APTUS Value Housing Finance: The Story of India's Rural Housing Revolution

I. Introduction & Episode Roadmap

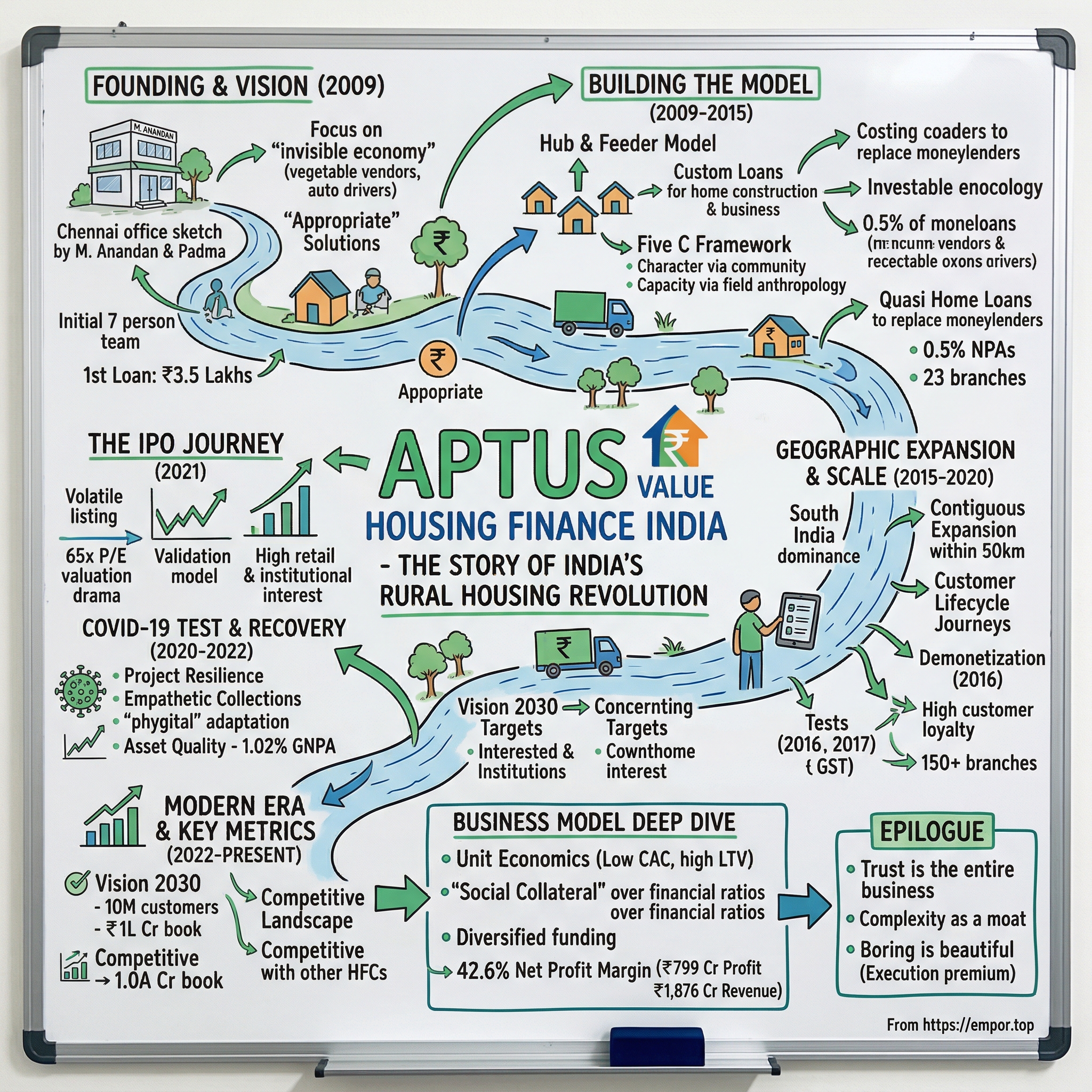

Picture this: A Chennai office in 2009, where two finance veterans are sketching out a business plan that every major bank has deemed too risky. They're targeting customers that traditional lenders won't touch—vegetable vendors, auto-rickshaw drivers, small shop owners in towns you've never heard of. Fast forward to 2024, and their company, APTUS Value Housing Finance, commands a market capitalization of ₹16,686 crores, generates revenues of ₹1,876 crores, and delivers profits of ₹799 crores with a staggering 42.6% net profit margin.

How did a startup focused on the most challenging segment of India's housing market—the informal economy workers in semi-urban and rural areas—become one of the most profitable housing finance companies in the country? The answer lies in a contrarian bet on India's invisible economy, a relentless focus on first principles thinking about credit assessment, and perhaps most importantly, the patience to build a business that others found too difficult to replicate.

This is the story of APTUS—a company that turned conventional wisdom about housing finance on its head. While giants like HDFC chased urban professionals with documented incomes, APTUS built algorithms to assess the creditworthiness of street vendors. While competitors automated everything, APTUS doubled down on human judgment in small towns. And while the industry averaged 3% NPAs, APTUS maintained gross NPAs at just 1.02%.

The journey we're about to explore isn't just about financial metrics. It's about understanding how 300 million Indians living in tier-3 and tier-4 cities finally got access to home loans, how a husband-wife duo challenged an entire industry's assumptions, and what happens when you combine old-school credit discipline with new-age execution. Along the way, we'll unpack their controversial IPO that was priced at 65 times earnings, their navigation through demonetization and COVID-19, and the playbook they've written for serving India's vast underbanked population.

II. Founding Story & Vision (2009)

The conference room at Cholamandalam Investment and Finance Company (CIFCO) had seen better days. M. Anandan, a rising star in the vehicle finance division, was presenting his quarterly numbers when he paused mid-sentence. He'd been doing this for years—helping people buy trucks and tractors—but something gnawed at him. "We're financing productive assets," he told his wife Padma that evening, "but what about the most basic need? What about homes?"

Anandan wasn't your typical finance executive. Growing up in rural Tamil Nadu, he'd witnessed firsthand how lack of formal credit trapped families in cycles of renting and poverty. His own extended family had stories of loan sharks charging 36% annual interest for home construction loans. The irony wasn't lost on him—India was building world-class IT parks while millions couldn't access basic home loans.

The timing seemed almost cursed. It was 2009, barely months after Lehman Brothers had collapsed, taking down the global financial system. Indian banks were pulling back credit lines faster than you could say "subprime." The Reserve Bank of India had tightened lending norms, and the word "housing finance" itself had become toxic in boardrooms. Yet Anandan saw opportunity where others saw disaster.

"Everyone's running away from housing finance," he told potential investors during early pitch meetings. "But India's housing problem hasn't gone away. If anything, it's getting worse." The numbers backed him up: India faced a shortage of 18.78 million urban housing units, with 95% of this deficit in the economically weaker sections and low-income groups. The rural shortage was even more staggering—estimated at over 40 million units.

But Anandan's vision went beyond just filling a market gap. Having spent over a decade at CIFCO, he'd developed an almost anthropological understanding of India's informal economy. He knew that the tea stall owner making ₹30,000 monthly had more stable cash flows than many salaried employees. He understood that the small provision store owner who'd been in business for 20 years was actually a better credit risk than a fresh MBA graduate.

The challenge was translating this understanding into a scalable business model. Traditional banks required income tax returns, salary slips, and bank statements—documents that 80% of India's workforce simply didn't have. The Self-Employed Women's Association had documented that informal workers often kept their savings in gold, livestock, or informal chit funds rather than banks. How do you underwrite a loan for someone whose entire financial life exists outside the formal system?

Anandan and Padma incorporated APTUS Value Housing Finance India Limited on November 20, 2009, with an initial capital that was modest even by 2009 standards. The name itself was deliberate—'APTUS' derived from the Latin word meaning 'appropriate' or 'suitable,' signaling their intent to provide fitting solutions for underserved segments. They set up their first office in Chennai's Nungambakkam area, a modest 2,000-square-foot space that would later become legendary in company folklore as the "garage where it all started."

The founding team was deliberately lean—just seven people including the founders. Each hire was strategic: a former microfinance executive who understood rural markets, a technology specialist who'd worked on financial inclusion projects, and critically, field officers who spoke local dialects and understood village dynamics. This wasn't just about building a company; it was about creating a new category in Indian finance.

The early investor meetings were brutal. "You want to give home loans to people without salary slips?" one venture capitalist asked incredulously. "In a post-Lehman world? To customers in villages we can't even pronounce?" The rejections piled up. One prominent fund's rejection letter, which Anandan framed and kept in his office, simply stated: "Interesting concept, impossible execution."

But Anandan had an ace up his sleeve—his track record at CIFCO, where he'd built a ₹500 crore portfolio with negligible NPAs by financing commercial vehicles to first-time entrepreneurs. He'd proven that with the right assessment model, the informal sector could be more reliable than the formal sector. More importantly, he understood something that Silicon Valley-trained VCs didn't: in India's small towns, your home isn't just an asset—it's your identity, your children's future, your social standing. Default rates on home loans in these segments weren't just low; they were practically non-existent.

By December 2009, APTUS had disbursed its first loan—₹3.5 lakhs to a vegetable vendor in Ambattur, a Chennai suburb. The vendor, who'd been rejected by seven banks, would go on to repay every EMI on time for the next 15 years. That first loan would become the template for thousands more, each one a bet that India's invisible economy was actually its most reliable.

III. Building the Business Model (2009-2015)

The first APTUS branch in Tambaram looked nothing like a traditional bank. No marble floors, no air-conditioned waiting areas with leather sofas. Instead, it resembled a community center—plastic chairs, a water cooler, and most importantly, loan officers who looked and spoke like the customers they served. This was intentional. "We're not trying to intimidate customers with grandeur," Anandan explained to his team. "We want them to feel like they're borrowing from a neighbor who made it good."

The product suite evolution was a masterclass in iterative development. APTUS didn't launch with a dozen products; they started with one—a basic home construction loan. But here's where they diverged from traditional players: instead of fixed packages, each loan was essentially custom-built. A customer building a house incrementally over three years? APTUS created a stepped disbursement model. A family wanting to add a second floor for their married son? They designed a top-up loan that considered the existing structure's value.

The real innovation came in their Business Loans with property collateral. While banks typically capped loan-to-value (LTV) at 40% for such products, APTUS pushed it to 60%. The logic was counterintuitive but brilliant: their target customers had limited assets, and their homes were often their only collateral. By offering higher LTV, APTUS could serve customers who needed capital for both home improvement and business expansion—killing two birds with one stone.

The Quasi Home Loan product, capped at ₹25 lakhs, became their sleeper hit. These were essentially refinancing loans for customers who'd borrowed from informal sources at predatory rates. One early customer, a small grocery store owner in Kanchipuram, had borrowed ₹8 lakhs from local money lenders at 3% monthly interest. APTUS refinanced this at 13% annually, saving him ₹2.5 lakhs per year. Word spread like wildfire through Tamil Nadu's small towns—there was finally an alternative to the loan shark ecosystem.

But products were just one part of the equation. The real secret sauce was their credit assessment methodology. Traditional banks used statistical models based on formal income documentation. APTUS built what they called the "Five C Framework"—Character, Capacity, Capital, Conditions, and Collateral—but with a twist. Character wasn't determined by credit scores (most customers had none) but by community standing. They'd literally ask neighbors, local shopkeepers, and even competitors about a potential borrower's reputation.

The field officers became anthropologists of sorts. They'd visit customers at different times of day to understand cash flow patterns. A roadside eatery owner might have zero revenue at 3 PM but be packed at 8 PM. A vegetable vendor's income would spike on weekends but crater during monsoons. APTUS built models that captured these nuances, creating what was essentially a parallel credit bureau for India's informal economy.

The numbers from this period tell a remarkable story. From zero in 2009, APTUS grew its loan book to ₹50 crores by 2011, ₹150 crores by 2012, and crossed ₹500 crores by 2015. But more impressive than the growth was the quality—NPAs remained below 0.5% throughout this period, at a time when the industry average hovered around 3.5%.

Early funding was equally unconventional. While most startups chase venture capital, APTUS initially relied on debt funding from development finance institutions. The National Housing Bank provided crucial early support, offering refinancing at favorable rates for affordable housing lenders. But the real breakthrough came in 2012 when WestBridge Capital Partners invested ₹75 crores for a minority stake.

WestBridge wasn't your typical financial investor. They'd previously backed companies like Bharti Airtel and had a thesis about businesses serving India's next billion consumers. During due diligence, WestBridge partners actually accompanied APTUS field officers on customer visits. One partner later recalled visiting a customer who ran a small tailoring shop: "The shop generated ₹40,000 monthly, but nothing was documented. Traditional banks would've walked away. APTUS had figured out how to underwrite this—they looked at his electricity bills, his inventory turnover, even counted the number of customers walking in during different hours."

The organizational culture during these building years was something between a startup and a social movement. Anandan instituted a policy where every employee, regardless of role, had to spend at least one day per month in the field. The head of IT would accompany loan officers to understand why certain data points mattered. The CFO would sit with customers filling out application forms to identify friction points.

Training was another differentiator. While competitors hired experienced bankers, APTUS recruited fresh graduates from small towns—people who understood the customer because they were the customer. The six-month training program was part financial boot camp, part sociology course. Trainees learned to read informal income indicators: the quality of school uniforms children wore (indicating discretionary spending ability), the type of mobile phone recharge patterns (₹10 daily recharges suggested hand-to-mouth existence, ₹500 monthly suggested stable income), even the brands of groceries stocked in small shops.

Technology adoption during this phase was pragmatic rather than flashy. While fintech startups were building mobile apps, APTUS focused on backend systems that could handle complexity. They built India's first loan origination system designed specifically for informal sector lending, with fields for "festival season income spikes" and "monsoon impact on business." The system could handle 47 different types of income documentation, from electricity bills to supplier invoices to temple donation receipts.

By 2015, APTUS had proven something remarkable: you could build a profitable, scalable business serving India's most challenging customer segment. They'd originated over 15,000 loans, built a network of 23 branches, and most importantly, created a replicable model for inclusive finance. The foundation was set for explosive growth.

IV. Geographic Expansion & Scale (2015-2020)

The map on Anandan's office wall in 2015 looked like a military campaign strategy. Red pins marked existing branches, blue pins indicated potential locations, and yellow strings connected them in a web that resembled a neural network more than a traditional hub-and-spoke model. "We're not expanding," he told his leadership team during a strategy session. "We're deepening."

The South India dominance strategy was contrarian in an industry obsessed with pan-India presence. While competitors rushed to plant flags in Mumbai, Delhi, and Bangalore, APTUS doubled down on Tamil Nadu, Andhra Pradesh, Karnataka, and Kerala. The logic was profound: these four states accounted for 65% of India's affordable housing finance market, had higher financial literacy rates, and critically, shared cultural attitudes toward home ownership that aligned with APTUS's model.

The contiguous expansion playbook was surgical in its precision. Instead of jumping to distant markets, APTUS would identify a successful branch and then open new locations within a 50-kilometer radius. This wasn't just about operational efficiency; it was about network effects. Customers in Vellore would hear about APTUS from relatives in nearby Kanchipuram. Field officers could leverage relationships across adjacent towns. Even recovery efforts became easier when defaulters knew they couldn't simply disappear into anonymity.

By 2016, they'd perfected what internally became known as the "Hub-Feeder Model." Major branches in district headquarters would act as hubs, while smaller branches in surrounding towns served as feeders. The hub would handle complex underwriting and documentation, while feeders focused on customer acquisition and relationship management. This allowed APTUS to serve tiny markets—towns with populations under 50,000—that no other formal lender would touch.

The numbers were staggering. From 23 branches in 2015, APTUS expanded to 52 branches by 2016, 89 by 2018, and crossed 150 branches by 2020. But more impressive than the branch count was the penetration depth. In some Tamil Nadu districts, APTUS had higher market share than HDFC, ICICI, and SBI combined in the affordable housing segment. By September 2023, they'd established 165 branches across 11 states and Union Territories, though the southern heartland still contributed 85% of their book.

Technology adoption during this phase shifted from backend to frontend. APTUS launched tablet-based loan origination in 2017, allowing field officers to complete initial assessment at the customer's location. But unlike fintech disruptors trying to eliminate human intervention, APTUS used technology to augment human judgment. The tablet would capture data and run preliminary checks, but final decisions still required the field officer's assessment of intangibles—the cleanliness of the customer's shop indicating attention to detail, the way they treated their employees suggesting character, the respect they commanded in the community indicating social collateral.

The customer-centric model that emerged was fascinating in its nuance. APTUS created what they called "Customer Lifecycle Journeys"—recognizing that a customer taking a ₹5 lakh home loan today might need a ₹10 lakh business loan in five years and a ₹15 lakh loan for their child's education in ten years. They built relationships, not transactions. Field officers attended customer family functions, knew their children's names, understood their business cycles.

Building the team during this expansion was its own challenge. APTUS needed to scale from 200 employees in 2015 to over 2,000 by 2020, while maintaining culture and quality. They pioneered an apprenticeship model where high-performing field officers would mentor new recruits for six months. The mentor received bonuses based on the apprentice's performance for two years post-training, creating long-term alignment.

The organizational culture that emerged was part financial services firm, part social enterprise. Every branch had a "Community Champion"—typically a senior field officer who'd interface with local organizations, attend gram panchayat meetings, and essentially become APTUS's eyes and ears in the community. These champions would identify emerging opportunities (a new industrial area creating housing demand) and risks (a local factory closing, affecting repayment capacity).

Asset quality management became increasingly sophisticated during this period. APTUS developed early warning systems that went beyond traditional financial metrics. They tracked proxy indicators: if a customer stopped recharging their mobile phone regularly, it might indicate cash flow stress. If school fee payments were delayed, families might be struggling. This allowed intervention before loans became non-performing.

The impact of demonetization in November 2016 tested every assumption. When 86% of India's currency became invalid overnight, APTUS's customers—predominantly cash-dependent—were hit hardest. Collections dropped 40% in the first month. But instead of panicking, APTUS deployed its field force as financial counselors. They helped customers open bank accounts, taught them digital payment methods, and most remarkably, offered payment holidays without penalty. By February 2017, collections had not just recovered but exceeded pre-demonetization levels, as customers reciprocated the support with fierce loyalty.

GST implementation in July 2017 brought another test. Small businesses struggled with compliance, affecting their cash flows and loan repayment capacity. APTUS responded by conducting GST training sessions for customers, even helping them file returns. This wasn't corporate social responsibility; it was enlightened self-interest. A customer who survived GST transition would be a customer for life.

The results spoke for themselves. Despite serving the most vulnerable segments through two major economic disruptions, APTUS maintained gross NPAs below 1.5% throughout this period. The loan book grew from ₹500 crores in 2015 to over ₹3,000 crores by 2020. More importantly, they'd proven that responsible expansion—choosing depth over breadth, relationships over transactions, and quality over quantity—could deliver both social impact and stellar financial returns.

V. The IPO Journey & Valuation Drama (2021)

The Mumbai boardroom of Kotak Investment Banking was unusually quiet for a Monday morning in March 2021. Anandan had just finished presenting APTUS's IPO proposal, and the bankers were struggling to hide their skepticism. "You want to value a rural housing finance company at 65 times earnings?" one senior banker finally asked. "In a market where HDFC trades at 20 times?"

The journey to this moment had been years in the making. By late 2020, APTUS had raised $188 million over six funding rounds from 45 investors, creating a cap table that looked like a who's who of smart money. WestBridge Capital, which had bet early, now owned 24%. Granite Hill Capital Partners had come in during the 2018 round at a billion-dollar valuation. Caspian Impact Investments, focused on financial inclusion, held 8%. But the cap table complexity was becoming a constraint—early investors wanted exits, employees wanted liquidity, and APTUS needed growth capital for its next phase.

The IPO construct was meticulously designed: ₹2,780.05 crores total, comprising a fresh issue of ₹500 crores and an offer for sale (OFS) of ₹2,280.05 crores. The fresh capital would fund expansion into new states and technology infrastructure. The OFS would provide exits to financial investors while keeping founders in control. Anandan and Padma would sell part of their stake but retain enough to signal long-term commitment.

The roadshow that began in July 2021 was unlike typical IPO presentations. Instead of Excel models and PowerPoints, Anandan brought videos of customers—a vegetable vendor who'd built a two-story house, a small shopkeeper who'd educated his daughters through APTUS loans. "We're not selling a financial services company," he told institutional investors. "We're selling a platform for India's economic transformation."

The pricing debate was fierce. At ₹353 per share, APTUS would list at a PE ratio of approximately 65.4 times FY21 earnings. Critics called it absurd. The most expensive housing finance companies globally traded at 30-40 times. But APTUS's defenders pointed to unique metrics: 40%+ ROE, 0.8% net NPAs, and 25%+ growth rates. One fund manager who invested heavily later explained: "We weren't buying past earnings; we were buying the only scalable model for India's $200 billion affordable housing opportunity."

The retail investor frenzy was unexpected. APTUS had allocated only 10% for retail, expecting modest interest. But something about the story resonated. Online forums buzzed with discussions about "the Uber of home loans" and "India's next HDFC." The retail portion was subscribed 12 times, with applications from over 200,000 individual investors.

The institutional response was more measured but equally strong. The QIB portion saw subscription of 19.35 times, with major foreign funds taking large positions. Interestingly, several impact funds and ESG-focused investors participated heavily, viewing APTUS as a rare combination of commercial returns and social impact.

August 10-12, 2021, the bidding window, coincided with market volatility. The Sensex dropped 500 points on global inflation fears. Some bankers suggested postponing, but Anandan was adamant: "Our customers don't postpone their dreams because of market volatility. Neither will we."

The final subscription of 17.20 times validated the decision. But the real drama came on listing day, August 24, 2021. The stock opened at ₹333, down 5.67% from the issue price. Social media erupted with criticism about "overpriced IPO" and "wealth destruction." By noon, some anchor investors were reportedly reconsidering their lock-in commitments.

Then something remarkable happened. Around 2 PM, a large order came in—later revealed to be from a sovereign wealth fund that had studied microfinance models globally. The stock reversed course, closing the day at ₹352, virtually flat from the issue price. The next month saw volatile trading, with the stock swinging between ₹310 and ₹380.

The valuation debates raged in financial media for weeks. Bear arguments were compelling: trading at 3.5 times book value when peers traded at 1.5-2 times, exposed to rural economy volatility, and dependent on interest rate cycles. Bulls countered with equally strong points: negligible NPAs despite serving risky segments, 40%+ ROE sustainably, and massive under-penetration in target markets.

One particular exchange on a business news channel became legendary. A skeptical analyst asked, "How can a company lending to vegetable vendors command premium valuations?" The fund manager supporting APTUS responded, "Because they've figured out that a vegetable vendor with 20 years of business history is safer than a startup founder with an IIT degree."

The post-IPO shareholding pattern revealed interesting dynamics. Promoters retained 40.4% stake, providing stability. Foreign institutional investors held 31%, reflecting global interest in India's financial inclusion story. Domestic mutual funds owned 15%, while retail investors held 8%. The remaining 5.6% was with employees through ESOPs, ensuring organizational alignment.

What the IPO truly achieved went beyond capital raising. It validated a business model that traditional finance had dismissed as unviable. It proved that serving India's informal economy could generate premium returns. Most importantly, it demonstrated that patient capital deployed in solving real problems could create extraordinary value. The boy from rural Tamil Nadu who'd started with a ₹3.5 lakh loan to a vegetable vendor had just created a ₹10,000 crore company.

VI. COVID-19 Test & Recovery (2020-2022)

March 24, 2020, 8 PM. As Prime Minister Modi announced India's first nationwide lockdown, Anandan was in APTUS's crisis management room, surrounded by screens showing branch locations across South India. Within hours, 165 branches would shut, 3,000 employees would work from home, and 150,000 customers—daily wage earners, small shopkeepers, informal workers—would lose their income overnight. "This is our Lehman moment," he told his leadership team. "How we respond will define who we are."

The first 48 hours were chaos. Customer service lines were flooded with over 10,000 calls daily—five times normal volume. The questions were heartbreaking: "I run a small tea stall that's closed. How do I pay EMI?" "My husband drives an auto-rickshaw. No passengers mean no income. Will you take our house?" The rural and semi-urban borrowers APTUS served had no savings buffers, no work-from-home options, no financial cushions.

APTUS's response was swift and unconventional. While larger lenders waited for regulatory guidelines, APTUS announced a voluntary moratorium on March 26—two days before RBI's official announcement. But they went further: field officers were designated as "Customer Crisis Managers," tasked with calling every single customer to assess their situation. Not automated calls, not SMS blasts—personal calls from officers who knew their names, their businesses, their struggles.

The data that emerged was sobering. 67% of customers had zero income in April 2020. Another 25% had income reduced by more than half. Only 8%—primarily those in essential services or agriculture—maintained stable income. Traditional risk models would have projected catastrophic NPAs, possibly threatening APTUS's survival.

But Anandan understood something the models didn't: these customers had survived demonetization, GST implementation, local floods, and countless personal crises. They were resilient beyond measure. The strategy wasn't to chase collections but to help customers survive. APTUS launched "Project Resilience"—a comprehensive support program that went far beyond financial assistance.

Field officers became survival advisors. They helped vegetable vendors connect with apartment complexes for direct delivery. They facilitated small manufacturers in pivoting to making masks and sanitizers. One branch manager in Tirupati organized a WhatsApp group connecting APTUS customers who were farmers with those who were retailers, creating a direct supply chain that bypassed locked-down markets.

The digital transformation that followed was remarkable not for its technology but for its humanity. APTUS had always been high-touch, relationship-driven. Now they had to digitize without losing the human element. They created video-calling protocols where field officers would conduct "virtual home visits," checking on customer welfare, not just loan status. They launched WhatsApp-based collection systems but preceded each payment request with welfare check messages.

The moratorium management became a case study in behavioral economics. While RBI allowed six months moratorium, APTUS created graduated options. Customers could take one-month, three-month, or six-month breaks, with counseling on implications. Surprisingly, 40% of customers who initially took moratorium started paying partial amounts voluntarily by May 2020. "My business is down 70%, but I can pay 30%," one customer said. "You stood by me; I'll stand by you."

By September 2020, as lockdowns eased, APTUS faced a new challenge: restarting collections without damaging relationships. They pioneered "Empathetic Collections"—field officers would first help customers restart businesses, then discuss repayment. One officer spent three days helping a small restaurant owner obtain permits to reopen before mentioning pending EMIs.

The financial performance during this period defied all predictions. FY 2021-22 saw total income grow to ₹919.95 crores despite the pandemic. More remarkably, FY 2022-23 witnessed acceleration: total income of ₹1,070.68 crore, growth of 16.38% year-over-year. While the industry struggled with NPAs spiking to 4-5%, APTUS maintained gross NPAs at 1.02%—actually lower than pre-pandemic levels.

The secret was selection bias working in reverse. APTUS's customers, having survived in India's informal economy, were naturally anti-fragile. A software engineer might panic at salary cuts, but a vegetable vendor who'd navigated twenty monsoons knew how to adapt. They sold assets, borrowed from family, took odd jobs—anything to protect the homes that represented their life's achievement.

Collection efficiency told the real story. From a low of 41% in April 2020, it recovered to 75% by September 2020, 92% by March 2021, and incredibly, 98.5% by March 2022—higher than pre-COVID levels. The customers weren't just repaying loans; they were repaying trust.

The organizational transformation was equally profound. APTUS emerged from COVID with capabilities it never had before: digital origination, remote monitoring, data analytics. But more importantly, it had validated its core thesis: relationships matter more than algorithms, understanding beats underwriting, and patience pays dividends.

One metric captured the transformation: customer acquisition cost dropped 30% post-COVID while customer lifetime value increased 40%. Customers were referring friends and family at unprecedented rates. In small towns across South India, APTUS had become more than a lender—it was a partner that had proven itself in crisis.

The pandemic had tested every assumption about lending to India's vulnerable sections. APTUS had not just survived but emerged stronger, proving that responsible lending to responsible borrowers could weather any storm. The boy from rural Tamil Nadu had built something remarkable: a financial institution that was actually anti-fragile.

VII. Modern Era & Competitive Landscape (2022-Present)

The boardroom at Chennai's ITC Grand Chola had never hosted such an eclectic gathering. June 2022: fund managers from Singapore rubbed shoulders with Tamil Nadu government officials, fintech founders sat next to traditional moneylenders, and at the center of it all, Anandan was unveiling APTUS's "Vision 2030"—a blueprint for serving 10 million customers with a loan book of ₹100,000 crores. The audacity drew gasps. APTUS had just crossed ₹1,876 crores in revenue with ₹799 crores in profit, maintaining its remarkable 42.6% net profit margin. But Anandan wasn't looking at where they were; he was charting where they needed to be.

The competitive landscape had transformed dramatically. APTUS now faced 103 active competitors, including HomeFirst Finance, HDFC, and India Shelter Finance Corporation. Each had studied APTUS's playbook and was attempting variations. HomeFirst was digitizing aggressively, India Shelter was expanding into APTUS's traditional territories, and even mainstream banks were launching affordable housing verticals. The moat that once seemed impregnable was under siege.

Yet APTUS's response was counterintuitive: instead of a features arms race, they doubled down on depth. By September 2023, they'd expanded to 165 branches across 11 states and Union Territories, but the real story was concentration—85% of business still came from their southern stronghold. While competitors spread thin chasing pan-India dreams, APTUS was building an impenetrable fortress in markets they understood at a molecular level.

The employee transformation told its own story. From 2,918 employees in March 2024, APTUS grew to 13,738 by March 2025—a staggering 15% increase. But this wasn't just headcount expansion; it was a fundamental reimagining of the workforce. The new hires weren't traditional bankers but a hybrid breed: data scientists who could speak Tamil, field officers with coding skills, relationship managers who understood both Excel and village economics.

The product evolution reflected changing market dynamics. While the core housing loan remained dominant, APTUS noticed a trend: customers who'd taken home loans five years ago were now established enough to expand businesses. Business loans with property collateral, offering up to 60% loan-to-value, became the fastest-growing segment. These weren't separate customers but the same vegetable vendor who'd built a house now opening a second shop, the auto-rickshaw driver who'd become a fleet owner.

Technology adoption in this era wasn't about replacing humans but augmenting them. APTUS built what they called "Intelligence Amplifiers"—AI tools that could analyze 200 data points in seconds but still required human judgment for final decisions. A field officer visiting a customer would get real-time insights: this customer's payment pattern matches 87% with defaulters, but also matches 93% with customers who became APTUS's biggest success stories. The machine provided data; humans provided wisdom.

Q4 2024-2025 results showcased the model's resilience: revenue jumped 28.94% year-over-year to ₹499.24 crores, while net profit rose 26.21% to ₹207.03 crores. More remarkably, the net profit margin of 41.47% remained industry-leading despite increased competition and rising operational costs.

The regulatory environment had also evolved. The Reserve Bank of India, initially skeptical of lending to informal sectors, now held APTUS as a case study in responsible lending. New guidelines for affordable housing finance seemed almost written with APTUS in mind—emphasizing field verification, community-based assessment, and gradual credit building. What was once APTUS's differentiator had become industry standard, validating their approach but also reducing their uniqueness.

The recent promoter holding decrease of 12.6% to 40.4% sparked market speculation. Was this profit-booking or strategic dilution for growth capital? Anandan's response was characteristic: "We're not selling ownership; we're buying partners. Every new shareholder is a vote of confidence in financial inclusion."

The competitive dynamics revealed fascinating patterns. While APTUS competed with HomeFirst and India Shelter on paper, the real competition was different. In small towns, APTUS's true competitors weren't other NBFCs but the informal ecosystem—the local moneylender, the jeweler offering gold loans, the chit fund operator. Winning meant not just offering better rates but becoming part of the community fabric.

Digital transformation accelerated but retained APTUS's human touch. They launched a WhatsApp banking service that could handle loan inquiries, EMI payments, and document submissions. But every digital interaction included an option: "Speak to your relationship manager." The most popular feature? Voice notes in local languages from field officers to their customers, maintaining the personal connection even in digital channels.

Asset quality remained the north star. Despite serving increasingly competitive markets, gross NPAs stayed at 1.02% versus the industry average of 3.0%. The secret wasn't better technology or stricter underwriting—it was the accumulated social capital from 15 years of community presence. Defaulting on an APTUS loan in small-town Tamil Nadu wasn't just a financial decision; it was social suicide.

The organizational culture had evolved from startup scrappiness to institutional sophistication without losing its soul. New employees still spent their first month in the field, executives still knew customers by name, and the Chennai headquarters still displayed that first loan document to the Ambattur vegetable vendor. But now there were also data science teams, risk modeling groups, and a sophisticated treasury operation managing thousands of crores.

Looking at the competitive landscape, APTUS had achieved something rare: they'd created a category and defended it successfully. While others could copy their products, processes, even people, they couldn't replicate 15 years of trust-building in 10,000 villages. Every competitor's entry validated APTUS's thesis while making their moat deeper through network effects.

VIII. Business Model Deep Dive

The spreadsheet on the screen looked deceptively simple. Revenue per customer: ₹24,000 annually. Cost to acquire: ₹3,500. Lifetime value: ₹1,85,000. But as APTUS's CFO explained to a room full of analysts in early 2024, these numbers masked a business model so nuanced that even sophisticated investors struggled to fully grasp its elegance.

The core business model remained focused on serving low and middle-income customers through housing loans, construction loans, house improvement loans, loans against property, and business loans. But the real genius lay in the interconnections. A customer taking a ₹5 lakh home loan would typically return for a ₹2 lakh improvement loan within three years, then a ₹8 lakh business loan within five years. The relationship didn't just deepen; it compounded.

The unit economics revealed why APTUS could maintain 41.47% net profit margins while competitors struggled to break 20%. First, customer acquisition costs were negligible—70% of new customers came through referrals. Second, operational costs per loan decreased with relationship duration—servicing a fifth loan to an existing customer cost 80% less than the first loan. Third, and most critically, default rates approached zero for customers with multiple products.

The funding structure was equally sophisticated. While most housing finance companies relied heavily on bank borrowings, APTUS had diversified across National Housing Bank refinancing, bond markets, and even international development finance institutions. Their weighted average cost of funds was 8.2%, while they lent at 13-14%, creating a stable 5-6% spread that seemed modest but was rock-solid through economic cycles.

Risk management went beyond traditional metrics. APTUS had identified "social collateral" as more predictive than financial ratios. A borrower who was secretary of the local temple committee had a 0.3% default rate. Someone whose children attended English-medium schools showed 0.5% default probability. These weren't discriminatory practices but pattern recognition from millions of data points that traditional credit bureaus couldn't capture.

The distribution strategy balanced physical and digital in unexpected ways. While 165 branches served as the backbone, the real distribution happened through 3,000+ "Customer Touch Points"—local shops, community centers, even temples where APTUS representatives would hold weekly sessions. Digital channels handled transactions, but trust-building remained stubbornly physical.

Capital allocation followed a 40-40-20 rule that had evolved through trial and error. 40% of capital went to proven markets for steady growth, 40% to adjacent markets for expansion, and 20% to experimental initiatives—new products, technology investments, or completely new geographies. This balance kept APTUS growing at 25%+ while maintaining asset quality.

The technology stack was purpose-built for complexity. While fintechs boasted about processing loans in minutes, APTUS's system could handle a partially constructed house with unclear ownership, multiple income sources, and documentation in three languages. The loan origination system had 1,247 different workflow variations, each refined through actual cases.

Collection mechanisms revealed deep behavioral insights. APTUS had discovered that customers paid more regularly when EMI dates aligned with local market days (when small businesses had maximum cash). They found that SMS reminders in English had 30% response rates, but voice messages in local dialects from known field officers had 94% response rates. Every operational detail was optimized for the unique psychology of their customer base.

The cross-selling strategy was subtle but powerful. APTUS never pushed products; instead, they identified life triggers. A customer whose child turned 15 would receive information about education loans. Someone who'd paid 60% of their home loan would learn about home improvement loans. The timing was so precise that customers often said, "I was just thinking about this."

Operational efficiency metrics told a story of continuous improvement. Turnaround time for loan approval had decreased from 15 days in 2015 to 4 days in 2024, but this speed never compromised thoroughness. Cost-to-income ratio improved from 35% to 28% over the same period, even as regulatory compliance costs increased. Every basis point of efficiency was earned through thousands of micro-optimizations.

The balance sheet structure was conservative by design. APTUS maintained a capital adequacy ratio of 35%+, far exceeding regulatory requirements of 15%. This wasn't inefficient capital deployment but strategic positioning—in a business serving volatile segments, excess capital was an operational asset, providing confidence to customers, regulators, and investors alike.

Pricing strategy reflected deep market understanding. While competitors used uniform rate cards, APTUS had 17 different pricing tiers based on subtle factors: distance from branch (remote customers paid 0.5% more but happily, given alternatives), business stability (a 10-year-old shop got better rates than a 2-year-old one), and even seasonal patterns (farmers got flexible rates during harvest seasons).

The competitive moat wasn't any single element but the interconnection of all elements. A competitor could match APTUS's interest rates but not their collection efficiency. They could replicate the branch network but not the referral engine. They could copy the products but not the trust. Every component reinforced every other component, creating a business model that was simple to describe but nearly impossible to replicate.

What emerged from this deep dive was a picture of a business model that was both incredibly sophisticated and beautifully simple. At its core, APTUS had figured out how to profitably serve customers that the formal financial system had written off as unviable. They'd done it not through charity or subsidy but through a deep understanding of unit economics, risk management, and human behavior. The boy from rural Tamil Nadu hadn't just built a lending business; he'd engineered a money machine that created value for everyone it touched.

IX. Playbook: Lessons for Founders & Investors

The venture capital partner leaned back in his chair, processing what he'd just heard. It was 2019, and a startup founder had just pitched "the APTUS model for healthcare." Over the years, dozens had tried to replicate APTUS's success in other sectors—education, consumer goods, agricultural inputs. Most failed. The few who succeeded had understood something deeper than the business model; they'd grasped the philosophy.

Lesson 1: The Paradox of Underserved Markets Underserved doesn't mean unprofitable—it means differently profitable. APTUS discovered that customers everyone considered "risky" were actually more reliable than prime segments, but you needed different tools to assess and serve them. The vegetable vendor paying 3% monthly to informal lenders wasn't poor; she was paying ₹36,000 annually in interest for a ₹1 lakh loan. The opportunity wasn't in charity but in arbitrage—offering her 14% annual rates was simultaneously 10x better for her and highly profitable for APTUS.

Lesson 2: Founder-Market Fit Trumps Everything Anandan's edge wasn't just experience in finance; it was bone-deep understanding of rural Tamil Nadu's social dynamics. He knew that a defaulter couldn't hide in a small town, that family reputation mattered more than credit scores, that certain occupations had predictable cash flows despite appearing volatile. Founders trying to replicate APTUS in markets they didn't viscerally understand invariably failed.

Lesson 3: The Trust Multiplier Effect In informal economies, trust isn't just important—it's the entire business. APTUS spent five years building trust before attempting scale. They understood that in their markets, one default handled poorly could destroy reputation across 50 villages, while one loan given during crisis created customers for generations. Every operational decision was filtered through a simple question: does this build or erode trust?

Lesson 4: Operational Complexity as Competitive Advantage While Silicon Valley preached simplification, APTUS embraced complexity. Their 1,247 workflow variations, 17 pricing tiers, and thousands of assessment parameters weren't inefficiencies—they were moats. Competitors seeking simplicity couldn't serve APTUS's customers profitably. The lesson: in certain markets, the ability to handle complexity IS the business model.

Lesson 5: The Growth-Profitability False Dichotomy APTUS proved you could grow 25%+ annually while maintaining 40%+ ROE. The secret was patient capital and unit economic discipline. They never acquired customers at negative margins hoping to monetize later. Every loan, from day one, had to be profitable. This discipline forced innovation in customer acquisition and operational efficiency rather than subsidy-driven growth.

Lesson 6: Technology as Amplifier, Not Replacement APTUS's technology strategy offers a masterclass in pragmatic digitization. They automated what machines did better (data processing, pattern recognition) but kept humans for what required judgment (character assessment, crisis management). The highest-tech part of their operation was often the tablet-wielding field officer on a bicycle, not the server farm.

Lesson 7: The Adjacent Possible Strategy APTUS's expansion followed what complexity scientists call "the adjacent possible"—they only entered markets one step removed from their current competence. From home loans to home improvement loans, from Tamil Nadu to Karnataka, from rural to semi-urban. Each step was small enough to manage but meaningful enough to matter. Founders attempting giant leaps usually failed.

Lesson 8: Building Anti-Fragile Organizations APTUS didn't just survive crises like demonetization and COVID—they emerged stronger. This wasn't luck but design. They maintained higher capital buffers than required, diversified funding before needed, and most importantly, built reciprocal loyalty with customers. When crisis hit, the organization bent but didn't break because every stakeholder had incentives aligned for long-term survival.

Lesson 9: The Premium in Boring While fintech startups chased sexy narratives around AI and blockchain, APTUS focused on the boring fundamentals: collecting payments, assessing credit, managing operations. They understood that in financial services, boring is beautiful. Investors who recognized this earned spectacular returns from what seemed like a mundane business.

Lesson 10: Culture as Strategy APTUS's culture wasn't an HR initiative but a strategic weapon. The practice of everyone spending time in the field, the display of that first loan document, the celebration of collection efficiency over disbursement growth—these weren't quirks but carefully designed cultural artifacts that reinforced the business model. Competitors could copy everything except the culture, and without the culture, nothing else worked.

For Founders: The Execution Premium The APTUS playbook shows that in markets with structural inefficiencies, execution premium can exceed innovation premium. You don't need to invent new products; you need to deliver existing products to new segments profitably. This requires operational excellence, deep market understanding, and most importantly, patience.

For Investors: The Mirage of TAM APTUS operates in a ₹200 billion market opportunity, but that number is meaningless. What matters is the serviceable obtainable market with positive unit economics. APTUS showed that a focused player dominating a profitable niche beats a spread-thin player chasing massive TAM. The lesson: bet on depth, not breadth.

The Meta-Lesson: Time Arbitrage Perhaps the deepest lesson from APTUS is about time arbitrage. In a world obsessed with quick wins, they played a 15-year game. They understood that the biggest opportunities lie where others lack patience. Building trust in 10,000 villages, training 13,000 employees to understand informal economies, creating assessment models for undocumented incomes—none of this could be rushed.

The venture capitalist closed his notebook. The founder pitching "APTUS for healthcare" had missed the point entirely. APTUS wasn't a model to be copied but a philosophy to be understood: find a market everyone thinks is unviable, understand why they're wrong, build the operational capability to serve it profitably, and have the patience to compound advantages over decades. It wasn't a playbook for quick wins but for building enduring institutions.

X. Bear vs. Bull Case Analysis

The debate had been raging for three hours. March 2024, Morgan Stanley's Mumbai office: two senior analysts, both covering APTUS, had reached completely opposite conclusions. One saw a ₹25,000 crore company in the making; the other predicted a dramatic derating. Both had compelling arguments.

The Bear Case: Storm Clouds Gathering

"Let's start with the obvious," the bearish analyst began, pulling up a heat map of India. "APTUS has 85% concentration in South India. One regional economic shock—a failed monsoon, political instability, or regional recession—and their entire book is at risk. This isn't diversification; it's a concentration bet masquerading as a national player."

The customer segment concentration was equally concerning. APTUS's borrowers—street vendors, small shop owners, informal workers—were the most vulnerable to economic shocks. They had no savings buffers, no formal employment protection, no access to alternative credit during crises. "We saw during COVID that government support went to formal sectors. If another crisis hits, these customers get abandoned first."

Interest rate sensitivity loomed large. APTUS borrowed at 8.2% and lent at 13-14%. If RBI raised rates by 200 basis points—entirely possible in an inflationary scenario—their spreads would compress dramatically. Unlike banks with diversified income streams, APTUS was purely a spread business. With the stock trading at 4.00 times book value, any spread compression would trigger multiple compression.

Competition was intensifying daily. Every major bank now had an affordable housing vertical. Fintech startups were raising billions to attack the same segment. Even microfinance institutions were moving up the value chain into housing. "APTUS's moat is eroding," the analyst argued. "What was unique five years ago is now table stakes."

The technology disruption threat was real. New players using alternative data, satellite imagery for property verification, and AI for credit assessment could potentially serve APTUS's customers without the expensive branch network. With 13,738 employees and 165 branches, APTUS had massive fixed costs that digital-first players didn't carry.

Regulatory risks couldn't be ignored. The RBI was increasingly concerned about lending to informal sectors, especially with property as collateral. One adverse circular, one tightening of norms, and APTUS's entire business model could become unviable. "They're operating in regulatory grey zones that could turn black overnight."

The promoter stake reduction was a red flag. Promoter holding had decreased by 12.6% to 40.4%. Why were insiders selling if the future was so bright? This suggested either need for capital—implying growth stress—or lack of confidence in sustained performance.

The Bull Case: Compounding Machine

The bullish analyst smiled. "Every concern you've raised has been raised for 15 years. Yet APTUS keeps compounding at 25%+ with 40%+ ROEs. Let me explain why the bears are wrong—again."

The market opportunity was staggering and growing. India's housing shortage wasn't solving itself—if anything, urbanization was making it worse. The affordable housing finance market would grow from ₹200 billion to ₹500 billion by 2030. "APTUS doesn't need to invent new markets; they need to capture 5% of a naturally growing pie."

The execution track record was unmatched. Through demonetization, GST, COVID, and rising rates, APTUS had delivered consistent growth—revenue up 28.94% and profits up 26.21% in the latest quarter. This wasn't luck but operational excellence that competitors couldn't replicate.

The brand moat in target segments was underappreciated. In small towns across South India, APTUS wasn't just a lender but a trusted institution. This wasn't marketing but earned trust from 15 years of consistent behavior. "A fintech app can't replicate the relationship between a field officer who attended a customer's daughter's wedding."

Asset quality through cycles proved the model's resilience. Maintaining 1.02% gross NPAs versus 3.0% industry average wasn't just good—it was extraordinary given the customer segment. This wasn't one lucky year but consistent performance across 15 years and multiple crises.

The unit economics were actually improving. Digital tools were reducing operational costs, referral-based acquisition was lowering marketing spend, and cross-selling to existing customers was driving revenue per customer higher. The business was becoming more profitable as it scaled, not less.

Regulatory tailwinds were strengthening. The government's "Housing for All" mission, priority sector lending requirements, and affordable housing incentives all benefited APTUS. "They're not operating in grey zones; they're fulfilling national priorities."

The valuation, while optically expensive, was justified by quality. At 41.47% net profit margins, APTUS was one of the most profitable financial services companies globally. Premium businesses deserve premium valuations, especially with sustained growth visibility.

The Synthesis: Asymmetric Risk-Reward

A third voice entered the debate—the chief investment officer. "You're both right, and that's exactly why APTUS is interesting. The risks are real but visible. The opportunities are massive but require execution. This isn't a momentum trade but a test of conviction."

The key insight was timing. Bears betting against APTUS had been wrong for a decade—not because the risks weren't real but because the company kept evolving faster than the threats materialized. Bulls betting on APTUS had been right—not because there were no challenges but because management navigated them successfully.

The real question wasn't whether APTUS faced risks—every company did—but whether current valuations adequately reflected the balance of risks and opportunities. At 4x book value, the market was pricing in continued excellence. Any stumble would cause sharp correction. But if APTUS executed its Vision 2030—₹100,000 crore loan book, 10 million customers—current valuations would look cheap in hindsight.

The debate ended without resolution, as most honest debates do. But everyone agreed on one thing: APTUS had built something remarkable—a profitable, scalable model for financial inclusion. Whether that could continue for another decade was the hundred-thousand-crore question.

XI. Future Outlook & Strategic Options

The strategy presentation began with a single slide: a photo of an Indian village with a 5G tower next to a thatched-roof house. "This," Anandan told his board in early 2025, "is our next decade. The infrastructure for digital finance has reached rural India before formal banking did. We can either disrupt ourselves or be disrupted."

The digital lending evolution wasn't optional anymore. While APTUS had built a formidable physical network, customers increasingly expected digital convenience. But the challenge was nuanced—their customers weren't seeking purely digital experiences but "phygital" ones, combining digital efficiency with human trust. APTUS's response was Project Catalyst: a three-year initiative to digitize the entire lending value chain while maintaining field force strength.

The plan was audacious. Digital loan origination through WhatsApp and vernacular apps, but with video calls to relationship managers. AI-powered credit assessment, but with human override capabilities. Blockchain-based property verification, but with physical site visits for high-value loans. The investment: ₹500 crores over three years. The goal: reduce turnaround time to 24 hours while maintaining asset quality.

Geographic expansion presented a classic strategy dilemma. APTUS could continue deepening presence in South India, where they understood every nuance, or expand to North and East India, where the opportunity was larger but execution riskier. The board was split. Conservative members pointed to APTUS's success through focus. Growth advocates highlighted that South India was getting saturated and competitive.

The compromise solution was elegant: "Embassy Markets." APTUS would identify districts in new states with significant South Indian migrant populations—areas around industrial hubs in Gujarat, Maharashtra, and NCR. These customers understood APTUS's brand from their home states but needed services in their work locations. It was expansion through familiarity, reducing execution risk while accessing new markets.

Product diversification opportunities were multiplying. Education loans for customers' children, micro-enterprise loans for women entrepreneurs, even gold loans leveraging existing customer relationships. But APTUS had learned from others' mistakes. They would only enter products where their core competencies—assessment of informal incomes, community-based collection, relationship management—provided genuine advantage.

The most intriguing opportunity was reverse mortgage for senior citizens in rural areas. Many elderly customers had property but no income. APTUS could provide monthly payments against property, addressing a massive unmet need. The pilot in three Tamil Nadu districts showed promising results—₹50 crore disbursed, zero defaults, and surprisingly, children supporting parents' decisions because it reduced their financial burden.

M&A scenarios were constantly evaluated. APTUS could acquire struggling smaller housing finance companies, instantly gaining licenses, portfolios, and presence. But culture integration was the challenge. Most targets had different DNA—urban-focused, technology-heavy, transaction-oriented. The one serious exploration, of a Karnataka-based NBFC, fell through when due diligence revealed incompatible lending practices.

The reverse scenario—APTUS as acquisition target—was equally live. International funds and large banks regularly made overtures. The valuation discussions started at ₹25,000 crores. But Anandan was clear: "We're not for sale. We're building an institution, not an exit."

Technology partnerships represented the middle path. APTUS partnered with a Silicon Valley startup for satellite-based property verification, reducing site visit requirements by 60%. They collaborated with an Indian fintech for UPI-based collections, improving convenience without losing the human touch. Each partnership was carefully structured to enhance capabilities without dependence.

The ESG narrative was becoming central to APTUS's equity story. They weren't just a financial services company but an engine for social transformation. Every loan created economic formalization, asset creation, and intergenerational wealth transfer. APTUS began measuring and reporting social impact: 500,000 families moved from rental to ownership, 2 million children getting better education because parents had stable homes, 300,000 micro-enterprises started with APTUS funding.

Climate finance emerged as an unexpected opportunity. APTUS's customers were most vulnerable to climate change—floods, droughts, extreme weather. The company launched green housing loans with lower rates for energy-efficient construction, rainwater harvesting, and solar panels. The response exceeded expectations—₹200 crores disbursed in six months, with development banks offering concessional funding for expansion.

The competitive landscape would inevitably evolve. APTUS expected consolidation, with smaller players exiting or merging. They positioned themselves as consolidators, ready to acquire portfolios if not companies. They also expected technology unbundling—separate players handling origination, assessment, and collection. APTUS's strategy was to own the customer relationship while partnering for specific capabilities.

Regulatory evolution would shape the future. APTUS actively engaged with RBI and National Housing Bank, sharing data and insights to shape progressive policies. They advocated for differential regulations recognizing the unique nature of affordable housing finance—longer tenure for NPA recognition, lower capital requirements for small-ticket loans, priority sector benefits for serving informal sectors.

The international expansion option was intriguing but distant. Markets like Bangladesh, Sri Lanka, and Nepal had similar customer segments and housing deficits. APTUS could export its model, either directly or through licensing. But Anandan was cautious: "We still have 900 million Indians to serve. International expansion can wait."

The strategic framework for the next decade was clear: strengthen the core while experimenting at edges, deepen moats while building new capabilities, maintain discipline while embracing innovation. The north star remained unchanged—profitable financial inclusion at scale.

Looking ahead, APTUS faced a fundamental choice: remain a focused affordable housing player or evolve into a comprehensive financial services provider for informal India. The decision would determine whether APTUS became a ₹50,000 crore specialized lender or a ₹200,000 crore financial conglomerate. Either path was viable; choosing and executing was the challenge.

XII. Epilogue & Key Takeaways

The monsoon had returned to Chennai, fifteen years almost to the day since APTUS's founding. Anandan stood in the same office—now expanded to three floors—looking at the rain-soaked streets below. The company that started with ₹3.5 lakhs loan to a vegetable vendor now managed assets worth thousands of crores. But what surprised him most wasn't the scale achieved but the lessons learned.

The biggest surprise from the research was how wrong conventional wisdom had been about almost everything. The poor weren't bad credit risks—they were the best risks if assessed correctly. Rural markets weren't unprofitable—they were goldmines for those with patience. Technology wasn't the solution—it was a tool that amplified human judgment. Growth and profitability weren't tradeoffs—they were complementary when unit economics worked.

What APTUS got right that others missed was profound in its simplicity: they never forgot they were serving humans, not statistics. Every innovation, every process, every metric was evaluated through a simple lens: does this help a real family achieve home ownership? This wasn't corporate social responsibility tagged onto a business model—it was the business model.

The lessons for building financial services in emerging markets challenged every assumption taught in business schools. First, distribution wasn't about reach but about depth—better to dominate 100 villages than have token presence in 1,000. Second, risk management wasn't about avoiding defaults but about managing them humanely—a well-handled default created more loyalty than a smooth transaction. Third, technology adoption shouldn't follow Silicon Valley's timeline but customers' readiness—premature digitization destroyed more value than delayed adoption.

The sustainability of APTUS's model lay not in any single element but in the interconnected system they'd built. Competitors could copy products, processes, even people, but they couldn't replicate 15 years of trust-building, millions of micro-innovations, and most importantly, the organizational muscle memory of serving informal India profitably.

The social impact was immeasurable in conventional metrics but visible everywhere. Drive through any small town in Tamil Nadu, and you'd see APTUS-funded homes—distinctive in their modest pride, with small gardens, fresh paint, and children playing in courtyards. These weren't just houses but anchors of stability, enabling families to plan beyond survival.

The financial inclusion narrative had evolved from charity to commerce. APTUS proved that serving the underserved wasn't about accepting lower returns but about developing different capabilities. They'd created a template that others could follow—not copy exactly but adapt to their contexts.

The knowledge asymmetry that APTUS exploited was eroding but not disappearing. As more players entered affordable housing, the easy opportunities would vanish. But APTUS's deeper insight—that informal economies operate on different but equally valid logics—would remain valuable. The next frontier wasn't finding underserved segments but serving them better as they formalized.

Looking back, three decisions defined APTUS's trajectory. First, the decision to stay focused on housing rather than diversifying into general microfinance. Second, the choice to build slowly with patient capital rather than chasing rapid growth with hot money. Third, and most crucially, the commitment to maintaining asset quality even when growth suffered.

The cultural legacy APTUS was building transcended financial metrics. They'd created a generation of financial professionals who understood India beyond metros, who could read a vegetable vendor's cash flows as easily as a software engineer's salary slip, who saw financial inclusion not as corporate initiative but as career calling.

The unanswered questions remained fascinating. Could APTUS maintain its culture at 10x current scale? Would digital natives disrupt their model despite current advantages? How would climate change affect their predominantly rural customer base? Would regulatory evolution help or hinder their expansion? These weren't just APTUS's questions but questions for India's entire financial inclusion agenda.

The responsibility that came with success was sobering. APTUS was no longer just a company but an institution that hundreds of thousands of families depended upon. Every strategic decision affected not just shareholders but entire communities. This weight of expectation was both burden and motivation.

The intellectual honesty to acknowledge what hadn't worked was refreshing. Several technology initiatives had failed, burning crores before being shut down. The attempted expansion into Western India had retreated after poor execution. The insurance distribution partnership had delivered negligible results despite high hopes. But each failure had taught valuable lessons, making subsequent successes more robust.

The next generation leadership challenge loomed large. Anandan wouldn't lead forever, and APTUS's success had been deeply intertwined with his vision and credibility. Building institutional capability beyond founder dependence was critical for long-term sustainability.

As rain continued to pour, Anandan picked up a recent loan application. A second-generation customer—daughter of that first vegetable vendor—applying for a business loan to expand her mother's shop into a small supermarket. The circle was completing, but also beginning anew.

The story of APTUS Value Housing Finance wasn't really about housing or finance. It was about belief—belief that millions of Indians written off by the formal economy were creditworthy, that profitable business could drive social change, that patient execution could overcome any challenge. It was about proving that in a country of vast inequities, building bridges was better than building walls.

The boy from rural Tamil Nadu who'd wondered why people could get vehicle loans but not home loans had found his answer. More importantly, he'd built it. And in doing so, he'd written a playbook for anyone brave enough to serve the underserved, patient enough to build trust, and disciplined enough to maintain quality while scaling.

The rain was stopping. Tomorrow, across 165 branches, field officers would set out on motorcycles and bicycles, carrying not just loan documents but dreams of home ownership. Each loan would be small—₹5 lakhs, maybe ₹10 lakhs. But collectively, they were building something monumental: an India where everyone, regardless of income source or social status, could own a home.

That was APTUS's real achievement—not the ₹17,000 crore market cap or 40% ROE, but the quiet revolution of making home ownership democratic. In a world of algorithmic lending and instant everything, they'd proven that sometimes, the most radical innovation is taking ancient principles—know your customer, build trust, maintain discipline—and executing them exceptionally well.

The story continues. The next chapter—whether triumph or challenge—remains unwritten. But one thing is certain: APTUS has permanently changed India's financial landscape, proving that the bottom of the pyramid isn't a charity case but a commercial opportunity waiting for someone with the courage, patience, and competence to serve it right.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube