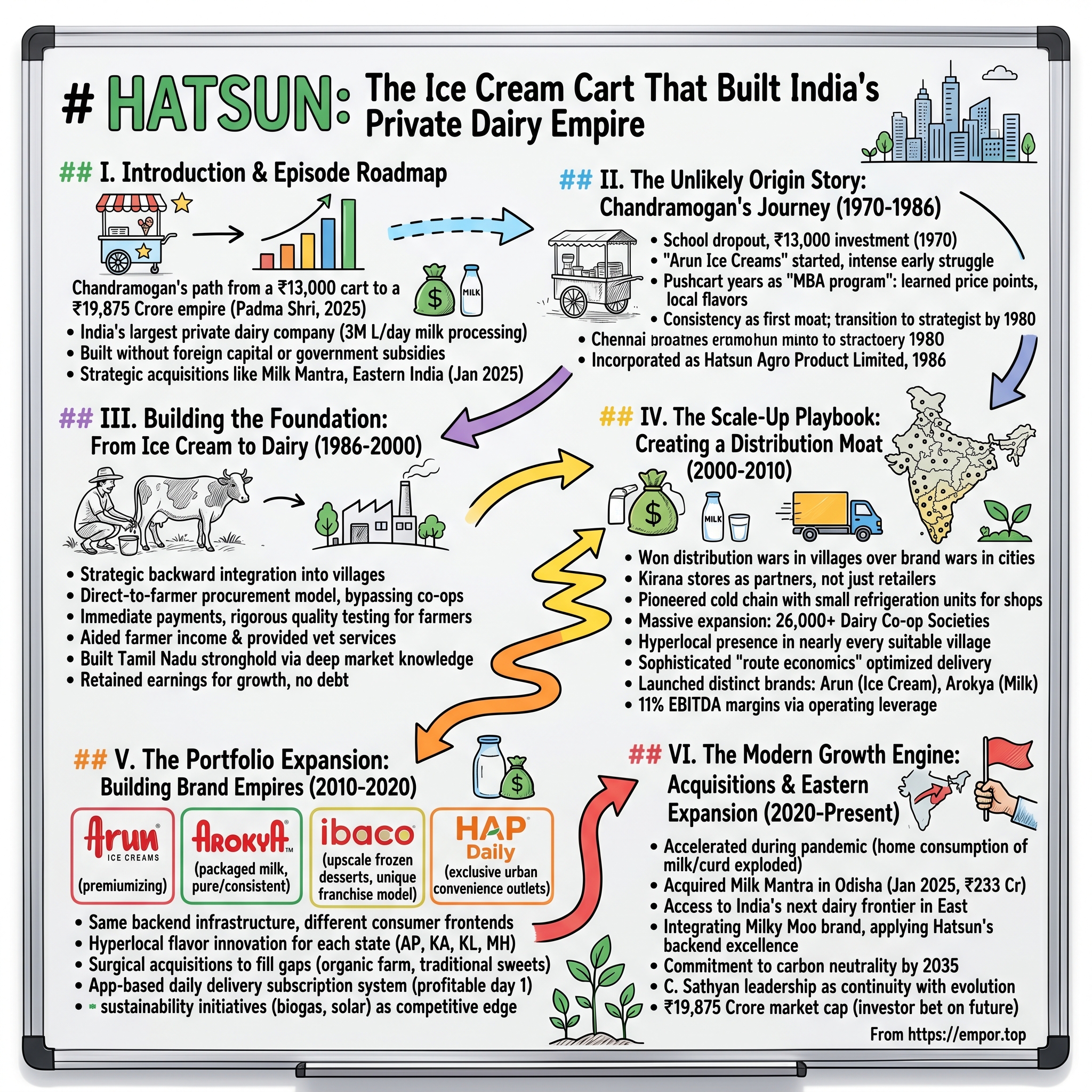

HATSUN: The Ice Cream Cart That Built India's Private Dairy Empire

I. Introduction & Episode Roadmap

Picture this: A 21-year-old school dropout in 1970, standing in a cramped 250-square-foot room in Chennai's Royapuram district, mixing ice cream by hand with three employees. His family had just sold their property to scrape together ₹13,000 for this venture. Fast forward five decades, and that same man—R.G. Chandramogan—commands a dairy empire worth ₹19,875 crores, having just received the Padma Shri, India's fourth-highest civilian honor, in January 2025.

This is the Hatsun story—a narrative that defies every conventional playbook about building a consumer empire in India. While multinational giants burned through capital trying to crack the Indian dairy market, and government cooperatives dominated through political muscle, Chandramogan built something different: India's largest private-sector dairy company, processing 3 million liters of milk daily, serving 2 million retail outlets, and touching the lives of 400,000 farmers. The market capitalization of ₹19,875 crores tells only part of the story. What makes Hatsun remarkable isn't just its scale—it's how Chandramogan built it: without foreign capital in the early decades, without government subsidies, and crucially, without compromising on a simple philosophy of fair pricing for farmers and quality for consumers.

Here's what we'll unpack over the next several hours: How a pushcart ice cream vendor created a distribution network that rivals Amazon's last-mile delivery in Tamil Nadu. Why Hatsun's direct-to-farmer procurement model became its greatest competitive advantage against both cooperatives and multinationals. How strategic acquisitions—including the recent ₹233 crore Milk Mantra acquisition in January 2025—are reshaping Eastern India's dairy landscape. And perhaps most intriguingly, why a company with poor five-year sales growth of just 10.3% and Q3 FY25 profit declining 28.6% still commands such respect from long-term investors.

This is a story about compound effects, regional dominance, and the power of starting with the end consumer in mind—then working backwards through the entire value chain. It's about building in "boring" industries where the TAM (Total Addressable Market) is measured not in app downloads but in the fundamental human need for nutrition. And it's about how sometimes, the best business model is the oldest one: buy from many, sell to more, and never forget who you serve.

Let's dive into how an ice cream cart became an empire.

II. The Unlikely Origin Story: Chandramogan's Journey (1970-1986)

The year is 1970. Richard Nixon is president, the Beatles have just broken up, and in the narrow lanes of Chennai's Royapuram district, a 21-year-old named R.G. Chandramogan is mixing ice cream in a 250-square-foot room that barely fits three people. His formal education ended before he could finish school—not by choice, but by circumstance. His family had just made the ultimate sacrifice: selling their property to raise ₹13,000, roughly $1,700 at the time, to fund what most saw as a foolish dream.

Think about that number for a moment. ₹13,000 in 1970. That's less than what a middle-class family might spend on a weekend trip today. Yet it represented everything Chandramogan's family had. The pressure must have been crushing—this wasn't venture capital that could be written off; this was survival money, retirement savings, the family's entire safety net liquidated for a venture in frozen desserts in a tropical country where refrigeration was a luxury.

Chandramogan named his venture "Arun Ice Creams"—a simple, approachable name that would resonate with Tamil families. But the early days were anything but simple. Without automated machinery, every batch was mixed by hand. Without refrigerated trucks, distribution meant racing against the Chennai sun. Without brand recognition, sales meant pushing a cart through the streets, calling out to skeptical customers who wondered why they should buy from this unknown vendor instead of established players.

The pushcart years of the 1970s weren't just about selling ice cream—they were Chandramogan's MBA program. Each day on the streets taught him something Harvard couldn't: the exact price point where a lower-middle-class family would splurge on a treat, the flavors that worked in South Indian palates, the routes where foot traffic peaked at different times. He learned that in Thiruthangal and surrounding areas, people didn't just want ice cream; they wanted an affordable moment of joy, a small luxury that didn't break the bank.

By 1975, five years into the venture, most founders would have either scaled significantly or shut down. Chandramogan was doing neither. He was surviving—barely. Multiple times, bankruptcy loomed so close he could taste it (ironic for someone in the taste business). Creditors would show up at the small facility. Employees would go unpaid for weeks, staying on only because Chandramogan's conviction was infectious. He would later tell reporters that there were nights he couldn't sleep, not from excitement about growth, but from the fear that tomorrow might be the day it all ended.

The survival tactics he employed during this period would become organizational DNA. When cash was tight, instead of cutting quality, he cut his own salary to zero. When refrigeration costs spiked, instead of raising prices, he found ways to optimize routes to minimize cooling time. When competitors undercut him, instead of matching their prices and margins, he focused on consistency—ensuring that an Arun ice cream tasted the same whether bought in Royapuram or Mylapore.

This obsession with consistency in an industry known for variability became his first moat. Street vendors noticed that Arun ice creams melted slower—Chandramogan had figured out the right stabilizer mix through trial and error. Small shops realized Arun products had longer shelf life without preservatives—he had optimized the fat-to-milk-solids ratio. Customers found that unlike other brands where quality varied by batch, Arun maintained standards that seemed impossible at that price point.

By 1980, a decade in, Arun Ice Creams had graduated from pushcarts to a small fleet of cycle rickshaws with ice boxes. Revenue was still modest—we're talking lakhs, not crores—but something fundamental had shifted. Chandramogan was no longer just surviving; he was building systems. Each rickshaw driver wasn't just a delivery person but a data collector, reporting back on which flavors sold where, what price points worked in different neighborhoods, which shops had refrigeration issues.

The period from 1980 to 1986 was when Chandramogan made the transition from entrepreneur to strategist. He realized that ice cream, while his entry point, was just one part of a much larger opportunity. Indians consumed dairy at every meal—milk with morning coffee, curd with lunch, buttermilk in the afternoon, ghee for dinner cooking. The same supply chain that brought milk for ice cream could be leveraged for all these products. The same cold chain infrastructure could serve multiple categories. The same retailer relationships could carry a portfolio instead of a single product.

This insight—that the real business wasn't ice cream but dairy, that the real asset wasn't the product but the procurement and distribution network—would drive the next phase. In 1986, sixteen years after starting with ₹13,000 and three employees, Chandramogan incorporated Hatsun Agro Product Limited. The name itself signaled ambition: "Agro Product," not just "Ice Creams." This wasn't a rebranding; it was a declaration of intent.

What's remarkable about these first sixteen years is what Chandramogan didn't do. He didn't raise external capital. He didn't expand beyond Tamil Nadu. He didn't diversify beyond dairy. He didn't compromise on quality to grow faster. In an era where entrepreneurs are celebrated for blitzscaling, Chandramogan was doing something radically different: building slowly, learning deeply, and creating a foundation that could support not just a company but an ecosystem.

The school dropout had learned something that no amount of formal education could teach: In a country like India, with its complex supply chains, diverse consumer preferences, and price-sensitive markets, the winners aren't always the fastest or the best funded. Sometimes, they're the ones who understand the ground reality so intimately that they can build solutions others can't even imagine. The pushcart wasn't just Chandramogan's beginning—it was his education, his research lab, and his direct connection to the consumer that would inform every decision for the next five decades.

III. Building the Foundation: From Ice Cream to Dairy (1986-2000)

The incorporation of Hatsun Agro Product Limited in 1986 marked a inflection point, but not in the way most business transformations occur. There was no press release, no venture funding announcement, no rebranding campaign. Instead, Chandramogan did something far more radical for its time: he went backward in the value chain.

While competitors focused on marketing and brand building in urban centers, Chandramogan headed to the villages. The logic was counterintuitive but brilliant. Ice cream was a downstream product—the end result of a complex dairy value chain. But to truly control quality, cost, and supply, you needed to start where the milk began: with the farmers and their cows.

The Tamil Nadu dairy landscape in the late 1980s was dominated by cooperatives—government-supported entities that had political backing, subsidized infrastructure, and decades-old farmer relationships. For a private player to enter this space was almost unthinkable. The cooperatives controlled collection, processing, and distribution. They set prices. They determined which areas got service. Breaking this monopoly seemed impossible.

But Chandramogan spotted inefficiencies that others dismissed as inevitable. Farmers often waited days for payment from cooperatives. Quality testing was rudimentary, with good milk mixed with average, destroying premium potential. Collection happened at fixed times that didn't align with milking schedules, leading to spoilage. And perhaps most critically, farmers had no direct relationship with the end consumer—they were just suppliers in an opaque chain.

Hatsun's approach was revolutionary for its simplicity: pay farmers immediately, test quality rigorously, and share the upside of premium products. The company began setting up collection centers not where it was convenient for trucks, but where it was convenient for farmers. Instead of twice-a-week collection, they collected twice daily, matching natural milking cycles. Instead of averaging prices across quality grades, they paid premiums for higher fat content.

The financial impact on farmers was immediate and dramatic. A typical small farmer with 2-3 cows saw income increase by 20-30% simply through better price realization and reduced spoilage. But Chandramogan went further. Hatsun began providing veterinary services, cattle feed on credit, and even small loans for cattle purchase. This wasn't corporate social responsibility—it was strategic backward integration disguised as farmer welfare.

By 1990, four years post-incorporation, Hatsun had built a network of over 500 direct farmer relationships. Each relationship was more than transactional. The company maintained detailed records: which farmers had which breeds, what their peak production seasons were, what challenges they faced. This data became invaluable for planning—Hatsun could predict supply fluctuations months in advance and adjust production accordingly.

The procurement network enabled the strategic pivot from just ice cream to the full dairy portfolio. Milk, curd, buttermilk, ghee—products that used different components of the same raw material—could now be produced based on real-time supply and demand. If milk procurement exceeded ice cream needs, it went to curd production. If cream supply was high, ghee production ramped up. This flexibility in product mix, impossible without direct procurement control, became a crucial margin driver.

The Tamil Nadu stronghold strategy during this period deserves special attention. While national players were spreading thin across India, Hatsun went deep in one state. By 1995, they weren't just present in Tamil Nadu—they understood it at a granular level. They knew that Coimbatore preferred thicker curd than Chennai. That Madurai consumed more buttermilk in summer than any other city. That coastal areas had different shelf-life requirements than inland regions.

This hyperlocal knowledge translated into product innovation. Hatsun launched pack sizes that matched local consumption patterns—500ml for nuclear families in Chennai, 1-liter for joint families in smaller towns. They introduced flavors that resonated with Tamil tastes—not just vanilla and chocolate, but jackfruit, sapota, and traditional kulfi. They even adjusted sweetness levels by region, recognizing that preferences varied significantly across the state.

The brand building during this period was subtle but effective. "Arun" wasn't positioned as aspirational or premium—it was positioned as reliable and accessible. The tagline wasn't about indulgence or international quality; it was about being part of daily life. Every small town that got an Arun ice cream cart felt included in a modern economy that usually ignored them. Every farmer who supplied to Hatsun felt like a partner, not just a vendor.

By 1998, Hatsun had quietly built something remarkable: a vertically integrated dairy business with procurement, processing, and distribution entirely under its control. Revenue had grown from lakhs to crores, but more importantly, the foundation was set. The company operated 15 processing plants, collected from 10,000+ farmers, and served 50,000+ retail outlets. The numbers were impressive, but the real asset was invisible: the trust of thousands of farmers who saw Hatsun not as a corporation but as a partner.

The financial discipline during this period was extraordinary. Despite rapid expansion, Hatsun maintained positive cash flows. Instead of debt-funded growth, they used retained earnings. Instead of glamorous corporate offices, they operated from functional spaces. Every rupee saved went back into the procurement network or processing capacity. Chandramogan's philosophy was clear: build the pipes before you pump the water.

As the millennium approached, Hatsun faced a crucial decision. The liberalization of the Indian economy had brought international players like Unilever and Nestle into the dairy market. These giants had marketing budgets that exceeded Hatsun's total revenue. They had global R&D centers, international brand recognition, and deep pockets for price wars. The conventional wisdom suggested Hatsun should either seek a buyer or remain a regional player.

But Chandramogan saw opportunity where others saw threat. The multinationals had everything except what Hatsun had spent 15 years building: direct farmer relationships, hyperlocal market knowledge, and a distribution network that reached where others couldn't. The foundation was complete. Now it was time to scale.

IV. The Scale-Up Playbook: Creating a Distribution Moat (2000-2010)

The year 2000 opened with Y2K fears that never materialized, but for Hatsun, a very real challenge was emerging. Multinational corporations were flooding the Indian dairy market with advertising budgets that dwarfed Hatsun's entire revenue. Amul was expanding beyond Gujarat with cooperative might. Local players were consolidating. In this environment, Chandramogan made a counterintuitive decision: instead of fighting the brand wars in cities, he would win the distribution wars in villages.

The math was compelling. India's top 50 cities accounted for just 10% of dairy consumption. The real market—90% of volume—was in the 600,000 villages and small towns where refrigeration was spotty, roads were rough, and consumers bought daily in small quantities. This was a market the MNCs couldn't crack with their hub-and-spoke models designed for urban efficiency. But for Hatsun, with its farmer network already in place, these villages weren't the last mile—they were the first.

The distribution transformation began with a simple insight: in rural India, distribution wasn't just about logistics—it was about relationships. The local kirana store owner wasn't just a retailer; he was a credit provider, information source, and trust anchor for the community. Win his confidence, and you won the village. Hatsun's approach wasn't to simply supply these stores but to make them partners in growth.

The company introduced what seemed like a mundane innovation but proved revolutionary: small-format refrigeration units provided on zero-interest loans to retailers. A typical unit cost ₹15,000—affordable for Hatsun, transformative for a small shop. Suddenly, stores that could only sell shelf-stable products could offer chilled milk, curd, and ice cream. The refrigerator carried Hatsun branding, creating permanent visibility. More importantly, once a shop invested in cold chain infrastructure for Hatsun, switching costs to competitors became prohibitive.

By 2005, midway through the decade, Hatsun had deployed over 10,000 refrigeration units. But the real innovation was the service model wrapped around them. Each unit came with free maintenance, immediate replacement guarantees, and—crucially—training for shop owners on inventory management. Hatsun field representatives didn't just deliver products; they helped optimize stock levels, suggested product mix based on local preferences, and even helped with promotional displays.

The farmer network, which had grown to 50,000 by 2003, became the backbone of an even more ambitious initiative: the dairy cooperative society model. Unlike government cooperatives that operated at tehsil or district levels, Hatsun created hyperlocal societies at the village level. By decade's end, the network had expanded to 26,000+ dairy cooperative societies—essentially, Hatsun had a presence in nearly every viable dairy-producing village in Tamil Nadu.

Each society wasn't just a collection point but a hub of activity. Hatsun provided veterinary services, conducting over 100,000 cattle health camps during the decade. They introduced artificial insemination services, improving cattle yields by 30-40%. They even started "Farmer Schools," teaching everything from fodder management to financial planning. The investment was massive—over ₹100 crore in farmer development programs—but the returns were multiplicative.

The procurement numbers tell the story: milk collection increased from 500,000 liters per day in 2000 to 2 million liters per day by 2008. But volume was just one metric. Quality improved dramatically—the percentage of high-fat milk increased from 20% to 45%. Spoilage reduced from 5% to less than 1%. Most remarkably, farmer loyalty became absolute—attrition rates dropped to near zero, unheard of in an industry where farmers routinely switched buyers for marginal price differences.

The retail footprint expansion was equally dramatic. From 50,000 outlets in 2000, Hatsun reached 2 million+ retail outlets by decade's end. But coverage alone doesn't explain the success. The company pioneered what they called "route economics"—sophisticated algorithms that optimized delivery routes not just for distance but for product mix, payment cycles, and even traffic patterns. A typical delivery van in 2000 served 30 outlets; by 2010, the same van served 70 outlets through better routing.

Technology adoption during this period was pragmatic rather than flashy. While competitors invested in ERP systems and corporate IT infrastructure, Hatsun focused on field technology. They introduced handheld devices for milk testing at collection points—farmers could see fat content, SNF (Solids-Not-Fat) levels, and payment calculations in real-time. They deployed GPS tracking on delivery vehicles, not for surveillance but for route optimization. They even created SMS-based ordering systems for retailers, revolutionary in an era before smartphones.

The multi-brand strategy that would define Hatsun's next phase began taking shape. Recognizing that different consumer segments had different needs, they moved beyond the single "Arun" brand. "Arokya" emerged for premium milk products. "Hatsun" became the value brand. "HAP Daily" targeted urban convenience seekers. Each brand had distinct positioning, but all leveraged the same backend infrastructure—procurement, processing, and distribution.

The financial performance during this period validated the strategy. Revenue grew from ₹400 crore in 2000 to ₹2,000 crore by 2010—a 5x increase. But more impressively, EBITDA margins improved from 6% to 11%, defying the conventional wisdom that says margins compress with scale. The key was the operating leverage: the same farmer who supplied milk for ice cream also supplied for curd, butter, and ghee. The same truck that delivered ice cream also carried milk and yogurt. The same retailer who stocked one Hatsun product typically stocked five.

By 2008, as the global financial crisis struck, Hatsun faced its first major external shock in the new millennium. Commodity prices spiked—milk procurement costs increased 40% in 18 months. Urban consumers cut discretionary spending. Rural credit dried up. Many dairy companies, leveraged for growth, faced existential crises. But Hatsun's conservative financial management paid off. With minimal debt and strong farmer relationships that prevented supply-side inflation, they not only survived but gained market share from struggling competitors.

The decade ended with Hatsun winning "The Fastest Growing Asian Dairy Company" award—recognition that transcended India. International dairy giants started paying attention. Private equity firms came calling. But Chandramogan, now 60, wasn't interested in exits or external capital. He had spent 40 years building not just a company but an ecosystem. With 150,000 farmers depending on Hatsun for livelihood, 2 million retailers for inventory, and millions of consumers for daily dairy needs, this was no longer just a business—it was infrastructure.

The moat was complete: any competitor wanting to challenge Hatsun in South India would need to replicate not just processing plants or brands but relationships built over decades, trust earned through countless transactions, and knowledge accumulated through millions of data points. The ice cream cart had become a distribution fortress.

V. The Portfolio Expansion: Building Brand Empires (2010-2020)

The new decade began with India's dairy market at an inflection point. Urban millennials were discovering artisanal ice creams. Health-conscious consumers wanted organic, premium dairy. Quick-commerce was reshaping consumption patterns. Yet rural India—still 65% of the population—remained price-sensitive and traditional. Hatsun's response wasn't to choose sides but to play all fields simultaneously through distinct brand architecture.

The portfolio strategy crystallized around a simple framework: same backend, different frontends. Arun Ice Creams remained South India's leading ice cream brand, but its positioning evolved. No longer just affordable indulgence, Arun began premiumizing with exotic flavors, sugar-free variants, and even protein-enriched options. The masterstroke was maintaining the mass-market products while adding premium SKUs—a ₹10 candy bar coexisted with a ₹150 sundae, both under the same trusted brand.

"Arokya" emerged as the flagship milk brand, but with a twist. While competitors fought commodity battles in loose milk, Arokya focused on packaged, standardized products. The pitch was simple: consistent quality, guaranteed purity, no adulteration. In a market scarred by milk scandals, this resonated. By 2015, Arokya had become Tamil Nadu's largest packaged milk brand, commanding premium prices despite intense competition.

The real innovation came with "Ibaco"—Hatsun's answer to the global frozen dessert chains entering India. Launched in 2012, Ibaco wasn't positioned as an Indian brand trying to be international, but as an international-quality brand that understood Indian tastes. The stores looked like they belonged in Milan, but sold flavors like tender coconut, fig, and anjeer that resonated with Indian palates. The pricing—₹200-400 per serving—was 10x regular ice cream, targeting the same consumers who frequented Starbucks and Pizza Hut.

Ibaco's expansion strategy defied conventional retail wisdom. Instead of company-owned stores requiring massive capital, Hatsun pioneered a unique franchise model. Franchisees invested ₹25-30 lakhs, Hatsun provided everything else—design, training, products, even marketing. The franchise success rate exceeded 90%, extraordinary in food retail. By 2020, Ibaco operated 100+ stores across India, generating revenues that, while small in absolute terms, carried margins exceeding 20%.

"HAP Daily" became the convenience play—small-format exclusive outlets that combined retail with consumption. Think of it as 7-Eleven meets dairy bar. Consumers could buy milk for home, grab a lassi for immediate consumption, and pick up ice cream for dessert. Located in high-footfall areas—bus stations, college campuses, office complexes—these outlets generated ₹50,000-100,000 monthly revenue from 200-square-foot spaces. By 2020, HAP Daily had grown to 3,900+ outlets, creating a exclusive distribution channel that competitors couldn't access.

The geographic expansion beyond Tamil Nadu required careful calibration. Andhra Pradesh and Karnataka were natural extensions—similar demographics, dietary preferences, and climate. But entering Kerala meant adapting to different taste preferences (less sweet, more fruit-based). Pushing into Maharashtra required price adjustments for a more value-conscious market. Each state wasn't just a new geography but a new puzzle requiring localized solutions.

The acquisition strategy during this period was surgical. Unlike peers who bought brands for vanity metrics, Hatsun acquired capabilities. A small organic dairy farm in Krishnagiri became the seed for premium organic products. A traditional sweet manufacturer in Madurai brought expertise in milk-based desserts. A logistics company specializing in cold-chain became the backbone for e-commerce fulfillment. Each acquisition was small (₹10-50 crore), but strategic, filling specific gaps in the portfolio or supply chain.

Technology integration accelerated, but always with ROI clarity. Hatsun launched one of India's first dairy-focused apps, allowing consumers to subscribe for daily delivery, modify orders, and even track their delivery person in real-time. But unlike tech startups burning cash for downloads, the app was profitable from day one—subscription prepayments improved working capital, route optimization reduced delivery costs, and direct consumer relationships enabled better demand forecasting.

The export business, often overlooked, became a quiet success story. Hatsun began shipping to Middle East, Singapore, and Malaysia—markets with significant Indian diaspora craving authentic products. The "Golden Trophy for largest dairy products exporter" wasn't just recognition but validation of product quality meeting international standards. Export revenues, while just 5% of total, carried 2x domestic margins due to premium positioning abroad.

Quality certifications accumulated: ISO 22000, HACCP, BRC—alphabet soup that meant little to consumers but everything to institutional buyers. Hotels, airlines, and restaurant chains—previously hesitant about local dairy suppliers—became major customers. A single contract with a hotel chain could mean ₹10 crore annual revenue with 45-day payment terms, far superior to retail economics.

The farmer ecosystem evolved from transactional to transformational. Hatsun launched "Project Pashu Vikas"—comprehensive cattle development program covering 100,000 farmers. The initiative included free vaccination camps, subsidized cattle feed, and even cattle insurance. The investment—₹200 crore over the decade—seemed excessive until you realized farmer productivity increased 40%, milk quality improved dramatically, and farmer loyalty became unshakeable.

Sustainability initiatives, initially driven by cost considerations, became competitive advantages. Biogas plants at processing facilities reduced energy costs by 30%. Solar panels on distribution centers cut electricity bills. Even packaging moved to recyclable materials. These weren't greenwashing exercises but hard-nosed business decisions that happened to align with environmental goals. The commitment to 25% carbon footprint reduction wasn't just corporate responsibility but operational efficiency.

The financial trajectory during 2010-2020 validated the portfolio approach. Revenue grew from ₹2,000 crore to ₹6,500 crore. But the composition changed dramatically—ice cream reduced from 60% to 35% of revenue, milk and milk products increased to 50%, and new categories contributed 15%. This diversification reduced seasonality (ice cream peaks in summer), improved capacity utilization (same plants, different products), and enhanced negotiating power with retailers (broader portfolio meant better shelf space).

The decade ended with Hatsun at an interesting crossroads. With ₹8,700 crore revenue run rate, they were knocking on the doors of becoming a ₹10,000 crore company—a psychological milestone in Indian business. The portfolio was complete, geography was expanding, and the brand had unprecedented strength. But new challenges emerged: D2C brands targeting premium segments, aggregators disrupting distribution, and most importantly, the need to expand beyond South India's saturating market.

The answer would come from an unexpected direction—not westward to Mumbai or northward to Delhi, but eastward to markets everyone else had ignored.

VI. The Modern Growth Engine: Acquisitions & Eastern Expansion (2020-Present)

The pandemic year 2020 started with existential questions for every business, but for Hatsun, it triggered an unexpected acceleration. While restaurants shut and ice cream sales plummeted in the initial lockdown, home consumption of milk, curd, and butter exploded. Families cooking three meals at home consumed 40% more dairy. The portfolio diversification of the previous decade—once seen as diluting focus—became the lifeline that kept cash flows strong when indulgence categories collapsed.

But Chandramogan, now 71, wasn't content playing defense. As competitors retrenched, he saw opportunity in chaos. The Eastern India dairy market—Odisha, West Bengal, Bihar, Jharkhand—had been historically underserved by organized players. Local cooperatives were inefficient, private players were subscale, and consumer trust in packaged dairy was low. It was Tamil Nadu of the 1980s all over again—a market waiting for someone patient enough to build it right.

The game-changer came in January 2025 with the ₹233 crore acquisition of Milk Mantra Dairy. This Odisha-based company, with its innovative "Milky Moo" brand, had built exactly what Hatsun needed: local credibility, established farmer networks, and consumer trust. With ₹276 crore revenue in FY24, Milk Mantra wasn't bought for its current scale but for its strategic footprint in Eastern India.

The Milk Mantra acquisition was textbook Hatsun—patient, strategic, and focused on operations over optics. Unlike typical acquisitions where brands get subsumed, Milky Moo would continue independently, leveraging local brand equity. But the backend would transform completely. Hatsun's procurement expertise would improve farmer yields. Their processing technology would enhance product quality. Most crucially, their distribution muscle would expand Milky Moo from Odisha-only to the entire Eastern region.

The strategic logic was compelling: Hatsun's existing North Andhra Pradesh operations could naturally extend into Odisha. West Bengal and adjoining states became accessible through the Odisha base. The Eastern expansion wasn't just geographic diversification—it was accessing India's next dairy frontier, where consumption was growing at 15% annually versus 8% in saturated South markets.

The integration playbook revealed Hatsun's operational maturity. Instead of immediate consolidation, they deployed a "teach and learn" approach. Hatsun executives spent months understanding Odisha's unique market dynamics—different cattle breeds, distinct taste preferences, varied festival consumption patterns. Simultaneously, Milk Mantra teams visited Tamil Nadu to learn Hatsun's procurement, quality, and distribution systems. This two-way knowledge transfer ensured acquisition success without cultural disruption.

Technology transformation accelerated post-pandemic. The HAP Daily app, initially a subscription platform, evolved into a full-stack dairy ecosystem. Consumers could schedule deliveries, farmers could track payments, retailers could manage inventory—all on one platform. The app processed 100,000+ daily transactions by 2024, generating invaluable consumption data that informed everything from production planning to new product development.

The sustainability narrative, once peripheral, became central to corporate strategy. Hatsun committed to carbon neutrality by 2035—ambitious for a company operating in traditional industries. But the pathway was pragmatic: electric vehicles for last-mile delivery (reducing fuel costs), solar power for processing plants (cutting electricity bills), and biodegradable packaging (appealing to premium consumers). Each green initiative had clear ROI metrics, ensuring sustainability aligned with profitability.

The financial performance in recent years reflects both success and challenges. Q3 FY25 revenue grew 6.5% to ₹2,010 crore, respectable but not spectacular. More concerning, profit declined 28.7% to ₹41 crore, pressured by input cost inflation and competitive intensity. The market capitalization of ₹19,875 crore implies investors are betting on future potential rather than current performance.

The competitive landscape has evolved dramatically. Amul, the 800-pound gorilla, is expanding aggressively beyond Gujarat. D2C brands like Country Delight and Sid's Farm are targeting premium urban consumers with farm-to-home propositions. Quick-commerce platforms like Blinkit and Zepto are disrupting traditional distribution. International players are returning with plant-based alternatives. The moats that seemed impregnable a decade ago are being tested.

Hatsun's response reveals strategic clarity. Instead of fighting D2C brands in their premium urban niche, Hatsun is going deeper into Tier 2/3 markets where infrastructure advantages matter more than marketing budgets. Instead of resisting quick-commerce, they're partnering selectively, using platforms for urban distribution while maintaining direct rural networks. Instead of dismissing plant-based alternatives, they're quietly developing their own line, ready to launch when market timing is right.

The leadership transition adds another dimension. C. Sathyan, Chandramogan's son and Executive Director since 2002, represents continuity with evolution. While Chandramogan built through frugality and farmer relationships, Sathyan brings technology focus and capital market sophistication. The generational transition, often fumbled in family businesses, appears smooth—the founder's wisdom guiding strategy while next generation drives execution.

The January 2025 Padma Shri award to Chandramogan wasn't just personal recognition but validation of a life's work. From pushcart to Padma Shri—the arc is cinematic. But Chandramogan, characteristically, used the platform to talk about farmers, consumers, and employees rather than personal achievement. The recognition came not for building a large company but for transforming an industry and uplifting hundreds of thousands of livelihoods.

Looking ahead, Hatsun stands at an inflection point. The ₹9,000 crore revenue target for FY25 seems achievable, but reaching ₹10,000 crore—joining India's elite corporate club—requires something more. The Eastern expansion through Milk Mantra provides geographic growth. The premium portfolio offers margin expansion. The sustainability initiatives ensure future readiness. But the real question is whether Hatsun can maintain its operational excellence while scaling beyond its traditional stronghold.

The answer might lie in Chandramogan's original insight: success in Indian consumer markets isn't about being the biggest or loudest—it's about being the most embedded in consumers' daily lives. Every morning, millions of Indians begin their day with Hatsun products without thinking about the company behind them. That invisibility, that taken-for-granted presence, that integration into daily routine—that's the ultimate moat.

VII. The Operating System: What Makes HATSUN Different

Walk into a Hatsun processing plant at 4 AM and you'll witness something remarkable: a ballet of efficiency where 3 million liters of milk transform into dozens of products without a drop wasted. But the real magic isn't in the stainless steel tanks or automated packaging lines—it's in the operating philosophy that treats inefficiency as the enemy and frugality as religion.

The direct farmer procurement model, Hatsun's crown jewel, operates on principles that seem obvious in hindsight but were revolutionary when implemented. Unlike cooperatives where farmers are members but not partners, or other private dairies where farmers are just suppliers, Hatsun's model creates genuine interdependence. The company doesn't just buy milk; it invests in cow productivity, farmer education, and veterinary care. The math is simple: a healthier cow produces more milk, a trained farmer manages resources better, and both translate to higher procurement quality at lower effective costs.

Consider the numbers: Hatsun's average milk procurement price is 5-7% higher than market rates, yet their input costs are 10% lower than competitors. This paradox resolves when you understand the total system. By paying promptly (within 10 days versus industry-standard 30 days), Hatsun eliminates the farmer's working capital costs. By providing veterinary services (preventing 15% cattle mortality), they ensure consistent supply. By offering cattle feed on credit (eliminating middleman margins), they reduce farmer expenses. The higher price paid is more than offset by supply chain stability and quality premiums.

The innovation framework at Hatsun defies Silicon Valley stereotypes. There's no innovation lab with beanbags and whiteboards. Instead, innovation happens on factory floors and farmer fields. When farmers complained about cattle feed costs, Hatsun didn't just negotiate better prices—they set up their own feed manufacturing, reducing costs by 20%. When retailers struggled with power cuts affecting refrigeration, Hatsun didn't just provide generators—they developed low-power cooling units that could run on inverters. Every innovation solves a real problem for a real stakeholder.

The technology adoption exemplifies this pragmatism. Hatsun uses Bactofuge technology to produce clarified liquid milk—removing bacteria without heat treatment, preserving nutrition while extending shelf life. But they didn't adopt this expensive technology everywhere—only in products where the premium justified the investment. Similarly, their cold chain uses IoT sensors for temperature monitoring, but only on high-value routes where spoilage costs exceed monitoring expenses.

Quality obsession at Hatsun transcends compliance—it's organizational DNA. Every milk tanker undergoes 23 different tests before acceptance. Random retail samples are tested daily at independent labs. Customer complaints trigger root-cause analysis that goes back to specific farmers and cows. This seems excessive until you realize that in Indian dairy, where adulteration scandals regularly destroy brands, trust is the ultimate asset. Hatsun has never had a major quality incident in 50+ years—a record that's worth more than any advertising campaign.

The frugality culture, inherited from Chandramogan's pushcart days, manifests in surprising ways. Senior executives fly economy class. The corporate office in Chennai is functional, not fancy. Marketing budgets are 2% of revenue versus industry-standard 5%. But this isn't penny-pinching—it's capital allocation discipline. Every rupee saved on corporate overhead goes into farmer development or distribution infrastructure. The company's return on capital employed (ROCE) consistently exceeds 20%, extraordinary for a capital-intensive industry.

Sustainability initiatives reveal similar pragmatism. The 25% carbon footprint reduction target isn't driven by ESG pressures but by cost mathematics. Solar panels reduce electricity costs. Biogas from cow dung powers rural processing units. Water recycling cuts utility bills. Even the push toward electric vehicles for distribution is motivated by total cost of ownership (TCO) calculations showing 30% savings over diesel vehicles' lifetime. Green and profitable aren't contradictory at Hatsun—they're complementary.

The human capital philosophy deserves special attention. In an industry notorious for blue-collar exploitation, Hatsun's 10,000+ employees enjoy benefits unusual for Indian manufacturing: health insurance covering families, education support for children, and even retirement planning assistance. But this isn't altruism—it's retention strategy. Training a quality control expert takes 18 months. Developing a procurement relationship manager requires 2 years. The cost of employee turnover far exceeds the cost of superior benefits. Result: attrition rates below 5% in an industry averaging 20%.

The distribution density strategy creates competitive advantages beyond logistics. In Tamil Nadu towns, you're never more than 500 meters from a Hatsun product. This ubiquity creates powerful network effects. Consumers develop brand habits because alternatives require effort to find. Retailers stock full portfolios because consumers expect availability. Competitors can't achieve minimum efficient scale because Hatsun already occupies finite shelf space. It's a virtuous cycle where density drives demand drives density.

Capital efficiency metrics reveal the model's power. Hatsun generates ₹1 of revenue for every ₹0.50 of fixed assets—2x better than peers. Working capital turns 12 times annually versus industry-standard 8 times. The cash conversion cycle is negative in many months—Hatsun gets paid by consumers before paying farmers. These aren't financial engineering tricks but natural outcomes of operational excellence.

The resilience of this model was tested during COVID-19. When supply chains globally collapsed, Hatsun barely hiccuped. Their direct farmer relationships ensured milk supply. Their own distribution network adapted to lockdown restrictions. Their diverse portfolio meant revenue shifted from ice cream to essential dairy without infrastructure changes. While competitors reported 30-40% revenue drops, Hatsun's declined just 15% in the worst quarter, recovering completely within six months.

But perhaps the most underappreciated aspect of Hatsun's operating system is information advantage. With 400,000 farmers, 2 million retailers, and millions of consumers, Hatsun sits on a data goldmine. They know milk production patterns two seasons in advance. They can predict consumption spikes before festivals. They understand price elasticity at SKU-level in specific neighborhoods. This information asymmetry—built over decades of direct relationships—is impossible to replicate quickly.

The operating system isn't perfect. The emphasis on frugality sometimes delays necessary investments. The focus on operational excellence occasionally blinds them to market shifts. The conservative culture can resist innovation that requires significant upfront investment. But these weaknesses are features, not bugs—they prevent the strategic drift that destroys focused companies pursuing too many opportunities.

VIII. Leadership & Culture: The Chandramogan Way

The Padma Shri ceremony in January 2025 was supposed to be R.G. Chandramogan's moment—national recognition for transforming Indian dairy. Instead, he spent the evening discussing farmer payment systems with a Ministry of Agriculture official. This scene captures the essence of leadership at Hatsun: recognition is pleasant, but operations are paramount.

Chandramogan's leadership philosophy evolved from his autobiography, written not in words but in actions over five decades. Unlike charismatic founders who inspire through speeches, Chandramogan leads through example. Employees tell stories of him visiting procurement centers at 5 AM, not for inspection but to understand ground realities. Of him sitting with factory workers during lunch, discussing process improvements over shared meals. Of him remembering the names of farmers he met once, years ago.

The IIM Ahmedabad case study on Hatsun, taught to MBA students nationwide, focuses on strategic brilliance and operational excellence. But it misses the cultural foundation that enables both. At Hatsun, hierarchy exists for coordination, not domination. A procurement manager can directly message the CEO about farmer concerns. A quality control technician's product rejection overrules production targets. A delivery driver's route feedback shapes distribution strategy. This isn't organizational democracy—it's competence-based authority where expertise trumps designation.

The frugality principle, often misunderstood as cheapness, is actually about resource respect. Chandramogan still drives a 10-year-old Toyota, not because he can't afford better but because it works perfectly. The corporate office uses tube lights, not because LEDs are expensive but because replacing functional fixtures is wasteful. Executive compensation is benchmarked to industry standards, not Silicon Valley fantasies. This isn't poverty mindset—it's sustainability before the term became fashionable.

The succession planning, with son C. Sathyan as Executive Director since 2002, reveals long-term thinking. Unlike dramatic founder-exits or succession battles that destroy family businesses, Hatsun's transition has been gradual and transparent. Sathyan spent years in operations before strategy, in factories before boardrooms. He earned respect through competence, not inheritance. The 23-year grooming period seems excessive until you realize that in a relationship-based business, trust transfer takes time.

The corporate citizenship initiatives—badminton center, Tennikoit academy, Chess academy—seem random until you understand the logic. These aren't CSR checkboxes but community integration strategies. The sports facilities are in rural areas where Hatsun operates, providing youth alternatives to urban migration. The chess academy partners with government schools, creating goodwill among teachers and parents who influence purchase decisions. Even philanthropy at Hatsun has ROI considerations.

The resilience mindset, forged through multiple near-bankruptcies in early years, permeates organizational culture. Hatsun maintains inventory buffers that seem excessive—until milk procurement disruptions hit competitors. They keep cash reserves that analysts call inefficient—until credit markets freeze. They maintain relationships with small suppliers despite scale disadvantages—until large suppliers exploit dependencies. This isn't paranoia but pragmatism learned through survival.

The learning culture manifests in unexpected ways. Hatsun sends factory supervisors to Japan to study Toyota production systems. Procurement managers visit Netherlands to understand dairy cooperatives. Quality teams train at international certification bodies. But the learning isn't one-way. Israeli agricultural experts study Hatsun's water-efficient farming techniques. Danish dairy companies analyze their cold-chain innovations. The student has become teacher in specific domains.

The decision-making framework at Hatsun follows what Chandramogan calls "the three-generation test": Will this decision benefit the company three generations hence? This long-term orientation explains seemingly irrational choices. Why maintain unprofitable rural routes? Because today's loss-making village is tomorrow's growth market. Why invest in farmer education? Because educated farmers produce better milk. Why resist private equity dilution? Because quarterly pressures destroy long-term value.

The innovation encouragement system is uniquely Indian. There's no "20% time" or "innovation Friday." Instead, every employee is expected to improve their specific function continuously. A driver who reduces fuel consumption by 5% gets recognized. A factory worker who prevents wastage gets rewarded. A farmer who improves milk yield gets celebrated. Innovation isn't separate from work—it IS work. This democratization of improvement creates thousands of micro-innovations that compound into macro-advantages.

The stakeholder balance philosophy treats all constituents as essential. Farmers aren't just suppliers but partners. Employees aren't resources but assets. Retailers aren't customers but collaborators. Even competitors aren't enemies but market-builders. This sounds idealistic until you see the practical benefits. Farmer loyalty ensures supply stability. Employee dedication drives productivity. Retailer partnership enables distribution density. Competitor respect prevents destructive price wars.

The communication style reflects operational clarity. Annual reports read like engineering documents—precise, factual, improvement-focused. Marketing messages emphasize function over emotion—"pure milk" not "happiness in a glass." Internal communications are refreshingly jargon-free—"increase farmer payment speed" not "optimize supplier relationship management." This linguistic discipline reflects thinking discipline.

The risk management approach balances conservatism with calculated aggression. Hatsun won't leverage beyond 1:1 debt-equity ratio but will invest ₹200 crore in farmer development without guaranteed returns. They won't enter categories without operational expertise but will expand geographically into unknown markets. They won't compromise quality for margins but will accept lower profitability for market share. These aren't contradictions but nuanced judgments about risk types.

The cultural transmission mechanisms ensure continuity beyond individuals. New employees undergo six-month field training regardless of role—even MBAs start at procurement centers. Promotion requires cross-functional experience—sales managers must understand production, finance executives must grasp logistics. Leadership development happens through apprenticeship, not workshops—high-performers shadow senior executives for years. This isn't just training but cultural programming.

The "Chandramogan Way" isn't codified in mission statements or values posters. It's embedded in daily decisions, operational choices, and resource allocations. It's the procurement manager who drives 100 extra kilometers to help a farmer with sick cattle. It's the factory supervisor who stays late to perfect a product batch. It's the delivery driver who ensures every retailer feels valued. Culture at Hatsun isn't what they say—it's what they do, repeatedly, consistently, obsessively.

IX. Playbook: Business & Investing Lessons

The transformation from ₹13,000 to ₹19,875 crores—a 15,000,000% return over 54 years—offers masterclass insights, but not the ones you'd expect. This isn't a story about brilliant strategy or perfect timing. It's about compound effects of small, correct decisions made consistently over decades.

Lesson 1: Starting Small is a Feature, Not a Bug

Chandramogan's ₹13,000 beginning seems like disadvantage until you realize it forced discipline that became competitive advantage. Without capital for advertising, he built through word-of-mouth, creating genuine brand loyalty. Without money for automation, he understood manual processes intimately, enabling better automation later. Without funds for multiple ventures, he focused monomaniacally on dairy, achieving depth impossible with breadth. Constraints breed creativity—abundance breeds complacency.

The investor parallel: Companies starting with minimal capital often develop superior unit economics. They can't afford inefficiency. Watch for businesses where frugality is philosophy, not necessity. These companies scale profitably because their foundational habits were formed under scarcity.

Lesson 2: Direct-to-Source Procurement as Ultimate Moat

Hatsun's farmer network isn't just supply chain—it's competitive immunity. Competitors can copy products, match prices, even poach employees. But they can't replicate 400,000 farmer relationships built over decades. Each relationship is individually small but collectively insurmountable. It's like trying to compete with Amazon by recruiting their millions of sellers one-by-one—theoretically possible, practically impossible.

The broader principle: Look for businesses with atomized supplier/customer bases where relationships matter more than transactions. These networks exhibit powerful winner-take-all dynamics because switching costs compound with scale. The moat isn't the network size but the relationship depth.

Lesson 3: Multi-Brand Portfolio Strategy for Market Segmentation

Hatsun's brand architecture—Arun for mass, Arokya for premium, Ibaco for aspiration, HAP for convenience—seems complex until you understand the elegance. Same cows produce milk for all brands. Same trucks deliver all products. Same factories process everything. But consumers see distinct propositions tailored to their specific needs. It's operational leverage with marketing precision.

For investors: Multi-brand strategies work when backend synergies exceed frontend complexity. If brands share infrastructure, suppliers, or technology while addressing distinct segments, the portfolio creates value. If brands require separate everything, the portfolio destroys value through complexity costs.

Lesson 4: Geographic Expansion Through Cultural Acquisition

The Milk Mantra acquisition reveals sophisticated thinking. Hatsun didn't buy revenue or assets—they bought cultural understanding and local relationships. Entering Odisha organically would require decades to build trust. Acquiring a trusted local player provides instant credibility. The ₹233 crore price seems high for ₹276 crore revenue until you factor in relationship value and time saved.

The pattern to recognize: When strong regional players expand nationally, watch for cultural fit over financial metrics in acquisitions. Companies buying revenue are rolling up. Companies buying relationships are building platforms. The latter creates lasting value.

Lesson 5: Surviving Near-Death Makes Companies Antifragile

Hatsun's multiple brushes with bankruptcy weren't setbacks but strengthening exercises. Each crisis taught lessons: the 1970s taught cash management, the 1980s taught supplier relationships, the 2008 crisis taught portfolio diversification. Companies that survive existential threats develop resilience that becomes competitive advantage during future crises.

Investment insight: Companies with crisis experience often outperform during downturns. They maintain higher cash reserves, diversified revenue streams, and conservative leverage. What seems like inefficiency during booms becomes survival advantage during busts. Look for management teams with scar tissue—they make better risk decisions.

Lesson 6: Building in "Unsexy" Industries with Massive TAM

Dairy isn't software. There's no exponential scaling, network effects are limited, and margins are single-digit. Yet Hatsun built enormous value because the TAM is everyone, consumption is daily, and competition is fragmented. While venture capital chased the next unicorn, Chandramogan built a real business serving fundamental needs.

The opportunity: Industries ignored by growth capital often offer superior risk-adjusted returns. Look for sectors with large TAMs, fragmented competition, and operational complexity that rewards excellence. These aren't sexy investments but they're often profitable ones.

Lesson 7: Distribution Density Creates Competitive Immunity

Hatsun's 2 million outlet coverage isn't just reach—it's fortress. In game theory terms, they've achieved "market saturation equilibrium" where competitors can't achieve minimum efficient scale. Every outlet stocking Hatsun products is one less spot for competitors. Every delivery route optimized for Hatsun volumes becomes uneconomical for subscale players.

For investors: Evaluate distribution not just by coverage but by density economics. Companies dominating specific geographies often generate superior returns to those spread thin nationally. Regional density beats national presence in consumer goods requiring physical distribution.

Lesson 8: The Power of Negative Working Capital

Hatsun's cash conversion cycle—getting paid by consumers before paying suppliers—seems impossible in capital-intensive manufacturing. But by collecting daily from retailers (cash business) while paying farmers weekly, they've engineered negative working capital. This isn't financial engineering but operational excellence manifesting as balance sheet efficiency.

Key insight: Companies achieving negative working capital in traditionally capital-intensive industries have operational advantages that financial statements don't fully capture. They're essentially getting interest-free loans from operations. This capital efficiency enables self-funded growth.

Lesson 9: Vertical Integration vs. Virtual Integration

Hatsun vertically integrated backward (farmers) and forward (retail) but not horizontally (many categories). They control what matters (quality, distribution) but don't manufacture everything (packaging, equipment). This selective integration optimizes capital efficiency while maintaining control over critical success factors.

The framework: Vertical integration makes sense when transaction costs exceed coordination costs. If managing suppliers is harder than doing it yourself, integrate. If suppliers are more efficient, outsource. Hatsun's selective integration reveals deep understanding of where value creation happens in their chain.

Lesson 10: Long-Term Thinking in Short-Term Markets

With promoter holding at 73.2%, Chandramogan never faced quarterly earnings pressure. This enabled decisions that hurt near-term profits but built long-term value: farmer investments, rural distribution, quality infrastructure. The compound effect over decades dwarfs any quarterly optimization.

For investors: High promoter ownership in profitable businesses often signals long-term orientation. These companies might underperform during momentum markets but outperform over complete cycles. Patient capital deployed in impatient markets generates alpha through time arbitrage.

X. Analysis & Bear vs. Bull Case

The investment case for Hatsun presents a fascinating paradox: stellar long-term execution coupled with recent operational challenges. Understanding both perspectives requires nuancing beyond simple metrics.

Bull Case: The Compounding Machine

1. Aligned Ownership Structure The 73.2% promoter holding isn't just high—it's optimal. Enough to ensure control without minority squeeze-out risk. The Chandramogan family has never diluted except for operations, never pledged shares for personal loans, and never extracted value through related-party transactions. This alignment means management thinks in decades, not quarters.

2. Structural Competitive Advantages The 400,000 farmer network and 2 million retail outlets aren't just numbers—they're impossibly high barriers to entry. A new competitor would need ₹5,000+ crores and 10+ years just to replicate infrastructure, without any guarantee of relationship replication. Meanwhile, Hatsun deepens these moats daily through continuous engagement.

3. Eastern Expansion Optionality The Milk Mantra acquisition opens Eastern India—a ₹50,000 crore dairy market growing at 15% annually. If Hatsun replicates even half their Tamil Nadu market share in the East, it adds ₹3,000 crores revenue. The acquisition price of ₹233 crores looks like venture capital returns if execution succeeds.

4. Portfolio Resilience Unlike mono-product companies vulnerable to category shifts, Hatsun's portfolio provides natural hedging. Economic downturns shift consumption from ice cream to milk—both Hatsun products. Health trends move consumers from regular to organic—Hatsun offers both. Urban premiumization and rural value-seeking happen simultaneously—Hatsun serves both.

5. Underappreciated Technology Integration While not a "tech company," Hatsun's operational technology is sophisticated. IoT-enabled cold chains, AI-driven route optimization, app-based farmer payments—these aren't buzzwords but margin drivers. As technology costs decrease, Hatsun's early investments compound into cost advantages.

Bear Case: Growth Deceleration Concerns

1. Disappointing Financial Momentum The five-year sales CAGR of 10.3% barely beats inflation. Q3 FY25's 28.6% profit decline suggests operational challenges beyond temporary disruptions. For a company in a growing industry with execution capabilities, these numbers disappoint.

2. Competitive Intensity Increasing Amul's national expansion, D2C brands' premium capture, and quick-commerce disruption create unprecedented competitive pressure. Hatsun's regional fortress strategy works until national players achieve scale economics that overwhelm regional advantages. The moats might be deep but the attackers are multiplying.

3. Input Cost Vulnerability Dairy is ultimately commodity processing—milk prices fluctuate, but consumer prices are sticky. Cost of materials consumed at ₹1,404 crore in Q3 represents 70% of revenue. Even small milk price inflation without corresponding price increases destroys margins. Climate change makes this volatility structural, not cyclical.

4. Geographic Concentration Risk Despite expansion talk, Tamil Nadu still contributes 60%+ revenue. This concentration creates vulnerability to state-level disruptions—political changes, weather events, or competitive intensity. The Eastern expansion might dilute this risk, but execution remains unproven.

5. Generational Transition Uncertainty While Sathyan's succession appears smooth, second-generation transitions in family businesses carry inherent risks. Will he maintain Chandramogan's frugality? Can he inspire similar loyalty? Does he have the same operational obsession? These intangibles matter enormously in relationship-based businesses.

Valuation Perspective

At ₹19,875 crores market cap on ₹8,700 crores revenue, Hatsun trades at 2.3x sales—reasonable for consumer goods but expensive for dairy. The P/E ratio exceeding 60x suggests markets are pricing in significant growth acceleration that recent results don't support.

However, valuation requires context. Hatsun's return on equity consistently exceeds 18%, extraordinary for capital-intensive manufacturing. The debt-to-equity ratio below 1x provides balance sheet flexibility. The negative working capital generates cash for growth. Traditional metrics might not capture the value of relationship moats and operational excellence.

Risk-Reward Assessment

The bear case centers on execution risk—can Hatsun maintain operational excellence while scaling beyond comfort zones? The bull case assumes relationship moats and regional dominance translate into national success. Reality likely lies between extremes.

For long-term investors, Hatsun offers exposure to India's dairy consumption growth with proven execution capabilities. The recent underperformance might be tactical entry opportunity if one believes in structural advantages. For momentum investors, better opportunities exist elsewhere until growth reaccelerates.

The key monitorables: Eastern expansion traction, margin recovery trajectory, and competitive response effectiveness. If Milk Mantra integration succeeds and margins recover to historical levels, today's valuation will seem cheap retrospectively. If execution falters and competition intensifies, multiple compression could be severe.

XI. Epilogue & Future Vision

Standing at the threshold of 2025, Hatsun embodies a fascinating duality—a company simultaneously looking backward to its roots and forward to its possibilities. Chandramogan, now wearing the Padma Shri but still visiting procurement centers at dawn, articulates a vision that's both ambitious and grounded: "Establishing robust presence in Eastern India" while deepening the southern stronghold.

The billion-dollar revenue milestone—₹10,000 crores—looms tantalizingly close. But unlike the Silicon Valley obsession with arbitrary valuations, this milestone matters operationally. It provides scale for national advertising, negotiating power with retailers, and capital access for transformation investments. Yet Chandramogan warns against milestone obsession: "We didn't build this company to reach numbers but to serve customers. Numbers are outcomes, not objectives."

The strategic choices ahead reveal sophisticated thinking about market evolution. Rather than pursuing national expansion through capital-intensive greenfield operations, Hatsun is building an acquisition platform. Small regional dairies with strong local presence but weak balance sheets become attractive targets. The Milk Mantra playbook—maintain local brand, upgrade operations, expand distribution—can be replicated across geographies.

The technology transformation agenda goes beyond digitization. Hatsun is experimenting with precision fermentation for lactose-free products, cellular agriculture for sustainable proteins, and even blockchain for supply chain transparency. But true to form, each experiment has clear success metrics and limited capital exposure. This isn't innovation theater but calculated preparation for industry disruption.

The sustainability roadmap reflects similar pragmatism. Electric vehicle adoption for distribution isn't just environmental compliance but economic inevitability as battery costs plummet. Solar power for processing plants isn't just carbon reduction but energy independence as grid reliability deteriorates. Water recycling isn't just resource conservation but cost management as water becomes scarcer. Every green initiative has green (dollar) justification.

The international expansion opportunity remains intriguing but cautious. The Middle East and Southeast Asian markets, with large Indian diaspora and growing dairy consumption, offer natural extension. But Hatsun learned from others' mistakes—international expansion requires local partners, cultural adaptation, and patient capital. They're exploring joint ventures rather than wholly-owned subsidiaries, licensing rather than direct operations.

The competitive response strategy reveals maturity. Against Amul's cooperative might, Hatsun emphasizes farmer relationships and local responsiveness. Against D2C premiumization, they leverage distribution density and portfolio breadth. Against quick-commerce disruption, they partner selectively while maintaining direct networks. This isn't one strategy but multiple responses to multiple threats.

The organizational evolution challenges become paramount. Scaling from 10,000 to potentially 25,000 employees requires different management systems. Expanding from one state to five states demands federal structure. Growing from ₹8,000 to ₹15,000 crores necessitates professional management layers. The family-run warmth that defined Hatsun must evolve without losing its essence.

What would the founders do if starting today? Chandramogan's answer is surprising: "Exactly the same, but faster." The fundamentals remain unchanged—solve real problems for real people, build trust through consistency, reinvest profits for growth. But modern tools—digital payments, data analytics, social media—would accelerate what took them decades. The pushcart would still exist, but it would have GPS tracking and QR-code payments.

The succession planning continues evolving. While Sathyan leads operations, the third generation is already in training. Chandramogan's grandchildren, educated at global universities but grounded in Tamil Nadu operations, represent continuity with modernization. The family understands that perpetuity requires meritocracy—future leaders will be family only if they're also the best candidates.

The capital allocation framework for the next decade prioritizes: farmer development (₹500 crores), Eastern expansion (₹1,000 crores), technology infrastructure (₹300 crores), and sustainability initiatives (₹200 crores). Note what's missing: no vanity acquisitions, no unrelated diversification, no financial engineering. Capital deployment remains boringly operational.

The stakeholder balance for the future acknowledges new constituents. Environmental activists become partners in sustainability. Technology companies become collaborators in digital transformation. Government becomes enabler through policy alignment. Even competitors become co-creators of category growth. The ecosystem expands while core relationships deepen.

Looking ahead, Hatsun's future isn't just about Hatsun—it's about Indian dairy's evolution. As the country's largest private player, their choices shape industry direction. Their quality standards become benchmarks. Their farmer practices become templates. Their technology adoption becomes catalyst. With great scale comes great responsibility, and Hatsun seems to understand both.

The ultimate question isn't whether Hatsun reaches ₹10,000 or ₹20,000 crores revenue. It's whether they maintain the soul that transformed a pushcart into an institution. Can they stay hungry despite success? Can they remain frugal despite resources? Can they keep learning despite expertise? Can they stay grounded despite recognition?

The answer lies not in strategy documents or analyst reports but in daily actions. In the procurement manager still visiting farmers during festivals. In the quality controller still rejecting substandard batches despite production pressure. In the CEO still driving his old Toyota. In the founder, Padma Shri in hand, still waking at 4 AM to check milk collection data.

The ice cream cart that started it all sits in Hatsun's Chennai office—not as museum piece but as reminder. Every empire begins with someone willing to push a cart through hot streets, calling out to skeptical customers, believing tomorrow will be better than today. For Hatsun, after 54 years, tomorrow still beckons with possibility. The cart has become a company, but the journey continues.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube