Great Eastern Shipping: India's Maritime Pioneer

I. Introduction & Episode Roadmap

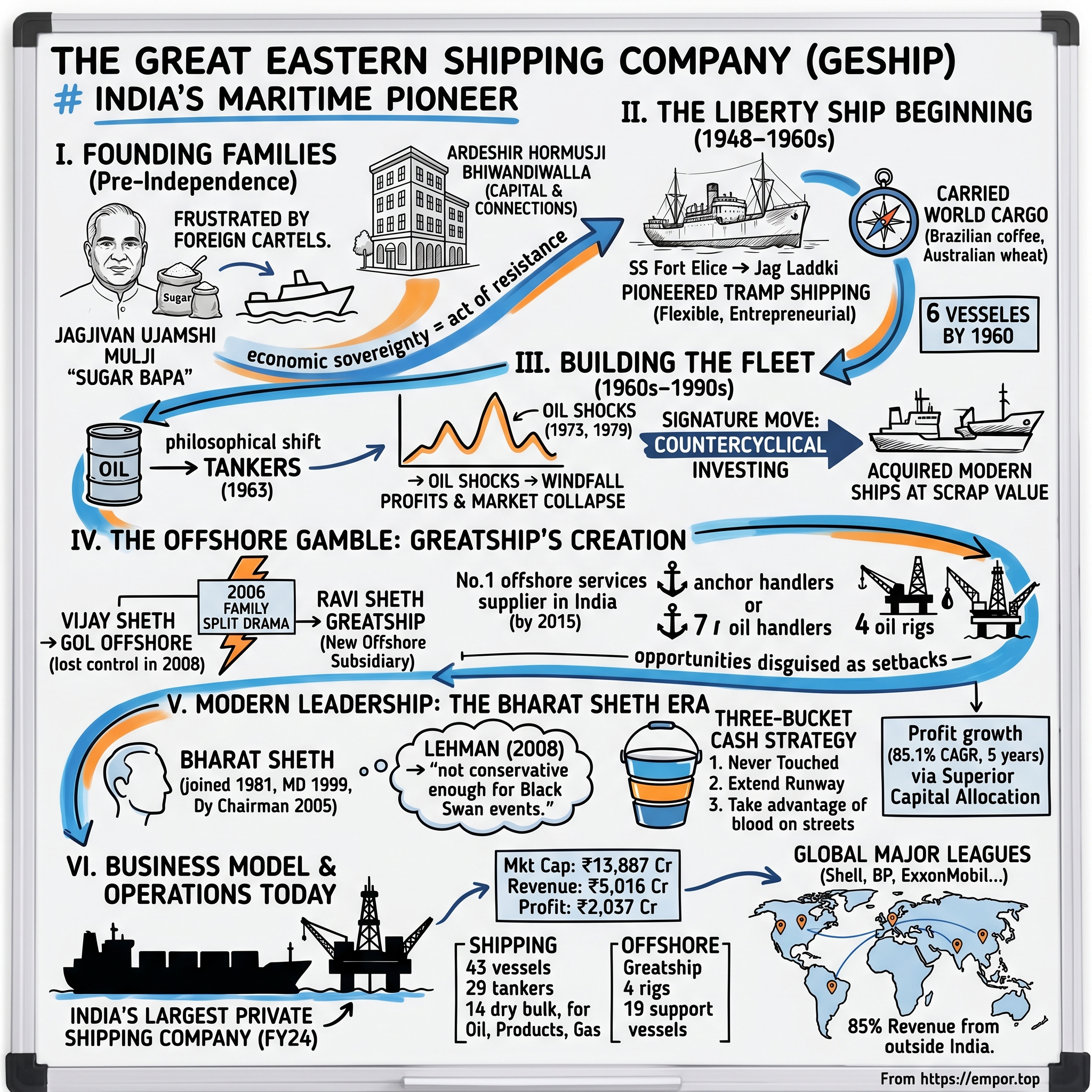

Picture this: It's 1948, and the monsoon winds are whipping across Bombay's docks. A mothballed Liberty ship—one of thousands built by America to win World War II—sits rusting in the harbor. Two trading families, flush with profits from sugar but frustrated by foreign shipping cartels, are about to make a bet that will transform Indian maritime history. They'll buy that ship, rename it, and launch what becomes India's largest private shipping empire.

Today, Great Eastern Shipping commands a fleet of 39 vessels and 23 offshore assets, generating over ₹5,000 crores in revenue. But this isn't just a shipping story—it's a masterclass in capital allocation, family business succession, and surviving brutal industry cycles that regularly bankrupt competitors.

The question that drives this episode: How did post-independence sugar traders build a shipping giant that would outlast government-backed competitors, survive multiple oil crises, and emerge as India's maritime champion? And perhaps more intriguingly—why does a company this successful trade at just book value?

We'll journey from those first Liberty ships to today's sophisticated offshore drilling operations, uncovering the playbook that allowed Great Eastern to thrive where others capsized. Along the way, we'll meet three generations of the Sheth family, witness a dramatic family split that created a rival empire, and decode the conservative philosophy that turned cyclical shipping into consistent wealth creation.

II. The Founding Families & Pre-Independence Context

The story begins not at sea, but in the sugar mills of Gujarat. Jagjivan Ujamshi Mulji—a name that would eventually prefix every Great Eastern ship as "Jag"—wasn't thinking about shipping when he built his trading empire in the 1920s. He was thinking about sugar, and how to move it from India's heartland to markets across the subcontinent and beyond.

Known as "Sugar Bapa" (Sugar Father), Jagjivan possessed what contemporaries described as an almost mystical understanding of commodity flows. But here's what frustrated him: every ton of sugar he wanted to export required negotiating with foreign shipping lines—British, Greek, Norwegian—who controlled India's maritime trade like a cartel. They charged what they wanted, sailed when they pleased, and treated Indian traders as second-class customers.

"Businessman by instinct, nationalist by thinking, humanist by tradition"—that's how company historians describe Jagjivan. The nationalist part mattered. This was pre-independence India, where economic sovereignty was inseparable from political freedom. Building an Indian shipping line wasn't just business; it was an act of resistance.

Enter Ardeshir Hormusji Bhiwandiwalla, the financial architect whose initials—AHB—still adorn Great Eastern's house flag and funnel. Where the Sheths brought trading acumen and operational expertise, Bhiwandiwalla brought something equally vital: capital and connections to Bombay's Parsi business elite. The Parsis had been India's pioneer industrialists, and Bhiwandiwalla understood that shipping required patient capital—the kind that could weather years of losses before turning profitable.

The two families formed an unusual partnership. Unlike the managing agency system that dominated Indian business (where British firms controlled Indian operations), this was genuinely indigenous capital funding an indigenous vision. They weren't just chartering ships anymore; they were going to own them.

By 1947, as India gained independence, the families had spent years studying shipping—not just the operations, but the economics. They understood that shipping was viciously cyclical, that fortunes were made and lost on timing, and that survival required something most Indian businesses lacked: a truly global perspective. When opportunity knocked in 1948, they were ready.

III. The Liberty Ship Beginning (1948–1960s)

The SS Fort Elice wasn't much to look at. Built in Portland, Oregon in 1943, she was one of 2,710 Liberty ships America mass-produced to win the Battle of the Atlantic. By 1948, hundreds sat mothballed, victims of peace. For the Sheth and Bhiwandiwalla families, she represented something else entirely: sovereignty on the seas.

Vasant J. Sheth, who would captain that maiden voyage, later called it "the most nervous moment of my life." Here was a 27-year-old from a trading family, about to sail a 10,000-ton vessel with an Indian crew into international waters where no Indian private flag had ventured before. The Lloyd's of London insurance inspector who came aboard in Bombay was skeptical: "You Indians want to run ships now? "The renaming ceremony was telling. The company's first vessel, SS Fort Elice, began its maiden voyage in 1948 under the entrepreneurial genius of Vasant J. Sheth. They christened her "Jag Laddki"—the first "Jag" prefix that would mark every Great Eastern vessel, honoring Jagjivan. But Vasant wasn't just sailing a ship; he was launching a philosophy.

Under Vasant's vision and business acumen, Great Eastern pioneered tramp shipping in India, waging a campaign for freedom of operation for Indian shipping for almost four decades. "Tramp shipping"—the term needs explaining. Unlike liner shipping with fixed routes and schedules, tramp ships went wherever cargo needed moving. It was the maritime equivalent of being a taxi rather than a bus—more flexible, more entrepreneurial, and much riskier.

The Indian government hated it. Post-independence policy favored state-controlled shipping on fixed routes serving "national priorities." Private tramp operators threatened this controlled ecosystem. Vasant spent the 1950s in Delhi's corridors of power, arguing that India needed maritime entrepreneurs, not just maritime bureaucrats. His argument was simple: "How can India trade freely if it cannot ship freely?"

The company often swam against the tide, turning the tides in its favour and laying a path for others to follow. While government-backed Shipping Corporation of India got preferential treatment for Indian coastal cargo, Great Eastern looked abroad. They carried Brazilian coffee to Europe, Australian wheat to Japan, American grain to India. Each voyage was a calculated bet on freight rates, bunker costs, and port congestion.

The numbers tell the story. By 1960, from that single Liberty ship, Great Eastern had expanded to six vessels. Small by global standards, but remarkable for a private Indian company operating without government support. More importantly, they'd proven something critical: Indian crews could compete globally, Indian capital could take maritime risks, and Indian shipping didn't need government protection to succeed.

IV. Building the Fleet: From Tramp to Tankers (1960s–1990s)

The 1960s brought a decision that would define Great Eastern's next half-century: oil. As India's refineries expanded and energy consumption soared, Vasant Sheth saw opportunity where others saw complexity. Tankers were different beasts—specialized vessels requiring different skills, different financing, different risk models. But oil was where the growth was.

The first tanker acquisition in 1963 was modest—a 16,000 DWT product carrier. But it represented a philosophical shift. Great Eastern wasn't just moving commodities anymore; they were becoming energy infrastructure. By 1970, tankers comprised half their fleet. By 1980, they were operating VLCCs (Very Large Crude Carriers) carrying Middle Eastern oil to Indian refineries.

This transformation coincided with global oil shocks. The 1973 Arab oil embargo quadrupled oil prices overnight. Tanker rates went parabolic—a VLCC that earned $10,000 per day in 1972 could command $100,000 in 1973. Great Eastern, having invested in tankers before the crisis, reaped windfall profits. But they also learned a crucial lesson: in shipping, the best money is made before everyone realizes there's money to be made.

The 1980s tested this philosophy severely. After the second oil shock in 1979, the tanker market collapsed. Daily rates fell 90%. Ships worth $40 million became worth $4 million. Global shipping giants like Sanko and Adriatic Tankers went bankrupt. Great Eastern survived through what would become their signature move: countercyclical investing.

While competitors desperately sold ships to raise cash, Great Eastern bought. They acquired modern tankers at scrap values, betting on eventual recovery. The discipline required was extraordinary—imagine buying assets that lose money every day they operate, knowing you might wait years for profitability. But when the tanker market recovered in the late 1980s, Great Eastern owned one of India's most modern fleets, acquired at fraction of replacement cost. By the 1990s, Great Eastern's fleet had evolved into what it remains today: transportation of crude oil, petroleum products, liquified gas and dry bulk commodities. The decision to remain private sector when peers went public sector proved prescient. Government-owned Shipping Corporation of India, despite massive subsidies and protected routes, struggled with bureaucratic decision-making. Great Eastern, answerable to markets rather than ministries, could move fast when opportunities appeared.

V. The Offshore Gamble: Greatship's Creation

The year 2006 marked Great Eastern's most dramatic transformation—and its most bitter family dispute. For decades, the company had watched as offshore drilling became the new frontier in oil exploration. Platforms and rigs commanded day rates that made ship earnings look pedestrian. A drilling rig earning $500,000 per day wasn't unusual during oil booms. The Sheth family saw opportunity, but they disagreed violently on execution. The split drama unfolded in 2006. Vijay Sheth, who was basically running Great Offshore, insisted that the company be hived off from its parent, India's largest private sector shipowner, Great Eastern Shipping. Cousins Bharat and Ravi Sheth reluctantly acquiesced to the separation, and Vijay walked off with what was re-named GOL Offshore, while Ravi, Bharat's younger brother, was tasked with setting up a new offshore subsidiary.

Ravi Sheth was appointed Managing Director of Greatship in November 2006. "There was virtually no time lag between the completion of the court process for divestment, and the launch of Greatship's operations," recalls the unassuming executive who suddenly found himself building an offshore empire from scratch.

What followed was remarkable. Ravi was actually instrumental in turning Colombo Dockyard (CDL) from a predominantly shiprepair facility into a serious shipbuilder. They eventually built 11 vessels for Greatship. The timing seemed terrible—oil prices were volatile, offshore day rates swinging wildly. But Ravi applied the Great Eastern playbook: build when others are scared, operate conservatively, and wait for the cycle to turn.

By 2015, the results were stunning. In nine short years since its launch of operations in March 2006, Greatship had become the undisputed No.1 offshore services supplier in India. The company boasted a 22-strong fleet – seven 80-tonne anchor handlers, four D-class PSVs, two M-class multipurpose vessels, two 150-tonne AHTSVs, and six R-class ROVSVs, plus four 350 ft four-legged cantilevered oil rigs.

The irony wasn't lost on industry observers. Vijay, who'd demanded the split to run his own offshore empire, eventually lost control of Great Offshore after pledging shares to meet margin calls during the 2008 crisis. Meanwhile, Ravi, forced to start from zero, built something arguably more valuable. Sometimes the best opportunities come disguised as setbacks.

VI. Modern Leadership: The Bharat Sheth Era

If there's a moment that defines Bharat Sheth's leadership philosophy, it came during a 2009 investor call, months after Lehman Brothers collapsed. An analyst asked why Great Eastern wasn't buying more ships when prices had crashed 80%. Bharat's response became company legend: "We were always conservative as a company. Lehman taught us we were not conservative enough for Black Swan events. "Think about this: after joining the family company in 1981 straight from St Andrews University, Bharat Sheth spent 18 years learning every facet of the business—chartering, sale & purchase, the most intricate parts of shipping—before becoming Managing Director in 1999. Then, in August 2005, he was appointed Deputy Chairman & Managing Director. By 2008, he'd seen every shipping cycle, survived every crisis. But Lehman was different.

"Having low leverage, high cash balances and a strict discipline on making acquisitions in low markets is the best mantra for long term survival," became his mantra. Today, Great Eastern maintains what Bharat calls a three-bucket cash strategy: cash that will never be touched (for Black Swan survival), cash to extend the runway (for downturns), and cash "to take advantage of blood on the streets" (for opportunities).

The philosophy extends beyond finance. "With a balance sheet in control, I can take an operational risk," Bharat explains. This means Great Eastern can enter volatile spot markets when others stick to long-term contracts, can buy older vessels when others chase new builds, can enter new geographies when others retreat.

The results speak volumes. While the company's sales growth has been modest—7.62% CAGR over five years—profit growth has exploded at 85.1% CAGR. This isn't revenue growth; it's margin expansion through superior capital allocation. "Be it buying bulk carriers, tankers or even buying back its own shares," as Bharat puts it, every capital decision is scrutinized.

The globalization under Bharat has been dramatic. From being fully India-centric in the 1990s, Great Eastern now generates just 30-35% of revenues from Indian operations. The company sails with "the big boys"—85% of revenue comes from outside India, serving clients like Shell, BP, ExxonMobil, Chevron Texaco, TotalFina.

VII. Business Model & Operations Today

Walk into Great Eastern's Mumbai headquarters today, and you're looking at the nerve center of an operation that would have seemed like science fiction to those Liberty ship pioneers. Real-time satellite tracking shows 39 vessels scattered across the world's oceans—a VLCC loading crude in Saudi Arabia, a product tanker discharging gasoline in Singapore, a dry bulk carrier hauling iron ore from Brazil to China. As of FY24, GES is India's largest private sector shipping company, owning and operating 39 ships and 23 offshore assets. The business is elegantly simple yet operationally complex, divided into two main segments: shipping and offshore.

The shipping business transports four categories of cargo: crude oil, petroleum products, liquefied gas, and dry bulk commodities. As of April 12, 2024, it operates a fleet of 43 vessels comprising 29 tankers, including 6 crude carriers, 19 product carriers, and 4 LPG carriers; and 14 dry bulk carriers with an aggregating 3.41 million dwt. Each category requires different expertise, different vessels, different market dynamics.

The offshore business, run through wholly-owned subsidiary Greatship (India) Limited, provides oilfield services—drilling rigs, offshore support vessels, the infrastructure that allows oil companies to explore and produce in deepwater fields. This includes four jack-up rigs and 19 offshore support vessels, representing one of India's largest and most modern offshore fleets.

What makes Great Eastern's operations distinctive isn't just scale—it's flexibility. The company operates through both voyage charters (spot market) and time charters (fixed contracts). In volatile markets, this optionality is gold. When spot rates spike, Great Eastern can capitalize. When they crash, time charter contracts provide stability.

The client list reads like a who's who of global energy: Shell, BP, ExxonMobil, Chevron Texaco, TotalFina. These aren't relationships built overnight. Major oil companies have stringent vetting processes—safety records, crew competence, vessel maintenance. Great Eastern's ISO 9001:2015, ISO 14001:2015, and ISO 45001:2018 certifications aren't just badges; they're tickets to play in the global major leagues.

The financial metrics tell the real story. Market cap of ₹13,887 Cr, Revenue of ₹5,016 Cr, Profit of ₹2,037 Cr. Company has delivered good profit growth of 85.1% CAGR over last 5 years. But here's what's remarkable: this profit growth came despite poor sales growth of 7.62% over past five years. This is margin expansion through operational excellence and capital discipline.

The asset acquisition and disposal strategy deserves special attention. Great Eastern doesn't just buy and hold; they actively trade vessels. In good markets, they sell older tonnage at premium prices. In bad markets, they acquire modern vessels at distressed prices. This isn't speculation—it's arbitraging the difference between market panic and intrinsic value.

VIII. Playbook: Capital Allocation & Risk Management

"They get it well on asset flipping and manage to buy at low prices and sell at high prices"—that's how one competitor describes Great Eastern's playbook. But calling it "flipping" misses the sophistication. This is systematic capital allocation elevated to an art form.

The focus of Great Eastern has been on superior capital allocation. Be it buying bulk carriers, tankers or even buying back its own shares. "Along with the right capital allocation, keeping the balance sheet light also helps us take greater operational leverage and this has worked well for us over the last few years," says Sheth.

The philosophy starts with understanding shipping cycles. Unlike manufacturing where capacity additions are gradual, shipping capacity comes in chunks—a new vessel order takes 2-3 years to deliver. This creates violent cycles. When freight rates are high, everyone orders ships. Three years later, oversupply crashes the market. Great Eastern has mastered playing these cycles.

Take their approach to leverage. "With a balance sheet in control, I can take an operational risk. While I have the cash today, a sudden spike in oil prices could change everything," emphasizes Sheth. This isn't just conservatism—it's optionality. Low leverage means Great Eastern can strike when others are paralyzed.

The three-bucket cash strategy mentioned earlier operates like a fortress with multiple walls. To survive a Black Swan event, there is cash that will never be touched, and that is the first bucket. The second is to extend the runway, and the third is "to take advantage of blood on the streets". To Sheth, the present moment is critical, and being debt-free is also about investing wisely and needing that big opportunity.

Managing through volatile freight markets requires a different skill—reading tea leaves before they're brewed. Great Eastern watches Chinese steel production (drives iron ore demand), OPEC production quotas (affects tanker demand), monsoon patterns (impacts grain trade). They're not trying to predict exact rates; they're positioning for probabilities.

The importance of being debt-averse in cyclical industries cannot be overstated. During the 2016 shipping crisis, when Baltic Dry Index hit all-time lows, leveraged players like Hanjin Shipping (world's seventh-largest container line) went bankrupt. Great Eastern not only survived but expanded, acquiring vessels at 20-30% of replacement cost.

IX. Analysis & Bear vs. Bull Case

Let's address the elephant in the room: Why does a company with such impressive operational metrics trade at just 0.98 times book value with a dividend yield of 3.05%? The bear and bull cases reveal a fascinating tension.

The Bear Case: Start with that poor sales growth of 7.62% over past five years. In a world obsessed with growth, Great Eastern looks stagnant. The shipping industry faces structural headwinds—overcapacity, environmental regulations, geopolitical tensions. The quote from Ravi Sheth during the oil downturn is sobering: "Every offshore services company, without exception, is in trouble at the moment."

ESG considerations and decarbonization pressures add another layer of concern. The International Maritime Organization's regulations requiring 50% emission reductions by 2050 mean massive capital expenditure for new, cleaner vessels. Great Eastern's fleet, while not ancient, will require significant upgrades or replacements.

Competition from global shipping giants remains intense. Maersk, Mediterranean Shipping Company, COSCO—these behemoths have scale advantages Great Eastern can't match. In offshore, companies like Transocean and Noble Corporation dwarf Greatship's capabilities. Being India's largest means less when competing globally.

Then there's the cyclicality. Shipping is notorious for destroying capital during downturns. Yes, Great Eastern has survived multiple cycles, but past performance doesn't guarantee future results. One prolonged downturn with the wrong asset mix could damage even conservative operators.

The Bull Case: But here's where it gets interesting. That good profit growth of 85.1% CAGR over last 5 years despite modest revenue growth? That's operational leverage at its finest. Great Eastern isn't chasing growth; they're maximizing returns on capital.

Stock is providing a good dividend yield of 3.05%. In a zero-interest-rate world, getting paid to wait while the company compounds value isn't terrible. The conservative balance sheet means this dividend is sustainable even through downturns.

Trading at 0.98 times book value implies the market believes Great Eastern will never earn its cost of capital. But shipping is cyclical—today's pessimism becomes tomorrow's opportunity. When (not if) the next shipping boom arrives, Great Eastern's leverage to rising rates is enormous.

India's growing energy needs provide a structural tailwind. India imports 85% of its oil, 50% of its gas, significant coal and iron ore. As India grows from a $3.7 trillion to potentially $10 trillion economy over the next decade, someone needs to carry those commodities. Great Eastern is perfectly positioned.

The family ownership—often seen as a governance negative—might actually be a positive here. The Sheth family thinks in decades, not quarters. They're willing to appear stupid in the short term (holding cash when they could lever up) to be smart in the long term (buying assets when others are forced sellers).

X. Future Vision & Strategic Priorities

The shipping industry stands at an inflection point, and Great Eastern's strategic priorities reveal how a 76-year-old company plans to navigate the next chapter. The commitment to sustainability isn't just PR—it's existential. Conducting trials with biofuel, marking milestone towards greener future represents the beginning of a massive transformation.

Digital transformation in shipping operations is accelerating. Great Eastern is implementing AI-powered route optimization, predictive maintenance using IoT sensors, blockchain for documentation. This isn't Silicon Valley buzzword bingo—each percentage point of fuel saved or day of downtime avoided drops straight to the bottom line.

India's growing energy needs create unprecedented opportunity. India's oil consumption is projected to grow from 5 million barrels per day to 7 million by 2030. LNG imports could double. The infrastructure to support this—ports, pipelines, storage—is being built now. Great Eastern's deep relationships with Indian refiners and global oil majors position them as the natural bridge.

Geopolitical shifts are reshaping shipping routes. The Russia-Ukraine conflict, Red Sea tensions, China-US trade tensions—each creates new flows, new opportunities. Great Eastern's ability to operate globally while maintaining Indian registry provides unique flexibility. They can serve markets others can't access.

The next generation leadership transition looms large. Mr. Rahul Sheth was appointed as a Non-Executive Director of Greatship (India) Limited in July 2024. Mr. Rahul Sheth has been working with The Great Eastern Shipping Company Limited (GE Shipping), the parent company, since October 2014 and is currently the Executive Assistant to the Deputy Chairman and Managing Director of GE Shipping. The fourth generation is being groomed, but can they maintain the discipline and vision that built the empire?

XI. Outro & Resources

Three-quarters of a century after that Liberty ship sailed from Bombay, Great Eastern Shipping stands as testament to a simple truth: in cyclical industries, survival is success, and discipline is alpha. The company that began as sugar traders' solution to shipping cartels has become India's maritime champion, navigating through independence, wars, oil shocks, and financial crises.

The key takeaways for investors transcend shipping:

First, capital allocation trumps operations. Great Eastern's modest revenue growth but spectacular profit growth proves that in capital-intensive industries, when you buy matters more than what you buy.

Second, family businesses can work when aligned with minority shareholders. The Sheth family's conservative approach might frustrate growth investors, but it's created tremendous value for patient shareholders.

Third, balance sheet strength is optionality. Great Eastern's low leverage isn't just defense—it's the ability to play offense when others can't. In cyclical industries, the strong get stronger during downturns.

Finally, understanding cycles beats predicting them. Great Eastern doesn't know where freight rates will be next year. But they know cycles exist, extremes don't persist, and patience pays.

As we've seen throughout this journey—from Vasant Sheth pioneering tramp shipping to Bharat Sheth's post-Lehman conservatism to Ravi Sheth building an offshore empire from scratch—Great Eastern's story isn't about predicting the future. It's about being prepared for multiple futures.

The stock trades at book value, offers a decent dividend, and is run by operators who've survived everything the market could throw at them. Is it a screaming buy? That depends on your timeline and temperament. But in a world of algorithmic trading and quarterly capitalism, there's something profound about a company that still names its ships after its founder, measures success in decades, and treats capital allocation as a sacred responsibility.

The question isn't whether Great Eastern will survive the next crisis—they've proven they will. The question is whether patient investors will be there to profit when they do. As Bharat Sheth might say, with characteristic understatement: "We want to sail with the big boys." After 76 years, they've earned their place at the table. The market just hasn't noticed yet.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube