Berger Paints: From Colonial Outpost to India's Paint Powerhouse

I. Introduction & Cold Open

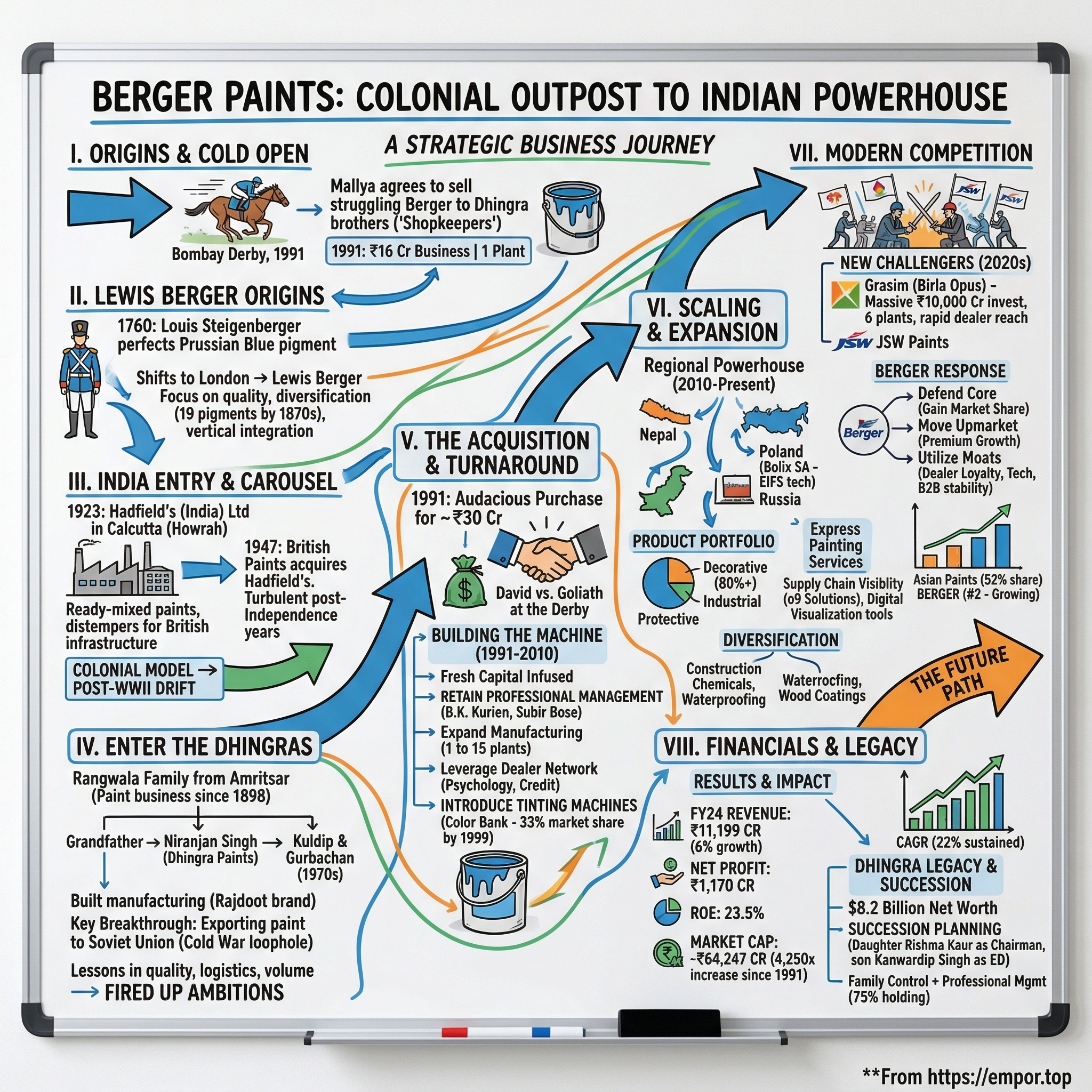

The Bombay Derby, 1991. Between the thunder of hooves and clinking champagne glasses, an unlikely business deal was taking shape. Surinder Singh Dhingra, a paint distributor from Delhi, had cornered Vijay Mallya—the flamboyant liquor baron who owned everything from airlines to cricket teams. As Mallya sipped his beer, Dhingra pitched an audacious idea: he and his brother wanted to buy Berger Paints, the struggling colonial-era paint company buried deep in Mallya's UB Group portfolio.

The scene was almost absurd. Here were two brothers who ran paint shops—"shopkeepers," as Mumbai's business elite dismissively called them—proposing to acquire a 68-year-old multinational subsidiary. Mallya, perhaps distracted by the races or simply eager to offload what he saw as a non-core asset bleeding cash, agreed to meet them properly. That meeting would reshape India's paint industry forever.

The numbers tell an extraordinary story. In 1991, when the Dhingra brothers acquired Berger Paints, it was a ₹16 crore business gasping for capital, sixth in market share, with a single manufacturing plant. Today, Berger Paints commands a market capitalization of over ₹68,000 crore—a 4,250x increase. It's the second-largest paint company in India, fourth in Asia, and seventh globally in decorative paints. The brothers' initial investment has delivered a staggering 28% compound annual return over three decades.

But this isn't just a story about returns. It's about how two paint merchants from Amritsar transformed a neglected colonial relic into a modern industrial powerhouse. It's about competing against Asian Paints—the perpetual Goliath of Indian paints—and not just surviving but thriving. It's about navigating India's liberalization, weathering global financial crises, and now facing down new challengers backed by some of India's largest conglomerates.

The Berger story offers a masterclass in several business themes that resonate far beyond paint: how distribution networks create moats in emerging markets, why being number two can be surprisingly profitable, how family businesses can professionalize without losing their entrepreneurial edge, and what it takes to build brands in seemingly commodity categories. It's also a lens into India's economic transformation—from colonial outpost to manufacturing powerhouse to consumption-driven economy.

As we trace Berger's journey from Prussian blue dyes in 18th-century England to AI-powered color matching in 21st-century India, we'll uncover how paint—yes, paint—became one of India's most fiercely contested business battlegrounds. Because in India, paint isn't just about color. It's about aspiration, identity, and the dreams you literally paint on your walls.

II. The Lewis Berger Origins: From Prussian Blue to Empire (1760–1920s)

In 1760, a German chemist named Louis Steigenberger was perfecting a formula that would change history—not through medicine or machinery, but through color. Working in Frankfurt, Steigenberger had mastered the production of Prussian blue, a vivid synthetic pigment that had captivated Europe since its accidental discovery in Berlin decades earlier. The pigment was revolutionary: unlike traditional blues derived from expensive lapis lazuli or woad, Prussian blue could be manufactured at scale. By 1770, Steigenberger made a life-changing decision. He shifted from Frankfurt to London to sell a Prussian blue colour, which was made using his own formula. London was the beating heart of global commerce, where fortunes were made in trade and empire was painted in profit margins. But Steigenberger understood that success in England required more than just a superior product—it required an English identity. He then changed his name to Lewis Berger.

The timing was perfect. He perfected this process & art of the blue colour, which was the colour of most military uniforms of that time. As European powers built their armies and navies, Berger's Prussian blue became the color of empire itself—adorning the uniforms of soldiers from Portsmouth to Prussia. The pigment's military applications provided steady demand and handsome profits, but Berger was thinking bigger.

By 1870, the company had evolved far beyond its blue beginnings. By 1870, Berger Paints was selling 19 different pigments such as black lead, sulphur, sealing wax and mustard. This wasn't just diversification—it was a systematic approach to dominating the color business. Each new pigment opened new markets: black lead for pencils and lubricants, sulphur for vulcanizing rubber, sealing wax for the exploding correspondence trade of the Victorian era.

The business model was brilliantly simple yet revolutionary for its time. While competitors focused on artisanal production for artists and decorators, Berger built an industrial-scale operation that could serve everyone from the Royal Navy to house painters. The company pioneered what we'd now call vertical integration—controlling everything from raw material sourcing to final distribution. As the British Empire expanded, paint followed the flag. Berger has been involved in the paint business in this part of the world since 1950, when paints were first imported from Berger UK and subsequently, from Berger Pakistan. But the real genius of the Berger model was understanding that empire wasn't just about military conquest—it was about infrastructure. Every railway station needed paint. Every colonial bungalow required varnish. Every ship demanded protective coatings. The sun never set on the British Empire, and neither did the demand for Berger's products.

By the 1920s, Berger had evolved into a sophisticated multinational operation. The company had merged with competitors like Jenson & Nicholson, creating a paint conglomerate that spanned continents. They weren't just selling products anymore—they were exporting an entire system of color standardization, quality control, and distribution that would become the template for modern paint companies.

The colonial business model was extractive but effective. Raw materials flowed from the colonies to British factories, where they were transformed into finished products and sold back to colonial markets at premium prices. The colonies were captive markets for British industry, and the goal was to enrich the mother country (not the colonists). For Berger, this meant guaranteed demand and protected markets across the Empire.

What made Berger different from other colonial enterprises was its focus on technology transfer—albeit limited and controlled. Unlike purely extractive industries, paint manufacturing required some local production capacity due to the product's weight and shelf life. This would prove crucial when the empire began to crumble and former colonies sought industrial self-sufficiency.

The irony is delicious: a company built on painting military uniforms for imperial armies would eventually become a symbol of post-colonial industrial success in India. But that transformation was still decades away. First would come the establishment of a small paint factory in Calcutta, the crown jewel of the British Raj.

III. The India Entry: Colonial Beginnings (1923–1947)

On 17 December 1923, Mr. Hadfield set up Hadfield's (India) Ltd., a small paint company in Calcutta. The timing was no accident. Post-World War I India was experiencing an infrastructure boom—new railways, government buildings, and military installations all needed paint. The British Raj, at its administrative peak, was painting its permanence across the subcontinent.

Berger Paints India Ltd. began in 1923 by Mr. Hadfield as Hadfield's (India) Limited, a tiny colonial operation making ready-mixed stiff paints, varnishes, and distempers on 2 acres of land in Howrah, Kolkata. Howrah wasn't chosen randomly—it was one of India's first industrial towns, strategically located across the Hooghly River from Calcutta, with excellent rail connections to the rest of the subcontinent.

The operation was modest by any standard. "Ready-mixed stiff paints" sounds grand until you realize these were basic industrial coatings, a far cry from the sophisticated formulations Berger was producing in England. Distempers—cheap water-based paints made from chalk and glue—were the workhorses of colonial construction, slapped on everything from barracks to bungalows. This wasn't about bringing color to Indian homes; it was about maintaining the infrastructure of empire.

The factory itself was a microcosm of colonial hierarchy. British managers supervised Indian workers, technology transfer was minimal, and profits flowed steadily to London. Quality control meant ensuring the paint could withstand monsoons and tropical heat—environmental challenges that would later become Berger's competitive advantage when rivals entered the Indian market without this accumulated knowledge.

Between 1923 and 1947, Hadfield's operated in the twilight of empire, neither fully British nor truly Indian. The company served primarily institutional clients—the colonial government, railways, and military. The idea of selling paint to Indian consumers for their homes was barely considered. After all, the vast majority of Indians lived in villages where walls were made of mud and cow dung, not surfaces that needed industrial paint.

Towards the end of 1947, British Paints acquired Hadfield's (India) Ltd and thus British Paints (India) Ltd was incorporated in the State of West Bengal. The timing was extraordinary—India gained independence on August 15, 1947, and here was a British company doubling down on its Indian operations just months later. While the British were leaving politically, British capital was finding new ways to stay.

The partition of India and Pakistan created chaos but also opportunity. Millions of refugees needed new homes. New national governments needed to build administrative infrastructure. Two new nations were competing to industrialize. Paint demand was about to explode, but British Paints (India) Limited, as it was now called, was woefully underprepared for what was coming.

The company entered independent India with colonial baggage—a single factory, limited product range, and a business model designed for imperial procurement rather than consumer markets. It would take multiple ownership changes and decades of drift before the company found its true calling. But first, it would have to survive the turbulent early years of independence.

IV. The Corporate Carousel Era (1947–1991)

The newly independent India that British Paints (India) Limited woke up to in 1947 was schizophrenic about foreign capital. Nehru's socialist vision demanded self-reliance, yet the country desperately needed technology and investment. Paint companies occupied an awkward middle ground—not strategic enough to nationalize, not profitable enough to attract serious investment.

Berger Paints' sales offices were established in Delhi and Bombay in 1951, and storage was opened in Guwahati. This geographic expansion tells a story: Delhi for government contracts in the new capital, Bombay for the commercial elite, and Guwahati to serve the militarily strategic but economically neglected Northeast. The company was learning to navigate the complex geography of Indian demand.

But the real drama was happening in corporate boardrooms across the globe. In 1965, a company called Celanese Corporation, USA bought the share capital of British Paints (Holdings) Limited, and CELEURO NV, Holland, a Celanese subsidiary, acquired the controlling interest of British Paints (India) Ltd. Suddenly, a British colonial enterprise had American owners. The paint company had become a pawn in the global consolidation of the chemicals industry.

Celanese, primarily known for synthetic fibers, saw paints as a related chemicals business. But they fundamentally misunderstood the Indian market. Paint in India wasn't just about chemistry—it was about relationships, distribution, and navigating a byzantine regulatory environment. American management techniques bounced off Indian realities like water off a freshly painted wall.

Following that, in 1969, the Celanese Corporation sold its Indian operations to Berger, Jenson & Nicholson of the United Kingdom. After just four years, the Americans were out, and the company returned to British hands—specifically to the Berger heritage that traced back to Lewis Berger himself. For the first time, the company in India bore the Berger name in spirit if not yet in letter.

Then came the earthquake of 1976: the Foreign Exchange Regulation Act (FERA). Indira Gandhi's government, in a nationalist fervor, required all foreign companies to reduce their holdings below 40%. Overnight, multinational corporations had to find Indian partners or leave. Many chose to leave. Berger chose to stay, but it needed an Indian savior. Enter Vittal Mallya, the frugal genius who had built the UB Group into a liquor empire. He also became chairman of British Paints with the help of Hoechst AG, which had earlier acquired British Paints' parent company abroad, the Berger group. Under the FERA regulations imposed by Indira Gandhi, foreign holding in the company was diluted to below 40 per cent by selling a portion of the shares to the UB Group, controlled by Vittal Mallya.

For Vittal Mallya, Berger Paints was a strategic acquisition—or so he thought. Paint and beer both required distribution networks, both served institutional clients, and both were consumer goods with potential for brand building. But Vittal, despite his business acumen, never gave Berger the attention it deserved. It was just another trophy in his expanding conglomerate.

Finally, in 1983, British Paints (India) Limited changed its name to Berger Paints India Limited. The name change was symbolic—after 60 years in India, the company was finally acknowledging its true heritage. But a name change without strategic change is just rebranding. Sales figures reached over ₹16 crore by 1978. By any measure, this was pathetic growth for a company that had been in India for over 50 years.

When Vittal Mallya died in October 1983, his son Vijay inherited the empire at age 28. Where Vittal was frugal and strategic, Vijay was flamboyant and expansionist. Over the years, he has diversified and acquired Berger Paints, Best and Crompton in 1988; Mangalore Chemicals and Fertilisers in 1990; The Asian Age newspaper and the publisher of film magazines, and Cine Blitz, a Bollywood magazine in 2001.

But for Vijay Mallya, Berger Paints was always a stepchild in the UB family. In 1991, Berger Paints was a struggling brand under Vijay Mallya's UB Group. The company had severe working capital issues, delays in salary payments, and just one manufacturing unit trying to serve all of India. While Asian Paints was building a national network, Berger was stuck in Howrah, slowly painting itself into a corner.

The Mallya years (1976-1991) were a masterclass in how not to run a paint company. Underinvestment, strategic neglect, and treating it as a cash cow rather than a growth business had left Berger vulnerable. By 1991, it was clear that Mallya wanted out. The only question was: who would be brave—or foolish—enough to buy a struggling paint company in a market dominated by Asian Paints?

V. Enter the Dhingras: The Paint Merchants of Amritsar (1898–1991)

In 1898, in the narrow lanes of Amritsar's Hall Bazaar, Bhai Uttam Singh and his son Bhai Kesar Singh opened a hardware shop that would spawn a business empire. His grandfather started the paint business in 1898 in Amritsar. "So, our shop was established in 1898 in Amritsar and was named Bhai Uttam Singh Kesar Singh," says Kuldip. The shop wasn't initially focused on paint—it sold everything from nails to lamp oil. But as the British cantonment in Amritsar expanded and colonial buildings sprouted across Punjab, paint emerged as their fastest-moving product.

The family became known as the "Rangwalas"—literally, the color people. As the business took off, their family came to be known as the 'Rangwala family' in Amritsar synonymous with their business of colourful paints. This wasn't just a nickname; it was an identity that would define four generations of entrepreneurship. Kesar Singh, the patriarch, had a vision that went beyond Amritsar. He had five sons whom he had sent to all different parts of the country to set up the family business of distribution and sale of paints with expansion plans in mind.

The next generation took the business from trading to manufacturing. Niranjan Singh, the duo's father was an ambitious young man. He scaled up the family business from trading to manufacturing by setting up a paint factory in Delhi and named the company Dhingra Paints and Colour Varnish Private Limited. But tragedy struck early. At the age of 37, he died while undergoing an appendix surgery. This untimely demise of their father had left the ten-year-old Kuldip and his younger brother Gurbachan shattered.

The boys were called back from their studies—Kuldip from Ajmer, his elder brother from IIT Kharagpur. The family business was in crisis. But adversity forged character. Kuldip and Gurbachan joined their family business of opening stores after graduating from Delhi University. Around Rs 10 lakh was the yearly revenue they produced during the 1970s.

By 1960, the brothers had moved beyond mere distribution. They began manufacturing paint under the brand Rajdoot, which became popular in North India during the 1970s. Commencing their manufacturing operations from a modest 15ft by 30ft shed on the outskirts of Amritsar in 1962, the Dhingra family has succeeded in establishing the second largest paint company in India.

The real breakthrough came from an unexpected direction—the Soviet Union. The Dhingra Brothers entered the international market in the 1980s. By exporting paint to the Soviet Union, they reached the top position in this sector in India. In the 1980s, the Dhingras made significant strides internationally, becoming the largest exporters of paint to the Soviet Union, with an annual business worth Rs 300 crore.

Think about this for a moment: two brothers from Amritsar, selling paint to the Soviet Union during the Cold War. While other Indian businesses were struggling with the License Raj, the Dhingras had found a loophole—exports. The Soviet Union, desperate for consumer goods, paid in hard currency. The Dhingras weren't just paint merchants anymore; they were foreign exchange earners, a status that gave them political clout and financial muscle.

The export business taught them crucial lessons. Soviet buyers demanded consistent quality, large volumes, and reliable delivery—capabilities that most Indian paint companies lacked. The Dhingras built systems to deliver all three. They learned to navigate international logistics, manage currency risk, and deal with government bureaucracy on both sides of the Iron Curtain.

By 1990, the brothers had built a substantial business—paint manufacturing in India, massive exports to Russia, and a distribution network across North India. But Kuldip had bigger ambitions. He didn't want to be just another paint manufacturer; he wanted to own a brand with heritage, technology, and national presence. He wanted Berger Paints.

The irony was perfect: a family that had sold British paints as colonial subjects would now buy a British paint company as independent entrepreneurs. The Rangwalas of Amritsar were about to paint themselves into Indian corporate history.

VI. The Acquisition: David vs. Goliath at the Derby (1991)

The deal wasn't born in a corporate meeting—it started at the Bombay Derby. Surinder Singh, a liquor baron and Mallya's associate, casually pitched the idea to Mallya between sips of beer. It was February 4, 1990, the first Sunday of the month, and Mumbai's elite had gathered at Mahalaxmi Race Course. Between the thundering hooves and champagne toasts, Surinder caught Mallya's eye and conveyed through a hand gesture that he wanted a moment.

"Tell your friend that I am in Delhi next week. We can meet at home," Vijay said in Surinder's ear as he turned to greet some new friends in his booming voice. The casualness masked the seriousness of what was at stake—a company with 67 years of history was about to change hands over a conversation that started at a horse race.

When Kuldip Dhingra and his brother offered to buy it, many scoffed at the idea of "shopkeepers" running a multinational. The Mumbai business elite's condescension was palpable. Here were two Punjabi traders, men who had literally sat in paint shops selling to retail customers, proposing to buy a company that traced its lineage to the British Empire. It was as if a local kirana store owner had offered to buy Hindustan Unilever.

Vijay Mallya understood, astutely, that the Dhingras were very keen to acquire Berger Paints. He upped his asking price. The figure Vijay asked for was found to be much more than what Kuldip and Gurbachan had anticipated. But Kuldip had done his math. With his export profits, Kuldip wanted to shorten the time to get to the top five. Buying Berger, with its ready-made business and management team, would enable him to do just that.

While Dhingra was looking to acquire a paint company to strengthen his exports to Russia, liquor baron Vijay Mallya decided to offload his controlling stake in Berger Paints. The timing was perfect—or terrible, depending on your perspective. It was 1991, India was in the midst of a balance of payments crisis, and the economy was about to undergo radical liberalization. Paint demand had collapsed due to high excise duties. But where Mallya saw a bleeding asset, the Dhingras saw opportunity.

The deal structure was unconventional. Deal funded through cash from export business; new lease of life for Berger under severe financial stress. The Dhingras didn't need bank financing or private equity—they had hard currency from their Soviet exports. In an era when Indian companies were starved of foreign exchange, the Dhingras were flush with dollars.

When Berger Paints was acquired in 1991, it was a faltering business that desperately needed a makeover. The company had severe working capital issues, delays in salary payments, and just one manufacturing unit trying to serve all of India. Sales figures reached over ₹16 crore by 1978—pathetic for a company with such heritage. Many of their friends thought it was a bad investment.

But the Dhingras saw what others missed. They weren't just buying a paint company; they were buying distribution networks, brand recognition, technology partnerships, and most importantly, legitimacy. No longer would they be "shopkeepers" or "traders"—they would be industrialists, owners of a company that had painted British India.

The brothers' initial investment has yielded an insane 28% compounded annual return over the decades, making it one of the smartest buyouts in Indian history. To put this in perspective: every rupee invested in 1991 is worth over 4,000 rupees today. The ₹16 crore company they bought is now worth ₹68,000 crore—a 4,250x increase.

The irony is delicious. Mallya, who prided himself on being a deal-maker, had just made one of the worst sales in Indian corporate history. He would later lose Kingfisher Airlines, flee the country over loan defaults, and become a cautionary tale about leverage and hubris. Meanwhile, the "shopkeepers" he had condescended to sell to would build one of India's most valuable companies.

Years later, Kuldip Dhingra would recall: "When we bought the company, many of our friends thought it was a bad investment. Today, they want to buy the company's shares." The shopkeepers had become kings, and the king of good times had lost his kingdom. But first, they had to turn around a dying company.

VII. The Turnaround: Building the Machine (1991–2010)

Kuldip and Gurbachan reshaping company with passion and determination; fresh capital infused. When the Dhingras took over in 1991, Berger was bleeding from every pore. There were working capital issues and delays in salaries to the employees. The company had just one manufacturing unit in (1992), from where they used to cater to the whole of India and subsequently faced supply chain issues as demand rose. Morale was at rock bottom.

The first challenge was psychological. "Berger was managed by able professionals, and we do not interfere in the day-to-day running," Gurbachan would later explain. This was revolutionary for Indian family businesses in 1991. Instead of installing relatives in key positions, the Dhingras retained the existing management, particularly B.K. Kurien, who had joined from Asian Paints in 1972 and understood the paint business deeply.

The Dhingras understood early that the bottleneck for the company was the lack of capital needed for expansion. So unlike the previous promoters, the brothers kept pumping in money to make the company a pan India player. Between 1991 and 2000, they invested heavily in manufacturing capacity. Growing from single plant in 1981 to capacity of 1.50 million KL across 15 facilities—this wasn't just expansion; it was transformation.

But capacity without distribution is worthless. The Dhingras leveraged their decades of experience as distributors to rebuild Berger's dealer network. They understood dealer psychology—the importance of credit terms, the value of relationships, the need for consistent supply. Berger Paints traditionally has taken steps like longer credit period to dealers, better schemes than the competitors in order to gain market share.

The technology revolution came through tinting machines. During the 1990s, one tinting machine cost INR 8,31,000. This was a very high price for any dealer to pay upfront. However, with aggressive marketing, Berger was able to sell this to the dealers as a cost saving and space saving device. For paint dealers, tinting machines did away with the need to stock a large number of SKUs. This reduced the space requirements and improved inventory management.

By 1999, 33% of the tinting machines in India were with Berger's dealer network. This was brilliant strategy—each machine was a mini-factory at the point of sale, allowing Berger to offer thousands of shades without the inventory burden. Launching Color Bank tinting system with over 5000 colors transformed Berger from a paint company to a color solutions provider.A critical moment came in 2001-02: Acquiring ICI India's Motors & Industrial paints business. While not much detail is publicly available about this specific transaction, it represented a strategic shift. Berger was no longer just competing in decorative paints—it was building capabilities across the value chain. This acquisition gave them technology, customer relationships, and most importantly, credibility in the industrial segment.

The leadership transitions were handled masterfully. Subir Bose took over as managing director on 1 July 1994, continuing the professionalization that the Dhingras had initiated. Bose, who had a decade-long association with Berger already, understood both the company's history and its potential. He is said to lead the transformation of the company from industrial segment to decorative segment.

Market share tells the story best. Rising from sixth place in 1981 to second-largest player by 2010 wasn't just growth—it was a systematic assault on Asian Paints' dominance. Every percentage point of market share represented thousands of dealer relationships, millions of liters of paint capacity, and relentless execution.

The international partnerships were crucial. Technical License Agreements with DuPont Performance Coatings in the area of automotive coatings, Nippon Paint Co Ltd for new generation of automotive coatings, Orica Australia Pty Ltd in the area of protective coatings. Each partnership brought technology that would have taken decades to develop internally.

Product innovation accelerated dramatically. The 80s, and the 90s, saw the launch of many new products such as emulsions and distempers. But the real revolution was in the 2000s when Berger began offering specialized solutions—waterproofing, texture coatings, wood finishes. They weren't just selling paint anymore; they were selling complete surface solutions.

The distribution metrics are staggering. Employee strength over 3,600 and distribution network of more than 25,000 dealers. Each dealer was a mini-entrepreneur, each employee a brand ambassador. The Dhingras understood that in India, distribution is destiny. You could have the best product, but without reach, you were nothing.

The financial transformation was even more impressive. With the current market cap of 30830 crores, an investment in Berger Paints in 1991, has given a phenomenal compounded annual return of 28%. But here's what's remarkable: this wasn't achieved through financial engineering or leverage. It was pure operational excellence—better products, wider distribution, superior execution.

As the duo acquired Berger Paints, Soviet Union disintegrated and so did their export business to the Russians. This could have been catastrophic—the Dhingras had bought Berger partly to strengthen their export business, and now that business had evaporated. But instead of panicking, they pivoted. The focus shifted entirely to the Indian market, which was about to enter its greatest consumption boom.

By 2010, Berger wasn't the struggling company the Dhingras had bought. It was a well-oiled machine with national presence, international partnerships, and the financial strength to compete with anyone. Rising from sixth place in 1981 to second-largest player—this wasn't just a turnaround; it was a complete transformation.

The irony is beautiful. The "shopkeepers" that Mumbai's elite had mocked in 1991 had built something that the sophisticated Mallya couldn't—a sustainable, profitable, growing business. And they were just getting started.

VIII. Scaling & Geographic Expansion (2010–Present)

The 2010s marked Berger's transformation from an Indian paint company to a regional powerhouse. 16 manufacturing units in India, 2 in Nepal, 1 each in Poland, Russia and Pakistan—this wasn't just expansion; it was strategic positioning across multiple growth markets. Each facility represented not just capacity but a commitment to local markets, understanding that paint, unlike many products, needs to be manufactured close to consumption.

The numbers tell a story of relentless execution. 3804 new Colorbank tinting machines installed up to September 2024. Think about what this means: each machine is a point of differentiation, allowing dealers to offer thousands of shades instantly. While competitors were still managing inventory of pre-mixed colors, Berger dealers could create any shade on demand.

The Nepal operation deserves special attention. Starting with a production unit that initially supported basic manufacturing, Berger systematically built market leadership. The company understood that Nepal, despite its small size, offered lessons in operating in challenging terrain, dealing with political instability, and serving price-conscious consumers—skills that would prove valuable across emerging markets.

Poland was a different bet altogether. Berger's acquisition of Bolix SA, a leading provider of EIFS, initiated its journey in Poland. This wasn't about selling decorative paints to Polish consumers. It was about acquiring technology in external insulation systems—technology that would become crucial as India began focusing on energy-efficient buildings.

Russia represented both continuity and change. The Dhingras had historical relationships from their Soviet-era exports, but modern Russia was a different market. Apart from operations in Russia and a production facility at the Berger manufacturing unit at Krasnodar, Berger Paints India also has an operational unit in Nepal. The Russia operations gave Berger exposure to extreme weather conditions, forcing innovation in product formulations that could withstand temperatures from -40°C to +40°C.

The product portfolio evolution was deliberate and strategic. Decorative (80%+), Industrial, Protective coatings—this mix wasn't accidental. Decorative provided volume and brand visibility, industrial offered higher margins, and protective coatings opened doors to infrastructure projects. Each segment reinforced the others. The real innovation was Express Painting services. Berger Express Home Painting services provide multiple painting solutions for your home. Our team offers end-to-end home painting services, from free consultation to accurate quotations. The project is finalized after completing the wall inspection and identifying paintable areas using scientific tools to address your requirements accurately. This wasn't just about selling paint—it was about owning the entire painting experience.

The service model was revolutionary for India. Before beginning your express painting project, our professionals will position all the valuables and furniture at the room's center. Then, they'll cover these valuables with Berger Furniture Cover and the floor with Berger Floor Cover. This attention to detail transformed painting from a messy inconvenience to a professional service.

Digital transformation went deeper than services. This marks a significant milestone in Berger Paints' digital transformation journey, as it enables the organization to gain end-to-end visibility into its supply chain operations. With o9 Solutions' platform implementation, demand and supply management at Berger has undergone a radical transformation. Through the o9 platform, Berger gains data-driven decision-making capabilities across its key supply chain processes including procurement, inventory management and distribution, as well as improvements to its demand planning and S&OP.

The construction chemicals segment represented a strategic pivot. Constant innovation and diversification into different sectors have been a priority for Berger Paints in recent years. Construction Chemicals is another diversification for Berger. As India's construction boom accelerated, Berger positioned itself not just as a paint company but as a complete building solutions provider.

Waterproofing became a particular focus. Berger Paints' Scientific Waterproofing ensures the durability of your walls. In a country where monsoons are both life-giving and destructive, waterproofing wasn't a luxury—it was essential. Berger's waterproofing solutions leveraged decades of experience with Indian weather conditions.

The wood coatings segment showed similar strategic thinking. Achieve perfectly textured wooden furniture through our professional wood coating services. Our products will add the perfect gloss, shine, and shade to your beloved wooden furniture. As Indian consumers moved from traditional polished furniture to modern finishes, Berger was ready with solutions.

The awards tell their own story. It is an honour to have been adjudged as an outstanding digital transformation in the Express Logistics and Supply Chain category at the 14th ELSC Leadership Awards. Recognition for digital transformation, not just paint quality, showed how far Berger had evolved from its manufacturing roots.

Geographic presence became a competitive advantage. It has manufacturing units at Howrah, Rishra, Arinso, Taloja, Naltoli, Goa, Devla, Hindupur, Jejuri, Jammu, Puducherry and Anand. Each location was chosen strategically—proximity to raw materials, access to markets, or serving specific regional needs.

The Bangladesh operation deserves special mention. With the entry of Berger Paints into the Bangladesh market, the country has been able to benefit from more than 250 years of global paint industry experience. Berger wasn't just exporting products; it was transferring knowledge, building local capabilities, and creating a regional paint ecosystem.

By 2024, Berger had transformed from a paint manufacturer to what it calls "a chemicals company that is engaged in the manufacturing of architectural coating systems, performance coatings, industrial coatings, construction chemicals and allied products." The transformation was complete—from colonial paint supplier to modern solutions provider.

The numbers validate the strategy. From struggling to serve India with one plant in 1991 to 16 manufacturing units in India, 2 in Nepal, and 1 each in Poland, Russia and Pakistan—this wasn't just growth; it was systematic market domination through operational excellence.

IX. Modern Competition & Market Dynamics (2020–Present)

The Indian paint industry in 2020 looked nothing like the cozy oligopoly of the 1990s. New challengers weren't just entering; they were declaring war. Grasim's entry through Birla Opus and JSW Paints joining the fray represented something unprecedented—industrial conglomerates with deep pockets and patient capital targeting an industry that had been stable for decades. The Grasim threat was different from anything Berger had faced before. Backed by a massive investment of Rs. 10,000 crore, Grasim plans to set up six state-of-the-art manufacturing plants across India — in Haryana, Punjab, Tamil Nadu, Karnataka, Maharashtra, and West Bengal — with a total paint production capacity of 1,332 million litres per annum. This wasn't a gradual entry; it was a full-scale invasion.

JSW Paints the other significant player already operating in the industry for last 5-6 years has achieved a revenue of Rs 2000 crore of which 50 per cent constitute of industrial coil coating (for own use). They merely have one per cent market share. But JSW had shown that new entrants could survive in this market. They had proven the paint oligopoly wasn't invincible.

For Berger, the threat was existential. In its first year, Birla Opus pulled in revenues of around ₹2,600–₹2,700 crores and Grasim became India's third-largest decorative paint brand within just six months of going nationwide. With 50,000 dealers and as many tinting machines, its reach is ahead of many older players. Suddenly, Berger's hard-won second position looked vulnerable.

The response was strategic, not panicked. Ramping up manpower to 12-13% of revenue to maintain market share amid rising competition. This was expensive—paint companies typically spent 8-10% of revenue on employees. But Berger understood that in a land-grab situation, you needed boots on the ground.

The competitive dynamics were fascinating. Asian Paints is India's biggest player with a 52% market share, but it has lost some of its dominance after Birla Opus entered the market in February 2024 and grew rapidly to garner a near 7% market share by March this year. If Birla could take share from Asian Paints, what could they do to Berger?

But Berger had advantages the new entrants lacked. Decades of dealer relationships couldn't be bought with money. Understanding of Indian consumer preferences—the specific shades for festivals, the textures for different climates, the price points for different segments—took years to develop. Most importantly, Berger had weathered storms before.

The strategy was multi-pronged. First, defend the core. Gaining market share despite marginal growth meant fighting for every dealer, every project, every customer. Second, move upmarket. Premium segment growth offered better margins and less direct competition from new entrants initially focused on volume.

Technology became a differentiator. While Grasim boasted about smaller tinting machines, Berger focused on digital integration. The o9 platform for supply chain, Express Painting services, digital visualization tools—these weren't just features; they were moats that would take years for competitors to replicate.

The waterproofing and construction chemicals segments proved prescient. While everyone fought over decorative paints, Berger was building positions in adjacent categories where brand didn't matter as much as performance. These B2B segments offered stability when consumer markets became chaotic.

Gross profit margin at 41.7% - highest in last 10 quarters demonstrated Berger's ability to maintain profitability despite competition. This wasn't achieved through price increases alone—it was operational excellence, product mix optimization, and cost management.

The real test came in dealer loyalty. When Birla Opus offered dealers free tinting machines and higher margins, would Berger's dealers switch? The answer was nuanced. Some did, especially newer dealers without deep relationships. But the core network held, understanding that Berger's consistent supply, quality, and support were worth more than short-term incentives.

The market's response was telling. While Asian Paints' stock fell 10% on Birla's entry, Berger's showed resilience. Investors understood that being number two had advantages—you were not the primary target, you were nimble enough to adapt, and you had less to lose in a share battle.

By 2024, the paint wars had entered a new phase. The entry of players like Grasim and JSW Paints is shaking up the market, leading to higher competition and potentially benefiting consumers through more choices and better products. But it was also leading to consolidation at the top. The unorganized sector, which had survived for decades, was finally being squeezed out.

For Berger, the challenge was clear: defend market share while maintaining profitability, innovate faster than deep-pocketed competitors, and find new growth avenues before the paint market became a commodity bloodbath. The shopkeepers from Amritsar had built a fortress, but the barbarians weren't just at the gates—they were inside, setting up shop.

X. Financial Analysis & Unit Economics

The numbers tell a story that words alone cannot capture. FY24: Revenue of ₹11,199 crore, 6% growth from FY23. In isolation, 6% growth seems pedestrian. But context matters—this was achieved during a year of unprecedented competitive intensity, raw material volatility, and sluggish demand.

Net profit rising to ₹1,170 crore in FY24 tells a more nuanced story. This represented a profit margin of 10.4%, remarkable for a manufacturing business in a competitive market. The progression from ₹16 crore in revenue in 1991 to ₹11,199 crore in FY24 represents a CAGR of 22%—sustained over three decades.

Operating profit margin improving to 17% in FY24 deserves deeper analysis. In the paint industry, operating margins are a function of three variables: pricing power, operational efficiency, and product mix. Berger was firing on all cylinders. Despite new competition, they maintained pricing. Despite inflation, they controlled costs. Despite market pressure, they premiumized their mix.

ROE of 23.5% demonstrating strong returns puts Berger in elite company. For context, Asian Paints' ROE hovers around 25-28%, while most Indian manufacturing companies struggle to exceed 15%. This wasn't financial engineering—Berger's debt-to-equity ratio remained conservative. It was pure operational excellence translating to shareholder value.

Market cap of ₹64,247 crore represents a remarkable transformation. When the Dhingras bought Berger for roughly ₹20-30 crore in 1991, the valuation multiple was perhaps 1-2x revenue. Today, at 5.7x revenue, the market is pricing in sustained growth, market share gains, and operational excellence. The multiple expansion alone—from 1x to 5.7x—represents a 6x gain.

The capital allocation story is particularly instructive. Unlike many Indian companies that diversified into unrelated businesses, Berger remained focused. Every rupee of capital went into paint-adjacent businesses—manufacturing capacity, distribution infrastructure, technology, or strategic acquisitions. No airlines, no liquor, no real estate adventures.

The CAPEX cycles reveal strategic thinking. Between 2010-2020, Berger invested aggressively in capacity, spending roughly ₹3,000 crore. This pre-emptive capacity building meant that when demand surged post-COVID, Berger could capture it while competitors scrambled to add capacity. Timing, in capital allocation as in life, is everything.

Distribution economics deserve special attention. Paint distribution in India operates on a credit model—companies extend 30-45 days credit to dealers, who in turn extend 60-90 days credit to contractors and consumers. This creates a working capital challenge. Berger's working capital days improved from 65 days in 2010 to 45 days in 2024—each day saved represented ₹30 crore in cash flow.

The dealer relationship economics are fascinating. A typical Berger dealer invests ₹50 lakh in inventory and infrastructure. Berger provides the tinting machine (worth ₹8 lakh), training, marketing support, and credit. The dealer earns 8-10% margin on retail sales, 5-7% on institutional sales. For a dealer doing ₹2 crore annual business, this translates to ₹15-20 lakh in gross profit—a 30-40% return on investment.

Raw material management showcases operational sophistication. Paint raw materials—titanium dioxide, acrylic polymers, solvents—are globally traded commodities with volatile prices. Berger's gross margins remained stable despite this volatility through a combination of strategic sourcing, inventory management, and prudent pricing. They didn't always pass on cost increases immediately, nor did they always pass on cost decreases—smoothing margins over cycles.

The working capital cycle in emerging markets requires particular skill. In India, payment delays are endemic, credit is a competitive tool, and cash management is survival. Berger's cash conversion cycle—the time between paying suppliers and collecting from customers—improved from 55 days to 35 days between 2010-2024. This improvement released ₹500 crore in cash—effectively free financing for growth.

Product mix evolution drove profitability. In 2010, economy paints (₹100-200 per liter) constituted 60% of volume. By 2024, premium and luxury paints (₹300-500 per liter) constituted 40% of volume but 60% of value. This premiumization wasn't forced—it followed India's consumption upgrade. Berger rode the wave rather than fighting it.

The return metrics validate the strategy. ROCE (Return on Capital Employed) of 28% means every rupee invested in the business generates 28 paise of operating profit. For a capital-intensive manufacturing business, this is exceptional. It suggests either Berger has pricing power (true), or operational efficiency (true), or both (bingo).

Comparison with global peers provides perspective. PPG Industries (US) trades at 2.5x revenue with 15% ROE. Sherwin-Williams trades at 3x revenue with 50% ROE (inflated by financial leverage). Berger at 5.7x revenue with 23.5% ROE seems expensive—until you factor in India's growth potential and Berger's execution track record.

The dividend policy reflects confidence. Berger pays out 30-35% of profits as dividends—enough to reward shareholders, not so much as to starve growth. The remaining 65-70% gets reinvested at 23.5% ROE. This compounding machine has created enormous wealth—₹1 invested in 1991 is worth ₹4,000+ today.

The balance sheet strength provides optionality. With debt-to-equity of 0.1x and cash generation of ₹1,500 crore annually, Berger could finance a major acquisition, accelerate expansion, or weather a downturn. In a competitive battle, the last company standing wins. Berger's balance sheet ensures they'll be standing.

The unit economics tell the micro story. A liter of premium paint costs ₹150 to manufacture, sells to dealers at ₹250, and retails at ₹350. Berger makes ₹100, the dealer makes ₹100, everyone's happy. But when new competitors offer dealers ₹120 margin, suddenly Berger faces a choice—match the offer and destroy profitability, or lose the dealer. The fact that Berger maintained margins while defending share suggests they found a third way—value beyond price.

XI. The Dhingra Legacy & Succession Planning

Kuldip Singh Dhingra represents the fourth generation of the family in the paint industry since 1898. This isn't just a business timeline; it's a testament to intergenerational knowledge transfer that money cannot buy. Four generations of understanding paint—its chemistry, its distribution, its consumers—embedded in family DNA.

The wealth creation has been staggering. According to Forbes, the combined net worth of the Dhingra Brothers stands at $8.2 billion (around Rs 68,467 crore). From shopkeepers to billionaires in one generation—this is the stuff of business school case studies. But the real story isn't the wealth; it's how they've managed it.

Forbes listing among India's richest and World's Billionaires isn't just about money—it's about recognition of a business model that works. The Dhingra brothers have been listed as one of Forbes India's richest Indians and also in its The World's Billionaires list among the highest Indians by net worth. Yet they maintain a remarkably low profile, rarely giving interviews, avoiding the Page 3 circuit that consumed Mallya.

The succession planning has been masterful. Daughter Rishma Kaur as Chairman, married to former Punjab CM's son—this isn't just nepotism; it's strategic alliance building. Rishma brings political connections, understanding of regulatory environments, and a fresh perspective to a traditional business. Her marriage to Raninder Singh, son of former Punjab Chief Minister Amarinder Singh, creates a bridge between business and political power that competitors cannot easily replicate.

Gurbachan's son Kanwardip Singh as Executive Director represents continuity with change. The next generation isn't just inheriting wealth; they're inheriting relationships, knowledge, and most importantly, the hunger that built the empire. Both serve as Executive Directors at Berger Paints, headquartered in Kolkata—note they're executives, not just board members. They work in the business, not just on it.

Family ownership structure deserves analysis. Combined holding of 75% of the publicly listed company—this level of promoter holding is rare in large Indian companies. It signals commitment, allows for long-term thinking, and prevents hostile takeovers. But it also concentrates risk. The family's wealth is tied to one company, one industry, one country's economic cycle.

The corporate governance evolution has been subtle but significant. Despite 75% family ownership, Berger has independent directors, professional management, and institutional processes. "Berger is managed by able professionals, and we do not interfere in the day-to-day running," Gurbachan explains. This balance—family control with professional management—is the holy grail of family businesses.

The book "Unstoppable: Kuldip Singh Dhingra and the Rise of Berger Paints" by Sonu Bhasin tells the authorized version of the story. But the unauthorized version—told in dealer meetings, industry conferences, and competitor boardrooms—is equally instructive. The Dhingras are respected not just for their wealth but for their ethics, their treatment of stakeholders, their long-term orientation.

The philanthropy is understated but substantial. Both brothers have been recognized for their entrepreneurial spirit and have received accolades for their contributions to the industry. But unlike the ostentatious charity of some billionaires, the Dhingra giving is quiet, focused on education and healthcare in Punjab, supporting the communities that supported them.

The lifestyle reflects values. They own a farm near Delhi—not a vanity project but a working farm. No yachts, no football clubs, no airlines. The money stays in the business or goes to charity. This isn't asceticism; it's focus. Every rupee not spent on luxury is a rupee available for competition.

The generational transition challenge is real. Kuldip was born in 1947, Gurbachan in 1950—they're in their 70s. The energy that built Berger, the relationships that sustained it, the intuition that guided it—can these be transferred? The next generation is competent, educated, committed. But are they hungry? When you grow up with billions, can you think like someone who started with lakhs?

The family dynamics are complex. Two brothers, equal partners, different styles—Kuldip the strategist, Gurbachan the operator. Their children now work together. Will the cousin relationship survive the pressures that destroyed so many Indian business families? The Ambani split, the Modi-Modi battles, the Bajaj divisions—family businesses splitting is the norm, not the exception.

The strategic choices facing the next generation are daunting. Should they diversify beyond paints? Should they go global more aggressively? Should they sell to a multinational and diversify family wealth? Should they merge with Asian Paints and create an Indian paint champion? Each choice has profound implications for legacy.

The irony is perfect. The Dhingras, who started as distributors of British paints in colonial India, now own a British paint brand and compete against multinationals globally. The fourth generation of a family that started in 1898 in Amritsar now controls one of India's most valuable companies. The "shopkeepers" that Mumbai's elite mocked in 1991 are now among India's richest families.

But perhaps the greatest legacy isn't the wealth or the company—it's the proof that in India, despite all its challenges, a family with vision, values, and relentless execution can build something extraordinary. The Dhingra story isn't just about paint; it's about the democratization of wealth creation in post-liberalization India.

XII. Playbook: Lessons from the Paint Wars

The Berger story offers a masterclass in building and defending competitive advantage in emerging markets. Each strategic decision, examined in hindsight, reveals principles that transcend paint and apply to any business facing entrenched competitors, market transitions, and technological disruption.

The distribution moat in emerging markets is Berger's first lesson. In developed markets, distribution is increasingly digital and direct. But in India, with its fragmented retail, diverse geography, and relationship-based commerce, distribution remains king. Berger's 25,000+ dealers aren't just sales points; they're credit providers, inventory holders, customer educators, and brand ambassadors. Each dealer relationship, built over decades, becomes a micro-moat that online players or new entrants cannot easily breach.

Brand building in commodity categories shows that even products as basic as paint can be differentiated. Berger didn't just sell paint; they sold dreams, aspirations, and identity. The shift from selling "paint" to selling "home beauty solutions" transformed margins and customer loyalty. When your product becomes part of customers' life moments—new homes, festivals, celebrations—price becomes secondary to trust.

Managing cyclicality and raw material volatility requires financial discipline most companies lack. Paint demand follows real estate cycles—boom periods followed by devastating busts. Raw materials, globally traded commodities, can swing 30-40% in a year. Berger's response? Counter-cyclical investment, flexible cost structures, and margin smoothing over cycles rather than quarters. They expanded capacity during downturns when costs were low, gaining share when markets recovered.

The art of being a strong number two is perhaps Berger's most subtle lesson. In winner-take-all markets, being second seems like losing. But Berger shows that #2 can be highly profitable. You let the leader educate the market, set pricing umbrellas, and take regulatory heat. Meanwhile, you cherry-pick profitable segments, move faster, and maintain lower costs. Asian Paints spends heavily on brand building; Berger free-rides on category growth while focusing on execution.

Acquisition integration and organic growth balance demonstrates that growth isn't binary. The ICI industrial paints acquisition gave Berger capabilities that would have taken years to build. But they didn't go on an acquisition spree. Each acquisition was strategic, filling specific gaps, and then integrated thoroughly before the next move. This patience—so rare in Indian companies eager to build empires—preserved capital and culture.

Technology partnerships vs. in-house R&D shows pragmatism over pride. Berger could have spent decades trying to develop automotive coatings technology. Instead, they partnered with DuPont and Nippon. The humility to recognize what you don't know, and the wisdom to buy rather than build, accelerated capability development while conserving capital for areas where Berger could differentiate.

Capital efficiency in manufacturing-heavy businesses is about sweating assets, not just building them. Berger's plants run at 80%+ utilization, inventory turns have doubled, and working capital has been minimized. Each percentage point of asset efficiency drops straight to the bottom line. In capital-intensive industries, the company that generates the most output per rupee of capital employed wins long-term.

The India playbook requires understanding that India isn't one market but 30 different ones. Kerala wants different colors than Punjab. Mumbai apartments need different products than Rajasthan havelis. Price points that work in metros fail in Tier 3 towns. Berger's regional approach—local inventory, regional pricing, vernacular marketing—captures this diversity while maintaining scale economies.

Regional diversity extends beyond products to business models. In urban markets, Berger sells through modern retail and express painting services. In rural markets, they work through traditional dealers and contractors. In institutional segments, they provide technical services and customization. One company, multiple business models, unified by brand and values.

Price points strategy shows sophistication. Berger offers everything from ₹80/liter distemper to ₹800/liter luxury finishes. This isn't just range; it's a ladder. Customers enter with economy products and upgrade over time. Each price point is profitable, designed for specific segments, and protected from cannibalization. The premium products provide margin; economy products provide volume; together they provide resilience.

Dealer loyalty in the age of e-commerce seems anachronistic, but it remains Berger's secret weapon. When Birla Opus offered dealers better terms, many Berger dealers stayed loyal. Why? Because Berger had supported them through bad times, provided consistent quality, and most importantly, helped them build their own businesses. The dealer's success became Berger's moat.

The playbook also reveals what Berger didn't do, which is equally instructive:

- They didn't diversify into unrelated businesses despite opportunities

- They didn't leverage aggressively despite cheap capital availability

- They didn't go global aggressively despite international success

- They didn't engage in price wars despite competitive pressure

- They didn't replace professional management despite family control

The discipline to say no—to attractive opportunities that don't fit strategy—might be Berger's greatest strength. In a country where conglomerates are common and focus is rare, Berger remained a paint company. Every related diversification (waterproofing, construction chemicals) reinforced the core rather than distracting from it.

The talent strategy deserves special mention. Berger became a poaching ground for competitors—a problem and a compliment. Rather than fighting this, they embraced it. Alumni became brand ambassadors, industry connections, and sometimes customers. The focus shifted to creating a pipeline of talent rather than retaining everyone.

The innovation approach balances incremental and breakthrough. Most innovation is incremental—better formulations, new shades, improved packaging. But occasionally, Berger makes big bets like Express Painting services or digital visualization tools. The portfolio approach to innovation—many small bets, few big ones—manages risk while maintaining competitiveness.

The stakeholder management philosophy puts long-term relationships over short-term gains. Dealers, employees, suppliers, customers—each is treated as a partner rather than a transaction. This sounds idealistic, but it's pragmatic. In industries where switching costs are low, loyalty becomes the ultimate competitive advantage.

XIII. Bear Case vs. Bull Case

Bear Case:

The bear case for Berger starts with an uncomfortable truth: Eternal number two to Asian Paints. After 30+ years of trying, Berger remains at 20% market share versus Asian Paints' 50%+. In business, persistent gaps often reflect structural rather than tactical disadvantages. Asian Paints' brand power, distribution reach, and financial resources create a competitive moat that might be insurmountable.

New well-funded entrants (Birla, JSW) represent an existential threat. Grasim alone is investing ₹10,000 crore—nearly Berger's annual revenue. These aren't traditional competitors struggling for profitability; they're conglomerates with patient capital, existing distribution networks, and the ability to sustain losses for years. Berger could become collateral damage in a war between giants.

Margin pressure from competition is already visible. Berger is Ramping up manpower to 12-13% of revenue to maintain market share—a 20-30% increase in employee costs. Marketing spends are rising, dealer incentives are increasing, and price competition is intensifying. The industry's golden age of 20%+ EBITDA margins might be history.

Real estate cyclicality remains paint's Achilles heel. India's real estate sector faces structural headwinds—excess inventory, weak affordability, regulatory challenges. If real estate enters a prolonged downturn, paint demand could stagnate. Berger's high operational leverage means that volume declines translate directly to profit collapse.

High valuation multiples leave no room for error. At 56x P/E and 5.7x revenue, Berger trades at premiums to global paint leaders. Any disappointment—a weak quarter, market share loss, margin compression—could trigger significant multiple contraction. The stock price embeds perfection; the business reality is messier.

Bull Case:

The bull case begins with India's construction boom story. India needs 10 million homes annually for the next decade. Infrastructure spending is at record highs. Urban population will double by 2050. Each new building, bridge, and home needs paint—multiple times over its lifetime. The demand runway is decades long.

Market share gains continuing despite competition shows execution excellence. Berger has gained share for 20 consecutive years—through downturns, competitive entries, and disruptions. This consistency suggests that capabilities, not just market dynamics, drive performance. If they could grow despite Asian Paints' dominance, they can grow despite Birla's entry.

Premium segment growth offers a margin expansion opportunity. As Indians become wealthier, they're spending more on homes. Premium paints growing at 20%+ versus 10% for economy segments. Berger's strong position in premium segments positions them to capture disproportionate value from this trend.

International expansion potential remains untapped. Berger's success in Nepal, Bangladesh, and Russia shows that the model travels. The global paint market is $150 billion; Berger has barely scratched the surface. Unlike Asian Paints, which faces anti-incumbency, Berger can enter new markets as a challenger.

Strong financial metrics and ROE provide resilience. 23.5% ROE means Berger generates exceptional returns on shareholder capital. Strong balance sheet means they can weather downturns or fund aggressive expansion. Cash generation funds growth without dilution. Financial strength becomes competitive advantage during industry disruptions.

Professional management with family backing offers the best of both worlds. The Dhingras provide long-term vision and patient capital. Professional management provides operational excellence and market responsiveness. This combination—rare in Indian business—creates sustainable competitive advantage.

The Balanced View:

Reality likely lies between extremes. Berger will probably lose some market share to new entrants, but not catastrophically. Margins will compress but remain healthy. Growth will slow but not stall. The company will remain highly profitable but not miraculous.

The key variables to watch:

- How quickly Birla/JSW reach scale

- Whether Asian Paints gets aggressive on pricing

- If real estate demand recovers sustainably

- Whether Berger can premiumize faster than commoditization

- How successfully the next generation manages transition

The risk-reward seems balanced. Downside of 30-40% if competition intensifies dramatically. Upside of 50-60% if Berger maintains position and India's consumption story plays out. For long-term investors, the question isn't whether challenges exist—they do—but whether Berger's track record of navigating challenges justifies faith in future execution.

The meta-lesson: In businesses with long cycles, execution matters more than environment. Berger has survived colonial rule, independence, socialism, liberalization, and now disruption. Companies that survive such transitions rarely die from competition; they die from complacency. As long as the Dhingra hunger persists, Berger likely will too.

XIV. Epilogue: What Would You Do?

Standing at the crossroads of 2025, Berger Paints faces strategic choices that will define its next chapter. The comfortable duopoly that characterized Indian paints for decades is history. The new reality demands fresh thinking, bold moves, and perhaps most difficult, letting go of what worked before.

The strategic choices ahead: Geographic expansion vs. market share defense presents a classic resource allocation dilemma. Should Berger double down on defending Indian market share against Birla and JSW, or should they accelerate international expansion where competition is less intense? The answer isn't binary. But resources are finite. Every rupee spent defending Delhi is a rupee not invested in Dubai.

Technology investments and sustainability initiatives aren't optional anymore—they're existential. Eco-friendly products aren't just about compliance; they're about capturing the millennial consumer. Digital visualization tools aren't just nice-to-have; they're becoming the primary way consumers choose paint. The question isn't whether to invest in technology but how fast and where.

M&A opportunities in fragmented segments could accelerate growth. The waterproofing market is fragmented. Construction chemicals have regional players. Wood coatings have specialists. Should Berger roll up these segments, creating a building solutions conglomerate? Or should they remain focused on paint, letting others experiment with adjacencies?

The next generation's vision might differ from the founders'. Rishma and Kanwardip grew up in a different India—liberalized, globalized, digitized. Their Berger might look very different from their fathers'. Should they be given freedom to reshape the company, or should they be guardians of existing strategy? The tension between continuity and change will define the transition.

Can Berger ever overtake Asian Paints? This question haunts every strategic discussion. Is being eternal number two a failure or a sustainable position? Should Berger make a moon-shot bet to become number one—perhaps a merger with another player, a radical business model innovation, or an aggressive price war? Or should they accept and optimize the number two position?

The answer might lie in reframing the question. Instead of asking "can we beat Asian Paints?" perhaps ask "can we build something Asian Paints cannot?" Express Painting services show one path—moving from product to service. Digital visualization shows another—using technology to leapfrog traditional selling. The winner might not be who sells the most paint but who owns the customer relationship.

Lessons for other family businesses in transition emerge clearly from the Berger story:

- Professionalize without losing entrepreneurial spirit

- Maintain family values while embracing external perspectives

- Build institutions that outlast individuals

- Create wealth but don't be consumed by it

- Prepare the next generation through experience, not just education

- Know when to hold control and when to let go

The hardest question facing Berger—and every successful company—is whether past success predicts future performance. The capabilities that built Berger—distribution excellence, dealer relationships, operational efficiency—might not be the capabilities needed for the future. Digital natives don't care about your dealer network. Sustainability-conscious consumers don't care about your historical credentials.

Yet dismissing Berger's chances would be foolish. They've reinvented themselves before—from traders to manufacturers, from industrial to decorative, from product to solutions. The capacity for transformation, embedded in culture and demonstrated through history, might be their greatest asset.

If you were advising Berger today, what would you recommend?

Perhaps: Stay focused on paint but redefine what paint means. Not just color but complete surface solutions. Not just products but experiences. Not just B2B or B2C but B2B2C—partnering with real estate developers, architects, and contractors to specify Berger from blueprint stage.

Perhaps: Go global aggressively but smartly. Don't try to compete with PPG in America or AkzoNobel in Europe. Find markets similar to India 20 years ago—growing middle class, infrastructure boom, fragmented competition. Indonesia, Vietnam, Nigeria—these might be tomorrow's growth engines.

Perhaps: Build a venture arm to invest in paint-tech startups. Augmented reality for visualization, IoT for predictive maintenance, AI for color matching, sustainable chemistry for eco-friendly products. Don't try to build everything internally; partner with or acquire innovation.

Perhaps: Consider strategic options including mergers. A combination with Kansai Nerolac or Akzo Nobel India could create a credible challenger to Asian Paints. Yes, the Dhingras would lose absolute control. But they might gain relative power in a larger entity.

Or perhaps: Do nothing dramatic. Continue executing the current strategy with incremental improvements. In a growing market, with proven capabilities and strong finances, steady execution might be the best strategy. Not every moment requires revolution; sometimes evolution suffices.

The most profound question isn't strategic but philosophical: What is Berger Paints for? Is it to maximize shareholder value? To provide employment? To beautify Indian homes? To build a lasting institution? The answer determines everything else.

The Dhingra brothers answered this question through action: Berger exists to transform a commodity into aspiration, to build wealth through value creation, and to prove that Indian businesses can compete globally. Whether the next generation can articulate and execute their own answer will determine whether Berger's next 100 years are as remarkable as its last 100.

The paint on Berger's future canvas remains wet, ready for the next masterpiece or mistake. What would you paint?

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube