfolio quality. The expectation to pay substantial dividends for government's fiscal needs limits capital retention for growth. Changes in government policies with electoral cycles create strategic discontinuity.

The competitive landscape intensification threatens market share and margins. Commercial banks, with lower cost of funds and diversified portfolios, cherry-pick quality assets leaving PFC with riskier exposures. International lenders offer longer tenures and competitive pricing for renewable projects. Fintech platforms are disintermediating traditional lending for smaller ticket sizes. Green bonds and ESG-focused funds bypass traditional lenders entirely. PFC's market share in incremental power sector financing has declined from over 30% to approximately 20% currently.

Technology disruption poses existential questions about PFC's relevance. Distributed generation through rooftop solar reduces need for large centralized projects. Peer-to-peer energy trading platforms could eliminate traditional utility models. Battery storage advancement might make grid infrastructure investments redundant. Blockchain-based project financing could disintermediate traditional lenders. While PFC invests in digital transformation, the fundamental business model premised on large-scale infrastructure financing faces disruption risk.

Asset quality concerns persist despite improving metrics. The power sector's structural issues mean today's performing assets could become tomorrow's NPAs with policy changes or technology shifts. The practice of restructuring stressed assets through extended tenures and reduced rates masks underlying stress. The concentration risk from large exposures to single projects or groups remains elevated. The interconnected nature of power sector stress means problems in one segment quickly cascade across the portfolio.

Concerns about state governments' financial discipline remain particularly pertinent. Electoral cycles drive populist policies like free power and loan waivers, destroying payment culture and financial discipline. State government guarantees, once considered sovereign comfort, increasingly lack credibility given fiscal stress. The unwillingness to implement cost-reflective tariffs perpetuates DISCOM losses and upstream payment delays. PFC's dependence on state government support for recovery creates vulnerability to political economy dynamics.

The human capital challenge increasingly constrains organizational capability. Public sector compensation constraints limit ability to attract specialized talent for emerging sectors like renewable energy, electric mobility, and smart cities. The average age of PFC employees exceeds 45 years, with limited fresh recruitment creating succession planning challenges. The cultural shift from traditional project financing to innovation funding requires mindset transformation that proves difficult in established organizations. Competition from private sector and startups for quality talent intensifies retention challenges.

International risks from currency fluctuations and global interest rate movements affect both assets and liabilities. While PFC primarily operates domestically, international borrowings for funding create currency exposure. Global interest rate increases impact refinancing costs and spread management. Climate change physical risks—floods, droughts, cyclones—threaten infrastructure assets and project viability. Transition risks from global decarbonization pressure could strand fossil fuel investments faster than anticipated.

IX. The Future: Energy Transition & Growth Strategy

India's power demand trajectory presents an unprecedented opportunity landscape that Power Finance Corporation is uniquely positioned to capitalize upon. The country's electricity consumption, currently at 1,200 units per capita compared to the global average of 3,200 units, suggests massive headroom for growth. With GDP projected to reach $7 trillion by 2030 and urbanization accelerating, electricity demand could double from current levels, requiring investments exceeding ₹30 lakh crore across generation, transmission, and distribution infrastructure.

The renewable energy financing opportunity represents the most transformative growth vector. India's commitment to 500 GW non-fossil fuel capacity by 2030 implies adding approximately 40-50 GW renewable capacity annually, requiring ₹3-4 lakh crore yearly investment. PFC has already facilitated development of over 50 GW renewable energy capacity, approximately 25% of the country's total installed capacity, positioning it as a dominant renewable energy financier. The evolution from funding large centralized thermal plants to distributed renewable installations requires fundamental reimagination of risk assessment, project structuring, and portfolio management approaches.

The electric mobility revolution opens entirely new financing verticals. With India targeting 30% electric vehicle penetration by 2030, the charging infrastructure requirement is staggering—an estimated 400,000 public charging stations and millions of private chargers. PFC's early moves into EV charging infrastructure financing, leveraging relationships with power distribution companies who control real estate and electrical infrastructure, provide first-mover advantages. The convergence of transport and energy sectors creates unique opportunities for integrated financing solutions.

Battery storage emerges as the critical enabler for renewable energy integration, representing a ₹2 lakh crore investment opportunity by 2030. PFC's technical expertise in power systems positions it to evaluate complex storage projects combining technology risk, merchant risk, and grid integration challenges. The ability to structure hybrid renewable-plus-storage projects, managing multiple revenue streams and technology interfaces, becomes a key differentiator. Early investments in battery manufacturing facilities and recycling infrastructure could create strategic positions in the storage value chain.

Green hydrogen production, targeting 5 million tonnes annually by 2030, requires massive renewable energy capacity and electrolyzer investments exceeding ₹8 lakh crore. PFC's relationships with industrial consumers, renewable developers, and technology providers enable ecosystem orchestration for this nascent sector. Financing structures for green hydrogen involve complex risk allocation across technology, off-take, and feedstock supply, requiring sophisticated financial engineering capabilities that PFC is developing through international partnerships.

The expansion into smart cities and urban infrastructure leverages PFC's project management expertise while diversifying revenue streams. Smart metering deployment across 250 million consumers, estimated at ₹1.5 lakh crore investment, combines PFC's utility relationships with technology financing capabilities. Urban metro rail projects, requiring ₹5 lakh crore investment over the decade, offer stable long-term assets with predictable cash flows. The integration of energy, transport, and digital infrastructure in smart cities creates holistic financing opportunities aligned with PFC's evolving capabilities.

Technology transformation within PFC accelerates operational efficiency and risk management sophistication. Artificial intelligence applications for credit assessment incorporate thousands of variables including weather patterns, commodity prices, and social media sentiment. Blockchain platforms for project documentation and payment processing reduce transaction costs and settlement times. Digital twins of financed assets enable real-time performance monitoring and predictive maintenance. These technology investments, while requiring significant upfront capital, promise dramatic productivity improvements and risk reduction.

International collaboration intensifies with strategic partnerships like the JBIC relationship, where PFC CMD Parminder Chopra emphasized: "Promoting non-fossil fuel-based energy is a key priority for the Government of India. With the support of international lenders like JBIC, PFC will play a pivotal role in advancing this vision". These partnerships provide not just capital but technology transfer, best practices, and global market access.

The Environmental, Social, and Governance (ESG) integration becomes central to PFC's strategy rather than compliance obligation. Sustainability-linked loans with interest rates tied to ESG performance create incentives for borrowers to improve environmental outcomes. Exclusion lists for polluting industries and mandatory environmental assessments for all projects reflect evolving stakeholder expectations. Social impact metrics including job creation, community development, and energy access become integral to project evaluation. Governance improvements through independent directors, stakeholder engagement, and transparency initiatives enhance institutional credibility.

Competition from private capital and international development finance intensifies but also creates partnership opportunities. Co-lending arrangements with commercial banks leverage PFC's project expertise and banks' low-cost deposits. Partnerships with international climate funds access concessional capital for innovative projects. Collaboration with private equity funds for renewable energy platforms combines PFC's debt financing with equity risk capital. The evolution from competition to "coopetition" reflects mature market dynamics where collaboration creates value for all stakeholders.

The path to supporting India's $5 trillion economy ambition requires PFC to transform from a power sector lender to an integrated infrastructure financier. Cross-sector linkages mean financing decisions cannot occur in isolation—a green hydrogen project requires renewable energy, water infrastructure, and industrial off-take coordination. The ability to structure and finance these complex, multi-stakeholder projects becomes PFC's unique value proposition. This requires developing expertise across sectors, building partnerships with specialized players, and creating innovative financing structures.

Regulatory evolution toward market-based mechanisms creates both opportunities and challenges. The introduction of market-based economic dispatch optimizes grid operations but creates merchant risk for generators. Real-time electricity markets offer price discovery but introduce volatility requiring sophisticated hedging. Carbon pricing mechanisms, when introduced, will fundamentally alter project economics favoring clean energy. PFC's ability to anticipate and adapt to regulatory changes, developing products that help clients manage new risks, determines future relevance.

The organizational transformation to support this ambitious growth agenda is underway but requires acceleration. New talent with expertise in emerging technologies, international markets, and sustainable finance joins traditional power sector specialists. Agile working methods replace hierarchical decision-making for faster response to market opportunities. Innovation labs experiment with new business models and financing structures. Cultural transformation from risk aversion to calculated risk-taking enables participation in emerging sectors. This human capital transformation, perhaps more than financial resources or market opportunities, determines PFC's ability to realize its future potential.

X. Playbook: Business & Investment Lessons

Building a specialized Non-Banking Financial Company in a complex sector like power requires deep domain expertise that transcends traditional financial analysis. Power Finance Corporation's journey illustrates that successful infrastructure financing demands understanding of technology evolution, regulatory dynamics, political economy, and social considerations beyond conventional credit assessment. The ability to evaluate a coal plant's heat rate efficiency, a solar panel's degradation curve, or a distribution network's technical losses becomes as important as analyzing financial ratios or cash flow projections.

The institutional knowledge accumulated over decades creates insurmountable competitive advantages. PFC's database of power project performance across fuel types, geographies, and developers provides pattern recognition capabilities that no algorithm can replicate. Understanding why certain Engineering, Procurement, and Construction (EPC) contractors consistently deliver projects on time, which equipment suppliers provide reliable after-sales service, or how different state governments honor commitments requires experiential learning over market cycles. This tacit knowledge, embedded in organizational processes and professional networks, represents PFC's true moat.

Managing government ownership while operating commercially requires delicate balancing that few institutions master successfully. PFC demonstrates that public sector enterprises can achieve commercial success without full privatization if granted operational autonomy and held accountable for performance. The key lies in transparent governance mechanisms that separate ownership from management, clear performance metrics that balance developmental and commercial objectives, and professional leadership insulated from political interference. The Maharatna status institutionalizes this autonomy, providing a replicable model for public sector reform.

Capital allocation in infrastructure demands long-term thinking that often conflicts with quarterly earnings pressure. Infrastructure projects have gestation periods spanning years and operational lives extending decades. PFC's ability to maintain patient capital deployment despite market volatility and earnings expectations reflects institutional maturity. The discipline to avoid chasing short-term gains through risky lending, maintaining focus on infrastructure despite lucrative opportunities in retail or corporate lending, demonstrates strategic clarity that creates long-term value.

The importance of sector expertise and relationships cannot be overstated in infrastructure financing. PFC's network spanning government officials, regulatory commissioners, utility executives, equipment suppliers, and EPC contractors enables information flow and problem-solving capabilities that pure financial players cannot replicate. These relationships, built over decades of consistent engagement, facilitate project restructuring during distress, enable coordinated sector interventions, and provide early warning signals about emerging risks. The social capital accumulated through reliable partnership proves as valuable as financial capital in infrastructure development.

Navigating regulatory complexity in India's federal structure requires sophisticated stakeholder management. Power being a concurrent subject means both central and state governments influence sector dynamics. PFC's ability to work with multiple stakeholders—central ministries setting policy, state governments owning utilities, regulators determining tariffs, courts adjudicating disputes—while maintaining commercial focus demonstrates institutional adaptability. Understanding that regulatory frameworks evolve and preparing for multiple scenarios rather than optimizing for single outcomes ensures resilience.

The REC acquisition lessons highlight that strategic intent must align with execution capabilities. While the acquisition provided immediate scale with PFC acquiring government's 52.63% stake for Rs 14,500 crore, the inability to fully merge due to regulatory constraints limited value creation. The episode demonstrates that financial engineering cannot substitute for operational integration, and ownership consolidation without organizational merger may satisfy political objectives but fails to create commercial synergies.

Creating value through policy implementation and advisory services extends influence beyond lending. PFC's role as nodal agency for government schemes provides insights into policy direction, relationships with key stakeholders, and implementation capabilities that pure lenders lack. The ability to shape policy through ground-level feedback, implement complex schemes requiring coordination across multiple agencies, and provide technical assistance to struggling utilities creates ecosystem value transcending financial returns. This positions PFC as an indispensable institution rather than replaceable lender.

The infrastructure financing playbook requires understanding that projects are means to developmental ends, not merely financial assets. Every power plant financed affects millions of citizens' quality of life. Each transmission line enables economic activity across regions. Distribution network investments determine industrial competitiveness and social development. This developmental perspective, while sometimes conflicting with commercial objectives, creates sustainable competitive advantages through government support, social legitimacy, and stakeholder trust that purely commercial players cannot replicate.

Risk management in infrastructure differs fundamentally from conventional lending given the long-term nature, political sensitivity, and technology evolution. Traditional metrics like debt service coverage ratios or loan-to-value ratios provide false comfort when technology disruption can strand assets or political decisions can impair recovery. PFC's evolution toward dynamic risk assessment incorporating scenario planning, stress testing, and early warning systems reflects learning from cycles of infrastructure boom and bust. The emphasis on portfolio diversification across sectors, geographies, and technologies provides resilience against concentrated shocks.

The lesson about building specialized NBFCs extends beyond power sector to other infrastructure verticals. The PFC model—deep sectoral expertise, patient capital, government partnership, commercial discipline—can be replicated in roads, ports, airports, or urban infrastructure. The key success factors remain consistent: domain knowledge that enables superior risk assessment, relationships that facilitate project development and restructuring, regulatory understanding that enables navigation of complex frameworks, and institutional patience that matches infrastructure development timelines.

The importance of maintaining focus despite diversification temptations resonates across financial services. While PFC expanded into related infrastructure sectors, it resisted venturing into unrelated areas like retail lending or capital markets despite potentially higher returns. This sectoral focus enables capability development, reputation building, and relationship deepening that generalists cannot achieve. The depth versus breadth trade-off consistently favors specialization in complex sectors requiring domain expertise.

XI. Analysis & Bull vs. Bear Case

Bull Case: The Infrastructure Finance Powerhouse

The bullish narrative for Power Finance Corporation rests on its position as an essential infrastructure financier with unmatched competitive advantages. The robust financial performance validates this thesis, with Q1 FY26 consolidated net profit surging 25% YoY to ₹8,981 crore, accompanied by declaration of ₹3.70 interim dividend per share. These aren't merely quarterly fluctuations but reflect structural strengths that position PFC for sustained outperformance.

The government backing provides incomparable advantages in infrastructure financing. The quasi-sovereign status enables borrowing at rates 50-75 basis points below private competitors, creating structural margin advantages. Implicit government guarantee ensures continuous access to capital even during market disruptions when private lenders retreat. The designation as nodal agency for government schemes creates captive business opportunities worth thousands of crores annually. This government relationship, impossible for private competitors to replicate, ensures PFC's relevance regardless of market cycles.

Asset quality improvements demonstrate exceptional risk management capabilities, with Net NPA at historical lows of 0.31% in Q1 FY26, down from 0.84% a year ago, while Gross NPA declined 150 basis points to 1.47%. These metrics, achieved despite power sector stress and economic disruptions, reflect sophisticated early warning systems, proactive restructuring capabilities, and strong recovery mechanisms. The ability to maintain asset quality while growing the loan book demonstrates that expansion doesn't require compromising underwriting standards.

The renewable energy transition creates unprecedented growth opportunities that PFC is uniquely positioned to capture. The 36% year-on-year growth in renewable energy portfolio in Q1 FY26 demonstrates successful execution of this strategic pivot. With India targeting 500 GW renewable capacity by 2030, the financing requirement exceeds ₹25 lakh crore, providing massive addressable market expansion. PFC's technical expertise, regulatory relationships, and project structuring capabilities position it as the preferred financier for this transformation.

The Maharatna status granted on October 12, 2021, provides operational flexibility that unlocks value creation potential. The ability to make investments up to ₹5,000 crore without government approval enables quick decision-making for strategic opportunities. Authority to form joint ventures and establish international operations facilitates partnerships with global investors and technology providers. Enhanced autonomy in organizational restructuring and human resource management enables agility competing with private players while maintaining public sector stability.

The dividend yield attractiveness makes PFC compelling for income-focused investors. With expectations of ~4.4% dividend yield by FY27 according to Motilal Oswal analysis, PFC offers superior income generation compared to fixed deposits or government securities. The consistency of dividend payments, supported by strong cash generation and government's fiscal needs, provides reliability that equity markets rarely offer. This positions PFC as a defensive play in volatile markets while offering growth potential from infrastructure expansion.

Capital efficiency metrics demonstrate exceptional execution capabilities. With approximately 550 employees managing assets exceeding ₹11 lakh crore, the operational leverage is extraordinary. The ability to generate ₹30,000+ crore annual profits with minimal workforce reflects process efficiency, technology adoption, and sectoral expertise that competitors cannot easily replicate. This efficiency translates to superior return ratios and competitive pricing capabilities.

Bear Case: Structural Headwinds and Disruption Risks

The bearish perspective highlights fundamental challenges that could impair PFC's growth trajectory and profitability. The poor sales growth of 11.4% over the past five years signals structural issues beyond temporary disruptions. This anemic growth, despite India's infrastructure boom, suggests market share losses and competitive pressures that could intensify.

Regulatory constraints severely limit growth potential, particularly post-REC acquisition, with the merged entity's lending capacity potentially halved due to NBFC exposure norms limiting debt to 25% per project. The inability to fully merge with REC despite common ownership reflects regulatory rigidities that prevent optimal corporate structures. These constraints become more binding as project sizes increase, potentially forcing PFC to cede market share to consortiums of smaller lenders.

Competition from banks and private capital intensifies margin pressure and cherry-picking of assets. Commercial banks with lower cost of funds and diversified portfolios increasingly dominate quality infrastructure financing. International lenders offer longer tenures and competitive pricing that PFC struggles to match. Private equity funds directly investing in infrastructure projects bypass debt financing entirely. The commoditization of infrastructure lending erodes PFC's historical advantages.

Asset quality risks from state utilities remain elevated despite current low NPA levels. State distribution companies' losses exceeding ₹90,000 crore annually create systemic risk that no amount of restructuring can eliminate. Political pressures for power subsidies and loan waivers destroy payment culture and commercial discipline. The concentration risk from exposure to state utilities means a few states defaulting could devastate PFC's asset quality. Historical experience shows power sector NPAs can spike rapidly during economic downturns.

The energy transition creates massive stranded asset risks for PFC's thermal portfolio. With renewable energy costs declining below thermal generation, capacity utilization for coal plants continues deteriorating. The ₹2 lakh crore exposure to coal-based generation could become non-performing as plants become economically unviable. Technology disruption from distributed generation and battery storage could make centralized power infrastructure obsolete faster than expected. The pace of transition could outrun PFC's ability to adapt its portfolio.

Government ownership increasingly becomes a liability in competitive markets. Political interference in lending decisions compromises commercial discipline and portfolio quality. Pressure to fund unviable projects for political considerations creates hidden asset quality risks. Bureaucratic decision-making processes delay responses to market opportunities. Public sector compensation constraints limit ability to attract specialized talent for emerging sectors. The expectation to support government fiscal needs through dividends limits capital retention for growth.

The lack of operational synergies from the REC acquisition questions management execution capabilities. Despite paying ₹14,500 crore for control, the inability to merge operations means duplicated costs persist. The promised synergies remain unrealized while acquisition debt burdens the balance sheet. The confused organizational structure with two separate entities under common ownership creates inefficiencies and stakeholder confusion. This failed integration raises concerns about management's ability to execute complex strategic initiatives.

Technology disruption threatens PFC's fundamental business model. Peer-to-peer energy trading could eliminate need for centralized utilities that PFC finances. Blockchain-based project financing platforms could disintermediate traditional lenders. Artificial intelligence-driven credit assessment could commoditize PFC's analytical advantages. The rise of green bonds and ESG funds creates alternative financing channels bypassing traditional lenders. PFC's technology investments, while substantial, may prove insufficient against digital-native competitors.

XII. Recent News

Power Finance Corporation reported strong Q1 FY26 results with net profit rising 21% year-on-year to ₹4,501.5 crore compared to ₹3,717.8 crore in the corresponding period last year. Total revenue from operations increased 15.6% to ₹13,773.42 crore, while Net Interest Income saw robust growth of 26%, reaching ₹5,469 crore.

In a landmark development, PFC signed a general agreement with Japan Bank for International Cooperation (JBIC) to set up a credit line of up to JPY 120 billion in January 2025, marking JBIC's largest green financing deal with any Indian company. The long-term loan facility, extended under JBIC's GREEN initiative with tenure up to 20 years, will enable PFC to finance renewable energy projects.

The company continues its shareholder-friendly approach, announcing an interim dividend of ₹3.70 per equity share for the financial year 2025-26, demonstrating confidence in sustained cash generation despite expansion investments.

Morgan Stanley initiated coverage on Power Finance Corporation with an Overweight rating in July 2025, projecting strong loan growth, attractive valuations, and a target price of ₹508, indicating significant upside potential. The report highlights PFC's stable asset quality and high dividend yields as compelling investment attributes.

Management commentary remains optimistic, with CMD Parminder Chopra highlighting that Q1 FY26 marked the company's highest-ever first-quarter disbursements with robust 16% year-on-year growth, while the renewable energy portfolio grew impressively by 36%.

Looking ahead, the Board of Directors approved a substantial ₹1,40,000 crore borrowing plan for 2025-26 in March 2025, along with declaration of fourth interim dividend of Rs 3.50 per equity share for 2024-25, signaling confidence in future growth prospects and commitment to shareholder returns.

XIII. Links & Resources

Company Resources: * Power Finance Corporation Annual Reports and Investor Presentations * REC Limited Financial Statements and Integration Updates * PFC Green Bond Framework and Sustainability Reports * Quarterly Earnings Calls and Transcripts

Regulatory Documents: * Reserve Bank of India NBFC Regulations and Infrastructure Finance Company Guidelines * Ministry of Power Policy Documents and Scheme Guidelines * CERC and SERC Regulatory Orders affecting Power Sector Financing * Competition Commission of India Orders on PFC-REC Acquisition

Industry Research: * India Energy Outlook by International Energy Agency * Power Sector Analysis by CRISIL, ICRA, and India Ratings * Renewable Energy Statistics by Ministry of New and Renewable Energy * State Electricity Board Performance Reports by Power Finance Corporation

Books on India's Infrastructure Development: * "The Turn of the Tortoise: The Challenge and Promise of India's Future" by T.N. Ninan * "India's Long Road: The Search for Prosperity" by Vijay Joshi * "The Third Pillar: How Markets and the State Leave the Community Behind" by Raghuram Rajan

Academic Papers: * "Development Finance in India: Historical Perspective and Current Challenges" - Economic and Political Weekly * "Infrastructure Financing in India: Challenges and Opportunities" - Reserve Bank of India Bulletin * "Energy Transition and Stranded Assets in India's Power Sector" - Institute for Energy Economics and Financial Analysis

Comparative Analysis: * China Development Bank - Infrastructure Financing Model * Brazilian Development Bank (BNDES) - Case Studies * European Investment Bank - Green Finance Initiatives * World Bank Infrastructure Finance Reports

ESG and Green Finance Resources: * Climate Bonds Initiative - India Green Bond Market Report * Task Force on Climate-related Financial Disclosures (TCFD) Framework * Sustainable Finance Initiatives by Indian Banks Association * Green Finance Study Group Reports by UNEP