HEG Limited: India's Graphite Electrode Giant

I. Introduction & Episode Roadmap

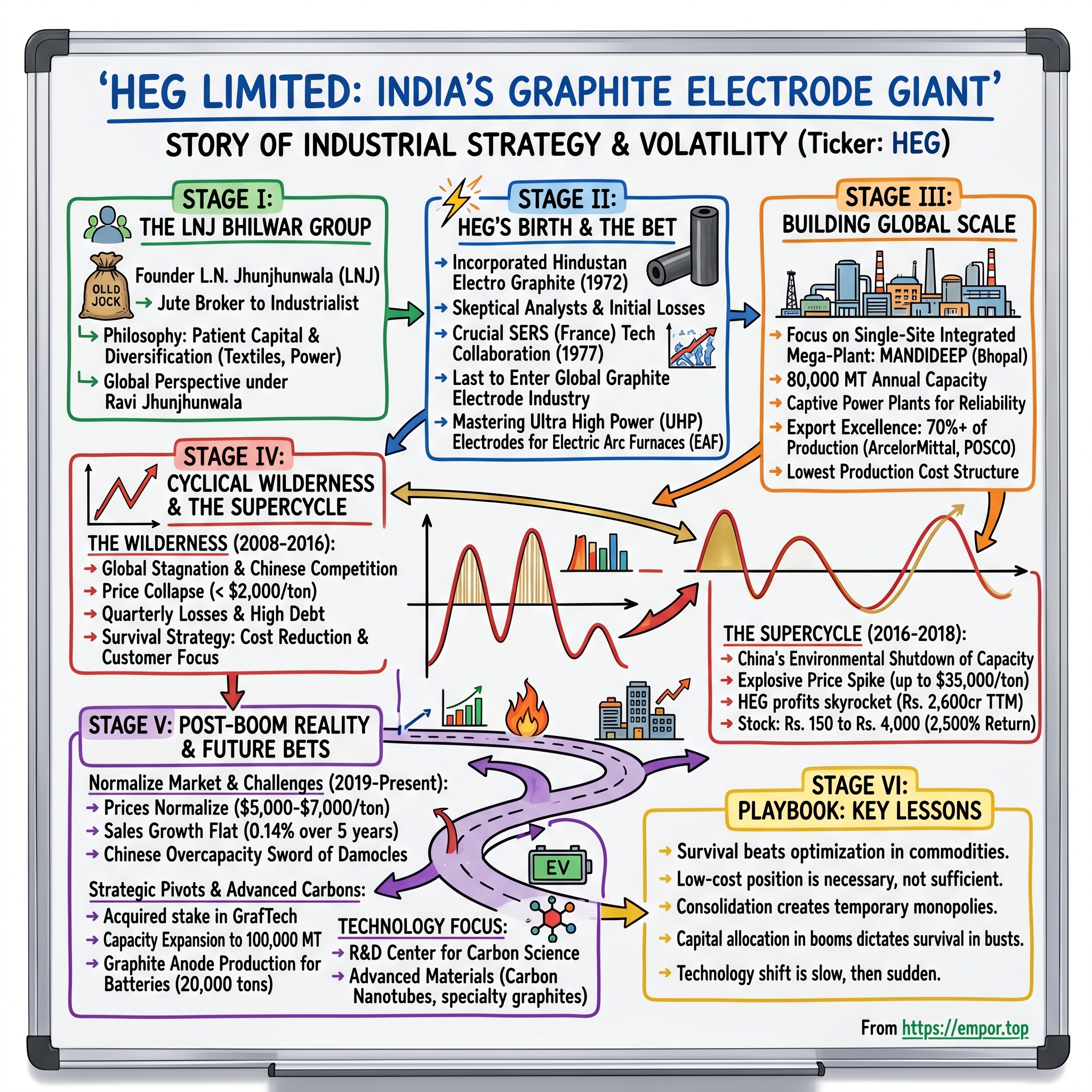

Picture this: March 2017. In a nondescript conference room in Noida, HEG Limited's management faces a room of skeptical analysts. The company has just declared a loss of ₹50 crores. Their stock languishes at ₹150, having drifted sideways for years. The graphite electrode industry—once a darling of the commodities boom—looks like a graveyard of overcapacity and crushed margins. Nobody in that room could have imagined that within 18 months, this same stock would touch ₹4,000, delivering a mind-bending 2,500% return.

This is the story of HEG Limited—India's leading graphite electrode manufacturer, operating what they claim is the world's largest single-site integrated graphite electrodes plant. It's a tale that spans five decades, from the controlled economy of the License Raj to the wild west of global commodity supercycles. At its heart lies a fundamental question that every industrial investor must grapple with: How do you build and sustain a business in an industry where your product can swing from being practically given away to becoming liquid gold overnight?

The company's journey reads like a masterclass in surviving—and occasionally thriving—through industrial cycles. Founded in 1972 as part of the LNJ Bhilwara Group's diversification push, HEG bet big on a highly technical, capital-intensive product that most Indians had never heard of: graphite electrodes. These aren't your everyday pencil leads. We're talking about massive carbon columns, some as tall as three meters and weighing over 2,700 kilograms, that conduct electricity at temperatures exceeding 3,000°C to melt scrap steel in electric arc furnaces.

What makes HEG's story particularly fascinating is how it embodies the broader narrative of Indian manufacturing—the struggles against global giants, the patient building of capabilities over decades, and the occasional windfall when global supply chains crack just right. The 2017-2018 supercycle wasn't just a financial event; it was a validation of a 40-year bet on a single product, in a single location, with a single-minded focus on scale and efficiency.

But here's where it gets interesting: unlike the typical Acquired story of compounding excellence, HEG's tale is one of extreme volatility. Between 2009 and 2018, the company posted losses four times while its peer Graphite India somehow stayed profitable throughout. The question isn't just how HEG survived these cycles, but why the market briefly valued it as one of India's most exciting industrial stories, and whether that thesis still holds today.

As we dive deep into this story, we'll explore several key themes that define not just HEG, but the entire landscape of industrial commodities: the ruthless nature of cyclicality, how industrial consolidation creates temporary monopolies, the role of China as both creator and destroyer of fortunes, and ultimately, what it means to be a "quality" company in a commodity business. We'll trace the journey from the textile mills of Bhilwara to the steel furnaces of the world, examining each strategic decision, each crisis survived, and each opportunity seized or missed.

This isn't just a story about graphite electrodes—it's about industrial strategy, family business evolution, and the peculiar dynamics of being an Indian manufacturer in a global commodity market. So buckle up as we explore how a company you've probably never heard of became, for a brief shining moment, one of the most profitable enterprises in India.

II. The LNJ Bhilwara Group & Founding Context

The story of HEG begins not in a boardroom or a factory, but in the narrow lanes of Calcutta's Burrabazar in the 1940s, where a young Lakshmi Niwas Jhunjhunwala worked as a small-time jute broker. L.N. Jhunjhunwala—or LNJ as he came to be known—possessed that peculiar combination of trading acumen and industrial ambition that defined many of India's first-generation entrepreneurs. By 1946, barely a year before independence, he had established his own trading firm, and by 1951—in a newly independent India hungry for foreign exchange—his company had become one of the country's top ten exporters.

But LNJ understood something fundamental about the Indian economy of the 1950s: trading alone wouldn't build lasting wealth. The real opportunity lay in manufacturing, particularly in sectors where the government's industrial licensing policy created artificial scarcity. His first major pivot came through iron ore exports to Japan, riding the post-war reconstruction boom. Yet even as the money rolled in from commodity exports, LNJ was plotting a more ambitious transformation.

In 1960, in what seemed like an unlikely move, LNJ established a textile mill in Bhilwara, a dusty town in Rajasthan known more for its proximity to marble quarries than industrial prowess. The choice of location was strategic—land was cheap, labor was available, and the Rajasthan government was eager to industrialize. But more importantly, it reflected LNJ's philosophy: build where others won't, create your own ecosystem, and control every variable you can.

The Bhilwara venture wasn't just about textiles. LNJ was building something more ambitious—a conglomerate that could weather the cycles inherent in any single industry. By the late 1960s, the LNJ Bhilwara Group was already diversifying. The group's philosophy was distinctly Indian in its approach: patient capital, family control, and a willingness to enter complex, capital-intensive businesses that required decades-long commitments. Today, the LNJ Bhilwara Group's turnover stands at ₹10,104 crores (approximately $1.2 billion), a testament to six decades of patient empire-building. The conglomerate now spans textiles, power generation, electro graphite, IT services, energy storage solutions, and skill development, employing 25,000 people across 21 manufacturing facilities.

What's remarkable about the group's evolution is how it maintained its core philosophy while adapting to changing times. The transition from founder LNJ to the current generation—led by his son Ravi Jhunjhunwala, who serves as Chairman and Managing Director of HEG Limited—was seamless, avoiding the succession dramas that plague many Indian family businesses. Ravi brought a different energy to the group: more global in outlook, more willing to take concentrated bets, and crucially, more focused on building world-scale facilities rather than subscale diversification. Ravi Jhunjhunwala, armed with a Bachelor's degree from the University of Delhi, joined the family business in 1982 and became Chairman and Managing Director of HEG Ltd. An active member of the World Presidents Organization, he brought a global perspective while maintaining the group's commitment to corporate social responsibility. Under his leadership, the group made a crucial strategic decision in the early 1970s: while others were chasing quick returns in trading or light manufacturing, LNJ Bhilwara would bet on graphite electrodes—a product so specialized that most Indians couldn't even pronounce it correctly, let alone understand its importance.

The group's philosophy—patient capital, technical excellence, and a willingness to endure cyclical pain for eventual gain—would prove particularly suited to the graphite electrode business. It's a philosophy that would be tested repeatedly over the next five decades, but one that would ultimately position HEG as a global player in one of the most volatile industries on earth. As we'll see, the decision to enter graphite electrodes in 1972 wasn't just about diversification—it was about finding a business where India's cost advantages could compete globally, where technical barriers would limit competition, and where patience would eventually be rewarded.

III. HEG's Birth: The Graphite Electrode Bet (1972–1990s)

October 1972. As India Gandhi consolidated power and the economy groaned under socialist controls, the LNJ Bhilwara Group made what seemed like an insane bet: they incorporated Hindustan Electro Graphite Limited (later shortened to HEG). The timing couldn't have been worse—or perhaps, in retrospect, better. The License Raj meant that getting permission to manufacture anything required navigating a Byzantine bureaucracy, but it also meant that once you got a license, competition was legally restricted.

The real breakthrough came in 1977 when HEG entered into a technical and financial collaboration with Société Des Electrodes Et Réfractaires Savoie (SERS), a subsidiary of French aluminum giant Pechiney. This wasn't just a licensing deal—it was a technology transfer that would catapult HEG from paper plans to actual production. The French brought not just equipment blueprints but something more valuable: the alchemy of turning petroleum coke and coal tar pitch into electrodes capable of withstanding the inferno of steel production.

To understand why graphite electrodes mattered, you need to understand steel. In traditional blast furnaces, iron ore is reduced using coke in a process that's been around since the Industrial Revolution. But there's another way: the Electric Arc Furnace (EAF), where scrap steel is melted using enormous electrical currents. The graphite electrode is the conductor—imagine a lightning rod that channels enough electricity to melt cars, refrigerators, and construction beams into liquid steel. A single electrode can be three meters tall, weigh nearly three tons, and cost tens of thousands of dollars.

The product portfolio HEG developed wasn't monolithic. They focused on three grades: Regular Power (RP), High Power (HP), and the crown jewel—Ultra High Power (UHP) electrodes. Each grade required different raw materials, different baking times, and crucially, different levels of technical sophistication. The UHP electrodes, which could handle current densities exceeding 25 A/cm², would eventually become HEG's calling card. These weren't commodities you could produce in a backyard furnace—the manufacturing process involved multiple stages of baking at temperatures exceeding 3000°C, graphitization that took weeks, and quality control that measured impurities in parts per million.

What's fascinating about HEG's early years is how they navigated the contradiction of being a global product manufactured in socialist India. The government wanted exports for foreign exchange but maintained suffocating controls on imports of raw materials. HEG had to source needle coke—the crucial raw material—from global suppliers while dealing with import licenses, foreign exchange allocations, and bureaucrats who didn't understand why you couldn't just use regular coal.

The entry barriers were formidable, and this was by design. HEG was literally the last company to enter the global graphite electrode industry when it started production in 1977. After them, the door essentially closed. The capital requirements were enormous—a single graphitization furnace could cost millions of dollars. The technical know-how was closely guarded—you couldn't just hire a few engineers and figure it out. And the customer relationships took decades to build—steel companies don't switch electrode suppliers lightly when a furnace failure can cost millions in lost production.

The early struggles were brutal. Quality issues plagued initial production runs. Indian steel companies, accustomed to importing electrodes, were skeptical of domestic production. Global customers wouldn't even return phone calls. The company bled money as it ramped up production, with capacity utilization hovering below 50% for years. There were moments when the board questioned whether they should cut their losses and focus on textiles.

But Ravi Jhunjhunwala and his team persisted with an almost religious faith in the business. They sent engineers to France for training, hired metallurgists from IIT, and slowly, painstakingly, improved quality. The breakthrough came in the mid-1980s when they finally achieved consistent UHP grade production. Suddenly, European steel companies started taking notice. An Indian company could produce electrodes that matched Japanese and American quality at 70% of the cost.

By the late 1980s, HEG had found its market fit. The company wasn't trying to be everything to everyone—they focused relentlessly on UHP electrodes for large steel producers. They built relationships with trading houses in Japan, technical partnerships in Europe, and gradually established a reputation for reliability. The domestic market, initially skeptical, became a stable base as Indian steel production grew and import duties made foreign electrodes expensive.

The foundation was set, but the real test would come in scaling up. As the 1990s dawned and India began liberalizing its economy, HEG faced a choice: remain a small, profitable niche player or bet everything on becoming a global scale manufacturer. They chose scale, and that decision would lead them to build what would become one of the most ambitious industrial projects in India.

IV. Building Scale: The Mandideep Plant Story (1990s–2000s)

The liberalization of 1991 changed everything. Suddenly, Indian companies could dream beyond the License Raj's artificial constraints. For HEG, this meant one thing: it was time to build at world scale. The vision was audacious—create a facility that could compete not just on cost but on every metric that mattered to global steel producers: quality, reliability, and capacity.

The chosen site was Mandideep, spread across 170 acres near Bhopal in Madhya Pradesh. The location wasn't random. Bhopal offered proximity to raw material sources, decent infrastructure, and crucially, a state government eager to attract investment after the industrial disaster of 1984 had scared away businesses. HEG negotiated favorable terms for land and power, understanding that in the graphite electrode business, electricity costs could make or break profitability.

The Mandideep plant wasn't just an expansion—it was a complete reimagining of what an Indian manufacturing facility could be. While competitors globally operated multiple small plants, HEG bet on a single, integrated mega-facility. Every step of the production process, from raw material mixing to final machining, would happen under one roof. This wasn't just about efficiency; it was about control. In a business where a tiny variation in baking temperature could ruin an entire batch worth millions, having everything integrated meant fewer variables, better quality control, and faster problem-solving.

The numbers were staggering for an Indian company in the 1990s. The initial phase aimed for 40,000 MT annual capacity, with plans to eventually double it. Each graphitization furnace—the heart of the operation—cost over $10 million. The company invested in state-of-the-art mixing equipment from Germany, baking furnaces from Japan, and machining centers from Italy. This wasn't frugal innovation; this was world-class manufacturing, full stop.

But perhaps the smartest move was the power play—literally. Graphite electrode production is incredibly energy-intensive; graphitization alone consumes about 3,500-4,500 kWh per ton. Rather than remain hostage to the state electricity board's erratic supply and pricing, HEG built its own power generation facilities. Three captive power plants with a combined capacity of 77 MW ensured uninterrupted production and controlled costs. When the grid failed—as it often did in industrial India—HEG's furnaces kept running. The scale-up happened in phases. From 30,000 MT in 2001, capacity increased to 52,000 MT in 2004-05, then to 66,000 MT, and eventually to 80,000 tonnes per annum when the graphite electrode capacity was increased from 66,000 tonnes/annum. Each expansion was timed to coincide with global steel production cycles, though as we'll see, timing the market in commodities is more art than science.

The export success was perhaps the most remarkable achievement. By the early 2000s, HEG was exporting over 70% of its production to more than 30 countries. The customer list read like a who's who of global steel: ArcelorMittal, POSCO, ThyssenKrupp, US Steel, Nucor. These weren't price buyers looking for the cheapest option—they were sophisticated customers who measured electrode performance in terms of consumption rates per ton of steel, breakage rates, and electrical resistance.

The company's export excellence wasn't accidental. HEG won the CAPEXCIL Export Award for 19 consecutive years, a testament to their consistency in quality and delivery. They established warehouses in strategic locations globally, understanding that in the steel business, just-in-time delivery could make the difference between winning and losing a contract.

The vision statement set in the 1990s captured the ambition perfectly: "A vibrant globally acknowledged top league player in Graphite Electrodes and allied businesses with commitment to growth, innovation, quality and customer focus". This wasn't corporate buzzword bingo—it was a clear articulation of intent to compete at the highest levels of global industry.

Quality certifications followed: ISO 9001 since 1996, ISO 14001 since 2001. These weren't just certificates to hang on the wall; they were table stakes for selling to global steel majors. The company invested heavily in testing equipment—spectrometers to measure trace elements, X-ray machines to detect internal cracks, and electrical resistance testing rigs that could predict electrode performance before shipping.

The Mandideep facility became a showcase for what Indian manufacturing could achieve. Foreign customers who visited expecting a low-cost, low-quality operation found instead a world-class facility that could match anything in Japan or Germany. The integration of power generation meant that HEG's production costs were among the lowest globally, while quality matched the best.

But even as HEG built this impressive capability, storm clouds were gathering. The global financial crisis of 2008 would test every assumption about demand, pricing, and the very viability of the graphite electrode industry. The cyclical wilderness years were about to begin.

V. The Cyclical Wilderness Years (2008–2016)

The graphite electrode industry in 2003-2007 looked unstoppable. Chinese steel production was growing at 20% annually, global infrastructure spending was booming, and electrode prices had risen from $2,000 per ton to over $5,000. Every manufacturer, including HEG, was expanding capacity. The positive sentiment regarding the steel industry led to many graphite electrode manufacturers including HEG Ltd increasing their capacity. However, soon thereafter, the 2008 financial crisis struck and the business cycle in the steel sector took a downturn. As a result, HEG Ltd had to scale down its expansion plans from 20,000 TPA to 6,000 TPA.

The timing couldn't have been worse. HEG had just completed a major capacity expansion in 2012, right as global steel production stagnated and Chinese manufacturers flooded the market with cheap electrodes. Prices collapsed from over $5,000 per ton to below $2,000. For a product where raw materials alone cost $1,500 per ton, the math was brutal.

The numbers tell a story of extreme volatility. Between FY2009 and FY2018, HEG posted losses four times. Operating margins swung wildly—from healthy double digits to negative territory and back again. Cash flows turned negative as working capital ballooned with unsold inventory. The stock price reflected this misery, trading in a range between ₹50 and ₹200 for most of the period, giving investors nothing but heartburn.

What made HEG's struggles particularly painful was the comparison with its domestic peer, Graphite India. While HEG bled red ink, Graphite India somehow remained profitable throughout the downturn. The difference wasn't just operational efficiency; it was about product mix, customer concentration, and critically, financial leverage. HEG had borrowed heavily for expansion, and interest costs ate into already thin margins.

March 2017 marked the nadir. The company declared a loss of ₹50 crores for FY2017. Morale at the Mandideep plant was at rock bottom. Engineers who had joined during the boom years questioned whether they'd backed the wrong horse. The board faced tough questions from minority shareholders about whether the graphite electrode business even had a future.

Industry consolidation during this period was savage but necessary. Globally, marginal producers shut down. In China alone, over 30 small manufacturers closed operations. In the West, historic names in the business either merged or exited. The global graphite electrode capacity, which had ballooned to over 2 million tons, began slowly contracting. This was creative destruction at its most brutal—and most necessary.

HEG's survival strategy during these years was textbook crisis management. First, they attacked costs with religious fervor. Power consumption per ton was reduced by 15% through process optimization. Manpower was rationalized—not through mass layoffs but through natural attrition and redeployment. Maintenance schedules were stretched, though carefully, to avoid compromising plant integrity.

Second, they doubled down on customer relationships. When prices are crashing and everyone is desperate for volume, the temptation is to chase any business. HEG did the opposite—they focused on their core customers, accepting lower volumes but maintaining pricing discipline. This meant utilization rates dropped to below 60%, but it preserved relationships that would prove invaluable when the cycle turned.

Third, and perhaps most importantly, they didn't stop investing in capability. Even as they cut operational costs, R&D spending continued. The focus shifted from capacity expansion to efficiency improvement—developing electrodes that could operate at higher current densities, last longer in the furnace, and reduce steel production costs for customers.

The management's communication during this period deserves credit. Rather than hiding behind optimistic projections, they were transparent about challenges. Annual reports from this era read like battlefield dispatches—acknowledging the harsh reality while maintaining faith in the long-term thesis. Ravi Jhunjhunwala's letters to shareholders didn't promise quick turnarounds; instead, they asked for patience, arguing that cycles are inherent to commodity businesses and that HEG was positioning itself for the next upturn.

The financial gymnastics required to survive were impressive. Working capital was squeezed through better inventory management and aggressive collection of receivables. Capital expenditure was limited to essential maintenance. Dividend payments were suspended—a painful decision for a promoter-driven company where dividends were often the family's primary income source.

But perhaps the most important decision was what HEG didn't do: they didn't diversify into unrelated businesses, they didn't make desperate acquisitions, and crucially, they didn't significantly dilute equity despite the pressure. The promoter group maintained their stake, betting their own wealth on eventual recovery.

By 2016, the global graphite electrode industry had been rationalized through the painful process of bankruptcy and consolidation. Capacity utilization globally was still low, but the supply-demand balance was slowly improving. Chinese steel production had stabilized, and more importantly, the Chinese government was beginning to talk about environmental controls and supply-side reforms.

Nobody could have predicted what would happen next. The same company that had declared a ₹50 crore loss was about to embark on one of the most spectacular profit runs in Indian corporate history. The China effect was about to transform HEG from a struggling survivor into a money-printing machine.

VI. The China Effect & The Supercycle (2016–2018)

In November 2016, something shifted in Beijing's power corridors. The Chinese government, facing apocalyptic pollution levels in major cities and international pressure on emissions, announced sweeping environmental reforms. The policy had an innocuous name—"Supply-Side Structural Reform"—but its impact on global commodity markets would be seismic. For the graphite electrode industry, it was the equivalent of half the world's supply vanishing overnight.

The mechanics were simple but devastating. China's pollution control measures in 2016 led to a shift to Electric Arc Furnace Technology resulting in 80% less pollution. Simultaneously, environmental inspectors began shutting down polluting industries, and graphite electrode plants—with their massive carbon emissions from the graphitization process—were prime targets. By early 2017, China had closed nearly 30% of its electrode capacity. Plants that had operated for decades were given 48 hours to shut down. No appeals, no extensions.

The first signs of the squeeze appeared in spot markets. Electrode prices, which had languished around $2,000 per ton, suddenly jumped to $3,000 in January 2017. By March, they hit $5,000. Steel producers, accustomed to treating electrodes as a minor cost item, suddenly found themselves in bidding wars. Some electric arc furnaces actually shut down because they couldn't source electrodes at any price.

At HEG's Mandideep plant, the transformation was surreal. The same sales team that had spent years begging for orders suddenly found their phones ringing non-stop. Customers who had previously negotiated ruthlessly over every dollar were now placing orders at whatever price HEG quoted. The order book, nearly empty in early 2017, was suddenly overflowing with demand stretching out 6-8 months.

The financial transformation was even more dramatic. HEG's stock, which had been trading at ₹150 in March 2017, began its moonshot. By September, it crossed ₹1,000. By December, ₹2,000. The velocity of the move stunned even bulls. Every quarterly result brought fresh surprises—margins that expanded from 10% to 30% to 50%. The company that had declared a ₹50 crore loss was suddenly printing ₹600 crore quarterly profits.

The numbers from this period read like fiction. HEG went from a Rs 50 crore loss to Rs. 2,600 crores trailing twelve-month profits. EBITDA margins touched 65%—levels typically associated with software companies, not commodity manufacturers. Return on equity exceeded 100%. The company was generating more cash in a quarter than it had in the previous decade combined.

What made this supercycle different from previous commodity booms was its concentration. With Chinese capacity offline and Western producers already operating at maximum utilization, the pricing power concentrated in the hands of a few players. The top five manufacturers globally controlled 75% of UHP electrode capacity. It was an oligopoly's dream scenario—inelastic demand meeting constrained supply.

HEG's management, to their credit, didn't get carried away. While electrode prices were skyrocketing, they maintained consistent pricing to long-term customers, understanding that relationships built over decades shouldn't be sacrificed for short-term gains. They also resisted the temptation to massively expand capacity, remembering the painful lessons of 2008.

The market's reaction was bifurcated. Momentum traders piled in, driving the stock to ₹4,000 by early 2018—a 2,500% gain in 18 months. But value investors remained skeptical. The P/E ratio during the boom stayed at just 5-6, reflecting the market's belief that these earnings were unsustainable. The debate on business channels was fierce: Was this a new normal for electrode pricing, or just another cycle peak waiting for a crash?

Inside HEG, the boom created its own challenges. Employees who had endured years of stagnant salaries suddenly expected windfalls. The company had to balance rewarding loyalty with maintaining cost discipline for the inevitable downturn. Raw material suppliers, seeing HEG's massive profits, demanded price increases. Even the state government wanted a larger share through various levies and taxes.

The strategic decisions made during this period would define HEG's future. First, they accelerated debt repayment, understanding that financial flexibility would be crucial when the cycle turned. Second, they invested in debottlenecking operations, squeezing additional production from existing assets rather than building new capacity. Third, and perhaps most importantly, they began preparing for the downturn even as profits soared.

The supercycle also revealed uncomfortable truths about the graphite electrode industry. The concentration of needle coke production—the key raw material—in a handful of suppliers meant that even as electrode prices soared, raw material costs also spiked. The spread expanded dramatically, but the absolute cost increases were significant. Moreover, the emergence of alternative technologies like hydrogen-based steel production raised questions about long-term electrode demand.

By late 2018, cracks began appearing. Chinese capacity was slowly coming back online as producers upgraded their environmental controls. Steel production growth was slowing globally. The trade war between the US and China created uncertainty about global demand. Electrode prices, which had touched $35,000 per ton for some grades, began their inevitable descent.

The supercycle was ending, but its impact would resonate for years. HEG had generated enough cash to transform its balance sheet, upgrade its operations, and prepare for the next phase of competition. The question now was whether they could maintain relevance in a normalizing market.

VII. Post-Boom Reality & Current Challenges (2019–Present)

The hangover was inevitable, but its severity still surprised many. By mid-2019, graphite electrode prices had crashed back to $5,000-7,000 per ton—still above the 2016 trough but a far cry from the $35,000 peaks. HEG's quarterly profits, which had touched ₹800 crores, normalized to ₹50-100 crores. The stock price followed suit, falling from ₹4,000 to below ₹1,000, wiping out nearly ₹15,000 crores in market capitalization.

The post-boom period revealed the structural challenges that the supercycle had temporarily masked. Recent performance showed poor sales growth of 0.14% over five years and low ROE of 7.43% over 3 years. The fundamentals of the graphite electrode business—overcapacity, Chinese competition, and technological substitution threats—reasserted themselves with vengeance.

FY 2024's financials told a story of a business searching for equilibrium. Revenue of ₹2,395 crores was respectable but flat. EBITDA of ₹526 crores translated to margins around 22%—healthy by most standards but a far cry from the 65% peaks. Net profit of ₹232 crores meant the company was solidly profitable but no longer the cash machine that had captured imaginations during the boom.

The current headwinds are multiple and interrelated. Graphite electrode prices remain under pressure as Chinese capacity has not only returned but expanded with newer, more efficient plants. Raw material costs, particularly needle coke, remain elevated due to competition from the lithium-ion battery industry, which uses the same precursor material. The spread between selling prices and raw material costs has compressed to levels that make capacity expansion uneconomical. Management's response has been multi-pronged. In June 2024, HEG incorporated a wholly-owned subsidiary, HEG Graphite Limited, signaling intentions to diversify within the graphite value chain. More significantly, in October 2024, HEG acquired an 8.23% stake in GrafTech International, a NYSE-listed graphite electrode manufacturer, for ₹250 crores. This wasn't just a financial investment—it was a strategic move to gain insights into global market dynamics and potentially explore operational synergies.

The company also approved plans to demerge its graphite business into a separate entity and merge Bhilwara Energy into itself, indicating a restructuring aimed at unlocking value and improving operational focus. These corporate actions suggest management's recognition that the status quo isn't sustainable and that structural changes are needed to navigate the post-boom reality.

Global competition has intensified significantly. Chinese manufacturers, having upgraded their environmental controls, are now producing at lower costs than during the pre-2016 period. Japanese and American producers have consolidated further, creating larger, more efficient entities. The industry has essentially returned to its pre-boom structure: oversupplied, intensely competitive, and subject to the whims of steel production cycles.

The demand outlook is mixed at best. While the long-term shift towards electric arc furnaces supports electrode demand—EAFs produce 80% less carbon emissions than blast furnaces—the pace of transition has been slower than expected. Steel companies, burned by the 2017-2018 price spike, are more cautious about EAF investments. Moreover, emerging technologies like hydrogen-based direct reduction threaten to bypass electrodes entirely.

Operational challenges have also mounted. The Mandideep plant, while world-class, is now over 25 years old in parts. Maintenance capital expenditure is rising, and the cost of staying technologically current is significant. The workforce, expanded during the boom, needs to be right-sized without losing critical expertise. Raw material sourcing remains challenging, with needle coke suppliers prioritizing battery manufacturers who offer more stable, long-term contracts.

The financial metrics reflect these challenges starkly. Working capital cycles have extended as customers demand longer payment terms. Return on capital employed, which exceeded 100% during the boom, has normalized to the mid-teens. The stock market has essentially written off any return to supercycle conditions, valuing HEG at less than 1.5 times book value despite the company's market leadership position.

Yet there are green shoots. The recent completion of capacity expansion from 80,000 to 100,000 tons per annum positions HEG as the world's largest single-site graphite electrode manufacturer. This scale advantage, combined with integrated power generation, gives HEG one of the lowest cost structures globally. When the next upturn comes—and in commodities, it always does—HEG will be positioned to capture disproportionate value.

VIII. Technology, R&D & Future Bets

Inside a nondescript building at the Mandideep complex, away from the roaring furnaces and humming power plants, sits HEG's real bet on the future: the R&D Center for Carbon Science and Technology. This isn't your typical corporate R&D setup with a few engineers tinkering on incremental improvements. It's a serious attempt to move beyond commodity graphite electrodes into advanced materials that could define the next generation of carbon products.

The R&D center's dual mandate reflects both pragmatism and ambition. On one hand, they focus on conventional carbon products—improving electrode performance, reducing production costs, optimizing raw material usage. On the other, they're pushing into exotic territories: carbon nanotubes that could revolutionize electronics, carbon fibers for aerospace applications, and specialty graphites for emerging battery technologies.

The collaborations read like a who's who of Indian technical institutions. IIT Kanpur brings fundamental research capabilities in material science. Regional Research Laboratory (RRL) Bhopal provides testing infrastructure that HEG couldn't justify building in-house. The Center for Environment, Fire and Explosive Safety (CEFES) in New Delhi helps navigate the increasingly complex regulatory landscape around carbon manufacturing. These aren't ceremonial MoUs—they represent active research programs with dedicated funding and clear commercial objectives.

The needle coke challenge has become existential. This petroleum-derived precursor, essential for high-quality electrodes, now faces fierce competition from lithium-ion battery manufacturers. Battery-grade synthetic graphite commands premium pricing and offers manufacturers long-term supply contracts that electrode makers can't match. HEG's response has been to explore alternative feedstocks—coal tar pitch modifications, bio-based precursors, even recycled carbon sources. None are commercially viable yet, but the research continues with urgency. The big strategic pivot is HEG's entry into battery materials. The company established a graphite anode production facility with a capacity of 20,000 tons, backed by a capital expenditure of approximately ₹1,800 crores. This isn't a casual diversification—it's a recognition that the future of graphite lies as much in energy storage as in steel production. The lithium-ion battery industry needs 1,100 tonnes of graphite anode for every GWh of cell production, and with India targeting 260 GWh of battery capacity by 2030, the opportunity is massive.

The Advanced Carbons Company (TACC), HEG's wholly-owned subsidiary formed for this venture, represents a calculated bet on India's energy transition. With over 90% of global anode production currently controlled by China and Japan, HEG sees an opportunity to leverage its decades of graphite expertise in a new, rapidly growing market. The facility will include a specialized innovation center for developing carbon derivative materials like graphene and carbon nanotubes—materials that could command prices orders of magnitude higher than commodity electrodes.

Sustainability initiatives have moved from corporate social responsibility checkbox to operational necessity. The Mandideep plant has invested heavily in pollution control equipment, understanding that environmental compliance isn't optional in a post-China-crackdown world. Energy efficiency improvements have reduced power consumption per ton by 20% over the past decade. Water recycling systems now recover 85% of process water. These aren't just feel-good initiatives—they're survival tactics in an industry where environmental credentials increasingly determine market access.

The recent capacity expansion to 100,000 MT per annum, completed in November 2023 at a cost of ₹1,200 crores, makes HEG the world's largest single-site graphite electrode manufacturer. This wasn't just about adding furnaces—it involved state-of-the-art equipment and technologies that are environmentally friendly, making it arguably the most modern plant globally. The expansion was completed in record time despite COVID interruptions, demonstrating the company's execution capabilities.

The technology roadmap reveals both ambition and pragmatism. While continuing to optimize electrode production—where even a 1% improvement in yield can add millions to the bottom line—HEG is simultaneously exploring frontier applications. Carbon nanotubes for aerospace, specialized graphites for nuclear reactors, high-purity carbons for semiconductor manufacturing—each represents a potential escape from the commodity trap.

But perhaps the most interesting technological development is in process innovation rather than product innovation. HEG has developed proprietary modifications to the graphitization process that reduce energy consumption by 15% while maintaining product quality. In an industry where energy costs can be 40% of total production costs, this is a significant competitive advantage. They've also pioneered recycling techniques that recover graphite from used electrodes—a circular economy approach that both reduces raw material costs and appeals to environmentally conscious customers.

The R&D efforts face significant challenges. The global leaders in graphite technology—companies like Showa Denko and Tokai Carbon—spend multiples of HEG's entire R&D budget. Chinese competitors, while less sophisticated, benefit from massive government subsidies for battery material research. HEG must be selective, focusing on niches where Indian cost advantages and specific technical capabilities converge.

Looking forward, HEG's technology strategy appears to be hedging multiple futures. If electric arc furnaces dominate steel production, their electrode business remains relevant. If hydrogen-based steel production takes off, their carbon expertise could pivot to other applications. If battery materials become the primary profit pool, they're positioned to capture value. It's a portfolio approach to R&D that acknowledges the uncertainty inherent in industrial transformation.

IX. Playbook: Business & Investing Lessons

After following HEG's journey from a License Raj experiment to a global manufacturer, through boom and bust cycles that would make a venture capitalist queasy, what lessons emerge for operators and investors? The playbook isn't just about graphite electrodes—it's about navigating extreme cyclicality, building competitive advantage in commodities, and the peculiar dynamics of being an emerging market player in a global industry.

Lesson 1: In commodities, timing isn't everything—survival is. HEG posted losses four times between 2009-2018 while competitor Graphite India remained profitable throughout. Yet when the cycle turned, HEG captured similar upside. The lesson? In extreme cyclicality, the ability to survive the downturn matters more than optimizing performance during it. This means maintaining financial flexibility, avoiding excessive leverage at cycle peaks, and having patient capital that won't force liquidation at the bottom.

Lesson 2: Being the lowest-cost producer is necessary but not sufficient. HEG's integrated facility at Mandideep, with captive power generation and single-site operations, gives it one of the lowest cost structures globally. But during downturns, even the lowest-cost producer can bleed cash if industry pricing falls below cash costs. The real advantage of low-cost production is the ability to remain cash-flow positive longer than competitors, potentially gaining market share as higher-cost producers exit.

Lesson 3: Industry consolidation creates temporary monopolies. The graphite electrode industry's consolidation—with the top five manufacturers controlling 75% of UHP electrode capacity—created conditions for the 2017-2018 supercycle. When supply is concentrated and demand is inelastic, even small supply disruptions can cause explosive price increases. Investors should track industry concentration metrics as leading indicators of potential pricing power.

Lesson 4: Export strategy in cyclical industries requires relationship capital. HEG exports over 70% of production to more than 30 countries. During downturns, these relationships provided volume even when domestic demand collapsed. During upturns, they provided access to premium markets. The 19 consecutive CAPEXCIL Export Awards weren't just trophies—they represented decades of relationship-building that paid off when cycles turned.

Lesson 5: Capital allocation during booms determines survival during busts. HEG's decision during the 2017-2018 boom to pay down debt rather than dramatically expand capacity proved prescient. The temptation during commodity booms is to extrapolate current prices and build for a future that never arrives. HEG's relatively conservative expansion—from 80,000 to 100,000 MT—balanced growth with prudence.

Lesson 6: Entry barriers in capital-intensive industries are real but temporal. HEG was the last entrant into the global graphite electrode industry in 1977. For decades, this created a cozy oligopoly. But technology evolution, environmental regulations, and shifts in end markets can suddenly lower these barriers. The emergence of Chinese capacity in the 2000s showed that entry barriers are powerful until they aren't.

Lesson 7: Vertical integration in commodities is about control, not just cost. HEG's backward integration into power generation wasn't just about reducing electricity costs—it was about ensuring uninterrupted production when the grid failed. In industries where process interruption can destroy millions in work-in-progress inventory, control over critical inputs becomes existential.

Lesson 8: Managing stakeholder expectations through volatility requires transparent communication. HEG's management deserves credit for honest communication during downturns. Rather than promising imminent turnarounds, they acknowledged the structural challenges while maintaining confidence in long-term fundamentals. This built credibility that proved valuable when explaining why the 2017-2018 boom was temporary.

Lesson 9: Geographic diversification of customers provides resilience. When Chinese demand collapsed, European and American customers sustained volumes. When Western economies slowed, Asian demand provided support. No single geography ever accounts for more than 40% of HEG's sales—a deliberate strategy that smooths regional cycles.

Lesson 10: Technology evolution in traditional industries happens slowly, then suddenly. For decades, the basic graphite electrode technology remained unchanged. Then, within a few years, battery applications emerged, hydrogen steel production became viable, and environmental regulations reshaped competitive dynamics. Companies that maintained R&D investment during stable periods were positioned to adapt when change accelerated.

The meta-lesson from HEG's playbook is that commodity businesses aren't just about riding cycles—they're about building structural advantages that compound over decades. Scale, cost position, customer relationships, and technical capabilities create a flywheel that accelerates during upturns and provides resilience during downturns. For investors, the challenge is distinguishing between cyclical headwinds and structural decline, between temporary pricing power and sustainable competitive advantage.

X. Analysis & Bear vs. Bull Case

Standing at the current juncture, HEG presents one of those quintessential investment dilemmas that make markets: a company with proven operational excellence in a structurally challenged industry, trading at valuations that could either represent deep value or a value trap. Let's examine both sides of this debate with the rigor it deserves.

The Bull Case: Structural Tailwinds Meeting Operational Excellence

The bulls start with a simple observation: the world needs cleaner steel, and electric arc furnaces are the only proven technology to deliver it at scale. EAF-based production generates 80% less carbon emissions than traditional blast furnaces. With over 100 million tonnes of new EAF capacity announced globally, and another 30 million tonnes expected operational by 2025, electrode demand should grow by 150,000-200,000 MT by 2030. In a market where global capacity outside China is roughly 800,000 MT, this represents a 20-25% demand increase.

India's position housing 20% of global graphite electrode capacity with only five major global players creates an oligopolistic market structure. The capital intensity of new capacity—roughly $50,000 per ton for a greenfield plant—combined with 18-24 month construction periods creates significant barriers to supply response. When demand exceeds supply by even 5%, prices can double or triple, as 2017-2018 demonstrated.

Environmental regulations globally are tightening, not loosening. China's dual control system for energy consumption, Europe's Carbon Border Adjustment Mechanism, and the US Infrastructure Act all incentivize EAF adoption. These aren't temporary policy whims but structural shifts reflecting climate commitments that will shape industrial policy for decades.

The battery anode opportunity represents optionality worth far more than its current investment. With India targeting 260 GWh of battery capacity by 2030, requiring approximately 286,000 tonnes of graphite anode, HEG's early mover advantage in a market dominated by China and Japan could prove transformative. Even capturing 10% market share would double HEG's revenue base at significantly higher margins than electrode production.

HEG's operational advantages are tangible and difficult to replicate. The Mandideep facility's scale, integration, and captive power generation create a cost structure that's globally competitive. The recent capacity expansion to 100,000 MT makes HEG the third-largest producer globally, providing leverage to any upturn in pricing.

The company's balance sheet has been transformed from the supercycle windfall. Debt is manageable, working capital is optimized, and the company has dry powder for opportunistic investments like the GrafTech stake acquisition. This financial flexibility means HEG can weather another downturn or capitalize on distressed assets.

The Bear Case: Structural Challenges in a Commoditized Market

The bears counter with an equally compelling narrative: HEG is a commodity producer in an industry with persistent overcapacity, facing technological disruption and geopolitical risks. The recent performance—sales growth of 0.14% over five years and ROE of 7.43% over three years—isn't a cyclical aberration but the new normal.

Extreme cyclicality makes this business essentially uninvestable for anyone except traders. The stock has been a wealth destroyer for anyone who bought outside the narrow windows of cycle turns. Even if you correctly predict the next upturn, the magnitude and timing are unknowable. The 2017-2018 supercycle was a once-in-a-generation event driven by China's supply shock—unlikely to repeat.

China remains the sword of Damocles hanging over the industry. Chinese electrode capacity has not only recovered but expanded with newer, more efficient plants. If China decides to flood global markets—as it has in steel, solar panels, and countless other industries—electrode prices could remain depressed for years. The recent environmental restrictions could reverse with a policy change, instantly adding hundreds of thousands of tonnes of supply.

Raw material pressures are structural, not cyclical. Needle coke producers prefer selling to battery manufacturers who offer stable, long-term contracts at premium prices. As battery demand grows, electrode manufacturers become the marginal buyers, facing volatile availability and pricing. This dynamic will only worsen as EV adoption accelerates.

Competition from alternative technologies poses an existential threat. Hydrogen-based direct reduction of iron ore, while nascent, could eliminate the need for electrodes entirely. Major steel producers like SSAB and ArcelorMittal are investing billions in hydrogen technology. Even a partial shift would devastate electrode demand.

The battery anode venture, while strategically sound, faces formidable challenges. Chinese competitors have decades of experience, massive scale, and government support. Japanese producers have technology advantages and established customer relationships. HEG is entering a market where it has no competitive advantage except proximity to potential Indian customers—who themselves are unproven in battery manufacturing.

The current valuation, while optically cheap, may be a value trap. The market is pricing HEG based on normalized earnings that may never materialize. The P/E ratio of 5-6 during the boom reflected investor skepticism about sustainability—skepticism that proved justified. Current multiples might still be too high if the industry enters a prolonged downturn.

The Synthesis: A Complex Risk-Reward Equation

The truth, as often happens, lies somewhere between these extremes. HEG is neither a hidden gem waiting to multiply investor wealth nor a melting ice cube destined for irrelevance. It's a well-run company in a difficult industry, with real competitive advantages offset by structural challenges.

For fundamental investors, HEG represents a complex probability-weighted outcome. If global steel production shifts meaningfully to EAF, if environmental regulations tighten as expected, if the battery anode venture gains traction, and if Chinese supply remains disciplined, HEG could deliver spectacular returns. But that's a lot of "ifs."

The investment case ultimately depends on one's view of industrial decarbonization. If you believe the world is serious about reducing emissions, EAF adoption must accelerate, and graphite electrodes become increasingly strategic. If you're skeptical about the pace of energy transition, or believe alternative technologies will leapfrog current solutions, HEG remains a cyclical commodity play best avoided except by specialized traders.

For long-term investors, perhaps the right framework isn't bull versus bear, but option value versus carrying cost. At current valuations, you're paying a modest premium for optionality on multiple positive scenarios. The question is whether you have the patience and stomach to wait for those scenarios to materialize—knowing that the wait could be long and volatile.

XI. Epilogue & Reflections

As we reach the end of HEG's story—or rather, the latest chapter in an ongoing saga—it's worth stepping back to consider what this journey teaches us about Indian manufacturing, global commodity cycles, and the nature of industrial capitalism itself.

The boom-bust nature of industrial commodities isn't a bug; it's a feature. These cycles, brutal as they are for participants, serve an essential economic function: they periodically clear out excess capacity, force technological innovation, and reallocate capital to more productive uses. HEG's survival through multiple cycles isn't just a testament to management competence—it's a case study in institutional resilience.

The 2017-2018 supercycle deserves special reflection. In those 18 months, HEG generated more profit than in its entire previous history. The company's market capitalization briefly exceeded $2 billion. Employees became paper millionaires through stock options. The Mandideep plant, for a brief moment, was one of the most profitable industrial facilities in India per square foot.

Yet the speed of the reversal was equally breathtaking. By 2019, the same analysts who had projected electrode shortages for years were warning of structural oversupply. The stock gave back 75% of its gains. The lesson isn't that markets are irrational—they're actually quite rational in recognizing that commodity supercycles are, by definition, temporary. The irrationality lies in expecting otherwise.

What would different capital allocation have looked like? Imagine if, during the 2017-2018 boom, HEG had returned even more capital to shareholders through special dividends or buybacks. Or conversely, what if they had made a transformational acquisition in an adjacent but less cyclical business? The path taken—moderate expansion, debt reduction, and maintenance of financial flexibility—was probably optimal given the information available. But it highlights how in cyclical industries, there are no perfect answers, only trade-offs.

HEG's position today—survivor or thriver—depends on your time horizon. In the near term, they're clearly surviving, grinding through another down cycle with discipline and patience. But the seeds of thriving may already be planted: the battery anode venture, the GrafTech investment, the steady improvement in operational metrics. Whether these seeds germinate into the next phase of growth remains uncertain.

The future of graphite electrodes in a decarbonizing world presents a fascinating paradox. On one hand, electrodes are essential for the cleanest form of large-scale steel production currently available. On the other, the ultimate goal of decarbonization might eliminate the need for traditional steel production altogether, replacing it with hydrogen-based processes or even alternative materials.

This uncertainty isn't unique to HEG or graphite electrodes. Across the industrial landscape, companies are grappling with similar transitions. Coal companies investing in renewable energy, oil companies becoming energy companies, automotive suppliers pivoting to electric vehicles—everyone is hedging, diversifying, trying to navigate a future that's fundamentally uncertain.

For HEG specifically, the next decade will likely determine whether it remains a regional champion in a niche industry or transforms into something larger. The building blocks are there: technical expertise in carbon materials, operational excellence in complex manufacturing, relationships with global customers, and now, exposure to the battery value chain. But building blocks don't automatically assemble themselves into castles.

The Indian context adds another layer of complexity. As India pushes for manufacturing self-reliance through initiatives like Make in India and PLI schemes, companies like HEG become strategic assets. They represent not just commercial enterprises but industrial capabilities that take decades to build. This might provide a floor to government support during severe downturns but also subjects them to political pressures during booms.

Perhaps the most profound lesson from HEG's journey is about the nature of industrial competition itself. In an age obsessed with software margins and platform effects, HEG reminds us that making physical things—especially complex, technical physical things—still matters. The knowledge embedded in the Mandideep plant, accumulated over decades of trial and error, can't be replicated by downloading an app or raising venture capital.

As we close this analysis, HEG stands at an inflection point that mirrors India's own industrial ambitions. Can a company built in the License Raj era reinvent itself for the climate transition era? Can operational excellence in traditional manufacturing translate into success in new energy materials? Can patient, family-controlled capital compete with state-backed Chinese giants and technology-focused Western corporations?

These questions don't have easy answers. But that's precisely what makes HEG's story worth following. In a market increasingly dominated by asset-light business models and winner-take-all dynamics, HEG represents something different: the slow, patient accumulation of industrial capability, the navigation of cycles that destroy the impatient, and the possibility—just the possibility—that making things still matters in the 21st century.

For investors, HEG remains what it has always been: a bet on industrial cycles, operational excellence, and the long arc of global development. It's not a comfortable investment, unlikely to feature in anyone's "sleep well at night" portfolio. But for those who understand its dynamics, accept its volatility, and believe in its underlying thesis, HEG offers something increasingly rare in modern markets: exposure to the real economy, with all its messiness, cyclicality, and occasional moments of spectacular profitability.

The story continues, the cycles turn, and somewhere in Mandideep, the furnaces keep running, turning petroleum coke into graphite electrodes, one batch at a time, waiting for the next turn of the global industrial wheel.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube