Indian Bank: The Swadeshi Movement's Banking Legacy

I. Introduction & Episode Roadmap

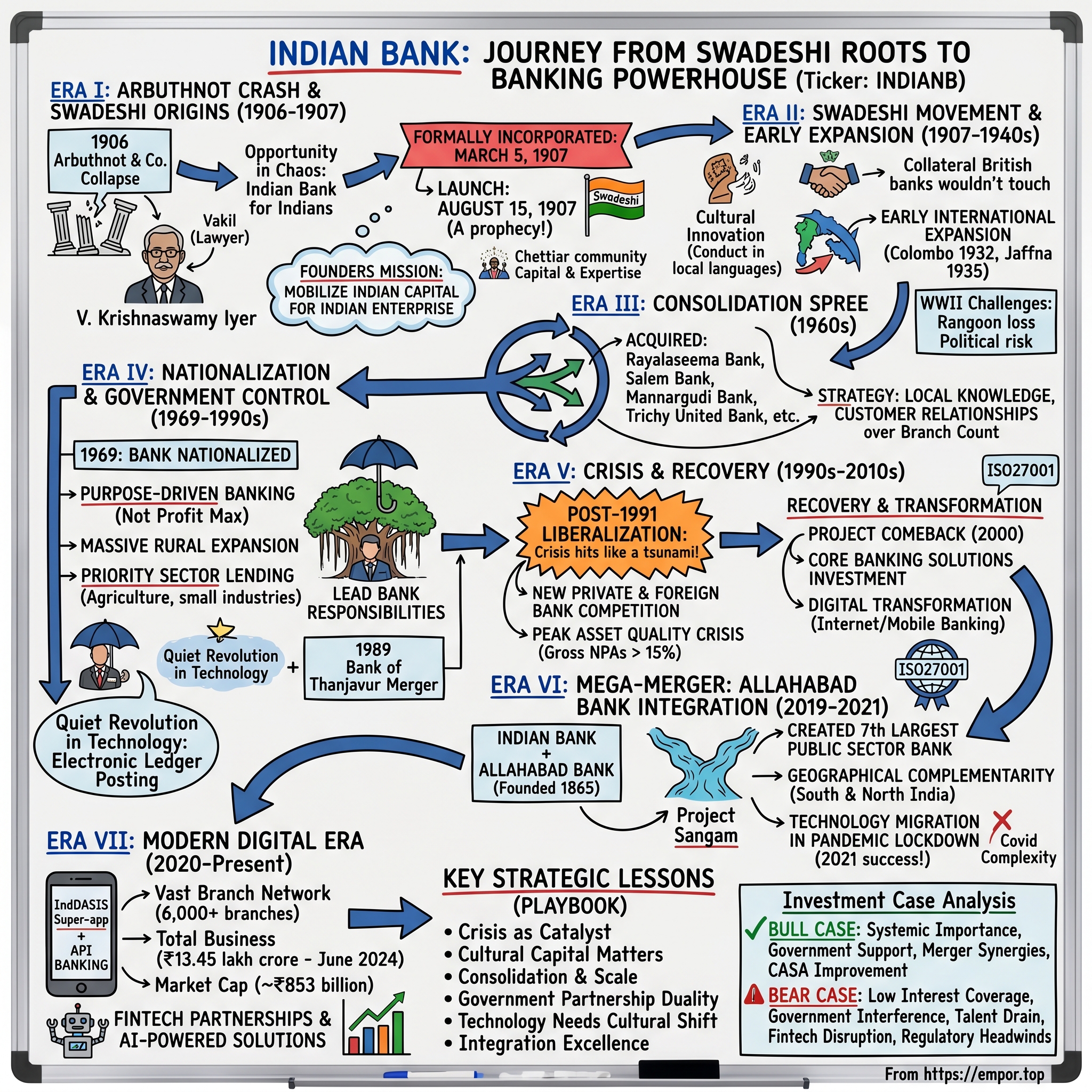

The year is 1906. Madras—now Chennai—is in chaos. Arbuthnot & Co., the crown jewel of British commerce in South India, has just collapsed, taking with it the savings of thousands and shaking faith in the entire financial system. In the wreckage stands a young lawyer named V. Krishnaswamy Iyer, surveying the damage as he handles the bankruptcy proceedings. What he sees isn't just financial ruin—it's an opportunity. An opportunity to build something that India desperately needs: its own bank, run by Indians, for Indians.

This is the origin story of Indian Bank, a financial institution that would grow from those ashes to become, 117 years later, the seventh-largest public sector bank in India. Today, with its distinctive blue and white logo adorning over 6,000 branches, Indian Bank serves more than 100 million customers and employs nearly 41,000 people. Its market capitalization hovers around ₹853 billion, making it a heavyweight in India's banking sector.

But this isn't just another banking success story. This is a tale of how nationalism became capitalism, how a movement for independence created a financial institution, and how that institution survived colonialism, navigated nationalization, weathered liberalization, and engineered one of India's most ambitious bank mergers—all while staying true to its founding mission of financial inclusion.

The central question we'll explore: How did a bank born from India's independence movement transform into a modern banking powerhouse while maintaining its soul? The answer involves equal parts idealism and pragmatism, tradition and innovation, government mandate and market competition.

Our journey will take us through four distinct eras: the Swadeshi origins when banking was an act of rebellion, the nationalization period when the bank became an instrument of state policy, the liberalization years when it had to compete or die, and finally, the mega-merger transformation that created today's banking behemoth. Each era demanded different skills, different strategies, and different sacrifices.

What makes Indian Bank particularly fascinating is how it has consistently turned crisis into catalyst. Born from the Arbuthnot collapse, strengthened through strategic acquisitions, tested by nationalization, and ultimately transformed through its merger with the 155-year-old Allahabad Bank during a global pandemic. This is institutional resilience at its finest.

So what for investors? Understanding Indian Bank's journey provides crucial context for evaluating its current position. The bank's history reveals deep competitive moats—government backing, cultural capital from its Swadeshi heritage, and hard-won expertise in navigating India's complex regulatory landscape. But it also exposes structural challenges that persist today: the tension between commercial objectives and social mandates, the burden of legacy systems, and the constant pressure to balance profitability with financial inclusion.

As we dive into this epic story, remember that Indian Bank isn't just a financial institution—it's a mirror reflecting India's economic evolution. From colonial exploitation to digital revolution, from villages without electricity to UPI transactions worth trillions, Indian Bank has been there, adapting, surviving, and occasionally thriving. Let's begin where it all started: in the ruins of a British banking house, where an idea was about to be born.

II. The Arbuthnot Crash & Birth from Crisis (1906-1907)

October 22, 1906. First Line Beach, Madras. A handwritten notice appears on the imposing gates of Arbuthnot & Co.: "Suspended payment till further notice." Within hours, thousands of depositors—rajas, zamindars, temple trusts, widows, pensioners—descend upon the building in panic. Police turn them away as alarmed investors besiege the gates. The unthinkable has happened: the firm that employed between 11,000 and 12,000 people, had 7,000 creditors and £1,000,000 in liabilities has collapsed overnight.

This wasn't just another bank failure. Arbuthnot had the reputation of paying a steady and unwavering interest of 5% on deposits, and enjoyed a clientele that comprised several of the Indian nobility, prominent Indian lawyers and other professionals, and a vast number of the middle class in South India. The firm's senior partner, Sir George Arbuthnot, was a pillar of Madras society, having served as Member of the Legislative Council besides having been Chairman of the Madras Chamber of Commerce several times and also President of the Board of Directors of the Bank of Madras. In colonial Madras, he was second only to the Governor in social standing.

The trigger for this catastrophe came from London. Patrick Macfadyen, who held an unenviable record of being an inveterate speculator, had gambled on the stock exchange requiring larger and larger sums of money being transferred to the London firm from Arbuthnot & Co., Madras. On the morning of October 21st, having asked his office to suspend payments, Macfadyen walked into the electric train tunnel near Old Street, London, throwing himself before a speeding train.

Into this maelstrom stepped V. Krishnaswamy Iyer, a young vakil (lawyer) who would transform personal tragedy into national opportunity. The depositors approached eminent lawyer V. Krishnaswami Iyer who fought Arbuthnot Bank on their behalf and obtained compensation for them. Krishnaswami became known when he was the contending advocate in the Arbuthnot bank case, playing a role in ensuring that the principal partner was imprisoned. Indeed, Arbuthnot was tried for the fraudulent activities the collapse revealed, and received a sentence of "18 months rigorous imprisonment".

But Krishnaswamy saw something larger in this crisis. The Arbuthnot collapse wasn't just financial fraud—it was symbolic of colonial exploitation. The most significant thing to come out of the scandal was the Indian response to the feeling that "European integrity and honesty (have come) under a cloud". It was a response led by V. Krishnaswamy Iyer, who got together eight prominent citizens of Madras and together they resolved "that a bank which depended on the savings of those in the South had to be incorporated locally and managed by Indians who were locally known and respected"

The idea crystallized quickly. On March 5, 1907, just five months after the Arbuthnot collapse, Indian Bank was formally incorporated. The founding group represented a cross-section of Madras society's progressive elite: lawyers, merchants, landowners, and crucially, members of the powerful Nagarathar Chettiar community. Ramasamy Chettiar, who became one of the first directors, brought not just capital but centuries of indigenous banking expertise. The Chettiars had been financing trade across Southeast Asia for generations, operating sophisticated hundis (indigenous credit instruments) networks that British banks couldn't penetrate.

The symbolism of the launch date—August 15, 1907—cannot be overstated. Forty years before India's independence, Indian Bank commenced operations on what would become the nation's Independence Day. This wasn't coincidence; it was prophecy. The bank's founders saw themselves as economic freedom fighters, building the financial infrastructure for a free India that existed only in their imagination. The bank started with a modest initial capital of ₹1 lakh, a seemingly small sum that represented enormous symbolic value. Every rupee raised was a vote for economic self-determination. The prospectus made the mission explicit: to mobilize Indian capital for Indian enterprise, breaking the stranglehold of European banks that extracted wealth from India while denying credit to Indian businesses.

The initial reception exceeded expectations. Within months, the bank had garnered deposits from temple trusts, merchant guilds, and thousands of small savers who saw banking with Indian Bank as a patriotic duty. In 1915, Annamalai Chettiar was inducted into the board, bringing additional Chettiar capital and expanding the bank's reach into Southeast Asian trade networks.

III. Swadeshi Movement & Early Expansion (1907-1940s)

Indian Bank was established as part of the Swadeshi movement to promote indigenous industries, but translating nationalist fervor into banking success required shrewd strategy. The early directors understood that survival meant walking a tightrope—radical enough to attract Indian depositors, conservative enough to maintain British regulatory approval.

The bank's first innovation was cultural: conducting business in Tamil and Telugu alongside English, employing local staff who understood indigenous business practices, and accepting forms of collateral that British banks wouldn't touch—agricultural land, jewelry, and promissory notes backed by community reputation rather than formal documentation.

With its head office in Parry's Building, Parry Corner, Madras, Indian Bank occupied prime commercial real estate, signaling its ambitions. The location was strategic—at the heart of Madras's business district, visible to both Indian merchants and British administrators, a daily reminder that Indians could run sophisticated financial institutions.

International expansion came surprisingly early. The bank opened its Colombo branch in 1932, recognizing that Tamil merchants and laborers in Ceylon needed banking services that understood their unique position—neither fully Sri Lankan nor Indian, but crucial to both economies. The Jaffna branch followed in 1935, and by 1940, Indian Bank had established itself in Rangoon, following the trail of South Indian migration and trade.

These weren't vanity projects. Each international branch tapped into existing networks of Indian traders, plantation workers, and money lenders who had been operating informally for decades. Indian Bank formalized these relationships, offering letters of credit for trade, remittance services for workers, and investment opportunities for successful merchants looking to diversify beyond traditional lending.

World War II brought unexpected challenges. The Japanese advance into Burma forced the closure of the Rangoon branch, with staff evacuating alongside thousands of Indian refugees in what became one of the war's forgotten humanitarian disasters. The Ceylon branches faced restrictions as colonial authorities tightened control over financial flows. Yet the bank survived, partly because its domestic operations benefited from wartime inflation and increased government spending.

The immediate post-independence period saw a cautious reopening of international operations. The Ceylon branches resumed full operations, though political tensions between India and Ceylon would periodically complicate matters. The Rangoon branch, however, was lost permanently as Burma's military government nationalized foreign banks. It was an early lesson in political risk that would shape Indian Bank's international strategy for decades.

By the late 1940s, Indian Bank had established a distinctive identity: conservative in its lending practices, innovative in its service delivery, and deeply embedded in South Indian commercial networks. With 38 branches and a growing deposit base, it had survived its first four decades through war, depression, and political upheaval. But the real test was coming.

IV. The Acquisition Spree & Growth (1960s)

The 1960s marked Indian Bank's first major growth phase through consolidation. In 1962, the bank acquired the Rayalaseema Bank, the Bank of Alagapuri, the Salem Bank, the Mannargudi Bank and the Trichy United Bank. These weren't random targets—each acquisition followed a strategic logic that would define Indian Bank's expansion philosophy.

Rayalaseema Bank brought access to the prosperous Krishna and Godavari delta regions of Andhra Pradesh. Bank of Alagapuri provided entry into textile towns of Tamil Nadu. Salem Bank offered agricultural financing expertise. Mannargudi Bank came with deep roots in the Thanjavur district, the rice bowl of Tamil Nadu. Trichy United Bank controlled strategic branches in the Kaveri basin.

What's remarkable is the efficiency of these acquisitions. All acquisitions added only 38 branches, bringing the total to 210 branches by 1967. This wasn't about branch count—it was about acquiring local knowledge, customer relationships, and most importantly, trained staff who understood regional nuances. Each absorbed bank brought specialists: Rayalaseema's expertise in financing rice mills, Salem Bank's knowledge of handloom cooperatives, Mannargudi's relationships with temple trusts.

The integration process pioneered techniques that would become standard in Indian banking. Rather than imposing uniform practices, Indian Bank allowed acquired branches to maintain certain local customs while standardizing back-office operations. Account numbering systems were unified, but relationship managers stayed in place. Lending committees were restructured, but local credit evaluation practices were preserved where they proved effective.

Competition during this period came from three directions. Foreign banks like Chartered Bank and Grindlays dominated corporate banking and trade finance. Other Indian banks, particularly Bank of India and Central Bank of India, competed for the growing middle-class market. And informal lenders—the very moneylenders Indian Bank was founded to displace—still controlled rural credit.

Indian Bank's response was segmentation before the term became fashionable. For large corporates, it offered consortium lending partnerships with foreign banks. For small businesses, it provided working capital loans with simplified documentation. For farmers, it introduced crop loans with flexible repayment schedules tied to harvest cycles. For urban salary earners, it launched systematic investment plans—precursors to today's recurring deposits.

By 1969, Indian Bank had grown into a formidable regional powerhouse with national ambitions. Its deposit base had crossed ₹100 crore, loan book exceeded ₹75 crore, and it employed over 3,000 people. The bank had weathered the 1962 war with China, the 1965 war with Pakistan, and the 1966 devaluation of the rupee. Management was confident, shareholders were satisfied, and expansion plans were ambitious.

Then, on July 19, 1969, Prime Minister Indira Gandhi appeared on All India Radio with an announcement that would change everything.

V. Nationalization & Government Control (1969-1990s)

In 1969, the bank was nationalized. It was appointed as the lead bank for nine districts in the States of Tamil Nadu, Andhra Pradesh and Kerala and the Union Territory of Pondicherry. The nationalization of Indian Bank, along with 13 other major commercial banks, represented both fulfillment and irony. The bank born from the Swadeshi movement to assert Indian control over Indian finance was now being taken over by the Indian government itself.

The immediate impact was transformational. Overnight, Indian Bank's mission shifted from profit maximization to developmental banking. The government's directive was clear: take banking to the masses. Priority sector lending targets were introduced—40% of credit had to flow to agriculture, small-scale industries, and other priority sectors. Rural branch expansion became mandatory—for every urban branch opened, four had to be established in unbanked rural areas.

This wasn't the genteel banking of Parry's Corner. Indian Bank's officers found themselves posted to villages without electricity, roads, or telephone connections. They learned to evaluate loan applications by candlelight, traveled to weekly markets on bullock carts, and conducted business under banyan trees. The cultural shock was immense—urbane, English-speaking bankers suddenly needed to understand crop cycles, cattle diseases, and village politics.

Yet Indian Bank adapted with remarkable ingenuity. It recruited local youth as banking correspondents, trained village accountants in basic banking, and pioneered mobile banking units—modified vans that brought banking to remote areas on market days. The bank developed vernacular banking materials, simplified forms for illiterate customers, and introduced thumbprint authentication decades before biometric technology made it fashionable. Technology adoption became another arena for quiet revolution. While the widely reported claim that Indian Bank introduced the first Automatic Teller Machine (ATM) in India in 1980 appears to be contested—HSBC opened the first ATM in India in Mumbai in 1987—Indian Bank was nonetheless among the early pioneers in banking technology. The bank embraced computerization in the early 1980s, introducing electronic ledger posting systems that dramatically reduced transaction processing time.

The lead bank responsibilities brought both opportunities and burdens. As lead bank for nine districts across Tamil Nadu, Andhra Pradesh, Kerala, and Pondicherry, Indian Bank coordinated credit planning, monitored priority sector lending, and convened quarterly meetings of all banks operating in these districts. This role positioned the bank as a crucial intermediary between government policy and ground-level implementation.

The 1970s and 1980s also saw Indian Bank develop specialized expertise in sectors that would become its competitive advantages. In Tamil Nadu's textile belt, the bank financed power loom cooperatives. In Kerala's spice gardens, it pioneered crop insurance-linked loans. In Andhra Pradesh's rice mills, it introduced warehouse receipt financing. Each innovation addressed specific local needs while building the bank's institutional knowledge.

Staff development during this period was transformational. The bank established training colleges in Chennai and Bangalore, sending thousands of officers through courses on rural lending, cooperative banking, and development economics. A generation of bankers learned to see themselves not just as financial intermediaries but as agents of social change. The culture shift was profound—from profit-focused to purpose-driven banking.

Yet tensions simmered. The aggressive rural expansion strained resources. Non-performing assets began accumulating as political pressures led to loan waivers and directed lending. Urban branches, which generated most profits, subsidized loss-making rural operations. Private sector employees, paid market rates, earned multiples of what equally qualified public sector bankers made. Brain drain became a persistent challenge.

The 1989 merger with Bank of Thanjavur, bringing 157 additional branches, demonstrated both the opportunities and challenges of this era. Bank of Thanjavur's rural network complemented Indian Bank's urban strength, but integrating two distinct organizational cultures proved complex. Different accounting systems, incompatible technology platforms, and varying credit evaluation standards created operational headaches that took years to resolve.

By the early 1990s, Indian Bank had grown into a massive institution—over 2,000 branches, 30,000 employees, deposits exceeding ₹5,000 crore. It had fulfilled the nationalization mandate of taking banking to the masses. But storm clouds were gathering. Economic liberalization was about to unleash forces that would test every assumption about public sector banking.

VI. Crisis, Recovery & Modernization (1990s-2010s)

The 1991 economic liberalization hit Indian Bank like a tsunami. Suddenly, the protected world of public sector banking was exposed to market forces. New private banks—HDFC, ICICI, Axis—entered with better technology, higher salaries, and freedom from government mandates. Foreign banks expanded operations. Capital markets offered alternatives to bank financing. The monopoly was broken.

Indian Bank's initial response was denial, then panic, then gradual adaptation. The Narasimham Committee reports of 1991 and 1998 prescribed bitter medicine: reduce government ownership, strengthen capital adequacy, improve asset quality, embrace technology, and prepare for competition. For an institution built on different principles, the adjustment was traumatic.

The asset quality crisis peaked in the late 1990s. Decades of directed lending, political interference, and weak recovery mechanisms had created a mountain of bad loans. Gross NPAs exceeded 15% by some estimates. The bank's capital adequacy ratio fell below regulatory minimums. Market share eroded as customers migrated to private banks offering better service and technology.

Recovery required radical surgery. Indian Bank launched "Project Comeback" in 2000, a comprehensive restructuring program. Voluntary retirement schemes reduced staff from 35,000 to 25,000. Unprofitable branches were closed or merged. Recovery teams were strengthened with legal backing from new debt recovery tribunals. The transformation was painful but necessary.

Technology became the new battlefield. Private banks offered anywhere banking, internet services, and phone banking while Indian Bank customers still filled paper forms in triplicate. The response was massive investment in core banking solutions. Between 2003 and 2008, the bank spent over ₹500 crore on technology, connecting all branches to a centralized system, launching internet banking, and introducing mobile services.

The achievement of ISO27001:2013 certification placed Indian Bank among very few banks certified worldwide, signaling its commitment to international standards in information security. This wasn't just about technology—it was about changing mindsets, retraining staff, and reimagining customer service.

The 2008 global financial crisis, paradoxically, helped Indian Bank's relative position. While international banks retreated and some private banks faced scrutiny over derivative losses, Indian Bank's conservative approach suddenly looked prudent. The government's stimulus spending flowed through public sector banks, boosting lending and profitability.

Digital transformation accelerated in the 2010s. Indian Bank launched mobile apps, partnered with fintech startups, and experimented with blockchain for trade finance. The bank recognized that survival required not just adopting technology but reimagining business models. Traditional branch banking gave way to digital channels. Product development shifted from one-size-fits-all to customized solutions.

Competition with private banks forced service improvements. Indian Bank introduced relationship managers for high-value customers, extended banking hours, and simplified loan processing. The cultural transformation was remarkable—from bureaucratic indifference to customer focus, from process orientation to outcome orientation.

Yet structural challenges persisted. Government ownership meant political interference in lending decisions. Priority sector obligations limited flexibility. Salary structures couldn't match private sector compensation. The Chennai-centric culture struggled to appeal to younger, urban customers across India. Market share in profitable segments like credit cards and wealth management remained minimal.

By 2019, Indian Bank had stabilized but not thrived. Net NPAs were under control at around 3%. Capital adequacy exceeded regulatory requirements. Digital adoption was respectable if not leading-edge. The bank was profitable but not growing rapidly. It needed something transformational to compete in the new era. That transformation would come through the most ambitious merger in Indian banking history.

VII. The Mega-Merger: Allahabad Bank Integration (2019-2021)

On August 30, 2019, Finance Minister announced that Allahabad Bank would be merged with Indian Bank. The proposal would create the seventh largest PSB in the country with assets of ₹8.08 lakh crore. For Indian Bank, this wasn't just another acquisition—it was a collision with history itself.

Allahabad Bank, founded on April 24, 1865, was India's oldest joint stock bank, predating Indian Bank by 42 years. It had financed India's freedom struggle, survived two world wars, and built a formidable presence across North India. With over 3,000 branches concentrated in Uttar Pradesh, Bihar, and West Bengal, Allahabad Bank brought geographical complementarity to Indian Bank's southern stronghold.

The numbers were staggering. The combined entity would have over 6,000 branches, 4,800 ATMs, 43,000 employees, and 120 million customers. Total business would exceed ₹8 lakh crore. But beyond numbers, this was a merger of two distinct banking cultures—Indian Bank's Tamil-centric, technology-forward approach meeting Allahabad Bank's Hindi heartland, relationship-based banking tradition.

The Union Cabinet approved the merger on March 4, 2020. Indian Bank assumed control of Allahabad Bank on April 1, 2020—coincidentally, just as India entered its first COVID-19 lockdown. The timing couldn't have been worse. Integration teams couldn't travel. Branches were shuttered. Employees worked from home. Customer service was disrupted. The pandemic turned a complex merger into a near-impossible challenge.

Indian Bank's response demonstrated remarkable organizational capability. An Integration Management Office was established with 24 workstreams covering everything from technology migration to cultural integration. Virtual war rooms coordinated activities across time zones. Daily video conferences connected thousands of employees. The merger playbook, carefully prepared over months, had to be rewritten on the fly.

Technology integration was the most complex challenge. Allahabad Bank operated on a different core banking platform. Customer data formats were incompatible. Product codes didn't match. Even simple things like account number structures differed. The solution required migrating 30 million customer accounts, 50 million transactions, and decades of historical data—all while maintaining uninterrupted service during a pandemic.

The human dimension was equally challenging. Allahabad Bank employees feared domination by Indian Bank's Tamil Nadu-centric culture. Indian Bank staff worried about dilution of their institutional identity. Salary structures differed. Promotion policies varied. Even working hours weren't aligned. The integration team launched "Project Sangam"—named after the confluence of rivers—to build unified culture while respecting both banks' heritage.

Customer retention became critical as private banks circled, hoping to poach confused or dissatisfied clients. Indian Bank launched massive communication campaigns, established dedicated helplines, and deployed relationship managers to hand-hold major clients through the transition. The message was consistent: you're not losing your bank; you're gaining a stronger one.

The technical migration, initially planned for December 2020, was delayed by COVID-19 complications. Finally, on February 15, 2021, over a single weekend, the entire Allahabad Bank technology infrastructure was migrated to Indian Bank's platform. It was one of the largest banking migrations ever attempted in India—and it worked. Monday morning, customers could access their accounts seamlessly.

Post-merger synergies emerged quickly. Duplicate branches were rationalized, reducing operational costs. Combined procurement lowered technology expenses. Unified treasury operations improved fund management. Cross-selling opportunities expanded—Indian Bank's strong MSME products to Allahabad's customer base, Allahabad's agricultural expertise to Indian Bank's rural markets.

The cultural integration, however, remains a work in progress. Language barriers persist—Tamil-speaking staff struggling in Hindi-belt branches and vice versa. Promotion policies had to be carefully calibrated to avoid favoring one legacy bank over another. Even something as simple as the official logo required months of deliberation to avoid alienating either institution's loyalists.

VIII. Modern Era & Digital Banking Push (2020-Present)

The post-merger Indian Bank emerged as a fundamentally different institution. The bank operates a vast network of branches, with over 6,000 branches and 12,000 ATMs across the country. Total business touched ₹13.45 lakh crore by June 2024, with market capitalization hovering around ₹853 billion. But size alone doesn't guarantee success in modern banking.

The digital transformation accelerated dramatically post-merger. Indian Bank launched "IndOASIS" (One Application for Smart Integrated Services), a super-app offering everything from account opening to loan applications, investment services to insurance products. The app onboarded 5 million users within 18 months, processing transactions worth ₹50,000 crore annually.

Fintech partnerships became strategic priorities. Collaborations with startups brought innovations in lending algorithms, payment solutions, and wealth management. The bank's API banking platform opened its services to third-party developers, creating an ecosystem of financial applications. Traditional banking was giving way to Banking-as-a-Service.

The MSME focus intensified with dedicated digital platforms for small businesses. "MSME Prerana" offered end-to-end digital lending with approval times reduced from weeks to hours. Supply chain financing solutions integrated with GST systems and e-commerce platforms. The bank processed over 100,000 MSME loans digitally in 2023 alone.

Retail banking saw revolutionary changes. Video KYC enabled account opening from home. AI-powered chatbots handled routine queries. Robo-advisors offered investment guidance. The branch transformation project converted traditional branches into digital experience centers where relationship managers used tablets instead of paper forms.

Recent financial performance reflects this transformation. The bank reported earnings of ₹21.90 per share versus ₹20.67 estimated, beating market expectations. Net interest margins improved to 3.2%. Fee income grew 25% year-on-year. Digital channels contributed 70% of transactions, reducing operational costs significantly.

Competition, however, has intensified across all fronts. Private banks like HDFC and ICICI dominate profitable urban markets. Payment banks and small finance banks nibble at the edges. Fintech unicorns like Paytm and PhonePe have captured digital payments. International tech giants eye India's financial services space. The competitive landscape has never been more challenging.

Indian Bank's response involves playing to its strengths while addressing weaknesses. The vast branch network, particularly in rural areas, provides last-mile connectivity that digital-only players can't match. Government backing ensures stability that startups lack. The Swadeshi heritage resonates with customers seeking trusted Indian brands. But execution remains key.

The talent challenge is acute. Indian Bank competes with private banks and tech companies for digital-skilled employees. The bank launched "Project Navigators," hiring 1,000 fresh graduates annually and training them in digital banking, data analytics, and customer experience design. Partnership with IITs and IIMs brings cutting-edge thinking into traditional banking.

Regulatory compliance has become increasingly complex. Requirements around data privacy, cyber security, and anti-money laundering demand massive investments. The bank spends over ₹200 crore annually on compliance technology. Regulatory reporting that once took weeks now happens in real-time through automated systems.

Customer expectations have fundamentally shifted. The benchmark isn't other banks but technology companies like Amazon and Google. Customers expect instant service, personalized products, and seamless experiences. Indian Bank's "Customer First 2.0" initiative reimagines every touchpoint from the customer's perspective, not the bank's operational convenience.

IX. Playbook: Strategic Lessons

The Indian Bank story offers profound lessons for institutional transformation. First, crisis as catalyst has been the recurring theme. The Arbuthnot collapse birthed the bank. Nationalization forced geographic expansion. Liberalization demanded modernization. The pandemic-era merger created scale. Each crisis, properly channeled, became an opportunity for revolutionary change rather than evolutionary adjustment.

Second, cultural capital matters more than financial capital. Indian Bank's Swadeshi heritage provides emotional connection that no amount of advertising can buy. Customers who remember their grandparents banking with Indian Bank display loyalty that transcends rational calculation. This cultural moat, carefully preserved through multiple transformations, differentiates Indian Bank from both new-age startups and other public sector banks.

Third, scale through consolidation works when executed properly. The 1960s acquisitions brought local expertise. The Thanjavur Bank merger added rural depth. The Allahabad Bank integration created national presence. Each consolidation was more than addition—it was multiplication of capabilities. The lesson: in banking, thoughtful consolidation beats organic growth.

Fourth, government partnership is both blessing and curse. State ownership provided stability during crisis, capital during expansion, and purpose during development. But it also brought interference in lending, constraints on compensation, and burdens of social mandates. Success requires navigating this duality—leveraging government support while minimizing political interference.

Fifth, technology adoption requires cultural transformation. Indian Bank's technology investments succeeded not because of systems but because of mindset changes. Training 40,000 employees to think digitally proved harder than installing software. The lesson: technology strategy is actually human resources strategy in disguise.

Sixth, integration excellence determines merger success. The Allahabad Bank merger succeeded because Indian Bank treated it as transformation, not absorption. Respecting both institutions' heritage, combining their strengths, and addressing their weaknesses created value. The pandemic complexity, rather than destroying the merger, forced innovative integration approaches that proved superior to traditional methods.

The strategic framework emerging from Indian Bank's journey suggests that successful institutional transformation requires: Clear vision that transcends financial metrics; patient capital that tolerates short-term pain for long-term gain; leadership that balances continuity with change; culture that adapts while preserving core values; and execution that maintains operations while transforming systems.

X. Analysis & Investment Case

Evaluating Indian Bank as an investment requires balancing compelling strengths against structural challenges. The bull case rests on solid foundations. As the seventh-largest public sector bank, Indian Bank enjoys systemic importance that virtually guarantees government support during crisis. The successful Allahabad Bank integration created synergies still being realized—cost savings from branch rationalization, revenue growth from cross-selling, and operational efficiencies from unified systems.

The dividend yield of 2.56% provides steady income in a low-interest environment. Government backing eliminates bankruptcy risk that haunts private sector banks globally. The vast branch network, particularly in rural areas, creates distribution advantages as India pushes financial inclusion. Digital transformation, while incomplete, has progressed faster than most public sector banks.

South Indian markets, Indian Bank's traditional stronghold, display India's highest literacy rates, entrepreneurial culture, and industrial development. The Chennai headquarters provides access to Tamil Nadu's manufacturing belt, Karnataka's technology sector, and Kerala's service economy. This geographic positioning captures India's most dynamic economic regions.

The bear case, however, raises serious concerns. Public sector bank constraints limit strategic flexibility. The government can direct lending to politically favored but economically unviable sectors. Management changes follow political cycles rather than performance metrics. Compensation structures can't match private sector banks, creating persistent talent drain.

Financial metrics flash warning signals. The low interest coverage ratio suggests vulnerability to economic downturns. Contingent liabilities of ₹2,94,918 crore represent massive off-balance-sheet exposure. Asset quality, while improved, remains vulnerable to agricultural loan waivers and MSME stress. The provision coverage ratio, though adequate, might prove insufficient during systemic crisis.

Competition from private banks intensifies annually. HDFC Bank's technology platform processes more transactions daily than Indian Bank handles weekly. ICICI Bank's corporate relationships span India's largest companies. Axis Bank's retail franchise attracts urban millennials. Foreign banks dominate investment banking. Fintech startups unbundle profitable products. Indian Bank risks being squeezed from all directions.

The fintech disruption threatens traditional banking models. UPI has commoditized payments, eliminating fee income. Digital lending platforms approve loans in minutes, not days. Robo-advisors democratize wealth management. Cryptocurrency experiments challenge monetary systems. Indian Bank's massive branch network might become a stranded asset if banking moves entirely digital.

Regulatory headwinds persist. Basel III capital requirements demand continuous fundraising. Priority sector lending mandates limit portfolio optimization. Interest rate caps reduce margins. The Reserve Bank of India's increasingly strict asset quality reviews might reveal hidden problems. Compliance costs escalate faster than revenues.

The investment decision ultimately depends on one's view of India's banking future. Optimists see Indian Bank leveraging government support, vast distribution, and cultural heritage to remain relevant despite technological disruption. Pessimists see a slow-moving giant unable to compete with nimble private players and tech-native startups. Realists recognize both possibilities coexist.

XI. Future Outlook & Strategic Priorities

Indian Bank's strategic priorities for the next decade focus on six critical areas. First, digital transformation must accelerate from current initiatives to fundamental reimagination. This means not just digitizing existing processes but creating digital-native products that couldn't exist in physical banking. The bank plans to invest ₹2,000 crore over three years in cloud infrastructure, artificial intelligence, and blockchain technology.

Second, CASA ratio improvement remains crucial for sustainable profitability. Current ratio around 35% lags private banks achieving 45-50%. The strategy involves leveraging the salary account franchise from government employees, deepening wallet share with existing customers, and using digital channels to acquire low-cost deposits. Target: reaching 40% CASA ratio by 2027.

Third, asset quality management requires constant vigilance. The bank is implementing early warning systems using machine learning to identify stress before defaults occur. Dedicated stressed asset resolution teams work with borrowers facing temporary difficulties. The agricultural loan portfolio is being diversified across crops and geographies to reduce concentration risk.

Fourth, fee income diversification must reduce dependence on interest income. Current fee income at 12% of total income significantly trails private banks at 20-25%. Opportunities exist in wealth management for increasingly affluent customers, bancassurance leveraging the vast customer base, and transaction banking for corporate clients. The target is 18% fee income contribution by 2026.

Fifth, branch rationalization post-merger offers significant cost savings. Initial analysis identified 800 branches within 500 meters of each other. The strategy involves converting duplicate branches into digital service points, relocating branches from saturated urban areas to underserved semi-urban markets, and creating hub-and-spoke models where one full-service branch supports multiple satellite units.

Sixth, competing in the fintech era requires fundamental strategic choices. Indian Bank cannot out-technology the startups but can offer what they lack—trust, stability, and comprehensive services. The strategy involves partnering rather than competing with fintechs, focusing on complex products requiring human interaction, and leveraging regulatory advantages that licensed banks enjoy.

The macroeconomic environment presents both opportunities and challenges. India's GDP growth trajectory suggests credit demand will expand faster than developed markets. Financial inclusion initiatives create new customer segments. Infrastructure investment drives project financing opportunities. But global uncertainty, inflation concerns, and technological disruption create unprecedented volatility.

Indian Bank's response involves scenario planning for multiple futures. In the optimistic scenario where traditional banking remains relevant, the bank leverages its scale and government backing to capture market share. In the pessimistic scenario where technology completely disrupts banking, the bank transforms into a financial services platform partnering with various providers. The most likely scenario involves hybrid models combining digital efficiency with human relationship management.

XII. Epilogue & Reflections

Standing at the corner of Armenian Street and Second Line Beach Road in Chennai, where Indian Bank's headquarters now towers over the cityscape, one can't help but reflect on the extraordinary journey from V. Krishnaswamy Iyer's protest against colonial banking to today's digital financial powerhouse. The building itself tells the story—classical architecture at the base representing heritage, modern glass towers above symbolizing transformation.

What would Krishnaswamy Iyer think of today's Indian Bank? He would certainly appreciate that his vision of Indian-controlled banking has been realized beyond imagination. The bank he founded with ₹1 lakh now manages assets worth ₹8 lakh crore. The single branch in Parry's Corner has multiplied to 6,000 across India and abroad. The handful of founding shareholders has grown to millions of stakeholders.

Yet he might question whether the soul survived the transformation. Has the merger with Allahabad Bank, an institution that predated Indian Bank and served different markets, diluted the original Tamil-centric identity? Has government ownership achieved the Swadeshi goal of indigenous control, or merely replaced British colonialism with political interference? Has digital transformation maintained the human touch that distinguished Indian banking from foreign institutions?

The answer lies in recognizing that institutional identity must evolve while preserving core values. Indian Bank's journey from Swadeshi movement to digital age demonstrates that survival requires adaptation, but success demands authenticity. The bank succeeded when it remained true to its mission of financial inclusion while embracing technological change. It struggled when it forgot customer service in bureaucratic processes or abandoned prudent banking for political expediency.

The lessons from Indian Bank's 117-year history resonate beyond banking. First, institutions outlive individuals only through constant renewal. Second, cultural heritage provides competitive advantage only when combined with contemporary capabilities. Third, scale without strategy is merely size, but strategy without scale is simply ambition. Fourth, government support enables but also constrains—success requires maximizing benefits while minimizing interference. Fifth, technology transforms operations, but culture determines outcomes.

Looking forward, Indian Bank faces existential questions. Can a 20th-century institution remain relevant in the 21st century? Can public sector banks compete with private efficiency and fintech innovation? Can traditional banking survive digital disruption? The answers will determine not just Indian Bank's future but the trajectory of India's financial system.

The story of Indian Bank ultimately reflects India's own journey—from colonialism to independence, from socialism to markets, from isolation to globalization, from physical to digital. Like India itself, the bank carries both the weight of history and the promise of transformation. Its success or failure will be measured not just in financial metrics but in its contribution to India's economic development and social progress.

As we conclude this analysis, remember that Indian Bank isn't just a financial institution—it's a testament to institutional resilience, a case study in organizational transformation, and a mirror reflecting India's economic evolution. From the ashes of Arbuthnot & Co. to the heights of digital banking, from Swadeshi idealism to global integration, from colonial protest to national champion, Indian Bank's journey continues.

The next chapter remains unwritten. Will Indian Bank leverage its unique combination of government backing, cultural heritage, and national scale to remain relevant in the digital age? Or will it become another casualty of technological disruption, its massive branch network and legacy systems dragging it toward irrelevance? The answer depends on choices being made today in boardrooms and branches, by regulators and customers, by employees and investors.

What's certain is that Indian Bank's story—like India's own—is far from over. The institution born from crisis, strengthened through adversity, and transformed through ambition faces its greatest challenge yet: remaining meaningful in an age when banking itself is being redefined. How it responds will determine whether Indian Bank celebrates another century of service or becomes a cautionary tale of institutional inertia.

For investors, employees, customers, and observers, Indian Bank represents both the promise and peril of institutional transformation. Its journey from Swadeshi movement to digital revolution offers lessons in resilience, warnings about complacency, and hope that even century-old institutions can reinvent themselves for new realities. The bank that began as an act of rebellion against colonial finance might yet become a leader in post-digital banking—if it can once again transform crisis into catalyst, challenge into opportunity, and heritage into advantage.

This is the continuing story of Indian Bank—not an ending but a comma in an institutional narrative that spans three centuries, touches hundreds of millions of lives, and reflects the dreams and struggles of a nation itself in constant transformation. The next chapters will be written by those who believe that banking is more than transactions, that institutions can outlive their founders' wildest imagination, and that the mission of financial inclusion remains as relevant in the digital age as it was in the colonial era.

From V. Krishnaswamy Iyer's vision in 1907 to today's digital reality, from Parry's Corner to pan-India presence, from Swadeshi movement to global integration, Indian Bank's journey continues—a testament to the enduring power of institutional purpose, the necessity of constant adaptation, and the possibility that even the oldest banks can learn new tricks. The story that began with the collapse of Arbuthnot & Co. continues with the rise of digital India, and the bank born from crisis might yet thrive in transformation.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube