Bank of India: The Century-Old Giant's Journey from Mumbai to the World

I. Introduction & Cold Open

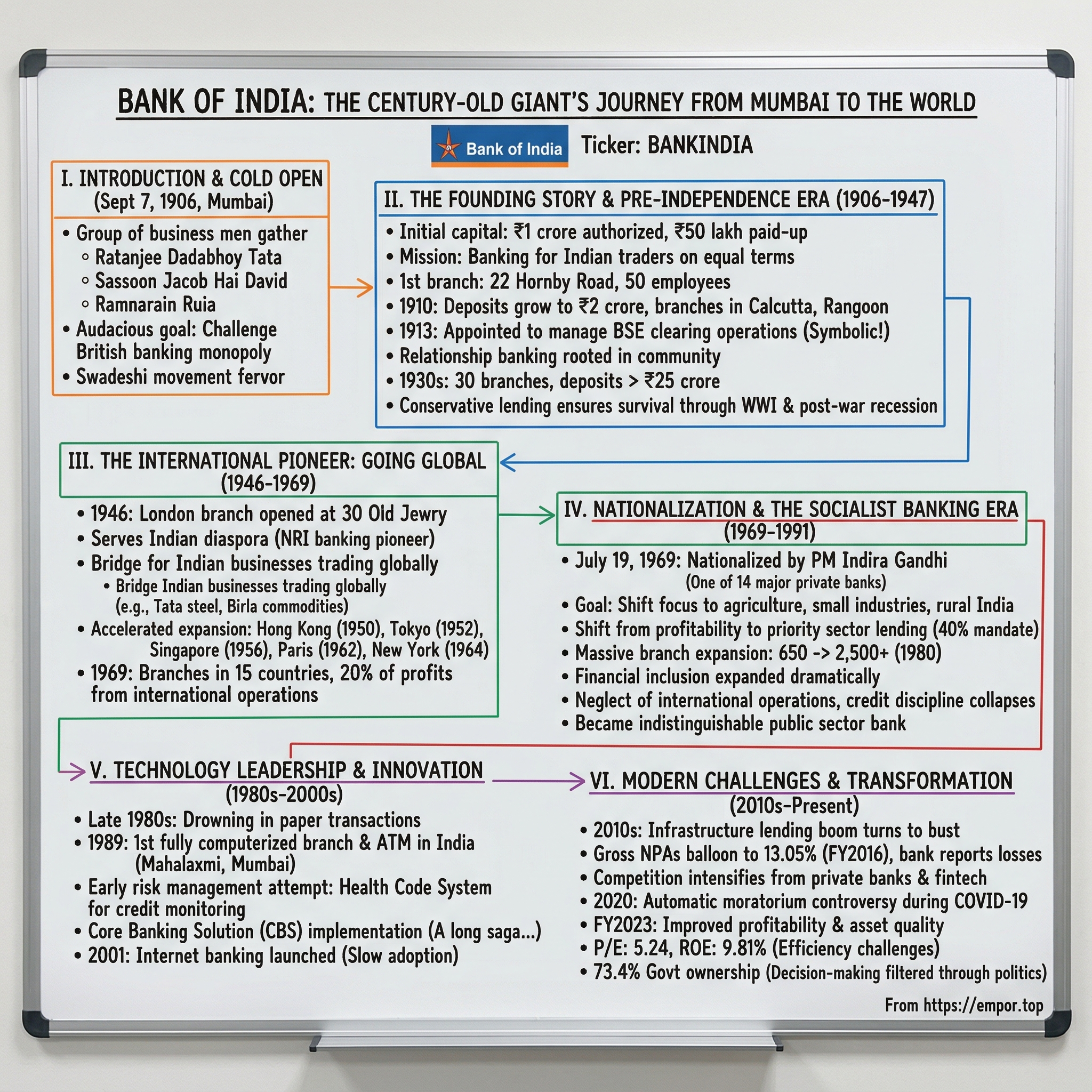

Picture this: September 7, 1906, Mumbai. The monsoon has just retreated, leaving the city's Gothic Revival buildings gleaming under a clearing sky. Inside a modest office near what would become the financial heart of India, a group of businessmen gather around a mahogany table. Among them sits Sassoon Jacob Hai David, the Baghdadi Jewish trader who built a cotton empire; Ramnarain Ruia, whose family would later create the Essar conglomerate; and most notably, Ratanjee Dadabhoy Tata—yes, that Tata family. They're signing papers to launch something audacious: an Indian-owned bank that would challenge the British banking monopoly.

Fast forward 118 years. That single-office operation with 50 employees and ₹50 lakh in paid-up capital has morphed into Bank of India—a ₹51,809 crore market cap behemoth, the sixth-largest nationalized bank in the country, managing ₹13.24 lakh crore in total business as of FY24. It operates across five continents, pioneered computerized banking in India, survived nationalization, and somehow maintains relevance in an era of UPI and neobanks.

But here's what makes this story compelling for investors and business historians alike: Bank of India isn't just another public sector bank groaning under government ownership. It's a case study in how institutions navigate seismic shifts—from colonialism to independence, from capitalism to socialism and back, from ledger books to algorithms. It's about how a bank founded during the Swadeshi movement to serve Indian merchants became an arm of state policy, then tried to transform itself into a modern financial institution while dragging along a century of legacy.

The numbers tell one story: a low P/E of 5.24, suggesting the market sees it as a value trap. An ROE hovering around 9.81% over three years, indicating efficiency challenges. Government ownership at 73.4%, which means every strategic decision gets filtered through political considerations. But the institution tells another story—one of resilience, adaptation, and the peculiar dynamics of Indian capitalism where private ambition and public purpose perpetually collide.

This is that story—how a bank born from nationalist fervor became a global pioneer, got swallowed by socialist ideology, and now struggles to define itself in India's digital age. It's about understanding not just where Bank of India has been, but what its journey reveals about Indian banking's past, present, and likely future.

II. The Founding Story & Pre-Independence Era (1906-1947)

The year 1906 was electric with possibility in Mumbai—then Bombay. The Swadeshi movement, sparked by Lord Curzon's partition of Bengal, had ignited economic nationalism across India. "Be Indian, Buy Indian" wasn't just a slogan; it was becoming a business model. Indian merchants, tired of depending on British banks that viewed them with suspicion and charged usurious rates, were pooling capital to create their own financial institutions.

Into this ferment stepped our unlikely coalition of founders. Sassoon David brought international trading acumen from his cotton empire that stretched from Mumbai to Manchester. The Ruia family contributed their understanding of commodity financing. But the masterstroke was getting Ratanjee Dadabhoy Tata on board—not for his capital alone, but for the credibility the Tata name lent to any enterprise. The Tatas had already proven with Tata Steel that Indians could build world-class industrial enterprises. Now they would help prove Indians could run banks too.

The founding document, preserved in the bank's archives, reveals fascinating details. The initial authorized capital was set at ₹1 crore—ambitious for an Indian enterprise but modest compared to British banks operating in India. The paid-up capital of ₹50 lakh was raised through 10,000 shares of ₹500 each, deliberately priced high to attract serious investors rather than speculators. The prospectus, written in English, Gujarati, and Marathi, explicitly stated the bank's mission: "To provide banking facilities to Indian traders and industrialists on terms no less favorable than those enjoyed by European businesses."

Those first months were precarious. The bank opened its sole branch at 22 Hornby Road (now Dadabhai Naoroji Road) with just 50 employees, most poached from other banks with promises of faster advancement—Indian clerks knew they'd never become managers at British banks. The first general manager, a Parsi gentleman named Sorabji Pochkhanawala, instituted practices that seem quaint now but were revolutionary then: ledgers maintained in both English and vernacular languages, a dedicated desk for small traders, and remarkably, banking hours that extended past 3 PM to accommodate Indian merchants who did business in the evening.

The early growth strategy was brilliantly simple: follow the money. Indian merchants dominated the cotton trade, controlled significant portions of the grain market, and were making inroads into manufacturing. Bank of India positioned itself as their financial partner, offering trade finance, hundis (indigenous credit instruments), and crucially, respect. While British banks required Indian merchants to remove their shoes and wait in separate areas, Bank of India treated them as valued clients.

By 1910, deposits had grown to ₹2 crore. The bank had opened branches in Calcutta (now Kolkata) and Rangoon (now Yangon), following Indian merchant networks. But the real validation came in 1913 when the bank was appointed to manage clearing operations for the Native Share & Stock Brokers' Association—the precursor to the Bombay Stock Exchange. This wasn't just a business win; it was symbolic. The beating heart of Indian capitalism would be served by an Indian bank.

World War I transformed everything. British banks, focused on war financing, left gaps in trade finance that Bank of India eagerly filled. Deposits surged to ₹10 crore by 1918. The bank funded everything from textile mills in Ahmedabad to jute factories in Bengal. More importantly, it began experimenting with what would now be called "financial inclusion"—small loans to farmers against gold ornaments, financing for small traders against personal guarantees rather than collateral.

The 1920s brought the first real test. The post-war recession hit Indian merchants hard. Cotton prices collapsed. Several smaller Indian banks failed, creating panic. Bank of India survived through conservative lending—Pochkhanawala's rule was simple: "Never lend more than what you can afford to lose, and always know your borrower's family." This wasn't modern credit scoring; it was relationship banking rooted in community networks.

The 1921 agreement to manage the BSE Clearing House operations marked a strategic pivot. The bank wasn't content being a commercial lender; it wanted to be at the center of India's emerging capital markets. This early connection to equity markets would later give it advantages in investment banking and treasury operations that peers lacked.

By the 1930s, Bank of India had grown to 30 branches with deposits exceeding ₹25 crore. But success brought scrutiny. The British colonial government, wary of Indian financial power, imposed restrictive regulations. The Reserve Bank of India, established in 1935, began supervising banks more closely. Yet the bank adapted, maintaining profitable growth while navigating colonial bureaucracy.

The pre-independence era climaxed with a decision that would define the bank's trajectory: in 1946, even as India stood on the cusp of independence and partition, Bank of India did something no Indian bank had done before—it went global. But that's a story that deserves its own telling, for it reveals how this Mumbai institution saw opportunity where others saw only uncertainty.

III. The International Pioneer: Going Global Before Others (1946-1969)

The boardroom at Bank of India's Mumbai headquarters was thick with cigarette smoke and tension on that humid August morning in 1945. World War II was ending, India's independence was inevitable, and the directors faced a decision that seemed either visionary or insane: should an Indian bank, operating under colonial rule, open a branch in London—the very heart of the Empire?

The man pushing hardest for this radical move was the bank's new chairman, Chintaman Deshmukh (who would later become India's first Indian Finance Minister). Deshmukh argued that independence would create a new class of Indian businesses needing international banking services. "We must be where our clients need us," he insisted, "not wait for them to need us where we are."

The logistics were staggering. In 1946, India didn't even have a clear path to independence, let alone foreign exchange regulations for its banks operating abroad. The Bank of England viewed the application with bewilderment—here was a colonial bank wanting to set up shop in the colonizer's capital. The diplomatic negotiations took months, requiring interventions from Indian business leaders in London and even sympathetic British parliamentarians who saw the winds of change.

On June 5, 1946, Bank of India opened its London branch at 30 Old Jewry, a stone's throw from the Bank of England. The first manager, K.C. Shroff, arrived with a staff of six, a manual typewriter, and what he later described as "enormous anxiety disguised as confidence." The branch's initial capital was a modest £100,000, but its symbolic value was incalculable—an Indian institution planting its flag in the financial capital of the Empire.

The timing proved genius. As Indian merchants and industrialists began trading globally post-independence, they needed a banker who understood both Indian business practices and international finance. Bank of India's London branch became the crucial bridge, handling letters of credit for Tata's steel exports, financing Birla's commodity trades, and managing foreign exchange for countless smaller Indian businesses taking their first international steps.

But the real innovation was in serving the Indian diaspora. By 1950, the London branch had pioneered what would become the NRI (Non-Resident Indian) banking model—remittance services for Indian workers, special deposit schemes for overseas Indians, and financing for Indians buying property abroad. The bank discovered what every international Indian bank would later learn: the diaspora was both emotionally attached to Indian banks and financially attractive as clients.

The international expansion accelerated through the 1950s and 1960s with an almost imperial ambition of its own. Hong Kong in 1950, to serve Indian traders in the Far East. Tokyo in 1952, becoming the first Indian bank in Japan. Singapore in 1956. Paris in 1962. New York in 1964. Each opening was a calculated bet on trade flows and diaspora populations.

The Singapore branch story illustrates the strategy perfectly. The bank identified that Indian merchants controlled significant portions of the Southeast Asian textile trade but were being poorly served by British banks. Within three years of opening, the Singapore branch was financing 30% of textile imports from India to Southeast Asia. The branch manager, a young Gujarati named Pravin Shah, became legendary for approving loans over lunch conversations in Little India, using his understanding of family networks and community ties as collateral assessment.

By 1969, just before nationalization, Bank of India operated in 15 countries across five continents with 47 branches and offices including subsidiaries. The international operations contributed nearly 20% of the bank's profits—remarkable for an era when most Indian companies barely looked beyond their borders. The foreign exchange dealing room in Mumbai was among the most sophisticated in Asia, with direct telex lines to major financial centers.

The international presence created unexpected advantages. The bank became the informal financial intelligence service for Indian businesses, providing insights on global markets, regulatory changes, and opportunities. Its treasury operations, honed through managing multiple currencies, became surprisingly sophisticated. The bank pioneered currency swaps and forward contracts for Indian exporters when such instruments were exotic in India.

But perhaps the most important legacy of this early internationalization was cultural. Bank of India developed a cadre of internationally trained bankers who understood global best practices. These officers brought back ideas about risk management, technology adoption, and customer service that were years ahead of domestic peers. The bank's internal training programs began including stints at international branches, creating a pipeline of globally minded executives.

The international expansion also revealed strategic tensions that would plague the bank for decades. Serving Indian businesses globally required risk-taking and innovation. But the conservative, relationship-based culture that ensured survival in India often clashed with the aggressive, transaction-focused banking needed to compete internationally. The London branch, for instance, lost several deals to Citibank and Standard Chartered because approval processes routed through Mumbai took weeks.

As 1969 dawned, Bank of India stood at a crossroads. It was India's most international bank, with a global network that rivals envied. But storm clouds were gathering domestically. Prime Minister Indira Gandhi's socialist agenda was gaining momentum, and whispers of bank nationalization grew louder. The question was: could a bank built on entrepreneurial vision survive becoming an instrument of state policy? The answer would reshape not just Bank of India, but the entire Indian banking landscape.

IV. Nationalization & The Socialist Banking Era (1969-1991)

The boardroom clock at Bank of India's Fort headquarters showed 8:25 PM on July 19, 1969. Chairman M.M. Mehta had just received a phone call that would end a 63-year era. Prime Minister Indira Gandhi was about to announce the nationalization of 14 major commercial banks at 8:30 PM. Bank of India, the institution that had pioneered Indian banking, was about to become government property.

The announcement shouldn't have been a complete surprise—whispers of nationalization had circulated for months. Yet the speed and secrecy of the decision stunned everyone. Between July 12 and 15, 1969, Haksar and Indira Gandhi had decided to shed their caution on bank nationalization, and just three days later, on July 19, the banks were indeed nationalized. The ordinance, prepared in absolute secrecy by a handful of officials working through the night, transformed India's banking landscape in a single stroke.

For Bank of India, this was particularly poignant. The bank was one of the 14 major private banks nationalized by the Government of India, ending its run as a symbol of Indian entrepreneurial success. The institution that had been founded to challenge British banking dominance was now being absorbed by the Indian state—a bitter irony not lost on its board members.

The official rationale was compelling on paper. Gandhi said the decision was taken after the banks failed to help farmers, provide credit for agricultural farming, and focus on small-scale industries and startups. Private banks, the government argued, served only urban elites and big business. Rural India, where 80% of the population lived, remained unbanked. Money lenders charged usurious rates. Agricultural credit was virtually non-existent. The stated reason for the nationalization was to give the government more control of credit delivery.

But Bank of India's executives knew the real motivations were as much political as economic. The announcement came just days after an assault on Indira Gandhi's authority with Sanjiva Reddy's announcement as the Congress's presidential candidate, followed by Morarji Desai's resignation. Nationalization was Gandhi's masterstroke—simultaneously asserting her socialist credentials, wrong-footing political opponents, and appealing to the masses.

The immediate aftermath was chaos. Bank of India's 2,000-odd branches received telegrams on July 20 informing them they were now government property. Senior executives who had spent careers building the institution watched as bureaucrats from the Finance Ministry arrived to take charge. The bank's sophisticated international operations, its carefully cultivated corporate relationships, its entrepreneurial culture—all would now be subordinated to government policy.

The transformation was jarring. Branch managers who had focused on profitability were suddenly evaluated on how many accounts they opened in villages without electricity. Loan officers trained to assess creditworthiness were ordered to lend to "priority sectors"—agriculture, small-scale industries, weaker sections—regardless of repayment capacity. The government mandated that 40% of credit go to these priority sectors, up from less than 15% before nationalization.

Yet the socialist banking era wasn't entirely destructive for Bank of India. The government's aggressive branch expansion program played to the bank's strengths. Between 1969 and 1980, Bank of India's branch network exploded from 650 to over 2,500 branches. The bank pioneered rural banking models that would later be emulated across the developing world—mobile branches using jeeps, simplified procedures for illiterate customers, agricultural extension services bundled with credit.

The numbers were staggering. Deposits grew from ₹800 crore in 1969 to ₹4,500 crore by 1980. The bank opened accounts for millions who had never seen the inside of a bank. In villages across Maharashtra, Gujarat, and Uttar Pradesh, Bank of India branches became symbols of modernity, offering not just banking but a connection to the formal economy.

But this growth came at a cost. Credit discipline collapsed. Loans were sanctioned based on political connections rather than commercial viability. The bank's international operations, once its crown jewel, withered from neglect—the government saw little value in serving global markets when rural India needed attention. Talented officers left for private sector opportunities. Those who remained adapted to a new reality where following government directives mattered more than generating profits.

In 1980, six more private banks were nationalized, and by then, the Government of India controlled around 91% of the banking business of India. Bank of India had become just another public sector bank, indistinguishable from its peers except for its history.

The socialist banking experiment did achieve some objectives. Financial inclusion expanded dramatically. Rural credit increased. Small industries got funding. But it also created problems that would haunt Indian banking for decades—poor asset quality, political interference, operational inefficiency. Bank of India's journey from 1969 to 1991 encapsulates this paradox: massive expansion coupled with institutional decay, social achievement shadowed by commercial failure.

By 1991, as India faced a balance of payments crisis and turned toward liberalization, Bank of India stood at another crossroads. It had fulfilled its social mandate but lost its commercial edge. The question was: could an institution reshaped by socialism adapt to capitalism's return? The answer would require confronting a challenge even more daunting than nationalization—modernization.

V. Technology Leadership & Innovation (1980s-2000s)

The year was 1989, and Bank of India's Mahalaxmi branch in Mumbai looked like something from a science fiction film—at least by Indian banking standards. Customers walked past armed guards into an air-conditioned hall where a machine dispensed cash without human intervention. Inside, clerks worked at computer terminals instead of ledger books. The bank had established India's first fully computerized branch and ATM at Mahalaxmi, Mumbai, becoming the first nationalized bank to embrace what would become the future of banking.

This technological leap didn't emerge from strategic vision but from desperation. By the late 1980s, Bank of India was drowning in paper. Its 3,000-plus branches generated millions of transactions daily, all recorded manually. Ledger reconciliation took months. Inter-branch transactions could take weeks. Customer complaints about lost drafts and delayed credits were mounting. Something had to change.

The push for computerization came from an unlikely source: V.P. Singh, the technocrat Finance Minister who would briefly become Prime Minister. Singh believed technology could cure the inefficiencies plaguing public sector banks. He found an eager partner in Bank of India's then Chairman and Managing Director, R.K. Talwar, a rare public sector banker who had spent time at the World Bank and understood global banking trends.

Talwar faced enormous resistance. The bank's powerful unions feared job losses—a computer could do the work of ten clerks. Senior managers, comfortable with existing systems, saw no need for change. The government itself was ambivalent, worried about the political fallout from automation. But Talwar persisted, arguing that technology would create new jobs even as it eliminated old ones.

The Mahalaxmi branch became Talwar's laboratory. He handpicked a team of young officers, sent them for training to IBM and TCS, and gave them carte blanche to reimagine banking. The results were revolutionary. Account opening that took days now took hours. Balance inquiries were instant. The ATM—India's first by a nationalized bank—operated 24/7, a concept so novel that the bank had to run advertisement campaigns explaining how to use it.

But the real innovation came in 1982, seven years before the Mahalaxmi experiment, when Bank of India had quietly pioneered something that would later become crucial for Indian banking: the Health Code System for credit monitoring. This wasn't glamorous technology—just a numerical coding system that classified loans based on repayment behavior. Yet it was arguably India's first systematic attempt at portfolio risk management, predating Basel norms by decades.

The international operations again proved catalytic for innovation. Bank of India had been a founding member of SWIFT (Society for Worldwide Interbank Financial Telecommunication) in India, connecting to the global financial messaging network in the early 1980s. This gave the bank capabilities in foreign exchange and trade finance that domestic peers couldn't match. The dealing room in Mumbai, equipped with Reuters terminals and direct lines to London and New York, looked more like a Wall Street trading floor than a government office.

The 1990s brought liberalization and with it, competitive pressure that made technology adoption existential rather than experimental. Private banks like HDFC and ICICI were building operations on modern technology platforms. Foreign banks were introducing phone banking and credit cards. Bank of India, despite its early start, found itself playing catch-up.

The core banking solution (CBS) implementation saga illustrates the challenges. Started in 1999, the project was supposed to connect all branches on a single platform within three years. It took nearly a decade. Every obstacle imaginable surfaced—vendor disputes, union resistance, infrastructure inadequacy (many rural branches lacked reliable electricity, let alone internet), and the sheer complexity of migrating decades of manual records to digital formats.

Yet there were bright spots. In 1997, the bank made its maiden public issue, using technology to manage what was then one of India's largest retail offerings. The issue, oversubscribed 5.7 times, demonstrated that public sector banks could access capital markets professionally. In 2008, the bank executed a Qualified Institutions Placement, raising ₹1,600 crore using sophisticated book-building technology that would have been impossible without its technology investments.

The internet banking launch in 2001 was another milestone, though it revealed the institution's split personality. The platform, developed by Infosys, was technically sophisticated—multi-factor authentication, real-time transactions, comprehensive services. But adoption was painfully slow. By 2005, less than 2% of the bank's customers used internet banking, compared to over 20% at private sector competitors.

The mobile banking journey was even more tortuous. Bank of India launched SMS banking in 2004, WAP-based mobile banking in 2008, and a smartphone app in 2012. Each iteration was late to market and clunky compared to competitors. The bank's technology teams, constrained by procurement rules and bureaucratic approvals, watched helplessly as nimbler rivals captured the digital generation.

By the late 2000s, a pattern had emerged: Bank of India could adopt technology but couldn't leverage it for competitive advantage. The bank had ATMs but fewer than private peers. It had internet banking but poor user experience. It had CBS but branches still demanded physical documents. Technology had become a cost center rather than a business enabler.

The numbers told the story. Despite spending over ₹2,000 crore on technology between 2000 and 2010, Bank of India's cost-to-income ratio remained stubbornly above 50%, compared to sub-40% for leading private banks. Customer acquisition costs were three times higher. Transaction processing times were twice as long. The early technology pioneer had become a digital laggard.

The fundamental problem wasn't technology but transformation. Bank of India had computerized existing processes rather than reimagining them. It had automated branches but not empowered them. It had connected systems but not integrated them. The bank was digital in form but analog in spirit—a challenge that would become even more acute as India entered the smartphone era and fintech disruption loomed.

VI. Modern Challenges & Transformation (2010s-Present)

The March 2020 lockdown announcement caught Bank of India's management in a crisis meeting. The RBI had just announced a moratorium on loan repayments, and the bank faced a decision that would define its pandemic response: should customers opt-in for relief, or should the moratorium be automatic? The bank chose automatic—a decision that seemed customer-friendly but would trigger a storm of controversy.

Bank of India implemented an automatic moratorium for all eligible borrowers without requiring a separate application procedure, automatically offering relief from servicing loan EMIs for the moratorium period and stalling all automated payments from March 1, 2020 to May 31, 2020. Customers who didn't want the moratorium had to actively opt-out—the opposite of what most banks did. The backlash was immediate. Affluent customers who could afford their EMIs found themselves automatically enrolled, accruing additional interest they hadn't asked for. The bank's customer service lines crashed under complaint volumes.

This episode crystallized Bank of India's modern predicament: good intentions undermined by poor execution, customer-centricity sabotaged by operational rigidity. It was a microcosm of the bank's broader challenges in the 2010s and beyond.

The decade had started promisingly. In FY2011, the bank reported a net profit of ₹3,046 crore with NPAs at a manageable 2.35%. The international operations were contributing healthily, technology investments were beginning to show results, and the bank seemed poised for sustainable growth. Then the wheels came off.

The infrastructure and power sector boom of the mid-2000s turned into a bust by 2012. Bank of India, like other public sector banks, had aggressively funded projects that now couldn't service their debt. By FY2016, gross NPAs had ballooned to 13.05%, among the highest in the industry. The bank reported its first loss in decades—₹6,089 crore in FY2018. The stock price collapsed from ₹400 in 2010 to under ₹50 by 2020.

The numbers tell a story of gradual recovery but persistent challenges. FY2023 saw the bank report income of ₹55,143 crore and a net profit of ₹4,023 crore, representing an 18.16% year-on-year growth. Operating profit surged 34%, suggesting improving operational efficiency. The bank's total business stood at ₹14.46 lakh crore, supported by 5,202 branches and 8,166 ATMs. Yet these improvements came from a low base and masked structural issues.

The competitive landscape had transformed beyond recognition. Private banks like HDFC and ICICI had built franchises worth 10-15 times Bank of India's market cap. New-age players like Kotak Mahindra leveraged technology to offer superior customer experience. Fintech companies were unbundling banking—payments to Paytm and PhonePe, lending to CRED and Slice, wealth management to Zerodha and Groww. Bank of India watched its market share in every profitable segment erode.

The digital transformation attempts revealed the institution's limitations. The bank launched BOI Mobile in 2012, but by 2020, it had less than 5 million active users compared to HDFC's 50 million. The UPI integration came late and performed poorly—transaction failures were three times the industry average. Young customers, the future of banking, saw Bank of India as their grandparents' bank—reliable but irrelevant.

Government ownership created unique challenges. Every loan above ₹50 crore required multiple committee approvals, making quick decisions impossible. Senior appointments were political, with chairmen changing every 2-3 years, preventing long-term strategic thinking. The bank was forced to participate in government schemes—Jan Dhan accounts, Mudra loans, loan melas—that generated negligible revenue but significant operational burden.

Yet there were bright spots. The bank's treasury operations, leveraging decades of expertise, consistently outperformed. The international franchise, though neglected, remained profitable, contributing 15% of total profits despite being less than 5% of assets. The rural and semi-urban network, built during the socialist era, provided a low-cost deposit base that private banks envied.

The asset quality improvement post-2018 showed the bank could execute when focused. Gross NPAs declined from 16.58% in FY2018 to 8.9% by FY2023. The provision coverage ratio improved to over 85%. Credit costs normalized. The bank seemed to have learned from its infrastructure lending mistakes, focusing on retail and MSME segments with better risk-adjusted returns.

The COVID-19 pandemic, despite the moratorium controversy, demonstrated some institutional strengths. The bank's conservative underwriting meant its portfolio weathered the crisis better than aggressive private lenders. The extensive branch network proved valuable when digital channels were overwhelmed. Government backing provided stability when private banks faced deposit runs.

But fundamental questions remained unanswered. With a market cap of ₹51,809 crore and a P/E of just 5.24, the market clearly didn't believe in the turnaround story. The ROE of 9.81% over three years suggested persistent efficiency challenges. The government's 73.4% ownership meant every strategic decision was filtered through political considerations.

As 2024 unfolds, Bank of India stands at a familiar crossroads. It has survived crisis and shown resilience. It has modernized in parts while remaining antiquated in others. It serves millions but excites few. The question isn't whether Bank of India can survive—government ownership ensures that. The question is whether it can thrive in an era where banking is becoming invisible, embedded in every digital interaction, and where century-old brands matter less than seamless user experience.

VII. Strategic Positioning & Competitive Landscape

The numbers paint a stark picture: Bank of India trades at a P/E of 5.24 while HDFC Bank commands 19.5. The market values every rupee of Bank of India's earnings at barely a quarter of what it pays for private sector banks. This isn't just a valuation discount—it's a vote of no confidence in the bank's ability to compete in modern India.

To understand this chasm, consider a simple comparison. In 2010, Bank of India and HDFC Bank had roughly similar loan books—around ₹2 lakh crore each. By 2024, HDFC Bank's loan book has grown to over ₹24 lakh crore while Bank of India struggles at ₹5.5 lakh crore. Same starting point, same market, vastly different outcomes. What explains this divergence?

The answer lies in strategic positioning—or more accurately, the lack thereof. Bank of India operates in three main segments: Treasury, Wholesale Banking, and Retail Banking. But unlike focused competitors, it's neither the best nor the most efficient in any segment. It's the classic "stuck in the middle" problem that strategy professors warn about.

In Treasury operations, the bank actually shows competence. Years of managing government securities, foreign exchange from international operations, and a sophisticated dealing room give it genuine expertise. The treasury contributed 35% of operating profits in FY2023 despite being just 20% of assets. But this is a volatile, low-growth business that can't drive the franchise.

Wholesale Banking tells a different story. The bank's corporate loan book, scarred by the infrastructure lending crisis, has barely grown in five years. While private banks cherry-pick the best corporates with competitive pricing and quick decisions, Bank of India gets what's left—often the borrowers that others rejected. The government ownership means it can't say no to certain "priority" projects, regardless of commercial merit.

The relationship management model in wholesale banking reveals deeper issues. A senior executive at a major conglomerate recently shared: "With HDFC or ICICI, I get the regional head on phone within hours. With Bank of India, it takes weeks to get past bureaucracy." The bank was indeed one of the big banks nationalized in 1969, but that legacy has become a burden in corporate banking where speed and flexibility matter.

Retail Banking presents the starkest contrasts. Bank of India has 5,202 branches—an enviable distribution network. Yet its retail loan book is a fraction of banks with half the branches. The average branch productivity is ₹27 crore in deposits versus ₹65 crore for private banks. The bank has customers but not relationships, presence but not engagement.

The CASA (Current Account Savings Account) ratio tells its own story. At 44%, it's respectable but not exceptional. More concerning is the composition—largely government salary accounts and rural deposits that are price-sensitive and prone to flight when alternatives emerge. The bank hasn't cracked the affluent urban segment that drives profitability in retail banking.

The international operations, once the crown jewel, have become an orphaned asset. Contributing 15% of profits but getting minimal investment, the overseas branches operate like time capsules. While Chinese and Middle Eastern banks aggressively expand in Bank of India's traditional markets, it watches market share erode. The NRI banking franchise, built over decades, is being poached by private banks offering superior digital services.

Against this backdrop, the competition has transformed the industry. State Bank of India, despite its public sector burden, has leveraged scale to build a digital platform (YONO) with 50 million users. ICICI Bank, once written off after its 2008 crisis, has reinvented itself as a technology-first institution. HDFC Bank maintains its execution machine reputation, growing steadily regardless of market conditions.

The new-age threats are even more concerning. Paytm Payments Bank reached 100 million accounts in three years—it took Bank of India a century. WhatsApp Pay processes more transactions daily than Bank of India's entire digital platform. These aren't competitors for the same business; they're making the business itself irrelevant.

Yet Bank of India possesses underappreciated strengths. The government ownership, while constraining, provides stability that becomes valuable during crises. The rural network, expensive to maintain, offers access to India's next consumption wave. The international presence, though underutilized, could be leveraged as Indian businesses globalize.

The bank's credit portfolio composition reveals both challenges and opportunities. Agriculture constitutes 18% of advances, well above the regulatory requirement but with thin margins. MSME lending at 25% offers better returns but higher operational costs. Retail loans at 30% are growing but from a low base. The remaining corporate book, though cleaned up, lacks the blue-chip names that drive profitable wholesale banking.

The efficiency metrics are sobering. Cost-to-income ratio at 52% compares poorly with private banks at 35-40%. Employee cost per branch at ₹3.2 crore is double that of new private banks. Technology spending at 5% of operating expenses lags the 8-10% at digital-focused competitors. These aren't just numbers—they represent structural disadvantages that compound over time.

The market's valuation discount reflects these realities. Investors see a bank that's too big to fail but too constrained to succeed. The low P/E isn't a buying opportunity—it's the market's assessment that earnings won't grow and returns won't improve. The 9.81% ROE over three years, barely covering cost of capital, validates this pessimism.

Strategic options exist but require courage to execute. The bank could focus on being the government's financial inclusion vehicle, accepting lower returns for social impact. It could leverage international operations to become the "India trade bank" for companies going global. It could transform select urban branches into wealth management centers, competing for affluent customers. But each option requires choices the current governance structure seems incapable of making.

The competitive landscape will only get tougher. Digital-only banks are coming. Foreign banks will get more licenses. Fintech will continue unbundling profitable products. Chinese banks might enter if regulations permit. In this environment, Bank of India's current strategy—trying to be everything to everyone while excelling at nothing—guarantees continued mediocrity.

VIII. Playbook: Lessons from a Century of Banking

After 118 years, what has Bank of India taught us about building and sustaining a financial institution? The lessons aren't always what MBA textbooks prescribe, but they're grounded in the messy reality of Indian banking.

Lesson 1: Trust Compounds Slower Than Technology But Lasts Longer

In 1921, when Bank of India managed the BSE clearing operations, trust was earned through personal relationships and community standing. The bank's early directors literally put their family names behind every loan. This relationship banking model seems quaint in the age of credit scores and machine learning, but it reveals an enduring truth: trust in financial services isn't just about algorithms—it's about presence and permanence.

Consider the 2008 financial crisis or the 2020 pandemic. Customers didn't rush to withdraw deposits from Bank of India, despite its weak financials. Why? Because three generations of families had banked there. The branch manager knew their stories. The government ownership provided psychological comfort. This "trust moat" is why Bank of India still manages ₹8.5 lakh crore in deposits despite inferior service and technology.

Lesson 2: Political Alignment Is a Double-Edged Sword

Bank of India's history is inseparable from India's political evolution. Founded during the Swadeshi movement, it benefited from nationalist sentiment. Nationalization in 1969 made it one of the major private banks taken over by the government, giving it resources for massive expansion but destroying its commercial culture. Each political era brought opportunities and constraints—socialist banking mandates, liberalization pressures, inclusion directives.

The lesson? In emerging markets, financial institutions can't be politically agnostic. But there's a difference between political awareness and political capture. Bank of India's mistake wasn't engaging with politics but becoming subordinate to it. The best-performing banks maintain constructive government relationships while preserving operational independence.

Lesson 3: International Expansion Is About Timing, Not Just Ambition

Bank of India's 1946 decision to open in London, before independence, was audacious. It captured the Indian diaspora market early, built foreign exchange capabilities, and created global networks. But timing mattered more than strategy. The bank expanded internationally when competition was minimal, regulations were forming, and the diaspora needed connection to home.

Today's equivalent isn't opening more foreign branches—it's being early in digital cross-border services, crypto-asset management, or climate finance. The playbook isn't about international presence but international relevance. Bank of India's mistake was treating international operations as branch banking abroad rather than evolving with global financial flows.

Lesson 4: Technology Adoption Versus Transformation

The 1989 computerized branch at Mahalaxmi was revolutionary, but it revealed a pattern: Bank of India could adopt technology but couldn't transform through it. The bank automated existing processes rather than reimagining them. It digitized paperwork instead of eliminating it. It brought computers to branches but didn't change how branches operated.

The lesson extends beyond banking. Large organizations often mistake technology procurement for digital transformation. They buy systems but don't change systems. They upgrade infrastructure but not mindsets. True transformation requires destroying existing processes, not just digitizing them—something established institutions find almost impossible.

Lesson 5: The Dual Mandate Trap

Since nationalization, Bank of India has struggled with dual mandates: be profitable but serve social objectives; expand credit but maintain asset quality; support government programs but compete with private banks. This isn't unique to Indian public sector banks—many institutions globally face similar tensions.

The successful ones don't try to optimize both simultaneously. They sequence priorities, making explicit trade-offs. China's state banks focused on infrastructure lending for two decades, accepting lower returns, then shifted to commercial objectives. DBS in Singapore transformed from development bank to regional champion by clearly separating phases. Bank of India never made these hard choices, trying to be everything simultaneously and excelling at nothing.

Lesson 6: Capital Allocation in Constrained Environments

Operating with government ownership means capital allocation follows different rules. Bank of India couldn't freely raise equity, pay market salaries, or close unprofitable branches. Yet within these constraints, choices existed. The bank could have focused resources on profitable segments, invested heavily in specific capabilities, or built centers of excellence.

Instead, it spread resources evenly—democratic but inefficient. Every region got investment, every segment got attention, every initiative got funding. This "peanut butter" approach ensured no area excelled. The lesson? Constraints require more strategic focus, not less. When you can't do everything, choosing what not to do becomes crucial.

Lesson 7: Risk Management Through Cycles

Bank of India's 118-year history spans multiple economic cycles—colonial extraction, independence upheaval, socialist stagnation, liberalization boom, infrastructure bust, digital disruption. The bank survived all of them, though not always profitably. What explains this resilience?

Conservative culture helped—the bank was late to every lending boom and thus missed some busts. Government backing provided capital during crises. Diversification across geographies and segments prevented concentration risks. But most importantly, the institution maintained organizational memory of past cycles, making it cautious about new ones.

The infrastructure lending crisis of the 2010s broke this pattern. The bank forgot historical lessons, chasing growth in unfamiliar segments. The ₹6,089 crore loss in FY2018 was the price of amnesia. Risk management isn't just about models and metrics—it's about institutional memory and cultural caution.

Lesson 8: The Talent Paradox

Bank of India once attracted India's best talent—in 1906, working for an Indian bank was prestigious and patriotic. By 2024, it's neither. The bank faces a talent crisis: unable to pay competitively, promote meritocratically, or offer exciting careers. Young engineers join Google, not government banks.

Yet the bank produced leaders who went on to run other institutions, regulatory bodies, even become Finance Ministers. This paradox—poor employer brand but strong alumni network—reveals something important. Institutions can be great training grounds even when they're not great employers. Bank of India inadvertently became India's banking university, training talent for the entire sector.

These lessons don't provide a formula for success, but they offer something more valuable: wisdom from failure and resilience. Bank of India's journey shows that institutional survival requires more than good strategy—it needs adaptability, patience, and occasionally, sheer luck. In a rapidly changing world, these qualities matter more than any playbook.

IX. Bear vs. Bull Case & Investment Analysis

The investment case for Bank of India presents a fascinating study in contrasts—a bank with ₹13.24 lakh crore in total business trading at just 0.6 times book value, while private peers trade at 2-3 times. Is this the market missing value or accurately pricing mediocrity?

The Bull Case: Deep Value with Hidden Catalysts

The optimists start with valuation. At ₹51,809 crore market cap against a book value of ₹86,000 crore, Bank of India trades at a 40% discount to its accounting value. The bank owns real estate in prime urban locations worth multiples of book value. The international operations, if separately valued, could be worth ₹15,000-20,000 crore alone. Even liquidation would yield more than the current market cap.

The operational turnaround is gaining momentum. Net profit grew 18.16% year-on-year to ₹4,023 crore in FY2023, with operating profit surging 34%. Asset quality has dramatically improved—gross NPAs declined from 16.58% in FY2018 to 8.9% by FY2023. The provision coverage ratio at 85% suggests the worst of the asset quality pain is behind.

The franchise value remains underappreciated. With 5,202 branches and 8,166 ATMs, Bank of India has distribution that would cost ₹50,000 crore to replicate. The customer base of 120 million, even if poorly monetized, represents enormous latent value. The CASA ratio at 44% provides a low-cost funding advantage that becomes more valuable as rates rise.

Government backing provides a floor. Unlike private banks that can fail, Bank of India enjoys implicit sovereign support. This "too big to fail" status means catastrophic risk is minimal. The government's 73.4% ownership might constrain operations but guarantees survival. For risk-averse investors, this safety net has value.

The India growth story benefits all banks eventually. With credit-to-GDP at 55% versus 150% in developed markets, the runway for growth is enormous. As formalization accelerates and financial inclusion deepens, even inefficient banks will grow. Bank of India doesn't need to win—it just needs to participate.

Hidden assets could surprise. The bank's stake in Star Health Insurance, Universal Sompo, and other subsidiaries aren't fully valued. The international operations, particularly in high-growth Asian markets, could see revaluation. The digital initiatives, though late, might finally gain traction with younger customers.

The Bear Case: Structural Decline Masked by Cyclical Recovery

The pessimists see value traps, not value opportunities. The low valuation reflects permanent impairment, not temporary dislocation. Bank of India's 9.81% ROE over three years barely covers cost of equity. Why pay any premium for a business that doesn't create economic value?

The competitive position continues deteriorating. Market share in profitable segments—urban retail, corporate banking, wealth management—keeps declining. The bank wins only in mandated lending where returns are negligible. Every year, the gap with private banks widens. Technology, talent, and brand disadvantages compound over time.

Government ownership is a permanent handicap. Political interference in lending decisions, inability to pay market salaries, forced participation in uneconomic schemes—these aren't temporary issues but structural realities. The 73.4% government ownership means every decision gets politicized. No strategic investor will partner with these constraints.

The asset quality improvement is cyclical, not structural. NPAs declined because the economy recovered and corporate stress reduced. But Bank of India hasn't fixed its underwriting, risk management, or collection processes. The next downturn will reveal the same weaknesses. The infrastructure lending mistakes of the 2010s will repeat in different forms.

Digital disruption makes physical distribution worthless. The 5,202 branches aren't assets—they're liabilities requiring constant investment with declining relevance. Young customers don't visit branches. UPI makes bank accounts interchangeable. Fintechs unbundle every profitable product. The extensive network becomes an albatross, not advantage.

The talent exodus is accelerating. The best employees leave for private sector opportunities. New graduates avoid public sector banks. The average employee age exceeds 45, with retirement waves approaching. The institutional knowledge walks out while fresh thinking doesn't walk in. This human capital crisis can't be fixed with current constraints.

The Realistic Assessment

The truth lies between extremes. Bank of India isn't going bankrupt—government ownership prevents that. But it's also not going to generate superior returns—structural constraints prevent that too. It's a widow-and-orphan stock, offering stability without growth, survival without success.

For value investors, the risk-reward is asymmetric but unclear. The downside seems limited given the discount to book value and government backing. But the upside requires either privatization (politically unlikely) or dramatic operational improvement (organizationally difficult). The stock could remain cheap indefinitely—value without catalyst is just dead money.

For growth investors, Bank of India offers nothing compelling. The ROE won't exceed 12% sustainably. Market share will continue eroding. Technology gaps will widen. Better opportunities exist in private banks, small finance banks, or fintech platforms. Why invest in yesterday's infrastructure when tomorrow's winners are accessible?

For yield investors, there's modest appeal. The dividend yield around 3-4% beats fixed deposits. The payout is sustainable given improved profitability. Government ownership ensures dividend continuity. But this is a bond-like return from equity-like risk—hardly attractive.

The investment case ultimately depends on timeframe and temperament. For traders, the volatility offers opportunities—the stock can move 20% on regulatory changes or quarterly results. For long-term investors, the structural challenges outweigh cyclical improvements. For indexers, it's a small weight in a large sector—ignorable but includable.

The market's verdict seems appropriate: Bank of India is neither dramatically undervalued nor obviously overvalued. It's fairly priced for what it is—a declining franchise with government support, improving operations but deteriorating competitiveness, valuable assets but poor returns. The 5.24 P/E isn't a bargain—it's what you pay for businesses that don't grow and barely earn their cost of capital.

X. Looking Forward: The Next Chapter

As Bank of India approaches its 120th anniversary in 2026, the institution faces an existential question: what is its purpose in an India racing toward a $5 trillion economy? The answer will determine whether the next decade brings renaissance or further decline.

Digital Transformation: Beyond Catch-Up

The bank's digital strategy reads like a 2015 playbook executed in 2024—mobile apps, internet banking, UPI integration. But digital transformation in 2030 won't be about channels; it'll be about embedded finance, artificial intelligence, and data monetization. Bank of India needs to leapfrog, not catch up.

Imagine Bank of India partnering with India Stack to become the financial backbone for government services—direct benefit transfers, subsidy management, tax collections. The bank's government relationship, usually a handicap, becomes an advantage. Or consider leveraging the rural network for last-mile delivery of financial services, using branch managers as relationship nodes in a digital web rather than transaction processors.

The international operations could be reimagined for the digital age. Instead of physical branches serving walk-in NRIs, build a global digital platform for the 32 million Indian diaspora. Offer everything from nostalgic fixed deposits to sophisticated wealth management, from education loans for children studying abroad to retirement planning for returning Indians. The trust and heritage that seem outdated domestically resonate powerfully internationally.

The Privatization Question

Privatization speculation surrounds every public sector bank, but Bank of India presents unique challenges. The government's 73.4% stake is worth ₹38,000 crore at current prices—substantial but not game-changing for fiscal math. More importantly, privatizing a bank with 5,202 branches and 50,000 employees would be politically explosive.

A more realistic scenario involves partial privatization—reducing government stake to 51% or even 26%, bringing in strategic investors, and granting operational autonomy. The Life Insurance Corporation model offers a template: government ownership with professional management and market discipline. But this requires political will that hasn't materialized in two decades of discussion.

The alternative is "privatization by stealth"—gradually improving governance, hiring laterally from private sector, partnering with fintechs for technology, and operating commercially within government ownership. DBS transformed from Singapore's development bank to regional champion without formal privatization. Chinese state banks became globally competitive while remaining government-owned. The ownership structure matters less than operational freedom.

Role in India's $5 Trillion Ambition

India's goal of becoming a $5 trillion economy by 2027-28 requires credit growth of 12-15% annually. Bank of India, with its ₹5.5 lakh crore loan book, could contribute ₹60,000-80,000 crore in annual credit growth. But where should this capital flow?

The obvious answer—infrastructure and manufacturing—carries ghosts of past mistakes. The bank's infrastructure lending crisis of the 2010s cost ₹50,000 crore in write-offs. Yet India needs $1.4 trillion in infrastructure investment by 2030. Can Bank of India participate without repeating history?

The solution lies in different structures—co-lending with development financial institutions, taking smaller tickets in syndicated deals, focusing on operational infrastructure rather than greenfield projects. The bank could specialize in renewable energy financing, leveraging government climate commitments. Or become the primary banker for PLI (Production Linked Incentive) scheme beneficiaries, using government backing to mitigate risks.

Fintech Collaboration Versus Competition

The fintech threat is existential. Paytm has more active users than Bank of India has customers. PhonePe processes more daily transactions than the bank's entire digital platform. But competition could become collaboration with the right mindset shift.

Bank of India possesses what fintechs desperately need—banking license, regulatory compliance, balance sheet capacity. Fintechs have what the bank lacks—technology, user experience, innovation speed. Strategic partnerships could combine strengths: Bank of India provides financial infrastructure while fintechs manage customer interface.

Consider a radical model: Bank of India as a "Banking-as-a-Service" platform. License its banking capabilities to hundreds of fintechs, earning fee income without customer acquisition costs. Transform from a B2C bank competing unsuccessfully for retail customers to a B2B2C platform powering others' growth. The extensive branch network becomes API endpoints rather than cost centers.

ESG and Sustainable Banking

Environmental, Social, and Governance considerations aren't just compliance requirements—they're strategic opportunities. Bank of India's public sector mandate naturally aligns with social objectives. The challenge is making this commercially viable.

Green financing offers possibilities. India needs $10 trillion for net-zero transition by 2070. Bank of India could become the "Transition Finance Bank," specializing in funding brown-to-green conversions rather than pure green projects. The government backing helps absorb transition risks that private banks won't take.

Financial inclusion remains undermonetized. The bank opened 40 million Jan Dhan accounts but earns negligible revenue from them. What if these became gateways for micro-insurance, micro-pensions, and micro-investments? Partner with insurtechs and wealthtechs to offer simple products that generate small tickets but massive volumes.

Success Metrics for 2030

What would success look like for Bank of India in 2030? Not becoming HDFC Bank—that ship has sailed. But perhaps:

- The Inclusion Champion: 200 million customers profitably served through digital-physical hybrid models, generating 15% ROE from previously unbanked segments

- The Government's Digital Treasurer: Processing 50% of government transactions, managing Direct Benefit Transfers, and becoming indispensable for Digital India

- The Diaspora Bank: $100 billion in NRI deposits, 10 million global Indian customers, and the primary financial bridge between India and its diaspora

- The Transition Financier: ₹2 lakh crore in sustainable finance assets, leading India's green transition while managing stranded asset risks

- The Platform Bank: Powering 500 fintech partners, earning ₹5,000 crore in fee income without direct customer acquisition

None of these scenarios require Bank of India to beat private banks at their own game. Instead, they leverage unique strengths—government relationship, extensive network, international presence, public purpose—while acknowledging limitations.

The next chapter won't be about recovering past glory or competing head-to-head with nimbler rivals. It'll be about finding a unique position in India's financial ecosystem where Bank of India's peculiar mix of strengths and constraints creates value. The institution that pioneered Indian banking must now pioneer its own reinvention.

XI. Recent News

Q3FY25 Results Show Continued Recovery

Bank of India's net profit rose by 35% year-on-year to Rs 2,517 crore during the third quarter ended December 2024 (Q3FY25), aided by better net interest income and gains from treasury operations. Sequentially, the Mumbai-based lender's net profit rose by 6% from Rs 2,374 crore in September quarter of 2024.

The latest quarterly results demonstrate Bank of India's ongoing operational recovery, though challenges remain. Net interest income expanded 11% year-on-year to Rs 6,070 crore in Q3FY25 compared to Rs 5,463 crore in the same quarter of the previous year. Advances grew by 15.3% year-on-year to Rs 5.65 trillion in Q3FY25, with retail advances growing by 21.22% year-on-year to Rs 1.27 trillion. Total deposits increased by 12.29% year-on-year to Rs 7.07 trillion.

Asset quality continues to improve significantly. Gross NPAs declined to 3.69% in December 2024 from 5.35% in December 2023. Net NPAs also declined to 0.85% in December 2024 from 1.41% in December 2023. The provision coverage ratio, including written-off accounts, stood at 92.48% in December 2024, compared to 89.95% a year ago.

The bank is maintaining its guidance for a net profit of Rs 8,000 crore for the current financial year (FY25). This ambitious target suggests management confidence in sustained operational improvement, though achieving it would require exceptional fourth-quarter performance.

Leadership Stability Under Rajneesh Karnatak

Rajneesh Karnatak has been the Managing Director and Chief Executive Officer of the bank since 2023. His appointment brought continuity after a period of frequent leadership changes that had hampered strategic consistency. He also serves as a Director with UBI Services Ltd., UBI (UK) Limited, PNB Housing Finance Ltd., and India SME Asset Reconstruction Company Limited. Earlier, he served as a Chief General Manager at Punjab National Bank.

Under Karnatak's leadership, the bank has focused on three key priorities: asset quality cleanup, digital transformation acceleration, and retail portfolio expansion. The quarterly results suggest these initiatives are gaining traction, though execution speed remains a concern given competitive pressures.

Competitive Dynamics in the PSB Sector

The public sector banking landscape continues to evolve with consolidation and digitalization themes dominating. State Bank of India maintains its dominance with sophisticated digital platforms, while smaller PSBs like Bank of India struggle to differentiate. The government's push for privatization has stalled, leaving banks in strategic limbo—unable to operate with full commercial freedom but expected to compete with private players.

Recent regulatory changes have added both opportunities and challenges. The RBI's emphasis on governance reforms benefits well-managed banks, but compliance costs burden all PSBs equally. The push for financial inclusion through digital channels plays to Bank of India's branch network strengths, provided it can effectively digitize these touchpoints.

Market Performance and Investor Sentiment

The stock's recent performance reflects continued skepticism despite operational improvements. Trading around ₹98-100 per share, the bank remains valued at steep discounts to both book value and peer multiples. Institutional investors remain cautious, citing governance concerns and limited growth visibility. Retail investors show sporadic interest during result announcements but lack conviction for long-term holdings.

The disconnect between improving fundamentals and stagnant valuations highlights the market's structural concerns about PSB banks. Until governance reforms accelerate or privatization prospects clarify, Bank of India will likely trade at persistent discounts regardless of quarterly performance.

XII. Links & Resources

Official Bank Resources

- Annual Reports: bankofindia.co.in/financial-result

- Investor Presentations: Available on the bank's investor relations section

- Regulatory Filings: BSE and NSE websites for quarterly disclosures

- Historical Archives: Bank of India Museum and Archives, Mumbai

Regulatory and Government Documents

- RBI Reports on Public Sector Banks: rbi.org.in

- Banking Regulation Acts and Amendments

- Nationalization of Banks Act, 1969

- Government of India Banking Reform Papers

- Parliamentary Standing Committee Reports on Banking

Industry Research and Analysis

- ICRA, CRISIL, and CARE Ratings reports on Bank of India

- Broker research from domestic institutions (ICICI Direct, Motilal Oswal, etc.)

- International banking comparisons from Moody's and S&P

- McKinsey Global Institute reports on Indian banking

- Boston Consulting Group studies on digital transformation in banking

Books and Academic Resources

- "The Evolution of State Bank of India" by A.K. Bagchi (for context on PSB history)

- "Banking on the State: The Political Economy of Public Savings Banks" (comparative analysis)

- "India's Banks: The Road Ahead" by Tamal Bandyopadhyay

- Various papers from Economic and Political Weekly on bank nationalization

- IIM and ISB case studies on Indian banking transformation

Technology and Digital Banking Resources

- Fintech reports from KPMG, PwC, and EY India

- NPCI documentation on UPI and digital payments infrastructure

- World Bank reports on financial inclusion in India

- BIS papers on central bank digital currencies and their implications

Historical and Archival Sources

- Reserve Bank of India Museum, Mumbai

- Bombay Stock Exchange historical records

- Times of India and Economic Times archives from 1906 onwards

- British Library India Office Records (for colonial banking history)

- Nehru Memorial Museum and Library (for post-independence banking policy)

International Banking Resources

- Bank for International Settlements reports on emerging market banks

- World Bank Global Findex Database

- IMF Financial Sector Assessment Programs for India

- Asian Development Bank studies on financial sector development

Conclusion: A Century of Paradoxes

Bank of India's 118-year journey reads like a chronicle of Indian capitalism itself—born from nationalist fervor, shaped by socialist ideology, challenged by liberalization, and now grappling with digital disruption. It's a story of an institution that pioneered Indian banking, went global before independence, got nationalized at its peak, and now struggles to find relevance in an era it helped create.

The numbers tell a sobering tale. A market capitalization of ₹51,809 crore for an institution managing ₹13.24 lakh crore in business. A P/E ratio of 5.24 when private peers command multiples of 15-20. An ROE of 9.81% that barely covers cost of capital. These metrics suggest the market has written off Bank of India as a value destroyer, not creator.

Yet this verdict seems both harsh and incomplete. The bank's recent performance—35% profit growth in Q3FY25, NPAs down to 3.69% from double digits, provision coverage above 92%—indicates operational recovery. The franchise value remains substantial: 5,202 branches, 120 million customers, presence in 15 countries. The government backing provides stability that becomes valuable during crises.

The fundamental question isn't whether Bank of India can survive—government ownership guarantees that. It's whether the institution can transcend its structural limitations to become relevant again. Can a bank conceived in 1906 to serve Indian merchants transform itself for Indians born after 2000? Can an organization shaped by decades of political control develop commercial instincts? Can a culture built on compliance embrace innovation?

History suggests institutions rarely transform themselves voluntarily. External shocks—technological disruption, regulatory changes, competitive threats—force evolution. For Bank of India, all three are converging. Fintech is unbundling profitable products. Regulations are tightening governance. Private banks are capturing market share. The next decade will determine whether these pressures catalyze renaissance or accelerate decline.

The investment case remains problematic. Value investors see discounts but no catalysts. Growth investors see an eroding franchise. Income investors find modest yields with equity risks. The stock seems destined to remain a perpetual "deep value" play—cheap for good reasons, unlikely to re-rate without fundamental change.

Yet Bank of India's story contains lessons beyond investment returns. It demonstrates how institutions reflect their times—entrepreneurial during the freedom movement, expansionist during socialism, struggling during liberalization. It shows how government ownership creates unique dynamics—social mandates competing with commercial objectives, political interference undermining professional management. It reveals how legacy can be both asset and liability—trust built over generations, but cultures resistant to change.

Perhaps Bank of India's greatest contribution isn't what it achieves but what it represents—the messy reality of Indian development where public purpose and private profit perpetually negotiate, where modern aspirations confront historical legacies, where global ambitions meet local constraints. It's a mirror reflecting India's own journey from colony to emerging power, complete with achievements and frustrations, progress and setbacks.

As Bank of India approaches its 120th year, its fate seems increasingly binary. Either it leverages unique strengths—government relationships, rural presence, international operations—to carve out a differentiated position. Or it continues declining into irrelevance, a zombie bank sustained by government support but offering little value to stakeholders.

The romantic might hope for transformation—a dramatic turnaround that restores past glory. The realist expects continued mediocrity—gradual improvement insufficient to excite investors or customers. The pessimist foresees eventual absorption—merger with another PSB or quiet wind-down of operations.

Most likely, Bank of India will muddle through, neither failing spectacularly nor succeeding brilliantly. It will remain what it has become—a second-tier public sector bank, important enough to preserve but not significant enough to reform, profitable enough to survive but not competitive enough to thrive. A monument to what Indian banking was, rather than what it could be.

In the end, Bank of India's century-long journey offers no clear lessons, only paradoxes. An institution can be historically important yet currently irrelevant. A bank can serve millions yet excite none. A business can have valuable assets yet create no value. These contradictions aren't failures of analysis but reflections of reality—the complex, often irrational nature of institutions shaped more by history than strategy, more by politics than economics, more by inertia than intention.

The story continues, but the ending seems increasingly predictable. Bank of India will celebrate its 125th anniversary, its 150th perhaps. It will adapt enough to survive, never enough to excel. It will remain a fixture in India's financial landscape—visible but not vital, present but not powerful. A bank that once symbolized Indian ambition, now embodying Indian acceptance of "good enough."

This isn't tragedy—tragedy requires greatness fallen. It's something more mundane and perhaps more poignant: potential unrealized, promises unfulfilled, an institution that could have been extraordinary settling for existence. Bank of India's next chapter won't be written in boardrooms or stock prices but in the quiet acceptance that not all stories have heroic endings, that sometimes survival itself is achievement enough.

For investors, customers, and observers, Bank of India offers a sobering reminder: in the long arc of institutional life, most organizations don't transform or collapse—they simply persist, carried forward by momentum rather than mission, sustained by structure rather than strategy. It's neither inspiring nor catastrophic, just the ordinary reality of how most institutions age—slowly, steadily, and with diminishing relevance.

The bank that once pioneered Indian finance now pioneers nothing except perhaps the art of institutional endurance. And in a rapidly changing world where disruption is celebrated and transformation is expected, that might be the most Indian story of all—the quiet persistence of an institution that refuses to die but has forgotten how to truly live.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube