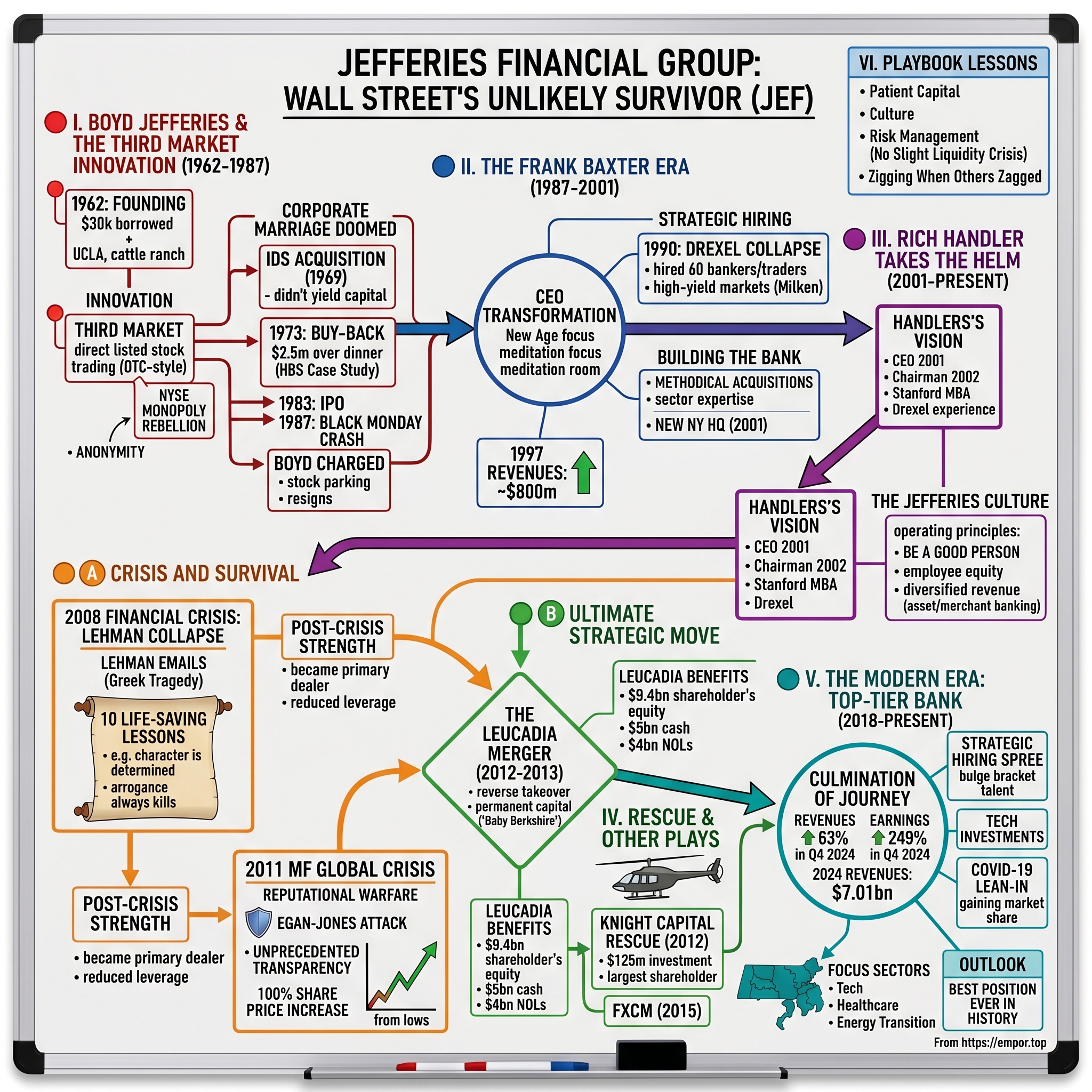

Jefferies Financial Group: Wall Street's Most Unlikely Survivor

I. Introduction & Episode Roadmap

Picture this: September 2008, the height of the financial crisis. Lehman Brothers, the 158-year-old Wall Street titan, is gasping its final breaths. In a Midtown Manhattan office, a relatively unknown CEO of a mid-sized investment bank types out an email to Dick Fuld, Lehman's embattled chief: "I have always been in awe of the company you built... I modeled much of Jefferies on the financial giant." Hours later, Lehman files for the largest bankruptcy in U.S. history. The sender of that email, Richard Handler, would not only survive the carnage but transform his firm into something extraordinary.

Today, Jefferies' fourth quarter 2024 net revenues of $1.96 billion, pre-tax earnings from continuing operations of $305 million and diluted earnings per share from continuing operations of $0.91 are 63%, 249% and 214% higher than the prior year quarter, respectively. The full year 2024 saw revenues of $7.01 billion (up 49% from 2023) and net income of $665.6 million (up 155%). The firm has climbed to become the fifth-largest advisor in global M&A and sixth in equity capital markets—a stunning transformation from a scrappy third market trading shop that started with $30,000 in borrowed money.

This is the story of how Jefferies defied every prediction, survived every crisis, and emerged as Wall Street's most unlikely success story. It's a tale of three distinct eras: the maverick founder who revolutionized stock trading, the visionary who built an investment bank from scratch, and the partnership that engineered one of finance's most audacious strategic moves. Along the way, we'll uncover the lessons from Lehman's collapse, the truth behind the MF Global attacks, and the unconventional merger that gave Jefferies something no other mid-sized bank possessed: permanent capital.

II. Boyd Jefferies & The Third Market Innovation

In 1962, the Pacific Coast Stock Exchange floor was a far cry from the marble halls of Wall Street. Boyd Jefferies borrowed $30,000 and purchased a seat on the Pacific Coast Stock Exchange, operating initially from what was essentially a telephone booth. After graduating from UCLA in 1952, Boyd spent several years working on his uncle's cattle ranch, where he learned the value of hard work, before taking an Assistant Clerk position on the floor of the Pacific Coast Stock Exchange.

The genius of Boyd's approach wasn't just trading—it was seeing what others couldn't. The firm was a successful trader and pioneer in what would be called the "third market", which allowed for the trading of listed stocks directly between institutional investors in an over-the-counter style, providing liquidity and anonymity to buyers. This wasn't just a technical innovation; it was a rebellion against the NYSE monopoly. In 1964, the firm pioneered the use of split commissions, further distinguishing itself.

The NYSE didn't take this challenge lying down. By 1967, Jefferies had joined the NYSE, but the battles were just beginning. Jefferies & Company was acquired in 1969 by the Minneapolis-based Investors Diversified Services, Inc. (IDS), the second largest financial services company in the country at the time. But the corporate marriage was doomed from the start. IDS did not yield the expected capital to Jefferies, nor did it conduct any trades with the firm. Because IDS didn't derive at least 50 percent of its gross income from broker-dealer operations, Jefferies had to quit the NYSE under Exchange Rule 318.

In August 1973 Boyd Jefferies bought back his company over dinner for $2.5 million. The story of the Jefferies acquisition was the subject of a later case study at Harvard Business School. The repurchase marked a new beginning, but also foreshadowed the pattern of independence and entrepreneurial spirit that would define the firm.

Jefferies went public on October 13, 1983, with an initial offering of 1.75 million shares at $13 per share. By 1984, according to Business Week, the firm was among the ten most profitable publicly held brokerages. International expansion beckoned, with Frank Baxter leading the charge to open a London office.

But success bred scrutiny. In 1987, Boyd Jefferies was charged by the government and the Securities and Exchange Commission with two securities violations: "parking" stock for a customer Ivan Boesky and a customer margin violation. Jefferies, who had also earlier testified against Boesky, pleaded guilty; receiving a fine and a probation barring him from the securities industry for five years. Boyd Jefferies resigned from the company in 1987.

The timing couldn't have been worse. October 19, 1987—Black Monday—saw the stock market crash, and the company suffered a $6.5 million loss on its principal holdings. The third market pioneer was gone, and his company teetered on the brink.

III. The Frank Baxter Era & Building Investment Banking

Frank Baxter took over as CEO in 1987 and under his leadership the company focused on diversification, moving beyond its third market niche. Baxter wasn't your typical Wall Street executive. A disciple of New Age guru Deepak Chopra and an avid practitioner of transcendental meditation, Baxter installed a meditation room in Jefferies' headquarters (which was later closed for lack of use).

Despite his unconventional style, Baxter had a clear vision: transform Jefferies from a pure trading shop into a full-service investment bank. In 1990, Jefferies derived approximately 80 percent of its revenues from equity block trades. That was about to change dramatically.

Following the collapse of Los Angeles-based Drexel Burnham Lambert, the fifth largest investment bank at the time, Jefferies hired 60 of its bankers and traders, including Jefferies' current chairman and CEO, Richard B. Handler. The hires marked the firm's entry into the high yield markets and investment banking.

This wasn't just a hiring spree—it was a cultural transplant. The Drexel refugees brought with them the high-octane, high-risk mentality that Michael Milken had instilled, but also the scars of watching their firm implode. Among them was a 28-year-old Handler, fresh from Stanford Business School, who had witnessed firsthand how quickly a Wall Street giant could fall.

The firm methodically built sector expertise through targeted acquisitions. In September 2001, the firm moved its headquarters from Los Angeles to New York. During this period, Jefferies built its investment banking division primarily by acquiring boutique advisory firms with specific sector expertise, most notably Randall & Dewey (energy) and Broadview (technology).

By 1997, the transformation was evident. The company had not had a losing year since Baxter took over, and 1997 revenues approached $800 million (a 47 percent increase over 1996), with earnings of $63.6 million. The meditation room might have been empty, but the trading floor was buzzing with newfound ambition. Frank Baxter had saved the company from Boyd's implosion and set the stage for what would come next.

IV. Rich Handler Takes the Helm (2001)

Handler joined Jefferies in April 1990 as a salesman and trader. He was appointed CEO on January 1, 2001 and Chairman in 2002, succeeding Frank E. Baxter. But Handler's path to the CEO suite was anything but conventional. The son of Alan and Jane Handler, Richard Handler grew up in New Jersey, graduating in 1979 from Pascack Hills High School in Montvale. He received a BA in economics from the University of Rochester magna cum laude in 1983 and an MBA from Stanford University in 1987.

Prior to Jefferies, he was an investment banker at First Boston and later he worked for Michael Milken at Drexel Burnham Lambert in the high-yield bond department. Handler was 28 years old when Drexel filed for bankruptcy on February 13, 1990, fresh out of Stanford Business School, newly married and months away from beginning a family. He worked incredibly hard to earn the honor of working for Drexel in Beverly Hills where the famous X-shaped trading desk with Michael Milken occupying the center, literally marked the very center of the global financial universe.

The Drexel experience shaped everything that followed. "I have learned in my 35 years since Drexel that when the truth eventually comes out in the right manner, the naysayers with agenda wilt and fade back into the darkness", Handler would later reflect. He remains grateful to Michael Milken who "in addition to changing the world for the better in so many ways, remains an important part of my life to this day. I am beyond appreciative for the many remarkable people I met through Drexel, many of whom today are invaluable clients, trusted business partners at Jefferies, and lifelong friends".

When Handler joined as CEO, Jefferies had been primarily known as a trading firm with expertise in the energy sector. Handler and John Shaw set out to build a fully integrated investment bank and to develop a merchant bank. The new leadership proposed to give equity to every employee and diversify the firm's revenue with asset management, a more aggressive buildup of investment banking and merchant banking.

The culture Handler instilled was different from Wall Street's typical eat-what-you-kill mentality. "Be a good person" became an actual operating principle. This wasn't just corporate happy talk—it was born from watching Drexel's collapse and understanding that arrogance and short-term thinking could destroy even the mightiest firms. "I was a cog in the giant wheel doing the 1988 $25 Billion LBO of RJR Nabisco at Drexel but got more personal satisfaction personally spearheading the 1990 $184 Million LBO of Buttrey's Supermarket at Jefferies. Nothing beats being an entrepreneur and when you start on your own, you usually have to start small. Better yet, working with your partners to build a company over decades that can eventually do the largest and most complex transactions in the financial world creates a feeling of pride that is impossible to fully express".

By the mid-2000s, Handler's vision was taking shape. The firm had become a primary dealer, expanded globally, and was steadily climbing the league tables. But the real test of his leadership—and the lessons from Drexel—would come during the darkest days of 2008.

V. The 2008 Financial Crisis: Learning from Lehman

The relationship between Handler and Dick Fuld made what happened next all the more poignant. Three days before Lehman's collapse, Handler reached out to the man he'd long admired. The emails between them, later made public, read like a Greek tragedy—one titan watching another fall, knowing he could be next.

When Lehman filed for bankruptcy on September 15, 2008, with more than $600 billion in debt, Handler sent a final email to Fuld: "I am so very sorry for you and the special company that you built". Fuld's response, two weeks later, thanking Handler for his support, would be one of his last acts as CEO of the fallen giant.

Handler didn't just mourn—he studied. From Lehman's collapse, he distilled ten life-saving lessons that would become Jefferies' survival guide: (1) There is no such thing as a "slight liquidity crisis" (2) Everything in life is fragile (3) Sometimes bad things happen to good people (4) Never take anything or anyone for granted (5) Leverage can't distinguish between good or bad, but it will happily magnify both (6) You never have as much time as you may think (7) Character is determined during tough times (8) Arrogance always kills (9) If your debt holders are at risk, your shareholders will probably be wiped out (10) If you stay positive through the storm, the sun always eventually rises, and life will go on.

These weren't just platitudes—they became operating principles. Jefferies reduced leverage, diversified funding sources, and most importantly, maintained a humility that kept them nimble. By 2009, Jefferies had transformed from a small equity trading shop to a primary dealer for the New York Fed, allowing it to participate in the open-market buying and selling of securities.

The firm that had modeled itself on Lehman had learned from Lehman's demise. While others were retreating, Jefferies was advancing, hiring talent from failed firms and expanding into abandoned markets. The crisis that killed Lehman made Jefferies stronger—but an even greater test was coming.

VI. The MF Global Crisis: False Attacks and Finest Hours (2011)

If 2008 taught Handler about systemic risk, November 2011 would teach him about reputational warfare. MF Global filed for bankruptcy on October 31, 2011, after making a wrong-way $6.3 billion bet on European sovereign debt. The trustee liquidating the company said that losses incurred by customers of MF Global stood at $1.6 billion.

Within hours, the sharks circled Jefferies. Jefferies was accused by Egan-Jones of having 77% of its shareholder's equity tied up in the same illiquid sovereign debt securities that just toppled MF Global. This was accompanied by a concurrent large-scale short seller attack and a campaign of what turned out to be misinformation.

Handler's response was unprecedented in Wall Street history. Rather than issue vague reassurances, he went nuclear with transparency. Handler and the management team responded with unprecedented immediacy and transparency, collapsed 75% of the position to prove the bonds were hedged and highly liquid, sharply reduced the rest of Jefferies balance sheet and publicly addressed every false accusation.

The firm published every position, down to the CUSIP numbers. "Some irresponsible individuals began to spread the rumor that we had 'sold our sovereign position to an affiliate' and effectively 'parked' it there with an obligation to buy it back. This is a malicious lie. Our sales and trading team sold and covered our positions with unaffiliated third parties. To be crystal clear, Leucadia did not purchase one bond and we have no obligation to purchase anything back in the future from anyone".

The letter to shareholders pulled no punches, describing the attacks as coming from "a group of people maliciously spreading rumors, half-truths and outright lies through every means possible." Handler named no names, but the message was clear: Jefferies would not go quietly into that good night.

This aggressive and unconventional response resulted in an eventual 100% increase in Jefferies share price from the November lows. Leucadia, a 29% shareholder, later called this event Jefferies' "finest hour". The firm had stared down an existential threat and emerged stronger. But Handler knew they needed something more permanent than just good crisis management. They needed a fortress.

VII. The Leucadia Merger: The Ultimate Strategic Move (2012-2013)

The merger of Jefferies and Leucadia was publicly announced on November 12, 2012 and consummated on March 1, 2013. But this wasn't your typical Wall Street deal. Richard Handler, Jefferies' CEO, had a long standing personal dream to one day run Leucadia, which was founded by two of his close friends, defendants Ian Cumming and Joseph Steinberg. Upon learning that Cumming and Steinberg had plans to retire and that Leucadia lacked a viable succession plan, Handler and Jefferies' President, defendant Brian Friedman, began negotiations with Cumming and Steinberg about a potential combination of the companies without informing the Jefferies Board. The negotiations continued for over four months before the Jefferies Board was even informed.

Leucadia is often referred to as a Baby Berkshire because of its similarities to Berkshire Hathaway. Jefferies was valued at $3.8 billion and at the time of the acquisition the newly combined company had $9.4 billion of shareholder's equity, over $5 billion of cash, and $4 billion of net operating loss ("NOL") tax credits.

The structure was brilliant in its simplicity. Richard Handler became CEO of Leucadia while retaining his position as CEO of Jefferies. Brian Friedman became President of Leucadia while retaining his duties at Jefferies. Mr. Steinberg became Chairman of the Board of Leucadia and continued to work full time as an executive. Mr. Cumming retired as Chairman of the Board and Chief Executive Officer of Leucadia upon the closing of the transaction and remained a Leucadia Director.

Cumming's endorsement was powerful: "Joe and I have been partners for 34 years. His role as Chairman of the Board, along with other Leucadia and Jefferies Directors, will ensure continuity and propel our continued success. My relationship with Rich and Brian, both as advisors and, more recently, as business partners and Jefferies Directors, showed me they can manage Leucadia profitably long into the future. Their ability to manage and grow Jefferies through the elongated financial bubble, successfully navigate the crises that followed where others could not, and protect the firm from the attacks based on false information exactly one year ago with deftness and grace, should comfort all!"

In May 2018, the company was renamed Jefferies Financial Group, completing the transformation. The scrappy trading shop had engineered a reverse takeover of a legendary investment vehicle, gaining permanent capital and the ultimate defense against short-term market panics.

VIII. Knight Capital Rescue & Other Strategic Plays

August 1, 2012, should have been just another trading day. Instead, it became a masterclass in crisis management and opportunistic investing. Knight Capital Group agreed to be acquired by Getco LLC in December 2012 after an August 2012 trading error lost $460 million. The glitch, caused by a software deployment gone wrong, had sent Knight on an automated buying spree, acquiring billions in unwanted positions in just 45 minutes.

Jefferies CEO Richard Handler and Executive Committee Chair Brian Friedman structured and led the rescue and Jefferies purchased $125 million of the $400 million investment and became Knight's largest shareholder. Within hours of the disaster, while others were calculating risks, Handler and Friedman were calculating opportunity.

The Knight Capital rescue wasn't just about making money—though Jefferies certainly did. It was about demonstrating that while the firm had Leucadia's balance sheet behind it, it could still move with the speed and decisiveness of a boutique. This combination of capital strength and entrepreneurial agility would become Jefferies' signature move, repeated with distressed assets throughout the decade.

The pattern continued with FXCM in 2015, when the Swiss Franc's appreciation caused massive losses across the foreign exchange market. Each crisis became an opportunity to deploy capital, build relationships, and demonstrate that Jefferies was a different kind of investment bank—one that showed up when others retreated.

The transition from merchant banking to pure-play investment bank accelerated post-Leucadia. The permanent capital base allowed Jefferies to hold positions longer, take calculated risks, and most importantly, never be a forced seller. This patient capital approach, borrowed from the Cumming-Steinberg playbook, transformed how Jefferies could compete against larger rivals.

IX. The Modern Era: Becoming a Top-Tier Bank (2018-Present)

Fourth quarter 2024 results show Investment Banking up 73%, including a record quarter in Advisory (up 91%), as well as another robust quarter for Equities (up 49%) and solid performance in Fixed income (up 15%). The primary driver behind last 12 months revenue was the Investment Banking and Capital Markets segment contributing a total revenue of $6.20 billion (88% of total revenue).

The numbers tell only part of the story. Behind them is a strategic hiring spree that brought in senior bankers from bulge brackets, lured by Jefferies' entrepreneurial culture and the promise of building something rather than maintaining something. Technology became a focus area, with significant investments in electronic trading platforms and data analytics capabilities that rivaled firms many times Jefferies' size.

COVID-19, rather than slowing the firm down, accelerated its transformation. While competitors retreated to preserve capital, Jefferies leaned in, gaining market share in virtually every product area. "Please refer to the just-released Jefferies Financial Group Annual Letter from our CEO and President for broader perspective on 2024, as well as our strategy and outlook"—these annual letters, in Handler's distinctive voice, became required reading on Wall Street, mixing financial results with philosophy and the occasional sharp elbow to competitors.

The firm's position heading into 2025 represents the culmination of a 60-year journey from telephone booth to top table. "We are beyond thrilled and proud of how far our Firm has come in a mere 60 years", Handler noted in a recent letter, adding that "Jefferies begins 2025 in the best position ever in our firm's sixty-two year history".

The strategic focus areas—technology, healthcare, energy transition—position Jefferies at the intersection of the economy's most dynamic sectors. The firm's ability to serve both mega-cap corporations and emerging growth companies gives it a breadth that many boutiques lack and an agility that bulge brackets envy.

X. Playbook: Business & Investing Lessons

The Jefferies story offers a masterclass in building a financial services firm against the odds. The first lesson is the power of patient capital. "In 2012, driven primarily by Joe Steinberg, Jefferies was merged into Leucadia and Joe (and Ian) selflessly gave every one of us the biggest gift possible: possession and control of their prized child, Leucadia". This wasn't just about money—it was about time horizons. With permanent capital, Jefferies could think in decades rather than quarters.

Building through acquisitions versus organic growth became an art form. Each acquisition—from the Drexel team in 1990 to boutique advisory firms in the 2000s—wasn't just about adding capabilities but transplanting culture. The firms Jefferies bought weren't just absorbed; they were integrated in a way that preserved their entrepreneurial spirit while adding Jefferies' resources.

Culture as competitive advantage sounds like consultant-speak, but at Jefferies it's measurable. "Approximately 70% of our banking revenues are from repeat clients"—a statistic that speaks to relationships built on trust rather than transactions. The "collaboration and integrity" mantra isn't wall art; it's embedded in compensation structures that reward long-term thinking and teamwork over individual glory.

Risk management lessons are written in scar tissue. "There is no such thing as a slight liquidity crisis" became an operating principle that kept Jefferies from the leverage excesses that felled others. The MF Global crisis taught them that perception could become reality in hours, not days, requiring a new playbook for crisis communication.

Being the "un-bank" bank meant zigging when others zagged. When bulge brackets retreated to core clients during crises, Jefferies expanded. When others sought government bailouts, Jefferies relied on its own capital. This contrarian approach required courage but created opportunities.

Capital allocation became a strategic weapon. "Knight opted to sell $400 million of preferred stock to an investor group led by Jefferies Group. This amounted to a sale of 73% of the company. Besides Jefferies, the investors included Blackstone and Getco". Each crisis investment wasn't just opportunistic but strategic, building relationships and capabilities that would pay dividends for years.

The value of relationships and loyalty in finance cannot be overstated. "When Drexel went bankrupt in 1990 and Jefferies had no business even pretending to be the investment banker to an investment grade company like Leucadia, Joe never hesitated. For the next decade, Jefferies was involved (leading) every deal that Joe and Ian executed. Jefferies did its first high-yield bond deal, first investment grade bond deal, first equity deal and first convert deal all with Leucadia".

XI. Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Porter's 5 Forces:

The competitive rivalry in investment banking is intense, with Jefferies competing against both bulge brackets with massive balance sheets and boutiques with specialized expertise. Yet Jefferies has carved out a differentiated position—large enough to compete for major deals but nimble enough to win on service and speed.

High barriers to entry protect incumbents through regulatory requirements, capital needs, and the relationship-based nature of the business. The Basel III capital requirements and Dodd-Frank regulations create moats that Jefferies, having already crossed, now benefits from.

The bargaining power of suppliers—primarily talent—remains Jefferies' greatest challenge and opportunity. The war for talent intensified post-COVID, but Jefferies' entrepreneurial culture and competitive compensation have made it a destination for top bankers fleeing bureaucratic bulge brackets.

Corporate clients' bargaining power is significant—they can choose from many banks—but Jefferies has cultivated sticky relationships through consistent execution and personal attention from senior bankers. The Board of Directors declared a quarterly cash dividend equal to $0.40 per Jefferies common share, a 14.3% increase from the prior dividend rate, signaling confidence in sustainable client relationships.

The threat of substitutes—direct lending, private credit, SPACs—represents both risk and opportunity. Jefferies has embraced these alternatives, building capabilities in private credit advisory and SPAC underwriting rather than fighting the tide.

Hamilton's 7 Powers:

Counter-positioning against bulge brackets has been Jefferies' masterstroke. While Goldman and Morgan Stanley chase mega-deals, Jefferies wins by being faster, more flexible, and more focused on sectors others ignore.

Scale economies remain elusive—Jefferies generates impressive returns but on a smaller revenue base than the top tier. Profit margin of 9.5% (up from 5.6% in FY 2023), driven by higher revenue, shows improving operating leverage but room for growth.

Switching costs in investment banking are moderate—relationships matter but aren't unbreakable. Jefferies creates stickiness through sector expertise and consistent team coverage rather than relying solely on institutional inertia.

Network effects are limited but growing in certain products, particularly in sectors where Jefferies has achieved critical mass. Their position in certain verticals creates a virtuous cycle of deal flow and expertise.

Process power—the unique ability to execute complex transactions quickly—has become a calling card. The Knight Capital rescue demonstrated this capability, moving from first call to signed deal in days, not weeks.

The "Handler brand" has evolved from unknown to unavoidable. Handler's public letters, social media presence, and willingness to engage critics have created a personal brand that enhances the institutional one.

The cornered resource of the Handler/Friedman partnership may be Jefferies' most valuable asset. Their combination of experience, relationships, and credibility cannot be replicated or recruited away.

XII. Bear vs. Bull Case

Bear Case:

The sub-scale challenge looms large. Despite impressive growth, Jefferies still generates a fraction of the revenues of Goldman Sachs or JPMorgan. In a business where scale provides resilience, being mid-sized means being vulnerable to market downturns that barely dent larger competitors.

The cyclical nature of investment banking revenues creates vulnerability. A prolonged deal drought could pressure profitability, particularly given the higher fixed cost base from recent hiring. The compensation ratio remains elevated as Jefferies invests in talent to compete with larger rivals.

Key person risk cannot be ignored. Handler is 63, and while succession planning exists, his departure would remove a unique asset. The Handler-Friedman partnership has been central to Jefferies' success—replacing it won't be simple.

Compensation pressures in today's hot talent market threaten margins. Every senior hire from a bulge bracket demands guarantees and buyout packages that pressure near-term profitability. The war for talent only intensifies as private equity and hedge funds compete for the same bankers.

Regulatory risks are increasing globally, from Europe's MiFID III to potential U.S. changes to carried interest taxation and SPAC rules. Each new regulation adds compliance costs that disproportionately impact mid-sized firms.

Bull Case:

Market share gains are accelerating across every product line. Full year 2024 revenue of $7.01 billion represents a 49.15% increase from 2023's $4.70 billion, with earnings up 156.48%. The momentum suggests Jefferies has reached escape velocity from its middle-market origins.

Operating leverage is improving dramatically as the revenue base grows faster than the cost base. The infrastructure investments of recent years can support significantly higher volumes without proportional cost increases.

Jefferies is the best positioned mid-market player globally, with capabilities that match bulge brackets in key sectors. The firm's focus on sectors like healthcare, technology, and energy transition aligns with economic megatrends.

The strong balance sheet post-Leucadia merger provides competitive advantage. Access to permanent capital allows Jefferies to commit to transactions, hold positions, and weather downturns that would cripple standalone investment banks.

Cultural advantages in attracting talent become self-reinforcing. Each high-profile hire from a bulge bracket validates Jefferies as a destination, making the next hire easier. The entrepreneurial culture attracts bankers tired of bureaucracy.

The 14.3% dividend increase and quarterly cash dividend of $0.40 per share demonstrates management's confidence in sustainable cash generation.

KPIs to Watch:

League table rankings remain the scorecard Wall Street watches. Movement into global top 5 for M&A would mark Jefferies' arrival as a true bulge bracket alternative.

Revenue per employee indicates operational efficiency and productivity. As Jefferies scales, this metric should improve, demonstrating operating leverage.

Investment banking backlog provides forward visibility into revenues. Growth here indicates market share gains and relationship deepening.

XIII. Epilogue & Future Outlook

The succession planning question hangs over Jefferies like morning mist over the Hudson. Handler, at 63, shows no signs of slowing, but the firm's dependence on his vision and relationships creates inevitable uncertainty. The deep bench of talent recruited over the past decade provides options, but replacing a founder-CEO is never simple.

Artificial intelligence and technology transformation in banking present both opportunity and threat. Jefferies' smaller size allows for agility in adoption, but lacks the massive technology budgets of JPMorgan or Goldman Sachs. The firm's approach—partnering rather than building—may prove prescient or problematic.

Consolidation in the middle market seems inevitable, with regulatory costs and technology requirements creating scale imperatives. Jefferies could be acquirer or acquired, though the Leucadia structure provides protection from hostile approaches. Geographic expansion opportunities abound, particularly in Asia where Jefferies remains subscale relative to ambitions.

The next crisis—and there's always a next crisis—will test whether the lessons of 2008 and 2011 remain embedded in Jefferies' DNA. The firm's positioning, with moderate leverage and diversified funding, suggests readiness, but each crisis is different.

Culture ultimately wins in investment banking. Products commoditize, talent moves, but culture endures. "We are incredibly proud of our history and eternally grateful, not just for the 5,000 employee-partners that are with us today, but for all of those who did the heavy lifting all along the way to allow us to reach the enviable position in which we find ourselves today".

The unlikely survivor has become an unlikely champion. From Boyd Jefferies' telephone booth to Handler's emails with Fuld to the Leucadia merger, each chapter seemed improbable until it became inevitable. The next chapter remains unwritten, but if history is any guide, it will surprise everyone—except maybe those who've been paying attention all along.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube