Indian Overseas Bank: The Story of India's International Banking Pioneer

I. Introduction & Episode Roadmap

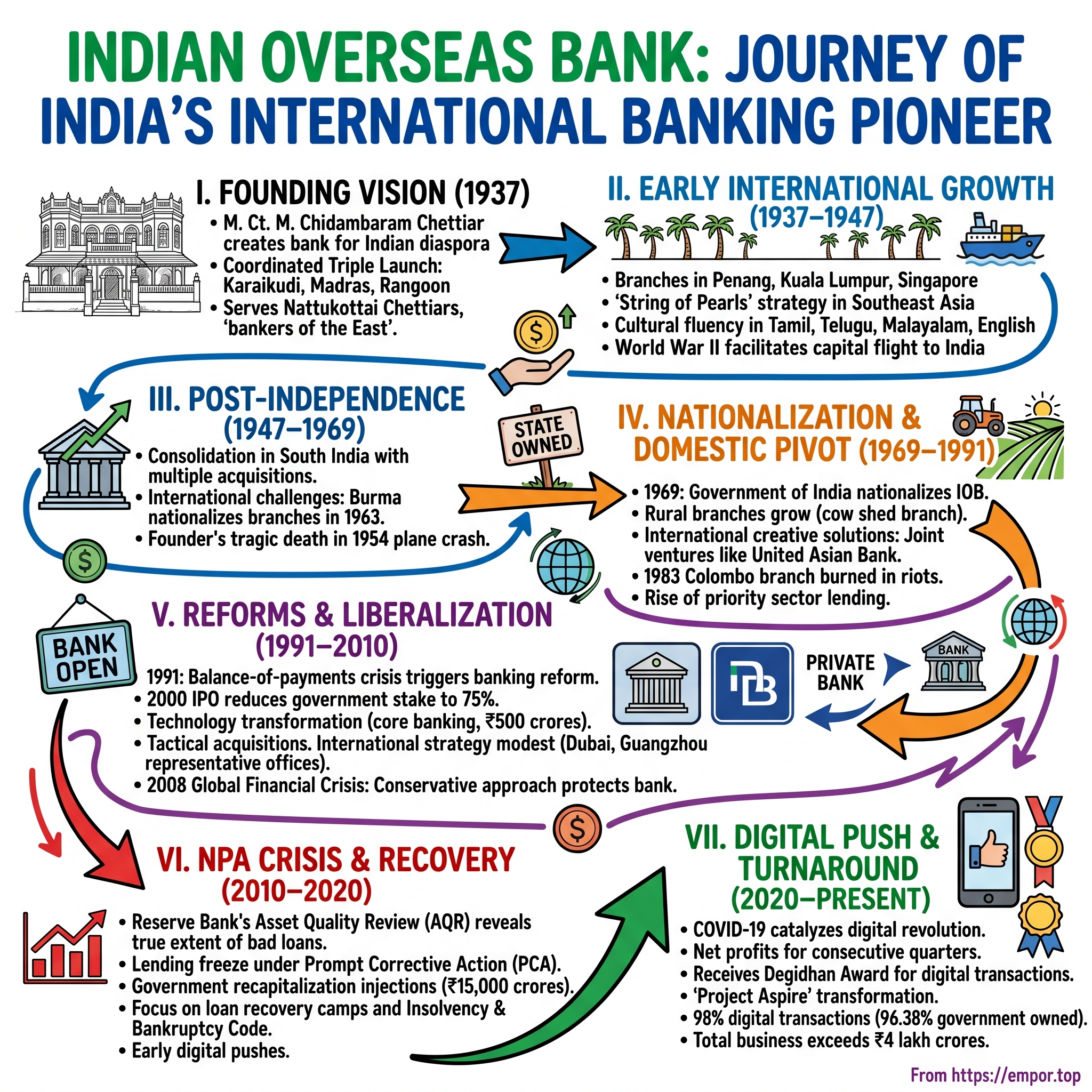

Picture this: It's 1937 in the dusty town of Karaikudi, deep in the Chettinad region of Tamil Nadu. While the world inches toward war and India struggles under colonial rule, a 29-year-old businessman named M. Ct. M. Chidambaram Chettiar is signing papers to launch a bank. Not just any bank—one designed to follow Indian merchants wherever they sailed, from the rubber plantations of Malaya to the rice mills of Rangoon. On that same day, two other branches open simultaneously: one in cosmopolitan Madras, another in bustling Rangoon. This coordinated triple launch wasn't just ambitious; it was unprecedented in Indian banking history.

Fast forward to today: Indian Overseas Bank commands a market capitalization of ₹68,958 crores, manages total business exceeding ₹4 lakh crores, and operates over 3,200 branches. The bank that once pioneered international banking for Indians abroad has morphed into something entirely different—a government-owned behemoth where 96.38% of shares rest with the Indian state. Last quarter alone, IOB posted a net profit of ₹1,111 crores, with digital transactions hitting 98% of total volume.

The central question we're exploring: How did a bank founded to serve Indian merchants in Southeast Asia's bustling ports transform into a domestically-focused public sector bank? And perhaps more intriguingly—after nationalization, crises, recoveries, and digital transformation—does IOB still carry the DNA of its international pioneering spirit?

This is a story of three distinct acts: the Chettiar dynasty's banking vision that connected Indian merchants across Asia, the dramatic pivot forced by nationalization in 1969, and the modern struggle to balance government ownership with competitive banking. Along the way, we'll encounter plane crashes that changed ownership structures, ethnic riots that burned branches, and digital transformations that would make the founder dizzy. We'll trace how a bank with ₹1 million in starting capital grew to manage assets worth ₹3.5 lakh crores, why it hasn't paid dividends despite years of profits, and what its 19% profit CAGR over five years really means for investors.

The narrative ahead isn't just banking history—it's the story of Indian capitalism itself, told through one institution's journey from private entrepreneurship to state control to potential renaissance.

II. The Chettiar Legacy & Founding Vision (1937)

The Chettinad mansion on Kanadukathan's main street stood resplendent in the morning heat, its Burma teak columns gleaming against Italian marble floors. Inside, young Chidambaram sat across from his uncle Ramaswami—founder of Indian Bank—studying ledgers written in Tamil script that tracked remittances from Rangoon to Karaikudi. Chidambaram was born at Kanadukathan on 2 August 1908, and was a nephew of Ramaswami Chettiar, founder of the Indian Bank. The year was 1930, and the 22-year-old had just taken his father's seat on Indian Bank's board following Sir M Ct. Muthiah Chettiar's death in 1929, with Chidambaram succeeding his father as a director of the Indian Bank.

But Chidambaram's vision extended beyond his uncle's creation. While Indian Bank served domestic needs, he watched his community—the Nattukottai Chettiars, who were a mercantile class that at the time had spread from Chettinad in Tamil Nadu state to Ceylon, Burma, Malaya, Singapore, Java, Sumatra, and Saigon—struggle with currency exchanges and international settlements. The Nattukottai Chettiars had established a sophisticated banking system, introducing financial instruments like the hundi (promissory note) and developing credit networks that extended from colonial India to Burma, Malaysia, and Singapore, earning them a reputation as the "bankers of the East" during the British Raj.

The Chettiar banking network was extraordinary but informal—based on trust, kinship, and hundis that moved millions across borders without a single institution to coordinate it all. By the late 19th century, the Chettiars were an extremely influential and wealthy community, with monopolistic power in the money lending business and natural entrepreneurial skills. They had financed much of Sri Lanka's transition from coffee to tea and rubber plantations by lending to local entrepreneurs, yet operated through individual family firms rather than consolidated banks.

Chidambaram wasn't just another merchant's son playing at banking. He was one of the founders of United India Assurance and in 1944 founded the Travancore Rayons Limited with a factory near Perumbavoor—India's first rayon manufacturing company. His entrepreneurial instincts told him that Indian merchants needed their own international bank, not as middlemen for British institutions, but as principals in their own right.

On February 10, 1937, at age 29, Chidambaram executed an audacious plan: he established the Indian Overseas Bank to encourage overseas banking and foreign exchange operations, with IOB starting up simultaneously at three branches, one each in Karaikudi, Madras, and Rangoon. The synchronized triple launch—unprecedented in Indian banking—signaled serious intent. Within months, the bank quickly opened branches in Penang, Kuala Lumpur (1937 or 1938), and Singapore (1937 or 1941).

The timing was prescient. The late 1930s saw the Chettiar community at its zenith—they rose to the peak of their power in the late 19th and early 20th centuries, and between 1850 and the end of World War II built over 10,000 lavish mansions in the region. IOB positioned itself as the institutional backbone for this sprawling commercial empire, offering something revolutionary: modern banking infrastructure married to traditional Chettiar trust networks.

What made IOB unique wasn't just its international footprint but its DNA. Unlike British exchange banks that treated Indians as subjects, or domestic banks that feared overseas ventures, IOB was built by and for the Indian diaspora. It was the bank that put the country's name on the map of banking in the Far East, lending assistance to hundreds of thousands of Indians. The bank understood the remittance patterns of textile merchants in Singapore, the seasonal cash needs of rubber planters in Malaya, and the complex web of family partnerships that moved capital across borders.

Chidambaram's broader business philosophy reflected in IOB's structure—this wasn't narrow ethnic banking but sophisticated international finance. His experience across industries—from insurance to synthetic fibers—informed a vision of IOB as more than a money-transfer mechanism. It would be a development bank for the Indian diaspora, financing trade, enabling currency arbitrage, and eventually funding industrialization.

The tragedy that would reshape IOB's destiny came suddenly. On 13 March 1954, Chidambaram died when the British Overseas Airways flight he was travelling on crashed at Kallang Airport, Singapore, killing 33 people out of 40 passengers and crew on board. At 45, the founder who had built IOB into an international presence was gone, leaving behind an institution that would soon face its greatest transformation: nationalization.

But in 1937, none of that was foreseeable. What mattered was that a young industrialist had recognized a gap in global finance and filled it with remarkable speed and ambition. IOB wasn't just another bank—it was the institutional expression of a centuries-old mercantile tradition, modernized for the twentieth century. The Chettiar boy from Kanadukathan had created something that would outlive him, though in forms he could never have imagined.

III. Pre-Independence International Expansion (1937–1947)

The telegram from Rangoon arrived at IOB's Karaikudi headquarters in late 1937: "Burma operations exceeding projections STOP Request additional capital allocation STOP." Within months of opening, the Rangoon branch had become IOB's crown jewel, processing more foreign exchange than Madras and Karaikudi combined. The reason was simple geography meeting destiny—Rangoon was where the Chettiar diaspora's money moved fastest.

By 1938, IOB had executed what modern strategists would call a "string of pearls" strategy across British Malaya and the Straits Settlements. The Penang branch opened to serve the island's thriving Chettiar community who controlled much of the region's pawnbroking and agricultural lending. Kuala Lumpur followed, tapping into tin mining finance and rubber plantation loans. Singapore's branch, opening between 1937 and 1941, positioned IOB at the nexus of Southeast Asian trade.

Each branch opening followed a pattern: Chidambaram would arrive with senior managers, meet local Chettiar leaders at their guild halls, and demonstrate IOB's foreign exchange capabilities with live transactions to India. The message was clear—no more waiting weeks for hundis to clear through informal networks. IOB could move money in days, legally, with full documentation that satisfied both British colonial authorities and Indian tax officials.

The numbers tell a remarkable story. Starting with capital of just ₹1 million in 1937, IOB's deposits grew to ₹8 million by 1940, with 70% coming from overseas branches. The bank pioneered what it called "nostro-vostro" accounts—reciprocal arrangements with international banks that allowed seamless currency conversion. A rubber planter in Malaya could deposit Straits dollars and have rupees credited to his family's account in Chettinad within 72 hours.

What distinguished IOB from British exchange banks wasn't just speed but cultural fluency. Branch managers spoke Tamil, Telugu, and Malayalam alongside English. They understood the Islamic banking needs of Mappila merchants in Singapore. They knew when Deepavali remittances would spike and pre-positioned currency accordingly. This wasn't colonial banking imposed from above but indigenous finance scaling up from below.

The competitive landscape was surprisingly thin. British banks like Chartered and Mercantile focused on large corporate accounts and government finance. Chinese banks served their own diaspora networks. Indian Bank, despite its earlier start, remained largely domestic. IOB found white space in the middle market—the thousands of Indian merchants, contractors, and professionals who were too small for Chartered Bank but too sophisticated for informal moneylenders.

Consider the typical IOB client circa 1940: a Chettiar merchant with a provision shop in Kuala Lumpur, importing rice from Burma and textiles from India, extending credit to local Malay farmers, and remitting profits back to Karaikudi to buy land. This merchant needed working capital loans, trade finance, foreign exchange hedging, and wealth management—a full spectrum of banking services that only IOB could provide in Tamil with terms he understood.

The bank's foreign exchange innovations deserve special attention. IOB introduced the "Chettiar draft"—a negotiable instrument that functioned like a modern letter of credit but relied on community trust networks for enforcement. If a merchant in Rangoon issued a draft drawn on IOB Singapore, the receiving party knew it was as good as gold. The bank's reputation became intertwined with the Chettiar community's commercial honor.

World War II's approach brought unexpected opportunities. As political tensions rose in 1940-41, capital flight from Burma and Malaya accelerated. Wealthy Indians wanted their money safely in India before the Japanese arrived. IOB processed record volumes, earning substantial fees while helping its community preserve wealth. The Singapore branch reportedly worked through the night in December 1941, processing last-minute transfers before the Japanese invasion.

The bank also pioneered trade finance innovations that seem obvious now but were revolutionary then. IOB created standardized contracts for common transactions—copra shipments from Ceylon, rubber from Malaya, rice from Burma—with pre-negotiated terms that reduced transaction costs. A merchant could walk into any IOB branch with a standard shipment and receive financing within hours, not days.

Employee development followed a distinctive pattern. Young men from Chettiar families would join as clerks in Karaikudi, train for six months, then ship out to an overseas branch to learn international banking by doing. This created a cadre of managers who understood both traditional Chettiar business practices and modern banking regulations—bicultural professionals before the term existed.

By 1945, with the war ending, IOB faced a crossroads. The bank had survived the conflict with most assets intact, though the Rangoon branches were damaged and Singapore operations disrupted. More fundamentally, the political landscape was shifting. Burma and Ceylon were moving toward independence. Malaya was restive. The age of empire that had enabled IOB's international expansion was ending.

The numbers at independence were impressive: 20 branches across six countries, deposits of ₹25 million, and a reputation as South Asia's premier diaspora bank. IOB had achieved what Chidambaram envisioned—putting Indian banking on the international map. But the map itself was about to be redrawn, and IOB would need to navigate the transition from colonial to post-colonial banking while maintaining its international character.

IV. Post-Independence Growth & Domestic Consolidation (1947–1969)

The morning of August 15, 1947, found IOB's senior management huddled in their Madras headquarters, studying maps with new borders. Pakistan had been carved out, Burma was independent, Ceylon would follow in 1948. The bank that had built its reputation on seamless cross-border operations suddenly faced a world of nation-states, each with its own currency controls, banking regulations, and political sensitivities.

Chidambaram's response was characteristically bold: if the world was fragmenting, IOB would consolidate. Between 1960 and 1967, the bank engineered a remarkable series of acquisitions that would transform it from an international niche player into a formidable domestic force. The strategy was clear—buy struggling local banks, absorb their branch networks, and create density in South India while maintaining international operations.

The acquisition spree began with Coimbatore Standard Bank in 1963, followed by Nanjinnad Bank and Coimbatore Vasunthara Bank (established June 1924) in 1964. Each target was carefully chosen: regional banks with loyal customer bases but weak capital positions, often family-owned institutions that couldn't meet new Reserve Bank regulations. IOB offered their owners face-saving exits and their employees job security.

Kulitalai Bank, established in 1933 with six branches, joined in 1964, followed by Srinivasa Perumal Bank (established November 1935 at Coimbatore) in 1966. The crown jewel came in 1967 with Venkateswara Bank, established in June 1931 as Salem Shevapet Sri Venkateswara Bank, with two branches in Salem. In seven years, IOB had absorbed seven banks and added nearly 30 branches to its network.

The integration challenges were immense. Each acquired bank had its own procedures, ledger systems, and organizational cultures. Venkateswara Bank's employees spoke primarily Telugu, Kulitalai Bank's staff knew only Tamil accounting methods, and Coimbatore Standard Bank used British bookkeeping practices from the 1920s. IOB created "integration committees" that spent months harmonizing operations, often keeping duplicate systems running until customers adjusted.

Internationally, the landscape was dramatically shifting. In 1963, Burma nationalized IOB's branches in Rangoon, Mandalay, and Moulmein, which became People's Bank No. 4. This was a crushing blow—the Rangoon branch alone had accounted for 15% of IOB's profits. The bank received compensation in worthless Burmese kyats, effectively writing off years of accumulated profits. It was a harsh lesson in political risk that would influence IOB's international strategy for decades.

Yet Chidambaram, until his untimely death in 1954, and his successors maintained the international vision. By 1955, IOB had branches in Hong Kong, Kuala Lumpur, Singapore, and Colombo. The Hong Kong branch, opened to serve the growing Indian textile trading community, became particularly profitable as the colony emerged as Asia's financial hub. These weren't vanity projects but profitable operations that provided foreign exchange earnings crucial for India's import-dependent economy.

The founder's death in the BOAC crash created a leadership crisis that took years to resolve. Without Chidambaram's personal relationships and vision, IOB became more bureaucratic, more cautious. The new management, drawn from professional bankers rather than the Chettiar community, focused on steady growth rather than bold expansion. They were preparing, perhaps unconsciously, for what many saw as inevitable: government takeover.

The 1960s consolidation served another purpose—making IOB too big to ignore. By 1968, the bank had 80 branches, deposits exceeding ₹100 crores, and a presence in every major South Indian city. When Prime Minister Indira Gandhi's government began discussing bank nationalization, IOB was clearly on the list. The bank's management, reading the political winds, began transferring international operations to structures that might survive government ownership.

Technology adoption during this period was modest but significant. IOB introduced mechanical accounting machines in major branches, telegram-based fund transfers between cities, and microfilming for record storage. The bank published India's first bilingual (English-Tamil) banking forms, recognizing that financial inclusion required linguistic inclusion. These seem like small steps now, but they positioned IOB as progressive within the conservative Indian banking sector.

The human dimension of this era deserves attention. IOB's employees, numbering about 3,000 by 1969, were a unique breed. Many were second-generation bankers, sons following fathers into the profession. They took pride in IOB's international heritage, even as operations became increasingly domestic. The bank's training programs, conducted in a colonial-era building in Madras, emphasized foreign exchange operations even for clerks who would never leave Tamil Nadu.

Customer relationships reflected old-world banking at its best and worst. Branch managers knew three generations of their clients' families, attended their weddings, and advised on everything from land purchases to children's education. But this also meant lending decisions were often based on community standing rather than cash flows, a practice that would later contribute to asset quality issues.

By early 1969, IOB's management sensed change coming. They accelerated loan recoveries, cleaned up balance sheets, and documented procedures that had long existed only in senior managers' heads. International branches were instructed to maintain maximum autonomy, keeping separate books that could survive a parent bank reorganization. It was prudent preparation for an earthquake everyone could feel coming.

The numbers on the eve of nationalization told a success story: ₹450 crores in deposits, 82 branches, profitable international operations, and a brand synonymous with reliable banking. IOB had successfully transformed from a Chettiar community bank into a regional powerhouse while maintaining its international DNA. But whether that DNA would survive government ownership remained an open question as July 19, 1969, approached—the day Indian banking would change forever.

V. The Nationalization Era & Pivot to Domestic Focus (1969–1991)

The announcement came over All India Radio at 8 PM on July 19, 1969: the Government of India had nationalized IOB along with 13 other major banks. In IOB's Madras headquarters, senior managers who had spent weeks preparing for this moment still felt stunned. The bank founded to serve Indian merchants across Asia was now property of the Indian state, subject to political directives and social banking mandates that would fundamentally alter its character.

The immediate aftermath was chaos wrapped in bureaucracy. Government-appointed directors replaced the board within weeks. The new chairman, a former Reserve Bank deputy governor, had never worked in commercial banking. His first directive: freeze all international expansion and focus on opening rural branches. IOB would now serve India's masses, not its merchants. The pivot from international to domestic wasn't a strategic choice—it was a political command.

Rural banking in 1970s India meant sending urban-trained officers to villages without electricity, much less banking infrastructure. IOB's first rural branch in Thanjavur district operated from a renovated cow shed, with the manager cycling five miles daily from the nearest town. The ledgers were handwritten, cash was stored in an old Godrej safe, and transactions were recorded by lamplight after sunset. This was a universe away from the foreign exchange dealing rooms of Singapore and Hong Kong.

Yet IOB adapted with surprising agility. The bank created a "rural banking cell" that developed simplified procedures for agricultural loans. Loan applications were printed in Tamil with pictographic instructions for illiterate farmers. Branch managers were authorized to approve crop loans up to ₹5,000 without headquarters approval—radical decentralization by Indian banking standards. By 1975, IOB had opened 200 rural branches, exceeding government targets.

The international operations, meanwhile, faced a different challenge: how to maintain global presence under government ownership that foreign regulators viewed with suspicion. Malaysian banking law explicitly prohibited foreign government-owned banks, threatening IOB's profitable Kuala Lumpur and Penang branches. The solution was creative financial engineering: In 1973, IOB, Indian Bank, and United Commercial Bank established United Asian Bank Berhad in Malaysia to comply with banking laws that prohibited foreign government banks from operating in the country, with each parent bank owning a third of the shares.

Similar creativity saved the Bangkok operations. IOB and six Indian private banks established Bharat Overseas Bank as a Chennai-based private bank to take over IOB's Bangkok branch. These weren't just regulatory workarounds but philosophical statements: IOB's management was determined to maintain international operations despite government ownership, even if it meant creating Byzantine corporate structures.

The 1970s brought unexpected international expansion opportunities. In 1977, IOB opened a branch in Seoul, serving Korean companies trading with India and Indian professionals working in Korea's booming construction sector. The bank also opened a branch in Tsim Sha Tsui, Kowloon, Hong Kong, and in 1979, opened a foreign currency banking unit in Colombo, Sri Lanka. These weren't political showpieces but profitable operations that generated precious foreign exchange.

Then came a stark reminder of political risk. In 1983, ethnic sectarian violence in the form of anti-Tamil riots resulted in the burning of IOB's branch in Colombo, while Indian Bank, which may have had stronger ties to the Sinhalese population, escaped unscathed. The images of the burned-out branch, with its IOB sign still visible among the ruins, became a symbol of the vulnerabilities facing Indian institutions abroad. The branch was eventually rebuilt, but the psychological damage lingered.

Priority sector lending—government-mandated loans to agriculture and small industry—became IOB's new reality. By 1985, 40% of all lending went to priority sectors, often at below-market rates with questionable repayment prospects. A typical priority sector loan: ₹10,000 to a marginal farmer for buying bullocks, secured only by the bullocks themselves, at 4% interest when inflation ran at 8%. The economics didn't work, but the politics demanded it.

The human cost of nationalization was profound. IOB's old guard, trained in international banking and foreign exchange, found themselves reviewing agricultural loan applications and attending village development meetings. Many took early retirement. Their replacements, recruited through government employment exchanges, were competent but lacked international exposure. The bank's culture shifted from entrepreneurial to bureaucratic, from profit-focused to target-driven.

Technology adoption during this period was government-driven and often counterproductive. IOB was forced to adopt the government's standardized banking software, which couldn't handle foreign exchange transactions properly. Branches maintained parallel manual systems for international operations, doubling work and increasing errors. The bank that had pioneered electronic fund transfers in the 1960s was now struggling with basic computerization.

The acquisition streak continued with a different flavor. In 1988-89, IOB acquired Bank of Tamil Nadu and its 99 branches in a rescue—the bank had been established in 1903 in Tirunelveli as the South India Bank. This wasn't strategic expansion but government-directed rescue of a failing institution. IOB inherited not just branches but massive non-performing assets, unfunded pension liabilities, and demoralized staff.

Yet amid the challenges, IOB's bankers displayed remarkable resilience. The Seoul branch manager learned Korean and built relationships that would pay dividends decades later. Rural branch managers became local champions, organizing farmer training programs and linking villages to markets. The Hong Kong operations quietly built expertise in trade finance that would become crucial when China opened up.

By 1991, as India teetered on the edge of a balance-of-payments crisis that would force economic liberalization, IOB was a fundamentally different institution than the one nationalized in 1969. It had over 1,000 branches, 90% of them in India, with rural and semi-urban branches outnumbering metropolitan ones. International operations, while profitable, were marginalized within the broader organization. The bank founded to serve Indians overseas had become a vehicle for Indian government policy.

The numbers told a mixed story: deposits had grown to ₹3,500 crores, but return on assets was below 0.5%. IOB had achieved the government's goal of financial inclusion, with millions of new account holders, but at the cost of operational efficiency and international competitiveness. As India prepared to liberalize its economy, IOB faced a new challenge: competing in a market economy while carrying the baggage of two decades of directed lending and political interference.

VI. Liberalization & Banking Reforms (1991–2010)

The Reserve Bank governor's fax arrived at IOB headquarters on a humid July morning in 1991: immediate freeze on lending, prepare for comprehensive asset quality review, expect new capital adequacy norms. India's balance-of-payments crisis had triggered economic liberalization, and banking reform was ground zero. For IOB, comfortable in its government-owned cocoon, the new world order was both threat and opportunity.

The Narasimham Committee Report of 1991 read like an indictment of public sector banking. Hidden non-performing assets, political interference in lending, overstaffing, technological obsolescence—every weakness IOB had accumulated during nationalization was now exposed. The prescription was harsh medicine: recognize bad loans, raise capital, reduce government ownership, and compete with soon-to-arrive private banks.

In 1992, Bank of Commerce, a Malaysian bank, acquired United Asian Bank, severing one of IOB's key international connections. The complex structure created to circumvent Malaysian banking laws had outlived its purpose. IOB received cash for its stake, but lost its Malaysian presence—a symbolic moment in the bank's retreat from international ambitions.

The push toward capital markets came in 2000. IOB engaged in an initial public offering that brought the government's share in the bank's equity down to 75%. The IPO roadshow was revealing: institutional investors grilled management about asset quality, technology plans, and competitive strategy. One fund manager's question captured the mood: "Why should we invest in a bank that lends to politicians' constituencies rather than creditworthy borrowers?"

Yet IOB found unexpected strengths. The rural network built under political pressure now provided low-cost deposit funding. While new private banks paid 9% for deposits, IOB's rural depositors accepted 6%, trusting the government guarantee. This three-percentage-point advantage became IOB's competitive moat, funding profitable corporate lending in cities with cheap rural deposits.

The acquisition strategy shifted toward tactical opportunities. In 2001, IOB acquired the Mumbai-based Adarsha Janata Sahakari Bank, which gave it a branch in Mumbai. This wasn't about adding branches but securing presence in India's financial capital. Then in 2009, IOB took over Shree Suvarna Sahakari Bank, which was founded in 1969 and had its head office in Pune. Each acquisition brought specific capabilities: Mumbai for corporate banking, Pune for IT sector exposure.

Technology transformation during this period was painful but necessary. IOB spent ₹500 crores on core banking implementation, connecting all branches to a central server. The project, plagued by vendor changes and resistance from unions, took seven years instead of the planned three. Branch managers who had never used computers were forced to learn, leading to early retirements and productivity losses that took years to recover.

New private banks like HDFC and ICICI were cherry-picking IOB's best customers with superior service and technology. A typical defection: a profitable textile exporter in Coimbatore, banking with IOB for three generations, moved to HDFC because they offered online banking and same-day international transfers. IOB's response—matching services two years later—came too late to prevent the loss of hundreds of similar accounts.

The international strategy during this period was modest but strategic. IOB opened an extension counter at New Kathiresan Temple complex in Sri Lanka in 2003, and in 2005 opened a representative office in Guangzhou, China. The next year IOB opened another representative office in Kuala Lumpur, and in 2009 opened one in Dubai. These weren't full branches but listening posts, maintaining presence while minimizing regulatory complexity.

In 2007, IOB took over Bharat Overseas Bank, reclaiming the entity it had helped create in the 1970s. The Bangkok operations, dormant for years, offered potential as Thailand-India trade grew. But IOB lacked the expertise and capital to fully leverage this opportunity, and the branch remained subscale throughout the decade.

Human capital challenges intensified as liberalization progressed. IOB's best performers were poached by private banks offering triple the salary. The bank's response—matching private sector pay for select positions—created internal equity issues. A risk manager hired from ICICI earned more than branch managers with 30 years' experience, breeding resentment that undermined collaboration.

The global financial crisis of 2008 provided unexpected vindication. While ICICI nearly collapsed from exposure to international derivatives and Lehman Brothers, IOB's conservative approach—born of government ownership and regulatory restrictions—protected it from the worst. The bank that international investors mocked for being unsophisticated had avoided sophisticated ways to lose money.

Priority sector lending remained an albatross. Despite reforms, IOB was still required to lend 40% to agriculture and small enterprises. The difference now was better risk assessment and recovery mechanisms. The bank pioneered self-help group lending, where peer pressure ensured repayment. It partnered with NGOs for financial literacy, reducing defaults through borrower education. These innovations made mandatory lending less loss-making, though hardly profitable.

By 2010, IOB was a bank in transition. Core banking was finally operational across all branches. The staff had been reduced from 30,000 to 20,000 through voluntary retirement. Asset quality, while improved, remained worse than private peers. The international presence, though maintained, was marginal to overall operations. The question facing management wasn't whether to reform further, but whether incremental reform was sufficient in an increasingly competitive market.

The numbers painted a picture of modest progress: return on assets improved to 0.9%, net NPA ratio fell to 1.2%, and fee income grew to 15% of total revenue. But these improvements looked inadequate against private banks posting 2% ROA and 30% fee income ratios. IOB had survived liberalization's first wave, but the second wave—digital banking, fintech competition, and consolidation pressure—was gathering force on the horizon.

VII. The NPA Crisis & Recovery Journey (2010–2020)

The conference room in IOB's Chennai headquarters fell silent as the chief risk officer presented slide 47: "Gross NPAs: ₹28,000 crores. Provision coverage: 42%. Expected credit loss: ₹16,000 crores." It was March 2016, and the Reserve Bank's Asset Quality Review had forced Indian banks to recognize the true extent of their bad loans. For IOB, the revelation was devastating—nearly 20% of its loan book was non-performing, double what it had reported just months earlier.

The roots of the crisis stretched back to the go-go years of 2006-2011, when Indian banks had funded everything from power plants to steel mills, believing India's GDP would grow at 9% forever. IOB, eager to prove it could compete with private banks, had jumped into infrastructure lending without adequate risk assessment. A typical bad loan: ₹500 crores to a power project in Andhra Pradesh, secured by equipment that couldn't operate because coal linkages never materialized.

The names on IOB's NPA list read like a who's who of Indian corporate distress: Essar Steel, Bhushan Power, Lanco Infratech. Each had borrowed hundreds of crores for projects that made sense on Excel spreadsheets but collapsed when commodity prices fell, environmental clearances stalled, or promoters siphoned funds. IOB's exposure to the "dirty dozen"—twelve large accounts that would eventually enter insolvency—exceeded ₹5,000 crores.

Government recapitalization became a lifeline and a leash. Between 2015 and 2019, the government injected ₹15,000 crores into IOB through various instruments. But capital came with conditions: board reconstitution, lending restrictions, mandatory recovery targets. IOB was placed under the Reserve Bank's Prompt Corrective Action framework, effectively preventing it from growing its loan book until asset quality improved.

The human toll was severe. IOB's stock price collapsed from ₹80 to ₹12, wiping out employee stock options and retail investor wealth. Morale plummeted as newspapers branded IOB a "weak bank" that might be merged out of existence. Branch managers, once respected community figures, faced public criticism for both lending to defaulters and refusing loans to genuine borrowers.

Recovery efforts ranged from innovative to desperate. IOB pioneered "loan recovery camps" where defaulters were offered one-time settlements in public forums, using peer pressure to encourage repayment. The bank hired former army officers as recovery agents, believing military discipline could succeed where traditional methods failed. It sold bad loans to asset reconstruction companies at steep discounts, crystallizing losses but cleaning balance sheets.

The Insolvency and Bankruptcy Code of 2016 offered hope but delivered mixed results. IOB recovered 43% of dues from Essar Steel after a protracted legal battle, better than expected but still a massive loss. Other cases dragged on for years, with promoters using every legal maneuver to delay resolution. The bank spent ₹200 crores on legal fees, hiring top law firms to navigate the new bankruptcy ecosystem.

Digital transformation accelerated as a survival strategy. With lending restricted, IOB focused on fee income through digital channels. The bank launched a mobile app that, while basic compared to private competitors, was revolutionary for customers accustomed to branch banking. Digital transactions grew from 20% of total volume in 2015 to 65% by 2019, reducing operational costs and improving customer retention.

Management changes brought fresh perspective but also disruption. IOB saw four CEOs between 2015 and 2020, each with different strategies. One focused on retail lending, another on recovery, a third on digital transformation. The lack of continuity meant initiatives were started but rarely completed, creating organizational whiplash that further damaged employee morale.

In 2009, IOB had acquired Pune-based Shree Suvarna Sahakari Bank, which had been established in 1969 with nine branches in Pune, two in Mumbai, and one in Shripur. This acquisition, initially seen as expanding IOB's presence in Maharashtra, now provided unexpected benefits. The acquired branches, focused on retail and small business lending, had better asset quality than IOB's corporate-heavy portfolio.

The priority sector lending that had been a burden became a relative bright spot. Agricultural loans, while yielding lower returns, also had lower default rates than corporate loans. IOB's deep rural presence, built during nationalization, provided stable deposit funding when urban customers fled to private banks. The bank discovered that boring retail banking was more sustainable than exciting infrastructure finance.

Technology partnerships offered scalability without capital investment. IOB partnered with fintech companies for loan origination, using their algorithms to assess creditworthiness while maintaining the customer relationship. These partnerships were controversial—unions feared job losses, and regulators worried about data security—but they allowed IOB to modernize without massive technology spending.

By March 2020, as the COVID pandemic began, IOB had turned the corner on asset quality. Gross NPAs had fallen to ₹13,410 crores, still high but manageable. The bank reported its first profit in three years, though it was too small to pay dividends. More importantly, IOB had learned hard lessons about risk management, diversification, and the dangers of following market fashions.

The recovery wasn't just financial but institutional. IOB developed robust credit assessment processes, with independent risk management reporting directly to the board. It created sector exposure limits, preventing concentration in any single industry. The bank that had nearly collapsed from bad corporate loans was rebuilding itself as a boring but stable retail and SME lender—perhaps what it should have been all along.

VIII. Modern Era: Digital Push & Turnaround (2020–Present)

The WhatsApp message pinged at 11:47 PM: "IOB account credited ₹50,000. New balance ₹2,35,420." The textile merchant in Tirupur smiled—his buyer in Germany had transferred payment instantly through IOB's new cross-border payment system. Five years ago, this transaction would have taken three days and multiple branch visits. This small moment captured IOB's dramatic digital transformation, culminating in receiving the Degidhan Award in 2021 for second-highest percentage of digital payment transactions among PSU banks.

The COVID-19 pandemic, rather than crushing IOB, catalyzed its digital revolution. When India locked down in March 2020, the bank faced an existential question: how to serve 35 million customers when branches were closed? The answer came through rapid deployment of digital solutions that had been in development for years but lacked urgency for implementation. Within six months, IOB rolled out video KYC, digital lending, and AI-powered customer service.

By March 2022, IOB's total business reached ₹417,960 crore, with 3,269 domestic branches, 2 DBUs (Digital Banking Units), and 4 foreign branches. But the real transformation was in business mix: digital transactions accounted for 85% of total volume, up from 30% in 2019. The bank processed 10 million UPI transactions daily, making it one of India's largest digital payment processors despite its public sector heritage.

The turnaround story accelerated in fiscal 2024-25. IOB posted net profits for 20 consecutive quarters, a remarkable streak after years of losses. The Q1 FY26 numbers told a story of sustained recovery: 12.19% year-on-year business growth, net profit of ₹1,111 crores, and gross NPAs at historic lows of 1.97%. Perhaps most impressively, digital transactions hit 98% of total volume, exceeding many private banks.

Leadership stability under CEO Partha Pratim Sengupta brought strategic clarity. Unlike his predecessors who chased multiple priorities, Sengupta focused on three goals: asset quality, digital transformation, and operational efficiency. He introduced "Project Aspire," a comprehensive transformation program that touched everything from branch design to credit underwriting. The results were visible: cost-to-income ratio fell from 58% to 51%, while fee income grew 40% annually.

The revenue mix transformation was deliberate and strategic. Corporate and wholesale banking contributed 38% of revenues but consumed 60% of capital—a deliberate reduction from earlier years. Retail banking, at 36% of revenues, became the growth engine with home loans growing 25% annually. Treasury operations, contributing 24%, provided stability through interest rate cycles. This balanced portfolio reduced concentration risk that had nearly destroyed IOB during the NPA crisis.

Government ownership, still at 96.38%, remained both blessing and curse. The sovereign guarantee attracted deposits, particularly from senior citizens seeking safety. But it also meant bureaucratic decision-making, political pressure for loan melas, and inability to match private sector compensation. IOB's solution was selective excellence—creating pockets of innovation within the broader bureaucratic structure.

The branch expansion strategy reflected new thinking. Instead of opening traditional branches, IOB launched 120 "digital branches"—small units with two employees and extensive self-service machines. These branches cost 70% less to operate while serving 90% of customer needs. Rural branches were retrofitted with solar power and satellite internet, bringing digital banking to villages previously served by manual ledgers.

Working capital management showed dramatic improvement. IOB reduced working capital requirements from 191 days to 111 days through supply chain financing initiatives. The bank partnered with e-commerce platforms to provide instant credit to sellers, with loans approved in minutes based on transaction history. This wasn't traditional banking but platform-based lending that leveraged data over collateral.

The international strategy, dormant for decades, showed signs of revival. IOB's foreign branches, particularly in Singapore and Hong Kong, benefited from India's growing trade with Asia. The bank processed $2 billion in trade finance annually, focusing on SME exporters ignored by larger banks. The representative offices in Dubai and Guangzhou, previously symbolic, became active in facilitating remittances and trade finance.

Technology partnerships accelerated innovation without capital strain. IOB partnered with Microsoft for cloud infrastructure, reducing IT costs by 30%. It collaborated with fintech startups for products it couldn't build internally: robo-advisory for wealth management, AI for fraud detection, blockchain for trade finance. These partnerships let IOB offer cutting-edge services while maintaining its public sector cost structure.

Employee transformation was perhaps the most remarkable change. IOB's average employee age dropped from 48 to 42 through strategic recruitment of technology specialists. The bank created "digital champions" in each branch—young employees who trained colleagues and customers on digital services. Performance metrics shifted from loans disbursed to digital adoption rates, changing behavior throughout the organization.

The numbers validated the transformation. IOB delivered 19.0% CAGR profit growth over five years, remarkable for a bank nearly written off in 2016. Return on equity reached 11.0%, approaching private bank levels. The stock price recovered to ₹40, still below book value but quadruple its 2016 lows. International rating agencies upgraded IOB's outlook from negative to stable, then to positive.

Yet challenges remained substantial. IOB hadn't paid dividends despite repeated profits, preserving capital for growth and potential bad loan surprises. Contingent liabilities of ₹1,76,039 crores—mostly guarantees and letters of credit—posed risks if the economy weakened. The interest coverage ratio remained low, suggesting vulnerability to rate cycles. Competition from fintech companies and digital-only banks intensified daily.

The modern IOB is unrecognizable from its founding vision yet strangely faithful to it. The bank created to serve Indian merchants abroad now serves Indian aspirations at home, using technology to bridge distances that ships once crossed. The digital transformation that seemed impossible five years ago now appears inevitable in hindsight. Whether this momentum sustains will determine if IOB remains independent or becomes fodder for the government's bank consolidation agenda.

IX. Playbook: Business & Investing Lessons

The boardroom wisdom from IOB's 87-year journey reads like a masterclass in institutional survival. When former CEO R. Subramania Kumar retired in 2015, he left behind a handwritten note: "We survived nationalization, the NPA crisis, and digital disruption. The lesson isn't that we were smart—it's that we were stubborn." That stubbornness, wrapped in strategic adaptation, offers profound lessons for both operators and investors.

Lesson 1: The Diaspora Advantage Is Real but Fragile

IOB's early dominance came from serving a specific diaspora—the Chettiars—with deep cultural understanding. The bank knew when remittances would spike (Deepavali), which trade routes mattered (Burma-Chennai rice trade), and how trust operated (community guarantees over collateral). This wasn't replicable by colonial banks that saw Indians as subjects, not clients.

The modern parallel is obvious: every immigrant community needs financial services that mainstream banks don't provide. Whether it's Latino remittances to Central America or Chinese students needing education loans, the opportunity remains massive. But the fragility is equally clear—political risk (Burma nationalization), community dispersion (Chettiars leaving traditional businesses), and generational change (young Chettiars banking with DBS, not IOB).

Lesson 2: Government Ownership Is a Devil's Bargain

The numbers tell the story: IOB's ROE averaged 18% before nationalization, 2% during government ownership, and has only recently recovered to 11%. Government backing provides cheap deposits and sovereign guarantees but destroys commercial discipline. Every loan becomes political, every branch opening a constituency favor, every CEO appointment a bureaucratic compromise.

Yet IOB also proves government banks can reform. The key was crisis—only when NPAs threatened the bank's existence did political interference recede. The current metrics show a bank delivering 19.0% CAGR profit growth over five years with ROE of 11.0%, competitive with many private peers. The lesson: government banks can perform, but only when politicians have no other choice.

Lesson 3: Technology Transformation Requires Crisis

IOB spent two decades discussing digital transformation but achieved more in two pandemic years than the previous twenty. The catalyst wasn't vision but necessity—serve customers digitally or cease to exist. The bank's digital transaction rate jumping from 30% to 98% in five years proves that institutional change, however difficult, is possible when survival depends on it.

The investment implication is counterintuitive: look for traditional institutions facing existential threats. They'll either transform dramatically or die quickly—binary outcomes that create asymmetric risk-reward. IOB at ₹12 in 2016 was priced for death; survival alone meant triple returns.

Lesson 4: Bad Loans Are Features, Not Bugs, of Banking Systems

IOB's NPA cycle—2% in 2007, 20% in 2016, 2% in 2024—mirrors Indian banking history. Every decade brings a credit boom (infrastructure, real estate, retail), followed by a bust, then recapitalization and reform. The pattern is so predictable it's almost tradeable: buy banks when NPAs peak, sell when credit growth accelerates.

The operational lesson is different: banks that survive multiple cycles develop institutional memory that newcomers lack. IOB's credit officers who lived through the 2016 crisis won't repeat those mistakes. This experience premium explains why boring old banks often outperform exciting new ones through full cycles.

Lesson 5: Financial Inclusion Is Expensive but Sticky

IOB's rural network, built under political pressure, seemed like dead weight during the 1990s. Who needed physical branches when private banks were going digital? But those rural relationships proved incredibly sticky—farmers who opened accounts in 1975 still bank with IOB, as do their children and grandchildren. The cost of acquisition was high, but the lifetime value was higher.

Today, IOB's priority sector lending to agriculture and MSMEs represents 41% of total loans. While yields are lower, so is volatility. When corporate loans imploded, agricultural loans kept paying. The lesson: serving underbanked segments requires patience but creates moats that technology alone can't breach.

Lesson 6: International Operations Need Local Ownership

IOB's overseas branches thrived when managed by expatriate Indians who understood both local markets and Indian business culture. They struggled when run by bureaucrats from Chennai who treated Singapore like Salem. The successful revival of international operations in recent years came from hiring local talent and giving them autonomy.

The broader principle: international expansion isn't about planting flags but building bridges. IOB succeeded when it connected Indian merchants to overseas opportunities. It failed when it tried to be a global bank competing with Citibank. Know your niche and own it completely.

Lesson 7: Balance Sheet Strength Beats Income Statement Growth

Throughout its history, IOB's troubles came from chasing growth—lending to infrastructure projects beyond its expertise, acquiring weak banks for size, expanding internationally without adequate capital. Its successes came from boring balance sheet management: maintaining provision coverage, diversifying funding sources, matching asset-liability duration.

Current investors should note: IOB trades at a P/E of 18.1 and book value of ₹17.5, suggesting the market values earnings over assets. History suggests this is backward—Indian banks trading below book value often outperform those trading at premium valuations through cycles.

Lesson 8: Cultural DNA Persists Through Ownership Changes

Despite nationalization, despite management changes, despite digital transformation, IOB retains its essential character as a relationship bank serving Indian business communities. The Chettiar merchant culture—conservative, relationship-focused, internationally oriented—persists in policies and practices. Branch managers still attend customer weddings. International trade finance remains a specialty. Tamil signage appears prominently even in Mumbai branches.

This persistence suggests that institutional culture, once established, is remarkably durable. Investors should look beyond ownership structures to underlying organizational DNA. A bank's founding mission often predicts its future better than its current strategy.

The meta-lesson from IOB's journey is that banking is ultimately about trust, and trust takes decades to build but moments to destroy. IOB has survived because, despite mistakes and crises, it never fundamentally betrayed depositor trust. In an era of algorithmic lending and digital disruption, this ancient banking wisdom remains surprisingly relevant.

X. Analysis & Bear vs. Bull Case

The spreadsheet glows at 2 AM in a Mumbai fund manager's office. She's modeling IOB for the fourth time this month, trying to reconcile spectacular recent performance with stubborn structural challenges. The numbers tell two completely different stories depending on the timeframe: a five-year view shows a phoenix rising from ashes, while a ten-year view reveals chronic underperformance. Which narrative should drive investment decisions?

The Bull Case: Transformation Is Real and Sustainable

The bulls start with undeniable momentum. IOB delivered 19.0% CAGR profit growth over the last five years, a trajectory that would make any growth investor salivate. This isn't accounting manipulation but genuine operational improvement: NPAs falling from 20% to 2%, digital adoption reaching 98%, and fee income growing 40% annually.

Government backing, rather than a liability, becomes an asset in the bull narrative. With 96.38% state ownership, IOB enjoys an implicit sovereign guarantee that attracts deposits at below-market rates. This funding advantage—typically 150 basis points versus private banks—drops straight to the bottom line. In a rising rate environment, this spread widens further.

The digital transformation story is particularly compelling. IOB spent just ₹500 crores on technology over five years but achieved digital penetration rates comparable to banks spending billions. This capital efficiency suggests management has finally learned to leverage partnerships over proprietary development. The recent Degidhan Award validates this transformation isn't just internal propaganda but recognized excellence.

Asset quality improvement appears structural, not cyclical. IOB's gross NPAs at 1.97% are below system averages, with provision coverage exceeding regulatory requirements. More importantly, the loan book composition has shifted from concentrated corporate exposure to diversified retail and SME lending. This isn't the same bank that nearly collapsed in 2016.

The valuation argument is straightforward: IOB trades at book value of ₹17.5, implying zero value for future earnings. With ROE at 11% and growing, the bank should trade at least at 1.5x book value, suggesting 50% upside. If IOB achieves its targeted 15% ROE by 2027, fair value approaches 2x book, implying the stock could double.

International operations offer hidden optionality. IOB's branches in Singapore, Hong Kong, and Seoul are perfectly positioned for India's growing trade with Asia. As Indian companies expand overseas, they need banking partners who understand both Indian regulations and international markets. IOB's heritage positions it uniquely for this opportunity.

The macro tailwinds are powerful. India's GDP growth, financial inclusion expansion, and digital payment adoption all benefit incumbent banks with established networks. IOB's 3,200 branches become distribution assets in an economy where 300 million people remain unbanked. The next decade's lending opportunity dwarfs anything in IOB's history.

The Bear Case: Structural Problems Persist Despite Cosmetic Improvements

Bears begin with a simple observation: IOB hasn't paid dividends despite 20 quarters of profits. This suggests management doesn't trust its own earnings quality or sees trouble ahead that requires capital preservation. For income investors, a bank that can't pay dividends isn't investible regardless of paper profits.

The interest coverage ratio tells a worrying story. Despite falling rates and improved operations, IOB struggles to cover interest costs from operating earnings. This suggests the bank remains leveraged to interest rate cycles and could quickly swing to losses if rates rise or asset quality deteriorates.

Contingent liabilities of ₹1,76,039 crores represent 5x the bank's net worth. These off-balance-sheet exposures—guarantees, letters of credit, derivative positions—could crystallize into real losses during economic stress. The bull case assumes benign conditions; the bear case models what happens when assumptions break.

Government ownership remains an albatross. Every lending decision faces political scrutiny. Every strategic initiative requires bureaucratic approval. Every CEO appointment becomes a political football. The recent proposal to merge IOB with another public bank hangs like a sword, creating uncertainty that depresses valuations regardless of operational performance.

Competition is intensifying from directions IOB can't match. Fintech companies offer instant loans through apps IOB can't build. Digital-only banks operate at cost structures IOB can't achieve. Foreign banks cherry-pick profitable customers IOB spent decades developing. The competitive moat is eroding faster than the bulls acknowledge.

Employee productivity remains abysmal. IOB has 20,000 employees generating ₹3,800 crores in profit—roughly ₹19 lakhs per employee. HDFC Bank generates ₹1 crore per employee, five times higher. This productivity gap isn't fixable without massive layoffs that government ownership makes impossible.

The technology transformation, while impressive, remains superficial. Core systems still run on 1990s architecture held together with digital band-aids. Real transformation requires replacing, not patching, legacy infrastructure—a multi-year, multi-thousand-crore investment IOB can't afford.

The loan book quality improvement may be cyclical, not structural. India hasn't faced a serious economic downturn since 2008. When the next recession hits—and economic cycles guarantee it will—IOB's improved underwriting standards remain untested. The same management that created the previous NPA crisis remains largely in place.

The Verdict: A Speculative Recovery Play, Not a Quality Compounder

The truth lies between extremes. IOB is neither the transformed digital bank bulls imagine nor the zombie institution bears describe. It's a recovering patient—out of intensive care but not ready to run marathons. The stock offers compelling risk-reward for specific investors: those with high risk tolerance, long time horizons, and belief in India's banking sector consolidation.

For fundamental investors seeking quality compounders, IOB fails multiple tests. The inability to pay dividends, government ownership overhang, and structural productivity challenges make it unsuitable for buy-and-hold portfolios. The stock is a trading vehicle, not an investment—suitable for playing recoveries and cycles, not for building wealth over decades.

The key monitorable metrics are clear: watch NPA trends for signs of new stress, track digital adoption for competitive positioning, monitor government stake sales for ownership clarity, and measure ROE progression toward management targets. If these improve, the bull case strengthens. If they stagnate, the recovery narrative collapses.

The investment decision ultimately depends on time horizon and risk appetite. For a two-year view, IOB offers attractive recovery potential. For a ten-year view, structural challenges likely limit returns. The bank that began serving diaspora merchants and became a government policy tool is still searching for its modern identity. Until it finds one, IOB remains a speculation on India's banking future, not a conviction bet on its own transformation.

XI. Epilogue & "If We Were CEOs"

Picture this thought experiment: The year is 2025, and through an improbable series of events, you've just been appointed CEO of Indian Overseas Bank. The government, desperate for fresh thinking, has given you unprecedented autonomy—five years to transform IOB without political interference. Your compensation is tied entirely to long-term value creation. What would you do?

The first Monday morning, walking through IOB's Chennai headquarters, past portraits of founder Chidambaram Chettiar and faded photographs of the original Rangoon branch, the weight of history is palpable. But history is both asset and anchor. The question isn't how to honor the past but how to leverage it for the future.

Priority 1: Reclaim the International Heritage

IOB's founding mission—serving Indians globally—remains more relevant than ever. The Indian diaspora has grown from 3 million in 1937 to 32 million today, controlling wealth exceeding $1 trillion. Yet IOB has virtually no presence in Dubai, where 3 million Indians live, or Silicon Valley, where Indian tech entrepreneurs raise billions. This isn't about opening branches but creating digital bridges.

The strategy would be "IOB Global"—a digital-first international banking platform targeting the diaspora. Partner with local banks for regulatory compliance while providing the technology layer. An Indian software engineer in Seattle could open an NRE account in minutes, get pre-approved mortgages for Indian property, and manage family wealth across borders. The tagline writes itself: "Banking Without Borders, Rooted in Trust."

Priority 2: The Great Unbundling

IOB currently operates as a monolithic institution trying to be everything to everyone. This is strategically incoherent and operationally impossible. The solution is to unbundle into focused business units, each with its own P&L, strategy, and eventually, ownership structure.

Create four distinct units: Rural (financial inclusion and agriculture), Retail (urban middle class), Corporate (mid-market companies), and Digital (new-age banking). Each unit gets its own CEO, technology stack, and performance metrics. Rural focuses on profitability through scale, Retail on customer acquisition, Corporate on risk-adjusted returns, Digital on innovation. This isn't organizational reshuffling but fundamental restructuring.

Priority 3: The Privatization Preparation

Government ownership at 96.38% is unsustainable. But rather than wait for political consensus on privatization, prepare IOB to thrive regardless of ownership. This means cleaning up the balance sheet, improving governance, and creating value that makes privatization inevitable rather than imposed.

Start by spinning off non-core assets: sell the real estate portfolio, monetize the branch network through sale-and-leaseback, divest non-performing subsidiaries. Use proceeds to boost capital ratios and technology investment. Create an independent board with genuine powers, even if the government remains the majority owner. Make IOB so valuable that not privatizing becomes politically untenable.

Priority 4: The Technology Leapfrog

Rather than spending billions trying to match private banks' technology, leapfrog them entirely. Partner with a global technology giant—imagine "IOB powered by Google" or "IOB on AWS"—to create India's first truly cloud-native bank. Not just digital banking but AI-first banking where every decision is data-driven.

The radical move: open-source IOB's technology stack. Let startups build on IOB's platforms, creating an ecosystem rather than a walled garden. Revenue comes not from proprietary technology but from transaction volumes and data insights. This transforms IOB from a bank that uses technology to a technology company with a banking license.

Priority 5: The Talent Revolution

IOB's 20,000 employees are simultaneously its greatest asset and biggest liability. Mass layoffs are politically impossible and morally questionable. The solution is radical reskilling and voluntary transformation. Create "IOB University"—a world-class training institution that transforms traditional bankers into digital-age financial professionals.

Partner with leading universities to offer degrees, with technology companies for certifications, with startups for internships. Employees who complete programs get significant pay raises and stock options. Those who don't want to change get generous early retirement. Within five years, transform the workforce from liability to asset.

Priority 6: The Customer Experience Obsession

IOB's Net Promoter Score is presumably negative—customers bank with IOB despite the experience, not because of it. This changes through radical simplification. Reduce products from 200 to 20. Eliminate forms that require physical signatures. Promise resolution of any issue within 24 hours or the customer gets compensated.

Create "IOB Prime"—a premium service for profitable customers that rivals private banking at mass-market prices. Include wealth management, tax planning, insurance, and concierge services. The goal: make IOB the primary financial relationship for India's emerging affluent, not just a salary account.

Priority 7: The Risk Culture Revolution

IOB's risk management oscillates between reckless lending and paranoid restriction. Create a true risk culture where taking intelligent risks is rewarded and avoiding all risks is penalized. This means reforming credit assessment from paperwork-based to data-driven, from collateral-focused to cash-flow-based.

Implement "Smart Lending"—AI-driven credit decisions for loans up to ₹50 lakhs, with human intervention only for exceptions. Track loan officers not just on volumes or defaults but on risk-adjusted returns. Create a "Bad Bank" within IOB to professionally manage NPAs rather than letting them fester on balance sheets.

The Five-Year Vision

By 2030, IOB would be unrecognizable: A focused international franchise serving the global Indian diaspora. Four specialized business units, each best-in-class in its segment. Government stake reduced to 26%, with strategic investors including a global bank and technology company. Technology infrastructure that others license, not legacy systems others mock. Employees who chose transformation, equipped with skills that make them valuable anywhere. Customers who recommend IOB to friends, not warn them away.

The financial targets would be ambitious but achievable: ROE of 18% (from current 11%), Cost-to-income ratio of 40% (from 51%), Digital transactions at 99.9%, Net NPAs below 1%, Market capitalization of ₹2 lakh crores (from ₹69,000 crores).

The Implementation Reality

Of course, this is fantasy. No CEO gets five years without interference. The government won't surrender control easily. Unions will resist change. Competitors won't stand still. Technology transformations fail more often than succeed. But strategy is about choosing direction, not guaranteeing outcomes.

The real insight from this exercise is that IOB's problems aren't insurmountable—they're political. The bank has assets (brand, network, customer base) that could be tremendously valuable if properly leveraged. It has liabilities (government ownership, legacy technology, unproductive workforce) that could be addressed with will and resources.

The tragedy of IOB isn't that it's a bad bank but that it could be a great one. Founded with a vision of connecting Indians globally, it became a vehicle for domestic political objectives. Built for innovation, it became bureaucratic. Created for merchants, it serves politicians. The gap between potential and reality is heartbreaking.

Perhaps the next CEO—whoever they are, whenever they're appointed—will read this and think: "Impossible but interesting." And perhaps, just perhaps, they'll try anyway. Because IOB's story isn't finished. The bank that Chidambaram Chettiar founded to serve Indians wherever they went still has chapters to write. Whether they're chapters of decline or renewal depends on choices made today.

The ultimate lesson from imagining ourselves as CEO isn't about specific strategies but about possibility itself. IOB proves that institutions can survive almost anything—nationalization, bad loans, technological disruption. If they can survive, they can thrive. It just requires leadership with courage to change what seems unchangeable. For IOB, for Indian banking, for any organization trapped between glorious past and uncertain future, transformation isn't just possible—it's essential.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube