Eternal Limited: From Restaurant Reviews to India's Quick Commerce Revolution

I. Introduction & Episode Roadmap

In the annals of Indian technology entrepreneurship, few stories rival the audacious transformation of Eternal Limited. What began as a simple scanner uploading restaurant menus to an internal website at Bain & Company in 2008 has evolved into a ₹2,90,958 crore behemoth that fundamentally reshaped how India eats, shops, and experiences urban life. This is the story of how two management consultants built not just a food delivery empire, but architected India's quick commerce revolution—a tale of relentless expansion, strategic pivots, and billion-dollar bets that would make even the most seasoned Silicon Valley investors pause.

The company now commands a market capitalization of ₹2,90,958 crore with revenue of ₹23,204 crore, positioning it as one of India's most valuable consumer internet companies. But the numbers only tell part of the story. The real narrative lies in understanding how Deepinder Goyal and Pankaj Chaddah navigated through multiple near-death experiences, fought off global giants, and ultimately engineered one of the most dramatic business model transformations in Indian startup history—the acquisition and scaling of Blinkit.

The central question that drives this analysis isn't just how they built a successful food delivery platform. It's far more intriguing: How did a company that started by digitizing paper menus evolve into a conglomerate spanning food delivery, quick commerce, event ticketing, and B2B supplies? And perhaps more importantly, how did they convince public markets to believe in a vision that required burning billions before turning profitable?

This journey takes us through four distinct epochs: The discovery phase where Zomato built the rails for restaurant information across the globe; the delivery wars where they battled Swiggy, UberEats, and others for dominance; the public market baptism during a global pandemic; and finally, the audacious Blinkit acquisition that redefined their entire trajectory. Each phase reveals critical lessons about platform economics, market timing, and the art of strategic patience in hypercompetitive markets.

II. Origins: Two Consultants and a Scanner (2008-2010)

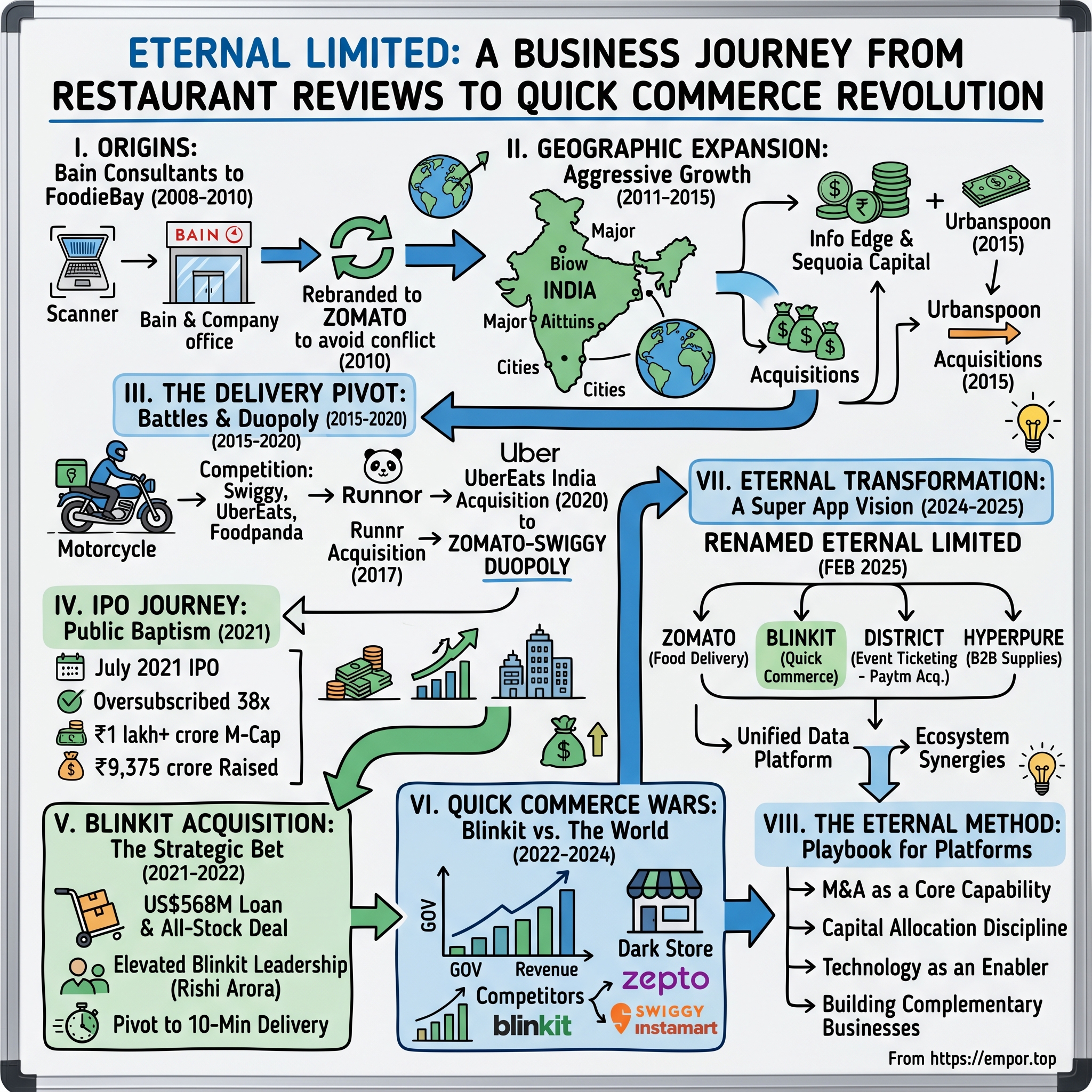

The genesis of what would become Eternal Limited traces back to the gleaming offices of Bain & Company in Gurgaon, where the monotony of lunch ordering would spark a billion-dollar idea. On July 10, 2008, Deepinder Goyal and Pankaj Chaddah launched a restaurant-listing website named FoodieBay, while working at Bain & Company. The problem they were solving was painfully personal—employees at Bain spent countless minutes daily navigating through paper menus in the pantry, trying to decide what to order for lunch.

Deepinder, a 2005 graduate from IIT Delhi, and Pankaj, graduating from the same institution in 2007, noticed that it was always a struggle to find menus of restaurants around. They had to either head to pantry areas or ask friends for the menus so that they could order food or head to a nice joint. This need helped the germination of the idea.

The solution was elegantly simple yet revolutionary for its time. Deepinder partnered with his colleague Pankaj Chaddah to create a website and scan all the restaurant menus that were around the area, and upload it on an intranet website for Bain employees. It was as good as a word document put up on the internet to simplify the restaurant or menu search for friends and colleagues. To their surprise, the website began to get a lot of traffic, far more than their imagination.

What started as an internal tool quickly revealed its commercial potential. The site was bought in April 2008 and operations started from July 2008 onwards. By this point, the duo had already begun to see beyond the walls of Bain & Company. The traffic patterns on their internal website suggested a massive unmet need in the broader market—millions of urban Indians were struggling with the same problem of restaurant discovery.

The early days were marked by incredible hustle and bootstrap mentality. Presently they had listed around 1400 restaurants in NCR region by late 2008. The approach was manual and labor-intensive—physically collecting menus, scanning them, and uploading them online. There was no sophisticated technology stack, no machine learning algorithms, just pure grunt work powered by a vision of organizing India's food ecosystem.

They quit their jobs in November 2009 to focus on the website full-time, and incorporated the company on 18 January 2010 as DC Foodiebay Online Services Private Limited. This decision to leave stable, well-paying consulting jobs wasn't taken lightly. Both came from middle-class backgrounds where such career moves were seen as risky at best, foolish at worst. Deepinder Goyal belonged to a middle-class family and completed his graduation from the prestigious Indian Institute of Technology, Delhi in the year 2005 in the field of Mathematics and Computing.

The turning point came with their first significant strategic decision—the rebranding. In November 2010, the website was renamed Zomato as they were unsure if they would "just stick to food" and to avoid a potential naming conflict with eBay. This wasn't just a cosmetic change. The name Zomato, derived from "tomato," was deliberately chosen to be globally pronounceable and memorable, signaling ambitions far beyond Delhi's restaurants.

The early product was remarkably simple compared to today's feature-rich platform. Users could browse restaurant menus, read basic information about establishments, and see contact details. There was no ordering capability, no reviews initially, and certainly no delivery infrastructure. But what it did have was comprehensive, accurate information at a time when such data was scattered and unreliable.

The joining of Pankaj is regarded by Deepinder as a turning point. He also calls Pankaj the lifeline of Foodiebay. This partnership dynamic would prove crucial—Deepinder's vision and external focus complemented by Pankaj's operational excellence and attention to detail. Together, they embodied the classic founder archetype: one looking outward at market opportunities, the other ensuring the machine ran smoothly.

By the end of 2010, Zomato had established itself as Delhi NCR's go-to platform for restaurant information. In a matter of just nine months, Foodiebay became the largest restaurant directory in Delhi NCR. The metrics were modest by today's standards but impressive for a bootstrapped operation—thousands of daily users, hundreds of restaurant listings, and most importantly, genuine product-market fit.

The foundation was set. What started as a solution to office lunch ordering had evolved into a platform with the potential to transform how India discovered and engaged with food. The next phase would test whether this Delhi success story could scale across India and eventually, the world.

III. The Expansion Playbook: Geographic Conquest (2011-2015)

The period from 2011 to 2015 marked Zomato's most aggressive phase of geographic expansion, a calculated bet that market leadership required presence before perfection. In 2011, Zomato expanded across India to Delhi NCR, Mumbai, Bangalore, Chennai, Pune, Ahmedabad and Hyderabad. This wasn't random selection—these cities represented India's economic powerhouses, with high smartphone penetration and a growing culture of eating out.

The expansion strategy was methodical yet bold. From 2012, it expanded internationally, and was operating in 21 countries by early 2015. This rapid international expansion was unprecedented for an Indian consumer internet company at the time. While companies like Infosys and TCS had gone global in services, Zomato was attempting something far more audacious—building a consumer brand across diverse markets.

The funding to fuel this expansion came at a crucial juncture. In 2010–2013, it raised approximately US$16.7 million from Info Edge across four rounds; Info Edge held a 57.9% stake in Eternal Limited in February 2013. In November 2013, Eternal Limited raised US$37 million from Sequoia Capital and Info Edge. Info Edge, the company behind Naukri.com, wasn't just a financial investor—they brought deep understanding of building internet businesses in India.

The relationship with Info Edge founder Sanjeev Bikhchandani proved transformative. Unlike typical VCs pushing for rapid monetization, Info Edge understood the value of building comprehensive databases and network effects. They had seen this playbook work with Naukri.com and believed restaurant discovery could follow a similar trajectory.

In November 2014, it completed another round of funding of US$60 million at a post-money valuation of ~US$660 million. This round of funding was led jointly by Info Edge and Vy Capital, with participation from Sequoia Capital. The valuation jump signaled market confidence in Zomato's expansion strategy.

The international expansion began with strategic acquisitions. In July 2014, the company made its first acquisition by buying New Zealand-based MenuMania. This set the template for Zomato's international strategy—acquire local players with established restaurant relationships and user bases, then integrate them into the Zomato platform.

The acquisition spree accelerated rapidly. The company pursued other acquisitions including lunchtime.cz and obedovat.sk for a combined US$3.25 million, followed by Poland-based restaurant search service Gastronauci. Each acquisition brought not just users and restaurants but also local market knowledge and relationships that would have taken years to build organically.

The crown jewel of this acquisition phase came in January 2015 with Urbanspoon. The US$60 million acquisition instantly gave Zomato presence in the United States, Canada, and Australia—markets that were considered the holy grail for any internet company. Urbanspoon brought with it 22 million monthly users and listings across thousands of cities.

But why prioritize geographic expansion over building delivery capabilities? The strategy reveals sophisticated platform thinking. Goyal and his team understood that restaurant discovery created a powerful moat—once users habituated to checking Zomato for restaurant information, adding transaction capabilities would be natural evolution. Moreover, owning discovery meant controlling the top of the funnel in the food value chain.

The content strategy during this period was equally important. Zomato didn't just list restaurants; it built comprehensive databases including menus, photos, reviews, and editorial content. The company hired food writers, photographers, and data collectors in each market. This commitment to content quality differentiated Zomato from competitors who relied solely on user-generated content.

The platform also introduced innovative features that went beyond basic discovery. In 2011, Zomato introduced online ticketing for events on its website, showing early signs of the company's ambition to own the entire "going out" experience. They even launched Zomato.xxx for food photography, demonstrating a playful approach to brand building that resonated with younger users.

In April 2015, Info Edge, Vy Capital and Sequoia Capital led another round of funding for US$50 million. By this point, Zomato was valued at over $1 billion, achieving unicorn status—a remarkable feat for a company that hadn't yet entered the food delivery business in earnest.

The organizational challenges of managing operations across 21 countries were immense. Each market had different restaurant ecosystems, user behaviors, and competitive dynamics. The Middle East loved food delivery, Southeast Asia was mobile-first, and Western markets valued detailed reviews and ratings. Zomato had to build local teams, establish restaurant partnerships, and adapt the product for each market while maintaining a coherent global platform.

The capital efficiency during this phase was remarkable in hindsight. With less than $200 million in total funding, Zomato had built a global presence that competitors would later spend billions trying to replicate. The focus on asset-light discovery rather than capital-intensive delivery allowed for rapid scaling without massive burn rates.

However, this geographic spread would soon be tested. The food-tech industry was about to undergo a fundamental shift from discovery to transactions, from content to commerce. The question was whether Zomato's broad but shallow presence could compete with focused local players who were building deep delivery networks. The next phase would determine whether the geographic expansion was strategic brilliance or dangerous distraction.

IV. The Pivot to Delivery: Fighting the Food Wars (2015-2020)

March 2015 marked a defining moment in Zomato's evolution. In March 2015, Zomato started its food delivery service in India, initially partnering with hyperlocal logistics companies such as Delhivery, Grab and Runnr to fulfill deliveries from restaurants that did not have their own delivery service. This wasn't just adding a feature—it was a fundamental transformation of the business model from an advertising-driven platform to a transaction-based marketplace.

The timing of this pivot was both forced and fortuitous. Forced because Swiggy, founded in 2014, had begun gaining serious traction with its delivery-first model. Fortuitous because smartphone penetration and digital payments were reaching inflection points in India. The market was ready for food delivery at scale, and Zomato's restaurant relationships provided a crucial head start.

The competitive landscape was brutal. Swiggy had raised significant capital and was expanding aggressively. TinyOwl and Foodpanda were burning cash to acquire customers. UberEats entered India in 2017 with the might of Uber's global resources. The food delivery market became a classic venture capital battlefield—whoever could raise the most money and sustain the highest burn rate would win.

Zomato's response was strategic acquisition and capability building. The company's acquisitions such as the Delhi-based startup MapleGraph that built MaplePOS (renamed Zomato Base), table reservation and restaurant management platform NexTable (renamed Zomato Book), and Gurgaon-based logistics technology startup Sparse Labs (renamed Zomato Trace) were integrated with Zomato. Each acquisition added a critical piece to the delivery puzzle—point-of-sale systems for restaurants, reservation management, and logistics optimization.

The most significant acquisition during this period was Runnr. In 2017, it acquired the delivery startup Runnr. Runnr brought not just technology but an entire fleet of delivery partners and operational expertise in last-mile logistics. This acquisition was crucial in helping Zomato compete with Swiggy's superior delivery infrastructure.

The technology stack evolution during this period was remarkable. Zomato built sophisticated algorithms for demand prediction, delivery partner allocation, and route optimization. The company had to solve complex problems like maintaining food quality during delivery, ensuring rider safety, and managing peak hour demand surges. Each solution required significant engineering investment and operational innovation.

The business model complexities were staggering. Unlike discovery, which had attractive unit economics, delivery was inherently challenging. Customer acquisition costs were high due to intense competition. Delivery costs often exceeded the delivery fees charged to customers. Restaurant commissions were kept low to ensure partner retention. The path to profitability seemed distant, if not impossible.

Zomato's approach to the delivery wars revealed strategic discipline despite the chaos. While competitors focused solely on order volume growth, Zomato maintained its discovery platform, generating advertising revenue that partially offset delivery losses. The company also selectively exited international markets where delivery economics didn't make sense, concentrating resources on India and select Middle Eastern markets.

The cloud kitchen experiment represented another strategic thrust. In 2017, the firm announced the launch of Zomato Infrastructure Services, a cloud kitchen infrastructure service to help partner restaurants expand their presence without incurring any fixed costs. In 2018, the company shut down operations of Zomato Infrastructure Services. While this initiative failed, it demonstrated Zomato's willingness to experiment with different models to improve unit economics.

The UberEats acquisition in January 2020 was a masterclass in strategic opportunism. Uber, facing pressure to achieve profitability globally, decided to exit India's food delivery market. Zomato acquired UberEats India in an all-stock deal, instantly gaining market share and eliminating a well-funded competitor. The deal terms weren't disclosed, but Uber received a 9.99% stake in Zomato, validating the company's long-term potential.

The organizational culture during the delivery wars was intense. Employees worked round the clock, monitoring metrics, fighting fires, and launching new initiatives. The company adopted a wartime mentality—move fast, take risks, and prioritize growth over everything else. This period forged the operational excellence that would later prove crucial in scaling Blinkit.

The marketing battles were equally fierce. Zomato and Swiggy engaged in aggressive discounting, celebrity endorsements, and creative campaigns. Zomato's witty social media presence became legendary, turning the brand into a cultural phenomenon. The company understood that in a commoditized delivery market, brand affinity could be a differentiator.

By early 2020, the food delivery market structure had crystallized into a duopoly. Zomato and Swiggy controlled over 90% of the market. UberEats had exited, Foodpanda had been acquired by Ola and subsequently shut down, and numerous smaller players had died. The war had been won, but at tremendous cost. Both companies had burned hundreds of millions of dollars, and profitability remained elusive.

The pandemic that arrived in March 2020 would dramatically alter the trajectory of food delivery. What had been a convenience for urban Indians became an essential service overnight. The industry that had struggled to justify its economics suddenly found itself at the center of a new consumer behavior paradigm. The stage was set for Zomato's next act—going public.

V. The IPO Journey: Public Market Baptism (2020-2021)

The COVID-19 pandemic transformed Zomato from a luxury for urban millennials into an essential service for millions under lockdown. Order volumes initially crashed as restaurants shut and movement restrictions kicked in, but by June 2020, a remarkable recovery was underway. Safety protocols, contactless delivery, and pent-up demand for restaurant food drove unprecedented growth.

The pandemic accelerated digital adoption by years. Customers who had never ordered online became regular users. Restaurants that resisted digital platforms had no choice but to embrace them. The total addressable market expanded dramatically, and suddenly, the unit economics that had seemed impossible started looking achievable.

In September 2020, it raised $62 million from Temasek, after previously committed investment from Ant Financial did not come through. In October 2020, as part of a Series J round of funding, Zomato raised $52 million from Kora, a US-based investment firm. These funding rounds were crucial in preparing for the public offering, providing runway and validating the business model with sophisticated investors.

The IPO preparation was meticulous. Zomato had to transform from a growth-at-all-costs startup to a company that could withstand public market scrutiny. Financial reporting was standardized, governance structures were strengthened, and a credible path to profitability was articulated. The company brought in independent directors, established audit committees, and implemented SOX-compliant processes.

July 23, 2021, marked a watershed moment not just for Zomato but for the entire Indian startup ecosystem. The company's IPO was oversubscribed 38 times, raising ₹9,375 crore. The listing day saw the stock price surge 65%, giving Zomato a market capitalization of over ₹1 lakh crore. This was India's first unicorn to go public, paving the way for other startups.

The IPO prospectus revealed fascinating details about the business. Zomato was operating in 526 cities in India, had 389,932 active restaurant listings, 161,637 active delivery partners, and 32.1 million average monthly transacting users. The company had processed 403.4 million orders in FY21, generating ₹1,994 crore in revenue. Losses stood at ₹816 crore, an improvement from ₹2,385 crore in FY20.

The public market reception was initially euphoric. Retail investors, who had watched Zomato become part of their daily lives, rushed to own a piece of the company. Institutional investors saw it as a proxy for India's digital consumption story. The successful listing validated the venture capital model in India and triggered a wave of startup IPOs.

However, the honeymoon was short-lived. By November 2021, Zomato's stock had fallen below its IPO price. Public market investors, unlike VCs, demanded quarterly performance and clear visibility on profitability. The company's adjusted EBITDA losses, aggressive investments in growth, and competitive intensity with Swiggy concerned traditional investors.

The pressure to show profitability while maintaining growth was intense. Zomato had to balance multiple stakeholders—restaurants wanting lower commissions, delivery partners seeking higher payouts, customers expecting discounts, and shareholders demanding returns. The company initiated several measures to improve unit economics, including dynamic pricing, reduced discounts, and operational efficiencies.

The governance challenges of being a public company were significant. Every decision was scrutinized, every metric analyzed, and every statement parsed for meaning. Deepinder Goyal, accustomed to the relative privacy of running a private company, had to adapt to the goldfish bowl of public markets. Quarterly earnings calls, analyst meetings, and regulatory compliance became new realities.

The strategic options available to Zomato changed dramatically post-IPO. Access to public markets meant easier capital raising through follow-on offerings. Stock became a currency for acquisitions. Employee stock options became more valuable and liquid. But it also meant less flexibility in making long-term bets that might depress short-term profitability.

The public listing also triggered introspection about Zomato's core identity. Was it a food delivery company? A restaurant tech platform? A logistics network? The answer would come through the next major strategic move—one that would redefine not just Zomato but the entire quick commerce industry in India.

VI. The Blinkit Acquisition: The $568M Bet (2021-2022)

The Blinkit acquisition represents one of the most consequential strategic decisions in Indian tech history. Blinkit was founded in December 2013 by Albinder Dhindsa and Saurabh Kumar as Grofers. What started as an online grocery delivery platform had undergone its own dramatic transformation into a quick commerce pioneer, promising 10-minute delivery of daily essentials.

The connection between Zomato and Grofers went back years. For Albinder Dhindsa, Founder and CEO of Blink Commerce, the acquisition marks a return to Zomato, where he was Head of International Operations between 2011 and 2014. This prior relationship would prove crucial in navigating the complex acquisition negotiations.

Grofers' journey to becoming Blinkit was itself remarkable. On 13 December 2021, Grofers changed its brand name to Blinkit in line with its vision to embrace quick-commerce. The company had pivoted from 90-minute grocery delivery to promising 10-minute delivery, building a network of dark stores across cities. By November 2021, the company was delivering 125,000 orders every day. In August 2021, it introduced 10-minute delivery in the top-12 cities, after completing over 20,000 under-15-minute deliveries per day across 10 cities.

The financial engineering of the acquisition was complex. In March 2022, Zomato Limited granted a US$150 million loan to Blinkit. Zomato had acquired a 10% stake in the company the year prior. Following numerous discussions, on 24 June 2022, Zomato announced that it would acquire Blinkit for US$568 million in an all-stock deal.

The market reaction was initially skeptical. Zomato's stock price fell nearly 20% in the days following the announcement. Investors questioned why a food delivery company burning cash would acquire a grocery delivery company burning even more cash. The synergies weren't immediately obvious, and the dilution to existing shareholders was significant.

Deepinder Goyal's rationale was strategic and long-term. Quick commerce represented the future of urban consumption. The same customers ordering food were also ordering groceries, and the delivery infrastructure could be leveraged across both use cases. More importantly, Blinkit's dark store network and operational expertise in sub-10-minute delivery were capabilities that would take years to build organically.

The acquisition was completed on 10 August 2022. The integration challenges were immense. Two different cultures, technology stacks, and operational philosophies had to be merged. Blinkit operated dark stores with inventory, while Zomato was a pure marketplace. The delivery partner networks were separate, and the customer apps served different use cases.

A crucial strategic decision was elevating key Blinkit executives to leadership positions. Rishi Arora, who had been with Blinkit since its early days, was named Co-founder of the combined entity. This wasn't just a retention tactic—it signaled that Blinkit wasn't being absorbed but rather becoming a core pillar of Zomato's future.

The operational improvements post-acquisition were rapid. Zomato's technology infrastructure, data analytics capabilities, and capital resources supercharged Blinkit's growth. Delivery times improved, order accuracy increased, and the dark store network expanded aggressively. The synergies that seemed questionable on paper started materializing in practice.

The financial impact was significant but strategic. While Blinkit added substantial losses to Zomato's P&L, it also brought massive growth. The quick commerce market was expanding at over 100% annually, and Blinkit was gaining market share. The bet was that scale would eventually drive profitability, just as it had in food delivery.

The competitive dynamics in quick commerce were different from food delivery. Zepto, backed by Y Combinator and other investors, was growing rapidly with a similar 10-minute delivery promise. Swiggy had launched Instamart, leveraging its food delivery infrastructure. BigBasket, Dunzo, and even Amazon were experimenting with quick delivery. The market was nascent but the stakes were enormous.

The strategic value of the acquisition became clearer over time. Quick commerce wasn't just about groceries—it was about owning the last-mile delivery infrastructure for instant gratification commerce. From groceries to electronics, medicines to fashion, anything that could be delivered in 10 minutes had potential. Blinkit gave Zomato a platform to capture this opportunity.

VII. The Quick Commerce Wars: Blinkit vs. The World (2022-2024)

The integration of Blinkit into Zomato coincided with an explosion in India's quick commerce market. What had seemed like an unsustainable luxury—10-minute delivery—suddenly became an expectation for urban consumers. The pandemic had normalized online ordering, and quick commerce took it to the next level, promising instant gratification for daily needs.

In Q1 FY26, Blinkit's revenue surged 155% YoY to ₹2,400 crore, up from ₹942 crore in the same period last year. Compared to Q4 FY25, revenue grew from ₹1,709 crore, driven by expanding demand and scale. Gross Order Value (GOV) saw a massive leap to ₹11,821 crore, up from ₹4,923 crore in Q1 FY25 and ₹9,421 crore in Q4 FY25.

The dark store expansion was aggressive and capital-intensive. Blinkit opened 243 net new stores in Q1 FY26. The company, which now has a total of 1,544 stores, said it is on track to reach 2,000 stores by December-end. Each dark store required careful location selection, inventory management, and staffing. The unit economics depended on achieving sufficient order density within a 2-3 kilometer radius.

The operational complexity of 10-minute delivery was staggering. Unlike food delivery where restaurants prepared the food, Blinkit had to manage inventory, picking, packing, and delivery. SKU selection was critical—stocking items with high turnover while avoiding dead inventory. The technology had to predict demand, optimize inventory placement, and coordinate delivery partners in real-time.

Competition intensified rapidly. Zepto raised $200 million at a $1.4 billion valuation, becoming the fastest Indian startup to achieve unicorn status. The company's founders, both Stanford dropouts, brought Silicon Valley-style execution to Indian quick commerce. Their growth was meteoric, expanding from Mumbai to multiple cities within months.

Swiggy Instamart leveraged the parent company's massive delivery fleet and customer base. The synergies were obvious—the same customer ordering lunch could order groceries for dinner. Swiggy's deep pockets and operational expertise made them a formidable competitor. The company committed billions to winning quick commerce.

The customer acquisition battle was intense but sophisticated. Unlike the crude discounting of early food delivery wars, quick commerce players focused on selection, speed, and reliability. The promise wasn't just cheap groceries but the convenience of getting anything within 10 minutes. Customer lifetime value became the key metric, not just order volume.

Blinkit's strategy under Zomato's ownership was distinctive. During the quarter, 3% of Eternal's Net Order Value came from owned inventory, particularly in the quick commerce segment. This strategy allowed Blinkit's revenue to outpace Net Order Value growth, and this share is expected to increase in the coming quarters. The shift from pure marketplace to inventory-led model improved margins but required working capital.

The technology innovations during this period were remarkable. Blinkit developed algorithms to predict what customers would order before they opened the app. Dark stores were organized for maximum picking efficiency. Delivery routes were optimized not just for speed but for order batching. The entire operation was a symphony of human and artificial intelligence.

The unit economics gradually improved through operational excellence. Order density increased as more customers adopted quick commerce. Average order values rose as customers added more items per transaction. Delivery costs per order decreased through route optimization and batching. The Average Order Value (AOV) for Blinkit remained steady at ₹669, marginally up from ₹665 in the previous quarter and ₹625 in the year-ago quarter.

However, Blinkit's aggressive dark store expansion strategy came at a cost. The segment posted an EBITDA loss of ₹162 crore, significantly wider than the ₹3 crore loss in Q1 FY25. Nevertheless, losses narrowed sequentially from ₹178 crore in Q4 FY25, indicating potential cost optimisation.

The market dynamics were fascinating. Unlike food delivery which was discretionary, quick commerce was becoming habitual. Customers ordered milk, eggs, and bread daily. The frequency of usage was unprecedented in Indian e-commerce. This high frequency created powerful network effects and customer lock-in.

The expansion into smaller cities revealed massive untapped demand. Tier-2 and Tier-3 cities, traditionally ignored by e-commerce due to logistics challenges, embraced quick commerce enthusiastically. The infrastructure investments in these cities, while expensive initially, promised long-term competitive advantages.

As Albinder Dhindsa noted: "We see enough room for store growth in all cities at this point, including those where we have good geographical coverage already. Delhi, for example, is still growing at 70 per cent+ YoY (NOV growth). We have visibility to get to 3,000 stores today, and we will communicate the timeline for getting there after we reach our current milestone of 2,000 stores by Dec '25".

VIII. The Eternal Transformation: Beyond Food (2024-2025)

The rebranding to Eternal Limited in February 2025 wasn't just cosmetic—it represented a fundamental reimagining of the company's identity and ambition. In February 2025, Zomato Limited was renamed as Eternal Limited. The name change signaled a shift from being a food delivery company to becoming a comprehensive platform for urban consumption.

The acquisition of Paytm's event ticketing business was a strategic masterstroke. In August 2024, it acquired Paytm's event ticketing subsidiaries Wasteland Entertainment Private Limited (WEPL) and Orbgen Technologies Private Limited (OTPL) for $244.2 million. This wasn't just about adding another revenue stream—it was about owning the entire "going out" experience for urban Indians.

In November 2024, the company launched its events and ticketing app called "District" after consolidating WEPL and OTPL. District represented Eternal's vision for the future—a super app for urban lifestyle. From ordering food to booking movie tickets, from getting groceries to reserving restaurant tables, Eternal wanted to be the default app for city living.

The four-pillar strategy crystallized the company's evolution. It is the parent company of Zomato, Blinkit, District and Hyperpure. Each pillar served a different need but shared common infrastructure, technology, and customers. The synergies were powerful—data from food delivery informed quick commerce inventory, event attendees ordered food, and restaurants sourced supplies from Hyperpure.

Hyperpure, the B2B supplies business, was particularly strategic. By controlling the supply chain to restaurants, Eternal could improve quality, reduce costs, and deepen restaurant relationships. Its Hyperpure supplies (B2B business) segment offers farm-to-fork supplies for restaurants in India. The business was asset-heavy but created powerful competitive moats.

The organizational restructuring revealed global ambitions tempered by regulatory realities. Eternal Limited (formerly Zomato Limited) is an Indian technology company. The company structured itself to comply with foreign investment regulations while maintaining flexibility for international expansion. The 49.5% foreign ownership cap forced creative structuring but also ensured Indian control.

The financial performance reflected this transformation. Eternal Ltd reported a 90% drop in net profit for Q1FY26 but saw a 70% increase in revenue. Shares surged 7.5% as investors reacted positively to Blinkit's performance and revenue growth in key segments. The market was willing to accept short-term profit compression for long-term strategic positioning.

The technology platform underlying these businesses was increasingly sophisticated. Eternal built a unified customer data platform that tracked behavior across all services. Machine learning models predicted not just what customers would order but when and through which service. The recommendation engines became increasingly accurate, driving higher engagement and order values.

The competitive landscape was evolving rapidly. While Swiggy remained the primary competitor in food delivery and quick commerce, new threats emerged. Amazon was investing heavily in quick commerce, Reliance's JioMart was leveraging its retail footprint, and Tata's BigBasket was expanding aggressively. The market was large enough for multiple players, but only the most efficient would survive.

The customer experience innovations were continuous. Eternal introduced Bistro, a 10-minute meal delivery service operating from cloud kitchens. This bridged the gap between quick commerce and food delivery, offering fresh, hot meals with the speed of instant delivery. The service was initially launched in select areas but showed promising early results.

As CEO Deepinder Goyal noted about the food delivery business: "I think the YoY growth is likely to bottom out now as we recover from the demand slowdown we started seeing in late 2024. For FY26, it looks unlikely that the business will deliver a 20 per cent-plus NOV growth but we should be north of 15 per cent and hopefully trending towards 20 per cent YoY growth in FY27".

The international strategy was more selective than the early expansion phase. Rather than pursuing presence everywhere, Eternal focused on markets where the integrated model made sense. The Middle East, with its high smartphone penetration and preference for delivery, remained a priority. Southeast Asian markets were evaluated for quick commerce potential.

The sustainability initiatives, while not core to profitability, became increasingly important for brand perception. Eternal introduced electric vehicles for delivery, reduced packaging waste, and partnered with NGOs for food donation. These initiatives resonated with environmentally conscious consumers and helped with regulatory relationships.

IX. Playbook: The Eternal Method

The Eternal playbook represents a masterclass in platform evolution and strategic patience. Over sixteen years, the company has consistently demonstrated key principles that separate enduring platforms from flash-in-the-pan startups. These lessons, extracted from multiple pivots and near-death experiences, offer a template for building category-defining companies in emerging markets.

Platform thinking has been central since day one. Even when Zomato was just scanning menus, the vision was to become the central node in the food ecosystem. Every subsequent move—reviews, delivery, supplies, quick commerce—added another layer to this platform. The network effects compounded: more restaurants attracted more users, which attracted more delivery partners, which enabled more services.

The M&A machine that Eternal built is unprecedented in Indian tech. With over 16 acquisitions ranging from small technology startups to billion-dollar companies like Blinkit, the company demonstrated remarkable integration capabilities. Each acquisition wasn't just about buying market share but acquiring capabilities, talent, and strategic options. The ability to successfully integrate diverse businesses into a coherent platform is a rare organizational competency.

Capital allocation discipline evolved dramatically over time. The early years saw prudent spending on international expansion with less than $200 million. The delivery wars required billions in subsidies and infrastructure. The public market phase demanded profitability demonstrations. Through each phase, management showed ability to adapt capital allocation to market realities while maintaining long-term vision.

The duopoly advantage in Indian markets proved powerful. In both food delivery and quick commerce, Eternal recognized that winner-take-all dynamics rarely materialize in India. Instead, rational duopolies emerge where two players achieve sufficient scale for unit economics while maintaining pricing discipline. This understanding allowed for strategic patience during the burn phases, knowing that consolidation would eventually occur.

Building complementary businesses versus pure diversification is a subtle but crucial distinction. Each new vertical—Hyperpure, Blinkit, District—leveraged existing assets while adding new capabilities. This wasn't conglomerate building but ecosystem expansion. The businesses reinforce each other, creating competitive moats that are difficult for single-vertical players to breach.

Managing public market expectations while investing for growth represents one of the most challenging aspects of Eternal's journey. Eternal Limited reported a 70% rise in revenue for the April-June 2025 quarter. But its net profit dropped by 90%. Despite the revenue growth, net profit dropped sharply. The company reported a net profit of ₹25 crore in Q1 FY26, compared to ₹253 crore in Q1 FY25, a decline of ₹228 crore or 90% year-on-year.

The technology architecture evolution reveals sophisticated thinking about scalability and flexibility. From monolithic applications to microservices, from batch processing to real-time systems, from rule-based to ML-driven decisions—each architectural decision balanced current needs with future possibilities. The ability to handle millions of concurrent users while maintaining sub-second response times required world-class engineering.

The brand building approach combined irreverence with reliability. Zomato's witty social media presence created cultural relevance beyond just food delivery. The brand became part of popular culture, referenced in memes, conversations, and entertainment. This emotional connection proved valuable during competitive battles and helped justify premium valuations.

Organizational culture emerged as a sustainable competitive advantage. The company attracted top talent from consulting firms, technology companies, and competitors. The culture balanced entrepreneurial risk-taking with operational discipline. The ability to maintain startup agility while building public company governance structures is rare.

The India-first but globally aware strategy proved prescient. While maintaining international presence for learning and optionality, Eternal concentrated resources on India. This focus allowed deep market understanding and operational excellence that foreign competitors couldn't match. The lessons from India are now applicable to other emerging markets with similar characteristics.

X. Analysis & Investment Case

The investment case for Eternal Limited presents a fascinating study in contrasts. The parent company of Zomato, Eternal Limited, recorded growth in revenue and a sharp fall of 90% in net profit during Q1FY26. On one hand, the company demonstrates remarkable revenue growth and market leadership. On the other, profitability remains elusive and competition intense.

The financial performance tells a complex story. Zomato earned ₹7,167 crore from its main operations in Q1 FY26. This was ₹2,961 crore more than the ₹4,206 crore earned in Q1 FY25, a 70% increase year-on-year. Revenue growth at this scale is exceptional, but it comes at a cost. The company's total expenses grew to ₹7,433 crore, from ₹4,203 crore in Q1 FY25, rising by 77% year-on-year.

The unit economics by segment reveal the underlying dynamics. The India food delivery unit, run by Zomato India, continued to be profitable. Revenue was ₹2,413 crore in Q1 FY26, up from ₹1,943 crore in Q1 FY25, a 24% increase. Net profit stood at ₹602 crore, rising from ₹470 crore last year, a ₹132 crore gain or 28% growth. The core food delivery business has achieved sustainable profitability, validating the model.

The bear case centers on several concerns. Competition remains intense with well-funded players like Swiggy and emerging threats from Zepto. Regulatory risks are mounting as the government scrutinizes quick commerce's impact on traditional retail. The massive investments required for dark store expansion pressure cash flows. The integration complexity of running four distinct businesses could lead to execution challenges.

The bull case is equally compelling. The company's B2C Net Order Value (NOV) surged 55 per cent YoY to Rs 20,183 crore, with quick commerce overtaking food delivery for the first time. Consolidated adjusted revenue rose 67 per cent YoY to Rs 7,563 crore. Market leadership in both food delivery and quick commerce creates powerful network effects. The expanding TAM as India digitizes presents massive growth opportunities.

Competitive positioning versus Swiggy reveals structural advantages. While Swiggy remains formidable, Eternal's diversified revenue streams provide resilience. The District acquisition opens new growth vectors that Swiggy hasn't matched. Hyperpure creates deeper restaurant relationships. The public company status provides easier access to capital.

The quick commerce battle with Zepto is more uncertain. Zepto's focus and execution are impressive, but Blinkit's scale and integration with Eternal's ecosystem provide advantages. Blinkit added 243 new stores during the quarter, with NOV growing 127 per cent YoY. The market is large enough for multiple winners, but operational excellence will determine relative success.

The profitability trajectory depends on multiple factors. Adjusted EBITDA dropped 42 per cent YoY to Rs 172 crore, primarily due to continued investments in Blinkit and the going-out segment. As growth moderates and operational efficiency improves, margins should expand. The question is timing—will public markets remain patient?

Valuation remains contentious. At ₹2,90,958 crore market cap, Eternal trades at approximately 12.5x revenue. For a company with minimal profits, this seems expensive by traditional metrics. However, for a platform controlling critical infrastructure in India's digital economy, it might be reasonable. The valuation ultimately depends on belief in the long-term vision.

The treasury income provides a cushion during the investment phase. The company closed Q1 FY26 with a Rs 18,857 crore cash balance. This war chest enables continued investment without immediate dilution. The financial flexibility to pursue strategic opportunities while maintaining operational independence is valuable.

Risk factors beyond competition deserve attention. Execution complexity increases with each new vertical. Regulatory scrutiny of platform businesses is intensifying globally. Labor relations with gig workers could become contentious. Technology disruptions like autonomous delivery could reshape economics. Any of these could materially impact the investment case.

XI. The Future: What's Next for Eternal?

The future of Eternal Limited extends far beyond food delivery and quick commerce. The company stands at the intersection of multiple massive trends reshaping India's consumer economy: urbanization, digitalization, and the rise of convenience culture. The strategic choices made in the next few years will determine whether Eternal becomes India's super app or remains a successful but limited platform.

The Blinkit Foods subsidiary represents an intriguing evolution. By combining cloud kitchens with quick commerce infrastructure, Eternal can offer freshly prepared meals with 10-minute delivery. This bridges the gap between restaurant food and home cooking, potentially creating an entirely new category. Early experiments in Delhi-NCR and Bangalore show promising unit economics and customer acceptance.

The inventory model shift has profound implications. The company moved from working only as a marketplace to also selling goods directly. In Q1 FY26, approximately 3% of the company's Net Order Value (NOV) was fulfilled through its own inventory. This inventory-led model means Eternal now buys products, stores them in warehouses, and delivers them to customers. While this increases working capital requirements, it also improves margins and control over customer experience.

International expansion possibilities are intriguing but complex. The integrated model of food delivery plus quick commerce could work in similar markets—dense urban areas with young populations and growing smartphone penetration. Southeast Asia, the Middle East, and parts of Latin America fit this profile. However, the capital and execution requirements for international expansion are massive.

The next acquisition targets are subject to speculation but follow logical patterns. Payment platforms would reduce transaction costs and increase customer stickiness. Health and wellness platforms would expand the addressable market. Fashion and electronics quick commerce would leverage existing infrastructure. Each acquisition would need to strengthen the ecosystem while maintaining focus.

Building India's super app remains the ultimate ambition. Unlike China where WeChat dominates, India hasn't seen a true super app emerge. Eternal's approach—starting with food and expanding to daily needs—has stronger product-market fit than payment-led or social-led approaches. The frequency of food ordering creates habitual usage that can be leveraged for other services.

The technology roadmap focuses on artificial intelligence and automation. Predictive ordering, where the platform anticipates customer needs before they're expressed, is becoming reality. Autonomous delivery vehicles, while years away from widespread deployment, could dramatically improve unit economics. Voice ordering in multiple Indian languages could expand the addressable market.

The regulatory landscape will significantly impact growth trajectory. The government's stance on quick commerce's impact on traditional retail remains uncertain. Data localization requirements could increase costs. Gig worker regulations might mandate benefits that impact unit economics. Navigating these challenges while maintaining growth will require sophisticated government relations.

The competitive dynamics will likely consolidate further. The cash burn required to compete in quick commerce is unsustainable for subscale players. Consolidation through acquisitions or shutdowns seems inevitable. The end state might be 2-3 large players with regional specialists in certain categories. Eternal's scale and capital access position it well for this consolidation.

The social impact initiatives could become differentiators. Feeding India, Zomato's non-profit addressing hunger and malnutrition, resonates with socially conscious consumers. Providing stable income to millions of delivery partners creates political goodwill. These initiatives, while not directly profitable, build long-term brand value and regulatory relationships.

The financial services opportunity is substantial but complex. With millions of transactions and rich data on spending patterns, Eternal could offer credit, insurance, and savings products. However, financial services require different capabilities and regulatory compliance. Partnerships might be more prudent than direct entry.

XII. Outro, Links & Recent News

The transformation of Eternal Limited from a restaurant menu scanner to India's quick commerce giant represents one of the most remarkable business journeys in global technology. Through multiple pivots, fierce competition, and massive capital requirements, Deepinder Goyal and his team have built a platform that touches millions of lives daily. The story is far from over—in many ways, it's just beginning.

The lessons from Eternal's journey extend beyond business strategy. It's a story about timing—entering markets at the right inflection point. It's about persistence—surviving when competitors with more capital failed. It's about vision—seeing beyond immediate opportunities to long-term platform potential. Most importantly, it's about execution—building operational excellence in incredibly complex businesses.

The recent developments continue to shape the narrative. Eternal Ltd shows strong stock performance, doubling its workforce and investing heavily in Blinkit, despite a significant profit drop in Q1 FY26. The market's confidence reflects belief in the long-term strategy despite short-term profitability challenges.

Management changes and strategic appointments signal future directions. The elevation of long-time executives to co-founder status, recruitment of technology leaders from global companies, and addition of independent directors with deep industry experience strengthen organizational capability. The team being assembled suggests ambitions beyond current businesses.

Strategic partnerships are expanding the ecosystem. Collaborations with FMCG brands for exclusive launches, partnerships with banks for financial products, and alliances with technology companies for innovation—each partnership adds capabilities without capital investment. The platform's attractiveness to partners increases with scale.

Market share data reveals competitive dynamics. In food delivery, the Zomato-Swiggy duopoly continues with roughly equal shares. In quick commerce, Blinkit leads but faces intense competition from Zepto and Swiggy Instamart. The market share battles will likely intensify before stabilizing.

Analyst perspectives remain divided but increasingly positive. Brokerages like Jefferies, Nomura, and ICICI Securities have raised targets, with Jefferies setting it as high as ₹400. The bull-bear debate centers on profitability timeline versus growth potential. Most analysts acknowledge the strategic positioning while questioning near-term returns.

Technology initiatives continue to differentiate the platform. Investments in artificial intelligence, machine learning, and automation are substantial. The technology team has grown to thousands of engineers, rivaling global technology companies. The innovation pipeline suggests continued product evolution.

The regulatory environment remains fluid. Government policies on e-commerce, gig workers, and data protection are evolving. Eternal's proactive engagement with regulators and compliance investments position it well, but regulatory surprises remain a risk.

Customer behavior evolution favors Eternal's model. The pandemic permanently changed consumption patterns. Convenience has become necessity. The generational shift toward digital-first consumption is irreversible. These trends provide long-term tailwinds for the business.

The India opportunity remains massive and underpenetrated. With over a billion people and growing urbanization, the addressable market expands continuously. Rising incomes, smartphone penetration, and digital payment adoption create favorable conditions. Eternal is positioned to capture disproportionate value from this growth.

The story of Eternal Limited is ultimately about transformation—of a company, an industry, and consumer behavior. From scanning menus in 2008 to delivering anything in 10 minutes in 2025, the journey represents the best of entrepreneurial ambition and execution. As India continues its digital transformation, Eternal's role in shaping that future seems assured. The question isn't whether the company will succeed, but how large and transformative that success will be.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube