IFCI: India's First Development Bank - From Nation-Building to Crisis and Reinvention

I. Introduction & Episode Roadmap

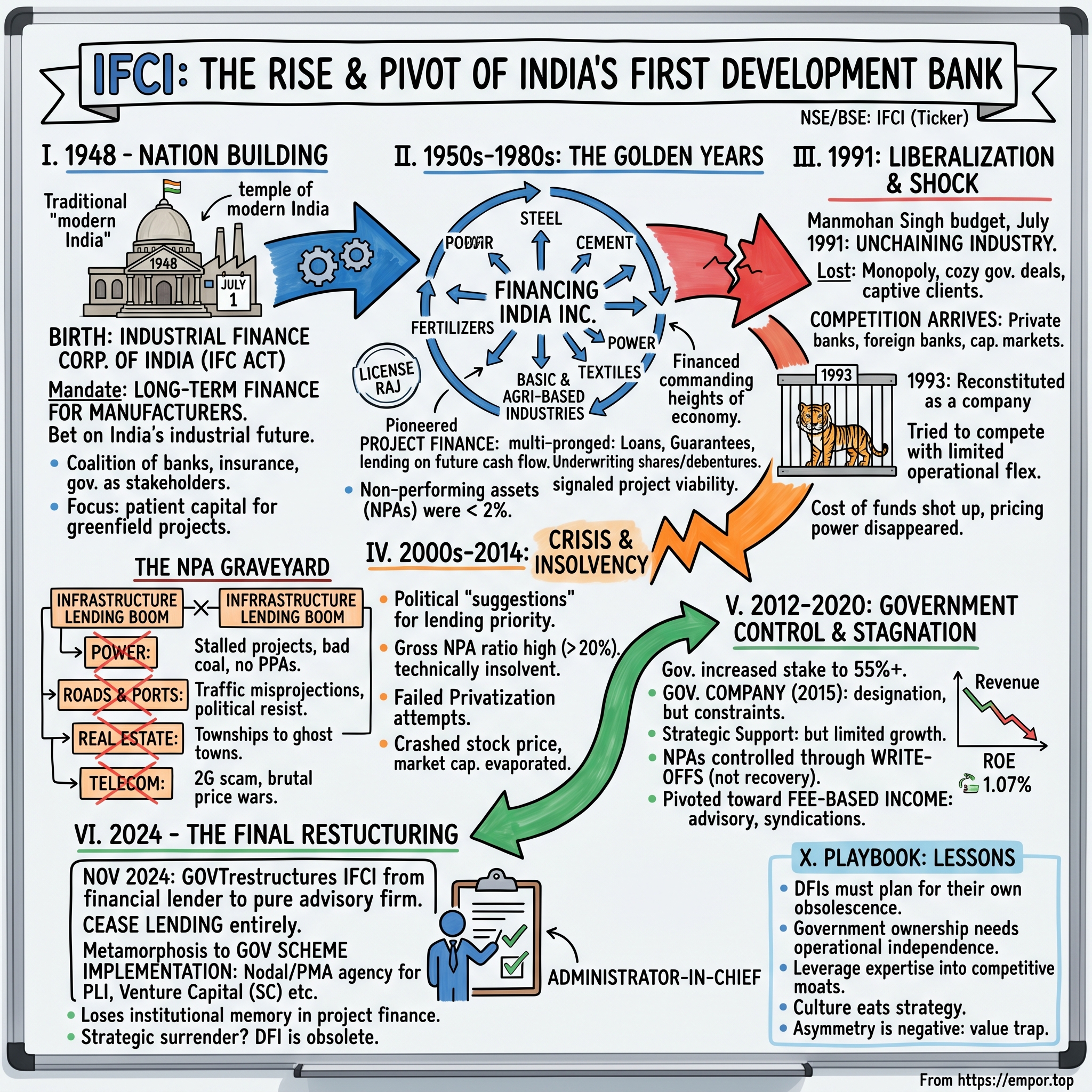

Picture this: July 1, 1948. The tricolor had been hoisted at Red Fort barely eleven months ago. Partition's wounds were still raw, refugees still streaming across borders, and a nascent nation was grappling with the monumental task of building an economy from scratch. In this crucible of hope and chaos, India's leaders made a bold move—they established the Industrial Finance Corporation of India, the country's first development financial institution. It was more than just a bank; it was an act of faith in India's industrial future.

Fast forward to November 2024. The same institution, now known as IFCI Limited and listed on the NSE with the ticker symbol IFCI, receives news that would have been unthinkable to its founders: the Government of India announces it will restructure IFCI from a financial lender to a pure advisory firm, effectively shuttering its lending operations entirely. The institution that once financed the steel plants, cement factories, and power stations that built modern India would no longer lend a single rupee.

This is the paradox of IFCI—India's pioneering development bank that helped industrialize a nation, only to become a cautionary tale of how public sector financial institutions struggle to reinvent themselves in liberalized markets. It's a story that mirrors India's own economic journey: from socialist planning to market reforms, from protected monopolies to cutthroat competition, from nation-building idealism to the harsh realities of non-performing assets and government bailouts.

Today, IFCI stands as a shadow of its former self, with a market capitalization of ₹14,374 crores—impressive in absolute terms, yet a fraction of what private sector banks that didn't even exist when IFCI was founded are now worth. The government holds 72.6% of its equity, making it effectively a state-controlled entity masquerading as a listed company. Its return on equity over the last three years? A pitiful 1.07%.

But this isn't just a story of decline. It's a narrative about institutional evolution, the challenge of transitioning development finance institutions in liberalized economies, and the eternal tension between public purpose and commercial viability. It's about how an institution can simultaneously be a success—having catalyzed India's industrialization—and a failure, unable to find relevance in the very market economy it helped create.

As we unpack IFCI's 76-year journey, we'll explore the rise and fall of development banks globally, the peculiar dynamics of government ownership in competitive markets, and what happens when institutions outlive their original purpose. This is as much a story about India's economic transformation as it is about one institution's struggle to adapt. And in an era where governments worldwide are rediscovering industrial policy and development finance, IFCI's trajectory offers lessons that extend far beyond Dalal Street.

II. Post-Independence India & The Birth of IFCI (1947–1948)

The monsoon of 1947 brought more than rain to the subcontinent. It brought freedom, partition, and unprecedented human migration. As trains carrying refugees crossed the newly drawn borders, another train of thought was racing through the minds of India's economic planners: How does a nation with barely any industrial base, a per capita income of ₹249, and capital markets so thin you could see through them, build an economy capable of lifting 330 million people out of poverty?

In the wood-paneled offices of what would soon become the Finance Ministry, officials pored over reports from Japan and Europe. The Japanese model was particularly intriguing—their Industrial Bank of Japan, established in 1902, had catalyzed the Meiji restoration's industrial miracle. Germany's Kreditanstalt für Wiederaufbau was already showing promise in post-war reconstruction. The message was clear: developing nations needed specialized institutions that could provide "patient capital"—long-term finance that commercial banks, obsessed with quarterly returns and liquidity, wouldn't touch.

At the time of independence in 1947, the Indian Capital Markets were relatively less developed. The demand for capital was growing rapidly, however, there was a dearth of providers of capital. The commercial banks that existed were not equipped well enough to provide for long term capital needs in any significant manner. Picture this market: the Bombay Stock Exchange had perhaps 200 actively traded securities, daily volumes that a modern algorithmic trader would execute in microseconds, and virtually no debt market to speak of. Industrial entrepreneurs—and there were precious few—had three options: beg foreign banks (who viewed Indian industry with colonial disdain), approach traditional moneylenders (at usurious rates), or abandon their dreams.

Enter Jawaharlal Nehru, architect of modern India, socialist by conviction, pragmatist by necessity. Nehru understood that state-led industrialization wasn't just an economic strategy—it was an assertion of sovereignty. Every steel mill was a declaration that India could forge its own destiny; every cement factory, proof that the country could build its own future. But rhetoric needed rupees, and rupees needed institutions.

The Government of India established The Industrial Finance Corporation of India (IFCI) on July 1, 1948 by enacting the IFC Act 1948. The timing wasn't coincidental—it came exactly one year and two weeks after the formation of the Planning Commission, signaling that industrial finance would be the tip of the spear in India's development strategy.

The authorized capital was set at ₹250 crores—a staggering sum when the entire union budget was barely ₹400 crores. The authorized capital of the IFCI is 250 crores and the Central Government can increase this as and when they wish to do so. But here's where it gets interesting: unlike a typical government department, IFCI was structured as a statutory corporation with a unique shareholding pattern. The IDBI, scheduled banks, insurance sector, co-op banks are some of the major stakeholders of the IFCI.

This wasn't just financial engineering—it was political architecture. By making scheduled banks and insurance companies shareholders, the government created a coalition of interests. Banks would benefit from IFCI taking on the riskier, longer-term loans they couldn't handle. Insurance companies got an investment avenue for their long-term liabilities. And the government got an institution that could channel savings into industrial investment without appearing overtly socialist to an increasingly Cold War-conscious world.

The mandate was deliberately broad yet focused. The main aim for the incorporation of IFCI was to provide long-term finance to the manufacturing and industrial sector of the country. But hidden in the legislative language was a more ambitious agenda: IFCI would be India's industrial pathfinder, identifying sectors that needed development, nurturing entrepreneurs who had ideas but no capital, and essentially picking winners in an economy that barely had any players.

The early board meetings, held in borrowed rooms in New Delhi's nascent government quarter, read like a who's who of India's economic future. Representatives from the Reserve Bank (itself only 13 years old), nominees from scheduled banks still finding their feet post-independence, and government officials who'd learned their craft under the British but were now tasked with undoing colonial economic structures.

What made IFCI revolutionary wasn't just that it would lend money—it was how it would lend. Commercial banks focused on working capital, trade finance, and short-term loans backed by current assets. IFCI would provide term loans for capital expenditure, backed not by existing assets but by future cash flows from projects yet to be built. It was betting on India's industrial future with money India didn't yet have.

The first applications started trickling in by August 1948: a textile mill in Ahmedabad seeking modernization funds, a small cement plant near Bombay wanting to expand capacity, a sugar mill in UP hoping to install new crushing equipment. Each application was more than a loan request—it was a test case for whether India could create industry from imagination, whether a nation of farmers could become a nation of factories.

As 1948 drew to a close, IFCI had approved its first few loans, modest amounts by today's standards but revolutionary for their time. The institution had no track record, no credit models, no industrial data to rely on. What it had was a mandate from a newly free nation and the audacious belief that India could industrialize its way to prosperity. The development bank model—patient capital, long-term vision, state backing but commercial discipline—would become the template not just for India but for dozens of developing nations watching India's experiment with interest.

III. The Golden Years: Building India Inc. (1950s–1980s)

The summer of 1955 brought unusual excitement to the sleepy industrial town of Durgapur in West Bengal. Soviet engineers in ill-fitting tropical clothes worked alongside Indian technicians, while bulldozers carved out what would become one of Asia's largest steel plants. At the makeshift IFCI field office, loan officer K.V. Raghavan was processing paperwork for a ₹15 crore loan—the largest industrial loan in India's history at that point. "We're not just financing a steel plant," he told his junior colleague, "we're financing India's tomorrow."

This was IFCI in its element—the maestro conductor of Nehru's "temples of modern India." Between 1950 and 1980, the institution would transform from a tentative lender into the architect of Indian industrialization, financing everything from textile mills in Coimbatore to fertilizer plants in Sindri, from paper mills in Nepanagar to chemical factories in Vadodara.

It has financed projects in sectors like steel, cement, textiles, fertilizers, and infrastructure. But these weren't just sectors—they were the building blocks of a modern economy. Every ton of steel meant railways could expand, every bag of cement meant dams could be built, every meter of textile meant exports could grow. IFCI wasn't picking winners; it was creating an ecosystem where winners could emerge.

The financing model was ingenious in its simplicity yet revolutionary for its time. While commercial banks obsessed over collateral and current ratios, IFCI pioneered project finance in India—lending based on future cash flows, taking construction risk, and accepting industrial assets as security. The main function of the IFCI is to provide medium and long-term loans and advances to industrial and manufacturing concerns. It looks into a few factors before granting any loans. They study the importance of the industry in our national economy, the overall cost of the project, and finally the quality of the product and the management of the company. If the above factors have satisfactory results the IFCI will grant the loan.

But IFCI did more than just lend. The Industrial Finance Corporation of India can also subscribe to the debentures that these companies issue in the market. The IFCI also provides guarantees to the loans taken by such industrial companies. When a company is issuing shares or debentures the Industrial Finance Corporation of India can choose to underwrite such securities. This multi-pronged approach meant IFCI could support companies at every stage of their capital structure, from debt to equity, from domestic to foreign currency needs.

The institution's reach during these golden years was staggering. In the last few decades, the Industrial Finance Corporation of India has made a significant contribution to the development of our economy. Also, it is responsible for the growth, expansion, and modernization of our industrial sector. The Industrial Finance Corporation of India has also been beneficial for the import and export industry, the cause of pollution control, energy conservation, import substitution, and many such initiatives and industries.

Consider the sectors that IFCI nurtured: Agricultural Based Industries like paper, sugar, rubber, etc. Service Industries like restaurants, hospitals, hotels, etc. Basic industries in any economy like steel, cemen[t]—each represented a bet on India's future. The sugar mills of UP weren't just processing sugarcane; they were providing rural employment and import substitution. The cement plants weren't just producing building material; they were enabling the construction of a nation.

IFCI bank has been a driving force behind the restructuring of Indian industry, trade facilitation, trade liberalisation, and the fostering of breakthrough industries, among other commercially viable and market-friendly operations, since its inception. This wasn't hyperbole—IFCI literally created markets where none existed. When private capital wouldn't touch sunrise industries, IFCI stepped in. When foreign technology needed Indian partners, IFCI provided the bridge financing. When entrepreneurs had ideas but no collateral, IFCI took the leap of faith.

The License Raj era, often maligned for its bureaucratic stranglehold, was paradoxically IFCI's finest hour. In a system where every industrial license was precious, where capacity expansion required government approval, where foreign exchange was scarcer than gold, IFCI operated as the financial arm of industrial policy. It knew which applications would be approved, which sectors would get priority, which regions needed development. This insider knowledge wasn't corruption—it was coordination, the kind that allowed scarce capital to flow to predetermined priorities.

The company has played a pivotal role in setting up various market intermediaries of repute in several niche areas like stock exchanges, entrepreneurship development organisations, consultancy organisations, educational and skill development institutes across the length and breadth of the coun[try] This institution-building role was perhaps IFCI's most enduring legacy. It wasn't content with just financing industries; it created the ecosystem they needed to thrive.

By the late 1970s, IFCI's loan book read like a roster of India Inc. The Tatas, Birlas, Goenkas, Mafatlals—every major industrial house had IFCI's fingerprints on their expansion stories. Small entrepreneurs who would later become industrial titans got their first institutional loans from IFCI. The institution had become so central to industrial finance that getting an IFCI loan was seen as a stamp of approval, a signal to other lenders that the project was viable.

But success bred its own challenges. As the sole development finance institution for over a decade (until ICICI's establishment in 1955), IFCI had developed a certain institutional arrogance. Loan approvals took months, documentation requirements grew byzantine, and the institution began believing its own mythology—that it, not the entrepreneurs, was the hero of India's industrial story.

The numbers from this period tell a story of dominance: By 1980, IFCI had sanctioned cumulative assistance of over ₹2,000 crores, astronomical for an economy where the entire Five Year Plan outlay was ₹4,000 crores. Its loan assets grew at 20% annually through the 1970s. Non-performing assets were under 2%—remarkable given it was financing greenfield projects in a developing economy.

Yet cracks were beginning to show. The very success of IFCI's model had created competition—ICICI (1955), IDBI (1964), and state financial corporations were all encroaching on IFCI's turf. Commercial banks, flush with deposits from bank nationalization in 1969, started eyeing project finance. The cozy relationship with government, once an asset, was becoming a liability as political interference in lending decisions increased.

As the 1980s dawned, IFCI stood at the peak of its influence—the undisputed emperor of industrial finance, the institution that had transformed India from an agricultural economy to an industrial power. It had financed the commanding heights of the economy, nurtured entrepreneurship, and built institutions that would outlast it. But empires built on monopolies rarely survive the arrival of competition. The liberalization winds were beginning to blow, and IFCI, comfortable in its dominance, was ill-prepared for the storm that was coming.

IV. Liberalization & Identity Crisis (1991–2000)

The morning of July 24, 1991, changed everything. As Finance Minister Manmohan Singh rose in Parliament to present what would become India's most consequential budget, IFCI's senior management huddled in their Nehru Place headquarters, watching the live broadcast with mounting anxiety. "Industry has been shackled for too long," Singh declared, announcing the dismantling of industrial licensing, opening up of foreign investment, and reduction of import tariffs. For most of India Inc., it was liberation day. For IFCI, it was the beginning of an existential crisis.

The Indian Capital Markets and Financial System saw considerable changes after the Indian economy was liberalised in 1991. What those changes meant for IFCI was nothing short of a complete upending of its raison d'être. The monopoly on long-term industrial finance—gone. The cozy relationship with government that guaranteed deal flow—evaporating. The captive market of entrepreneurs who had nowhere else to go—suddenly spoilt for choice.

The institution's response was swift but perhaps misguided. On 1 July 1993, it was reconstituted as a company to impart a higher degree of operational flexibility, transforming from a statutory corporation to Industrial Finance Corporation of India Ltd. The constitution of IFCI was converted from a statutory corporation to a company under the Indian Companies Act, 1956, to facilitate raising funds directly through capital markets.

The logic seemed impeccable: if IFCI was to compete with commercial banks and the emerging capital markets, it needed the flexibility to tap those very markets for resources. No longer would it depend on government allocations or statutory liquidity requirements that forced banks to subscribe to IFCI bonds. It would stand on its own feet, raise capital like any other company, and compete on merit.

But therein lay the fundamental miscalculation. IFCI's leadership, steeped in decades of monopolistic thinking, believed that removing statutory shackles would unleash entrepreneurial energy. They didn't realize that the institution's entire culture, systems, and mindset were products of a protected environment. It was like asking a zoo-bred tiger to suddenly hunt in the wild—the instincts had atrophied.

The company's name was subsequently changed to 'IFCI Limited' in October 1999. The name change was more than cosmetic—it was an attempt to signal transformation, to distance itself from the bureaucratic image of the old Industrial Finance Corporation. But changing names without changing DNA rarely works.

The competitive landscape that emerged post-liberalization was brutal for IFCI. Commercial banks, freed from directed lending requirements, aggressively entered project finance. HDFC, established in 1977 as a housing finance company, showed what a focused, professionally-run financial institution could achieve. ICICI, IFCI's younger sibling, proved more nimble in adapting to market realities. Foreign banks brought sophisticated financial products and cherry-picked the best corporate clients.

Because there was NPA increase, and it was making loss, then gov privatised it. The early signs of distress were already visible. IFCI's loan appraisal processes, designed for a shortage economy where every project got funded, couldn't cope with the new reality of choice and competition. Its staff, accustomed to entrepreneurs waiting months for appointments, watched in bewilderment as competitors offered same-day sanctions.

IFCI was allowed to acces[s] capital markets directly, but this freedom came with a curse. Unlike its statutory corporation days when it could borrow at concessional rates, IFCI now had to pay market rates for funds. Its cost of funds shot up precisely when its pricing power disappeared. Entrepreneurs who once had no choice but to accept IFCI's terms could now shop around for better rates.

The identity crisis was most acute in IFCI's strategic positioning. Was it a development bank with a social mandate or a commercial lender chasing profits? Should it continue funding infrastructure projects with long gestation periods or pivot to working capital loans with quicker returns? Should it maintain its pan-India presence or consolidate to profitable regions?

Each strategic review—and there were many—ended in paralysis. The board, a mix of government nominees, institutional representatives, and independent directors, couldn't agree on direction. Government wanted IFCI to continue its developmental role but without providing subsidized funding. Institutional shareholders wanted returns but weren't willing to accept the risks of aggressive lending. Management wanted autonomy but lacked the courage to make hard decisions.

The human dimension of this transformation was particularly poignant. IFCI's workforce, recruited in the 1960s and 1970s for their technical expertise in evaluating industrial projects, found themselves competing with MBAs from IIMs who spoke the language of derivatives, securitization, and fee income. The old guard's deep understanding of industrial processes—knowing why a cement plant needed a particular limestone quality or how textile machinery depreciation worked—suddenly seemed less valuable than skill in financial engineering.

By the late 1990s, IFCI's market share in industrial lending had plummeted from over 20% in 1990 to less than 5%. New disbursements were declining even as the economy was growing at 6-7% annually. The institution that once had entrepreneurs queuing outside its offices now had relationship managers desperately cold-calling for business.

The irony was stark: liberalization, which turbocharged Indian industry, nearly killed the institution that had nurtured that very industry. IFCI had succeeded so well in its original mission—creating industrial capacity—that it had made itself redundant. The very entrepreneurs it had supported in the 1960s and 1970s were now large enough to access capital markets directly or negotiate with global banks.

As the millennium approached, IFCI resembled a grand old mansion in a neighborhood that had transformed into glass-and-steel high-rises. Still imposing, still carrying the weight of history, but increasingly irrelevant to the contemporary landscape. The institution needed more than a new name or corporate structure—it needed a fundamental reimagination of its purpose. But that reckoning would only come after a near-death experience that would shake it to its very foundations.

V. The NPA Crisis & Near-Death Experience (2000s–2014)

The boardroom at IFCI's headquarters on a humid August morning in 2008 felt like a war room. Charts covered every wall—red lines plummeting, bar graphs showing mounting losses, pie charts where the "non-performing" slice had swallowed almost everything else. The Chairman's opening words to the emergency board meeting were stark: "Gentlemen, we are technically insolvent."

How had India's pioneering development bank reached this precipice? The answer lay not in a single catastrophic event but in a toxic cocktail of misaligned strategy, poor credit decisions, political interference, and an infrastructure lending boom that had turned into a spectacular bust.

In 2014, IFCI entered into a corporate debt restructuring process to address mounting non-performing assets (NPAs). But the crisis had been brewing for over a decade. The early 2000s saw IFCI, desperate to remain relevant post-liberalization, plunge headlong into infrastructure financing—power plants, roads, ports, airports. The logic seemed sound: India needed infrastructure, banks were still cautious about long-gestation projects, and IFCI had the expertise. What could go wrong? Everything, as it turned out.

The power sector alone became a graveyard of bad loans. Coal linkages that never materialized, power purchase agreements that states reneged on, environmental clearances that got stuck in courts—each stalled project added to IFCI's mounting pile of NPAs. A ₹500 crore loan to a power project in Orissa, sanctioned with great fanfare in 2006, hadn't seen a single rupee of interest payment by 2010. The plant existed only on paper.

By fiscal year 2023, the Gross NPA ratio had stood at 8.73%, down from a high of over 20% in prior years. But this improvement came after years of pain. The peak of the crisis saw IFCI's gross NPAs crossing 20%—meaning one in every five rupees lent was stuck. For context, international norms consider anything above 5% as concerning; IFCI was four times that threshold.

The infrastructure boom of 2003-2008 had been intoxicating. GDP growth averaging 8%, stock markets soaring, real estate prices doubling every few years—it felt like India's century had arrived early. IFCI, along with other lenders, threw caution to the wind. Due diligence became perfunctory, loan covenants were relaxed, and everyone assumed that in a growing economy, even mediocre projects would succeed.

Political interference compounded the problem. IFCI's board meetings often featured "suggestions" from the Ministry about which projects deserved "priority consideration." A steel plant in a Minister's constituency, a cement factory owned by a well-connected industrialist, a real estate project backed by political heavyweights—each came with implicit pressure to approve. Saying no required courage that few in IFCI's leadership possessed.

The management turmoil didn't help. Between 2000 and 2014, IFCI saw seven CEOs—an average tenure of two years. Each came with a new strategy, a fresh vision, a different priority. The organization lurched from one direction to another like a ship without a compass. One CEO would focus on retail lending, the next on corporate finance, the third on fee income. By the time a strategy could show results, there was a new captain at the helm.

The global financial crisis of 2008 was the knockout punch to an already staggering institution. Credit markets froze, refinancing became impossible, and borrowers who were barely managing to service debt simply stopped paying. IFCI's own borrowing costs spiked as rating agencies downgraded its debt to near-junk status. The institution that once lent at 12% was now borrowing at 14%—a recipe for certain doom.

In recent decades, India's banking sector has experienced two episodes of crisis with respect to the nonperformance of their advances or loans, one in the mid-1990s and the other which has been ongoing since 2014–2015. While there seem to be a few similarities between the two phases of the crisis, the current non-performing advances (NPA) crisis, however, is more severe in terms of the volume of failed loans turning into NPAs, thereby affecting the financial health of the banks.

IFCI found itself at the epicenter of this broader banking crisis. Unlike commercial banks that had diversified loan books and deposit bases to fall back on, IFCI was entirely dependent on wholesale funding. When that dried up, the institution faced an existential liquidity crisis.

The human cost was devastating. Employees who had joined IFCI as India's premier financial institution watched their stock options become worthless, their bonuses disappear, and their pride evaporate. Talented professionals fled to private banks and NBFCs. Those who remained were demoralized, going through the motions in an organization that seemed to have no future.

Recovery efforts were half-hearted at best. IFCI's legal team was overwhelmed—hundreds of cases in various courts, each moving at glacial pace. The SARFAESI Act, meant to expedite recovery, proved ineffective against large, politically-connected defaulters who could tie up cases in litigation for years. Asset Reconstruction Companies (ARCs) bought IFCI's bad loans at massive discounts—sometimes as low as 10 paise to the rupee—crystallizing enormous losses.

The numbers tell the story of decline: IFCI's loan book shrank from ₹25,000 crores in 2008 to less than ₹15,000 crores by 2012. Market share in project finance fell to less than 2%. The stock price, which had touched ₹75 in 2007, crashed to under ₹10 by 2013. Market capitalization evaporated by over 85%.

Government bailouts kept IFCI alive but barely breathing. Capital infusions of ₹500 crores here, ₹1,000 crores there—band-aids on a hemorrhaging patient. Each bailout came with promises of reform, strategic clarity, and improved governance. None materialized in any meaningful way.

The failed privatization attempts of this period were particularly telling. The government announced its intention to reduce stake below 50% multiple times, but no buyer showed serious interest. Who would want to buy an institution with unclear strategy, massive NPAs, demoralized workforce, and continued political interference? The few expressions of interest came with conditions the government wouldn't accept—massive write-downs, freedom from government control, ability to rightsize the workforce.

By 2014, when IFCI formally entered corporate debt restructuring, it wasn't a surprise but a long-overdue acknowledgment of reality. The institution that had once financed India's industrial dreams was now itself a candidate for restructuring. The irony was lost on no one.

This near-death experience would force a fundamental rethink of IFCI's existence. Could a development finance institution survive in a market economy? Did India still need IFCI? These questions, avoided for two decades, could no longer be ignored. The government's response would be to take back control, but whether that would revive IFCI or simply delay its inevitable demise remained to be seen.

VI. Government Takes Control & Stabilization (2012–2020)

The press conference on December 21, 2012, was a masterclass in bureaucratic euphemism. The Finance Secretary announced that the government would increase its stake in IFCI to 55.53%, making it a government-controlled entity. He called it "strategic support for a systemically important institution." Everyone in the room knew what it really meant: IFCI had become too big to fail and too sick to survive on its own. The government was taking it into intensive care.

IFCI became a Government controlled company subsequent to enhancement of equity shareholding to 55.53% by Government of India on December 21, 2012. This wasn't a rescue—it was a takeover. The institution that had been corporatized in 1993 to gain operational flexibility was being brought back under government control, a full-circle journey that spoke volumes about the failure of its privatization experiment.

The stabilization strategy that followed was both pragmatic and painful. First came the capital infusions—steady drips of government money that kept IFCI's heart beating. Between 2012 and 2020, the government pumped in over ₹3,000 crores through various mechanisms—direct equity, preference shares, and quasi-equity instruments. Each infusion came with stern warnings about reform and efficiency, warnings that were promptly forgotten once the money was transferred.

IFCI Ltd has now become a state- owned firm with the government increasing its stake in the infrastructure financing firm to 51.04 per cent. The formal transformation happened in April 2015. Government has acquired IFCI's 6,00,00,000 Preference shares of Rs 10 each from certain scheduled commercial banks and consequently increased its holding from 47.93 per cent to 51.04 per cent of the paid-up share capital. The preference share acquisition from public sector banks was financial engineering at its finest—the government essentially moved money from one pocket to another, but it achieved the legal threshold needed to make IFCI a government company.

As a result of...Increase in shareholding of the Government of India, IFCI has become a 'Government Company' as per the provisions of Section 2(45) of the Companies Act, 2013, with effect from April 7, 2015. This designation brought both benefits and burdens. On the plus side, IFCI's credit rating immediately improved—rating agencies viewed government backing as an implicit guarantee. Recently, CARE Ratings have upgraded the rating assigned to debt instruments of IFCI upward from "CARE A" to "CARE A+" for long term borrowings, from "CARE A1" to "CARE A1+" for short term bank facilities and Commercial Papers and from "CARE A-" to "CARE A" for Subordinate Bonds.

But government control also meant government constraints. Hiring decisions now needed ministry approval. Strategic initiatives required endless consultations. The Vigilance Department started breathing down executives' necks, making them risk-averse to the point of paralysis. IFCI had traded autonomy for survival, dynamism for stability.

The new management team installed by the government took a ruthlessly pragmatic approach to cleaning up the balance sheet. They stopped pretending that dead loans would miraculously revive. Write-offs accelerated—painful acknowledgments of past mistakes but necessary for moving forward. Assets were sold at whatever price the market would bear. Non-core investments divested. The corporate headquarters, once a symbol of IFCI's ambitions, was put on the block.

Company has reduced debt. The deleveraging was dramatic. From a debt-equity ratio of over 8:1 at the peak of the crisis, IFCI brought it down to more manageable levels. But this came at a cost—new lending virtually stopped. IFCI became a zombie institution, technically alive but economically moribund.

The shift in business model during this period was telling. Unable to compete in traditional project finance, IFCI pivoted toward fee-based income. Advisory services, arranging syndications for other lenders, project monitoring for government schemes—activities that required expertise but not capital. It was a humbling transformation for an institution that once financed India's industrial backbone.

After becoming a Government Company, IFCI is now better equipped to participate in the Country's growth movement by lending to diversified industries and thus contribute its share towards making `MAKE IN INDIA' programme a success. The official narrative was optimistic, but the reality was more complex. IFCI was being repositioned as an instrument of government policy rather than a commercial lender.

The government also found creative ways to use IFCI for its social agenda. In order to promote entrepreneurship among the scheduled castes and to provide concessional finance to them, IFCI Group has been entrusted with the setting up of a `Venture Capital Fund for Scheduled Castes' of the Government with an initial capital of Rs. 200 crore, which can be supplemented every year · IFCI has also been provided another Rs. 200 Crore for 'Credit Enhancement Guarantee Scheme for Scheduled Castes' Entrepreneurs' under the sponsorship of the Government. These schemes, while laudable in intent, further muddled IFCI's identity—was it a commercial lender, a development institution, or a vehicle for implementing government schemes?

Government of India (GoI), resulting an increase in shareholding of GoI from 66.35% to 70.32% and further to 71.72% in April, 2024. The government's stake continued to increase through the decade, each increment representing private investors' diminishing faith in IFCI's future. Promoter Holding: 72.6% By 2024, the government owned nearly three-quarters of the company—a listed entity in name but a government department in practice.

The stabilization achieved during this period was real but limited. NPAs were brought under control, not through recovery but through write-offs. The institution stopped bleeding money but also stopped growing. Employee morale improved from abysmal to merely poor. IFCI survived, but at what cost?

Company has delivered good profit growth of 22.6% CAGR over last 5 years The profit growth looked impressive on paper, but it was largely due to the low base effect—when you're starting from massive losses, any profit looks like spectacular growth. The company has delivered a poor sales growth of -8.22% over past five years. Company has a low return on equity of 1.07% over last 3 years. The underlying business metrics told the real story—a shrinking institution generating negligible returns on equity.

By 2020, IFCI had achieved a peculiar form of stability—the stability of stagnation. It wasn't dying anymore, but it wasn't really living either. The government had succeeded in preventing a messy collapse that would have had systemic implications, but it hadn't answered the fundamental question: What was IFCI's purpose in modern India?

The COVID-19 pandemic that struck in 2020 would provide an unexpected opportunity to answer that question. As the government launched massive economic stimulus programs, IFCI would find itself thrust into a new role—not as a lender but as an implementing agency for government schemes. It was another pivot in IFCI's long journey, one that would finally lead to the radical restructuring announced in 2024.

VII. The Infrastructure Years & Major Projects

Looking back at IFCI's infrastructure portfolio is like walking through a graveyard of India's economic ambitions—some monuments to success, others tombstones of failure. The conference room walls at IFCI's headquarters once displayed photographs of the projects they'd financed: gleaming airports, massive ports, power plants stretching to the horizon. By 2010, many of those same photographs had been quietly removed, their subjects having become non-performing assets.

The financing activities cover various kinds of projects such as airports, roads, telecom, power, real estate, manufacturing, services sector and such other allied industries. During its 70 years of existence, mega-projects like Adani Mundra Ports, GMR Goa International Airport, Salasar Highways, NRSS Transmission, Raichur Power Corporation, among others, were set up with the financial assistance of IFCI.

These weren't just projects—they were India's infrastructure dreams made concrete and steel. Take Adani Mundra Port, now India's largest commercial port. When Gautam Adani approached IFCI in the late 1990s with plans for a greenfield port in Gujarat's Kutch district, commercial banks laughed him out of their offices. A port in a earthquake-prone zone, promoted by a then-relatively unknown entrepreneur, in a state with limited industrial base? IFCI said yes, structuring a complex financing package that would eventually help create a facility handling over 200 million tonnes of cargo annually.

The various sectors covered under project finance are power, including renewable energy, telecommunications, roads, oil and gas, ports, airports, basic metals, chemicals, pharmaceuticals, electronics, textiles, real estate, smart cities and urban infrastructure, and others. The breadth of IFCI's infrastructure financing was staggering. But breadth, as IFCI would learn, could also mean lack of focus.

The power sector became IFCI's Vietnam—a quagmire from which it couldn't extract itself. Between 2000 and 2010, IFCI financed dozens of power projects, betting on India's insatiable energy demand. The math seemed simple: India needed electricity, private developers would provide it, state electricity boards would buy it. What could go wrong? Everything, as it turned out.

State electricity boards, hemorrhaging money from free power to farmers and transmission losses (a euphemism for theft), simply stopped paying. Power purchase agreements weren't worth the paper they were printed on. Coal linkages promised by Coal India never materialized. Environmental clearances got stuck in courts. The Ultra Mega Power Projects, meant to revolutionize India's energy landscape, became ultra mega disasters for their lenders.

Raichur Power Corporation, proudly listed among IFCI's success stories, tells a more complex tale. Yes, the 1,720 MW thermal power plant in Karnataka got built. Yes, it generates electricity. But the project faced massive cost overruns, delayed commissioning, and years of disputes over coal supply and tariffs. IFCI's exposure, initially projected at ₹400 crores, ballooned to over ₹800 crores as the project needed constant financial restructuring.

GMR Goa International Airport represented a different kind of challenge. Financing an airport in a tourism-dependent state seemed like a safe bet. Goa's beaches would always attract visitors, right? But IFCI hadn't factored in the politics of airport privatization, the complexities of land acquisition in a small state, and the resistance from local communities who saw the airport expansion as a threat to Goa's character. The project succeeded eventually, but not before years of delays and cost escalations that eroded returns.

The roads sector provided some respite. Salasar Highways and similar projects operated on a simpler model—build the road, collect tolls, pay back loans. The National Highways Authority's backing provided comfort. But even here, IFCI learned harsh lessons. Traffic projections prepared by consultants proved wildly optimistic. Competing free roads diverted vehicles. Toll resistance in certain regions led to violence and forced toll holidays. The supposedly safe infrastructure bet turned risky.

The company provide financial support for the diversified growth of Industries across the spectrum. The financing activities cover various kinds of projects such as airports, roads, telecom, power, real estate, manufacturing, services sector and such other allied industries. Real estate financing, which IFCI entered during the 2000s boom, became a particular nightmare. Luxury townships that were supposed to house India's growing middle class turned into ghost towns when the 2008 financial crisis hit. Mall projects in Tier-2 cities, financed on projections of retail revolution, stood empty as e-commerce killed physical retail. IFCI found itself owning half-built commercial complexes and land banks in locations where land had no value.

The telecom sector initially seemed like a winner. IFCI financed tower companies during the mobile revolution, betting on the exponential growth in subscribers. The bet paid off initially—India added 20 million mobile subscribers monthly at the peak. But then came the 2G scam, license cancellations, and brutal price wars triggered by Reliance Jio's entry. Several of IFCI's telecom borrowers went bankrupt virtually overnight.

NRSS Transmission represented the kind of technical infrastructure project where IFCI's expertise should have given it an edge. Power transmission lines are essential infrastructure with regulated returns. What IFCI didn't anticipate was the delay in connecting power plants to these transmission lines—having highways with no cars, essentially. The transmission assets existed but generated no revenue for years.

The manufacturing sector financing told a story of India's failed industrial ambitions. IFCI financed textile mills that couldn't compete with Bangladesh, chemical plants that couldn't match Chinese prices, pharmaceutical units that failed FDA inspections, electronics assembly units made obsolete by smartphone imports. Each failed manufacturing project represented not just a bad loan but a small death of Make in India dreams.

What's striking about IFCI's infrastructure years is not the failures—every lender has those—but the pattern of mistakes. IFCI consistently overestimated India's institutional capacity to execute complex projects. It underestimated the role of politics in infrastructure. It assumed that essential infrastructure would automatically generate returns. It believed consultant reports over ground reality.

The few successes—and there were some—shared common characteristics. They had strong sponsors with skin in the game (like Adani Ports). They operated in sectors with clear, simple business models (like toll roads). They avoided sectors with heavy government interface (unlike power). They were in states with relatively better governance (Gujarat, Karnataka) rather than the infrastructure-hungry but institutionally-weak states of the Hindi heartland.

By 2014, IFCI's infrastructure portfolio had become an albatross. Over 60% of its loan book was to infrastructure projects, and over 30% of that was non-performing. The institution that had once financed factories now found itself the reluctant owner of stalled projects across India. Board meetings devolved into discussions about whether to throw good money after bad to complete projects or cut losses and exit.

The tragedy wasn't just financial. Each stalled project represented jobs not created, services not delivered, growth not achieved. The half-built power plant in Chhattisgarh meant villages remaining in darkness. The incomplete road in Bihar meant farmers unable to get produce to market. The abandoned port in Andhra Pradesh meant trade diverted to congested facilities elsewhere.

IFCI's infrastructure years were meant to be its renaissance—a pivot from old economy manufacturing to new economy infrastructure. Instead, they nearly destroyed the institution. The lesson was harsh but clear: infrastructure financing in India required not just capital and expertise but also political acumen, patience beyond what any commercial institution could afford, and a risk appetite that no rational lender should have.

As IFCI limped out of its infrastructure misadventure, battered and nearly broken, it faced a stark choice: find a completely new business model or accept irrelevance. The government's decision would be to turn IFCI into something it had never been—an advisory firm and implementing agency for government schemes. It was an inglorious end to grand infrastructure ambitions, but perhaps the only practical path forward.

VIII. Pivot to Advisory & Government Schemes (2015–Present)

The transformation began with a WhatsApp message. In March 2015, a senior IFCI executive received a late-night forward from the Finance Ministry: "IFCI to be designated nodal agency for SC entrepreneur scheme. Prepare implementation framework. Meeting tomorrow 9 AM." That terse message marked the beginning of IFCI's metamorphosis from a lender searching for purpose to a government scheme administrator—a role nobody had envisioned for India's first development bank.

Further, the Government of India designated IFCI as a nodal agency for the "Scheme of Credit Enhancement Guarantee for Scheduled Caste (SC) Entrepreneurs" in March 2015, with the objective of encouraging entrepreneurship in the lower strata of society. Under the scheme, IFCI would provide guarantees to banks against loans to young and start-up entrepreneurs belonging to scheduled castes.

The irony wasn't lost on old-timers. IFCI, which couldn't manage its own credit risk, was now guaranteeing loans for others. But this wasn't about lending expertise anymore—it was about having the administrative machinery to implement government programs. IFCI had offices across India, systems for documentation, and most importantly, it needed a reason to exist. The government had schemes that needed implementation. It was a marriage of convenience, not love.

The Government of India has placed a Venture Capital Fund of Rs. 200 crore for Scheduled Castes (SC) with IFCI with an aim to promote entrepreneurship among the Scheduled Castes (SC) and to provide concessional finance. IFCI has also committed a contribution of Rs.50 crore as lead investor and Sponsor of the Fund. The Venture Capital Fund for Scheduled Castes was emblematic of IFCI's new avatar. Instead of evaluating steel plants and power projects, IFCI officers found themselves reviewing business plans for beauty parlors in Uttar Pradesh villages and mobile repair shops in Bihar towns.

The cultural shift was jarring. Engineers who had spent careers analyzing debt service coverage ratios for thousand-crore projects were now assessing loan applications for Rs. 10 lakh. The conference rooms that once hosted discussions about infrastructure financing now saw presentations about micro-entrepreneurship. One senior manager, a month before retirement, remarked bitterly: "I joined IFCI to finance India's industrialization. I'm retiring from a glorified subsidy distribution agency."

But something unexpected happened. As IFCI dove deeper into scheme implementation, it discovered a competence it didn't know it had—the ability to navigate government bureaucracy. Decades of being a public sector institution had given IFCI an intimate understanding of how government worked, what files needed to move where, which officials to approach for what clearance. This institutional knowledge, worthless in competitive lending, proved invaluable in scheme administration.

In Government Advisory, IFCI is appointed as a Project Management Agency (PMA) for various Production Linked Incentive (PLI) schemes launched under the aegis of "Atmanirbhar Bharat" by the Government of India. These schemes are aimed at boosting domestic manufacturing and to attract large investment in the identified sectors.

The Production Linked Incentive schemes became IFCI's ticket to relevance in the Modi government's economic agenda. As PMA for multiple PLI schemes, IFCI was suddenly at the center of India's manufacturing ambitions—not as a financier but as an administrator, verifier, and monitor. The work was unglamorous—checking documents, verifying production data, calculating incentive amounts—but it was steady, fee-generating, and most importantly, risk-free.

IFCI is also the Nodal Agency for monitoring loans of Sugar Development Fund (SDF) since 1984 The Sugar Development Fund monitoring role, which IFCI had performed quietly since 1984, suddenly became a template for other schemes. The government realized that IFCI could be its arms-length implementing agency for various programs—close enough to control but distant enough to blame if things went wrong.

The advisory services pivot was less successful but equally telling. IFCI also provides Government Advisory services and Corporate Advisory services. IFCI tried to position itself as an infrastructure advisory firm, leveraging its decades of project finance experience. But the market for advisory was brutally competitive. Global consulting firms like McKinsey and BCG dominated strategy consulting. Big Four accounting firms controlled financial advisory. Boutique firms led by ex-bankers captured deal advisory. What space was there for a lumbering public sector institution?

IFCI's advisory pitches became exercises in nostalgia. "We financed India's first private port," they'd say, not mentioning that the relevant executives had left decades ago. "We understand infrastructure," they'd claim, glossing over their infrastructure NPAs. Potential clients smiled politely and hired someone else.

The fee income from government schemes, however, provided a lifeline. Each scheme came with an administration fee—usually 1-2% of amounts disbursed or monitored. For an institution with negligible lending, these fees became critical. IFCI's revenue model had completely transformed: from interest income on loans to fee income for administration.

The employees adapted with typical public sector resilience. The same officers who once structured complex project finances now became experts in government scheme guidelines. They learned the new vocabulary—DBT (Direct Benefit Transfer), Aadhaar linkage, geo-tagging, social audit. They attended training programs on public financial management instead of credit analysis. They networked with ministry officials instead of corporate CFOs.

IFCI is also the Verifying & Monitoring Agency for various capital subsidy schemes. The verification and monitoring role revealed an uncomfortable truth about India's subsidy regime—it needed an elaborate machinery just to ensure money reached intended beneficiaries. IFCI became part of this machinery, adding layers of documentation and verification that increased costs but provided employment to IFCI's workforce.

The ESG advisory ambitions represented IFCI's attempt to stay relevant with contemporary trends. Under corporate advisory, IFCI is offering financial advisory, ESG advisory and other Project advisory services to the Corporate & Government sectors. But ESG advisory from an institution with no track record in sustainable finance was a hard sell. IFCI's ESG team consisted of redeployed credit officers who had attended a few sustainability workshops. They competed against specialized ESG consultants with global credentials and deep domain expertise.

By 2020, IFCI's transformation was complete. The lending portfolio continued to shrink—legacy loans getting repaid or written off, new lending virtually non-existent. The organization chart looked the same, but job descriptions had changed entirely. The credit department now focused on scheme documentation. The project finance team managed PLI applications. The recovery department... well, they still chased old defaulters, more out of habit than hope.

The financial metrics reflected this transformation. Fee income grew from less than 10% of total income in 2010 to over 40% by 2020. Operating expenses dropped as IFCI stopped maintaining the infrastructure needed for lending—branch offices were closed, credit officers not replaced, technology systems not upgraded. It was a managed decline, disguised as strategic transformation.

Critics called it a betrayal of IFCI's founding vision. What would the institution's founders, who dreamed of financing India's industrial revolution, think of IFCI processing subsidy claims? Supporters argued it was pragmatic evolution—better to serve some purpose than none at all. The truth, as always, lay somewhere in between.

The pivot to advisory and scheme implementation kept IFCI alive but at a cost. It lost whatever remained of its institutional memory in project finance. Young professionals stopped joining—who wanted "Scheme Administrator at IFCI" on their resume? The organization became a parking lot for bureaucrats between postings, a sinecure for the connected, a refuge for those who couldn't find opportunities elsewhere.

As 2024 approached, even this limited relevance was questioned. Digital India meant schemes could be implemented through technology platforms rather than physical institutions. Direct Benefit Transfer eliminated intermediaries. Artificial intelligence could verify documents better than IFCI's officers. The government's announcement in November 2024 that IFCI would stop lending entirely and become a pure advisory firm was merely formalizing what had already happened—IFCI had ceased to be a financial institution in any meaningful sense years ago.

IX. Financial Performance & Current State

The numbers tell a story of institutional schizophrenia. Mkt Cap: 14,221 Crore (down -26.6% in 1 year) · Revenue: 1,895 Cr · Profit: 499 Cr At first glance, a ₹14,000+ crore market cap and nearly ₹500 crore profit might suggest a healthy financial institution. Dig deeper, and you find an organization that's neither dead nor alive, generating profits that mean nothing and maintaining a market value based more on government ownership than business fundamentals.

Company has delivered good profit growth of 22.6% CAGR over last 5 years This seemingly impressive profit growth is the cruelest joke in IFCI's financial statements. When you're recovering from massive losses, any profit looks like spectacular growth. It's like celebrating a terminal patient's weight gain—technically positive but fundamentally meaningless.

The company has delivered a poor sales growth of -8.22% over past five years. This is the number that matters. Negative sales growth for a financial institution means one thing: the core business is dying. IFCI isn't growing slower than competitors; it's actively shrinking. Every year, the loan book gets smaller, the relevance diminishes, the institution fades a little more into irrelevance.

Company has a low return on equity of 1.07% over last 3 years. This might be the most damning statistic of all. A 1.07% ROE means that for every ₹100 of shareholder money, IFCI generates barely ₹1 in returns. You could literally put the money in a savings account and earn three times as much. This isn't a financial institution; it's a value destroyer masquerading as a company.

8 Aug - IFCI reports Q1 FY26 unaudited results; Rs.500 Cr preferential allotment; CRAR at -21.85%, consolidation plan approved. The Capital to Risk-weighted Assets Ratio (CRAR) of -21.85% is a shocking number. For context, RBI mandates a minimum CRAR of 9% for NBFCs. A negative CRAR means IFCI's capital has been completely eroded by losses. The institution is technically insolvent, kept alive only by government ownership and the fiction that it will somehow recover.

The ₹500 crore preferential allotment mentioned is another government bailout, disguised as capital raising. No rational investor would put money into an institution with negative CRAR, shrinking revenues, and 1% ROE. This is taxpayer money being poured into a dying institution because the government can't admit failure.

By fiscal year 2023, the Gross NPA ratio had stood at 8.73%, down from a high of over 20% in prior years. The improvement in NPA ratio from 20% to 8.73% looks positive until you realize how it was achieved—not through recovery but through write-offs. IFCI simply accepted massive losses, cleaned its books, and presented the cleaner balance sheet as progress. It's like claiming weight loss after amputating a gangrenous limb.

The composition of income reveals IFCI's transformation from lender to administrator. Interest income, once 90% of revenues, now contributes less than half. Fee income from government schemes and advisory services makes up the rest. But these aren't the high-margin fees investment banks earn from M&A advisory or capital markets transactions. These are processing fees for government schemes—steady but small, requiring significant operational infrastructure for minimal returns.

The balance sheet structure is equally telling. IFCI's loan book has shrunk to under ₹10,000 crores from peaks of over ₹25,000 crores. But operating expenses haven't declined proportionally. The institution maintains the cost structure of a much larger organization while generating revenues of a small NBFC. It's like maintaining a factory designed to produce thousand cars while actually producing a hundred.

Employee productivity metrics are abysmal. With roughly 500 employees and profits of ₹499 crores, IFCI appears to generate ₹1 crore profit per employee. Impressive? Not when you consider that most of this "profit" comes from reversals of provisions, stake sales in subsidiaries, and one-time gains rather than operational performance. The core business probably loses money on an operational basis.

The dividend policy—or lack thereof—speaks volumes. Though the company is reporting repeated profits, it is not paying out dividend Companies that don't pay dividends despite profits are either investing heavily for growth or preserving capital due to weakness. IFCI falls into the latter category. Every rupee of profit is needed to shore up the depleted capital base.

Promoter Holding: 72.6% The government's 72.6% stake is both IFCI's lifeline and its curse. It provides implicit guarantee that keeps the institution afloat but also ensures that IFCI can never take the hard decisions needed for genuine turnaround. No significant restructuring, no major layoffs, no strategic pivots can happen without political clearance, which never comes.

Market perception of IFCI is reflected in its valuation metrics. Trading at a massive discount to book value, the market clearly doesn't believe the book value is real. The price-to-earnings ratio, distorted by low earnings, is meaningless. Institutional investors have largely abandoned the stock. Retail investors who remain are either hoping for a government-led turnaround or are trapped at higher levels.

The quarterly results show wild volatility—profits one quarter, losses the next, depending on provision reversals and one-time items. There's no underlying business momentum, no growth trajectory, no strategic direction that investors can evaluate. Analyst calls, when they happen, are exercises in diplomatic evasion. Management talks about "challenging environment" and "strategic initiatives" without acknowledging the fundamental reality: IFCI has no viable business model.

Credit rating agencies maintain investment-grade ratings, but their reports read like obituaries written in financial jargon. "Adequate liquidity supported by government ownership" translates to "would be bankrupt without government support." "Challenging operating environment" means "no viable business." "Strategic repositioning ongoing" means "desperately searching for relevance."

The auditor's notes in annual reports have grown longer and more qualified over the years. Emphasis of matter paragraphs, notes about going concern assumptions, qualifications about asset valuations—each addition is another red flag. The statutory auditors, constrained by professional standards, can't say what everyone knows: IFCI is a zombie institution.

Peer comparison is embarrassing. While IFCI shrinks, other financial institutions that didn't exist when IFCI was founded have become giants. HDFC Bank, incorporated in 1994, has a market cap 50 times larger. Bajaj Finance, a relative newcomer, lends more in a quarter than IFCI does in a year. Even other government-owned financial institutions like PFC and REC have found viable niches while IFCI flounders.

The November 2024 announcement that IFCI would stop lending entirely wasn't a surprise to anyone watching the numbers. Lending had already effectively stopped. The loan book was in runoff mode. New sanctions were negligible. The announcement merely formalized what the numbers had been screaming for years: IFCI as a lending institution was finished.

Looking at IFCI's financial performance is like reading the medical chart of a patient in palliative care. The vital signs are still there—revenue, profit, market cap—but they're artificially maintained. The underlying business is dead. What remains is an institutional shell, kept alive by government support and bureaucratic inertia, generating numbers that satisfy regulatory requirements but represent no real economic activity or value creation.

X. Playbook: Lessons from IFCI's Journey

IFCI's seven-decade arc from pioneer to pensioner offers a masterclass in institutional failure—not the spectacular blow-up kind, but the slow, grinding descent into irrelevance that's far more instructive. Every development finance institution globally should study IFCI's journey, not for inspiration but for warnings of roads not to take.

The DFI Transition Challenge

The fundamental question IFCI never answered: What happens to a development finance institution when the economy it helped develop no longer needs it? This isn't unique to India. Japan's Industrial Bank merged into Mizuho. Korea's KDB struggles for relevance. Brazil's BNDES faces constant political pressure. But few fell as far as IFCI.

The successful transitions—like HDFC morphing from a housing finance company to a full-service bank—shared common elements: early recognition of change, decisive leadership, and most critically, the ability to shed legacy baggage. IFCI had none of these. It recognized change too late, had revolving-door leadership, and carried legacy loans like an albatross.

The lesson is brutal: DFIs must plan for their own obsolescence from day one. The very success of your mission—developing financial markets—makes you redundant. The institutions that survive transform before they're forced to. IFCI waited until transformation was no longer possible.

Government Ownership: The Double-Edged Sword

IFCI's relationship with government ownership resembles a toxic marriage—can't live with it, can't live without it. Government backing provided credibility, cheap funding, and implicit guarantees. But it also brought political interference, bureaucratic decision-making, and an inability to take hard commercial decisions.

Compare IFCI with Germany's KfW, still government-owned but highly successful. The difference? KfW maintained operational independence despite state ownership. Political interference was minimized through strong institutional frameworks. IFCI became a tool of whatever government was in power, its lending decisions influenced more by political compulsions than commercial logic.

The playbook lesson: Government ownership can work, but only with ironclad governance structures that protect institutional independence. The moment political considerations override commercial judgment, decline begins. IFCI crossed that line early and never looked back.

Asset-Liability Management in Long-Term Finance

IFCI's fundamental error was using short-term funding for long-term assets—the classic mistake that has killed banks throughout history. When IFCI could no longer access subsidized long-term funds post-liberalization, it should have either changed its asset profile or found new liability sources. It did neither effectively.

The infrastructure boom exposed this mismatch brutally. Thirty-year port projects funded by five-year bonds is a recipe for disaster. When refinancing markets froze in 2008, IFCI faced an existential liquidity crisis. The lesson: in long-term project finance, liability management is more important than asset selection. You can survive bad loans; you can't survive a funding crisis.

Strategic Clarity During Transitions

IFCI's post-liberalization strategy resembled a drunk person searching for keys under a streetlight—not because that's where they dropped them, but because that's where the light is. Infrastructure finance? Try it. Retail lending? Why not. Capital markets? Sure. Advisory? Worth a shot. This strategic ADHD meant IFCI never developed excellence in anything.

Contrast this with ICICI's focused transformation from DFI to universal bank, executed with surgical precision over a decade. Or HDFC's gradual expansion from housing finance to full-service banking, each step carefully planned. Strategic clarity doesn't mean rigidity—it means knowing what you're trying to become and having the discipline to get there.

Political Economy of Public Financial Institutions

IFCI's story is inseparable from India's political economy. In the socialist era, it was the government's industrial financing arm. Post-liberalization, it became an orphan—too public for private markets, too commercial for public purpose. This schizophrenia reflected India's own confused transition from socialism to capitalism.

The institutions that navigated this successfully—like SBI—did so by clearly defining their public purpose obligations while maintaining commercial discipline. IFCI never achieved this balance. It tried to be a commercial lender with a development mandate, satisfying neither objective.

Global DFI Comparisons

China Development Bank (CDB) offers the starkest contrast to IFCI. Both started as policy banks, but CDB became a global infrastructure financing powerhouse while IFCI shrank to irrelevance. The difference? CDB had clear state backing, defined policy objectives, and most importantly, grew with China's economy rather than despite it.

Brazil's BNDES, despite its problems, maintained relevance by constantly reinventing its role—from industrialization to privatization advisor to social program implementer. It stayed close to government priorities while maintaining operational competence. IFCI lost both government alignment and operational excellence.

Germany's KfW succeeded by finding niches commercial banks wouldn't serve—SME finance, environmental projects, development aid. It accepted lower returns but maintained discipline. IFCI tried to compete with commercial banks on their terms and lost.

The Successful Transformation: HDFC's Playbook

HDFC's journey from specialized housing financier to India's largest private bank offers the counterexample to IFCI's decline. Founded in 1977, HDFC recognized early that specialized lending would eventually face competition. It gradually built universal banking capabilities, culminating in the 2022 merger with HDFC Bank.

The key differences: HDFC was never government-owned, allowing commercial decision-making. It built capabilities organically rather than through forced pivots. Most importantly, it transformed from a position of strength, not crisis. IFCI's attempts at transformation always came during crises, limiting options and outcomes.

Risk Management vs. Risk Aversion

Post-crisis, IFCI swung from reckless lending to complete risk aversion. Neither extreme works in financial services. The art is calibrated risk-taking—understanding risks, pricing them correctly, and managing them actively. IFCI lost this capability, becoming alternately a gambler and a miser, never a prudent risk manager.

Institutional Memory and Human Capital

IFCI's greatest loss wasn't financial but human. The experienced project finance professionals who understood industrial processes, evaluated technical risks, and structured complex transactions left for private sector opportunities. They were replaced by generalists who understood neither lending nor development.

Successful institutions preserve institutional memory while refreshing talent. JPMorgan still has bankers who remember the Latin American debt crisis. Goldman Sachs partners study the firm's history religiously. IFCI's institutional memory walked out the door, taking decades of expertise with it.

The Technology Transition Failure

While IFCI struggled with basic lending, fintech companies built billion-dollar valuations doing exactly what IFCI should have evolved into—using technology to reduce lending costs, improve risk assessment, and reach underserved segments. IFCI's technology remained stuck in the mainframe era while the world moved to AI-driven credit decisions.

Regulatory Arbitrage and Competitiveness

IFCI operated under the worst of both worlds—regulated like a bank but without access to deposits, competing with private NBFCs but with public sector constraints. It couldn't exploit regulatory arbitrage like private players nor enjoy regulatory forbearance like banks. This regulatory purgatory made competitive positioning impossible.

The Network Effects That Never Materialized

IFCI's early monopoly should have created powerful network effects—relationships with every major industrial house, understanding of every significant sector, presence across India's industrial geography. These advantages evaporated because IFCI never leveraged them into sustainable competitive moats.

Culture: The Invisible Killer

Perhaps IFCI's deepest problem was cultural. It developed a bureaucratic, risk-averse, entitlement-driven culture that proved impossible to change. Attempts at cultural transformation failed because they tried to impose private sector practices on public sector mindsets without addressing underlying incentives.

The playbook lesson: culture eats strategy for breakfast. No amount of strategic planning, financial engineering, or government support can overcome a dysfunctional culture. IFCI's culture, shaped by decades of monopoly and political interference, ultimately sealed its fate.

The Ultimate Lesson

IFCI's journey teaches that institutional success requires constant evolution, but evolution requires capability for change. Once an institution loses that capability—through political capture, cultural ossification, or strategic confusion—decline becomes inevitable. IFCI lost its capacity for meaningful change sometime in the 1990s. Everything since has been elaborate denial of that fundamental reality.

XI. Analysis & Investment Perspective

No rational investor should touch IFCI stock with a ten-foot pole. That's the honest assessment, but since we're here to analyze, not advocate, let's examine both the bull and bear cases with the clinical detachment of a pathologist performing an autopsy.

The Bull Case (Such As It Is)

The optimist's argument rests on three pillars, each shakier than the last. First, government backing. Promoter Holding: 72.6% means the Indian government won't let IFCI fail messily. There's value in that implicit guarantee—zombie institutions can limp along for decades, generating small but steady returns for patient investors who buy at the right price.

Second, the advisory pivot might work. The November 2024 restructuring removes lending risk entirely. IFCI becomes a fee-earning administrator of government schemes. Boring? Yes. Stable? Potentially. In a world where government spending on development programs is rising, being the implementing agency isn't the worst position. Think of it as a call option on government inefficiency—the more schemes need administration, the more fees IFCI earns.

Third, hidden asset value. IFCI still owns stakes in subsidiaries, real estate, and investments made decades ago. The Stock Holding Corporation stake alone could be worth thousands of crores if properly valued. In a breakup scenario, IFCI might be worth more dead than alive—the classic cigar butt investment that Benjamin Graham would have loved and Warren Buffett learned to hate.

The Bear Case (Reality)

CRAR at -21.85% tells you everything. This isn't a troubled institution; it's an insolvent one kept alive by regulatory forbearance. The negative capital adequacy ratio means losses have eaten through not just profits but the entire capital base. You're not investing in a business; you're betting on government bailouts.

The company has delivered a poor sales growth of -8.22% over past five years. Company has a low return on equity of 1.07% over last 3 years. These aren't metrics of a struggling company finding its feet—they're evidence of an institution in terminal decline. Negative sales growth for five years isn't a rough patch; it's a death spiral. 1% ROE isn't low returns; it's value destruction.

The advisory business model is a fiction. IFCI has no competitive advantage in advisory. It's getting government schemes because the government owns it, not because it's good at implementing them. The moment a digital platform can distribute subsidies more efficiently—which is inevitable—IFCI's last remaining purpose disappears.

Valuation: Price Doesn't Equal Value

At ₹14,374 crores market cap, IFCI trades at roughly 0.6 times book value. Cheap? Only if you believe the book value. Given the history of NPAs, the quality of assets, and the negative CRAR, the book value is likely fictional. The market's discount suggests investors believe real book value is perhaps half of stated value.

The P/E ratio is meaningless when earnings consist mainly of provision reversals and one-time gains. The price-to-sales ratio would be concerning for a growth company; for a shrinking institution, it's irrelevant. Traditional valuation metrics break down when analyzing zombies.

The Comparative Landscape

Every other financial institution in India is a better investment than IFCI. HDFC Bank offers growth with quality. Bajaj Finance provides high-return consumer lending. Even other PSU financiers like REC or PFC have clearer business models and better fundamentals. IFCI stands alone in its combination of weak fundamentals, unclear strategy, and poor execution.

In the NBFC space, IFCI is particularly uncompetitive. While others leverage technology for lower costs and better risk assessment, IFCI operates with the efficiency of a 1980s institution. While others find profitable niches, IFCI stumbles from one failed pivot to another.

The ESG Angle: Lipstick on a Pig

Some might argue IFCI deserves ESG investment for its social mandate—supporting SC entrepreneurs, implementing development schemes. This confuses intent with impact. IFCI's bureaucratic implementation probably destroys more value than it creates. True social impact requires efficiency; IFCI delivers neither social nor financial returns effectively.

The governance issues alone should disqualify IFCI from any ESG portfolio. Board composition driven by political considerations, management changes based on bureaucratic rotations, strategic decisions influenced by political compulsions—this isn't governance; it's institutionalized dysfunction.

Future Scenarios

Scenario 1: Slow Decline (Most Likely) IFCI continues as a government scheme administrator, generating minimal returns, slowly shrinking, neither dying nor thriving. The stock trades between ₹30-60, providing volatility for traders but no returns for investors. This purgatory could last decades.

Scenario 2: Government Bailout and Merger (Possible) The government recapitalizes IFCI and merges it with another PSU financial institution. Shareholders might see a one-time bump, but given the government's track record, any premium would be minimal. Think 10-20% upside, not multibagger returns.

Scenario 3: Privatization (Unlikely) The government reduces stake below 50%, allowing professional management to restructure. This could unlock value, but after multiple failed privatization attempts, believing this time is different requires extraordinary optimism.

Scenario 4: Liquidation (Very Unlikely) The government winds down IFCI, distributing assets to shareholders. Given political sensitivities and employee unions, this is almost impossible. Even if it happened, recovered value would likely disappoint after liquidation costs.

Risk-Reward: Heads You Lose, Tails You Don't Win

The asymmetry is entirely negative. Downside risk is significant—the government could dilute existing shareholders through repeated capital infusions, the advisory business could evaporate, hidden losses could surface. Upside potential is minimal—at best, IFCI becomes a mediocre fee-earning administrator.

The opportunity cost is enormous. Every rupee in IFCI is a rupee not invested in India's actual growth stories—the banks financing consumption, the NBFCs enabling small business, the fintechs revolutionizing payments. IFCI represents the past; investing should be about the future.

The Trader's Perspective