UCO Bank: The Phoenix Rising from India's Banking Crisis

I. Introduction & Episode Roadmap

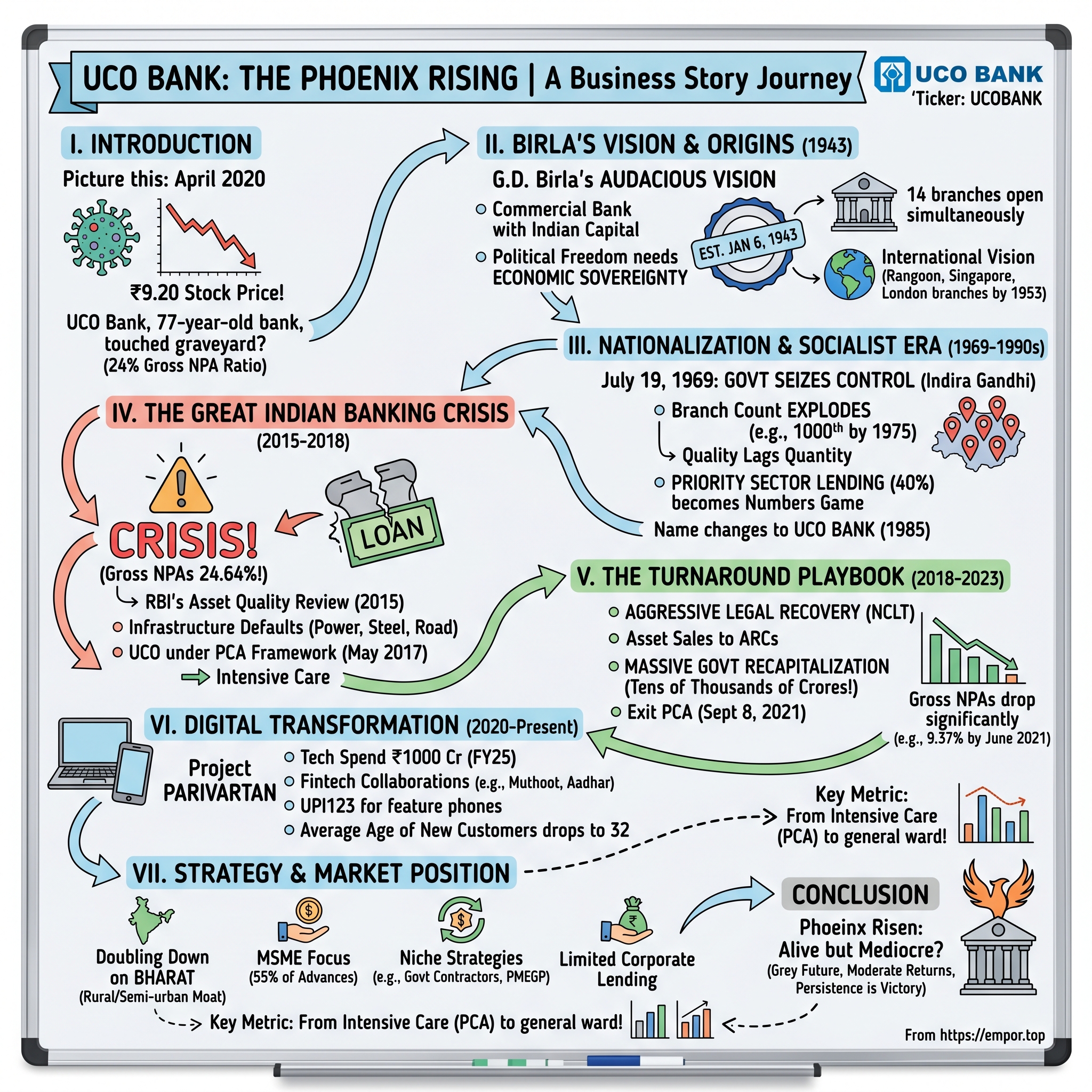

Picture this: April 2020. The world is gripped by pandemic panic, markets are in freefall, and in the depths of India's financial markets, a 77-year-old bank's stock touches ₹9.20—a price that values the entire institution at less than many Mumbai apartments. UCO Bank, once the proud creation of industrial titan G.D. Birla, seemed destined for the graveyard of failed public sector banks.

Fast forward to today. That same bank commands a market capitalization of ₹41,305 crore, manages total business of ₹5.13 lakh crore, and has engineered one of the most dramatic turnarounds in Indian banking history. How does a bank go from a grotesque 24% gross NPA ratio—essentially meaning one in four loans had gone bad—to becoming profitable and growing again?

This is the story of UCO Bank, the only Government of India-owned bank still headquartered in East India, nestled in the cultural capital of Kolkata. It's a tale that spans India's independence movement, socialist banking experiments, liberalization, a near-death experience during the great NPA crisis, and an unlikely resurrection through digital transformation and sheer governmental will.

The UCO story isn't just about banking metrics and regulatory frameworks. It's about how institutions reflect the nations they serve—how a bank born from the Quit India movement would embody both the aspirations and contradictions of independent India. It's about what happens when political imperatives collide with financial reality, when good intentions create bad loans, and when a crisis becomes so severe that failure isn't an option because the fallout would be too catastrophic.

For investors studying Indian financials, UCO presents a fascinating paradox: a bank that by all traditional metrics should have been wound down, yet survived through a combination of government support, regulatory forbearance, and management grit. Its recovery offers lessons about crisis management, the role of state ownership in banking, and the peculiar dynamics of "too big to fail" in an emerging market context.

Our journey begins in 1943, in the midst of World War II and India's freedom struggle, when a visionary industrialist decided that political independence meant nothing without economic sovereignty...

II. G.D. Birla's Vision & The Quit India Origins (1943–1969)

The year was 1942. The Quit India movement had erupted across the subcontinent, with Gandhi's call for immediate independence echoing through the streets. In this cauldron of nationalist fervor, Ghanshyam Das Birla—industrialist, freedom fighter, and close confidant of Gandhi—was contemplating a different kind of revolution. While others fought with protests and civil disobedience, Birla would fight with capital and commerce.

G.D. Birla understood something fundamental: political freedom without economic sovereignty was meaningless. Foreign banks—Grindlays, Chartered, Lloyd's—dominated India's financial landscape, their loyalties flowing toward London rather than Lucknow. Indian businesses struggled for credit, their applications scrutinized through colonial lenses, their ambitions constrained by foreign gatekeepers. Birla's vision was audacious yet simple: create a commercial bank with Indian capital, Indian management, and Indian priorities.

On January 6, 1943, United Commercial Bank was born with ₹2 crore in issued capital (₹1 crore paid up)—substantial money for the time, raised entirely from Indian investors. But what happened next was unprecedented in Indian banking history. Instead of the cautious, single-branch opening typical of new banks, UCB launched with explosive ambition: 14 branches opened simultaneously across India, from Calcutta to Bombay, Delhi to Madras. This wasn't just expansion; it was a declaration of intent.

The timing seemed insane. World War II raged on. The Bengal famine was devastating eastern India. Political uncertainty clouded the future. Yet Birla pressed forward, driven by an almost messianic belief that India's economic awakening couldn't wait for perfect conditions. He recruited talent aggressively, poaching managers from established banks with promises of building something uniquely Indian. The bank's early advertisements proudly proclaimed: "By Indians, For Indians. "What distinguished United Commercial Bank from other Indian financial institutions of the era was its ambition to match foreign banks at their own game. G.D. Birla, during the Quit India movement of 1942, conceived the idea of organising a commercial bank with Indian capital and management, and within the year the Bank opened 14 branches—an unprecedented pace of expansion for any Indian bank.

The international vision manifested early. By 1947, just four years after inception and in the very year of independence, UCB had established a branch in Rangoon. Singapore followed in 1951, Hong Kong in 1952, and remarkably, London in 1953—barely a decade after founding, this Indian bank was operating in the heart of the former colonial empire. This wasn't mere symbolism; it was strategic positioning for the post-colonial trade flows that Birla anticipated would define Asia's economic future.

The bank's early years coincided with tumultuous times. The partition of India in 1947 devastated its branch network in what became Pakistan. The Bank had several flourishing branches in Sind, Punjab and the North Western Provinces, many of which were lost overnight. Yet UCB persevered, compensating for western losses with aggressive eastern expansion. By 1946, confident in its trajectory, the subscribed capital was increased from Rs.2 crore to Rs. 4 crore, thereby increasing the paid-up capital from Rs.1 crore to Rs.2 crores.

The Birla touch was evident in UCB's operational philosophy. Unlike the conservative, bureaucratic approach of British banks, UCB pioneered relationship banking—branch managers were empowered to make quick decisions, loans were sanctioned based on character assessments alongside collateral, and the bank actively courted small and medium enterprises that foreign banks ignored. This wasn't charity; it was calculated risk-taking based on intimate knowledge of local markets. By the 1960s, UCB had emerged as a formidable mid-sized bank. By the late 1960s, the United Commercial Bank had thousands of branches in India, and had expanded into Singapore, Hong Kong, London and Malaysia. The international presence wasn't ornamental—these branches facilitated trade finance, foreign exchange operations, and served the growing Indian diaspora. The London branch, in particular, became a crucial node for Indian businesses seeking capital and connections in global markets.

Yet beneath this success lay tensions that would soon explode. The bank's ownership structure remained concentrated among industrialist families, its lending patterns favored established businesses, and despite Birla's nationalist origins, UCB's culture had grown increasingly elite. Rural India, where the vast majority lived, remained largely unbanked. This contradiction—between the rhetoric of serving India and the reality of serving India's privileged—would soon attract political attention.

The stage was set for a dramatic transformation. In the late 1960s, Prime Minister Indira Gandhi was consolidating power, pushing a populist agenda that promised to bring banking to the masses. For UCB and other private banks, the writing was on the wall. The era of gentlemanly capitalism, of banking as a private club for industrialists and traders, was about to end abruptly...

III. Nationalization & The Socialist Banking Era (1969–1990s)

July 19, 1969. In a single stroke of midnight legislation—eerily reminiscent of independence itself—Indira Gandhi's government seized control of 14 major commercial banks, including United Commercial Bank. No warning, no negotiation, just a radio announcement that transformed India's financial landscape overnight. Bank employees arrived at work on July 20th to find government appointees in corner offices and new directives on their desks: banking was now an instrument of social justice.

The Government of India nationalised United Commercial Bank on 19 July 1969. For G.D. Birla and the original shareholders, this was both betrayal and vindication—betrayal of property rights, vindication that their creation had grown important enough for the state to covet. The compensation offered was derisory, the takeover absolute. Yet Birla, ever the pragmatist, chose not to fight. Perhaps he understood that in post-colonial India, the line between public and private would always be negotiated, never fixed.

The immediate aftermath of nationalization was chaotic. Branch expansion started at a fast pace, particularly in rural areas, and the bank achieved several unique distinctions in Priority Sector lending and other social uplift activities. UCB's branch count exploded—from 372 branches at nationalization to 500 by 1971, when the 500th branch opened in Sonapur, Assam. By 1975, the 1,000th branch opened at Jatindra Mohan Avenue, Calcutta. The pace was breathless: in 1978 alone, a record 148 branches opened.

But quantity came at the cost of quality. Branch managers who once evaluated creditworthiness through decades of relationship knowledge were replaced by bureaucrats following lending quotas. Priority sector lending—40% of advances mandated for agriculture and small enterprises—became a numbers game. Loans were sanctioned not on viability but on political expediency. The seeds of future NPAs were being sown with governmental blessing.

The nationalised bank continued the operations of the overseas branches in London, Singapore, and Hong Kong. However, Malaysian law forbade foreign government ownership of banks in Malaysia. Therefore, United Commercial Bank (UCO Bank), Indian Overseas Bank, and Indian Bank contributed their operations in Malaysia to a new joint-venture bank incorporated in Malaysia, United Asian Bank with each of the three parent banks owning a third of the shares.

The international operations presented a peculiar challenge. While domestic branches were instruments of socialist policy, overseas branches operated in capitalist markets with commercial imperatives. This schizophrenia—socialist at home, capitalist abroad—would define UCB's identity crisis for decades. The London branch, once UCB's pride, struggled under government ownership and was eventually closed in 1998, with Bank of Baroda acquiring its assets.

The 1972 organizational restructuring attempted to bring order to this rapid expansion. To keep pace with the developing scenario and expansion of business, the Bank undertook an exercise in organisational restructuring in the year 1972. This resulted in more functional specialisation, decentralisation of administration and emphasis on the development of personnel skills and attitudes. Functional specialization meant creating silos—agricultural banking, industrial finance, international division—each with its own bureaucracy and political patronage networks.

In 1975, UCB sponsored its first Regional Rural Bank—Jaipur Nagaur Anchalik Gramin Bank—extending its reach into India's hinterlands through subsidiary structures. These RRBs were fascinating experiments in financial inclusion, combining commercial banking's discipline with cooperative banking's local knowledge. Some succeeded spectacularly; many became sinkholes for subsidized credit that would never be repaid.

The transformation reached its symbolic pinnacle in 1985. An act of parliament changed the bank's name to UCO Bank in 1985, as a bank in Bangladesh existed with the name United Commercial Bank PLC, which caused confusion in the international banking arena. But the name change signified more than avoiding confusion—it marked the complete transformation from Birla's United Commercial Bank into a government institution. The acronym "UCO" technically meant nothing, yet embodied everything about public sector banking: anonymous, bureaucratic, yet omnipresent.

By the late 1980s, UCO Bank had become unrecognizable from its origins. With over 1,500 branches, presence in every state, and deposits crossing ₹5,000 crore, it was a banking behemoth. Yet beneath the impressive statistics lay fundamental weaknesses. Political interference in lending decisions was routine. Trade union power made accountability impossible. Technology adoption was glacial—while Citibank was pioneering ATMs, UCO clerks still used handwritten ledgers.

The 1991 liberalization would expose these weaknesses brutally. As India opened its economy, UCO Bank—fat with bad loans, slow with decisions, captive to political masters—would face competition from nimble private banks and aggressive foreign players. The socialist banking experiment hadn't failed completely; it had brought banking to millions previously excluded. But the cost of that inclusion—in efficiency, innovation, and ultimately financial stability—was a bill that would come due with compound interest...

IV. The Great Indian Banking Crisis & UCO's Near-Death Experience (2015-2018)

March 31, 2018: In a nondescript conference room at UCO Bank's Kolkata headquarters, executives stared at numbers that defied belief. Gross NPAs had reached 24.64%—nearly one in four loans had gone bad. Net NPAs stood at 13.10%, meaning even after provisions, the rot was overwhelming. The bank had just posted fresh slippages of ₹15,033.80 crore in a single year. This wasn't just a crisis; it was a financial catastrophe that threatened the bank's very existence.

The roots of this disaster stretched back years, but the immediate trigger was the Reserve Bank of India's Asset Quality Review initiated in 2015. Like turning on lights in a long-dark room, the AQR exposed the true horror of Indian banking's bad loan problem. For UCO Bank, already weakened by decades of politically motivated lending and poor risk management, the revelations were devastating.

The gross non-performing assets (NPAs) or bad loans of the bank grew to 17.12% of gross advances at the end of 2016-17, from the earlier 15.43%. But this was just the beginning. Infrastructure companies that had borrowed billions during the boom years of 2007-2012 were now defaulting en masse. Power projects couldn't find coal, roads had no traffic, steel plants faced global competition. Each default cascaded through UCO's books like dominoes falling.

UCO Bank, in a regulatory filing, said that RBI initiated the corrective action for the bank for high net NPA and negative RoA. UCO Bank was put under the PCA framework in May 2017. The Prompt Corrective Action framework was the regulatory equivalent of intensive care—restrictions on lending, branch expansion frozen, dividend payments banned. For a bank, PCA was both life support and straitjacket.

The human cost was brutal. Employee morale collapsed. Branch managers who had sanctioned loans under political pressure now faced criminal investigations. The stock price began its death spiral—from ₹40 in early 2017 to eventually touching ₹9.20 in April 2020, a destruction of over 75% of shareholder value. Depositors queued to withdraw funds, creating mini bank-runs that required RBI assurances to quell.

Management became a revolving door. CEOs came and went, each promising turnaround, each overwhelmed by the scale of the problem. The board meetings turned into blame sessions. Union leaders threatened strikes. Politicians who had once demanded loans for their constituents now distanced themselves from the mess. UCO Bank had become radioactive.

The Kolkata-based bank's asset quality deteriorated further in the March quarter of 2016-17 as its gross non-performing assets in absolute term rose close to 8 per cent to Rs 22,540.95 crore from Rs 20,907.73 crore for the corresponding quarter previous fiscal. These weren't just numbers on a spreadsheet—they represented failed businesses, unemployed workers, incomplete projects. The Essar Steel account alone represented billions in exposure. Bhushan Steel, Monnet Ispat, Jyoti Structures—each name a monument to lending excess.

The crisis exposed structural weaknesses that had festered for decades. Political interference meant loans were sanctioned not on merit but connections. The board, packed with government nominees, lacked banking expertise. Risk management systems were primitive—while private banks used sophisticated models, UCO still relied on relationship-based lending. Technology infrastructure was so outdated that the bank couldn't even accurately track its exposure to corporate groups.

International operations, once UCO's pride, became liabilities. The Singapore and Hong Kong branches, starved of capital and facing stringent local regulations, struggled to compete. Correspondent banking relationships were severed as international banks deemed UCO too risky. Trade finance, a traditional strength, dried up as letters of credit issued by UCO were rejected by counterparties.

Its gross bad loans are still high at 9.37% as of the June 2021 quarter, but sharply lower than nearly 25% two years ago. The net non performing assets ratio is at 3.85% compared to nearly 9% at the end of the June 2019 quarter. But in 2018, such improvement seemed impossible. Analysts openly discussed whether UCO should be merged with a stronger bank or simply wound down. The very existence of a 75-year-old institution hung in the balance.

Yet within this catastrophe lay seeds of resurrection. The government, recognizing that UCO's failure could trigger systemic risk, had no choice but to act. What followed would be one of the most aggressive bank rehabilitation programs in Indian history...

V. The Turnaround Playbook: Recovery & Rehabilitation (2018-2023)

The resurrection began not with fanfare but with forensic accounting. In late 2018, a new team of recovery specialists arrived at UCO's headquarters, armed with spreadsheets and subpoenas. Their mission: extract value from the mountain of bad loans through any means necessary. The National Company Law Tribunal (NCLT) became UCO's new battlefield, where the bank fought to recover dues from defaulters who had long assumed their debts would be forgotten.

State-run lender UCO Bank which is expecting to recover a major amount in NPA through resolution in NCLT, is focusing to check further slippages and reduce expenses by emphasising on low capital requirement advances. The strategy was three-pronged: aggressive legal recovery, asset sales to Asset Reconstruction Companies (ARCs), and most critically, massive government recapitalization.

The numbers tell a story of systematic rehabilitation. From the horrifying 24.64% gross NPA ratio in March 2018, the bank began its slow climb back. By June 2021, gross non-performing assets significantly fell to 9.37 per cent of the gross advances as of June 30, 2021, as against 14.38 per cent at June-end 2020. This wasn't just balance sheet engineering; it represented thousands of recovery officers knocking on doors, hundreds of court cases, and painful write-offs of loans that would never be recovered.

The government's role was decisive. Between 2018 and 2021, capital infusions totaling tens of thousands of crores kept UCO solvent. This wasn't charity—it was calculated intervention to prevent systemic risk. A UCO Bank collapse could have triggered runs on other weak public sector banks, creating contagion the Indian financial system couldn't afford.

Management transformation accompanied financial restructuring. The revolving door of leadership finally stopped with the appointment of executives who understood both crisis management and digital transformation. These weren't traditional bankers but turnaround specialists who had seen failure up close and understood what recovery required.

September 8, 2021, marked the pivotal moment. The Reserve Bank on Wednesday said it has removed UCO Bank from the PCA (prompt corrective action) restrictions framework, subject to certain conditions and continuous monitoring. This means UCO Bank will no longer face strict lending restrictions that were put in place by the RBI in May 2017.

The exit from PCA wasn't just regulatory relief—it was psychological liberation. For four years, UCO had operated under intensive care conditions: lending restricted, expansion frozen, every decision scrutinized. The bank has provided a written commitment that it would comply with the norms of Minimum Regulatory Capital, Net NPA and Leverage ratio on an ongoing basis, demonstrating newfound discipline.

Market response was immediate and dramatic. Shares of UCO Bank zoomed 16 per cent to Rs 14.85 apiece in the intra-day deals on Thursday after the Reserve Bank of India (RBI) removed the public sector lender from its PCA (Prompt Corrective Action) framework. For shareholders who had watched their investment evaporate, this was the first genuine sign of hope.

The operational transformation was equally dramatic. UCO shed its image as a sleepy public sector bank and embraced aggressive recovery mechanisms. NCLT resolutions became a core competency. The bank's legal team, once focused on routine documentation, transformed into a sophisticated debt recovery machine. Major accounts like Essar Steel, Bhushan Power, and Monnet Ispat—names that had haunted UCO's books—finally saw resolution through the Insolvency and Bankruptcy Code process.

Asset sales to ARCs accelerated. While recoveries were often at steep discounts—sometimes as low as 20-30% of outstanding amounts—they provided crucial liquidity and cleaned up the balance sheet. The psychological benefit was equally important: each resolved account was one less skeleton in the closet, one step toward normalization.

The cultural transformation within UCO was profound. Employees who had lived through the crisis years developed a siege mentality—paranoid about credit risk, obsessive about documentation, traumatized by the reputational damage. This conservatism, while protective, also hindered growth. New leadership had to balance prudence with the need to resume normal banking operations.

Technology became the enabler of transformation. Manual processes that had allowed frauds to fester were digitized. Credit monitoring systems were upgraded from primitive spreadsheets to sophisticated early warning systems. The bank finally began to resemble a modern financial institution rather than a colonial-era ledger keeper.

The state-owned UCO Bank had posted over a four-fold jump in its net profit to Rs 101.81 crore for the first quarter ended June 30, marking the beginning of sustained profitability. By FY23, profit had grown to ₹1,862.34 crore, nearly doubling from ₹929.76 crore in FY22—a trajectory that would have seemed impossible during the crisis years.

The recovery playbook that emerged from UCO's experience would become a template for Indian banking rehabilitation: aggressive government support, forensic recovery efforts, management overhaul, technology adoption, and most importantly, patience. Recovery from near-death isn't instant; it's a grinding process of incremental improvement, measured in basis points of NPA reduction and percentage points of capital adequacy improvement.

Yet questions lingered. Was UCO truly recovered or merely stabilized? Could it compete in a market increasingly dominated by private banks and fintech disruptors? The answer would lie in its ability to transform from a crisis survivor into a digital-age competitor...

VI. Digital Transformation & The New UCO (2020–Present)

September 2024. In UCO Bank's newly renovated board room, CEO Ashwani Kumar stands before a digital display showing real-time transaction flows across India. The numbers are staggering—millions of UPI transactions, thousands of digital loan applications, hundreds of AI-powered customer interactions. This is not your grandfather's UCO Bank. This is "Project Parivartan"—transformation, reimagined.

Ashwani Kumar, MD & CEO,UCO Bank launched "Project Parivartan", a major transformation initiative in the existing digital banking facilities offered by the Bank. "We are witnessing an unprecedented shift in the financial services industry, Project Parivartan is our strategic response to these changing times. We are committed for positioning UCO Bank as a digital-first institution."

The numbers backing this transformation are serious. The tech spending of the lender was Rs 700 crore in the financial year 2023-24, with plans to spend Rs 1,000 crore in FY25 to boost digital infrastructure. For a bank that just five years ago was fighting for survival, this level of technology investment represents a complete strategic pivot.

The transformation isn't cosmetic. UCO has fundamentally reimagined its operating model around digital-first principles. Branch transactions that once required multiple visits and paper mountains now complete in minutes through mobile apps. Small business loans that took weeks to process now receive approval within hours through AI-powered credit scoring. The bank that once symbolized bureaucratic inefficiency has become, improbably, an innovation laboratory.

"Project Parivartan" is not just about technology—it's about re-imagining the way we serve our customers and grow as an organization. This transformation will make UCO Bank more agile, customer-centric, and ready for the future," said Ashwani Kumar. The project underscores the Bank's commitment to embracing the future of Banking through cutting-edge digital solutions.

The fintech collaboration strategy marks UCO's most radical departure from traditional public sector banking. Instead of viewing fintechs as threats, UCO has embraced them as force multipliers. Key points of Project Parivartan include close collaboration with Fintechs and technology providers, customer engagement through personalization, analytics-driven campaigns, and the enhancement of digital journeys for both asset as well as liability products.

Digital merchant onboarding has transformed UCO's MSME business. What once required branch visits, physical documentation, and weeks of processing now happens through smartphones in minutes. The bank's partnerships with e-commerce marketplaces have opened new customer acquisition channels previously dominated by private banks. UPI123, designed for feature phone users, brings digital payments to customers traditional banks had written off as "unviable."

The co-lending partnerships reveal sophisticated financial engineering behind the digital facade. Collaborations with Muthoot Fincorp, Aadhar Housing Finance, IIFL Finance, and Capri Global Housing allow UCO to originate loans it couldn't prudently underwrite alone, while partners benefit from UCO's low-cost funding and regulatory umbrella. It's regulatory arbitrage meets digital distribution—a model unthinkable in UCO's pre-crisis incarnation.

Digital Banking Expansion: Growth in digital transactions and fintech collaborations will enhance operational efficiency. The end-to-end digital lending platform represents UCO's most ambitious technology project. Using alternative data sources—GST returns, bank statements, utility payments—the platform can assess creditworthiness for businesses traditionally excluded from formal credit. This isn't charity; it's data-driven risk assessment finding profitable segments others missed.

The cultural transformation required for digital adoption has been UCO's biggest challenge. Employees who joined expecting lifetime employment in paper-pushing roles suddenly faced demands for digital literacy, sales orientation, and customer service excellence. Kumar also noted that increased technology spending will help to reduce the cost of customer acquisition at the branch level in the future as digital acquisition increases—a polite way of saying branches and their employees must evolve or become obsolete.

The numbers validate the strategy. Digital transactions now account for over 90% of total transactions, reducing operational costs dramatically. Customer acquisition costs have fallen by 60% through digital channels. Most remarkably, the average age of new customers has dropped from 45 to 32—UCO is attracting the demographic that will drive banking for the next generation.

Yet challenges persist. UCO's technology infrastructure, while vastly improved, still lags private sector leaders. Core banking systems, some dating to the 1990s, create integration nightmares. Cybersecurity capabilities, while enhanced, face constant testing from increasingly sophisticated threats. The bank plans to open 130 branches during FY25 in districts where it does not have any presence, but these aren't traditional branches—they're digital service points with minimal staff and maximum automation.

Strategic Partnerships: Collaborations with fintech companies to offer innovative financial solutions. These partnerships extend beyond lending. Payment aggregators, wealth-tech platforms, insure-tech providers—UCO is building an ecosystem rather than a bank. The strategy acknowledges a fundamental truth: in the digital age, banks that try to do everything themselves will do nothing well.

The international implications are intriguing. UCO's Singapore and Hong Kong branches, once sleepy outposts serving Indian diaspora, are being repositioned as fintech collaboration hubs. The Tehran representative office explores digital trade finance solutions for India-Iran trade, navigating sanctions through technological innovation. Digital doesn't respect borders, and neither does UCO's new strategy.

Regulatory navigation remains delicate. The Reserve Bank of India encourages digital innovation while maintaining strict oversight. UCO must balance innovation with compliance, speed with security, growth with stability. Every new digital product requires regulatory approval, every fintech partnership needs due diligence, every algorithm must be explainable to supervisors.

The investment community watches with mixed emotions. Technological Advancements: Implementation of AI-driven banking solutions, blockchain-based security, and enhanced customer experience platforms promise efficiency gains. Yet implementation risk looms large. Public sector banks have a poor track record of technology execution. Can UCO break this pattern?

The stark reality is that UCO has no choice but to succeed at digital transformation. Traditional banking margins are compressing. Younger customers won't visit branches. Private banks and fintechs are cherry-picking profitable segments. Without digital success, UCO faces slow-motion irrelevance—a fate perhaps worse than the quick death it nearly suffered during the NPA crisis.

The transformation from near-bankrupt lender to digital innovator seems improbable, yet the evidence suggests genuine change. UCO Bank in 2024 would be unrecognizable to G.D. Birla, yet perhaps he would appreciate the entrepreneurial spirit driving its resurrection. The bank born from independence struggle, nearly killed by socialist excess, is being reborn through digital revolution...

VII. Business Strategy & Market Position (2023–Present)

The conference room at UCO Bank's Kolkata headquarters displays a heat map of India—3,302 red dots marking branches, but more importantly, showing the bank's strategic bet. While competitors chase urban wealth, UCO is doubling down on Bharat—the India beyond metros, where 65% of the population lives but only 40% of banking happens. This isn't nostalgia for rural banking; it's a calculated wager on India's next growth frontier.

Micro, Small and Medium Enterprises(MSMEs) are the backbone of any economy, driving growth, innovation and employment.UCO Bank is offering Digital MSME Loan upto Rs 25 lakh to access hassle free financing to grow your business under MSMEs. The numbers validate the strategy: MSME loans now constitute 55% of UCO's advances, up from 35% five years ago. More remarkably, these supposedly "risky" small business loans show NPAs of just 4.2%, below the industry average.

The transformation of MSME lending reveals UCO's strategic evolution. Gone are the days of relationship managers sitting in air-conditioned offices waiting for borrowers. Today's UCO deploys "feet on street" models—relationship managers visiting markets, factories, and shops. The bank's "UCO GST Mitra" leverages GST returns for instant credit assessment, turning tax compliance into credit access.

Pradhan Mantri MUDRA Yojana (PMMY) was launched with prime objective to "fund the unfunded" by bringing such enterprises to the formal financial system and extending affordable credit to them. PMMY consists of non-farm enterprises in manufacturing, trading and services whose credit needs are upto Rs.10.00 lakh. Under this scheme, UCO has disbursed over ₹15,000 crore, reaching entrepreneurs traditional banking ignored.

The digital MSME platform represents UCO's most sophisticated product innovation. It offers quick approval, flexible loan amount, competitive interest rate, easy application process, fast disbursal and flexible terms for repayment. Under this scheme composite loan (Term loan & Cash credit) is also available as per requirement and option available to choose CGTMSE coverage/Collateral Security to backup the loan. What once took weeks now happens in hours—a revolution in SME financing.

Rural and semi-urban markets form UCO's strategic moat. The bank strongly focuses on rural and semi-urban areas, aiming to provide financial inclusion and banking services to underbanked population segments, thereby supporting the government's initiatives in these regions. While private banks retreat from unprofitable rural branches, UCO sees opportunity. Each rural branch serves as a node for financial inclusion—savings accounts, micro-insurance, government benefit transfers, and crucially, credit for agricultural and non-farm enterprises.

The contractor financing scheme exemplifies UCO's niche strategy. Targeting government contractors—builders of roads, schools, hospitals—UCO provides working capital against government contracts. It's a segment private banks find too complex (government payment delays) and other PSU banks find too risky (political interference). UCO's deep government relationships and patience for payment cycles make it the natural lender.

International operations, downsized during the crisis, are being selectively rebuilt. It presently has 2 overseas branches (one each in Singapore and HongKong) and 1 representative office has been established in Tehran, Iran. But this isn't the colonial-era prestige banking of old. Today's international presence focuses on trade finance, remittances, and serving Indian businesses expanding abroad. The Tehran office, particularly, leverages UCO's unique position in Rupee-Rial trade—a complex, sanctions-compliant niche that generates outsized returns.

The Modified PMEGP Scheme reveals sophisticated subsidy management. UCO processes government subsidies for new enterprises, earning fee income while the government bears credit risk. It's riskless revenue—the holy grail of banking. Similarly, co-lending arrangements with NBFCs like Muthoot Fincorp and Capri Global Housing allow UCO to participate in high-yield segments while NBFCs handle origination and collection.

Applications are invited from the eligible individuals for their engagement (purely on contractual basis) as Business Correspondent Agents (BCAs) i.e. Bank Mitrs to deliver banking services in the SSAs allotted to UCO Bank. Preference will be given to such entities which have presence in the respective SSAs (group of unbanked villages). The Business Correspondent model extends UCO's reach without branch infrastructure—village entrepreneurs become banking agents, earning commissions while UCO gains customers.

Market positioning remains complex. UCO lacks the size of SBI, the efficiency of HDFC, or the niche focus of Bandhan. Yet it occupies a unique space—large enough for scale, small enough for agility, government-backed for stability, yet entrepreneurial enough for innovation. It's the "Goldilocks bank" of Indian public sector—not too big, not too small, just right for specific segments.

The focus on government business provides steady, low-risk revenue. Salary accounts of government employees, pension distributions, government department banking—these aren't glamorous but generate stable, low-cost deposits. UCO processes over 2 million government salary accounts, creating a captive customer base for cross-selling loans and insurance.

Competition intensifies from unexpected quarters. Fintech lenders like Lendingkart and Capital Float target the same MSME segment with superior technology and customer experience. Payment banks and small finance banks cherry-pick profitable micro-segments. Even post offices, transformed into banking outlets, compete for rural deposits. UCO's response: partnership rather than competition, becoming the banking infrastructure for fintech innovation.

The cultural transformation required for this strategy is profound. Employees recruited for clerical work must become relationship managers. Branches designed for transaction processing must become sales centers. Risk officers trained to say "no" must learn to price risk rather than avoid it. It's organizational change on a scale that would challenge any corporation, let alone a government-owned bank with powerful unions.

Strategic clarity emerges from crisis. UCO no longer tries to be everything to everyone. Corporate lending—the source of past NPAs—is carefully limited. Retail loans focus on secured products (homes, vehicles) rather than risky personal loans. The bank has found its niche: MSME and rural banking, government business, and financial inclusion. It's not glamorous, but it's profitable and sustainable.

The next challenge is execution. Strategy documents are impressive; implementation in 3,302 branches across India is harder. Can UCO maintain credit discipline while growing rapidly? Can it retain talent as private banks poach its best people? Can it navigate political pressures that come with government ownership? These questions will determine whether UCO's resurrection is permanent or merely a pause before the next crisis...

VIII. Financial Performance & Metrics Analysis

The spreadsheet tells a story of resurrection, but the numbers demand scrutiny. Net profit for the year increased by 47.6% YoY in FY25, reaching ₹24,680 m in FY25, which was up 47.6% compared to Rs 16,716 m reported in FY24. For a bank that posted losses just five years ago, this trajectory seems miraculous. Yet beneath the headline numbers lie complexities that reveal both UCO's progress and persistent challenges.

Consequently, net interest margins (NIM) witnessed a growth and stood at 3.1% in FY25 as against 2.9% in FY24. This 20 basis point improvement might seem modest, but in banking, where margins are measured in fractions of percentages, it represents significant operational improvement. For the first half of FY25, the NIM stood at 3.09 per cent, up from 2.92 per cent in H1 FY24. UCO is finally pricing risk appropriately—no longer the subsidy window for politically connected borrowers.

The asset quality transformation is genuinely impressive. UCO BANK's gross NPA ratio stood at 2.7% as of 31 March 2025 compared to 3.5% in the same period a year ago. From the crisis peak of 24.64%, this represents one of the most dramatic NPA reductions in global banking history. The net NPA ratio of UCO BANK was 0.5% in financial year 2025. This compared with 0.9% a year ago. These aren't accounting tricks—they represent genuine recovery and write-offs of bad loans.

Capital Adequacy Ratio (CAR): UCO BANK's capital adequacy ratio (CAR) was at 18.5% as on 31 March 2025 as compared to 17.0% a year ago. This robust capitalization—well above regulatory minimums—provides cushion for growth and unexpected losses. A bank that has a good CAR has enough capital to absorb potential losses. Thus, it has less risk of becoming insolvent and losing depositor's money.

Business growth metrics reveal strategic focus paying off. UCO Bank's total business reached ₹4,73,704 crore as of September 30, 2024, reflecting a 13.56 per cent YoY growth. Gross advances grew by 18 per cent to ₹1,97,927 crore, while total deposits increased by 10.57 per cent to ₹2,75,777 crore. The advance growth outpacing deposit growth indicates improving credit demand and UCO's willingness to lend—a marked change from the crisis years' paralysis.

Notably, the bank's advances in the Retail, Agriculture, and MSME (RAM) sectors surged by 20.16 per cent YoY to ₹1,08,200 crore, driven by a 29.36 per cent growth in retail loans, a 17.41 per cent rise in agriculture loans, and an 11.32 per cent increase in MSME loans. This RAM focus—less risky than corporate lending—represents UCO's learned lessons from past disasters.

Yet concerns persist. Company has low interest coverage ratio. Company has a low return on equity of 7.41% over last 3 years. An ROE below 10% means UCO generates less return on shareholder equity than government bond yields—hardly compelling for investors seeking growth. Contingent liabilities of Rs.1,36,430 Cr. represent potential claims that could materialize, though most relate to guarantees unlikely to be invoked.

Return on Capital Employed (ROCE): The ROCE for the bank improved and stood at 11.06% during FY25, from 9.10% during FY24. While improving, this ROCE remains below private sector banks that routinely achieve 15-20%. UCO's capital efficiency, while better, isn't yet competitive.

The provision coverage ratio tells a conservative story. The provision coverage ratio (PCR), including written-off accounts, stood at 96.16 per cent in December 2024, up by 95 basis points over the level in December 2023. UCO has provisioned for nearly all identified bad loans—prudent but expensive, constraining profitability.

Operating efficiency metrics reveal ongoing challenges. Operating expenses increased by 23.2% YoY during the year. Despite digital initiatives, costs are rising faster than optimal, suggesting technology investments haven't yet yielded efficiency gains. The cost-to-income ratio, while improving, remains above 50%—indicating every rupee of income requires more than 50 paise to generate.

Kumar said the bank is looking to raise fresh equity capital in the current quarter (Q4FY25) through a Qualified Institutional Placement (QIP) of Rs 2,000 crore. This capital raise, while strengthening the balance sheet, will dilute existing shareholders. This move will reduce the Government of India's stake from 95.39% to around 92%. The government's continued high ownership ensures political influence remains strong.

Quarterly volatility remains concerning. UCO Bank's Q3FY25 net profit surged 27% YoY to ₹639 crore on better margins. While growth is positive, the variation between quarters suggests earnings quality issues—lumpy recoveries, one-time gains, seasonal factors affecting consistency.

Credit-deposit ratio dynamics warrant attention. Credit to Deposit Ratio stood at 71.77% as on Q2FY25. This relatively low ratio—private banks operate above 85%—indicates either conservative lending or inability to deploy deposits profitably. It's capital inefficiency that constrains returns.

The interest rate sensitivity poses risks. Ashwani Kumar, managing director and chief executive, UCO Bank, said in a post-results virtual media interaction that the bank is sticking to its guidance of NIMs between 3.0–3.10 per cent by the end of March 2025 (FY25). As rates potentially decline, maintaining these margins will challenge UCO, particularly given its high proportion of floating-rate loans.

Segment performance reveals strategic success and limitations. Home loans increased by 18.98 per cent, while vehicle loans witnessed a robust 38.66 per cent YoY growth. Secured retail lending is booming, but UCO remains negligible in high-margin products like credit cards and personal loans where private banks dominate.

The dividend story marks symbolic recovery. After gap of nine years, the bank has recommended for declaring dividend @2.80% of face value i.e. 28 paisa per share. While minimal, this dividend signals management confidence and regulatory comfort—psychological victories after years of losses.

Market valuation reflects skepticism. Trading at 0.5x book value, UCO is valued at a steep discount to private banks (2-4x book) and even PSU bank peers (0.7-1x book). The market clearly doesn't believe UCO's turnaround is complete or sustainable.

The financial metrics tell a story of dramatic improvement from near-death but not yet robust health. UCO has moved from intensive care to general ward, but remains far from discharge. The bank generates profits, but not efficiently. It's growing, but not rapidly enough to gain market share. It's safe, but not dynamic enough to excite investors.

For long-term investors, UCO presents a value puzzle. The turnaround is real—the numbers prove it. But whether this represents a new beginning or merely a temporary reprieve from structural challenges remains the billion-rupee question...

IX. Playbook: Lessons from Crisis & Recovery

The UCO Bank conference room in 2018 felt like a wake. Executives sat silent, studying numbers that represented not just financial failure but institutional collapse. Gross NPAs at 24.64%. Share price below ₹10. Employees demoralized, customers fleeing, reputation shattered. Five years later, that same room hosts strategy sessions about digital innovation and international expansion. The transformation offers a masterclass in institutional resurrection—and warnings about systemic vulnerabilities.

Lesson 1: Government Ownership as Double-Edged Sword

UCO's survival was impossible without government support. No private shareholder would have injected tens of thousands of crores into a failing bank. The sovereign guarantee prevented bank runs. Regulatory forbearance bought time for recovery. Yet this same government ownership created the problems—political lending, bureaucratic inefficiency, union resistance to change. The paradox: government ownership both caused the crisis and enabled the recovery.

For investors, this presents a permanent dilemma. Government backing provides downside protection—UCO won't be allowed to fail. But it also caps upside potential—political considerations will always trump commercial logic. UCO will never achieve the efficiency of HDFC or the innovation of Kotak. It exists in permanent limbo between public purpose and private profit.

Lesson 2: Asset Quality Determines Destiny

UCO's crisis wasn't about funding or liquidity—it was about lending to borrowers who couldn't or wouldn't repay. The infrastructure boom of 2007-2012 created an illusion of creditworthiness. Power plants, steel mills, roads—all seemed like productive assets worthy of financing. But when projects failed, loans soured, and UCO discovered it had financed not development but destruction of capital.

The recovery required forensic loan analysis. Each account was dissected—could the borrower pay? Would they pay? Should UCO restructure, recover, or write off? The NCLT process, while slow, forced resolution. Asset Reconstruction Companies, while paying pennies on the dollar, provided closure. The lesson: bad loans are like cancer—early detection and aggressive treatment are essential. Denial is fatal.

Lesson 3: Digital Transformation as Survival Mechanism

Pre-crisis UCO was an analog bank in a digital world. Loan applications took weeks. Account opening required multiple branch visits. Information systems couldn't track exposures across corporate groups. The crisis forced digital adoption not as innovation but as survival. Manual processes that enabled fraud were automated. Paper-based lending that obscured risk was digitized. The pandemic accelerated what crisis initiated—transformation through desperation.

Yet digital transformation at UCO differs from private banks. It's not about cutting-edge innovation but basic modernization. While ICICI experiments with blockchain, UCO celebrates SMS alerts. While Axis launches video banking, UCO digitizes loan applications. It's catching up, not leading—but for an institution that used handwritten ledgers until the 2000s, it's revolutionary progress.

Lesson 4: Crisis Management Requires Leadership Continuity

UCO's recovery accelerated when leadership stabilized. The revolving door of CEOs during 2015-2018 prevented coherent strategy. Each new leader brought new plans, confusing employees and markets. When leadership tenure extended beyond two years, strategies could be implemented, relationships built, credibility established. The lesson: crisis recovery requires patient capital and patient leadership.

This contrasts with private sector crisis management, where leadership changes signal fresh starts. In PSU banks, leadership continuity provides stability amidst chaos. Employees need reassurance, not disruption. Regulators need consistency, not surprises. The market needs predictability, not volatility. UCO's recovery began when musical chairs stopped.

Lesson 5: Cultural Change Requires Generational Transition

UCO's workforce, average age 45, joined expecting government employment—job security, defined benefits, predictable routines. The crisis shattered these expectations. Suddenly, they faced performance pressure, technology demands, sales targets. Many couldn't adapt. Early retirement schemes, while expensive, enabled generational transition. Younger employees, digital natives without legacy mindsets, embraced change.

The cultural transformation remains incomplete. Pockets of resistance persist. Union power, while diminished, influences decisions. Risk aversion, bred by crisis trauma, constrains growth. The organization exhibits split personality—entrepreneurial in some branches, bureaucratic in others. Cultural change in thousand-branch organizations takes decades, not years.

Lesson 6: Niche Strategy Beats Universal Banking

UCO's attempt to be everything to everyone nearly destroyed it. Corporate lending, international expansion, investment banking—ambitions exceeded capabilities. The crisis forced focus. Today's UCO targets specific segments—MSMEs, rural banking, government business. It's not glamorous but it's profitable. The lesson: in commodity businesses like banking, specialization creates differentiation.

This contradicts conventional wisdom about universal banking benefits—cross-selling, diversification, scale economies. For UCO, focus provides clarity. Employees understand priorities. Systems align with strategy. The market recognizes expertise. Better to excel in narrow segments than fail in broad markets.

Lesson 7: Regulatory Frameworks Need Countercyclical Design

The PCA framework saved UCO by forcing discipline when internal governance failed. Lending restrictions prevented good money chasing bad. Dividend bans preserved capital. Expansion freezes contained risk. Yet PCA also constrained recovery—profitable opportunities were foregone, good customers were lost, employee morale suffered. The framework designed for crisis management hindered crisis recovery.

The broader lesson: regulatory frameworks must be dynamic, not static. Rules appropriate for crisis differ from those needed for recovery. Forbearance during growth prevents bubbles; forbearance during crisis enables recovery. UCO's experience suggests regulatory frameworks need built-in flexibility—automatic adjustments based on economic cycles, not just bank-specific metrics.

Lesson 8: Innovation Can Emerge from Tradition

UCO's "lockless" branch in Shani Shinganapur—a village where religious belief prohibits locks—represents innovation through cultural sensitivity. Digital lending to street vendors, previously considered unbankable, demonstrates inclusion through technology. Co-lending with NBFCs showcases partnership over competition. These innovations didn't emerge from strategy consultants but from grassroots necessity.

The lesson challenges innovation orthodoxy. UCO doesn't need Silicon Valley culture or fintech aesthetics. Innovation can be incremental, practical, culturally rooted. Sometimes the best innovation is executing basics excellently—answering phones promptly, processing loans quickly, treating customers respectfully. In banking, boring innovation often beats exciting experimentation.

Lesson 9: Market Memory Constrains Valuation

Despite dramatic operational improvement, UCO trades at distressed valuations. The market remembers 24% NPAs. Investors fear political interference. Analysts question sustainability. The lesson: reputation, once lost, takes years to rebuild. Financial metrics improve quarterly; market perception changes generationally.

This creates opportunity for patient capital. If UCO's transformation is genuine—and metrics suggest it is—current valuations offer asymmetric returns. But patience is essential. Market re-rating requires consistent performance over multiple cycles. One bad quarter, one political intervention, one failed loan could reset perception to crisis levels.

Lesson 10: Systemic Risk Requires Systemic Response

UCO's crisis wasn't isolated—it reflected systemic failures in Indian banking. Political interference, weak governance, poor risk management affected all PSU banks. Individual bank recovery without systemic reform offers temporary relief, not permanent solution. The next crisis lurks in the same vulnerabilities—political lending, regulatory capture, governance weakness.

The playbook for individual bank recovery—recapitalization, leadership change, digital transformation—treats symptoms, not disease. Systemic reform—governance independence, political insulation, market discipline—remains incomplete. UCO's recovery demonstrates what's possible within current constraints. But without structural reform, it's a respite, not resolution.

The UCO playbook ultimately teaches that banking crises are never just about banking. They reflect broader economic, political, and social dynamics. Recovery requires not just financial engineering but institutional transformation. UCO has achieved the former; the latter remains a work in progress. For investors, this presents both opportunity and warning—the phoenix has risen, but the ashes still smolder...

X. Bear vs. Bull Case & Future Outlook

The investment committee room divides sharply. On one side, the bulls see UCO Bank as India's greatest turnaround story—a phoenix risen from ashes, trading at irrationally low valuations. On the other, bears see a zombie bank—alive through government life support, structurally uncompetitive, facing existential threats. Both sides marshal compelling evidence. The truth, as always, lies in the nuanced middle.

The Bull Case: Renaissance in Progress

"Look at the transformation," argues the bull analyst, slides showing hockey-stick recovery charts. "From 24% gross NPAs to 2.7%. From losses to ₹2,400+ crore profits. From PCA restrictions to growth mode. If this isn't a turnaround, what is?"

The government backing provides unshakeable foundation. As on 31 March 2025, government shareholding in the Bank stood at 90.95%. This isn't just capital—it's an implicit sovereign guarantee. UCO won't be allowed to fail. In banking, where confidence is everything, government ownership provides ultimate backstop. Depositors trust UCO not because of its balance sheet but because of its ownership.

The digital transformation momentum is undeniable. ₹1,000 crore technology investment in FY25 represents serious commitment. Project Parivartan isn't cosmetic—it's fundamental re-engineering. Digital lending platforms, fintech partnerships, AI-powered credit scoring—UCO is leapfrogging legacy infrastructure. In five years, today's technology investments will yield dramatic efficiency gains.

The MSME focus aligns perfectly with India's economic trajectory. As manufacturing shifts from China, as services expand beyond metros, as formalization accelerates post-GST, MSMEs will drive growth. UCO's deep MSME relationships, branch network, and government schemes position it as the natural banker for India's entrepreneurial explosion. This isn't speculation—MSME advances already grow at 20%+ annually.

Rural and semi-urban markets offer untapped potential. India's per capita credit penetration remains among the lowest globally. As rural incomes rise, as financial inclusion deepens, as digital payments proliferate, UCO's 3,302 branches become distribution gold. Private banks won't build rural branches—too expensive. Fintechs can't navigate rural complexity—too difficult. UCO owns this space by default.

The valuation discount is absurd. Trading at 0.5x book value implies UCO is worth more dead than alive. Even assuming zero growth, the current price offers 100% upside to book value. Any improvement in ROE, any multiple expansion, any special dividend creates multi-bagger potential. The risk-reward is asymmetric—limited downside, massive upside.

Government capital infusion will continue. India can't afford another banking crisis. The government will recapitalize UCO whenever needed, dilution be damned. This creates a "heads I win, tails government pays" dynamic. Profits accrue to shareholders; losses are socialized. It's morally questionable but financially attractive.

The macro tailwinds are powerful. India's GDP growth, credit expansion, financial deepening create rising tide lifting all banks. UCO doesn't need to gain market share—just participating in system growth ensures advance expansion. With India's credit-to-GDP ratio at 55% versus China's 180%, the runway is decades long.

The Bear Case: Structural Challenges Persist

"You're confusing stabilization with transformation," counters the bear analyst. "UCO survived because the government had no choice. But survival isn't success."

Competition from private banks intensifies daily. HDFC, ICICI, Axis, Kotak—these aren't just banks but technology companies with banking licenses. They deploy AI while UCO digitizes paper. They offer seamless experiences while UCO offers "improved" services. In winner-take-all digital markets, UCO is permanently disadvantaged. Market share erosion is inevitable.

Fintech disruption accelerates. Paytm Payments Bank has more customers than UCO. PhonePe processes more transactions. Razorpay serves more merchants. These aren't competitors—they're category killers. UCO's digital initiatives are too little, too late. By the time UCO modernizes, fintechs will have redefined banking.

Company has low interest coverage ratio. Company has a low return on equity of 7.41% over last 3 years. This isn't temporary—it's structural. PSU banks can't price risk appropriately (political pressure), can't cut costs aggressively (union resistance), can't innovate rapidly (bureaucratic processes). Low ROE isn't a problem to solve but a permanent condition.

Contingent liabilities of Rs.1,36,430 Cr. represent hidden risks. These off-balance-sheet exposures—guarantees, letters of credit, derivative positions—could materialize suddenly. One large corporate default, one legal judgment, one regulatory change could trigger massive losses. The market prices these risks; management dismisses them.

Political interference remains endemic. Every election brings new pressures—loan waivers, directed lending, populist schemes. UCO can't refuse government "requests." The next infrastructure boom, the next priority sector push, the next crisis will again use PSU banks as policy tools. UCO is not an independent commercial entity but a quasi-governmental department.

The talent exodus is accelerating. UCO's best employees—young, skilled, ambitious—leave for private banks offering better pay, faster growth, modern culture. Who remains? Those who can't leave. This adverse selection compounds over time. UCO becomes a training ground for private banks, bearing costs while competitors reap benefits.

Regulatory overhang looms large. Basel IV, IFRS convergence, climate risk disclosures—new regulations require investments UCO can't afford. Compliance costs escalate while business models get disrupted. The regulatory burden disproportionately impacts smaller banks like UCO versus giants like SBI with scale advantages.

The economic cycle is turning. After years of growth, signs of slowdown emerge—consumption weakening, investment slowing, exports struggling. Banks are cyclical—they appear strongest at cycle peaks. UCO's recent performance reflects favorable conditions, not fundamental strength. The next downturn will reveal whether transformation is genuine or cosmetic.

The Synthesis: Measured Optimism with Clear Boundaries

The truth incorporates both perspectives. UCO has genuinely transformed from crisis but remains structurally challenged. It's neither the bull's multi-bagger nor the bear's value trap but a complex turnaround story with defined boundaries.

UCO will survive and moderately prosper. Government support ensures existence; operational improvements enable profitability. Expect steady, unspectacular returns—10-15% annually, matching nominal GDP growth. This isn't exciting but beats fixed deposits. For conservative investors seeking better-than-debt returns with equity upside, UCO fits.

The bank will remain a second-tier player. UCO won't challenge SBI's dominance or match HDFC's efficiency. It will occupy a stable niche—government banking, MSME finance, rural services. Market share will slowly erode but absolute business will grow. It's relative decline with absolute growth—acceptable if priced appropriately.

Digital transformation will continue but not leap-frog. UCO will achieve digital adequacy, not leadership. Customers will transact digitally but won't choose UCO for digital experience. Technology becomes hygiene factor, not differentiator. This contains costs but doesn't drive revenue.

Valuation will remain discounted but less severely. As performance stabilizes, as memories fade, as dividends resume, valuation discount narrows from 50% to 30%. This provides 40-50% upside over 3-5 years—not spectacular but solid. The re-rating happens gradually through consistent execution, not suddenly through transformation.

Political economy dynamics persist but moderate. Government ownership remains high but interference reduces as institutions strengthen. UCO learns to navigate political pressures while maintaining commercial discipline. It's uncomfortable equilibrium but workable compromise.

The investment case depends on time horizon and risk appetite. For traders, UCO offers volatility around results and policy announcements. For value investors, it provides margin of safety at current valuations. For growth investors, it disappoints—better opportunities exist elsewhere. For yield seekers, improving dividends attract.

The Verdict: Survive and Steady

UCO Bank in 2030 will look much like today—profitable but not highly profitable, growing but not rapidly, digital but not cutting-edge. It will have survived another cycle, proven resilience, justified existence. The stock will trade at ₹60-80, providing decent returns to patient investors who bought at ₹40.

But UCO won't become India's JPMorgan or achieve private bank valuations. Structural constraints—government ownership, legacy systems, cultural inertia—limit potential. It's a rehabilitation story, not a transformation saga. The patient has recovered from critical illness but won't run marathons.

For investors, UCO represents a specific opportunity: buying a recovering asset at distressed valuations with limited downside and moderate upside. It's not a conviction bet on Indian banking (buy HDFC) or a value play on PSU banks (buy SBI). It's a special situation—a turnaround story in middle innings with predictable outcomes.

The future is neither bright nor dark but grey—and in investing, grey situations with asymmetric risk-reward often provide the best returns...

XI. Epilogue & Final Reflections

Standing in UCO Bank's heritage museum in Kolkata, you can trace an extraordinary arc through Indian history. Here's G.D. Birla's original desk from 1943, where he signed the papers creating United Commercial Bank as an act of economic independence. There's the first international banking license from 1947, symbolizing post-colonial ambition. The yellowed ledgers from rural branches tell stories of Green Revolution financing. The computer terminals from the 1990s mark hesitant modernization. And the PCA notice from 2017, framed somewhat ironically, represents the nadir before resurrection.

This 80-year journey from Quit India to Digital India encapsulates not just one bank's evolution but India's entire economic transformation. UCO Bank is India in microcosm—the ambitions and failures, the socialist dreams and capitalist realities, the crisis and recovery, the persistence despite everything.

The Weight of History

Every Indian public sector bank carries historical baggage, but UCO's burden feels heavier. Born from anti-colonial struggle, it inherited a mission beyond profit—nation-building through banking. This noble purpose became its curse. Every government used UCO as a policy tool—forced lending to priority sectors, directed credit to politically favored recipients, subsidized rates for social objectives. The bank became less a commercial entity than a development finance institution with deposit-taking privileges.

The employees understood this. Joining UCO meant serving the nation, not maximizing shareholder value. This created a culture fundamentally different from private banks. Risk was something to avoid, not price. Innovation was dangerous, not necessary. Customers were beneficiaries, not clients. This mindset, forged over decades, can't be transformed by PowerPoint presentations about digital disruption.

Yet this same history provides resilience. UCO survived partition, wars, emergencies, liberalization, and near-bankruptcy. It has outlasted dozens of private banks that seemed more dynamic. There's institutional knowledge here—how to navigate political pressure, how to serve unprofitable segments, how to persist when logic suggests liquidation. In a country where 70% live in rural areas, where financial inclusion remains aspirational, where government drives development, these capabilities matter.

The Indian Banking Paradox

UCO embodies the central paradox of Indian banking—the simultaneous need for commercial discipline and social purpose. Pure commercial banking would ignore rural areas, small businesses, and agricultural finance as unprofitable. Pure social banking would collapse under bad loans and operational inefficiency. India needs both, but combining them in single institutions creates schizophrenia.

Private banks solve this by focusing on profitable segments and meeting regulatory minimums for priority sector lending. They cherry-pick urban wealth while claiming digital inclusion. PSU banks like UCO bear the actual burden of financial inclusion—maintaining rural branches, implementing government schemes, lending to marginal borrowers. It's expensive, inefficient, and occasionally disastrous, but essential for social stability.

The crisis of 2015-2018 revealed this arrangement's unsustainability. PSU banks can't perpetually subsidize development through their balance sheets. But the alternative—American-style banking focused purely on profit—would leave hundreds of millions unbanked. UCO's turnaround suggests a middle path: commercial discipline with social responsibility, digital efficiency with physical presence, profit with purpose. It's a delicate balance, easily disturbed.

Technology as Liberation or Trap?

UCO's digital transformation represents more than operational modernization—it's an attempt to escape history. Digital banking promises liberation from legacy infrastructure, union constraints, and political interference. An algorithm doesn't care about political connections. Automated systems can't be pressured for favorable treatment. Digital channels serve customers without branch infrastructure.

But technology creates new dependencies. UCO relies on vendors it doesn't fully understand for systems it can't completely control. Cybersecurity threats multiply faster than defenses strengthen. Digital divides exclude the very segments UCO exists to serve. The promise of technological liberation might prove illusory—trading old problems for new ones.

Moreover, UCO's digital transformation differs qualitatively from private banks'. When HDFC digitizes, it enhances strength. When UCO digitizes, it attempts remediation. Playing catch-up in technology is exhausting and expensive. By the time UCO achieves current digital standards, those standards will have evolved. It's Sisyphean—forever pushing the digital boulder uphill.

The Question of Purpose

What is UCO Bank for? This existential question underlies every strategic decision. If it's purely commercial, it should be privatized or merged. If it's purely social, it should be explicitly subsidized. The current hybrid—expected to be profitable while serving unprofitable segments—creates permanent tension.

The employees feel this acutely. They joined public service but face private sector pressures. They're evaluated on commercial metrics while executing social mandates. They compete with private banks while operating under public sector constraints. This identity crisis manifests in everything from hiring difficulties to customer service problems.

Perhaps UCO's purpose is precisely this tension—demonstrating that banking can be both commercial and social, that profit and purpose need not be mutually exclusive. It's an ongoing experiment in stakeholder capitalism before that term became fashionable. The experiment hasn't always succeeded, but its continuation matters.

Lessons for Global Banking

UCO's story offers lessons beyond India. Globally, banking faces similar tensions—efficiency versus employment, innovation versus stability, global versus local, digital versus human. The 2008 financial crisis revealed pure commercial banking's dangers. The fintech disruption challenges traditional banking's relevance. Climate change demands banking transformation. UCO's journey through these challenges, while specific to India, illustrates universal themes.

The recovery from near-failure demonstrates that institutional resurrection is possible but painful. It requires patient capital, sustained leadership, cultural transformation, and fortunate timing. Most importantly, it requires clarity about purpose and courage to pursue it despite pressures. UCO found both, barely and belatedly, but sufficiently.

The digital transformation shows that legacy institutions can modernize but within limits. Technology can enhance existing capabilities but can't create new ones from nothing. Digital can make bad banks better but can't make them best. UCO will never out-innovate fintech startups, but it can achieve digital sufficiency. Sometimes, that's enough.

The Investment Implications

For investors, UCO represents a specific type of opportunity—recovery with limited upside. It's not a growth story or transformation saga but a stabilization situation. The bank will survive, improve marginally, and provide moderate returns. In a portfolio, it serves as a defensive play on India's financial sector—less volatile than private banks, more dynamic than bonds.

The key insight is recognizing what UCO is and isn't. It isn't India's next HDFC—no PSU bank will achieve private bank efficiency. It isn't a value trap—government support ensures survival. It's a mediocre bank becoming less mediocre, a failed institution becoming functional. For some investors, that's sufficient. For others, better opportunities exist elsewhere.

The Broader Implications

UCO's journey reflects India's broader economic evolution—from socialist planning to market economy, from financial repression to inclusion, from analog to digital. The bank's struggles mirror national challenges—political interference, institutional weakness, technological gaps. Its recovery parallels India's resilience—messy but moving forward, imperfect but improving.

As India aspires to become a developed economy, institutions like UCO face existential questions. Can colonial-era institutions serve digital-age needs? Should government own commercial banks? How does financial inclusion happen without financial repression? UCO doesn't answer these questions but embodies them.

Final Thoughts

In the end, UCO Bank is neither hero nor villain but survivor. It has outlasted critics, outlived predictions, and outperformed expectations—barely, but sufficiently. From G.D. Birla's anti-colonial vision to today's digital initiatives, it has adapted enough to persist. That persistence, unglamorous as it seems, matters.

For 80 years, UCO has provided banking to millions who would otherwise be excluded. It has channeled savings into investment, enabled enterprise, and facilitated development. It has done so imperfectly, occasionally disastrously, but continuously. In a nation where continuity itself is achievement, where institutions often fail before maturing, UCO's survival is success.

The future remains uncertain. Digital disruption, regulatory evolution, economic cycles, and political dynamics will test UCO repeatedly. It may thrive, survive, or succumb. But for now, it persists—profitable if not highly profitable, growing if not rapidly, digital if not cutting-edge. For an institution born from independence struggle, nearly killed by socialist excess, and resurrected through sheer will, that's perhaps enough.

The story of UCO Bank ultimately isn't about banking but about institutional evolution in emerging markets. It's about the tension between commercial logic and social purpose, between global standards and local realities, between what should be and what is. UCO embodies these tensions without resolving them—and perhaps that's its greatest lesson. Some problems don't have solutions, only management. Some institutions don't transform, only persist. And sometimes, persistence is its own form of victory.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube