Axis Bank: From UTI's Shadow to Digital Banking Powerhouse

I. Introduction & Episode Roadmap

In the pantheon of Indian private sector banking, Axis Bank stands as a testament to transformation—a financial institution that has reinvented itself multiple times over three decades, emerging as India's third-largest private sector bank by assets and fourth-largest by market capitalization. With a balance sheet exceeding ₹16 trillion and a market presence that spans from Mumbai's financial corridors to rural villages in Bihar, Axis Bank's journey is nothing short of remarkable.

The story of Axis Bank is fundamentally a story about evolution—from a government-backed entity born out of India's largest mutual fund to a digital-first powerhouse competing toe-to-toe with HDFC and ICICI. It's a narrative that encompasses dramatic leadership transitions, strategic pivots from corporate to retail banking, and ultimately, a bold bet on digital transformation that has redefined what it means to be a bank in 21st century India.

How did a bank that started as UTI Bank—essentially an extension of a government mutual fund—transform itself into India's digital banking pioneer? How did it navigate the treacherous waters of Indian banking through multiple economic cycles, regulatory changes, and technological disruptions? And perhaps most importantly, what can entrepreneurs and investors learn from its playbook of reinvention?

This is a story that spans multiple eras of Indian banking: the liberalization years of the 1990s when private banks were first allowed to flourish, the infrastructure boom of the 2000s that created massive corporate lending opportunities, the retail banking revolution of the 2010s, and now, the digital transformation that's reshaping finance globally. Each era brought its own challenges and opportunities, and Axis Bank's response to these shifts offers profound lessons in corporate strategy and adaptation.

At its core, this is a story about three transformative leaders—P.J. Nayak, who built the corporate fortress; Shikha Sharma, who pivoted to retail; and Amitabh Chaudhry, who's orchestrating the digital revolution. Each brought their own vision, faced their own crises, and left their distinct mark on the institution. Their successes and struggles illuminate broader truths about leadership transitions in large financial institutions.

The Axis Bank story also offers a window into India's economic transformation. From serving large corporates building India's infrastructure to enabling millions of retail customers to access credit, from traditional branch banking to becoming a leader in UPI transactions, Axis Bank's evolution mirrors India's own journey from a controlled economy to an aspirational, digitally-enabled marketplace.

What makes this story particularly compelling is its timeliness. As we sit in 2025, with artificial intelligence reshaping banking, digital currencies emerging, and fintech startups challenging traditional models, Axis Bank's transformation offers crucial insights into how established financial institutions can not just survive but thrive in an era of disruption. The recent acquisition of Citibank's consumer business and the push into cloud computing demonstrate that even thirty-year-old institutions can embrace radical change.

This analysis will take you through the complete arc of Axis Bank's journey—from its genesis as UTI Bank through its current position as a digital banking leader. We'll examine the strategic decisions, the pivotal moments, the near-misses, and the masterstrokes that shaped this institution. Along the way, we'll extract the patterns and principles that can guide anyone thinking about transformation, whether in banking or beyond.

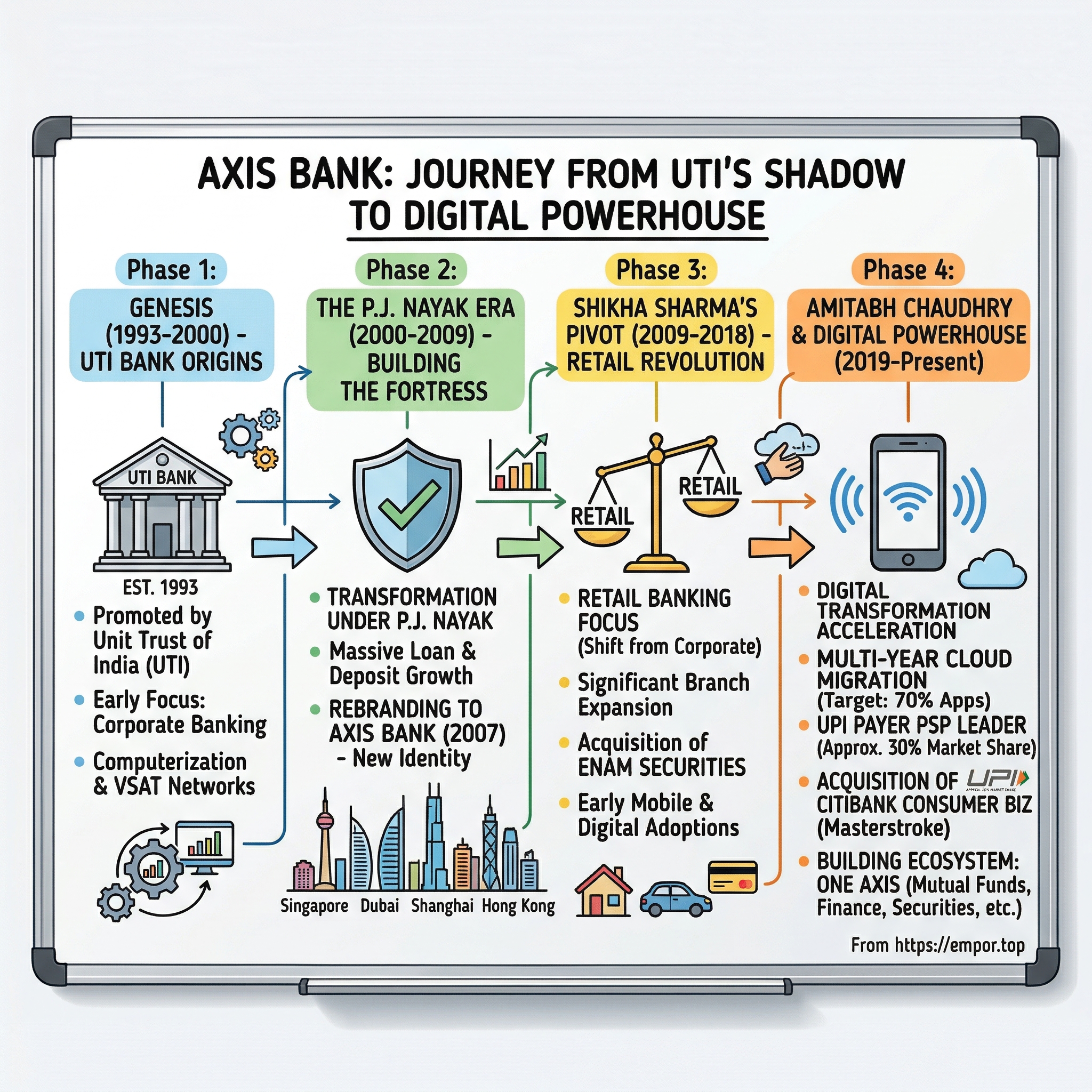

II. Genesis: The UTI Foundation & Early Years (1993–2000)

The December winter of 1993 marked a watershed moment in Indian banking history. As the Reserve Bank of India opened its doors to private sector participation for the first time since bank nationalization in 1969, an unlikely protagonist emerged from the corridors of India's most powerful financial institution. The bank was founded on 3 December 1993 as UTI Bank as a part of Unit Trust of India, a Government of India entity, and started its operations in 1994, becoming among the first private sector banks set up under the 1993 RBI guidelines.

The story begins not in a corporate boardroom but in the offices of Unit Trust of India, a behemoth that had fundamentally shaped how ordinary Indians thought about investing. UTI was a public sector investment institution set up by RBI in 1963. It was the largest and for a long time, the only mutual fund available to Indian citizens, set up by the Reserve Bank of India and functioned under the Regulatory and administrative control of the Reserve Bank of India. With a staggering 35 million unitholders and a corpus of Rs. 48,000 crores by the early 1990s, UTI had become synonymous with middle-class India's investment dreams.

The genesis of UTI Bank was thus unlike any other private bank being conceived at the time. While HDFC Bank and ICICI Bank emerged from housing finance and development finance institutions respectively, UTI Bank was born with a unique advantage—it carried the trust and recognition of millions of Indian savers who had invested their life savings in UTI's schemes over three decades. This wasn't just a new bank; it was an extension of an institution that had already touched millions of Indian households.

The Bank was promoted in 1993 by SUUTI, LIC and other general insurance companies, jointly by Specified Undertaking of Unit Trust of India (SUUTI) (then known as Unit Trust of India), Life Insurance Corporation of India (LIC), General Insurance Corporation of India (GIC), National Insurance Company Ltd.(NIC), The New India Assurance Company Ltd.(NIA), The Oriental Insurance Company Ltd. (OIC) and United India Insurance Company Ltd.(UIIC). This consortium of India's largest public sector financial institutions gave UTI Bank an institutional heft that few private banks could match.

The timing couldn't have been more fortuitous. India was in the midst of historic economic liberalization. The Narasimha Rao government, with Dr. Manmohan Singh as Finance Minister, had unleashed reforms that were dismantling the License Raj and opening up the economy. The banking sector, long dominated by inefficient public sector banks, was crying out for innovation and efficiency. The RBI's 1993 guidelines for new private sector banks represented a fundamental shift in India's financial architecture—for the first time in over two decades, private capital was being invited back into banking.

UTI Bank opened its registered office in Ahmedabad and corporate office in Mumbai in December 1993. The first branch was inaugurated on 2 April 1994 in Ahmedabad by Dr. Manmohan Singh, the then Finance Minister of India. The symbolism was powerful—here was the architect of India's economic reforms personally inaugurating a bank that represented the new India he envisioned.

What made UTI Bank's early strategy particularly astute was its ability to leverage the UTI brand while building a modern banking infrastructure. The bank didn't just inherit a name; it inherited trust. In a country where banking relationships were built over generations, UTI Bank started with a 30-year head start. Rural teachers who had invested in UTI schemes, urban middle-class families who swore by UTI's returns, small business owners who trusted UTI with their surplus—all became natural customers for the new bank.

The operational philosophy in these early years was conservative yet ambitious. The bank focused initially on corporate banking, leveraging relationships that UTI had built with Indian corporations over decades. Large companies that had invested their treasury surpluses with UTI naturally gravitated toward UTI Bank for their banking needs. This wasn't the retail banking push that would come later; this was about establishing credibility in the corporate corridors of Nariman Point and Connaught Place.

The technology infrastructure that UTI Bank built from day one was remarkably forward-thinking for its time. While public sector banks struggled with ledger books and manual processes, UTI Bank invested heavily in computerization. Every branch was connected through VSATs (Very Small Aperture Terminals), a satellite-based communication technology that was cutting-edge in the mid-1990s. This wasn't just about efficiency; it was about building a bank for the future.

The human capital strategy was equally distinctive. UTI Bank recruited aggressively from India's premier business schools and chartered accountancy institutes. Unlike public sector banks where careers progressed at a glacial pace, UTI Bank offered rapid growth, performance-linked compensation, and a corporate culture that was more Silicon Valley than South Block. Young professionals who joined UTI Bank in 1994-95 often found themselves heading branches or divisions within five years—unthinkable in traditional Indian banking.

By 1996, UTI Bank had established itself as a serious player in corporate banking. The bank's corporate loan book grew at an impressive clip, funding everything from textile mills in Coimbatore to software companies in Bangalore. The non-performing asset ratio was negligible—a testament to the conservative underwriting standards that would become a hallmark of the institution. The bank was profitable from its second year of operations, a remarkable achievement for a startup in the capital-intensive banking sector.

The geographic expansion strategy during these early years was calibrated and strategic. Rather than pursuing a branch-in-every-town approach, UTI Bank focused on India's commercial centers. Mumbai, Delhi, Chennai, Kolkata, Bangalore—these metros became the backbone of the bank's network. Each branch was conceived not as a mere transaction point but as a relationship center, staffed with relationship managers who understood that banking was as much about trust as it was about interest rates.

One of the most innovative aspects of UTI Bank's early strategy was its approach to technology partnerships. In 1997, the bank partnered with international technology providers to launch one of India's first Internet banking platforms. While Internet penetration in India was still minimal, this move signaled the bank's intent to be at the forefront of digital banking—a prescient bet that would pay rich dividends two decades later.

The regulatory environment of the late 1990s presented both opportunities and challenges. The RBI was still finding its feet in supervising private sector banks, leading to a regulatory framework that was sometimes inconsistent. UTI Bank navigated these waters carefully, maintaining excellent relationships with regulators while pushing the boundaries of innovation. The bank's compliance culture, established early, would prove invaluable as banking regulations became more complex.

The Asian Financial Crisis of 1997-98 provided an early test of the bank's risk management framework. While many Asian banks collapsed under the weight of bad loans and currency mismatches, UTI Bank emerged unscathed. The crisis actually strengthened the bank's position as foreign banks retrenched and corporate India sought stable banking partners. The bank's conservative approach to foreign exchange exposure and its focus on domestic corporate lending proved to be winning strategies.

As the decade drew to a close, UTI Bank had established itself as more than just another private sector bank. With assets crossing Rs. 10,000 crores and a network of over 100 branches, it had become a force to reckon with in Indian banking. The bank's return on equity consistently exceeded 20%, making it one of the most profitable banks in India. More importantly, it had built the foundations—technological, human, and strategic—that would enable its transformation in the coming decades.

The cultural DNA established during these formative years would prove crucial to the bank's future evolution. This was a bank that believed in technology before digital became fashionable, that valued relationships over transactions, that balanced growth with prudence. The approximately 3,000 employees who worked at UTI Bank by the year 2000 weren't just bankers; they were evangelists for a new way of banking in India.

Looking back, the period from 1993 to 2000 wasn't just about building a bank; it was about proving that Indian private sector banking could match and exceed global standards. UTI Bank's success during these years helped pave the way for the broader transformation of Indian banking. It demonstrated that efficiency and profitability weren't incompatible with the Indian context, that technology could transform banking even in a country where millions remained unbanked, and that professional management could create value in a sector long dominated by government ownership.

The foundation years also established patterns that would recur throughout the bank's history—bold vision coupled with conservative execution, technology innovation balanced with relationship focus, rapid growth tempered by risk management. These early years were like laying the foundation of a skyscraper; invisible to most observers but absolutely critical to everything that would be built above.

As the new millennium dawned, UTI Bank stood at a crossroads. It had proven its viability and established its credibility. The question now was whether it could transform from a successful niche player to a banking powerhouse that could compete with the HDFCs and ICICIs of the world. That transformation would require new leadership, new strategies, and perhaps most importantly, a new identity. The stage was set for the next chapter in what would become one of Indian banking's most remarkable transformation stories.

III. The P.J. Nayak Era: Building the Corporate Fortress (2000–2009)

The turn of the millennium brought with it a new era for UTI Bank, and at its helm stood Pangal Jayendra Nayak—a figure who would transform the institution from a respectable mid-tier player into a banking powerhouse. Nayak had been an IAS officer of Karnataka cadre. He did his MA and got Ph D from Cambridge University, U.K. Mr. Nayak, the chairman and chief executive officer of Axis Bank Ltd, came at the helm of affairs in January 2000 and carried it to newer heights.

The circumstances of Nayak's appointment itself spoke volumes about the changing dynamics of Indian banking. Here was a career bureaucrat, a man who had spent decades navigating the labyrinthine corridors of government, now tasked with competing against nimble private sector rivals. Axis Bank's share price nearly tripled in two months (the period between 30 November 1999 and 4 February 2000), based purely on the news of Nayak taking charge. The market's euphoria, however, wasn't shared universally within the bank.

Having dealt with civil servants in the Ministry of Finance, bankers did not think highly of a civil servant's financial acumen and managerial ability. In fact, a fair amount of scepticism prevailed amongst senior bankers regarding Nayak's ability to alter the waning fortunes of the bank. This skepticism would prove to be profoundly misplaced.

Nayak's first moves were masterful in their simplicity and effectiveness. 'There was trepidation about a CMD who was an IAS officer and a bureaucrat with no banking experience.' The scepticism did not last very long and in his very first address to the employees, Nayak was able to break the ice and win the confidence of many senior employees. 'When we met him, the first thing everyone noticed was the erudition and clarity of thought. He joined on 1 January 2000 and by the end of January, he started talking about, for example, how there is a need for a separate marketing department'.

The transformation under Nayak was nothing short of spectacular. Their profits climbed up to 50% in Nayak's reign. The bank also witnessed a remarkable growth of 61% in their deposits, much higher than its peers. Axis Bank's stunning run from FY01–08 spoke volumes about Nayak's leadership. This wasn't just growth; it was a fundamental reimagining of what an Indian bank could be.

One of the most significant strategic decisions during Nayak's early tenure was the attempted merger with Global Trust Bank in 2001. In 2001 UTI Bank agreed to merge with Global Trust Bank, but the Reserve Bank of India (RBI) withheld approval and the merger did not take place. In 2004, the RBI put Global Trust under moratorium and supervised its merger with Oriental Bank of Commerce. While the merger didn't materialize, it signaled UTI Bank's ambitions to grow through consolidation—a strategy that would resurface decades later with the Citibank acquisition.

The international expansion under Nayak was particularly visionary. The following year, UTI bank was listed on the London Stock Exchange. In 2006, UTI Bank opened its first overseas branch in Singapore. The same year it opened an office in Shanghai, China. In 2007, it opened a branch in the Dubai International Financial Centre and branches in Hong Kong. This wasn't mere geographic expansion; it was positioning the bank to serve Indian corporations going global and to tap into the growing NRI market.

The technology investments during this period laid the foundation for the bank's future digital leadership. The new IT system was in place by April 2000. Now that the IT system was set, duties given and salaries established, the next priority was to inculcate professionalism across the bank. Nayak understood that banking was becoming a technology business, and he invested accordingly.

But perhaps the most dramatic moment of Nayak's tenure was the rebranding from UTI Bank to Axis Bank. The decision wasn't just about avoiding royalty payments; it was about creating an independent identity. As per the agreement between govt. and UTI in 1993, the brand 'UTI' could be used freely by the bank only up till 31 December 2007. From 2008, the bank was supposed to pay a royalty to UTI for using their name. For Nayak, this was the best moment to get rid of UTI's affiliation in order to rebrand the bank.

On 30 July 2007, UTI Bank changed its name to Axis Bank. The new name—Axis—suggested centrality, balance, and a pivot point around which things turn. It was modern, global, and completely divorced from the public sector heritage. The rebranding was executed flawlessly, with minimal customer confusion and no significant deposit flight—a testament to the trust Nayak had built.

The cultural transformation under Nayak was equally profound. This involved breaking the region-based coteries that had developed within the bank—the most powerful being the Bengal Club, due to the large number of new hires who came from SBI's Bengal circle (one of the most prominent circles within SBI) and SBBJ. In fact, there was a time when Axis Bank was called the 'State Bank of Bengal' among bankers. Nayak did away with these groups by realigning employees' priorities with the bank, instead of the regions of their origin.

Nayak's management style was characterized by a unique blend of bureaucratic thoroughness and entrepreneurial aggression. He brought the discipline and process orientation of government service but coupled it with the performance culture of private enterprise. Compensation was linked to performance, promotions were merit-based, and mediocrity was not tolerated. This created a high-performance culture that attracted talent from across the industry.

The corporate banking strategy under Nayak was particularly astute. Rather than competing head-on with State Bank of India in the mass market or with foreign banks in the ultra-premium segment, Axis Bank carved out a niche serving mid-to-large Indian corporates. The bank became the go-to institution for companies looking to expand, offering not just loans but comprehensive financial solutions including cash management, trade finance, and capital market services.

The risk management framework established during this period would prove crucial during the 2008 global financial crisis. While banks globally were collapsing under toxic assets, Axis Bank's conservative underwriting standards and focus on cash-flow based lending kept its books relatively clean. The bank's gross NPA ratio remained under 1% for most of Nayak's tenure—remarkable for a rapidly growing institution.

Innovation was a constant theme during the Nayak years. The bank launched innovative products like the Quantum Optima savings account for the mass affluent, introduced sophisticated cash management solutions for corporates, and pioneered structured finance products in the Indian market. Each innovation was carefully calibrated—pushing boundaries without taking excessive risks.

The branch expansion strategy was equally thoughtful. Rather than the scatter-gun approach of opening branches everywhere, Nayak focused on strategic locations. Each branch was viewed as a profit center, expected to break even within 18-24 months. Branch managers were given significant autonomy but held strictly accountable for performance. This decentralized-yet-controlled model became a hallmark of Axis Bank's operations.

However, as the decade progressed, tensions began to emerge. He is accused of not building the second line capable of running the Bank efficiently. He had been a great performer, but he is branded as autocratic and headstrong. The very qualities that had driven the bank's spectacular growth—Nayak's commanding presence and centralized decision-making—began to create succession challenges.

The succession drama that unfolded in 2009 was unprecedented in Indian banking. In a day of high drama, Axis Bank Chairman P J Nayak today resigned after the board voted against his opposition to the appointment of Shikha Sharma as the next managing director and CEO. Nayak's term was coming to an end in July this year.

The nomination committee of the board had recommended Sharma for the job, but Nayak did not agree to that. A vote was taken, in which eight members supported Sharma's name and the only person who opposed it was Nayak. The board felt that Shikha Sharma, currently MD & CEO of ICICI Prudential Life Insurance, had a more rounded experience than Hemant Kaul, who was Nayak's candidate.

The board meeting on April 20, 2009, became the stuff of banking legend. The board meeting went on for seven hours, though the entire duration was not spent on the succession issue. In all my meetings with Axis Bank's employees and even board members present at that fateful meeting in 2009, the common thread shared with me was that there was a high level of acrimony between Nayak and the other members of the board. Most of these members were professional, independent directors. Nayak had two obvious choices for a successor: Hemant Kaul (ED, retail banking) and Manmohan Agarwal (ED, corporate banking). Depending on whom you speak to, there are varying versions regarding who was Nayak's favourite. However, for reasons that remain unclear, the board refused to consider either of Nayak's protégés as a worthy successor.

Hence, Nayak resigned in April 2009 in a huff three months before his scheduled end of his stint. His dramatic exit marked the end of an era, but the institution he had built was strong enough to not just survive but thrive under new leadership.

Looking back at the Nayak era, several key achievements stand out. He transformed UTI Bank from a sleepy public sector offspring into Axis Bank, a dynamic private sector leader. He built a corporate banking franchise that remains one of the strongest in India. He established an international presence that positioned the bank for global growth. He created a performance culture that attracted and retained top talent. And perhaps most importantly, he proved that Indian banks could compete with anyone—domestic or international—on quality, innovation, and service.

The numbers tell their own story. When Nayak took over in 2000, UTI Bank had assets of approximately Rs. 10,000 crores. By the time he left in 2009, Axis Bank's assets had grown to over Rs. 150,000 crores—a fifteen-fold increase. The bank's market capitalization had grown from less than Rs. 2,000 crores to over Rs. 30,000 crores. The employee base had expanded from around 3,000 to over 20,000. These weren't just numbers; they represented thousands of careers built, millions of customers served, and a fundamental shift in Indian banking.

But Nayak's legacy extends beyond numbers. He demonstrated that leadership transitions in Indian banking didn't have to follow the predictable path of promoting the senior-most executive. He showed that performance mattered more than seniority, that merit trumped connections. He also, inadvertently, highlighted the challenges of succession planning in founder-led or dominant-leader organizations—a lesson that resonates across corporate India.

The irony of Nayak's exit was that it paved the way for an even more dramatic transformation under Shikha Sharma. The institution was strong enough to handle a contentious leadership transition, emerge unscathed, and continue its growth trajectory. This resilience, this ability to transcend individual leaders, might be Nayak's greatest achievement.

As we look at Axis Bank today—a digital leader, a retail powerhouse, an institution that successfully absorbed Citibank's operations—we see the foundations that Nayak laid. The technology infrastructure, the risk management culture, the performance orientation, the international outlook—all bear his imprint. The boy from Karnataka who became a bureaucrat and then transformed into a banker had, in nine tumultuous years, rewritten the rules of Indian banking.

IV. Shikha Sharma's Transformation: From Corporate to Retail (2009–2018)

When Shikha Sharma quit ICICI Bank to lead Axis Bank after being headhunted by Egon Zehnder in April 2009, the banking community watched with intense curiosity. Here was one of ICICI's most successful executives, a woman who had built ICICI Prudential Life into India's largest private life insurer, taking over a bank in the midst of succession turmoil. Shikha Sharma (born 19 November 1958) is an Indian economist and banker. She was the managing director and CEO of Axis Bank from 2009 to 2018.

Sharma's background was as impressive as it was unconventional for a banker. Her father served in the Indian Army, reaching the rank of brigadier in the ordnance corps and fought in the 1965 and 1971 Indo-Pakistani wars. Due to his military service, Shikha grew up across the country, attending seven schools in as many cities. Despite an interest in studying physics, she graduated with a BA (Honours) in Economics from the Lady Shri Ram College in Delhi and an MBA from Indian Institute of Management Ahmedabad.

The journey to Axis Bank had been circuitous but formative. After graduating from IIM Ahmedabad, Shikha Sharma joined ICICI Ltd. in 1980. During her 29-year tenure with the group, she worked with K. V. Kamath and former Prudential plc CEO Mark Tucker. She was instrumental in setting up ICICI Securities – a joint venture between ICICI and J.P. Morgan, besides setting up various group businesses for ICICI, including investment banking and retail finance. She served as the managing director and CEO of ICICI Personal Financial Services from May 1998 to December 2000; and as the managing director and CEO of the ICICI Prudential Life Insurance Company from December 2000 to June 2009. Sharma and Chanda Kochhar were contenders to succeed K. V. Kamath as the CEO and managing director of ICICI Bank in 2009.

Taking charge at Axis Bank in June 2009, Sharma inherited a strong corporate banking franchise but faced immediate challenges. The bank was largely a corporate bank with retail portfolio accounting for one-fifth of the loans and advances. The global financial crisis was still reverberating through the economy, credit growth was slowing, and there were questions about whether Axis Bank could compete effectively with HDFC and ICICI in the retail space.

Sharma's response was swift and strategic. In June 2009, she stated the "Vision 2015" strategy for the bank, focusing growing retail banking to "balance the corporate business." The share retail loans to 46% of the bank's total books during her tenure, from 21% in June 2009. This wasn't just a shift in portfolio mix; it was a fundamental reimagining of what Axis Bank could be.

"There were no set goals specified, but opportunity was to grow the consumer lending business and also fill up some of the gaps in corporate banking," says Sharma. The modesty of this statement belies the ambition of the transformation she orchestrated. Sharma took corporate banking a step ahead by focusing on a holistic relationship (salary account, cash management, forex), instead of a mere lending relationship with clients.

The retail transformation wasn't just about lending; it was about creating a comprehensive retail franchise. Sharma also dramatically changed the branch composition. Six years ago, the branch network was more urban with more than 70 per cent of the branches in metros and urban centres. Today, the bank has more than 50 per cent of its branches in the rural and semi-urban areas, though it is partly because of the mandatory rural branch obligations.

One of Sharma's most controversial yet ultimately vindicated decisions was the acquisition of Enam Securities. Axis Bank, India's fourth-largest bank in terms of market capitalisation, has acquired the investment banking and equity capital market business of Enam in an all-stock deal valued at Rs2,067 crore. Following this, Enam will become an Axis Bank subsidiary, headed by Enam Director Manish Chokani. The acquisition is expected to provide a strong fillip to Axis Bank's share in capital market transactions, as Enam is one of the leading investment banks and has been part of most large equity offerings, including Coal India.

The Enam acquisition faced significant headwinds. In 2010, when she decided to take over Enam in a Rs 1,400-crore deal at a time when the stock markets were not doing particularly well, Shikha Sharma was under fire from analysts for the high valuation. The deal went through many changes and regulatory hurdles and very few were willing to listen to her when she said Axis Bank needed to fix the gaps in its business mix. But Sharma persisted, seeing what others couldn't—the value of creating a one-stop financial services shop.

The digital transformation under Sharma was particularly prescient. At our Bank too, we continue to see strong momentum towards the adoption of digital channels by our customers. The transaction volumes on our award winning mobile application (Axis Mobile) have gone up almost four times compared to that of last year, outpacing every other channel by a wide margin. Electronic channels now contribute 87% of all customer induced transactions in our retail base.

Technology wasn't just about digitizing existing processes; it was about reimagining banking itself. Sharma, known as the silent architect, initiated digitisation to simplify customer needs and aided expansion of the bank in various spheres. The bank invested heavily in mobile banking, becoming one of the first Indian banks to offer a comprehensive suite of services through mobile apps. This digital-first approach would prove invaluable during the COVID-19 pandemic years later.

The cultural transformation under Sharma was equally significant. Coming from ICICI, known for its aggressive, sales-driven culture, Sharma brought a more balanced approach to Axis Bank. She emphasized customer-centricity over pure volume growth, relationship banking over transactional banking, and sustainable growth over quarterly targets.

"Axis penetration in terms of large groups was much lower six years ago. Shikha's focus has been on getting top tier clients for multiple banking relationships," says V. Srinivasan, Deputy Managing Director at Axis Bank. This focus on quality over quantity became a hallmark of the Sharma era.

The financial performance during Sharma's tenure validated her strategy. Over the past six years, Sharma has managed to grow the bank with an average 24 per cent growth in net profit between FY10 and FY15. In the same period, return on equity grew at an average of 18.89 per cent. The balance sheet in the same period more than trebled from Rs 1,47,722.05 crore at the end of March 31, 2009, to Rs 4,61,932 crore at the end of March 31, 2015.

Recognition followed performance. "Best Domestic Bank in India" (2010) by Asset Triple A Country Awards, 'Banker of the Year' for 2014–15 by Business Standard, AIMA - J. R. D. Tata Corporate Leadership Award for the Year 2014, 'India's Best Woman CEO' by Business Today – 2013. Perhaps most notably, Harvard Business School has published a case study on Managing Change at Axis Bank in 2013, cementing Sharma's reputation as a transformational leader.

The subsidiary ecosystem flourished under Sharma. Axis Capital continues to be one of the leading investment banks in India. Axis Asset Management Company (AMC) gained market share during the year and is now ranked 11th in assets under management among participants in the mutual funds industry. This wasn't just diversification; it was building a comprehensive financial services powerhouse.

However, the later years of Sharma's tenure were marked by challenges. The Indian banking sector faced a massive non-performing asset crisis, and Axis Bank wasn't immune. Gross NPAs steadily grew under her tenure, from 0.96% in March 2009 to 5.28% in March 2017 to 6.77% in March 2018. The demonetization of 2016 created additional operational challenges, with some Axis Bank employees being implicated in money laundering activities.

The succession drama that marked Sharma's exit was eerily reminiscent of her own appointment. Axis Bank notified the National Stock Exchange of India on 9 April 2018 that Sharma would retire as the managing director and CEO on 31 December 2018. The announcement came despite the bank's board approving a three-year extension of her term, due to start on 1 June 2018, amid reports that the RBI was unhappy with the bank's performance and was reviewing the decision to approve the extension. The bank's shares rose by 3.44% in the Bombay Stock Exchange after the announcement of her retirement.

The market's reaction was telling—while Sharma had transformed Axis Bank into a formidable retail franchise, investors believed it was time for fresh leadership to tackle the asset quality challenges. She was succeeded by Amitabh Chaudhry on 1 January 2019.

Looking back at the Sharma era, several achievements stand out. She successfully transformed a corporate-focused bank into a balanced universal bank. Sharma successfully transformed Axis, which had a corporate lending and retail liability portfolio, into a financial institution focused on sustained profitable growth. The retail loan book grew from 21% to 46% of total advances. The branch network expanded dramatically, with a particular focus on semi-urban and rural areas. Digital banking capabilities were built from scratch, positioning the bank for the digital revolution that would follow.

Perhaps most importantly, Sharma proved that transformation doesn't require destruction. Unlike some of her peers who pursued growth at any cost, Sharma maintained asset quality discipline while growing the balance sheet. She built new capabilities while preserving existing strengths. She brought in fresh talent while retaining institutional knowledge.

The cultural impact of Sharma's leadership extended beyond numbers. As one of the few women CEOs in Indian banking, she became a role model for aspiring women professionals. Her leadership style—collaborative yet decisive, ambitious yet grounded—offered an alternative to the testosterone-driven culture often associated with banking.

Shikha Sharma loves watching Bollywood movies, maintains a fitness regime, reads books of all sorts and even sings Hindustani classical music. But not many know that the 57-year-old MD & CEO of Axis Bank is also a devotee of the Hindu god Shiva. "I have worshiped Shiva for a long time," says the soft-spoken Sharma, seated in her eighth floor corner room in Central Mumbai. The daughter of an army officer, she has never missed fasting for Lord Shiva on Monday since the time she started her career with the ICICI group in the early 80s.

This personal discipline perhaps explains her professional approach—patient, persistent, and purposeful. The Sharma era at Axis Bank wasn't marked by dramatic headlines or bold acquisitions (Enam aside). Instead, it was characterized by steady execution, consistent performance, and gradual transformation.

As Indian banking entered a new phase of challenges—rising NPAs, digital disruption, new competition from payment banks and small finance banks—Sharma had positioned Axis Bank to not just survive but thrive. The retail franchise she built, the digital capabilities she developed, and the talent she nurtured would all prove invaluable in the years to come.

Sharma, who has already put in motion a vision 2020 with more specified goals of rewarding shareholders and improving the share of low cost deposits, called current and savings account (CASA). The bank has a return of equity (ROE) of 18.57 per cent and a CASA of 45 per cent. While she wouldn't be there to see Vision 2020 through, the foundations she laid would enable her successor to take the bank to new heights.

V. The Digital Revolution: Amitabh Chaudhry's New Axis (2019–Present)

When Amitabh Chaudhry took charge of Axis Bank on January 1, 2019, the institution stood at a critical juncture. The asset quality issues that had plagued the later years of Shikha Sharma's tenure needed resolution, digital disruption was accelerating, and competition from both traditional banks and fintech startups was intensifying. He joined the bank in January 2019, after successfully leading HDFC Life for nine years.

Chaudhry brought an unusual mix of experiences that would prove invaluable for Axis Bank's transformation. Before joining Axis Bank, Amitabh had a long stint as the CEO of HDFC Life, when he built one of the most valued life insurance franchises in the country. He built a culture of product innovation and a digital-first approach, shaping the industry's thought process and future aspirations. Amitabh started his career with Bank of America where he donned diverse roles like head of technology investment banking for Asia, regional finance head for wholesale bank and CFO (India). After 16 years of banking, he switched careers and became part of the founding leadership team at Infosys BPM in 2003. He built a successful process outsourcing business in his 8 years stint, that set a benchmark on the nature of work that could transition to India along with profitability.

This unique background—combining traditional banking, technology services, and insurance—positioned Chaudhry perfectly to lead Axis Bank's digital transformation. Under him, Axis Bank is undergoing a well-outlined multi-year transformation program. The transformation wasn't just about technology; it was about fundamentally reimagining what a bank could be in the digital age.

The numbers from Chaudhry's first three years tell a remarkable turnaround story. In March 2022—Chaudhry stepped into the corner room in January 2019 from HDFC Life, where he was MD and CEO—Axis Bank's net profit rose to Rs 13,025 crore, a multi-fold jump from Rs 1,627 crore in FY20, and an even lower Rs 276 crore in FY18. The profits at its subsidiaries have also pole-vaulted from Rs 347 crore to Rs 1,195 crore in these three years.

But the real revolution was happening beneath these headline numbers. Axis Bank is on track to take 70 percent of its applications and infrastructure on the cloud in the next two years, said Amitabh Chaudhry, CEO and Managing Director of Axis Bank. Last year, its management decided that all new customer-facing apps will be cloud-native. "Today, 15% of the bank's apps are on the cloud," said Chaudhry at the AWS Summit Online India on Tuesday.

The cloud migration strategy wasn't just about modernizing infrastructure; it was about building the foundation for a fundamentally different kind of bank. Axis Bank has 240 million customers and processes around 50 million transactions a day. The process of upgrading its technology infrastructure and applications for the cloud is necessary for Axis Bank's transformation to be future-relevant, he added.

The transformation strategy under Chaudhry focused on three key elements. Axis Bank's focus has been on three key elements. One, reimagining customer journeys, which is about giving them distinctive experiences. In this context, Chaudhry (who was appointed Axis Bank CEO in January 2019) said he is proud that its app is the highest-rated amongst peer banks and financial institutions in India. The second element is upgrading the bank's core technology infrastructure to make it relevant for the new age, where cloud has been a vital factor. And the third element is about delightful employee-experience. "The technology led simplification of operations should enable our employees to become more efficient and effective both internally, as well as externally for our customers," Chaudhry pointed.

The digital payments revolution under Chaudhry has been particularly spectacular. Axis Bank, one of the largest private sector banks in India, proudly announces its achievement as the leading UPI Payer Payment Service Provider (PSP) Bank in India. According to the data published by the National Payments Corporation of India (NPCI), as of September 2024, Axis Bank holds a market leading share of 30.87% in the UPI Payer PSP space. This achievement is a testament to the bank's unwavering commitment to innovation, customer-centric solutions, and strategic partnerships.

This wasn't just market share growth; it was strategic positioning for the future of payments. Axis Bank has strategically focused on partnering with onboarding not only large fintech giants who were early entrants in the UPI space, but also joining hands with new entrants in this space. The objective of these tie-ups is to capture the captive base of these new entrants and offer them UPI solutions directly on their apps. Coupled with a robust IT infrastructure encompassing both on-premise and cloud-based systems, this approach has propelled the Bank's growth in the UPI ecosystem.

The breadth of partnerships is impressive. Axis Bank collaborates with 15 prominent Third-Party Application Providers (TPAPs), including Google Pay, PhonePe, WhatsApp, Paytm, Amazon, Samsung Pay, Navi and Cred. Additionally, the UPI functionality is available through Axis Mobile "Open," BHIM Axis Pay, and Freecharge, a subsidiary of the Bank.

The API integration story exemplifies the pace of transformation. When Chaudhry joined, Axis had five digital API integrations. Today, it has 80 with the likes of Flipkart, Google Pay, Amazon Pay and PhonePe. This wasn't just technical integration; it was about becoming the rails on which India's digital economy runs.

The credit card business has emerged as another growth engine. Currently, Axis Bank is a top 4 credit card player in India with an attained CIF (Cards in force) market share of 14% running on TSYS' PRIME payments stack. The bank has launched innovative products like the FIBE AXIS BANK credit card, India's first-ever numberless credit card intended for tech-savvy Gen Zs, and PRIMUS, the first credit card proposition for ultra-high net worth individuals.

The SME transformation under Chaudhry has been equally dramatic. Under Chaudhry, Axis created an integrated commercial banking group for a sharper focus on SME needs. Axis initiated a tech-driven transformation project called Sankalp, which is all about using data analytics, simplification of product offerings, and meeting the holistic needs of SMEs. Today, the SME book is largely working capital loans, more granular and well diversified across three dozen sectors.

The 'One Axis' strategy represents a fundamental shift in the bank's operating model. Historically, the bank was known to be a balance sheet lender. In fact, it used to leave the cream on the table, very often, for other banks. The big focus now is to deliver one Axis to clients. This means offering the full spectrum of financial services—from banking to insurance to investment banking—as an integrated proposition.

Digital adoption metrics showcase the transformation's success. Today, 68 per cent of the bank's retail FDs by volume, 46 per cent of the new mutual fund SIP sales by volume, 46 per cent of personal loans and 78 per cent of its credit cards issued in 2021-22 are opened digitally. This isn't just digitization of existing processes; it's a fundamental reimagining of customer acquisition and service.

The technology investments have earned recognition. During the year, the Bank won the Best Cyber Security Project, Best Financial AI Project and Best Risk Management Project at The Asset Digital Awards. The Bank also won the award for best use of IT in Risk Management at the Dun & Bradstreet BFSI Summit & Awards 2020; these awards serve as a testament of our strong digital and IT capabilities.

The pandemic proved to be an accelerator rather than an impediment. When the pandemic led to lockdowns in India last year, Chaudhry said the bank anticipated hyper-growth. It created a dedicated cloud-ready infrastructure to handle the volume of UPI (Unified Payments Interface) transactions. Unsurprisingly, Axis Bank had a 20 percent share of the monthly UPI transactions which clocked 2 billion transactions in October 2020.

Chaudhry's vision for the future of banking is particularly prescient. The future of banking, he said, is about becoming invisible, embedded and unbundled. Customers want to buy a house, a car, the latest phone, but do not want a loan. "Successful banks will evolve into something which looks like a good tech company," Chaudhry said. A bank won't decide its offerings to customers, but will create the platform for customers to choose what each of them wants. "With hyper-personalisation, sachet-isation of financial products, we are rapidly moving to this particular normal," he asserted.

The innovation momentum continues to accelerate. The bank has launched industry-first solutions like UPI-ATM, an integrated Android Cash Recycler with Unified Payments Interface technology for cardless cash withdrawal and deposits. The bank was among the first to actively participate in RBI's CBDC pilot with over one million users and 262,000 merchants.

Leadership development under Chaudhry has been transformational. Amitabh runs Axis Bank, a financial conglomerate, together with a world class leadership team and a clearly defined vision of being a bank that fulfils the aspirations of a new, resurgent India through smart banking solutions. Over the past five years, Axis Bank has turned in industry leading performance on growth, profitability, and sustainability through a mix of deep investments in digital, focus on customer experience, making a strategic bet on Bharat and being prudent on risk.

The recent reappointment of Chaudhry signals continuity and confidence. Axis Bank has confirmed the re-appointment of Amitabh Chaudhry as Managing Director and Chief Executive Officer for an additional three years, following approval from the Reserve Bank of India (RBI). Chaudhry's extended term will commence in January 2025 and conclude on December 31, 2027.

The cloud-native transformation continues to gather pace. It is investing a lot in shifting applications to the cloud, automating processes, reducing the number of legacy apps and building new apps on an agile platform. "In the last year, 100 per cent of the customer-facing applications that we launched are cloud native. These are video KYC, credit card journey, BNPL, current account journey and merchant cash," says Sameer Shetty, Head of Digital Banking.

The cultural transformation under Chaudhry has been as significant as the technological one. An engineer from BITS, Pilani, with management spurs from the prestigious IIM Ahmedabad, Chaudhry has set in motion close to two dozen transformation projects and is making the bank, which has had a public (erstwhile UTI Bank) character, more process driven. This shift from relationship-based to process-driven banking represents a fundamental change in how the bank operates.

The transformation isn't without challenges. Competition from digital-native players continues to intensify. Regulatory requirements are becoming more stringent. Customer expectations are rising exponentially. But Chaudhry's approach—combining deep technology investments with human-centered design—positions Axis Bank well for these challenges.

"We are now asking ourselves the question: what will it take for us to become a very large, important, successful player on the digital side? That's the journey we're embarking on now," says Chaudhry. This isn't just ambition; it's a recognition that in the digital age, banks must either transform or become irrelevant.

The Chaudhry era at Axis Bank represents more than just another leadership transition. It's a fundamental reimagining of what an Indian bank can be in the digital age. From cloud migration to UPI dominance, from API integration to customer experience transformation, every aspect of the bank is being reinvented. The boy from BITS Pilani who spent time at Bank of America, Infosys, and HDFC Life has brought a unique perspective that combines global best practices with deep local understanding.

As we look at Axis Bank today—with its 30.87% market share in UPI payments, its cloud-native infrastructure, its top-rated mobile app—we see not just a transformed institution but a glimpse of the future of banking itself. The digital revolution that Chaudhry is orchestrating isn't complete, but its trajectory is clear: Axis Bank is positioning itself not just as a bank that uses technology, but as a technology company that happens to be in banking.

VI. The Citibank Acquisition: A Strategic Masterstroke (2021–2023)

VI. The Citibank Acquisition: A Strategic Masterstroke (2021–2023)

The morning of April 29, 2021, brought news that would reshape India's banking landscape. Citigroup announced its decision to exit consumer banking operations in thirteen markets globally, including India—a market where it had operated for over a century. For most Indian banks, this represented a once-in-a-generation opportunity. For Amitabh Chaudhry and Axis Bank, it was the moment they had been preparing for. The speed with which Chaudhry moved was remarkable. When Citi announced exit from consumer banking in 13 markets, Chaudhry moved quickly to form strategy and M&A team, commissioned market survey. Unlike the cautious approach that characterized many Indian banks' acquisition strategies, Axis Bank approached the opportunity with the confidence of a predator sensing perfect prey.

The strategic rationale was compelling on multiple fronts. It has granted us access to 2.4 million large, affluent, and profitable Citi customers, ~3,200 Citibank employees with deep domain expertise and best-inclass client servicing and operations through Citi Phone Banking. This wasn't just about buying customers; it was about acquiring a premium franchise that had taken Citibank decades to build.

Mumbai-headquartered Axis Bank has completed the acquisition of the India consumer business of the Citigroup-owned foreign bank Citibank for Rs 12,325 crore prior to evaluation of the closing position of Citibank India's assets, assets under management, and liabilities as of January 31, 2023. Post evaluation, the deal is valued at around Rs 11,603 crore. The final price adjustment reflected market realities, but the strategic value far exceeded the financial cost.

The transaction scope was comprehensive. The sale, which Citi and Axis first announced in March 2022, includes credit cards, retail banking, wealth management and consumer loans, as well as the transfer of approximately 3,200 Citi employees. This wasn't a cherry-picking exercise; Axis Bank was acquiring an entire ecosystem.

The credit card portfolio acquisition was particularly transformative. The bank said it expects its market share to improve from 11.4 per cent to 16.2 per cent. Besides, the acquired portfolio would also boost the Axis Bank's credit card customer base by 19 per cent, with an addition of 1.8 million cards. In one stroke, Axis Bank had catapulted itself into the top tier of India's credit card market.

What made this acquisition particularly astute was the quality of the customer base being acquired. Citibank's Indian customers weren't just affluent; they were the crème de la crème of Indian banking—multinational executives, high-net-worth individuals, professionals who valued service over price. These customers had average ticket sizes and wallet shares that were multiples of typical Indian banking customers.

The integration strategy was meticulously planned. We have a clear plan across 60+ synergy levers identified. Rather than rushing to rebrand and integrate, Axis Bank took a phased approach that prioritized customer experience over operational efficiency. Now, there will be an 18-month integration period during which Citi customers will be migrated to Axis' technology platforms.

The technological integration presented unique challenges. Citibank operated on global platforms with sophisticated capabilities that many Indian banks couldn't match. Axis Bank had to ensure that the migration didn't result in a downgrade of services for Citi customers accustomed to world-class digital banking. The solution was elegant—maintain Citi systems initially while gradually migrating customers to enhanced Axis platforms.

The migration of your Citi-branded card will be completed by 15th July 2024. Upon completion of the migration, i.e., 15th July 2024 onwards, you will be able to enjoy the benefits of Axis Bank cards on your existing Citi-branded card (s). This patient approach ensured minimal disruption while maximizing value capture.

The wealth management opportunity was particularly significant. Overall assets under management of Burgundy customers stood at ₹5.92 trillion as on March 31, 2025. The integration of Citi's wealth management capabilities with Axis Bank's Burgundy private banking created one of India's largest wealth management franchises, positioning the bank to capture the explosive growth in Indian wealth creation.

The human capital integration was handled with unusual sophistication. Through the acquisition, Axis Bank onboarded 3,200 employees trained in global best practices and experienced leadership with deep domain expertise. Rather than the typical post-merger purge, Axis Bank retained and integrated Citi talent, recognizing that these employees were crucial to maintaining service quality and customer relationships.

The regulatory navigation was equally masterful. Unlike many Indian M&A transactions that get bogged down in regulatory approvals, Axis Bank worked closely with the RBI and other regulators to ensure smooth approval. The transaction is expected to result in a regulatory capital benefit of US$1.4 billion for Citigroup globally, aligning incentives for a swift closure.

The market response validated the strategic logic. While there was an initial capital impact—This deal will have a 177 basis points bearing on Axis Bank's CET1 capital ratio—investors recognized the long-term value creation potential. The acquisition wasn't just about size; it was about acquiring capabilities and customers that would have taken decades to build organically.

The cultural integration presented its own challenges. Citibank's culture—global, sophisticated, process-driven—was different from Axis Bank's more entrepreneurial, relationship-focused approach. The integration team worked to preserve the best of both cultures, maintaining Citibank's service excellence while infusing Axis Bank's growth orientation.

The product integration strategy was particularly thoughtful. Rather than immediately discontinuing Citi products, Axis Bank maintained them while gradually introducing enhanced versions. For instance, premium Citi credit cards were mapped to equivalent or superior Axis Bank products, ensuring customers felt they were upgrading rather than being forced to switch.

The branch integration was strategic. Citibank operated from prime locations in India's major cities—real estate that would have been impossible for Axis Bank to acquire independently. After the Transfer Date, Citibank branches & ATMs will be re-branded as Axis Bank branches and ATMs. While the branch timings will change, the locations of the branches and ATMs will remain the same.

The cross-selling opportunity was immense. Citi customers who previously had limited product relationships could now access Axis Bank's full suite of services—from home loans to insurance to investment banking. Early data suggested that revenue per Citi customer was increasing significantly post-acquisition.

The technology transfer was another hidden gem. Citibank's global technology platforms, risk management systems, and operational processes represented decades of investment and refinement. While not all systems could be retained, Axis Bank carefully identified and preserved the most valuable capabilities, particularly in areas like fraud detection and wealth management.

Looking at the broader strategic implications, the Citibank acquisition represented a watershed moment for Indian banking. It demonstrated that Indian banks had the capability and confidence to acquire and integrate operations from global giants. It also signaled a shift in global banking dynamics, with international banks retreating from retail banking in emerging markets while local champions filled the void.

The timing of the acquisition, completed in March 2023, proved fortuitous. As India's economy rebounded strongly from the pandemic and wealth creation accelerated, Axis Bank was perfectly positioned to capture this growth with an enhanced platform and expanded customer base. The premium customer segment acquired from Citi was particularly well-placed to benefit from India's economic expansion.

The acquisition also accelerated Axis Bank's transformation from a traditional bank to a financial services powerhouse. With Citi's wealth management capabilities, sophisticated product suite, and premium customer base, Axis Bank could now compete effectively in segments previously dominated by foreign banks and boutique wealth managers.

As we assess this acquisition two years later, it's clear that this wasn't just a successful transaction—it was a transformational moment. The Citibank acquisition gave Axis Bank capabilities that would have taken decades to build, customers that were nearly impossible to acquire, and credibility that money couldn't buy. It was, in every sense, a strategic masterstroke that redefined Axis Bank's trajectory and position in Indian banking.

VII. Building the Ecosystem: One Axis Strategy

The vision of 'One Axis' represents more than a catchy corporate slogan—it embodies a fundamental reimagining of how a financial services conglomerate can create value in the 21st century. Under Chaudhry's leadership, Axis Bank has transformed from a traditional balance sheet lender into an integrated financial ecosystem serving every aspect of customers' financial lives. The architecture of the One Axis strategy is elegantly simple yet powerfully comprehensive. Under the 'One Axis' umbrella, the organization offers a wide range of financial services to its customers. It has established a strong subsidiary ecosystem, to address the needs of varied consumers, that includes Axis Mutual Fund, Axis Capital, Axis Finance, Axis Securities, Axis Trustee, Freecharge, A.Treds and Axis Pension.

The transformation from a standalone bank to an integrated financial ecosystem began long before Chaudhry's arrival but accelerated dramatically under his leadership. Axis Bank and its subsidiaries held a 19.02% stake (as on March 31, 2025) in Axis Max Life Insurance, a joint venture between Max Financial Services and Axis Bank. This insurance partnership represents just one piece of a carefully constructed financial services mosaic.

The One Axis ecosystem is at the heart of the distinctiveness that we offer. Within the framework of One Axis, our group operates a versatile banking platform designed to cater to various business segments. This isn't mere corporate rhetoric—it represents a fundamental shift in how the bank creates and captures value.

The historical context is important. Historically, the bank was known to be a balance sheet lender. In fact, it used to leave the cream on the table, very often, for other banks. The big focus now is to deliver one Axis to clients. This transformation from product-push to solution-pull represents a philosophical shift that permeates every aspect of the organization.

Axis Capital, the investment banking arm, exemplifies the power of the integrated model. Axis Capital Q1FY25 PAT grew 220% YOY to `49 crores and executed 22 investment banking deals in Q1FY25. The subsidiary doesn't operate in isolation—it leverages the bank's corporate relationships to win mandates while providing the bank's clients with sophisticated capital market solutions.

The mutual fund business has emerged as a particularly strong performer. Axis Asset Management Company (AMC) gained market share during the year and is now ranked 11th in assets under management among participants in the mutual funds industry. Axis AMC's Q1FY25 PAT up 27% YOY, Axis Securities Q1FY25 PAT up 171% YOY. These aren't just impressive growth numbers; they represent successful cross-selling into the bank's extensive customer base.

Axis Finance, the NBFC subsidiary, plays a crucial role in serving segments where traditional banking faces regulatory constraints. Axis Finance Q1FY25 PAT up 26% YOY, ROE at 14.7%, total CAR healthy at 19.4%, asset quality metrics improve with GNPA declining 10 bps YOY to 0.55%. The subsidiary's strong performance demonstrates the value of having multiple lending vehicles within the ecosystem.

The securities business has been transformed from a sleepy brokerage into a dynamic wealth solutions provider. The sales and securities business, including the retail broking business of Axis Capital Ltd, was merged with ASL on 25 May 2013. ASL is a wholly owned subsidiary of the bank and offers retail asset products, credit cards and retail brokerage services.

Freecharge, acquired in 2017, represents the bank's bet on digital payments. Freecharge Payment Technologies Private Ltd. was acquired by the Bank (from Jasper Infotech Private Ltd.) on 6th October 2017 post receiving the approval from RBI. Freecharge is now a wholly-owned subsidiary of the Bank. While the acquisition initially faced skepticism, Freecharge has become an important part of the bank's digital payments ecosystem.

The newest addition to the ecosystem showcases continued innovation. Axis Pension Fund Management Limited (APFML) was incorporated on 17th May 2022 to undertake pension fund management business under the National Pension System. APFML received its Certificate of Registration from Pension Fund Regulatory and Development Authority as a Pension Fund on 1st July 2022. This entry into pension fund management positions Axis to capture India's growing retirement savings market.

The trustee services business, while less glamorous, plays a critical infrastructure role. Axis Trustee Services Limited is engaged in trusteeship activities, acting as a debenture trustee and as a trustee to various securitization trusts. These services deepen relationships with corporate clients while generating steady fee income.

The synergy metrics are compelling. Total Q1FY25 PAT of domestic subsidiaries at `436 crores, up 47% YOY; Return on investments of 54% in domestic subsidiaries. This 54% return on subsidiary investments far exceeds what the bank could earn from traditional lending, validating the ecosystem strategy.

Cross-selling has become a science at Axis Bank. Axis Bank has developed a robust subsidiary ecosystem, through which we can cater to the diverse needs of our corporate clients. We have developed a robust subsidiary ecosystem, through which we can cater to the diverse needs of our corporate clients, providing you with comprehensive financial solutions that help you grow and succeed in the competitive business landscape.

The corporate banking integration is particularly sophisticated. When Axis Bank wins a corporate banking mandate, it's not just about providing working capital. The relationship manager brings in Axis Capital for equity raising, Axis AMC for treasury management, Axis Trustee for bond issuances, and Axis Finance for specialized lending needs. This comprehensive approach dramatically increases wallet share and customer stickiness.

For retail customers, the One Axis experience is equally transformative. A customer walking into an Axis Bank branch for a savings account can seamlessly access mutual funds, insurance, trading accounts, and pension products. The integration is technological—single sign-on across platforms—but also human, with relationship managers trained to identify and fulfill comprehensive financial needs.

The digital integration deserves special mention. In the digital-first era, our pioneering initiatives like 'open' by Axis and 'NEO' are catalysing transformative change, redefining banking experiences for customers. These platforms don't just offer Axis Bank products; they create marketplaces where customers can access the entire ecosystem's offerings through unified interfaces.

The cultural transformation required to make One Axis work has been profound. These activities aim to amplify the spirit and promise of, "delighting customers, every day", and embracing it as a continuous process and standard practice for all employees across the bank and its subsidiaries. Breaking down silos between subsidiaries, aligning incentives for cross-selling, and creating a unified customer experience required fundamental changes in how employees think and operate.

The regulatory navigation has been complex. Each subsidiary operates under different regulatory frameworks—RBI for banking, SEBI for capital markets, IRDAI for insurance, PFRDA for pensions. Axis Bank has built sophisticated compliance structures that ensure regulatory adherence while maintaining operational integration.

The technology architecture enabling One Axis is remarkably sophisticated. 410+ APIs hosted on Bank's API Developer Portal with 285+ Retail APIs. These APIs don't just connect systems; they create a digital nervous system that enables real-time data sharing, integrated risk management, and seamless customer experiences across subsidiaries.

The financial impact of the One Axis strategy extends beyond direct subsidiary profits. Customer acquisition costs decrease when existing relationships can be leveraged for cross-selling. Credit risk improves with better customer understanding across products. Operational efficiency increases through shared infrastructure and services.

The competitive advantage created by One Axis is substantial and sustainable. While competitors can replicate individual products, recreating an integrated ecosystem requires years of investment, regulatory approvals, and cultural transformation. The network effects—where each additional product makes all other products more valuable—create formidable barriers to entry.

International expansion adds another dimension to the ecosystem. The bank has nine international offices with branches at Singapore, Hong Kong, Dubai (at the DIFC), Shanghai, Colombo and representative offices at Dhaka, Dubai, Sharjah and Abu Dhabi, which focus on corporate lending, trade finance, syndication, investment banking and liability businesses. These international touchpoints enable Axis to serve Indian corporates globally while accessing international markets for its domestic clients.

The strategic discipline in building the ecosystem is noteworthy. Not every opportunity is pursued—the recent closure of the UK subsidiary demonstrates willingness to exit non-core areas. As part of Bank's strategy for international business, it was decided to close the subsidiary and exit UK markets. AUK submitted its application for cancellation of banking license (Part 4A Permission), which was approved by the regulators on 24 October 2024.

Looking forward, the One Axis strategy positions the bank for multiple growth vectors. As India's wealth grows, the investment management and insurance subsidiaries are poised to capture disproportionate value. As corporates become more sophisticated, the investment banking and trustee services become more relevant. As digital payments explode, Freecharge and the payments infrastructure become critical assets.

The One Axis strategy also provides resilience. When net interest margins compress, fee income from subsidiaries provides cushioning. When credit growth slows, capital market activities can compensate. When regulatory changes impact one business, others can provide stability. This diversification isn't just financial engineering; it's strategic risk management.

Perhaps most importantly, One Axis represents a vision for the future of banking—not as a monolithic institution but as an ecosystem of specialized capabilities united by common purpose, shared technology, and integrated customer experience. It's a model that recognizes that in the 21st century, customer needs are too complex and varied to be served by any single entity, no matter how large or sophisticated.

The execution of this vision under the One Axis umbrella demonstrates that Axis Bank isn't just adapting to the future of financial services—it's actively creating it. The ecosystem isn't complete—gaps remain in areas like health insurance and specialized lending—but the foundation is robust, the strategy is clear, and the execution has been exceptional.

VIII. The Rural & SME Push: Bharat Banking

The statistics tell a compelling story of two Indias: one that orders groceries on Blinkit and invests through Zerodha, another that still walks miles to the nearest bank branch and keeps savings under the mattress. 47% branches in rural and semi-urban region as of March 31, 2025. This strategic positioning in India's hinterlands represents not just CSR compliance but a fundamental bet on India's economic future. The transformation of Axis Bank's rural and SME strategy under the Bharat Banking initiative represents more than a growth strategy—it's a recognition that India's future economic growth will be driven not from Nariman Point or Cyber City but from the villages and small towns that constitute the real India. Our Bharat Banking initiative is a key strategic priority aimed at integrating rural and semi-urban India (RuSu) into the economic fabric while addressing their diverse financial needs.

The vision articulated by leadership is unambiguous. 'Bharat' is the big opportunity of this decade as the farm sector reforms, infrastructure investments and digital inclusion story plays out in our Tier III towns and rural India. We are ready to lead in this space and are now creating a separate growth-focused 'Bharat Bank' to increase our presence manifold over the next 3 years, said Amitabh Chaudhry.

The strategic importance of this push is evident in the organizational structure. Axis Bank has roped in financial services veteran Munish Sharda who joins in as Group Executive & Head of Bharat Banking. The creation of a dedicated leadership position at the Group Executive level signals that this isn't a CSR initiative or regulatory compliance exercise—it's a core growth driver.

The numbers validate the strategy. With the success and tremendous response to its Deep Geo initiative, which focused on servicing over 80 lakh customers in semi-urban and rural regions across 2,065 branches during the pandemic, this segment saw an annualised loan growth of 18%, while contributing to 25% of incremental retail disbursements. The rural deposits also grew at 19% over the previous year.

The product innovation for rural markets demonstrates sophisticated understanding of customer needs. Through Sampann, Axis Bank will offer exclusive benefits such as discounts on farming devices, agriculture inputs like pesticides, seeds and a wide range of value-add services like crop advisory, weather forecasting, and real-time information. This isn't just lending money; it's becoming an integral part of the agricultural ecosystem.

The launch of 'Sampann', a premium banking proposition specifically curated for the growth focused and progressive customer segment based in rural and semi-urban regions, challenges conventional wisdom. Premium banking in rural India? The very concept would have been laughable a decade ago. Yet Axis Bank recognizes that rural India isn't monolithic—it includes progressive farmers, agri-entrepreneurs, and rural businesses that need sophisticated financial services.

The partnership strategy amplifies reach without proportional cost increases. The Bank will leverage ITCMAARS (Meta Market for Advanced Agricultural Rural Services), a full-stack Agri-tech application for reaching out to the farmers and addressing their financial requirements. By partnering with ecosystem players like ITC, Axis Bank can access millions of farmers without building expensive last-mile infrastructure.

The SME transformation under project Sankalp represents another dimension of the Bharat push. Tech-driven transformation project called Sankalp for SMEs, using data analytics and simplification of products; SME book now largely working capital loans, well diversified across three dozen sectors. The diversification across three dozen sectors provides resilience against sector-specific shocks.

The metrics speak to the success of the SME strategy. SME loans up 20% YOY, with the SBB+SME+MC mix at ₹2,100 bn | 21% of total loans, up ~800 bps in last 4 years. This isn't just growth; it's a fundamental shift in the loan book composition toward more granular, higher-yielding assets.

The technology enablement of rural banking is particularly innovative. The Bank launched 'UPI-ATM', an integrated Android Cash Recycler with Unified Payments Interface (UPI) technology for cardless cash withdrawal and deposits. In rural areas where card penetration remains low but mobile phone usage is ubiquitous, this innovation bridges the digital divide.

The distribution strategy balances physical and digital presence. As on March 31, 2025, the Bank's distribution network comprises 5,876 branches, 13,941 ATMs and cash recyclers, with close to 47% branches in rural and semi-urban region. But physical presence is augmented by digital channels and partnerships with CSCs (Common Service Centers) and VLEs (Village Level Entrepreneurs).

The human capital investment is substantial. The Bank expects to add more than 3,000 people to focus on rural MSMEs, CSC coverage and corporate agriculture ecosystem. These aren't just tellers or loan officers; they're relationship managers who understand local dynamics, speak local languages, and can navigate the complex social structures of rural India.

The risk management approach to rural lending has evolved significantly. Rather than the traditional collateral-based lending that excluded most rural borrowers, Axis Bank uses data analytics, cash flow-based lending, and ecosystem partnerships to manage risk. The partnership with Next Bharat Ventures to provide financing solutions for impact-driven entrepreneurs exemplifies this new approach.

The financial inclusion impact is measurable. Additionally, it will also offer an extensive range of products and services to the farmers through its rural-urban and semi-urban (RUSU) branches located across 656 districts of India. Covering 656 of India's approximately 750 districts means Axis Bank has near-universal geographic coverage.

The agricultural lending strategy goes beyond traditional crop loans. Through partnerships and technology, the bank offers comprehensive solutions including warehouse receipt financing, supply chain finance for agri-businesses, and equipment financing for farm mechanization. This holistic approach addresses the entire agricultural value chain.

The Bharat Connect for Business platform represents technological innovation tailored for SMEs. This proposition will function as an interoperable, seamless, open loop ecosystem to facilitate and digitise flow of funds till the last mile. It will integrate multiple business applications for clients to streamline their accounts payables/receivables. This addresses a critical pain point for SMEs—working capital management.

The cultural sensitivity in product design is noteworthy. Products are designed considering local festivals, agricultural cycles, and social customs. Loan repayment schedules align with harvest cycles. Banking hours in rural branches accommodate local market days. This isn't standardization; it's localization at scale.

The government program participation amplifies impact. The bank actively participates in schemes like PM Kisan, PM Mudra Yojana, and Stand-Up India. These programs provide not just lending opportunities but also data that helps in credit assessment and customer acquisition.

The rural wealth management opportunity is emerging. As rural incomes rise and land values appreciate, there's growing demand for investment products, insurance, and wealth management services. The Sampann offering targets this emerging affluent rural segment with premium banking services previously available only in urban areas.

The ecosystem approach to rural banking is comprehensive. The Bank is creating a distinctive 'Bharat Bank' unit with tailored rural products, increased footprint through branches and digital presence, partnerships with facilitators like CSCs and VLEs and by enabling multiple agri-commodities focused ecosystems. This isn't just banking; it's building rural financial infrastructure.

The impact metrics go beyond financial returns. Through this strategic collaboration reinforces our commitment to financial inclusion, giving us the opportunity to support the next generation of socially impactful business leaders. The focus on impact-driven entrepreneurship in rural areas could catalyze broader economic transformation.