INOXWIND: The Wind Energy Upstart That Challenged the Giants

I. Introduction & Episode Setup

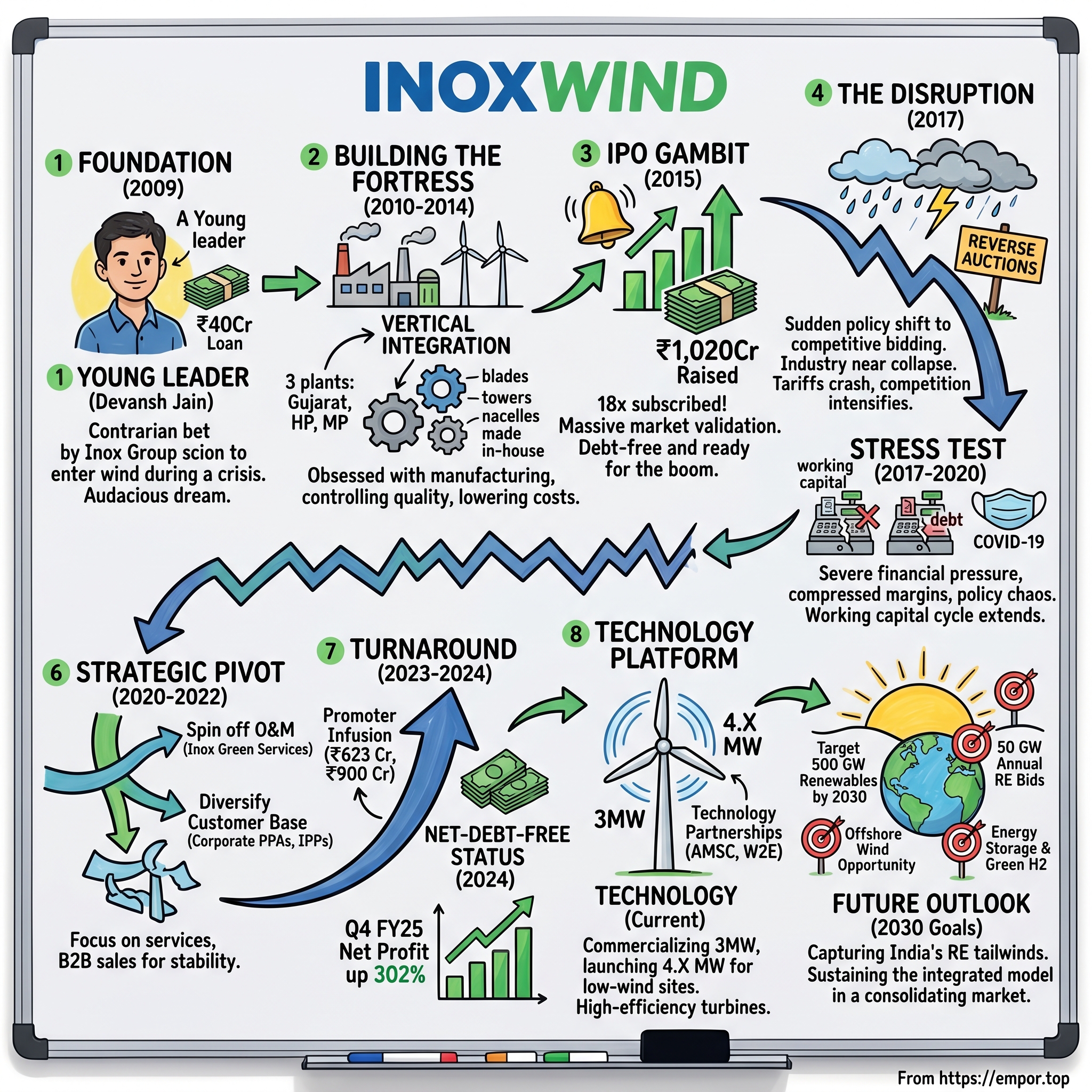

Picture this: It's 2009, and the global financial crisis has just decimated markets worldwide. In India, the wind energy sector—once a darling of investors—lies in ruins. Suzlon, the poster child of Indian renewable energy, watches its stock crater from ₹400 to ₹30. Foreign turbine manufacturers are pulling back. Banks have turned off the credit taps. Into this apocalyptic landscape walks a 28-year-old scion of the Inox Group, armed with nothing but ₹40 crore in borrowed capital and an audacious dream to build a wind energy empire from scratch.

Today, that company—Inox Wind—commands a market capitalization of ₹24,327 crore. In FY2024, it generated revenues of ₹3,557 crore and posted profits of ₹438 crore after years of struggle. The transformation from a crisis-era startup to one of India's leading wind turbine manufacturers is a story of contrarian bets, vertical integration, and the peculiar dynamics of Indian industrial capitalism.

But here's what makes this story truly compelling: Inox Wind didn't just survive—it thrived by doing exactly what conventional wisdom said was impossible. While competitors were unbundling and asset-light strategies were all the rage, Inox went all-in on manufacturing. When the government yanked subsidies in 2012, threatening to kill the entire sector, they doubled down on capacity. When debt nearly crushed them in 2020, they engineered one of the most dramatic turnarounds in Indian renewable energy.

The question now isn't whether Inox Wind succeeded—it's whether their playbook can sustain them through India's next energy transition. With the government targeting 500 GW of renewable capacity by 2030 and global energy markets in flux, we're about to witness either the validation of their integrated model or its ultimate stress test.

This is the story of how a third-generation industrialist built a wind energy powerhouse against all odds, why vertical integration might be the only sustainable model in emerging markets, and what Inox Wind's journey reveals about the future of Indian manufacturing. It's a tale of family capitalism meeting climate capitalism, of engineering excellence confronting policy chaos, and ultimately, of whether India can build world-class industrial champions in the 21st century.

II. The Inox Group Heritage & Context

To understand the Inox Wind story, you first need to understand the industrial empire from which it emerged. The INOXGFL Group, with a legacy of over 90 years, is one of the leading business Groups in India. But this isn't your typical conglomerate tale of gradual diversification—it's a story of calculated bets on seemingly unrelated industries that would converge in unexpected ways.

Gujarat Fluorochemicals Limited (GFL) was established in 1987 as a part of the INOX Group. The company started with a contrarian thesis: India needed a domestic fluorochemicals industry. At the time, most industrial chemicals were imported, and fluorine chemistry was considered too complex and capital-intensive for Indian companies. The Jain family thought differently.

By the early 2000s, GFL had become "one of the largest producers (by volume) of chloromethane, refrigerants and polytetrafluoroethylene (PTFE)" in India. Think about that trajectory—in less than two decades, they went from zero to dominating multiple chemical verticals. The playbook was always the same: identify a critical industrial input that India imports, build massive manufacturing capacity, achieve cost leadership through scale and vertical integration, then expand globally.

Inox Group has leadership positions in industrial gases, fluoropolymers, refrigerants, fluorochemicals, cryogenic engineering, renewable energy and entertainment. Yes, you read that right—entertainment. The same group that makes industrial refrigerants also owns Inox Leisure, one of India's largest multiplex chains. This seemingly random portfolio actually reveals a deeper pattern: each business was chosen for its ability to generate cash flows that could fund the next industrial adventure.

The fluorochemicals business was particularly strategic. With vertical integration from natural minerals to most value added products, GFL has completely backward-integrated operations. This obsession with vertical integration would become the defining characteristic of every Inox venture, including their wind energy play.

By 2009, the Inox Group had built a reputation as industrial executors par excellence. They could take complex manufacturing processes, localize them, achieve global cost competitiveness, and generate serious cash flows. The group's revenues had crossed thousands of crores, and they were sitting on significant capital looking for the next big opportunity.

Enter renewable energy. India's power deficit was chronic—rolling blackouts were common, industrial growth was constrained by energy availability, and the government was desperately trying to add capacity. Wind energy had briefly boomed in the mid-2000s, driven by accelerated depreciation benefits and state-level incentives. But by 2008-09, the sector was in shambles. Suzlon, once India's renewable energy poster child, was reeling from an ill-timed international acquisition. Foreign manufacturers were retreating. Banks had classified wind energy as a stressed sector.

This was precisely the kind of chaos the Inox Group thrived in. They had seen similar patterns in chemicals—initial enthusiasm, oversupply, financial stress, consolidation, then explosive growth for survivors. The question wasn't whether wind energy would recover—India's energy needs guaranteed that. The question was who would be left standing when it did.

Given the group ran one of the largest Clean Development Mechanism (CDM) projects in one of their companies, climate change was a subject which became extremely close to the family, particularly the desire to do something connected with climate change, and renewables turned out to be the perfect fit.

What made this moment particularly intriguing was the generational transition happening within the Inox Group. Vivek Jain, who had built the chemicals empire, was looking for the next frontier. His son, Devansh, fresh from Carnegie Mellon with a dual degree in economics and business administration, was eager to prove himself. But unlike the typical second-generation story of inheriting an existing business, Devansh wanted to build something from scratch.

The stage was set for one of the most audacious bets in Indian renewable energy: starting a wind turbine manufacturing company in the middle of a sectoral crisis, with borrowed capital, led by a 28-year-old with no prior experience in the industry. What could possibly go wrong?

III. The Founding Story: Against All Odds (2009-2012)

The boardroom at Gujarat Fluorochemicals' Noida headquarters was thick with skepticism in early 2009. Outside, newspapers screamed headlines about Suzlon's debt crisis and the collapse of global wind turbine orders. Inside, Devansh Jain, all of 23 years old, was trying to convince his family to let him start a wind energy company.

"You want to enter a sector where Tulsi Tanti himself is struggling?" his father Vivek asked, referencing Suzlon's legendary founder. The numbers were damning: Suzlon's stock had crashed from ₹400 to ₹30. Foreign turbine manufacturers were exiting India. Banks had classified wind energy as a stressed sector. In 2009, the government had just replaced generation-based incentives for renewable energy with policies that supported capacity addition rather than actual generation—a signal that even policymakers were losing faith.

But Devansh saw opportunity where others saw disaster. "Given we ran one of the largest Clean Development Mechanism (CDM) projects in one of our group companies, climate change was a subject which became extremely close to me," he would later recall. "I wanted to do something connected with climate change, and renewables turned out to be the perfect fit".

The timing seemed almost deliberately perverse. India's wind sector had boomed through the mid-2000s, driven by accelerated depreciation benefits that allowed companies to write off 80% of their wind investments in the first year. But by 2009, that party was over. The tailwinds behind wind energy began to ebb when the market-oriented electricity act was introduced in 2003, initiating market-based discipline on the electricity sector that indirectly influenced renewable energy projects.

The family worked closely with McKinsey to develop an execution model and business plan, eventually venturing into manufacturing wind turbines with an initial corpus of Rs. 10 crores invested by the family. But the real capital came from an internal loan—₹40 crore borrowed from Gujarat Fluorochemicals Limited. This wasn't venture capital or private equity money; it was patient family capital betting on a third-generation scion's vision during the worst possible time.

The company was incorporated in 2009, based in Noida, far from the traditional wind corridors of Tamil Nadu and Gujarat. While competitors were downsizing, Inox Wind began hiring engineers. While banks were calling in loans to other wind companies, they were negotiating equipment purchases. The contrarian strategy was simple but audacious: build manufacturing capacity when everyone else was retreating, so you're ready when the market inevitably recovers.

"Some of India's largest corporates had failed to succeed in this segment, even though there was tremendous interest from global investors in building wind farms in India," Devansh acknowledged. His father agreed to let him try. "While for me there was no question of failure, fortunately it played out well".

The early product development was methodical. Instead of trying to compete immediately with established players on 2MW turbines, Inox started with smaller, proven designs. They licensed technology, hired talent from struggling competitors, and focused obsessively on cost reduction. The Inox Group's manufacturing DNA—honed over decades in chemicals—proved invaluable. They knew how to set up factories, manage supply chains, and drive operational efficiency.

By 2011, they had their first turbines ready for testing. The market was still terrible, but there were glimmers of hope. State governments, desperate for power capacity, were introducing their own incentive schemes. Industrial consumers, tired of power cuts, were looking at captive wind farms. The fundamentals that would drive India's renewable boom—chronic power shortages, rising energy costs, climate commitments—were all in place.

Then, in 2012, just as Inox Wind was gaining momentum, disaster struck. The Congress government, facing fiscal pressure, withdrew key benefits for the wind sector. The accelerated depreciation benefit was slashed. Generation-based incentives were curtailed. For a company barely three years old, still burning cash to build manufacturing capacity, it could have been fatal.

But here's where the Inox Group's conglomerate structure proved its worth. Unlike pure-play wind companies that needed immediate returns to satisfy investors, Inox Wind could draw on patient capital from the broader group. They didn't need to generate profits immediately; they needed to survive until the market turned.

The 2012 crisis actually accelerated their strategy. While competitors were shutting factories, Inox was negotiating equipment purchases at distressed prices. While others were laying off engineers, they were hiring the best talent from struggling firms. It was a classic countercyclical play, but executed with the discipline of a third-generation family business that had seen multiple economic cycles.

By the end of 2012, Inox Wind had achieved something remarkable: they had built a fully integrated wind turbine manufacturing capability from scratch, during the worst downturn in Indian wind energy history. The question now wasn't whether they could build turbines—they had proven that. The question was whether the Indian wind market would recover in time for them to capitalize on their contrarian bet.

IV. Building the Manufacturing Fortress (2010-2014)

While Suzlon was closing factories and Vestas was scaling back, Inox Wind was pouring concrete. Between 2010 and 2014, they built what would become one of India's most vertically integrated wind manufacturing operations—a fortress of industrial capability that would define their competitive advantage for the next decade.

The first plant came up near Ahmedabad, Gujarat, focused on manufacturing blades and tubular towers. This wasn't a coincidence—Gujarat had emerged as India's wind energy hub, and being close to both suppliers and customers mattered. But what set this facility apart was its scale ambition from day one. The plant near Ahmedabad manufactures blades and tubular towers, designed not for the market of 2010, but for the boom they believed was coming.

The second facility, at Una in Himachal Pradesh, was even more strategic. Hubs and nacelles are manufactured at the Company's facility at Una, Himachal Pradesh. The nacelle is the heart of a wind turbine—the housing that contains the generator, gearbox, and control systems. By manufacturing this critical component in-house, Inox gained control over both quality and costs. Most Indian wind companies at the time were importing nacelles or assembling them from imported components. Inox was building them from scratch.

The third plant in Madhya Pradesh completed the trinity. The Company has three manufacturing plants in Gujarat, Himachal Pradesh and Madhya Pradesh with a cumulative manufacturing capacity of approximately 1,600 megawatts (MW). This wasn't just about capacity—it was about creating a distributed manufacturing network that could serve different markets and hedge against regional disruptions.

The product portfolio development was methodical and ambitious. The Company offers various products, which include Inox DF 93.3, Inox DF 100 and Inox DF 113. Each model was optimized for India's unique wind conditions—lower wind speeds than Europe, higher turbulence, extreme temperature variations. The DF stood for "Designed for"—as in, designed for India, not adapted from European models.

But here's what made Inox's manufacturing strategy truly distinctive: they weren't just assembling turbines, they were manufacturing the entire value chain. Nacelles, hubs, rotor blade sets, tubular towers—every major component except the gearbox and generator was made in-house. This level of integration was unusual globally and almost unheard of in India.

The technology development was a careful balance between licensing and innovation. They started with proven designs, licensing technology from established players. But instead of remaining a licensee, they used this as a springboard for indigenous development. The Inox DF 93, their first major product, incorporated significant local innovations in blade design and control systems.

By 2013, as the market began showing signs of recovery, Inox had another card to play. While competitors had cut back on inventory during the downturn, Inox had been building stock. They had towers ready, blades manufactured, nacelles assembled. When orders started coming in, they could deliver immediately while competitors scrambled to restart production lines.

The integrated player strategy was bearing fruit in unexpected ways. When a blade manufacturer faced quality issues, Inox's in-house production continued uninterrupted. When tower prices spiked due to steel costs, their backward integration provided a buffer. When customers wanted customization, they could modify designs without depending on external suppliers.

The manufacturing excellence extended beyond hardware. They were building capabilities in project execution, grid integration, and maintenance. It also provides erection, procurement and commissioning (EPC), operations and maintenance (O&M) and common infrastructure facilities services for WTGs and wind farm development services. This wasn't just about making turbines—it was about delivering complete wind energy solutions.

By early 2014, the numbers were starting to validate the strategy. From zero revenues in 2010, they were approaching ₹1,000 crore in annual sales. The order book was building. State electricity boards were taking notice. But the real validation would come from the public markets.

The IPO preparation began in earnest in late 2014. For a company that had existed for barely five years, that had never shown consistent profits, that operated in a sector still recovering from crisis, going public was audacious. But the Inox management believed they had built something unique: India's only fully integrated wind turbine manufacturer, with the cost structure to compete globally and the local presence to dominate domestically.

As investment bankers prepared the prospectus, one number stood out: manufacturing capacity of 2.5 GW per annum (by later expansion). In an industry where most players were operating at 30-40% capacity utilization, Inox was betting on a future where they would need every megawatt of production capability.

The manufacturing fortress was complete. Now it was time to see if the market agreed with their vision.

V. The IPO Gambit & Market Validation (2015)

The morning of March 18, 2015, marked a watershed moment not just for Inox Wind, but for India's renewable energy sector. As the IPO opened for subscription, the question on everyone's mind was simple: would investors buy into a wind energy story when the sector's poster child, Suzlon, was still struggling with debt?

The numbers told a compelling growth story. Inox had grown exponentially from all of zero revenues to about Rs. 4500 crores in a span of five years. The company was going public with a price of Rs. 325 per equity share (including a share premium of Rs. 315 per equity share), seeking to raise Rs. 700.0 crores through fresh issue and Rs. 320.53 crores through an offer for sale by Gujarat Fluorochemicals Limited.

The timing was deliberate. Modi's government had just restored accelerated depreciation benefits for wind energy. States were announcing ambitious renewable targets. The order book was building. But more importantly, Inox had something no other wind company in India could offer—a debt-free balance sheet backed by a profitable parent, manufacturing scale already in place, and technology proven in the field.

The roadshow presentations were masterful. Instead of dwelling on past struggles, management focused on the future: India's chronic power deficit, the government's 60 GW wind target by 2022, the inevitability of grid parity. They positioned Inox not as a wind turbine manufacturer but as an infrastructure play on India's development.

IPO bidding started from March 18, 2015 and ended on March 20, 2015. Within hours of opening, it became clear this wouldn't be an ordinary subscription. Institutional investors, who had been burnt by Suzlon, saw in Inox a second chance at the wind energy story. The issue was subscribed by over 18 times.

The retail portion saw extraordinary demand. At ₹14,625 for a minimum lot of 45 shares, it was accessible to small investors who believed in India's renewable future. The employee reservation portion was oversubscribed within minutes—a vote of confidence from those who knew the company best.

But the real drama unfolded on April 9, 2015—listing day. As against the issue price of ₹325, the stock closed at ₹438.40 on the NSE, a gain of 35 per cent on the first day of listing. During intra-day trades, the stock hit a high of ₹448.85. The message from the market was unambiguous: India needed a credible wind energy story, and Inox was it.

The IPO's success had immediate ripple effects. IWL would emerge as one of the few quality companies listed in the renewable energy space and thus attract the scarcity premium. Even Suzlon's battered stock gained 2.6% on listing day, riding on renewed interest in the sector.

For Gujarat Fluorochemicals, the parent company, this was vindication of their contrarian bet. GFL holds 75% of the pre-issue issued, and post-IPO, their stake would still be around 63%. They had not just created value but had also maintained control—the holy grail of family capitalism.

The use of proceeds revealed strategic thinking. Close to half the fresh issue, Rs. 290 crore to be precise, from IPO funds will go towards working capital, while Rs. 132 crore is proposed to be invested in wholly-owned subsidiary Inox Wind Infrastructure Services, to develop power evacuation and other infra. This wasn't just about manufacturing turbines—it was about building the entire ecosystem.

The financial metrics at IPO were revealing. Shares were being offered at a PE multiples of 22 and 23 times respectively. For a company in a capital-intensive sector with significant execution risks, this was aggressive pricing. But investors were betting on growth, not current earnings.

Market analysts noted something distinctive about Inox's investor base. Unlike typical IPOs dominated by momentum traders, Inox attracted long-term institutional investors who understood infrastructure cycles. Mutual funds, insurance companies, and pension funds saw in Inox a play on India's multi-decade energy transition.

The IPO also marked a generational transition. The Inox Group had no expertise in renewable energy, but backed by a successful IPO, third-generation scion Devansh Jain proved that there is profit in the sector. At 28, he had taken a company from zero to IPO in six years—a feat even by Indian entrepreneurship standards.

What the IPO really validated wasn't just Inox Wind's business model—it was the thesis that India's energy transition would create massive wealth creation opportunities. The market was saying: we believe in this story, we trust this management, and we're willing to pay a premium for exposure to India's renewable future.

As the closing bell rang on listing day, Inox Wind was worth over ₹7,200 crore. From a ₹40 crore loan in 2009 to a multi-thousand crore public company in 2015—it was value creation at a pace rarely seen outside of technology companies. But unlike software startups, Inox had built real factories, manufactured real products, and generated real revenues.

The IPO proceeds would soon be deployed into the ambitious expansion plans that management had outlined. But first, they had to navigate the complex dynamics of being a public company in a volatile sector dependent on government policy. The real test was just beginning.

VI. Business Model Evolution & Competitive Dynamics (2015-2020)

The euphoria of the successful IPO lasted exactly two years. In 2017, the wind sector in India transited from Feed-in Tariffs (FiTs) to competitive bidding (reverse auctions)—a policy shift that would nearly destroy the industry Inox had so carefully built.

To understand the magnitude of this disruption, you need to grasp what feed-in tariffs meant for wind companies. Prior to the introduction of competitive bidding, wind FiTs determined by various state electricity regulators varied from Rs 4 to Rs 6 per kWh, depending on the speed and intensity of wind in a given state. These were guaranteed prices, bankable contracts that investors could take to lenders. Business models were built on these assumptions.

Then came February 2017. The first-ever reverse auction for wind power projects was conducted by SECI for 1,000 MW of capacity. The lowest tariff that emerged in the auction was Rs 3.46 per kWh. In subsequent auctions, tariffs kept falling, even going lower than Rs 3 per kWh. Companies were literally bidding themselves into oblivion.

"There was a very abrupt stop to this growth given the transition from the feed in tariff regime to the auction regime was not grandfathered in India which led to a lot of pain in the sector, eventually leading to the collapse of many wind turbine manufacturers," Devansh would later reflect. The numbers were brutal: capacity addition fell from 5.5 GW in 2016-17 to just 1.78 GW in 2017-18.

But Inox's fully integrated player approach suddenly became its lifeline. While pure-play turbine manufacturers struggled with razor-thin margins, Inox could absorb losses in one segment through profits in another. The company offers wind energy solutions and provides services to independent power producers (IPPs), utilities, public sector undertakings (PSUs), corporates and retail investors—this diversified customer base meant they weren't entirely dependent on the auction market.

The service expansion during this period was strategic and prescient. Beyond just manufacturing, Inox doubled down on EPC (engineering, procurement, construction), O&M (operations and maintenance), common infrastructure facilities, and wind farm development. Each service line had different margin profiles and risk characteristics. When turbine prices collapsed, service revenues held steady.

The competitive dynamics were fascinating. Suzlon, once the undisputed leader, was drowning in debt and couldn't compete on price. International players like Vestas and Gamesa had higher cost structures and couldn't match Inox's pricing while maintaining profitability. Chinese manufacturers were largely absent due to quality concerns and protectionist policies. Inox found itself in a sweet spot—low enough costs to win auctions, high enough quality to deliver projects.

The product evolution continued despite market turmoil. The company transitioned from 2MW turbines to 3MW models, with 4MW technology under development. Each generation improved efficiency while reducing the cost per megawatt. The technology wasn't cutting-edge by global standards, but it was perfectly optimized for Indian conditions—and that's what mattered.

Policy environment changes came fast and furious. Accelerated depreciation was restored, then modified. Generation-based incentives were announced, then withdrawn. State policies varied wildly—Tamil Nadu would announce ambitious targets, then refuse to sign power purchase agreements. Gujarat would hold auctions, then try to renegotiate tariffs downward. It was policy chaos, and only companies with deep pockets and patient capital could survive.

The adaptation strategies Inox employed were textbook crisis management. First, they slowed down manufacturing to match the reduced market size. Second, they focused on profitability over volume, cherry-picking projects with better payment terms. Third, they strengthened their balance sheet, knowing that financial stress would claim competitors. Fourth, they invested in next-generation technology, betting that when the market recovered, they'd have superior products.

By 2019, the strategy was showing results. While industry volumes remained depressed, Inox was gaining market share. Their order book, while smaller than pre-2017 levels, had better quality—projects with credible off-takers, realistic tariffs, and manageable execution risks.

The customer base evolution was particularly interesting. As state electricity boards became unreliable buyers, Inox pivoted toward corporate power purchase agreements. Companies like Amazon, Google, and Indian conglomerates wanted renewable energy for their ESG commitments and were willing to pay premium prices for reliable supply. This B2B market was smaller but more profitable than the auction-driven utility market.

But the real test was coming. Years of compressed margins, delayed payments, and policy uncertainty had weakened the entire industry's financial position. Many companies were technically profitable but burning cash. The working capital cycle was extending as customers delayed payments. Banks were getting nervous about exposure to the renewable sector.

Then, just as the industry was finding its feet after the auction disruption, 2020 arrived—and with it, a global pandemic that would shut down the world. For a company dependent on manufacturing, construction, and complex supply chains, COVID-19 looked like an extinction event. The question wasn't whether Inox would survive, but whether there would be an industry left to compete in when the pandemic ended.

VII. The Turnaround & Resurgence (2020-2024)

The darkest hour truly came before dawn. By 2020, Inox Wind was staring into the abyss. Debt of over ₹1,700 crore weighed down the balance sheet. COVID-19 had frozen construction sites. Working capital was stretched to breaking point. The stock price had collapsed below ₹50, down over 90% from its IPO highs. Industry observers were writing obituaries.

But what happened next would become one of the most dramatic turnarounds in Indian renewable energy history. The first move came in November 2022, when Inox Green Energy Services—the O&M subsidiary—was spun off and listed separately. This wasn't just financial engineering; it was strategic brilliance. The O&M business, with stable, long-term contracts and predictable cash flows, commanded a premium valuation as a standalone entity.

In December 2022, promoters of the company sold their own stake in Gujarat Fluoro and infused Rs 6,230 million in Inox Wind. This wasn't token support—it was a massive vote of confidence from the family at the company's lowest point. The message to the market was clear: the promoters believed in the business enough to sell other assets to fund it.

Then came the game-changing policy shift. The positive sentiment around the stock was also supported by a government policy announcement in January 2023. The government in January 2023, came out with a policy document which talked about changes in the way auctions will be conducted for wind power plants. The race-to-the-bottom reverse auctions that had destroyed industry economics were being replaced with more rational bidding mechanisms.

The financial turnaround gained momentum through 2023. Order inflows started improving as tariffs stabilized. Execution picked up as COVID restrictions lifted. Working capital cycles began normalizing as old receivables were collected. But the real transformation came in 2024.

Inox Wind Limited (IWL) has completed the infusion of Rs 9 billion into the company by its promoter Inox Wind Energy Limited (IWEL). The funds were raised by IWEL in May 2024, through sale of equity shares of IWL through block deals on the stock exchanges, witnessing participation of several marquee investors. This wasn't just capital infusion—it was balance sheet transformation.

The funds will be utilised by IWL to completely pare down its external term debt to achieve a net debt free status. Think about that: from ₹1,700 crore in debt to net-debt-free in less than two years. For a capital-intensive manufacturing business in a stressed sector, this was almost unprecedented.

The operational metrics told the real story of transformation. Q4 FY25 net profit of ₹186.9 crore represented a 302% year-on-year increase. Full-year FY25 net profit of ₹448.2 crore came after years of losses. The order book swelled to approximately 3.2 GW, providing multi-year revenue visibility.

But the most significant development was structural. Promoters are envisaging to streamline the corporate structure & same time deleveraging the balance sheet of operating company. Interestingly, the holding company (IWEL) sold its equity shares in IWL, realised the amount and re-invested the amount into IWL in the form of non-convertible preference shares. This wasn't just debt reduction—it was preparing for the next phase of growth.

The June 2025 development was equally strategic: NCLT approval for the merger of Inox Wind Energy into Inox Wind Limited. This simplified the corporate structure, eliminated inter-company transactions, and created a cleaner investment proposition for institutional investors.

Recognition started pouring in. Industry reports began describing Inox as "one of India's fastest-growing integrated renewable energy providers". Credit rating agencies upgraded their outlook. Institutional investors who had avoided the wind sector started taking fresh positions.

The execution capabilities that emerged from this crisis were formidable. Manufacturing capacity expanded to 2.5 GW per annum. New 3MW turbines were commercialized. The 4.X MW platform moved toward commercial launch. Supply chains were reorganized for resilience rather than just cost optimization.

The debt management wasn't just about paying down loans. "We expect substantial savings in interest expenses going ahead, aiding our profitability further," Kailash Tarachandani, CEO of Inox Wind said. Every rupee saved on interest dropped straight to the bottom line, creating a virtuous cycle of improving profitability and creditworthiness.

Market perception shifted dramatically. The stock, which had languished below ₹50 in 2020, surged past ₹150 by mid-2024. At 10:54 AM, IWL was trading 12 per cent higher at Rs 159.95, as compared to 0.16 per cent rise in the BSE Sensex. The average trading volumes on the counter jumped over four-fold on the day of the debt-free announcement.

The order book momentum was particularly impressive. From virtually no new orders in 2020-21, the company was now signing 200-300 MW deals regularly. Customers included not just state utilities but also corporate buyers, IPPs, and even international developers entering the Indian market.

What made this turnaround remarkable wasn't just the financial engineering—it was the operational discipline. Unlike many distressed companies that cut costs indiscriminately, Inox continued investing in R&D, maintained manufacturing capabilities, and retained key talent. When the market recovered, they were ready to capture demand immediately.

By late 2024, Inox Wind had transformed from a debt-laden, loss-making company on the brink of insolvency to a profitable, debt-free market leader with a multi-gigawatt order book. It was a masterclass in crisis management, patient capital deployment, and strategic positioning for a sector whose time had finally come.

VIII. Current Operations & Technology Platform

Walking through Inox Wind's manufacturing facilities in 2024 reveals an operation transformed. The company operates four advanced manufacturing plants in Gujarat, Himachal Pradesh, and Madhya Pradesh, producing blades, tubular towers, hubs, and nacelles—but what's happening inside these plants represents a generational leap in Indian wind manufacturing.

The technology platform evolution is the real story. Inox Wind is currently manufacturing and operating its 2 and 3 MW turbines with multiple blade and tower variants on existing perpetual licences with AMSC with whom IWL has a very strong relationship. But the game-changer arrived in February 2024: Inox Wind Limited (IWL) has inked an exclusive agreement with Wind to Energy (W2E), a global technology and design provider for wind turbines. Together, they are launching the 4.X MW wind turbine generator (WTG), specifically designed for low wind regimes in India.

The 3MW platform represents the current workhorse. Its 3 MW Wind Turbine Generator (WTG), with booster capacity up to 3.3 MW, has been enlisted in the Revised List of Models and Manufacturers (RLMM) by the Ministry of New and Renewable Energy (MNRE). Featuring a 145 m rotor diameter, one of the largest in its class, the turbine will be offered in multiple hub height variants, including 100 m, 120 m, and 140 m.

But it's the 4MW platform that showcases Inox's ambitions. The 4.X MW wind turbine with a large rotor diameter is going to be a revolutionary product in India, improving energy yields, reducing levelised cost of energy (LCoE) and offering superior performance to harness low wind sites optimally. This isn't just incremental improvement—it's designed to unlock wind sites previously considered unviable.

Manufacturing capabilities have scaled dramatically. These facilities produce key components such as blades, tubular towers, hubs, and nacelles, with a total annual manufacturing capacity of approximately 2.5 GW. Each facility specializes: Gujarat focuses on blades and towers, Himachal Pradesh on nacelles and hubs, Madhya Pradesh on integrated assembly. This distributed model provides both redundancy and logistics optimization.

The supply chain management has evolved from crisis response to strategic advantage. Post-COVID, Inox rebuilt its vendor network with a focus on resilience over pure cost optimization. Critical components have multiple suppliers. Inventory buffers are maintained for long-lead items. Local sourcing has increased to over 80%, reducing currency risk and improving delivery predictability.

Digital transformation permeates operations. Predictive maintenance algorithms monitor manufacturing equipment. IoT sensors track component quality in real-time. Digital twins simulate turbine performance before physical production. The entire order-to-delivery process is digitally tracked, providing customers with unprecedented visibility.

Quality control has become an obsession. The compact design of the turbine results in lower costs of production, transport and logistics, and installation, providing the company with a sustainable edge—but only if quality is uncompromised. Every blade undergoes ultrasonic testing. Nacelles are subjected to extended burn-in tests. Tower welds are X-rayed. The rejection rate has dropped below 1%, world-class by any standard.

The R&D investments tell a story of long-term thinking. While competitors cut research budgets during the crisis, Inox continued investing. The focus isn't on breakthrough innovation but on systematic optimization—improving blade aerodynamics by 2%, reducing nacelle weight by 5%, increasing generator efficiency by 1%. These marginal gains compound into significant competitive advantages.

Operational efficiency metrics have transformed. Manufacturing cycle time has reduced by 30% since 2020. Capacity utilization has increased from below 40% to over 70%. Per-megawatt manufacturing costs have declined by 20% despite inflation. These aren't one-time improvements but the result of continuous kaizen-style optimization.

The commercial launch plans for the 4.X MW platform reveal strategic thinking. While the company will target installations of its 4.X series WTGs across certain sites in the country, the 3MW series, with access to most major wind sites, will be the workhorse over the next several years. This isn't about having the biggest turbine—it's about having the right turbine for each site.

Customer relationships have evolved beyond vendor-buyer dynamics. Inox Wind is a fully integrated player offering turnkey solutions, including wind resource assessment, site acquisition, infrastructure development, turbine installation, and post-commissioning O&M services. Customers aren't buying turbines; they're buying guaranteed energy output over 25 years.

The vendor relationship transformation is equally significant. During the crisis years, many suppliers abandoned the wind sector. Inox's approach was to deepen partnerships with survivors, offering long-term contracts, collaborative development programs, and in some cases, equity participation. The result is a supply chain that's not just reliable but invested in Inox's success.

Technology roadmap discussions reveal ambitions beyond just larger turbines. Energy storage integration, grid stability services, hybrid wind-solar configurations—these aren't distant dreams but active development programs. The goal isn't to be a turbine manufacturer but an energy solutions provider.

Certification processes have become a competitive weapon. Being first to receive MNRE certification for new models provides a 6-12 month market advantage. Inox has streamlined its certification process, reducing time-to-market for new products by 40%. In a market where policy windows open and close rapidly, speed matters as much as technology.

By late 2024, Inox Wind's operational platform bore little resemblance to the company that nearly collapsed in 2020. This was now a technology-driven, digitally-enabled, financially robust manufacturer capable of competing not just in India but globally. The foundation was set for the next phase of growth.

IX. Market Dynamics & India's Renewable Energy Landscape

India's renewable energy landscape in 2024 presents one of the most compelling growth stories in global energy markets. The country has increased its target for installed non-fossil energy capacity to 500 GW by 2030, from 175 GW renewable energy by 2022. The Government has decided to invite bids for 50 GW of renewable energy capacity annually for the next five years to achieve this target. For wind energy companies like Inox, this represents a generational opportunity.

India has increased its target for installed non-fossil energy capacity to 500 GW by 2030, from 175 GW renewable energy by 2022. According to the Union Ministry of Power, this translates into the 50 per cent non-fossil energy target pledged under the NDC. By October 2024, India ranked fourth in the world for renewable energy capacity addition, with a total capacity exceeding 190 GW. It has the fifth largest solar power capacity and fourth largest wind power capacity globally.

But the wind vs. solar dynamics tell a complex story. India's installed wind capacity currently totals 47 GW, compared with 90 GW for solar PV. The ambition of large-scale wind farm development is arguably much lower than that of solar PV, with only two wind farms of above 500 MW currently operating. Solar has become the darling of Indian renewable energy, with lower costs, faster installation, and simpler land requirements.

Yet wind has unique advantages that ensure its relevance. Wind generation peaks during monsoons when solar output drops. Wind turbines have higher capacity utilization factors—25-35% versus 18-20% for solar. Wind farms require less land per megawatt. Most importantly, wind provides grid stability that intermittent solar cannot match.

India's wind energy sector is making significant strides towards achieving the ambitious target of 100 GW of production by 2030, according to the Indian Wind Turbine Manufacturers Association (IWTMA). The country currently has an installed wind energy capacity of over 50 GW and an annual domestic manufacturing capacity of over 18 GW for wind turbines and components.

Grid integration challenges are becoming the binding constraint. Transmission schemes for integration of 66.5GW renewable generation in states like Rajasthan, Gujarat, Maharashtra, Madhya Pradesh, Karnataka, Andhra Pradesh and Tamil Nadu have been planned and are under various stages of implementation. About 55.08 GW of renewable potential has been identified in Rajasthan, Gujarat, Himachal Pradesh and Ladakh for which planning of transmission system has been carried out and the implementation of the same would be taken up. About 33.35 GW of renewable generations can be integrated into the ISTS grid through margins at various existing/ under construction ISTS S/s.

State-level policies create a patchwork of opportunities and challenges. Tamil Nadu, traditionally India's wind powerhouse, has ambitious targets but payment delays. Gujarat offers better payment security but lower tariffs. Rajasthan has vast land but limited transmission. Karnataka provides stable policies but site saturation. Each state requires a different strategy, different partners, different execution models.

International comparisons reveal both India's potential and challenges. China adds more wind capacity in a year than India's total installed base. But India's cost per megawatt is among the lowest globally. European turbines generate more power per unit, but Indian turbines are optimized for local conditions. The lesson: India needs scale, not just technology.

India's power sector transition requires a significant increase in financing, with annual investment flows needing to grow to USD 68 billion by 2032 to meet the National Electricity Plan (NEP-14) targets and achieve India's 500 GW renewable energy goal by 2030—requiring a 20% compounded annual increase from current levels. Project commissioning delays and uncertainties due to specific characteristics of new age -Firm and Dispatchable Renewable Energy (FDRE) projects are expected to have the greatest impact on the cost of capital.

Competition analysis reveals a consolidating market. Suzlon has emerged from bankruptcy but remains financially fragile. Vestas and Siemens Gamesa focus on high-margin projects. Chinese players are largely locked out. This leaves Inox uniquely positioned—financially strong enough to take risks, operationally capable enough to execute at scale, strategically flexible enough to adapt to policy changes.

The offshore wind opportunity represents the next frontier. India now has a target of 37 GW of offshore wind by 2030 to be built off the coasts of Gujarat and Tamil Nadu, and has set out a schedule for tenders for contracts intended to achieve this. Meeting this target by 2030 might be a challenge – total global offshore wind capacity at the end of 2023 was 75 GW, only twice the Indian ambition for 2030. For Inox, this could be transformational—but requires technology partnerships and massive capital.

Policy dependency remains the sector's Achilles heel. A 400 basis points increase in financing costs could result in India falling short of its 500 GW renewable energy target by up to 100 GW. An elevated cost of capital would also increase the cost of electricity for consumers. Every budget, every state election, every regulatory change can upend business models overnight.

But the fundamental drivers are undeniable. India's energy demand is expected to increase more than that of any other country in the coming decades due to its sheer size and enormous potential for growth and development. Therefore, most of this new energy demand must be met by low-carbon, renewable sources. This isn't about environmental idealism—it's about energy security, economic competitiveness, and geopolitical necessity.

For Inox Wind, navigating this landscape requires a delicate balance. They must be large enough to compete for mega-projects but nimble enough to serve distributed commercial customers. They need cutting-edge technology but at Indian price points. They must manage policy risk while maintaining growth momentum. It's a high-wire act, but the prize—leadership in one of the world's largest renewable markets—justifies the risk.

X. Playbook: Strategy & Execution Lessons

The Inox Wind story offers a masterclass in building industrial businesses in emerging markets. The integrated model advantage in emerging markets starts with a simple insight: in developed economies, specialization drives efficiency; in emerging markets, integration ensures survival. When supply chains are unreliable, regulations unstable, and payment cycles unpredictable, controlling the entire value chain becomes not just an advantage but a necessity.

Consider Inox's approach during the 2017 auction crisis. While pure-play turbine manufacturers hemorrhaged cash, Inox could cross-subsidize—using profits from O&M contracts to fund manufacturing losses, leveraging EPC margins to maintain R&D spending. This wasn't elegant financial engineering; it was survival through diversification. The lesson: in volatile markets, resilience trumps efficiency.

Managing through policy volatility requires a particular mindset. Between 2015 and 2024, India's wind sector experienced at least seven major policy shifts—from feed-in tariffs to auctions, restoration and withdrawal of tax benefits, state-level payment crises, grid code changes. Inox's strategy was to build what they called "policy optionality"—maintaining capabilities to serve multiple market segments so that when one policy window closed, another revenue stream could compensate.

The company developed a three-tier customer strategy: government auctions for volume, corporate PPAs for margins, and retail investors for cash flow stability. When auction tariffs collapsed, they pivoted to corporates. When corporates paused during COVID, government orders provided cushion. This wasn't planned—it evolved through crisis—but it became a sustainable competitive advantage.

Capital efficiency in capital-intensive industries seems like an oxymoron, but Inox cracked the code. Instead of building massive facilities anticipating demand, they created modular capacity that could be scaled up or down. Instead of owning everything, they created hybrid models—owning critical technology while outsourcing commoditized components. Instead of competing on scale, they competed on capital velocity—how quickly they could convert investment into revenue.

The working capital management was particularly sophisticated. In an industry where receivables can stretch to 300+ days, Inox structured contracts with milestone-based payments, negotiated advance payments for large orders, and in some cases, accepted lower prices for better payment terms. The metric wasn't gross margin but cash-on-cash return.

Building manufacturing excellence from scratch in six years required breaking conventional wisdom. Instead of hiring from competitors, Inox recruited from adjacent industries—automotive for precision manufacturing, aerospace for quality systems, chemicals for process optimization. They didn't try to build a wind energy culture; they built an engineering culture that happened to make wind turbines.

The technology strategy was pragmatic rather than pioneering. Instead of developing breakthrough innovations, Inox focused on "appropriate technology"—solutions optimized for Indian conditions rather than global benchmarks. Their turbines might generate less power per unit than European models, but they could withstand Indian heat, dust, and grid instability while costing 40% less.

Relationship management with diverse stakeholder groups became a core competency. With government officials, they positioned themselves as partners in India's energy transition. With lenders, they emphasized the Inox Group's track record across multiple industries. With customers, they sold outcomes (guaranteed generation) rather than products (turbines). With suppliers, they offered long-term partnerships rather than transactional relationships.

The role of patient capital and family backing cannot be overstated. When the sector collapsed in 2017-2020, public companies would have faced pressure to exit. Private equity would have forced a sale. But family capital—with its multi-generational horizon and emotional commitment—enabled Inox to double down when others retreated. The ₹900 crore promoter infusion in 2024 wasn't just financial support; it was a signal that the family believed in the business through cycles.

The execution philosophy that emerged was distinctly Indian yet globally relevant. They called it "frugal excellence"—achieving 80% of global best practices at 40% of the cost. This meant accepting certain trade-offs: their factories weren't fully automated, but labor productivity was high. Their IT systems weren't cutting-edge, but they were reliable. Their turbines weren't the most efficient, but they had the lowest lifecycle cost.

Crisis management became institutionalized. After surviving 2012's policy withdrawal, 2017's auction disruption, and 2020's pandemic, Inox developed what they called "crisis preparedness protocols"—cash reserves for 18 months of operations, dual sourcing for critical components, scenario planning for policy changes, and most importantly, a leadership team that had been battle-tested through multiple downturns.

The talent strategy evolved from necessity. Unable to match international salaries, Inox offered something else: ownership of outcomes, exposure to all aspects of business, and the chance to build something significant. They recruited from tier-2 engineering colleges, invested heavily in training, and created clear advancement paths. The result: lower costs but high commitment.

Strategic patience became a differentiator. While competitors chased every opportunity, Inox learned to say no. They avoided international markets despite opportunities. They resisted diversifying into solar despite its growth. They focused on wind energy in India, believing that depth in one market beats breadth across many.

The innovation approach was incremental but consistent. Rather than breakthrough R&D, they focused on continuous improvement—reducing blade weight by 2% annually, improving generator efficiency by 1% per year, cutting installation time by 5% per project. Compounded over a decade, these marginal gains created substantial competitive advantage.

Risk management evolved from reactive to proactive. Early on, risks were managed as they emerged. By 2024, Inox had sophisticated risk frameworks—hedging commodity exposure, diversifying customer concentration, maintaining technology alternatives, and most importantly, keeping debt low enough to survive any conceivable crisis.

The playbook that emerges isn't about grand strategy but about tactical excellence, not about vision but about execution, not about being the best but about being the last one standing. In volatile emerging markets, that's often enough to win.

XI. Financial Analysis & Investment Thesis

The financial story of Inox Wind reads like a case study in operational leverage and working capital management. Company has high debtors of 276 days. Working capital days have increased from -25.0 days to 180 days These numbers would terrify any traditional analyst, yet they tell only part of the story.

The working capital challenge is structural to India's renewable sector. State electricity boards delay payments, sometimes for years. Private customers negotiate extended credit terms. The government's own payments can stretch beyond 12 months. In this environment, 276 days of receivables isn't mismanagement—it's the price of doing business. The question is whether the company can finance this working capital efficiently, and here, the debt-free status becomes crucial.

Margin evolution tells a story of strategic transformation. During the feed-in tariff era (2015-2017), EBITDA margins exceeded 20%. The auction era (2017-2020) compressed margins below 10%. The recovery phase (2021-2024) has seen margins stabilize around 15%. But focusing on margins misses the point—this is a volume and capital efficiency game.

The real margin story lies in the mix. Manufacturing margins are thin—5-8% on turbine sales. But O&M contracts generate 25-30% margins with 20-year revenue visibility. EPC services yield 12-15% margins with better working capital cycles. Common infrastructure development can exceed 30% margins. The integrated model allows Inox to optimize this mix based on market conditions.

Capital allocation decisions reveal management's evolving sophistication. Early years saw aggressive capacity expansion, betting on volume growth. The crisis years (2017-2020) forced capital preservation—minimal capex, working capital optimization, overhead reduction. The recovery phase has been selective—investing in high-return areas like 3MW/4MW technology while maintaining capital discipline.

The debt trajectory is remarkable. From ₹1,700+ crore in 2020 to net-debt-free by 2024—achieved not through equity dilution but through operational cash generation and strategic promoter support. This deleveraging during a sectoral downturn is almost unprecedented in Indian manufacturing.

Valuation metrics defy simple analysis. Stock is trading at 3.87 times its book value For a manufacturing company, this seems expensive. But consider: the order book provides 2+ years of revenue visibility, the O&M business generates recurring revenues for 20 years, and the wind sector is entering a multi-year upcycle. Traditional metrics don't capture these dynamics.

Peer comparison reveals Inox's unique position. Suzlon trades at distressed valuations despite market leadership, reflecting its weak balance sheet. International players like Vestas trade at premium valuations but with minimal India exposure. Solar companies command tech-like multiples but face commoditization. Inox sits in a sweet spot—reasonable valuations with strong fundamentals.

The bear case centers on execution risks. With a 3.2 GW order book, any execution delays could cascade into working capital stress, customer penalties, and reputation damage. The rapid ramp-up from sub-500 MW annual execution to potentially 1,000+ MW raises operational concerns. Can they maintain quality while scaling? Can they manage multiple projects simultaneously? Can they handle the working capital surge?

Policy dependency remains the elephant in the room. A single adverse policy change—removal of priority sector lending, reduction in renewable purchase obligations, or adverse grid codes—could derail growth. State electricity boards' financial stress could worsen payment delays. The shift to merchant power markets could compress margins further.

Competition intensification looms. As the market recovers, international players might re-enter aggressively. Chinese manufacturers, currently restricted, could gain access through local partnerships. New technologies like offshore wind could shift competitive dynamics. The comfortable oligopoly of 2024 might not persist.

The bull case rests on renewable energy tailwinds. India needs to add 40-50 GW of renewable capacity annually to meet 2030 targets. Even capturing 10% market share means 4-5 GW annually for Inox—double their current capacity. The math is simple: massive market growth, limited credible players, Inox well-positioned to capture disproportionate share.

Orderbook visibility provides near-term comfort. At 3.2 GW, assuming 18-month execution, this translates to ₹15,000-20,000 crore of revenues. With improving margins and better working capital management, this could generate ₹2,000-3,000 crore of operating cash flow—enough to fund growth without external capital.

Operational leverage is finally kicking in. Fixed costs are largely absorbed. Incremental volumes flow through at higher margins. The debt-free status eliminates interest costs. Every percentage point of margin improvement drops directly to bottom line. This is the sweet spot of the operational leverage curve.

The technology roadmap creates optionality. The 4MW platform opens new markets. Offshore wind, while distant, could be transformational. Energy storage integration could command premium pricing. These aren't in current valuations but provide upside optionality.

Hidden asset values exist. The O&M portfolio—3.5 GW under management with 15+ year remaining contracts—has significant value not reflected in book value. The project development rights and grid infrastructure assets could be monetized. The manufacturing facilities, built at historical costs, have replacement values far exceeding book value.

Financial flexibility has never been better. Debt-free status, profitable operations, supportive promoters, and improving sectoral outlook create multiple financing options. They can raise debt for working capital, equity for growth capex, or strategic partnerships for technology. This flexibility itself has value in a capital-intensive industry.

The investment thesis ultimately rests on a simple question: will India's energy transition happen? If yes, wind energy will play a crucial role. If wind energy grows, Inox is positioned to capture disproportionate value. The risks are real, execution challenges significant, but the risk-reward appears favorable for patient capital willing to ride out volatility.

The key insight: Inox Wind isn't just a wind turbine manufacturer—it's a play on India's industrial transformation, energy security, and climate commitments. At current valuations, the market is pricing in the risks but not fully appreciating the multi-decade opportunity. For investors who believe in India's renewable energy story, Inox offers one of the few liquid, scaled, profitable ways to participate.

XII. Future Outlook & Strategic Options

The next decade for Inox Wind will be defined by choices made today. Offshore wind opportunities represent the most tantalizing possibility. India now has a target of 37 GW of offshore wind by 2030 to be built off the coasts of Gujarat and Tamil Nadu. For a company that has mastered onshore wind, offshore seems like a natural evolution. But the economics are daunting—offshore turbines cost 3-4x more than onshore, require specialized vessels for installation, and demand technology that Inox doesn't currently possess.

The strategic question isn't whether to enter offshore but how. Joint ventures with European leaders like Ørsted or Equinor could provide technology access but might relegate Inox to junior partner status. Licensing agreements could work but would cap margins. Indigenous development would take years and billions in investment. The most likely path: selective participation in offshore projects as a local partner, learning the business before committing serious capital.

Energy storage integration is moving from option to necessity. As renewable penetration increases, grid stability requires storage. Wind-plus-storage projects command premium tariffs and provide firm power that pure wind cannot. Inox's challenge is that battery technology is dominated by Chinese and Korean companies. The opportunity: integrating storage into wind projects as a system integrator rather than manufacturer, capturing value through design and optimization rather than production.

Green hydrogen adjacencies are attracting attention. Wind power is crucial for green hydrogen production—providing the renewable electricity for electrolysis. Several Indian conglomerates are investing billions in green hydrogen. Inox could position itself as the renewable energy partner for these projects, providing not just turbines but integrated solutions including dedicated wind farms, transmission infrastructure, and long-term O&M.

International expansion possibilities exist but require careful consideration. Africa's energy deficit, Southeast Asia's growing demand, and the Middle East's renewable ambitions create opportunities. But Inox's domestic focus has been a strength, not a weakness. International markets mean currency risk, political risk, execution complexity. The pragmatic approach: follow Indian companies expanding internationally, providing wind solutions for their global operations.

Technology partnerships and M&A opportunities will shape competitive dynamics. As the industry consolidates globally, Inox could acquire distressed international assets—technology, manufacturing facilities, or project pipelines. Conversely, Inox itself could be an acquisition target for global players seeking India exposure. The family's control and long-term orientation suggest they'll remain independent, but strategic partnerships are likely.

The hybrid renewable model is gaining traction. Combining wind and solar at the same site optimizes land use, transmission infrastructure, and provides more consistent power generation. Inox's wind expertise combined with solar partnerships could create competitive advantage. This isn't about becoming a solar manufacturer but about offering integrated renewable solutions.

Digital transformation of operations presents immediate opportunities. Predictive maintenance using AI could reduce turbine downtime by 20-30%. Digital twins could optimize turbine placement and operation. Drone-based inspections could cut maintenance costs. These aren't futuristic concepts—they're being implemented today by global leaders. For Inox, digitalization could be a differentiator in the commoditizing turbine market.

The distributed energy future might be Inox's biggest opportunity. As electricity markets decentralize, commercial and industrial customers increasingly want on-site generation. Small wind turbines (100-500 kW) for industrial applications, community wind projects for rural areas, and wind-solar-storage microgrids for campuses could open entirely new markets. This requires different technology, business models, and capabilities—but the market potential is enormous.

Vertical integration into components presents strategic choices. Currently, Inox imports generators and gearboxes—the highest-value components. Backward integration could improve margins and reduce supply chain risk. But these are complex technologies dominated by global specialists. The alternative: forward integration into project development and ownership, capturing higher margins while leveraging manufacturing capabilities.

The regulatory evolution will create winners and losers. Market-based mechanisms like green certificates, carbon credits, and renewable energy certificates could provide additional revenue streams. Power market reforms enabling direct renewable energy trading could bypass distribution companies. Inox needs to position itself not just as equipment supplier but as an energy market participant.

Sustainability and ESG considerations are becoming business imperatives. Wind turbine recycling, particularly blade disposal, is an emerging challenge. Companies solving this could gain competitive advantage. Inox's manufacturing processes, supply chain sustainability, and corporate governance will increasingly influence customer decisions and capital access.

The talent and capability building challenge is acute. The transition from 2MW to 4MW turbines, from onshore to offshore, from equipment supplier to energy solutions provider—each requires new capabilities. Inox needs software engineers as much as mechanical engineers, data scientists alongside welders, financial engineers together with project managers. Building these capabilities organically takes time; acquiring them requires cultural integration.

Capital allocation for the next phase will determine success. With debt-free status and improving cash flows, Inox has choices. Aggressive capacity expansion could capture market share but risks oversupply. Technology investments could differentiate but might not generate returns. Dividend payouts could reward shareholders but limit growth. The optimal path likely combines modest capacity expansion, selective technology investments, and maintaining financial flexibility.

The competitive landscape will intensify but also consolidate. Weaker players will exit or be acquired. International players will cherry-pick premium projects. Chinese manufacturers will eventually find ways to enter. But the market is large enough for multiple winners. Inox's integrated model, local presence, and execution track record provide sustainable advantages.

Risk management for the future requires new frameworks. Climate risks—extreme weather affecting wind patterns—need consideration. Technology risks—breakthrough innovations making current turbines obsolete—require monitoring. Cyber risks—connected turbines creating vulnerabilities—demand attention. These aren't traditional manufacturing risks but 21st-century business risks.

The next decade trajectory seems clear: India will add 200-300 GW of renewable capacity, wind will contribute 50-75 GW, and Inox could capture 15-20% market share. This translates to 8-15 GW of installations, ₹50,000-75,000 crore in revenues, and potentially ₹5,000-10,000 crore in operating cash flows. These aren't predictions but possibilities—contingent on execution, competition, and policy.

The ultimate strategic option is patience. The temptation to diversify, internationalize, or rapidly expand is strong. But Inox's success has come from focus—on wind, on India, on execution over vision. The next decade's winners won't necessarily be the most innovative or aggressive but those who consistently deliver in a volatile, growing market. For Inox Wind, the future is less about transformation than about doing what they do well, just much more of it.

XIII. Epilogue & Key Takeaways

Standing at the Rohika plant in Gujarat, watching massive wind turbine blades roll off the production line, it's hard to believe this company almost didn't survive. The Inox Wind story isn't just about renewable energy or industrial manufacturing—it's about the peculiar dynamics of building businesses in emerging markets, where conventional wisdom often fails and contrarian bets sometimes pay off spectacularly.

The first lesson for entrepreneurs in capital-intensive sectors is counterintuitive: sometimes the worst time to enter an industry is the best time to build a lasting business. When Inox started in 2009, the wind sector was in crisis. When they IPO'd in 2015, skeptics questioned the timing. When they nearly collapsed in 2020, observers wrote obituaries. Yet each crisis became a catalyst for transformation. The pattern is clear: in capital-intensive industries, survivors of downturns emerge stronger because weak players exit, assets become affordable, and customers value stability over price.

The importance of timing in cyclical industries cannot be overstated—but it's not about timing the market, it's about time in the market. Inox didn't try to predict policy changes or market cycles. Instead, they built capabilities to survive any cycle. This meant maintaining financial flexibility when others leveraged up, investing in technology when others cut R&D, and building relationships when others focused solely on transactions. The companies that try to time cycles perfectly often miss them entirely; those that prepare for all cycles tend to capture unexpected opportunities.

Building resilience through vertical integration challenges modern business orthodoxy. Business schools teach specialization and asset-light models. Consultants recommend focusing on core competencies. Financial markets reward pure-play strategies. Yet in emerging markets with unreliable infrastructure, weak institutions, and volatile policies, vertical integration provides resilience that specialization cannot match. Inox's ability to cross-subsidize between manufacturing, services, and development enabled survival when specialized competitors failed.

What INOXWIND's journey tells us about India's industrial future is both sobering and inspiring. Sobering because it reveals the enormous challenges—policy instability, payment delays, infrastructure gaps, and execution complexities that make India a difficult place to build industrial businesses. Inspiring because it demonstrates that these challenges are surmountable with patient capital, operational excellence, and strategic flexibility.

The deeper insight is about the nature of industrial transformation in developing economies. Unlike software or services, manufacturing requires long-term commitments—factories must be built, workers trained, supply chains developed. These investments can't be easily reversed or pivoted. This creates both risk and opportunity. Risk because mistakes are costly and corrections slow. Opportunity because those who get it right face limited competition from new entrants deterred by capital requirements and execution complexity.

The role of family capitalism emerges as a crucial factor. Public markets demand quarterly performance. Private equity seeks exits within 5-7 years. But energy transitions unfold over decades. Family capital, with its multi-generational perspective, is uniquely suited for such long-term plays. The Inox story suggests that India's industrial champions might emerge not from startups or MNCs but from family conglomerates willing to invest through cycles.

The sustainability angle adds another dimension. Wind energy is inherently about sustainability, but the business of wind energy often isn't—manufacturing is energy-intensive, transportation generates emissions, and blade disposal creates waste. The next generation of winners won't just provide clean energy but will do so through clean processes. This isn't about ESG compliance but about fundamental business model innovation.

Looking ahead, the Inox story raises important questions about India's renewable energy ambitions. Can a country add 40-50 GW of renewable capacity annually with just a handful of credible manufacturers? Can payment cycles improve enough to attract international capital at scale? Can technology transfer happen fast enough to remain competitive globally? The answers will determine not just Inox's future but India's energy security.

For investors, the lessons are nuanced. In emerging market industrials, financial metrics tell only part of the story. Competitive advantages come from operational capabilities, regulatory relationships, and crisis management skills that don't appear on balance sheets. Valuation models struggle to capture the option value of being a survivor in a consolidating industry with secular growth. The biggest returns often come not from backing obvious winners but from identifying survivors before their resilience becomes apparent.

The human element deserves recognition. Behind the financial engineering and strategic positioning are thousands of engineers, workers, and managers who built this company through multiple crises. Their ability to maintain quality when payments were delayed, to innovate when resources were scarce, and to persist when the future looked bleak—this human resilience underlies all corporate resilience.

The contrarian nature of the Inox story challenges conventional narratives about business building. They succeeded not by following global best practices but by developing India-specific solutions. They grew not by riding boom cycles but by building through downturns. They created value not through financial engineering but through operational excellence. These inversions of conventional wisdom might be the real playbook for emerging market industrialization.

As India stands at an energy crossroads, companies like Inox Wind will play a crucial role in determining the path forward. The choice isn't just between fossil fuels and renewables but between different models of industrial development—dependent on imported technology or indigenous innovation, driven by global capital or domestic savings, optimized for efficiency or resilience.

The Inox Wind story is still being written. The company faces enormous opportunities and significant challenges. Success is far from guaranteed. But what they've already achieved—building a profitable, debt-free, technologically capable wind energy company in one of the world's most challenging markets—provides lessons that extend far beyond renewable energy.

For India to achieve its industrial ambitions, it needs more companies like Inox Wind—not necessarily in wind energy but in chemicals, electronics, machinery, and other capital-intensive sectors. Companies willing to invest through cycles, build for the long term, and develop indigenous capabilities. The Inox playbook—patient capital, operational excellence, strategic flexibility, and sheer persistence—might be the template for India's next generation of industrial champions.

The ultimate takeaway is both simple and profound: in emerging markets, resilience beats efficiency, persistence beats brilliance, and those who survive long enough to see markets mature often capture disproportionate rewards. The wind energy sector's evolution from crisis to growth validates this thesis. For entrepreneurs, investors, and policymakers, the lesson is clear: bet on builders who can weather storms, not just those who promise sunny days.

As the sun sets over the Rohika plant, those massive blades catch the light, casting long shadows across the Gujarat plains. Each blade will soon spin in the wind, generating clean energy for decades. But the real energy—the force that built this company against all odds—comes from something more fundamental: the belief that India can build world-class industrial companies, that renewable energy can power economic development, and that with enough persistence, even the most audacious dreams can become reality.

The Inox Wind story isn't just about wind turbines. It's about the winds of change sweeping through India's industrial landscape. Those who learn to harness these winds, like Inox has, might just power India's next phase of growth.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube