ICICI Bank: From Post-Independence Development Finance to India's Digital Banking Powerhouse

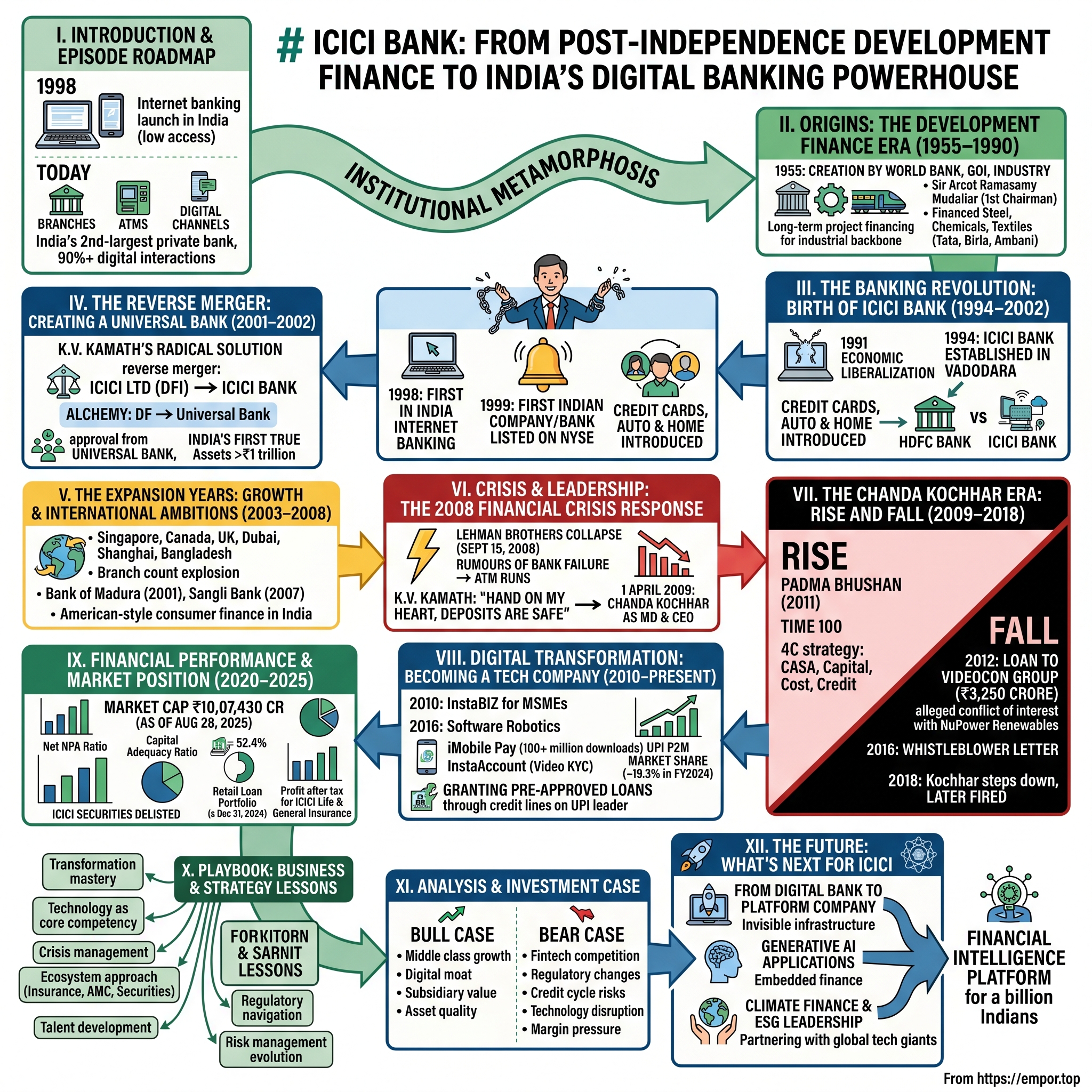

I. Introduction & Episode Roadmap

Picture this: It's 1998, and while most Indian banks are still processing loan applications with carbon paper and ledgers, a young bank in Vadodara launches something radical—internet banking. Not in New York or London, but in India, where less than 0.4% of the population even has internet access. That bank was ICICI, and this audacious move would set the template for everything that followed.

Today, ICICI Bank stands as India's second-largest private sector bank, with 7,066 branches sprawling from Kashmir to Kanyakumari, 13,376 ATMs humming with transactions, and digital channels processing over 90% of all customer interactions. But here's the real question that keeps competitors up at night: How did a World Bank-backed development finance institution, created to fund steel mills and chemical plants in post-independence India, transform into the country's most aggressive digital innovator?

The answer isn't just about technology or market timing. It's a story of institutional metamorphosis so complete that comparing ICICI's origin to its current form is like comparing a caterpillar to a butterfly—except this butterfly learned to code, survived a global financial crisis, weathered a massive governance scandal, and emerged stronger each time.

This is a tale of three distinct acts: First, the development finance era where ICICI helped build India's industrial backbone. Second, the great transformation into universal banking that rewrote the rules of Indian finance. And third, the digital revolution that's still unfolding, where a traditional bank is competing not just with other banks but with Silicon Valley-funded fintechs and global tech giants.

Along the way, we'll encounter visionary leaders like K.V. Kamath who saw banking's digital future before anyone else, witness the spectacular rise and fall of Chanda Kochhar in one of Indian banking's most dramatic governance failures, and decode how ICICI built a technology moat that even HDFC Bank—its eternal rival—struggles to match.

What makes this story particularly fascinating for investors isn't just ICICI's past transformations, but what they reveal about its DNA: an institution that has reinvented itself every decade, consistently betting on the future before that future becomes obvious. As India stands at the cusp of becoming the world's third-largest economy, understanding ICICI's playbook isn't just about analyzing a bank—it's about understanding how financial institutions evolve, adapt, and occasionally, revolutionize entire industries.

II. Origins: The Development Finance Era (1955–1990)

The year was 1955. India had been independent for just eight years, and Prime Minister Jawaharlal Nehru's vision of a self-reliant, industrialized nation faced a fundamental problem: Who would fund the factories, power plants, and infrastructure that would lift 350 million people out of poverty? Traditional banks wouldn't touch long-term industrial projects. Foreign capital was scarce and came with strings attached. Enter the World Bank with a proposition that would reshape Indian finance. The creation of ICICI wasn't just another bureaucratic exercise. ICICI was formed in 1955 at the initiative of the World Bank, the Government of India and representatives of Indian industry. The principal objective was to create a development financial institution for providing medium-term and long-term project financing to Indian businesses. This tripartite structure was revolutionary—combining international expertise, government backing, and private sector dynamism in a way that had never been attempted in post-colonial Asia.

Sir Arcot Ramasamy Mudaliar was elected as the first Chairman of ICICI Ltd. A distinguished civil servant who had served as India's representative to the United Nations, Mudaliar brought gravitas and international credibility to the fledgling institution. Under his leadership, ICICI pioneered a unique model: It was structured as a joint-venture of the World Bank, India's public-sector banks and public-sector insurance companies to provide project financing to Indian industry.

The timing was critical. This was the era of the License Raj, where every business decision required government approval, from importing machinery to expanding production capacity. In this suffocating environment, ICICI occupied a unique position—it had the government's blessing but operated with relative autonomy, thanks to its World Bank parentage and private sector participation.

Until the late 1980s, ICICI primarily focused its activities on project finance, providing long-term funds to a variety of industrial projects. But these weren't just any projects. ICICI was literally building India's industrial backbone—financing steel plants in Bhilai, chemical complexes in Gujarat, textile mills in Tamil Nadu. Each loan wasn't just a financial transaction; it was a bet on India's industrial future.

What made ICICI different from government-owned development banks was its commercial rigor. While institutions like IDBI often made politically motivated loans, ICICI's World Bank DNA insisted on proper project evaluation, cash flow analysis, and risk assessment. This discipline would prove invaluable decades later when ICICI transformed into a commercial bank.

The relationships forged during these early years would define ICICI's future. The Ambanis, Tatas, Birlas—every major industrial house in India had borrowed from ICICI. These weren't just client relationships; they were partnerships in nation-building. When Dhirubhai Ambani needed financing for his polyester plant in the 1970s, ICICI was there. When the Tatas wanted to expand their steel operations, ICICI structured the deal.

By the late 1980s, ICICI had become synonymous with industrial finance in India. But the institution's leadership sensed change in the air. The socialist economic model was creaking, foreign exchange reserves were dwindling, and whispers of economic liberalization were growing louder. The caterpillar was about to enter its chrysalis.

III. The Banking Revolution: Birth of ICICI Bank (1994–2002)

The summer of 1991 changed everything. India, with foreign exchange reserves that could cover barely two weeks of imports, stood at the precipice of economic collapse. Finance Minister Manmohan Singh, in his historic budget speech, uttered words that would reshape the nation: "No power on earth can stop an idea whose time has come." Economic liberalization wasn't just policy—it was survival.

For ICICI, this moment presented an existential question. The controlled economy that justified development finance institutions was disappearing. Companies could now access international capital markets, foreign banks were entering India, and the cozy world of project finance was about to face brutal competition. The institution had two choices: fade into irrelevance or reinvent itself completely. The answer came in 1994, in the unlikely city of Vadodara, Gujarat's cultural capital but hardly a financial hub. ICICI Bank was established by ICICI as a wholly owned subsidiary in 1994 in Vadodara. The choice of location was deliberate—far from the bureaucratic oversight of Mumbai and Delhi, giving the new entity room to experiment and innovate.

But the real masterstroke came with technology. While established banks like State Bank of India were still debating whether computers would replace ledgers, ICICI Bank made a decision that would define its DNA forever. The young bank, barely four years old, launched something that seemed like science fiction to most Indians: internet banking.ICICI Bank launched Internet Banking operations in 1998, making it the first bank in India to offer this service when most Indians hadn't even seen a computer. The audacity of this move cannot be overstated. This wasn't Wells Fargo launching online banking in Silicon Valley—this was a four-year-old bank betting that Indians would embrace digital transactions in a country where electricity itself was unreliable.

But the real coup came a year later. In 1999, ICICI became the first Indian company and the first bank or financial institution from non-Japan Asia to be listed on the New York Stock Exchange. The symbolism was powerful: An Indian financial institution ringing the opening bell at the temple of global capitalism, signaling that India Inc. had arrived on the world stage.

The race with HDFC Bank—founded the same year as ICICI Bank—had begun in earnest. Both were new-age private banks, both targeted the emerging middle class, but their strategies diverged dramatically. HDFC Bank, under Aditya Puri's leadership, focused on operational excellence and branch banking. ICICI Bank, meanwhile, was betting everything on technology and scale.

By 2000, ICICI Bank had introduced credit cards, auto loans, and home mortgages—products that traditional banks considered too risky for the Indian market. The bank's strategy was clear: capture the young professional who was buying their first car, their first home, building their first investment portfolio. These weren't just customers; they were relationships that would grow over decades.

The retail banking infrastructure was being built at breakneck speed. ATMs sprouted across cities—not just in upscale neighborhoods but in markets, near railway stations, in residential complexes. Each ATM was a billboard, a physical manifestation of ICICI's ambition to be everywhere, available 24/7, breaking the tyranny of banking hours.

But beneath this aggressive expansion lay a fundamental question: Could a development finance institution's DNA truly transform into that of a retail bank? The answer would come through one of the most audacious corporate restructurings in Indian banking history.

IV. The Reverse Merger: Creating a Universal Bank (2001–2002)

K.V. Kamath sat in his corner office at ICICI Towers, Mumbai, staring at a whiteboard covered with complex organizational charts. It was late 2000, and the managing director faced a problem that would have seemed absurd just a decade earlier: ICICI, the parent company, was being constrained by its own success. As a development finance institution, it couldn't accept deposits. Meanwhile, its subsidiary, ICICI Bank, had the banking license but lacked the capital and relationships to compete with the State Bank of Indias of the world.

The solution Kamath proposed was radical: kill the parent to strengthen the child. A reverse merger where ICICI Ltd., along with two subsidiaries, would merge into ICICI Bank. The development finance institution with 45 years of history would cease to exist, absorbed into its six-year-old banking subsidiary.

After consideration of various corporate structuring alternatives in the context of the emerging competitive scenario in the Indian banking industry, and the move towards universal banking, the managements of ICICI and ICICI Bank formed the view that the merger of ICICI with ICICI Bank would be the optimal strategic alternative. This wasn't just corporate restructuring—it was institutional alchemy, transforming a lender of last resort into a lender of first choice.

The boardroom debates were intense. Old-timers who had spent careers financing steel plants and power stations worried about becoming retail bankers. Investment bankers questioned whether project finance expertise could translate into credit card risk management. International investors wondered if this complex restructuring would work in India's heavily regulated environment.

In October 2001, the Boards of Directors of ICICI and ICICI Bank approved the merger of ICICI and two of its wholly-owned retail finance subsidiaries, ICICI Personal Financial Services Limited and ICICI Capital Services Limited, with ICICI Bank. The announcement sent shockwaves through Dalal Street. Here was a blue-chip institution essentially admitting that its traditional business model was obsolete.

The merger was approved by shareholders of ICICI and ICICI Bank in January 2002, by the High Court of Gujarat at Ahmedabad in March 2002, and by the High Court of Judicature at Mumbai and the Reserve Bank of India in April 2002. Each approval was a milestone, each court hearing a test of whether India's regulatory system could accommodate such ambitious financial engineering.

The integration challenges were monumental. ICICI brought deep corporate relationships and a culture of long-term thinking. ICICI Bank brought retail aggression and technological sophistication. Merging these cultures was like mixing oil and water—except both liquids were combustible.

Kamath's masterstroke was framing the merger not as a defensive move but as an offensive strategy. The merger would enhance value for ICICI shareholders through access to low-cost deposits and transaction-banking services, while ICICI Bank shareholders would benefit from a large capital base, strong corporate relationships built over five decades, and entry into new business segments.

The numbers told the story: The merged entity would have assets of over ₹1 trillion, making it India's second-largest bank. But more importantly, it would be India's first true universal bank—offering everything from project finance to credit cards, from investment banking to insurance, all under one roof.

Consequent to the merger, the ICICI group's financing and banking operations, both wholesale and retail, were integrated in a single entity. This wasn't just a merger; it was the birth of a new species in Indian banking—a hybrid that combined the stability of traditional banking with the innovation of a fintech before fintech was even a word.

The market's verdict was swift and positive. ICICI Bank's stock surged, market share in retail banking grew, and corporate clients now had access to a full suite of banking products. The transformation was complete: The caterpillar had emerged as a butterfly, ready to soar into banking's new digital age.

V. The Expansion Years: Growth & International Ambitions (2003–2008)

The year 2003 marked a turning point. With the merger complete and integration challenges largely resolved, ICICI Bank was ready to paint on a larger canvas. The strategy was audacious: become not just an Indian bank with international presence, but a truly global institution with Indian roots. In 2003, ICICI Bank expanded its operations to Canada, the UK, and Singapore, and also established representative offices in Dubai and Shanghai. The bank established an office in Bangladesh in 2004. This wasn't just opening branches abroad—it was following the Indian diaspora, capturing remittance flows, and building bridges for Indian corporations going global.

The Singapore branch, established in August 2003, became ICICI's beachhead in Asia. It wasn't just serving NRIs; it was financing trade between India and Southeast Asia, providing treasury services, and establishing ICICI as a pan-Asian player. The Canada subsidiary, incorporated in December 2003, targeted the massive Indo-Canadian community, offering everything from mortgages in Toronto to remittance services to Punjab.

Back home, the expansion was even more aggressive. Branches were opening at a rate of two per day during peak periods. The strategy was simple but expensive: be everywhere. Shopping malls, residential complexes, business districts—if there was economic activity, ICICI wanted to be there. The branch count exploded from a few hundred to thousands in just five years.

The retail product suite was expanding rapidly. Credit cards with rewards programs, auto loans with same-day approval, personal loans disbursed in 48 hours—ICICI was bringing American-style consumer finance to India. The bank's "No Questions Asked" personal loans became legendary, both for their convenience and, later, for the credit quality issues they would create. The acquisition strategy was equally ambitious. In 2001, ICICI acquired the Bank of Madura, which was established in 1943. This wasn't just buying branches; it was acquiring a 58-year-old franchise with deep roots in Tamil Nadu. In 2007, the bank acquired Sangli Bank, which had 158 branches in Maharashtra and 31 branches in Karnataka, further strengthening its presence in western India.

Technology investments during this period were laying the foundation for future dominance. While competitors were still debating whether to invest in core banking systems, ICICI was already thinking about mobile banking, algorithmic credit scoring, and automated loan processing. The bank's IT budget rivaled that of some technology companies.

But this aggressive expansion came with a cost. Credit quality was deteriorating as the bank chased growth. The "No Questions Asked" personal loans were turning into "No Answers Found" when it came to recoveries. Retail banking, it turned out, wasn't just about disbursing loans—it was about collecting them too.

By 2008, ICICI Bank had become a formidable force: Over 1,400 branches, presence in 18 countries, a product suite that rivaled any global bank. But storm clouds were gathering. The global financial system was about to face its biggest test since the Great Depression, and ICICI Bank, with its aggressive growth strategy and international exposure, would find itself in the eye of the storm.

VI. Crisis & Leadership: The 2008 Financial Crisis Response

September 15, 2008, 9:30 PM IST. Chanda Kochhar, then Joint Managing Director of ICICI Bank, was in her Mumbai office when the news flashed across Bloomberg terminals: Lehman Brothers had filed for bankruptcy. The unthinkable had happened—a 158-year-old Wall Street institution had collapsed. Within hours, her phone began ringing with a question that would define the next 48 hours: "What is ICICI's exposure to Lehman?"

The panic was palpable. ICICI Bank, with its aggressive international expansion and complex derivative positions, was seen as the Indian bank most vulnerable to the global contagion. Rumors began circulating on SMS and email—that new weapon of mass hysteria in the digital age—claiming ICICI Bank had massive exposure to toxic assets. During the 2008 financial crisis, customers rushed to ICICI ATMs and branches in some locations due to rumours of bank failure. The scenes were surreal—educated professionals, who had never stepped into a branch in years, standing in queues to withdraw their deposits. Social media didn't exist yet, but SMS forwards were creating a digital bank run.

On 15 September 2008, the announcement of US-based investment banking major Lehman Brothers that it was closing down due to its exposure to subprime mortgage loans had a huge impact on ICICI Bank. Soon after, on 16 September 2008, Chanda Kochhar, MD and CEO, ICICI Bank, issued a press statement stating that the bank's UK subsidiary had just a 1 percent exposure to Lehman Brothers.

But the damage was done. The statement, meant to reassure, only confirmed that there was some exposure. In crisis communication, sometimes acknowledging a small problem can create perception of a bigger one. The queues at branches grew longer.

The Reserve Bank of India issued a clarification on the financial strength of ICICI Bank to dispel the rumours. This was unprecedented—the central bank publicly vouching for a private bank. Behind the scenes, Finance Minister P. Chidambaram was working the phones, coordinating between RBI, ICICI management, and even considering more dramatic interventions if needed.

K.V. Kamath, then Chairman, finally went on television with a message that would become legendary in Indian banking circles: "Hand on my heart, the deposits are safe." The personal guarantee from one of India's most respected bankers, combined with RBI's backing, finally stemmed the panic. The crisis also marked a changing of the guard. On 19 December 2008 ICICI bank named Chanda Kochhar as the successor of KV Kamath as its Managing Director and CEO from 1 April 2009. She is the youngest and first woman CEO of ICICI bank. At 47, Kochhar was taking the helm at one of the most challenging moments in global finance.

Her appointment was both historic and strategic. As the bank's Chief Financial Officer during the crisis, she had proven her mettle in managing liquidity, communicating with investors, and maintaining operational stability. But more importantly, she represented a new generation of leadership—one that had grown up in liberalized India, comfortable with both traditional banking and digital innovation.

The immediate priority was clear: restore confidence, strengthen the balance sheet, and prepare for the inevitable economic slowdown. ICICI Bank pulled back from aggressive lending, focused on deposit mobilization, and quietly wrote off bad loans. The go-go years were over; it was time for consolidation.

But even as the bank navigated the crisis, seeds of future problems were being sown. The aggressive growth of the previous decade had created a complex web of relationships, loans, and business dealings that would later come back to haunt the institution and its leadership.

VII. The Chanda Kochhar Era: Rise and Fall (2009–2018)

Chanda Kochhar's corner office on the 12th floor of ICICI Towers commanded a sweeping view of Mumbai's Bandra-Kurla Complex, the gleaming financial district that had risen from swampland to rival Nariman Point. It was April 2009, her first day as CEO, and the symbolism wasn't lost on her—like BKC itself, ICICI Bank needed to be rebuilt from the ground up after the financial crisis. Her early years as CEO were marked by steady achievements. Kochhar received an honorary doctorate from Carleton University, Canada in 2014, in recognition of her pioneering work in the financial sector, effective leadership in a time of economic crisis and support for engaged business practices. She was conferred with the Padma Bhushan, one of India's highest civilian honours, in 2011. The recognition wasn't just personal—it validated ICICI Bank's emergence from the crisis stronger than before.

Under her leadership, ICICI Bank focused on what she called the "4C strategy": CASA (Current Account Savings Account) growth, Capital conservation, Cost control, and Credit quality. The aggressive expansion of the previous decade gave way to measured growth. Branch openings slowed, but digital investments accelerated. The bank that had once chased every customer now became selective, focusing on profitable relationships.

The retail franchise, which Kochhar had built from scratch in the early 2000s, became the crown jewel. Credit cards, home loans, and wealth management services generated steady fees. The corporate banking business, while smaller, focused on high-quality names and transaction banking. The strategy was working—market share was stable, profits were growing, and the stock price reflected investor confidence.

But beneath this success story, a time bomb was ticking. In 2012, Chanda Kochhar-led ICICI Bank sanctioned a massive loan of ₹3,250 crore to the Videocon Group, a consumer electronics and oil exploration company owned by Venugopal Dhoot. This loan was part of a ₹40,000 crore debt financing deal arranged by a consortium of 20 banks for Videocon. The contribution of ICICI Bank was one of the largest in this syndicated loan.

What seemed like a routine corporate loan would later become the epicenter of one of Indian banking's biggest scandals. The allegations were explosive: Videocon group promoter Venugopal Dhoot provided crores of rupees allegedly to NuPower Renewables Pvt Ltd (NRPL), a firm he had set up with Chanda Kochhar's husband Deepak Kochhar and two relatives six months after the Videocon group got ₹3,250 crore as loan from ICICI Bank in 2012. He allegedly transferred proprietorship of the company to a trust owned by Deepak Kochhar for ₹9 lakh.

The unraveling began in 2016 when whistleblower Arvind Gupta wrote to the Prime Minister's Office alleging conflict of interest. Initially, the allegations were dismissed. ICICI Bank's board reviewed its processes and gave Kochhar a clean chit. But the story wouldn't die. In March 2018, investigative journalists began connecting the dots, tracing complex financial transactions through shell companies and trusts.

The pressure mounted. What had been whispers in banking circles became front-page news. The woman who had been featured in TIME's 100 Most Influential People, who had received the Padma Bhushan, was now fighting for her reputation. On October 4, 2018, Kochhar stepped down from her position, citing personal reasons.

But resignation wasn't the end. She resigned from her positions in 2018 due a case of conflict of interest. Subsequently, she was fired by ICICI Bank, a decision which was later upheld by the Supreme Court of India. The bank's internal inquiry, led by retired Supreme Court judge Justice B.N. Srikrishna, found violations of the bank's code of conduct.

The fall was complete. From being India's most powerful woman banker to facing criminal charges, Kochhar's journey became a cautionary tale about corporate governance, conflict of interest, and the importance of ethical leadership. The scandal not only destroyed her legacy but also cast a shadow over ICICI Bank's reputation that would take years to overcome.

VIII. Digital Transformation: Becoming a Tech Company (2010–Present)

While the Videocon scandal dominated headlines, something remarkable was happening in ICICI Bank's technology labs in Hyderabad. Engineers who had once worked for Google and Amazon were building something that would fundamentally transform Indian banking. The vision was audacious: don't just digitize banking—reimagine it entirely.ICICI Bank is investing in emerging technologies to accelerate its digital transformation strategy. AI, big data, blockchain, cloud, and payments are among the key technologies under focus for the company. The annual ICT spending of ICICI Bank was estimated at $1.1 billion in 2024. This isn't just IT spending—it's strategic investment in becoming a technology company that happens to have a banking license.

The transformation began with a simple observation: customers were using branches for transactions they could do online, if only the online experience was better. So ICICI built InstaBIZ in 2010, empowering 8 million+ MSMEs with instant digital current accounts. No paperwork, no branch visits, just instant account opening from a mobile phone.

In 2016, the bank introduced Software Robotics for 24/7 back-office operations. These weren't physical robots but software bots that could process loan applications, verify documents, and handle customer service queries without human intervention. A loan that once took 7 days to process could now be approved in 7 minutes.

The UPI revolution found ICICI perfectly positioned. The Bank's market share in value of UPI P2M transactions is about 19.3% in fiscal 2024. But ICICI didn't just adopt UPI—it innovated on top of it. Punjab National Bank, Axis Bank, State Bank of India, and ICICI Bank had already started using the UPI credit line product on a trial basis. When it comes to granting pre-approved loans through credit lines on UPI, ICICI Bank is the industry leader.

The crown jewel of ICICI's digital arsenal is iMobile Pay, combining UPI, investments, loans, and insurance in one app with 100+ million downloads. This isn't just a banking app—it's a financial super-app that competes with PhonePe and Google Pay while offering the trust and regulatory protection of a full-service bank.

ICICI has streamlined the account opening process with its 'InstaAccount' service, allowing customers to open a fully operational bank account in a few minutes, completely online, without any paperwork. The technology stack behind this—combining video KYC, AI-based document verification, and real-time account activation—is more sophisticated than what most Silicon Valley fintechs have built.

Digital channels continue to account for over 90% of financial and non-financial transactions. But this isn't just about moving transactions online—it's about reimagining what banking means. AI chatbots handle customer queries, machine learning models predict loan defaults before they happen, and blockchain technology secures international trade finance.

The bank's partnerships with fintechs are particularly strategic. Rather than viewing them as competition, ICICI has built an ecosystem where startups can plug into its banking infrastructure through APIs. A fintech can focus on customer acquisition and user experience while ICICI handles the regulated banking backend—a win-win that has created one of India's most vibrant financial ecosystems.

Looking ahead, ICICI's technology investments are becoming even more ambitious. The bank is experimenting with generative AI for personalized financial advice, quantum computing for risk modeling, and embedded finance that puts banking services inside non-banking apps. The vision is clear: Banking shouldn't be something you do; it should be something that happens invisibly in the background of your digital life.

IX. Financial Performance & Market Position (2020–2025)

The numbers were staggering. Market Cap ₹ 10,07,430 Cr, up from virtually nothing when ICICI Bank was just a development finance institution. ICICI Bank has a market cap or net worth of $114.06 billion as of August 28, 2025, making it one of Asia's most valuable financial institutions. But raw market capitalization tells only part of the story.

Profit before tax excluding treasury grew by 12.8% year-on-year to ₹ 15,289 crore (US$ 1.8 billion) in Q3-2025. Core operating profit grew by 13.1% year-on-year to ₹ 16,516 crore (US$ 1.9 billion) in Q3-2025. These weren't just numbers—they represented the culmination of three decades of transformation, from financing steel mills to processing millions of UPI transactions per second.

The efficiency metrics told an even more compelling story. Net NPA ratio declined to 0.39% at March 31, 2025 from 0.42% at December 31, 2024. For context, when Chanda Kochhar took over during the 2008 crisis, NPAs were threatening to overwhelm the entire banking system. Provisioning coverage ratio on non-performing loans was 76.2% at March 31, 2025—a fortress-like buffer against potential credit losses.

Capital adequacy painted a picture of strength. Total capital adequacy ratio was 16.55% and CET-1 ratio was 15.94%, on a standalone basis, at March 31, 2025 after reckoning the impact of proposed dividend. These weren't just regulatory requirements being met—they were war chests for future expansion, ammunition for the next phase of digital transformation.

The Board has recommended a dividend of ₹ 11 per share for FY2025, continuing ICICI's tradition of rewarding shareholders even while investing heavily in technology and expansion. The dividend yield might seem modest compared to some peers, but for growth investors, the retained earnings were being deployed at ROEs that traditional banks could only dream of.

The retail portfolio's evolution was particularly striking. The retail loan portfolio grew by 10.5% year-on-year and 1.4% sequentially, and comprised 52.4% of the total loan portfolio at December 31, 2024. From zero retail presence in the 1990s to becoming predominantly a retail bank—this transformation would be studied in business schools for decades.

But the real story was in the segments driving growth. The business banking portfolio grew by 31.9% year-on-year and 6.4% sequentially at December 31, 2024. This wasn't just lending to SMEs—it was building India's entrepreneurial ecosystem, one loan at a time. The InstaBIZ platform had democratized business banking in ways that would have seemed impossible in the License Raj era.

The subsidiary performance added another dimension to the growth story. The annualised premium equivalent of ICICI Prudential Life Insurance (ICICI Life) was ₹ 10,407 crore (US$ 1.2 billion) in FY2025 compared to ₹ 9,046 crore (US$ 1.1 billion) in FY2024. Value of New Business (VNB) of ICICI Life was ₹ 2,370 crore (US$ 277 million) in FY2025 compared to ₹ 2,227 crore (US$ 261 million) in FY2024.

The profit after tax of ICICI General grew by 30.7% to ₹ 2,508 crore (US$ 293 million) in FY2025 compared to ₹ 1,919 crore (US$ 225 million) in FY2024. The insurance businesses weren't just subsidiaries—they were integral parts of a financial ecosystem that touched every aspect of customers' financial lives.

ICICI Securities' story took an interesting turn. Pursuant to the Scheme of Arrangement amongst ICICI Bank Limited and ICICI Securities Limited and their respective shareholders, ICICI Securities Limited has been delisted from stock exchanges on March 24, 2025 and became a wholly-owned subsidiary of the Bank. This wasn't just corporate restructuring—it was recognition that in the age of super-apps and integrated financial services, having a separately listed securities business made less strategic sense.

The geographic diversification continued to evolve. While the international push of the 2000s had been scaled back post-2008, ICICI maintained strategic presence in key markets, focusing on NRI banking and trade finance rather than trying to be a global universal bank. The lessons of overreach had been learned.

Looking at valuation metrics, the market was pricing in continued excellence. Trading at multiples that reflected both its digital leadership and growth potential, ICICI Bank had become a proxy for India's financial sector transformation. Foreign investors who wanted exposure to India's growing middle class and digital economy invariably had ICICI Bank in their portfolios.

X. Playbook: Business & Strategy Lessons

The ICICI playbook reads like a masterclass in institutional evolution. Each transformation wasn't just reactive—it anticipated where Indian finance was heading and positioned the bank to lead rather than follow.

Transformation mastery stands as the most remarkable achievement. Three complete metamorphoses in six decades—from development bank to universal bank to digital platform—each requiring not just strategic vision but cultural revolution. The ability to kill successful business models before they became obsolete, as seen in the reverse merger of 2002, demonstrated rare institutional courage.

Technology as core competency emerged not from Silicon Valley consultants but from deep conviction. When ICICI launched internet banking in 1998, it wasn't copying Western banks—it was betting that India would leapfrog traditional banking entirely. The ₹1.1 billion annual technology spend isn't an expense; it's the price of admission to banking's future.

Crisis management became part of ICICI's DNA through repeated tests. The 2008 financial crisis response—transparent communication, liquidity management, capital preservation—became the template. But the real test came with the Videocon scandal. The bank's ability to separate institutional credibility from individual failures, to reform governance while maintaining business momentum, showed remarkable resilience.

Ecosystem approach differentiated ICICI from traditional banks. Insurance, asset management, securities—these weren't just cross-selling opportunities but integrated financial solutions. A customer getting a home loan could buy insurance, invest the surplus in mutual funds, trade stocks, all within the ICICI ecosystem. This wasn't just convenient—it created switching costs that traditional banks couldn't match.

Talent development created a finishing school for Indian banking. Alumni of ICICI have gone on to lead banks, start fintechs, run mutual funds. The aggressive, entrepreneurial culture that Kamath fostered in the 1990s created a generation of leaders who thought differently about finance.

Regulatory navigation showed sophistication in working within India's complex financial system. From convincing RBI to allow the reverse merger to managing through demonetization to adapting to UPI's disruption, ICICI demonstrated that innovation and compliance weren't mutually exclusive.

Risk management evolution tracked the bank's journey from concentrated corporate loans to granular retail portfolios. The credit scoring models, collection mechanisms, and portfolio diversification strategies developed over two decades became industry benchmarks. The shift from relationship-based lending to data-driven decisions marked a fundamental change in Indian banking.

The playbook's most important lesson: transformation is continuous. ICICI never arrived at a destination; it kept moving toward the next horizon.

XI. Analysis & Investment Case

The Bull Case rests on structural trends that seem unstoppable. India's middle class, projected to reach 547 million by 2030, needs mortgages, car loans, credit cards, insurance—exactly ICICI's sweet spot. The financialization of savings, with households moving from gold and real estate to financial assets, creates massive wealth management opportunities.

Digital leadership provides a moat that's widening. While competitors scramble to build digital capabilities, ICICI has already moved to the next phase—embedded finance, AI-driven personalization, ecosystem plays. The technology investments of the past decade are now generating returns that drop straight to the bottom line.

The subsidiary value remains underappreciated. ICICI Prudential Life, ICICI Lombard General Insurance, ICICI AMC—each could be a standalone success story. The sum-of-parts valuation suggests the market isn't fully pricing in this diversification.

Asset quality has become a strength rather than concern. The retail focus, improved underwriting, and collection mechanisms have created a loan book that can weather economic cycles. The provision coverage ratio provides additional comfort.

Market share gains seem inevitable. As public sector banks struggle with legacy issues and smaller private banks lack scale for technology investments, ICICI and HDFC Bank are consolidating the profitable segments of Indian banking.

The Bear Case can't be ignored. Competition from well-funded fintechs is real. Companies like PhonePe and Google Pay have shown that payments—once a banking moat—can be unbundled. While ICICI has responded well, the threat of further disintermediation remains.

Regulatory changes could impact profitability. The RBI's occasional interventions on fees, interest rates, and lending practices create uncertainty. The push for financial inclusion, while socially important, often comes at the cost of profitability.

Credit cycle risks persist despite improvements. India's retail credit boom has never been tested through a serious economic downturn. Rising interest rates and inflation could stress the retail portfolio in ways not captured by historical models.

Technology disruption could accelerate. Central Bank Digital Currency (CBDC), blockchain-based cross-border payments, or new forms of digital assets could disrupt traditional banking revenue streams. While ICICI is well-positioned, the pace of change creates uncertainty.

Margin pressure seems structural. The days of wide net interest margins are likely over. Competition for deposits, regulatory caps on lending rates, and the commoditization of basic banking services all point to margin compression.

Valuation and Returns present a nuanced picture. The stock's performance reflects both achievement and expectation. Trading at premium multiples to book value acknowledges the franchise value, but also prices in continued execution excellence.

ROE trajectory remains impressive but faces headwinds. The easy gains from retail expansion and digital adoption are behind. Future ROE improvement requires either margin expansion (unlikely) or further efficiency gains (challenging but possible).

The growth versus profitability trade-off becomes more acute. Maintaining market share requires continued technology investment and competitive pricing. Improving profitability might mean ceding growth to hungrier competitors.

XII. The Future: What's Next for ICICI

The next decade will test whether ICICI can execute a fourth transformation—from digital bank to platform company. The vision is already taking shape: Banking becomes invisible infrastructure while ICICI orchestrates financial services across the ecosystem.

Generative AI applications are moving from experiment to production. Imagine a personal CFO in your pocket, analyzing spending patterns, suggesting investments, negotiating better rates, all powered by AI that knows your financial life intimately. ICICI's data advantage—millions of customers, billions of transactions—becomes the training ground for AI that no fintech can match.

Embedded finance represents the next frontier. Why go to a bank app for a loan when it can be embedded in the car dealer's app? ICICI is building the rails for this future, where banking happens everywhere but the bank itself becomes invisible.

International expansion will be selective and strategic. Rather than chasing global universal bank dreams, ICICI will likely focus on specific corridors—India-UAE remittances, India-Singapore trade finance, serving the global Indian diaspora. The ambition is calibrated by experience.

Climate finance and ESG leadership aren't just compliance requirements—they're business opportunities. Financing India's energy transition, from solar farms to electric vehicles, positions ICICI at the intersection of profit and purpose. The green bonds, sustainability-linked loans, and carbon credit mechanisms being developed today will be massive markets tomorrow.

The threat from global tech giants remains real but manageable. While Amazon, Google, and Apple have financial ambitions, regulatory moats and local knowledge provide protection. ICICI's strategy of partnering rather than competing, of being the regulated backbone for tech companies' financial ambitions, shows pragmatic wisdom.

Digital banking licenses could reshape competition. If RBI issues digital-only banking licenses, new competitors could emerge without legacy branch costs. But ICICI's digital capabilities mean it could launch its own digital-only subsidiary, competing with itself before others compete with it.

The platform future isn't just about technology—it's about reimagining the role of a bank. From a place you go to get money to an intelligence layer that optimizes your financial life. From a product provider to a life partner. From a bank to a platform.

XIII. Outro & Resources

The ICICI story defies simple categorization. It's simultaneously a development success story, a privatization triumph, a digital transformation case study, and a governance cautionary tale. The institution that helped build India's industrial base now helps millions buy their first homes, start businesses, and build wealth.

Three surprises stand out from this deep dive. First, the consistency of transformation—ICICI has reinvented itself every decade, suggesting this isn't luck but organizational capability. Second, the technology investments preceded the returns by years, sometimes decades, requiring patient capital and visionary leadership. Third, the resilience through crises—from 2008 to Videocon—shows institutional strength beyond individual leaders.

What can other banks learn? That transformation is possible but painful. That technology investment must be massive and sustained. That governance failures can destroy decades of reputation building. That the future of banking might not involve banks as we know them.

The broader implications for India's financial sector are profound. If ICICI and HDFC Bank continue consolidating market share, India could see an oligopolistic banking structure similar to Canada or Australia. The question is whether this concentration is good for financial inclusion and innovation.

For investors, ICICI Bank represents a complex proposition. It's a bet on India's economic future, on continued digital adoption, on management execution, and on regulatory stability. The multiples reflect these multiple bets, pricing in success across all dimensions.

The ultimate question isn't whether ICICI Bank will succeed—it's what success means in a world where banking is being unbundled, rebundled, and fundamentally reimagined. The institution that transformed from development bank to digital leader faces its next transformation: becoming something that doesn't yet have a name.

Perhaps that's the real lesson of the ICICI story. In finance, as in evolution, it's not the strongest that survive but the most adaptable. And few institutions have proven more adaptable than this shape-shifting giant of Indian finance.

As we close this episode, remember that every transformation begins with a simple question: What if things could be different? ICICI has been asking and answering that question for seven decades. The next chapter of that answer is being written now, in code and algorithms, in AI models and blockchain protocols, in the dreams of entrepreneurs and the swipes of smartphones.

The caterpillar that became a butterfly is preparing to transform once again. What emerges might not be a bank at all, but something entirely new—a financial intelligence platform for a billion Indians navigating their economic futures. And that story, still being written, might be the most remarkable transformation of all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube