IIFL Capital Services: From Research Startup to India's Capital Markets Powerhouse

I. Introduction & Episode Roadmap

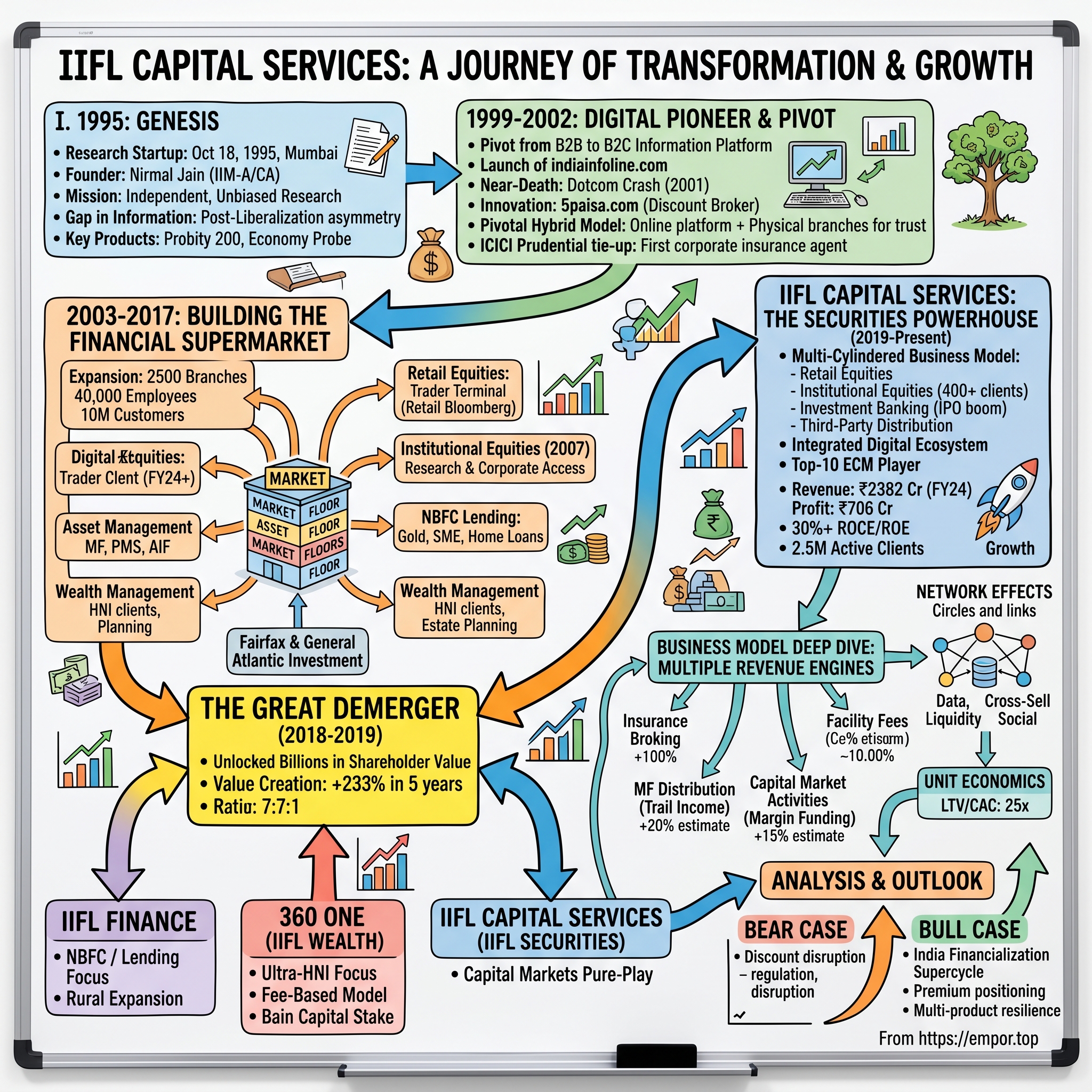

Picture this: October 18, 1995. The Indian economy is barely four years into liberalization. Foreign investors are still tiptoeing around the country's byzantine regulations. The Bombay Stock Exchange has just introduced electronic trading. And in a modest Mumbai office, a 28-year-old IIM Ahmedabad graduate named Nirmal Jain is launching what seems like an impossibly ambitious venture—an independent research firm that would dare to compete with the established financial houses of Dalal Street.

Fast forward to 2024. That startup, IIFL Capital Services, commands a market capitalization of ₹9,419 crores. It generates ₹2,382 crores in revenue and ₹706 crores in profit. More remarkably, it has survived and thrived through the dotcom bust, the 2008 financial crisis, demonetization, GST implementation, and a global pandemic. It has demerged twice, pivoted multiple times, and somehow emerged stronger each time.

How did a research boutique transform into one of India's largest independent capital markets players? The answer isn't just about riding India's growth story—though that certainly helped. It's about strategic pivots executed with surgical precision, near-death experiences that became catalysts for innovation, and perhaps most importantly, a demerger strategy that unlocked billions in shareholder value while most conglomerates were still trying to build empires.

This is the story of three transformations. First, how a research firm became a digital pioneer in Indian broking. Second, how a broker became a full-service financial supermarket. And third, how a conglomerate had the wisdom to split itself into focused entities—each now worth more than the original whole.

The journey from research reports to robo-advisory, from five employees to forty thousand, from serving corporates to serving ten million retail customers—this is what building in post-liberalization India really looks like. Not the sanitized version you read in business school case studies, but the messy, exhilarating, occasionally terrifying reality of creating a financial services empire in one of the world's most complex markets.

II. The Genesis: Nirmal Jain & India's Liberalization Story

The year 1995 wasn't just another year in India—it was Year Four of the country's economic awakening. Prime Minister P.V. Narasimha Rao and Finance Minister Manmohan Singh had unleashed forces that would transform a socialist economy into a capitalist powerhouse. Foreign institutional investors were pouring $2 billion annually into Indian markets. The BSE Sensex had jumped from 1,000 to 3,000 in just three years. And amid this chaos of opportunity, a young chartered accountant saw a gap that nobody else seemed to notice.

Nirmal Jain wasn't your typical entrepreneur. A 1986 Mumbai University graduate who'd topped his CA exams and then added an IIM Ahmedabad MBA for good measure, he could have walked into any corner office on Nariman Point. Instead, he chose the uncertainty of entrepreneurship at a time when "startup" wasn't even a word in the Indian business lexicon.

The insight was elegantly simple: India's liberalization had created an information asymmetry of epic proportions. Foreign investors desperately needed quality research on Indian companies. Indian corporates needed to understand their newly liberalized markets. Everyone was flying blind, making decisions worth millions based on gut feel and newspaper clippings.

On October 18, 1995, India Infoline was born—not as a broker or a wealth manager, but as an independent research house. The proposition was audacious: produce institutional-quality research that was unbiased, comprehensive, and actually useful. In a market where "research" often meant recycled press releases and where analysts were routinely pressured to write favorable reports, IIFL promised something revolutionary: the truth.

The early client list read like a who's who of Indian business. Hindustan Lever (now Hindustan Unilever) needed sectoral analysis. The Tata Group wanted competitive intelligence. CRISIL required specialized economic research. McKinsey was entering India and needed local insights. State Bank of India and Citibank sought credit research. These weren't small accounts—they were validation that IIFL's research had real value.

The company's flagship products became legendary in Mumbai's financial circles. "Probity 200" offered detailed analysis of India's top companies—not just financials, but management quality, competitive positioning, and growth prospects. "Economy Probe" dissected macroeconomic trends with a clarity that government reports couldn't match. Sector reports went deep into industries that foreign investors were just discovering—textiles, pharmaceuticals, software services.

But here's where the story gets interesting. By 1999, Jain realized that producing world-class research was only half the equation. The real challenge was distribution. You could write the best report in the world, but if only fifty people read it, what was the point? The internet was arriving in India, and with it, the possibility of reaching not hundreds but millions of potential customers.

The decision to go digital wasn't just about technology—it was about democratization. If information was power, then the internet could redistribute that power from the corridors of Nariman Point to every corner of India. A textile trader in Surat could access the same research as a fund manager in Mumbai. A retired government servant in Chennai could make investment decisions based on professional analysis, not tips from his broker.

This pivot from B2B research to B2C information platform would prove to be the first of many transformations. It would also nearly kill the company. But in 1999, as Jain and his team built their first website, they couldn't have imagined that they were laying the foundation for what would become one of India's most successful financial services companies. They were just trying to solve a simple problem: how do you get good information to people who need it?

The consulting-to-platform pivot that seemed so logical would soon collide with the harsh realities of the dotcom bubble. But that's a story for the next chapter—a story of how IIFL went from the brink of bankruptcy to becoming India's digital trading pioneer.

III. The Dotcom Revolution & Near-Death Experience (1999–2002)

In 1999, the internet was magic. At least, that's what investors believed. Yahoo's market cap exceeded that of Disney. Amazon was worth more than Sears. And in Mumbai, a four-year-old research firm was about to bet everything on pixels and bandwidth.

The launch of www.indiainfoline.com wasn't just a website—it was a declaration of war against the old guard of Indian finance. While established brokers still operated from crowded trading rings, shouting orders across chaotic floors, IIFL was building something that seemed like science fiction: a platform where anyone with a dial-up connection could access professional-grade financial information.

The timing seemed perfect. Commonwealth Development Corporation (CDC), the UK government's development finance institution, saw the potential immediately. They cut a check for $1 million—IIFL's first institutional funding. For context, this was serious money in 1999 India, where the average urban salary was ₹3,000 per month. It was validation that IIFL wasn't just another dotcom dreamer.

Then came the masterstroke that would define IIFL's future: 5paisa.com.

Launched in 2000, 5paisa wasn't just another online broker. It was a pricing revolution wrapped in a technology disruption. While traditional brokers charged 1-1.5% commission, 5paisa offered trades at 0.05%—a 95% discount that seemed economically suicidal. The name itself was brilliant marketing: 5 paisa (₹0.05) was less than the cost of a photocopy, positioning stock trading as something anyone could afford.

Intel Capital joined the party, adding more fuel to the rocket ship. International investors were mesmerized by the math: India had 300 million middle-class citizens, fewer than 10 million demat accounts, and internet penetration growing at 50% annually. The TAM (Total Addressable Market) calculations showed a trillion-dollar opportunity.

By early 2001, IIFL was burning cash building India's most sophisticated retail trading platform. They called it "Trader Terminal"—a Bloomberg for the masses. Three years of development, hundreds of features, real-time data feeds, advanced charting, portfolio analytics. It was beautiful, powerful, and launching just in time for the apocalypse.

March 2001. The NASDAQ crashed 78% from its peak. In India, the dotcom graveyard filled with names like Bazee.com, Firstandsecond.com, and dozens of others. Funding evaporated overnight. The same investors who'd thrown money at anything with ".com" in its name now wouldn't return phone calls.

IIFL's burn rate was ₹2 crores per month. The bank account showed three months of runway. The board meetings turned grim. Should they shut down the online business and return to research? Could they raise emergency funding? Would anyone even buy the company?

Here's where Nirmal Jain pulled off one of the great pivots in Indian business history. Instead of retreating to pure digital or pure offline, he chose both. The insight: India wasn't ready for pure-play online broking, but it desperately needed better financial products distribution.

The strategic tie-up with ICICI Prudential in 2001 was genius hiding in desperation. IIFL became India's first corporate agent for life insurance—a license to print money in a country where insurance penetration was below 2%. Suddenly, those expensive branch offices weren't cost centers; they were distribution goldmines. The same relationship managers who explained online trading could now sell insurance, mutual funds, and fixed deposits.

The numbers tell the story. Insurance commission: 15-35% in year one. Mutual fund distribution: 1-2% upfront. Corporate FD distribution: 0.25-0.5%. Stack enough of these products, multiply by thousands of customers, and suddenly you have a sustainable business model.

By 2002, IIFL had survived what killed most of its peers. The company that nearly died from being too early to digital had discovered something profound: in India, the future wasn't digital or physical—it was both. Technology would be the enabler, but trust would be built through human relationships. Products would be sophisticated, but distribution would be everywhere.

This hybrid model—high-tech platform meets high-touch service—would become IIFL's signature. It wasn't sexy. It wouldn't win Silicon Valley pitch competitions. But it would build one of India's most successful financial services companies.

The dotcom crash had taught IIFL a lesson that would guide every decision thereafter: in India, you don't disrupt incumbents by being radically different. You win by being radically better at what customers actually need. And what they needed wasn't just low prices or fancy technology—they needed someone to hold their hand through India's bewildering financial maze.

IV. Building the Financial Supermarket (2003–2017)

The year 2003 marked a turning point. The dotcom hangover was lifting. India's GDP growth hit 8%. And IIFL, having survived its near-death experience, was about to embark on one of the most aggressive expansion phases in Indian financial services history.

The Trader Terminal, three years in the making, finally launched to widespread acclaim. This wasn't just another trading platform—it was a retail investor's own Bloomberg terminal. Real-time quotes, advanced charting, news feeds, fundamental data, technical indicators—all in one interface that actually worked on India's creaky internet infrastructure. While competitors offered basic buy-sell functionality, IIFL gave retail traders tools that were previously exclusive to institutions.

But the real masterstroke was the "financial supermarket" strategy. Rather than competing in one vertical, IIFL would offer everything a customer might need across their financial lifecycle. Young professional? Start with a demat account and term insurance. Growing family? Add mutual funds and a home loan. Approaching retirement? Wealth management and estate planning. The same customer who traded stocks could get a loan against shares, buy insurance, invest in mutual funds, and eventually graduate to portfolio management services.

The expansion was breathtaking in scope. From a handful of offices in 2003, IIFL grew to 2,500 branches across India by 2017. The employee count exploded from under 100 to over 40,000. Customer base: 10 million and counting. This wasn't organic growth—this was a land grab of epic proportions.

The institutional equities breakthrough came in 2007. After years of being dismissed as a "retail shop," IIFL finally cracked the code to serving foreign institutional investors. The key? Leveraging their deep research heritage while adding a crucial ingredient: corporate access. IIFL could arrange meetings between fund managers and Indian CEOs that competitors couldn't. Their analysts didn't just crunch numbers; they had relationships built over a decade of covering these companies.

Smart money noticed. Prem Watsa's Fairfax Financial, the "Warren Buffett of Canada," took a strategic stake. General Atlantic, the growth equity powerhouse, invested $100 million. CDC returned with more capital. These weren't just financial investors—they were validation that IIFL had graduated to the big leagues.

The 2008 financial crisis should have been devastating. Lehman Brothers collapsed. Bear Stearns disappeared. Indian markets crashed 60%. But IIFL didn't just survive—it thrived. While pure-play brokers struggled with plummeting volumes, IIFL's diversified model provided stability. Insurance commissions kept flowing. Loan books, though stressed, didn't collapse. The financial supermarket model had proven its resilience.

Technology investments accelerated post-crisis. While competitors viewed tech as a cost center, IIFL saw it as the ultimate differentiator. They built one of India's first mobile trading apps—primitive by today's standards but revolutionary in 2010. They invested in data analytics before "big data" became a buzzword. They automated backend processes while competitors still pushed paper.

The NBFC (Non-Banking Financial Company) expansion was particularly clever. Rather than competing with banks for vanilla home loans, IIFL focused on underserved segments. Loans against property for SME owners. Gold loans for rural customers. Microfinance for the unbanked. Each product targeted a specific niche where traditional banks were absent or inefficient.

By 2015, IIFL had achieved something remarkable: it was simultaneously a discount broker and a full-service provider, a technology company and a branch network, serving day traders and ultra-HNIs (High Net Worth Individuals). The numbers validated the strategy:

- Revenue CAGR (2003-2017): 45%

- Customer base growth: 100x

- Branch network: 2,500 across 500 cities

- Products offered: 25+ across asset classes

The wealth management division deserves special mention. While everyone chased retail broking volumes, IIFL quietly built relationships with India's wealthy. By 2017, they managed over ₹1 lakh crore in assets—not just executing trades but providing estate planning, tax advisory, and alternative investments. The economics were beautiful: 1-2% annual management fees on sticky, high-value relationships.

But success bred complexity. By 2017, IIFL was trying to be everything to everyone. The same brand served day traders and ultra-wealthy families. The same management oversaw lending and capital markets. The same balance sheet funded mortgages and margin trading. Something had to give.

The board meetings in late 2017 were intense. Should they continue as a conglomerate? Should they sell some divisions? Or was there a third way—a structural solution that could unlock value while preserving the businesses they'd built?

The answer would be one of the boldest corporate actions in Indian financial services: a three-way demerger that would create focused entities, each with its own strategy, management, and investor base. It would be complex, risky, and potentially transformative.

V. The Great Demerger: Strategic Masterstroke (2018–2019)

In the history of Indian corporate actions, few match the audacity of IIFL's 2018 demerger announcement. While conglomerates from Tata to Reliance preached the gospel of synergy, IIFL chose radical surgery: split the company into three distinct entities, each with its own focus, capital structure, and destiny.

The logic was hidden in plain sight. IIFL Finance, the lending business, needed steady capital and conservative investors. IIFL Wealth, serving India's ultra-rich, needed premium valuations and patient capital. IIFL Securities, the capital markets business, needed agility and risk capital. Housing them under one roof was like forcing a marathon runner, a weightlifter, and a gymnast to train together—possible, but profoundly suboptimal.

The demerger ratio was elegantly simple: every seven shares of IIFL Holdings would convert to seven shares each of IIFL Finance and IIFL Securities, plus one share of IIFL Wealth. No cash changed hands. No investor was forced to choose. Everyone got a piece of each business, then could decide what to keep or sell.

The NCLT (National Company Law Tribunal) approval on March 7, 2019, came after months of legal gymnastics. Indian regulations weren't designed for three-way demergers. There were tax implications, regulatory approvals across multiple agencies, and the complexity of separating shared services that had been integrated for years.

But the real challenge was cultural. Employees who'd joined "IIFL" suddenly had to choose between three companies. The wealth management rainmakers didn't want to be associated with microfinance. The investment bankers didn't want to be confused with retail brokers. The lending team wanted their own credit rating, separate from the volatility of capital markets.

The market's initial reaction was confused. The combined market cap immediately post-demerger was actually lower than the pre-demerger value—a classic conglomerate discount in reverse. Analysts struggled to value three entities where there had been one. Some investors, forced to hold three stocks instead of one, simply sold everything.

Then something magical happened. Each business, freed from the constraints of the others, began to flourish:

IIFL Finance could finally pursue aggressive lending growth without worrying about capital markets volatility. They raised dedicated debt, partnered with international development finance institutions, and expanded into rural markets. The stock re-rated from a conglomerate discount to a pure-play NBFC multiple.

IIFL Wealth underwent the most dramatic transformation. Rebranded as 360 ONE (though still legally IIFL Wealth), it positioned itself as India's largest non-bank wealth manager. The client list read like India's Forbes list. The business model—2% annual fees on ₹3 lakh crore of assets—was a money-printing machine. When Bain Capital took a 25% stake at a ₹25,000 crore valuation in 2022, it validated the demerger thesis spectacularly.

IIFL Securities (now IIFL Capital Services) could finally embrace its identity as a capital markets pure-play. No longer worried about lending regulations or wealth management conflicts, they could pursue aggressive broking strategies, launch new products, and invest in technology without committee approvals from unrelated divisions.

The numbers tell the story: - Pre-demerger market cap (2019): ~₹12,000 crore - Combined market cap (2024): ~₹40,000 crore - Value creation: 233% in five years

The demerger wasn't just financial engineering—it was strategic clarity. Each entity could now: - Raise optimal capital (debt for lending, equity for wealth, hybrid for securities) - Attract specialized talent (credit officers vs. relationship managers vs. traders) - Pursue focused M&A (buying loan books vs. wealth portfolios vs. broking firms) - Build distinct cultures (risk management vs. client service vs. innovation)

For Nirmal Jain, who remained involved with all three entities, it was vindication of a profound insight: in India's specialized financial markets, focused execution beats diversified stability. The financial supermarket had served its purpose—building scale, relationships, and capabilities. But the future belonged to specialists.

The demerger also solved a succession challenge. Rather than one CEO trying to manage everything, each business got leadership suited to its needs. The lending business got a credit specialist. The wealth business got a relationship master. The securities business got a technology visionary.

By late 2019, as the three entities settled into their new identities, the transformation was complete. The company that started as a research boutique, became a dotcom pioneer, survived as a financial supermarket, had now evolved into three focused champions. Each was stronger alone than they'd been together.

VI. IIFL Capital Services Reborn: The Securities Powerhouse (2019–Present)

November 2024. The news was symbolic but significant: IIFL Securities Limited officially became IIFL Capital Services Limited. It wasn't just a name change—it was a declaration of ambition. No longer just a broker, but a full-stack capital markets powerhouse.

Post-demerger, IIFL Capital Services faced an existential question: In the age of Zerodha and zero brokerage, what's the role of a full-service broker? The answer they crafted was sophisticated: don't compete on price, compete on value. Don't chase day traders, serve serious investors. Don't just execute trades, enable wealth creation.

The business model that emerged was multi-cylindered:

Retail Equities: Yes, they still served 5 million retail clients. But instead of racing to zero on brokerage, they focused on value-added services. The flagship "Trader Terminal" evolved into "Trader Workstation"—a platform that could compete with international standards. Research reports, previously reserved for institutions, were packaged for retail consumption. The "Markets" app didn't just execute trades; it provided portfolio analytics, tax optimization, and goal-based investing.

Institutional Equities: This became the crown jewel. Serving 400+ institutional clients including the who's who of global finance—sovereign funds, pension funds, mutual funds, hedge funds. The offering went beyond execution. IIFL provided research coverage on 200+ companies, arranged 3,000+ corporate meetings annually, and hosted investor conferences that became must-attend events. The economics were attractive: institutional brokerage rates of 10-15 basis points, sticky relationships, and high-margin ancillary services.

Investment Banking: From almost nothing in 2010, IIFL had become a top-10 player in Indian ECM (Equity Capital Markets). They'd managed IPOs for new-age companies, QIPs for established corporates, and complex restructurings for stressed assets. The 2021-2024 IPO boom was a bonanza—IIFL was involved in transactions worth ₹50,000+ crore. Investment banking fees—typically 1-3% of deal value—dropped straight to the bottom line.

Third-Party Distribution: The unsung hero of the business model. Distributing mutual funds (₹50,000 crore AUM), insurance (₹5,000 crore annual premium), bonds, PMS, AIFs—all generating steady, predictable fees. Trail commissions from mutual funds alone generated ₹400+ crore annually. No balance sheet risk, no capital requirements, just pure fee income.

The financial performance validated the strategy: - Revenue (FY24): ₹2,382 crore - Profit (FY24): ₹706 crore - 5-year profit CAGR: 36.0% - ROCE: 34.6% - ROE: 33.2%

These aren't just good numbers—they're exceptional for a capital markets business. The 30%+ returns on capital place IIFL among the most efficient financial services companies globally.

The technology transformation accelerated post-demerger. Free from legacy constraints, IIFL rebuilt its tech stack from scratch: - Cloud-native architecture for scalability - AI-powered research tools for analysts - Algorithmic trading capabilities for institutions - Robo-advisory for mass affluent clients - Blockchain experiments for settlement efficiency

But the masterstroke was the integrated platform. A client could: 1. Research stocks using institutional-grade analysis 2. Execute trades through multiple channels 3. Pledge shares for margin funding 4. Invest surplus in mutual funds 5. Track everything through a unified dashboard

The competitive moat wasn't any single feature—it was the ecosystem. Switching costs weren't just financial; they were behavioral. Clients had years of data, saved watchlists, customized alerts, and established relationships with relationship managers.

The recent performance has been stellar. In FY24 alone: - Average daily turnover: ₹75,000+ crore - Active clients: 2.5 million - Mobile app downloads: 10 million+ - Research reports published: 5,000+ - Corporate access meetings: 3,000+

The transformation from IIFL Securities to IIFL Capital Services represents more than semantic evolution. It's a recognition that in India's financializing economy, the opportunity isn't just in broking—it's in becoming the investment bank for India's growth story. Every startup IPO, every corporate fundraise, every wealth creation journey—IIFL wants a piece of that action.

VII. Business Model Deep Dive: Multiple Revenue Engines

To understand IIFL Capital Services, you need to understand a fundamental truth about Indian financial services: the money isn't where you think it is. While everyone obsesses over broking volumes and races to zero on pricing, the real profits hide in adjacent services that clients don't price-shop.

Let's dissect the four-cylinder engine that powers IIFL's economics:

Capital Market Activities (65% of revenue) This isn't just broking—it's an ecosystem play. Yes, retail broking contributes, but at 10-20 basis points (vs. 3-5 basis points for discount brokers), IIFL extracts premium pricing for premium service. The institutional broking business operates at even better economics—15-20 basis points for foreign institutions who value research and corporate access over raw execution.

The real genius is in the auxiliary services. Margin funding at 12-14% interest rates. Securities lending and borrowing for arbitrageurs. Depository services charging annual fees on assets held. Each client who comes for trading stays for five other services.

Investment banking is the highest-margin business within this segment. A single IPO can generate ₹20-50 crore in fees. A QIP might yield ₹10-20 crore. An M&A advisory mandate could be worth ₹30-100 crore. With virtually no capital employed, these fees flow straight to profit.

Insurance Broking (15% of revenue) This is the definition of a toll booth business. IIFL doesn't underwrite risk or hold capital. They simply connect insurance companies with customers and collect 15-35% of first-year premiums as commission. A ₹10 lakh term insurance policy yields ₹35,000 in commission. A ₹1 crore ULIP might generate ₹5 lakh.

The beauty is in the renewal trail. Even after year one, IIFL continues collecting 5-10% annually for policies that renew automatically. It's the closest thing to recurring revenue in financial services.

Third-Party Distribution (15% of revenue) Mutual funds are the gift that keeps giving. Upfront commission of 1% on equity funds, then trail commission of 0.5-1% annually for as long as the client holds. With ₹50,000 crore in mutual fund AUM, that's ₹250-500 crore in annual trail commission—pure profit with zero risk.

Fixed deposits, bonds, and NCDs add another layer. Corporate FDs pay 0.25-0.5% for distribution. Bonds might pay 0.5-1%. Small percentages, but on large volumes with no credit risk to IIFL.

Facility & Ancillary Services (5% of revenue) The forgotten revenue streams that add up: account opening fees, demat charges, transaction charges, SMS alerts, research subscriptions, data feeds. None significant individually, but collectively contributing ₹100+ crore to the top line with 80%+ margins.

The Network Effects

Here's what most analysts miss: IIFL's business model exhibits powerful network effects unusual for traditional financial services:

- Data Network Effects: Every transaction generates data that improves research, risk management, and product development

- Cross-Sell Network Effects: Each product sold makes the next sale easier and cheaper

- Liquidity Network Effects: More clients mean better price discovery and execution

- Social Network Effects: HNI clients refer other HNIs; institutional clients validate retail offerings

Unit Economics Deep Dive

Let's follow a typical customer journey: - Year 1: Opens demat account (₹500 revenue), trades actively (₹5,000 broking), takes margin funding (₹3,000 interest) - Year 2: Buys term insurance (₹10,000 commission), starts SIP in mutual funds (₹2,000 initial + trail) - Year 3: Takes loan against securities (₹5,000 interest), subscribes to research (₹1,000) - Year 5: Becomes PMS client (₹20,000 annual fees), refers two friends (₹10,000 indirect value)

Customer acquisition cost: ₹2,000 Lifetime value: ₹50,000+ LTV/CAC ratio: 25x

These unit economics explain why IIFL can afford 40,000 employees and 2,500 branches while discount brokers operate with skeleton crews. Every relationship manager who converts one HNI client pays for themselves for years.

Technology as Margin Expander

While technology is often viewed as a cost center, at IIFL it's a margin expander: - Automated research reports reduce analyst costs by 60% - Algorithmic trading reduces execution costs by 40% - Digital onboarding reduces acquisition costs by 70% - AI-powered customer service reduces support costs by 50%

The result: operating leverage that shows up in the numbers. Revenue per employee has grown from ₹15 lakh to ₹60 lakh over the past decade, even as employee costs have risen only marginally.

VIII. Competition & Market Dynamics

The Indian broking industry in 2024 is a fascinating study in contrasts. On one side, discount brokers like Zerodha have commoditized basic trading, driving revenues to zero and forcing a race to the bottom. On the other, premium players like IIFL Capital Services have moved upmarket, offering services that justify fees 10x higher than discounters. It's a barbell market with nothing in the middle—you're either free or full-service.

The Discount Disruption

Zerodha's rise is the stuff of Silicon Valley dreams, except it happened in Bangalore. Zero brokerage on equity delivery, ₹20 flat on intraday trades, no branches, no relationship managers, just pure technology. They now have 13 million clients and generate ₹8,000 crore in revenue with just 1,200 employees. That's ₹6.6 crore revenue per employee versus IIFL's ₹0.6 crore.

Groww and Upstox followed the playbook, adding their own twists. Groww started with mutual funds and moved to broking. Upstox targeted the derivatives traders. Angel One went mass market with aggressive digital marketing. The message was consistent: why pay for something you can get free?

IIFL's Differentiation Strategy

IIFL's response wasn't to match prices—it was to change the game entirely. While discounters competed on price, IIFL competed on value:

- Research Advantage: Publishing 5,000+ research reports annually when Zerodha publishes zero

- Relationship Management: Dedicated RMs for HNI clients versus pure self-service models

- Product Suite: 25+ financial products versus 3-4 for discounters

- Physical Presence: 2,500 branches for complex transactions and trust-building

- Institutional Capability: Serving global funds that discounters can't even onboard

The strategy is working. While IIFL has "only" 2.5 million active clients versus Zerodha's 13 million, IIFL's revenue per client is 5x higher. More importantly, IIFL clients are sticky—the churn rate is under 10% annually versus 25-30% for discount brokers.

Traditional Competitors

The old guard—ICICI Securities, HDFC Securities, Kotak Securities—face their own challenges. Tied to parent banks, they lack IIFL's independence and agility. Their cost structures, burdened by banking overheads, can't match IIFL's efficiency. Most importantly, they're conflicted—pushing parent bank products rather than best-in-class solutions.

ICICI Securities, despite having ICICI Bank's 100 million customers to cross-sell, generates lower returns on capital than IIFL. HDFC Securities, part of India's largest private bank, has struggled to differentiate beyond the parent brand. Kotak Securities maintains premium positioning but lacks IIFL's multi-product ecosystem.

The Wealth Management Battlefield

In wealth management, IIFL competes with private banks (Kotak, ICICI, HDFC), foreign banks (Citi, Standard Chartered), and independent wealth managers (Anand Rathi, Centrum). Each has strengths: - Private banks leverage existing relationships - Foreign banks bring global expertise - Independents offer personalized service

IIFL's edge? The combination of independence (no proprietary products to push), scale (₹3 lakh crore AUM), and track record (30 years of trust). When IIFL Wealth demerged and became 360 ONE, it instantly became India's largest non-bank wealth manager—validation that focused strategy beats diversified presence.

Regulatory Dynamics

SEBI (Securities and Exchange Board of India) has been both catalyst and constraint. Recent regulations have: - Capped mutual fund commissions, hurting distribution revenues - Mandated higher margins for derivatives, reducing leverage - Introduced peak margin rules, impacting intraday volumes - Required segregation of client assets, increasing operational costs

But regulation also creates barriers to entry. New brokers need significant capital, compliance infrastructure, and operational capability that wasn't required a decade ago. IIFL's scale allows it to absorb regulatory costs that would cripple smaller players.

Market Structure Evolution

India's capital markets are undergoing structural transformation: - Retail participation exploding: 150 million demat accounts by 2024 vs. 40 million in 2020 - Derivatives dominating volumes: 99% of NSE volume is F&O - Financialization accelerating: Household savings shifting from gold/real estate to financial assets - Digital adoption mainstream: 80% of trades now on mobile apps

IIFL is positioned to benefit from each trend. More retail participants need education and guidance. Derivatives traders need sophisticated tools. Financialization creates demand for diverse products. Digital adoption reduces costs while maintaining premium pricing for value-added services.

The Competitive Moat

IIFL's moat isn't any single advantage—it's the combination that's hard to replicate: - Trust: 30-year track record that startups can't match - Relationships: 10 million customer relationships built over decades - Technology: ₹500 crore invested in platforms that work at scale - Licenses: Banking, insurance, mutual fund—permissions that take years to obtain - Network: 2,500 branches that provide physical comfort in a digital world - Brand: "IIFL" recognition that transcends financial services

The result is a competitive position that's resilient against both traditional and digital threats. Discount brokers can't match the service. Traditional brokers can't match the technology. New entrants can't match the trust. It's a sweet spot that explains those 30%+ returns on capital.

IX. Playbook: Business & Investing Lessons

Every successful company teaches lessons, but IIFL's journey offers a masterclass in building financial services in emerging markets. These aren't MBA case study theories—these are battle-tested strategies that created billions in value.

Lesson 1: The Art of the Pivot

IIFL didn't just pivot once—they mastered serial transformation: - 1995-1999: Research firm to information portal - 2000-2002: Portal to online broker - 2003-2017: Broker to financial supermarket - 2018-2019: Conglomerate to focused entities

Each pivot wasn't desperation—it was strategic evolution. The key insight: don't abandon what works, layer new capabilities on existing strengths. The research DNA from 1995 still drives institutional equities in 2024. The branches built for insurance distribution now anchor wealth management. Nothing was wasted; everything was repurposed.

Lesson 2: Surviving Crisis as Strategy

IIFL didn't just survive multiple crises—they used them as catalysts: - Dotcom bust (2001): Forced hybrid online-offline model that became their signature - Financial crisis (2008): Diversification into lending when capital markets froze - Demonetization (2016): Accelerated digital adoption when cash disappeared - COVID-19 (2020): Proved resilience of multi-cylinder model when markets went haywire

The pattern is consistent: when crisis hits, don't just hunker down—reimagine the business. Every crisis creates opportunities for those willing to adapt. IIFL's crisis playbook: preserve capital, cut costs surgically (not indiscriminately), and position for the recovery before it's obvious.

Lesson 3: The Demerger Algorithm

The 2019 demerger provides a template for value creation through simplification:

When to demerge: - Business units have divergent capital needs - Customer segments have conflicting requirements - Regulatory regimes create operational complexity - Management attention is spread too thin - Market values the sum less than the parts

How to execute: - Ensure each entity is independently viable - Give shareholders proportional ownership (no forced choices) - Separate cleanly—shared services create ongoing friction - Communicate relentlessly—confusion destroys value - Move fast—prolonged uncertainty hurts all businesses

The proof is in the 233% value creation post-demerger. Sometimes the best growth strategy is division, not addition.

Lesson 4: Building in Emerging Markets

IIFL's success formula for emerging markets is replicable:

Distribution + Technology, not Distribution or Technology: Pure digital works in developed markets with high trust and literacy. Pure physical is too expensive to scale. The hybrid model—technology for efficiency, humans for trust—is the sweet spot in emerging markets.

Serve the Ecosystem, not just the Transaction: Don't just execute trades—provide research, education, credit, insurance, planning. The profit isn't in the core service; it's in the adjacent offerings that customers discover after they trust you.

Premium Pricing for Premium Segments: Let discounters fight over price-sensitive customers. Focus on segments that value service over savings. IIFL's HNI clients pay 10x more than discount broker clients and stay 3x longer.

Lesson 5: Capital Allocation in Multi-Business Models

Running multiple businesses requires disciplined capital allocation: - Broking: Asset-light, working capital only, ROE target >25% - Investment Banking: Human capital intensive, bonus-driven, episodic revenues - Distribution: Zero capital, pure fee income, scale through technology - Lending: Capital hungry, regulatory constraints, ROE ceiling ~15%

IIFL's insight: allocate capital based on marginal returns, not historical performance. When lending ROEs dropped below 15%, they demerged it. When wealth management needed growth capital, they raised dedicated funding. Dynamic allocation beats static optimization.

Lesson 6: Managing Regulatory Complexity

Financial services means regulatory complexity. IIFL's approach: 1. Embrace, don't resist: First to comply, even if it hurts short-term 2. Turn compliance into competitive advantage: Higher standards keep out weak competitors 3. Maintain regulatory surplus: Always exceed minimum requirements 4. Engage proactively: Shape regulations through industry associations 5. Diversify regulatory risk: Multiple licenses across entities reduce concentration risk

The result: while competitors fought regulations, IIFL used them as competitive moats.

Lesson 7: Network Effects in Traditional Industries

Financial services isn't supposed to have network effects—but IIFL created them: - Data Network: Every transaction improves risk models and product design - Product Network: Each product sold reduces cost of selling the next - Trust Network: Every successful client interaction builds reputational capital - Partner Network: Relationships with product manufacturers create exclusive opportunities

The lesson: network effects aren't limited to technology platforms. Any business with recurring customer interactions can build compounding advantages.

Lesson 8: The Talent Equation

In financial services, talent is everything. IIFL's approach: - Pay for performance: Top performers earn multiples of average - Promote from within: 80% of senior management grew internally - Invest in training: IIFL University for continuous education - Align incentives: ESOPs worth ₹1,000+ crore distributed to employees - Separate cultures: Each business has distinct talent strategies

The result: IIFL alumni have founded dozen successful financial services companies—the ultimate validation of talent development.

X. Analysis & Future Outlook

The investment case for IIFL Capital Services hinges on a fundamental question: In an era of zero-commission broking and robo-advisors, what's the value of a full-service financial intermediary? The answer isn't simple, and both bulls and bears have compelling arguments.

The Bear Case: Structural Headwinds

The pessimists point to undeniable trends. Discount brokers are eating market share with every passing quarter. Zerodha added more clients in 2023 than IIFL has accumulated in 30 years. The math is brutal: if broking goes to zero, how do you sustain 40,000 employees and 2,500 branches?

Regulatory pressure continues mounting. SEBI's true-to-label circular threatens mutual fund distribution revenues. The derivatives margin requirements have killed intraday trading volumes. Every year brings new compliance costs that discount brokers, with their lean structures, absorb more easily.

Technology disruption accelerates. ChatGPT can now provide investment advice. Robo-advisors manage portfolios for 0.25% annually. Blockchain threatens traditional settlement. Cryptocurrency offers an alternative financial system. Where does a traditional broker fit in this future?

Margin compression seems inevitable. Institutional brokerage rates have fallen from 25 basis points to 15 in five years. Mutual fund commissions are capped and falling. Insurance regulations are tightening. Even investment banking, the crown jewel, faces pressure as companies explore direct listings and alternative fundraising.

Competition intensifies from unexpected quarters. Banks are getting serious about capital markets. Technology companies are embedding financial services. Even Zerodha, the discount champion, is moving upmarket with advisory services. IIFL's comfortable position between discount and premium is getting squeezed from both sides.

The Bull Case: India's Financialization Supercycle

The optimists see a different movie. India's capital markets are where America's were in the 1980s—early stages of a multi-decade boom. Consider the numbers: - 150 million demat accounts today, potentially 500 million by 2030 - Household savings in financial assets: 7% today vs. 30% in developed markets - Mutual fund penetration: 15% of households vs. 50%+ potential - Insurance penetration: 3% vs. 8-10% in peer economies

IIFL isn't just participating in this boom—they're enabling it. Every new investor needs education. Every growing portfolio needs diversification. Every wealth creator needs estate planning. The TAM isn't shrinking; it's exploding.

The premium positioning becomes more valuable, not less, as wealth grows. India is creating millionaires at an unprecedented pace—70,000 new millionaires annually. These aren't Zerodha's price-sensitive traders; they're IIFL's ideal clients who value relationships, need complex solutions, and pay for quality.

Digital transformation, rather than threat, is opportunity. IIFL's technology investments allow them to serve premium clients at mass-market scale. AI doesn't replace relationship managers; it makes them superhuman. Automation doesn't eliminate branches; it makes them more productive.

The multi-product model provides resilience that pure-plays lack. When broking revenues fall, insurance commissions rise. When markets crash, gold loans boom. When regulations tighten in one area, opportunities open in another. It's portfolio theory applied to business models.

Current Valuation: The Market's Verdict

At ₹9,419 crore market cap, IIFL Capital Services trades at: - P/E: 14.0x (vs. 25x for Zerodha's implied valuation) - P/B: 4.0x (vs. 2x for traditional banks) - EV/Revenue: 4.0x (vs. 10x+ for global capital markets leaders)

The valuation suggests skepticism—the market prices IIFL like a melting ice cube, not a growth story. This creates opportunity if you believe the bull case, or validates caution if you're in the bear camp.

Digital Transformation Roadmap

IIFL's digital strategy isn't about competing with Zerodha—it's about building "Goldman Sachs for India's mass affluent." The roadmap includes: - AI-Powered Advisory: Personalized recommendations at scale - API Banking: Embedding IIFL services in third-party apps - Blockchain Settlement: Reducing costs and risks in securities settlement - Digital Assets: Preparing for crypto/tokenization when regulations allow - Meta Platform: Virtual branches in the metaverse for next-gen investors

The investment—₹500 crore over three years—is significant but necessary. The question is whether they can transform fast enough to stay relevant.

International Expansion Potential

IIFL's international ambitions remain largely unrealized. Despite operations in Singapore, Dubai, and New York, international contributes less than 5% of revenues. The opportunity is massive: - 30 million NRIs globally with $600 billion in wealth - Indian companies raising $50 billion annually overseas - Global investors allocating $100 billion to India

The challenge is execution. International expansion in financial services is notoriously difficult. Regulations differ. Competition is fierce. Brand recognition is limited. But if IIFL can crack the code, it's a multi-billion dollar opportunity.

The Next Decade: Three Scenarios

Scenario 1: The Gradual Decline (30% probability) Discount brokers continue gaining share. Regulations continue tightening. IIFL becomes a niche player serving a shrinking base of traditional investors. The stock re-rates to 8-10x P/E, implying 40% downside.

Scenario 2: The Steady State (50% probability) IIFL successfully defends its premium positioning. Growth slows but remains positive. Margins compress but stay healthy. The business generates steady cash flows, paying rising dividends. The stock trades sideways, delivering returns through dividends.

Scenario 3: The Transformation (20% probability) Digital transformation succeeds spectacularly. IIFL becomes India's Charles Schwab—combining technology leadership with human touch. International expansion works. New businesses (crypto, private markets) boom. The stock re-rates to 25x P/E, implying 100%+ upside.

The future isn't predetermined. It depends on execution, regulation, competition, and luck. But one thing is certain: IIFL's next chapter will be as dramatic as its first 30 years.

XI. Epilogue & Key Takeaways

Standing back from the details, IIFL Capital Services' journey from a five-person research startup to a ₹10,000 crore market cap financial services leader isn't just a business success story—it's a template for building in complex, regulated, emerging markets.

The company that Nirmal Jain founded in 1995 has survived and thrived through India's most tumultuous economic period: liberalization, multiple market crashes, regulatory overhauls, technological disruption, and a global pandemic. That's not luck—that's adaptability elevated to art form.

For Founders: The Pivot Paradox

IIFL's story teaches a counterintuitive lesson about pivots. The popular narrative celebrates dramatic pivots—Twitter starting as a podcasting platform, Instagram as a check-in app. But IIFL's pivots were different. They never abandoned their core; they expanded from it. Research became the foundation for broking. Broking became the gateway to distribution. Distribution became the platform for lending. Each new business was built on the trust and capabilities of the previous one.

The lesson: successful pivots aren't about starting over—they're about evolving. Your current business isn't a failure to be abandoned; it's a foundation to be built upon. The customers you serve today are the gateway to the customers you'll serve tomorrow.

For Investors: Beyond the Numbers

The financial metrics tell only part of the story. Yes, 36% profit CAGR and 33% ROE are exceptional. But the real story is in the intangibles: - Trust accumulated over 30 years: You can't buy this, only earn it - Relationships at every level: From retail traders to sovereign funds - Regulatory knowledge: Understanding not just rules but regulators - Cultural DNA: A research mindset that permeates everything - Founder involvement: Nirmal Jain still actively engaged after three decades

These intangibles don't show up in financial statements but drive long-term value creation. When evaluating IIFL or any financial services company, the question isn't just "what are the numbers?" but "what creates those numbers?"

The India Opportunity: Demographics, Digitization, and Democratization

IIFL's next decade will be shaped by three massive tailwinds:

Demographics: India adds 10 million people to its workforce annually. The median age is 28. The middle class is exploding. This isn't abstract—it's millions of new investors, insurance buyers, loan takers, wealth creators.

Digitization: India's digital public infrastructure—UPI, Aadhaar, GST—has created the world's most advanced digital economy. IIFL can now onboard a customer in minutes, not days. Serve them for rupees, not hundreds. Scale to millions, not thousands.

Democratization: Financial services are no longer elite preserves. A farmer in Bihar can access the same mutual funds as a CEO in Mumbai. A small trader in Gujarat can get the same research as a fund manager in Singapore. IIFL is both enabler and beneficiary of this democratization.

Building in Complex Regulated Markets

Perhaps IIFL's greatest lesson is how to build in markets where the rules keep changing, regulators are powerful, and compliance is expensive. Their playbook: 1. Treat regulation as moat, not burden: Higher standards keep out weak competitors 2. Diversify regulatory risk: Multiple licenses across entities 3. Stay ahead of requirements: Exceed minimums to build regulatory capital 4. Engage constructively: Shape rules through participation, not opposition 5. Build compliance into culture: Not a department but a mindset

This approach is why IIFL has thrived while hundreds of brokers have shut down. In regulated industries, the winners aren't those who resist regulation but those who master it.

The Demerger Template

The 2019 demerger should be studied by every conglomerate. The courage to split a successful company into three parts, the execution through complex regulations, the value creation post-split—it's a masterclass in corporate strategy.

The key insight: conglomerates destroy value when business units have:

- Different capital needs

- Different customer segments

- Different risk profiles

- Different growth trajectories

- Different talent requirements

The solution isn't to manage harder—it's to separate smarter. Give each business freedom to pursue its destiny. Let investors choose their exposure. Allow management to focus. The 233% value creation post-demerger validates this approach spectacularly.

What IIFL Teaches About Platform Building

In an era obsessed with platforms, IIFL built one without calling it that. They aggregated customers, products, and services into an ecosystem that exhibits network effects, scales economically, and resists disruption. The platform principles: - Start with a wedge (research), expand to adjacencies (broking, distribution) - Own the customer relationship, partner for products - Build switching costs through data, relationships, and convenience - Extract value from the ecosystem, not just transactions

This isn't the asset-light, pure-technology platform of Silicon Valley dreams. It's a capital-intensive, regulation-heavy, human-dependent platform. But it works—generating 30%+ returns on capital in a business others consider commoditized.

The Next 30 Years

As IIFL Capital Services approaches its fourth decade, the challenges are clear. Discount brokers aren't going away. Regulations will tighten further. Technology will continue disrupting. International players will enter India. The easy growth is behind them.

But so are the opportunities. India's capital markets are still nascent. Wealth creation is accelerating. Financial literacy is improving. Technology enables services previously impossible. The companies going public in the next decade will dwarf those of the past.

IIFL's success won't come from defending the past but from inventing the future. Can they become the trusted advisor for India's new wealthy? Can they democratize institutional-quality services? Can they bridge physical and digital, traditional and crypto, domestic and global?

The answer will determine whether IIFL Capital Services is a chronicle of India's past or a architect of its future. Either way, it's been one hell of a ride. And the best chapters might still be unwritten.

The Final Word

From a research startup in 1995 to three listed companies worth ₹40,000 crore in 2024, IIFL's journey demonstrates that building in emerging markets requires different rules. You can't just copy developed market models. You can't just be digital or physical. You can't just serve institutions or retail.

Success requires synthesis—combining opposites into something new. High-tech and high-touch. Global standards and local insights. Scale and personalization. Growth and profitability.

IIFL didn't just build a financial services company. They built a template for how to create value in complex, regulated, emerging markets. That template—pivot strategically, survive creatively, demerge courageously, execute relentlessly—is their greatest contribution.

For entrepreneurs, it's inspiration that anything is possible. For investors, it's a framework for evaluating emerging market opportunities. For India, it's proof that homegrown companies can compete globally.

The story of IIFL Capital Services isn't finished. But the chapters written so far are worth studying, debating, and learning from. Because in the end, every great company is both a product of its time and a creator of its future.

And IIFL? They're still creating.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube