Cube Highways Trust: India's Infrastructure InvIT Powerhouse

I. Introduction & Episode Roadmap

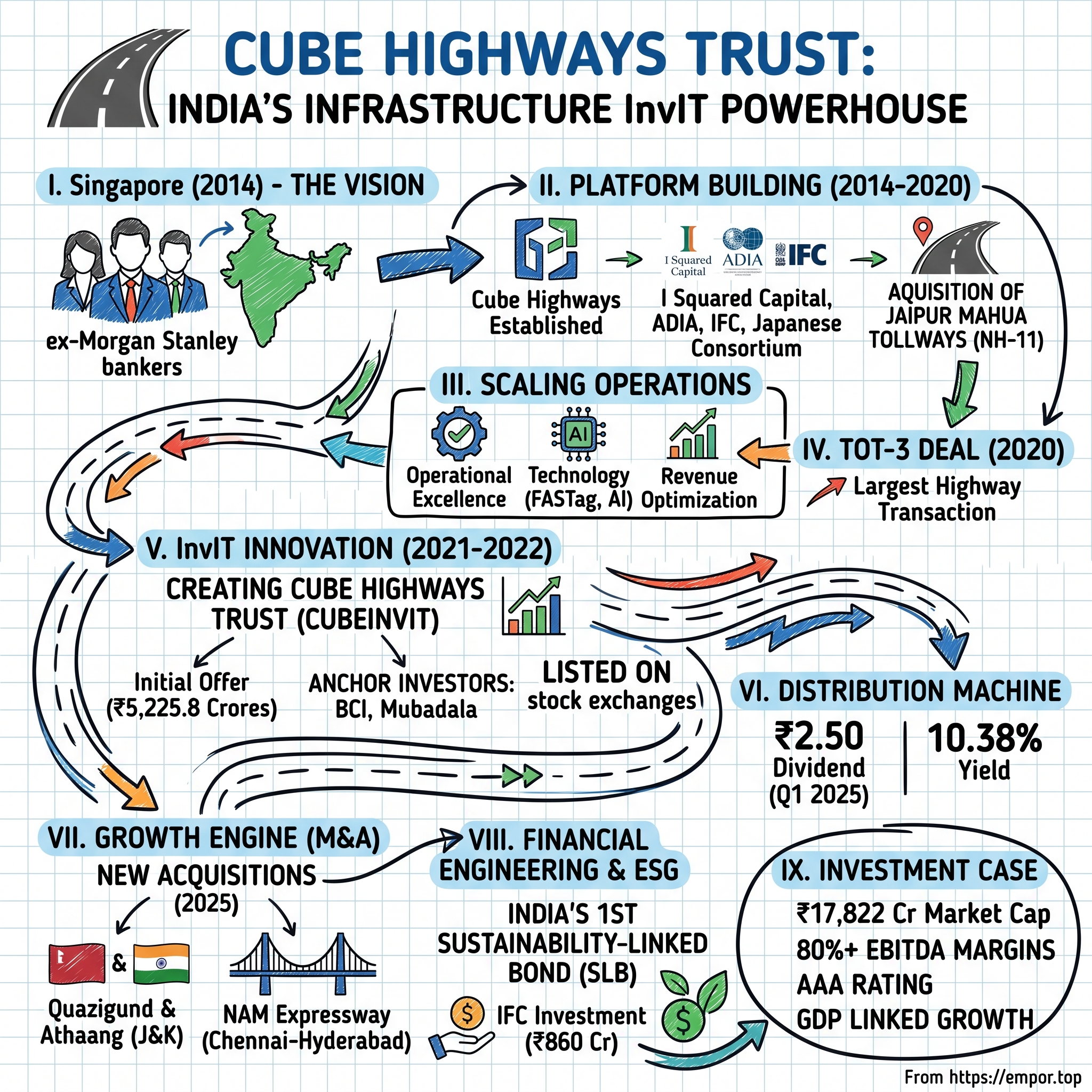

Picture this: It's a sweltering May afternoon in 2014, and a team of former Morgan Stanley infrastructure bankers sits in a Singapore boardroom, staring at a map of India dotted with red pins. Each pin represents a toll road—some operational, others distressed, all ripe for consolidation. The team, led by Sadek Wahba and his partners at the newly formed I Squared Capital, sees what others don't: India's highways aren't just asphalt and concrete. They're cash-flowing assets waiting to be financialized, packaged, and sold to yield-hungry global investors.

Fast forward to today, and that vision has materialized into Cube Highways Trust—one of India's largest Infrastructure Investment Trusts (InvITs) managing 25 road assets spanning 1,940 kilometers across 12 states. With 27 toll plazas collecting fees from millions of vehicles daily, Cube has transformed from a Singapore-based acquisition vehicle into a ₹17,822 crore market cap infrastructure powerhouse that's rewriting how India finances its ambitious infrastructure dreams.

But how did a group of Wall Street veterans crack the code on Indian toll roads? How did they convince global sovereign wealth funds from Abu Dhabi to British Columbia to bet billions on Indian highways? And why does their story matter for understanding the future of infrastructure investing globally?

This is the story of financial engineering meets nation-building—where sophisticated capital markets innovation collides with the mundane reality of toll collection in rural India. It's about turning traffic jams into investment returns, transforming government concessions into tradeable securities, and convincing retail investors that owning a slice of the Mumbai-Pune Expressway beats keeping money in fixed deposits.

The InvIT revolution that Cube Highways pioneered represents something bigger than just another financial product. It's the democratization of infrastructure ownership, the solution to India's $1.5 trillion infrastructure financing gap, and potentially the template for how emerging markets worldwide can bridge the chasm between infrastructure needs and available capital.

Our journey takes us from the glass towers of Morgan Stanley's infrastructure group to the dusty construction sites of National Highway 11 in Rajasthan. We'll explore how regulatory innovation created an entirely new asset class, why Singapore became the unlikely headquarters for India's toll road empire, and how a company that didn't exist until 2021 became the go-to vehicle for global institutions seeking Indian infrastructure exposure.

The timing couldn't be more critical. India stands at an infrastructure inflection point—the government has committed ₹111 lakh crore for infrastructure development through 2025, highway construction hit record levels of 40 kilometers per day, and vehicle ownership is exploding as millions join the middle class. Yet traditional financing models—government budgets and bank loans—can't keep pace. Enter the InvIT model, and specifically Cube Highways Trust, offering a solution that's part financial innovation, part operational excellence, and entirely dependent on India's economic transformation story playing out as promised.

What makes Cube's playbook particularly fascinating is its counter-intuitive approach. While tech unicorns chase growth at any cost, Cube methodically acquires mature, cash-generating assets. While startups pivot constantly, Cube's business model hasn't changed since day one: buy toll roads, operate them efficiently, distribute cash to investors. It's boring, predictable, and exactly what infrastructure investors crave.

II. The I Squared Capital Story & Infrastructure Revolution

The conference room at 280 Park Avenue hummed with tension in early 2012. Sadek Wahba, Morgan Stanley's global head of infrastructure investing, had just dropped a bombshell on his team: they were leaving to start their own fund. After building Morgan Stanley Infrastructure Partners into a $4 billion platform, Wahba and his lieutenants—Adil Rahmathulla and Gautam Bhandari—believed the real opportunity lay beyond Wall Street's constraints.

"Infrastructure is eating the world," Wahba told potential investors during their initial fundraising roadshow, borrowing Marc Andreessen's famous phrase about software. His thesis was simple yet profound: emerging markets needed $2 trillion annually in infrastructure investment, traditional sources could provide maybe half, and the gap represented the greatest investment opportunity of the next decade. By 2012, Wahba formed I Squared Capital alongside Adil Rahmathulla and Gautam Bhandari, all veterans of Morgan Stanley's infrastructure team. Wahba had spent 14 years at Morgan Stanley, where he started Morgan Stanley Infrastructure Partners and was Chief Executive Officer of Morgan Stanley Infrastructure. The timing was perfect—institutional investors desperately sought yield in a zero-interest-rate world, emerging markets needed capital, and infrastructure offered the holy grail: predictable, inflation-protected cash flows with limited correlation to public markets.

In 2015, the firm closed its first fund, ISQ Global Infrastructure Fund LP, with $3 billion in total commitments. But what distinguished I Squared wasn't just capital raising prowess—it was their platform-building philosophy. "We are known for the development of investment platforms in infrastructure where we start small and grow big", became their mantra.

India quickly emerged as the crown jewel in their emerging markets strategy. The country's infrastructure deficit was staggering—roads, power, ports all needed massive investment. But more importantly, India offered something China didn't: rule of law, English-language contracts, and a democracy that, while messy, provided predictable property rights protection. Cube Highways was established in 2014 to acquire and operate a diversified portfolio of toll roads and related infrastructure assets in India. The December 2014 acquisition of Jaipur Mahua Tollways—a 109-kilometer stretch on National Highway 11 in Rajasthan—marked I Squared's first concrete step into Indian highways. It was a relatively small deal, but it proved the thesis: stable toll collection, predictable traffic growth, government backing.

What I Squared saw that others missed was the infrastructure arbitrage opportunity. Indian toll roads were trading at 8-10x EBITDA multiples while similar assets in developed markets commanded 15-20x. The yield spread was massive—Indian roads offered 15-18% project IRRs versus 6-8% in the US or Europe. Yes, there were risks—regulatory uncertainty, traffic volatility, currency fluctuations—but for patient capital with operational expertise, the risk-reward equation was compelling.

The platform strategy was elegant in its simplicity. Rather than compete deal-by-deal with local players, I Squared would build a scaled platform—Cube Highways—that could become the consolidator of choice. The shareholders included I Squared Capital, a wholly-owned subsidiary of the Abu Dhabi Investment Authority, International Finance Corporation, and a consortium of Japanese investors including Mitsubishi Corporation. This wasn't just about capital; each investor brought something unique. ADIA provided patient sovereign wealth, IFC offered development finance expertise and regulatory relationships, while the Japanese consortium—including toll road operators—contributed operational know-how.

By 2020, I Squared had grown to manage $40 billion in assets under management, with India becoming an increasingly important geography. The infrastructure revolution Wahba envisioned was playing out in real-time. India's GDP was growing at 6-7% annually, vehicle ownership was exploding, and the government had launched ambitious programs like Bharatmala Pariyojana targeting 83,677 kilometers of highway development.

The brilliance of the I Squared approach wasn't just identifying the opportunity—it was structuring it for institutional capital. Infrastructure in emerging markets had historically been the domain of development banks and brave corporates. I Squared packaged it into something pension funds and sovereign wealth funds could understand: contracted cash flows, limited development risk, professional management, and clear exit strategies.

III. Building Cube Highways: The Platform Play (2014–2020)

The Singapore Airlines lounge at Changi Airport became an unlikely war room in late 2014. Dr. Harikishan Reddy, freshly recruited to lead Cube Highways as CEO, sat with his laptop open, juggling calls between Mumbai bankers, Delhi lawyers, and Singapore regulators. The mission was audacious: build India's premier toll road platform from scratch, starting with zero assets and ending with market leadership.

Why Singapore? The answer revealed the sophisticated thinking behind Cube's structure. Singapore offered tax treaties with India, a stable regulatory environment, proximity to Asian capital markets, and credibility with international investors. It was financial engineering at its finest—using Singapore as the holding company jurisdiction while operations remained firmly rooted in India.

The early days were anything but glamorous. Reddy and his initial team of five operated from a serviced office in Gurgaon, cold-calling distressed asset owners, poring over traffic studies, and building financial models late into the night. The team assembled from scratch brought approximately 5,960 years of combined experience across Operations and Maintenance, M&A, Project Finance, Capital Markets, ESG, Finance and Compliance.

The first major breakthrough came with the acquisition strategy. Rather than chase greenfield projects with construction risk, Cube focused on operational assets with proven traffic history. The logic was compelling: eliminate construction risk, buy assets with 15-20 years of remaining concession life, optimize operations, and generate predictable cash flows. It was boring, unsexy, and exactly what infrastructure investors wanted.

Between 2014 and 2018, Cube methodically acquired assets across India. Each acquisition followed a disciplined playbook: comprehensive due diligence, conservative traffic projections, operational improvements post-acquisition, and aggressive refinancing to lower cost of capital. The Western UP Tollway connecting Meerut and Muzaffarnagar, the Nellore-Tada road in Andhra Pradesh, the Krishnagiri-Walajapet corridor in Tamil Nadu—each added scale and geographic diversification.

An ADIA subsidiary first invested in Cube Highways in 2018, marking a watershed moment. The Abu Dhabi sovereign wealth fund's entry validated the platform's institutional quality. With ADIA's backing, Cube could now compete for larger transactions, access cheaper debt, and attract other blue-chip investors.

But the real game-changer came in 2020. The National Highways Authority of India (NHAI) announced the TOT (Toll-Operate-Transfer) Bundle 3—nine operational highways available as a package for a 30-year concession. The deal size was massive: $684 million upfront payment to NHAI for the right to collect tolls for three decades.

Completing the financial closure during the Covid-19 pandemic demonstrated the capabilities of the Cube Highways team and the strength of the platform, with Gautam Bhandari calling it "a defining transaction for transportation Public Private Partnerships globally". While competitors struggled with pandemic disruptions, Cube closed the largest highway transaction in Indian history.

The TOT-3 acquisition transformed Cube overnight. The bundle included strategic corridors across Bihar, Jharkhand, Tamil Nadu, and Uttar Pradesh. Traffic patterns were diverse—industrial cargo, agricultural produce, passenger vehicles—providing natural hedging. The assets were mature with established toll collection systems, eliminating operational risk.

By late 2020, Cube had assembled an enviable portfolio. The platform owned and operated nearly 8,400 lane-kilometers of highways across 27 roads, making it one of India's largest owners and operators of toll roads. The transformation from zero to hero took just six years.

What distinguished Cube wasn't just scale but operational excellence. The company developed proprietary in-house expertise to de-risk assets with state-of-the-art technologies and material science to operate and maintain its portfolio of highways. Electronic toll collection systems reduced leakage, predictive maintenance algorithms minimized downtime, and customer service initiatives improved user experience.

The numbers told the story. Toll collection efficiency improved from industry-average 94% to Cube's 98%. Operating expenses dropped 15-20% through centralized procurement and standardized processes. Debt costs fell 200-300 basis points through refinancing. Each improvement flowed directly to the bottom line, creating value for investors while maintaining service quality.

By March 2021, Cube Highways had been the most active investor in the Indian roads sector, with 13 new acquisitions under its belt. The platform approach had worked—Cube was now the counterparty of choice for sellers, the employer of choice for talent, and increasingly, the investment of choice for global institutions.

IV. The InvIT Innovation: Creating Cube Highways Trust (2021–2022)

The boardroom at Cube's Mumbai office buzzed with nervous energy on a humid September morning in 2021. The team was about to attempt something unprecedented: transform a private Singapore holding company into a publicly-listed Indian Infrastructure Investment Trust. The stakes couldn't be higher—success would unlock permanent capital and create liquidity for investors; failure would strand billions in illiquid assets. India's Infrastructure Investment Trust (InvIT) regulations, introduced by SEBI in 2014, had created a new asset class tailor-made for infrastructure assets. Think of InvITs as the infrastructure equivalent of REITs—they pool investor money, buy cash-generating infrastructure assets, and distribute most of the income to unit holders. For toll roads with predictable cash flows and long concession periods, the structure was perfect.

Cube Highways Trust was settled on December 7, 2021 by Cube Highways and Transportation Assets Advisors Private Limited and registered as an Infrastructure Investment Trust under the InvIT Regulations on April 5, 2022. The timing was strategic—India's infrastructure sector was booming, institutional investors sought yield in a low-rate environment, and the government actively promoted InvITs as a financing solution.

The structuring phase revealed the complexity of financial engineering required. Twenty-seven separate project SPVs (Special Purpose Vehicles) needed to be rolled up into a single trust structure. Each had different debt terms, concession agreements, and operational peculiarities. The legal gymnastics alone took six months—converting Singapore entities to Indian subsidiaries, harmonizing debt covenants, obtaining NOCs from lenders.

The Trust made an Initial Offer of 522,582,727 Ordinary Units through a private placement, aggregating to Rs 5,225.8 Crores, comprising 380,259,172 Ordinary Units aggregating to Rs 3,802.6 Crore through Fresh Issue and 142,323,555 Ordinary Units aggregating to Rs 1,423.2 Crore through Offer For Sale in April 2023.

The private placement route was deliberate. Rather than chase retail investors through a public IPO, Cube targeted sophisticated institutions who understood infrastructure investing. The anchor book read like a who's who of global infrastructure investors—British Columbia Investment Management Corporation (BCI), Mubadala Investment Company, and leading domestic institutional investors.

What made the offering compelling was the yield proposition. In an environment where 10-year Indian government bonds yielded 6-7%, Cube offered distribution yields of 9-12% backed by operating toll roads. The pitch was simple: government-backed concessions, contracted toll increases, proven traffic growth, professional management, and quarterly distributions.

The rating agencies loved it. The Trust was rated "Provisional Ind AAA/Stable" from three rating agencies—the highest possible rating for an Indian InvIT. The AAA rating wasn't just a badge of honor; it dramatically lowered borrowing costs and attracted conservative institutional investors like pension funds and insurance companies.

The governance structure balanced sponsor control with investor protection. Cube Highways and Infrastructure Pte. Ltd. and Cube Highways and Infrastructure III Pte. Ltd. remained sponsors, retaining significant skin in the game while independent directors and trustees protected minority investors. The investment manager—Cube Highways and Transportation Assets Advisors—handled day-to-day operations, ensuring professional management separate from sponsor interests.

Post-listing, Cube InvIT became a distribution machine. In the quarter ending June 2025, Cube Highways Trust declared dividend of ₹2.50 per share—translating to a dividend yield of 10.38%. These weren't promises of future growth like tech stocks; these were real cash distributions from toll collections hitting investor accounts every quarter.

The transformation from private platform to public InvIT solved multiple problems simultaneously. For I Squared and early investors, it provided liquidity and partial exit. For new investors, it offered access to infrastructure returns previously available only to large institutions. For India, it demonstrated how to channel domestic savings into infrastructure development. And for Cube itself, it created permanent capital to fund future growth.

V. The Portfolio & Business Model Deep Dive

Standing at the toll plaza on the Mumbai-Pune Expressway at 6 AM, you witness India's economic engine in motion. Trucks loaded with manufactured goods heading to JNPT port, IT professionals commuting between cities, families traveling for weekend getaways—each vehicle represents a micro-payment flowing into Cube's revenue stream. Multiply this scene across 27 toll plazas, and you understand the business model's elegant simplicity.

Cube operates 25 road assets, including 18 NHAI toll road assets, 1 NHAI annuity, 6 NHAI HAM and one state toll project, with an aggregate length of 1,940 km (8,450 lane kms) spread across 12 states. But the portfolio diversity goes beyond mere numbers—it's a carefully orchestrated mix of revenue models, geographies, and risk profiles.

The toll road assets form the portfolio's backbone. These Build-Operate-Transfer (BOT) concessions allow Cube to collect user fees directly from vehicles. The beauty lies in the pricing mechanism—toll rates increase annually based on WPI (Wholesale Price Index) inflation, providing natural hedging against rising costs. Traffic growth compounds the effect—as India's economy expands, vehicle ownership increases, industrial activity intensifies, and toll collections surge.

Take the Western UP Tollway connecting Meerut and Muzaffarnagar. This 78-kilometer stretch on National Highway 334 serves as a critical industrial corridor. Sugar mills, textile factories, and agricultural markets dot the route. During harvest season, thousands of trucks transport sugarcane and wheat. The traffic isn't glamorous, but it's predictable, essential, and growing at 6-8% annually.

The annuity projects offer a different risk-return profile. Here, Cube doesn't collect tolls directly. Instead, NHAI pays fixed semi-annual payments regardless of traffic levels. It's like converting a variable-rate mortgage into a fixed-rate one—lower upside but guaranteed returns. The single annuity project in the portfolio provides stability during economic downturns when traffic might dip.

HAM (Hybrid Annuity Model) projects blend both approaches. Cube receives 40% of project cost as construction support from NHAI and raises the remaining 60%. Post-construction, NHAI pays annuities covering debt service and equity returns. These projects offer the sweet spot—some traffic upside with downside protection through government payments.

Geographic diversification reads like an economic geography lesson. Tamil Nadu assets benefit from manufacturing and port traffic. Rajasthan roads carry marble and minerals. West Bengal corridors serve as gateways to the Northeast. Each region has different economic drivers, weather patterns, and growth trajectories, creating natural portfolio hedging.

The operational excellence isn't immediately visible but drives profitability. Electronic Toll Collection (FASTag) now accounts for 97% of transactions, reducing cash leakage and manpower costs. Weigh-in-motion systems catch overloaded vehicles, generating penalty revenue. LED lighting cuts electricity bills by 40%. Solar panels at toll plazas reduce grid dependence. Each efficiency gain drops directly to the bottom line.

Technology deployment goes beyond cost-cutting. Artificial intelligence algorithms predict traffic patterns, optimizing toll booth staffing. Drone surveillance monitors road conditions, identifying maintenance needs before they become problems. Mobile apps provide real-time traffic updates, improving customer experience and potentially increasing route preference.

The moat becomes apparent when you examine the competitive dynamics. These aren't commodity businesses anyone can enter. Concession agreements are won through competitive bidding requiring massive capital, operational expertise, and government relationships. Once operational, switching costs are infinite—you can't move a highway. Network effects emerge as Cube's scale allows centralized procurement, shared best practices, and operational synergies smaller operators can't match.

Financial performance validates the model. Revenue reached 3,523 Crores with EBITDA margins exceeding 80% for mature toll projects. These aren't software margins achieved through zero marginal costs—they're infrastructure margins achieved through operational excellence and monopolistic positioning.

The contract structures provide additional protection. Most concessions span 20-30 years with clear exit clauses. If traffic falls below projected levels, concession periods extend. Force majeure clauses protect against black swan events. Termination payments ensure capital recovery even in worst-case scenarios. It's belt-and-suspenders risk management institutionalized in legal agreements.

Revenue quality matters as much as quantity. Unlike consumer businesses facing fickle preferences, toll roads serve non-discretionary demand. People must move goods, commute to work, and travel between cities. Economic downturns might reduce traffic 5-10%, not the 50-80% collapses seen in discretionary sectors. This stability translates to predictable cash flows that debt and equity investors prize.

VI. M&A Machine: Growth Through Acquisitions

The war room at Cube's Gurgaon headquarters operates 24/7 during deal season. Multiple screens display traffic data, financial models, and legal documents. The M&A team, recruited from investment banks and infrastructure funds, evaluates dozens of opportunities monthly. But unlike typical private equity shops chasing returns through financial engineering, Cube's acquisition machine runs on operational Alpha—buying decent assets and making them great. The pattern recognition capabilities developed over years of deals created Cube's edge. In 2025, Cube signed agreements with the National Investment and Infrastructure Fund Limited (NIIF) to acquire two road assets at an enterprise value of Rs 4,184 crore. The assets—Quazigund Expressway Private Limited and Athaang Jammu Udhampur Highway Private Limited—both operate on annuity models in Jammu and Kashmir.

What others saw as remote, conflict-prone assets, Cube recognized as strategic infrastructure with government-guaranteed payments. Quazigund Expressway includes one of India's longest bi-directional tunnels, while Athaang forms an essential link between Jammu and Srinagar. The annuity structure meant zero traffic risk—NHAI pays fixed semi-annual amounts regardless of vehicle volumes. In a portfolio dominated by toll roads, these annuity assets provide countercyclical stability.

The NAM Expressway acquisition, completed in February 2025 for ₹717.60 crore, showcased Cube's ability to identify undervalued assets with strong fundamentals. This 212-kilometer stretch connecting Narketpally and Medarametla serves as the shortest route between Chennai and Hyderabad—two of South India's economic powerhouses. With 14 years of remaining concession life and established toll collection since 2014, NAM represented exactly the type of de-risked, cash-flowing asset Cube excels at optimizing.

The acquisition playbook follows a disciplined script. First, source deals through multiple channels—distressed sellers, government divestments, international funds exiting India. Second, conduct forensic due diligence—not just financial audits but physical road inspections, traffic pattern analysis, and local market studies. Third, structure creatively—using deferred payments, earn-outs, or contingent considerations to bridge valuation gaps. Fourth, integrate rapidly—standardizing systems, optimizing operations, and refinancing debt within 100 days.

The valuation discipline separates Cube from aggressive competitors. While others chase growth through overpaying, Cube walks away from 90% of opportunities. The target metrics are clear: acquire at 7-9x EV/EBITDA, optimize to achieve 10-12x exit multiples, generate 15-18% project IRRs. This isn't about finding hidden gems—it's about paying fair prices for good assets and creating value through operational improvements.

Deal sourcing leverages Cube's unique position. As India's largest toll road operator, Cube becomes the natural buyer for various seller types. Distressed developers need quick exits—Cube provides certainty of closure. International funds face redemption pressure—Cube offers liquidity. Government wants to monetize assets—Cube has the balance sheet and track record. This positioning creates a proprietary deal flow competitors can't replicate.

The ROFO (Right of First Offer) pipeline strategy adds another dimension. When I Squared or other sponsors acquire assets not immediately suitable for the InvIT, Cube gets first rights when they mature. This creates a captive pipeline of future acquisitions at pre-negotiated terms. It's like having options on infrastructure assets—minimal capital commitment today, guaranteed access tomorrow.

Integration excellence drives post-acquisition value creation. Within weeks of closing, Cube teams descend on newly acquired assets. Toll collection systems get upgraded to latest technology. Maintenance contracts are renegotiated using Cube's scale. Insurance premiums drop through portfolio policies. Working capital cycles improve through centralized cash management. Each improvement might seem minor—saving 50 basis points here, improving efficiency 2% there—but collectively they transform returns.

The M&A machine's efficiency shows in the numbers. Cube Highways has been the most active investor in the Indian roads sector, completing 13 acquisitions in just 12 months during one period. Yet despite this pace, the portfolio maintains operational excellence with 98% toll collection efficiency and industry-leading safety records.

VII. Capital Markets & Financial Engineering

The Treasury office at Cube's Mumbai headquarters resembles a sophisticated trading floor more than a traditional corporate finance department. Multiple screens track bond yields, currency movements, and interest rate curves. The team, recruited from investment banks and debt capital markets, manages a complex web of financing structures that would make most CFOs dizzy. But this complexity serves a purpose—optimizing every basis point of funding cost directly impacts distribution yields. The February 2025 sustainability-linked bond (SLB) issuance marked a watershed moment—not just for Cube but for Indian infrastructure financing. IFC invested ₹860 crore (~$98.35 million) in India's first sustainability-linked bond (SLB) in the road sector, issued by Cube Highways Trust, which will fund the acquisition of NAM Expressway Limited (NAM), a strategic highway connecting Chennai and Hyderabad, and support Cube Highways Trust's long-term corporate objectives, including sustainability and inclusion initiatives.

The innovation lay in the structure. Unlike traditional bonds where interest rates remain fixed, SLBs link pricing to sustainability performance targets. If Cube achieves predetermined ESG goals—reducing carbon emissions, improving safety metrics, increasing local employment—interest rates decrease. Miss the targets, and rates increase. It's financial engineering with a conscience, aligning investor returns with societal outcomes.

Pankaj Vasani, Group CFO of Cube InvIT, said, "This milestone strengthens Cube InvIT's leadership in sustainable infrastructure finance, making it one of the first highway InvITs to integrate sustainability into its funding strategy. This financing marks the first in a series of SLBs that Cube InvIT intends to issue, which aim to drive the transformation of India's highway infrastructure while upholding the highest environmental, social, and governance standards."

The debt optimization journey showcases sophisticated treasury management. In April 2025, Cube Highways Trust raised ₹1,152 crore via the issuance of AAA-rated non-convertible debentures (NCDs) across two tenures – three-year and seven-year. The three-year series was raised at a coupon of 7.25 per cent with a premium over face value and a subscription of approximately 2.6 times the offer for refinancing of the existing rupee loan.

The oversubscription demonstrates investor appetite. In a market where government bonds yield 6-7%, Cube's 7.25-7.30% coupons offered attractive spreads for minimal incremental risk. The AAA rating—highest possible for an Indian corporate—meant insurance companies and pension funds could invest without regulatory constraints.

Distribution policy forms the cornerstone of investor appeal. InvIT regulations require distributing 90% of distributable cash flows to unit holders. But Cube goes further, maintaining consistent quarterly distributions even during volatile periods. The predictability matters more than magnitude—investors can model cash flows with confidence.

The capital structure optimization reflects textbook financial theory applied to infrastructure reality. Project-level debt at individual SPVs gets refinanced at InvIT level, reducing rates by 150-200 basis points. Short-term working capital facilities smooth cash flow timing mismatches. Long-term bonds match asset lives, eliminating refinancing risk. Currency hedging protects against rupee volatility for foreign investors.

Managing leverage requires delicate balancing. Too little debt leaves returns on the table; too much creates refinancing risk. Cube targets 60-70% debt-to-enterprise value, providing headroom for acquisitions while maintaining investment-grade ratings. The debt service coverage ratio exceeds 1.5x even in stress scenarios, ensuring distribution sustainability.

The InvIT structure provides unique advantages over traditional corporate structures. Pass-through taxation eliminates double taxation—the trust pays no tax if it distributes 90% of income. Investors pay tax only on distributions received, at their applicable rates. For foreign investors, the 5% withholding tax on distributions beats the 20% dividend distribution tax on regular companies.

Refinancing strategies demonstrate continuous optimization. As assets mature and traffic patterns stabilize, risk profiles improve, enabling lower-cost debt. Cube systematically refinances high-cost acquisition debt with cheaper long-term bonds. The April 2025 NCD issuance refinanced existing loans, reducing interest costs by 75-100 basis points.

The innovation extends beyond traditional debt markets. Green bonds fund solar installations at toll plazas. Social bonds support community development along highway corridors. Masala bonds tap overseas Indian rupee markets. Each instrument diversifies funding sources while potentially lowering costs.

VIII. India's Infrastructure Story & Market Dynamics

Standing on the newly inaugurated Eastern Peripheral Expressway, you witness India's infrastructure transformation in real-time. Eight-lane highways where bullock cart tracks existed a decade ago. Electronic toll collection replacing manual booths. GPS-tracked construction progress versus the paper-based systems of yesteryear. This isn't just about roads—it's about a nation reimagining its economic geography through concrete and asphalt.

India's infrastructure deficit remains staggering despite recent progress. The country needs $1.5 trillion in infrastructure investment through 2030 to sustain 7-8% GDP growth. Roads alone require $500 billion. Traditional funding sources—government budgets and bank loans—can provide perhaps half. The gap represents both challenge and opportunity, explaining why global infrastructure funds circle India like hawks.

The National Highways Authority of India (NHAI) stands at this transformation's center. From constructing 12 kilometers of highways daily in 2014 to 40 kilometers in 2024, NHAI has engineered one of history's largest infrastructure buildouts. The Bharatmala Pariyojana program alone targets 83,677 kilometers of highway development with ₹10 lakh crore investment. The PPP (Public-Private Partnership) evolution tells the story of India's infrastructure financing innovation. From the early BOT (Build-Operate-Transfer) model where private players took both construction and traffic risk, to HAM (Hybrid Annuity Model) where government shares 40% of project cost, to TOT (Toll-Operate-Transfer) where operational assets are monetized—each iteration reflected learning from past failures and market feedback.

MoRTH managed to complete 12,349 km of national highways in 2023-24, up from 10,993 km the previous year. The construction of national highways in India has increased steadily over the past decade, growing 1.6 times from 91,287 km in 2014 to 146,145 km in 2023. The quality of the highway network has also improved, with four-lane national highways increasing 2.5 times, from 18,387 km in 2014 to 46,179 km in 2023.

The traffic growth story underpins everything. Vehicle ownership in India stands at just 22 per 1,000 people versus 980 in the US or 850 in Europe. As incomes rise, this gap will narrow dramatically. E-commerce explosion drives freight traffic—every Amazon delivery, every Flipkart package traverses these highways. The shift from railways to roads for time-sensitive cargo adds another growth vector.

Competition has intensified but remains rational. Other InvITs like IRB InvIT, India Grid Trust, and the newly launched National Highways InvIT compete for assets. Private players like IRB Infrastructure, Ashoka Buildcon, and PNC Infratech bid aggressively for new projects. International funds from Canada Pension Plan to Singapore's GIC scout for opportunities. Yet the market remains undersupplied—there are more buyers than quality assets available.

The regulatory environment has steadily improved. SEBI's InvIT regulations provide clear frameworks for governance, distributions, and investor protection. NHAI has standardized concession agreements, reducing negotiation friction. Dispute resolution through arbitration has become faster and more predictable. The government's commitment to honoring contracts, even through political transitions, has built investor confidence.

A pipeline of 33 projects, totalling 2,700 km and valued at Rs 600 billion according to ICRA, has been identified for monetisation in 2024-25. These projects will be monetised through a combination of NHAI's InvIT and the TOT model, offering significant opportunities for investment and development.

Policy tailwinds continue strengthening. In 2024, the government of India presented an ambitious 'Vision 2047' plan envisioning the construction of up to 50,000 km (31,000 mi) of access-controlled highways and expressways, with Indians gaining access to the expressways at a distance of 100–125 km (62–78 mi) from any point in the country. The infrastructure push isn't just about roads—it's about economic transformation.

Electronic toll collection through FASTag has revolutionized the sector. From near-zero penetration in 2016 to 97% today, FASTag has eliminated toll plaza queues, reduced leakage, and improved user experience. The data generated—vehicle types, travel patterns, peak hours—enables sophisticated traffic management and revenue optimization.

The financing ecosystem has matured remarkably. Banks understand highway projects better, offering longer tenors and competitive rates. Bond markets provide alternatives to bank funding. InvITs create permanent capital vehicles. International funds bring patient capital. This financing depth ensures projects don't stall for lack of funding—a common problem a decade ago.

GDP correlation remains the fundamental driver. Every 1% GDP growth typically translates to 1.5-2% traffic growth on highways. With India targeting 7-8% GDP growth through 2030, highway traffic could compound at 10-12% annually. Layer in inflation-linked toll increases, and revenue growth becomes compelling.

Yet challenges persist. Land acquisition remains contentious despite the Right to Fair Compensation Act. Environmental clearances can delay projects. Local political pressures sometimes prevent toll rate increases. Construction cost inflation—steel, cement, bitumen—squeezes margins. These aren't existential threats but operational realities requiring active management.

IX. Playbook: Infrastructure Investment Lessons

The conference room at I Squared's Miami headquarters displays a simple framework on the whiteboard: "Platform > Projects, Operations > Financial Engineering, Patient > Quick." This philosophy, refined through decades of infrastructure investing across continents, drives every Cube Highways decision. The lessons learned offer a masterclass in infrastructure investing applicable far beyond Indian toll roads.

Platform versus asset-by-asset approach represents the fundamental strategic choice. Most infrastructure investors chase individual projects—win a road here, a port there, maybe a power plant somewhere else. Cube chose differently. Build a platform first—management team, operational systems, financing relationships—then acquire assets that fit the platform. The upfront investment seems inefficient, but the long-term advantages are overwhelming.

Consider the counterfactual. Without a platform, each acquisition requires assembling teams, negotiating financing, building systems from scratch. Transaction costs explode. Operational synergies vanish. Knowledge doesn't transfer between assets. You're essentially starting over each time. The platform approach inverts this—each new asset slots into existing infrastructure, immediately benefiting from accumulated expertise.

Operational excellence matters more than financial engineering in infrastructure. Wall Street types often miss this. You can't Excel-model your way to success when dealing with physical assets exposed to weather, requiring maintenance, serving real customers. Cube's operational innovations—predictive maintenance algorithms, centralized procurement, standardized training programs—create more value than any clever financing structure.

The numbers prove the point. Reducing toll leakage from 6% to 2% through better collection systems adds more to returns than shaving 50 basis points off interest rates. Extending road surface life by two years through superior maintenance dwarfs the impact of optimizing the debt-equity ratio. Operations drive returns; finance just enables them.

Capital recycling strategies separate sophisticated infrastructure investors from asset hoarders. The temptation is to hold assets forever—after all, they generate steady cash flows. But intelligent recycling—selling mature assets at peak multiples to fund new acquisitions at lower multiples—accelerates value creation. Cube's InvIT structure facilitates this, allowing partial exits while maintaining operational control.

Managing government relationships requires delicate balance. Infrastructure assets inherently involve government—as regulators, counterparties, sometimes competitors. The naive approach involves either confrontation (asserting rights aggressively) or capitulation (accepting whatever government demands). Cube's approach is nuanced: firm on principles, flexible on details, always maintaining dialogue.

This manifests in practical ways. When toll rate increases lag inflation, Cube doesn't immediately rush to arbitration. Instead, they document the shortfall, engage in discussions, and often receive compensating benefits—extended concession periods, relaxed performance obligations, or preferential treatment in future bids. The relationship is repeated game, not one-shot interaction.

ESG integration has evolved from nice-to-have to must-have. The sustainability-linked bond isn't just clever marketing—it reflects fundamental business reality. Better environmental practices reduce costs (solar power, LED lighting). Strong social engagement prevents project delays from local protests. Good governance attracts institutional capital. ESG creates value, not just good PR.

The safety record illustrates this. Cube's accident rates are 40% below industry average. This isn't charity—fewer accidents mean less downtime, lower insurance premiums, better relationships with regulators. Every accident prevented saves money while saving lives. Doing good and doing well align perfectly.

Why infrastructure is becoming financialized globally reflects deeper economic trends. Negative real rates in developed markets push investors toward real assets. Aging populations need steady income streams that pensions once provided. Governments lack fiscal capacity for infrastructure investment. Technology enables remote monitoring and management. These forces converge to transform infrastructure from government domain to investment asset class.

India represents the vanguard of this transformation. What InvITs accomplish in India, similar structures will achieve elsewhere. The playbook transfers—identify quality operating assets, consolidate fragmented ownership, professionalize operations, package for institutional investors, distribute stable yields. Replace "Indian toll roads" with "Brazilian airports" or "Indonesian ports"—the formula remains valid.

Risk management in infrastructure differs fundamentally from financial assets. Market risk barely exists—people don't stop driving because stock markets crash. Credit risk is minimal with government counterparties. The real risks are operational—maintenance failures, accidents, technology obsolescence. Cube's risk framework focuses on these practical challenges rather than elaborate financial models.

The insurance approach exemplifies this. Rather than just buying standard policies, Cube works with insurers to reduce premiums through safety improvements. Installing better lighting reduces nighttime accidents. Regular road surface monitoring prevents deterioration. Driver education programs at toll plazas improve behavior. Lower risk means lower premiums means higher returns.

Technology adoption in traditional infrastructure seems contradictory but proves transformative. Cube deploys drones for road inspection, AI for traffic prediction, IoT sensors for infrastructure monitoring. These aren't gimmicks—they reduce costs, improve safety, and enhance customer experience. The future of infrastructure isn't just concrete and steel but also silicon and software.

The human capital strategy often gets overlooked but drives everything else. Cube recruits from IITs for engineering talent, IIMs for management expertise, and Big Four firms for financial acumen. But crucially, they also promote from within—the toll plaza supervisor who becomes regional manager, the maintenance engineer who leads operations. This blend of external expertise and internal knowledge creates sustainable competitive advantage.

X. Analysis & Investment Case

The Excel model sprawled across two monitors tells a compelling story: ₹17,822 crore market capitalization, ₹3,523 crore revenue, 80%+ EBITDA margins, 10%+ distribution yields. But numbers alone don't capture the investment case. Understanding Cube Highways Trust requires examining the intersection of India's infrastructure ambitions, global capital seeking yield, and operational excellence creating value where others see commodity assets.

The unit performance since listing reflects market recognition of the model's durability. While tech stocks gyrate wildly and banks face credit cycles, Cube units trade in a narrow band around NAV, with volatility coming mainly from distribution announcements. This isn't exciting for momentum traders but perfect for institutions seeking bond-like returns with equity upside.

Competitive positioning versus other InvITs reveals Cube's advantages. Scale matters—at 25 assets, Cube achieves operational efficiencies smaller trusts can't match. Sponsor quality differentiates—I Squared's global platform provides access to capital and expertise purely domestic sponsors lack. Asset quality distinguishes—Cube's portfolio of operational roads eliminates construction risk that haunts competitors with under-construction assets.

Growth drivers stack up impressively. India's infrastructure spending targets ₹111 lakh crore through 2025. Traffic growth compounds at 6-8% annually. Toll rates increase with inflation. New monetization opportunities emerge as government seeks to recycle capital. M&A pipeline remains robust with distressed sellers and government divestments. Each driver independently justifies optimism; together they create compelling momentum.

The bull case writes itself: India's decade of infrastructure has arrived. GDP growth, urbanization, and rising incomes drive traffic growth. Government commitment to infrastructure remains unwavering across political parties. Global investors desperately seek yield in zero-rate environments. InvITs provide the perfect vehicle—liquid, regulated, tax-efficient. Cube sits at the intersection of these megatrends.

Imagine India in 2030: GDP doubled to $7 trillion, vehicle ownership up 50%, e-commerce penetration tripled. Every trend drives highway traffic higher. Meanwhile, government fiscal constraints mean private capital must fund infrastructure expansion. InvITs become the primary financing vehicle. Cube, with first-mover advantage and operational excellence, captures disproportionate value.

The distribution sustainability looks solid. Current yields of 10%+ seem high, but coverage ratios exceed 1.2x. As debt gets refinanced at lower rates and traffic grows, distributions could increase while maintaining prudent coverage. The InvIT structure's tax efficiency means most returns come as tax-advantaged distributions rather than capital gains.

Yet the bear case deserves consideration. Leverage, while manageable at 60-70% of enterprise value, amplifies risks. Interest rate increases directly impact refinancing costs and distribution capacity. Traffic volatility—from economic slowdowns, fuel price spikes, or black swan events like COVID—can pressure revenues. Regulatory changes, while unlikely, could alter economics fundamentally.

Execution risks multiply with scale. Each acquisition integration challenges operations. Maintenance backlogs can emerge if capital allocation tilts too heavily toward growth. Key person dependencies—if senior management departs—could disrupt the platform. Technology disruption, perhaps from autonomous vehicles changing traffic patterns, represents a long-term wildcard.

Competition intensifies as success attracts imitators. New InvITs launch monthly, chasing the same assets. Private equity funds raise India-dedicated infrastructure vehicles. Sovereign wealth funds establish direct presence rather than investing through intermediaries. Asset prices inflate as buyers multiply faster than sellers.

The interest rate sensitivity requires careful analysis. Every 100 basis point rate increase impacts distributions by approximately 8-10%. In a rising rate environment, yields must increase to maintain attractiveness versus fixed income alternatives. While inflation-linked toll increases provide some hedge, the impact lag creates temporary pressure.

Regulatory risks, while manageable, persist. Populist pressures could prevent toll increases. Environmental regulations might require expensive retrofitting. Changes to InvIT regulations could alter distribution requirements or tax treatment. While India's track record suggests stability, infrastructure's political sensitivity creates tail risks.

The ESG considerations increasingly influence institutional allocations. Cube's sustainability initiatives—solar installations, safety improvements, community development—position it well. But infrastructure inherently involves environmental trade-offs. Roads enable development but increase emissions. Balancing these tensions while maintaining returns challenges management.

Valuation frameworks vary by investor type. Yield investors focus on distribution sustainability and growth. Growth investors emphasize traffic increases and M&A potential. Value investors analyze NAV discounts and asset replacement costs. Each framework suggests different entry points and return expectations.

The comparable analysis spans geographies and asset classes. Versus global toll road operators like Transurban or Atlantia, Cube offers higher growth at lower multiples. Versus Indian infrastructure companies, Cube provides superior corporate governance and capital access. Versus fixed income, Cube delivers higher yields with inflation protection. The relative value appears compelling across comparisons.

XI. Future Vision & Closing Thoughts

The helicopter hovers over the under-construction Delhi-Mumbai Expressway, eight lanes of pristine asphalt cutting through the Aravalli hills. Below, thousands of workers and hundreds of machines push India's infrastructure ambitions forward, kilometer by kilometer. This scene, replicated across thousands of construction sites, represents not just Cube Highways' future but India's economic transformation through infrastructure.

Expansion beyond highways beckons inevitably. The infrastructure platform Cube has built—operational expertise, financing relationships, regulatory know-how—transfers naturally to adjacent sectors. Airports share similar characteristics: long-term concessions, regulated returns, and essential service nature. Ports offer comparable economics with additional growth from India's manufacturing ambitions. Power transmission provides stable, contracted cash flows. Each sector leverages Cube's core competencies while diversifying risk.

The conversations in Cube's boardroom increasingly focus on these opportunities. Not whether to expand beyond roads, but when and how. The playbook seems clear: identify a distressed or undervalued asset in an adjacent sector, acquire it at reasonable multiples, apply operational excellence, then build sector scale through follow-on acquisitions. It worked for highways; why not replicate elsewhere?

Technology and digitalization of toll collection represent the immediate frontier. While FASTag revolutionized payments, the next wave promises more radical transformation. Satellite-based tolling eliminates physical toll plazas entirely—vehicles are tracked via GPS, and tolls are deducted automatically based on distance traveled. Dynamic pricing adjusts rates based on congestion, time of day, and vehicle type. Blockchain-based systems enable seamless inter-operator settlements.

These aren't futuristic fantasies but near-term realities. NHAI has announced satellite tolling pilots on select corridors. Cube's technology team collaborates with global vendors developing these systems. Early adoption provides competitive advantages—lower operating costs, better customer experience, richer data analytics. The companies that master technology-enabled infrastructure will dominate the next decade.

International expansion possibilities intrigue but require careful consideration. I Squared's global footprint provides natural entry points—portfolio companies needing Indian expertise, cross-border infrastructure corridors, and regional platforms seeking consolidation. The ASEAN markets, with similar development trajectories and infrastructure needs, offer logical expansion territories.

Yet international expansion isn't inevitable or necessarily desirable. Cube's competitive advantages—local relationships, regulatory expertise, operational knowledge—don't automatically transfer across borders. The failed international ventures of many Indian infrastructure companies provide cautionary tales. If Cube expands internationally, it will likely follow I Squared's existing investments rather than venturing independently.

The role of InvITs in India's infrastructure financing has evolved from experiment to essential. The government now views InvITs as the primary vehicle for infrastructure monetization. Private developers structure projects anticipating eventual InvIT exits. International investors allocate to India through InvIT vehicles. What began as financial innovation has become market infrastructure.

This transformation accelerates as success breeds success. Each successful InvIT listing encourages others. Rising valuations incentivize asset owners to pursue InvIT routes. Deepening secondary markets provide liquidity previously absent. Regulatory refinements address initial shortcomings. The virtuous cycle strengthens with each iteration.

Key takeaways for investors and operators crystallize from Cube's journey. First, infrastructure investing requires operational excellence, not just financial engineering. Second, platform approaches beat project-by-project strategies over time. Third, patient capital aligned with long-term value creation outperforms quick-flip approaches. Fourth, government relationships matter but shouldn't dominate strategy. Fifth, ESG integration creates value, not just compliance checkboxes.

For operators, the lessons are equally clear. Professional management beats founder-led operations in institutional markets. Transparent governance attracts premium valuations. Technology adoption drives efficiency gains financial engineering can't match. Scale matters but focus matters more—better to dominate one sector than dabble in many.

What this means for infrastructure investing globally extends beyond India's borders. The InvIT model pioneered in India will spread to other emerging markets seeking infrastructure financing solutions. The operational excellence standards Cube established will become table stakes globally. The marriage of infrastructure and capital markets, once unthinkable, will become standard.

Consider the broader implications. If India successfully finances its infrastructure needs through InvIT-type vehicles, it provides a template for Africa, Southeast Asia, and Latin America. If operational excellence can transform "boring" toll roads into attractive investments, imagine the possibilities for other essential infrastructure. If global capital can be efficiently channeled into emerging market infrastructure, development accelerates worldwide.

The transformation won't be smooth or linear. Setbacks will occur—failed projects, regulatory reversals, market corrections. Some InvITs will underperform or fail entirely. Competition will compress returns. Technology disruption will challenge existing models. These are features, not bugs, of market evolution.

Yet the fundamental drivers remain compelling. The world needs $100 trillion in infrastructure investment through 2040. Governments can fund perhaps one-third. Private capital must bridge the gap. Vehicles like Cube Highways Trust that efficiently connect capital with infrastructure needs will thrive. The companies that master this connection will shape the next generation of global infrastructure.

Standing at toll plaza #27 on the Mumbai-Pune Expressway as the sun sets, watching the endless stream of vehicles, one thing becomes clear: this isn't just about toll collection or investment returns. It's about enabling economic growth, connecting communities, and building the physical foundations of prosperity. Cube Highways Trust, for all its financial sophistication, ultimately succeeds by fulfilling this basic promise—turning savings into infrastructure, infrastructure into growth, and growth into returns.

The story that began in a Singapore boardroom with former Wall Street bankers studying Indian maps has become something larger—a blueprint for infrastructure transformation applicable from Mumbai to Manila, from Delhi to Dhaka. The next decade will test whether this model can scale, replicate, and evolve. Based on the evidence so far, bet on the builders.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube