Finolex Industries: From Partition Refugees to India's PVC Pipe Kings

I. Introduction & Opening Hook

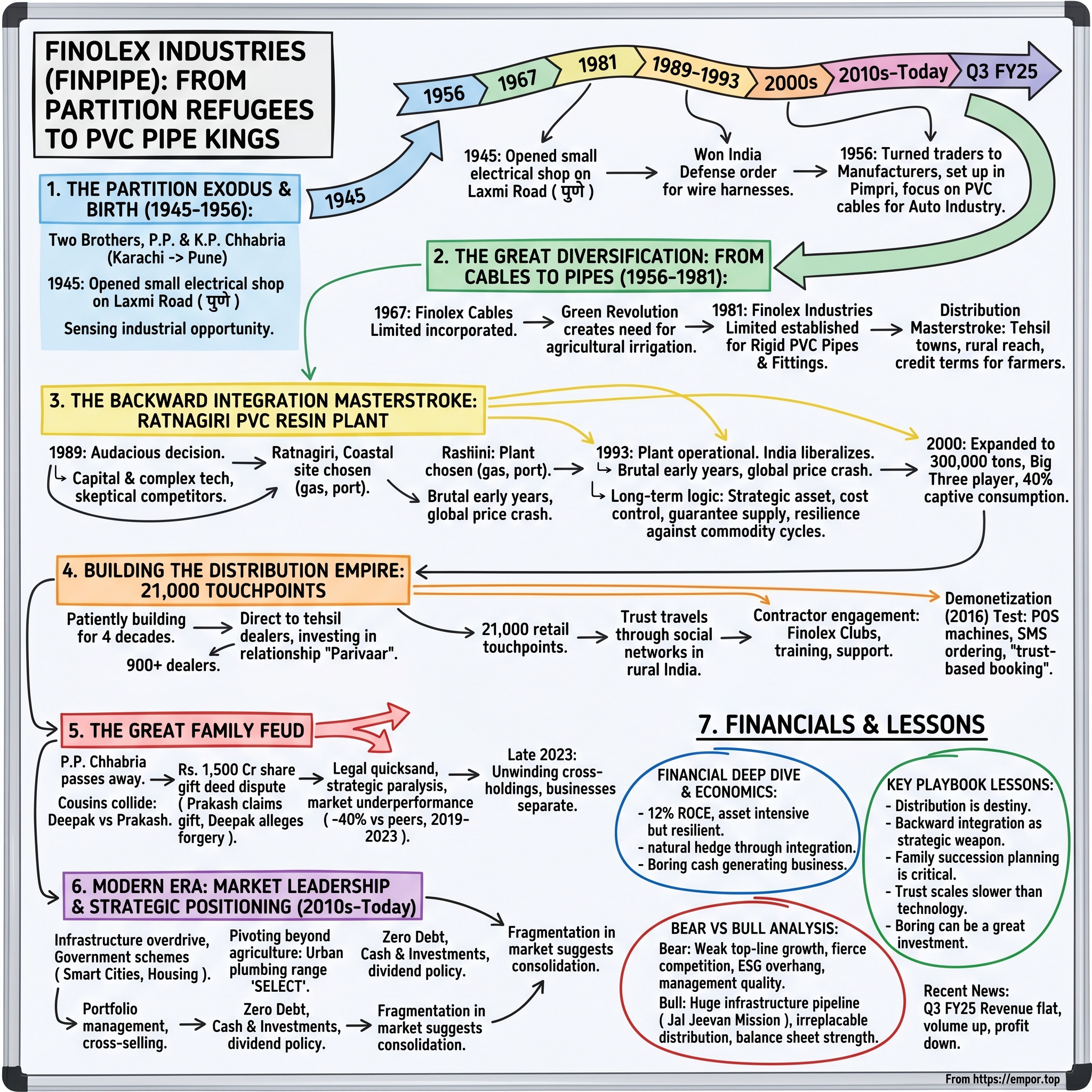

Picture this: July 1945, Pune. Two young brothers step off a train from Karachi, carrying little more than determination and the clothes on their backs. The partition of India hasn't happened yet, but the Chhabria brothers—P.P. and K.P.—can sense the winds of change. Within six months, they've scraped together enough to open a small electrical shop. Fast forward to today: that tiny shop has morphed into Finolex Industries, a ₹11,700+ crore market cap behemoth that's the backbone of India's water infrastructure.

This is the untold story of how partition refugees built India's PVC empire—a tale of backward integration brilliance, distribution mastery, and yes, a family feud that would make the Roys of Succession look tame. Finolex Industries isn't just another pipes company. It's India's only fully backward-integrated pipes and fittings manufacturer, the third-largest PVC resin player, and the second-largest PVC pipe manufacturer in the country.

But here's what makes this story truly fascinating: while tech unicorns grab headlines with their growth-at-all-costs playbooks, Finolex built a commodity empire the old-fashioned way—through vertical integration, patient capital allocation, and a distribution network so deep it reaches farmers in villages most Indians can't pronounce. They've done it while remaining virtually debt-free, navigating commodity super-cycles, and somehow managing to thrive despite a boardroom battle that's been playing out in courtrooms for years.

The company today operates from two main hubs: their pipes and fittings operations in Pune, where it all began, and their crown jewel—a PVC resin manufacturing facility in Ratnagiri on India's west coast that transformed them from just another pipe manufacturer into a vertically integrated powerhouse. With over 900 dealers and 21,000 retail touchpoints, they've built what might be India's most extensive non-FMCG distribution network outside of fertilizers.

Yet beneath this industrial success story lies a cautionary tale about family businesses, succession planning, and what happens when brothers' sons collide over thousands of crores worth of inheritance. It's a uniquely Indian story—one where partition trauma births entrepreneurial hunger, where boring businesses build lasting moats, and where family feuds can destroy decades of value creation.

II. The Partition Exodus & Birth of an Empire (1945–1956)

The monsoon of 1945 brought more than rain to Pune—it brought the Chhabria brothers, who would fundamentally reshape India's infrastructure landscape. P.P. Chhabria and K.P. Chhabria weren't your typical entrepreneurs. They were economic migrants before partition made that term a humanitarian crisis, sensing opportunity in Pune's emerging industrial corridor while Karachi still hummed with pre-partition commerce.

Within six months of arrival, the brothers had pooled their meager savings to open a small electrical goods shop on Laxmi Road—Pune's commercial artery. They weren't manufacturers yet, just traders buying from Bombay wholesalers and selling to local electricians and contractors. But even in those early days, the brothers displayed an uncanny ability to spot gaps in the market. While others sold standard electrical items, the Chhabrias focused on specialized cables and wires that Pune's nascent industrial units desperately needed.

The real turning point came in the mid-1950s when India's defense establishment came calling. The Indian Army needed wire harnesses for military trucks and tanks—specialized components that few could supply reliably. The Chhabrias won a sizeable order, but here's where the story gets interesting: instead of simply trading these components, they decided to manufacture them. This wasn't just ambition; it was strategic genius. Post-independence India was pursuing import substitution, and the government was actively supporting local manufacturing through licenses and protective tariffs.

The name "Finolex" itself tells you everything about their aspirations. "Fine" for quality, "Flex" for flexible cables, and that distinctive "O" with an electric arc across it—a logo that would eventually become synonymous with reliability in millions of Indian homes. The brothers weren't just creating a company; they were building a brand in an era when Indian businesses rarely thought beyond survival.

By 1956, they had transformed from traders to manufacturers, setting up a small-scale industrial unit in Pimpri, then a dusty suburb of Pune that would later become one of India's major auto hubs. Their focus? PVC insulated cables for the automobile industry. This wasn't random—Pune was emerging as India's Detroit, with Bajaj, Kinetic, and later Tata Motors setting up operations. The Chhabrias were betting on derived demand, a sophisticated strategy for first-generation entrepreneurs.

What made the brothers special wasn't just their business acumen but their complementary skills. P.P. was the visionary, always pushing for expansion and new products. K.P. was the operator, obsessed with quality and efficiency. Together, they created a culture that valued both growth and operational excellence—a balance that would define Finolex for decades.

The partition context here is crucial. Unlike established business families who had generational wealth and connections, the Chhabrias were building from scratch in a new nation. This hunger, this need to prove themselves, drove decisions that established players might have considered too risky. They reinvested every rupee of profit, lived modestly despite growing success, and most importantly, they understood that in a newly independent India, infrastructure would be everything. As the 1950s drew to a close, the brothers were already planning their next move—one that would take them from cables to an entirely different vertical.

III. The Great Diversification: From Cables to Pipes (1956–1981)

The 1960s opened with India facing an agricultural crisis. The country was importing millions of tons of wheat, living "ship to mouth" as critics called it. But by 1965, something remarkable was stirring—the Green Revolution. High-yielding variety seeds, chemical fertilizers, and most crucially, irrigation were about to transform Indian agriculture. The Chhabria brothers, now established cable manufacturers, saw an opportunity that others missed: every farm that adopted modern agriculture would need water, and water meant pipes.

But first, they had to formalize their cable business. In 1967, they incorporated Finolex Cables Limited, taking their informal partnership into the corporate realm. This wasn't just paperwork—it was preparation for scale. The cable business was generating steady cash flows, they had established relationships with suppliers and customers, and most importantly, they had learned how to work with PVC, a material that would define their future.

The real masterstroke came in 1981 with the establishment of Finolex Industries Limited. While Finolex Cables would continue focusing on electrical products, this new entity would manufacture rigid PVC pipes and fittings. The timing was perfect—India's agriculture was booming, tube wells were being dug across Punjab and Haryana, and the government was pouring money into irrigation infrastructure.

But here's what separated the Chhabrias from dozens of other pipe manufacturers sprouting across India: they understood that agriculture wasn't just about products—it was about reach. A farmer in rural Maharashtra couldn't drive to Pune to buy pipes. The pipes had to reach him. From day one, Finolex Industries focused on distribution, appointing dealers not just in cities but in tehsil towns, building relationships with local irrigation contractors, and crucially, offering credit terms that matched agricultural cycles.

The product strategy was equally clever. While competitors chased industrial and urban plumbing markets with their higher margins, Finolex focused on agricultural pipes—lower margins but massive volumes. They standardized on a few key sizes that covered 80% of agricultural needs, allowing them to achieve scale economies that boutique manufacturers couldn't match. They also invested heavily in quality control, understanding that a pipe failure could mean crop failure for a farmer.

By the mid-1980s, Finolex Industries was already among India's top five pipe manufacturers. But the brothers weren't satisfied with being just another pipe company. They were studying their supply chain, analyzing cost structures, and they noticed something troubling: nearly 70% of their costs came from PVC resin, which India largely imported. Price volatility in global PVC markets could wipe out margins overnight. Worse, during supply crunches, resin suppliers played favorites, leaving smaller manufacturers scrambling.

The solution was audacious for a company their size: backward integration into PVC resin manufacturing. This wasn't like adding a new product line—PVC resin production required massive capital investment, complex technology, and most challengingly, access to feedstock chemicals that were tightly controlled in India's license raj economy. Most industry veterans thought the Chhabrias were overreaching. The next decade would prove them wrong.

IV. The Backward Integration Masterstroke: Ratnagiri PVC Resin Plant

In 1989, when the Chhabrias announced plans to build a PVC resin plant in Ratnagiri, the reaction from competitors ranged from skepticism to outright mockery. PVC resin manufacturing wasn't just capital-intensive—it was technically complex, requiring expertise in chemical engineering that few Indian companies possessed. The minimum economic scale was massive, and the plant would need to compete with established global giants like Formosa Plastics and Shin-Etsu.

Ratnagiri wasn't chosen randomly. This coastal town, 350 kilometers south of Mumbai, offered three critical advantages: proximity to ONGC's gas terminals for ethylene feedstock, access to seawater for cooling (PVC production generates tremendous heat), and crucially, port facilities for importing vinyl chloride monomer (VCM) when needed. The Chhabrias had spent two years studying locations, and Ratnagiri emerged as the only site that ticked all boxes.

The numbers were staggering for a mid-sized Indian company. The initial investment exceeded ₹200 crores—more than Finolex Industries' entire market cap at the time. They had to import technology from European firms, hire chemical engineers (many poached from public sector giants like IPCL), and most challengingly, navigate India's byzantine regulatory environment to secure feedstock allocations.

But here's where the story gets interesting. While competitors saw PVC resin as a commodity, the Chhabrias understood it as a strategic asset. By producing their own resin, they wouldn't just save on margins—they'd guarantee supply during crunches, control quality from molecule to finished pipe, and most importantly, they'd have intelligence on global PVC markets that pure pipe manufacturers lacked.

The plant came online in 1993, just as India was liberalizing its economy. Perfect timing? Not quite. The early years were brutal. Global PVC prices crashed as new capacity from Asia flooded markets. The plant operated at barely 60% capacity. Many nights, P.P. Chhabria would walk the Ratnagiri facility, wondering if they'd bet the company on a losing hand.

Then, gradually, the strategic logic became apparent. When PVC prices spiked in 1995, pipe manufacturers saw margins evaporate, but Finolex Industries actually benefited—their resin division's profits offset pipe division losses. When resin supplies tightened in 1997, competitors scrambled for allocations while Finolex's pipe division hummed along at full capacity. The vertical integration wasn't just about cost savings; it was about resilience.

By 2000, the Ratnagiri plant had expanded to 300,000 tons annual capacity, making Finolex Industries one of India's "Big Three" in PVC resin alongside Reliance and DCM Shriram. But unlike these conglomerates who sold resin to third parties, Finolex kept 40% for captive consumption—enough to supply their pipe division while still generating merchant sales for cash flow.

The real genius of backward integration revealed itself in the 2000s commodity super-cycle. As China's construction boom drove global PVC prices from $600 to $1,500 per ton, pure pipe manufacturers faced existential pressure. Many sold out to larger players or simply shut down. Finolex Industries not only survived but used the crisis to gain market share, offering stable prices to dealers when competitors couldn't honor commitments. This reliability during volatility built trust that no advertising campaign could buy—dealers learned that in tough times, Finolex would deliver.

V. Building the Distribution Empire: 21,000 Touchpoints

Walk into any agriculture supply store in rural Maharashtra, Karnataka, or Gujarat, and you'll likely spot the distinctive Finolex logo. This isn't accidental—it's the result of four decades of patient distribution building that created what might be India's deepest non-FMCG network outside of fertilizers and seeds.

The foundation was laid in the 1980s when the Chhabrias made a counterintuitive decision: instead of appointing distributors in major cities and letting them handle rural areas, they went directly to tehsil towns. A typical tehsil dealer in 1985 might handle ₹10 lakhs of annual business—hardly worth the attention of major manufacturers. But Finolex didn't just appoint these dealers; they invested in them. Company representatives would spend days training local staff on pipe specifications, help design storage facilities, and crucially, extend credit terms that matched agricultural seasons.

The numbers tell only part of the story: 900+ dealers and 21,000 retail touchpoints. What they don't capture is the relationship depth. Many Finolex dealers are second or third generation, having inherited not just a business but a relationship. In their annual reports, the company refers to this network as their "parivaar"—family—and this isn't corporate speak. During the 2008 financial crisis, when banks tightened credit, Finolex extended payment terms to dealers facing cash crunches. No dealer was forced to shut shop.

The distribution strategy evolved through three distinct phases. Phase one (1980s-1990s) was about coverage—getting pipes to every farming district. Phase two (2000s) focused on depth—multiple retailers in each tehsil, exclusive Finolex stores in key markets. Phase three (2010s onwards) added sophistication—CRM systems, automated ordering, loyalty programs that would make FMCG companies envious.

But here's what makes Finolex's distribution truly special: they understood that in rural India, trust travels through social networks, not advertisements. A farmer doesn't buy pipes based on TV commercials; he buys what the local contractor recommends. So Finolex invested heavily in contractor engagement—training programs, technical support, even financing schemes. They created "Finolex Clubs" where contractors could network, learn about new products, and yes, earn loyalty rewards.

The company also pioneered what they called "below-the-line" marketing in rural markets. Instead of billboards, they painted water tanks. Instead of TV spots, they sponsored local irrigation exhibitions. They printed crop calendars with pipe selection guides, distributed free at agriculture offices. This wasn't glamorous marketing, but it built brand recall where it mattered—in the fields where purchase decisions were made.

The real test came during demonetization in 2016. Rural India ran on cash, and suddenly, nobody had any. Pipe sales crashed 40% industry-wide in Q3 FY17. But Finolex's response showcased their distribution strength. Within weeks, they'd equipped dealers with POS machines, created SMS-based ordering systems for retailers, and most remarkably, introduced a "trust-based booking" system where known contractors could book orders without immediate payment. By Q4, while competitors were still struggling, Finolex had recovered to 90% of normal sales.

This distribution network isn't just a sales channel—it's a moat. A new entrant can build a PVC plant, might even produce better pipes, but replicating thousands of relationships built over decades? That's the kind of competitive advantage that doesn't show up in financial models but defines market leadership. As one dealer in Kolhapur told me, "My father sold Finolex, I sell Finolex, and god willing, my son will too. It's not just business; it's trust built over generations."

VI. The Great Family Feud: When Brothers' Sons Collide

The boardroom of Finolex Industries must be one of the most awkward places in corporate India. Since 2019, cousins who grew up together, built businesses together, now sit across tables with lawyers, unable to agree on basic decisions. The story of how the Chhabria family went from united empire builders to warring factions is a masterclass in how succession planning—or the lack thereof—can destroy value.

When Pralhad P. Chhabria died in April 2023 at 86, he left behind more than a business empire—he left a family at war. The trouble had been brewing for years. After the founding brothers stepped back, their sons—Deepak (son of K.P.) and Prakash (son of P.P.)—took charge. Deepak became chairman of Finolex Cables, Prakash helmed Finolex Industries. On paper, a clean split. In reality, a ticking time bomb.

The explosion came via a Rs. 500 non-judicial stamp paper—the kind you'd use for a house rental agreement. On it, a gift deed transferring Rs. 1,500 crore worth of shares. Prakash claimed his late father had gifted him shares in both companies. Deepak cried foul, alleging forgery. Courts got involved. Suddenly, board meetings needed court observers, strategic decisions got stuck in legal quicksand, and a company that prided itself on quick execution found itself paralyzed.

The cross-holding structure made everything worse. Finolex Industries owns 32% of Finolex Cables. Finolex Cables owns shares in Finolex Industries. Family members have personal holdings in both. It's a structure that made sense when brothers trusted each other, but became a gordian knot when cousins went to war. Any major decision in one company affected the other, and with family members unable to agree, both companies entered strategic paralysis.

The courtroom drama reads like a soap opera script. Allegations of forged signatures, claims of mental incapacity, accusations of board meeting manipulation. In 2021, Prakash attempted to remove Deepak's nominees from Finolex Industries' board. Deepak retaliated by challenging decisions in Finolex Cables. Independent directors resigned rather than navigate the family minefield. The companies' governance scores plummeted.

But here's what makes this feud particularly destructive: it's not happening in a private company where families can fight behind closed doors. These are listed entities with thousands of minority shareholders watching their investments stagnate while cousins battle over control. Between 2019 and 2023, while the broader Indian market rallied, Finolex Industries underperformed peers by 40%. That's thousands of crores in market value evaporated—not because of business problems, but family dynamics.

The business impact goes beyond stock price. Key strategic decisions got delayed—expansion plans shelved, acquisition opportunities missed, senior talent departing for calmer waters. Competitors like Prince Pipes and Astral Poly, unburdened by boardroom battles, gained market share. The company that once prided itself on quick decision-making became known for strategic paralysis.

The resolution, when it came, was typically Indian—a family settlement that satisfied nobody but ended the public spectacle. In late 2023, the families agreed to gradually unwind cross-holdings, separate the businesses completely, and most importantly, stop washing dirty linen in public. But the damage was done. The Finolex name, once synonymous with reliability and trust, had become a cautionary tale about family business succession.

What's tragic is how preventable this was. The founding brothers, focused on building the business, never created clear succession structures. They assumed family bonds would survive business pressures—a costly mistake repeated across Indian family enterprises. No family constitution, no professional mediation mechanism, no clear separation between family wealth and company ownership. The very informality that enabled quick decisions in early years became a liability when the second generation took charge.

VII. Modern Era: Market Leadership & Strategic Positioning (2010s–Today)

The 2010s began with India in infrastructure overdrive. The government promised "Housing for All by 2022," smart cities were being planned, and rural water supply schemes received unprecedented funding. For a company making PVC pipes and resins, this should have been a golden decade. For Finolex Industries, it was—but not in the way anyone expected.

The market structure had evolved dramatically from the company's agricultural roots. By 2015, agriculture accounted for just 35% of PVC pipe demand—plumbing and sewerage had become the growth drivers. This shift favored urban-focused players like Astral Poly and Prince Pipes, who'd built their distribution around plumbing contractors rather than irrigation dealers. Finolex found itself needing to pivot without abandoning its rural stronghold.

Their response was textbook portfolio management. They launched Finolex SELECT, a premium plumbing range targeting urban markets. They introduced column pipes for borewells, capturing the growing groundwater extraction market. Most cleverly, they leveraged their agricultural relationships to cross-sell plumbing products as rural housing improved. A dealer selling agri-pipes could now offer plumbing solutions for the same farmer's new pucca house.

The numbers paint a picture of steady but unspectacular growth. Revenue grew from ₹2,800 crores in FY15 to ₹4,045 crores in FY24—a 6.77% CAGR that barely beat inflation. But this top-line view misses crucial nuances. The PVC resin business faced brutal cyclicality—prices swung from $700 to $1,400 per ton based on global oil prices and Chinese demand. The pipes business battled intense competition, with over 300 organized players and countless unorganized ones fighting for market share.

What kept Finolex afloat was their integrated model. When resin prices crashed in 2015-16, their pipes division enjoyed expanded margins. When pipe competition intensified in 2018-19, resin profits provided cushion. This natural hedge, built through backward integration decades ago, proved its worth repeatedly.

The balance sheet tells its own story. As of FY24, the company sits on virtually zero debt—remarkable for a capital-intensive manufacturer. Cash and investments exceed ₹500 crores. This isn't financial conservatism; it's strategic optionality. In a commodity business with volatile working capital needs, cash is oxygen. During COVID-19 when competitors scrambled for liquidity, Finolex extended credit to dealers, gaining loyalty that transcended economic cycles.

The market structure remains fascinating. Supreme Industries leads with 14% market share, Finolex Industries holds 11%, Astral Poly at 9%, and Prince Pipes at 7%. The top 10 players control just 60% of the market—fragmentation that suggests consolidation opportunities. But unlike FMCG where brands drive consolidation, pipes are sold on trust and availability. A contractor in Sangli doesn't care about national market share; he cares whether pipes are available when his project needs them.

Competition has also evolved beyond traditional metrics. Astral Poly built a brand through celebrity endorsements—something unheard of in industrial products. Prince Pipes went public and used capital for aggressive expansion. Chinese imports flooded the market with cheaper alternatives. Yet Finolex maintained share, not through innovation or marketing brilliance, but through sheer distribution depth and dealer loyalty.

The recent windfall—a ₹417 crore gain from land sale in Pune—highlights another reality. Companies that industrialized early now sit on valuable real estate. This Chinchwad land, bought for manufacturing in the 1960s, is now prime urban property. It's value creation through patience, not strategy—yet it provides capital for whatever strategic moves the company contemplates post-family settlement.

Today's Finolex Industries is at an inflection point. The family feud is settling, the balance sheet is strong, and India's infrastructure spending shows no signs of slowing. The new Jal Jeevan Mission promises piped water to every rural household by 2024—a ₹3.6 lakh crore opportunity. The question isn't whether Finolex can capture this growth, but whether it can transform from a steady incumbent to an aggressive consolidator. The next decade will tell.

VIII. Financial Deep Dive & Unit Economics

The numbers tell a story of a business caught between commodity hell and distribution heaven. Start with the headline metrics: ₹4,045 crores in revenue, ₹370 crores in profit, EBITDA margins hovering around 11.5%. For a company in commoditized products, these aren't terrible numbers. But dig deeper, and you'll find a business model that's both resilient and frustrating.

The PVC resin business is pure commodity economics. Input costs (ethylene, chlorine) track global petrochemical prices. Output prices follow international PVC rates with a lag. When oil prices spike, margins compress before selling prices adjust. When China dumps excess capacity, realizations crash regardless of input costs. In FY23, resin EBIT margins ranged from 3% to 15% across quarters—volatility that would give CFOs nightmares.

The pipes business operates on different economics. Gross margins are steadier—around 18-20%—because pricing power exists at the retail level. A farmer needing pipes for irrigation won't haggle over 5%; he needs water for his crops. But operating leverage is limited. Distribution costs eat 7-8% of sales, marketing another 2-3%. Net margins settle around 8-9%, respectable but not spectacular.

Working capital dynamics reveal the business's true nature. Inventory days average 45-50—you can't stock-out when a farmer needs pipes urgently. Receivable days run 60-70—dealers get credit, that's non-negotiable in rural markets. Payable days are just 30-35—resin suppliers don't extend generous terms. This working capital intensity means growth requires cash, explaining why the company maintains hefty bank balances despite low debt.

The ROCE story is where things get interesting—and disappointing. Over the last five years, return on capital employed averaged just 12%, while ROE languished at 7%. For context, even State Bank of India generates better returns. The culprit? Asset intensity. The Ratnagiri plant, while strategically brilliant, ties up enormous capital. The company employs ₹3,500 crores in operating assets to generate ₹4,000 crores in sales—asset turnover of just 1.1x.

But here's the paradox: this capital intensity is also the moat. A new entrant would need ₹1,000+ crores just to build a subscale resin plant. Add distribution infrastructure, working capital, and brand building—you're looking at ₹2,000 crores to compete seriously. In a business generating 12% returns, that math doesn't work for financial investors. This is why private equity, despite scouring the pipes sector for years, largely stayed away.

Cash flow generation tells a more optimistic story. Operating cash flow averaged ₹400 crores annually over the last five years—consistent, if not growing rapidly. Capex requirements are modest—₹100-150 crores annually for maintenance and minor expansions. This leaves ₹250+ crores in free cash flow, explaining the generous dividend policy. The company paid out ₹150+ crores in dividends in FY24, yielding 2.5% at current prices.

The land sale windfall—₹417 crores from Pune property—adds a twist. This one-time gain exceeds annual operating profit, providing dry powder for strategic moves. Management hints at capacity expansion, but history suggests caution. The last major expansion in 2011 took three years to reach optimal utilization. In commodity businesses, timing is everything, and Finolex has learned that growing for growth's sake destroys value.

Segment analysis reveals strategic choices. The company could chase higher-margin specialty pipes—CPVC, SWR, industrial applications. Margins here exceed 15%, double the agricultural segment. But Finolex stays focused on agriculture and basic plumbing, accepting lower margins for larger volumes and deeper moats. It's a choice between being a high-margin niche player versus a low-margin market leader. They've chosen the latter.

The balance sheet strength—zero debt, cash reserves, conservative accounting—provides optionality. In downturns, they can support dealers while competitors retrench. In upturns, they can invest counter-cyclically. During COVID, while peers cut dealer credit, Finolex extended terms, gaining share. This financial flexibility, boring as it seems, is competitive advantage in a working capital intensive business.

The financial story, ultimately, is about resilience over growth, stability over spectacular returns. It's a business that won't make anyone rich quickly but won't go bankrupt either. For investors seeking excitement, look elsewhere. For those valuing predictability in an unpredictable world, Finolex offers something increasingly rare—a boring business that just keeps generating cash.

IX. Playbook: Business & Investing Lessons

After studying Finolex for decades, patterns emerge that transcend pipes and resins. These aren't MBA case study insights but hard-won lessons from building a commodity empire in emerging markets.

Lesson 1: In commoditized industries, distribution is destiny. Finolex doesn't make better pipes—PVC extrusion is standardized technology. They don't have cost advantages—everyone buys the same raw materials. What they have is 21,000 touchpoints built over 40 years. When a farmer in rural Karnataka needs pipes, the local dealer stocks Finolex. That availability, that trust, that relationship—that's the moat. Tech entrepreneurs obsess over network effects; Finolex built physical network effects before the term existed.

Lesson 2: Backward integration is a strategic weapon, not just cost savings. The Ratnagiri plant doesn't generate spectacular returns on capital. But it provides intelligence on global PVC markets, ensures supply during crunches, and most importantly, signals commitment. When you've invested ₹1,000 crores in resin capacity, customers know you're not exiting the pipes business. This permanence builds trust that no marketing campaign can create.

Lesson 3: Family businesses face an inevitable succession crisis. The Chhabria feud wasn't unique—it's the norm. Birlas split, Ambanis fought, Munjals separated. First generations build together because they must. Second generations inherit wealth they didn't create, positions they might not merit. Without professional governance structures, family bonds fracture under business pressure. The lesson isn't to avoid family businesses but to invest only in those with clear succession planning.

Lesson 4: Boring businesses can be great investments—at the right price. Finolex will never be a multibagger story stock. It won't disrupt industries or create new categories. But it generates ₹400 crores in operating cash flow, pays reliable dividends, and serves essential needs that won't disappear. In a world chasing moonshots, steady compounders are undervalued. The key is patience and price discipline.

Lesson 5: In emerging markets, trust scales slower than technology. You can build a factory in two years, create products in months, but trust? That takes decades. Finolex's dealers aren't just commercial partners; they're relationships spanning generations. This social capital, invisible in financial statements, is the ultimate competitive advantage in markets where formal institutions are weak.

Lesson 6: Capital allocation matters more than growth. Finolex could have chased growth—entered new geographies, launched premium products, acquired competitors. Instead, they focused on their core, maintained balance sheet strength, and returned cash to shareholders. In commodity businesses, disciplined capital allocation beats aggressive expansion. Growing slowly but surviving downturns creates more value than growing fast but risking bankruptcy.

Lesson 7: Operational excellence compounds quietly. Finolex's factories aren't cutting-edge, but they run at 90%+ capacity utilization consistently. Their working capital management isn't aggressive, but they've never faced liquidity crunches. These operational basics, executed consistently over decades, create advantages that flashy strategies can't replicate.

Lesson 8: Market leadership in fragments markets requires patience. The PVC pipes market has 300+ organized players and countless unorganized ones. Consolidation has been predicted for 20 years; fragmentation persists. Why? Because in India, local relationships matter more than national scale. Finolex understood this, building density in core markets rather than spreading thin nationally. Sometimes, being strong regionally beats being weak nationally.

Lesson 9: Financial conservatism is strategic in cyclical industries. Zero debt seems suboptimal when capital is cheap. But in commodity businesses, leverage amplifies cyclical pain. Finolex's conservative balance sheet let them survive when resin prices spiked, extend dealer credit when competitors couldn't, and acquire assets during downturns. In volatile industries, survival matters more than optimization.

Lesson 10: The best moats are built accidentally, then recognized retrospectively. Finolex didn't set out to build India's deepest rural distribution network—they just wanted to sell pipes to farmers. They didn't backward integrate for strategic reasons—they needed reliable resin supply. These decisions, made for immediate practical reasons, created moats that planned strategies couldn't have built. Sometimes, the best business strategies emerge from solving immediate problems, not grand visions.

X. Bear vs. Bull Case Analysis

The Bear Case: Why Finolex Could Disappoint

The bearish argument starts with growth—or the lack thereof. A 6.77% revenue CAGR over five years barely beats inflation. In a country growing at 7% nominally, this is market share loss by stealth. The ROE of 7% is abysmal—investors could earn better returns in fixed deposits without equity risk. For a company in infrastructure, supposedly India's mega-theme, these numbers are inexcusable.

Competition is intensifying from every direction. Organized players like Astral and Prince are growing faster, building brands, and innovating in products. Unorganized players, who don't pay taxes or maintain quality standards, undercut prices by 15-20%. Chinese imports, despite duties, remain 10% cheaper. Finolex's response? Stick to the same strategy from the 1980s. In dynamic markets, standing still is moving backward.

The family feud's resolution doesn't eliminate overhang—it just shifts it. Cross-holdings need unwinding, board composition needs overhaul, and management bandwidth spent on legal battles can't be recovered. Competitors gained ground while Finolex fought itself. Regaining momentum after years of paralysis is harder than maintaining it.

Commodity cyclicality isn't going away. PVC resin prices depend on crude oil, Chinese demand, and global capacity additions—all beyond management control. The integrated model provides hedging, but it also concentrates risk. If both resin and pipe markets face headwinds simultaneously—as happened in 2019—the company has nowhere to hide.

Technology disruption looms larger than acknowledged. New materials like HDPE and PPR are gaining share in plumbing applications. Installation technologies are evolving, potentially reducing pipe consumption. Digital commerce platforms are disintermediating traditional distribution. Finolex's analog moats might prove less durable than assumed.

The ESG overhang is real and growing. PVC production is carbon-intensive, and plastic pipes face environmental scrutiny. European markets are mandating recycled content, standards India will eventually adopt. Finolex hasn't articulated a sustainability strategy beyond compliance. For ESG-conscious investors, this is increasingly problematic.

Management quality remains questionable. The family's focus on control over competence shows in board composition—few independent voices, limited sectoral expertise. Strategic vision seems limited to capacity expansion rather than innovation or transformation. In businesses where management quality drives outcomes, this is concerning.

The Bull Case: Why Finolex Could Surprise

The bullish argument rests on India's infrastructure reality. The Jal Jeevan Mission alone requires ₹3.6 lakh crores investment by 2024. Housing for All, Smart Cities, urban sewerage—the pipeline of projects extends beyond 2030. Finolex doesn't need to gain share; just maintaining position in a growing market ensures growth.

The distribution network is more valuable than perceived. Those 21,000 touchpoints aren't just sales outlets—they're last-mile infrastructure that tech platforms can't replicate. As rural incomes rise, as agriculture modernizes, as villages become towns, each touchpoint becomes more valuable. This physical network, built over 40 years, would cost billions to replicate today.

Balance sheet strength provides strategic flexibility. Zero debt and ₹500+ crores cash in a capital-intensive industry is remarkable. This allows countercyclical investments, opportunistic acquisitions, or aggressive pricing when competitors face stress. In commodity businesses, the strongest balance sheet often wins by outlasting competitors.

The backward integration moat is underappreciated. As environmental regulations tighten, new PVC resin capacity becomes harder to build. Existing integrated players enjoy grandfathered advantages. The Ratnagiri plant, fully depreciated and environmentally compliant, is virtually irreplaceable. This isn't reflected in book value but represents enormous strategic value.

Valuation provides margin of safety. At ₹11,700 crores market cap, you're paying 1x sales for a business generating ₹400 crores operating cash flow. The land bank alone—industrial properties in Pune and Ratnagiri—might be worth ₹1,000+ crores. The replacement cost of assets exceeds market cap. This isn't a growth story but a value play with optionality.

The family settlement removes the biggest overhang. With cousins agreeing to separate, professional management can finally emerge. Board reconstruction is underway, strategic decisions are accelerating. The company paralyzed for five years is finally moving. Sometimes, removal of negatives matters more than addition of positives.

Government focus on water infrastructure is multi-decade, not cyclical. Unlike roads or power where investment is lumpy, water infrastructure requires consistent spending. Pipes need replacement every 15-20 years, ensuring recurring demand. This isn't boom-bust infrastructure spending but steady, essential investment.

The "boring is beautiful" theme favors Finolex. In a world of disruption anxiety, investors are rediscovering stable, cash-generating businesses. Finolex won't be the next tech unicorn, but it also won't go to zero. For investors seeking sleep-at-night holdings, boring PVC pipes offer something exciting—predictability.

XI. Epilogue & "If We Were Running Finolex"

If we were running Finolex Industries today, the first order of business would be governance reconstruction. The family settlement provides a reset opportunity—use it. Bring in independent directors with operational expertise, not just compliance credentials. Someone who's run chemical plants, someone who understands rural distribution, someone who's navigated commodity cycles. The board needs voices that challenge, not just approve.

The strategic choice is stark: double down on the core or diversify into adjacencies. Our choice would be the former. Finolex's strength is rural distribution and agricultural markets. Instead of chasing urban plumbing where competition is fierce, dominate rural water infrastructure. The Jal Jeevan Mission is a once-in-generation opportunity. Build dedicated project teams, create government liaison cells, bid aggressively for rural water projects. This isn't glamorous, but it leverages existing strengths.

On capital allocation, the land sale windfall demands discipline. The temptation will be massive capacity expansion or unrelated diversification. Resist both. Instead, invest in distribution technology—digital ordering systems, dealer financing platforms, contractor training infrastructure. These investments don't show up as assets but create competitive advantages. The next war in pipes won't be fought in factories but at retailer touchpoints.

The M&A opportunity is compelling but requires patience. With 300+ players and inevitable consolidation, acquisition targets will emerge. But don't buy market share—buy distribution networks in adjacent geographies or complementary product lines. A small CPVC manufacturer with strong plumbing contractor relationships might be worth more than a large commodity pipe player.

Technology adoption shouldn't mean disruption but augmentation. Use IoT for inventory management, AI for demand forecasting, digital platforms for dealer engagement. But remember—farmers and contractors buy from people they trust, not apps. Technology should strengthen human relationships, not replace them.

The sustainability challenge needs proactive addressing. PVC isn't going away, but perception matters. Invest in recycling infrastructure, create take-back programs, develop bio-based alternatives. This isn't greenwashing but future-proofing. The company that solves PVC's environmental challenge will dominate the next decade.

On the resin business, the strategic question is focus versus scale. Our bias would be toward focus—optimize for integration rather than merchant sales. Let competitors chase market share in commodity resin. Finolex should focus on specialty grades for captive consumption, accepting lower utilization for higher strategic value.

The organizational challenge is cultural. Forty years of family management creates certain patterns—centralized decision-making, relationship-based processes, informal communication. Professionalizing doesn't mean destroying this culture but evolving it. Maintain the family values of trust and long-term thinking while adding professional disciplines of measurement and accountability.

Finally, the communication strategy needs overhaul. Finolex's story—partition refugees building infrastructure backbone—is compelling but untold. Management barely meets investors, provides minimal disclosure, treats capital markets as necessary evil. This needs to change. Not through hype but through consistent, transparent communication about strategy, challenges, and progress.

The ultimate question: Is Finolex a value trap or a patient compounder? Our view: it's a patient compounder trapped in a value stock valuation. The business generates cash, serves essential needs, and owns irreplaceable assets. It won't excite growth investors or momentum traders. But for investors who understand that wealth is created through patience, not brilliance, Finolex offers something valuable—a boring business in an essential industry with competitive advantages that compound quietly over time.

The Chhabria brothers, arriving in Pune with nothing, built an empire through persistence, not genius. Their successors' challenge isn't to revolutionize but to evolve—maintaining what works while adapting to what's changing. In pipes, as in life, the winners aren't always the most innovative but often the most persistent.

XII. Recent News

The Q3 FY25 results released in February 2025 paint a mixed picture. Total income from operations was Rs. 1,001.24 crore for Q3 FY25, down 2% against Rs. 1,019.69 crore in Q3 FY24. However, the volume story was more encouraging. Volume in Pipes & Fittings segment increased by 5% to 85,767 MT against 81,312 MT in Q3 FY24. More impressively, Volume in the PVC Resin segment increased by 30% to 56,830 MT against 43,737 MT in Q3 FY24.

The profitability picture was challenging. PAT stood at Rs. 70.96 crore in against PAT of Rs. 89.21 crore in Q3 FY24, a decline of about 20% year-over-year. Management commentary from Executive Chairman Prakash P. Chhabria was measured: "FIL has registered modest volume growth in Pipes & Fittings volume in spite of weak demand scenario during the quarter. The operating performance of the company is muted mainly due to weaker realisation."

The board approved dividends worth Rs. 3.60 per share for FY25, comprising a final dividend of Rs. 2 per fully paid up equity share of Rs. 2 each and a special dividend of Rs. 1.60 per equity share, maintaining the company's tradition of generous shareholder returns despite operational challenges.

On the family feud front, while the intense public battles of 2019-2023 have subsided, governance challenges persist. Four of the independent directors (IDs) of Finolex Industries put up for appointment to serve their respective second five-year terms could not get the requisite votes for the special resolution to succeed. In corporate history, this must be the maximum wickets to fall in a single AGM. The cross-holding structure between Finolex Industries and Finolex Cables continues to create complexity, though both companies are attempting to professionalize their boards.

The industry dynamics are evolving rapidly. The government has extended the Jal Jeevan Mission till 2028 with significantly enhanced funding. The allocation for the Department of Drinking Water and Sanitation has increased substantially to ₹74,226 cr., with ₹67,000 cr. specifically for JJM. This represents a tripling of the previous year's allocation, signaling the government's commitment to achieving universal rural water coverage.

Competitive intensity has increased. Companies like JTL Industries are winning orders under JJM, with JTL Industries receiving an order worth Rs. 24 crore under Jal Jeevan Mission. New materials like HDPE and PPR pipes are gaining traction in certain applications, though PVC remains dominant in agricultural segments.

The company's recent management changes signal potential strategic shifts. The managing director of Finolex Industries, Ajit Venkataraman, resigned, adding to leadership transitions as the company navigates post-feud restructuring.

XIII. Links & Resources

Annual Reports & Investor Materials: - Finolex Industries Investor Relations: www.finolexpipes.com/investors/ - Latest Annual Report FY24: Available on BSE/NSE websites - Quarterly Results & Presentations: Updated on company website post earnings

Industry Reports: - CRISIL Report on PVC Pipes Industry (2024) - India Brand Equity Foundation - Water Infrastructure Sector Analysis - McKinsey India - Infrastructure Investment Opportunities Report

Government Resources: - Jal Jeevan Mission Official Portal: jaljeevanmission.gov.in - Ministry of Jal Shakti - Policy Documents - NITI Aayog - Water Resources Strategy Papers

Books on Indian Family Businesses: - "The Inheritors" by Sanjay Puri - Analysis of Indian business families - "Business Maharajas" by Gita Piramal - Classic on Indian business dynasties - "India's New Capitalists" by Harish Damodaran - Caste dynamics in Indian business

Academic Case Studies: - IIM Ahmedabad Case Study: "Backward Integration in Commodity Industries" - ISB Hyderabad: "Distribution Networks in Rural India" - Harvard Business Review: "Family Business Succession in Emerging Markets"

Technical Resources: - PVC Resin Manufacturing - Chemical Engineering Handbook - IS Standards for PVC Pipes - Bureau of Indian Standards - Water Infrastructure Design Manual - Central Public Health Engineering Organisation

Competitor Analysis: - Supreme Industries Annual Reports - Astral Poly Technik Investor Presentations - Prince Pipes IPO Prospectus and Updates

News & Analysis Platforms: - Moneycontrol - Finolex Industries Page - Screener.in - Financial Analysis Dashboard - Trendlyne - News Aggregation and Analytics

Podcast Episodes: - The Seen and Unseen: "Infrastructure in India" episode - Founding Fuel: "Building Distribution Networks" - Business Story: "From Partition to Prosperity - Indian Business Families"

Documentary & Video Resources: - "The Partition: 1947" - Context on refugee entrepreneurs - CNBC TV18 Documentary: "Pipes & Prosperity - India's Water Story" - YouTube: Finolex Factory Tours and Process Videos

Court Documents & Legal Resources: - NCLT Mumbai - Finolex matters (Public documents) - Supreme Court Judgments Database - Corporate governance cases - SEBI Orders on related party transactions and governance

Industry Associations: - All India Plastic Manufacturers Association (AIPMA) - Indian Plumbing Association - Plastic Pipes and Fittings Manufacturers Association

ESG & Sustainability: - CDP Water Disclosure Reports - Sustainability Reports - Finolex Industries - UNEP Report on Plastic Industry Transformation

Market Research: - Frost & Sullivan - Indian Pipes Market Analysis - TechSci Research - PVC Resin Market Forecast - Ken Research - Rural Water Infrastructure Report

This comprehensive resource list provides investors, analysts, and business students with materials to conduct deeper research into Finolex Industries, the PVC pipes sector, and the broader themes of family business, infrastructure development, and emerging market dynamics that define this compelling industrial story.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube